Embed Size (px)

DESCRIPTION

Â

Citation preview

BRAZIL BENEFITSGUIDE2014

HELLOmy name is

We are a boutique insurance brokerage and consulting service focused on benefits programs management. With a high standard professional team, we manage benefits for over than 280 thousand lives.

Part of UIB Group (United Insurance Brokers) – world’s eightest insurance and reinsurance broker, with representatives in 17 countries, present in Europe, Middle East, North Africa, Asia and Latin America – we are one of the few brokers focused on the final user health and quality of life, always in balance with your economic reality.

Get to know more about us on uibbeneficios.com

WE ARE UIB BENEFÍCIOS

THIS WAYto Brazil

DEMOGRAPHICS

MALE POPULATION (BY AGE)

FEMALE POPULATION (BY AGE)

LEVEL OF COVERAGE MAP

TYPE OF CONTRACTS

CONTRACTS & COVERAGE

MARKET PLAYERS

SOCIAL SECURITY SYSTEM

RETIREMENT BENEFITS

WORKER COMPENSATION

CONTRIBUTION

FGTS: GOVERNMENT SEVERANCE INDEMNITY FUND

FOR EMPLOYEES

TRANSPORTATION VOUCHER

UNEMPLOYMENT INSURANCE

OTHER BENEFITS

PRIVATE BENEFITS – GENERAL MARKET PRACTICE

HEALTH CARE

NATIONAL HEALTH AGENCY

PLAN DESIGN

KEY ASPECTS

CONDITIONS FOR RENEWAL

DENTAL CARE

GROUP LIFE

PENSION

7

8

9

10

11

12

13

14

16

18

19

20

22

23

24

25

26

28

29

30

31

32

33

34

INDEX

THIS WAYto Brazil

7

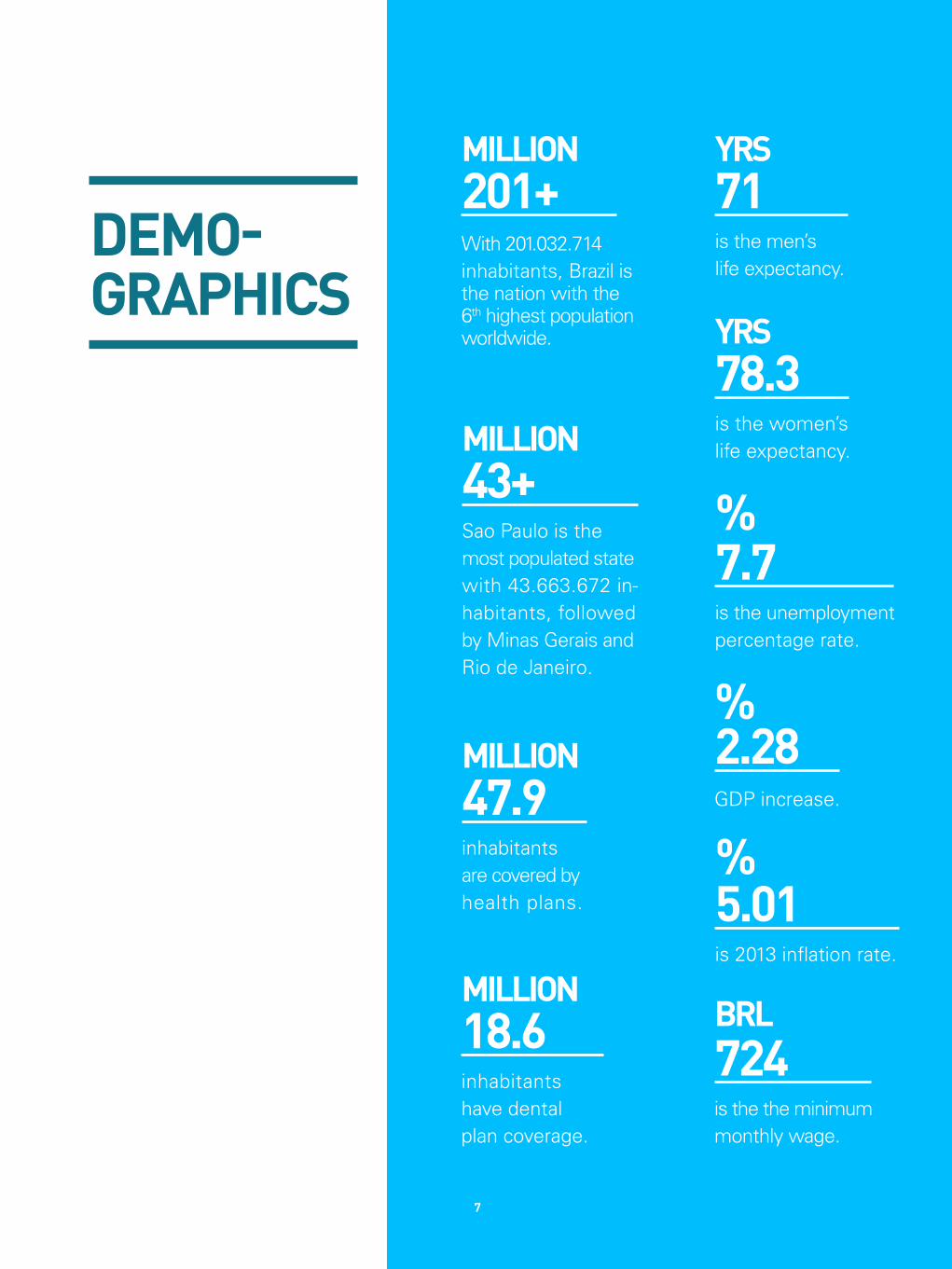

million 201+ With 201.032.714 inhabitants, Brazil is the nation with the 6th highest population worldwide.

million 43+ Sao Paulo is the most populated state with 43.663.672 in- habitants, followed by Minas Gerais and Rio de Janeiro.

million 47.9 inhabitants are covered by health plans.

million18.6 inhabitants have dental plan coverage.

yrs 71 is the men’s life expectancy.

yrs 78.3 is the women’s life expectancy.

%2.28 GDP increase.

%5.01 is 2013 inflation rate.

brl 724 is the the minimum monthly wage.

%7.7 is the unemployment percentage rate.

DEMO-GRAPHICS

8

MALE POPULATION (BY AGE)

OVERALL POPULATIONCOVERED POPULATION

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

%1.5

1.0

0.5

0100

AGE

9

FEMALE POPULATION (BY AGE)

