Embed Size (px)

Citation preview

18th September 2015

BRING OUT YOUR BEST CHINA

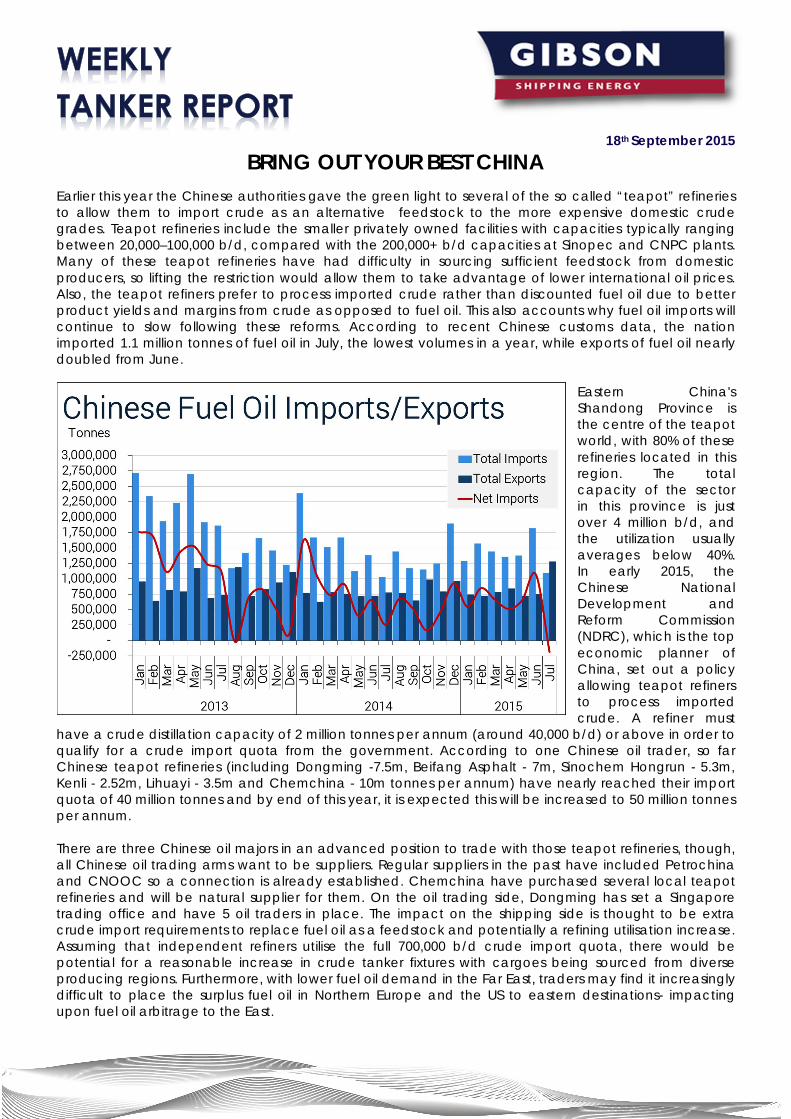

Earlier this year the Chinese authorities gave the green light to several of the so called “teapot” refineries to allow them to import crude as an alternative feedstock to the more expensive domestic crude grades. Teapot refineries include the smaller privately owned facilities with capacities typically ranging between 20,000–100,000 b/d, compared with the 200,000+ b/d capacities at Sinopec and CNPC plants. Many of these teapot refineries have had difficulty in sourcing sufficient feedstock from domestic producers, so lifting the restriction would allow them to take advantage of lower international oil prices. Also, the teapot refiners prefer to process imported crude rather than discounted fuel oil due to better product yields and margins from crude as opposed to fuel oil. This also accounts why fuel oil imports will continue to slow following these reforms. According to recent Chinese customs data, the nation imported 1.1 million tonnes of fuel oil in July, the lowest volumes in a year, while exports of fuel oil nearly doubled from June.

