Embed Size (px)

DESCRIPTION

C-PEM Introduction Webinar. Stuart Hartley FCA [email protected]. Agenda. C-PEM challenges and solutions Tips for reducing the cost of audits Other changes in C-PEM . Introducing C-PEM Released in June 2010 Volume 1 Core concepts Audits, reviews and compilations - PowerPoint PPT Presentation

Citation preview

© Copyright FocusROI Inc 2010

Agenda..

C-PEM challenges and solutions Tips for reducing the cost of

audits Other changes in C-PEM

© Copyright FocusROI Inc 2010

Introducing C-PEM Released in June 2010

Volume 1 Core concepts Audits, reviews and

compilations

Volume 2 Practical Guidance Includes 2 integrated case

studies Part A Audits Part B Reviews Part C Compilations Part D Practice Aids

(forms, etc. on a CD)

© Copyright FocusROI Inc 2010

The C-PEM Case StudiesCase Study A

Cambridge Furniture Inc.─ Case Study B

Kennedy & Co. ─

Business Furniture m anufacturing

$1.5 m illion $ 230,000

8 2 + owner

Sales

Staff

Furniture m anufacturing

Sam ple audit docum entation provided in C-PEMVolum e 2

Prim arily standard C-PEM

forms

Prim arily m emos to file

and condensedC-PEM form s

© Copyright FocusROI Inc 2010

C-PEM Challenges & Solutions ….

1. Auditing standards have been clarified/revised Major changes The C-PEM Solution

2. Multiple Financial Reporting frameworks Major changes The C-PEM Solution

3. Applying CASs to Micro Sized Entities The C-PEM Solution

4. Reviews, compilations and other

© Copyright FocusROI Inc 2010

Challenge #1ALL Auditing standards have been clarified -- some revised (Re-written!)

© Copyright FocusROI Inc 2010

“Clarified” Standards Italics to specific

“shalls” New structure for auditing standards

1. Introduction2. Objectives3. Definitions4. Requirements (the auditor shall…) 5. Application and Other Explanatory Material

Current Italics

Change in number of paragraphs (not content) "Shalls"

282 A 100% increase in requirements 532

© Copyright FocusROI Inc 2010

Impact of Clarified Standards Plus

Structure makes them easier to read/use Framework provides a consistent

approach “Shalls” make very clear what is required

Minus “Shalls” make very clear what is

required Standards are more prescriptive Change in practice is required New terminology to learn

© Copyright FocusROI Inc 2010

The CAS Structure

1. 2. 3 Plan the audit

Performrisk assessment

procedures

Evaluate the audit evidence obtained

Prepare theauditor’s reportRi

s k A

sses

sme n

t

Ris k

Res

pons

e

Repo

rti n

g

Implement responses

to assessed RMM

© Copyright FocusROI Inc 2010

CAS 200 - Overall Objectives 200.18

The auditor shall comply with all CASs relevant to the audit. A CAS is relevant to the audit when the CAS is in effect and the circumstances addressed by the CAS exist.

200.19 The auditor shall have an understanding of the entire text of a

CAS, including its application and other explanatory material, to understand its objectives and to apply its requirements properly.

200.21 To achieve the overall objectives of the auditor, the auditor shall

use the objectives stated in relevant CASs in planning and performing the audit

© Copyright FocusROI Inc 2010

Tip 1… Read & understand the CAS

requirements CICA Handbook Part 1 C-PEM Volumes 1 and 2 Use of C-PEM Forms and practical aides

Staff training courses Webinars, etc.

