Embed Size (px)

Citation preview

Gamesa EnergíaNobody knows more about wind

September 24, 2010, Madrid

2

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline breakdown and balance sheet value

Accounting and financial modeling

Gamesa Energía´s history

5

6

Strategy

Valuation

7

Conclusions8

Financing

3

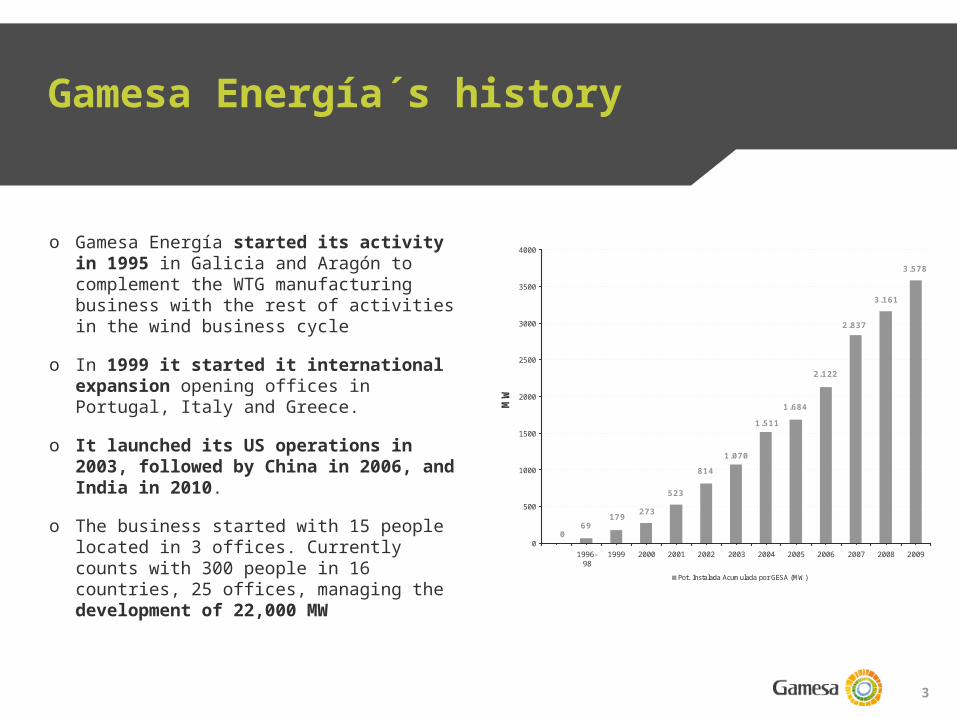

Gamesa Energía´s history

o Gamesa Energía started its activity in 1995 in Galicia and Aragón to complement the WTG manufacturing business with the rest of activities in the wind business cycle

o In 1999 it started it international expansion opening offices in Portugal, Italy and Greece.

o It launched its US operations in 2003, followed by China in 2006, and India in 2010.

o The business started with 15 people located in 3 offices. Currently counts with 300 people in 16 countries, 25 offices, managing the development of 22,000 MW

179 27369

523

8141.070

1.511

1.684

2.122

2.837

3.161

3.578

00

500

1000

1500

2000

2500

3000

3500

4000

1996-98

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

MW

Pot. Instalada Acumulada por GESA (MW)

4

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline breakdown and balance sheet value

Accounting and financial modeling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

5

Business model and value generation alternatives

Business model description1

2

3

4

5

Procurement of WTG – relationship with the manufacturing business

Key considerations in the sale of a wind farm

Alternatives and evolution of current business model

Competitive advantages

6 Site selection: wind resource expertise

6

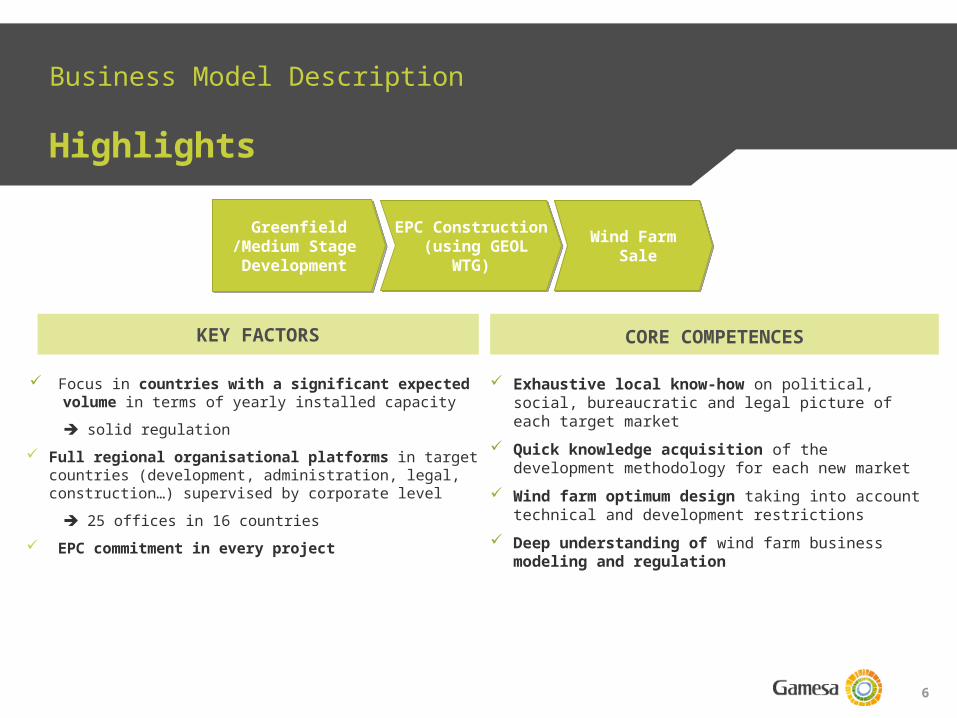

Business Model Description

Highlights

EPC Construction (using GEOL

WTG)Wind Farm

SaleGreenfield

/Medium Stage Development

Focus in countries with a significant expected volume in terms of yearly installed capacity

solid regulation Full regional organisational platforms in target

countries (development, administration, legal, construction…) supervised by corporate level

25 offices in 16 countries EPC commitment in every project

KEY FACTORS

Exhaustive local know-how on political, social, bureaucratic and legal picture of each target market

Quick knowledge acquisition of the development methodology for each new market

Wind farm optimum design taking into account technical and development restrictions

Deep understanding of wind farm business modeling and regulation

CORE COMPETENCES

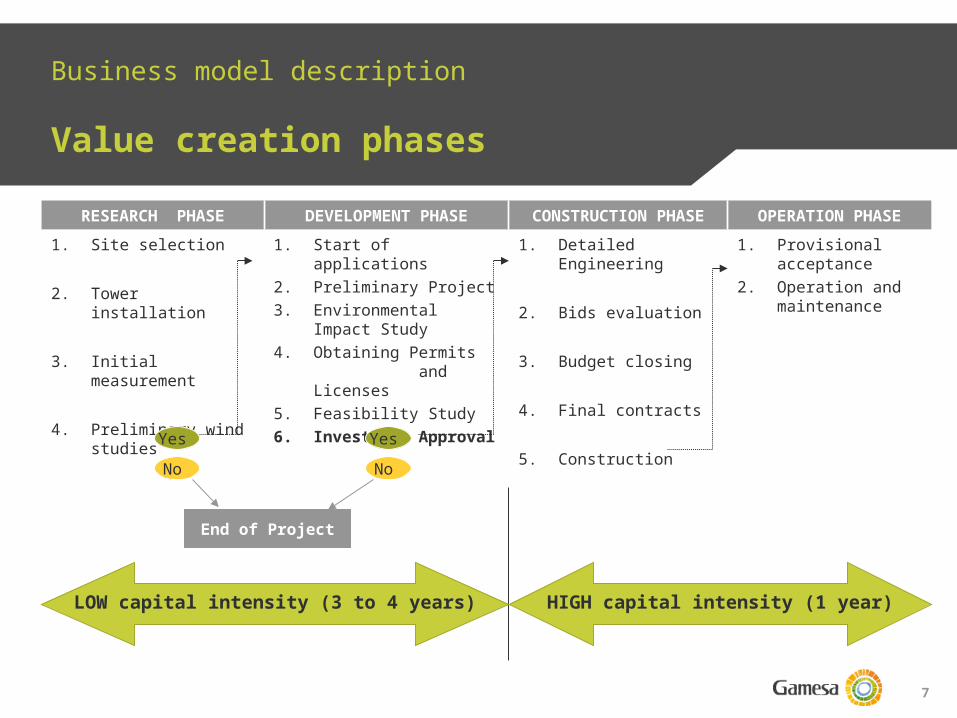

7

RESEARCH PHASE DEVELOPMENT PHASE CONSTRUCTION PHASE OPERATION PHASE

1. Site selection

2. Tower installation

3. Initial measurement

4. Preliminary wind studies

1. Start of applications2. Preliminary Project3. Environmental Impact

Study4. Obtaining Permits

and Licenses5. Feasibility Study6. Investment

Approval

1. Detailed Engineering

2. Bids evaluation

3. Budget closing

4. Final contracts

5. Construction

1. Provisional acceptance

2. Operation and maintenance

Yes No

End of Project

Business model description

Value creation phases

No Yes

LOW capital intensity (3 to 4 years) HIGH capital intensity (1 year)

8

Business model and value generation alternatives

Business model description1

2

3

4

5

Procurement of WTG – relationship with the manufacturing business

Key considerations in the sale of a wind farm

Alternatives and evolution of current business model

Competitive advantages

6 Site selection: wind resource expertise

9

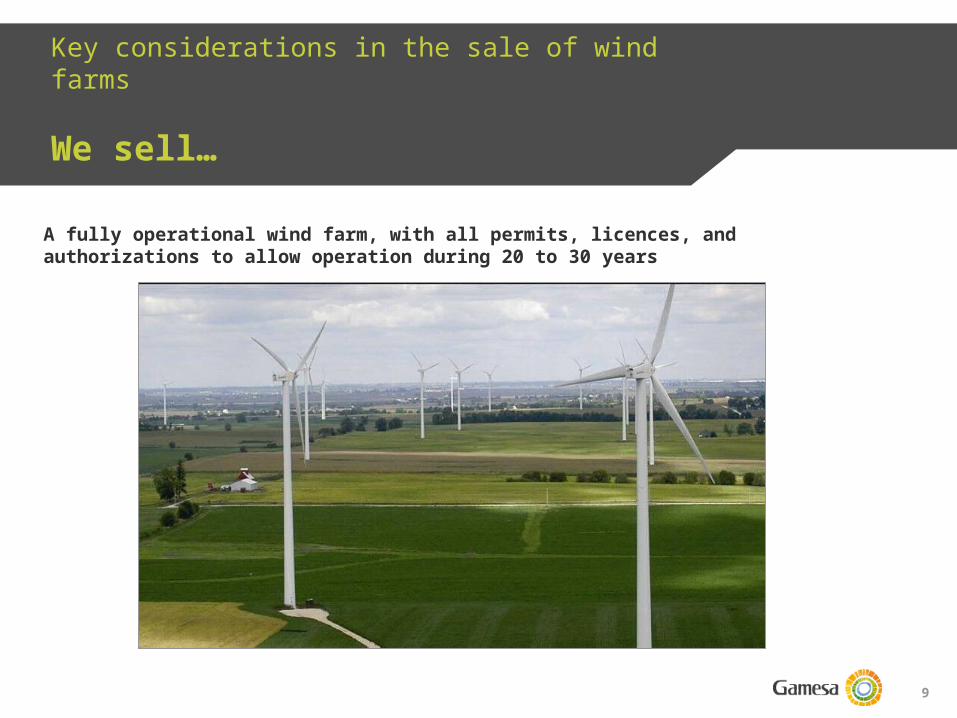

Key considerations in the sale of wind farms

We sell…

A fully operational wind farm, with all permits, licences, and authorizations to allow operation during 20 to 30 years

10

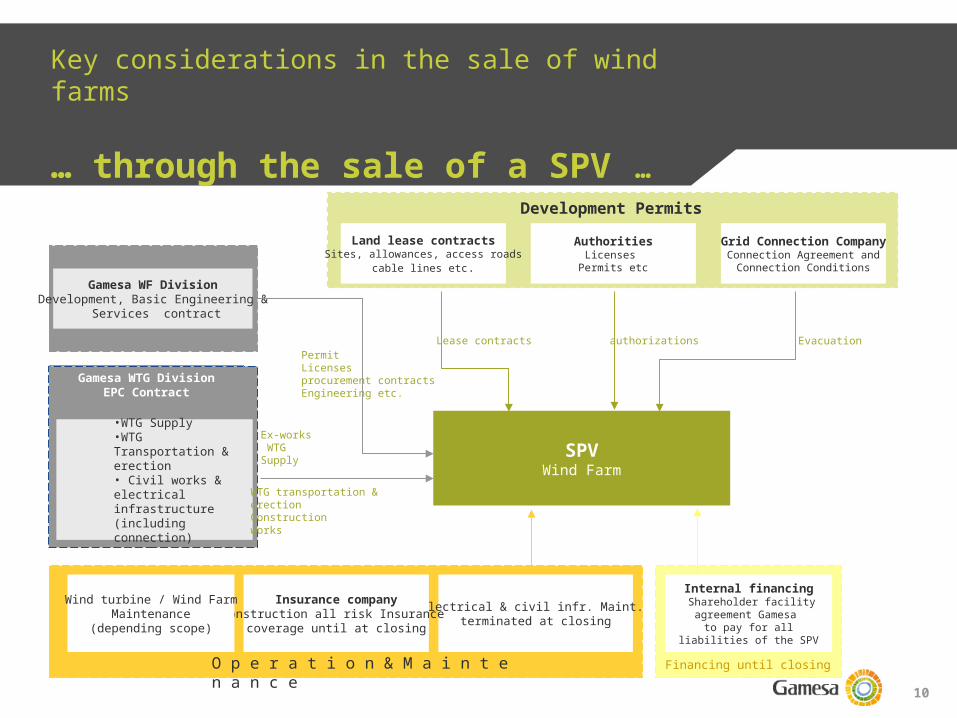

SPVWind Farm

Gamesa WF DivisionDevelopment, Basic Engineering &

Services contract

•WTG Supply•WTG Transportation & erection• Civil works & electrical infrastructure (including connection)

Internal financing Shareholder facility agreement Gamesa

to pay for all liabilities of the SPV

Land lease contractsSites, allowances, access roads

cable lines etc.

Lease contractsPermitLicensesprocurement contractsEngineering etc.

