Embed Size (px)

Citation preview

British Telecommunications plc 2018

BT Group plcQ3 2017/18 - investor meeting slide pack

February and March 2018

1

British Telecommunications plc 2018

Contents

2

Page

1. Overview and Strategy 3

2. Group 8

3. Consumer 17

4. EE 22

5. Business and Public Sector 26

6. Global Services 31

7. Wholesale and Ventures 35

8. Openreach 39

9. Appendix 44

10. IR contact details; cautionary statement 57

Page

23 February 2018

Overview and Strategy

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Who we are, what we sell to our customers

4

BT Group

Consumer EEBusiness andPublic Sector

Global ServicesWholesale and

VenturesOpenreach

B2C B2BFixed network infrastructure

£4.9bn £5.1bn £4.8bn £5.5bn £2.1bn £5.1bnRevenue1

UK Consumers

Lines, broadband,TV, BT Sport

mobile

Global MNCs3

Managed network IT

services

UK Consumers

Mobilebroadband,

lines,TV

UK SMEs2,Corporates,

Public Sector

Broadband, networking,

voice, mobile, IT services

CommunicationsProviders

Broadband, Ethernet, voice,

mobile, ventures services

Communications Providers

Fibre andcopper

broadband, Ethernet

Products

Customers

£1.0bn £1.2bn £1.5bn £0.5bn £0.8bn £2.6bnEBITDA1

Divisions

1 FY 2016/17 2 Small-medium enterprises 3 Multi-national corporations

£0.7bn £0.6bn £1.3bn (£0.2bn) £0.6bn £1.3bnFCF1

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Our purpose, goal, and strategy

5

1 ee.co.uk/our-company/about-us/customer-service-results-2017bt.com/help/home/customer-service-performancehomeandwork.openreach.co.uk/OurResponsibilities/our-performance.aspx

Transformour costs

Differentiated content, servicesand applications

Best network in the UK

Fully converged service provider

Market leadership in all UK segments

Focus onmultinational

companies globally

Our strategy

Growth – to deliver sustainable profitable revenue growth

Invest for growth

Our goal

Deliver greatcustomer experience1

Our purpose To use the power of communications to make a better world

Broaden and deepen our customer relationships

Best place to workA healthy organisation

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Strategic focus area

6

Transform our costsInvest for growthDeliver great customer experience

• Operational performance improvement– procurement, eg focus on major suppliers– customer and performance transformation

project

• EE integration synergies– £150m delivered FY16/17 vs. target £100m– £250m delivered in H1 FY17/18– £400m by FY19/20

• Restructuring programme– Global Services, Group functions and TSO– £300m to be saved over 2 years– 4,000 roles to be removed from back office– £300m restructuring charge over 2 years, specific

item

• Largest superfast broadband network– 27.4m premises access to superfast– 3m FTTP by mid 2020s– 10m G.fast under review

• The leading mobile network– largest 4G network (90% geographic coverage)– 4G Pro, aim to be 5G leader– most spectrum

• Only UK telco which owns fixed and mobile network– economies of scale– strong position for convergence and content

• Investing in our people– more people (call centres and engineers)– more training/fewer touch points– onshoring

• Investing in our products and services– add value/innovation and move to digital

products– designed to have fewer faults– self service

• Better outcomes– net promoter score– Right First Time– fewer missed appointments– reducing propensity to contact

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Capital allocation framework

7

Maintain strong balance sheet

Progressive dividends

Supportpension fund

Invest forgrowth

Drive sustainable, profitable revenue growth

Grow EBITDA

Grow free cash flow

Invest for growth

Support pension fund

Progressive dividends

Maintain strong balance sheet

Group

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Key areas of focus

9

• Openreach ‘Fibre First’ programme • WLA reviewRegulation and investment

Bringing together EE and BT Consumer

Cost transformation

Customer experience

Pension deficit

• EE integration synergies• restructuring programmes• operational performance improvement

• investing in people, products and innovation• improvements in customer service performance• TV deal with Sky

• simplify operational model• strengthen accountabilities• accelerate transformation

• triennial valuation on track for 1H of calendar 2018• reviewing BTPS scheme following consultation with members• considering funding options

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Win-win solution for all stakeholders

• Broad support for consultation on large scale deployment; co-operation needed on key enablers including:

– achieving low build and connection costs

– achieving rapid take-up of and generating incremental revenue from the platform

– supportive regulatory and public policy framework

• Already building our ultrafast network - mix of G.fast and FTTP1

– bringing at least 100Mbps broadband speeds

– 886,000 premises passed as at end of December 2017

• Improving deployment methods

– including trenching machines, connectorised blocks and plug and play fibre frames

– estimated £300 - £400 per premise passed2, plus £150 - £175 to connect3

Openreach ‘Fibre First’ programme – 3m FTTP by end of 2020

10

• Commitment to reach 3m FTTP by end of 2020, ambition to reach 10m by mid-2020s, if conditions are right

– 8 cities out of 40 named in first phase of the programme

1 Fibre-to-the-Premises 2

for first 10m premises passed 3excludes cost of battery back-up for the majority of customers

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Current regulatory topics

11

WLA2 review – pricing certainty for key products

• Openreach direct financial impact from GEA3 40/10 charge controls:

− 2018/19: revenue & profit down £80m-120m YoY

− 2019/20 & 20/21: down low to mid tens of millions of pounds each YoY

− Openreach’s cost base will also increase to meet more demanding minimum service levels

• Indirect negative financial impact also expected from market pressure on the wholesale prices of other products

• However, net Group impact depends on retail market dynamics

• We are considering the implications of the restriction on BT’s ability to geographically vary GEA and G.fast wholesale rental charges

DCR1: Openreach to be legally separate company within BT

• Openreach Board: independent chair, majority independent members

• Greater delegation of responsibility: strategy, operations and budget

• Enhanced industry consultation process

• Openreach CEO to report to Openreach chair− except for certain duties around BT’s plc listing

• BT to adopt voluntary Commitments to replace 2005 Undertakings

• c.30,000 employees to transfer to Openreach Ltd, following TUPE and replicating Crown Guarantee

• Assets and trading to stay with BT plc

• Openreach Ltd brand no longer features BT logo

• Agreement to be comprehensive and enduring

1 Digital Communications Review 2 Wholesale Local Access 3 Generic Ethernet Access (Openreach’s fibre-to-the-cabinet access product)