Applying the new CASs effectively requires an investment to be made

© Copyright FocusROI Inc 2010

Overall objective: Reduce audit risk to an acceptably low level

Overall Audit Objectives CA S 200

Specific CAS Objectives CA Ss 210-720

47 “sha lls”

11 “sha lls ”

474 “sha lls ”

Applicationm ate ria l

Applicationm ate ria l

Applicationm ate ria l

Firm Wide QC CSQC1

“Reducing audit risk to an acceptably low level”

© Copyright FocusROI Inc 2010

CASs with more than 5 new “shalls”

CAS CAS Title Italics Shalls New Old HBCAS 600 Audits of group financial statements 7 40 33 6930CAS 700 Forming an opinion/reporting on F/S 12 38 26 5400CAS 250 Consideration of laws and regulations 3 18 15 5136CAS540 Estimates 1 16 15 5305CAS 570 Going concern 0 15 15 N/A CAS 550 Related Parties 5 18 13 6010CAS 705 Modifications to the opinion 10 23 13 5510CSQC1 CANADIAN STANDARD ON QUALITY CONTROL 35 47 12 GSF 1

CAS 210 Agreeing the terms of audit engagements 5 16 11 5110CAS 710 Comparative information 2 13 11 5701CAS 530 audit sampling 0 10 10 N/A CAS 510 Initial audit engagements — opening balances 0 9 9 variousCAS 560 Subsequent events 3 12 9 6550CAS 240 Fraud in an audit of financial statements 28 36 8 5135CAS 450 Evaluation of misstatements identified 3 11 8 5142CAS 260 Communication with those charged with governance 7 13 6 5751CAS 505 External Confirmations 4 10 6 5303CAS 330 The auditor's responses to assessed risks 21 26 5 5143CAS 580 Written representations 7 12 5 5370

© Copyright FocusROI Inc 2010

Objective for EstimatesThe objective of the auditor is to obtain sufficient

appropriate audit evidence about whether:(a) accounting estimates, including fair

value accounting estimates, in the financial statements, whether recognized or disclosed, are reasonable; and

(b) related disclosures in the financial statements are adequate, in the context of the applicable financial reporting framework.

© Copyright FocusROI Inc 2010

Estimates5305 Estimates CAS540

Current Italics

Subject matter "Shalls"

Risk Assessment Procedures 2Identifying and Assessing RMM 2Responses to the Assessed Risks 3Further Substantive Procedures 3Evaluating Reasonableness of Estimates 1