Ex-works WTG Supply

WTG transportation & erectionConstructionworks

AuthoritiesLicenses

Permits etc

authorizations

Financing until closing

Grid Connection CompanyConnection Agreement and

Connection Conditions

Evacuation

Electrical & civil infr. Maint. terminated at closing

Insurance companyConstruction all risk Insurance

coverage until at closing

Wind turbine / Wind FarmMaintenance

(depending scope)

O p e r a t i o n & M a i n t e n a n c e

Gamesa WTG DivisionEPC Contract

Development Permits

Key considerations in the sale of wind farms

… through the sale of a SPV …

11

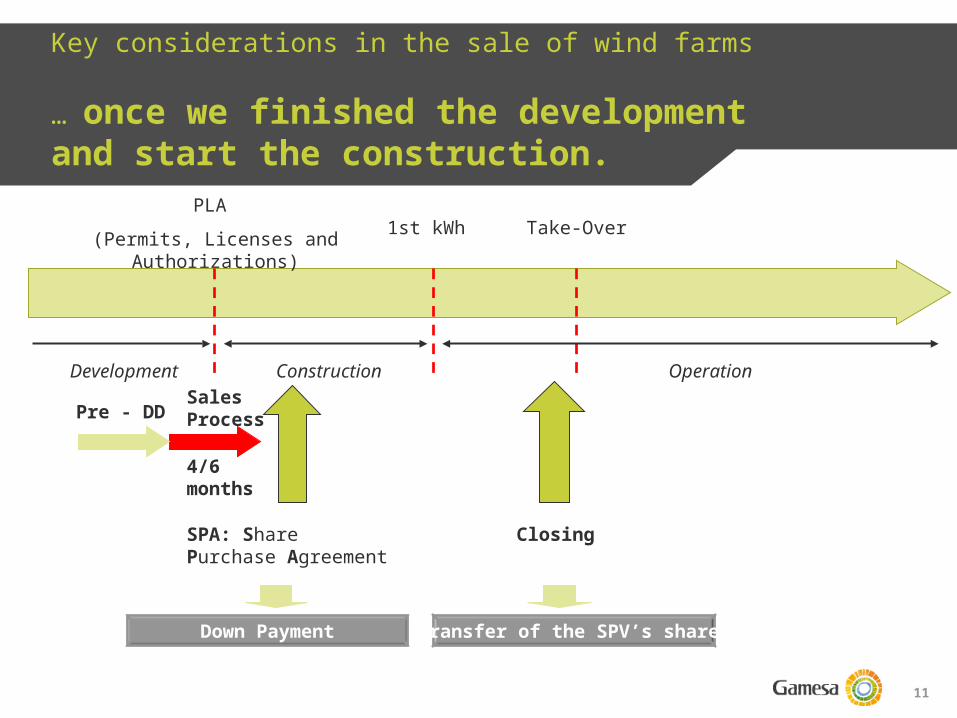

Key considerations in the sale of wind farms

… once we finished the development and start the construction.

PLA (Permits, Licenses and

Authorizations)1st kWh Take-Over

Development Construction Operation

SPA: Share Purchase Agreement

Closing

Sales Process

4/6 months

Pre - DD

Down Payment Transfer of the SPV’s shares

12

Key considerations in the sale of wind farms

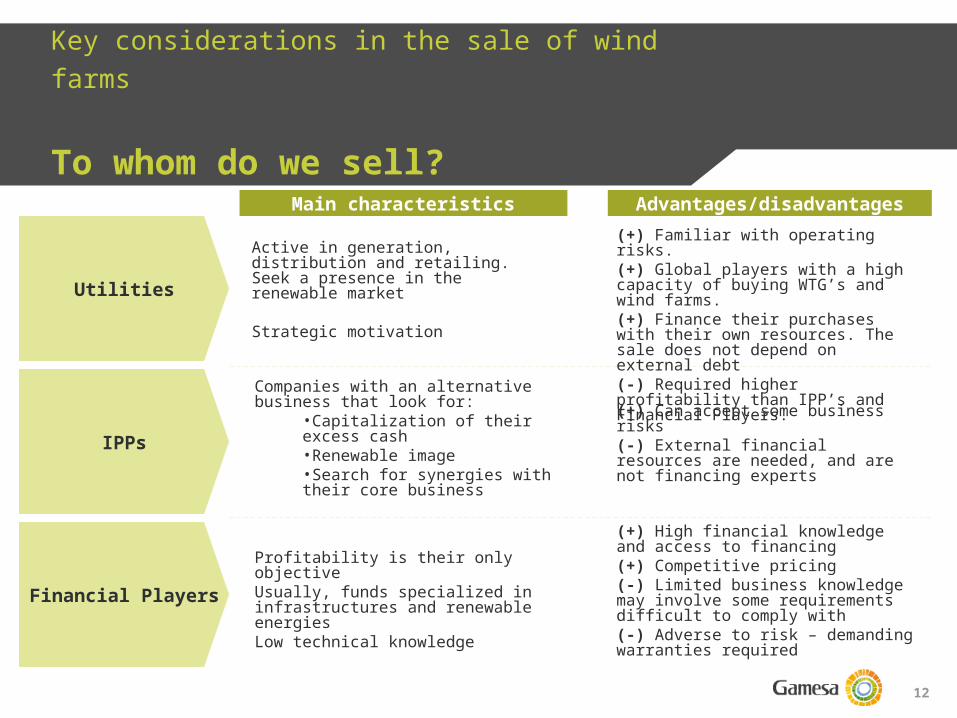

To whom do we sell?

Utilities

Main characteristics Advantages/disadvantages

IPPs

Financial Players

Active in generation, distribution and retailing. Seek a presence in the renewable market

Strategic motivation

Companies with an alternative business that look for:

•Capitalization of their excess cash•Renewable image•Search for synergies with their core business

Profitability is their only objectiveUsually, funds specialized in infrastructures and renewable energiesLow technical knowledge

(+) Familiar with operating risks.(+) Global players with a high capacity of buying WTG’s and wind farms.(+) Finance their purchases with their own resources. The sale does not depend on external debt(-) Required higher profitability than IPP’s and Financial Players.

(+) Can accept some business risks(-) External financial resources are needed, and are not financing experts

(+) High financial knowledge and access to financing (+) Competitive pricing (-) Limited business knowledge may involve some requirements difficult to comply with(-) Adverse to risk – demanding warranties required

13

o B&Bo Viridiso Taiga Mistral

o Iberdrolao Edisono Endesao ENEL

o Electrabelo Eono EWEo Duke Energy

o Gestampo Genera Avanteo Naturener

o Acciona / CESAo Aldesao Ikeao ACS

o Fortunyo Marubeni

Key considerations in the sale of wind farms

Some of our clients

Utilities

IPPs

Financial Players

Core Market

Increasing weight market

opportunity

14

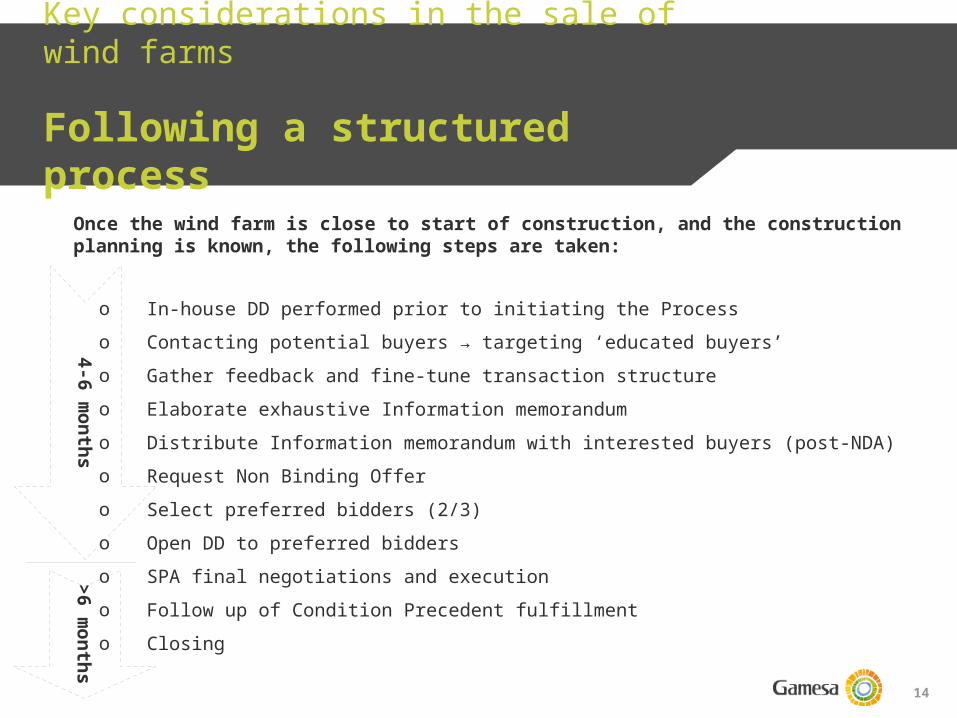

o In-house DD performed prior to initiating the Processo Contacting potential buyers → targeting ‘educated buyers’o Gather feedback and fine-tune transaction structureo Elaborate exhaustive Information memorandumo Distribute Information memorandum with interested buyers (post-NDA)o Request Non Binding Offero Select preferred bidders (2/3)o Open DD to preferred bidderso SPA final negotiations and executiono Follow up of Condition Precedent fulfillmento Closing

Once the wind farm is close to start of construction, and the construction planning is known, the following steps are taken:

Key considerations in the sale of wind farms

Following a structured process

4-6 months

>6 m

onths

15

Business model and value generation alternatives

Business model description1

2

3

4

5

Procurement of WTG – relationship with the manufacturing business

Key considerations in the sale of a wind farm

Alternatives and evolution of current business model

Competitive advantages

6 Site selection: wind resource expertise

16

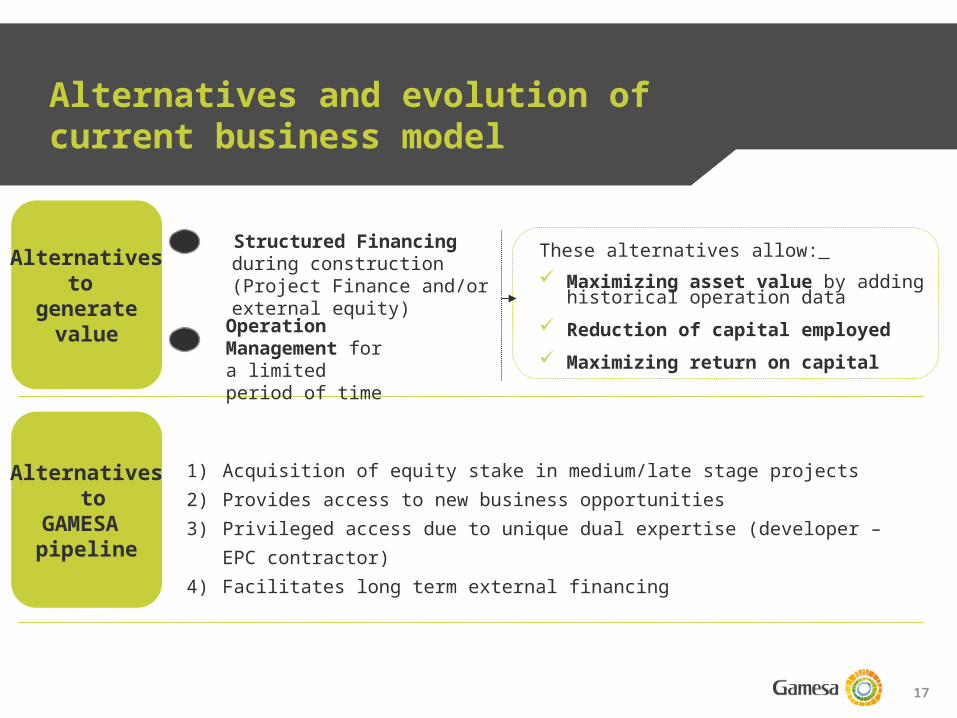

Alternatives and evolution of current business model

GESA does not intend to become an IPP

17

Alternatives and evolution of current business model

Alternativesto

generatevalue

Alternatives to

GAMESA pipeline

These alternatives allow: Maximizing asset value by adding historical operation data Reduction of capital employed Maximizing return on capital

Structured Financing during construction (Project Finance and/or external equity)

1

Operation Management for a limited period of time

2

1) Acquisition of equity stake in medium/late stage projects2) Provides access to new business opportunities3) Privileged access due to unique dual expertise (developer – EPC

contractor)4) Facilitates long term external financing

18

Business model and value generation alternatives

Business model description1

2

3

4

5

Procurement of WTG – relationship with the manufacturing business

Key considerations in the sale of a wind farm

Alternatives and evolution of current business model

Competitive advantages

6 Site selection: wind resource expertise

19

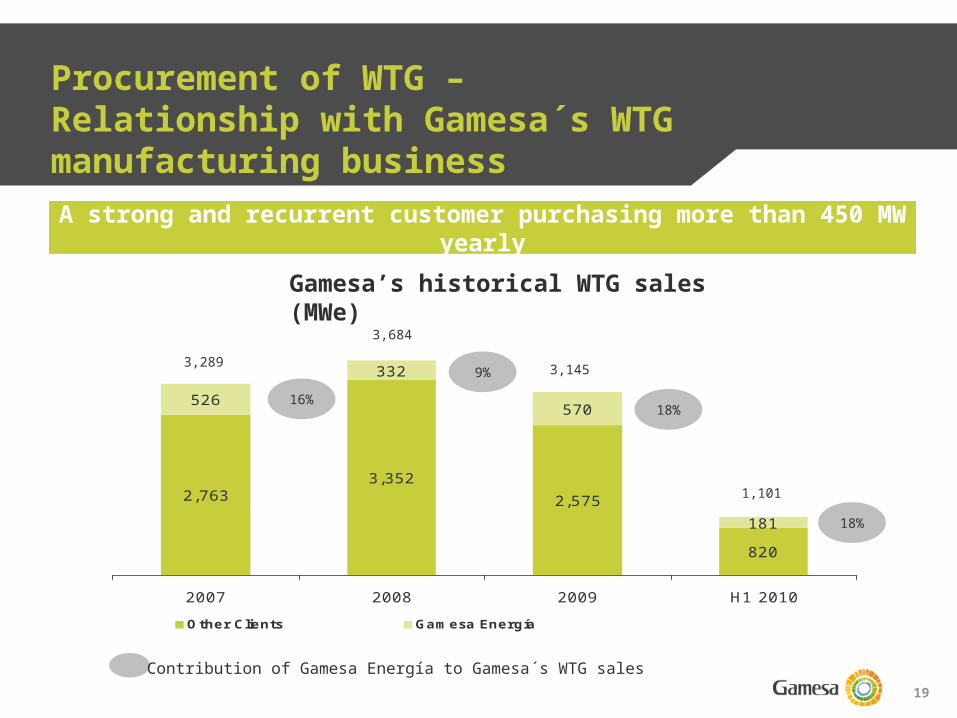

MWe WTG

820

526332

570

1812,575

3,3522,763

2007 2008 2009 H1 2010Other Clients Gamesa Energía

16%9%

18%

18%

Contribution of Gamesa Energía to Gamesa´s WTG sales

3,2893,684

3,145

1,101

Procurement of WTG – Relationship with Gamesa´s WTG manufacturing businessA strong and recurrent customer purchasing more than 450 MW

yearlyGamesa’s historical WTG sales (MWe)

