Embed Size (px)

Citation preview

Bank of Baroda(Registration number 1997/012717/10)

Trading as Bank of Baroda, Consolidated South African OperationsAnnual financial statements

for the year ended 31 March 2019

These annual financial statements were prepared by:Vijay Saradhi Yasam

Senior Manager (Compliance)

These annual financial statements have been audited in compliance with the applicable requirements of theCompanies Act 71 of 2008.

Issued 29 July 2019

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

General Information

Country of incorporation and domicile South Africa, domiciled in Durban and Johannesburg

Nature of business and principal activities The South African operations of the Bank of Baroda (hereinafterreferred to as the "Company") is focused on providing a premierbanking solution to the medium-sized business market in South Africa.The Branch has been operating since incorporation from 1997 onward.

Directors Manoj Kumar Jha

Vijay Saradhi Yasam

Sakharam Bhandarkar

Registered office 2nd Floor, Atrium on 5th

Sandton City East Tower

Johannesburg

South Africa, Gauteng

2196

Business address 2nd Floor, Atrium on 5th

Sandton City East Towers

Johannesburg

South Africa, Gauteng

2196

Postal address 2nd Floor, Atrium on 5th

Sandton City East Tower

Johannesburg

South Africa, Gauteng

2196

Bankers Nedbank

Auditors Nexia SAB&T

Chartered Accountants (SA)

Registered Auditors

119 Witch-Hazel avenue

Highveld Technopark

Centurion

0046

Company registration number 1997/012717/10

Tax reference number 9665707718

Level of assurance These annual financial statements have been audited in compliancewith the applicable requirements of the Companies Act 71 of 2008.

1

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Index

Page

Directors' Responsibilities and Approval 3

Independent Auditor's Report 4 - 8

Directors' Report 9 - 10

Statement of Financial Position 11

Statement of Profit or Loss and Other Comprehensive Income 12

Statement of Changes in Equity 13

Statement of Cash Flows 14

Accounting Policies 15 - 21

Notes to the Annual Financial Statements 22 - 42

2

INDEPENDENT AUDITOR’S REPORT To the Directors of Bank of Baroda South African Operations Report on the Audit of the Annual Financial Statements Qualified Opinion We have audited the annual financial statements of Bank of Baroda South African Operations (the Bank) set out on pages 11 to 42, which comprise the statement of financial position as at March 31, 2019, and the statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies. In our opinion, except for the possible effect of the matter described in the Basis for Qualified Opinion section of our report, the annual financial statements present fairly, in all material respects, the financial position of the Bank as at March 31, 2019, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards and the requirements of the Companies Act of South Africa.

Basis for Qualified Opinion Advances, interest receivable and other receivables The Bank’s advances, interest receivable and other receivables are carried in the statement of financial position as part of Assets classified as held for sale at R398 million (2018: R683 million). We have identified objective evidence for an additional impairment of advances, interest receivable and other receivables that creates a possible misstatement regarding the recoverability of advances, interest receivable and other receivables. The Bank’s records indicate that, had management raised an additional allowance for doubtful advances, interest receivable and other receivables, an amount of R296 million (2018: R207 million) would have been required. Accordingly, advances, interest receivable and other receivables would have been decreased by R296 million (2018: R207 million). We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Annual Financial Statements section of our report. We are independent of the group in accordance with the sections 290 and 291 of the Independent Regulatory Board for Auditors’ Code of Professional Conduct for Registered Auditors (Revised January 2018) (IRBA Code (Revised January 2018)), parts 1 and 3 of the Independent Regulatory Board for Auditors’ Code of Professional Conduct for Registered Auditors (Revised November 2018) (IRBA Code (Revised November 2018)) and other independence requirements applicable to performing audits of financial statements in South Africa. We have fulfilled our other ethical responsibilities in accordance with the IRBA Code (Revised January 2018), the IRBA Code (Revised November 2018) and in accordance with other ethical requirements applicable to performing audits in South Africa. Sections 290 and 291 of the IRBA Code (Revised International Ethics Standards Board for Accountants Code of Ethics

for Professional Accountants. Parts 1 and 3 of the IRBA Code (Revised November 2018) are consistent with parts 1 and 3 of the International Ethics Standards Board for Accountants’ International Code of Ethics for Professional Accountants (including International Independence Standards). We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified opinion.

Key Audit Matters Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the annual financial statements of the current period. These matters were addressed in the context of our audit of the annual financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. In addition to the matter described in the Basis for Qualified Opinion section, we have determined the matters described below to be the key audit matters to be communicated in our report. Key Audit Matter

How our audit addressed the key audit matter

Recoverability of long outstanding receivables The Bank reflected R398 million (2018: R683 million) worth of receivables as at 31 March 2019 as disclosed in note 9 to the financial statements against which an allowance for doubtful advances and receivables of R80 million (2018: R179 million) has been recognised. Where there is objective evidence of impairment, the bank is required to determine and recognise an appropriate allowance for doubtful advances and receivables. Due to the nature of the Bank’s operations, advances and receivables are expected to be settled on maturity date and therefore advances and receivables outstanding beyond this period would be at risk of non-recovery. Determining the value of the allowance requires a high degree of judgement and estimation. Accordingly, the determination of the allowance for doubtful advances and other receivables are considered to be a key audit matter.

Our audit procedures focused on the evaluation of the key judgements and estimates used in managements’ determination of the allowance for doubtful advances and other receivables. The procedures on key judgements included but were not limited to:

Analysis of the classification of the advances and other receivables to ensure the correct aging bracket of debt has been applied;

Analysis of the value of the secured and unsecured portions of the advances and other receivables to ensure the correct portion has been included in the assessment;

Analysis of the provision at a category level as a proportion of total advances and other receivables to identify and investigate unusual fluctuations;

Testing the mathematical accuracy of the model to ensure the allowance ratio per aging bracket of debt has been accurately applied to current year debt.

Additional impairment on advances and other receivables not recorded by management is raised in the basis for qualified opinion paragraph.

Compliance by the Bank

The Bank as a regulated entity is required to comply with various laws and regulations notably Financial Intelligence Centre Act (FIC), National Credit Act (NCA), Money Laundering and Terrorist Financing Control Regulations, and the Banks Act, all of which are integral to the operations of the Bank. Non-compliance may have public interest implications in terms of potentially substantial harm to investors, creditors, employees or the general public. In the light of additional requirements to respond to non-compliance with laws and regulations, as well as certain information which is in the public domain, compliance with the above-mentioned laws and regulations are considered to be a key audit matter.

In responding to the key audit matter identified, our audit procedures included but were not limited to:

Review of the banks Financial Crime Reporting Manager system’s functionality on identifying items flagged and closed off.

Inspection of other reports submitted by the Bank and correspondence in respect of the Bank’s compliance requirements;

Inspection of a sample of client documents to verify the Bank’s processes on compliance; and

The use of checklists to assess compliance with the Financial Intelligence Centre Act (FIC), National Credit Act (NCA), Money Laundering and Terrorist Financing Control Regulations and the Banks Act.

Non-compliance in terms of the FIC Act and laws and regulations is raised in the Report of other legal and regulatory requirements of the audit report.

Other Information The directors are responsible for the other information. The other information comprises the information included in the document titled “Bank of Baroda Annual Financial Statements for the year ended 31 March 2019”, which includes the Directors’ Report as required by the Companies Act of South Africa. The other information does not include the annual financial statements and our auditor’s report thereon. Our opinion on the annual financial statements does not cover the other information and we do not express an audit opinion or any form of assurance conclusion thereon. In connection with our audit of the annual financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the consolidated and separate financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed on the other information obtained prior to the date of this auditor’s report, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard. Responsibilities of the Directors for the Annual Financial Statements The directors are responsible for the preparation and fair presentation of the annual financial statements in accordance with International Financial Reporting Standards and the requirements of the Companies Act of South Africa, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the annual financial statements, the directors are responsible for assessing the group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the group or to cease operations, or have no realistic alternative but to do so. Auditor’s Responsibilities for the Audit of the Annual Financial Statements Our objectives are to obtain reasonable assurance about whether the annual financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements. As part of an audit in accordance with ISAs, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

Identify and assess the risks of material misstatement of the annual and separate financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the group’s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the directors.