Disclosures 2Indicators of Possible Management Bias 1Written Representations 1

1 Documentation 1

1 Totals 16

© Copyright FocusROI Inc 2010

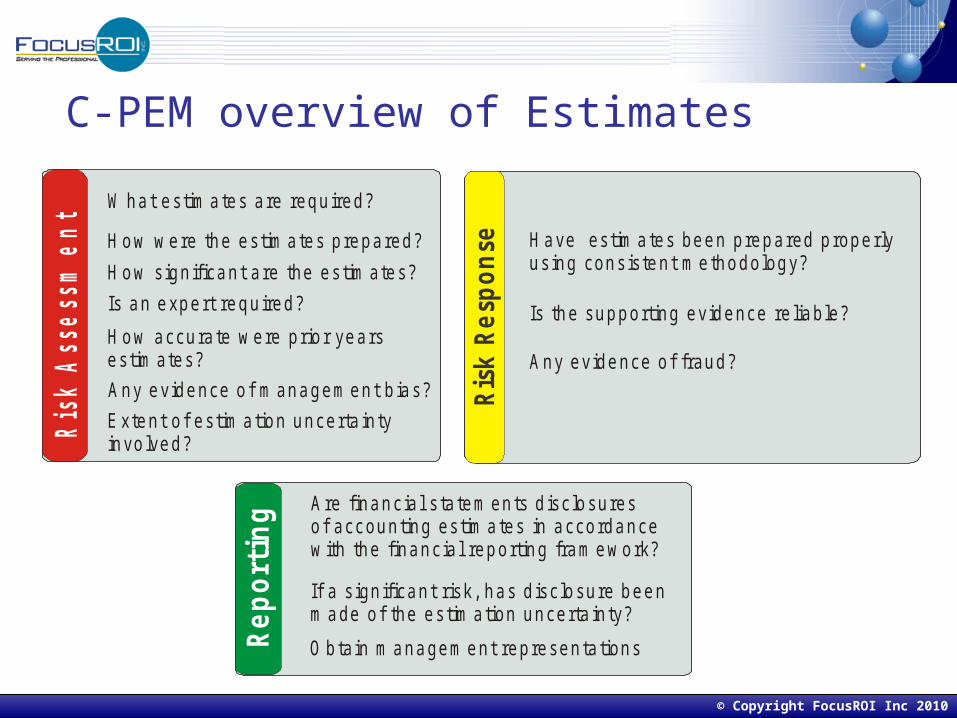

Risk

Ass

essm

ent

Risk

Res

pons

e

Repo

rtin

gW hat estim ates are required?

Have estim ates been prepared properlyusing consistent m ethodology?

Is the supporting evidence re liable?

How were the estim ates prepared?

How accurate were prior years estim ates? Any evidence of m anagem ent b ias?

Any evidence of fraud?

Are in accordance

w ith the of accounting estim ates

financial reporting fram ework?

financial s tatem ents d isclosures

If a sign ificant risk, has d isclosure been m ade of the estim ation uncerta inty?

O btain m anagem ent representa tions

Extent o f estim ation uncerta in ty involved?

How sign ificant are the estim ates?Is an expert required?

C-PEM overview of Estimates

© Copyright FocusROI Inc 2010

Related Parties 6010 Related Parties CAS 550

Current Italics

Subject matter "Shalls"

1 Risk Assessment Procedures 71 Identifying and Assessing RMM 21 Responses to the Assessed Risks 5

Evaluating Accounting/Disclosure of Related Parties 11 Written Representations 11 Communication with Those Charged with Governance 1

Documentation 1

5 Totals 18

© Copyright FocusROI Inc 2010

Risk

Ass

essm

ent

Risk

Res

pons

e

Repo

rtin

gIdentify re la ted parties including changes from previous periods

Identify any other re lated parties and if found ask why not previously identified

Understand nature, extent and purpose of transactions

If outside norm al course of business inspect underlying docum ents.

O btain evidence to support m anagem ents assertions about the

.nature, extent and

purpose of transactions

Is financia l sta tem ent d isclosure adequate?Does audit op in ion need to be m odified if insufficient evidence available?O btain m anagem ent representations

Report on any find ings

Consider s ign ificant risks

Consider potentia l for fraud

Consider possib le fraud

Rem ain a lert for rela ted partytransactions throughout audit

C-PEM Overview of Related Parties

© Copyright FocusROI Inc 2010

Use of External Confirmations5303 External Confirmations CAS 505

Current Italics

Subject matter "Shalls"

Use of confirmations 1Management's Refusal to allow confirm 2

2 Results of the External Confirmation Procedures 5Negative Confirmations 1

1 Evaluating the Evidence Obtained 11 Confirming accounts recievable 4 Totals 10

© Copyright FocusROI Inc 2010

SamplingAudit sampling CAS 530

Current Italics

Subject matter "Shalls"

Sample Design, Size and Selection of Items for Testing 3Performing Audit Procedures 3Nature and Cause of Deviations and Misstatements 2Projecting Misstatements 1Evaluating Results of Audit Sampling 1

0 Totals 10

© Copyright FocusROI Inc 2010

Subsequent Events6550 Subsequent events CAS 560

Current Italics

Subject matter "Shalls"

1 Events between Date of F/S and Date of Auditor's Report 41 Facts after Date of Report but before Date F/S are Issued 41 Facts Known to Auditor after F/S Issued 4

3 Totals 12

© Copyright FocusROI Inc 2010

Materiality CAS 320

Financialstatem ent

leve l

‘Overall’ Materiality

‘ Overal l ’ Materiali tyPerformance

‘ Specifi c’ Material ity

Performance

‘Specifi c’ MaterialityAccount balance,class of transactions

and disclosures level

Q uantitative amo unt $

© Copyright FocusROI Inc 2010

Going Concern Going concern CAS 570

Current Italics

Subject matter "Shalls"

