Embed Size (px)

Citation preview

1

Basel II – What does it mean for Canadian banks and investors?

Presented by:

Vivek Wadhwa, McKinsey & Company

January 25, 2008

2

Basel II OverviewBackground and TimingNew Concepts

Impact on CapitalBuilding Blocks to Capital Calculations Supervisory Review and Sanity ChecksRegulatory Capital - Basel I vs. Basel IIFactors Contributing to Differences between FIs

Reporting and disclosuresPillar 3 – New Concepts and DisclosuresImplications for Investors and FIs

Agenda

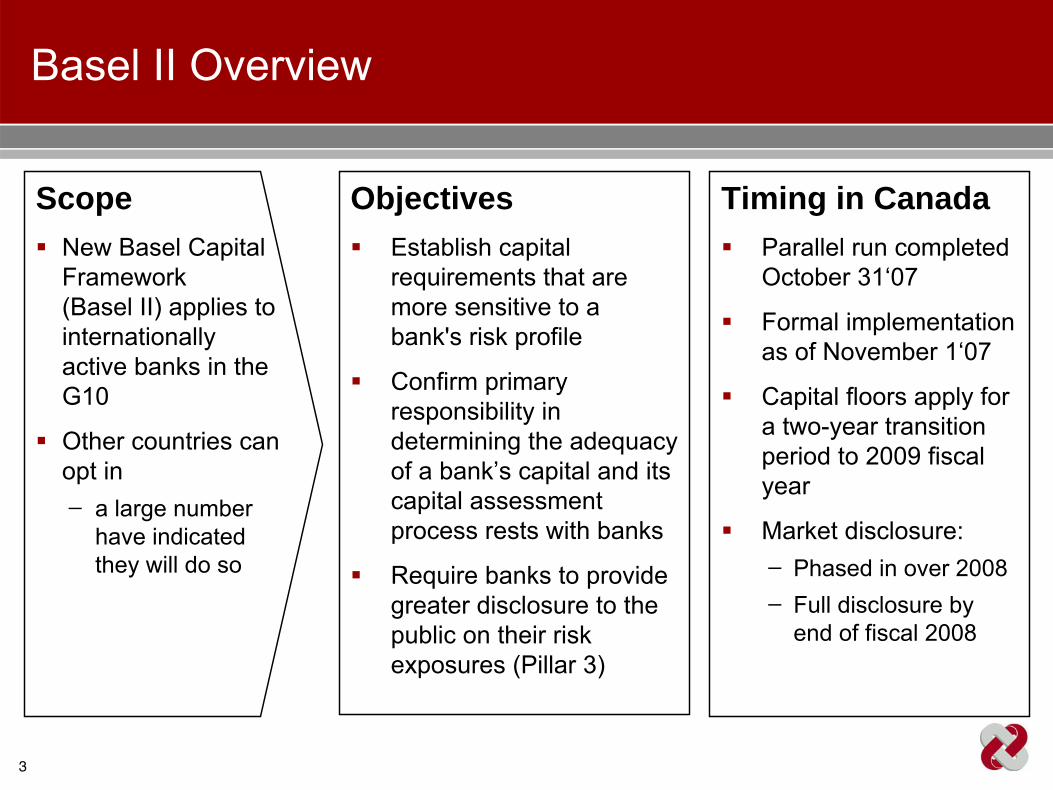

3

Basel II Overview

ScopeNew Basel Capital Framework (Basel II) applies to internationally active banks in the G10

Other countries can opt in ̶ a large number

have indicated they will do so

ObjectivesEstablish capital requirements that are more sensitive to a bank's risk profile

Confirm primary responsibility in determining the adequacy of a bank’s capital and its capital assessment process rests with banks

Require banks to provide greater disclosure to the public on their risk exposures (Pillar 3)

Timing in Canada Parallel run completed October 31‘07

Formal implementation as of November 1‘07

Capital floors apply for a two-year transition period to 2009 fiscal year

Market disclosure:̶ Phased in over 2008̶ Full disclosure by

end of fiscal 2008

4

Basel II Overview

The Basel II Framework has three mutually reinforcing pillars

Minimum Capital Requirements

Credit RiskOperational RiskMarket Risk ‘98

Supervisory ReviewInternal Standards for Capital Assessment

Market DisclosureRisk AssessmentCapital Adequacy

Pillar 1 Pillar 2 Pillar 3

New Basel Capital Accord

5

Basel II Overview

Basel II calculates minimum capital requirements based on exposure to different risks

