Embed Size (px)

Citation preview

15-16 September 2005 Sofitel, Brisbane AUSTRALIA

Australia's premier coal industry event

Coaltrans Australia 2005 conference highlights:� Leading faculty of Australia’s top coal executives� Choice of three optional post-conference Field Trips:

16-18 September 2005 – Northern & Southern Bowen Basin andHunter Valley mines, ports and rail operations

� Gala Reception and Australian Bush Dinner

Early Bird Discount Save AUD$250 book by 5 August 2005

GOLD SPONSORS SPONSORS OFFICIAL PUBLICATION

SUPPORTERS

Coaltrans Conferencesorganises the world’s largestcoal conferences which attracthundreds of delegates from all

over the world. It also runs regional events,exhibitions, field trips and training courses and has areputation for employing the highest organisationalstandards. Coaltrans is currently planning events inFrance, Canada, Singapore, USA, South Africa, India,Indonesia and China. www.coaltrans.com

The Australian Coal Association (ACA) isthe industry body representing Australia'sblack coal producers. The ACA is formedby the coal company members of the NewSouth Wales Minerals Council and the

Queensland Resources Council. A major ACAobjective is promoting and facilitating the uptake ofclean coal technologies in Australia and COAL21 isat the heart of that development.www.australiancoal.com.au

WCI is a global association of coal enterprises -providing a voice forcoal in internationalpolicy debates onenergy and theenvironment andpromoting awarenessof coal’s importance asa clean, efficient fuel,essential to both thegeneration of theworld’s electricity andmanufacture of theworld’s steel.www.wci-coal.com

In September 2005 Coaltrans Australia will bring to Brisbane the industry’s keyproducers, consumers, traders and shippers – the community that represents theworld’s largest coal exporting nation, now comprising over 30% of global coal exports.

Gearing Up for More ProductionA surge of new mining ventures are under development– with over 18 greenfield and more than 25 brownfieldexpansions being planned for the period 2005-2008.According to AME Mineral Economics this is scheduledto lift production capacity by 87MT to 311MT.

Transport Infrastructure - the critical factorConstraints and bottlenecks at export ports and raildevelopments are major challenges that need to beovercome if Australia is to take advantage of this periodof unprecedented growth. Skills shortages, extendedequipment supply times and strained water resourcespose additional hurdles for industry planners.

What about the Competition?China remains the enigma, as both an exporter andgrowing importer of both metallurgical and thermal coal.For the last two years, it has largely consolidated itsexports at about 85MT, but how long will this last, andhow strong is demand in the internal domestic markets?

Indonesia is set to become the world’s largest exporterof thermal coal in 2005. What threat does this pose toAustralia’s producers?

South Africa, Russia, and to a lesser extent Canadaare all targeting the lucrative Asian market. Whatcompetition do they pose to Australia?

These and many other topics will be discussed atCoaltrans Australia.

AUSTRALIA’S PREMIER COAL

ORGANISED BY THE INDUSTRY

2

INDUSTRY EVENT 15-16 September 2005, Sofitel, Brisbane

COMPLIMENTARY SPOUSE TOURS

THE VENUE

Half Day City Tour of Brisbane – Wednesday 14 September: 0930 – 1230Discover historic Brisbane! Morning tea at RomaStreet Parklands allows travellers to view thebeautiful gardens, boasting wonderful sculpturesthroughout the Parklands. Then travel up to MtCoot-tha for spectacular views of Brisbane.

*Full Day Tour to the Sunshine Coast – Thursday 15 SeptemberHead north from Brisbane to the Australia Zoo,home of ‘The Crocodile Hunter’ and a huge rangeof animals - meet the cuddly koalas, view themajestic birds of prey and feed the kangaroos orcamels. Continue onto Noosa and wander alongcosmopolitan Hastings Street, or visit the NationalPark to see koalas in the wild. The SunshineBeach Surf Club is the place for a classic Aussielunch with fantastic views of the beach, beforereturning to Brisbane in the late afternoon.

OR

*Full Day Tour to O’Reilly’s NationalPark/Mount Tamborine – Thursday 15 September Climb high above the surrounding coastal plain tothe cool rainforests of Lamington Plateau, viaMount Tamborine, with its spectacular views of theGold Coast and glistening waters of the PacificOcean. Then head toward the ‘Green Mountains’of O'Reilly's, traversing old logging tracks andreliving the epic adventures of early settlers.

Enjoy a guided walk through the tree-tops 16metres above the forest floor, looking out for theAntarctic Beach trees and the Bellbirds, Rosellasand Parrots. Travel through Canungra, the oldsawmilling town, now home of the AustralianArmy's Jungle Warfare Training Centre, beforearriving back in Brisbane in late afternoon.

* There will only be one full day tour on 15 September, this will be decided by popular demand

Positioned in one of the city’s most central locations is the magnificent Sofitel Brisbane. Originally the firstinternational hotel in Brisbane, today a 5-star hotel of refined elegance and truly personal service.

The Sofitel has four dining and entertainment venues and an award winning brigade of chefs, asupervised health and fitness centre, sauna and spa, hotel masseur and 12m heated pool, a fullyequipped business centre, babysitting service and hair and beauty salon.