Risk Assessment Procedures 2Evaluating Management's Assessment 4Additional Audit Procedures when events identified 1Audit Conclusions and Reporting 1Material Uncertainty Exists 3Going Concern Assumption Inappropriate 1Management Unwilling to Extend Its Assessment 1Communication with Those Charged with Governance 1Significant Delay in Approval of Financial Statements 1

0 Totals 15

© Copyright FocusROI Inc 2010

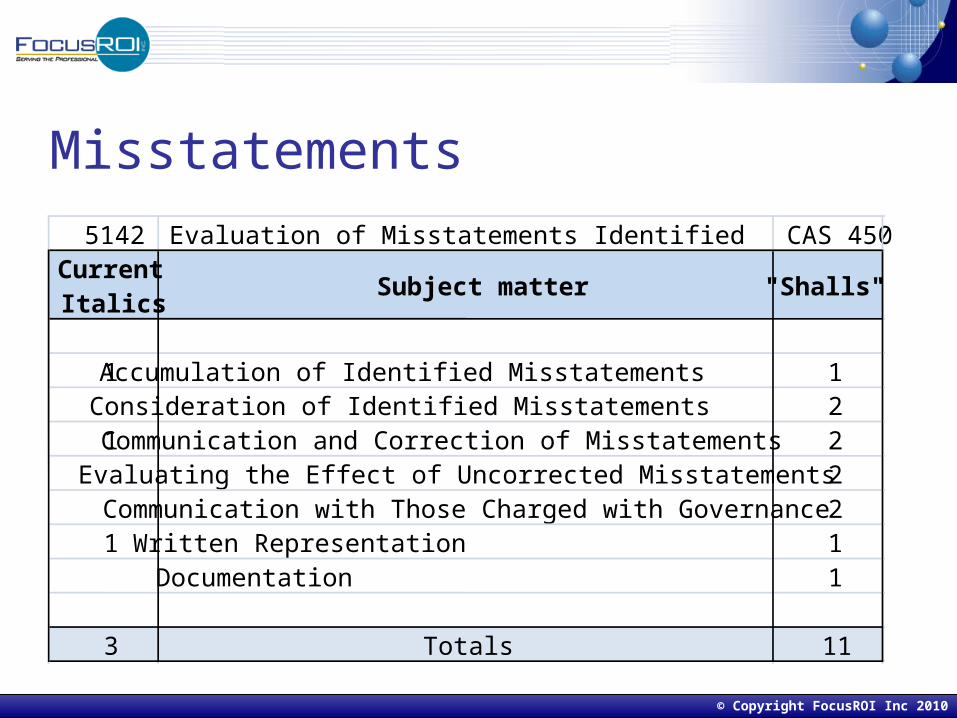

Misstatements5142 Evaluation of Misstatements Identified CAS 450

Current Italics

Subject matter "Shalls"

1 Accumulation of Identified Misstatements 1Consideration of Identified Misstatements 2

1 Communication and Correction of Misstatements 2Evaluating the Effect of Uncorrected Misstatements 2Communication with Those Charged with Governance 2

1 Written Representation 1Documentation 1

3 Totals 11

© Copyright FocusROI Inc 2010

Challenge #2 Multiple Appropriate

Financial Reporting Frameworks (AFRFs)

© Copyright FocusROI Inc 2010

GAAP until recently

Canadian GAAP

Privateentity

Listedentity

Governm ententity

Not forProfit

© Copyright FocusROI Inc 2010

GAAP from 2011 Onwards

ASPE

ASPE+NFP

IFRS

IFR Sfor SM E?