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

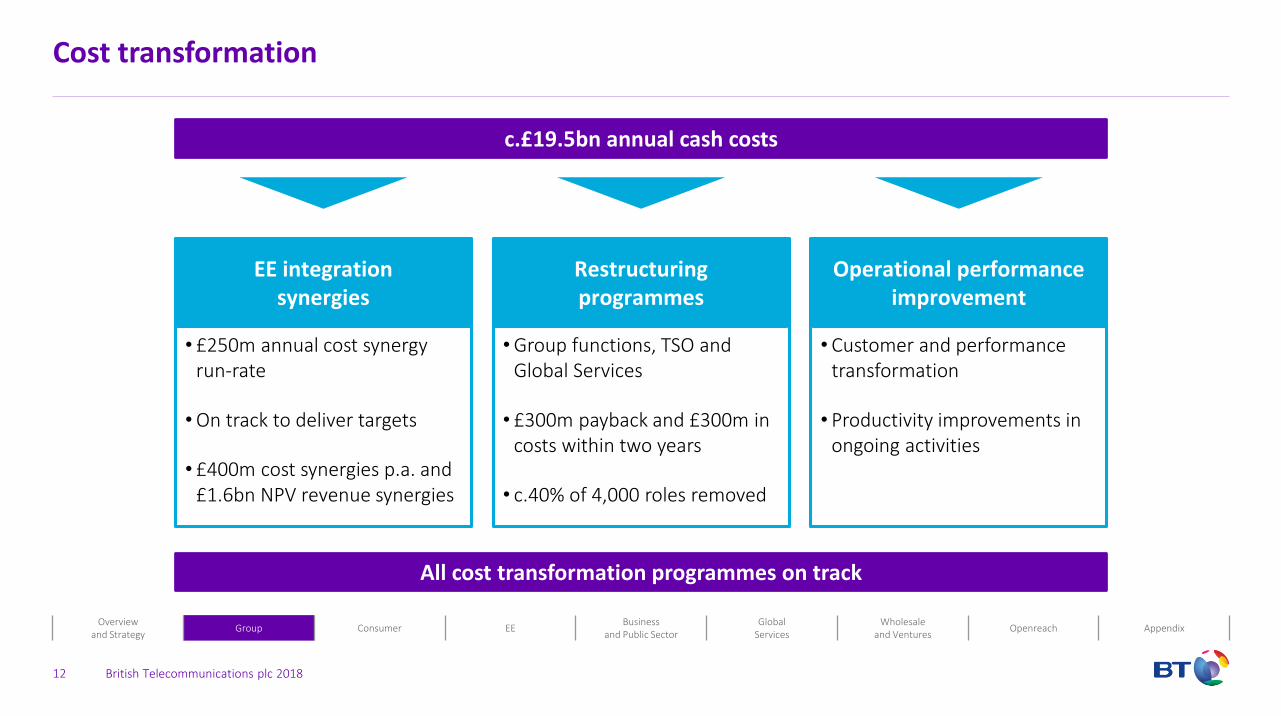

Cost transformation

12

c.£19.5bn annual cash costs

EE integrationsynergies

Restructuringprogrammes

Operational performance improvement

All cost transformation programmes on track

• £250m annual cost synergy run-rate

•On track to deliver targets

• £400m cost synergies p.a. and £1.6bn NPV revenue synergies

•Group functions, TSO and Global Services

• £300m payback and £300m in costs within two years

• c.40% of 4,000 roles removed

• Customer and performance transformation

• Productivity improvements in ongoing activities

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

New Consumer business to be created

13

• Bringing together EE and BT Consumer from 1 April 2018

• Pro forma c.40% of group revenue, c.32% of EBITDA

• Three distinct brands – BT, EE and Plusnet

• Fixed and mobile networks, consumer products and services

and content

• Simplify operating model, strengthen accountabilities,

accelerate transformation

• Marc Allera (prev. CEO of EE) leading since 1 September 2017

Drive converged products and accelerate transformation

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Using multiple brands to address different segments, and enable convergence

14

Customers’ brand consideration index:

multi-brand >50% higher

Multi-brand consideration Distinct brand positions to compete

100

133156

Singlebrand

Dualbrand

Multi-brand

Premium, high qualityTrustworthy, reliable, credible

British heritageFamily-focused

Home, fibre, family

Brand strengths

Heartland

InnovativeModern and up-to-date

Social and outgoingOut of home and on the move

On the go, mobile, personal

Brand strengths

Heartland

Honest, straight-talkingPlayful

Yorkshire charmValue for money

Home, broadband, value

Brand strengths

Heartland

Establishing leadership in convergence

Simple converged fixed and mobile bundles

BT Sport offered to EE postpaid customers

BT Family SIM launched in Oct 2016

Plusnet entered quad-play market in Nov 2016

BT and EE implementing joined-up approach to value creation

Competitors

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Customer Experience - improving results from investment in CX

15

Group• Net promoter score +5.5pts

• Right First Time +3.6%

Customer Experience

Consumer• > 2m MyBT App downloads

• Average call waiting time reduced to

<60 seconds YoY

• 5,000 agents trained on consumer.com

• Multiskilling agents

Innovation• >4,900 patents

• G.fast

• InLinkUK from BT

• SmartCity MK

• Agile Connect

Openreach• Copper network faults 4.1% lower YoY

• On-time repair performance remained

>80%

Products• Superfast broadband available to 95%

of UK premises

• 4G target 95% geographic coverage

• Leadership in FTTP and 5G

• Driving convergence

EE• Onshore call answering 100%

• Call centre satisfaction +7%

• Ofcom complaints lowest ever

• >600 stores

Confidence to publish our customer service performance:

Consumer: www.bt.com/help/home/customer-service-performance/EE: http://ee.co.uk/our-company/about-us/customer-service-results-2017

Openreach: www.homeandwork.openreach.co.uk/OurResponsibilities/our-performance.aspx

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Pension

16

• BTPS has c.300,000 members, assets of £49.9bn, liabilities of £58.9bn (IAS19 at 31 Dec 2017)

• Benefits expected to be paid over c.70 years, requires long term approach

• BTPS deficit driven by continued very low discount rate, increasing liabilities

• Actuarial valuation every 3 years; BTPS Trustee and BT agree deficit and negotiate payment plan

− triennial valuation drives deficit repair payments

− assumptions differ from more volatile quarterly IAS 19 accounting estimate

• BT has constructive relationship with BTPS Trustee

BT Pension Scheme (BTPS)

• Expect to announce outcome in H1 calendar 2018

• Deficit repair payments agreed for following three years

− 2014 triennial agreement was for £2.1bn cumulative payments 2017/18 – 2019/20

• Relationship between size of deficit and payments in following three years is not linear

• Proactive approach

− following 60 day consultation with BTPS members we have closed the DB scheme for managers. Discussions continue with team members and their union

− consideration of alternatives to paying cash into scheme

− launching appeal of the High Court decision not to allow move away from RPI indexation

30 June 2017 triennial valuation

Consumer

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

1.7

1.8

1.9

2.0

2.1

£20

£25

£30

£35

£40

£45

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

RG

Us

pe

r cu

sto

mer

Mo

nth

ly A

RP

U

Consumer ARPU RGUs per customer

Consumer - at a glance

• Deepen customer relationships– emphasis on growing RGU per customer– more services lead to higher ARPU, and lower churn

• Strengthen TV and Sport– sport content a key differentiator: a reason to join

and stay with BT– building our entertainment offer, in a disciplined way

• Drive convergence– convergence in UK lags behind European markets– opportunity for Consumer

• Customer experience– happier customers, with higher NPS3, are more loyal– customer service is improving, still not where we want

it to be

18

ARPU1 and RGU2 progression

Operational metrics

2015/16 2016/17 2017/18

Q3 YoY changeARPU 4.8%

RGUs/customer 3.1%

1 Average Revenue Per User 2 Revenue Generating Units 3 Net Promoter Scorec

Q2 2016/17

Q3 2016/17

Q4 2016/17

Q1 2017/18

Q2 2017/18

Q3 2017/18

Retail BB customers (‘000) 9,193 9,276 9,276 9,286 9,307 9,342

Retail share of BB net adds 65% 44% 35% 53% 34% 22%

Retail BB market share 46% 46% 46% 45% 45% 45%

Fibre BB as % of BB base 49% 51% 53% 55% 57% 59%

TV customer base (‘000) 1,684 1,736 1,750 1,758 1,765 1,760

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

BT Consumer - Strong BT Sport viewing and premium TV content deal agreed

Q3 2017/18 Q3 2016/17 Change

Revenue £1,261m £1,262m -

EBITDA £250m £260m (4)%

Capex £66m £54m 22%

Season to date3 BT Sport viewing4 at an all-time high

• Revenue flat– increased ARPU

1offset by voice line losses

– 12-month rolling ARPU up 4.8%

– RGUs2

per customer up 3.1%

• EBITDA down 4%, reflecting investment in customer

experience and broadband speed upgrades

• Superfast growth, ultrafast product launches– 152Mbps and 314Mbps

– with minimum speed guarantees of 100Mbps

– 59% of broadband customers now on fibre

• TV agreement with Sky– launch in early 2019

• BT Sport – BT Sport viewing

4up 23% YoY

– all customers5 now pay for BT Sport1 Average Revenue Per User 2 Revenue Generating Units 3 average weekly viewing from start of football season 4 ex digital 5 excluding employees