OVERALL POPULATIONCOVERED POPULATION

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

%1.5

1.0

0.5

0100

AGE

10

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

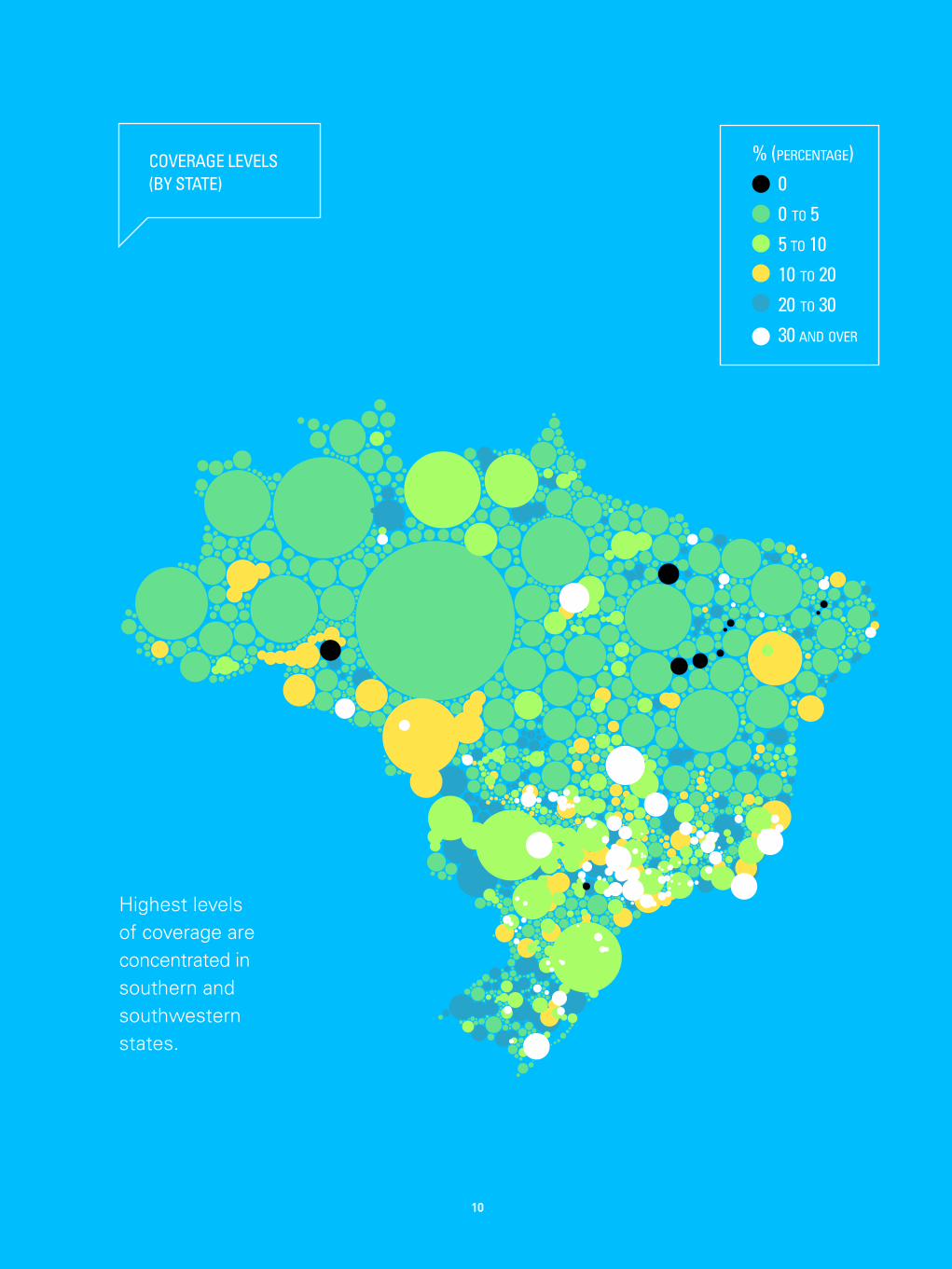

Highest levels of coverage are concentrated in southern and southwestern states.

00 to 55 to 1010 to 2020 to 3030 and over

% (percentage)COVERAGE LEVELS(BY STATE)

11

As illustrated below (in %), most contracts are offered by employers, representing

63.6% of the market.

not informed individual collective membership corporate

TOTAL

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

63.6

13.7

20.6

2.1

COOPERATIVE

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

24.8

15.7

58.3

1.2

PHILANTROPY

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

35.5

13.3

47.7

3.5

GROUP MEDICINE

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

26.2

8.9

61.5

3.4

INSURER

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

26.2

7.1

85.7

7.2

SELF INSURED

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

66.1

30.5

3.4

12

Due to the size of the country, most

insurance contracts offer nationwide

coverage.

city state choicestate nationwidecity choice

TOTAL

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

4.5

6.4

7.3

41.9

39.9

INSURER

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

3.6

6.9

88.8

GROUP MEDICINE

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

7.1

11.8

3.1

60.6

17.4

SELF INSURED

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

13.5

14.3

16.3

55.6

COOPERATIVE

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

3.0

12.2

41.6

42.8

PHILANTROPY

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

26.4

1.1

70.2

13

INSURANCE COMPANIES Mostly with nationwide coverage, reimbursement options, managing their networks through accreditation. Eg: Bradesco, Sul América and Seguros Unimed.