PSAB

Privateentity

Listedentity

Governm ententity

Not forProfit

© Copyright FocusROI Inc 2010

Multiple AFRFsIFRS IFRS for

SMEsASPE ASPE +

NFP PSAB

Number of Pages

2500 220 700 740 ?

Focus Listed Entities

SMEs SMEs NFPs Government

Source IASB IASB

IFRS and ASPE are Canadian GAAP

© Copyright FocusROI Inc 2010

Challenge #3 Applying CASs to

Micro Sized Entities

In Europe: Less than 1 million euros in revenue

– Equivalent to 1.3 million Canadian dollars Less than 10 employees

© Copyright FocusROI Inc 2010

Reality of Micro Entity Audits Limited number of F/S users

Reduced risk

Unsophisticated business processes and accounting systems Few employees Ownership is concentrated Nature/quality of audit evidence available is less

than larger entity

Cost of an audit disproportionately high as compared to larger

entities

© Copyright FocusROI Inc 2010

How CASs address SME audits… “The auditor’s objectives are the same for audits

of entities of different sizes and complexities. This does not mean that every audit will be

planned/performed in exactly the same way.

CASs recognize that specific audit procedures to be undertaken may vary considerably based on size of entity

“Applying ISAs Proportionately with the Size and Complexity of an Entity” issued by IFAC in August 2009.

© Copyright FocusROI Inc 2010

CAS Applicability to SMEs

CAS Objectives

‘Auditor shall..’

Application &other material

Largerentities

Smallerentities

Practical guidance+

Considerations Specific to Sm aller Entities

Practical guidanceon m eaning andim plem entation

© Copyright FocusROI Inc 2010

Overall Audit Scope does not change

Entity Objectives Financ ial Statements

& Assertions

Governance

Leadership/ management

RevenueP rocesses

OtherP rocesses

Transactions

PurchasingP rocesses

PayrollP rocesses

Perv

asive

Pervasive (entity level)

Informat ion Systems

Inhe

rent

Risk

s Controls

© Copyright FocusROI Inc 2010

Still Required to Understand Internal Control

Pervasive areoften called entity level controls

Specific are oftencalled business process or application controls

© Copyright FocusROI Inc 2010

Tip 2…Do not ignore the ‘Control Environment’.

The active involvement of an owner-manager may serve to mitigate transactional risks

(where segregation of duties not possible) in a small entity;

ControlEn v ironm e nt

© Copyright FocusROI Inc 2010

Traditional Audit Phases

Client Acceptance Planning Form

OpinionPerform

Procedures

CompletedChecklists

M em o to file ConclusionsM em o for file

CompletedChecklists

BUT Where does the required risk assessment fit?

© Copyright FocusROI Inc 2010

Tip 3…‘Risk assessment’ is NOT simply an ADD ON to rest of audit.

Risk assessment should enable the auditor to focus work on areas where the RMM is the highest and to reduce work on low risk areas.

This applies in any size audit.

Client Acceptance Planning Form

OpinionPerform

Procedures

Com pletedChecklists

M em o to file ConclusionsM em o for file

Com pletedChecklists

+ Risk Assessm ent?x

© Copyright FocusROI Inc 2010

Client Acceptance Planning

Form Opinion

Perform Procedures

Risk Assessment Risk Response Reporting

AnalyticalProcedures

P relim im ary procedures A ud it p re-conditions

A ssessed R isks o f m aterial m iss tatem entat the FS & A ssertion Leve ls

Team D iscussionsO vera ll audit strategy

Tests ofdetail

Tests ofcontrol?