20

Business model and value generation alternatives

Business model description1

2

3

4

5

Procurement of WTG – relationship with the manufacturing business

Key considerations in the sale of a wind farm

Alternatives and evolution of current business model

Competitive advantages

6 Site selection: wind resource expertise

21

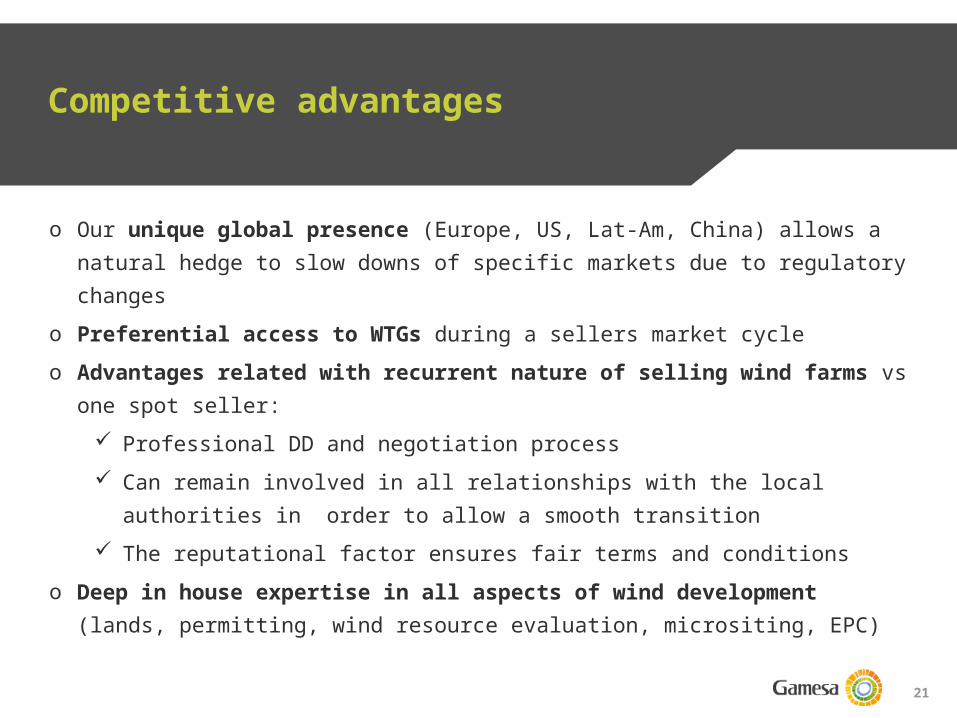

o Our unique global presence (Europe, US, Lat-Am, China) allows a natural hedge to slow downs of specific markets due to regulatory changes

o Preferential access to WTGs during a sellers market cycleo Advantages related with recurrent nature of selling wind farms vs

one spot seller: Professional DD and negotiation process Can remain involved in all relationships with the local authorities in

order to allow a smooth transition The reputational factor ensures fair terms and conditions

o Deep in house expertise in all aspects of wind development (lands, permitting, wind resource evaluation, micrositing, EPC)

Competitive advantages

22

Business model and value generation alternatives

Business model description1

2

3

4

5

Procurement of WTG – relationship with the manufacturing business

Key considerations in the sale of a wind farm

Alternatives and evolution of current business model

Competitive advantages

6 Site selection: wind resource expertise

23

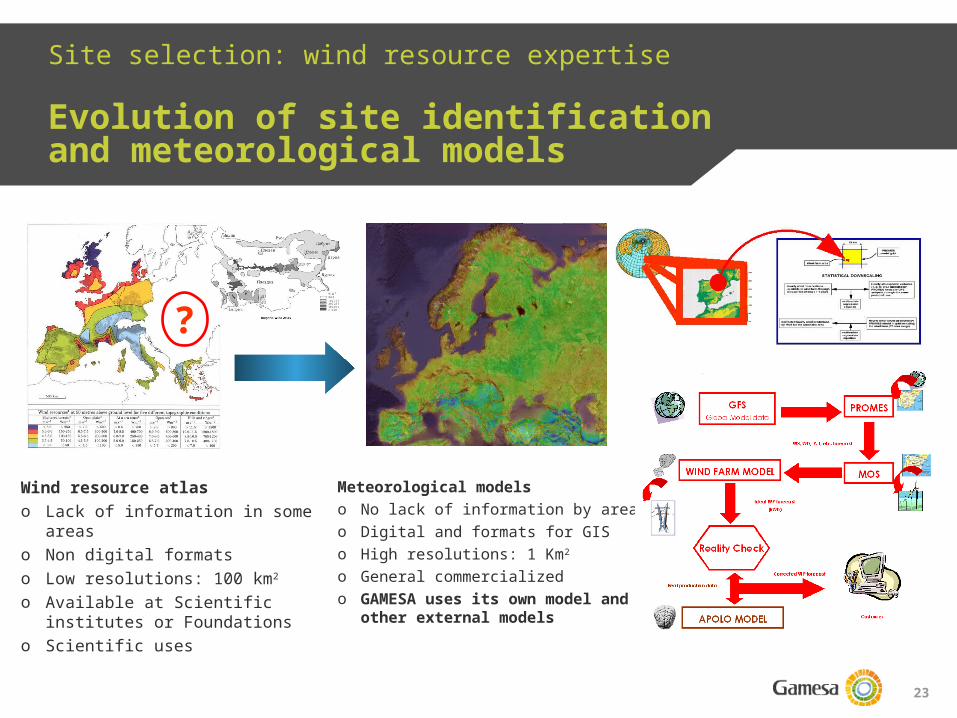

Site selection: wind resource expertise

Evolution of site identification and meteorological models

Wind resource atlaso Lack of information in some areaso Non digital formats o Low resolutions: 100 km2

o Available at Scientific institutes or Foundations

o Scientific uses

Meteorological modelso No lack of information by areaso Digital and formats for GISo High resolutions: 1 Km2

o General commercializedo GAMESA uses its own model

and other external models

?

24

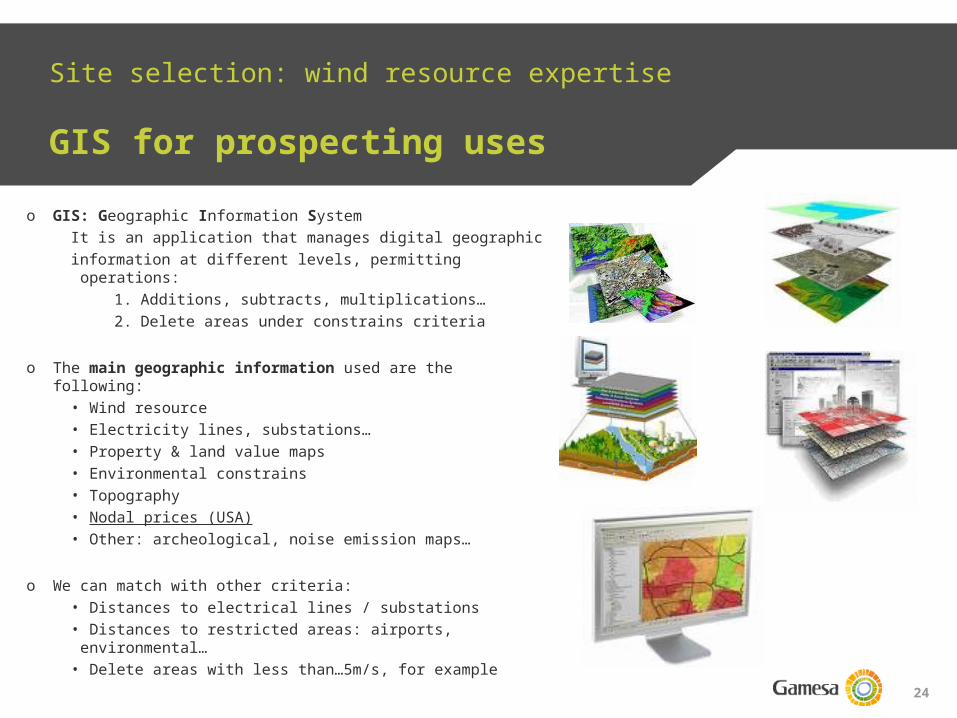

Site selection: wind resource expertise

GIS for prospecting uses

o GIS: Geographic Information SystemIt is an application that manages digital geographicinformation at different levels, permitting operations:

1. Additions, subtracts, multiplications…2. Delete areas under constrains criteria

o The main geographic information used are the following:• Wind resource• Electricity lines, substations…• Property & land value maps• Environmental constrains• Topography• Nodal prices (USA)• Other: archeological, noise emission maps…

o We can match with other criteria:• Distances to electrical lines / substations• Distances to restricted areas: airports, environmental…• Delete areas with less than…5m/s, for example

25

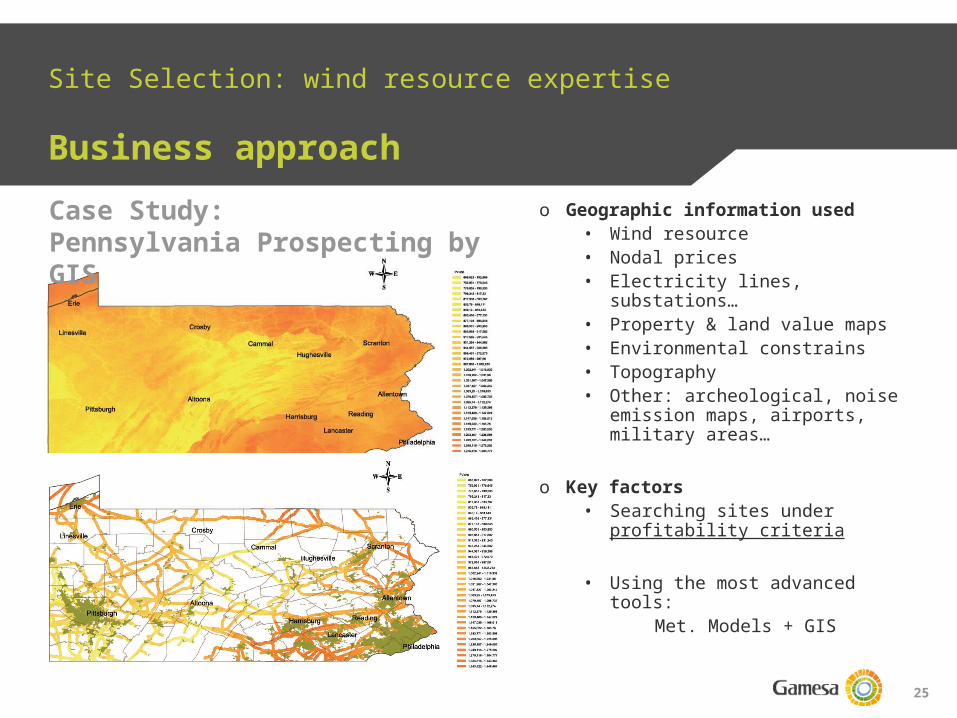

Site Selection: wind resource expertise

Business approachCase Study:Pennsylvania Prospecting by GIS

o Geographic information used• Wind resource• Nodal prices• Electricity lines, substations…• Property & land value maps• Environmental constrains• Topography• Other: archeological, noise

emission maps, airports, military areas…

o Key factors• Searching sites under

profitability criteria

• Using the most advanced tools:Met. Models + GIS

26

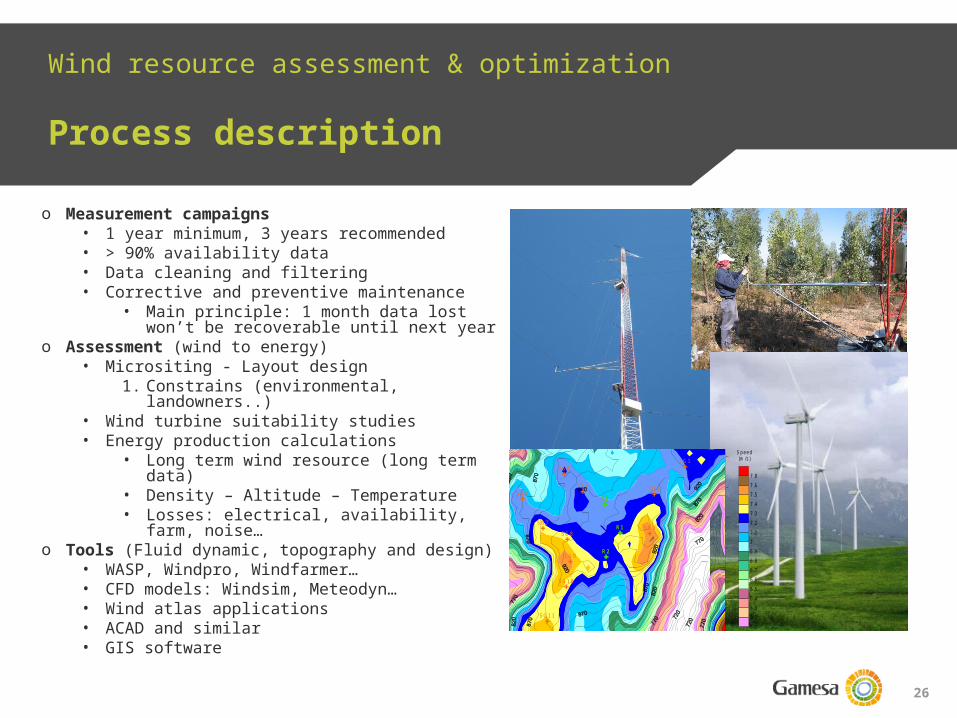

Wind resource assessment & optimization

Process description

o Measurement campaigns• 1 year minimum, 3 years recommended• > 90% availability data• Data cleaning and filtering• Corrective and preventive maintenance

• Main principle: 1 month data lost won’t be recoverable until next year

o Assessment (wind to energy) • Micrositing - Layout design

1. Constrains (environmental, landowners..)• Wind turbine suitability studies• Energy production calculations

• Long term wind resource (long term data)

• Density – Altitude – Temperature• Losses: electrical, availability, farm,

noise…o Tools (Fluid dynamic, topography and design)

• WASP, Windpro, Windfarmer…• CFD models: Windsim, Meteodyn…• Wind atlas applications• ACAD and similar • GIS software

632000 632500 633000 633500 634000 634500 635000 635500

4524

000

4524

500

4525

000

4525

500

4526

000

4526

500

4527

000

SG1

SG2

SG3

SG4

SG5

SG6

SG7SG8

SG9

SG10

SG11

SG12

R1

R2

R3

R1

R2

R3

6.1

6.2

6.3

6.4

6.5

6.6

6.7

6.8

6.9

7

7.1

7.2

7.3

7.4

7.5

7.6

7.8

M ean speed at 120m at S ao G ens area

Speed (m /s)

27

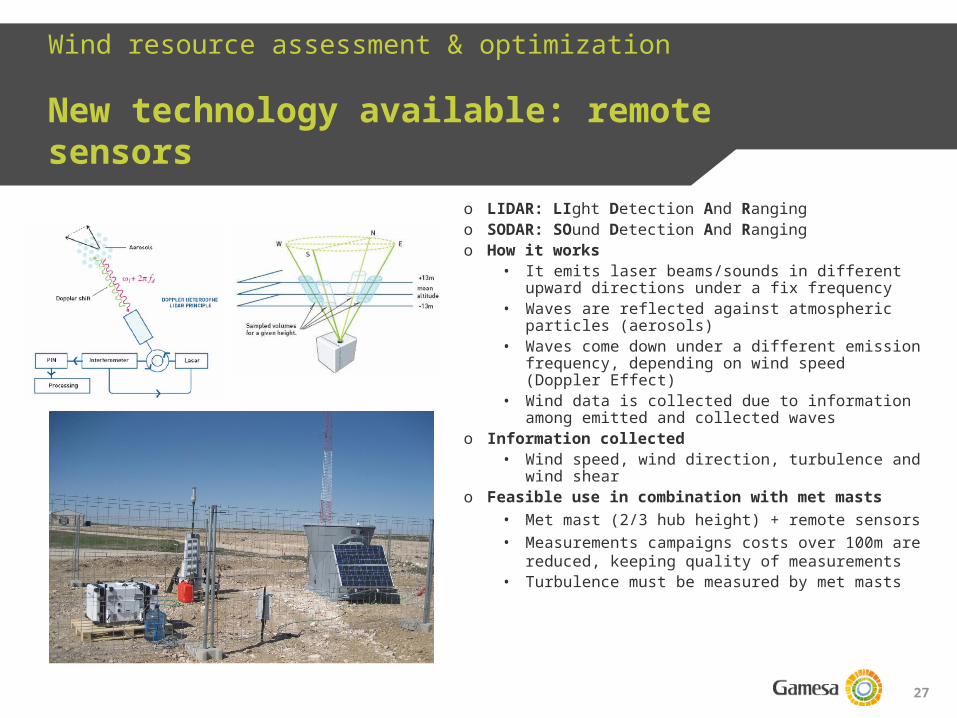

Wind resource assessment & optimization

New technology available: remote sensors

o LIDAR: LIght Detection And Rangingo SODAR: SOund Detection And Rangingo How it works

• It emits laser beams/sounds in different upward directions under a fix frequency