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

COOPERATIVESThe main feature of this system is a comprehensive network. Physicians also own the company and service is offered through cooperators agreements. Eg: Unimed.

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

GROUP MEDICINEHave their own hospitals and clinics, while coverage can be offered through accredited networks. Eg: Medial, Hapvida, Amil and Intermédica.

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

MARKET PLAYERS

14

Managed by INSS – Instituto Nacional de Seguridade Social – (National Institute of Social Security), brazilian social security system assures coverage for state pensions, such as retirement, disability, maternity, family wage, illness, reclusion aid, death and elderly assistance.

ELIGIBILITY

Any INSS contributor has the right to the above mentioned benefits.

CONTRIBUTION

INSS benefits are financed by both employers and employees. For employees, contribution varies depending on monthly earnings, according to the following graph:

SOCIAL SECURITY SYSTEM

OVERALL POPULATION

COVERED POPULATION

OVERALL POPULATION

COVERED POPULATION

20002001

20022003

20042005

20062007

20082009

20102011

20122013

2%

4%

6%

8%

10%

12%

14%

16%

OVERALL POPULATION

COVERED POPULATION

OVERALL POPULATION

COVERED POPULATION

20002001

20022003

20042005

20062007

20082009

20102011

20122013

2%

4%

6%

8%

10%

12%

14%

16%

OVERALL POPULATION

COVERED POPULATION

OVERALL POPULATION

COVERED POPULATION

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2%

4%

6%

8%

10%

12%

14%

16%

15

1.317,07

8 9 11

2.195,12

4.390,24

BRL

CONTRI-BUTION %

minbrl 724

maxbrl

4.396However, the methodology to calculate benefits will vary

according to employee’s retirement option (full or proportional retirement).

