Embed Size (px)

Citation preview

AUTOMATIC DISCOVERY OF LATENT CLUSTERS IN GENERAL REGRESSIONMODELS

By

MINHAZUL ISLAM SK

A DISSERTATION PRESENTED TO THE GRADUATE SCHOOLOF THE UNIVERSITY OF FLORIDA IN PARTIAL FULFILLMENT

OF THE REQUIREMENTS FOR THE DEGREE OFDOCTOR OF PHILOSOPHY

UNIVERSITY OF FLORIDA

2017

© 2017 Minhazul Islam Sk

I dedicate this dissertation to my parents for their help and contributions in my life.

ACKNOWLEDGMENTS

First of all, I would like to thank all the people who have helped me in my graduate

life. I would like to thank my Ph.D. advisor Dr. Arunava Banerjee, without whom I could

not have completed my dissertation. I cannot thank him enough for his help, contribution

and motivation in my entire graduate life. I owe a lot of this journey to him as a graduate

student.

I would also like to thank my Ph.D. committee members: Dr. Anand Rangarajan, Dr.

Alireza Entezari, Dr. Malay Ghosh for their invaluable suggestions.

I would like to thank Rafael Nadal and Bernie Sanders who have inspired me in

my life with their passion, accomplishments and fight for standing up for what is right,

especially in the time of despair.

I would also like to take this opportunity to thank my entire family for helping me

to reach this stage of my life, for their financial and moral help in time of distress, for

supporting and believing in me and raising me to prepare for every adversities in my life.

4

TABLE OF CONTENTS

page

ACKNOWLEDGMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

LIST OF TABLES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

LIST OF FIGURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

ABSTRACT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

CHAPTER

1 INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Introduction to the Variational Inference of the DP Mixtures of GLM . . . . . . . 13Automatic Detection of Latent Common Clusters in Multigroup Regression . . . 16Automatic Discovery of Common and Idiosyncratic Effects in Multilevel Re-

gression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Denoising Time Series by a Flexible Model for Phase Space Reconstruction . . 22Organization of the Dissertation . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

2 MATHEMATICAL BACKGROUND . . . . . . . . . . . . . . . . . . . . . . . . . 27

Generalized Linear Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Probability Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Linear Predictor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Link Function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Bayesian Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Bayes’ Theorem and Inference . . . . . . . . . . . . . . . . . . . . . . . . 29MAP Estimate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Conjugate Prior . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Nonparametric Bayesian . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Dirichlet Distribution and Dirichlet Process . . . . . . . . . . . . . . . . . . 30Stick Breaking Representation . . . . . . . . . . . . . . . . . . . . . . . . 31Chinese Restaurant Process . . . . . . . . . . . . . . . . . . . . . . . . . 31Dirichlet Process Mixture Model . . . . . . . . . . . . . . . . . . . . . . . . 33Hierarchical Dirichlet Process . . . . . . . . . . . . . . . . . . . . . . . . . 33Chinese Restaurant Franchise . . . . . . . . . . . . . . . . . . . . . . . . 34

3 VARIATIONAL INFERENCE FOR INFINITE MIXTURES OF GENERALIZEDLINEAR MODELS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

GLM Models as Probabilistic Graphical Models . . . . . . . . . . . . . . . . . . 37Normal Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Logistic Multinomial Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Poisson Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

5

Exponential Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Inverse Gaussian Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Multinomial Probit Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Variational Inference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Variational Distribution of the Models . . . . . . . . . . . . . . . . . . . . . . . . 41

Normal Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Logistic Multinomial Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Poisson Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42Exponential Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42Inverse Gaussian Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43Multinomial Probit Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Generalized Evidence Lower Bound (ELBO) . . . . . . . . . . . . . . . . . . . . 43Parameter Estimation for the Models . . . . . . . . . . . . . . . . . . . . . . . . 44

Parameter Estimation for the Normal Model . . . . . . . . . . . . . . . . . 45Parameter Estimation for the Multinomial Model . . . . . . . . . . . . . . . 47Parameter Estimation for the Poisson Model . . . . . . . . . . . . . . . . . 47Parameter Estimation for the Exponential Model . . . . . . . . . . . . . . . 48Parameter Estimation for the Inverse Gaussian Model . . . . . . . . . . . 49Parameter Estimation for the Multinomial Probit Model . . . . . . . . . . . 51

Predictive Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51Experimental Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Datasets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54Timing Performance for the Normal Model . . . . . . . . . . . . . . . . . . 54Accuracy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55Tool to Understand Stock Market Dynamics . . . . . . . . . . . . . . . . . 56

4 AUTOMATIC DETECTION OF LATENT COMMON CLUSTERS OF GROUPSIN MULTIGROUP REGRESSION . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Models Related to iMG-GLM . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60iMG-GLM Model Formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Normal iMG-GLM-1 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 61Logistic Multinomial iMG-GLM-1 Model . . . . . . . . . . . . . . . . . . . . 62Poisson iMG-GLM-1 Model . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Variational Inference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Normal iMG-GLM-1 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 63Logistic Multinomial iMG-GLM-1 Model . . . . . . . . . . . . . . . . . . . . 63Poisson iMG-GLM-1 Model . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Parameter Estimation for Variational Distribution . . . . . . . . . . . . . . . . . 64Parameter Estimation of iMG-GLM-1 Normal Model . . . . . . . . . . . . . 64Parameter Estimation of iMG-GLM-1 Multinomial Model . . . . . . . . . . 64Parameter Estimation of Poisson iMG-GLM-1 Model . . . . . . . . . . . . 65Predictive Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

iMG-GLM-2 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66Information Transfer from Prior Groups . . . . . . . . . . . . . . . . . . . . 66

6

Posterior Sampling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67Prediction for New Group Test Samples . . . . . . . . . . . . . . . . . . . 68

Experimental Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68Trends in Stock Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68Clinical Trial Problem Modeled by Poisson iMG-GLM Model . . . . . . . . 70

5 AUTOMATIC DISCOVERY OF COMMON AND IDIOSYNCRATIC LATENTEFFECTS IN MULTILEVEL REGRESSION . . . . . . . . . . . . . . . . . . . . 74

Models Related to HGLM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74An Illustrative Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74iHGLM Model Formulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

Normal iHGLM Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75Logistic Multinomial iHGLM Model . . . . . . . . . . . . . . . . . . . . . . 76

Proof of Weak Posterior Consistency . . . . . . . . . . . . . . . . . . . . . . . . 77Gibbs Sampling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78Predictive Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80Experimental Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Clinical Trial Problem Modeled by Poisson iHGLM . . . . . . . . . . . . . . 81Height Imputation Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . 83Market Dynamics Experiment . . . . . . . . . . . . . . . . . . . . . . . . . 84

6 SECOND PROBLEM: TIME SERIES DENOISING . . . . . . . . . . . . . . . . 87

Time Delay Embedding and False Neighborhood Method . . . . . . . . . . . . 87NPB-NR Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Step One: Clustering of Phase Space . . . . . . . . . . . . . . . . . . . . 88Step Two: Nonlinear Mapping of Phase Space Points . . . . . . . . . . . . 89Step Three: Restructuring of the Dynamics . . . . . . . . . . . . . . . . . 90

Experimental Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91An Illustrative Description of the NPB-NR Process . . . . . . . . . . . . . 91Prediction Accuracy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92Noise Reduction Experiment . . . . . . . . . . . . . . . . . . . . . . . . . 95Power Spectrum Experiment . . . . . . . . . . . . . . . . . . . . . . . . . 95Experiment with Dimensions . . . . . . . . . . . . . . . . . . . . . . . . . 97

7 CONCLUSION AND FUTURE WORK . . . . . . . . . . . . . . . . . . . . . . . 100

REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

BIOGRAPHICAL SKETCH . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

7

LIST OF TABLES

Table page

3-1 Description of variational inference algorithms for the models . . . . . . . . . . 53

3-2 Run time for Gibbs sampling and variational inference . . . . . . . . . . . . . . 55

3-3 Log-likelihood of the normal model of the predictive distribution . . . . . . . . . 56

3-4 MSE and MAE of algorithms for the datasets . . . . . . . . . . . . . . . . . . . 57

3-5 List of influential stocks on individual stocks . . . . . . . . . . . . . . . . . . . . 58

4-1 Description of variational inference algorithm for iMG-GLM-1 normal model . . 66

4-2 Clusters of Stocks from Various Sectors . . . . . . . . . . . . . . . . . . . . . . 71

4-3 Mean abosulte error for all stocks for iMG-GLM-1 . . . . . . . . . . . . . . . . . 71

4-4 MSE and MAE for clinical trial and patients datasets . . . . . . . . . . . . . . . 72

5-1 Description of Gibbs sampling algorithm for iHGLM . . . . . . . . . . . . . . . . 81

5-2 List of stocks with top 3 significant stocks influencing each stock . . . . . . . . 85

5-3 MSE and MAE of the algorithms for the height imputation dataset . . . . . . . . 85

5-4 MSE and MAE of the algorithms for the clinical trial and patients datasets. . . . 86

6-1 Step-wise description of NPB-NR process. . . . . . . . . . . . . . . . . . . . . 91

6-2 Minimum embedding dimension of the attractors . . . . . . . . . . . . . . . . . 98

6-3 MSE and standard deviation of datasets for all algorithms . . . . . . . . . . . . 98

6-4 Noise reduction percentage of the attractors . . . . . . . . . . . . . . . . . . . . 99

8

LIST OF FIGURES

Figure page

2-1 Stick breaking for the Dirichlet Process . . . . . . . . . . . . . . . . . . . . . . . 32

2-2 Chinese Restaurant Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2-3 Plate notation for DPMM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

2-4 Plate notation for HDPMM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

2-5 Plate notation for HDPMM with indicator variables . . . . . . . . . . . . . . . . 35

2-6 Chinese Restaurant Franchise for HDP . . . . . . . . . . . . . . . . . . . . . . 36

3-1 Posterior trajectory of the normal model . . . . . . . . . . . . . . . . . . . . . . 53

3-2 Timings for synthetic datasets per dimension . . . . . . . . . . . . . . . . . . . 55

4-1 Graphical representation of iMG-GLM-1 model. . . . . . . . . . . . . . . . . . . 61