• Waves are reflected against atmospheric particles (aerosols)

• Waves come down under a different emission frequency, depending on wind speed (Doppler Effect)

• Wind data is collected due to information among emitted and collected waves

o Information collected• Wind speed, wind direction, turbulence and

wind shearo Feasible use in combination with met masts

• Met mast (2/3 hub height) + remote sensors• Measurements campaigns costs over 100m

are reduced, keeping quality of measurements• Turbulence must be measured by met masts

28

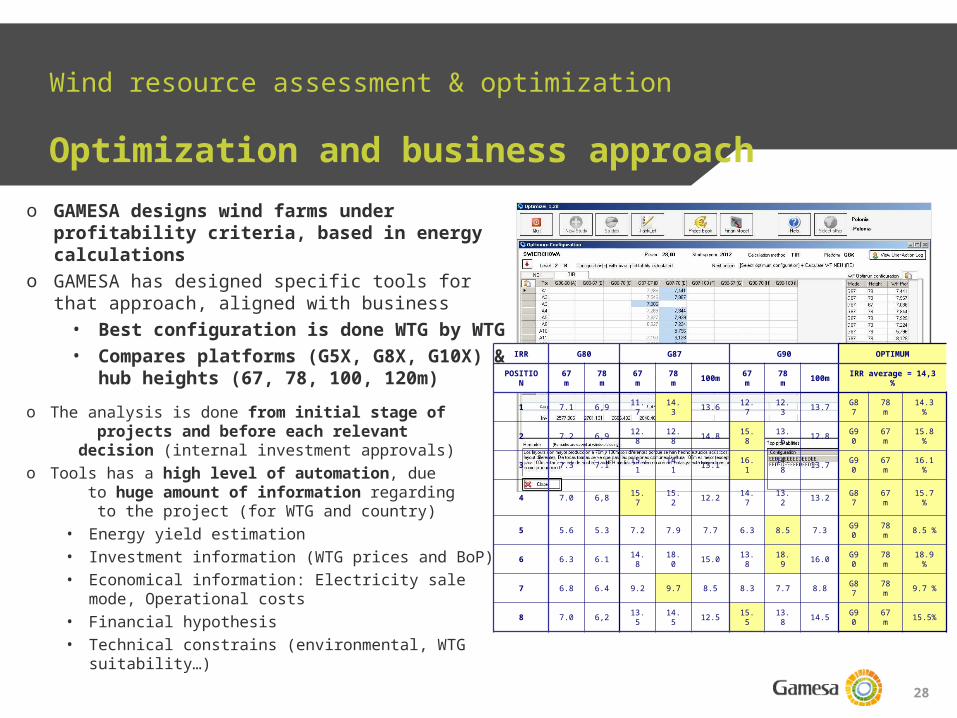

Wind resource assessment & optimization

Optimization and business approach

IRR G80 G87 G90 OPTIMUM

POSITION

67 m

78 m

67 m

78 m

100m

67 m

78 m

100m

IRR average = 14,3 %

1 7.1 6,9 11.7

14.3 13.6 12.

712.3 13.7 G

8778 m

14.3 %

2 7.2 6,9 12.8

12.8 14.8 15.

813.6 12.8 G

9067 m

15.8 %

3 7.3 7.1 15.1

14.1 13.1 16.

114.8 13.7 G

9067 m

16.1 %

4 7.0 6,8 15.7

15.2 12.2 14.

713.2 13.2 G

8767 m

15.7 %

5 5.6 5.3 7.2 7.9 7.7 6.3 8.5 7.3 G90

78 m 8.5 %

6 6.3 6.1 14.8

18.0 15.0 13.

818.9 16.0 G

9078 m

18.9 %

7 6.8 6.4 9.2 9.7 8.5 8.3 7.7 8.8 G87

78 m 9.7 %

8 7.0 6,2 13.5

14.5 12.5 15.

513.8 14.5 G

9067 m

15.5%

o GAMESA designs wind farms under profitability criteria, based in energy calculations

o GAMESA has designed specific tools for that approach, aligned with business

• Best configuration is done WTG by WTG• Compares platforms (G5X, G8X, G10X) &

hub heights (67, 78, 100, 120m)o The analysis is done from initial stage of

projects and before each relevant decision (internal investment approvals)

o Tools has a high level of automation, due to huge amount of information regarding to the project (for WTG and country)

• Energy yield estimation• Investment information (WTG prices and BoP)• Economical information: Electricity sale mode,

Operational costs• Financial hypothesis• Technical constrains (environmental, WTG

suitability…)

29

The importance of wind resource expertise

o Gamesa introduces maximizing profitability criteria from initial stages of the projects

o Site selection and wind resource assessment are difficult tasks which requires complex computer tools and internal know-how

o Gamesa has the needed internal knowledge and expertise to design internal tools, always improving profitability of projects

o Gamesa invests in knowledge to test new technologies for client support with a business approach

30

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline breakdown and balance sheet value

Accounting and financial modeling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

31

Accounting and financial modeling

1

2

3 Accounting example

Example of a recent transaction

Cash flow and P&L through the project life

4

Accounting process

32

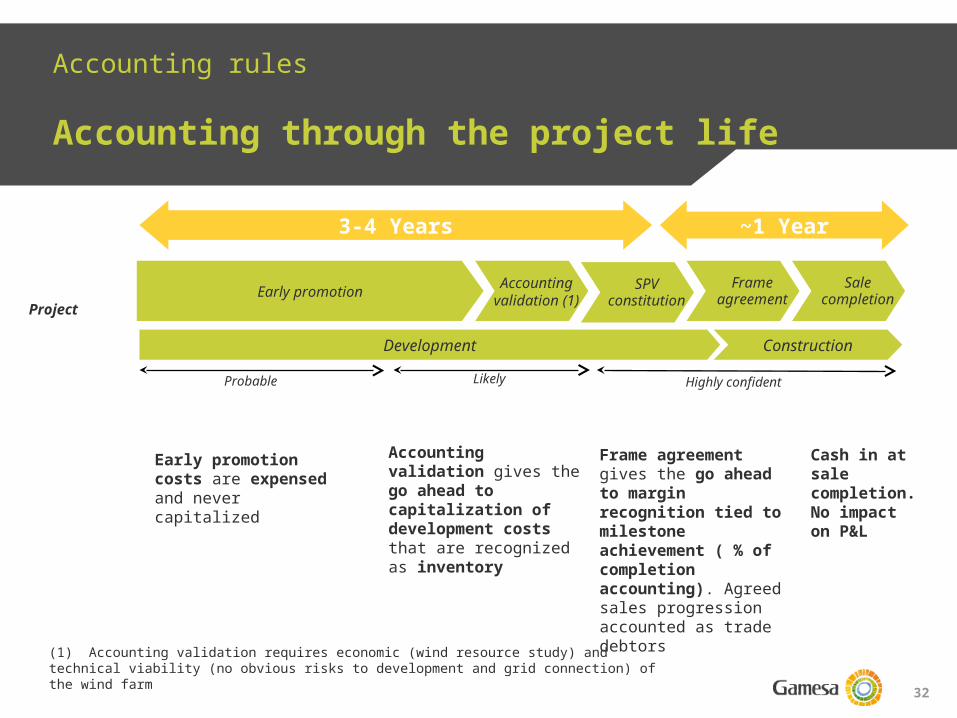

Accounting rules

Accounting through the project life

Early promotion costs are expensed and never capitalized

Accounting validation gives the go ahead to capitalization of development costs that are recognized as inventory

Frame agreement gives the go ahead to margin recognition tied to milestone achievement ( % of completion accounting). Agreed sales progression accounted as trade debtors

Cash in at sale completion. No impact on P&L

(1) Accounting validation requires economic (wind resource study) and technical viability (no obvious risks to development and grid connection) of the wind farm

Accounting validation (1)Early promotion

3-4 Years

Project

Probable Likely Highly confident

SPV constitution

Development Construction

Frame agreement

Sale completion

~1 Year

33

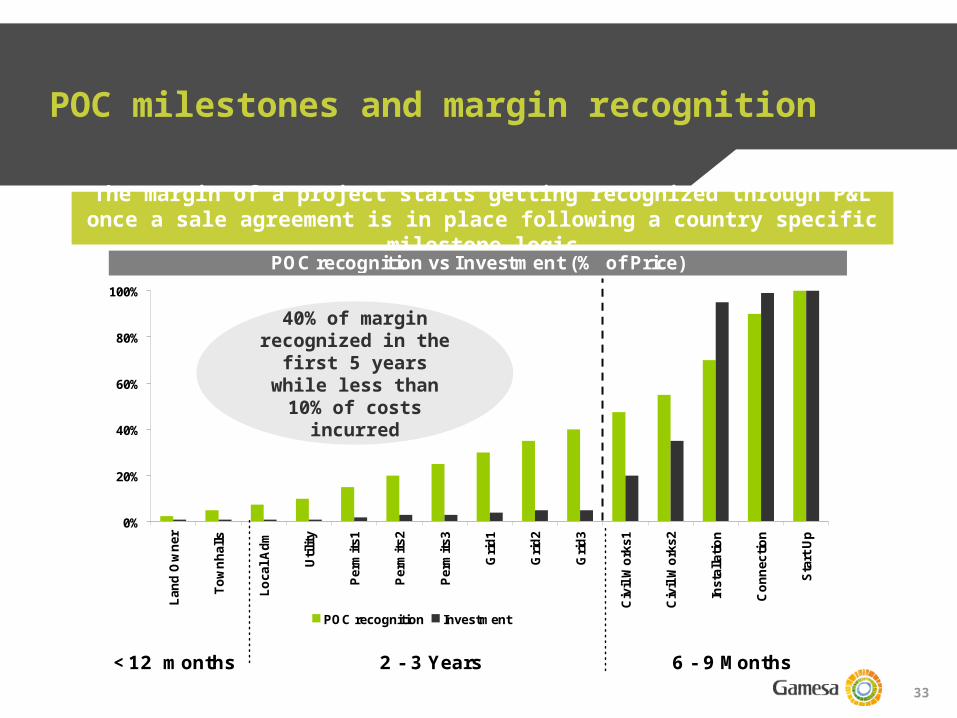

POC milestones and margin recognition

40% of margin recognized in the first 5 years while less than 10% of costs incurred

The margin of a project starts getting recognized through P&L once a sale agreement is in place following a country specific milestone

logic

<12 months

POC recognition vs Investment (% of Price)

2 - 3 Years 6 - 9 Months

0%

20%

40%

60%

80%

100%

Land

Ow

ner

Tow

nhal

ls

Loca

l Adm

Util

ity

Perm

its1

Perm

its2

Perm

its3

Grid

1

Grid

2

Grid

3

Civ

il W

orks

1

Civ

il W

orks

2

Inst

alla

tion

Con

nect

ion

Star

t Up

POC recognition Investment

34

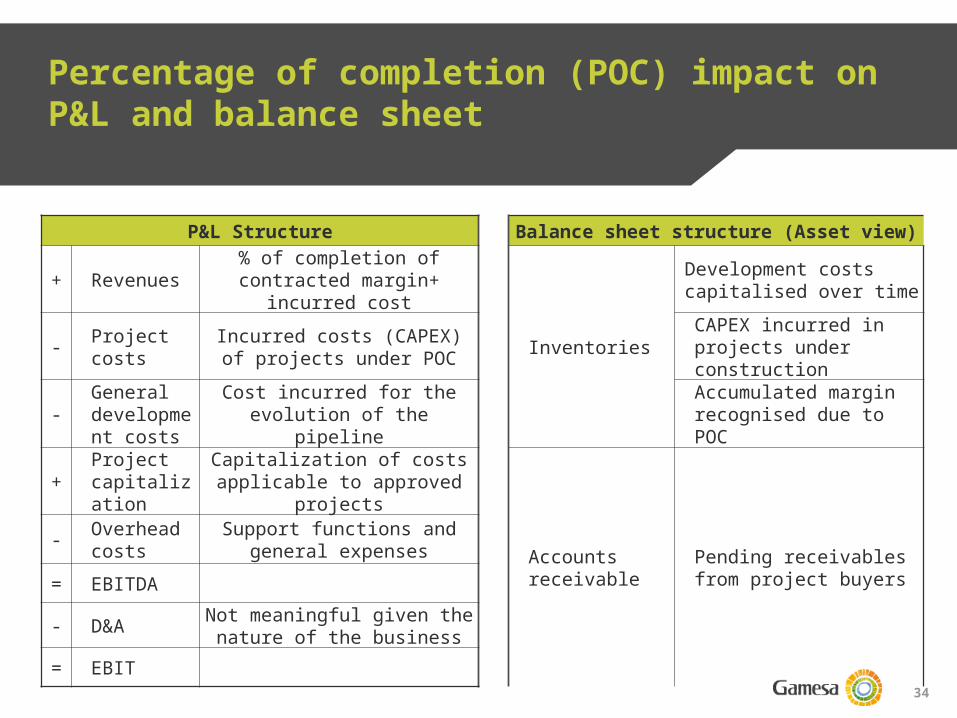

Percentage of completion (POC) impact on P&L and balance sheet

P&L Structure Balance sheet structure (Asset view)

