Embed Size (px)

Citation preview

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Annual Financial Report

As of and for the year ended June 30, 2013

Watervi'orks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Annual Financial Statements As of and for the year ended June 30, 2013

Table of Contents

Page

INDEPENDENT AUDITOR'S REPORT 1 - 2

REQUIRED SUPPLEMENTARY INFORMATION (UNAUDITED)

Managements' Discussion and Analysis 3 - 5

BASIC FINANCIAL STATEMENTS

Proprietary Fund Statements -Statements of Net P'osition 6

Statements of Revenues. Hxpenses and Changes in

Net Position 7

Statements of Cash Flows 8

Notes to the Financial Statements 9 - 16

REPORTS REQUIRED BY GOVERNMENT AUDITING STANDARDS

INDHPENDENT AUi:)l lOR'S REPORT ON IN lERNAL CON 1 ROE OVER FINANCIAE REPORFING AND ON COMPEIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL s I ATEMF:N rs PERFORMED IN ACCORDANCE wi i H

G()lTJ<\Mh\\r AUDITJNG STANDARDS 17-18

Schedule of Findings 19

Schedule of Prior Year Findings 20

W. Kathleen Beards CPAy LLC 10191 BuecheRd, Bueche^LA 70729

Member: Email: Kbeardcpa@Yal'ioo,(om American Institute of CPA's Telephone: (225) 627-4537 Louisiana Society of CPA's FAX (225) 627-4584

INDEPENDENT AUDITOR'S REPORT ON FINANCIAL STATEMENTS

Members ofthe Board oI'Diiectois Waterworks District No. I ofthe Parish ol'Avoyclles Burdelonvillc, Louisiana

Report on Financial Staitements

1 have audited the accompanying financiai stateinents ofthe business-type activities of Waterworks District No. 1 ofthe Parish of Avoyelles {A Component Unit ofthe Avoyelles Parish Police Jury) as of and for the year ended June 30. 2013. and the related notes to the financial statements, which collectively comprise the District's basic financial statements as hslcd in the table of contents.

Management's Responsibility for the Financial .Statements

Management is responsible for the preparation and fair presentation of these Iniancial statements in accordance vvith accounting principles generally accepted in the Jnited States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that arc free from material misstateinent, whether due to fraud or error.

Auditor's Responsibility

M> responsibility is to express opinions on these financial statements based on my audit. I conducted m\ audit in accordance with auditing standaids generally accepted in Ihe United Stales of America and the standards applicable to Hnancial audits contained in (jDvernnicnf Auditing Standards, issued by the Comptroller General of the United Slates. Those standards require thai I plan and perfoi'iii the audit to obtain reasonable assurance about whether the basic tuiancial statements are free of material misstatement.

An audit involves performing procedures to otitain audit evidence about the amounts and disclosures in the financial statements. Hie procedures selected depend on the auditor's judgment, including the assessment ofthe risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation ofthe financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of e.xpressing an opinion on the effectiveness ofthe entity's internal control. Accordingly, I express no such opinion. An audit also includes evaluating the appropriateness of accoiinting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation ofthe financial statements.

I believe that the audit CMdence I have obiained \>. sufficient and appropriate to provide a basis for my opinions.

Members ofthe Board of Commissioners Waterworks District No. I ofthe Parish of Avoyelles Bordelonville. Louisiana

Opinions

In my opinion the financial statements referred lo above present fairly, in all material respects, the respective financial position ofthe business-type activities of Waterworks District No. 1 ofthe Parish of Avoyelles as of,lune 30, 201 ?, and the respective changes in financial poshion thereof for the year then ended, in accordance with accounting principles generally accepted in the United States of America.

Rmphasis of Matter

As described in Note I to the financial statements, in 2013, false Waterworks District No. 1 ofthe Parish of Avoyelles adopted new accounting guidance, GASB Statennent No. 63 Financial Reporting of Deferred OutfJows of Resources. Deferred Inflows of Resoiirce.s. and Net Position. My opinion is not modified with respect to this matter.

Other Matters

RequiredSiipj)leiiienfary Information

Accounting principles generally accepted in the United States of America require that management's discussion and analysis on pages 3 through ^ be presented to supplement the basic financial statements. Such information, ahhough not a part ofthe basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. I have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in Ihe United Stales of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to my inquiries, the basic financial statements, and other knowledge I obtained during my audit of the basic financial statements. I do not express an opinion or provide any assurance on the inlbrmation because the limited procedures do not provide me with sutflcieiiil evidence lo express ar opinion or provide any assarance.

