Embed Size (px)

Citation preview

Board of Assessment Board of Assessment ReviewReview

Training Session

Presented by:

Dutchess County Real Property Tax Service Agency

Dutchess County Real Property Tax Service Agency

22 Market StreetPoughkeepsie, NY 12601

Eric Axelsen, DirectorPhone (845) 486-2140

Website www.dutchessny.gov

Authority on Training and CertificationAuthority on Training and Certification

NYS Dept. of Taxation & Finance Office of Real Property Services (ORPTS)

WA Harriman State CampusAlbany, NY 12227

Colleen Sheehan, Educational ServicesPhone (518) 474-1764

E-mail [email protected]

ORPS website www.orps.state.ny.us

Unit 1Unit 1Introduction and Equity in Introduction and Equity in

Assessment AdministrationAssessment Administration

Lesson 1 – Reasons for Training and Course Overview

Reasons for Training

Real Property Tax Law requires initial appointees and re-appointees must attend training session given by County Director

Course Overview

1. Equity in assessment administration2. Board of Assessment Review profile3. Grievance Day preparation4. Powers and duties of the BAR5. Assessment of Real Property6. Holding grievance hearings7. Grounds for complaint8. Determinations of BAR9. Second Meeting(s) of BAR and subsequent

complaint routes10. Video

The Real Property Tax

Ad Valorem Tax – based on ‘value’Value is defined as ‘market Value’Tax is determined by municipal budgetsEquitable assessments fairly distribute the

property tax Property owners can only grieve their

assessments, not their tax amount

New York statutes set forth the procedure to be followed by property owners who have a complaint about their assessment

Filing a petition with the Board of Assessment Review is a required (very important) first step

Small Claims Assessment Review (hearing officer)

Tax Certiorari (Court Proceeding)

Lesson 2 - Role of the Assessor

Primary responsibilities of the assessor

Discover, list, and place a value on all real property

Establish market value as of July 1 of prior year (valuation date)

Assess according to ‘condition and ownership’ as of March 1 (taxable status date)

Determine exemption eligibility

Role of the Assessor in relation to the Board of Assessment Review

Assessor files a tentative assessment roll by May 1

Assessor publishes notice of filing which includes dates and times that the Board of Review will meet

Must attend all hearingsCan request an adjournment

Lesson 3 – Role of the Board of Assessment Review

1. Quasi-judicial body – charged with the judicial responsibility to get the facts, apply the law

2. Each member shoulda) possess judicial temperament b) provide a fair hearingc) safeguard constitutional guarantees of due

process of lawd) abstain if personally involved

Unit 2 - Board of Assessment Unit 2 - Board of Assessment Review ProfileReview Profile

Lesson 1 - Profile

Composition – BAR consists of not less than three nor more than five members

Majority can not be officers or employees of local government

5 year term – staggered Oct 1 – Sept 30Temporary members can be appointed

for 1 year to create hearing panels

Qualifications

Knowledge of property values18 yrs oldU.S. CitizenResident of the TownMust file an oath of office

Hearing PanelsHearing Panels

RPTL 523-a allows temporary members to be appointed in any year (usually in re-val year)

1 year terms Maximum of 2 temporary members for each

regular member Must meet same qualifications, same training Same powers as BAR, EXCEPT will NOT

determine final value Temps make recommendations to BAR Temps can not fill in for absent permanent

BAR members

Lack of quorum

Must have two of a three member board present or three of a four or five member board present

If not –

County treasurerChairman of the legislatureClerk of the legislature shall serve as acting Board of Assessment Review

New hearing date scheduled around 3rd week in June (RPTL 527)

Lesson 2 – Training and Certification

RPTL 523 (d)Mandates initial appointees and re-appointees

attend this trainingExtensions can only be granted by request of

NYS ORPS Educational Services

Unit 3 - Grievance Day Unit 3 - Grievance Day PreparationPreparation

Lesson 1 – Grievance day preparation by the BAR

Grievance day is 4th Tuesday in MayIf assessor in more than one town a Local Law can be

adopted to change that date, but no later than 2nd Tuesday in June OR

assessor can appoint one or more members of staff to fill in

Board members must have training certificationMust select a chairperson

Chairperson’s role is to facilitate the meeting, keep order, administer oaths

Informational Meeting with assessor

Get generally acquainted with tentative assessment roll

Assessor’s techniques and methods for valuation

Fact sheet – LOA, RAR, Equalization Rate, Trends

Most important in reassessment and sustaining equity municipalities

Local “Fact Sheet”Local “Fact Sheet”

Veteran’s Exemption Ceiling values.