2013/14 2014/15 2015/16 2016/17 2017/18

19

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Fibre supports higher ARPU, lower churn and upsell opportunities

• Early move on fibre led to significant upside− 59% of the retail broadband base on Infinity (vs. 33% for

other communication providers)− churn for BT Infinity is about a third lower− higher ARPU, and attracts new customers

• Investing to maintain broadband leadership− superior performance in Ofcom speed report, especially

at peak times− 52Mbps now minimum for Infinity 1− customers upgraded to Care Level 2 (24-hour response)

• Fibre remains key to our future plans− 86% say they will never go back to copper− 3x more customers take TV with fibre vs. copper− Ultrafast products launched with 100Mbps minimum

guarantee

20

BT Infinity fibre broadband offers the best experience

Fibre penetration continues to improve

Faster home wi-fiwith

BT Smart Hub

Access to >5m public hotspots

with BT Wi-fi

Preferential pricing for mobile

and sport

18% 29% 39% 48% 53% 59%

2012/13 2013/14 2014/15 2015/16 2016/17 Q32017/18

BT retail broadband subscribers with fibre service

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

TV and Sport platform, a foundation for growth

21

Improvements in audience and content• Multi-year agency deal for BT to market and sell Sky’s NOW

TV service to BT TV customers, starting from 2019

• 1.8m TV and well over 5m BT Sport customers

• total BT Sport audience +23% YoY1

• disciplined approach to content rights

• Premier League matches on BT Sport for a further three years

from 2019/20 season

Strong roster of channels and sports rights Multiple routes to value creation

• Broadband lines, TV/BT Sport customers, EE customers

• BT Broadband, BT Sport Pack, EE, Sky

• c.30,000 pubs and clubs

• Wholesale sport deals, e.g. with Virgin Media and Setanta

• Advertising and programme sponsorship

Charging

Commercial

Volumes

Wholesale

Advertising

Starter Entertainment Max

• 80 channels• Pause & rewind

• 100 channels• Record 300 hours

• 141 channels, 21 HD• Record 600 hours• Free BT Sport inc 4K UHD

Innovative approach• Netflix embedded in user interface

• inventive formats, such as ‘The Goals Show’, using connected

red button on BT TV and BT Sport App

• UEFA finals made available on social media platforms

• multi-platform digital strategy

1 excluding Showcase and digital

EE

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

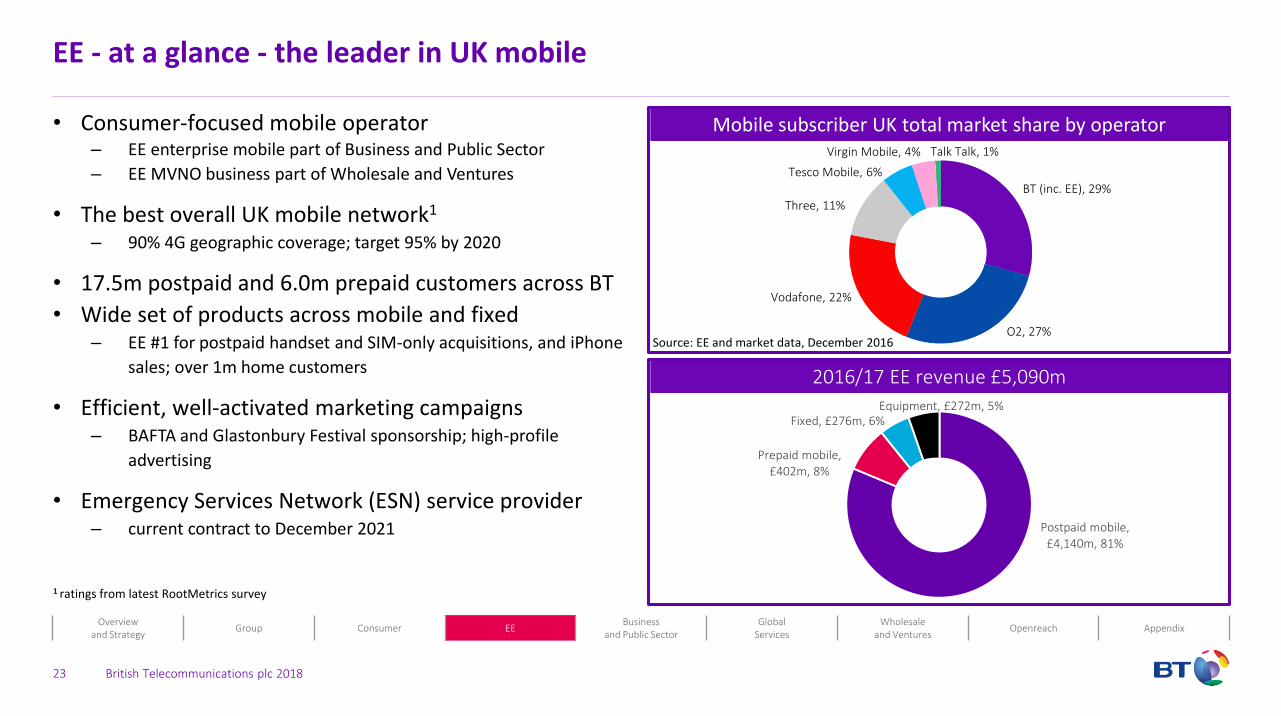

EE - at a glance - the leader in UK mobile

23

• Consumer-focused mobile operator– EE enterprise mobile part of Business and Public Sector

– EE MVNO business part of Wholesale and Ventures

• The best overall UK mobile network1

– 90% 4G geographic coverage; target 95% by 2020

• 17.5m postpaid and 6.0m prepaid customers across BT

• Wide set of products across mobile and fixed– EE #1 for postpaid handset and SIM-only acquisitions, and iPhone

sales; over 1m home customers

• Efficient, well-activated marketing campaigns– BAFTA and Glastonbury Festival sponsorship; high-profile

advertising

• Emergency Services Network (ESN) service provider– current contract to December 2021

Mobile subscriber UK total market share by operator

BT (inc. EE), 29%

O2, 27%

Vodafone, 22%

Three, 11%

Tesco Mobile, 6%

Virgin Mobile, 4% Talk Talk, 1%

Source: EE and market data, December 2016

2016/17 EE revenue £5,090m

Postpaid mobile, £4,140m, 81%

Prepaid mobile, £402m, 8%

Fixed, £276m, 6%Equipment, £272m, 5%

1 ratings from latest RootMetrics survey

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

EE - EBITDA down 6%, driven by high customer investment costs

24

Q3 2017/18 Q3 2016/17 Change

Revenue £1,357m £1,311m 4%

EBITDA £259m £277m (6)%

Capex £122m £153m (20)%

Apple’s premium handset price evolution1

• Revenue up 4% – postpaid up 6%; prepaid down 15%

– Group postpaid mobile ARPU down 1.9%

– Group churn 1.2%

• Group mobile base 29.8m– 235,000 postpaid adds, group base now 17.5m

– 299,000 prepaid decline, group base now 6.0m

• EBITDA down 6%– reflecting investment in premium handsets and smart

watches

– expect strong recovery in Q4

• Investing to improve customer experience– 4G geographic coverage now 90% of UK landmass