Other Reporting Required by Government Auditing Standards

In accordance with Cjovernmeni Audilini^ Slundards. 1 have also issued a report dated September 30, 20M., on nu' consideration of the District's internal control over financial reporting and my tests of its compliance with ceitain provisions ol' laws, regulations, contracts and grant agreements and other matters. The purpose of that report is to describe the scope ol'my testing ofinlernal control over financial |-eporling and compliance and the results of that testing, and not to provide an opinion on the inieinal control over financial reporting or on compliance. I'hat report is an integral part of an audit performed in accordance with Government Auditing Standards and should be read in conjunction with this report in considering the results ofmv audit.

Certified Public Accountant Bueche. Louisiana September 30. 2013

REQUIRED SUFPLEIMENTARY INFORMATION

W a t e r w o r k s Distr ict No. 1 o f the Parish of Avoyelles Bordelonville, Louisiana

Management's Discussion and Analysis (Unaudited)

Our discussion and analysis of Waterworks District No. 1 of Avoyelles Parish, Louisiana's linancial performance pro\'ides an overview of Waterworks District No. I's financial activities for the fiscal year ended June 30. 2013 Please read it in conjunction with the District's basic financial statements.

Financial Highlights

The assets ofthe District exceeded its liabilities at June 30. 2013 by $895,808 (net position). Of this amount $517,334 was unrestricted and may be used to meet the District's ongoing obhgations. Net position increased by $99,085 in fiscal year 2012.

Overview ofthe Financial Statements

The annual report consists of three parts: IVIanagement discussion and analysis, basic iiiiancial statements and supplementary information. The basic fmancial statements present information for the District and is designed lo make the statements easier to understand. The basic fmancial statements consist ofthe fund financial statements and notes to the financial statements.

Current and other assets Capital assets

"fotal Assets

Long term outstanding debt Other liabilities

total Liabilities

Net Position Invested in capital assets, net of related debt Unrestricted

Total Net Position

Table 1 Net Position

$

—

%

2012 494.314 390.576 884.890

-0-88.167 88.167

390,576 406,147 796.723

$

—

$

2013 616.147 378.474 994.621

-0-98.813 98,813

378.474 517.334 895.808

Net position is assets restricted as to the purposes they can be used for, or, are invested in capital assets (buildings, water equipment, etc.)- Un::estricted net position is those assets that do not have any hmitations for which these amounts may be used.

W a t e r w o r k s District No. 1 o f t h e Par ish of Avoyelles Bordelonville, Louisiana

Management's Discussion and Analysis (Unaudited) (Continued)

Table 2 Changes in Net Position

2012 2013 Revenue

Operating -Charges tor services

Non-operating -Gain from sale of capital assets Interest revenue

'YoVdl revenue

Lx DC uses Operating Non-operating -

Interest expense Total expenses

$ 342,678

-0-2,729

345.407

333.892

-0-333,892

$ 443.282

3.000 2.193

448.475

349.389

-0-349.389

Change in Net Position

Beginning Net Position

Ending Net Position

1.514

785.209

.L?96J2_3

99.085

796.723

$ 895.808

CAPl lAI. ASSET AND DEBf ADMINIS fRATlON

Capital Assets

At June 30, 2013. the District had $1,311,151 invested in capital assets, including buildings, water wells, tanks and lines, and equipment. There were additions to capital assets of $22,755 and dispositions of capital assets of $22,321 deletions during 2013.

1 he District had not outstanding indebtedness at June 30, 2013.

Waten\orks District No. 1 ofthe Parish of Avoyelles Bordelonville, Louisiana

Management's Discussion aiid Analysis (Unaudited) (Continued)

Contacting the District's Management

Ihis financial report is designed to prcvide our customers, citizens and taxpayers vvith a general overview ofthe Districfs fnianccs and to show the District's accountability for the money it recei\es. If you have any questions about this report or need additional information, contact the AxoyeUes Waterworks District No.I's office in Bordelonville. Louisiana.

