Embed Size (px)

Citation preview

June 2, 2016

2

19.4

76.9

7.4

103.8

20.7

82.8

7.3

110.9

Fishing Salmon Other Seafood TOTAL

Revenues: Jan – Mar

All figures in millions of dollars

+7%

-1%

2015 2016

+8%

+7%

3

Results Jan – Mar

EBITDA (before Fair Value)

Profit/Loss

2015 2016

-7.0

4.3

-0.3

-3.0 -3.6

1.4

-0.5

-2.7

Fishing Salmon Other Seafood TOTAL

-4.3

8.2

0.3

4.1

-1.2

-6.0

-0.2

-7.3

Fishing Salmon Other Seafood TOTAL

4

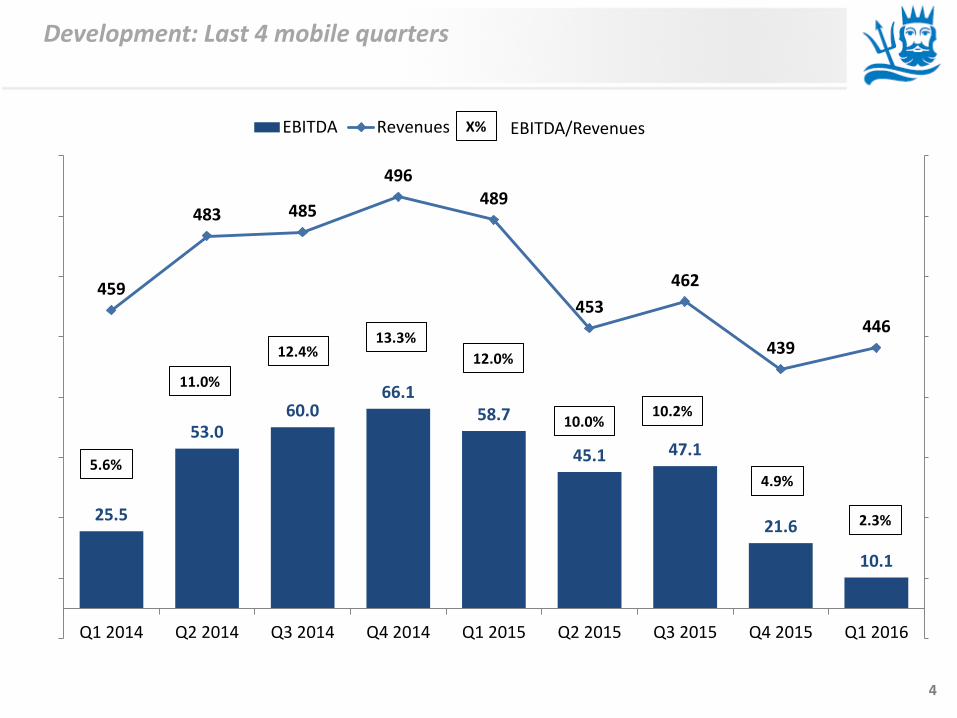

25.5

53.0 60.0

66.1 58.7

45.1 47.1

21.6

10.1

459

483 485

496 489

453

462

439 446

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

EBITDA Revenues

Development: Last 4 mobile quarters

10.0%

5.6%

11.0%

12.4% 13.3%

X% EBITDA/Revenues

12.0%

10.2%

4.9%

2.3%

5

20

1

27

21 18

22

2015 2016 2015 2016 E 2015 2016 2015 2016

Q1 Q2 Q3 Q4

Anchovy: No catches due to impact of El Niño.

Pelagic Fishing

Thousands of tons

87

95

2015 2016 E

Year

Anchovy catches include own and third parties. Company’s estimations are based on current information, which could change due to deviations

6

73

45

42

44

2015 2016 E

Year

19 22 29

7 2

23

4

23

31

19

8

2015 2016 2015 2016 E 2015 2016 2015 2016

Q1 Q2 Q3 Q4

J. Macker.: Favorable fishing conditions (56% of the annual quota catched in 1Q 2016). Sardine: Higher catches vs Q1 2015, but low presence in the 8th region (third parties).