Conclude on the appropriateness of the directors’ use of the going concern basis of accounting and based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the annual financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the group to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the annual financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the group to express an opinion on the annual financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with the directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit. We also provide the directors with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the directors, we determine those matters that were of most significance in the audit of the annual financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Report on Other Legal and Regulatory Requirements In terms of the IRBA Rule published in Government Gazette Number 39475 dated 4 December 2015, we report that Nexia SAB&T has been the auditor of Bank of Baroda South African Operation for 4 years. In accordance with our responsibilities in terms of sections 44(2) and 44(3) of the Auditing Profession Act, we report that we have identified reportable irregularities in terms of the Auditing Profession Act. We have reported such matters to the Independent Regulatory Board for Auditors. The matter pertaining to the reportable irregularities has been described below:

During the course of the 31 March 2019 financial year, the Bank did not keep appropriate and complete ‘‘Know Your Client’’ (‘‘KYC’’) records as required by Section 22 of the FIC Act. The Bank however took steps against the clients that did not submit their KYC documents by freezing their accounts but failed to maintain the correctness of particulars in accordance with regulation 19 and regulation 22 as they did not report this to the FIC.

Nexia SAB&T S Kleovoulou Director Registered Auditor 29 July 2019 119 Witch-Hazel Avenue Centurion

Pretoria

0169

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Directors' Report

The directors have pleasure in submitting their report on the annual financial statements of Bank of Baroda, ConsolidatedSouth African Operations for the year ended 31 March 2019.

1. Incorporation

The company was incorporated on 04 August 1997 and obtained its certificate to commence business on the same day.

2. Nature of business

Bank of Baroda, South African Operations is a South African registered branch of foreign Bank i.e. Bank of Baroda, aGovernment of India owned Bank, and is domiciled in Johannesburg and Durban.

The Company specialises in providing a diverse range of financial products and services to a niche client base whichoperates principally within South Africa. The Company continued to service its customer base as a commercial bank. Itsfocus during the year under review remained on medium sized entrepreneurial businesses and small corporate's as well.

In February 2018, the bank announced its intention to cease operations in South Africa and has undertaken thenecessary steps in order to settle all its deposits and other payables and receive all of its advances and otherreceivables.

The company will however continue its presence until all the statutory requirements are complete.

3. Review of financial results and activities

The annual financial statements have been prepared in accordance with International Financial Reporting Standards andthe requirements of the Companies Act 71 of 2008. The accounting policies have been applied consistently compared tothe prior year, except for the adoption of new or revised accounting standards as set out in note 1.

Full details of the financial position, results of operations and cash flows of the company are set out in these annualfinancial statements.

4. Share capital

The Bank holds a capital contribution of R100 000 000 relating to the initial capital investment as required by The SouthAfrican Reserve Bank for branches operating from South Africa for foreign Banks.

5. Dividends

No dividends were declared in the current year under review.

6. Directorate

The directors in office at the date of this report are as follows:

Directors Office Designation Nationality ChangesManoj Kumar Jha Chief Executive Officer Executive IndianVijay Saradhi Yasam Chairperson Executive Indian Appointed 07 July 2018Sakharam Bhandarkar Chairperson Executive Indian Appointed 07 July 2018

7. Property, plant and equipment

There was no change in the nature of the property, plant and equipment of the company or in the policy regarding theiruse.

8. Holding company

The company's holding organisation is Bank of Baroda headquarted in Mumbai, India. The holding organisation hascontinued to support the Company, and the Directors have no reason to believe that this support will not continue.

9

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Directors' Report

9. Borrowing powers

In terms of the policies of the company, the directors may exercise all the powers of the company to borrow money, astheir Head Office in India consider appropriate.

10. Going concern and events after the reporting period

In February 2018, the bank announced its intention to cease operations in South Africa and has undertaken thenecessary steps in order to settle all its deposits and other payables and recover all its advances and other receivables.

The bank will however continue to operate for the Bank of Baroda India within South Africa until the processes neededhave been satisfied in order for the cessation of operations to become effective.

We draw attention to Note 25 in the financial statements which indicate that the Bank incurred a net loss of R114 672 879for the year ended 28 February 2019, and as of that date, the Bank's current liabilities exceed the current assets by R265778 313 (excluding the assets and liabilities classified as held for sale). The directors believe that the company hasadequate financial resources to continue the operations of the Bank and accordingly the annual financial statements havebeen prepared on a going concern basis.

11. Auditors

Nexia SAB&T has been appointed as auditors of the current financial year and will be eligible for election to continue inoffice in accordance with section 90 of the Companies Act of South Africa.

12. Liquidity and solvency

The directors have performed the required liquidity and solvency tests required by the Companies Act of South Africa andthere are no instances of contravention noted in terms of the requirements as set forth by the Companies Act of SouthAfrica or the requirements of the Reserve Bank of South Africa.

10

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Statement of Financial Position as at 31 March 20192019 2018

Note(s) R R

Assets

Non-Current Assets

Property, plant and equipment 3 552 864 804 396

Deferred tax 4 - 44 375 572

552 864 45 179 968

Current Assets

Cash and cash equivalents 5 57 852 773 2 240 224 258

Advances and other receivables 6 5 356 053 308 803

Interest receivable 895 166 22 104 891

Other financial assets 7 341 427 900 44 651 446

VAT receivable 27 356 -

Loans to group companies 8 - 3 117 609

Current tax receivable 965 275 16 425 626

406 524 523 2 326 832 633

Assets classified as held for sale 9 398 239 804 683 298 841

Total Assets 805 317 191 3 055 311 442

Equity and Liabilities

Equity

Capital contribution 10 112 703 160 112 703 160

Retained income 3 408 953 118 081 832

116 112 113 230 784 992

Liabilities

Current Liabilities

Deposits and other borrowings 11 638 722 2 557 564

Interest payable 455 493 1 295 644

Loans from group companies 8 343 602 600 794 647 919

Other financial liabilities 12 344 508 263 -

VAT payable - 290 285

689 205 078 798 791 412

Liabilities directly associated with assets classified as held for sale 9 - 2 025 735 038

