Embed Size (px)

Citation preview

01.09.2014

1

0

Becoming a solution provider of choice in premium & value

Thomas Dressendörfer, CFOGoldman Sachs Healthcare conference

London, 4 September 2014

Strong financial and strategic progress

1

REVENUE BEST PERFORMERS GROSS MARGIN

CHF 359m APAC & ROW 78.9%

H1: +5% (organic) Q2: +3% (organic) Double-digit growth in both regions

+1.6% points (excl. FX) driven by strong implant volumes, optimized plant utilization and product mix

EBIT MARGIN TOTAL SOLUTION PROVIDER GROWTH STRATEGY

20.9% Portfolio expansionGeographic and segment expansion

Underlying margin1 improved 4.3% points driven by improved gross profit and reduced OPEX

New prosthetics range launched, new generation tapered implant, full regenerative range, innovation leadership

Investments in China and ‘value-brand’ platform

1 Excluding exceptionals in prior year and currency exchange rate effects2 The term ‘organic’ in this presentation means excluding the effects of acquisitions, divestitures and currency exchange rates

01.09.2014

2

2014 guidance

Rightsizing and re-organisation

measures

* Straumann, Nobel Biocare, Zimmer Dental, Biomet 3i, Dentsply Implants - based on company and SEC reports as well as management comments.

2

Fifth consecutive quarter of above-market growth

1Straumann, Nobel Biocare, Zimmer Dental, Biomet 3i, Dentsply Implants, based on company and SEC reports, as well as management comments. 2

Q2: revenue of CHF 179mn (+3% in l.c.)

Easter effect

1

Tracking the progress of our key priorities

3

Lean, high performance organization

Address changed market dynamics

Target unexploited growth markets

Cost reduction measures

New organization with increased customer focus

Continuing cost discipline

Customer- and market-driven Solutions

Immediate edentulous solutions

New tapered implant Ceramic implant Innovative Smileloc More CARES solutions Full regenerative range

Increase presence in fast-growing underpenetrated markets

Distribution take-over & new hybrid approach in China

Address value segment

Instradent set up and Neodent rolled-out

Investments in MegaGen & Biodenta

01.09.2014

3

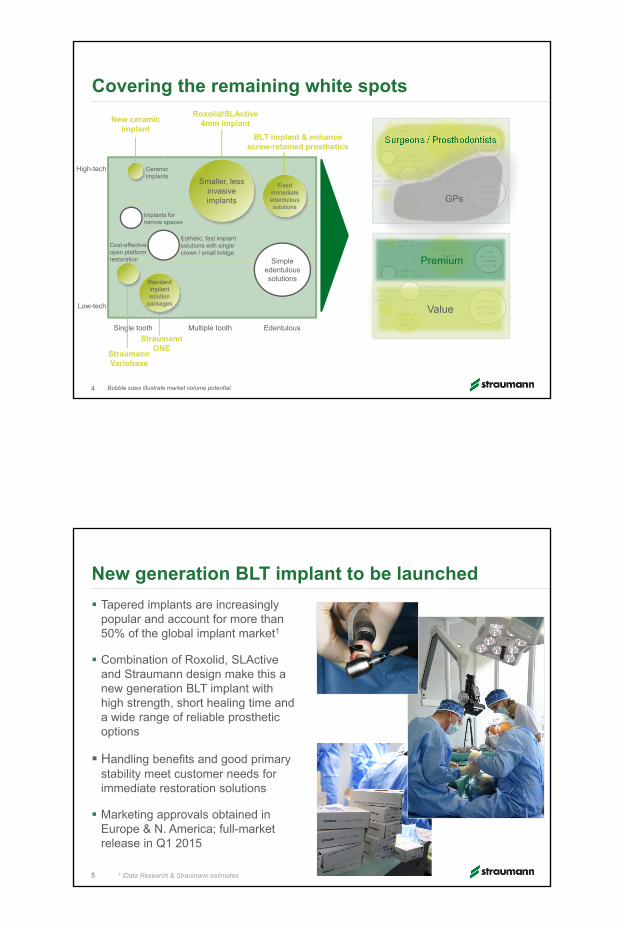

Covering the remaining white spots

Surgeons / Prosthodontists

GPs

Premium

Value

New ceramicimplant

Roxolid/SLActive 4mm implant

Single tooth Multiple tooth Edentulous

Ceramic implants

Simpleedentulous solutions

Implants for narrow spaces

Esthetic, fast implant solutions with single crown / small bridge

Low-tech

High-tech

4

Straumann ONE

Straumann Variobase

Cost-effective, open platform restoration

Bubble sizes illustrate market volume potential

BLT implant & enhance screw-retained prosthetics

Standard implant solution

packages

Fixed immediate edentulous solutions

Smaller, less invasive implants

Tapered implants are increasingly popular and account for more than 50% of the global implant market1

Combination of Roxolid, SLActive and Straumann design make this a new generation BLT implant with high strength, short healing time and a wide range of reliable prosthetic options

Handling benefits and good primary stability meet customer needs forimmediate restoration solutions