Pelagic Fishing

Jack Mackerel

Sardine

Thousands of tons

89

115

Sardine catches include own and third parties. Company’s estimations are based on current information, which could change due to deviations

7

Fishmeal Price

1,605 1,763 1,780

1,813 1,803

1,532

1,398 1,492

1,567

1,850

2,013

2,247

1,844

1,613

1,760

1,570

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

Prices hit a peak in Q1 2015, and fell after normalization of the Peruvian quotas. Current prices show recovery due to the effects of El Niño and expectations of lower quota for Peru (under 2 M ton). US$ / ton (Camanchaca)

1,825

Prime Fishmeal Price (Chile) IFFO Week 20 2016

May to Jul: 2.5 MM Ton (68% catched)

Nov to Jan: 2.5 M Ton

May to Jul: 2 M Ton

Nov to Jan: No quota

Peru’s Fishing Quota (North-Centre Region):

Nov to Jan: 1.1 M Ton (99% catched)

May to Jul: 2.6 MM Ton (98% catched)

8

China: port off-takes and stocks

Stocks in China bellow the average and higher port off-takes to final consumers

Source: IFFO

9

March 31, 2016 December 31, 2015 March 31, 2015

VOLUME Months of

Production ThUS$ VOLUME ThUS$ ThUS$

SALMON

Atlantic Salmon (Tons) 4,864 2.2 34,089 7,458 42,198 32,940

Salmon Total 34,089 42,198 32,940

FISHING

Fishmeal (Tons) 7,873 1.8 8,136 5,793 6,937 12,454

Fish oil (Tons) 1,987 1.9 2,314 846 1,896 1,534

Frozen Jack Mackerel (Tons) 378 0.3 222 1,185 694 14

Canned Fish (thousands of boxes) 632 8.0 6,373 43 664 2,100

Langostino Lobster (Tons) 85 1.1 1,308 225 2,824 3,880

Fishing Total 18,353 13,015 19,982

OTHER SEAFOOD

Mussels (Tons) 2,521 3.5 5,337 2,280 5,304 3,884

Abalone (Tons) 82 4.6 1,855 86 1,969 3,711

Scallops (Tons) 19 1.0 147 19 157 857

Other Seaafood Total (Tons) 7,339 7,430 8,452

COMPANY TOTAL 59,781 62,643 61,374

Stocks (valued at cost)

Rise in canned fish due to productive focus and decrease in salmon due to higher sales with less production