+ Revenues% of completion of

contracted margin+ incurred cost

Inventories

Development costs capitalised over time

- Project costs

Incurred costs (CAPEX) of projects under POC

CAPEX incurred in projects under construction

-General development costs

Cost incurred for the evolution of the pipeline

Accumulated margin recognised due to POC

+Project capitalization

Capitalization of costs applicable to approved

projectsAccounts receivable

Pending receivables from project buyers

- Overhead costs

Support functions and general expenses

= EBITDA- D&A Not meaningful given the

nature of the business= EBIT

35

Accounting and financial modeling

1

2

3 Accounting example

Example of a recent transaction

Cash flow and P&L through the project life

4

Accounting process

36

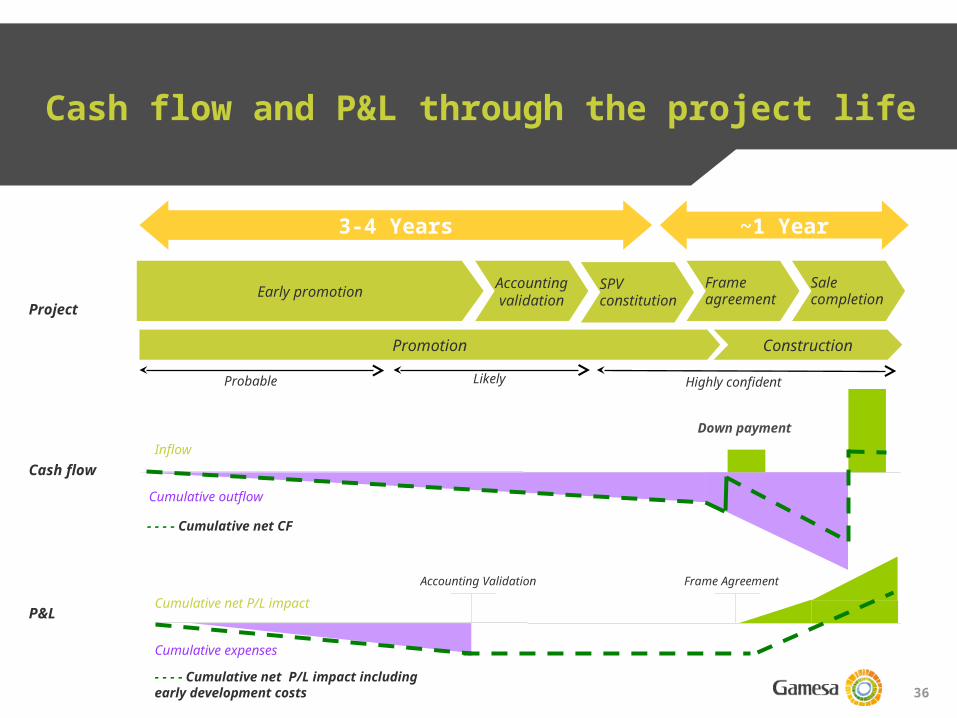

Cash flow and P&L through the project life

Cash flow

P&L

Accounting Validation Frame Agreement

Inflow

Cumulative outflow

Cumulative net P/L impact

Cumulative expenses

Down payment

- - - - Cumulative net CF

Accounting validationEarly promotion

Project

Probable Likely Highly confident

SPV constitution

Promotion Construction

Frame agreement

Sale completion

- - - - Cumulative net P/L impact including early development costs

3-4 Years ~1 Year

37

Accounting and financial modeling

1

2

3 Accounting example

Example of a recent transaction

Cash flow and P&L through the project life

4

Accounting process

38

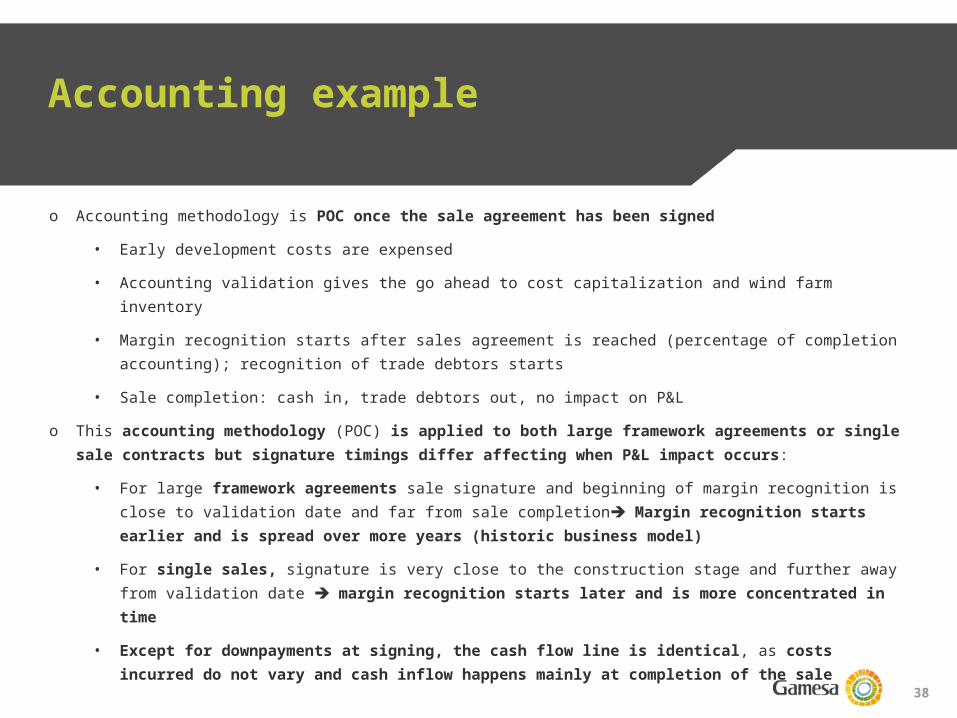

Accounting example

o Accounting methodology is POC once the sale agreement has been signed

• Early development costs are expensed

• Accounting validation gives the go ahead to cost capitalization and wind farm inventory

• Margin recognition starts after sales agreement is reached (percentage of completion accounting); recognition of trade debtors starts

• Sale completion: cash in, trade debtors out, no impact on P&L

o This accounting methodology (POC) is applied to both large framework agreements or single sale contracts but signature timings differ affecting when P&L impact occurs:

• For large framework agreements sale signature and beginning of margin recognition is close to validation date and far from sale completion Margin recognition starts earlier and is spread over more years (historic business model)

• For single sales, signature is very close to the construction stage and further away from validation date margin recognition starts later and is more concentrated in time

• Except for downpayments at signing, the cash flow line is identical, as costs incurred do not vary and cash inflow happens mainly at completion of the sale

39

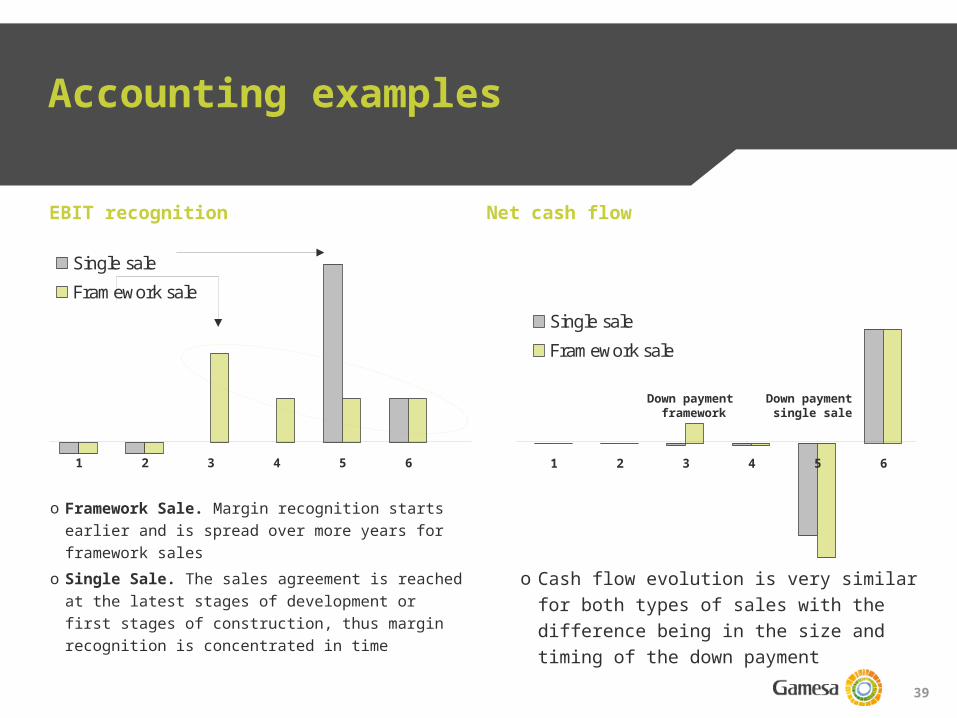

X

Accounting examples

1 2 3 4 5 6

Single saleFramework sale

EBIT recognition

o Framework Sale. Margin recognition starts earlier and is spread over more years for framework sales

o Single Sale. The sales agreement is reached at the latest stages of development or first stages of construction, thus margin recognition is concentrated in time

1 2 3 4 5 6

Single saleFramework sale

Net cash flow

o Cash flow evolution is very similar for both types of sales with the difference being in the size and timing of the down payment

X

xx

Down payment framework

Down payment single sale

40

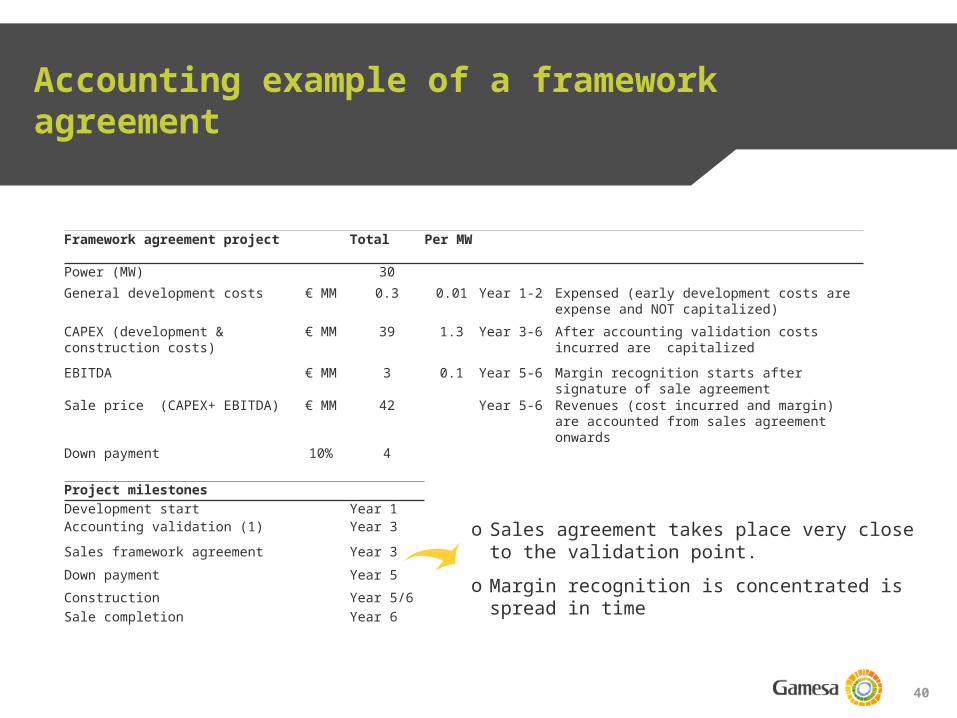

Accounting example of a framework agreement

Framework agreement project Total Per MW

Power (MW) 30General development costs € MM 0.3 0.01 Year 1-2 Expensed (early development costs are

expense and NOT capitalized)CAPEX (development & construction costs)

€ MM 39 1.3 Year 3-6 After accounting validation costs incurred are capitalized

EBITDA € MM 3 0.1 Year 5-6 Margin recognition starts after signature of sale agreement

Sale price (CAPEX+ EBITDA) € MM 42 Year 5-6 Revenues (cost incurred and margin) are accounted from sales agreement onwards

Down payment 10% 4

Project milestonesDevelopment start Year 1Accounting validation (1) Year 3Sales framework agreement Year 3Down payment Year 5Construction Year 5/6Sale completion Year 6

o Sales agreement takes place very close to the validation point.

o Margin recognition is concentrated is spread in time

41

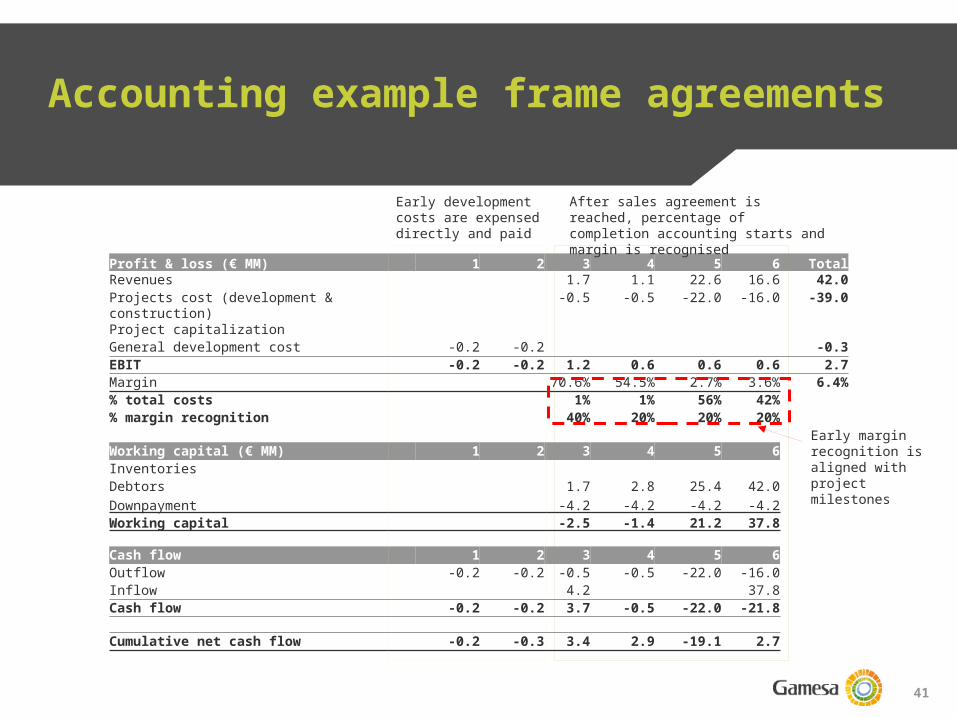

Accounting example frame agreements

Profit & loss (€ MM) 1 2 3 4 5 6 TotalRevenues 1.7 1.1 22.6 16.6 42.0Projects cost (development & construction) -0.5 -0.5 -22.0 -16.0 -39.0Project capitalizationGeneral development cost -0.2 -0.2 -0.3EBIT -0.2 -0.2 1.2 0.6 0.6 0.6 2.7Margin 70.6% 54.5% 2.7% 3.6% 6.4%% total costs 1% 1% 56% 42%% margin recognition 40% 20% 20% 20%

Working capital (€ MM) 1 2 3 4 5 6InventoriesDebtors 1.7 2.8 25.4 42.0Downpayment -4.2 -4.2 -4.2 -4.2Working capital -2.5 -1.4 21.2 37.8

Cash flow 1 2 3 4 5 6Outflow -0.2 -0.2 -0.5 -0.5 -22.0 -16.0Inflow 4.2 37.8Cash flow -0.2 -0.2 3.7 -0.5 -22.0 -21.8

Cumulative net cash flow -0.2 -0.3 3.4 2.9 -19.1 2.7

Early development costs are expensed directly and paid

After sales agreement is reached, percentage of completion accounting starts and margin is recognised

Early margin recognition is aligned with project milestones

42

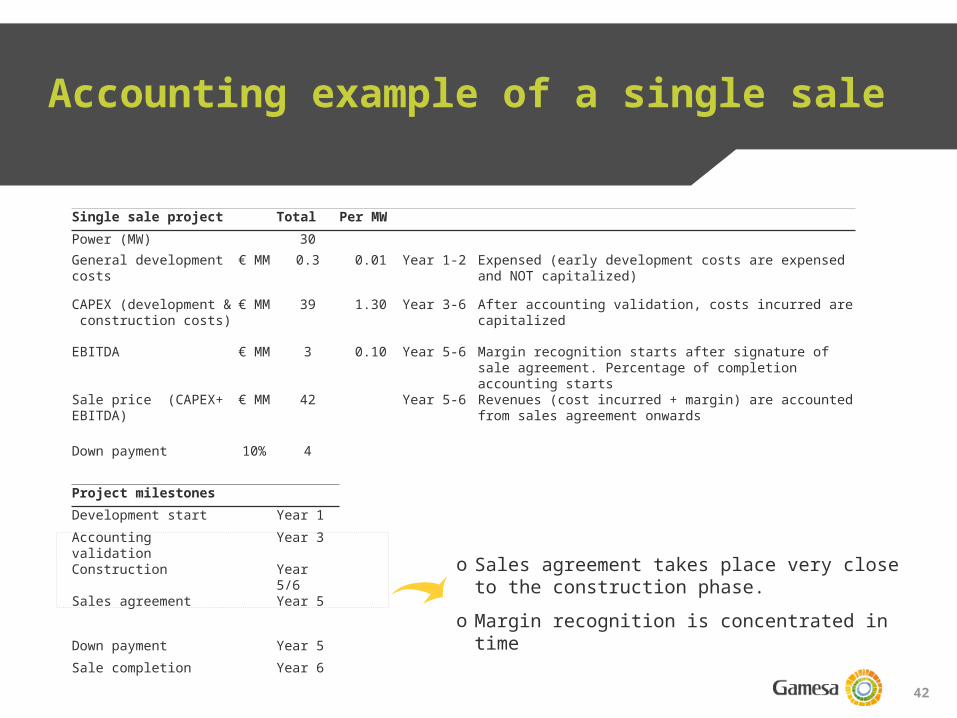

Accounting example of a single sale

Single sale project Total Per MWPower (MW) 30General development costs

€ MM 0.3 0.01 Year 1-2 Expensed (early development costs are expensed and NOT capitalized)

CAPEX (development & construction costs)

€ MM 39 1.30 Year 3-6 After accounting validation, costs incurred are capitalized