Marketing approvals obtained in Europe & N. America; full-marketrelease in Q1 2015

5 1 iData Research & Straumann estimates

New generation BLT implant to be launched

01.09.2014

4

6

1 Commercially pure cold-worked grade 4 titanium2 Full-market release

Straumann’s comprehensive implant portfolio

Tissue Level4mm short

implantBone Level Bone Level Tapered2 PURE

Monotype

SLA SLActive SLActive SLA SLActive SLA SLActive ZLA

Titanium1

Roxolid

Ceramic

Q1 2015

Shorter/ thinner

More primary stability

Aesthetics

7

Growth of private hospital and practice segment expected to exceed public hospital segment, which Straumann leads

Agreement with former distributor Beijing Finest Medical Instrument Co. Ltd. to take over certain assets

fixed considerations of CHF 9mn plus variable consideration up to CHF 18mn depending on business performance until 2016

Greater control of business in China; access to distribution network, customers, market data etc.

Further sales growth through hybrid multi-distributor model approach

Significant investments to build a consultative sales force and local training-&-education organization with target of growing in private segment, where Straumann is under-represented

New hybrid multi-distributor model in China

01.09.2014

5

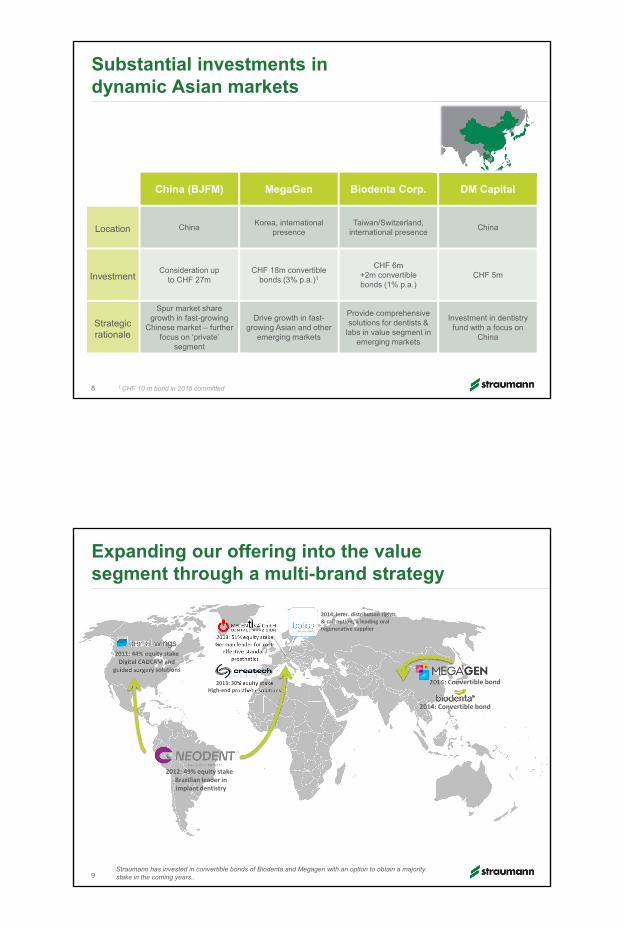

8 1 CHF 10 m bond in 2015 committed

Substantial investments in dynamic Asian markets

China (BJFM) MegaGen Biodenta Corp. DM Capital

Location ChinaKorea, international

presenceTaiwan/Switzerland,

international presenceChina

InvestmentConsideration up

to CHF 27mCHF 18m convertible

bonds (3% p.a.)1

CHF 6m +2m convertiblebonds (1% p.a.)

CHF 5m

Strategic rationale

Spur market sharegrowth in fast-growing

Chinese market – further focus on ‘private’

segment

Drive growth in fast-growing Asian and other

emerging markets

Provide comprehensivesolutions for dentists &

labs in value segment in emerging markets

Investment in dentistryfund with a focus on

China

9

Expanding our offering into the valuesegment through a multi-brand strategy

9Straumann has invested in convertible bonds of Biodenta and Megagen with an option to obtain a majority stake in the coming years..

2012: 49% equity stakeBrazilian leader in implant dentistry

2013: 51% equity stake German leader for cost‐

effective standard prosthetics

2014: Convertible bond

2013: 30% equity stake High‐end prosthetic solutions

2011: 44% equity stakeDigital CADCAM and

guided surgery solutions

2014: Convertible bond

2014: Inter. distribution rights & call option; a leading oral regenerative supplier