4-2 Average MAE for 51 stocks for 50 random runs for iMG-GLM-1 model . . . . . 73

4-3 Average MAE for 10 new stocks for 50 random runs for iMG-GLM-2 model . . . 73

5-1 Posterior trajectory of the synthetic dataset with 4 groups . . . . . . . . . . . . 75

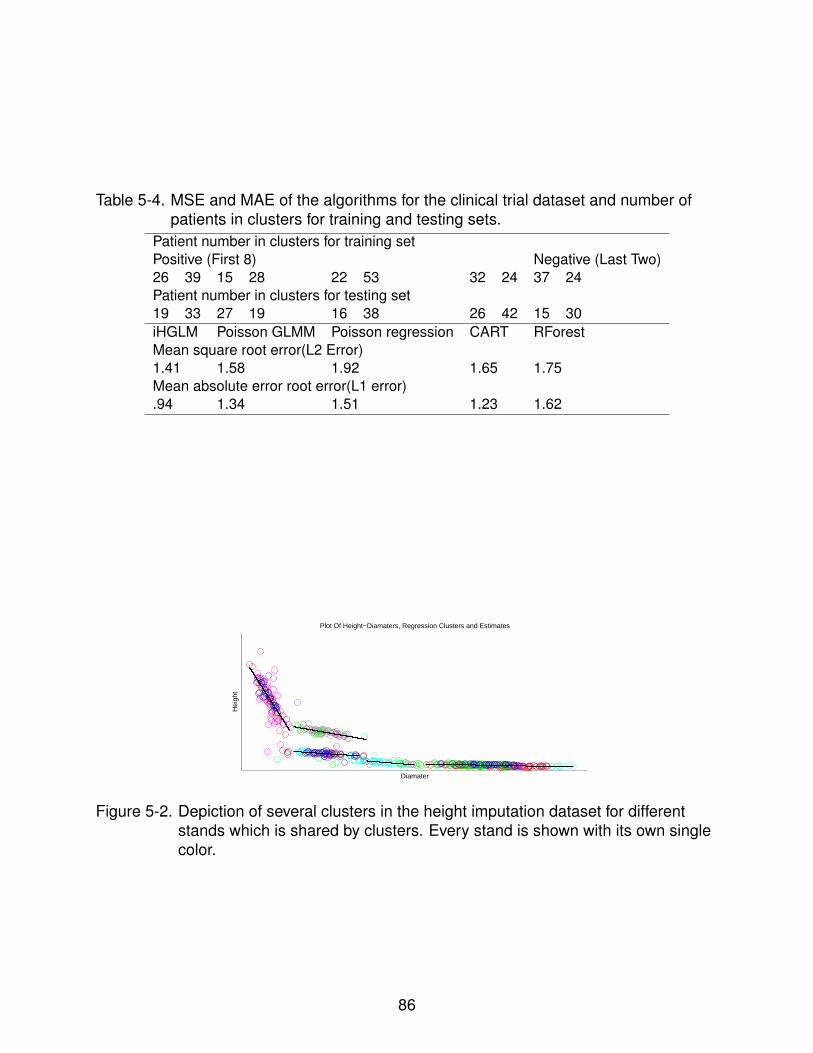

5-2 Depiction of several clusters in the height imputation dataset . . . . . . . . . . 86

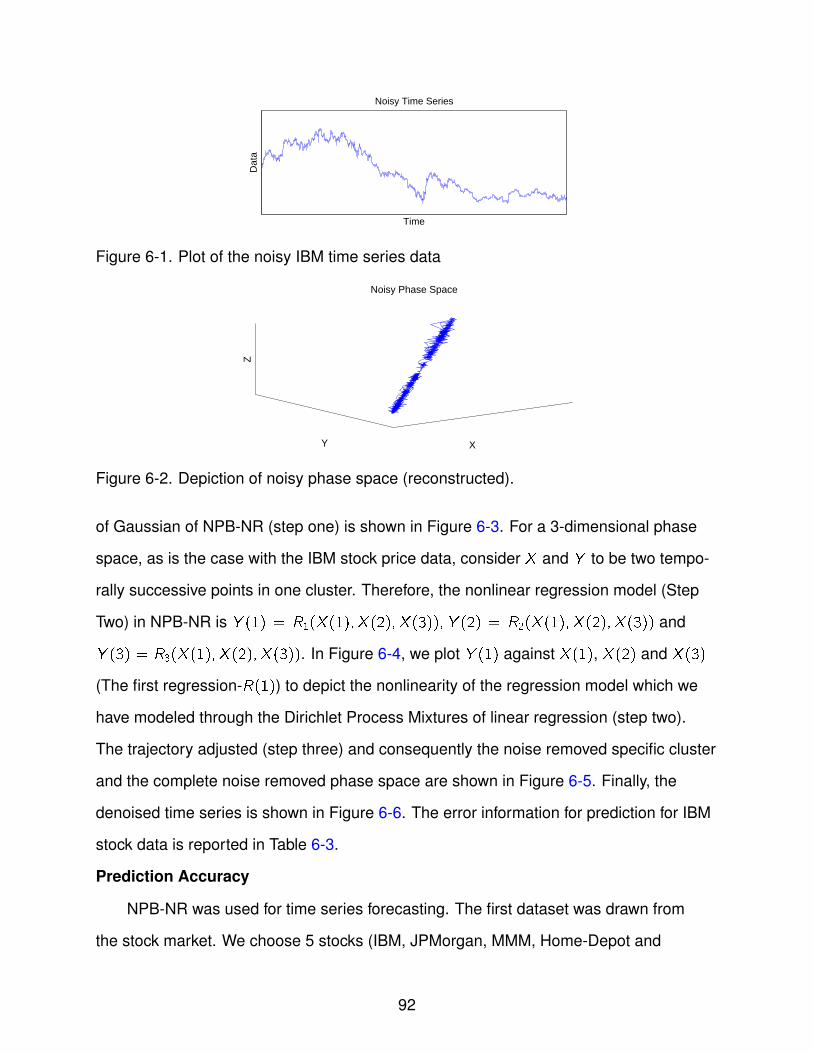

6-1 Plot of the noisy IBM time series data . . . . . . . . . . . . . . . . . . . . . . . 92

6-2 Depiction of noisy phase space (reconstructed). . . . . . . . . . . . . . . . . . 92

6-3 Clustered phase space and one single cluster . . . . . . . . . . . . . . . . . . . 93

6-4 Regression data: Y(1) regressed with covariate as X(1), X(2) and X(3) . . . . . 93

6-5 Single noise removed cluster and whole noise removed phase space . . . . . . 93

6-6 Plot of the noise removed time series data . . . . . . . . . . . . . . . . . . . . . 93

6-7 Power spectrum and phase space plot of attractors . . . . . . . . . . . . . . . . 96

9

Abstract of Dissertation Presented to the Graduate Schoolof the University of Florida in Partial Fulfillment of theRequirements for the Degree of Doctor of Philosophy

AUTOMATIC DISCOVERY OF LATENT CLUSTERS IN GENERAL REGRESSIONMODELS

By

Minhazul Islam Sk

August 2017

Chair: Arunava BanerjeeMajor: Computer Science

We present a flexible nonparametric Bayesian framework for automatic detection

of local clusters in general regression models. The models are built using techniques

that are now considered standard in statistical parameter estimation literature, namely

Dirichlet Process (DP), Hierarchical Dirichlet Process (HDP), Generalized Linear

Model (GLM) and Hierarchical Generalized Linear Model (HGLM). These Bayesian

nonparametric techniques have been widely applied to solve clustering problems in the

real world.

In the first part of this thesis, we formulate all traditional versions of the infinite

mixture of GLM models under the Dirichlet Process framework. We study extensively

two different inference techniques for these models, namely, variational inference and

Gibbs sampling. Finally, we evaluate their speed, and accuracy in synthetic and real

word datasets across various dimensions.

In the second part, we present a flexible nonparametric generative model for

multigroup regression that detects latent common clusters of groups. We name this

“Infinite MultiGroup Generalized Linear Model” (iMG-GLM). We present two versions

of the core model. First, in iMG-GLM-1, we demonstrate how the use of a DP prior on

the groups while modeling the response-covariate densities via GLM, allows the model

to capture latent clusters of groups by noting similar densities. The model ensures

different densities for different clusters of groups in the multigroup setting. Secondly, in

10

iMG-GLM-2, we model the posterior density of a new group using the latent densities of

the clusters inferred from previous groups as prior. This spares the model from needing

to memorize the entire data of previous groups. The posterior inference for iMG-GLM-1

is done using variational inference and that for iMG-GLM-2 using a simple Metropolis

Hastings algorithm. We demonstrate iMG-GLM’s superior accuracy in comparison to

well known competing methods like Generalized Linear Mixed Model (GLMM), Random

Forest, Linear Regression etc. on two real world problems.

In the third part, we present a flexible nonparametric generative model for multilevel

regression that strikes an automatic balance between identifying common effects

across groups while respecting their idiosyncrasies. We name it “Infinite Mixtures

of Hierarchical Generalized Linear Model” (iHGLM). We demonstrate how the use

of a HDP prior in local, group-wise GLM modeling of response-covariate densities

allows iHGLM to capture latent similarities and differences within and across groups.

We demonstrate iHGLM’s superior accuracy in comparison to well known competing

methods like Generalized Linear Mixed Model (GLMM), Regression Tree, Bayesian

Linear Regression, Ordinary Dirichlet Process regression, and several other regression

models on several synthetic and real world datasets.

For the final problem we present a framework that shows how infinite mixtures of

Linear Regression (Dirichlet Process mixtures) can be used to design a new denoising

technique in the domain of time series data that presumes a model for the uncorrupted

underlying signal rather than a model for the noise. Specifically, we show how the

nonlinear reconstruction of the underlying dynamical system by way of time delay

embedding yields a new solution for denoising where the underlying dynamics is

assumed to be highly nonlinear yet low-dimensional. The model for the underlying data

is recovered using the nonparametric Bayesian approach and is therefore very flexible.