BASIC FINANCIAL STATEMEM S

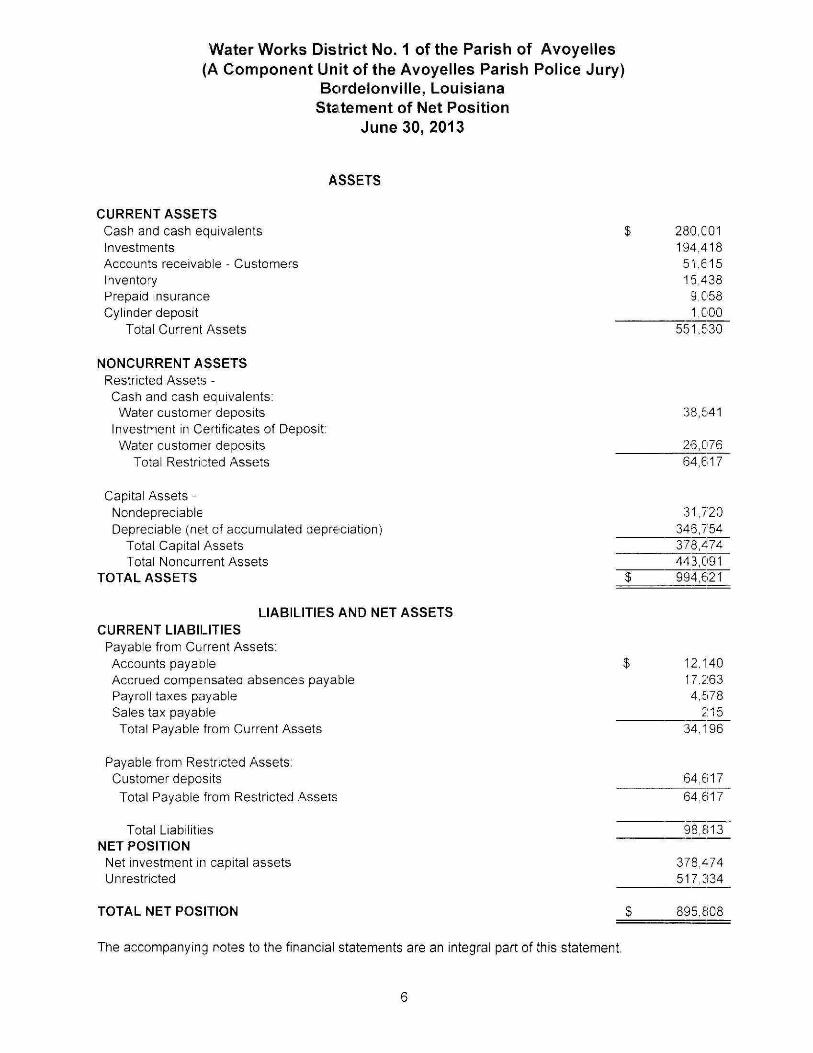

Water Works District No. 1 of the Parish of Avoyelles (A Component Unit of the Avoyelles Parish Police Jury)

Bordelonville, Louisiana Statement of Net Position

June 30, 2013

ASSETS

CURRENT ASSETS Cash and cash equivalents Investments Accounts receivable - Customers Inventory Prepaid insurance Cylinder deposit

Total Current Assets

$ 280,001 194,418 51,615 15,438 9,058 1,000

551,530

NONCURRENT ASSETS Restricted Assets -Cash and cash equivalents: Water customer deposits

Investment in Certificates of Deposit: Water customer deposits

Total Restricted Assets

38,541

26,076 64,617

Capital Assets -Nondepreciable Depreciable (net of accumulated depre^ciation)

Total Capital Assets Total Noncurrent Assets

TOTAL ASSETS

LIABILITIES AND NET ASSETS CURRENT LIABILITIES

Payable from Current Assets: Accounts payable Accrued compensated absences payable Payroll taxes payable Sales tax payable Total Payable from Current Assets

31,720 346,754 378,474 443.091 994.621

12,140 17,263 4,578

215 34,196

Payable from Restricted Assets: Customer deposits Total Payable from Restricted Assets

Total Liabilities NET POSITION

Net investment in capita! assets Unrestricted

TOTAL NET POSITION

64,617

64,617

98,813

378,474 517,334

$ 895,808

The accompanying notes to the financial statements are an integral part of this statement.