10

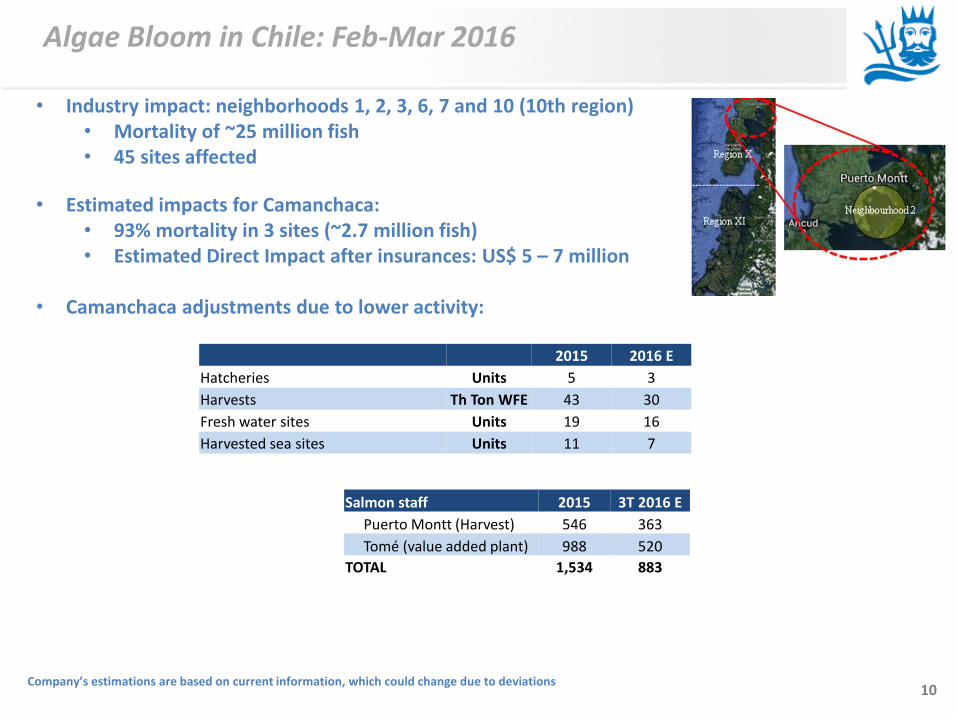

Algae Bloom in Chile: Feb-Mar 2016

• Industry impact: neighborhoods 1, 2, 3, 6, 7 and 10 (10th region) • Mortality of ~25 million fish • 45 sites affected

• Estimated impacts for Camanchaca: • 93% mortality in 3 sites (~2.7 million fish) • Estimated Direct Impact after insurances: US$ 5 – 7 million

• Camanchaca adjustments due to lower activity:

Company’s estimations are based on current information, which could change due to deviations

2015 2016 E

Hatcheries Units 5 3

Harvests Th Ton WFE 43 30

Fresh water sites Units 19 16

Harvested sea sites Units 11 7

Salmon staff 2015 3T 2016 E

Puerto Montt (Harvest) 546 363

Tomé (value added plant) 988 520

TOTAL 1,534 883

11

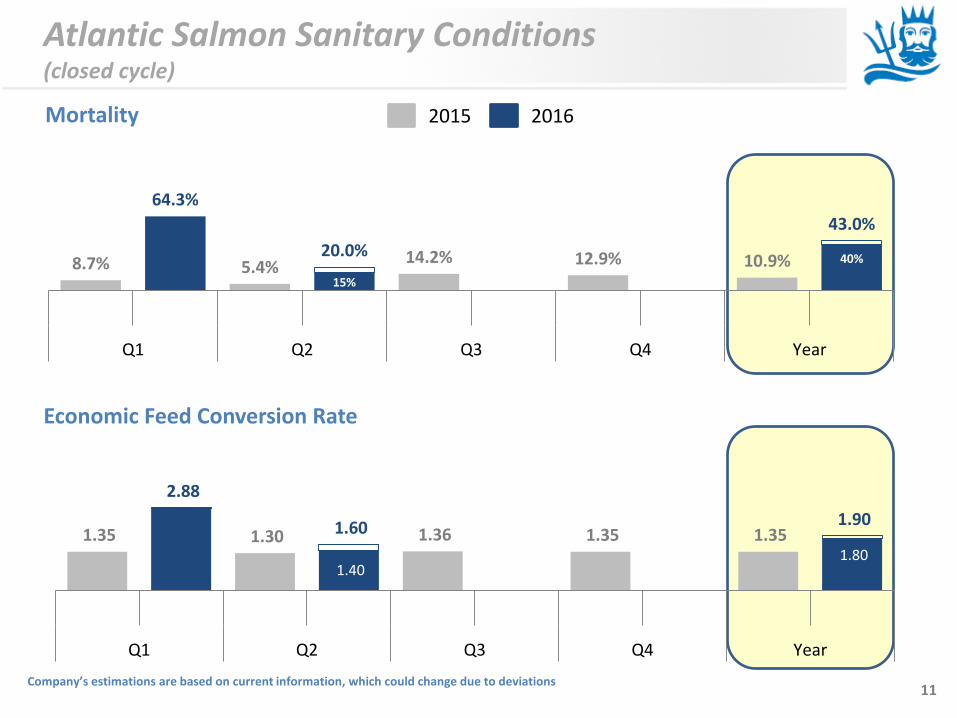

Mortality

Economic Feed Conversion Rate

2015 2016

Atlantic Salmon Sanitary Conditions (closed cycle)