11

CHAPTER 1INTRODUCTION

This dissertation comprises, primarily, of two parts, with nonparametric Bayesian

theories providing the central theme. The first part deals with a Bayesian nonparametric

approach to clustering of regression models in various hierarchical settings. This part

is divided into three subtopics. In the first subtopic, we outline variational inference al-

gorithms for already existing classes of infinite mixture of Generalized Linear Models. In

the second subtopic, we present a generative model framework for automatic detection

of latent common clusters of groups in multigroup regression. In the third subtopic,

we formulate a generative model for automatic discovery of common and idiosyncratic

latent effects in multilevel regression. The second part deals with a problem of denoising

time series by way of a flexible model for phase space reconstruction using variational

inference of infinite mixtures of linear regression. Each part is outlined in the following

paragraphs.

In machine learning and statistics, regression theory is a process for approximating

functional relationships among different entity/variables. This comprises of methods

for modeling relationship between multiple variables, where the first set is termed

as independent variables or predictors or covariates, while the other set is called

dependent variable or response variables. In general, regression theory evaluates the

value of expectation of the conditional distribution of the response given the covariates.

Another important parameter is the variance of the response conditional density given

the covariates. In the first part of this dissertation, we present flexible nonparametric

Bayesian frameworks for automatic detection of local clusters in general regression

models in various grouped as well as non-grouped data. In the other part, we lay out a

time series denoising technique using a dynamical system approach that uses phase

space reconstruction of the time series under consideration and then removes the noise

12

in the phase space and finally reconstructs the original noise removed time series all in

the context of Bayesian nonparametrics.

Introduction to the Variational Inference of the Dirichlet Process Mixtures ofGeneralized Linear Models

Generalized Linear Model (GLM) was proposed in Nelder and Wedderburn (1972)

to bring erstwhile disparate techniques such as, Linear regression, Logistic regression,

Poisson regression, Inverse Gaussian, Multinomial Probit, and Exponential regression

under a unified framework. Generally, regression in its canonical form assumes that

the response variable follows a given probability distribution with its support determined

by a linear combination of the covariates. Formally stated, Y |X ∼ f(XTβ). f , in the

case of Linear regression is the Normal distribution, in the case of Logistic and Poisson

regression, they are the Multinomial and Poisson distributions respectively. There are

two pieces to the above equation that GLM generalizes. Firstly, f is generalized to the

exponential family. Secondly, the function that maps the response mean (µ) to XTβ,

which in the case of linear regression is the identity function(XTβ = g (µ) = µ

), is

generalized to one of any member of a set of link functions. Common link functions

include Logit, Probit and the complementary log-log function. A GLM model is formally

defined as:

f (y ; θ,ψ) = exp

{yθ − b (θ)

a (ψ)+ c (y ;ψ)

}(1–1)

Here, ψ is a dispersion parameter. The mean response is given by the following

equation,

E [Y |X] = b (θ) = µ = g−1(XTβ)

(1–2)

Here g is the link function and XTβ is the linear predictor.

13

Notwithstanding its generality, GLM suffers from two intrinsic weaknesses, which

the authors in Hannah et al. (2011) addressed where they used the Gaussian Model.

Firstly, the covariates are associated with the model via only a linear function. Secondly,

the variance of the responses are not associated with the individual covariates. We

resolve the issues in line with Hannah et al. (2011) by introducing a mixture of GLM,

and furthermore, in order to allow the data to choose the number of clusters we impose

a Dirichlet Process prior as formulated in Ferguson (1973). Additionally, we extend the

models from just Linear and Logistic regression to all the traditional models of GLM

which we have mentioned above.

For inference, a widely applicable MCMC algorithm, namely Gibbs sampling Neal

(2000a) was employed in Hannah et al. (2011) for prediction and density estimation

using the Polya urn scheme of Dirichlet Process Blackwell and MacQueen (1973).

In spite of the generality and strength of these models, the inherent deficiencies of

Gibbs sampling significantly reduces its practical utility. As is well known, Gibbs sam-

pling approximates the original posterior distribution by sampling using a Markov chain.

However, Gibbs sampling is prohibitively slow and moreover, its convergence is very

difficult to diagnose. In high dimensional regression problems, Gibbs sampling seldom

converges to the target posterior distribution in suitable time, leading to significantly

poor density estimation and prediction Robert and Casella (2001). Although, there are

theoretical bounds on the mixing time, in practice they are not particularly useful.

To alleviate these problems, we introduce a fast and deterministic mean field

variational inference algorithm for superior prediction and density estimation of the GLM

mixtures. Variational inference is deterministic and possesses an optimization criterion

which can be used to assess convergence.

Variational methods were introduced in the context of graphical models in M. Jordan

and Saul (2001). For Bayesian applications, variational inference was employed in

Ghahramani and Beal (2000). Variational inference has found wide applications in

14

hierarchical Bayesian models such as, Latent Dirichlet Allocation D. Blei and Jordan

(2003), Dirichlet process mixtures Blei and Jordan (2006) and Hierarchical Dirichlet

Process Teh et al. (2006). To the best of our knowledge, this dissertation introduces

variational inference for the first time to nonparametric Bayesian regression.

The main contributions of this part are as follows:

• We derive the variational inference model separately for all GLM models according

to the stick breaking representation of the Dirichlet Process Sethuraman (1994).

These models differ significantly in terms of the type of covariate and response

data, which directs to markedly different variational distributions, parameter

estimation and predictive distributions. In each case, we formulate a class of

decoupled and factorized variational distributions as surrogates for the original

posterior distribution. We then maximize the lower bound (resulting from imposing

Jensen’s inequality on the log likelihood) to obtain the optimal variational parame-

ters. Finally, we derive the predictive distribution from the posterior approximation

to predict the response variable conditioned on a new covariate and the past

response-covariate pairs.

• We demonstrate the accuracy of the our variational approach across different

metrics such as, relative mean square and absolute error in high dimensional

problems against Linear regression, Bayesian and variational Linear regression,

Gaussian Process regression, and the Gibbs sampling inference in various train-

ing/testing data splits. We evaluate the log likelihood of the predictive distribution

in varying dimensions to show the superiority of variational inference against

Gibbs sampling in accuracy. Gibbs sampling fails to converge as the dimension

progressively rises.

• We experimentally show that variational inference converges substantially faster

than Gibbs sampling, thereby becoming a natural choice for practical high dimen-

sional regression problems. We show the timing performance per dimension with

15

the dimension varying from a low to a very large value for both variational and

Gibbs sampling inference in a synthetic dataset, a compiled stock market dataset,

and a disease dataset.

Introduction to Automatic Detection of Latent Common Clusters of Groups inMultiGroup Regression

Multigroup regression is the method of choice for research design whenever

response-covariate data is collected across multiple groups. When a common regressor

is learned on the amalgamated data, the resultant model fails to identify effects for

the responses specific to individual groups because the underlying assumption is that

the response-covariate pairs are drawn from a single global distribution, when the

reality might be that the groups are not statistically identical, making the joining of them

inappropriate. Modeling separate groups via separate regressors results in a model that

is devoid of common latent effects across the groups. Such a model does not exploit the

patterns common among the groups ensuring in turn the transferability of information

among groups in the regression setting. This is of particular importance when the

training set is very small for many of the groups. Joint learning, by sharing knowledge

between the statistically similar groups, strengthens the model for each group, and the

resulting generalization in the regression setting is vastly improved.

The complexities that underlie the utilization of the information transfer between

the groups are best motivated through examples. In Clinical trials, for example, a group

of people are prescribed either a new drug or a placebo to estimate the efficacy of the

drug for the treatment of a certain disease. At a population level, this efficacy may be

modeled using a single Normal or Poisson mixed model distribution with mean set as

a (linear or otherwise) function of the covariates of the individuals in the population.

A closer inspection might however disclose potential factors that explain the efficacy

results better. For example, there might be regularities at the group level—Caucasians

as a whole might react differently to the drug than, say, Asians, who might, furthermore,

16

comprise many groups. Identifying this across group information would therefore

improve the accuracy of the regressor. Similarly in the stock market, future values and

trends for a group of stocks are predicted for various sectors such as energy, materials,

consumer discretionary, financial, technology, etc. Within each sector, various stocks

share trends and therefore predicting them together (modeling them with the same time

series via autoregressive density) is usually much more accurate than predicting and

capturing individual trends. Modeling the latent common clustering effects of cross-

cutting subgroups is therefore an important problem to solve. We present a framework

here that accomplishes this.

For multigroup regression, Generalized Linear Mixed Model (GLMM) Breslow and

Clayton (1993) and Hierarchical Generalized Linear Mixed Model Lee and Nelder (1996)

have been developed where similarities between groups is captured though a fixed

effect and variation across groups is captured through random effects. Statistically,

these models are very rigid since every group is forced to manifest the same fixed

effect, while the random effect only represents the intercept parameter of the linear

predictors. Cluster of groups may have significantly different properties from other

clusters of groups, a feature that is not captured in these traditional GLM based models.

Furthermore, various clusters of groups may have different uncertainties with respect to

the covariates which we denote as heteroscedasticity. In recent progress, Bakker and

Heskes (2003) has proposed a Bayesian hierarchical model, where a prior is used for

the mixture of groups. Nevertheless, individual groups are given weights as opposed to

jointly learning various groups. Also, the number of mixtures are fixed in advance.

Before, presenting our algorithm, we describe our basis for identifying group-

correlation. First, two groups are correlated if their responses follow the same distri-

bution. Second, two groups that have the same response variance with respect to the

covariates are deemed to be correlated. This is achieved via a Dirichlet Process prior

17

on the groups and the covariate coefficients (β). The posterior is obtained by appropri-

ately combining the prior and the data likelihood from the given groups. The prior helps

cluster the groups and the likelihood from the individual groups help in the sharing of

trends between groups to create the single posterior density between the many potential

groups, thereby leading to group-correlation.