EBITDA € MM 3 0.10 Year 5-6 Margin recognition starts after signature of sale agreement. Percentage of completion accounting starts

Sale price (CAPEX+ EBITDA)

€ MM 42 Year 5-6 Revenues (cost incurred + margin) are accounted from sales agreement onwards

Down payment 10% 4

Project milestonesDevelopment start Year 1Accounting validation Year 3Construction Year 5/6Sales agreement Year 5

Down payment Year 5Sale completion Year 6

o Sales agreement takes place very close to the construction phase.

o Margin recognition is concentrated in time

43

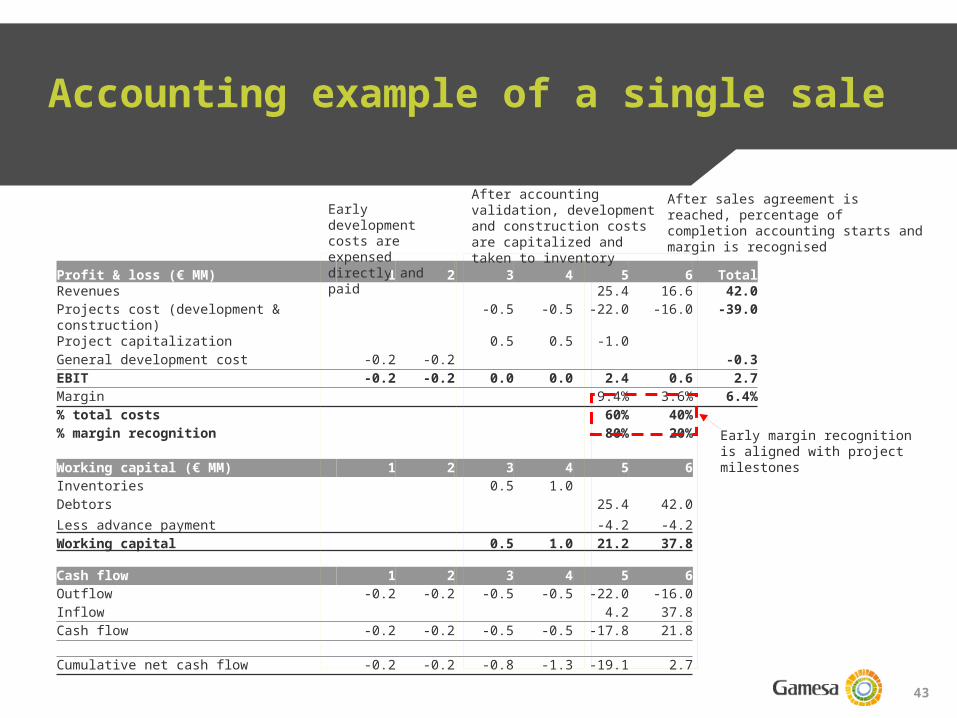

Accounting example of a single sale

Profit & loss (€ MM) 1 2 3 4 5 6 TotalRevenues 25.4 16.6 42.0Projects cost (development & construction)

-0.5 -0.5 -22.0 -16.0 -39.0

Project capitalization 0.5 0.5 -1.0General development cost -0.2 -0.2 -0.3EBIT -0.2 -0.2 0.0 0.0 2.4 0.6 2.7Margin 9.4% 3.6% 6.4%% total costs 60% 40%% margin recognition 80% 20%

Working capital (€ MM) 1 2 3 4 5 6Inventories 0.5 1.0Debtors 25.4 42.0Less advance payment -4.2 -4.2Working capital 0.5 1.0 21.2 37.8

Cash flow 1 2 3 4 5 6Outflow -0.2 -0.2 -0.5 -0.5 -22.0 -16.0Inflow 4.2 37.8Cash flow -0.2 -0.2 -0.5 -0.5 -17.8 21.8

Cumulative net cash flow -0.2 -0.2 -0.8 -1.3 -19.1 2.7

Early development costs are expensed directly and paid

After accounting validation, development and construction costs are capitalized and taken to inventory

After sales agreement is reached, percentage of completion accounting starts and margin is recognised

Early margin recognition is aligned with project milestones

44

Accounting and financial modeling

1

2

3 Accounting example

Example of a recent transaction

Cash flow and P&L through the project life

4

Accounting process

45

Final cash in cleans balance

sheet with no P&L impact

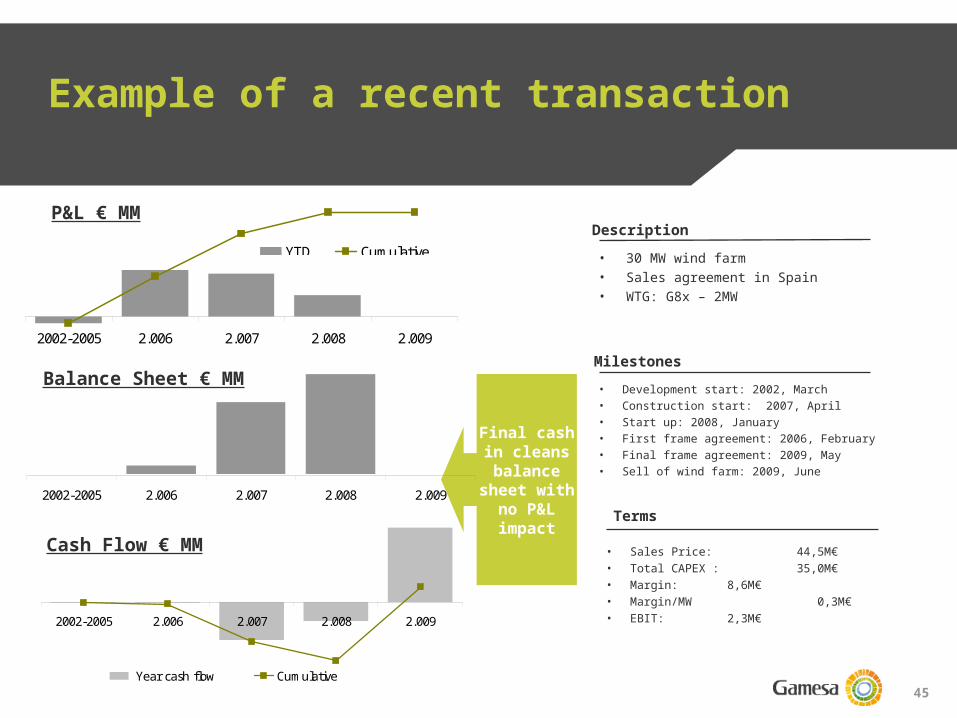

Example of a recent transaction

2002-2005 2.006 2.007 2.008 2.009

YTD Cumulative

2002-2005 2.006 2.007 2.008 2.009

Year cash flow Cumulative

• 30 MW wind farm• Sales agreement in Spain• WTG: G8x – 2MW

Description

Milestones• Development start: 2002, March• Construction start: 2007, April• Start up: 2008, January• First frame agreement: 2006, February• Final frame agreement: 2009, May• Sell of wind farm: 2009, June

Terms

• Sales Price: 44,5M€• Total CAPEX : 35,0M€• Margin: 8,6M€• Margin/MW 0,3M€• EBIT: 2,3M€

2002-2005 2.006 2.007 2.008 2.009

Cash Flow € MM

P&L € MM

Balance Sheet € MM

46

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline breakdown and balance sheet value

Accounting and financial modeling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

47

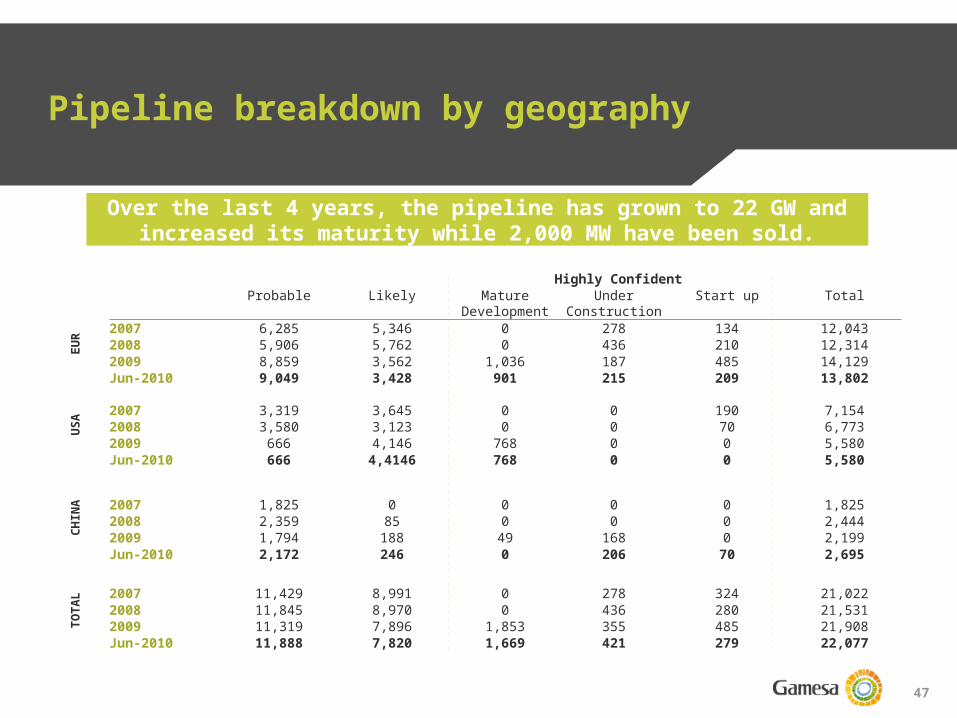

Pipeline breakdown by geography

Highly ConfidentProbable Likely Mature

DevelopmentUnder

ConstructionStart up Total

2007 6,285 5,346 0 278 134 12,0432008 5,906 5,762 0 436 210 12,3142009 8,859 3,562 1,036 187 485 14,129Jun-2010 9,049 3,428 901 215 209 13,802

2007 3,319 3,645 0 0 190 7,1542008 3,580 3,123 0 0 70 6,7732009 666 4,146 768 0 0 5,580Jun-2010 666 4,4146 768 0 0 5,580

2007 1,825 0 0 0 0 1,8252008 2,359 85 0 0 0 2,4442009 1,794 188 49 168 0 2,199Jun-2010 2,172 246 0 206 70 2,695

2007 11,429 8,991 0 278 324 21,0222008 11,845 8,970 0 436 280 21,5312009 11,319 7,896 1,853 355 485 21,908Jun-2010 11,888 7,820 1,669 421 279 22,077

EUR

CHIN

AU

SATO

TAL

Over the last 4 years, the pipeline has grown to 22 GW and increased its maturity while 2,000 MW have been sold.

48

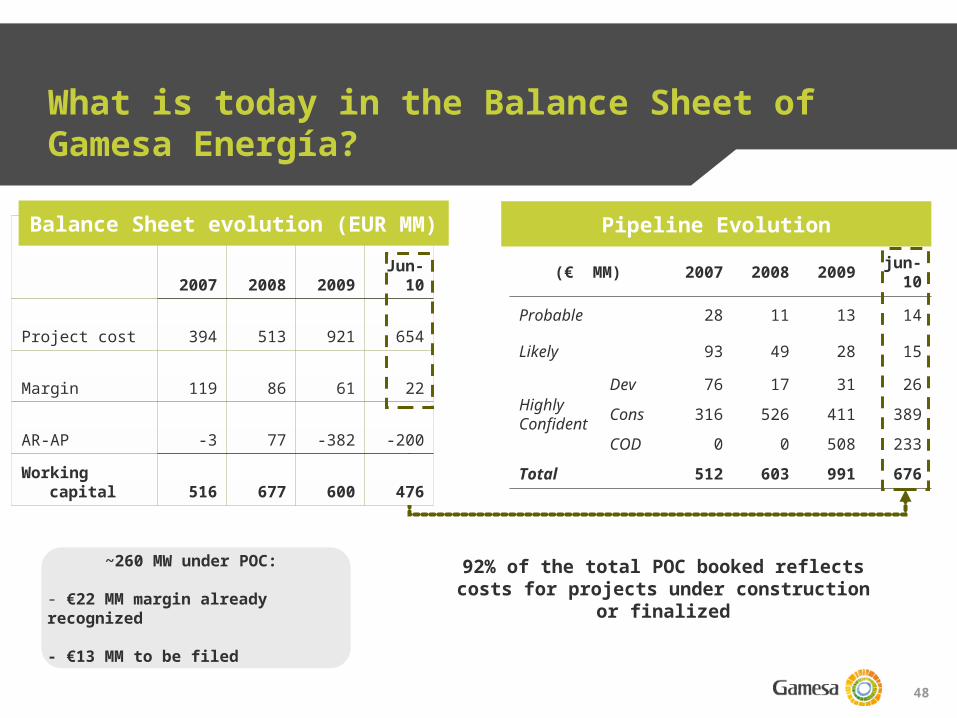

What is today in the Balance Sheet of Gamesa Energía?

2007 2008 2009

Jun-10

Project cost 394 513 921 654

Margin 119 86 61 22

AR-AP -3 77 -382 -200Working

capital 516 677 600 476

Balance Sheet evolution (EUR MM) Pipeline Evolution

(€ MM) 2007 2008 2009 jun-10

Probable 28 11 13 14

Likely 93 49 28 15

Highly Confident

Dev 76 17 31 26Cons 316 526 411 389COD 0 0 508 233

Total 512 603 991 676

92% of the total POC booked reflects costs for projects under construction or

finalized

~260 MW under POC:

- €22 MM margin already recognized

- €13 MM to be filed

49

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline description and evolution

Accounting and financial modeling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

50

Gamesa Energia strategy

Integration vs. pure play1

2

3

4 Agreement with Iberdrola Renovables

Value creation opportunities

Strategy by geographic area

51

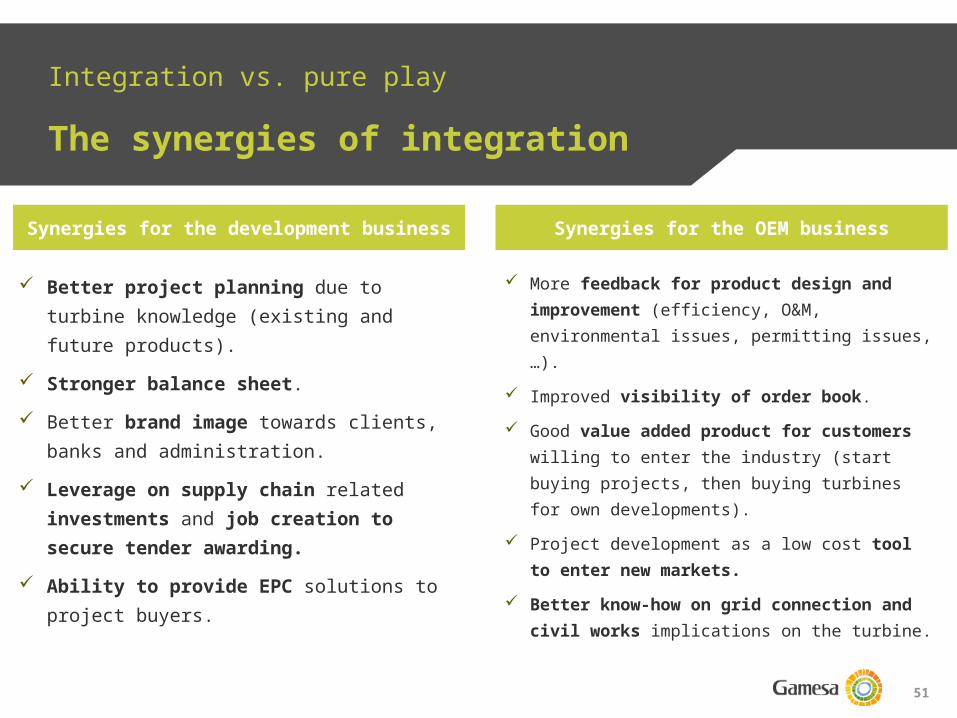

Integration vs. pure play

The synergies of integration

Synergies for the development business Synergies for the OEM business

Better project planning due to turbine knowledge (existing and future products).