Total Liabilities 689 205 078 2 824 526 450

Total Equity and Liabilities 805 317 191 3 055 311 442

11

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

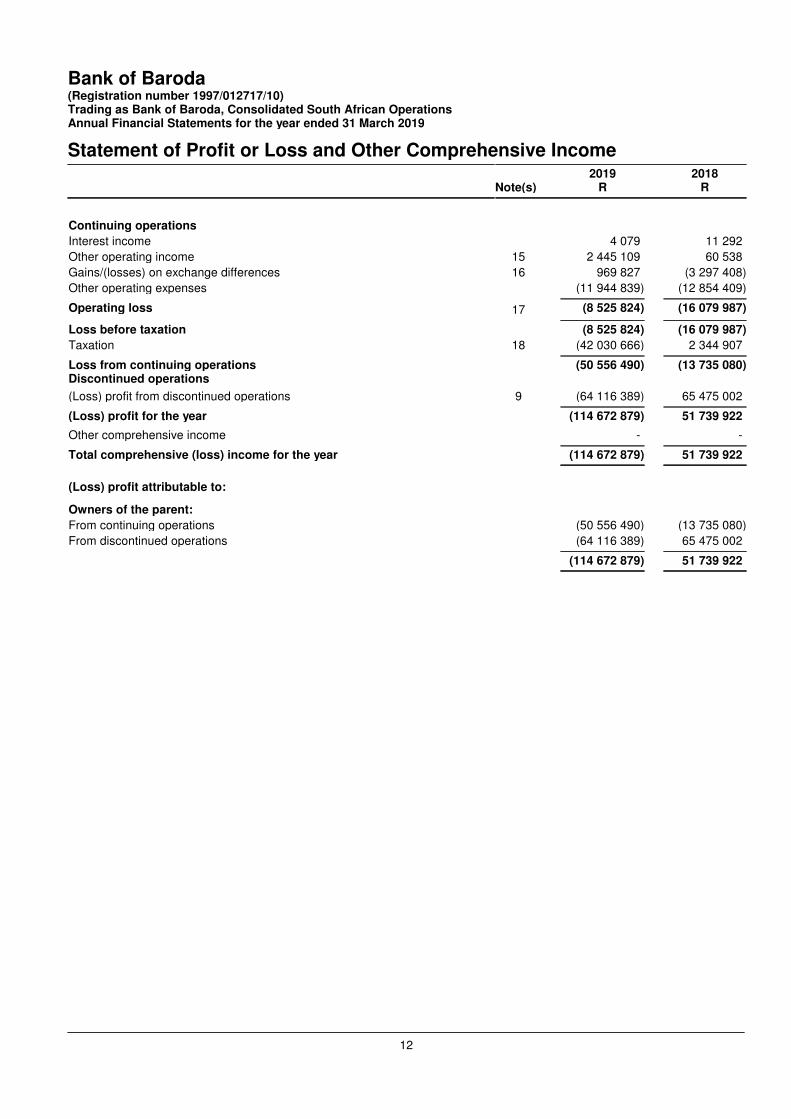

Statement of Profit or Loss and Other Comprehensive Income2019 2018

Note(s) R R

Continuing operations

Interest income 4 079 11 292

Other operating income 15 2 445 109 60 538

Gains/(losses) on exchange differences 16 969 827 (3 297 408)

Other operating expenses (11 944 839) (12 854 409)

Operating loss 17 (8 525 824) (16 079 987)

Loss before taxation (8 525 824) (16 079 987)

Taxation 18 (42 030 666) 2 344 907

Loss from continuing operations (50 556 490) (13 735 080)Discontinued operations

(Loss) profit from discontinued operations 9 (64 116 389) 65 475 002

(Loss) profit for the year (114 672 879) 51 739 922

Other comprehensive income - -

Total comprehensive (loss) income for the year (114 672 879) 51 739 922

(Loss) profit attributable to:

Owners of the parent:

From continuing operations (50 556 490) (13 735 080)

From discontinued operations (64 116 389) 65 475 002

(114 672 879) 51 739 922

12

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Statement of Changes in EquityCapital

ContributionRetainedincome

Total equity

R R R

Balance at 01 April 2017 112 703 160 66 341 910 179 045 070

Profit for the year - 51 739 922 51 739 922Other comprehensive income - - -

Total comprehensive income for the year - 51 739 922 51 739 922

Balance at 01 April 2018 112 703 160 118 081 832 230 784 992

Loss for the year - (114 672 879) (114 672 879)Other comprehensive income - - -

Total comprehensive Loss for the year - (114 672 879) (114 672 879)

Balance at 31 March 2019 112 703 160 3 408 953 116 112 113

Note 10

13

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Statement of Cash Flows2019 2018

Note(s) R R

Cash flows from continuing operating activities

Cash used in operations 19 4 759 684 (236 344 708)

Tax (paid) received 17 805 257 (2 982 048)

Discontinued operations (1 787 890 148) 65 136 444

Net cash from continuing operating activities (1 765 325 207) (174 190 312)

Cash flows from investing activities

Purchase of property, plant and equipment 3 (39 949) (48 075)

Net proceeds (payments) on sale of property, plant and equipment 3 91 813 (71 958)

Net cash from continuing investing activities 51 864 (120 033)

Cash flows from financing activities

Proceeds from loans from group companies 3 117 609 701 118 000

Repayment of loans from group companies (451 045 319) (22 465 754)

Repayment of financial instruments (313 678 695) -

Proceeds on swap agreement 344 588 263 210 837 218

Net cash from continuing financing activities (417 098 142) 889 489 464

Total cash movement for the year (2 182 371 485) 715 179 119

Cash at the beginning of the year 2 240 224 258 1 525 045 139

Total cash at end of the year 5 57 852 773 2 240 224 258

14

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1. Significant accounting policies

The principal accounting policies applied in the preparation of these annual financial statements are set out below.

1.1 Basis of preparation

The annual financial statements have been prepared in accordance with, and in compliance with International FinancialReporting Standards ("IFRS") and International Financial Reporting Standards Committee ("IFRS") interpretations issuedand effective at the time of preparing these annual financial statements and the Companies Act 71 of 2008 of SouthAfrica, as amended.

These annual financial statements comply with the requirements of the SAICA Financial Reporting Guides as issued bythe Accounting Practices Committee and the Financial Reporting Pronouncements as issued by the Financial ReportingStandards Council.

The annual financial statements have been prepared on the historic cost convention except for the statement of cashflows which is prepared on a cash basis, and incorporate the principal accounting policies set out below. They arepresented in Rands, which is the company's functional currency.

These accounting policies are consistent with the previous period, apart from standards that became effective and wereimplemented in the year under review.

1.2 Significant judgements and sources of estimation uncertainty

The preparation of annual financial statements in conformity with IFRS requires management, from time to time, to makejudgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities,income and expenses. These estimates and associated assumptions are based on experience and various other factorsthat are believed to be reasonable under the circumstances. Actual results may differ from these estimates. Theestimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates arerecognised in the period in which the estimates are revised and in any future periods affected. Significant judgementsinclude:

Advances, held to maturity investments and other receivables

The company assesses its advances, held to maturity investments and other receivables for impairment at the end ofeach reporting period. In determining whether an impairment loss should be recorded in profit or loss, the companymakes judgements as to whether there is observable data indicating a measurable decrease in the estimated future cashflows from a financial asset.

The specific impairment is calculated by considering all loans that are categorised as bad (greater than 90 days inarrears). Each advance is then scrutinised to determine whether impairment is required by assessing the future cashflows against the current carrying value of the financial asset. Where the future recoverable cash balance is not sufficientto cover the current carrying value as at year end and impairment will be recognised.

The portfolio impairment is calculated based on the guidance from Bank of Baroda Head Office who annually reviews thatallocated percentage of portfolio impairments which is applied by the company as a standard provision against all loansand advances, held to maturity investments and other receivables.

The impairment for advances, held to maturity investments and other receivables is calculated on a portfolio basis. Referto Note 6 for further details on impairment allowance.

15

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1.2 Significant judgements and sources of estimation uncertainty (continued)

Taxation

Judgement is required in determining the provision for income taxes due to the complexity of legislation. There are manytransactions and calculations for which the ultimate tax determination is uncertain during the ordinary course of business.The company recognises liabilities for anticipated tax audit issues based on estimates of whether additional taxes will bedue. Where the final tax outcome of these matters is different from the amounts that were initially recorded, suchdifferences will impact the income tax and deferred tax provisions in the period in which such determination is made.

The company recognises the net future tax benefit related to deferred income tax assets to the extent that it is probablethat the deductible temporary differences will reverse in the foreseeable future. Assessing the recoverability of deferredincome tax assets requires the company to make significant estimates related to expectations of future taxable income.Estimates of future taxable income are based on forecast cash flows from operations and the application of existing taxlaws in each jurisdiction. To the extent that future cash flows and taxable income differ significantly from estimates, theability of the company to realise the net deferred tax assets recorded at the end of the reporting period could be impacted.

1.3 Property, plant and equipment

The cost of an item of property, plant and equipment is recognised as an asset when:• it is probable that future economic benefits associated with the item will flow to the company; and• the cost of the item can be measured reliably.

Property, plant and equipment is initially measured at cost.

Costs include costs incurred initially to acquire an item of property, plant and equipment and costs incurred subsequentlyto add to, replace part of, or service it. If a replacement cost is recognised in the carrying amount of an item of property,plant and equipment, the carrying amount of the replaced part is derecognised.

Property, plant and equipment is being depreciated over their expected useful lives to their estimated residual value.

Property, plant and equipment is carried at cost less accumulated depreciation and any impairment losses.