We now present an overview of our iMG-GLM framework. Our objective is to

achieve (a) shared learning of various groups in a regression setting, where data may

vary in terms of temporal, geographical or other modalities and (b) automatic clustering

of groups which display correlation. iMG-GLM-1 solves this task. In iMG-GLM-2, we

model a completely new group after modeling previous groups through parameters

learned in iMG-GLM-1. In the first part, the regression parameters are given a Dirichlet

Process prior, that is, they are drawn from a DP with the base distributions set as the

density of the regression parameters. Since a draw from a DP is an atomic density,

to begin, one group will be assigned one density of the regression parameters which

signifies the response density with respect to its covariates. As the drawn probability

weight from the DP increases, the cluster starts to consume more and more groups

in this multigroup setting. We employ a variational Bayes algorithm for the inference

procedure in iMG-GLM-1 for computational efficiency. iMG-GLM-1 is then extended

to iMG-GLM-2 for modeling a completely new group. Here we transfer the information

(covariate coefficients) obtained in the first part, to learning a new group. In essence,

the cluster parameters (covariate coefficients for the whole group) are used as a prior

distribution for the model parameters of the new group’s response density. This therefore

leads to a mixture model where the weights are given by the number of groups that

one cluster consumed in the first part and the mixture components are the regression

parameters obtained for that specific cluster. The likelihood comes from the data of

the new group. We use a simple accept-reject based Metropolis Hastings algorithm to

generate samples from the posterior for the new group regression parameter density.

18

For both iMG-GLM-1 and iMG-GLM-2, we use Monte Carlo integration for evaluating the

predictive density of the new test samples.

We evaluate both iMG-GLM-1 and iMG-GLM-2 Normal models in two real world

problems. The first is the prediction and finding of trends in the stock market. We

show how information transfer between groups help our model to effectively predict

future stock values by varying the number of training samples in both previous and new

groups. In the second, we show the efficacy of i-MG-GLM-1 and i-MG-GLM-2 Poisson

model against its competitors in a very important clinical trial problem setting.

Introduction to Automatic Discovery of Common and Idiosyncratic Latent Effectsin Multilevel Regression

Hierarchical Generalized Linear Model (HGLM), proposed in Lee and Nelder (1996),

extends GLM to already grouped observations. Hierarchical Generalized Linear Model is

formally defined as:

f (y ; θ,ψ, u) = exp

{yθ − b (θ)

a (ψ)+ c (y ;ψ)

}(1–3)

Here, ψ is a dispersion parameter and u is the random effect component. The mean

response is E [Y |X] = b (θ) = µ = g−1(XTβ + v

), where g is the link function, XTβ

is the linear predictor and v is a strictly monotonic function of u,{v = v (u)}. Here, v

signifies over-dispersion. u has a prior distribution chosen appropriately.

Therefore, in HGLM, the separate densities are characterized by two main com-

ponents. First, there is a fixed effect parameter,(XTβ

)of the density which includes

the covariates X and its coefficients (β). They are same for all the groups. Secondly,

there is a random effect part (v ) which is different in different groups. Notwithstanding

its generality and effectiveness, the inherent assumptions in HGLM limit its performance

and need to be relaxed.

Firstly, the random effect (u) is not a function of the linear transformation of the

covariates, XTβ. Therefore, this automatically assumes that the mean function and the

19

variance of the outcomes in different groups depend neither on the covariate, X , nor on

the coefficients. This makes the model suitable only for grouped data where properties

of the outcomes in different groups vary independently of covariates. Secondly, although

the response-covariate pairs are grouped, two different pairs in the same group may

come from different response-covariate densities. Likewise, any two pairs from two

different groups may be generated from the same density. Therefore, we need a

robust model that captures this hidden intra/inter clustering effect in already grouped

data. Thirdly, the covariate (XTβ) is associated with the response-covariate density

only through a linear function. Although we can introduce a non-linear function for

the response at the output, it does not include the covariates. Finally, data may be

heteroscedastic within the individual group also, i.e. the variance of the response may

be a function of the predictors within each groups. The response variance however

does not depend on the predictors in ordinary HGLM. Some later version Lee and

Nelder (2001a) of HGLM picks heteroscedasticity between the groups (different variance

for different groups), but within specific groups response variance does not vary with

covariates.

Many examples of the kind of problem that motivates us can be found in Clinical

trials, tree height imputation and in other areas. In clinical trialsIBM (2011), a group of

people are given either a new drug or a placebo to estimate the effect of the new drug

for treatment of a certain disease. Normally, these are modeled by Normal or Poisson

Mixed model, which predicts the effectiveness of the new drug. In practice, it has been

found that different people react differently to new drugs. Also, persons in different

groups can behave similarly to the new drug. Therefore, prediction of usefulness of

the new drugs as a whole is not perfect. Also, the variability of the reaction must be

different among people within groups and different groups and they must depend on

the covariates such as, treatment center size, gender, age etc. In height imputation

Robinson and Wykoff (2004) for forest stands, heights are generally regressed with

20

various tree attributes like tree diameter, past increments etc., which gives a projection

for forest development under various management strategies. These are modeled by

traditional Normal GLMM where the free coefficient(β0) becomes the random effect. The

underlying assumption is that trees in one stand have the same growth properties while

having completely different growth properties in different stands, which is not true. We

need a robust enough model to capture these shared growth properties among stands

for proper projection of overall forest development. Also, the model should pick up the

variance in growth measurements w.r.t. the diameters, past increments and other tree

attributes across stands.

In this dissertation, we alleviate these assumptions of HGLM by developing iHGLM,

a Non-parametric Bayesian Mixture Model of the Hierarchical Generalized linear Model.

The iHGLM framework is specified to all the models of HGLM, i.e. Normal, Poisson,

Logistic, Inverse Gaussian, Probit, Exponential etc.

In iHGLM, we model outcomes in the same group via mixtures of local densities.

This captures locally similar regression patterns, where each local regression is ef-

fectively a GLM. To force the density of the covariate, X , and its coefficients, β, to be

shared among groups, we make the coefficients, β, and the covariates, X , for different

groups be generated from the same prior atomic distribution. An atomic distribution

places finite probabilities on a few outcomes of the sample space. When the coeffi-

cients, β, and the covariates, X , are drawn from this atomic density, it enables the X and

β in different groups to share densities. In this way, in the Bayesian setting, along with

the density of random effect (u), the density of fixed effect (XTβ) is also shared among

groups. We obtain this prior atomic density for fixed and random effect, while ensuring

a large support, through a Hierarchical Dirichlet Process (HDP) priorY. W. Teh and Blei

(2006).

From the HDP prior, our main goal is to generate prior densities of fixed effect u

and (XTβ) for each group. We draw a density G0 from a Dirichlet Process (DP(γ,H))

21

Ferguson (1973). In this case, the H (the base distribution) is basically the set of

densities in the parameter space of fixed (u) and random effect (XTβ). According

to Sethuraman (1994), this ensures that G0 is atomic, yet having a broad support.

Therefore, G0 is an atomic density in the parameter space of u and (XTβ) which puts

finite probabilities on several discrete points which acts as its support. Then, for each

group, we draw group specific densities Gj from DP(α,G0). Since G0 is already atomic,

and therefore according to Sethuraman (1994), Gj is also atomic and hence the support

of group specific densities Gjs must share common points in their respective parameter

space of fixed (u) and random (XTβ) effect. Now, this Gj acts as prior densities for the u

and XTβ for each group. Subsequently, both u and XTβ are modeled through mixture of

local densities which are shared among groups.

For each component (clusters within groups) in the mixture of response-covariate

densities in a single group, although the mean function is linear, marginalizing out

the local distribution creates a non-linear mean function. In addition, the variance of

the responses vary among mixture components (clusters), thereby varying among

covariates. The non-parametric model ensures that the data would determine the

number of mixture components (clusters) in specific groups and the nature of the local

GLMs.

Introduction to Denoising Time Series by Way of a Flexible Model for Phase SpaceReconstruction

In this part, we outline a technique for denoising a time series by way of a flexible

model for phase space reconstruction. Noise is a high dimensional dynamical system

which limits the extraction of quantitative information from experimental time series

data. Successful removal of noise from time series data requires a model either for the

noise or for the dynamics of the uncorrupted time series. For example, in wavelet based

denoising methods for time series Mallat and Hwang (1992); Site and Ramakrishnan

(2000), the model for the signal assumes that the expected output of a forward/inverse

22

wavelet transform of the uncorrupted time series is sparse in the wavelet coefficients.

In other words, it is presupposed that the signal energy is concentrated on a small

number of wavelet basis elements; the remaining elements with negligible coefficients

are considered noise. Hard-threshold wavelet Zhang et al. (2001) and Soft-threshold

wavelet David and Donoho (1995) are two widely known noise reduction methods that

subscribe to this model. Principal Component Analysis, on the other hand, assumes a

model for the noise: the variance captured by the least important principal components.

Therefore, denoising is accomplished by dropping the bottom principal components and

projecting the data onto the remaining components.

In many cases, the time series is produced by a low-dimensional dynamical system.

In such cases, the contamination of noise in the time series can disable measurements

of the underlying embedding dimension Kostelich and Yorke (1990), introduce extra

Lyapunov Exponents Badii et al. (1988), obscure the fractal structure Grassberger et al.

(1991) and limit prediction accuracy Elshorbagy and Panu (2002). Therefore, reduction

of noise while maintaining the underlying dynamics generated from the time series is of

paramount importance.

A widely used method in time series denoising is Low-pass filtering. Here noise

is assumed to constitute all high frequency components without reference to the

characteristics of the underlying dynamics. Unfortunately, low pass filtering is not well

suited to non-linear chaotic time series Wang et al. (2007). Since the power spectrum of

low-dimensional chaos resembles a noisy time series, removal of the higher frequencies

distorts the underlying dynamics, thereby, adding fractal dimensions Mitschke et al.

(1988).

In this dissertation, we present a phase space reconstruction based approach to

time series denoising. The method is founded on Taken’s Embedding Theorem Takens

(1981), according to which a dynamical system can be reconstructed from a sequence

of observations of the output of the system (considered, here, the time series). This

23

respects all properties of the dynamical system that do not change under smooth

coordinate transformations.

Informally stated, the proposed technique can be described as follows: Consider

a time series, x(1), x(2), x(3)..... corrupted by noise. We first reconstruct the phase

space by taking time delayed observations from the noisy time series (for example,

⟨x(i), x(i + 1)⟩ forms a phase space trajectory in 2-dimensions). The minimum embed-

ding dimension (i.e., number of lags) of the underlying phase space is determined via

the False Neighborhood method Kennel et al. (1992). Next, we cluster the phase space

without imposing any constraints on the number of clusters. Finally, we apply a nonlinear

regression to approximate the temporally subsequent phase space points for each point

in each cluster via a nonparametric Bayesian approach. Henceforth, we refer to our

technique by the acronym NPB-NR, standing for nonparametric Bayesian approach to

noise reduction in Time Series.