15%

40% 8.7%

64.3%

5.4% 20.0% 14.2% 12.9% 10.9%

43.0%

Q1 Q2 Q3 Q4 Year

1.40

-

1.80 1.35

2.88

1.30 1.60 1.36 1.35 1.35 1.90

Q1 Q2 Q3 Q4 Year

Company’s estimations are based on current information, which could change due to deviations

12

Cost reduction

Atlantic Salmon - Cost ex-cage liveweight (US$ / kg)

3.41 3.01

Impacts in Q4-15 and Q1-16 due to SRS and lower oxygen in the 10th region since October 2015.

3.72 3.81

3.35 3.07 2.95 2.92 3.02 3.08

3.66

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

Others

Medicine

Labor

Smolt

OPEX

Feed

13

43

30

4.4

5.2

E

Year

11.6 9.1

4.9 6.5

11.2

15.6

4.8

4.2 4.5

5.5

4.4 4.1

E

Q1 Q2 Q3 Q4

Atlantic Salmon Price

Prices upwards due to decreasing global supply. 2016 lower harvests due to algae bloom.

Company’s estimations are based on current information, which could change due to deviations

Δ-12%

Δ+22% Δ+18%

2015 2016

Harvest (Thousands of Tons) Price (US$ / Kg WFE)

14

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

jan

-04

jul-

04

jan

-05

jul-

05

jan

-06

jul-

06

jan

-07

jul-

07

jan

-08

jul-

08

jan

-09

jul-

09

jan

-10

jul-

10

jan

-11

jul-

11

jan

-12

jul-

12

jan

-13

jul-

13

jan

-14

jul-

14

jan

-15

jul-

15

jan

-16

Atlantic Salmon Price: Long-term trend

Urner Barry Equivalent Trim C 2-3 *- US$/Lb

Market prices on its trend line due to falling global supply. Effect on Camanchaca’s prices: starting from the 2nd quarter.

may

-16

* Equivalent Trim C

15

Hike in price

Prices every week: Chilean salmon (UB trim D 3-4 lb)

Source: ABG Sundal Collier (05/16/2016)

UB price hike to levels of US$ 5.95 /lb

16

Camanchaca’s Atlantic Salmon RMP

Camanchaca vs Market (Salmonex, January 2013 = Base 100)

March 2016: Camanchaca prices below UBarry and Salmonex indexes (-86 and -55 cents respectively) due to sharp rise in the spot price. Q1 2016: Tie with Salmonex and 8 cents below UBarry.

60

80

100

120

140

160

180

ene-

13

abr-

13

jul-

13

oct

-13

ene-

14

abr-

14

jul-

14

oct

-14

ene-

15

abr-

15

jul-

15

oct

-15

ene-

16

abr-

16

Urner Barry Salmonex Camanchaca

17

Price GAP 2016 By Country

Average price per Lb - Miami - Fillet Trim D 2-4 (Norway Price = Base 100)

63

83

0

20

40

60

80

100

120

Jan Feb Mar Apr May

Chile Norway Canada

Price GAP reduction in the last 5 months

18

70

90

110

130

150

170

190

210

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Raw Material Cost and RMP (Raw Material Return) Base 100 = RMP January 2013

RM cost before processing RMP

Negative margin in Q1 2016, but reversed in April

10th region sites 11th region sites

Development of Atlantic Salmon Margins

Porcelana

Benjamín

Tahuenahuec

Izaza Cabudahue

Fiordo Largo

Pilpilehue

Ahoní

Loncochalgua

Leptepu

Cahuelmó

Lamalec

Licha Puelche

Contao

Mañihueico

Islotes

Edwards

Izaza

|F.Largo|

|-------P.Arg.------|

|---Cabudahue---|

|--Pilpilehue--|

|-----Ahoní-----|

Leptepu

Cahuelmó

Porc. Loncoch.