Credit Risk Operational Risk Market Risk

Risk of losses in on-and off-balance sheet positions arising from movements in market

prices

Potential that a bank borrower or

counterparty will fail to meet its obligations in

accordance with agreed terms

Major changes

Risk of loss resulting from inadequate or

failed internal processes, people and

systems or from external events

New element Minimal change

6

Basel II Overview

Credit Risk Operational Risk Market Risk

Internal Ratings Based (IRB) Approaches

Advanced IRB (AIRB)

Foundation IRB (FIRB)

Standardized Approach

Advanced Measurement Approach (AMA)

Standardized Approach

Basic Indicator Approach

Internal Model Approach (IMA)

Standardized Approach

Minimum Capital

Basel II offers a range of capital calculation approaches

7

Basel II Overview

Basel II also offers a range of risk reducing treatmentsPrescribed eligible types of collateral Methods of reflecting credit risk mitigation (CRM) impact

Understanding implications of these different approaches to risk and risk mitigation is critical to any basis of comparability of FIs

8

Basel II Overview

Impact on CapitalBuilding Blocks to Capital Calculations

Credit Risk including Securitization and Equity HoldingsOperational RiskMarket Risk

Supervisory Review and Sanity ChecksRegulatory Capital - Basel I vs. Basel IIFactors Contributing to Differences Between FIs

Reporting and Disclosures

Agenda

9

Building Blocks to Capital CalculationsCredit Risk

OSFI Expectation that:

Banks meeting the following criteria must use AIRB approach for Credit and at a minimum Standardized approach for Operational Risk:

Regulatory capital in excess of $5 billion, or

> 10% of assets or liabilities that are international

Each FI must meet all minimum requirements and obtain approval for AIRB

To adopt an alternate approach for specific credit portfolios orsubsidiaries requires OSFI approval

All other FIs can opt for approach of their choice, subject to OSFI approval

10

Building Blocks to Capital CalculationsCredit Risk – OSFI Guidance

OSFI permits:

A phased in adoption of the AIRB approach for material credit portfolios, if an FI requests a “Waiver” of same

Permanent exemption for non material portfolios if requested, subject to approval

A 3 year conversion to AIRB for material portfolios outside Canada, subject to granting an extension to the FI with clear roll out plan

11

Building Blocks to Capital Calculations Credit Risk – New Concepts and Definitions

Basel II Credit Risk language

Takes into account outstanding exposures andpotential exposure risks in the event of default

EADExposure at DefaultCan use contractual maturity or effective maturityMMaturity

Driven by the Facility Risk Rating (FRR)May reflect guarantees and/or collateral

LGDLoss Given Default

Driven by borrower characteristics, including Borrower’s Risk Rating (BRR)May reflect guarantees