O vera ll R esponses

D esign Fu rther A ud it p rocedu res

S uffic ien t appropriate audit evidence

C onc lusions d raw nbased on ev idence ob ta ined

Evaluate the audit evidence obtained

Risk assessm entprocedures

© Copyright FocusROI Inc 2010

The Solution

Applying C-PEM to smaller entities

© Copyright FocusROI Inc 2010

C-PEM A completely new version of PEM

that: Reflects the new clarified CASs

Additional guidance on reviews and compilations

Aims for an enlarged base of users An attractive book (in full color) for

partners/staff to read on the bus/train/gym workout or at home

More practical “how to” guidance Integrated case studies and completed

forms/memos

© Copyright FocusROI Inc 2010

C-PEMForms

What C-PEM forms to use is always based on professional judgment

C-PEM Forms facilitate: Compliance with CAS requirements Ease of use with new objectives and instructions Capture of relevant audit evidence in one place Reuse (after updating) - for up to 3-4 years Ease of file review

C-PEM Forms require some staff training on their use. Designed for use by a knowledgeable auditor

C-PEM “Worksheets” are ONLY to be used when applicable

StandardForms

C ondensedForm s M em os

(based on form s)

S ize o f en tityLarge r S m alle r

© Copyright FocusROI Inc 2010

Tip 4… Select appropriate Forms to Use

Select what C-PEM forms to use BEFORE work begins1. Standard forms2. Condensed forms3. Memo to file (using standard forms as a guide)

There is no reason why all three types of documentation cannot be used on the same audit.

If a matter is significant use the standard form, if straightforward use the condensed and if really simple use a memo.

Worksheets are only to be used when applicable

© Copyright FocusROI Inc 2010

C-PEM forms structureFinancial Statements 100

seriesTax matters 200File completion 300

Planning 400Risk Assessment 500Risk Response 600Detailed audit plans A-ZZIncome statement 700Disclosure checklists 900

Form numbering

NOTE: Some form numbers have changed to better reflect their position in the audit process

© Copyright FocusROI Inc 2010

Financial Reporting Frameworks – existing GAAP

900 – 999 FINANCIAL REPORTING FRAMEWORKS

905 FRF — Accounting standards for private enterprises To come—

959 FRF (Financial reporting framework) — Existing Canadian GAAP Read first

960 FRF — Existing GAAP — General

962 Worksheet FRF — Income taxes

963 Worksheet FRF — Long-term investments

964 Worksheet FRF — Leases

965 Worksheet FRF — Deferred charges, intangibles and goodwill

966 Worksheet FRF — Employee future benefits

967 Worksheet FRF — Financial instruments

968 Worksheet FRF — Supplementary

970 FRF Supplement — Not-for-profit entities

© Copyright FocusROI Inc 2010

Key C-PEM Forms Planning (400 series)

Form # Name Year 1 Year 2 Year 3 Year 4 Year 5405-410 Preliminary activities

420 Materiality424 Scoping (+ later risk assessment)

425 Audit Team Discussions430 Overall Audit Strategy435 Risk assessment procedures

New Form prepared Form Updated

© Copyright FocusROI Inc 2010

TIP 5… Spend time planning and saving costs

W hat does th is entity do?W ho are the key people? W hat are the key risks?

W hat materiality to use?Identify financia l s tatem ent use rs and the ir needs

How could fraud occur?C onsider opportunities, p ressu res and m otives . D eve lop som e fraud risk scenarios.

How w ill fraud risk be addressed?W hat changes are required to audit strategy?W ho is doing what, why and w hen?W hat docum entation is required?How w ill team com m unications take place?

W hat is our response to risks?W here is (using judgem ent)- m ore work required?- less or no w ork required?

W hat's changed th is year?Any new risk factors to address?

