Embed Size (px)

Citation preview

Building the future

Stine Bosse – CEO UBS - Stockholm

2 September 2010

Presentation can bedownloaded at Tryg.com

2

Disclaimer

Certain statements in this presentation are based on the beliefs of our management as well as assumptions made by

and information currently available to the management. Forward-looking statements (other than statements of

historical fact) regarding our future results of operations, financial condition, cash flows, business strategy, plans and

future objectives can generally be identified by terminology such as “targets”, “believes”, “expects”, “aims”, “intends”,

“plans”, “seeks”, “will”, “may”, ”anticipates”, “continues” or similar expressions.

A number of different factors may cause the actual performance to deviate significantly from the forward-looking

statements in this presentation including but not limited to general economic developments, changes in the

competitive environment, developments in the financial markets, extraordinary events such as natural disasters or

terrorist attacks, changes in legislation or case law and reinsurance.

We urge you to read our annual report available on tryg.com for a discussion of some of the factors that could affect

our future performance and the industry in which we operate.

Should one or more of these risks or uncertainties materialise or should any underlying assumptions prove to be

incorrect, our actual financial condition or results of operations could materially differ from that described herein as

anticipated, believed, estimated or expected.

We are not under any duty to update any of the forward-looking statements or to conform such statements to actual

results, except as may be required by law.

3

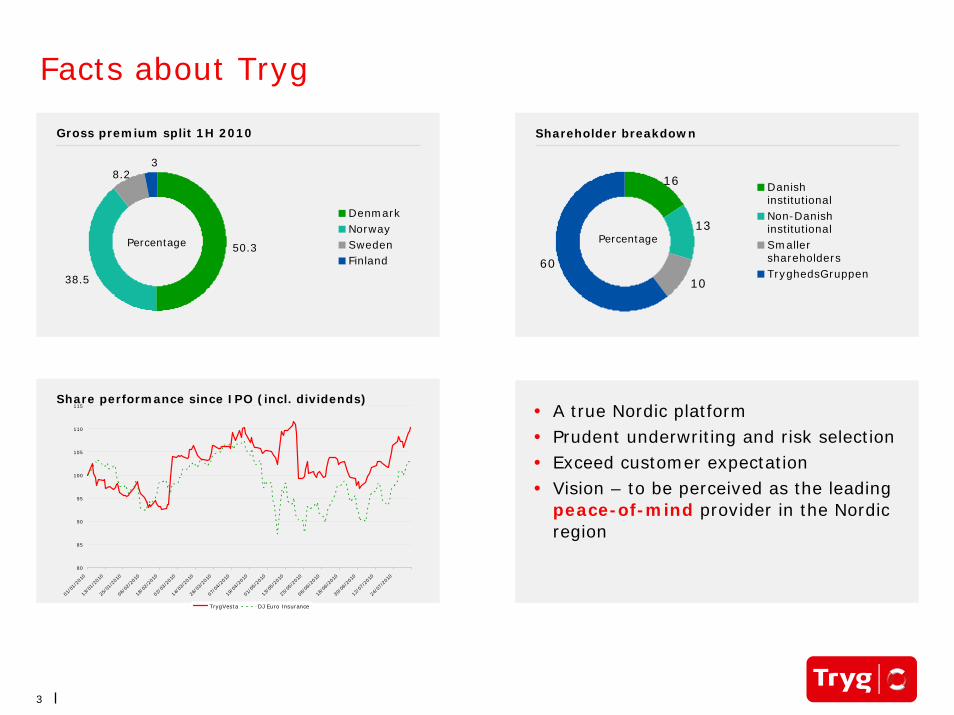

Share performance since IPO (incl. dividends)