The useful lives of items of property, plant and equipment have been assessed as follows:

Item Average useful life

Furniture and fixtures 18%Motor vehicles 25%IT equipment 33%

The residual value, useful life and depreciation method of each asset are reviewed at the end of each reporting period. Ifthe expectations differ from previous estimates, the change is accounted for as a change in accounting estimate.

The gain or loss arising from the derecognition of an item of property, plant and equipment is included in profit or losswhen the item is derecognised. The gain or loss arising from the derecognition of an item of property, plant andequipment is determined as the difference between the net disposal proceeds, if any, and the carrying amount of the item.

16

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1.4 Financial instruments

Classification

The company classifies financial assets and financial liabilities into the following categories: Held-to-maturity investment Loans and receivables measured at amortised costs Financial liabilities measured at amortised cost

Classification depends on the purpose for which the financial instruments were obtained / incurred and takes place atinitial recognition.

Initial recognition and measurement

Financial instruments are recognised initially when the company becomes a party to the contractual provisions of theinstruments.

The company classifies financial instruments, or their component parts, on initial recognition as a financial asset, afinancial liability or an equity instrument in accordance with the substance of the contractual arrangement.

Financial instruments are measured initially at fair value, except for equity investments for which a fair value is notdeterminable, which are measured at cost and are classified as available-for-sale financial assets.

For financial instruments which are not at fair value through profit or loss, transaction costs are included in the initialmeasurement of the instrument.

Transaction costs on financial instruments at fair value through profit or loss are recognised in profit or loss.

Subsequent measurement

Loans and receivables are subsequently measured at amortised cost, using the effective interest method, lessaccumulated impairment losses.

Held-to-maturity investments are subsequently measured at amortised cost, using the effective interest method, lessaccumulated impairment losses.

Financial liabilities at amortised cost are subsequently measured at amortised cost, using the effective interest method.

Derecognition

Financial assets are derecognised when the rights to receive cash flows from the investments have expired or have beentransferred and the company has transferred substantially all risks and rewards of ownership.

Loans to (from) group branches

These include loans to and from holding companies, fellow branches and associates and are recognised initially at fairvalue plus direct transaction costs.

Loans to group companies are classified as loans and receivables, and are subsequently measured at amortised cost.

Loans from group companies are classified as financial liabilities, and are subsequently measured at amortised cost.

Loans to shareholders, directors, managers and employees

These financial assets are classified as loans and receivables, and are subsequently measured at amortised cost.

17

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1.4 Financial instruments (continued)

Advances, loans and other receivables

Trade and other receivables are classified as loans, advances and other receivables and are subsequently measured atamortised cost.

Financial assets carried at amortised cost are impaired if the asset is considered to be a non-performing asset, which is aresult of non-payment of contractually agreed installment and obligatory interest beyond 90 days.

Impairments are accounted on non-performing assets which are carried against the carrying value of the financial assets.Loans together with the associated allowance are written off when there is no realistic prospect of future recovery and allcollateral has been realised or transferred to the Company.

An allowance for non-performing assets are only reversed when there is objective evidence that the credit quality hasimproved to the extent that there is reasonable assurance of timely collection of principal and interest in terms of theoriginal contractual agreement.

Provisions or impairments of non-performing financial assets held at amortised cost are recognised in profit and loss.

At each reporting date the company assesses all financial assets, to determine whether there is objective evidence that afinancial asset or group of financial assets has been impaired.

Where financial assets are impaired through use of an allowance account, the amount of the loss is recognised in profit orloss within operating expenses. When such assets are written off, the write off is made against the relevant allowanceaccount. Subsequent recoveries of amounts previously written off are credited against operating expenses in profit orloss.

Deposits, borrowings and other payables

Deposits, borrowings and other payables are initially measured at fair value, and are subsequently measured at amortisedcost, using the effective interest rate method.

Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand deposits, and other short-term highly liquid investmentsthat are readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value. Theseare initially recorded at fair value, and subsequently measured at amortised cost.

Bank overdraft and borrowings

Bank overdrafts and borrowings are initially measured at fair value, and are subsequently measured at amortised cost,using the effective interest rate method. Any difference between the proceeds (net of transaction costs) and thesettlement or redemption of borrowings is recognised over the term of the borrowings in accordance with the company’saccounting policy for borrowing costs.

Held to maturity

These financial assets are initially measured at fair value plus direct transaction costs.

At subsequent reporting dates these are measured at amortised cost using the effective interest rate method, less anyimpairment loss recognised to reflect irrecoverable amounts.

Financial assets including placements with other banks and term loans included in advances and other receivables, aswell as government treasury bills included in other financial assets, that the company has the positive intention and abilityto hold to maturity have been classified as held to maturity.

18

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1.5 Tax

Current tax assets and liabilities

Current tax for current and prior periods is, to the extent unpaid, recognised as a liability. If the amount already paid inrespect of current and prior periods exceeds the amount due for those periods, the excess is recognised as an asset.

Current tax liabilities (assets) for the current and prior periods are measured at the amount expected to be paid to(recovered from) the tax authorities, using the tax rates (and tax laws) that have been enacted or substantively enacted bythe end of the reporting period.

Deferred tax assets and liabilities

A deferred tax liability is recognised for all taxable temporary differences, except to the extent that the deferred tax liabilityarises from the initial recognition of an asset or liability in a transaction which at the time of the transaction, affects neitheraccounting profit nor taxable profit (tax loss).

A deferred tax asset is recognised for all deductible temporary differences to the extent that it is probable that taxableprofit will be available against which the deductible temporary difference can be utilised. A deferred tax asset is notrecognised when it arises from the initial recognition of an asset or liability in a transaction at the time of the transaction,affects neither accounting profit nor taxable profit (tax loss).

A deferred tax asset is recognised for the carry forward of unused tax losses to the extent that it is probable that futuretaxable profit will be available against which the unused tax losses can be utilised.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset isrealised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted by theend of the reporting period.

Tax expenses

Current and deferred taxes are recognised as income or an expense and included in profit or loss for the period, except tothe extent that the tax arises from: a transaction or event which is recognised, in the same or a different period, to other comprehensive income, or a business combination.

Current tax and deferred taxes are charged or credited to other comprehensive income if the tax relates to items that arecredited or charged, in the same or a different period, to other comprehensive income.

Current tax and deferred taxes are charged or credited directly to equity if the tax relates to items that are credited orcharged, in the same or a different period, directly in equity.

1.6 Leases

A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. Alease is classified as an operating lease if it does not transfer substantially all the risks and rewards incidental toownership.

Operating leases – lessee

Operating lease payments are recognised as an expense on a straight-line basis over the lease term. The differencebetween the amounts recognised as an expense and the contractual payments are recognised as an operating leaseasset. This liability is not discounted.

Any contingent rents are expensed in the period they are incurred.

19

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1.7 Non-current assets held for sale

Non-current assets are classified as held for sale if their carrying amount will be recovered through a sale transactionrather than through continuing use. This condition is regarded as met only when the sale is highly probable and the assetis available for immediate sale in its present condition. Management must be committed to the sale, which should beexpected to qualify for recognition as a completed sale within one year from the date of classification.

Non-current assets held for sale are measured at the lower of its carrying amount and fair value less costs to sell.

A non-current asset is not depreciated (or amortised) while it is classified as held for sale, or while it is part of a disposalgroup classified as held for sale.

1.8 Impairment of non-financial assets

The company assesses at each end of the reporting period whether there is any indication that an asset may be impaired.If any such indication exists, the company estimates the recoverable amount of the asset.

If there is any indication that an asset may be impaired, the recoverable amount is estimated for the individual asset. If itis not possible to estimate the recoverable amount of the individual asset, the recoverable amount of the cash-generatingunit to which the asset belongs is determined.

The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs to sell and its valuein use.

If the recoverable amount of an asset is less than its carrying amount, the carrying amount of the asset is reduced to itsrecoverable amount. That reduction is an impairment loss.

An impairment loss is recognised for cash-generating units if the recoverable amount of the unit is less than the carryingamount of the units. The impairment loss is allocated to reduce the carrying amount of the assets of the unit, pro rata onthe basis of the carrying amount of each asset in the unit.