3

WEDNESDAY 14 SEPTEMBER 2005

1700 - 2100 Pre-registration

1830 - 2030 Welcome Reception hosted by Sedgman Pty Ltd Sofitel Hotel

DAY ONE: THURSDAY 15 SEPTEMBER 2005

0700 Registration & Refreshments hosted by TFS Energy

0800 Exhibition opens

0900 WELCOME REMARKSGerard Strahan, Managing Director, Coaltrans Conferences Ltd.

SESSION 1: NEW DEVELOPMENTS IN THE AUSTRALIAN COAL SECTOR

CHAIR: Michael Roche, Chief Executive, Queensland Resources Council

0910 KEYNOTE ADDRESSA SMART FUTURE FOR COAL� Australia's Mining Industry - powering growth in world

markets� Prospects for Queensland's coal industry � Related public and private sector investmentsThe Hon. Peter Beattie, MP, Premier of Queensland &Minister for Trade

0930 CRITICAL SUCCESS FACTORS FOR THEAUSTRALIAN COAL INDUSTRY� People, skills and social infrastructure � Physical infrastructure � Sustainability John Pegler, President, Queensland ResourcesCouncil/CEO, Ensham Resources Pty Limited

0950 STRATEGIC CONSIDERATIONS IN THEDEVELOPMENT OF NEW MINING CAPACITYPeter Coates, Chief Executive Officer, Xstrata Coal

1010 THE POSITIVE OUTLOOK FOR AUSTRALIANCOAL EXPORTS� Strong demand from Asian power and steel sectors drives

Australian export performance � China and India: key determinants for Australian coal

export opportunities� Coal supply capacity and infrastructure issuesBrian Fisher, Executive Director, ABARE

1030 Questions & Answers

1045 Refreshmentshosted by TFS Energy

SESSION 1: NEW DEVELOPMENTS IN THE AUSTRALIAN COAL SECTOR (cont)

CHAIR: Shaun Browne, Executive Chairman, AME Mineral Economics

1115 CHALLENGES FOR AN EXPANDING PRODUCER� Managing a diverse portfolio of developing mining assets� Transport infrastructure issuesTony Haggarty, Managing Director, Excel Coal Ltd.

1135 COAL - TOWARDS A CLEANER TOMORROW� Rio Tinto's position on climate change� The case for coal in the future energy mix� Exciting new technologies and their impact on coal use � Challenges which lie aheadGrant Thorne, Managing Director, Rio Tinto Coal Australia

1155 SOUTHERN QUEENSLAND – FUEL FOR THE FUTURE� Australia’s sub-bituminous ‘A’ coal resources� Increasing demand for high quality, low pollutant

sub-bituminous coalGraeme Robertson, Managing Director, New Hope Corporation Limited

1215 THE COAL21 PROGRAM AND RECENTDEVELOPMENTS IN CLEAN COAL TECHNOLOGIES� Background and current activities of the COAL21 program� Recent developments in advanced power generation and

CO2 capture and storage� The future for coal-based power generation in AustraliaMark O’Neill, Executive Director, Australian Coal Association

1235 Questions & Answers

1245 Lunchhosted by Global Resource Asset Exchange Pty Ltd.

SESSION 2: INNOVATIONS IN BANKING & FINANCE FOR THE COAL INDUSTRY

CHAIR: Shaun Browne, Executive Chairman, AME Mineral Economics

1415 M&A ACTIVITY AND CORPORATE FINANCE IN THECOAL INDUSTRY� How is the structure of the coal industry changing?� What's driving the coal equity market?� What funding opportunities are available?Richard Price, Executive Director, Macquarie Bank

*Commentsfrom previousCoaltrans events

"The most professional conference I have attended"4

CONFERENCE PROGRAMME

"We never had the chance to meet so many contacts under one roof. It also gave us a chance to introduce our company to many new end-users and miners"

1435 TRADE FINANCE IN PERSPECTIVE� Open terms risk on buyers - options to protect your

sales proceeds� Sovereign risk - does it matter?� Letter of credit confirmationsLeigh Pedler & Karen Amos, Executive Managers -Commodities & Trade Finance, Société Générale Australia Branch

1455 Questions & Answers

1500 Refreshmentshosted by TFS Energy

SESSION 3: CHALLENGES FOR THE COAL SUPPLYCHAIN & TRANSPORT INFRASTRUCTURE

CHAIR: Phil Williams, Partner, Accenture Australia Ltd

1530 PARTNERING FOR SOLUTIONS IN THE COAL CHAIN� Investment - meeting future growth� Results and achievements� InnovationRobert Scheuber, Chief Executive, Queensland Rail

1550 THE EXPANSION OF THE DALRYMPLE BAYCOAL TERMINAL� Operating in a regulated environment � Planned expansion of the terminal Chris Chapman, Chief Executive Officer, Prime Infrastructure Management Limited

1610 GROWING PORT CAPACITY IN LINE WITH NEWMINING DEVELOPMENTS � Gladstone/RG Tanna Terminal expansion plans� Potential new coal terminal at Wiggins IslandLeo Zussino, Chief Executive Officer, Gladstone Port Authority

1630 A CO-OPERATIVE MODEL FOR MAXIMISING COAL CHAINCAPACITY: LESSONS FROM THE HUNTER VALLEY� Revolutionising the approach to capacity creation in a

highly fragmented coal chain� Delivering record coal exports while minimising demurrage costs� Ensuring that infrastructure is not a constraint in meeting

export demandAnthony Pitt, General Manager, Hunter Valley CoalChain Logistics Team