Senior’s income limits for County, Town, Village, and all Schools in your town.

Homestead for Town or School(s)?

Other Local Options.

Unit 4Unit 4Powers and Duties of the Board of Powers and Duties of the Board of

Assessment ReviewAssessment ReviewLesson 1

1. Administer oaths2. Take Testimony3. Hear proofs4. Require personal appearances5. Require more information6. Determine the final assessment/exemption status

Evidence should accompany the complaint filedComplainant can offer additional documentation at the

hearingAll oral and written testimony is taken under oathEach person testifying is sworn in individually

Hearing testimony and taking proof

Personal appearances not necessaryBoard may require a personal appearanceComplainant not entitled to any reduction if willful neglect or refusal

to supply requested information (dismissal) (RPTL 525 (2))

Minutes

Minutes of the proceedings must be taken and filed with the town clerk

Disclosure of interest (RP523-dcl)

BAR Member must file if he has any interest in a property coming before the board and should abstain from the discussion (recusal).

Agreements between municipalities can allow board member’s grievance to be heard in the other municipality (RPTL 523 (3))

Unit 5Unit 5Assessment of Real PropertyAssessment of Real Property

Lesson 1 – Assessment of Real Property

Standard of Assessment

RPTL 300 – All real property is subject to taxation unless specifically exempted by statute

RPTL 302 – Real property must be assessed according to its condition and ownership as of taxable status date (March 1)

RPTL 305 – The standard of assessment in NYS is that all real property in each assessing unit be assessed at a uniform percentage of value

What is value?

Value has been defined by the courts to mean ‘Market Value’

Assessor must assess property at its ‘value in current use’ not highest and best or future potential use (farms, residence in commercial zone, etc.)

Exception is vacant land parcels not being put to any particular use can be assessed at highest and best use

Level of AssessmentLevel of Assessment

Level of Assessment (a/k/a Uniform Percent of Value) tells us what percent of market value is being used that year to determine assessments. It is stated by the assessor – must appear on roll and bill.

