Embed Size (px)

Citation preview

BRIEFING ON ISLAMIC HOME FINANCING FOR

DELEGATES FROM CENTRAL BANK OF AFGHANISTAN

15 AUGUST 2014

Strictly Private & Confidential

TABLE OF CONTENTS

INTRODUCTIONINTRODUCTION

BANK ISLAM's HOME FINANCING BANK ISLAM's HOME FINANCING PRODUCT STRUCTURESPRODUCT STRUCTURES

HOME FINANCING PRODUCT FEATURESHOME FINANCING PRODUCT FEATURES

Sec 1

Sec 2

Sec 3

Originating Department Page 2

HOME FINANCING PRODUCT FEATURESHOME FINANCING PRODUCT FEATURES

CREDIT UNDERWRITING CRITERIACREDIT UNDERWRITING CRITERIA

RECOVERYRECOVERY

RISK PROFILINGRISK PROFILING

Sec 3

Sec 4

Sec 5

Sec 6

INTRODUCTION

Page 3

INTRODUCTION

� Since its establishment in 1983, home financing is one of Bank Islam’s key offerings to

provide Muslim communities with Shariah compliant financing for acquiring their houses.

� Home financing provides the Bank with stable stream of income over its facility tenure and

it is categorized as secured financing

� As for Shariah contracts, Home Financing has seen the application of various

contracts/concepts; from local acceptance to global standards

Background

HOME FINANCINGSHARIAH CONTRACTS

Bai’ Bithaman Ajil

Home Financing-i

(Bai’ Inah)

Musyarakah

Mutanaqisah Home

Financing

Ijarah Muntahiah

Bit Tamlik Home

Financing

Property

Financing-i

(Tawarruq)

HOME FINANCING

Page 4

� 20% discount on stamp duty for Islamic primary documents

� Cost benefit to client (no commitment fee and fixed finance cost)

� Capitalize on innovative & dynamic alternative product (eg: fixed rate combination with

floating rate and ceiling rate as protection)

WHY GO FOR ISLAMIC HOME FINANCING?

� Conversion (refinance) of conventional loan to Islamic facility is stamp duty exempted

� Sound Legal framework

� Islamic banking falls within regular civil court’s jurisdiction

� Centralised National Shariah Advisory Council

� New Islamic Financial Services Act (IFSA) was established to provide a

comprehensive legal framework that promotes Shariah compliance in all aspects of

regulation and supervision

Page 5

BANK ISLAM'S HOME

FINANCING PRODUCT

Page 6

FINANCING PRODUCT

STRUCTURES

JOURNEY OF BANK ISLAM'S HOME FINANCING

Bai Bithamin

Ajil / Inah

Musharakah

Mutanaqisah

Ijarah

Tawarruq

Ijarah

Muntahiah

Bit Tamlik

1983 – Dec 2012 Jan 2013 – onwards

(interim)

To be launched….

PRODUCT STRUCTURE: BAI' INAH / BAI BITHAMAN AJIL

Highlights:

1) No inter-conditional

Page 8

2) Preferred mode for Bank to

acquire and sell on piece meal

basis

3) Downsides:

� Inventory risk

� Market risk

� High capital charge

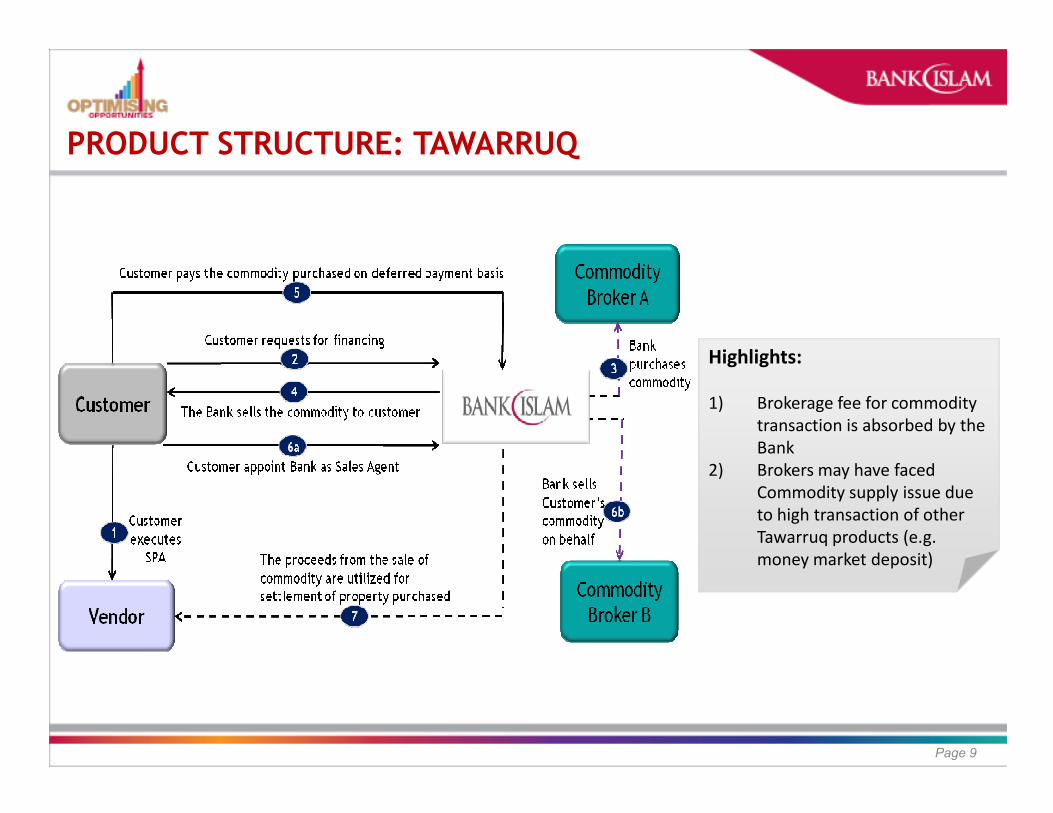

PRODUCT STRUCTURE: TAWARRUQ

Highlights:

1) Brokerage fee for commodity

Page 9

1) Brokerage fee for commodity

transaction is absorbed by the

Bank

2) Brokers may have faced

Commodity supply issue due

to high transaction of other

Tawarruq products (e.g.

money market deposit)

PRODUCT STRUCTURE: IJARAH MUNTAHIAH BIT TAMLIK

Highlights:

1) Cost of maintaining house

Page 10

1) Cost of maintaining house

� Major maintenance – Bank

� Periodical maintenance –

Customer

2) To secure the house in favor of

the Bank is by way of Deed

instead of charge

PRODUCT STRUCTURE: MUSHARAKAH MUTANAQISAH

Bank and customer execute MM agreement.

a) Bank purchases part of customer’s share e.g. 90%. Bai’ Musawamah)

b) Customer promises to purchase Bank’s share from time to time.

The MM contract is dissolved

when ALL the Bank’s share

Partnership3

5

Page 11

Customer enters into SPA with the vendor.

Customer applies for financing

JV leases the property to the customer (Ijarah).Rents shall be divided between Bank and

customer’s acquisition of the Bank’s share.

when ALL the Bank’s share transferred to the customer.