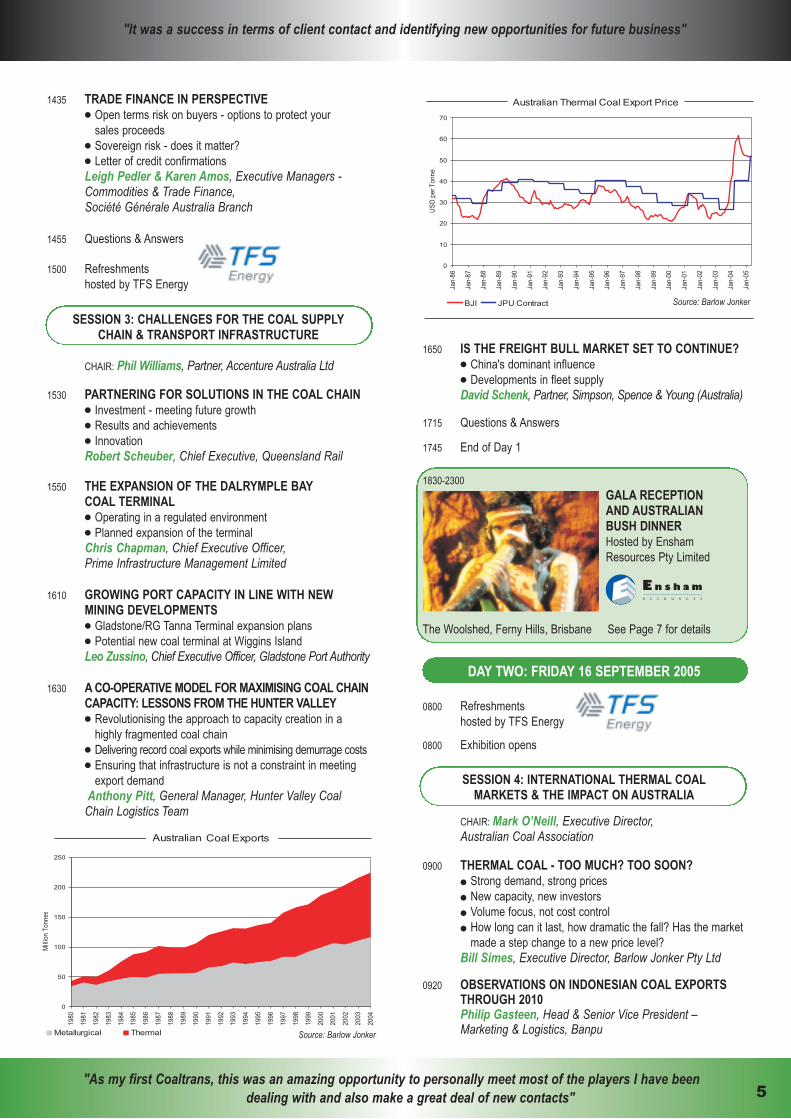

1650 IS THE FREIGHT BULL MARKET SET TO CONTINUE?� China's dominant influence� Developments in fleet supplyDavid Schenk, Partner, Simpson, Spence & Young (Australia)

1715 Questions & Answers

1745 End of Day 1

1830-2300

GALA RECEPTIONAND AUSTRALIAN BUSH DINNERHosted by EnshamResources Pty Limited

The Woolshed, Ferny Hills, Brisbane See Page 7 for details

DAY TWO: FRIDAY 16 SEPTEMBER 2005

0800 Refreshmentshosted by TFS Energy

0800 Exhibition opens

SESSION 4: INTERNATIONAL THERMAL COALMARKETS & THE IMPACT ON AUSTRALIA

CHAIR: Mark O’Neill, Executive Director,Australian Coal Association

0900 THERMAL COAL - TOO MUCH? TOO SOON?� Strong demand, strong prices� New capacity, new investors� Volume focus, not cost control� How long can it last, how dramatic the fall? Has the market

made a step change to a new price level?Bill Simes, Executive Director, Barlow Jonker Pty Ltd

0920 OBSERVATIONS ON INDONESIAN COAL EXPORTSTHROUGH 2010Philip Gasteen, Head & Senior Vice President –Marketing & Logistics, Banpu

"It was a success in terms of client contact and identifying new opportunities for future business"

"As my first Coaltrans, this was an amazing opportunity to personally meet most of the players I have beendealing with and also make a great deal of new contacts" 5

0

50

100

150

200

250

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

MillionTonnes

Metallurgical Thermal

Australia Coal Exports

0

10

20

30

40

50

60

70

Jan-86

Jan-87

Jan-88

Jan-89

Jan-90

Jan-91

Jan-92

Jan-93

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

USDperTonne

BJI JPU Contract

Australian Thermal Coal Export Price

Source: Barlow Jonker

Source: Barlow Jonker

Australian

0940 COAL PURCHASING STRATEGIES FOR KOREA� Electricity demand growth for Korea� Coal's role in the Korean energy mix� Australia's importance as a long-term supplierY.J.Lee, Team Leader/Senior Manager, Fuel Team,KOSEP

1000 PROSPECTS FOR ASIAN COAL-FIRED GENERATION� Can coal compete with LNG?� Who will build new coal-fired capacity, and where?� How much of the capacity will use imported coal?Martin Daniel, Editor – Power in Asia, Platts

1020 THE ELECTRICITY SUPPLY / DEMAND OUTLOOK INAUSTRALIA TO 2020� An assessment of the timing and extent of new generation

needs� Identification of the key challenges needing resolution to

support large scale capital investment Brad Page, Chief Executive Officer, Energy Supply Association of Australia

1040 Questions & Answers

1100 Refreshmentshosted by TFS Energy

SESSION 5: COKING COAL – HOW LONG WILL THE BOOM LAST?