Stronger balance sheet. Better brand image towards clients, banks

and administration. Leverage on supply chain related

investments and job creation to secure tender awarding.

Ability to provide EPC solutions to project buyers.

More feedback for product design and improvement (efficiency, O&M, environmental issues, permitting issues, …).

Improved visibility of order book. Good value added product for

customers willing to enter the industry (start buying projects, then buying turbines for own developments).

Project development as a low cost tool to enter new markets.

Better know-how on grid connection and civil works implications on the turbine.

52

Gamesa Energia strategy

Integration vs. pure play1

2

3

4 Agreement with Iberdrola Renovables

Value creation opportunities

Strategy by geographic area

53

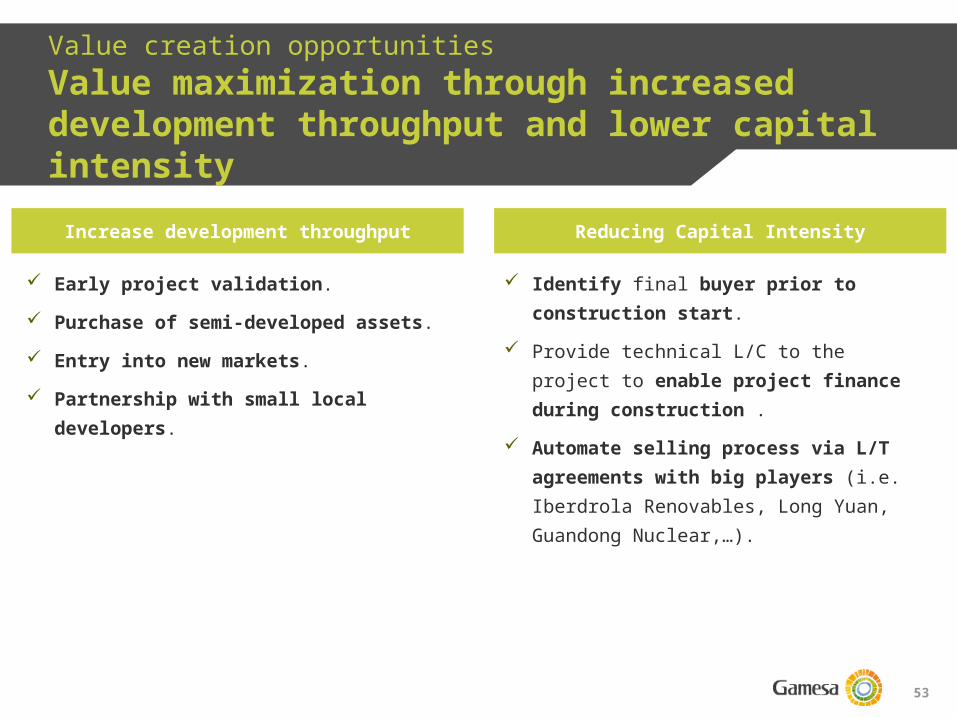

Value creation opportunitiesValue maximization through increased development throughput and lower capital intensityIncrease development throughput Reducing Capital Intensity

Early project validation. Purchase of semi-developed assets. Entry into new markets. Partnership with small local

developers.

Identify final buyer prior to construction start.

Provide technical L/C to the project to enable project finance during construction .

Automate selling process via L/T agreements with big players (i.e. Iberdrola Renovables, Long Yuan, Guandong Nuclear,…).

54

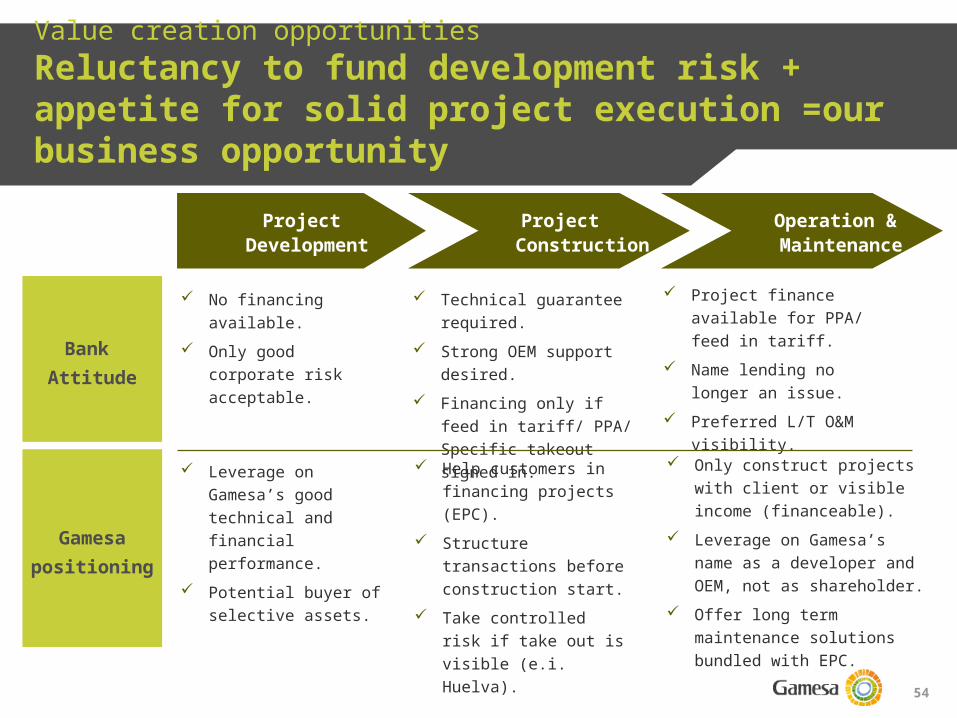

Value creation opportunitiesReluctancy to fund development risk + appetite for solid project execution =our business opportunity

No financing available.

Only good corporate risk acceptable.

Project Development

Project Construction

Bank Attitude

Gamesapositioning

Operation & Maintenance

Leverage on Gamesa’s good technical and financial performance.

Potential buyer of selective assets.

Technical guarantee required.

Strong OEM support desired.

Financing only if feed in tariff/ PPA/ Specific takeout signed in.

Project finance available for PPA/ feed in tariff.

Name lending no longer an issue.

Preferred L/T O&M visibility.

Help customers in financing projects (EPC).

Structure transactions before construction start.

Take controlled risk if take out is visible (e.i. Huelva).

Only construct projects with client or visible income (financeable).

Leverage on Gamesa’s name as a developer and OEM, not as shareholder.

Offer long term maintenance solutions bundled with EPC.

55

Gamesa Energia strategy

Integration vs. pure play1

2

3

4 Agreement with Iberdrola Renovables

Value creation opportunities

Strategy by geographic area

56

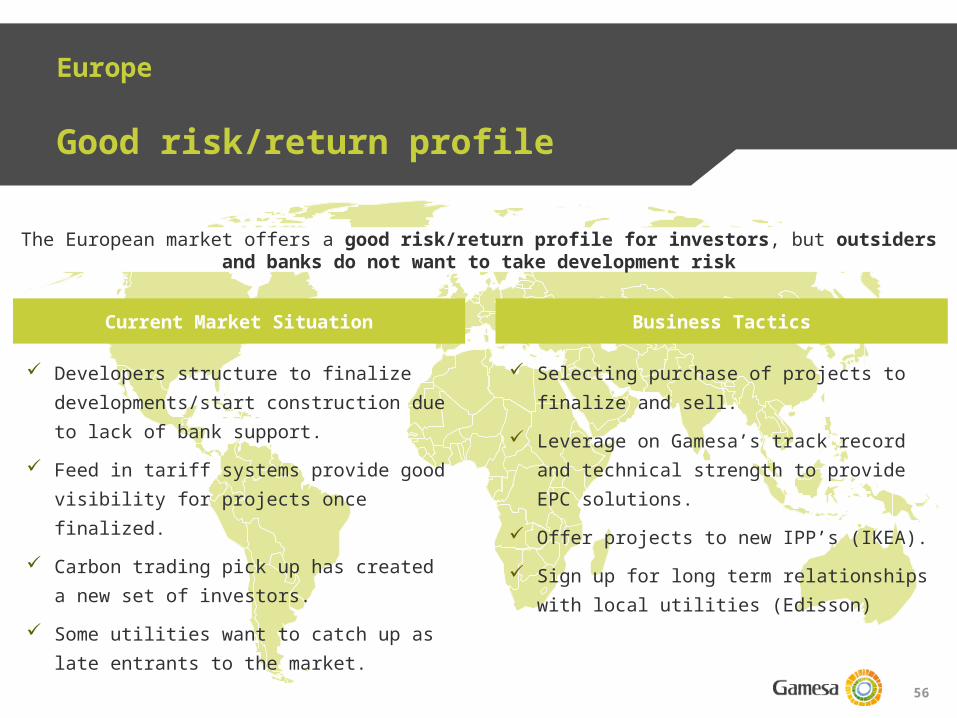

Europe

Good risk/return profile

Current Market Situation Business Tactics

Developers structure to finalize developments/start construction due to lack of bank support.

Feed in tariff systems provide good visibility for projects once finalized.

Carbon trading pick up has created a new set of investors.

Some utilities want to catch up as late entrants to the market.

Selecting purchase of projects to finalize and sell.

Leverage on Gamesa’s track record and technical strength to provide EPC solutions.

Offer projects to new IPP’s (IKEA). Sign up for long term relationships with

local utilities (Edisson)

The European market offers a good risk/return profile for investors, but outsiders and banks do not want to take development risk

57

USA

PPAs are the key challenge

Current Market Situation Business Tactics

Low cost of Natural Gas keeps power prices low to historical levels.

A significant amount of developers are struggling due to lack of financing.

Utilities still lacking green assets to achieve RPS required levels.

Cash grant expires in December 2010.

Accelerate development in areas of high energy consumptions (higher energy prices).

Selecting project acquisition to speed up development.

Approach utilities looking to purchase projects to own and operate (no need for PPA).

Start construction of feasible projects during 2010.

The key challenge is finding acceptable PPAs to make projects appealing for the financing banks

58

ChinaUnder-penetrated market with strong growth opportunities

Current Market Situation Business Tactics

Only 4 utilities investing in projects massively.

New utilities starting to develop from scratch want to catch up.

Turbine demand for foreign manufacturers limited to 20% of total local demand.

Kyoto protocol (CDM) forces to have Chinese company controlling the project to access Green Certificates.

Offer our projects as a tool to accelerate entrance to a sizeable installed base.

Increase turbine demand by selling projects developed by Gamesa.

Continue talks to foreign investors to measure the value of the project without CDM.

The Chinese market is booking with very few players and new local utilities starting to grow

59

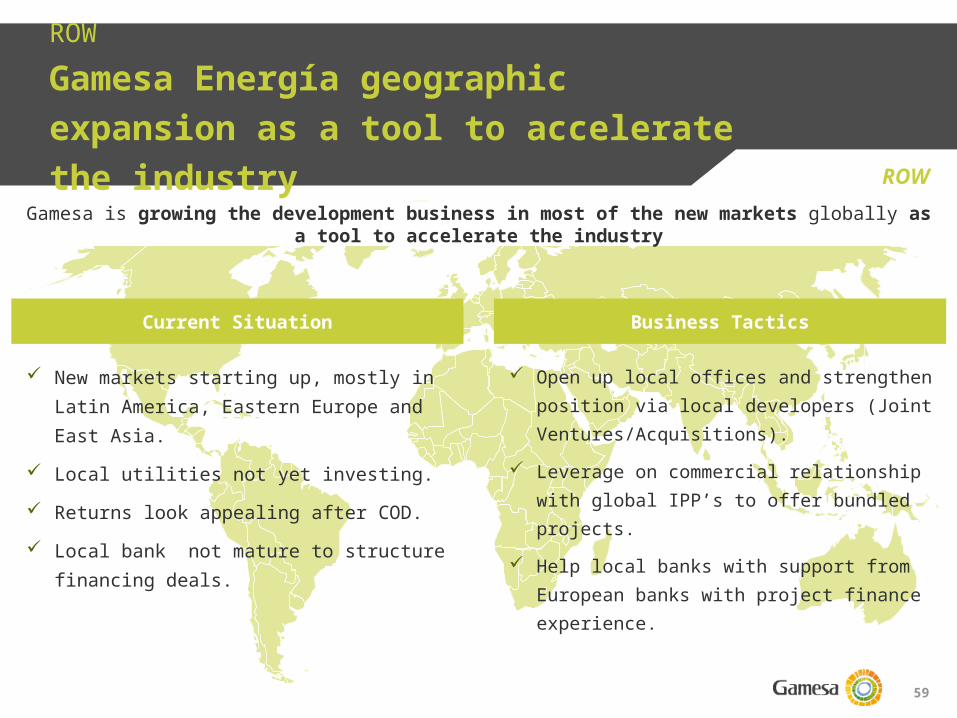

ROWGamesa Energía geographic expansion as a tool to accelerate the industry ROW

Current Situation Business Tactics

New markets starting up, mostly in Latin America, Eastern Europe and East Asia.

Local utilities not yet investing. Returns look appealing after COD. Local bank not mature to structure

financing deals.

Open up local offices and strengthen position via local developers (Joint Ventures/Acquisitions).

Leverage on commercial relationship with global IPP’s to offer bundled projects.

Help local banks with support from European banks with project finance experience.