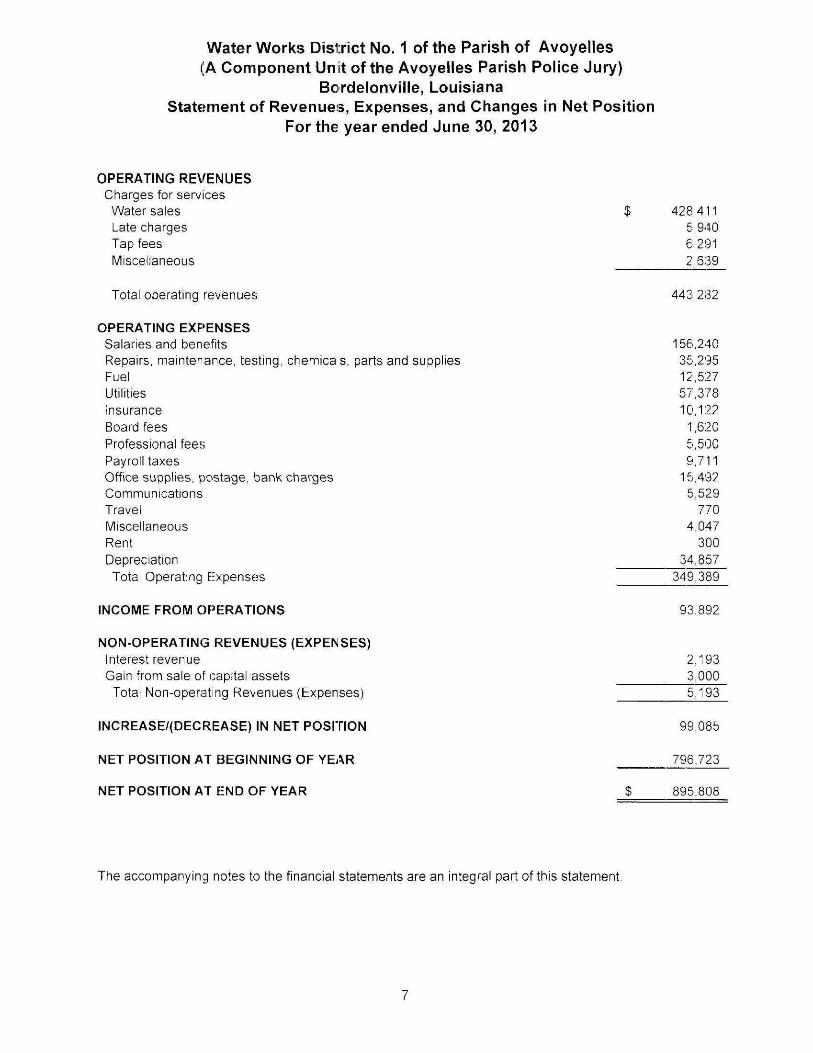

Water Works DisUict No. 1 of the Parish of Avoyelles (A Component Unit of the Avoyelles Parish Police Jury)

BoTdelonvllle, Louisiana Statement of Revenues, Expenses, and Changes in Net Position

For the year ended June 30, 2013

OPERATING REVENUES Charges for services Water sales Late charges Tap fees Miscellaneous

Total operating revenues

OPERATING EXPENSES Salaries and benefits Repairs, maintenance, testing, chemicas, parts and supplies Fuel Utilities Insurance Board fees Professional fees Payroll taxes Office supplies, postage, bank charges Communications Travel Miscellaneous Rent Depreciation Total Operating Eixpenses

INCOME FROM OPERATIONS

$ 428,411 5,940 6,291 2,639

443,282

156,240 35,295 12,527 57,378 10,122

1,620 5,500 9,711

15,492 5,529

770 4,047

300 34,857

349,389

93,892

NON-OPERATING REVENUES (EXPENSES) Interest revenue Gain from sale of capital assets Total Non-operating Revenues (Expenses)

INCREASE/{DECREASE) IN NET POSITION

NET POSITION AT E3EGINNING OF YEAR

NET POSITION AT END OF YEAR

2,193 3,000 5,193

99,085

796,723

895,808

The accompanying notes to the financial statements are an integral part of this statement.

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit of the Avoyelles Parish Police Jury)

Bordelonville, Louisiana Statement of Cash Flows

For the year ended June 30, 2013

CASH FLOWS FROM OPERATING ACTIVITIES Cash received from customers Cash payments to suppliers for goods and services Cash payments to employees for services

Net Cash Provided by (Used for) Operating Activities

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES Acquisition of capital assets Proceeds from sale of capital asset

Net Cash (Used for) Capital and Related Financing Activities

CASH FLOWS FROM INVESTING ACTIVITIES Interest on Investments (Increase)/Decrease in Investments

Net Cash Provided by (Used for) ln\/esting Activities

INCREASE (DECREASE) IN CASH

Cash and Cash Equivalents. Beginning of Year CASH AND CASH EQUIVALENTS, END OF YEAR

RECONCILIATION OF OPERATING INCOME TO NET CASH PROVIDED BY (USED FOR) OPERATING ACTIVITIES lncome/(loss} from operations Adjustments to reconcile operating income to net cash provided

by (used for) operating activities: Depreciation Net Change in Assets and Liabilities -

(Increase) Decrease in accounts receivable (Increase) Decrease in inventory (Increase) Decrease in prepaid expense Increase (Decrease) in accounts payable Increase (Decrease) in accrued compensated absences Increase (Decrease) in payroll taxg'S payable Increase (Decrease) in sales tax payable Increase (Decrease) in customer security deposits

Total Adjustments Net cash provided by (used for) operating activities

Cash and Cash Equivalents - Unrestricted Cash and Cash Equivalents - Restricted

456,615 (152,943) (154,313) 149,359

(22,755) 3,000

;i9,755)

2,193 (1,182) 1,011

130,615

187,927 $ 318,542

93,892

34,857

10,362 (266) (131)

4,539 1.928 1,039

168 2.972

55,467 $ 149,359

280,001 38,541

318,543

The accompanying notes to the financial statements are an integral part of this statement.

Waterworks District No. 1 of tlie Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police .)ur>)

Notes to the Financial Statements June 30, 2013

Introduction

Waterworks District No. 1 ofthe Parish of Avoyelles was created on February 5. 1969 by the Avoyelles Parish Police Jury. The "District" operates under a president-board Ibrm ofgoxermnent whose appointments are made by the Avoyelles Parish Police Jury.

