Embed Size (px)

DESCRIPTION

Accountancy and Bookkeeping Made Easy

Citation preview

Author © Graham Thomas 2005Edited by Deanna Kilworth 2005

Designed and Illustrated © the Designlinc - Lincoln Kilworth 2005

w w w . b i l l y t h e g o o s e . c o m

illy had no trouble getting out of bed this morning. This was to be the fi rst day as his

own boss and he was excited! He didn’t even mind going in to work at a much earlier 7:30am start, because he knew that any extra time was for his benefi t and not for some slave driver boss. Who would have thought that at 26 years of age he would be operat-ing his own business? His school-teachers, who would always be quick to point out that he would never “amount to anything,” would eat their words once they knew of his success!

He arrived at the “Lumpy Mattress and Furniture Company” and proudly parked his car in the space reserved for the owner. Entering through the small, back door, he turned off the security alarm and fl icked on the light switch. Billy loved the new smell of the furni-ture and spreadeagled himself on the nearest king size bed with the famous “lumpy mattress” brand.

Paul and Paula Pillow arrived at 8:30am as required by the contract of sale and turned on the air-con-ditioning system.

“Good morning Billy,” Paul remarked, “how are you feeling today?”

“A mixture of all sorts of emotions, anxiety, excitement but worst of all the fear that no one will come to the store and buy today”

“I can identify with that”, replied Paul, “the fi rst time we set up the business six years ago no one did come in on the fi rst day and Paula and I wondered what we had done. But don’t worry, although Monday isn’t the best day, you’ll be kept busy enough”

At that moment, Luscious Lucy, the fi rst of the casual employees breezed through the back door with a cheery “Hi” and proceeded to unlock the main front, sliding doors.

2

Whilst carrying out his due dili-gence, (See Billy the Goose Buys a Business) Billy had met Lucy but hadn’t noticed how beautiful she was.

“Lucy is our best sales person,” off ered Paul, “so she works the most hours. The other two help us out on late night and week-end trading”

Completing the task of opening the store for business, Lucy came toward Billy and extended her hand. “Welcome to your fi rst day Mr Goose”.

“Call me Billy, please”

“Thank you. Now, I’ll continue to follow this check list so we can be ready for our fi rst customer, if that’s O.K. with you?”

TIP: A GOOD BUSINESS WILL FOLLOW A SET OF PROVEN PROCEDURES OR SYSTEMS.

Billy’s accountant, Felicity Figures, had recommended that all money collected from sales be deposited intact in the business bank account and all expenses, except for petty cash, be paid by cheque or internet transfer.

Felicity explained that a number of reasons existed for this viz:

• The bank statements were an independently prepared record of the business transactions and should accurately refl ect the total sales and expenses.

• In the event of an audit for taxation or the need to prepare fi gures for sale, they provided an independent verifi cation.

• Accounting records would be less complex and more accurate as manual records of cash disbursements from the till prior to banking were subject to human error with no means of cross checking.

• It provided a control on em-ployees who may be tempted to pocket cash on the sale of small items whilst claiming use of the sales proceeds to “pay” a business expense.

• The bank charged interest on bank overdrafts on a daily basis so it was important to keep the outstanding balance as low as possible.

• Banking daily also reduced the risk of loss through robbery.

3

Chapter 1I T B E G I N S

Author © Graham Thomas 2005Edited by Deanna Kilworth 2005Designed and Illustrated © the Designlinc - Lincoln Kilworth 2005

Felicity surprised Billy by warning that the biggest thief in the business was often the owner because of the temptation to view the sales takings as an opportu-nity to buy personal or “lifestyle” items. She suggested that Billy take a regular ‘wage’ or drawing and transfer this to a personal cheque account solely for private expenses. This would ensure that he kept on a fi nancial budget and didn’t treat the business as some sort of welfare system.

TIP: USE YOUR BOOKKEEPER AND ACCOUNTANT ON A REGULAR AND TIMELY BASIS. DON”T TRY TO COMPETE WITH THEIR KNOWLEDGE, REMEMBER THAT IS THEIR FULL TIME JOB AND THEY ARE MOST LIKELY BETTER AT IT THAN YOU.

“Well, Billy, a $2,385 taking for a Monday is a good result”, Paul commented. “This is a 5% increase on the same day last year.”

“Thanks for your help today, Paul. Do you always compare current turnover fi gures with those for the same day a year ago?”

“Yes, but I’m more interested in the weekly and monthly totals as this is an early indication of a positive or negative trend in our sales pattern.”

“Why don’t you use the infor-mation recorded on the ‘Quick Books’ accounting programme and compile a ‘profi t and loss’ report?”

TIP: STICK WITH WELL KNOWN SOFTWARE SUCH AS MYOB OR QUICKBOOKS ETC AS THIS HAS BEEN WELL ROAD TESTED, HAS WIDE SUPPORT AND YOUR ACCOUNTANT IS MORE LIKELY TO BE FAMILIAR WITH IT.

“This is used regularly but it can only give us historical or dated in-formation. We also monitor the number of sales enquiries that convert to actual sales to measure team selling effi ciency, the number of customers that come into the shop, the average value of each sale and the number of times a customer deals with us. We have regular team meetings where the trend in these numbers is dis-cussed so we can take appropriate action on a ‘real time’ basis.” (see Billy the Goose examines Business Development)

“There is obviously a lot more stuff to learn than how to ‘keep the books’”, Billy lamented, but I intend to do some research and see an old family friend, a retired ac-countant, who will hopefully, help me to understand the fi nancial reports more fully”.

4

TIP: ACCOUNTING SOFTWARE DOESN’T MAKE THE USER AN ACCOUNTANT ANY MORE THAN A MANUAL ABOUT YOUR CAR MAKES YOU A MECHANIC.

“That’s a good idea Billy! Paula and I will head off home now and see you tomorrow morning”.

“Yes, thanks again Paul. See you tomorrow.”

TIP: ALWAYS BACK UP ELECTRONIC DATA AND STORE IN A SEPARATE LOCATION

Billy felt tired but elated as he locked the door completing his very fi rst day in business for himself.

TIP: KEY PERFORMANCE INDICATORS MEASURE THE DAILY HEALTH OF A BUSINESS RATHER THAN BY HISTORICAL FINANCIAL REPORTS. A GOOD BUSINESS OPERATOR WILL ALWAYS MEASURE SO HE CAN MANAGE.