1.9 Share capital and equity

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of itsliabilities.

Equity capital reflects the assigned capital from the Company's Head Office in India.

1.10 Employee benefits

Short-term employee benefits

The cost of short-term employee benefits, (those payable within 12 months after the service is rendered, such as paidvacation leave and sick leave, bonuses, and non-monetary benefits such as medical care), are recognised in the period inwhich the service is rendered and are not discounted.

The expected cost of compensated absences is recognised as an expense as the employees render services thatincrease their entitlement or, in the case of non-accumulating absences, when the absence occurs.

The expected cost of profit sharing and bonus payments is recognised as an expense when there is a legal orconstructive obligation to make such payments as a result of past performance.

1.11 Provisions and contingencies

Provisions are recognised when: the company has a present obligation as a result of a past event; it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation; and a reliable estimate can be made of the obligation.

The amount of a provision is the present value of the expenditure expected to be required to settle the obligation.

20

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Accounting Policies

1.11 Provisions and contingencies (continued)

Provisions are not recognised for future operating losses.

Contingent assets and contingent liabilities are not recognised in the statement of financial position. Contingenciesinclude the issue of letters of credit and guarantees to clients.

1.12 Revenue

Revenue consists of interest income, fee and commission income, investment income arising from customer operation,investment income arising from balance sheet management and other trading activities and other operating income.

Revenue is recognised when it can be reliably measured and it is probable that the economic benefits will flow to theentity. Revenue related to provision of services is recognised when the related services are performed. Revenue ismeasured at the fair value of the consideration received or receivable.

Interest income is recognised in profit or loss using the effective interest method. Fees charged on lending transactionsare included in the effective yield calculation to the extent that they form an integral part of the effective interest rate yield,but exclude those fees earned for a separately identifiable significant act,which are recognised upon completion of theact. Fees and commissions charged are recognised as non-interest income.

The effective interest method is based on the estimated life of the underlying instrument and, where this estimate is notreadily available, the contractual life.

Fee and commission income includes fees earned from providing advisory services as well as portfolio management.

1.13 Borrowing costs

All borrowing costs on deposits are recognised through profit and loss in the statement of comprehensive income as anexpense using the effective interest rate method in the period in which they are incurred.

1.14 Translation of foreign currencies

Foreign currency transactions

The presentation currency of the Bank is South African Rands, being the functional currency of the Company.

A foreign currency transaction is recorded, on initial recognition in Rands, by applying to the foreign currency amount thespot exchange rate between the functional currency and the foreign currency at the date of the transaction.

At the end of the reporting period: foreign currency monetary items are translated using the closing rate; non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the

exchange rate at the date of the transaction; and non-monetary items that are measured at fair value in a foreign currency are translated using the exchange rates at

the date when the fair value was determined.

Exchange differences arising on the settlement of monetary items or on translating monetary items at rates different fromthose at which they were translated on initial recognition during the period or in previous annual financial statements arerecognised in profit or loss in the period in which they arise.

Cash flows arising from transactions in a foreign currency are recorded in Rands by applying to the foreign currencyamount the exchange rate between the Rand and the foreign currency at the date of the cash flow.

1.15 Statement of cash flows

The statement of cash flows are prepared using the indirect method.

21

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements2019 2018

R R

2. New Standards and Interpretations

2.1 Standards and interpretations effective and adopted in the current year

In the current year, the company has the following standards and interpretations that are effective for the current financialyear and that are relevant to its operations:

IFRS 9 Financial Instruments

IFRS 9 issued in November 2009 introduced new requirements for the classification and measurements of financialassets. IFRS 9 was subsequently amended in October 2010 to include requirements for the classification andmeasurement of financial liabilities and for derecognition, and in November 2013 to include the new requirements forgeneral hedge accounting. Another revised version of IFRS 9 was issued in July 2014 mainly to include a)impairmentrequirements for financial assets and b) limited amendments to the classification and measurement requirements byintroducing a "fair value through other comprehensive income" (FVTOCI) measurement category for certain simple debtinstruments.

Key requirements of IFRS 9: All recognised financial assets that are within the scope of IAS 39 Financial Instruments: Recognition and

Measurement are required to be subsequently measured at amortised cost or fair value. Specifically, debtinvestments that are held within a business model whose objective is to collect the contractual cash flows, and thathave contractual cash flows that are solely payments of principal and interest on the outstanding principal aregenerally measured at amortised cost at the end of subsequent reporting periods. Debt instruments that are heldwithin a business model whose objective is achieved by both collecting contractual cash flows and selling financialassets, and that have contractual terms of the financial asset give rise on specified dates to cash flows that aresolely payments of principal and interest on outstanding principal, are measured at FVTOCI. All other debt andequity investments are measured at fair value at the end of subsequent reporting periods. In addition, under IFRS 9,entities may make an irrevocable election to present subsequent changes in the fair value of an equity investment(that is not held for trading) in other comprehensive income with only dividend income generally recognised in profitor loss.

With regard to the measurement of financial liabilities designated as at fair value through profit or loss, IFRS 9requires that the amount of change in the fair value of the financial liability that is attributable to changes in the creditrisk of the liability is presented in other comprehensive income, unless the recognition of the effect of the changes ofthe liability's credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit orloss. Under IAS 39, the entire amount of the change in fair value of a financial liability designated as at fair valuethrough profit or loss is presented in profit or loss.

In relation to the impairment of financial assets, IFRS 9 requires an expected credit loss model, as opposed to anincurred credit loss model under IAS 39. The expected credit loss model requires an entity to account for expectedcredit losses and changes in those expected credit losses at each reporting date to reflect changes in credit risksince initial recognition. It is therefore no longer necessary for a credit event to have occurred before credit lossesare recognised.

The effective date of the standard is for years beginning on or after 01 January 2018.

Management of the bank has not undertaken the IFRS 9 exercise as the bank is in the process of winding down it'soperations and had the bank undertook the IFRS 9 exercise, there would not be any material impact on the annualfinancial statements.

IFRS 15 Revenue from Contracts with Customers

IFRS 15 supersedes IAS 11 Construction contracts; IAS 18 Revenue; IFRIC 13 Customer Loyalty Programmes; IFRIC 15Agreements for the construction of Real Estate; IFRIC 18 Transfers of Assets from Customers and SIC 31 Revenue -Barter Transactions Involving Advertising Services.

22

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

2. New Standards and Interpretations (continued)

The core principle of IFRS 15 is that an entity recognises revenue to depict the transfer of promised goods or services tocustomers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for thosegoods or services. An entity recognises revenue in accordance with that core principle by applying the following steps:

Identify the contract(s) with a customer

Identify the performance obligations in the contract

Determine the transaction price

Allocate the transaction price to the performance obligations in the contract

Recognise revenue when (or as) the entity satisfies a performance obligation.

IFRS 15 also includes extensive new disclosure requirements.

The effective date of the standard is for years beginning on or after 01 January 2018.

The company has adopted the standard for the first time in the 2019 annual financial statements.

Amendments to IFRS 15: Clarifications to IFRS 15 Revenue from Contracts with Customers

The amendment provides clarification and further guidance regarding certain issues in IFRS 15. These items includeguidance in assessing whether promises to transfer goods or services are separately identifiable; guidance regardingagent versus principal considerations; and guidance regarding licenses and royalties.The effective date of the amendment is for years beginning on or after 01 January 2018.The company has adopted the amendment for the first time in the 2019 annual financial statements.

2.2 Standards and interpretations not yet effective

The company has chosen not to early adopt the following standards and interpretations, which have been published andare mandatory for the company’s accounting periods beginning on or after 01 April 2019 or later periods:

IFRS 16 Leases

IFRS 16 Leases is a new standard which replaces IAS 17 Leases, and introduces a single lessee accounting model. Themain changes arising from the issue of IFRS 16 which are likely to impact the company are as follows:

Company as lessee: Lessees are required to recognise a right-of-use asset and a lease liability for all leases, except short term leases or

leases where the underlying asset has a low value, which are expensed on a straight line or other systematic basis. The cost of the right-of-use asset includes, where appropriate, the initial amount of the lease liability; lease

payments made prior to commencement of the lease less incentives received; initial direct costs of the lessee; andan estimate for any provision for dismantling, restoration and removal related to the underlying asset.