PDProbability of DefaultDescriptionAbbr.Risk Parameter

Risk parameters are assigned based on the obligor’s and facility’s risk profile

12

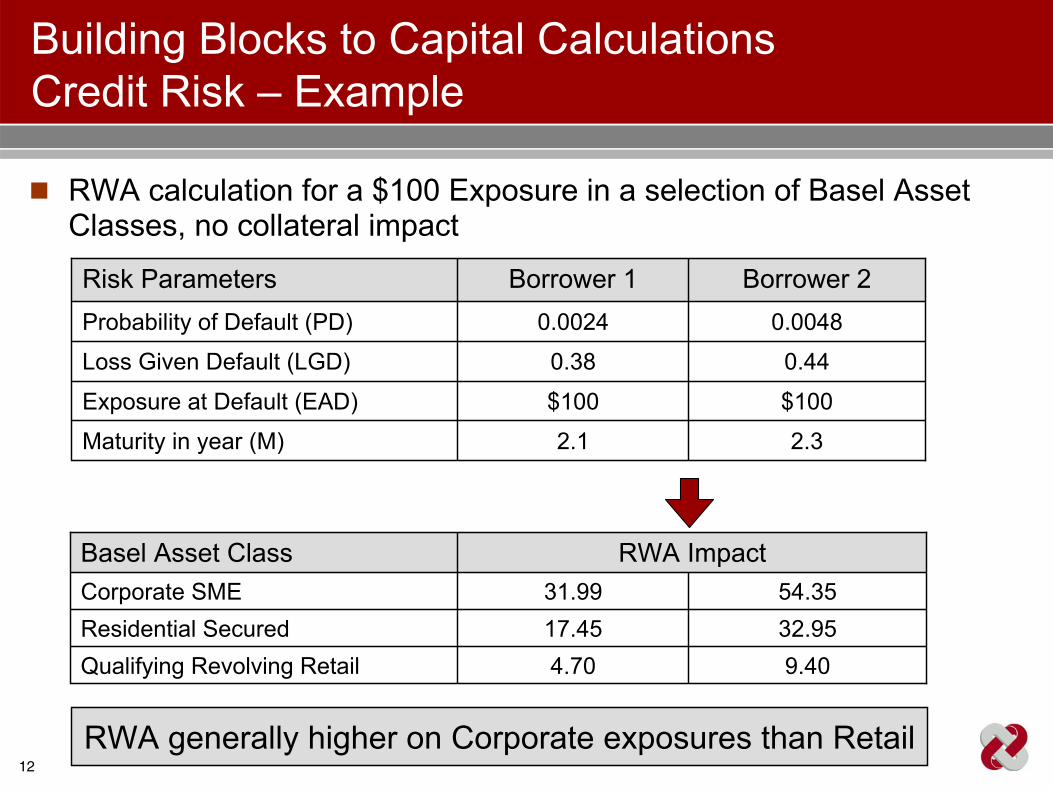

Building Blocks to Capital Calculations Credit Risk – Example

RWA calculation for a $100 Exposure in a selection of Basel Asset Classes, no collateral impact

2.32.1Maturity in year (M)

$100$100Exposure at Default (EAD)

0.440.38Loss Given Default (LGD)

0.00480.0024Probability of Default (PD)

Borrower 2Borrower 1Risk Parameters

9.404.70Qualifying Revolving Retail32.9517.45Residential Secured54.3531.99Corporate SME

RWA ImpactBasel Asset Class

RWA generally higher on Corporate exposures than Retail

13

Building Blocks to Capital Calculations Securitization

Basel II addresses two key areas of securitization

Holdings of securities issued by securitization vehicles

Provision of credit enhancements (mainly liquidity facilities) to securitization vehicles

Basel II treatment very different from Basel I Risk weights are mapped from internal ratings (under Internal Assessment Approach)

Range from 7% to 650% with a 100% Credit Conversion Factor on everythingCan result in dollar-for-dollar capital deduction for facilities with an equivalent rating level below BB-

Basel II treatment is similar to revised Basel I Risk weights are associated with ratings levels

The Basel II risk weights are generally favourable compared with the Basel I risk weightsUnrated positions and those with low agency ratings are deducted from capital in both frameworks

14

Building Blocks to Capital Calculations Equities in the Banking Book

Only allowed for:non-tier 1 perpetual pref. shares without redeemable feature perpetual pref. shares with redeemable feature at the issuer’s option

PD’s must satisfy same requirements as bank’s PD estimate Minimum 90% LGD5 year maturity adjustment

Standardized Approach

Prescribed risk weights:

100% in most cases

Internal Ratings Based

Market Based Approach PD/LGD Method

Simple Risk WeightNon material - similar to Standardized Material - risk weighted at 300% (publicly traded), 400% (other equities)

Internal ModelsCapital – same as Internal VaR model Subject to floors equivalent to: 200% (publicly traded), 300% (all other)

IRB also allows for Grandfathering – up to 10 years under Basel I for equity positions as at July 2004

15

Building Blocks to Capital Calculations Operational Risk

Standardized Approach Advanced Management Approach

Based on risk measure generated by internal operational risk measurement systemMust reasonably estimate expected and unexpected losses based on:

internal and external loss datascenario analysisbank-specific business environment internal control factors

Requires credible, documented and verifiable approachRequired capital driven by analysis of expected and unexpected losses

Based on Gross income which: Acts as a proxy for the size of the business Serves as an indicator of the operational risk

Grouped into eight regulatory business lines

Each line charged a rate prescribed by the FrameworkAverage over 3 years for each business line X business line’s rate

Required capital driven by the type and size of business lines

16

Building Blocks to Capital Calculations Market Risk

Market Risk capital calculations remain largely unchanged from Basel I

Standardized Internal Model

Use requires OSFI approval

17

Basel II Overview

Impact on CapitalBuilding Blocks to Capital Calculations

Credit Risk including Securitization and Equity HoldingsOperational RiskMarket Risk

Supervisory Review and Sanity ChecksRegulatory Capital - Basel I vs. Basel IIFactors Contributing to Differences Between FIs

Reporting and Disclosures

Agenda

18

Framework for banks to assess their own capital adequacy and processes, including:

Assessment of regulatory capital in conjunction with economic capitalStress testing regulatory capital calculated under Pillar 1Internal capital adequacy assessment processCapital plan

Framework for supervisors to review banks’ capital adequacy and processes, including:

Evaluation of bank’s internal capital adequacy, assessment and strategies, as well as bank’s ability to monitor and ensure compliance with regulatory capital ratio and relevant standardsEarly intervention if a bank’s risks are deemed to be out of proportion with its capitalResolution strategiesFramework to address all other risks not captured in Pillar 1