5

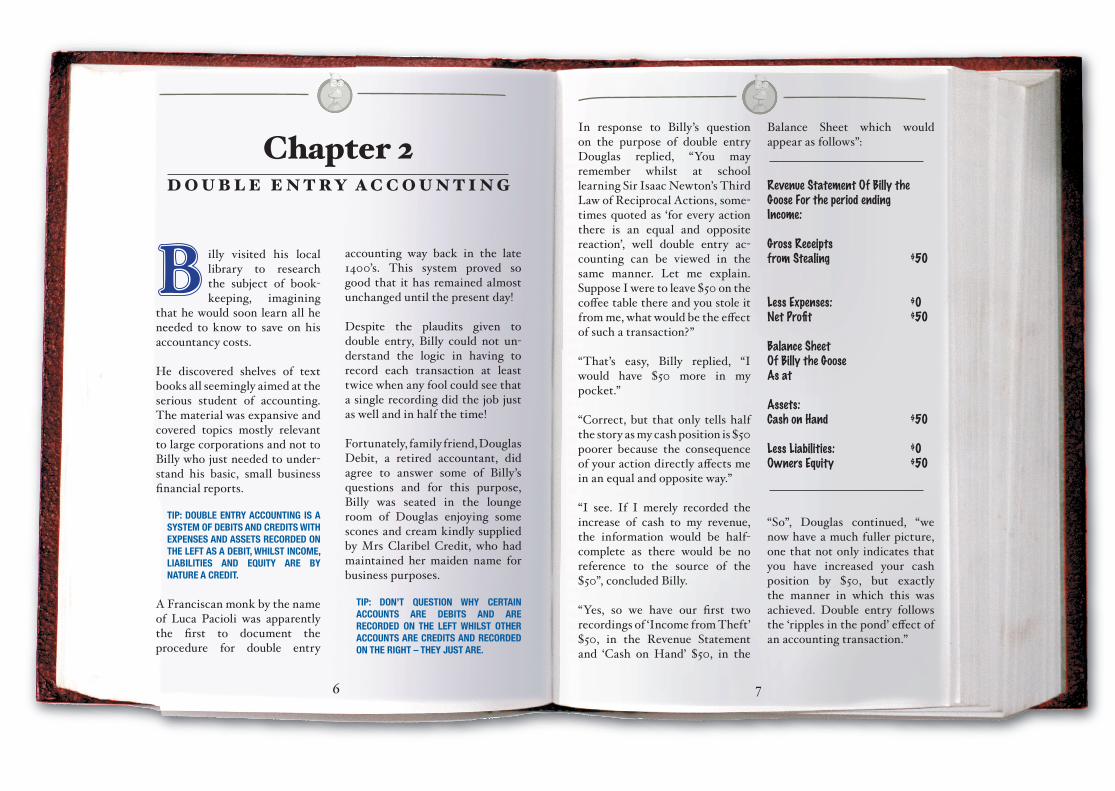

illy visited his local library to research the subject of book-keeping, imagining

that he would soon learn all he needed to know to save on his accountancy costs.

He discovered shelves of text books all seemingly aimed at the serious student of accounting. The material was expansive and covered topics mostly relevant to large corporations and not to Billy who just needed to under-stand his basic, small business fi nancial reports.

TIP: DOUBLE ENTRY ACCOUNTING IS A SYSTEM OF DEBITS AND CREDITS WITH EXPENSES AND ASSETS RECORDED ON THE LEFT AS A DEBIT, WHILST INCOME, LIABILITIES AND EQUITY ARE BY NATURE A CREDIT.

A Franciscan monk by the name of Luca Pacioli was apparently the fi rst to document the procedure for double entry

accounting way back in the late 1400’s. This system proved so good that it has remained almost unchanged until the present day!

Despite the plaudits given to double entry, Billy could not un-derstand the logic in having to record each transaction at least twice when any fool could see that a single recording did the job just as well and in half the time!

Fortunately, family friend, Douglas Debit, a retired accountant, did agree to answer some of Billy’s questions and for this purpose, Billy was seated in the lounge room of Douglas enjoying some scones and cream kindly supplied by Mrs Claribel Credit, who had maintained her maiden name for business purposes.

TIP: DON’T QUESTION WHY CERTAIN ACCOUNTS ARE DEBITS AND ARE RECORDED ON THE LEFT WHILST OTHER ACCOUNTS ARE CREDITS AND RECORDED ON THE RIGHT – THEY JUST ARE.

6

In response to Billy’s question on the purpose of double entry Douglas replied, “You may remember whilst at school learning Sir Isaac Newton’s Third Law of Reciprocal Actions, some-times quoted as ‘for every action there is an equal and opposite reaction’, well double entry ac-counting can be viewed in the same manner. Let me explain. Suppose I were to leave $50 on the coff ee table there and you stole it from me, what would be the eff ect of such a transaction?”

“That’s easy, Billy replied, “I would have $50 more in my pocket.”

“Correct, but that only tells half the story as my cash position is $50 poorer because the consequence of your action directly aff ects me in an equal and opposite way.”

“I see. If I merely recorded the increase of cash to my revenue, the information would be half-complete as there would be no reference to the source of the $50”, concluded Billy.

“Yes, so we have our fi rst two recordings of ‘Income from Theft’ $50, in the Revenue Statement and ‘Cash on Hand’ $50, in the

Balance Sheet which would appear as follows”:

Revenue Statement Of Billy the Goose For the period endingIncome:

Gross Receipts from Stealing $50

Less Expenses: $0Net Profi t $50

Balance SheetOf Billy the GooseAs at

Assets:Cash on Hand $50

Less Liabilities: $0Owners Equity $50

“So”, Douglas continued, “we now have a much fuller picture, one that not only indicates that you have increased your cash position by $50, but exactly the manner in which this was achieved. Double entry follows the ‘ripples in the pond’ eff ect of an accounting transaction.”

7

Chapter 2D O U B L E E N T R Y A C C O U N T I N G

TIP: INTERESTED THIRD PARTIES, (EG. THE TAX OFFICE) CAN USE THE CHANGE IN ASSETS, LIABILITIES AND EQUITY TO DETERMINE IF INCOME HAS BEEN CORRECTLY REPORTED. THE CHANGE IN NET EQUITY PLUS THE ESTIMATED ‘LIFESTYLE’ EXPENSES CAN GIVE A VERY CLEAR PICTURE OF THE INCOME EARNED.

“Suppose you were to lend me the $50, Douglas, how would this need to be recorded in accounting terms?”“A student of classical or text book accounting would record the transaction as follows:

Balance Sheet Of Billy the GooseAs at

Assets:Cash on Hand $50

Less Liabilities: Loan D Debit $50Owners Equity $0

You’ll notice that all the transactions are contained in the Balance Sheet and none appear on the Revenue Statement. This occurs because the transaction involves an increase in an asset (Cash) off set by the same increase in a liability (Loan) and no earning of income or revenue. However, I

have found that a small business operator may have trouble with understanding changes in a Balance Sheet and before the advent of personal computers and accounting programmes, the business would record, in a 20 or more columnar cashbook, each expense and income transaction and reconcile the progressive balance with the bank statements. The record would look something like this:

This would enable the business owner to know:

• What the bank balance should be, after adjusting the bank state-ment for unpresented cheques and outstanding deposits.

• How the business spent, its money and the category of all income received.