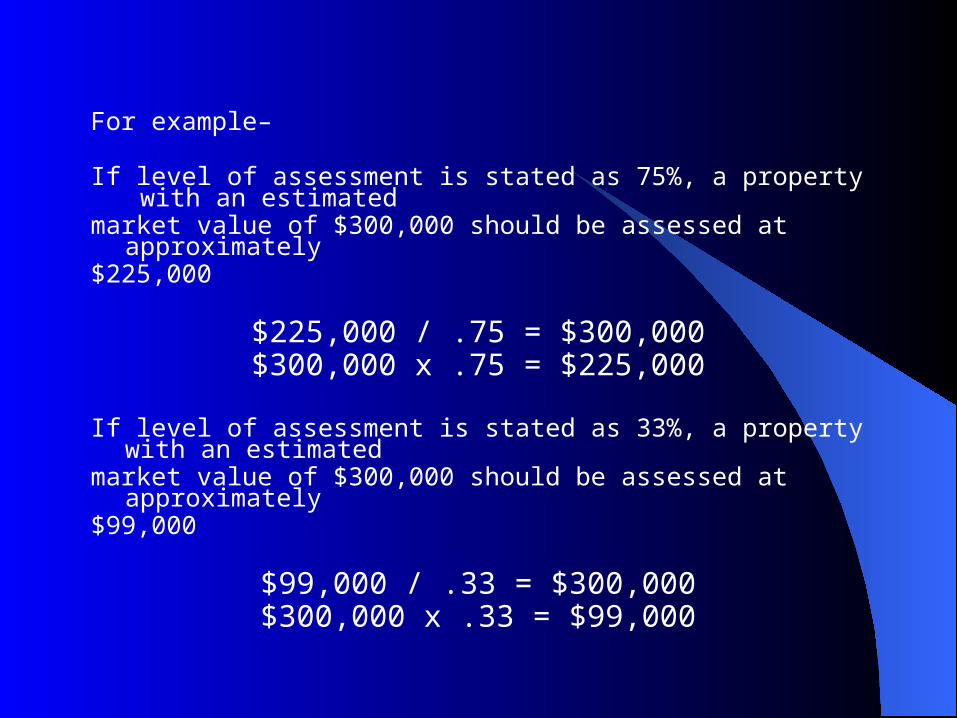

For example–

If level of assessment is stated as 75%, a property with an estimated

market value of $300,000 should be assessed at approximately

$225,000

$225,000 / .75 = $300,000$300,000 x .75 = $225,000

If level of assessment is stated as 33%, a property with an estimated

market value of $300,000 should be assessed at approximately

$99,000

$99,000 / .33 = $300,000$300,000 x .33 = $99,000

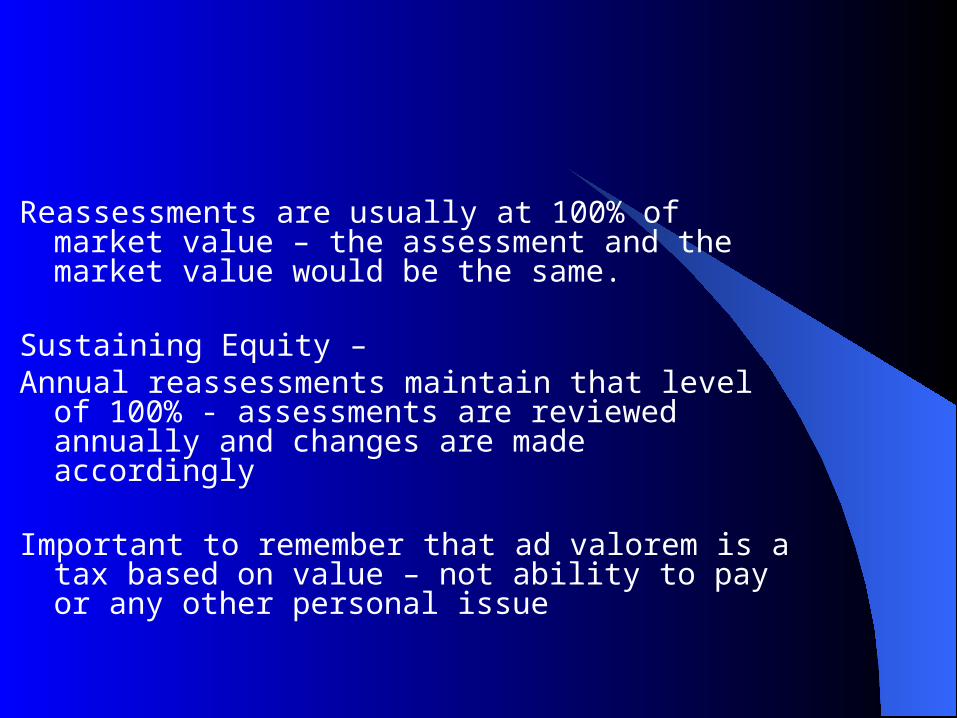

Reassessments are usually at 100% of market value – the assessment and the market value would be the same.

Sustaining Equity – Annual reassessments maintain that level of

100% - assessments are reviewed annually and changes are made accordingly

Important to remember that ad valorem is a tax based on value – not ability to pay or any other personal issue

3 approaches to value

Market Value approach – for property types readily bought and sold

Income approach – used for rental propertiesCost approach – specialty property, utilities

Assessor is responsible for collecting the data and applying the most appropriate method

Annual re-assessment

Systematic review of all locally assessed property in the municipality

Systematic analysis is a methodical, thorough and regular review and examination of assessments

CAMA – Computer Assisted Mass AppraisalAssessments to Sale Price ratios are used to

determine trendsDifferent areas or neighborhoods can have

different trendsThese trends are applied to assessments to

maintain those assessments at 100% of value

Unit 6Unit 6Grievance HearingsGrievance Hearings

Lesson 1 – Holding Grievance Hearings

Grievance hearings must be in compliance with the open meetings law (accessible, open to public)