Eastern China's Shandong Province is the centre of the teapot world, with 80% of these refineries located in this region. The total capacity of the sector in this province is just over 4 million b/d, and the utilization usually averages below 40%. In early 2015, the Chinese National Development and Reform Commission (NDRC), which is the top economic planner of China, set out a policy allowing teapot refiners to process imported crude. A refiner must

have a crude distillation capacity of 2 million tonnes per annum (around 40,000 b/d) or above in order to qualify for a crude import quota from the government. According to one Chinese oil trader, so far Chinese teapot refineries (including Dongming -7.5m, Beifang Asphalt - 7m, Sinochem Hongrun - 5.3m, Kenli - 2.52m, Lihuayi - 3.5m and Chemchina - 10m tonnes per annum) have nearly reached their import quota of 40 million tonnes and by end of this year, it is expected this will be increased to 50 million tonnes per annum. There are three Chinese oil majors in an advanced position to trade with those teapot refineries, though, all Chinese oil trading arms want to be suppliers. Regular suppliers in the past have included Petrochina and CNOOC so a connection is already established. Chemchina have purchased several local teapot refineries and will be natural supplier for them. On the oil trading side, Dongming has set a Singapore trading office and have 5 oil traders in place. The impact on the shipping side is thought to be extra crude import requirements to replace fuel oil as a feedstock and potentially a refining utilisation increase. Assuming that independent refiners utilise the full 700,000 b/d crude import quota, there would be potential for a reasonable increase in crude tanker fixtures with cargoes being sourced from diverse producing regions. Furthermore, with lower fuel oil demand in the Far East, traders may find it increasingly difficult to place the surplus fuel oil in Northern Europe and the US to eastern destinations- impacting upon fuel oil arbitrage to the East.