To elaborate, the second step clusters the reconstructed phase space of the time

series through an Infinite Mixture of Gaussian distribution via Dirichlet Process Ferguson

(1973). We consider the entire phase space to be generated from a Dirichlet Process

mixture (DP) of some underlying density Escobar and West (1995). DP allows the

phase space to choose as many clusters as fits its dynamics. The clusters pick out small

neighborhoods of the phase space where the subsequent non-linear approximation

would be performed. As the latent underlying density of the phase space is unknown,

modeling this with an Infinite mixture model allows NPB-NR to correctly find the phase

space density. This is because of the guarantee of posterior consistency of the Dirichlet

Process Mixtures under Gaussian base densityS. Ghosal and Ramamoorthi (1999).

Therefore, we choose the mixing density to be Gaussian. The posterior consistency acts

as a frequentist justification of Bayesian methods—as more data arrives, the posterior

density concentrates on the true underlying density of the data.

24

In the third step, our goal is to non-linearly approximate the dynamics in each clus-

ter formed above. We use a DP mixture of Linear regression to non-linearly map each

point in a cluster to its image (the temporally subsequent point in the phase space). In

this infinite mixtures of regression, we model the data in a specific cluster via a mixtures

of local densities (Normal density with linear combination of the covariates (βX ) as the

Mean). Although the mean function is linear for each local density, marginalizing over

the local distribution creates a non-linear mean function. In addition, the variance of

the responses vary among mixture components in the clusters, thereby varying among

covariates. The nonparametric model ensures that the data determines the number of

mixture components in specific clusters and the nature of the local regressions. Again,

the basis for the infinite mixture model of linear regression is the guarantee of posterior

consistency Tokdar (2006).

In the final step, we restructure the dynamics by minimizing the sum of the deviation

between each point in the cluster and its pre-image (previous temporal point) and

post-image (next temporal point) yielded by the non-linear regression described above.

To create a noise removed time series out of the phase space, readjustment of the

trajectory is done by maintaining the co-ordinates of the phase space points to be

consistent with time delay embedding.

We demonstrate the accuracy of the NPB-NR model across several experimental

settings such as, noise reduction percentage and power spectrum analysis on several

dynamical systems like Lorenz, Van-der-poll, Buckling Column, GOPY, Rayleigh and

Sinusoid attractors, as compared to low pass filtering. We also show the forecasting

performance of the NPB-NR method in time series datasets from various domain like

the “DOW 30” index stocks, LASER dataset, Computer Generated Series, Astrophysical

dataset, Currency Exchange dataset, US Industrial Production Indices dataset, Darwin

Sea Level Pressure dataset and Oxygen Isotope dataset against some of its competitors

like GARCH, AR, ARMA, ARIMA, PCA, Kernel PCA and Gaussian Process regression.

25

Organization of the Dissertation

In chapter 2, we briefly describe Generalized Linear Models and Bayesian inference

theory, with focus on the nonparametric Bayesian framework and its various represen-

tations. In Chapter 3, we outline the variational inference of Dirichlet Process mixtures

of Generalized Linear Models. Chapter 4 presents the clustering models for multigroup

regression. Chapter 5 outlines the automatic detection of latent Common and idiosyn-

cratic effects in multilevel regression. Finally, in Chapter 6, we present the time series

denoising method in details. Chapter 7 discusses future directions.

26

CHAPTER 2MATHEMATICAL BACKGROUND

Generalized Linear Model

Overview

Generalized Linear Models were proposed in Nelder and Wedderburn (1972)

to generalize Linear Regression by allowing the outcome/response variables to be

distributed according to many other distributions other than the standard Normal

distribution. It brought together several regression models such as Logistic Regression,

Poisson regression, Probit regression etc. under a common framework.

In a Generalized Linear Model (GLM), the response variable given the covari-

ates/independent variables follows a exponential family distribution (which therefore

includes the Normal, Binomial, Poisson and Gamma distributions etc). The expec-

tation/mean of the distribution, µ, generally depends on the covariates/independent

variables, X, via the following equation:

E(Y) = µ = g−1(Xβ) E(Y) = µ = g−1(Xβ) (2–1)

Here E(Y) is the mean of the response distribution or the expected value of re-

sponse and Xβ is the linear combination of the covariates with coefficients β and g is

termed as the link function. The unknown parameters, β, are generally estimated with

maximum quasi-likelihood, maximum likelihood or Bayesian techniques.

The GLM framework operates using three components:

• Exponential family probability distribution

• A linear combination of the covariates, linear predictor, Xβ.

• A link function g, which links the linear predictor to the mean of the response

distribution, such that Xβ = g(µ), so that E(Y ) = µ = g−1(Xβ).

27

Probability Distribution

A GLM model is therefore formally defined in terms of probability distribution as:

f (y ; θ,ψ) = exp

{yθ − b (θ)

a (ψ)+ c (y ;ψ)

}(2–2)

Here, ψ is a dispersion parameter. There are many common distributions that

belong to this exponential family. They are Normal, Gamma, Beta, Dirichlet, Multinomial

etc.

Linear Predictor

The linear predictor is the linear combination of the independent variables, X . This

is the entity that gathers the information about the independent variables and then

includes them in the model. This is also tightly related to the link function which we

describe in the next section

η = Xβ.

Link Function

The link function links the expectation/mean of the response distribution to the

linear predictor. So, the linear predictor goes into the model via this function which

is the response of the distribution. There are many commonly used link functions in

Generalized Linear Model family. For Normal model, Xβ = µ, the identity link function.

For Exponential and Gamma model, it is the inverse link, Xβ = µ−1. For Inverse

Gaussian model, the link function is the inverse squared, Xβ = µ−2. For Poisson model,

the link function is the log link, Xβ = ln(µ). For Bernoulli, Categorical/Multinomial Model,

it is the Logit function, ln( µ1−µ

).

28

Bayesian Statistics

Bayes’ Theorem and Inference

Bayesian inference is a manner of doing statistical inference where we use Bayes’

theorem to calculate the the probability for an unknown quantity as we gather more and

more information. There is a prior distribution P(θ|β) for the unknown quantity θ, (here, β

is the hyper parameter) and the observed data (X1,X2, ......)is modeled to be distributed

independently and identically (i.i.d.) according to a distribution P(X |θ). Now, given this

data, according to Bayes’ rule, the posterior distribution of θ is given by

P(θ|X, β) = P(X|θ)P(θ|β)P(X|β)

=P(X|θ)P(θ|β)∫

θP(X|θ)P(θ|β)dθ (2–3)

Here, P(X |β) is known as the marginal likelihood.

MAP Estimate

MAP estimate is the mode (optima) of the posterior distribution. This is nothing

but a point estimate of the unknown parameter based on the observed data. This is

accomplished by optimizing the posterior with respect to the unknown parameter θ. This

is given by,

θMAP = argmaxθ

P(θ|X, β) (2–4)

This is easy to evaluate when the posterior has a closed form known distribution,

which brings the idea of conjugate prior.

Conjugate Prior

When the posterior distribution, p(θ|X , β) has the same analytical from as the prior

distribution p(θ|β), they are termed as conjugate to each other. In that case, the prior

becomes a conjugate prior for that likelihood p(X |θ). This is an algebraic convenience

where the posterior distribution can be determined in a closed form. For example,

29

the Gaussian distribution is conjugate to another Gaussian (where only the mean is

unknown), Dirichlet distribution is conjugate for Multinomial likelihood, Beta density is the

conjugate for Binomial likelihood. Every exponential family distribution has a conjugate

prior.

Nonparametric Bayesian

The analytical form of the data distribution is assumed in parametric Bayesian

theory. This is very limiting in the sense that the number of parameters in the model

does not depend on the data, rather this is pre-fixed. But, in nonparametric Bayesian

statistics, the parameter space is infinite-dimensional. As the model obtains more and

more data, it automatically evaluates the status of the existing parameters or adds more

parameters to suitably reflect the data. Nonparametric Bayesian statistics have been

studied extensively in machine learning in the domain of classification, regression,

financial markets, time series prediction, dynamical systems etc.

Dirichlet Distribution and Dirichlet Process

The Dirichlet distribution is a multivariate version of the Beta distribution. It is

defined on the K-dimensional simplex. If, x = (x1, x2, , , xK) represents a K-dimensional

probability space, such that ∀i , xi ≥ 0and∑K

k=1 xk = 1, then the Dirichlet distribution is

given by,

Dir(x1, , , , xK |α1,α2, , , ,αK) =�(∑K

k=1 αk)

��(αk)�Kk=1x

αk−1k

(2–5)

Here, E [xk ] = αk∑Kk=1 αk

, Var [xk ] =αk(αk−

∑Kk=1 αk)

(∑K

k=1 αk))2(∑K

k=1 αk)+1)

The Dirichlet distribution is the conjugate prior to the categorical and multinomial

distribution. Therefore, when the data likelihood follows a categorical/multinomial

distribution, the prior should be a Dirichlet distribution to get a Dirichlet distribution as

the posterior.

30

A Dirichlet Process Ferguson (1973), D (α0,G0) is defined as a probability measure

over (X ,B(X )), such that for any finite partition of X = A1 ∪ A2 ∪ A3... ∪ AK .

(G(A1),G(A2), ...,G(AN)) ∼ Dir(α0A1,α0A2, ...,α0AK) (2–6)

D (α0,G0) is defined as a probability distribution on a sample space of probability

distribution. Here, α0 is the concentration parameter and G0 is the base distribution.

Here, E [G(A)] = G0(A) and V [G(A)] = G0(A)(1 − G0(A))/(α0 + 1), where, A is any

subset of X belonging to its sigma algebra.

There are two well known representations of Dirichlet Process which we would

describe below.

Stick Breaking Representation

According to the stick-breaking construction Sethuraman (1994) of DP, G , which is a

sample from DP, is an atomic distribution with countably infinite atoms drawn from G0.