CHAIR: Stephen Gye, Executive Director, Barlow Jonker Pty Ltd.

1130 THE OUTLOOK FOR AUSTRALIAN METALLURGICALCOAL MARKETS: SUPPLY, DEMAND AND LOGISTICS� Will recent price settlements encourage excess of supply in

metallurgical coal markets?� How long will logistical constraints be an issue in matching

supply with demand?� Can strong demand be sustained at current coal and

steel prices?Dr Peter Richardson, Global Metals & Mining Strategist& Head of Global Commodity Research, Deutsche BankGlobal Research

1150 AN INDIAN INVESTOR’S VIEW OF COKING COALMINING PROSPECTS IN AUSTRALIAArun Kumar Jagatramka, Vice Chairman & ManagingDirector, Gujarat NRE Coke Ltd, India

1210 NORTH EAST BRITISH COLUMBIA - AN EMERGINGCOMPETITOR TO AUSTRALIAN COAL� A review of existing Canadian production� Rapid growth and expansion potential of low volatile PCI

and hard coking coal Gary K. Livingstone, President, Western Canadian Coal

1230 COKING COAL OUTLOOK FOR THE INDIAN STEELINDUSTRY� Expansion of the Indian steel industry� Strategic options for metallurgical coal procurementK.K. Khanna, Technical Director, Steel Authority of India Ltd

1250 Questions & Answers

1300 Lunchhosted by Macquarie Bank

SESSION 6: COAL TRADING & RISK MANAGEMENT

CHAIR: Kevin Gallagher, Chief Representative, Sumitomo Coal

1415 THE CHANGING COAL MARKET - FROM THEBEGINNING TO NOW� The history of coal derivatives so far� Drivers for a successful coal swap market � Why we need coal swaps

- How derivatives can be used- An example for the producer and consumer

Mike Hopkins, Energy Marketing Manager, TFS, Australasia

1435 THE ROAD TO COAL COMMODITISATION IN THE PACIFIC� What is coal commoditisation?� Should we even be travelling this road - does it take us to

the wrong destination?� Trade-offs between security of supply and flexibility� Does commoditisation mean increased risk?� How long is this journey going to take?Jeremy Peters, Director, Constellation Energy

1455 FINANCIAL COAL SWAPS - GROWING IN IMPORTANCE� Relative size of coal markets versus gas, power and crude� Users of financial coal swaps growing steadily in Europe� Increased liquidity and the importance of index linked

physical transactionsJames Morrison, Head of Commodities – Asia Pacific,Barclays Capital

"The speakers chosen were excellent and the perspective of coal planning and supply was very well handled."

"The event was well organised, focussed on the key issues and highly enjoyable"6

0

20

40

60

80

100

120

140

Jan-86

Jan-87

Jan-88

Jan-89

Jan-90

Jan-91

Jan-92

Jan-93

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

USDperTonne

Australian Hard Coking Coal Export Price

Source: Barlow JonkerJSM Contract

1515 EMISSIONS TRADING FOR THE COAL INDUSTRY:NOT WHY BUT WHEN� Obtaining credits at lowest cost � Differentiating credit classes � Why forest plantations are good for coal � Trading risks � Hedging over a 30 year period: strategies and options Andrew Grant, Managing Director, CO2 Australia Limited

1535 Questions & Answers

1545 Refreshmentshosted by TFS Energy

SESSION 7: MINING OPERATIONS & ECONOMICS

CHAIR: Stewart Butel, Director Coal Operations, Wesfarmers Energy

1600 AUSTRALIAN LONGWALLS - WHERE TO FROM HERE?� Australian longwall performance� Why don't we do better?� Is more power, technology or capital the answer?Brian Nicholls, Mining Engineer, Brian Nicholls Mining Consultants

1620 CAN TODAY’S PROJECTS SURVIVE WHEN PRICES FALL?� Developers are hustling new projects, but record prices

won’t last � Is coking coal pricing now different to steam and PCI coal?� Can today’s projects survive? How much new infrastructure

is needed? Professor Donald W. Barnett, Managing Director, MINEC Pty Ltd.

1640 LONGWALL TOP COAL CAVING AND ITS APPLICATIONFOR AUSTRALIA’S COAL MINING INDUSTRY� Chinese investor reviews their new Australian operations� Mine start-up plans, recovery and new technologyLia Cunliang, Managing Director, Yancoal Australia

1700 Questions & Answers

1715 End of Conference

1800 Departure for Post-Conference Field Trips

"Extremely well run and organised with a very good venue and facilities"

Gala Reception andAustralian Bush DinnerBack to the Future Spectacular

Thursday 15 September 2005 1900-2300

hosted by Ensham Resources Pty Limitedto celebrate Ensham's 50 Millionth Tonne

of Production

To mark production of its 50 millionth tonne, Ensham Resources ishosting an Australian Bush Dinner and entertainment extravaganza,featuring indigenous Australian performers, art and music, all within thesetting of a typical Australian wool shed. The evening promises to befull of fun and surprises, and will include a celebrity auction for charity.