The lease liability takes into consideration, where appropriate, fixed and variable lease payments; residual valueguarantees to be made by the lessee; exercise price of purchase options; and payments of penalties for terminatingthe lease.

The right-of-use asset is subsequently measured on the cost model at cost less accumulated depreciation andimpairment and adjusted for any re-measurement of the lease liability. However, right-of-use assets are measured atfair value when they meet the definition of investment property and all other investment property is accounted for onthe fair value model. If a right-of-use asset relates to a class of property, plant and equipment which is measured onthe revaluation model, then that right-of-use asset may be measured on the revaluation model.

The lease liability is subsequently increased by interest, reduced by lease payments and re-measured forreassessments or modifications.

Re-measurements of lease liabilities are affected against right-of-use assets, unless the assets have been reducedto nil, in which case further adjustments are recognised in profit or loss.

The lease liability is re-measured by discounting revised payments at a revised rate when there is a change in thelease term or a change in the assessment of an option to purchase the underlying asset.

23

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

2. New Standards and Interpretations (continued) The lease liability is re-measured by discounting revised lease payments at the original discount rate when there is a

change in the amounts expected to be paid in a residual value guarantee or when there is a change in futurepayments because of a change in index or rate used to determine those payments.

Certain lease modifications are accounted for as separate leases. When lease modifications which decrease thescope of the lease are not required to be accounted for as separate leases, then the lessee re-measures the leaseliability by decreasing the carrying amount of the right of lease asset to reflect the full or partial termination of thelease. Any gain or loss relating to the full or partial termination of the lease is recognised in profit or loss. For allother lease modifications which are not required to be accounted for as separate leases, the lessee re-measures thelease liability by making a corresponding adjustment to the right-of-use asset.

Right-of-use assets and lease liabilities should be presented separately from other assets and liabilities. If not, thenthe line item in which they are included must be disclosed. This does not apply to right-of-use assets meeting thedefinition of investment property which must be presented within investment property. IFRS 16 contains differentdisclosure requirements compared to IAS 17 leases.

The effective date of the standard is for years beginning on or after 01 January 2019.

The company expects to adopt the standard for the first time in the 2020 annual financial statements.

It is unlikely that the standard will have a material impact on the company's annual financial statements.

24

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

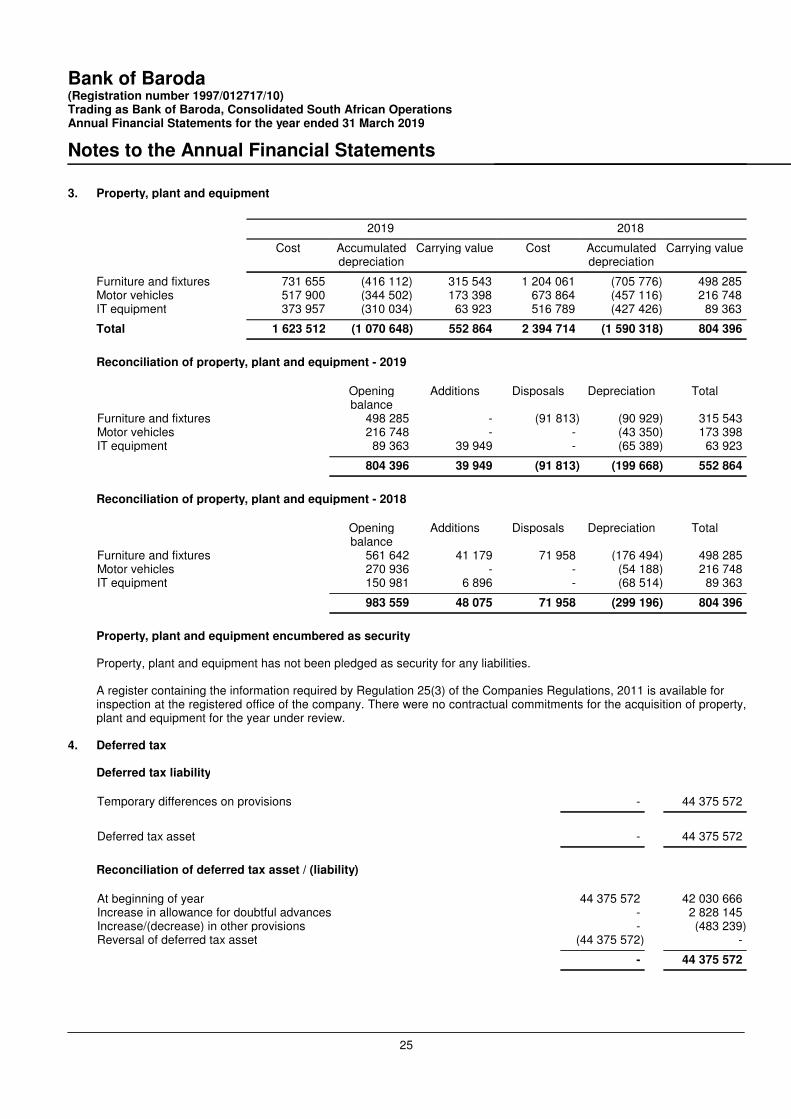

3. Property, plant and equipment

2019 2018

Cost Accumulateddepreciation

Carrying value Cost Accumulateddepreciation

Carrying value

Furniture and fixtures 731 655 (416 112) 315 543 1 204 061 (705 776) 498 285Motor vehicles 517 900 (344 502) 173 398 673 864 (457 116) 216 748IT equipment 373 957 (310 034) 63 923 516 789 (427 426) 89 363

Total 1 623 512 (1 070 648) 552 864 2 394 714 (1 590 318) 804 396

Reconciliation of property, plant and equipment - 2019

Openingbalance

Additions Disposals Depreciation Total

Furniture and fixtures 498 285 - (91 813) (90 929) 315 543Motor vehicles 216 748 - - (43 350) 173 398IT equipment 89 363 39 949 - (65 389) 63 923

804 396 39 949 (91 813) (199 668) 552 864

Reconciliation of property, plant and equipment - 2018

Openingbalance

Additions Disposals Depreciation Total

Furniture and fixtures 561 642 41 179 71 958 (176 494) 498 285Motor vehicles 270 936 - - (54 188) 216 748IT equipment 150 981 6 896 - (68 514) 89 363

983 559 48 075 71 958 (299 196) 804 396

Property, plant and equipment encumbered as security

Property, plant and equipment has not been pledged as security for any liabilities.

A register containing the information required by Regulation 25(3) of the Companies Regulations, 2011 is available forinspection at the registered office of the company. There were no contractual commitments for the acquisition of property,plant and equipment for the year under review.

4. Deferred tax

Deferred tax liability

Temporary differences on provisions - 44 375 572

Deferred tax asset - 44 375 572

Reconciliation of deferred tax asset / (liability)

At beginning of year 44 375 572 42 030 666Increase in allowance for doubtful advances - 2 828 145Increase/(decrease) in other provisions - (483 239)Reversal of deferred tax asset (44 375 572) -

- 44 375 572

25

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

4. Deferred tax (continued)

Reversal of deferred tax asset

In the current financial year the deferred tax asset was reversed due to the Bank not being able to generate sufficienteconomic benefits to utilise the deferred tax asset in the forseeable future. This is based on the knowledge that the entityis winding down and in the process of transferring the income-generating assets or providing for the losses thereof due toit being non-performing assets.

5. Cash and cash equivalents

Cash and cash equivalents consist of:

Cash on hand 1 610 20 420Operational bank balances and current accounts 7 758 954 35 314 366Placements with other financial institutions 17 092 209 2 068 389 472Balances held with the South African Reserve Bank 33 000 000 136 500 000

57 852 773 2 240 224 258

Credit quality of cash at bank and short term deposits, excluding cash on hand

The credit quality of cash at bank and short term deposits, excluding cash on hand that are neither past due nor impairedcan be assessed by reference to external credit ratings. As there have been no defaults in the previous financial periods,the credit quality of these cash and cash equivalents are considered high.