A udit TeamD iscuss ions

© Copyright FocusROI Inc 2010

Tip 6 … Scope out low risk areas

Scope out immaterial/low risk areas or

Combine them and treat as one F/S area

Consider where work can be reduced EACH year

But consider whether an immaterial area is only small because of missing transactions

© Copyright FocusROI Inc 2010

Key C-PEM Forms Risk Assessment (500 series)

Form # Name Year 1 Year 2 Year 3 Year 4 Year 5

510Identifying risks through understanding the entity

520/522 Risk assessment525 Going concern

530/532 Entity Level control545-560 Control design/implementation

424 Summary of Assessed Risks

New Form prepared Form Updated

© Copyright FocusROI Inc 2010

Identify & assess risk Scope of required

risk assessment CAS 315.11-12

Key PointIdentify sources of risks not just effects on the F/S

Sources of Risk

External riskfactors

Internal risk factors(nature o f en tity)

R isks resu lting fromentity ob jectives &

stra teg ies

R isks from accounting

policies used

R isks identified from use o f Industry

perform anceindicators

Absence o f re levant

In te rnal controlsM ap sources of risk to possib le

errors/fraud in theF ina ncia l

S tatem ents

* R M M = R isks o f m ate ria l m iss ta te m e n t

How: C-PEM 510, 510c or NFP 510

© Copyright FocusROI Inc 2010

TIP 7 … Focus on causes of risks not the effects

The e ffectWater com ing through cie ling

The causeHole in the roof

Invento ry is overva lued S low dow n in econom y C u t o ff e rro rs found B ookkeeper p rone to m istakesEstim ates a re conservative O w ner w ants to m in im ize taxes

© Copyright FocusROI Inc 2010

Assess Risks in One Place

Source of risk Result of risk Risk Assessment

© Copyright FocusROI Inc 2010

Nature of Internal Control

Risks of material misstatement (RMM)

IC to prevent/detect error

Residual RMM

Low Risk High risk

Objective = F/S free from material misstatement

© Copyright FocusROI Inc 2010

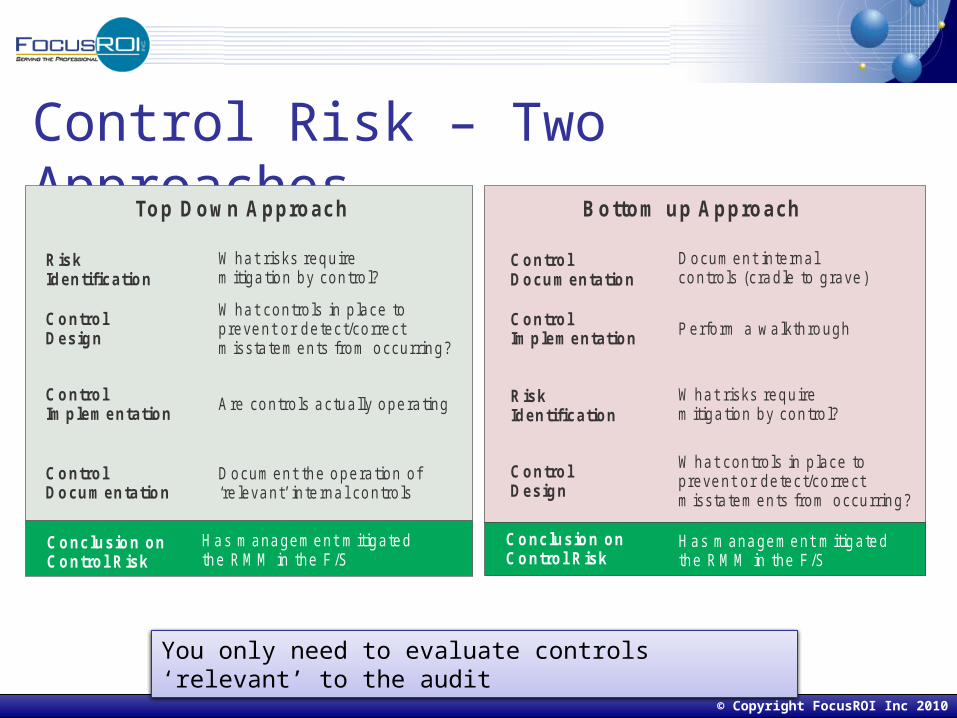

Control Risk – Two ApproachesTop Down Approach Bottom up Approach

W hat risks requirem itigation by control?

W hat risks requirem itigation by control?