1. Summary of Sionificant Aecountin}^ Policies

A. Basis of Presentation

The District's llnanciai statements are prepared in accordance with generally accepted accounting principles (CiAAP). J he CJovernmental Accounting Standards Board (G/VSB) is responsible for establishing (iAAP for state and local governments thrt>ugh its pronouncements {Standards and Inlerprelalions).

B. Reporting tiility

Governmental Accounting Standards Board Statement No. 14 established criteria for determining v/hich component units should be considered part ofthe reportmg entity, for tniancial reporting purposes. The basic criterion for including a potential component unit within the reporting entity is llnanciai accountability. The (JASB has set forth criteria Ui be considered in determining tuiancial accountability, fhis criteria includes: (1) appointing a voting majorily of an t)rgani/ation's governing body, and the ability ofthe police jury to impose its will on that organization, and/or the potential for the organization let provide specific financial bcneiUs to or impose specilic fmancial burdens on the police jury; (2) organizations for which the police jury does not appoint a voting majorily but are fiscally dependent on the police jury: and (3) urganizations for which the reporting entity linancial statements would be misleading if data ofthe organization is not included because ofthe nature or significance of the relationship.

Because the Avoyelles Parish Police Jury appoints the governing board and because of ihe scope of public service, the District is deemed to be a component unit ofthe Avoyelles Parish Police Jury, the governing body cf the parish and the governmental bod> with oversight responsibility. *fhe accompanying tuiancial statements present information only on the funds maintained b;' ihe District and do not present information on the police jury, the general government services pro\'ided by that governmental unit, or the olher governmental uniis that comprise the governmental reporting entity.

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Notes to the Financial Statements June 30, 2013

1. Summary of Significant Accounting Policies (Continued)

C. Basic Financial Statements - Fund Financial Statements

The focus of proprietary I'und metisurement is upon determination of operating income. changes in net assets, financial position, and cash flows. The generally accepted accounting principles applicable are those similar to businesses in the private sector. The Waterworks District No. I of .Avoyelles Parish reports a single proprietary fund.

The District is organized and operated on the basis of funds whereby a separate self- balancing set of accounts (Fnterprisc Fund) is maintained that comprise its assets, liabilities, fund equity, revenue and expense. The operations are ilnanced and operated in a manner similar to a private business enterprise - where the im.ent ofthe governing body is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis be ilnanced or recovered primarily through user charges. The enterprise fund is used to account for water services provided to the residents and businesses within the District.

D. Measurement Focus. Basis of Accounting and Financial Statement Presentation

fhe proprietary fund financial statements are reported using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless ofthe timing of related cash Hows. Cirants and similar items arc recognized as revenue as soon as all eligibility requirements imposed by the prosider have been met.

Governments are also required to follow the pronouncements ofthe Financial Accounting Standards Board (FASB) issued tirough November 30, 1989 {when applicable) that do not conflict with, or contradict GASB' pronouncements. Although the District has the option to apply FASB pronouncements issued after that date, the District has chosen not to do so.

Amounts reported as program revenues include 1) charges to customers or applicants for goods. services or privileges provided. 2i operating grants and contributions, including special assessments.

F. Use of Restricted Recourses

Restricted recourses are comprised of customer utility deposits and are held by the District as an agent and can only be used to satisfy customer utility accounts or refund to customer.

10

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Notes to the Financial Statements June 30, 2013

1, Summary of Significant Accounting Policies (Continued)

F. Cash and Cash Equivalents

For purposes ofthe Statement of Cash Flows, cash on hand and all restricted and unrestricted cash in banks (demand deposits, interest-bearing demand deposits and money markel accounts) and highly liquid investments, having a maturity of three months or less when purchased are considered to be cash equivalents

G. Investments

Investments at June 30. 2013 are stated at fair value.

II. Receivables

Customer accounts receivable are reported at gross, the direct write-off method is used to record bad delbts, therctbre no allowance for uncollectible accounts is maintained. Use of this method does not materially differ from the allowance method.

1. Inventories and prepaid expenses

Inventories consist of parts and materials and are recorded as an expense when consumed. Inventories are valued at the lower of cost, utilizing the first in - first out method of \aIuation. Certain payraents to vendors represent payments for future periods and are therefore reported as prepaid expense.

J. Capital Assets

ihe cost of properly, plant and ecuipmcnt, including signitleant betterments to existing facilities and iinfrastructure is recorded in the enterprise llmd on its balance sheet. Interest costs incurred during construction are capitalized. Depreciation of all exhaustible capital assets are charged as an expense against operations and has been computed under the straight - line method based on the estimated useful lives ofthe individual assets. Estimated useful lives are as follows:

Distribution system 50 years Storage tanks 40 years Pumping stations and buildings 20 years Other Equipment 3-10 years Software 5 years

All capital assets are slated at historical cost. Donated assets are valued at their estimated fair value on the date donated. For the fiscal year ended June 30, 2013, there was no interest charges capitalized on capital assets acquired or constructed.