8

• Monthly totals of income and expenses enabling the calculation of an annual (or any desired period) “cash” profi t and loss report.

• A mathematical cross checks to account for the correct recording of all items. In the above example, the total of the expenses (250 + 750 + 5 + 1100) is 2105 whilst the total of the income is (1000 + 1500) 2500.

This means that the income is greater than the expenses by (2500 – 2105) 395 which agrees with the upward movement in the bank account of 115 to 510.

• The fi nancial records presented to the accountant are categorised and agree with the incomings and outgoings refl ected in the bank statement.

This was much simpler as the

business operator didn’t need to think in terms of debits, credits, assets, liabilities, cash, accrual, revenue or expense but only how the expense or income was to be classifi ed. It was also quite logical to realise that the balance in the cash book needed to reconcile with the balance on the bank statement and any diff erences accounted for. In such a system, the reports would now appear as follows.

9

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510Total 250 750 5 1100 1000 1500 395

Date. Description Chq No. Accty Advtg Assets Bnk Fees Stock Capital Sales Total Balance1/1/xx Open Bal 1151/1/xx Per Bnk Stat - 5 5 1102/1/xx Yellow Pages 103 250 250 (140)2/1/xx Sales & B Goose 1000 1500 2500 236015/1/xx Fridge 104 750 750 161030/1/xx Pillow & Co 105 1100 510

10 11

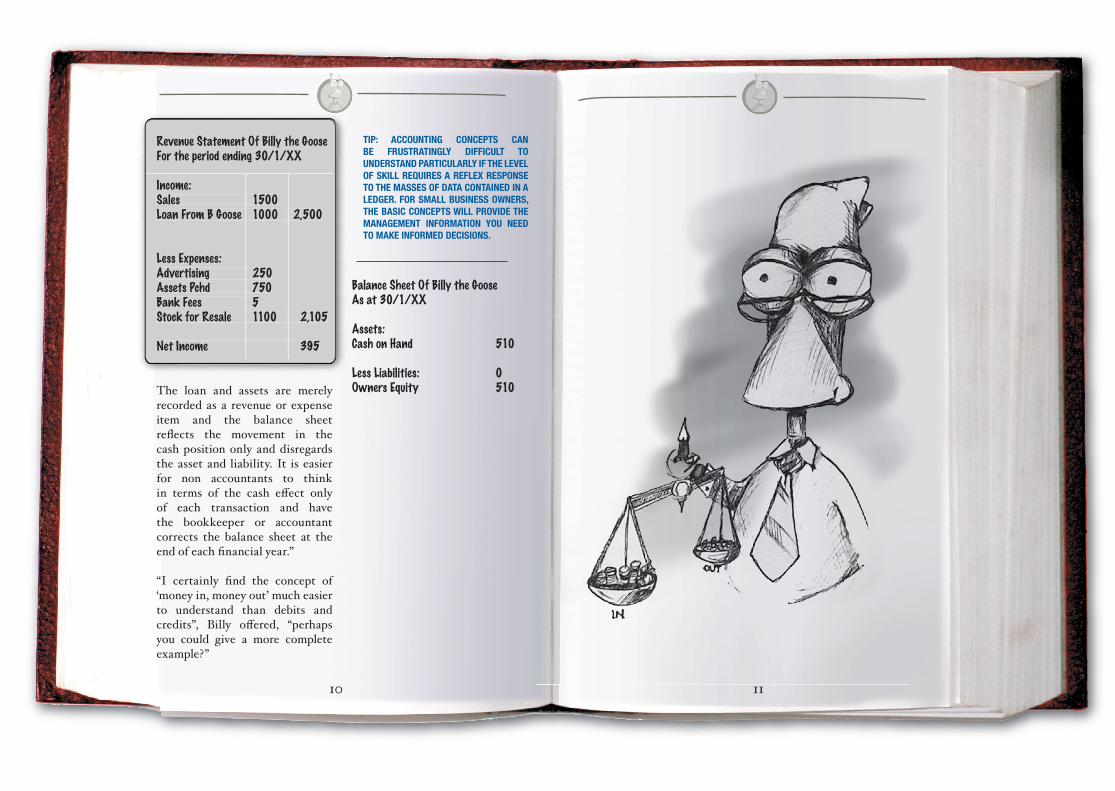

Revenue Statement Of Billy the GooseFor the period ending 30/1/XX

Income:Sales 1500Loan From B Goose 1000 2,500

Less Expenses: Advertising 250Assets Pchd 750Bank Fees 5Stock for Resale 1100 2,105

Net Income 395

The loan and assets are merely recorded as a revenue or expense item and the balance sheet refl ects the movement in the cash position only and disregards the asset and liability. It is easier for non accountants to think in terms of the cash eff ect only of each transaction and have the bookkeeper or accountant corrects the balance sheet at the end of each fi nancial year.”

“I certainly fi nd the concept of ‘money in, money out’ much easier to understand than debits and credits”, Billy off ered, “perhaps you could give a more complete example?”

TIP: ACCOUNTING CONCEPTS CAN BE FRUSTRATINGLY DIFFICULT TO UNDERSTAND PARTICULARLY IF THE LEVEL OF SKILL REQUIRES A REFLEX RESPONSE TO THE MASSES OF DATA CONTAINED IN A LEDGER. FOR SMALL BUSINESS OWNERS, THE BASIC CONCEPTS WILL PROVIDE THE MANAGEMENT INFORMATION YOU NEED TO MAKE INFORMED DECISIONS.

Balance Sheet Of Billy the GooseAs at 30/1/XX

Assets:Cash on Hand 510

Less Liabilities: 0Owners Equity 510

Loan From B Goose 1000 2,500

Stock for Resale 1100 2,105

Net Income 395

Sales 1500Loan From B Goose 1000 2,500

Advertising 250Assets Pchd 750Bank Fees 5Stock for Resale 1100 2,105

Net Income 395

12 13

ouglas occupied himself over the next fi fteen minutes creating a document that he photocopied on the fax machine giving a copy to Billy. It read as follows:

impact on the operating profi t of the lawn mowing round?”

“I guess not”, Billy surmised, “This amount is merely a voluntary contribution by the owner and is not part of the business operation”.

“Absolutely correct. Why do you suppose the owner put in the $5,000 in the fi rst place?”

“Because he would have run out of cash at the bank had he not injected the funds? This means the ‘loss’ of $14,340 has increased to $19,340 so this guy really needs to fi nd a job!”

“Not quite!” Douglas countered. “Look at the expenses in the profi t and loss and identify any that you consider not to be business related”.

Billy checked the expenses again but became confused because each seemed related to being in business. Perplexed, he asked for Douglas’ assistance.

“Let’s look at them one at a time. Please remember that we need to place the fi nancial viability of a business operation on a level

Chapter 3THE PROFIT & LOSS STATEMENT

Balance SheetG Green – Your Lawns Barber

Assets:Cash at Bank $2,872Less Liabilities: $0Owners Equity $2,872

“What do you make of this little mowing round Billy?” queried Douglas.