|-Marilmó-|

|-Forsyth-|

Johnson 2

Company’s estimations are based on current information, which could change due to deviations

Jun

-16

19

Development of Atlantic Salmon Margins

0.64 -0.10

0.87

-0.72 -0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

EBIT (US$/Kg WFE) before Fair Value

Atlantic Salmon Business includes other Revenues and Costs due to services and sales to third parties, and intercompany salmon sales to our offices abroad.

20

Benchmarking Jan – Mar 2016 Salmon Producers with Public Information

Revenues x Gross Margin (before FV)

Gross Margin (before FV) / Revenues

E1 E2

E3

E4

E5

E6

Camanchaca

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

-16 -14 -12 -10 -8 -6 -4 -2 0

21

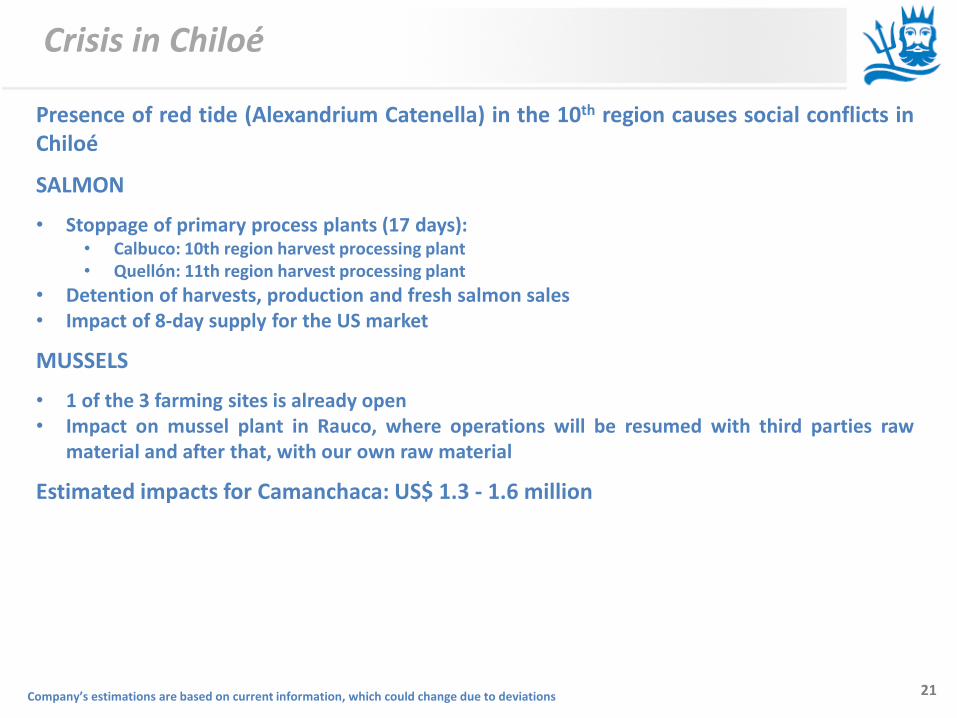

Crisis in Chiloé

Presence of red tide (Alexandrium Catenella) in the 10th region causes social conflicts in Chiloé

SALMON

• Stoppage of primary process plants (17 days): • Calbuco: 10th region harvest processing plant • Quellón: 11th region harvest processing plant

• Detention of harvests, production and fresh salmon sales • Impact of 8-day supply for the US market

MUSSELS

• 1 of the 3 farming sites is already open • Impact on mussel plant in Rauco, where operations will be resumed with third parties raw

material and after that, with our own raw material

Estimated impacts for Camanchaca: US$ 1.3 - 1.6 million

Company’s estimations are based on current information, which could change due to deviations

22

0.35 0.35

0.54

0.30

0.54

0.40

0.49 0.43

0.50

0.40

Q1 Q2 Q3 Q4 Year

2015 2016

Q1 2016: A constant volume, fuel savings of US$ 1.1 million.