Shareholder breakdown

Facts about Tryg

• A true Nordic platform • Prudent underwriting and risk selection • Exceed customer expectation • Vision – to be perceived as the leading

peace-of-mind provider in the Nordic region

Gross premium split 1H 2010

38.2

38.5

50.3

DenmarkNorwaySwedenFinland

Percentage

16

13

10

60

Danishinstitutional Non-DanishinstitutionalSmallershareholdersTryghedsGruppen

Percentage

80

85

90

95

100

105

110

115

01/0

1/20

1013

/01/

2010

25/0

1/20

1006

/02/

2010

18/0

2/20

1002

/03/

2010

14/0

3/20

1026

/03/

2010

07/0

4/20

1019

/04/

2010

01/0

5/20

1013

/05/

2010

25/0

5/20

1006

/06/

2010

18/0

6/20

1030

/06/

2010

12/0

7/20

1024

/07/

2010

TrygVesta DJ Euro Insurance

4

Competitive position

19.6

26.8

5

10.513.8

20.8

3.5

TrygAlm. BrandIfOtherAlkaCodanTopdanmark 14.2

10

29.1

18.2

28.5 TrygGjensidigeSparebank1OtherIf

17.5

29.4

14.216.92.6

19.4

ModernaFolksamLänsforsäkringarOtherIfCodan

25.3

2.323.4

18.6

10.6

19.8

TrygTapiolaFenniaOtherIfPohjola

Norway

NOK 39.2bn/EUR 4.6bn

Finland

EUR 3.4bn

Percentage

Percentage

Denmark

DKK 43.9bn/EUR 5.9bn

Percentage

Sweden

SEK 57.3bn/EUR 5.6bn

Percentage

5

Recession impact on group

0

20

40

60

80

100

120

140

160

2004 2005 2006 2007 2008 2009 Q22010

60

62

64

66

68

70

72

74

Building index Burglaries Unemployment DK Group claims ratio (RHH)

Index %

Building index Q1 dataSource: Danish National Statistics

6

Claims ratio

71.0 70.274.9

70.9 73.7 73.8 76.2 76.2 76.3 75.2

15.1

50

60

70

80

90

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

Combined ratio

87.9 87.3 90.9 90.3 90.9 91.5 92.0 94.0 93.3 92.5

15.1

50

60

70

80

90

100

110

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Key performance indicators

Gross premiumDKKm

4,2334,338

4,4254,327

4,117

4,4974,637 4,611 4,650

4,890

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

Expense ratio

15.2 14.7

18.2

15.514.6

13.214.5 13.9 14.5

15.4

1.5 1.91.3

1.2

3.0

2.4

3.3 2.81.7

3.1

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

16.9 17.1 16.0 19.4 17.2 17.6 15.8 17.8 17.0 17.3

Denmark & Norway Finland & Sweden

108.4

Winter impactCombined ratio

91.4

Winter impactClaims ratio

Data before 2009 is not corrected for the sale of Marine Hull business

}

Given the same interestlevel as Q2 2009, CR would have been 91.6%

7

Living in a low interest environment

Discounting rate

2.00

3.00

4.00

5.00

6.00

Q3 2006 Q2 2007 Q1 2008 Q4 2008 Q3 2009 Q2 2010

%

1% increase in interest level will:

•increase pre-tax result by approx. + DKK 300m

•improve combined ratio by approx. 1 %-point

8

50

60

70

80

90

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Gross claims ratio Underlying claims ratio

Claims development

Q2 2009

Q2 2010

72.7 73.1

-4.8

-0.1

3.6

2.8

74.7

-5.0

-1.4

4.0

3.7

74.0

H1 2009

H1 2010

Gross claims ratio

71.2 80.8

Large claims -3.1 -3.9

Weather claims -0.8 -8.0

Run-off 4.3 3.9

Interest rate 4.0 3.4

Underlying claims ratio

75.6 76.1

*Data before 2009 is not corrected for the sale of Marine Hull business.

*

9

2002 2003 2004 2005 2006 2007 2008 2009

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2002 2003 2004 2005 2006 2007 2008 2009

Investment (Gross)

Insurance result

Net result before tax

Strong insurance operations are keyCrisis

Management

Cost

EfficiencyOptimising

Innovation

Growth

Innovation

Growth

Customer

add-onsPrice

increasesPrice

increases

10

Repricing and timing

Average prices in Denmark

3,000

3,500

4,000

4,500

5,000

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Average prices in Norway

3,000

3,500

4,000

4,500

5,000

Q1 05

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Annual impact from price increases