“Obviously, he needs to do something else because the business is losing money”, replied Billy, pleased with his newfound fi nancial interpre-tive skills.

TIP: REMEMBER MOST SPORTING EVENTS ARE RUN WITH NUMBERS AND STATISTICS AND NO ONE WOULD BE COMFORTABLE OPERATING A MOTOR VEHICLE OR PLANE WITHOUT GAUGES AND DIALS GIVING VITAL INFORMATION. DON’T TREAT YOUR BUSINESS ANY DIFFERENTLY.

Douglas stroked his chin before sagely asking:“Take a closer look at the $5,000 put into the business by the owner and reported as income in the profi t & loss. Do you suppose this is business income and should it have any

Profi t & Loss Statement - Garry your Lawns Barber - For Period Ending:Profi t & Loss Statement - Garry your Lawns Barber - For Period Ending:

Income: $ $

Lawn mowing 65,380Loans from G Green 5,000 70,380

Less Expenses:Accountancy 750Advertising 900Bank Fees 485Casual Labour 1,000Fuel & Oil (Mowers) 650 Hire of Equipment 800Income Tax Paid 6,800Insurance (Business) 1,000Insurance (Income Protection) 1,500 Loan Repayments 5,000

Expenses Cont: $ $ $

Repairs & Replacements (Equipment) 1,300

Ute Expenses:Fuel 1,560Loan Repayments 6,300Repairs 1,200Registration & Insurance 1,050Speeding Fine 175Washes & Polishes 250 10,535Superannuation 2,000Wages for G Green 52,000 84,720

NET INCOME (LOSS) (14,340)

Income: $ $

Lawn mowing 65,380Loans from G Green 5,000 70,380

Accountancy 750Advertising 900Bank Fees 485Casual Labour 1,000Fuel & Oil (Mowers) 650 Hire of Equipment 800Income Tax Paid 6,800Insurance (Business) 1,000Insurance (Income Protection) 1,500 Loan Repayments 5,000

Income: $ $

Loans from G Green 5,000 70,380

Insurance (Income Protection) 1,500

Expenses Cont: $ $ $

Repairs & Replacements (Equipment) 1,300

Fuel 1,560Loan Repayments 6,300Repairs 1,200

Insurance 1,050Speeding Fine 175Washes & Polishes 250 10,535Superannuation 2,000Wages for G Green 52,000 84,720

NET INCOME (LOSS) (14,340)

Expenses Cont: $ $ $

Wages for G Green 52,000 84,720

NET INCOME (LOSS) (14,340)

Expenses Cont: $ $ $

(Equipment) 1,300

Washes & Polishes 250 10,535Superannuation 2,000Wages for G Green 52,000 84,720

NET INCOME (LOSS) (14,340)

footing by excluding all income and expenses that are peculiar or specifi c to the operating methods of a particular owner. For example, the fi rst one we come across is income tax of $6,800 which needs to be excluded.”

“But surely, income tax is a part of operating a business and should be included”, Billy suggested.

“Not at all Billy as income tax is levied according to the individual circumstances of the owner and no two cases would be the same. For example, one person may be eligible for tax rebates or deductions for negative gearing which will greatly alter the benchmark tax position.”

“You mean, I could have a depen-dant wife, or the ability to split income which would lower the total amount of tax paid on the same income,” Billy responded.

“Exactly, that and a host of other permutations that would be peculiar only to that individual. The idea here is to create a ‘level playing fi eld’. Now in the light of this, can you recognise any other expenses that should be excluded?”

Studying the Profi t & Loss statement in more detail, Billy asked, “What is the $5,000 in loan repayments for?”

“Supposes I told you that he was paying off his house mortgage, would you consider this to be an expense against his profi t?”

“Well, no because he is choosing to pay off his home from the business bank account and so the expense is not related to the operation of the business.”

“Good! This is merely how he is spending the money of the business. The payment needs re-cording to account for the reduc-tion in the bank account but it is the owners personal or lifestyle expense. Would the situation be any diff erent if he were paying off the loan he raised to buy the business?”

“I’m not sure,” Billy responded, it does seem to be a business expense but it doesn’t seem fair to deduct this from profi ts when another person may have paid cash and not needed to repay a loan.”

“Correct!” Douglas agreed, “Although the interest component

14

of the loan will be an expense for income tax purposes, the repay-ment of the principal part of the loan is paying for the business or buying an asset. The owner is using the profi ts to gain equity in the business.”

“In that case, the same logic would apply to the $6,300 in Ute repayments as a loan is reduced with equity in the Ute increasing. It isn’t an expense as the owner is getting the benefi t of an asset.”

“Yes, a true expense is limited to the period during which the income was earned, but the purchase of a Ute (or asset) benefi ts future income producing periods as well,” added Douglas. “It is therefore unfair to charge the expense of the Ute solely to the period of time in which it was purchased. As explained before, any interest on the loan to purchase the Ute would be tax deductible and an allowance for depreciation on the cost price of the vehicle.”

“I don’t understand the term ‘de-preciation,” Billy countered.

“I thought that might be your next question. Suppose you paid $20,000 cash for the motor vehicle, would it seem reasonable

to charge the full $20,000 as an expense against the income earned in that period?”

“Well, no. The $20,000 could be more than the total taken in earnings during that month and clearly the vehicle would be used in future periods.”

“Good, Billy now let’s suppose we consider that the vehicle has a working or useful ‘life’ of fi ve years then the cost needs to be apportioned over fi ve years or $4,000 per year assuming the Ute has no value at the end of the period.”

“So, we can say that $4,000 per year is the rate at which this Ute ‘wears out’ in doing the work of the business and this won’t agree with the amount of the repay-ments on the loan to buy the Ute,” Billy replied.

“You’ve got it, Billy, but for the moment let’s take out the cash payment of $6,300 to calculate the ‘profi t’ in this lawn mowing business. What else can you see in the fi gures that need to be excluded?”

“I reckon the speeding fi ne of $175 because it is a totally avoid-able expense and relates only

15

to the current owner’s driving habits.”

“Right again, Billy. Even though he may well have incurred the expense whilst at work, the decision to speed is a personal or lifestyle choice, and not a very good one!

In just the same way as we may have to eat to work but as we have to eat anyway, the cost of food is not an expense in doing business. What else can you see in the ‘profi t and loss’ account????”

“I’m guessing that the $2,000 paid in superannuation is for the owner C Green as there are no other wages, other than the $52,000 paid to him and some casual wages of $1,000. If this is the case then a further $54,000 of expenses need to be excluded.”