CRUDE

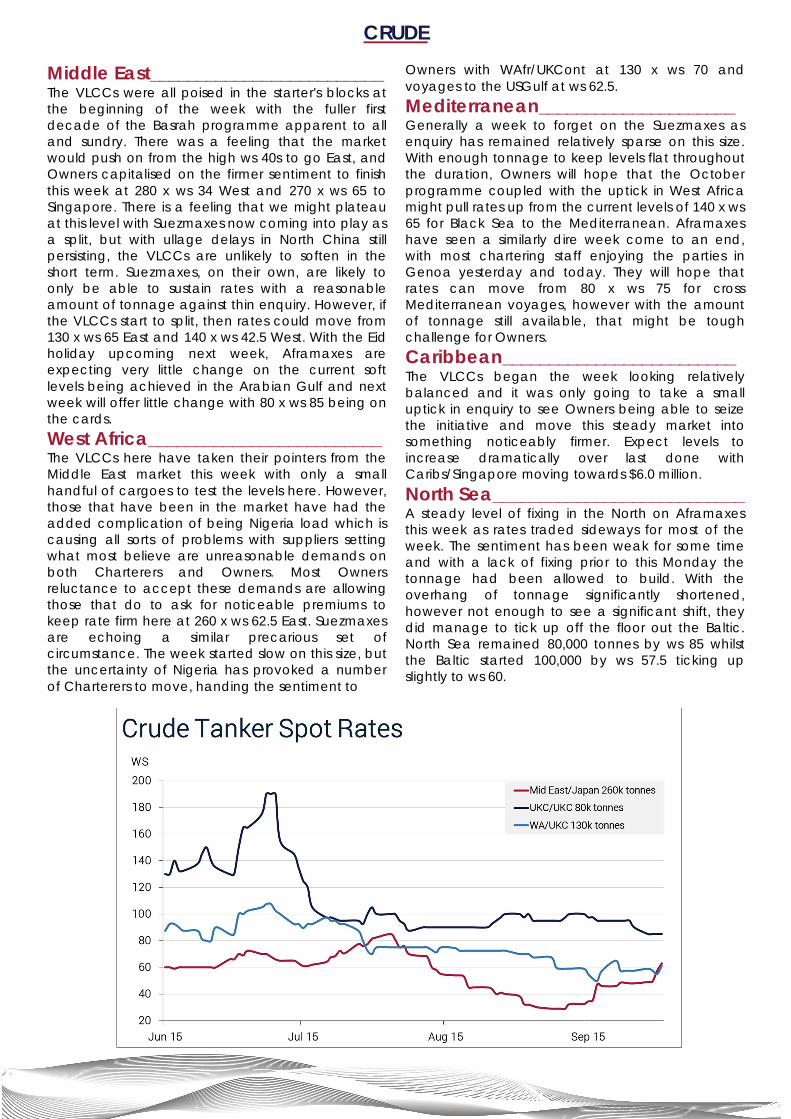

Middle East_________________________ The VLCCs were all poised in the starter's blocks at the beginning of the week with the fuller first decade of the Basrah programme apparent to all and sundry. There was a feeling that the market would push on from the high ws 40s to go East, and Owners capitalised on the firmer sentiment to finish this week at 280 x ws 34 West and 270 x ws 65 to Singapore. There is a feeling that we might plateau at this level with Suezmaxes now coming into play as a split, but with ullage delays in North China still persisting, the VLCCs are unlikely to soften in the short term. Suezmaxes, on their own, are likely to only be able to sustain rates with a reasonable amount of tonnage against thin enquiry. However, if the VLCCs start to split, then rates could move from 130 x ws 65 East and 140 x ws 42.5 West. With the Eid holiday upcoming next week, Aframaxes are expecting very little change on the current soft levels being achieved in the Arabian Gulf and next week will offer little change with 80 x ws 85 being on the cards. West Africa_________________________ The VLCCs here have taken their pointers from the Middle East market this week with only a small handful of cargoes to test the levels here. However, those that have been in the market have had the added complication of being Nigeria load which is causing all sorts of problems with suppliers setting what most believe are unreasonable demands on both Charterers and Owners. Most Owners reluctance to accept these demands are allowing those that do to ask for noticeable premiums to keep rate firm here at 260 x ws 62.5 East. Suezmaxes are echoing a similar precarious set of circumstance. The week started slow on this size, but the uncertainty of Nigeria has provoked a number of Charterers to move, handing the sentiment to

Owners with WAfr/UKCont at 130 x ws 70 and voyages to the USGulf at ws 62.5. Mediterranean_____________________ Generally a week to forget on the Suezmaxes as enquiry has remained relatively sparse on this size. With enough tonnage to keep levels flat throughout the duration, Owners will hope that the October programme coupled with the uptick in West Africa might pull rates up from the current levels of 140 x ws 65 for Black Sea to the Mediterranean. Aframaxes have seen a similarly dire week come to an end, with most chartering staff enjoying the parties in Genoa yesterday and today. They will hope that rates can move from 80 x ws 75 for cross Mediterranean voyages, however with the amount of tonnage still available, that might be tough challenge for Owners. Caribbean_________________________ The VLCCs began the week looking relatively balanced and it was only going to take a small uptick in enquiry to see Owners being able to seize the initiative and move this steady market into something noticeably firmer. Expect levels to increase dramatically over last done with Caribs/Singapore moving towards $6.0 million. North Sea___________________________ A steady level of fixing in the North on Aframaxes this week as rates traded sideways for most of the week. The sentiment has been weak for some time and with a lack of fixing prior to this Monday the tonnage had been allowed to build. With the overhang of tonnage significantly shortened, however not enough to see a significant shift, they did manage to tick up off the floor out the Baltic. North Sea remained 80,000 tonnes by ws 85 whilst the Baltic started 100,000 by ws 57.5 ticking up slightly to ws 60.