Docum ent the operation of‘re levant’ in ternal controls

Docum ent internal controls (cradle to grave)

Are controls actually operating

Perform a walkthrough

Has m anagement m itigated the RM M in the F/S

Has m anagement mitigated the RM M in the F/S

W hat controls in p lace toprevent or detect/correct m isstatem ents from occurring?

W hat controls in p lace toprevent or detect/correct m isstatem ents from occurring?

ControlDesign

ControlDesign

ControlDocum entation

ControlDocum entation

ControlIm plem entation

Conclusion on Control Risk

Conclusion on Control Risk

ControlIm plem entation

RiskIdentification

RiskIdentification

You only need to evaluate controls ‘relevant’ to the audit

© Copyright FocusROI Inc 2010

Consider using the matrices…Process xyz

Risk A Risk B Risk C Risk D Assertion C E A A C AControl IC Com

Control Procedure 1 CA P PControl Procedure 2 IS D

Control Procedure 3 CA P P PControl Procedure 4 M D

Control Procedure 5 CA P

Control Procedure 6 IS D D D

Conclusion on Control Design Y Y N Y

Can you identify the control weaknesses, control strengths & key controls?

© Copyright FocusROI Inc 2010

Tip 8 … Focus on Changes

For risk assessment in year 2 focus only on changes

Identify any new risks and related controls Evaluate whether the relevant controls already

identified are still in operation (implementation) If risk factors have not changed simply ensure the controls

identified in year one are STILL in operation. If no change, both control design and implementation

have been addressed

© Copyright FocusROI Inc 2010

Tip 9 … ROLL FORWARD Plan for forms to be carried forward and updated

Most planning/risk assessment forms should ONLY be completed from scratch every 3-4 years (unless major changes have occurred)

Document evidence so that data collected can be reused.

Focus audit effort in year two onwards on what has changedand needs updating – not re-documenting existing data

© Copyright FocusROI Inc 2010

Tip 10… Customize Your Risk Response

Base your response on the risk assessment --- Ensure work is directed to high risk areas and away from low risk areas

© Copyright FocusROI Inc 2010

Key C-PEM Forms Risk Response (600 series)

Form # Name Year 1 Year 2 Year 3 Year 4 Year 5

6??

Applicable worksheets such as overall responses, sampling, estimates, related parties etc.

645Litigation, claims and non-compliance

650 Subsequent events

670 Use of journal entries A-UU Detailed audit plans7?? Income statement

900+ Financial reporting disclosures

New Form prepared Form Updated

© Copyright FocusROI Inc 2010

File completionForming an Opinion (300 series)

Form # Name Year 1 Year 2 Year 3 Year 4 Year 5310 Checklist — Audit completion

320Notes on significant audit decisions

335Worksheet — Summary of identified misstatements

350 Written representations

360 Legal and other correspondence

370Worksheet — Matters for future consideration

New Form prepared Form Updated

© Copyright FocusROI Inc 2010

Other changes in C-PEM

© Copyright FocusROI Inc 2010

Review Engagements C-PEM Material

expanded Road map Forms basically

unchanged

The FoundationThe basic understanding of the entity

Volume 2 C hapter 35

Design and perform ance of review

engagem ent proceduresVolume 2 C hapter 35, 36

Assess PlausibilityVolume 2 Chapter 37

Review engagem ent

reportVol. 2 Chapter 38

© Copyright FocusROI Inc 2010

Other Material in C-PEM Compilations

Updated material FOFI

No changes Primer on fraud Expanded sampling guidance Tips for Client Interviews

© Copyright FocusROI Inc 2010

C-PEM Summary – A must BUY Comprehensive guide to all the new

CASs Two bound volumes

Illustrations in color Integrated case studies

Ideal training tool Extra copies available for staff

members User friendly forms

Practical and flexible practical aids

© Copyright FocusROI Inc 2010

QuestionsPlease