– network coverage and performance recognised in latest

RootMetrics reports

1 Apple selling price of smallest capacity premium model at launch

£0

£250

£500

£750

£1,000

iPhone 6 Plus iPhone 6S Plus iPhone 7 Plus iPhone X

Sep 2014 Sep 2015 Sep 2016 Nov 2017

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

EE - network leadership and customer experience drive ‘more for more’ revenue growth

25

Maintain network leadership

• 4G to reach 95% UK geographic coverage by 2020– plan to have over 450 new sites live in 2018

• Consistently ranked No.1 in network tests

• Introduced the new ‘Time on 4G’ metric – e.g. using to planning specific rail coverage upgrades

• Preparing to lead the way on 5G– researching with a number of partners

4G geographic coverage acceleration

Illustrative coverage only

90% 95%

Q3 2017/18 2020

Online chat increasing and propensity to call falling

Transform customer experience

• Ambition to become the best operator for customer

experience

• Calls: 100% answered in UK and Ireland

• Digital: My EE app has >10m registrations; investment in

online

• Stores: bringing personal service to more customers– plan to have c.700 total stores by end of 2019

Q1 2016/17 Q1 2017/18

Online chat users Propensity to call

Business and Public Sector

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

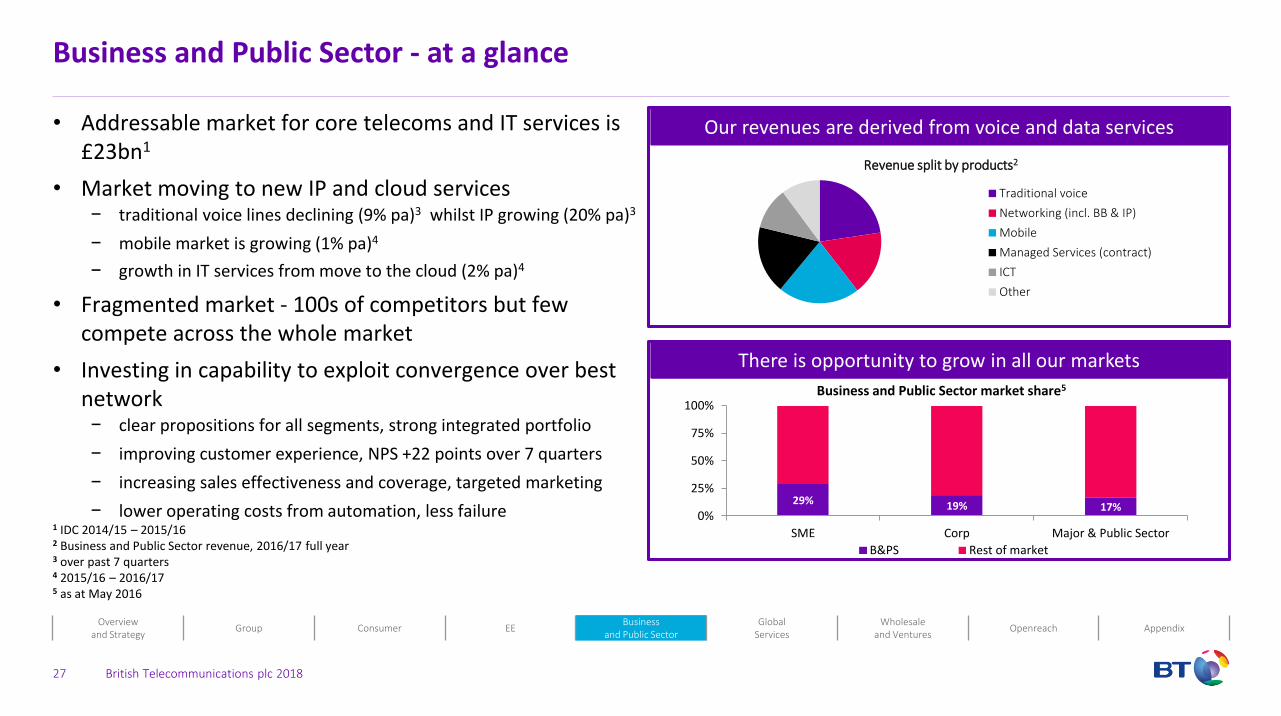

Business and Public Sector - at a glance

• Addressable market for core telecoms and IT services is £23bn1

• Market moving to new IP and cloud services− traditional voice lines declining (9% pa)3 whilst IP growing (20% pa)3

− mobile market is growing (1% pa)4

− growth in IT services from move to the cloud (2% pa)4

• Fragmented market - 100s of competitors but few compete across the whole market

• Investing in capability to exploit convergence over best network− clear propositions for all segments, strong integrated portfolio

− improving customer experience, NPS +22 points over 7 quarters

− increasing sales effectiveness and coverage, targeted marketing

− lower operating costs from automation, less failure

27

Our revenues are derived from voice and data services

There is opportunity to grow in all our markets

1 IDC 2014/15 – 2015/16 2 Business and Public Sector revenue, 2016/17 full year3 over past 7 quarters4 2015/16 – 2016/175 as at May 2016

29% 19% 17%0%

25%

50%

75%

100%

SME Corp Major & Public Sector

Business and Public Sector market share5

B&PS Rest of market

Revenue split by products2

Traditional voice

Networking (incl. BB & IP)

Mobile

Managed Services (contract)

ICT

Other

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Business and Public Sector - steady progress

28

25%

30%

35%

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Cumulative mobile net adds (LHS) Mobile market share (RHS)

• Underlying revenue ex transit down 6%– declines in traditional voice and lower equipment sales,

partially offset by continued growth in mobile

– Progress on IP voice – base up 55% YoY

– SME down 3%, Corporate down 7%, Public Sector and

Major Business down 6%

• EBITDA down 8%– reflecting reduction in revenue and strong prior year

comparator

• Order intake down 22%– 12-month rolling up 12%

Q3 2017/18 Q3 2016/17 Change

Revenue– u/l ex transit

£1,125m £1,190m (5)%(6)%

EBITDA £362m £393m (8)%

Capex £69m £74m (7)%

Continued growth in BPS mobile and mobile market share1

2016/17 2017/182015/161 Source: BT, IDC

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Public Sector - managing transition of large contracts

29

We are adapting the business to respond

• Managing transition of ceased contracts; majority of revenue ceased by end of 2017/18

• Significant investment in growing regional sales teams with some early wins in Scotland and Wales

• Investing to standardise and scale Managed Service capability

• Growth in mobile and networking

• Improved Net Promoter Score by +26 points over 7 quarters

Public Sector market has undergone major changes

• Core telecoms and IT market of c.£10bn, with further c.£8bn in IT and other outsourcing contracts

• Public sector spend is increasingly devolved and being consolidated locally

• Larger integrated contracts being replaced by smaller individual product deals

• BT’s major contracts are ending and impact is still working through the business

• Growth in new areas will take time to offset declines in these contracts

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Corporate and SME - good performance, well positioned for future

30

Corporate: growth in core portfolio

• Strong profit growth over year

• Mobile and networking grew market share

• Successful integration of EE and BT into one sales team, with strong ‘Why BT?’ message

• Focused marketing of Voice and IP

• Future opportunities:

− exploit well integrated converged proposition of mobile, IP and network

− further revenue and cost synergies from integration

SME: PSTN1 decline with some offset in mobile and networking

• #1 in SME mobile: strong growth, 2% market share gain

• Fibre broadband: now > half the base

• Network services: strong revenue performance

• Traditional lines decline: some offset from growth in IP Voice

• Bundles increasingly important

• Good progress on EE integration and cross sell

• Future opportunities:

− digital campaigns to target cross sell

− extend bundling capability and offers

1 Public Switched Telephone Network

Global Services

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Global Services - at a glance - global scale to support multi-country customers

32

• We supply ICT1 services globally

− 5,500 customers, 17,000 employees, 180 countries

• Focus is MNCs in key industry verticals globally, public

and private sector customers outside UK

− c.70% of revenue from MNCs2

− c.70% of revenue from customers served in multiple regions

• Multi-country model combined with global account

management

− our 20 highest priority countries generate >90% of revenue

− partners extend geographic reach in sales and service in

smaller country markets

Revenue mix by geography and by portfolio

37%

30%

21%

12%

UK

Europe

Americas

AMEABT AdviseIndustriesBT ComputeBT ContactSecurity

BT One(fixed, mobile, unified comms)

BT Connect(network services)

Our customer model

% share of revenue

Majorglobal

accounts (50%)

Top accounts (30%)

Key accounts (20%)

Largest, multi-region MNC customers

MNCs and domestic customers with narrower geographic focus

Smaller customers with high potential

1

2

3

1 Information and Communications Technology 2 Multinational companies

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Global Services - managed declines in low margin business

33

Q3 2017/18 Q3 2016/17 Change

Revenue– u/l ex transit

£1,266m £1,398m (9)%(6)%

EBITDA £143m £40m 258%

Capex £64m £69m (7)%

Global Services’ revenue and EBITDA movements

• Underlying revenue ex transit down 6%– managed decline in low-margin business

• Restructuring continues– new digital products launched with key suppliers

– progress update at Q4 2017/18 results

• Order intake down 11% to £1.1bn– 12-month rolling down 25%

– reflecting ongoing challenging market conditions

• Strong growth in security services– increasingly important as customers move away from

dedicated MPLS1 to more hybrid networks

• EBITDA up £103m– reflecting one-off items and prior year Italy impact;

broadly in line excluding these items

1 Multi-Protocol Label Switching2 Global Wholesale Voice

Revenue EBITDA

2

£1,398m

£1,266m

Q32016/17

Prioryear Italy

impact

GWV &equipsales

Trading FX andOther

Q32017/18

£40m

£143m

Q32016/17

Prioryear Italy

impact

GWV &equipsales

Trading FX andOther

Q32017/18

2

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

• Strategic way forward− Focus on global multi national corporations

− Focus on strong customer relationships – NPS continues to improve

− Market focus where we have strong leadership and we deliver repeatable solutions

− Technology trends mean less dependent on owning physical local network

Global Services - moving to a more focused operating model

34

• Reposition as a focused digital business− Prioritise platform based solutions such as cloud based services, and SDN e.g. launch of BT Connect SD-WAN

− Cloud of clouds ecosystem continues to develop e.g. IBM cloud connected

− AWS partnership and IBM cooperation announced

− Emphasis on security - continues to grow

− BT’s global network remains at the core

• Creating a simpler operating model− two-year restructuring of operations

− Simplification and streaming of core processes underway

Improve financials, risk profile, and long-term value to BT

Wholesale and Ventures

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

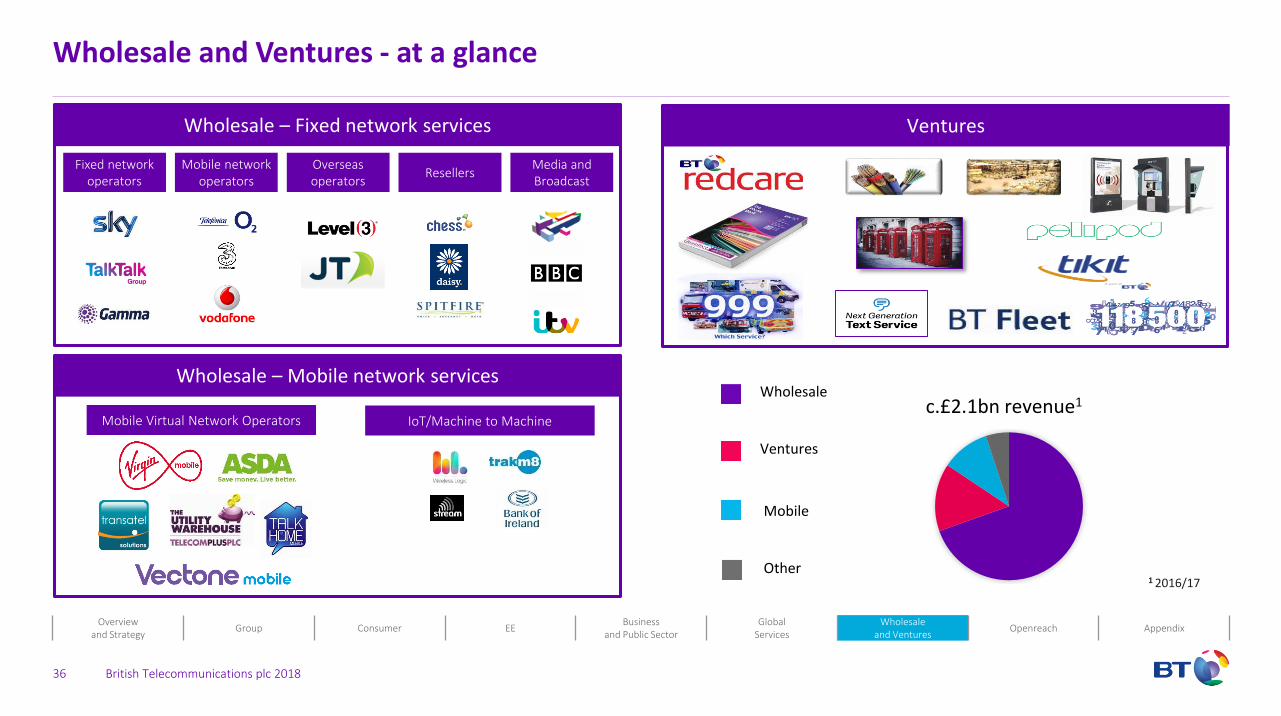

Wholesale – Fixed network services

Wholesale and Ventures - at a glance

36

Wholesale

Ventures

c.£2.1bn revenue1

Mobile

Other1 2016/17

Media and Broadcast

ResellersFixed network

operatorsMobile network

operatorsOverseas operators

Wholesale – Mobile network services

Mobile Virtual Network Operators

Ventures

IoT/Machine to Machine

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Our strategy is based on selling new products and services, supported by brilliant customer experience

37

Create a better business

Mobile network operator solutions

Converged communications

Sell MVNO to Wholesale CPs

Ventures strategic solutions

Digital kiosksInternet of Things

Professional services

Cross-sell products Turn products into services Create new business models

Combined with a brilliant customer experience

Brilliant People

Easy to do business

Engaged Customers

Customer-centric decisions

Leverage our market position

Fixed Wholesale

Mobile Wholesale

#1

#2

#1

#1

#1

#1

#1

#1

#1

#1

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Wholesale and Ventures - stronger Ventures revenue