11

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Notes to the Financial Statements June 30, 2013

1. Summary of Significant Accounting Policies (Continued)

K. Compensated Absences

The District has adopted a policy for paid vacation and sick leave for all full time employees. Employees with 1 - 5 years of service arc granted 14 days annual leave: employees with over 5 years of service are granted 14 days annual leave plus 1 day for each additional year of service lo a maximum of 25 days. Unused vacation leave is lost at the end ofthe calendar year. Employees hired before June 30, 1996 are allowed to carry forward any unused vacation leave as of that date, however, vacation leave earned after that date is non-cumulative. Sick leave may be accumulated indefinitely. At June 30, 2013, the amount of unused paid leave has been reported in these financial statements.

F Defining Operating Revenues and Eixpenses

The District distinguishes betwee:i operating and non-operating revenues and expenses -operating revenues and expenses ofthe District consist of charges for services {including tap fees) and the costs of providing those services, including depreciation and excluding interest cost. All other revenue and expenses are reported as nom-operating.

M. Net Assets

Proprietary fund net position is divided into three components:

• Net investment in capital assets—consist ofthe historical cost of capital assets less accumulated depreciation and less any debt that remains outstanding that was used to tlnance those assets.

• Restricted net position—consist of net position that is restricted by the District's credilors {for example, through debt covenants^ by the state enabling legislation {through restrictions on shared revenues), by grantors (both federal and state), and by other contributors.

• Unrestricted—all other net position is reported in this category.

N. Impact of Recently Issued and Adopted Accounting Principles

In December 2010, the GASB issued Statement 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows oj Resources, and Net Position. GASB 63 provides guidance for reporting deferred outflows of resources, deferred inllows of resources, and net position in a statement of financial position and related disclosures. The statement of net assets is renamed the statement of net position and includes four components, assets, deferred outflows of resources, liabilities and deferred inflows of resources. The provisions of this Statement are effective for financial statements for periods beginning after December 15. 2011.

12

Waterworks District No, 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Notes to the Financial Statements June 30, 2013

2. Deposits and Investments

Deposits - Under state law, federal deposit insurance or the pledge of securities owned by the fiscal agent bank must secure these deposits (or resulting bank balances). The market value ofthe pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent. At year-end. the carrying amount ofthe Districfs deposits was $318,543 and the bank balance was $325,383. Ofthe bank balance. $250,000 was covered by federal depository insurance and $75,383 of pledged securities held by the custodial bank in the name ofthe fiscal agent bank (GASIB Category 3).

Investments - State law allows the District to invest in any direct obligation ofthe United States Ireasury; other debt issued or guaranteed by the full faith and credit ofthe United States: certificates of deposit of any bank in Louisiana; mutual finds which are registered with the Securities and Exchange Commission and invest in securities ofthe U. S. government or its agencies; guaranteed investment contracts issued by banks or insurance companies or invcsunent grade commercial paper of domestic U. S. corporations.

Change in Investments Certificates of Deposit Cost Fair Value

Balance. Jul\ 1,2012 $ 219,312 $ 219.312 Add: Investment purchase (capitalized interest) 2,813 2^1_3 Balance, June 30,2013 $ 222,125 $ 222,125

Custodial Risk of hivestments Custodial credit risk for investments is the risk that, in the e\ent oi failure ofthe counter parly, the District will not be able to recover the value ofthe investment or collateral securiiies that are in the possession of an outside parly. Investment securities are exposed to custodial credit risk if the securiiies are insured and are not registered in the Jiame ofthe District and are held by either the counter-party's trust department or agents but not in the Districfs name. The District has no custodial credit risk at June 30, 2013 since all investments are insured by federal depository insurance.

1 he District has not formally adoptee deposit and investment policies that limit the Distiict^s allowable deposits or investments and address the specific types of risk to which the District is exposed, 'fhe Districfs investment in certificates of deposit represents their acceptance of lower rate of return in exchange for lower r.sk.

Restricted deposits and investments represent customer deposits held by the District for recourse against non-payment of utility accounts.

