Embed Size (px)

Citation preview

6-7 March 2006The Taj Palace HotelNew Delhi

India’s premier coal industry event

Coaltrans India 2006 will examine:� The drive to achieve energy security � Key import markets for India, and opportunities for overseas investment� Development of the major coal consuming industries in India� Challenges in port infrastructure, coal transport and logistics

Plus: Pre-conference networking and social programmePlus: New dedicated conference stream looking at Coal Mine

Operations and EconomicsPlus: Delegate e-Message Communications SystemPlus: Networking Breakfast

Early Bird Discount Save 10% book by 27 January 2006

GOLD SPONSOR

SILVER SPONSORS

GENERAL SPONSORS

BRONZE SPONSOR

SUPPORTERS

PLATINUM SPONSORS

OFFICIALPUBLICATION

Coaltrans India 2006 will focus on theprincipal challenges facing the Indiancoal markets, both from the producers’and consumers’ perspectives. Keysessions will focus on the overwhelmingneed to reduce stock shortages and thesteps being taken to achieve this.Focused presentations will consider thechallenges of building a competitivecoal market in India, raising productionin an environmentally sustainable way,and the critical need to ensure energysecurity through strategic overseasinvestment.

Coaltrans India 2006 will examine all thecrucial issues pertinent to the future of theIndian coal producing and consumingindustries, including:

� Expected growth and development ofthe Indian steel industry

� Availability of coking coal to the Indiansteel industry

� Development of the power industry –the consumers perspective

� Key markets for imports to India� Potential role of coal bed methane in

satisfying India’s energy needs� Consolidation in the cement industry,

and likely impact on coal demand� Creating efficiencies in port

infrastructure, coal transport andlogistics

The development of the Indian economy is leading to a boom in coalimports as India fights to secure energy for its future. Major consumersare looking to new markets for supply, whilst Australia, Indonesia andSouth Africa are taking on increasing importance. New sources of coalsupplies are being sought as Indian coal consumers push to acquireoverseas mining rights, as well as seeking allocations of new domesticcoal blocks for development under newly liberalised licensing proposals.

For FY-06, Coal India is expected to produce 363mt of coal. However,current projections indicate that India could face an 80mt/year shortfall incoal supplies by 2011, compared to today’s estimated shortfall of 20mt.

2

6-7 March 2006, The Taj Palace Hotel, New Delhi

3

The Taj Palace Hotel, New DelhiLocated in the diplomatic area,the hotel is 20 minutes from theairport and a short distance tothe city centre. In a survey thehotel has been named "The BestBusiness Hotel in India" and is amember of The Leading Hotels ofthe World.

NEW FOR COALTRANS INDIA 2006

Dedicated stream - MineOperations and EconomicsThis new optional half-day session (seepage 8) will cover coal production, contractmining, coal processing and economics. Theprogramme features a faculty of expertswho will review major developments in themining sector and give delegates a first-hand opportunity to understand current bestmining practices. Delegates can choose to attend this, or theparallel conference programme on shippingand infrastructure at no extra cost. (Pleasestate your choice when you register, page 10)

Delegate e-MessageCommunications SystemThis will enable delegates to contact eachother via email on-site at Coaltrans India

2006. Multiple terminals will be providedin the Coaltrans Exhibition area, and anonline Company Profile directory ofregistered attendees will be available toassist delegates in setting up meetings.This directory will also be available in thedelegate documentation. When youregister please ensure you complete theCompany Profile section (see Registrationpage 10) with a short description of yourorganisation, to a maximum of 20 words.

Networking Breakfast Networking breakfast with roving microphone(Delegates will have the opportunity tobriefly introduce themselves to their fellowconference attendees to enable them tomake additional business contacts at theconference.)

About the Organisers:Coaltrans Conferences organises large-scale internationalcoal conferences, which attract delegates from all over theworld. It also runs focused regional events, exhibitions, fieldtrips and training courses. It has a reputation for employingthe highest organisational standards. Coaltrans Conferencesis running events in 2006 in Brazil, China, Greece,Indonesia, South Africa, the UK and the USA.

SUNDAY 5 MARCH 2006

1000 – 1600COMPLIMENTARY SIGHTSEEING TOUR OF NEW & OLD DELHISightseeing tour of Old Delhi includes a drive along Red Fort; visit to theJama Masjid and the Chandni Chowk where you can feel the hustle &bustle of everyday life; lunch at a speciality restaurant and a visit to theRaj Ghat – memorial of Mahatma Gandhi, Father of the nation.