Venue: The Woolshed, Ferny Hills, BrisbaneDress: Smart/Casual

Attendance is complimentary to all delegates and their partners

Programme1830 - Depart Sofitel to Ferny Hills1900 - Gala Reception begins1930 - Australian Bush Dinner2030 - Dazzling Entertainment Programme2200 - Guest speaker – Nick Farr-Jones, Managing

Director Mining Finance, Société GénéraleAustralia Branch & Wallaby and Rugby World Cup Captain

- Charity Auction of Ensham's 50 Millionth Tonne and a selection of memorabilia items

2300 - Depart for Brisbane

"Coaltrans was a well managed event covering most of the contemporary issues facing the coal sector.Participation as well as management of the event were world class"

7

FIELD TRIP A – NORTHERN BOWEN BASIN – QUEENSLAND

MINES

Burton Coal Mine

Burton Mine was established in 1996 as a high qualitycoking coal mine with production now exceeding 4MTp/a. Burton Mine is a successful Joint Venture

arrangement with 95% ownership by Peabody Energy and 5% by Thiess, withoperational responsibility for mining, coal preparation, haulage and rail loadingof the coal. The coal seams range in thickness from 6-11 metres and dip to thesoutheast at approximately 22 degrees, which requires a special extractiontechnique called terrace mining. This optimises production and providesflexibility in terms of the number of working platforms at different elevations,thus less risk of being interrupted by flooding after heavy rain.

Hail CreekHail Creek is an open cut coking coal mine operating nearMackay in Central Queensland with approximately 250employees. After opening in 2003, Hail Creek's productionin 2004 totalled 5.1MT, for markets in Japan, Korea,

Taiwan, India, Europe, China and Brazil. An A$338million expansion of theoperation, taking capacity to 8MT p/a, has recently begun, and studies for optionsbeyond that capacity are also underway. Hail Creek is a joint venture between RioTinto (82%), Nippon Steel Corporation (8%), Marubeni Coal Pty Ltd (6.33%) andSumisho Coal Development Queensland Pty Ltd (3.67%).

Millennium Now under construction, this new open-cut coking coalmine is set to produce 1.5MT initially, starting in 2006 andbuilding up to 3MT in 2007. It is located 25km SE ofMoranbah, is owned 86% by Excel and involves a jointventure with BHP Mitsui Coal. Delegates will be able tosee the ongoing developments at the mine, including mineand coal preparation infrastructure construction.

PORTS

Dalrymple Bay Coal Terminal (DBCT)

DBCT was established in 1983 by the QueenslandGovernment as a common User coal export facility. Theterminal is linked to the Bowen Basin coalfields by theelectrified Goonyella rail system operated by QR. DBCT

exports approximately 52MT p/a of PCI, thermal and coking coal, making itQueensland's largest export coal terminal. DBCT currently has 9 major miningcustomers of which 7 are operating 11 local mines. The terminal is a significantcommon-user facility with a large number of users and its operation is uniquecompared to other coal terminals.

Hay Point Terminal

Hay Point Coal Terminal, located 38km south ofMackay, Queensland, is one of the world’s largest andmost efficient coal receival, stockpiling and shippingfacilities. Operated by Hay Point Services for the BHP

Billiton Mitsubishi Alliance (BMA), the terminal is currently being upgraded toincrease annual throughput capacity by 6MT tonnes to 40MT p/a. Hay PointCoal Terminal is a key link in BMA’s plan to capture a major share of theforecast strong growth

8

POST-CONFERENCE FIELD TRIPS16-18 September 2005

Coaltrans Australia 2005 will be followed by a choice of three optional Field Trips, to give delegates theopportunity to visit mines, ports and rail operations, and see at first hand new mining and infrastructuredevelopments within Australia’s coal industry.

Why participate in these Field Trips?A Coaltrans Field Trip will provide you with:

� A unique opportunity to meet exclusively with senior management � Comprehensive visits to mine, port and rail facilities� Social activities and networking

OUTLINE ITINERARYFriday 16 September 2005Evening flight, Brisbane-MackayStay overnight at Mackay

Saturday 17 September 2005Site visit by coach to:1. Hail Creek, hosted by Rio Tinto2. Burton, hosted by Peabody Coal3. Millennium, hosted by ExcelDinner and stay overnight at Mackay

Sunday 18 September 2005AM: Site visit to Hay Point Terminal, hosted by BMASite visit to Dalrymple Bay Coal Terminal, hosted by Prime IndustriesPM: Flight from Mackay to Brisbane

Post-Conference Field Trips

Delegate fees

AUD$2,985 + 10% GST = AUD$3284

The delegate fee covers: - Flights from Brisbane- All ground transportation- Overnight accommodation and all meals on September 16-18

Please note that places on Field Trips are limited and allocatedon a strictly first-come first-served basis. Field Trips are subjectto a minimum number of registered delegates.