Waterworks District No. 1 ofthe Parish of Avoyelles A Component Unit ofthe Avoyelles Parish Police Jury)

Notes to the Financial Statements June 30,2013

3. Capital Assets

The following is a summary ofthe capital asset activity for the year ended June 30. 2013

Non-depreciable Assets -Land

Depreciable Assets -

Water System

Buildings

Equipment Office Equipment

Total Depreciable

July 1, 2012

S 31,720

1,028,941

114,951

129,150 5,955

1,278,997

Additions

S

11,510

--

11,245

22,755

Deletions

S

--

{22,321) -

{22,321)

June 30, 2013

$ 31,720

1,040,451

114,951 106,829 17,200

1,279,431

Total Capital Assets 1,310,717 22,755 (22,321) 1,311,151

Accumulated Depreciation -

Water System

Buildings

Equipment

Office Equipment

Total Accum Dept

Capital Assets - Book Value $

812,539

28,738

72,908

5,955

920,141

390,576

17,618

2,874

i:?,117

2,248

34,857

-

-

(22,321) -

(22,321)

$

830,157

31,612

62,704

8,203

932.676

378,475

14

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component linit ofthe Avoyelles Parish Police Jur>)

Notes to the Financial Statements June 30, 2013

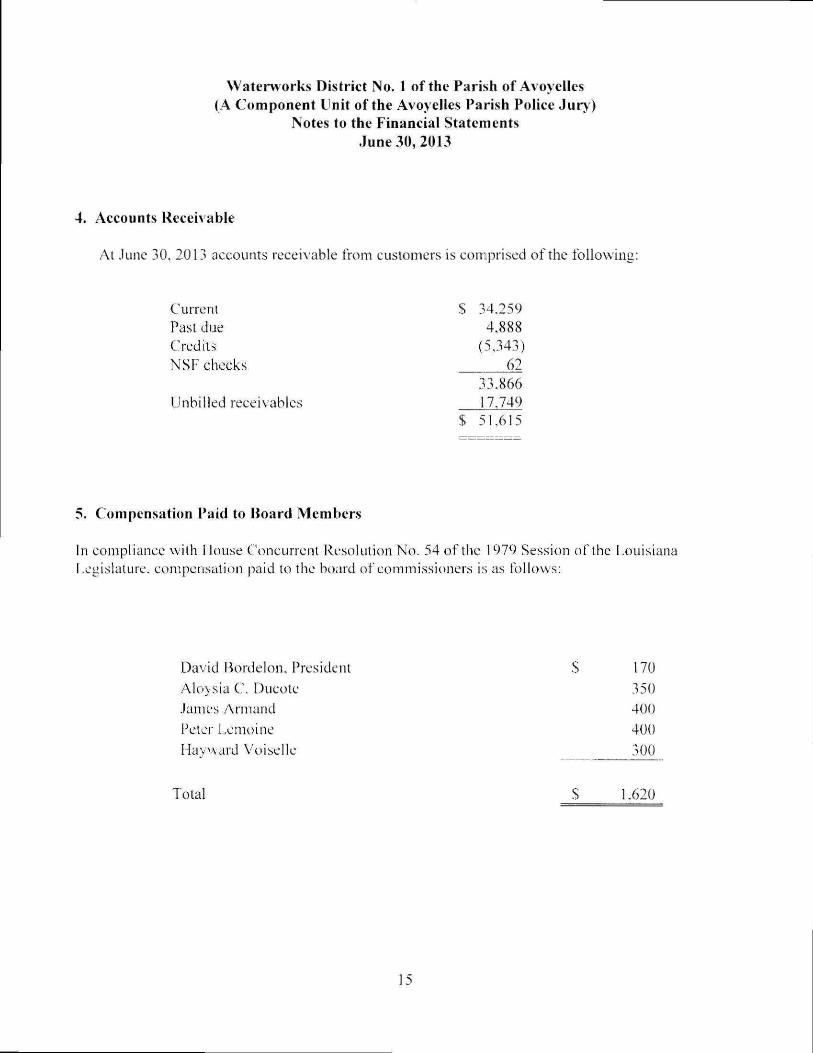

4. Accounts Kcceivable

At June 30. 2013 accounts recei\'able from customers is comprised ofthe following;

Current S 34.259 Past due 4.888 Credits {5,343) NSF checks 62

33.866 Unbilled receivables 17.749

$ 51.615

5. Compensation Paid to Board Members

In compliance with House Concurrent Resolution No. 54 ofthe 1979 Session ofthe Fonisiana Fcgislalure. compensation paid to the board of commissioners is as follows:

David Bordelon. President

Aloysia C. Ducote

James Arniand

Fetor Lemoine

Hayward Voiselle

Total

S

s

170 350 400 400 300

1.620

15

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jur>)

Notes to the Financial Statements June 30, 2013

6. Retirement Commitments

Employees ofthe District are members ofthe social .security reiirement system. The District has no further liabilit;- for retirement commitments.

7. Litigation and C laims

At June 30. 2013 ihe District was not involved in litigation or is aware of any unasserted claims.

8. Risk Management

ihe District is exposed lo various risks of loss for which the District purchases commercial insurance. The District maintains insurance policies to cover risks related to workers compensation, general liability, public ofllcials errors and omissions, commercial property damage. and automobile c<u'erage. including collision. There have been no reductions in insurance coverage during the last year, Settled claims have not exceeded coverage in the last three years.