Diesel Price: favorable effects on costs US$/lt

-44%

Company’s estimations are based on current information, which could change due to deviations

23

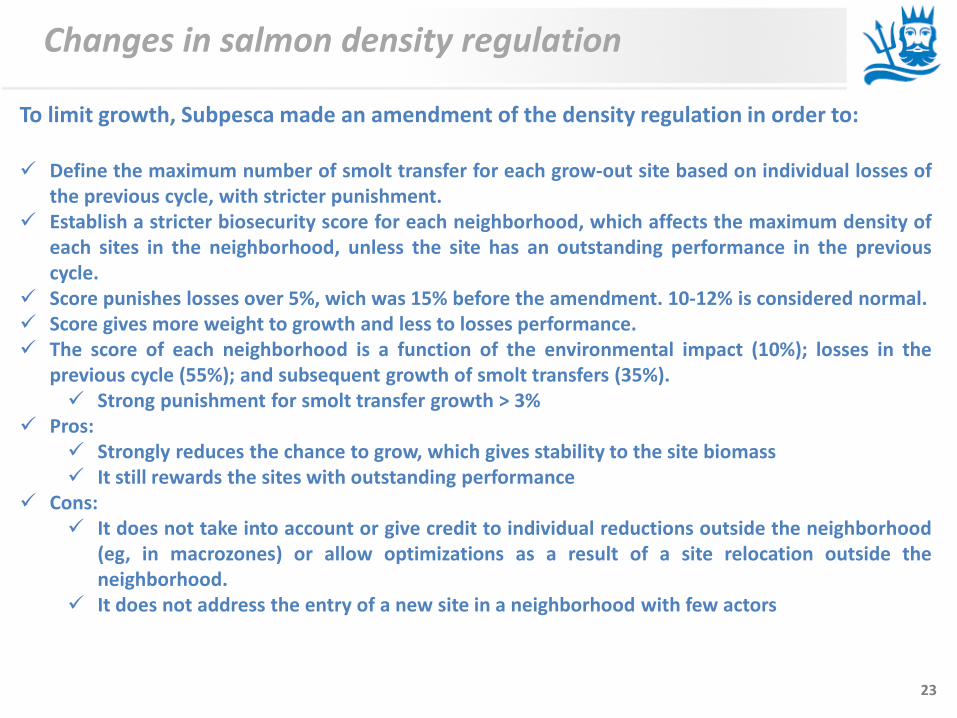

Changes in salmon density regulation

To limit growth, Subpesca made an amendment of the density regulation in order to: Define the maximum number of smolt transfer for each grow-out site based on individual losses of

the previous cycle, with stricter punishment. Establish a stricter biosecurity score for each neighborhood, which affects the maximum density of

each sites in the neighborhood, unless the site has an outstanding performance in the previous cycle.

Score punishes losses over 5%, wich was 15% before the amendment. 10-12% is considered normal. Score gives more weight to growth and less to losses performance. The score of each neighborhood is a function of the environmental impact (10%); losses in the

previous cycle (55%); and subsequent growth of smolt transfers (35%). Strong punishment for smolt transfer growth > 3%

Pros: Strongly reduces the chance to grow, which gives stability to the site biomass It still rewards the sites with outstanding performance

Cons: It does not take into account or give credit to individual reductions outside the neighborhood

(eg, in macrozones) or allow optimizations as a result of a site relocation outside the neighborhood.