“You’re analysing now, Billy and you’re quite correct. The super-annuation is the decision of the owner to put aside for his retire-ment and is a saving. It may well be a tax deduction but again this is a lifestyle choice and is not an expense of mowing lawns. In the same way, this business operator has decided to take out $1,000 per week, or $52,000 per year as his personal drawings. This

fi gure is totally arbitrary and has no bearing whatsoever on the op-eration of the business except in how the cash is utilised. Let’s take a look at the fi nancial report after adding back non-business income and expenses.”

TIP:TO QUOTE WINSTON CHURCHILL, “ALL GREAT THINGS ARE SIMPLE” AND IN OVER 30 YEARS IN PUBLIC PRACTICE CLIENTS HAVE OFTEN ONLY CONSIDERED THE TAX POSITION OF A BUSINESS PURCHASE WITHOUT ASKING THE QUESTION, “CAN WE AFFORD IT ?”...ALWAYS SPEND LESS THAN YOU EARN.

16

“I’m certainly learning that a set of fi nancials can reveal a lot about how a person conducts his or her life,” enthused Billy, “from this small set of numbers we can learn:”

• The ‘profi t’ is $52,935 before paying off the car and business loans.

• The taxable income will be reduced to account for depreci-ation of $4,000 for the Ute and

interest paid on the business loans.

• The owner, Garry Green, takes $1,000 a week for living expenses, which is extravagant in his circumstances.

• Although the profi t supports this, the business is ‘cash starved’ and cannot aff ord the loan repayments for the Ute and the purchase of the business.

17

Profi t & Loss Statement - Garry your Lawns Barber - For Period Ending:Profi t & Loss Statement - Garry your Lawns Barber - For Period Ending:

Income: $ $

Lawn mowing 65,380Loans from G Green Excluded 65,380

Less Expenses:Accountancy 750Advertising 900Bank Fees 485Casual Labour 1,000Fuel & Oil (Mowers) 650 Hire of Equipment 800Income Tax Paid ExcludedInsurance (Business) 1,000Insurance (Income Protection) 1,500 Loan Repayments Excluded

Expenses Cont: $ $ $

Repairs & Replacements (Equipment) 1,300

Ute Expenses.Fuel 1,560Loan Repayments ExcludedRepairs 1,200Registration & Insurance 1,050Speeding Fine ExcludedWashes & Polishes 250 4,060Superannuation ExcludedWages for G Green Excluded 12,445

NET INCOME (LOSS) 52,935

Expenses Cont: $ $ $

Wages for G Green Excluded 12,445

NET INCOME (LOSS) 52,935

Fuel 1,560Loan Repayments ExcludedRepairs 1,200

Insurance 1,050Speeding Fine Excluded

Polishes 250 4,060Superannuation ExcludedWages for G Green Excluded 12,445

Expenses Cont: $ $ $

(Equipment) 1,300

Polishes 250 4,060Superannuation ExcludedWages for G Green Excluded 12,445

NET INCOME (LOSS) 52,935

Income: $ $

G Green Excluded 65,380

(Income Protection) 1,500

Income: $ $

Lawn mowing 65,380

G Green Excluded 65,380

Accountancy 750Advertising 900Bank Fees 485Casual Labour 1,000Fuel & Oil (Mowers) 650 Hire of Equipment 800Income Tax Paid ExcludedInsurance (Business) 1,000

(Income Protection) 1,500 Loan Repayments Excluded

Regular reconciliation of bank and other accounts is necessary whether the system is computerised or manual. This is the beauty of the double entry system. It allows forensic accountants to piece together a fi nancial story from incomplete records. Remember, there must

b e at least two sides to every transaction so if we know one we can often take an educated guess at what the others might be. This can be a very useful tool used by the Taxation and other authorities. It can also be very useful where records are incomplete

or missing especially when the balance sheet is reconstructed.”

“Thank you Douglas,” replied Billy, “I’ve learnt so much my head is spinning. It’s getting late and I need to go to bed! Can we look at the balance sheet another time please?”

“Of course, Billy, I’m glad I could be a help. Give me call when you’re ready to discuss the secrets of a balance sheet!”

• It was necessary to re-pay $5,000 into the business to prevent the bank account going into overdraft.

• Garry will need to either take less than $52,000 as drawings or increase his lawn mowing income by about $15,000 per year to meet his cash require-ments.

• Garry drives too fast.

• Garry appears to be a hard worker, doing most of the mowing work himself and em-ploying casual labour only oc-casionally.

• Garry is conscious of future needs in providing for his re-tirement in superannuation.

• The payment of income protec-tion insurance suggests Garry is willing to provide against unexpected events. (It could be argued that this is a lifestyle choice expense and shouldn’t be part of the business operat-ing costs.)

• The lawn mowing equipment is probably old and ‘tired’ judging

by the amount spent on repairs during the last twelve months.

• Garry did not have a lot of capital when he purchased the business and relied heavily on borrowed money.

• He would appear to be non safety-conscious judging by the lack of spending on protective clothing and sunscreens.

• Garry is probably not a ‘handyman’ and relies on outside help for his repair work.

“Well now, you’ve changed your tune from the ‘he should get a job comment’ made earlier!” said Douglas accompanied by a shake of his head. “You are right, of course, the business in itself is quite sound when we match the true expenses incurred against the income earned relative to the same period in time. We also can have confi dence in the recording accuracy of the cash income and expenses by reconciling the balance sheet cash fi gure of $2,872 with the actual bank statement. The bank statement may appear as follows:

18

“This won’t tell us whether the expenses and income have been correctly classifi ed but it will ensure we haven’t missed recording an item and is also a check against the accuracy of the bank statement,” continued Douglas. “In my experience, the bank statement is usually correct and an item, like bank fees, has been omitted from the cash book or values have been transposed, 393 instead of 339, for example.

19

Regular reconciliation of

system is computerised or

or missing especially when the

Bank Reconciliation As at: $ $ $

Balance per Bank Statement 3,600

Add:Deposit not yet on bank statement 150 3,750

Less:Unpresented Chq#118 525Unpresented Chq#121 290Bank Fees on Statement 63 878

Balance as per Cash Book (or ledger) 2,872

As at: $ $ $

on bank statement 150 3,750

Statement 63 878

Cash Book (or ledger) 2,872

As at: $ $ $

Bank Statement 3,600

on bank statement 150 3,750

Statement 63 878

Cash Book (or ledger) 2,872

As at: $ $ $

Bank Statement 3,600

on bank statement 150 3,750

Unpresented Chq#118 525Unpresented Chq#121 290

Statement 63 878

Cash Book (or ledger) 2,872

illy had given a great deal of thought about the fi nancial informa-tion he desired to know

from his operation. He made a list of the following;

• How much he had in his business bank account.

• His sales or turnover fi gures for the period.

• Where his money came from and how it was spent.

• How effi cient he was to the rest of the industry.

• Was he meeting his own pro-jections and expectations.

• Could he meet his debts as and when they fell due.

• Could he survive a tax offi ce audit.

• Would his systems uncover any fraud committed by employees.

• Are the records tax effi cient so the minimum, legal amount is paid.