Fair value of cash and cash equivalents

The fair value of cash and cash equivalents approximates the carrying value of the cash and cash equivalents due to theshort term nature thereof.

6. Advances and other receivables

Other receivables 135 632 271 293Deposits 250 000 37 510Advances and other receivables 4 970 421 -

5 356 053 308 803

Credit quality of advances and other receivables

The credit quality of trade and other receivables that are neither past nor due nor impaired can be assessed by referenceto external credit ratings (if available) or to historical information about counterparty default rates:

Credit rating

High 5 356 053 308 803

Credit risk relating to advances and other receivables are detailed in Note 25 of the annual financial statements.

None of the financial assets that are fully performing have been renegotiated in the last year.

7. Other financial assets

Held to maturity investment

Governmental treasury billsThe other financial assets consist of South African government treasurybills with a maturity date shorter than 12 months.

- 44 651 446

26

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

7. Other financial assets (continued)

Loans and receivables

Swap assetsDuring the year under review the entity entered into a swap agreement tothe value of USD 23 550 000 with the State Bank of India at an exchangerate of R14,45. On maturity date, the bank is obliged to repay the amountat an exchange rate of R14,60. The maturity date is on 24 May 2019.

341 427 900 -

Total other financial assets 341 427 900 44 651 446

Current assetsHeld to maturity - 44 651 446Loans and receivables 341 427 900 -

341 427 900 44 651 446

Held to maturity investments past due but not impaired

Held to maturity investments which are less than 3 months past due are not considered to be impaired. There were noinvestments past due or impaired.

Held to maturity financial assets are denominated in South African Rand.

Fair value of held to maturity investments

There were no gains or losses realised on the disposal of held to maturity financial assets in 2019 and 2018, as all thefinancial assets were disposed of at their redemption date.

The fair value of the other financial assets equal its carrying value due to the short term nature thereof.

Credit quality of other financial assets

The credit quality of financial assets that are neither past due nor impaired can be assessed by reference to externalcredit ratings (if available) or to historical information about counterparty default rates. As there have been no defaults inthe previous financial periods, the credit quality of these other financial assets are considered high.

Held to maturity instruments

Credit ratingHigh - 44 651 446

Loans and receivables

Credit ratingHigh 341 427 900 -

8. Loans to (from) group companies

Loans from fellow branches

Singapore branchThe loan of 8 million USD, bears interest at 2.55%, is repayable on 14June 2018 and is unsecured.

- (93 482 400)

27

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

8. Loans to (from) group companies (continued)

Loans from holding company

Bank of Baroda India - TreasuryThe loan of 60 million USD is unsecured, bears interest at 2.65%, matureson 09 April 2018.

- (701 118 000)

Bank of Baroda India - TreasuryThe loan of 60 million USD is unsecured, bears interest at 3.15%, matureson 25 May 2019.

(343 602 600) -

(343 602 600) (701 118 000)

Loans to fellow branches

Mumbai branch - 29 824Brussels branch - 52 599New York branch - 2 985 452London branch - 2 215

- 3 070 090

The above loans are interest free, unsecured and have no fixed repaymentterms.

Current assets - 3 117 609Current liabilities (343 602 600) (794 647 919)

(343 602 600) (791 530 310)

Credit quality of loans to group companies

The credit quality of loans with group branches with foreign operations that are neither past due nor impaired can beassessed by reference to external credit ratings (if available) or to historical information about counterparty default rates.As the loans to group branches have not previously defaulted the credit rating is considered to be high.

Fair value of loans to and from group companies

Due to the short term nature of the loans with group companies its carrying value approximates its fair value.

Loans with group companies impaired

As of 31 March 2019, there were no loans with group companies impaired and provided for.

The carrying amount of loans to and from group companies with foreign operations are denominated in US Dollar, Euro,Pound Sterling and Indian Rupee.

28

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

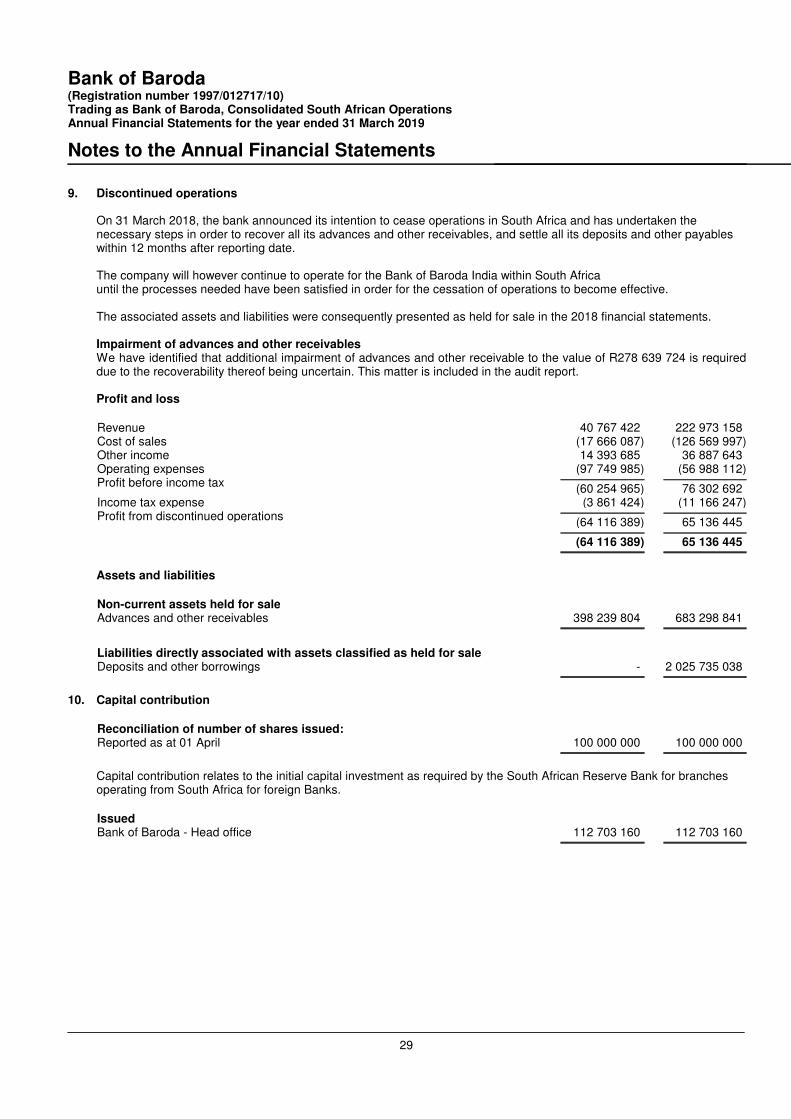

9. Discontinued operations

On 31 March 2018, the bank announced its intention to cease operations in South Africa and has undertaken thenecessary steps in order to recover all its advances and other receivables, and settle all its deposits and other payableswithin 12 months after reporting date.

The company will however continue to operate for the Bank of Baroda India within South Africauntil the processes needed have been satisfied in order for the cessation of operations to become effective.

The associated assets and liabilities were consequently presented as held for sale in the 2018 financial statements.

Impairment of advances and other receivablesWe have identified that additional impairment of advances and other receivable to the value of R278 639 724 is requireddue to the recoverability thereof being uncertain. This matter is included in the audit report.

Profit and loss

Revenue 40 767 422 222 973 158Cost of sales (17 666 087) (126 569 997)Other income 14 393 685 36 887 643Operating expenses (97 749 985) (56 988 112)Profit before income tax

(60 254 965) 76 302 692Income tax expense (3 861 424) (11 166 247)Profit from discontinued operations

(64 116 389) 65 136 445

(64 116 389) 65 136 445

Assets and liabilities

Non-current assets held for saleAdvances and other receivables 398 239 804 683 298 841

Liabilities directly associated with assets classified as held for saleDeposits and other borrowings - 2 025 735 038

10. Capital contribution

Reconciliation of number of shares issued:Reported as at 01 April 100 000 000 100 000 000

Capital contribution relates to the initial capital investment as required by the South African Reserve Bank for branchesoperating from South Africa for foreign Banks.