It does not address the entry of a new site in a neighborhood with few actors

24

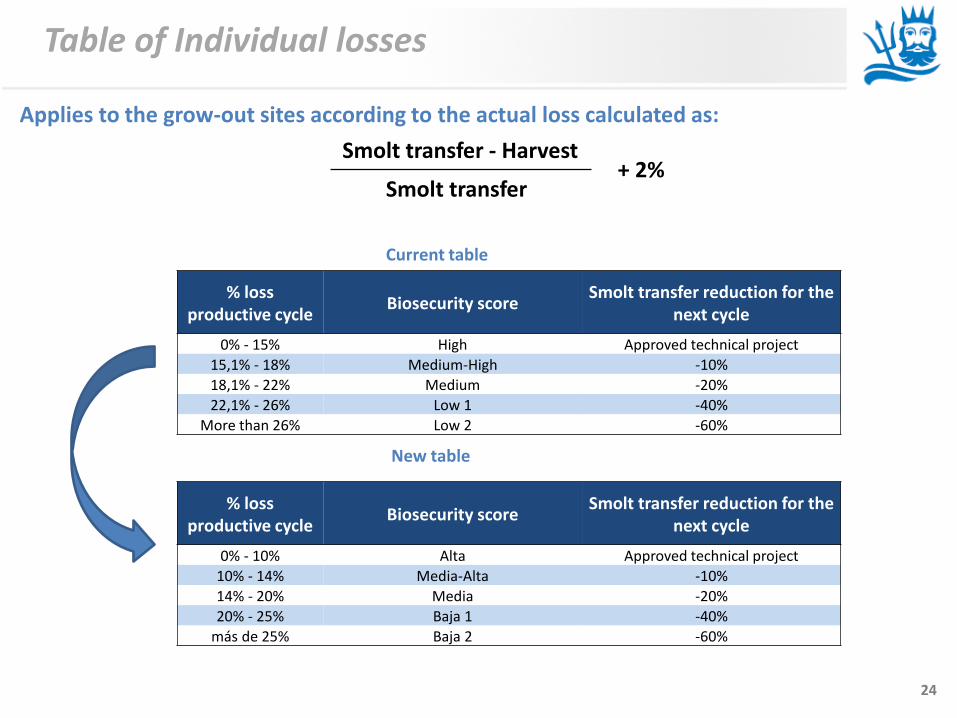

Table of Individual losses

Applies to the grow-out sites according to the actual loss calculated as:

% loss productive cycle

Biosecurity score Smolt transfer reduction for the

next cycle

0% - 15% High Approved technical project

15,1% - 18% Medium-High -10%

18,1% - 22% Medium -20%

22,1% - 26% Low 1 -40%

More than 26% Low 2 -60%

% loss productive cycle

Biosecurity score Smolt transfer reduction for the

next cycle

0% - 10% Alta Approved technical project

10% - 14% Media-Alta -10%

14% - 20% Media -20%

20% - 25% Baja 1 -40%

más de 25% Baja 2 -60%

Current table

New table

Smolt transfer + 2%

Smolt transfer - Harvest

25

Neighborhood score

Environmental element: unchanged

Environmental impact (INFA) % of sites operating with a positive last INFA

Score Weighing

75,1% - 100% 100

10% 50,1% - 75% 75

25,1% - 50% 50

0% - 25% 25

Change in sanitary element

Losses Score Weighing

0% - 15% 100

65% 15,1% - 17% 75

17,1% - 20% 50

More than 20% 25

Losses Score Weighing

0% - 5% 100

55%

5% - 15% 75

15% - 17% 50

17% - 20% 25

More than 20% 0

Current table

New table

26

Neighborhood score

Change in productive element

Smolt transfer projections (relative to the previous period)

Score Weighing

0 - 100% 100

25% 100,1 - 110% 75

110,1 - 120% 50

More than 120% 25

Smolt transfer projections (relative to the previous period)

Score Weighing

0% - 60% 200

35%

60% - 80% 150

80% - 100% 100

100% - 103% 50

103% - 110% 0

More than 110% -100

Current table

New table

27

Neighborhood score

Change in density table

Current table

New table

Total biosecurity score

Biosecurity Level

Maximum Salar density (kg/m3)

Individual site biosecurity

Maximum Salar density (kg/m3)