38

Q3 2017/18 Q3 2016/17 Change

Revenue– u/l ex transit

£506m £528m (4)%(4)%

EBITDA £189m £211m (10)%

Capex £54m £53m 2%

Wholesale and Ventures order book

• Underlying revenue ex transit down 4%– Managed Solutions down 8%; Data and Broadband

down 8%; Voice down 3%

– Mobile revenue down 5% reflecting specific MVNO1

contractual commitments last year

– Ventures revenue up 9% - good growth in bulk messaging and Fleet Solutions

• EBITDA down 10%

– reflecting continued legacy decline and revenue mix

• Order intake £372m, down 61%

– 12-month rolling down 38%

– reflecting two large contracts in prior year

• 86 InLinkUK units live at end of Q3

– providing free calls, wi-fi and other services

– generating advertising revenue 2016/17 2017/18

-

200

400

600

800

1,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3

£m

1 Mobile Virtual Network Operator

Openreach

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Openreach - at a glance

40

Openreach serves c.26m customers through CPs

OPENREACH>590 Communications Providers with access to c.30m end customers

Access products, eg copper, Fibre, ISDN Ethernet and backhaul products

c.5mbusiness

connections

• Fibre

• New sites

• Data centres

Business and Corporate Infrastructure

• Maintains and builds access network between homes

and business and exchanges; huge engineering operation

• 27.4m premises passed with superfast fibre broadband

network

• Commitment to serving >590 CPs nationwide on equal

access terms

• Supplies copper and fibre access products, Ethernet and

backhaul

• Ofcom regulates >90% revenue; charge controls c.75%

c.21mend customers

Consumer / Residential

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Openreach - access network

41

Homes/Businessesc.30m locations

Distribution Pointc.4.7m locations

Typically ~35m from premises

Cabinetc.101,000 locations

Typically 350m from premises

Exchange>5,500 locations

Typically 3.5km from premises

Backhaul

Copper

Fibre

Copper

CopperCore

network

Fibre

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Openreach - continued strong fibre growth

42

Q3 2017/18 Q3 2016/17 Change

Revenue £1,286m £1,284m -

EBITDA £641m £676m (5)%

Capex £477m £409m 17%

Openreach fibre net adds2

• Revenue flat– continued strong growth in fibre broadband, up 23%

• EBITDA down 5%– increased business rates and higher pension charge

• Normalised free cash flow down 8%– increased opex and capex

• Fibre broadband now available to c.27.4m1 premises– record 600,000 fibre broadband net additions2

– 9.2m premises connected

• Ahead on all 60 copper minimum service levels

• 4.1% reduction year to date in copper network faults

• Targeting 3m premises with FTTP by the end of 2020– first eight cities announced

k

2017/182016/172015/162014/152013/142012/13

0

100

200

300

400

500

600

1 Using latest Ordnance Survey addressing product 2 Including BT Northern Ireland

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Faster speeds and broader coverage - Superfast and Ultrafast plans

43

Superfast

– Beyond BDUK 95% coverage

Ultrafast

– G.fast and FTTP

• ‘Fibre First’ commitment to deliver FTTP to 3m premises by end 2020, ambition for 10m by mid-2020s, if conditions are right

• G.fast remains critical component of Openreach’s Ultrafast strategy

Plans Progress

1 Multi-Dwelling Units 2 Universal Service Obligation

• Launched two G.fast variants 160/30Mbps and 330/50Mbps, live since September

• Extending our FTTP footprint; targeting new sites, MDUs1, SMEs and hard-to-reach areas

• 886,000 ultrafast capable premises, growing quickly

• 95% coverage achieved

• Respect the Government’s decision on USO2

– waiting for outline of approach including

funding mechanism

• Multiple solutions: FTTP deployment techniques, fixed wireless broadband and satellite

• Trialling trenching machines currently

– 300m a day for as little as £3 per metre

– duct laid 6 times quicker than before

Appendix

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

9.6

6.9

2.92.92.2 2.2

0

2

4

6

8

10

1% pt fall in discountrate

0.9% pt increase toinflation rate

1.35yr increase to lifeexpectancy

Increase in liabilities

increase in deficit

Pension - sustained low discount rate necessitates more proactive approach

45

• Q3 IAS 19 deficit £7.9bn net of tax (Q2 £7.7bn)

− continued low real discount rate (Q3 -0.82%, Q2 -0.68%)

− increase in assets (Q3 £49.9, Q2 £48.7bn), and liabilities (Q3 £58.9bn, Q2 £57.7bn)

− 2017-18 operating charge expected to increase by c.£100m

-9

-3.9

-7

-12

-10

-8

-6

-4

-2

0

Dec

-08

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

12

Sep

12

Dec

12

Mar

13

Jun

13

Sep

13

Dec

13

Mar

14

Jun

14

Sep

14

Dec

14

Mar

15

Jun

15

Sep

15

Dec

15

Mar

16

Jun

16

Sep

16

Dec

16

Mar

17

Jun

17

Sep

17

Dec

17

Pen

sio

n v

alu

atio

n, £

bn

IAS 19 (gross of tax) IAS 19 (net of tax) Actuarial (gross of tax)

2009/102008/9 2010/11 2012/132011/12 2013/14 2014/15 2015/16 2016/17 2017/18

IAS 19 Actuarial

Measure Accounting measure Actuarial measure

Frequency Quarterly Triennial

Purpose Regular updates Sets cash deficit payments

Discount rate Yield curve for AA corporate bonds Prudent expected return (BTPS assets)

Longevity Future expectations Prudent overall approach

Inflation Future expectations Prudent overall approach

Assets Market value Market value

1 the scheme actuary has assessed the risk of these events as occurring no more than once in 20 years; the impact shown for each scenario assumes this is the only change – in practice a combination of changes could arisea scenario assumes a one percentage point fall in the yields on both government and corporate bondsb assuming RPI, CPI, pension increases and salary increases all increase by 0.9 percentage points