• Can a net profi t be easily calcu-lated at the end of each month.

• Would the records satisfy an inspection by a potential buyer should he decide to sell.

He decided to set up his chart of accounts according to the follow-ing categories:

PROFIT & LOSS Dr Cr• Sales Received x• GST (or VAT) Received x• Capital Loan B Goose x• Accountancy & Bookkeeping x• Advertising x• Assets Purchased x• Bank Fees x• Cleaning x• Electricity & Power x• GST (or VAT) Paid x• Hire of Plant & Equipment x• Income Tax Paid x• Insurance x• Loan Repayments xMotor Vehicle:• Fuel x• Insurance & Rego x• Repairs & Mntce x• Repayments x• Other x

20

Dr Cr Rent x• Repairs to Plant & Equip x• Stock Purchases x• Superannuation (Employees) x• Superannuation (Billy) x• Sundry x• Telephone x• Wages & Tax Staff x• Wages (Drawings) Billy x

BALANCE SHEET• Cash at the Bank x x

Billy thought through the process with a few transactions and dis-covered the following:

If he paid his accountant $900 plus GST (or VAT) of $90 then he would record:

Dr. Accountancy & Bookkeeping $900Dr. GST Paid $90Cr. Cash at the Bank $990

The accounting system automati-cally credited the bank account and he fi gured this made sense as the bank was $990 less because of the payment.

Billy then thought through a receipt of cash of $1,100 for the sale of furniture and decided the transaction would show:

Dr. Cash at the Bank $1,100Cr. Sales $1,000Cr.GST Received $100 Again, the accounting system entered the $1,100 increase in the bank account automatically but in a manual cashbook system, postings to the Sales, GST and Cash at the Bank columns entered and the running bank balance calculated.

The entries concerning a $1,000 withdrawal of Billy’s wages or drawings would appear as:

Dr. Wages (Drawings) Billy $1,000Cr. Cash at the Bank $1,000

Whilst cash of $1,500 lent to the business would appear as:

Dr. Cash at the Bank $1,500Cr. Capital Loan B Goose $1,500

Billy considered the cash purchase of a computer and decided the entry would be:

Dr. Assets Purchased (Computer) $1,400Cr. Cash at the Bank $1,400

But he wasn’t sure how he would record the purchase of the

21

Chapter 4B A C K A T W O R K I N T H E O F F I C E

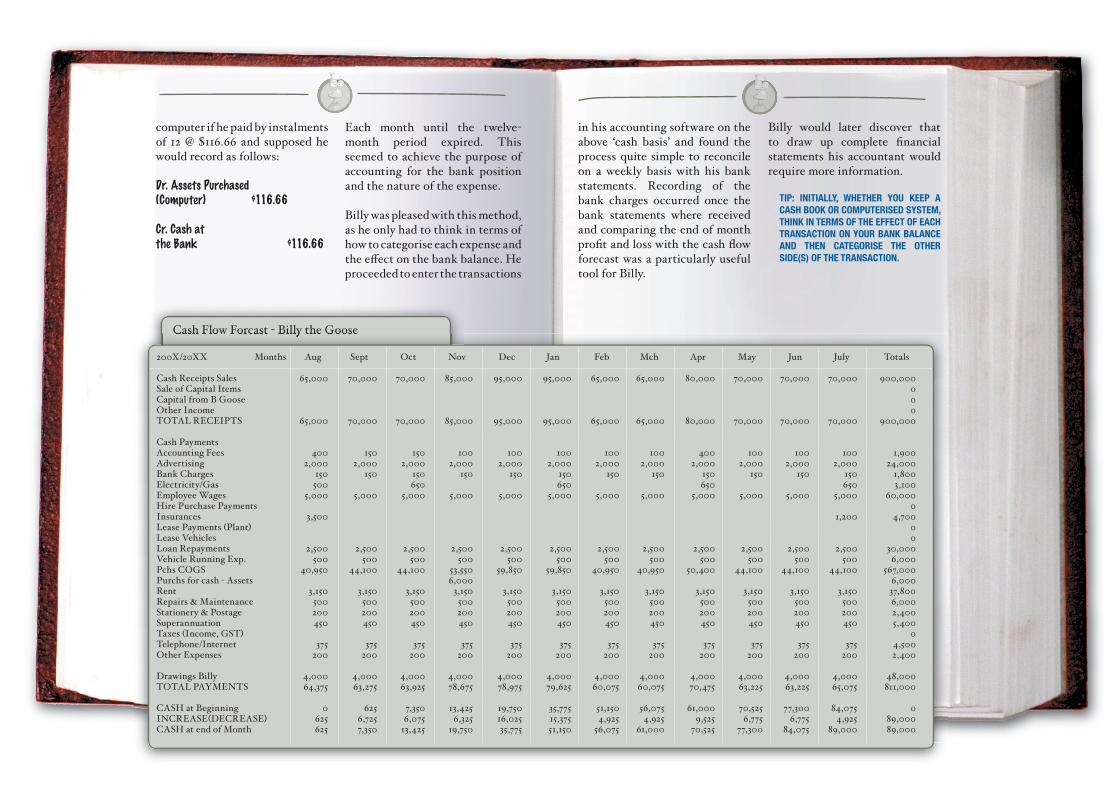

Cash Flow Forcast - Billy the Goose

computer if he paid by instalments of 12 @ $116.66 and supposed he would record as follows:

Dr. Assets Purchased (Computer) $116.66

Cr. Cash at the Bank $116.66

Each month until the twelve-month period expired. This seemed to achieve the purpose of accounting for the bank position and the nature of the expense.

Billy was pleased with this method, as he only had to think in terms of how to categorise each expense and the eff ect on the bank balance. He proceeded to enter the transactions

22

in his accounting software on the above ‘cash basis’ and found the process quite simple to reconcile on a weekly basis with his bank statements. Recording of the bank charges occurred once the bank statements where received and comparing the end of month profi t and loss with the cash fl ow forecast was a particularly useful tool for Billy.

23

Billy would later discover that to draw up complete fi nancial statements his accountant would require more information.

TIP: INITIALLY, WHETHER YOU KEEP A CASH BOOK OR COMPUTERISED SYSTEM, THINK IN TERMS OF THE EFFECT OF EACH TRANSACTION ON YOUR BANK BALANCE AND THEN CATEGORISE THE OTHER SIDE(S) OF THE TRANSACTION.