01.09.2014

6

10 1 Selected countries

Global presence in the value segment

Europe1 NAM LATAM APAC

Impl

ant s

yste

ms

Implants

Standard prosthetics

CADCAM

Abu

tmen

ts

Abutmentsfor 3rd partyimplants

Bars/bridgesfor 3rd partyimplants

11§§§

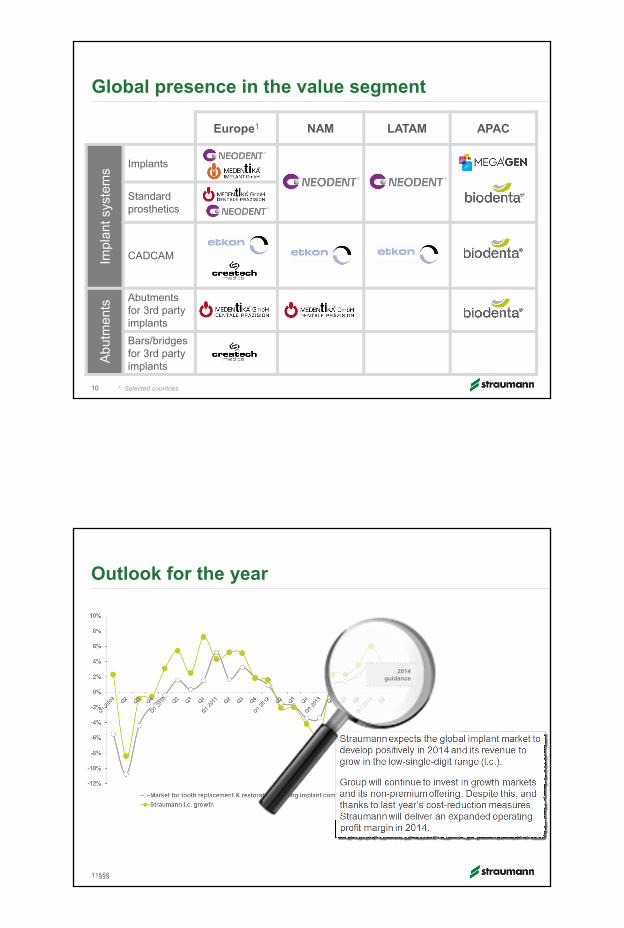

Outlook for the year

11

2014 guidance

01.09.2014

7

Calendar of upcoming events

2014

04 September Goldman Sachs Healthcare conference London

05 September Investor meetings London

15 September Investor meetings Frankfurt

23 October Third‐quarter results Webcast

20 November Credit Suisse Swiss Midcap conference Zurich

03 December Berenberg European conference Bagshot/London

04 December Investor meetings London

2015

27 February Full‐year 2014 results Basel HQ

1212 Results publication and corporate events. More information on straumann.com → Events

Appendix

13

01.09.2014

8

General practitioner (GP) segment gaining importance with different needs than the specialists segments

Female dentists becoming more and more important

Value players gaining share on behalf of premium players

Young dentist with different needs when it comes to T&E

To source differentiated treatment components from single supplier is a differentiating factor

Prosthetics decision maker becoming more and more driver for implant choice

14

Pressure to adapt to market trends

Source: iData Research, US data, 2012

2008

2014Implant specialistsGPs placing implantsGPs restoring implants

60 600

87 400GPs restorebut don’t place implants

15 900

29 700GPs place implants

GPs are increasingly important and have different preferences

15

01.09.2014

10

2201 2170

23612452

2517

23132217

2278

2008 2009 2010 2011 2012 H12013

2013 H12014

Global worforce (period‐end)

Organization adapted to match market development

18

Headcount reduced by 300 to pre-economic crisis level

Overall restructuring/downsizing costs in 2013 amount to a net CHF 8m1

Strong, engaged team of professionals retained

New organizational set-up focuses more on customer needs

Cost optimization

measures implemented

1 Including severance packages and curtailed pension obligations

77.8%

(0.5%)

77.3%

0.8%

1.2% (0.4%)

78.9%

H1 gross profitmargin

FX effect Adj. H1 grossprofit margin

Price / volume /mix

Inventory change COGS (highervolumes)

H1 gross profitmargin

In % of revenue, rounded

Higher implant sales and efficiency gains lift gross profit margin

191 Change in finished and semi-finished goods in H1 2014 compared with prior year

1

20142013

+160 bps

01.09.2014

11

16.0%

(0.9%) 1.6%

16.7%

1.6%

2.6% 0.0%

20.9%

Reported H1EBIT

FX effect Restructuringcosts

Adjusted H1EBIT

Gross marginimprovement

OPEX reduction Other income Reported H1EBIT

EBIT margin clears 20% threshold

20

+420 bps

20142013

1 Exceptional costs of CHF 6 million related to last year’s cost optimization measures

In % of revenue, rounded

1

20

21

Straumann’s currency exposure

Cost breakdown 20131

Revenue breakdown 2013

1 These distribution charts represent the total net revenues and the total COGS as well as OPEX expenses in the various currencies. All numbers are rounded and based on 2013 figures.

Average exchange rates (rounded) FX sensitivity (+/- 10%) on...

FY 2013 YTD 2014 Revenue EBIT

EURCHF 1.23 1.22 +/- 25 million +/- 15 million

USDCHF 0.93 0.90 +/- 17 million +/- 7 million

JPYCHF 0.95 0.88 +/- 4 million +/- 2 million

21

EUR 40%

CHF 12%

USD / CAD / AUD 28%

Other 20%

EUR 21%

CHF 45%

USD / CAD /

AUD 22%

Other 12%

70

90

110

2013 2014

Development of Straumann’s main exchange rates since 2013

USDCHF EURCHF JPYCHF