CLEAN PRODUCTS

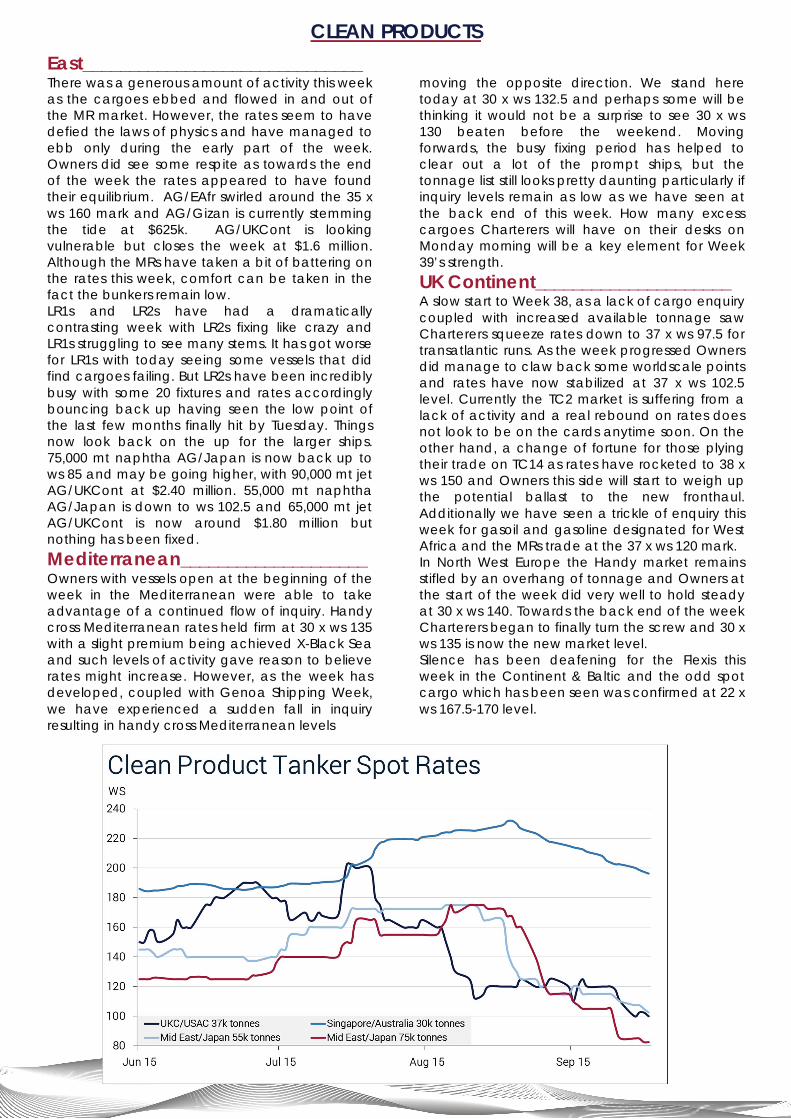

East______________________________ There was a generous amount of activity this week as the cargoes ebbed and flowed in and out of the MR market. However, the rates seem to have defied the laws of physics and have managed to ebb only during the early part of the week. Owners did see some respite as towards the end of the week the rates appeared to have found their equilibrium. AG/EAfr swirled around the 35 x ws 160 mark and AG/Gizan is currently stemming the tide at $625k. AG/UKCont is looking vulnerable but closes the week at $1.6 million. Although the MRs have taken a bit of battering on the rates this week, comfort can be taken in the fact the bunkers remain low. LR1s and LR2s have had a dramatically contrasting week with LR2s fixing like crazy and LR1s struggling to see many stems. It has got worse for LR1s with today seeing some vessels that did find cargoes failing. But LR2s have been incredibly busy with some 20 fixtures and rates accordingly bouncing back up having seen the low point of the last few months finally hit by Tuesday. Things now look back on the up for the larger ships. 75,000 mt naphtha AG/Japan is now back up to ws 85 and may be going higher, with 90,000 mt jet AG/UKCont at $2.40 million. 55,000 mt naphtha AG/Japan is down to ws 102.5 and 65,000 mt jet AG/UKCont is now around $1.80 million but nothing has been fixed. Mediterranean____________________ Owners with vessels open at the beginning of the week in the Mediterranean were able to take advantage of a continued flow of inquiry. Handy cross Mediterranean rates held firm at 30 x ws 135 with a slight premium being achieved X-Black Sea and such levels of activity gave reason to believe rates might increase. However, as the week has developed, coupled with Genoa Shipping Week, we have experienced a sudden fall in inquiry resulting in handy cross Mediterranean levels