βi |α0,G0 ∼ Beta(1,α0), θi |α0,G0 ∼ G0

πi = vi

i−1∏l=1

(1− vl) , G =

∞∑i=1

πi .δθi

(2–7)

Chinese Restaurant Process

A second representation of the Dirichlet process is given by the Polya urn Process

Blackwell and MacQueen (1973). This clearly proves the clustering property of the

Dirichlet Process. Let θ1, θ2, ... be independent and identically distributed draws from G .

Then the conditional distribution θn|θ1, θ2, ..........θn−1 is given by,

θn|θ1, θ2θ3θn−1,α0,G0 ∼n−1∑i=1

1

n − 1 + α0δθi +

α0n − 1 + α0

G0 (2–8)

31

Figure 2-1. Stick Breaking for the Dirichlet Process

Figure 2-2. Chinese Restaurant Process

Basically, an atom, θ would be drawn with more probability if the atom has been

drawn before. Each time a new atom may be drawn with probability α0.

32

Figure 2-3. Plate notation for DPMM

Dirichlet Process Mixture Model

In the DP mixture model Antoniak (1974), Escobar and West (1995), DP is used as

a nonparametric prior over parameters of an infinite mixture model Ishwaran and James

(2001).

zn| {v1, v2, ...} ∼ Categorical {π1,π2,π3....}

Xn|zn, (θi)∞i=1 ∼ F (θzn)

(2–9)

Here, F is a distribution parametrized by θzn .

Hierarchical Dirichlet Process

Hierarchical Dirichlet Process was proposed in Y. W. Teh and Blei (2006) to model

grouped data. Here, an individual group is modeled according to a mixture model. A

Hierarchical Dirichlet Process is defined as a distribution over a set of random probability

measures. There is a random probability measure Gj for each group and a universal

33

random probability measure G0. The universal measure G0 is a draw from a Dirichlet

process parametrized by concentration parameter γ and base probability measure H.

G0|γ,H ∼ DP(γ,H) (2–10)

Now, each Gj is a draw from a DP parametrized by α0 and G0.

Gj |α0,G0 ∼ DP(α0,G0) (2–11)

The HDP Mixture model is given by,

θj ,i |Gj ∼ Gj

xj ,i |θj ,i ∼ F (θj ,i)

(2–12)

Here, θj ,i is the latent parameter for i th element in the j th group and xj ,i is the i th

element in the j th group. Now that, G0 is a draw from a DP, this forms an atomic distri-

bution according to the previous section. When Gjs are drawn, they invariably share

some of those atoms because they all are drawn from the same G0. Therefore, Hierar-

chical Dirichlet Process has this unique capability of picking shared latent parameters in

grouped data in an infinite mixture model setting.

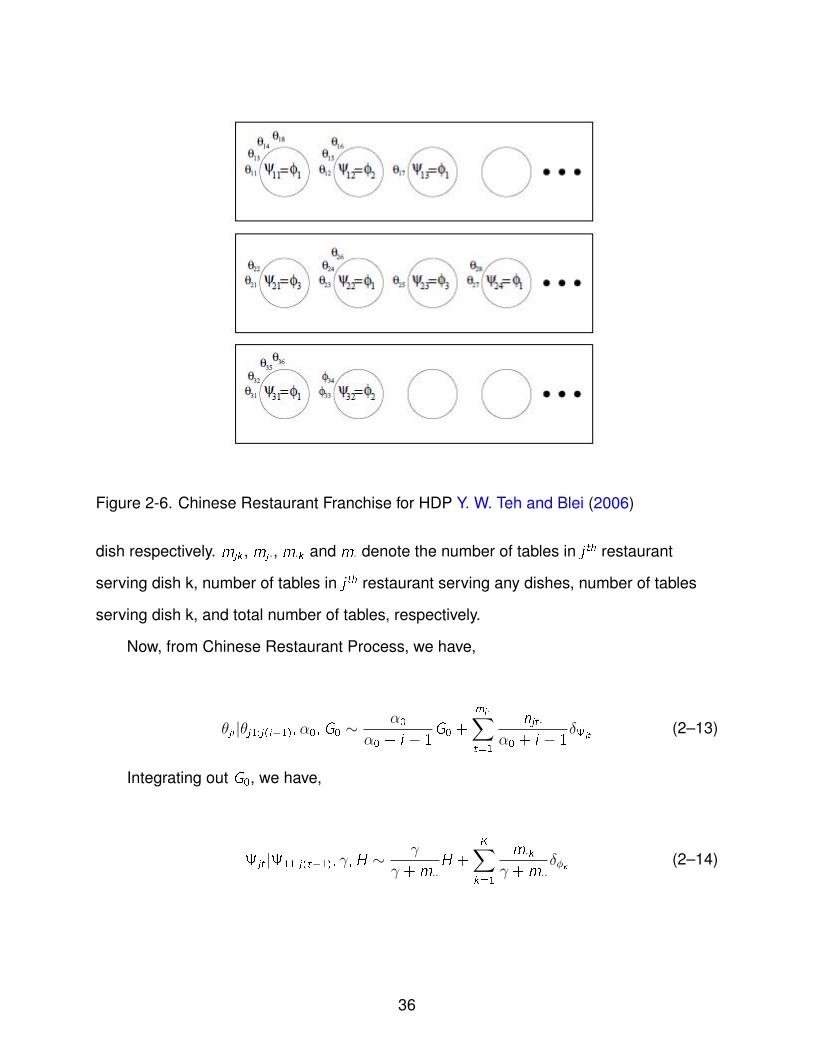

Chinese Restaurant Franchise

In the Chinese Restaurant Franchise (CRF), we have a finite number of restaurants

(groups) with infinite number of tables (clusters) with shared dishes (parameter) among

all restaurants. Let θji be the customers, ϕ1:K be the global dishes, jt be the table-

specific dishes, tji be the table index of j th restaurant (jt) and i th customer (θji ), kjt be

the table menu index of the j th restaurant (jt) and tth table (ϕk ). Again, njt· and nj ·k

denotes the number of customers in the tth table-j th restaurant and j th restaurant-k th

34

Figure 2-4. Plate notation for HDPMM

Figure 2-5. Plate notation for HDPMM with indicator variables

35

Figure 2-6. Chinese Restaurant Franchise for HDP Y. W. Teh and Blei (2006)

dish respectively. mjk , mj ·, m·k and m· denote the number of tables in j th restaurant

serving dish k, number of tables in j th restaurant serving any dishes, number of tables

serving dish k, and total number of tables, respectively.

Now, from Chinese Restaurant Process, we have,

θji |θj1:j(i−1),α0,G0 ∼α0

α0 + i − 1G0 +

mj·∑t=1

njt·

α0 + i − 1δjt

(2–13)

Integrating out G0, we have,

jt |11:j(t−1), γ,H ∼ γ

γ +m··H +

K∑k=1

m·k

γ +m··δϕk (2–14)

36

CHAPTER 3VARIATIONAL INFERENCE FOR INFINITE MIXTURES OF GENERALIZED LINEAR

MODELS

GLM Models as Probabilistic Graphical Models

We begin by assuming the continuous covariate-response pairs in the models as a

probabilistic graphical model according to its stick breaking representation. The Normal

and Multinomial Model was presented in Hannah et al. (2011), we extend to the other

models.

Normal Model

In Normal Model, the generative model of the covariate-response pair is given by

the following set of equations.

vi |α1,α2 ∼ Beta(α1,α2)

{µi ,d ,λx ,i ,d} ∼ N(µi ,d |mx ,d , (βx ,d ,λx ,i ,d)

−1)

Gamma (λx ,i ,d |ax ,d , bx ,d)

{βi ,d ,λy ,i} ∼ N(βi ,d |my ,d , (βy ,λy ,i)

−1)

Gamma (λy ,i |ay , by)

zn| {v1, v2, .....} ∼ Categorical {M1,M2,M3....}

Xn|zn ∼ N (µzn,d ,λx ,zn,d)

Yn|Xn, zn ∼ N

(βzn,0 +

D∑d=1

βzn,dXn,d ,λ−1y ,zn

)

(3–1)

Here, Xn and Yn represents the continuous response-covariate pairs. {z , v , ηx , ηy} is

the set of latent variables and the distributions, {µi ,d ,λx ,i ,d} and {βi ,d ,λy ,i} are the base

distributions of the DP.

Logistic Multinomial Model

In the logistic multinomial model, the continuous covariates are modeled by a

Gaussian mixture and a multinomial logistic framework is used for the categorical

37

response. In this model, the covariate and zn are modeled identically as the Normal

Model above. Hence, we present only the response distribution.

{βi ,d} ∼ N(βi ,d |my ,d ,k , s

2y ,d ,k

)Yn|Xn, zn ∼

exp(βzn,0,k +

∑D

d=1 βzn,d ,kXn,d

)∑K

k=1 exp(βzn,0,k +

∑D

d=1 βzn,d ,kXn,d

) (3–2)

Here, {z , v , ηx , ηy} are the latent variables and {µi ,d ,λx ,i ,d} and {βi ,d} are the DP

base distributions.

Poisson Model

In the Poisson Model, the categorical covariate is modeled by a mixture of Multino-

mial and a Poisson distribution is used for the count response data. Here, too vi and zn

follow the same distributions as before. The remainder of the generative model is given

by,

{pi ,d ,j} ∼ Dir (ad ,j) , {βi ,d ,j} ∼ N(βi ,d ,j |md ,j , s

2d ,j

)λzn = exp

(βzn,0 +

D∑d=1

K(d)∏j=1

(βi ,d ,jXn,d ,j)norm(Xn,d ,j)

)

Xn|zn ∼ Categorical (pzn,d ,j) , Yn|Xn, zn ∼ Poisson (λzn)

(3–3)

The latent variable, pi ,d ,j , is parametrized by ad ,j and the response comes from a

Poisson distribution parametrized by exp(βX ). Here, norm (Xn,d ,j) = 1, if Xn,d belongs to

the j th category and is zero otherwise. K (d) is the number of category of d th dimension.