9. Subsequent Fvents

Subsequent events were evaluated through September 30. 2013 which is the date the financial statements were available to be issued. It was determined that there are no significant events requiring recognition or disclosure through this date.

16

REPORTS REQUIRKD BY GOVERNMENT STANDARDS

W, Kathleen Beard Certified Public Accountant

10191 Bueche Road Erwinville. Louisiana 70729

(225) 627-4537F.4X(225) 627-4584

Member: American Institute ufCerlified Public Accountants

Societ\ of Loiiisiaita Cenilled Public Aecuunlanls

IN[)li:PENDENT AUDITORS' REPORT ON INTERNAL C O N T R O L OVER FINANCL\L REPORTING AND ON COIVIPLIANCE AND OTHER IV1ATTERS

BASED ON AN AUDIT OF THE BASIC FINANCIAL STATEMENTS PERFORMED IN ACCORDAP^CE WITH GOVERf^MENTAVDITII^GSTAND.4RDS

Members olHlie Roai'd of C'oininissioncrs W''atcr\vorl<s t;)isTrici No, I of tlic Parish of A voye ties Bordelonville, Louisiana

1 have audited, in accordance wilh the auditing standards generally accepted In tlie United States of America und the standards applicable to linancial audits contained in Govcrnincnl Auditing Standards, issued by tlie Comptroller Ceneral of the United States, the tuiancial staleinents of the business-type activities of Waterworks District No. I of the I-'arish of Avoyelles (the "Districl"). a component unit of the Avoyelles Parish Police .lury. as of and for the year ended .June 30, 2013, and the related notes to the linancial statements, which collectively comprise the Commission's basic financial statements and have issued iny report thereon dated September 50. 2013.

Internal Control Over Financiai Reporting

In planning and performing my audit of the finaacial statements, ! considered the District's internal control over linancial reporting {internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing my opinions on the financial statements, bill not for the purpose uf expressing an opinion on the effectiveness of the l^isiricl's internal control. Accordingly, I do not express an opinion on the effectiveness of the District's internal control.

A deficiency in internal control exists when the Jesigii or operation of a control does not allow management or employee, in the normal course of performing rheir assigned ftinclions, to prevent, oi detect and correct misstatements on a linieK basis. A material weakness is a dellciency, or a combination of deficiencies, in internal control such that diere is a reasonable possibiht> that a material misstatement ofthe entity's tniancial .statements will not be prevented, or delected and corrected on a timely basis. A significanl defidency is a deficiency, or a combination of detlciencies. in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

My consideration of internal control over financial reporting was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or. significant deficiencies. Given these limitations, during my audit I did not identify any deficiencies in internal control that 1 consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

17

Compliance anil Other Matters

As part of obtaining reasonable assurance at'out whether the District's financial statements are free of inaterial misstatement, t performed tests of its compliaice with certain provisions of laws, regulations, contracts and grants, noncompliance with which could have a direct ;ind inaterial effect on the determination of financial statement ainounts. However, providing an opinion on compliance v\ith those provisions was not an objective of my audit and. accordingly. 1 do not express such an opinion. The results of ny tests disclosed no instances of noncoinpliance that are required to be reported under Oovefivnenl Auditing Standards.

Purpose of this Report

The purpose of this repott is solely to describe the scope of my testing of internal control and compliance and the resLilts of that testing, and not to provide an opinion on tfe effectiveness ofthe District's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government .Auditing Standards in considering the Commission's internal control and compliance. /Vccordingly. this communication is not suitable for any other purpose.

70. X^Me^ S&stnd Certified Public Accountant E3ueche. Louisiana September 30, 2013

18

Waterworks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Schedule of Findings For the Year Ending June 30, 2013

A. Summarv of Audit Results

1. The auditor's report expresses an unqualified opinion on the basic financial statements ofthe Waterworks District No I ofthe Parish of Avoyelles.

2. No control deficiencies were disclosed during the audit ofthe basic financial statements in the report on internal control over financial reporting and compliance and other matters based on an audit of financial statements performed in accordance with Government Auditing Standards.

3. No instances of noncompliance material to the basic financial statements ofthe Waterworks District No 1 ofthe Parish of .\voyelles were disclosed during the audit.

B. Findings - Financial Statements Audit

There were no findings.

C. Manaacmtnt Letter

No management letter was issued.

19

VVatenvorks District No. 1 ofthe Parish of Avoyelles (A Component Unit ofthe Avoyelles Parish Police Jury)

Schedule of Prior Year Audit Findings For the Year Fnding June 30, 2013

A. Internal Control and C ompliancc Material to the Financial Statements

There were no findings.

B. Management Letter

No mana^ement letter was issued.

20

![The Avoyelles pelican (Marksville, La.) 1861-03-16 [p ]](https://img.dokumen.tips/doc/110x75/61b2de373d764509cf5afdfe/the-avoyelles-pelican-marksville-la-1861-03-16-p-.jpg)