Supervisory Review and Sanity Checks

19

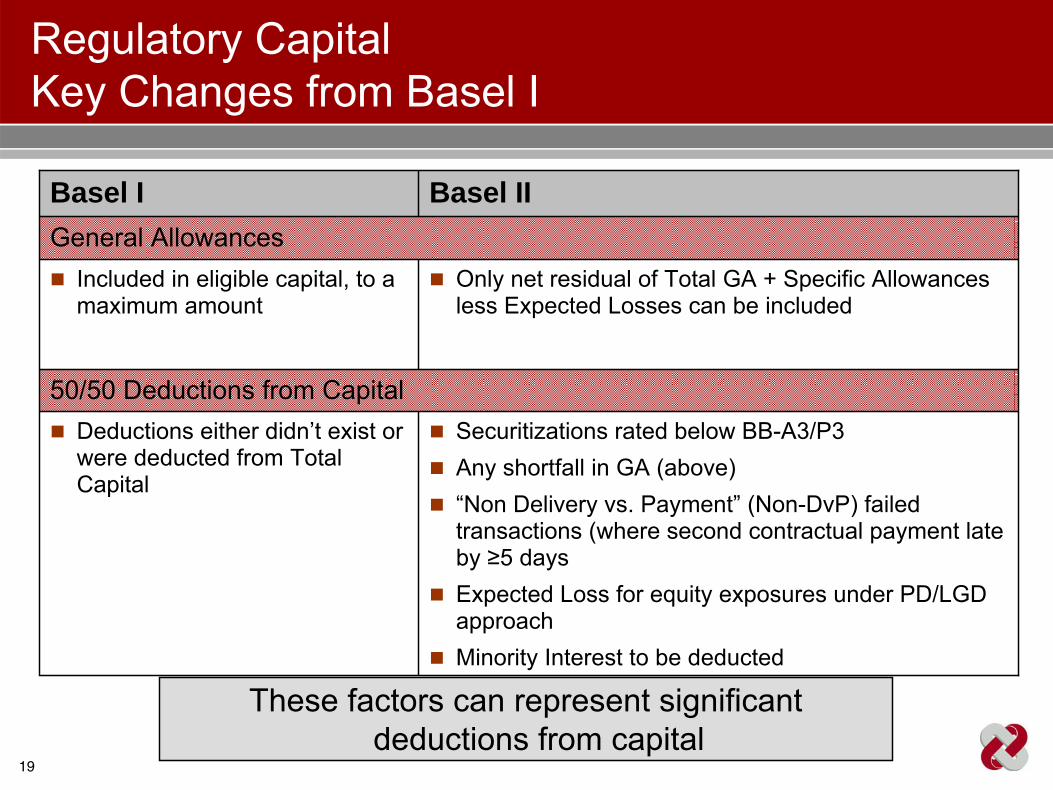

Regulatory CapitalKey Changes from Basel I

50/50 Deductions from Capital

General Allowances

Securitizations rated below BB-A3/P3Any shortfall in GA (above)“Non Delivery vs. Payment” (Non-DvP) failed transactions (where second contractual payment late by ≥5 daysExpected Loss for equity exposures under PD/LGD approachMinority Interest to be deducted

Deductions either didn’t exist or were deducted from Total Capital

Only net residual of Total GA + Specific Allowances less Expected Losses can be included

Included in eligible capital, to a maximum amount

Basel IIBasel I

These factors can represent significant deductions from capital

20

Regulatory CapitalTransition Period

Individual FI’s regulatory capital requirement is subject to:

Capital Floors during Transition (if approved by OSFI)FYE 2008: Capital floor is 90% of Basel I calculationFYE 2009: Capital floor is 80% of Basel I calculation

Full benefits of Basel II may not accrue to FI’s during the Transition Period as a result of floors or choices made by the banks

OSFI has the right to increase and/or maintain the floor at their discretion including post Transition Period

OSFI approval required on the methodologies, models, and related estimates for banks implementing AIRB