Exponential Model

In the exponential model, the generative model of the covariate-response pair is

given by,

38

vi |α1,α2 ∼ Beta(α1,α2)

{λx ,i ,d} ∼ Gamma (λx ,i ,d |ax , bx)

{βi ,d} ∼ Gamma (βi ,d |cy ,d , by ,d)

zn| {v1, v2, .....} ∼ Categorical {M1,M2,M3....}

Xn,d |zn ∼ Exp (Xn,d |λx ,zn,d)

Yn|Xn, zn ∼ Exp

(Yn|βzn,0 +

D∑d=1

βzn,dXn,d

)(3–4)

Here, Xn and Yn represents the continuous response-covariate pairs. {z , v ,λx ,i ,d , βi ,d}

is the set of latent variables and the distributions, {λx ,i ,d} and {βi ,d} are the base distri-

butions of the DP.

Inverse Gaussian Model

In the Inverse Gaussian Model, the covariate and the response is modeled by an

Inverse Gaussian distribution. Here, too vi and zn follow the same distributions as before.

The remainder of the generative model is given by,

{µi ,d ,λx ,i ,d} ∼ N(µi ,d |ax ,d , (bx ,d ,λx ,i ,d)−1

)Gamma (λx ,i ,d |cx ,d , dx ,d)

{βi ,d ,λy ,i} ∼ N(βi ,d |ay ,d , (by ,λy ,i)−1

)Gamma (λy ,i |cy , dy)

Xn,d |zn ∼ IG (Xn,d |µzn,d ,λx ,zn,d)

Yn|Xn, zn ∼ IG

(Yn|βzn,0 +

D∑d=1

βzn,dXn,d ,λy ,zn

)(3–5)

Here, Xn and Yn represents the continuous response-covariate pairs. {z , v ,µi ,d ,λx ,i ,d , βi ,d ,λy ,i}

is the set of latent variables and the distributions, {µi ,d ,λx ,i ,d} and {βi ,d ,λy ,i} are the

base distributions of the DP.

39

Multinomial Probit Model

In the Multinomial Probit model, the continuous covariates are modeled by a

Gaussian mixture and a Multinomial Probit framework is used for the categorical

response. Here, too vi and zn follow the same distributions as before. The remainder

of the generative model of the covariate-response pair is given by the following set of

equations.

{µi ,d ,λx ,i ,d} ∼ N(µi ,d |ax ,d , (bx ,d ,λx ,i ,d)−1

)Gamma (λx ,i ,d |cx ,d , dx ,d)

Xn,d |zn ∼ N(Xn,d |µzn,d ,λ−1

x ,zn,d

)βi ,d ,k ∼ N

(βi ,d ,k |my ,d ,k , s

2y ,d ,k

)λy ,i ,k ∼ Gamma (λy ,i ,k |ay ,k , by ,k)

Y ∗n,k,i |Xn, zn ∼ N

(Yn|βi ,0,k +

D∑d=1

βi ,d ,kXn,d ,λ−1y ,i ,k

)

Yn|Y ∗n,k,zn

∼Y ∗n,k,zn∑K

k=1 Y∗n,k,zn

(3–6)

Here,{z , v ,µi ,d ,λx ,i ,d , βi ,d ,k ,λy ,i ,k ,Y

∗n,k,i

}are the latent variables and the distribu-

tions, {µi ,d ,λx ,i ,d}, {βi ,d ,k}, {λy ,i ,k} and{Y ∗n,k,i

}are the DP base distributions.

Variational Inference

Variational methods in Bayesian setting aims to find some joint distribution of

some hidden variables to approximate a true distribution of the hidden variables and

minimizes the KL divergence between the true/variational distribution. The simple

form of variational distribution is chosen because this can later be used as factorized

distribution and can be sampled from. It can also lead to computational feasibility of

predictive distribution. The likelihood of the model is the sum of a lower bound (obtained

from Jensen’s inequality and a function of a variational distribution parameters) and

the KL divergence of the true and variational distribution. Therefore, maximizing the

40

bound is equivalent to minimizing the divergence (as the likelihood is constant), leading

to the optimal variational parameters. This completes the computation of the variational

distribution.

Variational Distribution of the Models

The inter-coupling between Yn, Xn and zn in all three models described above

makes computing the posterior of Yn analytically intractable. We therefore introduce the

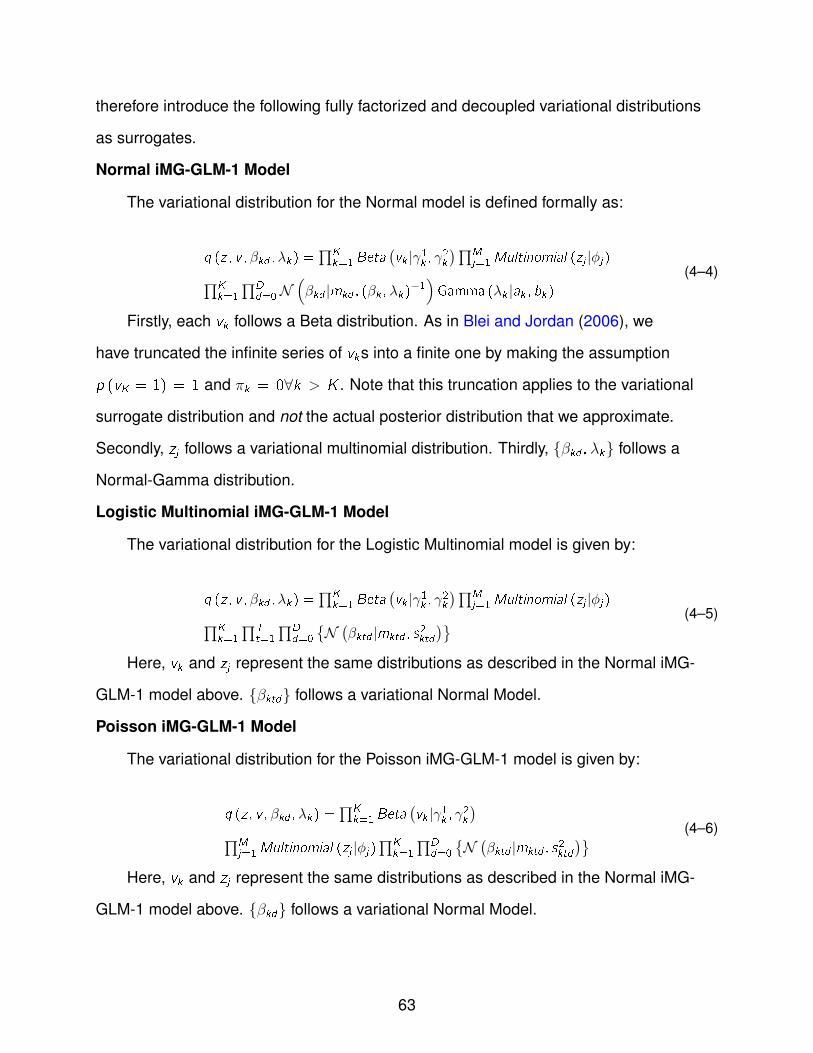

following fully factorized and decoupled variational distributions as surrogates.

Normal Model

The variational distribution for the Normal model is defined formally as:

q (z,v,ηx ,ηy) =T−1∏i=1

q (vi |γi)N∏n=1

q (zn|ϕn)

T∏i=1

D∏d=1

q(µi ,d |mx ,i ,d , (βx ,i ,d ,λx ,i ,d)

−1)q (λx ,i ,d |ax ,i ,d , bx ,i ,d)

T∏i=1

D∏d=0

q(βi ,d |my ,i ,d , (βy ,i ,λy ,i)

−1)q (λy ,i |ay ,i , by ,i)

(3–7)

Firstly, each vi follows a Beta distribution. As in Blei and Jordan (2006), we

have truncated the infinite series of vis into a finite one by making the assumption

q (vT = 1) = 1 and Mi = 0∀i > T . Note that this truncation applies to the variational

surrogate distribution and not the actual posterior distribution that we approximate.

Secondly, zn follows a variational multinomial distribution. Thirdly, ηx = {µi ,d ,λx ,i ,d} and

ηy = {βi ,0 : βi ,D ,λy ,i}, both follow a variational Normal-Gamma distribution.

Logistic Multinomial Model

The variational distribution for the Logistic Multinomial model is given by:

41

q (z,v,ηx ,ηy) =T−1∏i=1

q (vi |γi)N∏n=1

q (zn|ϕn)

T∏i=1

D∏d=1

q(µi ,d |mx ,i ,d , (βx ,i ,d ,λx ,i ,d)

−1)q (λx ,i ,d |ax ,i ,d , bx ,i ,d)

T∏i=1

D∏d=0

K∏k=1

{q(βi ,d ,k |my ,i ,d ,k , s

2y ,i ,d ,k

)}(3–8)

Here, vi and zn represent the same distributions as described in the Normal model.

ηx = {µi ,d ,λx ,i ,d} and ηy = {βi ,0,0 : βi ,D,K} follows a variational Normal-Gamma and a

Normal distribution respectively.

Poisson Model

The variational distribution for the Poisson Model is

q (z,v,ηx ,ηy) =T−1∏i=1

q (vi |γi)N∏n=1

q (zn|ϕn)

T∏i=1

D∏d=1

Dir (pi ,d ,j |ai ,d ,j)T∏i=1

D∏d=0

K(d)∏j=1

q(βi ,d ,j |mi ,d ,j , s

2i ,d ,j

) (3–9)

Here, βi ,d ,j follows a Normal distribution and pi ,d ,j comes from a mixture of varia-

tional Dirichlet distribution.

Exponential Model

The variational distribution for the Exponential model is defined formally as:

q (z,v,λx ,i ,d ,βi ,d) =T−1∏i=1

q (vi |γi)N∏n=1

q (zn|ϕn)

T∏i=1

D∏d=1

q (λx ,i ,d |ax ,i ,d , bx ,i ,d)T∏i=1

D∏d=0

q (βi ,d |cy ,i ,d , dy ,i ,d)

(3–10)

zn follows a variational multinomial distribution. Thirdly, {λx ,i ,d} and {βi ,0 : βi ,D}, both

follow a variational Gamma distribution.