Cash Flow Forcast - Billy the Goose

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000 Cash Payments Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400 Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000 CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000

Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400

Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000

CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

200X/20XX Months Aug Sept Oct Nov Dec Jan Feb Mch Apr May Jun July Totals

Cash Receipts Sales 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000Sale of Capital Items 0Capital from B Goose 0Other Income 0TOTAL RECEIPTS 65,000 70,000 70,000 85,000 95,000 95,000 65,000 65,000 80,000 70,000 70,000 70,000 900,000

Accounting Fees 400 150 150 100 100 100 100 100 400 100 100 100 1,900Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 24,000Bank Charges 150 150 150 150 150 150 150 150 150 150 150 150 1,800Electricity/Gas 500 650 650 650 650 3,100Employee Wages 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 60,000Hire Purchase Payments 0Insurances 3,500 1,200 4,700Lease Payments (Plant) 0Lease Vehicles 0Loan Repayments 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 2,500 30,000Vehicle Running Exp. 500 500 500 500 500 500 500 500 500 500 500 500 6,000Pchs COGS 40,950 44,100 44,100 53,550 59,850 59,850 40,950 40,950 50,400 44,100 44,100 44,100 567,000Purchs for cash - Assets 6,000 6,000Rent 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 3,150 37,800Repairs & Maintenance 500 500 500 500 500 500 500 500 500 500 500 500 6,000Stationery & Postage 200 200 200 200 200 200 200 200 200 200 200 200 2,400Superannuation 450 450 450 450 450 450 450 450 450 450 450 450 5,400Taxes (Income, GST) 0Telephone/Internet 375 375 375 375 375 375 375 375 375 375 375 375 4,500Other Expenses 200 200 200 200 200 200 200 200 200 200 200 200 2,400

Drawings Billy 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 4,000 48,000TOTAL PAYMENTS 64,375 63,275 63,925 78,675 78,975 79,625 60,075 60,075 70,475 63,225 63,225 65,075 811,000

CASH at Beginning 0 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 0INCREASE(DECREASE) 625 6,725 6,075 6,325 16,025 15,375 4,925 4,925 9,525 6,775 6,775 4,925 89,000CASH at end of Month 625 7,350 13,425 19,750 35,775 51,150 56,075 61,000 70,525 77,300 84,075 89,000 89,000

fter a month of trading, Billy was feeling reasonably

comfortable that he was correctly recording

the transactions originating from his bank statement records. The cash received from sales didn’t reach the expected forecast target, but his purchases for stock were lower and the insurance fell due in the following month so the bank account position fi nalised at $410. He adjusted the cash fl ow forecast on the spreadsheet to account for the actual result and started to improve his intuitive fi nancial sense.

He decided to telephone Douglas.

“Hello Doug, this is Billy, is this a good time to talk to you?”

”Billy, how’s things? I was won-dering whether I would hear from you. I didn’t know whether you had been scared off by our last session!”“Not at all. In fact, I was hoping

we could discuss the workings of the balance sheet this time.”

“Come over tomorrow night but you’ll need a clear head because this is a more diffi cult area to un-derstand.”

“Thanks, I think I’m ready so I’ll look forward to seeing you tomorrow.”

TIP: IF YOU WANT TO BE AN ACCOUNTANT THEN STUDY TO BE AN ACCOUNTANT BUT IF YOU WANT TO BE AN ENTREPRENEUR THEN DO THE WORK OF THE ENTREPRENEUR AND NOT THE ACCOUNTANT

The jam and scones where already on the coff ee table when Billy arrived at the Debit’s home the next evening.

After the greetings and chit chat where fi nalised, Billy addressed Douglas with, “Where do we start?”

“I can see you’re eager to begin so, tell me, how much would

24

you estimate your home to be worth?”

“About $475, 000,” replied Billy.

“And you owe?”

“I have a mortgage of $100,000.”

“That means you have a net value of $375,000, being the amount you’d be left with should you decide to sell the property. This is called your equity or net worth and would appear on a balance sheet as follows:”

Balance SheetOf Billy the GooseAs at 30/1/XX

Assets:Property $475,000

Less Liabilities: Mortgage to Bank $100,000Net Assets $375,000

“You’ll notice that the net assets are calculated by subtracting the liabilities from the assets,” Douglas continued.

“That seems to be obvious,” Billy responded, “but that is only correct at this point in time as

the value of the property may increase, or decrease and the loan will change according to my repayments.”

TIP: THE BALANCE SHEET IS A ‘SNAP SHOT’ OF THE ASSETS, LIABILITIES AND EQUITY AT A FROZEN POINT IN TIME. IF AN ITEM ON THE BALANCE SHEET CAN BE PROVEN INCORRECT, DOUBLE ENTRY NECESSARILY MEANS THAT THE OTHER SIDE OF THE TRANSACTION MUST ALSO BE INCORRECT.

“Quite correct, Billy. The balance sheet is a fi nancial ‘snapshot’ in the same way a photograph freezes the subject to the point of time of the taking of the pho-tograph. A photograph of me twenty years ago is vastly diff er-ent to how I look now! I’ve got hair for a start!”

“So, is that why balance sheets always have the heading of ‘as at’ followed by the date? Similar to the date of a photograph so viewers are not misled into thinking you’re still a young stud with plenty of hair!”

“Yes,” replied Douglas with a wry grin, “now let’s complicate it a little more. Up ‘till now we’ve only considered the eff ect of transactions that are based in cash and for many small businesses this is adequate.

25

Chapter 5T H E B A L A N C E S H E E T

*NB The speeding fi ne and superannuation have been left in the profi t & loss statement. They could be excluded which would increase the profi t by $2,175 to $55,685G and increase drawings on the balance sheet by $2,175 to $54,175 7. The equity remains unchanged at $16,922H.

However, we need to understand some further areas such as debtors. Suppose our friend Mr Green had business customers. It would be unlikely for this type of customer to pay cash immediately as they would expect a 30 day account. If, during a month, Mr Green had invoiced $1,100 (inclusive of GST or VAT) for account customers the following entries would occur:

Dr. Debtors $1,100Cr. Sales $1,000Cr. Tax Liability $100

26

“You’ll see that the “loss” has reduced by $2,750 due to the net eff ect of the extra $3,000(1) in money not yet received and the $250(6) of expenses not yet paid. The balance sheet now shows:”

Balance SheetG Green – Your Lawns BarberAs at:

Assets:Cash at Bank $2,872Debtors $3,000 $5,872Less Liabilities:Creditors $250Owners Equity $5,622

“Let me see if I’ve understood this correctly,” responded Billy, “the net result has improved by $2,750 due to taking into consideration the $3,000 still to be collected from the account customers and the $250 owing for repairs to the mechanic. Because no cash has changed hands and the bank account remains unchanged, the transactions are recorded in the balance sheet as “debtors” and “creditors”.

“Yes,” replied Douglas, which also means the equity has increased by $2,750 to refl ect the better trading results”.

TIP: YOUR ACCOUNTANT CAN MAKE THIS TYPE OF “BALANCE DAY ADJUSTMENT” FOR YOU BY PUTTING THE TRANSACTIONS THROUGH AS JOURNAL ENTRIES. YOU WILL NEED TO HAVE THE DEBTORS, CREDITORS, STOCK ON HAND ETC AVAILABLE AT THE END OF THE REPORTING PERIOD.