21

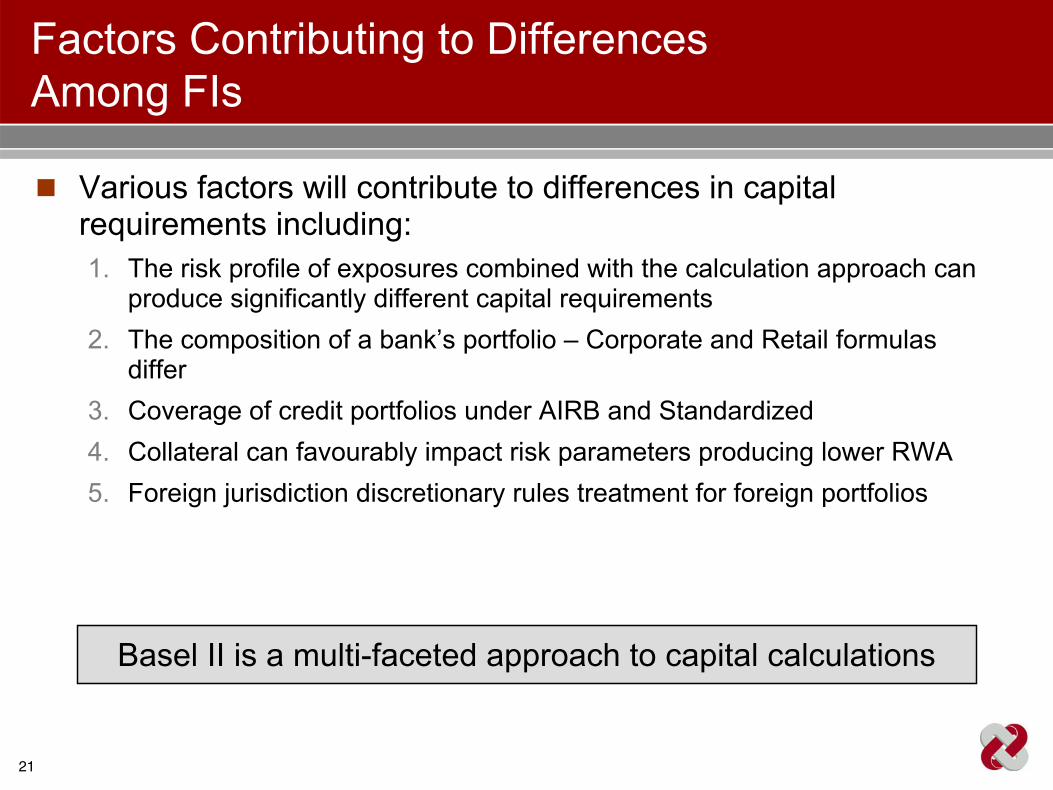

Factors Contributing to Differences Among FIs

Various factors will contribute to differences in capital requirements including:1. The risk profile of exposures combined with the calculation approach can

produce significantly different capital requirements2. The composition of a bank’s portfolio – Corporate and Retail formulas

differ3. Coverage of credit portfolios under AIRB and Standardized4. Collateral can favourably impact risk parameters producing lower RWA5. Foreign jurisdiction discretionary rules treatment for foreign portfolios

Basel II is a multi-faceted approach to capital calculations

22

Factors Contributing to Differences Between FIs

1. The risk profile of exposures combined with the calculation approach can produce significantly different capital requirements:

Higher risk profile = higher RWA

Under AIRB approach

A bank’s own risk parameters are assigned to each individual exposure based on risk profile (PD, LGD)

Maturity date

EAD factors on undrawn commitments

Under Standardized approachRange of risk weights (0% up to 150%) prescribed by the Framework - linked to external credit ratings, LTVs (mortgages), and/or other risk characteristics

Longer maturities = higher RWA

Higher factors = higher RWA

Higher risk = higher RWA

23

Factors Contributing to Differences Between FIs

2. Composition of portfolioCorporate AIRB capital calculation formula different than Retail IRBRetail has no Maturity factorSMEs can be treated as Corporate or Retail, SME adjustment to formula reduces capitalAll things being equal, Corporate formula will produce higher RWA than Retail

3. Coverage of credit portfolios under AIRB and StandardizedStandardized approach typically produces higher RWA

If Bank A has 20% of its portfolios under the Standardized approach and Bank B has 50%, it is reasonable to expect higher RWA for Bank B, all things being equal

24

Factors Contributing to Differences Between FIs

4. Credit Risk Mitigation approaches can favourably impact risk parameters producing lower RWA

GuaranteesExample (IRB approach – PD substitution):

Assume a mortgagor is assigned a PD of 20% prior to taking collateral into accountIf the exposure is an NHA insured mortgage, the exposure is treated as ‘Sovereign’ with associated risk parameters (as low as 0% PD)RWA will be reduced significantly

CollateralExample (IRB approach – LGD substitution):

Assume a Corporate loan is secured by US T-BillsThe collateralized loan’s RWA is calculated using secured LGD, which will be much lower than the unsecured LGDRWA will be reduced significantly

25

Factors Contributing to Differences Between FIs

5. Foreign jurisdiction discretionary rules for foreign portfolios OSFI typically allows use of foreign national supervisor’s treatment for discretionary items – if treatment is not too dissimilar to Canadian treatmentExample:

If exposure to a foreign Public Sector Entity (PSE) is allowed to be treated as ‘Sovereign’ by the foreign national supervisor, OSFI will allow this exposure to be treated as ‘Sovereign’

OSFI allows preferential treatment to local currency exposures to foreign governments or central banks, provided the respective national supervisors give similar treatmentExample:

If foreign supervisor allows local banks to assign 0% risk weight for their local dollar sovereign debt, OSFI will allow similar treatment

26

Basel II Overview

Impact on Capital

Reporting and DisclosuresPillar 3 – New Concepts and DisclosuresImplications for Investors and FIs

Agenda

27

Reporting and DisclosuresPillar 3 - Market Discipline

What is Pillar 3?