MONTHLY RETIREMENT

INCOME (JAN 2014)

16

RETIREMENT BENEFITS

OLD AGE RETIREMENT*

*Both with affiliation before July 24th, 1991.

MEN 65 years old and at least 15 years of contribution.

WOMEN 60 years old and at least 15 years of contribution.

17

MEN 53 years old and at least 35 years of contribution.

WOMEN 48 years old and at least 30 years of contribution.

NORMAL AGE RETIREMENT

MEN AND WOMEN 15, 20 or 25 years of work in hazardous occupations.

SPECIAL RETIREMENT

18

WORKER COMPENSATION

brl 724

brl 4.159

MONTHLY WAGES RANGE (JAN 2014)

Federal Government manages worker compensations and INSS guarantees the benefits in case of partial or total disability caused by a labor accident.

Any salaried employee that suffer injury at a work site, while commuting to or from work has access to this benefit.

Will be fully paid by the employer in case of temporary disability. 15

DAYS

first

Is the worker compensation starting day.

16th

DAY

19

Employer contributions vary in accordance with performance rate related to accidents and diseases. Businesses may accrue a discount on their contribution or increase up to 100% of payroll as a penalty due to poor performance. These changes became effective in January 2010 and are still valid. See below:

CONTRI BUTION

1%

2%

3%

0.5% TO 2%

1% TO 4%

1.5% TO 6%

LOW

MEDIUM

HIGH

CONSULTING FIRMS

BANKING

MANUFACTURING

PAYROLL CONTRIBUTION

(JAN 2010)RISK LEVEL

INDUSTRY (EXAMPLE)

PAYROLL CONTRIBUTION

(DEC 2009)

20

GOVERNMENT SEVERANCE INDEMNITY FUND FOR EMPLOYEES

Any salaried worker dismissed without just cause is entitled to this benefit. Federal Government mandates that all employers fund a severance pay plan at a contribution rate of 8% of their employee’s monthly wage.

Contribuions are deposited in a blocked account on employee’s behalf and managed by Caixa Econômica Federal. In addition to any accrued amounts, employees receive a 40% supplementary payment from the employer as a law required penalty. This is applicable to all contributions made by the employer to FGTS’s fund during the employee’s period of employment.

FGTS

21

Government fully funds the Health Care System; there is no contribution by patients or companies. Health Ministry (Ministério da Saúde) is responsible for providing public health, government hospitals and medical services.

All legally established persons are able to be covered by the Health Care System which provides full coverage including: doctors visit, exams, therapies, in-patient treatments, vaccines, etc. Unfortunately, depending on the region, waiting periods can be longer than 3 months.

PUBLIC HEALTH SYSTEM

22

Employer must share transportation costs with their employees related to one or more vouchers, depending on the distance to the employer’s residence.

Employers can deduct up to 6% of the total cost, while the other portion is to be fully paid. Companies who provide their own transportation are not obliged to provide these vouchers.

TRANSPORT VOUCHER

23

It is provided to any legally employed worker dismissed without just cause who has contributed to social security for at least 15 months during a 2 years period.

Workers receive temporary financial assistance that ranges from 3 to 5 installments and values are calculated based on the average of at least three salaries prior to dismissal.

UNEMPLOYMENT INSURANCE

From 6 to 11 months

3INSTALLMENTS

From 12 to 23 months

4INSTALLMENTS

From 24 to 36 months

5INSTALLMENTS

24

OTHER BENEFITS

VACATIONEmployees are entitled to a 30 day vacation after 12 months of service. They may trade vacations time for additional pay.

In addition, the employer must pay a vacation bonus of 1/3 of the employee’s monthly salary.

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

13th

13th SALARYEmployee receive a 13th check paid in December equivalent to their highest monthly salary.

25

PRIVATE BENEFITS: GENERAL MARKET PRACTICE

26

Historically, health plan costs have been increasing over the years. Inclusion of new procedures, new technologies and constant intervention from government are some of the ingredients that led to 11,23% increase in costs last year.