“I’ll now get more complicated and show you how the accountant would treat the other numbered items in the balance sheet,” Douglas continued.

27

“Note that in a cash sale the debit entry changes to cash at bank whilst the others remain the same.”

“This is the reason I don’t record the sale until the cash is banked,” noted Billy, “it seems to be much easier!”

“Let’s take a look at our friend Garry Green and take account of $3,000 in money owing to Garry for lawns mowed but not yet received and $250 in a repair bill that he hasn’t yet paid.

Douglas continued.

Balance Sheet G Green – Your Lawns Barber - As at:

*NB The speeding fi ne and superannuation have been left

Balance Sheet G Green – Your Lawns Barber - As at:

Assets: $ Totals

Cash at Bank 2,872Debtors 3,000Lawn Business A 50,000Motor Vehicle (Ute)B 30,000 85,872Less Liabilities:Creditors 250Business Loan C 50,000Less Loan Repayments(4) (5,000)Vehicle Loan D 30,000Less Loan Repayments(5) (6,300) 68,950 16,922 E

Owners Equity Opening Balance F 17,212Profi t for Period G 53,510Plus Owners Capital(2) 5,000Less Owners Drawings(7) 52,000Less Income Tax Paid(3) 6,800 16,922 H

Assets: $ Totals

Cash at Bank 2,872Debtors 3,000

50,000 30,000 85,872

Creditors 250 50,000

(5,000) 30,000

(6,300) 68,950

17,212 53,510

5,000 52,000

6,800

Assets: $ Totals

30,000 85,872

(6,300) 68,950

Profi t & Loss Statement - Garry Green – Your Lawns Barber -For Period Ending:Profi t & Loss Statement - Garry Green – Your Lawns Barber -For Period Ending:

Income: $ $

Lawn mowing 68,380(1)

Loans from G Green 5,000(2) 73,380Less Expenses:Accountancy 750Advertising 900Bank Fees 485Casual Labour 1,000Fuel & Oil (Mowers) 650Hire of Equipment 800Income Tax Paid 6,800(3)

Insurance (Business) 1,000Insurance (Income Protection) 1,500 Loan Repayments 5,000(4)

Income: $ $

Lawn mowing 68,380Loans from G Green 5,000

Accountancy 750Advertising 900Bank Fees 485Casual Labour 1,000Fuel & Oil (Mowers) 650Hire of Equipment 800Income Tax Paid 6,800Insurance (Business) 1,000

(Income Protection) 1,500 Loan Repayments 5,000

Income: $ $

73,380

Expenses Cont: $ $ $

Repairs & Replacements (Equipment) 1,300Ute Expenses:Fuel 1,560Loan Repayments 6,300(5)

Repairs 1,450(6)

Registration & Insurance 1,050Speeding Fine 175*Washes & Polishes 250 10,785Superannuation 2,000*Wages for G Green 52,000(7) 84,970NET INCOME (LOSS) (11,590)

Balance $ $

Loss 11,590 (11,590)Add loan from G Green 5,000 (16,590)

Less Income Tax Paid 6,800 (9,790)Less Loan Repayments 5,000 (4,790)Less Ute Loan Repayments 6,300 1,510Less Wages G Green 52,000 53,510

“Wow! This is more detail than the cash report,” exclaimed Billy.

“Yes it is, but the bulk of most small business transactions are conducted through the bank account so if these are correctly summarised balance sheet infor-mation can be added to complete the picture. Let me now explain where the additional items in the balance sheet came from and why they are not in the profi t and loss account.

Lawn Business AThis $50,000 is the amount Mr Green paid for the lawn mowing round. He has acquired an asset and hopes that he can increase the value of this asset, ‘goodwill’ when he comes to sell the business. This is not an expense in the profi t and loss as it is not a cost against earning the day to day income of the business.

Motor Vehicle (Ute) BThis is the cost price of vehicle that Mr Green uses to travel to the customers properties. It is in the balance sheet because it is an asset and has ongoing value. It would be unfair to charge the whole cost of the Ute to the period in which it was pur-chased as the Ute will benefi t

future income earning periods. To overcome this, a charge called de-preciation is apportioned against the estimated life of the vehicle. This is something the accountant can do for you.

Business Loan C This notes the amount of money borrowed to buy the business and as repayments are made, the re-duction in principal is recorded (see (4) ) so that the outstanding liability appears on the balance sheet. Any interest on the loan is an expense recorded in the profi t and loss.

Vehicle Loan DBecause Mr Green didn’t have the money to buy the utility outright he was forced to take a loan as in the explanation above. The balance sheet is the place where the amount outstanding on the loan can be viewed and each payment of principal reduces the balance owing to the fi nance company. The diff erence between the value of the vehicle and the amount outstanding to the fi nance company is the equity in that particular asset.

Assets less Liabilities EThis simple sum represents the value of the business owners

28

equity and in accounting terms this is known as the accounting equation.

ASSETS – LIABILITIES = PROPRIETORSHIP (OR EQUITY)

Opening Balance FThis is the closing balance of the equity account at the end of the previous period brought forward to be the opening balance of the new period. For example, the closing balance of $16,922 in H will become the opening balance for the next period.

Profi t for Period GNow that all the expenses are correctly classifi ed the “loss” of $11,590 on the original Profi t & Loss Statement becomes a profi t as per the following:

In a small business the break down of cash expenditure will give a good indication of profi tability provided the above simple adjustments are made.

Closing Balance Equity HThis fi gure represents the money the owner (G Green) would be left with if all the assets were sold at the value recorded on the balance sheet and all the liabilities

were paid out as at the date the balance sheet was drawn up. These values are called “book values” and are theoretical in that it is the market that decides on value and not the balance sheet. The balance sheet also becomes outdated very quickly as each day brings new transactions and changes however, it is the only measure we have and it is better than nothing. Note that the equity must always balance with the sum of the assets – liabilities, hence the term “balance sheet.”

Douglas could see that Billy was feeling the pressure, and not wishing to make things worse he suggested:

“I’ll tell you what Billy, how about if I give you a check list just to recap your progress so far, and then we can call it a day”

29

Balance $ $

Loss 11,590 (11,590)Add loan from G Green 5,000 (16,590)

Less Income Tax Paid 6,800 (9,790)Less Loan Repayments 5,000 (4,790)Less Ute Loan Repayments 6,300 1,510Less Wages G Green 52,000 53,510

Balance $ $

Loss 11,590 (11,590)Add loan from G Green 5,000 (16,590)

Less Income Tax Paid 6,800 (9,790)Less Loan Repayments 5,000 (4,790)Less Ute Loan Repayments 6,300 1,510Less Wages G Green 52,000 53,510

Billy seemed relieved, it had been a long day.

THE CHECK LIST.

1. Accounting is generally per-formed on a ‘historical basis’. This means the information can be out of date when it is reviewed.

2. ‘Key performance indicators’ are a good way to measure trends as they happen and so action can be taken in ‘real time’.