A set of disclosure requirements to increase transparency and enable market participants to assess important information about a bank’s:

Risk profileRisk management processes Level of capitalization

Particularly important due to reliance on internal methodologies in Advanced Approaches

Use and acceptance of internal methodologies by the Regulator is contingent on a number of criteria including appropriate disclosure

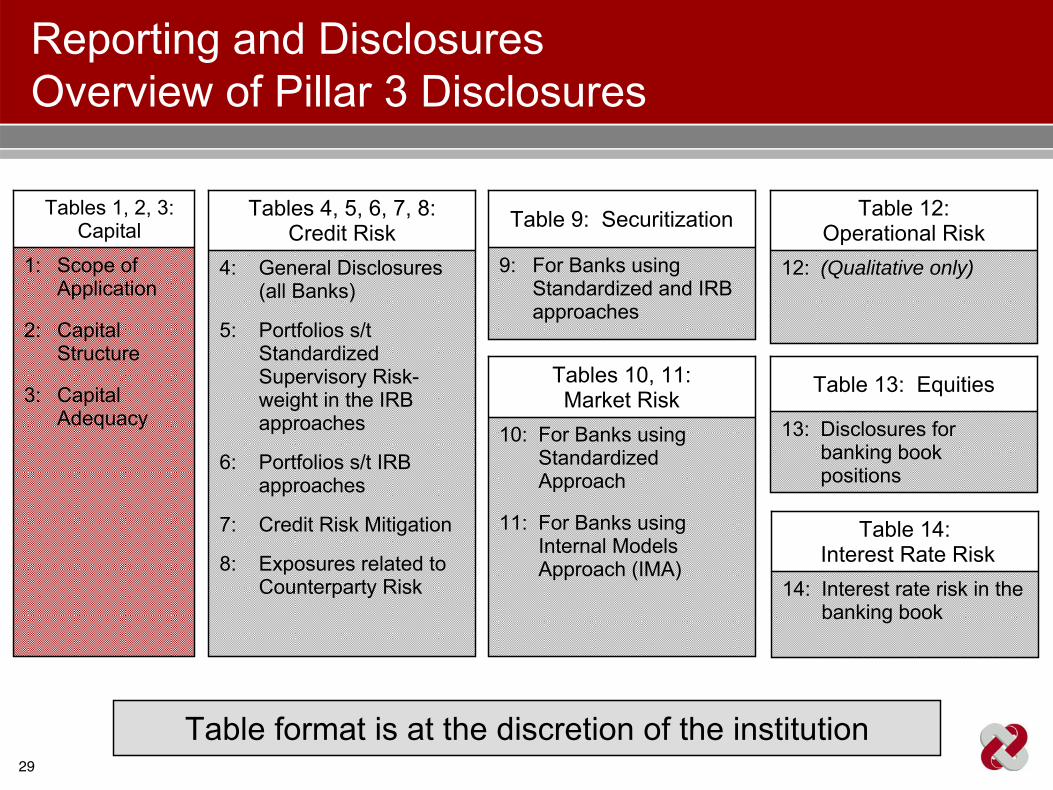

The Framework imposes minimum disclosure requirements on banks, which include 14 tables covering qualitative and quantitative disclosures

28

Reporting and DisclosuresPillar 3 Deliverables / Timing

Deliverable Description DisclosureFrequency

ImplementationTiming

Qualitative Disclosures

Information on risk management objectives and processes

Annually Required by year-end 2008

Quantitative Disclosures

Tables detailing risk exposures and capital requirements

Quarterly Canadian banks phasing in over 2008

All disclosures required by year-end 2008

Location of disclosures is at the discretion of the institution, but FIs are encouraged to provide related information in one

location, to the extent possible

29

Reporting and DisclosuresOverview of Pillar 3 Disclosures

1: Scope of Application

2: Capital Structure

3: Capital Adequacy

Tables 1, 2, 3: Capital

4: General Disclosures (all Banks)

5: Portfolios s/t Standardized Supervisory Risk-weight in the IRB approaches

6: Portfolios s/t IRB approaches

7: Credit Risk Mitigation

8: Exposures related to Counterparty Risk

Tables 4, 5, 6, 7, 8:Credit Risk

9: For Banks using Standardized and IRB approaches

Table 9: Securitization

10: For Banks using Standardized Approach

11: For Banks using Internal Models Approach (IMA)