Health-related inflation has been increasing quicker than other financial indicators over the last 5 years, as shown on the next page:

HEALTH CARE

27

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

UIB BENEFÍCIOS DATABASE INPCA ANS INPC

HEALTH-RELATED INFLATION

28

ANS – Agência Nacional de Saúde (National Health Agency) – is the regulatory agency for the private health system. It determines the minimum coverage for health care plans, what differs between them is the reimbursement level, accommodation offers, network level and additional coverages.

Nearly all of national and multinational companies provide a private health care system to their employees and dependents in Brazil.

NATIONAL HEALTH AGENCY

There are usually two or three plan levels. Companies usually resort to co-insurance in doctors visit and simple exams (from 10% to 30% of the total cost of procedure).

PLAN DESIGN

29

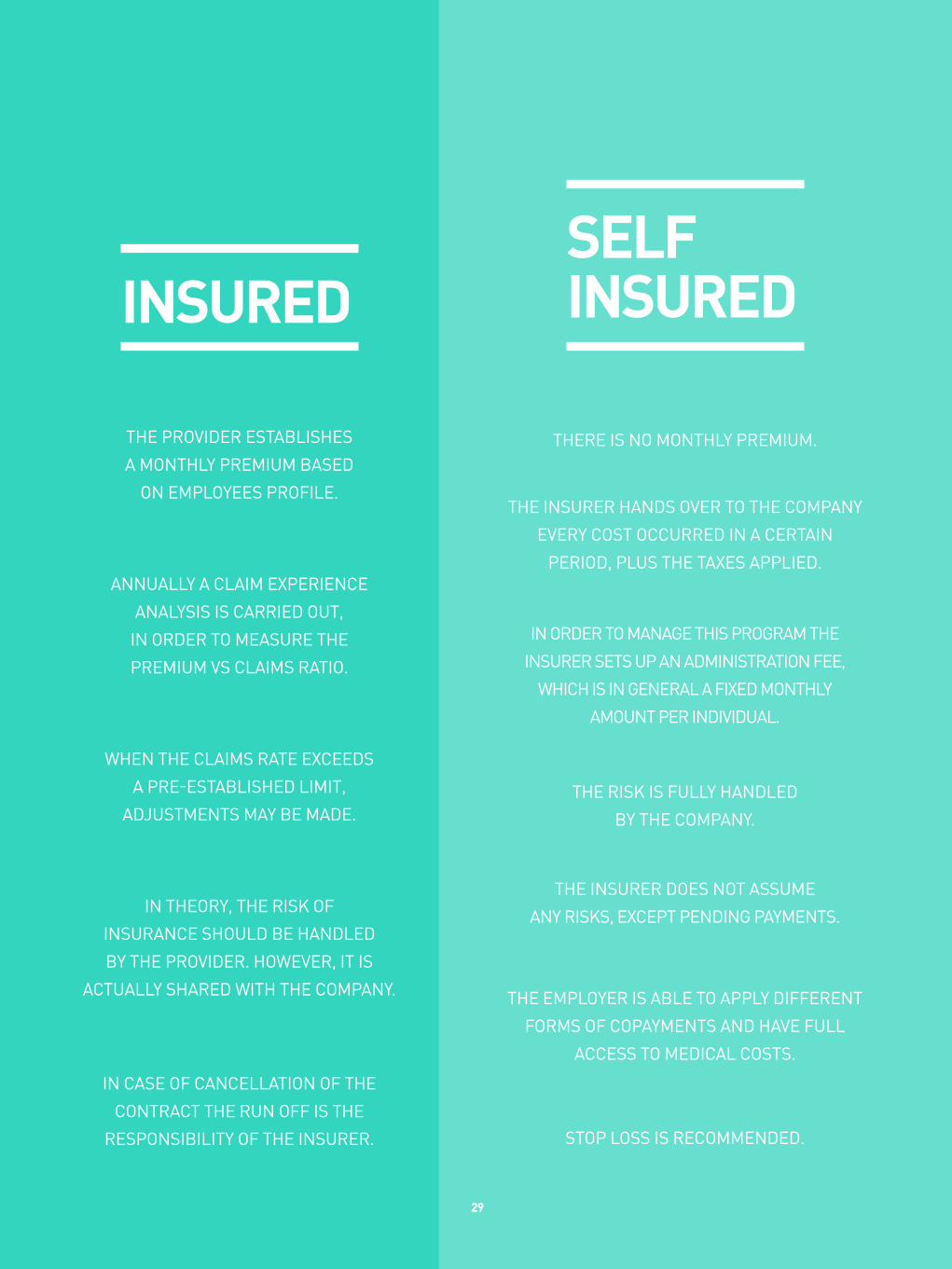

INSUREDSELF INSURED

THE PROVIDER ESTABLISHES

A MONTHLY PREMIUM BASED

ON EMPLOYEES PROFILE.