1600 – 1800PRE-CONFERENCE REGISTRATION

1900 WELCOME EVENING RECEPTIONSponsored by Merrill Lynch Commodities

CONFERENCE PROGRAMME

DAY 1: MONDAY 6 MARCH 2006

0730 RegistrationPre-conference refreshments sponsored by SSM

0800 Exhibition opens

0900 WELCOME AND OPENING REMARKSGerard Strahan, Managing Director, Coaltrans Conferences

SESSION 1: OPENING KEYNOTES

0910 GOVERNMENT PLANS FOR THE INDIAN COALINDUSTRYHonourable Dr Dasari Narayan Rao, Minister of State for Coal and Mines

0930 COAL INDIA - FUTURE VISION� Present and future production and energy generation plans� Developing new coal blocks� Spot market opportunities� Overseas coal mine investment opportunities� Coal India as the role model for the industryShashi Kumar, Chairman, Coal India Limited

0950 INDIA’S ROLE IN A CLEANER WORLD � The role for cleaner coal technologies� Carbon capture and sequestration� The international architecture of climate changeMilton Catelin, Chief Executive, World Coal Institute

1010 COAL – TOWARDS A CLEANER TOMORROWGrant Thorne, Managing Director, Rio Tinto CoalAustralia

1030 Refreshment breakSponsored by SSM

SESSION 2: TRENDS IN INDIAN AND GLOBALENERGY MARKETS

Chair: M.K Palanivel, Sr. Vice President - All India (Bulk & Tramp Division), Samsara Group

1100 INDIA AND THE GLOBAL ENERGY MARKETS� The global grab for energy� India as a competitor for energy assets/resources in the

global marketBishal Thapa, Managing Director, ICF Consulting(India)

1120 TRENDS IN WORLD COAL MARKETS ANDINDIAN COAL INDUSTRY OVERVIEW� Dynamics of the global coal market, price volatility

and freight� View on how coal production, consumption and pricing

trends impact the Indian market� Dynamics of the Indian coal market � Assessment of current import markets for India and

potential opportunities Robin Griffin, Senior Consultant, Barlow Jonker

SESSION 3: COKING COAL AND STEEL INDUSTRY

Chair: Rajiv Vohra, Director, SGK Consultants Pvt Ltd

1140 INDIAN STEEL INDUSTRY – EXPECTEDGROWTH AND DEVELOPMENT� Future for the steel industry in India – plans for growth� Ensuring security of raw material supplies for the

steel industry� Key markets for coking coal around the world � Availability of coking coal to the Indian consumer� Recent price volatility and possible trends for the futureRajiv Vohra, Director, SGK Consultants Pvt Ltd

1155 DEVELOPMENTS IN THE GLOBAL COKING COALMARKET AND THE IMPLICATIONS FOR INDIA� Overview of world markets� Freight constraints from marginal markets – economics of

imports from distant markets� USA – growth in demand in India for US coal and petcoke� Russia� New Zealand as an alternative to Australian coalRonnie Cecil, Senior Consultant Steelmaking RawMaterials, CRU Analysis

*Comments fromCoaltrans India2005 participants

"Coaltrans was a well managed event covering most of the contemporary issues facing the coal sector. Participation as well as management of the event were world class"4

PRE-CONFERENCE PROGRAMME

"Excellent platform for new opportunities in coal for users & suppliers in India"

1210 INDIAN COKE DEVELOPMENTS� Development of coking batteries� Overview of cokeries in India� Increase in coking coal importsS K Jain, Joint Director (Operations), Steel Authority of India

1225 ANTHRACITE� Benefits of anthracite in the steel production process� Anthracite as a blending product� Potential future role of anthracite in the Indian market Paul Chappell, Director Commercial OperationsAsia, SSM Coal BV

1240 COAL BLEND QUALITY FOR COKE MAKING G I S Chauhan, Executive Director, Steel Authority of India.

1255 NEW SOURCES OF SUPPLY FOR INDIA – CANADA � Traditional sources of coal may not be sufficient to fuel

India’s booming economy � Several mining companies are opening new coal mines in

Northeastern British Columbia to produce high quality met coal for export

� Shipping from Canada’s West Coast ports ensures a diverse and reliable coal supply

Gary Livingstone, President and CEO, Western Canadian Coal Corp.