2010 2011 2012

Before DKK ~900m DKK ~700m DKK ~300m

Next wave DKK ~300m DKK ~300m

11

Building margin

Combined ratio

80

85

90

95

100

105

110

2000 2001 2002 2003 2004 2004* 2005 2006 2007 2008 2009 Q12010

Q22010

2011 2012

• 2002-2004 substantial premium increases of DKK 2.1bn implemented. Reduced combined ratio from 107 to 94

• 2009-2012 premium increases of ~ DKK 2.5bn will improve combined ratio in the coming years

Extraordinary

winterPrice increases

Price increases

*IFRS from 2004. Previous years are Danish GAAP

Data before 2009 is not corrected for the sale of Marine Hull business

12

-134 -141-165,00

-200

-150

-100

-50

0

50

100

150

2007 2008 2009 E2010 E-2011 E-2012

Profitability focus in Sweden and Finland

Changed focus is expected to improve result by DKK 250m from 2007–E 2012

Corresponding to +10% of 2008 technical result of TrygVesta Group

ROE is expected to be positively impacted by approx. 3%

CR approaching 95

DKKmGross premiumsDKKm Result

1.553

634

358

-

500

1.000

1.500

2.000

2.500

3.000

3.500

2007 2008 2009 E2010 E-2011 E-2012

0%

20%

40%

60%

80%

100%

120%

140%

160%

2007 2008 2009 E2010 E-2011 E-2012

Claims ratio Ceeded business Expense ratio

13

Unemployment rate

Opportunities in our new markets

38% 39% 35%48%

19% 18% 23%16%

22% 22% 13%16%

21% 22% 29% 20%

0%

25%

50%

75%

100%

Inhabitants Households Summer houses Cars

Sweden Norway Denmark Finland

The market place

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2007 2008 2009 2010E 2011E

Denmark Norway Sweden Finland Euro-area

14

Price increases crucial

Average premiums - Private Motor

60

80

100

120

140

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Norwegian market Tryg Norway

Index2003 = 100

• The Norwegian market increases prices with about same level

and pace as Tryg’s Norwegian business

• Danish market are also up-pricing private lines

• Next wave of price increases will be more focused on the commercial market

Average premiums - Private House

50

80

110

140

170

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Norwegian market Tryg Norway

Index2001 = 100

Examples of price development in Tryg Norway compared to market:

15

Premium increase in Commercial

• Successful re-pricing of agricultureof 15% fulfilled during 2009-2010

• Premium increases in Commercial Property insurances of 10-15% accelerated to start October 2010

• Re-pricing of Commercial will continue until profitability is re-established

• Focus on cost reduction in distribution, claims procurement and training of sales force

Cost ratio in business linesQ2 2010

15.5

25.7

13.9

Private Commercial Corporate

16

Rebalancing pricing and customer retention

• Retention rate stable and strong• Danish retention rate remains high despite influence from

premium increases• High retention support competitive strength and cost ratio

Nordic retention since 2005

82%

84%

86%

88%

90%

92%

Q105

Q205

Q305

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

17

Expense ratio

Breakdown of Group expense ratio

16.6 16.0 15.4 15.814.2

14.9 14.3

0.40.8

1.31.5

2.72.5

2.9

2005 2006 2007 2008 2009 1H 09 1H 10

17.0 16.8 16.7 17.3 16.9 17.4 17.2

Denmark & Norway Finland & Sweden

Continued focus on expenses drives expense ratio downwards by

• streamlining the distribution platform

• digital and paperless process handling

• in-house rotation reduces need for external hiring

• investments in branding and processes by new IT systems

Number of employees reduced by 127 or 3% in DK/NO since Q2 2009

Expense ratio

16.616.2

15.5

16.4

15.915.616.0

50

60.464.5

45.8

26.130.1

34.6

2005 2006 2007 2008 2009 1H 09 1H 10

Denmark & Norway Finland & Sweden

Data before 2009 is not corrected for the sale of Marine Hull business.