ANNUALLY A CLAIM EXPERIENCE

ANALYSIS IS CARRIED OUT,

IN ORDER TO MEASURE THE

PREMIUM VS CLAIMS RATIO.

IN THEORY, THE RISK OF

INSURANCE SHOULD BE HANDLED

BY THE PROVIDER. HOWEVER, IT IS

ACTUALLY SHARED WITH THE COMPANY.

WHEN THE CLAIMS RATE EXCEEDS

A PRE-ESTABLISHED LIMIT,

ADJUSTMENTS MAY BE MADE.

IN CASE OF CANCELLATION OF THE

CONTRACT THE RUN OFF IS THE

RESPONSIBILITY OF THE INSURER.

THERE IS NO MONTHLY PREMIUM.

THE INSURER HANDS OVER TO THE COMPANY

EVERY COST OCCURRED IN A CERTAIN

PERIOD, PLUS THE TAXES APPLIED.

THE RISK IS FULLY HANDLED

BY THE COMPANY.

IN ORDER TO MANAGE THIS PROGRAM THE

INSURER SETS UP AN ADMINISTRATION FEE,

WHICH IS IN GENERAL A FIXED MONTHLY

AMOUNT PER INDIVIDUAL.

THE INSURER DOES NOT ASSUME

ANY RISKS, EXCEPT PENDING PAYMENTS.

THE EMPLOYER IS ABLE TO APPLY DIFFERENT

FORMS OF COPAYMENTS AND HAVE FULL

ACCESS TO MEDICAL COSTS.

STOP LOSS IS RECOMMENDED.

30

Under the Brazilian Legislation, an employee who contributes a fixed amount to his health plan and has been laid off without just cause has the right to remain in the plan from 6 to 24 months. The remaining period will be defined by 1/3 of the contribution time. In case of retirement, the remaining period can be extended to lifetime.

In case of extension, it is important to remember that the employee must assume the plan cost.Liability calculation is mandatory for employers that share the cost with their employees in accordance to the laws as follows:

KEY ASPECTS

AMERICAN COMPANIES

EUROPEAN COMPANIES

BRAZILIANCOMPANIES

IAS 19

CVM 600

FAS 106

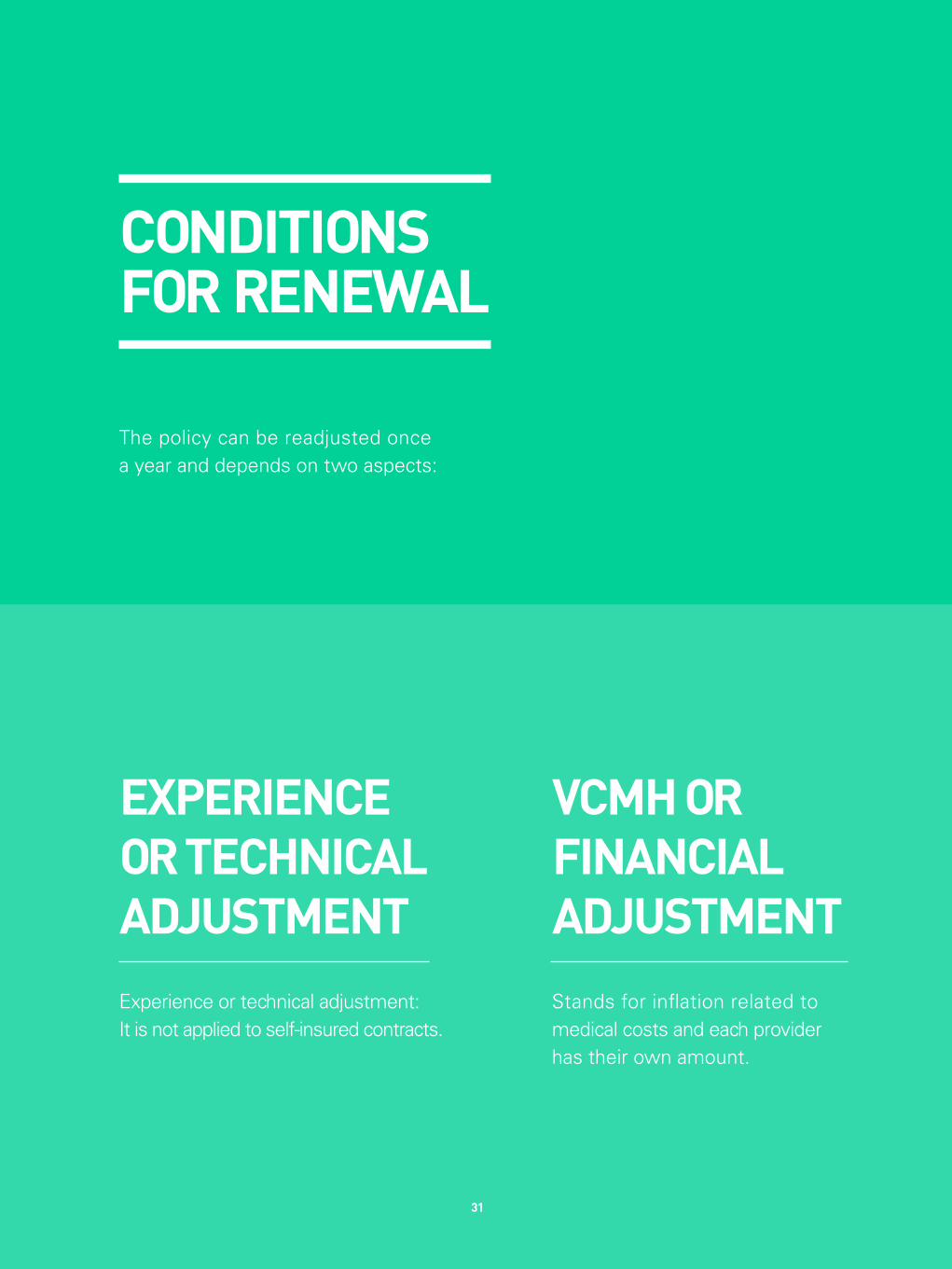

The policy can be readjusted once a year and depends on two aspects:

CONDITIONS FOR RENEWAL

EXPERIENCE OR TECHNICAL ADJUSTMENTExperience or technical adjustment: It is not applied to self-insured contracts.

VCMH OR FINANCIAL ADJUSTMENTStands for inflation related to medical costs and each provider has their own amount.

31

Approximately 89% of national and multinational companies provide private dental care to employees and their dependents. As with medical plans, ANS also regulates dental plans and determines a minimum coverage. Usually, companies offer basic coverage (Level 1) and employees can upgrade to a higher level bearing the extra cost.

Copayment is usually applied to prosthesis and orthodontics in cases where these are offered in the program.

The guaranteed treatments vary in accordance with the following practices:

DENTAL CARE

LEVEL 1 Minimum coverage

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

LEVEL 2 Minimum coverage + orthodontics or prosthesis

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16% LEVEL 3 Minimum coverage + orthodontics + prosthesis