Please register on page 12

FIELD TRIP B – SOUTHERN BOWEN BASIN - QUEENSLAND

MINES

Blair Athol

Blair Athol is Australia's largest export thermal coalmine, operating near Clermont in Central Queenslandwith approximately 180 employees. Mining at Blair Atholis from a single seam up to 30 metres thick, and

production in 2004 totalled 12.2MT. Power utilities in Japan use over 6MT ofBlair Athol Mine coal every year, and more than 5MT is sold to customers inAsia, Europe, the Middle East and South America. Blair Athol is a jointventure between Rio Tinto (57.2%), Leichhardt Coal (31.4%) (which is acompany owned by Uni Super, Rio Tinto and EPDC (Australia) Pty Ltd),Japanese power utilities EPDC (Australia) Pty Ltd (8%) and JCD AustraliaPty Ltd (3.4%).

Ensham Mine Ensham is on the move - from 8MT p/a in 2004of thermal and semisoft coal from dragline andtruck/shovel operations, to 20MT p/a in 2009from expanded surface and new underground

operations. The Ensham coal resource contains more than 1bn tonnes of highenergy coal, mostly saleable without beneficiation. Skilled employees, workarrangements with a residential village and flexible work practices providebenchmark productivity and reliability of supply.

Rolleston Rolleston Coal Mine is an A$516 million project that is currentlybeing developed to commence operation in the final quarter of2005. It is a long-life, open-cut, export and domestic thermal coaloperation located in the Bowen Basin, in Central Queensland.The mine will produce some 1MT in 2005, with full production

of 6MT for export per annum (mtpa) and 2MT of domestic production expectedin 2008.

PORTS

Port of GladstoneCentral Queensland Ports Authority (CQPA) is responsible forthe management of both the Port of Gladstone and Port Alma.The Port of Gladstone is Queensland’s largest multi-commodityport and is home to the world’s fifth largest coal export terminal– the RG Tanna Coal Terminal. Both port centres serve CentralQueensland’s major industries through the import of materialssuch as bauxite and ammonium nitrate and the export of

products including coal, alumina, and meat products.

FIELD TRIP C – HUNTER VALLEY - NSW

MINES

Bulga Complex Xstrata Coal’s Bulga Complex, comprising Beltana highwallunderground mine and Bulga open cut, produces export thermaland semi soft coal. In 2004, Bulga Complex produced almost9MT of product coal, with the coal preparation plant handling13.5MT of ROM coal. Beltana is the most cost-effective and

highest producing longwall mine in Australia. In 2004, its first full year ofproduction, Beltana produced almost 6MT of ROM coal.

Mount Arthur North Mt Arthur Coal is a large open cut coal mine less than 5km fromthe town of Muswellbrook. The mine is located in the UpperHunter region of New South Wales and is surrounded by ruralproperties, horse studs, vineyards, olive groves and residential

suburbs. Integrating operations in a sympathetic manner with our neighbours is a keyphilosophy of the operation. The mine will produce up to 15MT p/a of raw energy coalwhen full production is achieved in 2006, for domestic and export markets.

Wambo Wambo is Excel Coal’s largest operating mine, and the open cutmining operations are contracted to Roche Mining, and will produceapproximately 5MT of ROM coal in 2005. The quality andconsistency of its coal has gained wide market acceptance

amongst the major Japanese power utilities for over 20 years. Wambo is currentlybeing expanded, with a 15km rail spur and loop and associated clean coal handlingand rail loading facilities. New mining equipment in 2005 will increase open cutproduction capacity by around 40%. Plans are also well advanced for developing a2MT p/a longwall mine in the Wambo Seam, accessible from the open cut highwall.

PORTS

Port Waratah Coal Terminal Port Waratah Coal Services Limited operates two terminals:Carrington and Kooragang and receives, assembles and loads HunterValley coal for export to customers around the world. Drawing on lessthan 20 diverse coal suppliers and using sophisticated blending andquality control techniques, PWCS is a world leader in coal handling

and works closely with coal exporters, rail and port organisations to improvecommunication and joint planning within the Hunter coal handling industry. A$170m ofcapital expenditure to increase throughput at PWCS to 102MT by Q4 2007 hasrecently been approved. Plans are also afoot to boost overall capacity to 120MT.

Hunter Valley Coal Chain Logistics Team Presentation on the operation of the HVCCLT, its planningprocesses and business model.- An overview on the Hunter Valley Coal Chain performanceand outlook for capacity in the Hunter Valley Coal Chain overthe next ten years

- Walk through of the office facility and planning approach - Demonstration of the new technology being developed for the HVCCLT. This is aconstraint based planning and scheduling system that will ultimately manage all coalthrough the largest coal export chain in the world.

9

OUTLINE ITINERARY

Friday 16 September 2005Flight, Brisbane-EmeraldStay overnight Emerald

Saturday 17 September 2005Site visits by coach to:1. Blair Athol, hosted by Rio Tinto2. Ensham Mine, hosted by Ensham ResourcesStay overnight, Emerald

Sunday 18 September 2005AM: Site visit to Rolleston, hosted by Xstrata CoalPM: Flight – Emerald to GladstoneSite visit to Port of GladstoneFlight from Gladstone to Brisbane

OUTLINE ITINERARYFriday 16 September 2005Evening flight, Brisbane-NewcastleStay overnight Hunter Valley

Saturday 17 September 2005Site visits by coach to:1. Bulga Complex, hosted by Xstrata Coal2. Wambo, hosted by Excel3. Mount Arthur North, hosted by BHP Billiton Stay overnight Hunter Valley

Sunday 18 September 2005AM: Site visit to Port Waratah PM: Departure for Sydney/Newcastle/Brisbane

See page 10 for Field Trip location map

10

Field Trip location map (see page 8-9 for field trip details)

Field Trip A

POST-CONFERENCE FIELD TRIPS16-18 September 2005

Field Trip B

Field Trip C

SPONSORSHIP AND EXHIBITION

Sponsorship and exhibition stand opportunitiesEnhance your market position by taking one of these businessdevelopment options

SPONSORSHIP

EXHIBITION STANDS

Sponsorship at Coaltrans Australia is a prime opportunity toraise your company’s profile. You will receive increasedexposure to senior energy industry representatives andcompanies operating in Australia.