moving the opposite direction. We stand here today at 30 x ws 132.5 and perhaps some will be thinking it would not be a surprise to see 30 x ws 130 beaten before the weekend. Moving forwards, the busy fixing period has helped to clear out a lot of the prompt ships, but the tonnage list still looks pretty daunting particularly if inquiry levels remain as low as we have seen at the back end of this week. How many excess cargoes Charterers will have on their desks on Monday morning will be a key element for Week 39’s strength. UK Continent_____________________ A slow start to Week 38, as a lack of cargo enquiry coupled with increased available tonnage saw Charterers squeeze rates down to 37 x ws 97.5 for transatlantic runs. As the week progressed Owners did manage to claw back some worldscale points and rates have now stabilized at 37 x ws 102.5 level. Currently the TC2 market is suffering from a lack of activity and a real rebound on rates does not look to be on the cards anytime soon. On the other hand, a change of fortune for those plying their trade on TC14 as rates have rocketed to 38 x ws 150 and Owners this side will start to weigh up the potential ballast to the new fronthaul. Additionally we have seen a trickle of enquiry this week for gasoil and gasoline designated for West Africa and the MRs trade at the 37 x ws 120 mark. In North West Europe the Handy market remains stifled by an overhang of tonnage and Owners at the start of the week did very well to hold steady at 30 x ws 140. Towards the back end of the week Charterers began to finally turn the screw and 30 x ws 135 is now the new market level. Silence has been deafening for the Flexis this week in the Continent & Baltic and the odd spot cargo which has been seen was confirmed at 22 x ws 167.5-170 level.