Gamesa is growing the development business in most of the new markets globally as a tool to accelerate the industry

60

Gamesa Energia strategy

Integration vs. pure play1

2

3

4 Agreement with Iberdrola Renovables

Value creation opportunities

Strategy by geographic area

61

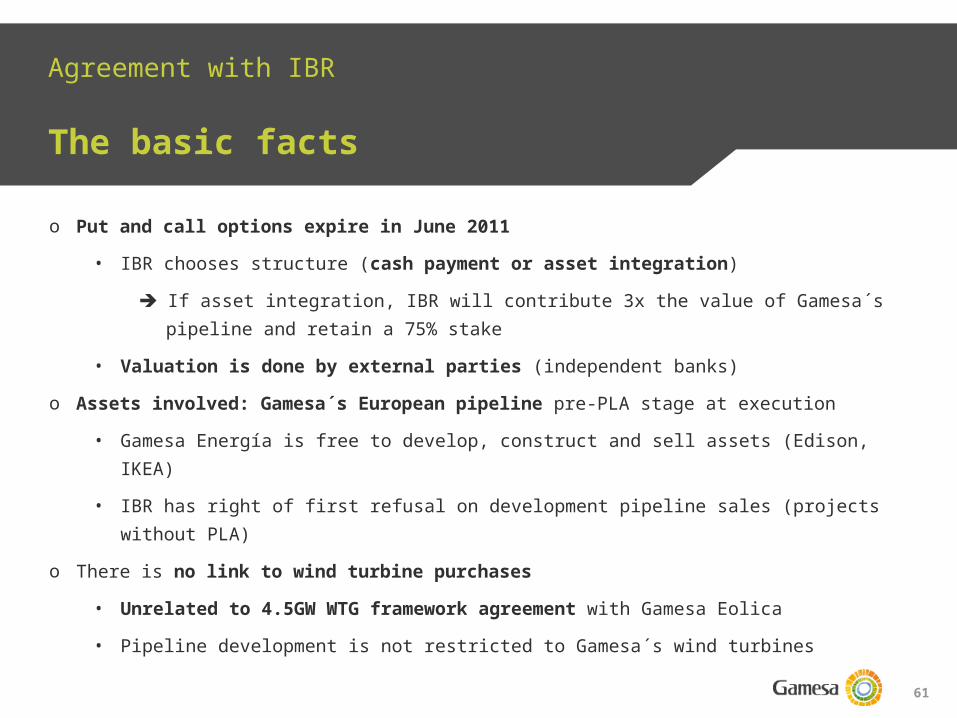

Agreement with IBR

The basic facts

o Put and call options expire in June 2011

• IBR chooses structure (cash payment or asset integration) If asset integration, IBR will contribute 3x the value of Gamesa´s pipeline and

retain a 75% stake• Valuation is done by external parties (independent banks)

o Assets involved: Gamesa´s European pipeline pre-PLA stage at execution• Gamesa Energía is free to develop, construct and sell assets (Edison, IKEA)• IBR has right of first refusal on development pipeline sales (projects without PLA)

o There is no link to wind turbine purchases

• Unrelated to 4.5GW WTG framework agreement with Gamesa Eolica• Pipeline development is not restricted to Gamesa´s wind turbines

62

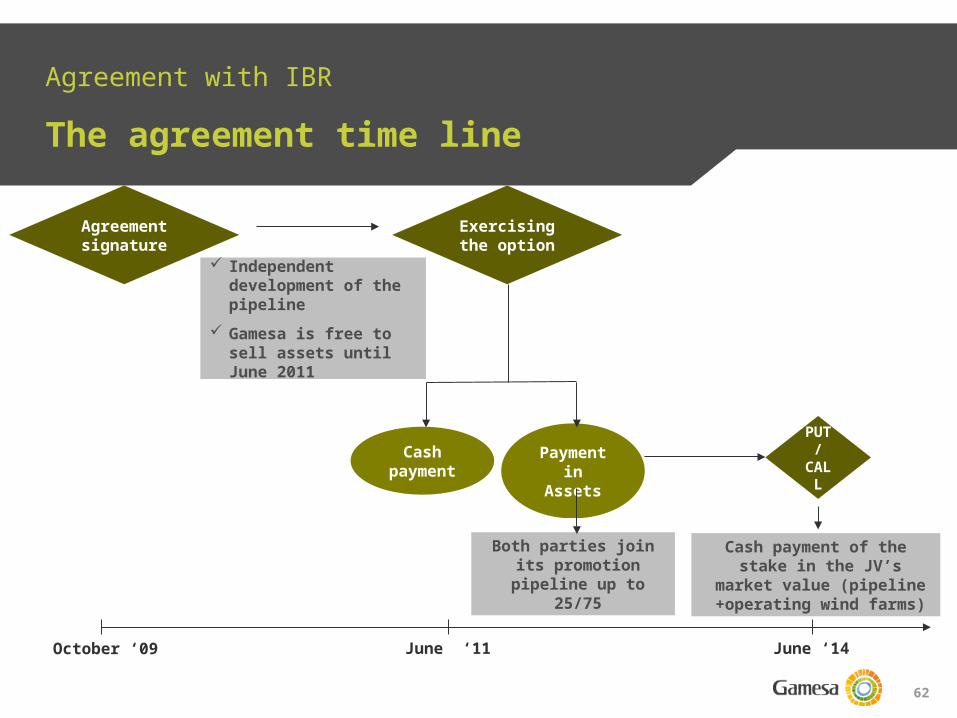

Agreement with IBR

The agreement time line

June ‘11October ‘09 June ‘14

Agreement

signatureExercising the option

PUT /

CALL

Cash payment of the stake in the JV’s market

value (pipeline +operating wind farms)

Payment in Assets

Independent development of the pipeline

Gamesa is free to sell assets until June 2011

Both parties join its promotion pipeline

up to 25/75

Cash payment

63

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline description and evolution

Accounting and financial modelling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

64

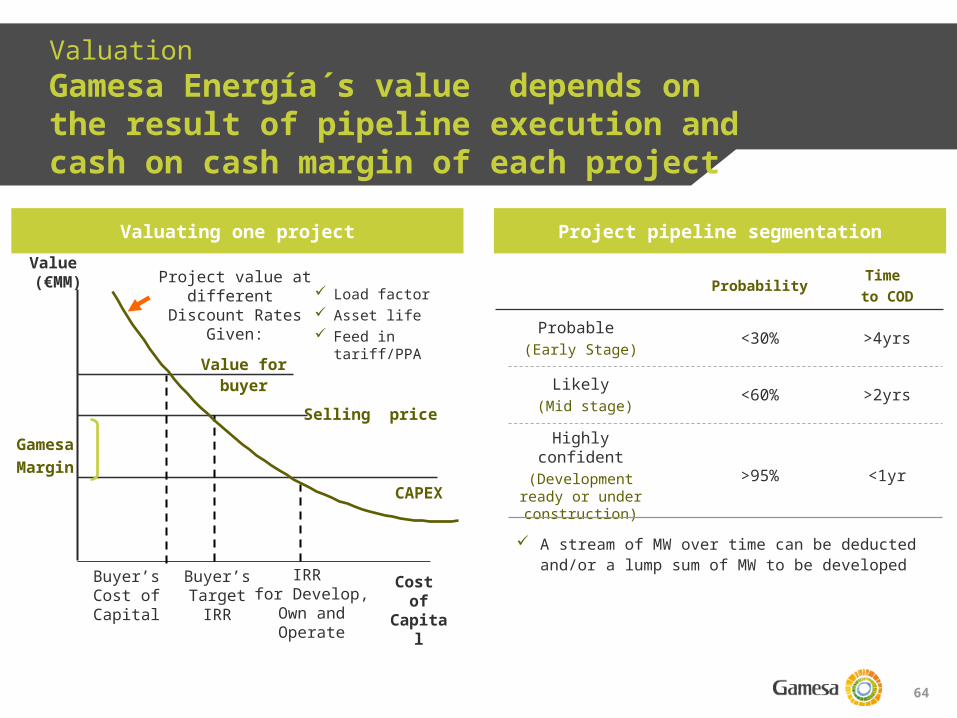

Probability Time to COD

Probable (Early Stage) <30% >4yrs

Likely (Mid stage) <60% >2yrs

Highly confident(Development ready

or under construction)

>95% <1yr

ValuationGamesa Energía´s value depends on the result of pipeline execution and cash on cash margin of each project

Valuating one project Project pipeline segmentation

A stream of MW over time can be deducted and/or a lump sum of MW to be developedBuyer’s

Cost ofCapital

Buyer’sTarget

IRR

IRR for Develop,

Own and Operate

Cost of

Capital

Project value at different

Discount Rates Given:

Selling price

CAPEX

Value forbuyer

Value (€MM)

Load factor Asset life Feed in tariff/PPA

GamesaMargin

65

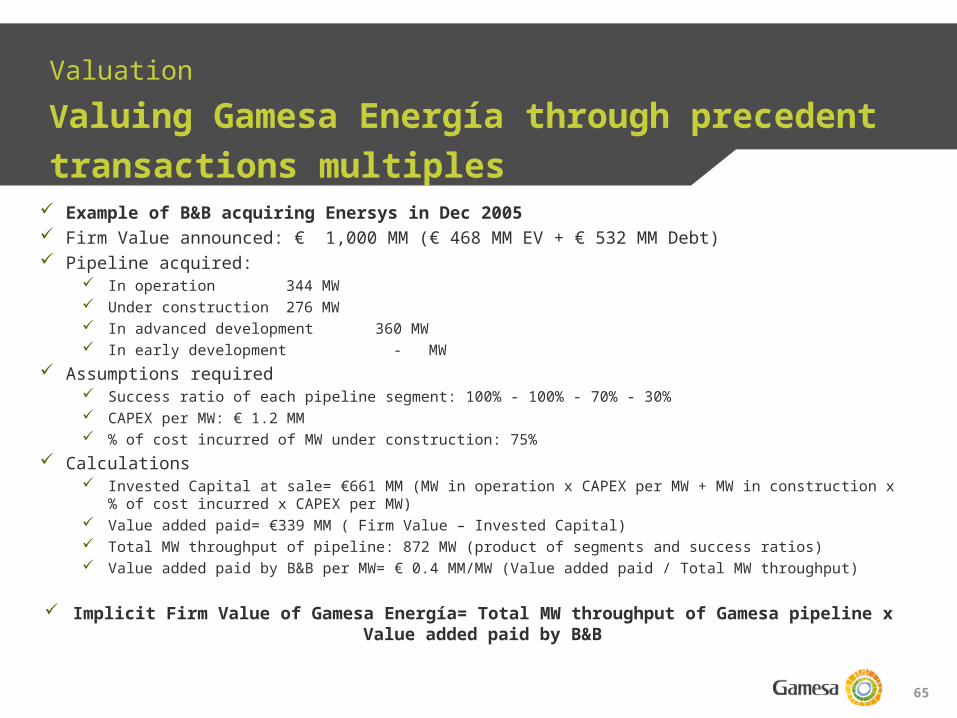

ValuationValuing Gamesa Energía through precedent transactions multiples

Example of B&B acquiring Enersys in Dec 2005 Firm Value announced: € 1,000 MM (€ 468 MM EV + € 532 MM Debt) Pipeline acquired:

In operation 344 MW Under construction 276 MW In advanced development 360 MW In early development - MW

Assumptions required Success ratio of each pipeline segment: 100% - 100% - 70% - 30% CAPEX per MW: € 1.2 MM % of cost incurred of MW under construction: 75%

Calculations Invested Capital at sale= €661 MM (MW in operation x CAPEX per MW + MW in construction x % of cost

incurred x CAPEX per MW) Value added paid= €339 MM ( Firm Value – Invested Capital) Total MW throughput of pipeline: 872 MW (product of segments and success ratios) Value added paid by B&B per MW= € 0.4 MM/MW (Value added paid / Total MW throughput)

Implicit Firm Value of Gamesa Energía= Total MW throughput of Gamesa pipeline x Value added paid by B&B

66

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline description and evolution

Accounting and financial modelling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

67

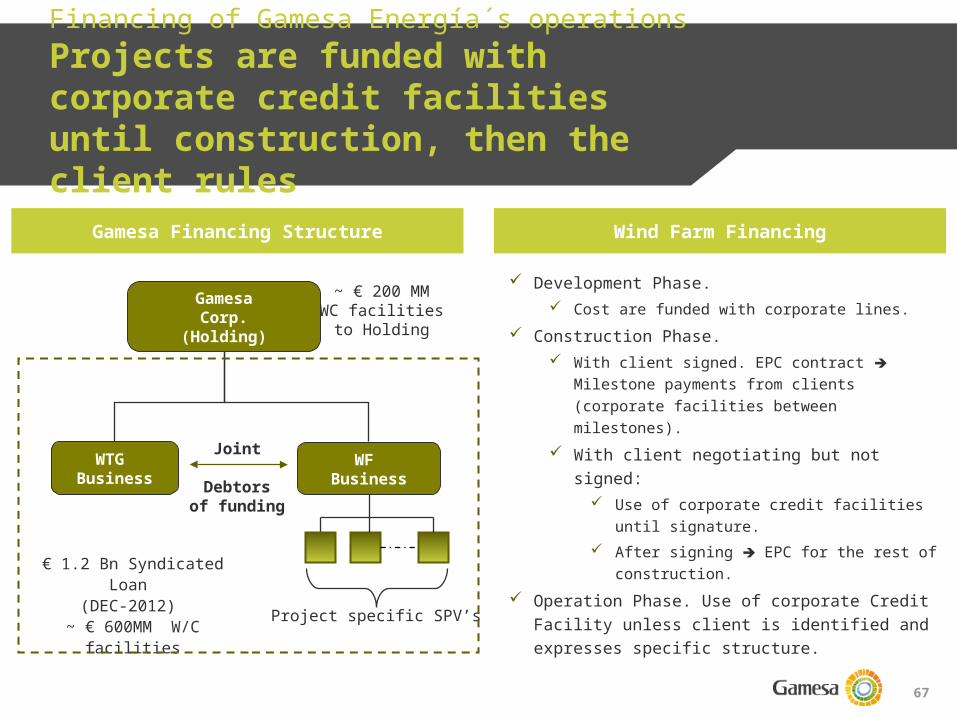

Financing of Gamesa Energía´s operationsProjects are funded with corporate credit facilities until construction, then the client rules

Gamesa Financing Structure Wind Farm Financing

Development Phase. Cost are funded with corporate lines.

Construction Phase. With client signed. EPC contract

Milestone payments from clients (corporate facilities between milestones).

With client negotiating but not signed: Use of corporate credit facilities

until signature. After signing EPC for the rest of

construction. Operation Phase. Use of corporate Credit

Facility unless client is identified and expresses specific structure.

GamesaCorp.

(Holding)

WTG Business

WF Business

~ € 200 MMWC facilitiesto Holding

Joint

Debtorsof funding

€ 1.2 Bn Syndicated Loan

(DEC-2012) ~ € 600MM W/C

facilitiesProject specific SPV’s

68

Table of contents

1

2

3

4

Business model and value generation alternatives

Gamesa Energía pipeline description and evolution

Accounting and financial modelling

History of Gamesa Energía

5

6

Strategy

Valuation

7

Conclusions8

Financing

69

Conclusions

o Gamesa Energía is a leading WF developer with 3,500 MW constructed over 15 years and strong synergies with the OEM business

o The value of Gamesa Energía relies on a 22GW pipeline and a track record of more than 450 MW developed and constructed per year

o The company has a strong balance sheet with assets (€ 476 MM) associated to mature projects under construction or in operation (680 MW)

o The strategy of the company is to sell projects recurrently, not being an IPPo The geographical spread of the pipeline mitigates riskso The company is seeking value enhancing strategies through geographical

growth, selective development pipeline acquisition and new financing structures

70

Questions & Answers

Muchas GraciasThank you

谢谢!

71

“This material has been prepared by Gamesa Corporación Tecnológica, S.A., and is disclosed solely as information.This material may contain declarations which constitute forward-looking statements, and includes references to our current intentions, beliefs orexpectations regarding future events and trends that may affect our financial condition, earnings and share value.These forward-looking statements do not constitute a warranty as to future performance and imply risks and uncertainties. Therefore, actual resultsmay differ materially from those expressed or implied by the forward-looking statements, due to different factors, risks an uncertainties, such aseconomical, competitive, regulatory or commercial changes. The potential investor should assume the fact that the value of any investment may rise orgo down, and furthermore, it may not be recovered, partially or completely. Likewise, past performance is not indicative of future results.The facts, opinions, and forecasts included in this material are furnished as to the date of this document, and are based on the company’s estimationsand on sources believed to be reliable by Gamesa Corporación Tecnológica, S.A., but the company does not warrant its completeness, timeliness oraccuracy, and therefore it should not be relied upon as if it were.Both the information and the conclusions contained in this document are subject to changes without notice. Gamesa Corporación Tecnológica, S.A.undertakes no obligation to update forward-looking statements to reflect events or circumstances that occur after the date the statements were made.The results and evolution of the company may differ materially from those expressed in this material.None of the information contained in this document constitutes a recommendation, solicitation or offer to buy or sell any securities, futures, options orother financial instruments or provide any investment advice or service. This material does not provide any recommendation of investment, or legal, taxor any other type of advise, and it should not be relied upon to make any investment or decision.Any and all the decisions taken by any third party as a result of the information, materials or reports contained in this document, are the sole andexclusive risk and responsibility of that third party, and Gamesa Corporación Tecnológica, S.A. shall not be responsible for any damages derived fromthe use of this document or its content.This document has been furnished exclusively as information, and it must not be disclosed, published or distributed, partially or totally, without the priorwritten consent of Gamesa Corporación Tecnológica, S.A.The images captured by Gamesa in the work environment or at corporate events are solely used for professional purposes to inform third parties aboutcorporate activities and to illustrate them.English version for information purposes only. In case of doubt the Spanish version will prevail.”

Disclaimer