Sponsorship options include Platinum, Gold, Silver orBronze options, each of which come with attendant benefits.There are also a variety of other sponsorship choices,which incorporate all budget needs and commercialrequirements.

The Coaltrans Australia exhibition will be located in an areaadjacent to the main conference auditorium, and will be thecentral focus for refreshment breaks, with meeting areas toallow maximum contact with delegates. Stand spaces areavailable in 6sqm, 9sqm and 18sqm packages. Pre-builtstands are designed to allow you to exhibit with the minimumof effort. This is the ideal opportunity to establish newbusiness contacts and promote new products or services tothe coal and energy markets.

To make enquiries and receive a detailed sponsorshippackage or stand details, please contact: AlastairMacDonald, Coaltrans Conferences, Nestor House, Playhouse Yard, London EC4V 5EX, United Kingdom. Tel: +44 20 7779 8917, Fax: +44 20 7779 8946, Email: [email protected] Web: www.coaltrans.com

Sponsors as of 27 May 2005

GOLD SPONSORS

CO-ORGANISERS SUPPORTERS OFFICIAL PUBLICATION

SPONSORS

11

Exhibition Floor plan

x Stands reserved as at 27 May 2005

Post: Coaltrans Conferences Ltd

Nestor House, Playhouse Yard London EC4V 5EX, UK

Four other waysto register

Fax:

+44 20 7779 8946

Telephone: +44 20 7779 8945

(quoting brochure ref:)

The easiest way to register is online at www.coaltrans.com/australia

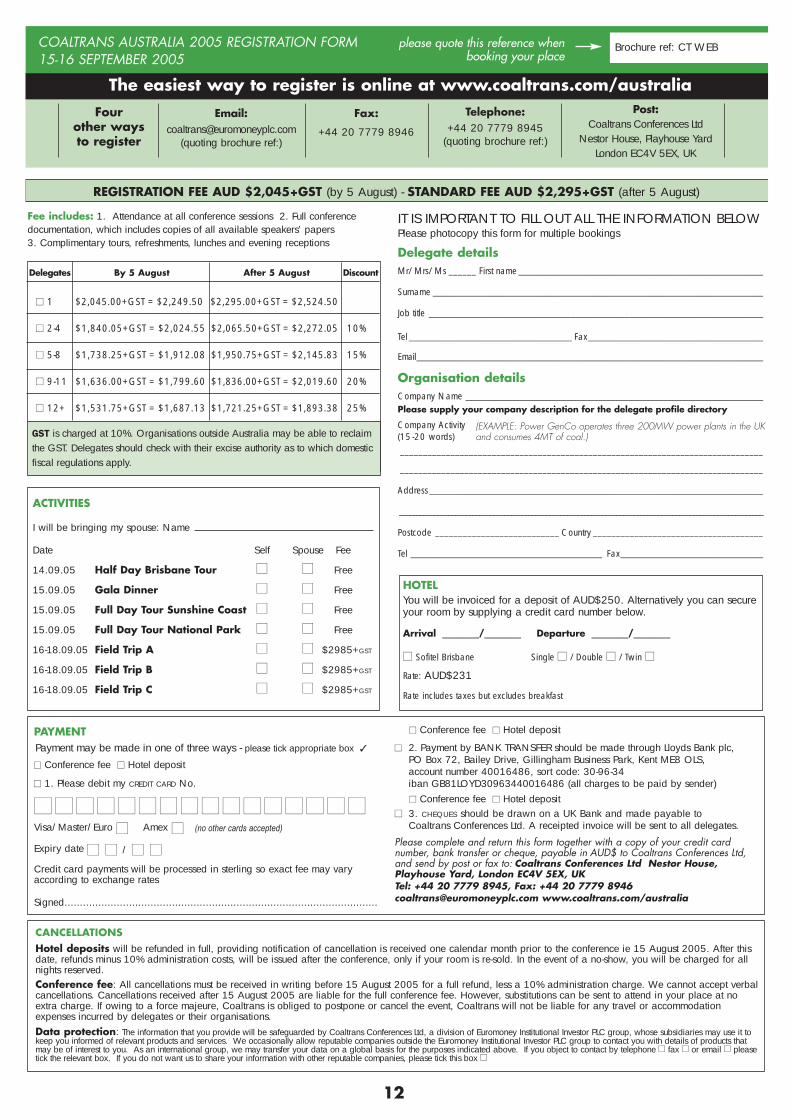

REGISTRATION FEE AUD $2,045+GST (by 5 August) - STANDARD FEE AUD $2,295+GST (after 5 August)