Customer

Vendor1

2

4

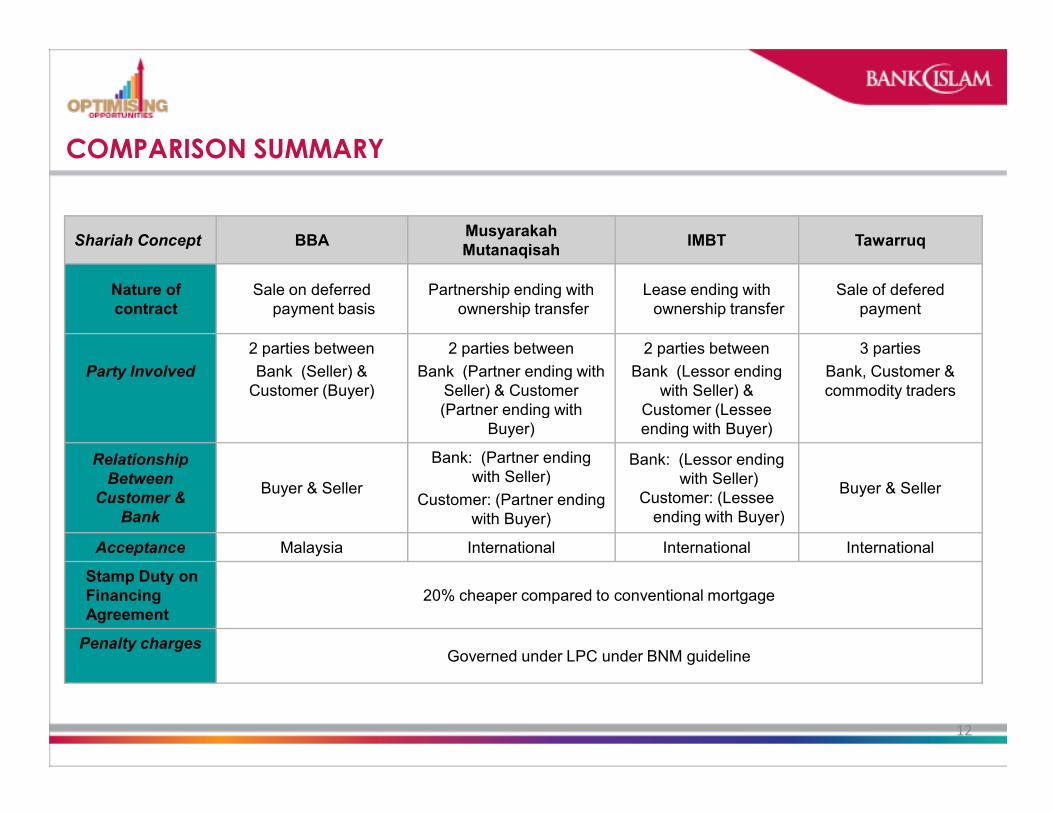

Shariah Concept BBAMusyarakah

MutanaqisahIMBT Tawarruq

Nature of

contract

Sale on deferred

payment basis

Partnership ending with

ownership transfer

Lease ending with

ownership transfer

Sale of defered

payment

Party Involved

2 parties between

Bank (Seller) &

Customer (Buyer)

2 parties between

Bank (Partner ending with

Seller) & Customer

(Partner ending with

2 parties between

Bank (Lessor ending

with Seller) &

Customer (Lessee

3 parties

Bank, Customer &

commodity traders

COMPARISON SUMMARY

12

(Partner ending with

Buyer)

Customer (Lessee

ending with Buyer)

Relationship

Between

Customer &

Bank

Buyer & Seller

Bank: (Partner ending

with Seller)

Customer: (Partner ending

with Buyer)

Bank: (Lessor ending

with Seller)

Customer: (Lessee

ending with Buyer)

Buyer & Seller

Acceptance Malaysia International International International

Stamp Duty on

Financing

Agreement

20% cheaper compared to conventional mortgage

Penalty chargesGoverned under LPC under BNM guideline

HOME FINANCING

Page 13

HOME FINANCING

PRODUCT FEATURES

GENERIC PRODUCT FEATURES

PRODUCT PROGRAMPRODUCT PROGRAM BAITIBAITI WAHDAH (REFINANCING)WAHDAH (REFINANCING)

Purpose Financing the purchase of :

� Under construction

properties

� Completed properties

Refinancing of completed properties

not less than RM100,000

Tenure Up to 35 years or age 70; whichever is earlier

Page 14

Tenure Up to 35 years or age 70; whichever is earlier

Margin of Financing Up to 90% against

SPA/OMV + 10% (legal

fee/stamp

duty/valuation

fee/MRTT/LTHT)

Up to 90% OMV + 10% (legal fee/stamp

duty/valuation fee/MRTT/LTHT)

Takaful Coverage � MRTT – Compulsory

� LTHT – Compulsory (if applicable)

PRODUCT PROGRAMPRODUCT PROGRAM BAITIBAITI WAHDAH (REFINANCING)