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

LEVEL 4 Minimum coverage + orthodontics + prosthesis + implants

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

32

33

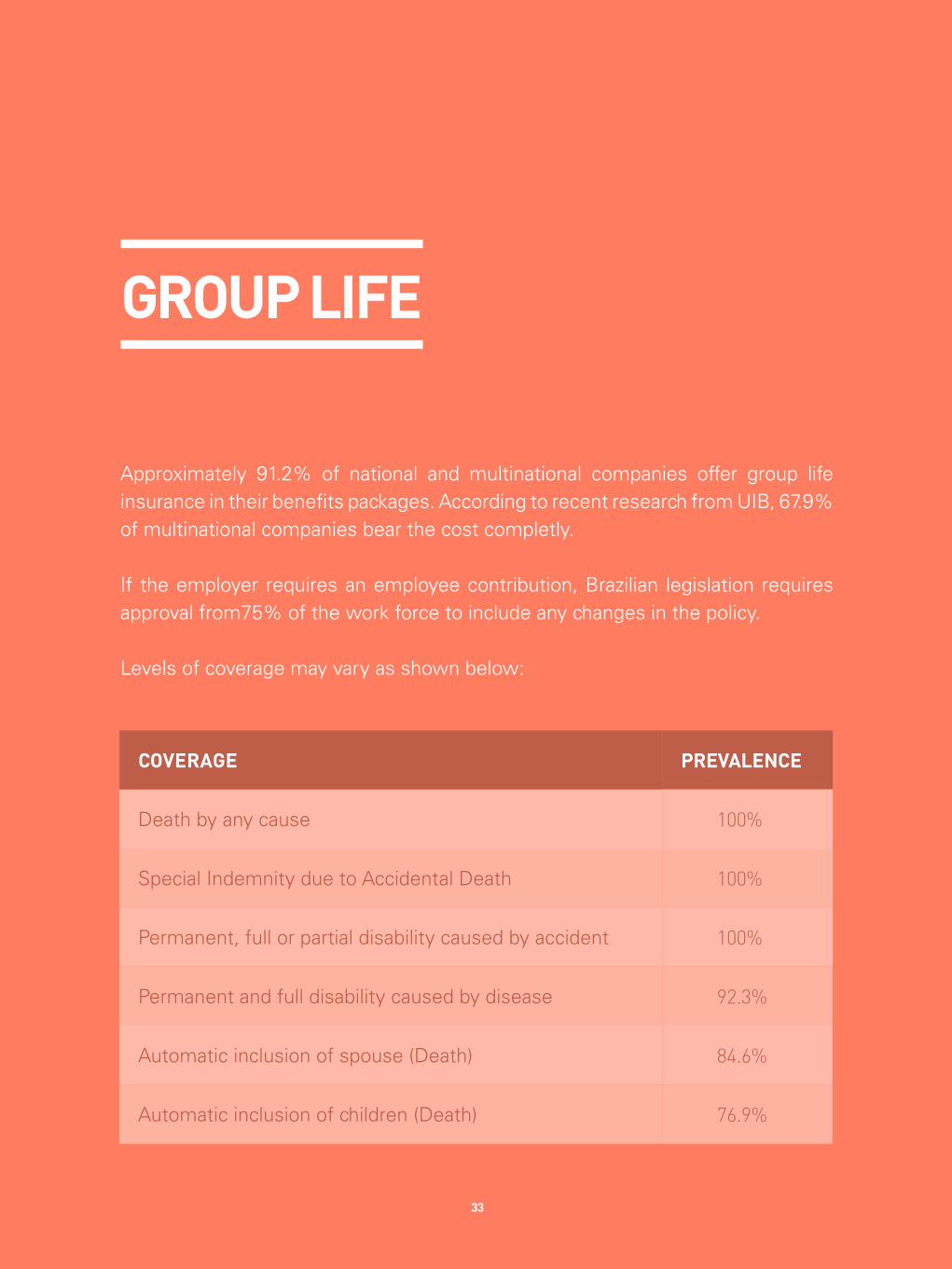

Approximately 91.2% of national and multinational companies offer group life insurance in their benefits packages. According to recent research from UIB, 67.9% of multinational companies bear the cost completly.

If the employer requires an employee contribution, Brazilian legislation requires approval from75% of the work force to include any changes in the policy. Levels of coverage may vary as shown below:

GROUP LIFE

PREVALENCE

100%Special Indemnity due to Accidental Death

84.6%Automatic inclusion of spouse (Death)

100%Permanent, full or partial disability caused by accident

76.9%Automatic inclusion of children (Death)

100%Death by any cause

COVERAGE

92.3%Permanent and full disability caused by disease

34

% 50 to 200 The matching contribution may vary from 50% to 200% depending on the industry sector.

Usually the pension plan is offered to all employee levels, although these are not compulsory benefits.

PENSION

% 64.7of national and multinational companies offer Pension plans under the benefits packages.

35

In accordance with our recent survey, vesting period may vary depending on

industry sector; however, general practice requires from 5 to 10 years to reach 100% of employer’s contribution.

INSURANCE COMPANIES

open entities

SELF-SPONSORED OR MULTI-SPONSORED PLANS

OVERALL POPULATION COVERED POPULATION OVERALL POPULATION COVERED POPULATION

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

2%

4%

6%

8%

10%

12%

14%

16%

closed entities

Private pension plans are divided into two main vehicles:

Av. Nações Unidas, 12.551WTC – 23rd Floor - 2303

Brooklin Novo, São Paulo / SP - Brazilt. +55 11 3043-7773uibbeneficios.com

–

© 2014 All rights reserved toUIB Benefícios Consultoria e Corretora de Seguros Ltda.