DIRTY PRODUCTS

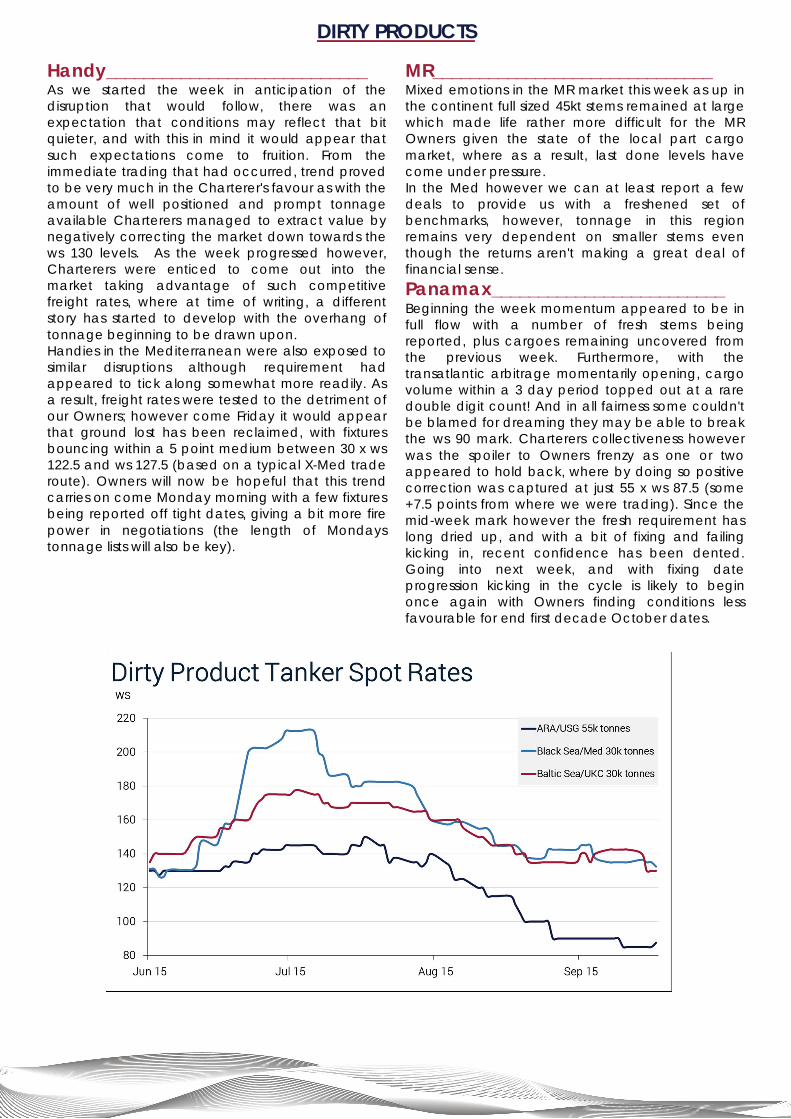

Handy____________________________ As we started the week in anticipation of the disruption that would follow, there was an expectation that conditions may reflect that bit quieter, and with this in mind it would appear that such expectations come to fruition. From the immediate trading that had occurred, trend proved to be very much in the Charterer's favour as with the amount of well positioned and prompt tonnage available Charterers managed to extract value by negatively correcting the market down towards the ws 130 levels. As the week progressed however, Charterers were enticed to come out into the market taking advantage of such competitive freight rates, where at time of writing, a different story has started to develop with the overhang of tonnage beginning to be drawn upon. Handies in the Mediterranean were also exposed to similar disruptions although requirement had appeared to tick along somewhat more readily. As a result, freight rates were tested to the detriment of our Owners; however come Friday it would appear that ground lost has been reclaimed, with fixtures bouncing within a 5 point medium between 30 x ws 122.5 and ws 127.5 (based on a typical X-Med trade route). Owners will now be hopeful that this trend carries on come Monday morning with a few fixtures being reported off tight dates, giving a bit more fire power in negotiations (the length of Mondays tonnage lists will also be key).

MR______________________________ Mixed emotions in the MR market this week as up in the continent full sized 45kt stems remained at large which made life rather more difficult for the MR Owners given the state of the local part cargo market, where as a result, last done levels have come under pressure. In the Med however we can at least report a few deals to provide us with a freshened set of benchmarks, however, tonnage in this region remains very dependent on smaller stems even though the returns aren't making a great deal of financial sense. Panamax_________________________ Beginning the week momentum appeared to be in full flow with a number of fresh stems being reported, plus cargoes remaining uncovered from the previous week. Furthermore, with the transatlantic arbitrage momentarily opening, cargo volume within a 3 day period topped out at a rare double digit count! And in all fairness some couldn't be blamed for dreaming they may be able to break the ws 90 mark. Charterers collectiveness however was the spoiler to Owners frenzy as one or two appeared to hold back, where by doing so positive correction was captured at just 55 x ws 87.5 (some +7.5 points from where we were trading). Since the mid-week mark however the fresh requirement has long dried up, and with a bit of fixing and failing kicking in, recent confidence has been dented. Going into next week, and with fixing date progression kicking in the cycle is likely to begin once again with Owners finding conditions less favourable for end first decade October dates.

JLI/SH/OD/DP/LHT

Produced by Gibson Consultancy and Research Visit Gibson’s website at www.gibson.co.uk for latest market information

E.A. GIBSON SHIPBROKERS LTD., AUDREY HOUSE, 16-20 ELY PLACE, LONDON EC1P 1HP Switchboard Telephone: (UK) 020 7667 1000 (International) +44 20 7667 1000

E-MAIL: [email protected]: 94012383 GTKR G FACSIMILE No: 020 7831 8762 BIMCOM E-MAIL: 19086135

This report has been produced for general information and is not a replacement for specific advice. While the market information is believed to be reasonably accurate, it is by its nature subject to limited audits and validations. No responsibility can be accepted for any errors or any consequences arising therefrom. No part of the report may be reproduced or circulated without our prior written approval. © E.A. Gibson Shipbrokers Ltd 2015.