18

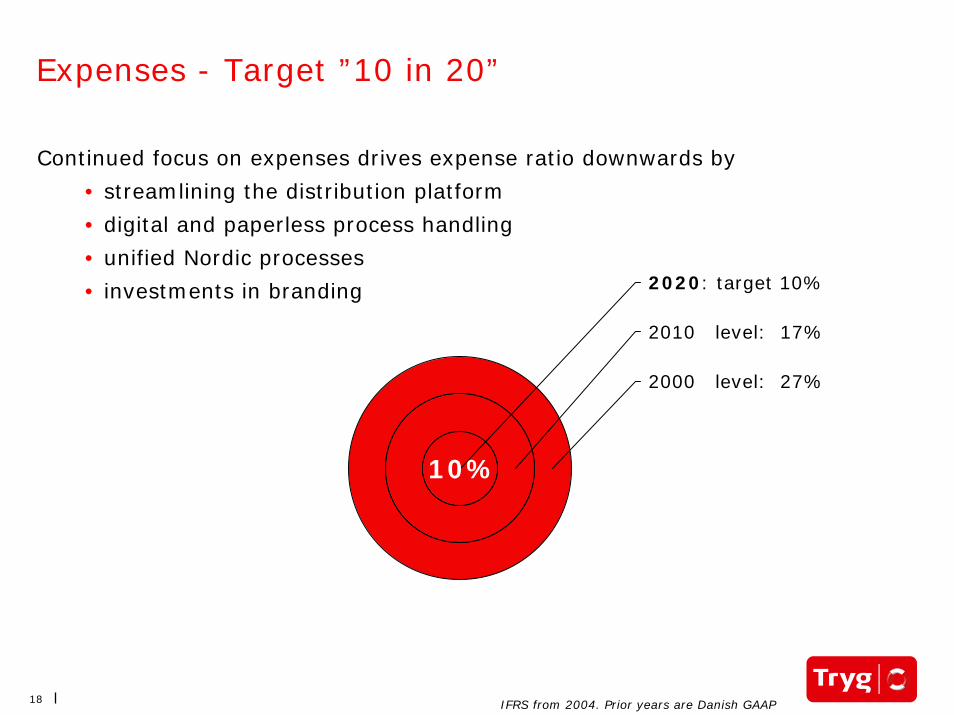

Expenses - Target ”10 in 20”

Continued focus on expenses drives expense ratio downwards by

• streamlining the distribution platform

• digital and paperless process handling

• unified Nordic processes

• investments in branding

2000 level: 27%

2010 level: 17%

2020: target 10%

10%

IFRS from 2004. Prior years are Danish GAAP

19

New proces revolution….

From the customers’ point of view From the employees’ point of view

SM

S

My-page

20

Outlook and capitalisation

20 2. september 2010

21

Outlook 2010

Assumptions: Run-off expected at DKK 0, large claims at DKK 500-600m and weather claims at DKK 200-300

DKKm Actual 2009

Outlook 2010 February

Outlook 2010 May

Outlook 2010 August

Discouting rate 3.6% 3.2% 2.9%

Premium growth in local currency (%) 4.7 3-4 3-4 3-4

Technical result 1,200-1,600 300-700 400-800

Investment result, net 200-300 300-400 100-200

Pre-tax profit 1,400-1,800 600-1,000 600-1,000

Effective tax rate approx. 25% approx. 25% Approx. 27%

Combined ratio before run-off

Before winter

95.9 93-95 97-99

94-96

96-98

93-95

Return assumption p.a. in investment portfolio

Equity 7.0%Bonds 2.3%Real estate 6.0%

22

Capitalisation

6,000

7,000

8,000

9,000

10,000

11,000

12,000

2006

Q1 0

7Q2

07

Q3 0

7

2007

bef

ore

payo

ut

2007

afte

r pay

out

Q1 0

8Q2

08

Q3 0

8

2008

bef

ore

payo

ut

2008

afte

r pay

out

Q1 0

9Q2

09

Q3 0

9

2009

bef

ore

payo

ut

2009

afte

r pay

out

Q1 2

010

(*)

Q1 2

010

Q2 2

010

(*)

Q2 2

010

Capital requirement Buffer (5%) Surplus capital

DKKm

(*) Includes share buy back program based on 2009 earnings, which began on 16 April 2010.

23

Questions?

23 2. september 2010

Lars MøllerInvestor Relations Manager

+45 22 66 66 [email protected]

Ole SøebergInvestor Relations director

+45 40 30 00 [email protected]

Investor relations contacts