BAR must meet to make final determinations (executive session, closed)

Lesson 2 – Fair hearings

Keeping an open mind

All persons involved have a full opportunity to make statements, present testimony and produce evidence

Basic objective is to review the facts presented to you so that a fair decision can be made

Complaint requirements

RPTL 524 (3) requires complainants to file a written complaint on a prescribed form (RP 524)

Complainant must specify the full market value of the property and the requested amount of the reduced assessment

Complaint may be filed with the assessor prior to grievance day or with the Board on grievance day

Adjourned hearing dates1. Assessor requests2. Further documentation required3. Too many to hear(No new complaints can be filed at an adjourned

hearing)

Unit 7Unit 7Grounds for ComplaintGrounds for Complaint

Lesson 1- Complaint form – RP524

Must be completely filled out so that parcel can be identified and to give the board a clear understanding of what is being requested

Examples – exemption not properly grantedassessed value too highmisclassification in homestead

status

Lesson 2 – grounds for complaint

Unequal – assessed at a higher percentage of value than other property on the assessment roll

Excessive – assessed greater than market value; denial of partial exemption

Unlawful – Property outside of assessing unit; property can not be identified; assessed by person without authority; special franchise exceeds value set by State Board

Misclassification – Only applies to jurisdictions that have adopted the homestead provisions of Article 19 RPTL

Unit 8Unit 8Determinations of the Board of Determinations of the Board of

Assessment ReviewAssessment ReviewLesson 1 - Determinations

Making determinations

After hearing all testimony, decisions must be madeMust meet in private – not an open meeting-no minutes

taken; assessor, public officials (with the exception of BAR legal counsel) NOT allowed to be present

Can lower assessment or leave unchanged

Burden of Proof

Presumption under the law is that the assessor is correct

Burden of proof is on the property owner whoMust present clear and convincing evidence -

comparables, sales listings, appraisal - for your review

Assessor’s role in determinations

Give testimony in defense of an assessmentRecommend a reduction in assessmentStipulate an assessed value

BAR is expected to ratify stipulations if they do not, charges can be brought

against BAR and court will decide if BAR’s refusal was justified

Weighing the evidence

BAR should not re-appraise the propertyBAR must decide if complainant has supported

his complaint with evidence beyond that of the assessor

Final determination

After the board has met and made its determinations all changes must be listed, verified and delivered to the assessor so that the tentative roll can be changed

The vote of each member must be recorded

Complainant must be notified of the decision, the reason for the decision and how each member voted

Unit 9Unit 9Second MeetingSecond Meeting

Why a second (and third) meeting? To review assessment changes pursuant to

‘corrections of errors’ RPTL 553Assessor submits petitions to the boardBoard must meet to approve petitions

When?One meeting set between July 15 and August 10

(after final roll but before school bills are processed)

Another between October 1 and November 1 (after school bills but before county/town bills are processed)

Lesson 2 - Subsequent complaint routes

Two judicial remedies

Small Claims Assessment Review1,2,3 family residence, owner occupiedcertain vacant land only

Tax Certiorari – court proceeding All property eligible

These remedies are subsequent to the administrative review – not instead of

Unit 10Unit 10Summary and ReviewSummary and Review

Basic premise for your determination

Assessment challenged/not taxes

Has the property owner supplied sufficient and convincing evidence to prove the assessment is incorrect?

Yes? Make appropriate reductionNo? Assessment remains unchanged

Check out integrated tax maps, aerial photos and current assessment information on

ParcelAccess at www.dutchessny.gov

This presentation is on the web – This presentation is on the web – www.dutchessny.govwww.dutchessny.gov go to go to RPT pageRPT page

Visit Visit www.orps.state.ny.us for more information on Real for more information on Real Property Property Tax and Assessment informationTax and Assessment information

Any Questions?Any Questions?

Newly appointed must stay for videoNewly appointed must stay for video

Re-appointed – video optionalRe-appointed – video optional

Don’t forget your copy of certificationDon’t forget your copy of certification

Don’t forget to file your Oath of OfficeDon’t forget to file your Oath of Office