42

Inverse Gaussian Model

The variational distribution for the Inverse Gaussian Model is given by:

q (z,v,µi ,d ,λx ,i ,d ,βi ,d ,λy ,i) =T−1∏i=1

q (vi |γi)N∏n=1

q (zn|ϕn)

T∏i=1

D∏d=1

q(µi ,d |ax ,i ,d , (bx ,i ,d ,λx ,i ,d)−1

)q (λx ,i ,d |cx ,i ,d , dx ,i ,d)

T∏i=1

D∏d=0

q(βi ,d |ay ,i ,d , (by ,i ,λy ,i)−1

)q (λy ,i |cy ,i , dd ,i)

(3–11)

{µi ,d ,λx ,i ,d} and {βi ,0 : βi ,D ,λy ,i} both follows a variational Normal-Gamma distribu-

tion.

Multinomial Probit Model

The variational distribution for the Multinomial Probit Model is

q (z,v,ηx ,ηy) =T−1∏i=1

q (vi |γi)N∏n=1

q (zn|ϕn)

T∏i=1

D∏d=1

q(µi ,d |ax ,i ,d , (bx ,i ,d ,λx ,i ,d)−1

)q (λx ,i ,d |cx ,i ,d , dx ,i ,d)

T∏i=1

D∏d=1

K∏k=1

q(βi ,d ,k |my ,i ,d ,k , s

2y ,i ,d ,k

) K∏k=1

T∏i=1

q (λy ,i ,k |ay ,i ,k , by ,i ,k)

N∏n=1

K∏k=1

T∏i=1

q

(Y ∗n,k,i |βi ,0,k +

D∏d=1

βi ,d ,kXn,d ,λ−1y ,i ,k

)(3–12)

Here, βi ,d ,k follows a Normal distribution. {µi ,d ,λx ,i ,d} and{Y ∗n,k,i ,λy ,i ,k

}follows a

variational Normal-Gamma distribution. βi ,d ,k follows a normal distribution.

Generalized Evidence Lower Bound (ELBO)

We bound the log likelihood of the observations in the generalized form of the

models(same for all the models) using Jensen’s inequality, ϕ (E [X ])≥E[ϕ (X )], where, ϕ

is a concave function and X is a random variable.

43

log {p (X,Y|A)} = log

∫ ∑z

p (X,Y,z,v,ηx ,ηy |A) dvdηxdηy

= log

∫ ∑z

p (X,Y,z,v,ηx ,ηy |A) q (z,v,ηx ,ηy)q (z,v,ηx ,ηy)

dvdηxdηy

≥∫ ∑

z

q (z,v,ηx ,ηy) log {p (X,Y,z,v,ηx ,ηy |A)} dvdηxdηy

−∫ ∑

z

q (z,v,ηx ,ηy) log {q (z,v,ηx ,ηy)} dvdηxdηy

= Eq [log {p (X,Y,z,v,ηx, ηy|A)}]− Eq [log {q (z,v,ηx, ηy)}]

= Eq [log {p (v)}] + Eq [log {p (z|v)}] + Eq [log {p (ηx)}]

+Eq [log {p (ηy)}] + Eq [log {p (X)}] + Eq [log {p (Y)}]

−Eq [log {q (ηx)}]− Eq [log {q (ηy)}]− Eq [log {q (z)}]

−Eq [log {q (v)}]

(3–13)

This generalized ELBO is the same for all the three models under investigation

and it is a function of the variational parameters as well as the hyper-parameters.

We maximize this bound with respect to the variational parameters which gives the

estimates of these quantities. {A} above is the set of hyper-parameters of the generative

model.

Parameter Estimation for the Models

We bound the log likelihood of the observations (same for all the models) using

Jensen’s inequality, ϕ (E [X ])≥E[ϕ (X )], where, ϕ is a concave function and X is a

random variable. This generalized ELBO is the same for all the three models under

investigation and it is a function of the variational parameters as well as the hyper-

parameters. We differentiate the individual ELBOs with respect to the variational

parameters of the specific models to obtain their respective estimates.

44

Parameter Estimation for the Normal Model

We differentiate the derived ELBO above w.r.t. γ1i and γ2i and set them to zero to

obtain estimates of γ1i and γ2i ,

γ1i = α1 +N∑n=1

ϕn,i , γ2i = α2 +N∑n=1

T∑j=i+1

ϕn,j (3–14)

Estimating ϕn,i is a constrained optimization with∑ϕn,i = 1. We differentiate the

Lagrangian w.r.t. ϕn,i to obtain,

ϕn,i =exp (Mn,i)∑T

i=1 exp (Mn,i)(3–15)

The term Mn,i is represented as,

Mn,i =

i∑j=1

{(γ2j)−

(γ1j + γ2j

)}+ Pn,i (3–16)

where,

Pn,i =1

2

D∑d=1

{log(

1

2π

)+(ax ,i ,d)− log (bx ,i ,d)

−β−1x ,i ,d −

ax ,i ,d

bx ,i ,d(Xn,d −mx ,i ,d)

2}+ 1

2{log

(1

2π

)+(ay ,i)− log (by ,i)− β−1

y ,i

(1 +

D∑d=1

X 2n,d

)

−ay ,i

by ,i

(Yn −my ,i ,0 −

D∑d=1

my ,i ,dXn,d

)2

}

(3–17)

The variational parameters for the covariates are found by maximizing the ELBO

w.r.t. them.

45

βx ,i ,d = βx ,d +

N∑n=1

ϕn,i , ax ,i ,d = ax ,d +

N∑n=1

ϕn,i (3–18)

bx ,i ,d =1

2{βx ,d (mx ,i ,d −mx ,d)

2 + 2bx ,d

+

N∑n=1

ϕn,i (Xn,d −mx ,i ,d)2}

(3–19)

mx ,i ,d =

∑N

n=1 ϕn,iXn,d + βx ,dmx ,d∑N

n=1 ϕn,i + βx ,d(3–20)

The variational parameters of the distribution of βi ,d is obtained as,

βy ,i =(D + 1)βy +

∑N

n=1 ϕn,i

(1 +

∑D

d=1 X2n,d

)D + 1

(3–21)

ay ,i =

D∑d=0

ay +1

2

N∑n=1

ϕn,i (3–22)

by ,i =1

2{

D∑d=0

βy (my ,i ,d −my ,d)2 + 2by

+

N∑n=1

ϕn,i

(Yn −my ,i ,0 −

D∑d=1

my ,i ,dXn,d

)2

}

(3–23)

my ,i ,0 =

myβy +∑N

n=1 ϕn,i

(Yn −

∑D

d=1my ,i ,dXn,d

)βy +

∑N

n=1 ϕn,i

(3–24)

46

my ,i ,d =my ,dβy

βy +∑N

n=1 ϕn,iX2n,d

+

∑N

n=1 ϕn,i (Yn −my ,i ,0 +my ,i ,dXn,d)

βy +∑N

n=1 ϕn,iX2n,d

−∑N

n=1 ϕn,i∑D

d=1my ,i ,dXn,d

βy +∑N

n=1 ϕn,iX2n,d

(3–25)

Parameter Estimation for the Multinomial Model

For the Logistic Multinomial Model, the estimation of γ1i , γ2i ,ϕn,i and βx ,i ,d ,mx ,i ,d , ax ,i ,d , bx ,i ,d

are identical to the Normal model with the only difference being that Pn,i is given as,

Pn,i =1

2

D∑d=1

{log(

1

2π

)+(ax ,i ,d)− log (bx ,i ,d)

−β−1x ,i ,d −

ax ,i ,d

bx ,i ,d(Xn,d −mx ,i ,d)

2}

+

K∑k=1

Yn,k

(mi ,0,k +

D∑d=1

Xn,dmi ,d ,k

) (3–26)

And, mi ,0,k = md ,k + s2d ,k∑N

n=1 ϕn,iYn,k

mi ,d ,k = md ,k + s2d ,k

N∑n=1

ϕn,iYn,kXn,d (3–27)

Parameter Estimation for the Poisson Model

Again, in the Poisson Model, estimation of γ1i , γ2i ,ϕn,i , are similar to the Normal

model with the only difference being that the term Pn,i is given as,

Pn,i =

D∑d=1

K(d)∑j=1

Xn,d ,j

((ai ,d ,j)−

(K(d)∑j=1

ai ,d ,j

))

+ {n, i}th term of Eq [log {p (Y|X, z, ηy)}]

(3–28)

47

And, ai ,d ,j = ad ,j +∑N

n=1 ϕn,i . The equation involving mi ,d ,j is

mi ,d ,j

s2d ,j+ exp (mi ,d ,j)

N∑n=1

ϕn,i

(Xn, d , j

s2i ,d ,j

)=

N∑n=1

ϕn,iYnXn,d ,j (3–29)

The expression for Eq [log {p (Y|X, z, ηy)}] is shown in Supplementary Materials.

mi ,d ,j , here, does not have a close form solution. However, it can be solved quickly via

any iterative root-finding method.

Parameter Estimation for the Exponential Model

We differentiate the ELBO w.r.t. γ1i and γ2i and set them to zero to obtain estimates

of γ1i and γ2i ,

γ1i = α1 +N∑n=1

ϕn,i , γ2i = α2 +

N∑n=1

T∑j=i+1

ϕn,j (3–30)

Estimating ϕn,i is a constrained optimization with∑ϕn,i = 1. We differentiate the

Lagrangian w.r.t. ϕn,i to obtain,

ϕn,i =exp (Mn,i)∑T

i=1 exp (Mn,i)(3–31)

The term Mn,i is represented as,

Mn,i =

i∑j=1

{(γ2j)−

(γ1j + γ2j

)}+ Pn,i (3–32)

where,

48

Pn,i =

N∑n=1

T∑i=1

D∑d=1

{(ax ,i ,d)− ln (bx ,i ,d)− Xn,d

ax ,i ,d

bx ,i ,d

}+

N∑n=1

T∑i=1

{−cy ,i ,0

dy ,i ,0−

D∑d=1

Xn,d

cy ,i ,d

dy ,i ,d− Yn

� (cy ,i ,0)

(dy ,i ,0 + 1) cy ,i ,0

+Yn

D∑d=1

� (cy ,i ,d)

(dy ,i ,d + Xn,d) cy ,i ,d}

(3–33)

The variational parameters for the covariates and responses are found by maximiz-

ing the ELBO w.r.t. them.

ax ,i ,d = ax ,d +

N∑n=1