Source: BT Annual Report and Form 20-F 2017, p211

BT Pension Scheme sensitivity analysis1

a b

£bn

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

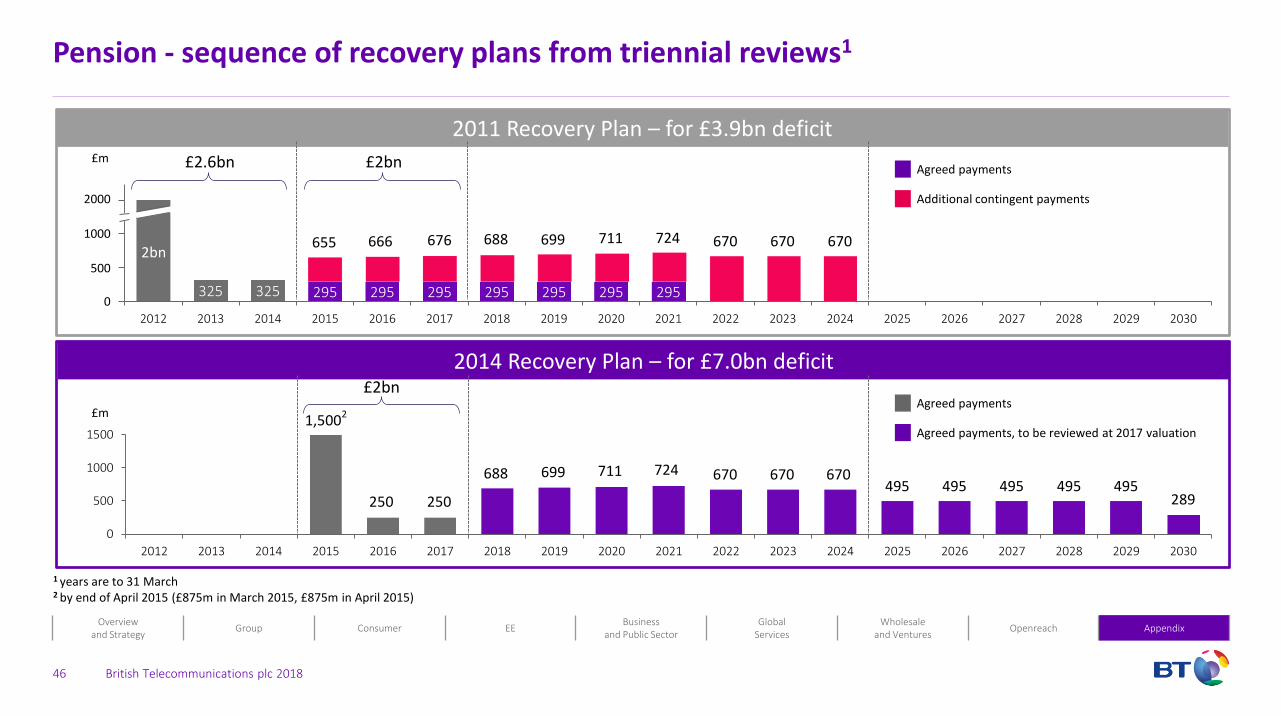

Pension - sequence of recovery plans from triennial reviews1

46

0

500

1000

1500

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

325 325 295 295 295 295 295 295 295

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

2011 Recovery Plan – for £3.9bn deficit

2014 Recovery Plan – for £7.0bn deficit

655 666 676 688 699 711 724 670 670 670

1,5002

250 250

688 699 711 724 670 670 670495 495 495 495 495

289

£2bnAgreed payments

Agreed payments, to be reviewed at 2017 valuation

1 years are to 31 March2 by end of April 2015 (£875m in March 2015, £875m in April 2015)

£m

£m £2bn Agreed payments

Additional contingent payments

2bn

2000

1000

500

0

£2.6bn

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Key regulatory market reviews

47

2020/212018/192016/17 2019/20 2021/22 2022/232017/182015/16

UK PolicyFramework

700MHz spectrum auction 2020

2.3 and 3.4GHz spectrum auctions 2018

Brexit

Narrowband markets

(WNBMR and NCC)

NBMR Oct 13 to Sep 16 NBMR Dec 17 to Mar 21

Consultation Consultation

Final statement Final statement

Lacuna

LacunaFibre, copper access

(FAMR and WLA)

FAMR to Mar 17 WLA Apr 18 to Mar 21

Consultation Consultation

Final statement Final statement

Business Connectivity

(BCMR/LLCC)

BCMR Apr 13 to Mar 16

BCMR Apr 19 to Mar 22

Appeal Post CAT Consultation

Post CAT statement

BCMR Apr 16 to Mar 19 Post CAT lacuna

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Regulatory certainty key to investment landscape

48

• Further regulatory impacts on revenue and EBITDA from:

− Wholesale Local Access Market Review (MPF1, GEA2, DPA3)

− Business Connectivity Market Review, including dark fibre

− Narrowband Market Review (WLR4, ISDN5, Solus voice)

2016/17 and 2017/18

• 2016/17 regulation impacted Openreach revenue and EBITDA by c.£230m

− c.£180m from Business Connectivity Market Review (BCMR)

− c.£50m from Fixed Access Market Review (FAMR)

• 2017/18 EBITDA impacted by:

− c.£120m Openreach impact from BCMR and from MPF price cut during lacuna period

− c.£60m Openreach impact between new business rates implementation and regulatory reviews

− high tens of millions of pounds impact from EU mobile roaming cuts

2018/19 and beyond

1 Metallic Path Facility 2 Generic Ethernet Access 3 Duct and Pole Access 4 Wholesale Line Rental 5 Integrated Services Digital Network

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

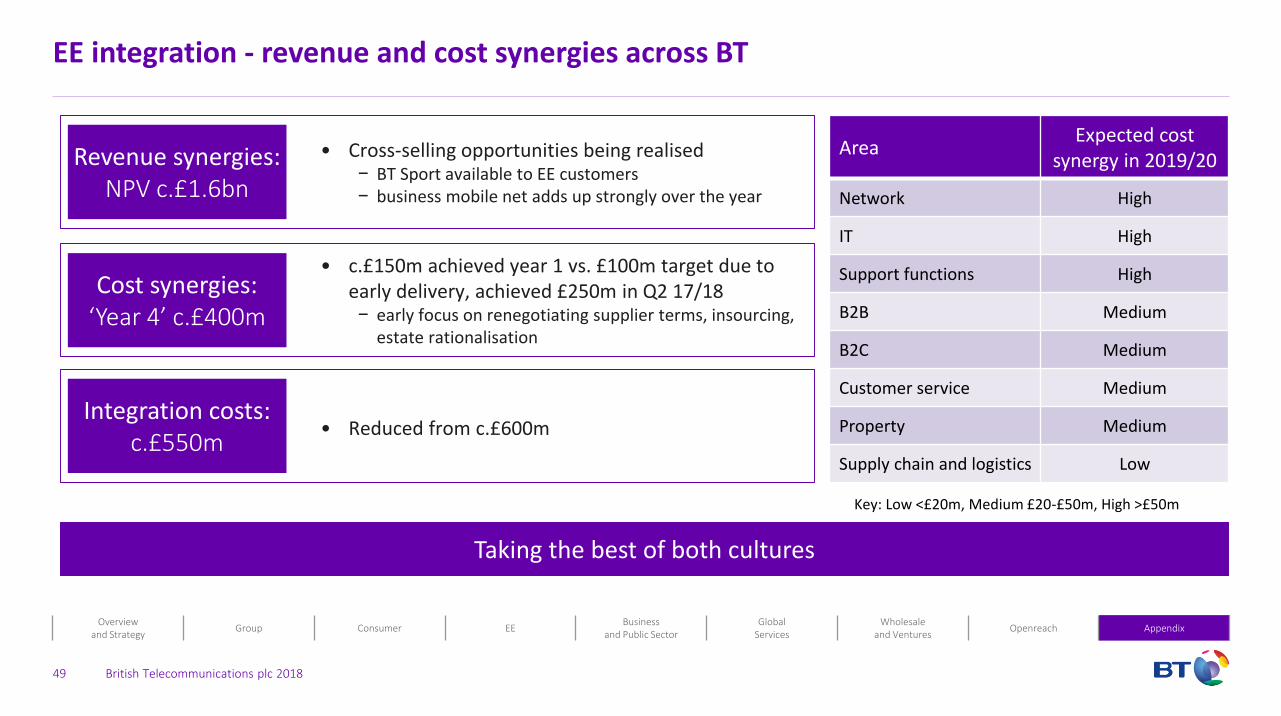

EE integration - revenue and cost synergies across BT

49

Taking the best of both cultures

Revenue synergiesRevenue synergies:

NPV c.£1.6bn

• Cross-selling opportunities being realised− BT Sport available to EE customers− business mobile net adds up strongly over the year

Cost synergiesCost synergies:

‘Year 4’ c.£400m

• c.£150m achieved year 1 vs. £100m target due to early delivery, achieved £250m in Q2 17/18 − early focus on renegotiating supplier terms, insourcing,

estate rationalisation

Integration costsIntegration costs:

c.£550m• Reduced from c.£600m

AreaExpected cost

synergy in 2019/20

Network High

IT High

Support functions High

B2B Medium

B2C Medium

Customer service Medium

Property Medium

Supply chain and logistics Low

Key: Low <£20m, Medium £20-£50m, High >£50m

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Co

sts

Rev

enu

e

Co

sts

Rev

enu

e

Impact of IFRS 15 on revenue recognition

50

• Move away from cash-based accounting

• Earlier revenue and EBITDA recognition

• Accounting of handset contracts is the largest change for BT

• Adoption from Q1 2018/19

• Accelerated profit may lead to a one-off additional cash tax charge, split between 2018/19 and 2019/20