Fee includes: 1. Attendance at all conference sessions 2. Full conferencedocumentation, which includes copies of all available speakers’ papers 3. Complimentary tours, refreshments, lunches and evening receptions

Brochure ref: CT WEB

Delegates By 5 August After 5 August Discount

�� 1 $2,045.00+GST = $2,249.50 $2,295.00+GST = $2,524.50

�� 2-4 $1,840.05+GST = $2,024.55 $2,065.50+GST = $2,272.05 10%

�� 5-8 $1,738.25+GST = $1,912.08 $1,950.75+GST = $2,145.83 15%

�� 9-11 $1,636.00+GST = $1,799.60 $1,836.00+GST = $2,019.60 20%

�� 12+ $1,531.75+GST = $1,687.13 $1,721.25+GST = $1,893.38 25%

please quote this reference whenbooking your place

COALTRANS AUSTRALIA 2005 REGISTRATION FORM15-16 SEPTEMBER 2005

12

ACTIVITIES

I will be bringing my spouse: Name

Date Self Spouse Fee

14.09.05 Half Day Brisbane Tour �� �� Free

15.09.05 Gala Dinner �� �� Free

15.09.05 Full Day Tour Sunshine Coast �� �� Free

15.09.05 Full Day Tour National Park �� �� Free

16-18.09.05 Field Trip A �� �� $2985+GST

16-18.09.05 Field Trip B �� �� $2985+GST

16-18.09.05 Field Trip C �� �� $2985+GST

IT IS IMPORTANT TO FILL OUT ALL THE INFORMATION BELOWPlease photocopy this form for multiple bookings

Delegate detailsMr/Mrs/Ms ______ First name ____________________________________________________________

Surname _________________________________________________________________________________

Job title __________________________________________________________________________________

Tel ________________________________________ Fax___________________________________________

Email_____________________________________________________________________________________

Organisation detailsCompany Name __________________________________________________________________________Please supply your company description for the delegate profile directory

Company Activity (15-20 words)_______________________________________________________________________________

_______________________________________________________________________________

Address ___________________________________________________________________________________

________________________________________________________________________________________________________

Postcode ___________________________ Country _____________________________________

Tel _______________________________________________ Fax___________________________________

PAYMENTPayment may be made in one of three ways - please tick appropriate box �

�� Conference fee �� Hotel deposit

�� 1. Please debit my CREDIT CARD No.

�� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��Visa/Master/Euro �� Amex �� (no other cards accepted)

Expiry date �� �� / �� ��Credit card payments will be processed in sterling so exact fee may varyaccording to exchange rates

Signed......................................................................................................

�� Conference fee �� Hotel deposit

�� 2. Payment by BANK TRANSFER should be made through Lloyds Bank plc, PO Box 72, Bailey Drive, Gillingham Business Park, Kent ME8 OLS, account number 40016486, sort code: 30-96-34 iban GB81LOYD30963440016486 (all charges to be paid by sender)�� Conference fee �� Hotel deposit

�� 3. CHEQUES should be drawn on a UK Bank and made payable toCoaltrans Conferences Ltd. A receipted invoice will be sent to all delegates.

Please complete and return this form together with a copy of your credit cardnumber, bank transfer or cheque, payable in AUD$ to Coaltrans Conferences Ltd,and send by post or fax to: Coaltrans Conferences Ltd Nestor House,Playhouse Yard, London EC4V 5EX, UK Tel: +44 20 7779 8945, Fax: +44 20 7779 [email protected] www.coaltrans.com/australia

GST is charged at 10%. Organisations outside Australia may be able to reclaimthe GST. Delegates should check with their excise authority as to which domesticfiscal regulations apply.

HOTELYou will be invoiced for a deposit of AUD$250. Alternatively you can secureyour room by supplying a credit card number below.

Arrival ________/________ Departure ________/________

�� Sofitel Brisbane Single �� /Double �� /Twin ��

Rate: AUD$231

Rate includes taxes but excludes breakfast

Email: [email protected]

(quoting brochure ref:)

(EXAMPLE: Power GenCo operates three 200MW power plants in the UKand consumes 4MT of coal.)

CANCELLATIONSHotel deposits will be refunded in full, providing notification of cancellation is received one calendar month prior to the conference ie 15 August 2005. After thisdate, refunds minus 10% administration costs, will be issued after the conference, only if your room is re-sold. In the event of a no-show, you will be charged for allnights reserved.Conference fee: All cancellations must be received in writing before 15 August 2005 for a full refund, less a 10% administration charge. We cannot accept verbalcancellations. Cancellations received after 15 August 2005 are liable for the full conference fee. However, substitutions can be sent to attend in your place at noextra charge. If owing to a force majeure, Coaltrans is obliged to postpone or cancel the event, Coaltrans will not be liable for any travel or accommodationexpenses incurred by delegates or their organisations.Data protection: The information that you provide will be safeguarded by Coaltrans Conferences Ltd, a division of Euromoney Institutional Investor PLC group, whose subsidiaries may use it tokeep you informed of relevant products and services. We occasionally allow reputable companies outside the Euromoney Institutional Investor PLC group to contact you with details of products thatmay be of interest to you. As an international group, we may transfer your data on a global basis for the purposes indicated above. If you object to contact by telephone �� fax �� or email �� pleasetick the relevant box. If you do not want us to share your information with other reputable companies, please tick this box ��