IssuedBank of Baroda - Head office 112 703 160 112 703 160

29

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

11. Deposits and other borrowings

Current accounts with other banks - 3 371Provision for legal fees - 1 500 000Accrued expense 638 722 788 495Sundry deposits - 265 698

638 722 2 557 564

Fair value of deposits and other borrowings

The fair value of the deposits and other borrowings equal its carrying value due to the short term nature thereof.

The carrying amounts of deposits and other borrowings are denominated in South African Rand.

12. Other financial liabilities

Unclaimed deposits 584 063 -

Swap liabilityDuring the year under review the entity entered into a swap agreement tothe value of USD 23 550 000 with the State Bank of India at an exchangerate of R14,45. On maturity date, the bank is obliged to repay the amountat an exchange rate of R14,60. The maturity date is on 24 May 2019.Refer to Note 9.

343 924 200 -

344 508 263 -

Current liabilitiesAt amortised cost 344 508 263 -

13. Financial assets by category

The accounting policies for financial instruments have been applied to the line items below:

2019

Loans andreceivables

Held tomaturity

investments

Total

Advances and other receivables 5 356 053 - 5 356 053Cash and cash equivalents 57 852 773 - 57 852 773

63 208 826 - 63 208 826

2018

Loans andreceivables

Held tomaturity

investments

Total

Advances and other receivables 308 803 - 308 803Other financial assets - 44 651 446 44 651 446Loans with group branches 3 117 609 - 3 117 609Cash and cash equivalents 2 240 224 258 - 2 240 224 258Interest income receivable 22 104 891 - 22 104 891

2 265 755 561 44 651 446 2 310 407 007

30

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

14. Financial liabilities by category

The accounting policies for financial instruments have been applied to the line items below:

2019

Financialliabilities at

amortised cost

Total

Loans from group branches 343 602 600 343 602 600Interest payable 439 673 439 673

344 042 273 344 042 273

2018

Financialliabilities at

amortised cost

Total

Loans from group branches 794 647 919 794 647 919Interest payable 1 295 644 1 295 644Deposits and other borrowings 269 069 269 069

796 212 632 796 212 632

15. Other operating income

Other recoveries 43 200 -Sundry income 2 401 909 60 538

2 445 109 60 538

16. Other operating gains (losses)

Foreign exchange gains (losses)Net foreign exchange gains (losses) 969 827 (3 297 408)

17. Operating profit (loss)

Operating loss for the year is stated after charging (crediting) the following, amongst others:

Auditor's remuneration - externalAudit fees 690 815 1 453 697

Employee costs

Salaries, wages, bonuses and other benefits 7 924 312 5 647 150

Leases

Operating lease chargesPremises 1 661 813 3 075 375

DepreciationDepreciation 199 667 299 196

31

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

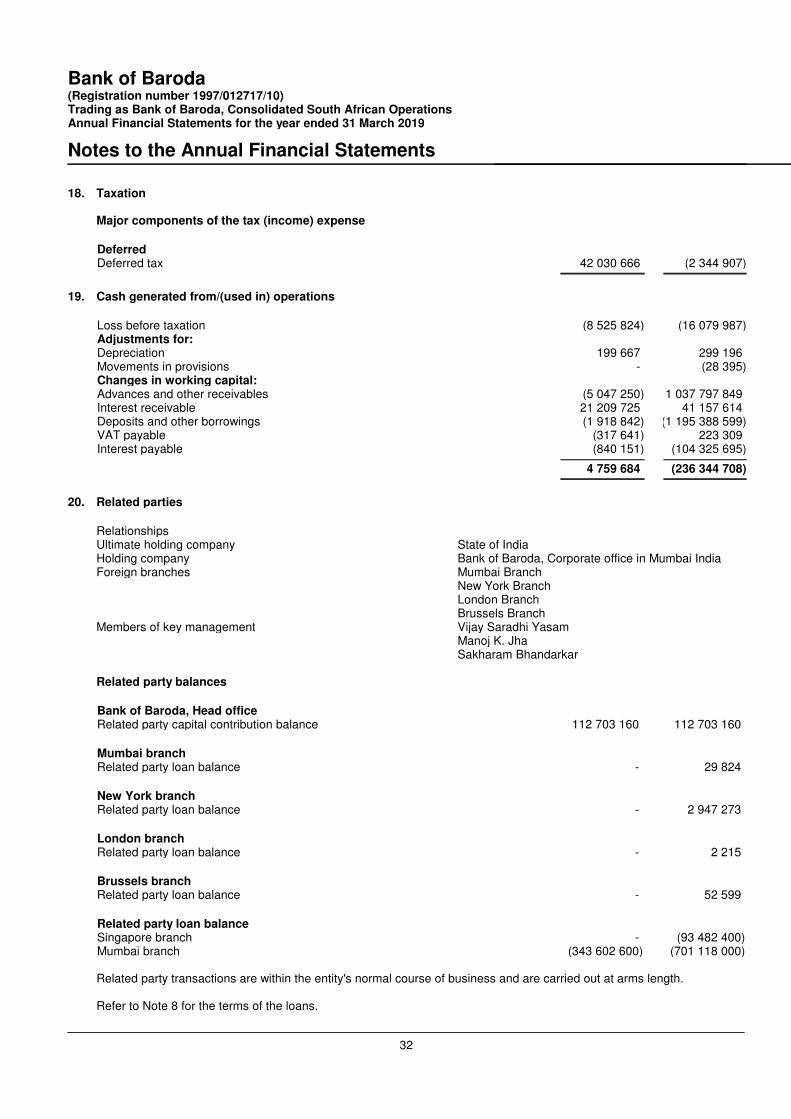

18. Taxation

Major components of the tax (income) expense

DeferredDeferred tax 42 030 666 (2 344 907)

19. Cash generated from/(used in) operations

Loss before taxation (8 525 824) (16 079 987)Adjustments for:Depreciation 199 667 299 196Movements in provisions - (28 395)Changes in working capital:Advances and other receivables (5 047 250) 1 037 797 849Interest receivable 21 209 725 41 157 614Deposits and other borrowings (1 918 842) (1 195 388 599)VAT payable (317 641) 223 309Interest payable (840 151) (104 325 695)

4 759 684 (236 344 708)

20. Related parties

`

RelationshipsUltimate holding company State of IndiaHolding company Bank of Baroda, Corporate office in Mumbai IndiaForeign branches Mumbai Branch

New York Branch London Branch Brussels Branch

Members of key management Vijay Saradhi YasamManoj K. JhaSakharam Bhandarkar

Related party balances

Bank of Baroda, Head officeRelated party capital contribution balance 112 703 160 112 703 160

Mumbai branchRelated party loan balance - 29 824

New York branchRelated party loan balance - 2 947 273

London branchRelated party loan balance - 2 215

Brussels branchRelated party loan balance - 52 599

Related party loan balanceSingapore branch - (93 482 400)Mumbai branch (343 602 600) (701 118 000)

Related party transactions are within the entity's normal course of business and are carried out at arms length.

Refer to Note 8 for the terms of the loans.

32

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

21. Directors' emoluments

Executive

2019

Services to thecompany

Pension paidor payable

Total

Manoj Kumar Jha 368 653 14 202 382 855Vijay Saradhi Yasam 255 755 8 576 264 331Sakharam Bhandarkar 255 755 11 099 266 854

880 163 33 877 914 040

2018

Services to thecompany

Pension paidor payable

Total

Manoj Kumar Jha 435 147 14 148 449 295

33

Bank of Baroda(Registration number 1997/012717/10)Trading as Bank of Baroda, Consolidated South African OperationsAnnual Financial Statements for the year ended 31 March 2019

Notes to the Annual Financial Statements

22. Risk management

Capital risk management