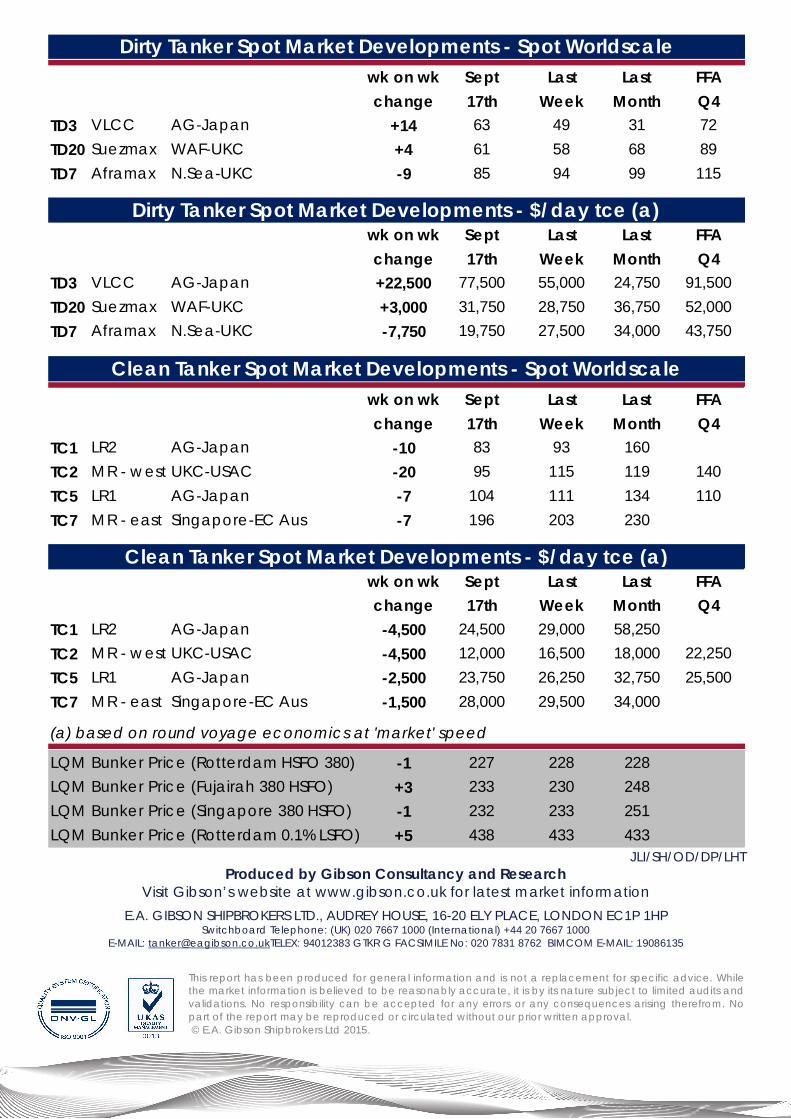

wk on wk Sept Last Last FFAchange 17th Week Month Q4

TD3 VLCC AG-Japan +14 63 49 31 72TD20 Suezmax WAF-UKC +4 61 58 68 89TD7 Aframax N.Sea-UKC -9 85 94 99 115

wk on wk Sept Last Last FFAchange 17th Week Month Q4

TD3 VLCC AG-Japan +22,500 77,500 55,000 24,750 91,500TD20 Suezmax WAF-UKC +3,000 31,750 28,750 36,750 52,000TD7 Aframax N.Sea-UKC -7,750 19,750 27,500 34,000 43,750

wk on wk Sept Last Last FFAchange 17th Week Month Q4

TC1 LR2 AG-Japan -10 83 93 160TC2 MR - west UKC-USAC -20 95 115 119 140TC5 LR1 AG-Japan -7 104 111 134 110TC7 MR - east Singapore-EC Aus -7 196 203 230

wk on wk Sept Last Last FFAchange 17th Week Month Q4

TC1 LR2 AG-Japan -4,500 24,500 29,000 58,250TC2 MR - west UKC-USAC -4,500 12,000 16,500 18,000 22,250TC5 LR1 AG-Japan -2,500 23,750 26,250 32,750 25,500TC7 MR - east Singapore-EC Aus -1,500 28,000 29,500 34,0000

LQM Bunker Price (Rotterdam HSFO 380) -1 227 228 228LQM Bunker Price (Fujairah 380 HSFO) +3 233 230 248LQM Bunker Price (Singapore 380 HSFO) -1 232 233 251LQM Bunker Price (Rotterdam 0.1% LSFO) +5 438 433 433

(a) based on round voyage economics at 'market' speed

Dirty Tanker Spot Market Developments - Spot Worldscale

Dirty Tanker Spot Market Developments - $/day tce (a)

Clean Tanker Spot Market Developments - Spot Worldscale

Clean Tanker Spot Market Developments - $/day tce (a)