85,1 - 100 High 17 - 17

64,1 - 85 Medium 15 High (losses < 13%) 17

43,1 - 64 Low 1 13 High (losses < 13%) 15

0 - 43 Low 2 11 High (losses < 13%) 15

Total biosecurity score

Biosecurity Level

Maximum Salar density (kg/m3)

Individual site biosecurity

Maximum Salar density (kg/m3)

79 - 100 High 17 - 17

69 - 79 Medium 15 High (losses < 13%) 17

59 - 69 Low 1 13 High (losses < 13%) 15

42 - 59 Low 2 11 High (losses < 13%) 13

Less than 42 Low 3 8 High (losses < 13%) 11

28

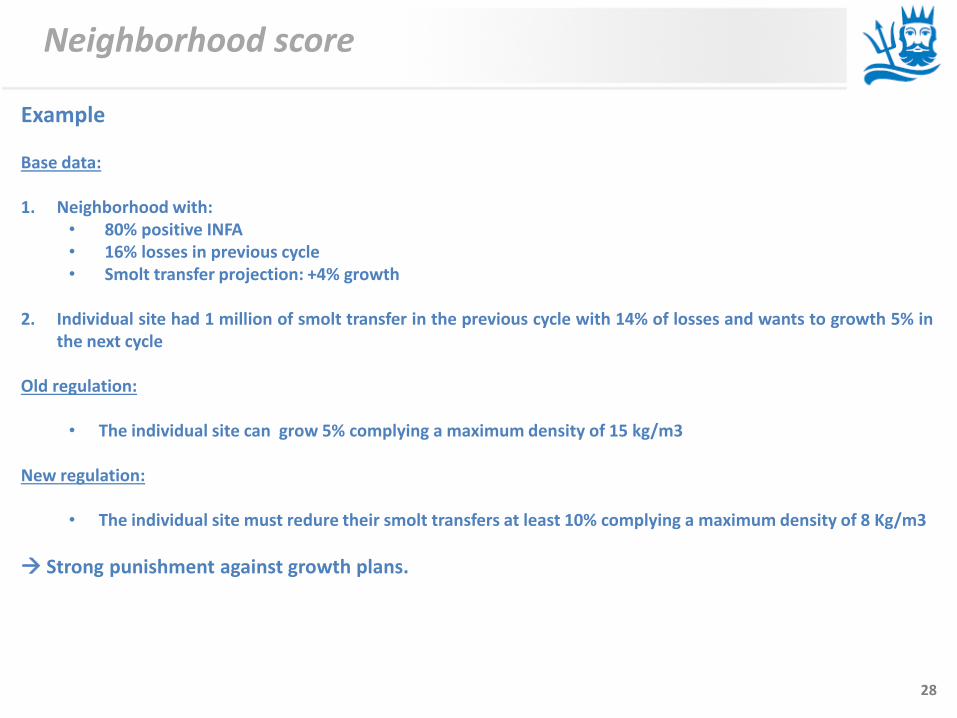

Neighborhood score

Example Base data: 1. Neighborhood with:

• 80% positive INFA • 16% losses in previous cycle • Smolt transfer projection: +4% growth

2. Individual site had 1 million of smolt transfer in the previous cycle with 14% of losses and wants to growth 5% in

the next cycle

Old regulation:

• The individual site can grow 5% complying a maximum density of 15 kg/m3

New regulation:

• The individual site must redure their smolt transfers at least 10% complying a maximum density of 8 Kg/m3

Strong punishment against growth plans.

29

Debt payment on May 25

Refinanced debt in May 2013: US$ 234 million On May 25, 2016: a payment of US$ 15.6 million is made:

Amortization quota: US$ 8.5 million Cash Sweep (Southern fishing): US$ 4.5 million Interests: US$ 2.6 million

Debt balance after payment: US$ 196 million

![Announces Q1 results [Result]](https://img.dokumen.tips/doc/110x75/577cb4121a28aba7118c4992/announces-q1-results-result.jpg)