Early settlement/

Lock in Period

� No lock-in period

� Package customer to reimburse the actual cost incurred under ZEC if

redeemed within 5 years

Profit Rate Ranges from BFR-1.30% p.a to BFR-2.40% p.a based on the customer’s

grade scoring

GENERIC PRODUCT FEATURES, CONTINUED

Page 15

grade scoring

Tawidh As per BNM rulings

Processing Fees Waived

Payment Holiday � Customer can enjoy rest payment in Nov & Dec every year

� Applicable for floating rates only

� Minimum property value RM100,000

CREDIT UNDERWRITING

Page 16

CREDIT UNDERWRITING

CRITERIA

RISK ACCEPTANCE CRITERIA

CustomerCustomer

Property TypeProperty Type

� Salary Earner

� Self Employed

Note: Preference is direct salary deduction from employer

� Townhouses

� Semi Permanent Bungalow

� Apartment

� Service apartment

Property ValueProperty Value

Property Property

LocationLocation

� Semi Permanent Bungalow

� Condominium

� Service apartment

� Flat

� Purchase from developer

� Refinancing / Sub sale

� Property situated not too close to retention

pond, dumping site, incinerator, transmission

station, generator-sub station

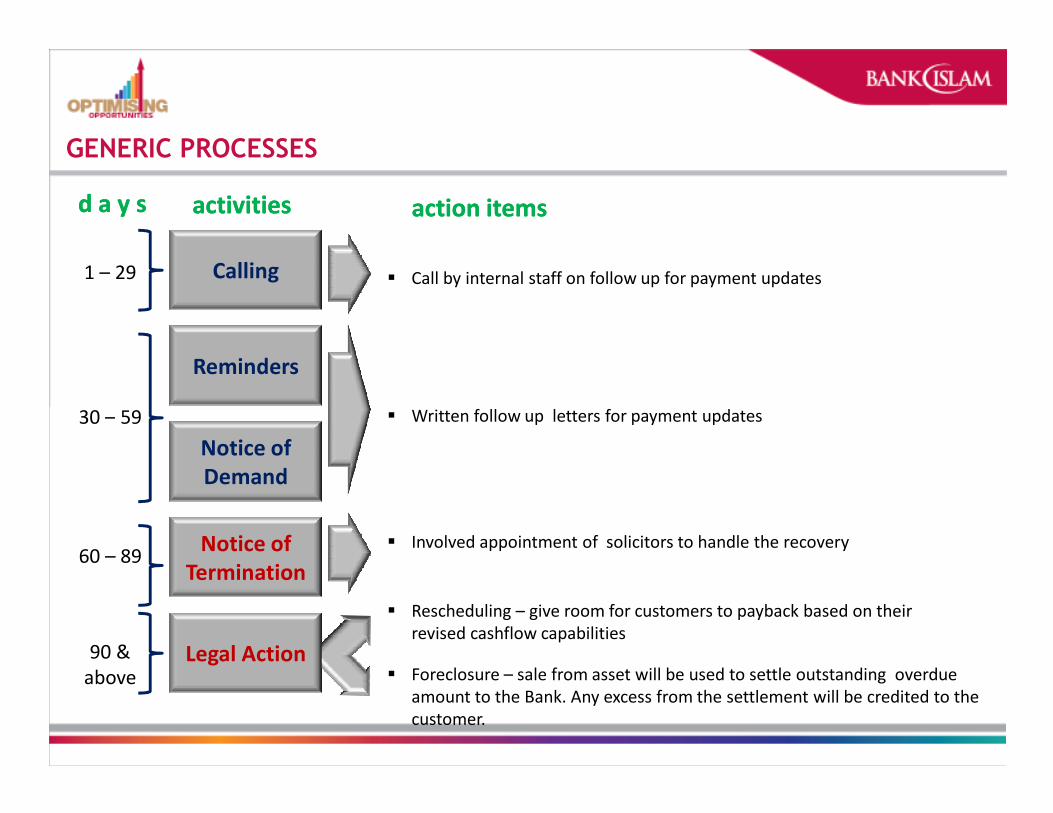

RECOVERY

Page 18

RECOVERY

THE APPROACHTHE APPROACH

Soft Approach

� Rescheduling

� Ease customer

cashflow

� Tenor may be

Hard Approach

� Civil proceeding

� Foreclosure

Note:� Tenor may be

lengthen

� No new aqad

� Restructuring

� New facility terms

� New aqad

� New documentation

Note:

Sale from asset will be used

to settle outstanding

overdue amount to the

Bank. Any excess from the

settlement will be credited

to the customer.

RECOVERYRECOVERY

Calling

Reminders

1 – 29

30 – 59

d a y sd a y s

� Call by internal staff on follow up for payment updates

� Written follow up letters for payment updates

activitiesactivities action itemsaction items

GENERIC PROCESSES

Notice of

Demand

Notice of

Termination

30 – 59

60 – 89

90 &

above � Foreclosure – sale from asset will be used to settle outstanding overdue

amount to the Bank. Any excess from the settlement will be credited to the

customer.

� Rescheduling – give room for customers to payback based on their

revised cashflow capabilities

Legal Action

� Involved appointment of solicitors to handle the recovery

� Written follow up letters for payment updates

RISK PROFILING

Page 21

RISK PROFILING

CREDIT RISK PROFILING – HFA (DEC '12 – JUN '14)

HFA- GENDER, AGE, PACKAGE TYPE

The weighted average age bracket unchanged despite the increase in the middle aged group TOS%

concentration (30-40 years old) bracket.

Page 5G

CREDIT RISK PROFILING – HFA (DEC '12 – JUN '14)

HFA- STATE & PROPERTY TYPE

“State” profile for HFA customers remained unchanged with highest concentration in Central Region. There is an

unchanged profile for Property Type- despite improved Impaired rates in Jun’14.

Page 5I

CREDIT RISK PROFILING – HFA (DEC '12 – JUN '14)

HFA- OCCUPATION

“Occupation” profile for HFA customers as at Jun’14 recorded Government employees, Executive (Higher Level)

and Executive (Medium Level) being among the Top 3 occupation profile.

Page 5J

Question &

AnswerAnswer

Page 25

Page 26