Tables 10, 11: Market Risk

12: (Qualitative only)

Table 12: Operational Risk

13: Disclosures for banking book positions

Table 13: Equities

14: Interest rate risk in the banking book

Table 14: Interest Rate Risk

Table format is at the discretion of the institution

30

Reporting and DisclosuresNew Concepts and Definitions

Basel Counterparty Types under the IRB ApproachMultiple new classifications which provide added granularity of reporting:

CorporateSovereignBankRetail

Residential SecuredQualifying Revolving Retail (e.g. credit cards and unsecured lines of credit)All Other Retail

Basel classifications will likely not align directly with existing reporting practices

31

Reporting and DisclosuresNew Concepts and Definitions

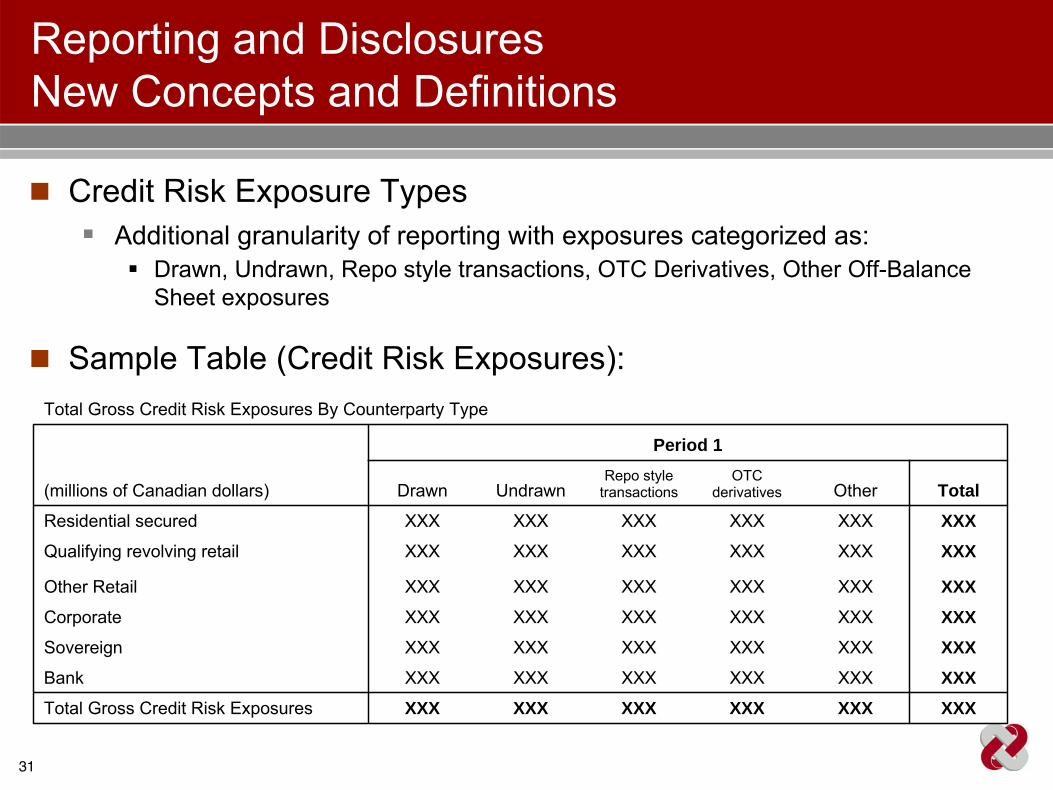

Credit Risk Exposure Types Additional granularity of reporting with exposures categorized as:

Drawn, Undrawn, Repo style transactions, OTC Derivatives, Other Off-Balance Sheet exposures

Sample Table (Credit Risk Exposures):

XXXXXXXXXXXXXXXXXXTotal Gross Credit Risk Exposures

XXXXXXXXXXXXXXXXXXBank

XXXXXXXXXXXXXXXXXXSovereign

XXXXXXXXXXXXXXXXXXCorporate

XXXXXXXXXXXXXXXXXXOther Retail

XXXXXXXXXXXXXXXXXXQualifying revolving retail

XXXXXXXXXXXXXXXXXXResidential secured

TotalOtherOTC

derivativesRepo style

transactionsUndrawnDrawn

Period 1

(millions of Canadian dollars)

Total Gross Credit Risk Exposures By Counterparty Type

32

Reporting and DisclosuresImplications for Investors and FI’s

Enhanced granularity of data will allow for more in-depth analysis and improved understanding of underlying risks