Mobile revenue recognition - AfterMobile revenue recognition - Before

Handset ServiceHandset Service

Time Time

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Group governance and controls

51

• Italy and Global Services review:

− detailed balance sheet reviews in seven large countries outside UK, supported by EY. With Italy covers c. 2/3 by asset value of operations outside UK

− no similar issues or areas of concern identified elsewhere, giving comfort this was isolated to Italy

− KPMG independent review of systems and controls relating to our Italian business. We also conducted a broader review of financial processes, systems and controls across the group

• Steps taken in Italy:

− suspended number of senior management in Italy who have now left business

− new President of our European operations, new CEO and CFO of BT Italy, from outside Italy

− implementing improvements to governance, compliance and control culture and capabilities of our people in the organisation

• Group-wide steps to improve control, governance and compliance environment:

− increasing resources and improving capabilities of the controlling function and the audit function outside the UK

− further developing our integrated risk and assurance reporting processes

− enhancing controls and compliance programme to strengthen awareness of the standards we expect, the capabilities of our people, and to reinforce the importance of doing business in an ethical, disciplined and standardised way

− new CEO and CFO of BT Italy will continue to review Italian management and finance teams, and work with BT Group Ethics and Compliance to improve the governance, compliance and financial safeguards

− continue to rotate senior management among all countries in Global Services

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

2017/18 financial outlook

52

Underlying revenue1 ex transit Broadly flat

EBITDA2 £7.5bn - £7.6bn

Normalised free cash flow3 £2.7bn - £2.9bn

1 excludes specific items, foreign exchange movements and disposals2 before specific items 3 before specific items, pension deficit payments and the cash tax benefit of pension deficit payments

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Shareholder distributions

• Progressive dividend policy unchanged: to maintain or grow the dividend each year whilst reflecting a

number of factors including underlying medium term earnings expectations and levels of business

reinvestment

• From next year the interim dividend per share will be fixed at 30% of the prior year’s full year dividend.

However, in this transitional year we have decided to hold interim dividend at 4.85p per share

• £221m shares bought back in H1, more than fulfils 17/18 planned buyback of c.£100m, to counteract

dilutive effect of employee share option plans

53

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

17/18 18/19 19/20 20/21 21/22 22/23 23/24 24/25 25/26 After 2026

£m

Debt and maturity profile

• Strong balance sheet with cash and current investments of £4.9bn and undrawn committed credit facilities of £2.1bn

• BBB+ (or equivalent) credit rating with Fitch, Moody’s and S&P

54

Term debt maturity profile

Effective rate1

1 the effective rate represents the weighted average interest rate on bonds maturing in each period after the impact of hedging2 As at 30 Dec 2017

7.10% 3.67% 4.31% 2.34% 2.33% 2.23% 4.43% 5.6%

30 Sept2017

NormalisedFCF

Specificitems

Pension deficitpayments

Tax benefit ofpension deficit

payments

Dividends Other 31 Dec2017

Change in net debt

£9.5bn

£8.9bn

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

Our purpose is to use the power of communications to make a better world

• Delivering our purpose creates measurable societal and environmental value. It also promotes sustainable revenue growth and helps with risk mitigation

Being ethical and responsible Social impact 1 Environment

• We're committed to respecting human rights and we use the UN Guiding principles on business and Human Rights to inform our approach. This includes working with our suppliers to ensure conditions in the work place and to combat modern slavery

• We protect our customers from online threats. We are co-founders of ‘Internet Matters’ which helps children stay safe online

• Being ethical helps us build trust and mitigate reputational and operational risks

• In 2016/17 we helped customers reduce carbon by 1.8 times BT’s end-to-end carbon emissions (target: 3:1 by 2020)

• We do this by using conferencing, flexible working, M2M2 solutions and other products and services to help customers cut carbon, whilst also working to reduce our own end-to-end carbon emissions

• £5.3bn of 2016/17 revenue was generated from products and services that help our customers save carbon emissions. This is 22%of our group revenue

• Helped 1.5m children receive better teaching in computing and tech skills since 2014/15 (as at November 2017, target: 5m by 2020)

• Generated £422m for good causes using our skills and technology since 2012/13 (target: >£1bn by 2020)

• Inspired 31% of our people to volunteer their time and skills in 2016/17 (target: 66% by 2020)

• Helped 3.9m people overcome social disadvantage through the benefits our products and services since 2014/15 (target: 10m by 2020)

1 By end 2016/17 financial year unless otherwise stated 2Machine-to-machine

55

British Telecommunications plc 2018

Overviewand Strategy

Group Consumer EEBusiness

and Public SectorGlobal

ServicesWholesale

and VenturesOpenreach Appendix

0

5

10

15

20

25

30

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Other fibre BT fibre Other DSL BT DSL VMED

UK broadband connections - move to faster technologies

56

Virgin Mediac.5.1m (+25%)

BTc.9.3m (+60%)

- of which 5.5m fibre

Other CPsc.11.3m (+11%)

- of which 3.7m fibre

m

Other CPs10.2m

BT6.0m

VMED4.1m

Fall in ‘Other CPs’ due to EE becoming part of BT

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

British Telecommunications plc 2018

@BTGroup

LSE: BT.A

NYSE: BT

Investor Relations - contact details

Forward looking statements caution

Certain statements in this presentation are forward-looking and are made in reliance on the safe harbour provisions of the US Private Securities Litigation Reform Act of 1995. These statements include, without

limitation, those concerning: our outlook for 2017/18 including revenue, EBITDA and free cash flow; dividend growth and share buyback; net debt; charges to the BT Pension Scheme; group restructuring; accelerating

cost transformation; investment in customer experience and digital infrastructure; Universal Broadband Commitment; and FTTP roll out .

Although BT believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. Because these statements

involve risks and uncertainties, actual results may differ materially from those expressed or implied by these forward-looking statements.

Factors that could cause differences between actual results and those implied by the forward-looking statements include, but are not limited to: material adverse changes in economic conditions in the markets served

by BT whether as a result of the uncertainties arising from the UK’s exit from the EU or otherwise; future regulatory and legal actions, decisions, outcomes of appeal and conditions or requirements in BT’s operating

areas, including the outcome of Ofcom’s strategic review of digital communications in the UK and the implementation of the DCR commitments, as well as competition from others; consultations and market reviews

including the outcome of Ofcom’s consultation on the Wholesale Local Access market and the results of any future spectrum auctions; selection by BT and its lines of business of the appropriate trading and marketing

models for its products and services; fluctuations in foreign currency exchange rates and interest rates; technological innovations, including the cost of developing new products, networks and solutions and the need to

increase expenditures for improving the quality of service; prolonged adverse weather conditions resulting in a material increase in overtime, staff or other costs, or impact on customer service; developments in the

convergence of technologies; external threats to cyber security, data or resilience; political and geo-political risks; the anticipated benefits and advantages of new technologies, products and services not being realised;

the timing of entry and profitability of BT in certain markets; significant changes in market shares for BT and its principal products and services; the underlying assumptions and estimates made in respect of major

customer contracts proving unreliable; the anticipated benefits, synergies and cost savings of the EE integration not being delivered; the outcome of the BTPS triennial valuation and discussions of the pensions review;

the aims of and anticipated cost savings from the group’s restructuring programmes not being delivered; the improvements to the control environment proposed following the investigations into BT’s Italian business not

being implemented successfully or effectively; and general financial market conditions affecting BT’s performance and ability to raise finance. BT undertakes no obligation to update any forward-looking statements

whether as a result of new information, future events or otherwise.

57

tel: +44 (0)207 356 4909

email: [email protected]

web: www.bt.com/ir