However, disclosures will be based on new and/or modified concepts and definitions, making historical comparisons more challengingBanks may select different levels of granularity for their disclosures (e.g. number of Probability of Default (PD) bands)

It will be difficult to compare banks relative to their Basel IIdisclosures, especially in the initial stages of implementation

Calculation approach(es) taken by one bank will likely differ from othersLinks to Basel I and financial statement disclosures are likely to differ at the outset and may become more comparable over timeFI’s have the choice of location of disclosures - MD&A, financial statements, web site - expect refinements over time

33

Reporting and DisclosuresImplications for Investors and FI’s

The implementation of Basel II will be an evolution Aggregate amount of capital in the banking system is not expected to change significantly. However, shifts will occur over time as

AIRB coverage of portfolios including international and US subsidiaries increases and other risk parameters evolveRisk management processes become richer and data, testing and models are enhanced

The alignment of risk, capital requirements and business strategy will continue

FIs will continue to more closely align pricing, portfolio composition and risk-adjusted performance with risk and capital

34

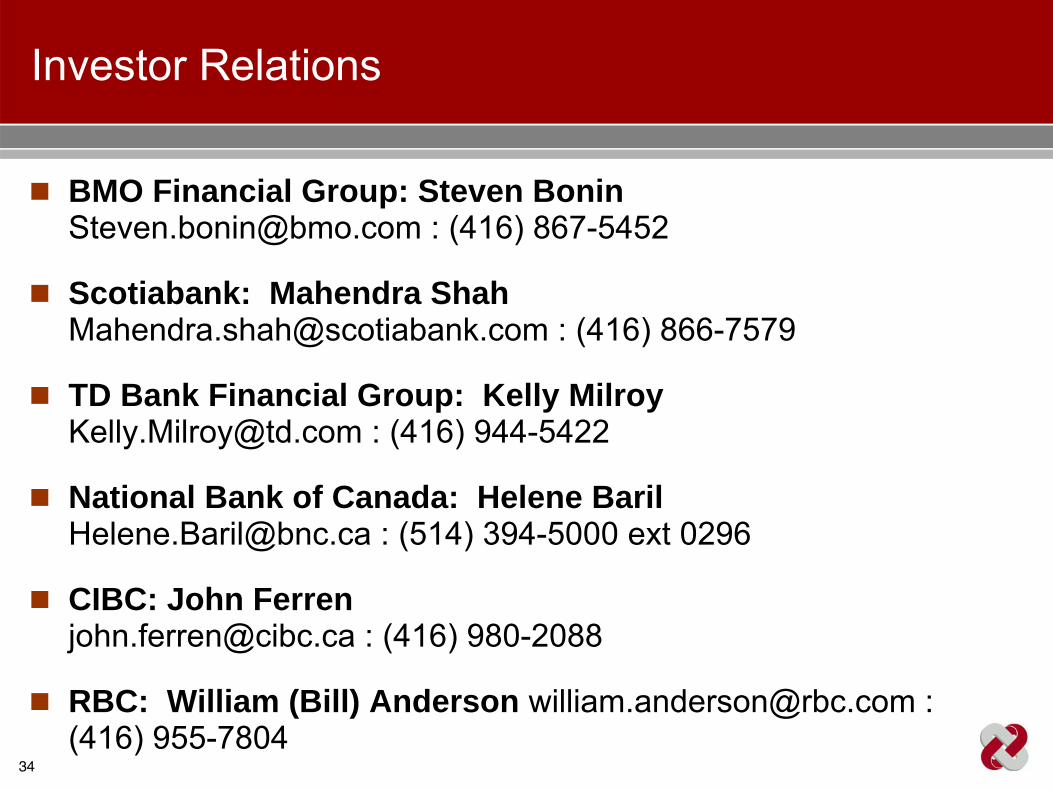

Investor Relations

BMO Financial Group: Steven [email protected] : (416) 867-5452

Scotiabank: Mahendra [email protected] : (416) 866-7579

TD Bank Financial Group: Kelly [email protected] : (416) 944-5422

National Bank of Canada: Helene [email protected] : (514) 394-5000 ext 0296

CIBC: John [email protected] : (416) 980-2088

RBC: William (Bill) Anderson [email protected] : (416) 955-7804

35

Media Relations

BMO Financial Group: Ralph [email protected] : (416) 867-3996

Scotiabank: Ann [email protected] : (416) 933-1344

TD Bank Financial Group: Simon Townsend [email protected] : (416) 944-7161

National Bank of Canada: Denis Dubé[email protected] : (514) 394-8644

CIBC: Rob [email protected] : (416) 980-3714

RBC: Beja [email protected] : (416) 974-5506