1310 Questions & Answers

1315 Lunch Sponsored by United Shippers Limited

SESSION 4: INVESTMENT OPPORTUNITIES IN INDIA AND ABROAD

Chair: Jim Nicholson, Global Business DevelopmentManager, Argus Media Limited

1430 CRITERIA FOR INVESTMENT IN AUSTRALIA� Why invest?� Recent Indian and Asian investments in Australian coal mines� Pitfalls of investing in the Australian market for the

overseas investor� Working with local JV partnersGary Cochrane, Managing Director, ResourceManagement International Pty Ltd

1450 FUTURE FOR INVESTMENT INTO THE INDIANCOAL INDUSTRY� FDI into the Indian mining sector� Opportunities and barriers to be overcome� Business models to attract foreign investment into Indian mines� Proposals for privatisation, making FDI a more attractive option

1510 Questions & Answers

SESSION 5: COAL PRICING AND TRADING

Chair: Jim Nicholson, Global Business DevelopmentManager, Argus Media Limited

1520 E-AUCTIONS AND FUTURES TRADING FORCOAL IN INDIA� The role of e-auctions in transforming the Indian

coal market� Future developments� Potential for a futures market to develop for coal in IndiaVinaya Varma, General Manager, e-Sales andFinancial Services, Coal Junction

1540 COAL HEDGING AND MANAGING PRICE RISK� Defining optimum coal buying strategies for the end-user in

the light of price volatility - role of futures vs long-term contracts vs spot price

� Different purchasing options - best practice methodologies for coal purchasing

� Risk mitigation and management strategies for fuel Chan Bhima, Director of Commodities Trading, Coal and Freight, Merrill Lynch Commodities

1600 Questions & Answers

1610 Refreshment breakSponsored by SSM

SESSION 6: ALTERNATIVE PRODUCTS FOR THE INDIAN MARKET

1640 COALBED METHANE� Potential for development of the CBM market in India� Estimates of reserves � Production challenges� CBM and coal production� Potential role of CBM in satisfying India’s energy needsYogendra Kr. Modi, Chairman & ManagingDirector, Great Eastern Energy Corporation Ltd

1700 PETCOKE� Global demand for petcoke � Growing demand for petcoke in India� Balancing supply and demand� Ensuring users’ equipment can cope with the demands

of petcoke

1720 Questions & Answers

1745 Close of Day One

"Coaltrans India has been highly inspirational for us from a business perspective. There is great potential in the Indian market"

"Coaltrans India was a very well organised event which provided a platform for major buyersand traders to discuss and share their views and ideas in the common interest" 5

1900 GALA DINNER AND NETWORKING RECEPTION

Attendance is open to all delegates and their partners

Hosted By Coal and Oil Group

DAY 2: TUESDAY 7 MARCH 2006

0730 RegistrationPre-conference refreshments sponsored by SSM

0800 Exhibition opens

0800 Networking breakfast with roving microphone(Delegates will have the opportunity to briefly introducethemselves to their fellow conference attendees to enablethem to make additional business contacts at theconference.)

0900 WELCOME AND OPENING REMARKSAllison Lindsay, Director of Conferences, Coaltrans Conferences

SESSION 7: POWER AND CEMENT INDUSTRY

Chair: Senior Representative, Vedanta Resources

0910 STEAM COAL OVERVIEW� Review of coal quality around the world – quality,

availability, calorific values� Availability to the Indian consumer� Mix of indigenous coal and imports as a solution to the

shortage of steam coal in IndiaGraham Chapman, Managing Director, Energy Edge Ltd

0930 COAL SUPPLY AND THE ECONOMICS OF THEPOWER INDUSTRY� Impact of coal imports on the economics of the

power industry� Blending imported and domestic coal to achieve the

best economics� Energy security for IndiaMP Gupta, Director (Marketing), MMTC Limited

0950 GAS VS COAL� Comparison of the economics and viability of gas and

coal for the Indian end-user� Role of LNG in the Indian energy marketsRavi Suri, Managing Director, Head, Project &Export Finance Middle East and South Asia,Standard Chartered

1010 Questions & Answers

1020 PANEL: CEMENT INDUSTRY PROSPECTS� Consolidation in the cement industry – likely impact on

coal demand� Increasing need for coal imports to satisfy the growing

demand of the Indian cement industry� Potential for use of petcoke as an alternative fuel for the

cement industry� Cement industry in PakistanH S Patel, Joint President, Ambuja Cement

Alok Gupta, Vice President - Purchasing, Lafarge India Pvt. Ltd

B. J. Rao, Senior Manager - Purchasing, Lafarge India Pvt. Ltd

1040 Refreshment breakSponsored by SSM

1110 PANEL: POWER INDUSTRY IN INDIA - VIEWFROM THE ELECTRICITY PRODUCERS � Expected demand for coal in light of increasing power

needs for India� Impact of coal imports on the economics of the

power industry� Blending domestic and international coals to improve

the economics � Ensuring security of supply for coal to the

power industry- Imports- Captive mining developments

Moderator: Ahmed Buhari, President and CEO, Coal and Oil GroupPanel:

P. H. Rana, Director (technical), Gujarat Urja VikasNigam Limited Subrato Trivedi, Executive Director – WesternRegion, NTPC Limited

H M Jain, Member Generation, Punjab StateElectricity Board

D K Narasimhan, Additional Chief Engineer/Coal, Tamil Nadu Electricity Board

"Excellent place to get connected with coal world"

"This superbly organised event provided significant opportunities to meet with key individuals from all aspects of the Indian coal industry"

6

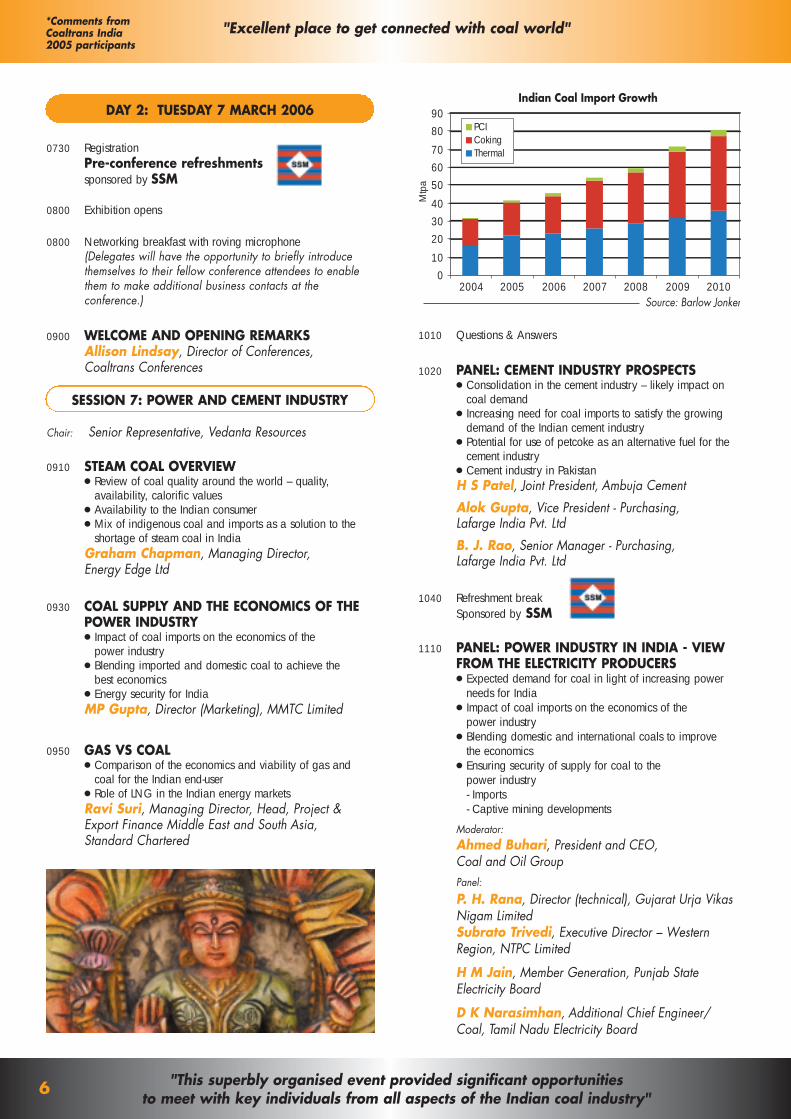

Indian Coal Import Growth

010

203040

506070

8090

2004 2005 2006 2007 2008 2009 2010Source: Barlow Jonker

Mtp

a

PCICokingThermal

*Comments fromCoaltrans India2005 participants

SESSION 8: INTERNATIONAL IMPORTS

Chair: Suresh Iyer, President, The Iyer Group

1145 PROSPECTS FOR THERMAL COAL IMPORTSINTO PAKISTANMuhammad Najib Balagamwala, Chief Executive, Seatrade Group

PANEL: KEY INTERNATIONAL MARKETS FOR STEAM COAL IMPORTS TO INDIA

1205 INDONESIA � Export & Supply Issues Pascual S Cominconde Jr., Regional MarketingDirector, Banpu Public Company Limited

1220 AUSTRALIARoss Crump, Managing Director, Excel CoalMarketing Limited

1235 SOUTH AFRICA � Movement of coal from South Africa globally� Coal qualities� Future prospects for South African coal to be imported

to IndiaA Senior Representative, Eyesizwe Coal (Pty) Ltd

1250 Followed by Questions & Answers

Lunch Sponsored by Noble Energy

START OF STREAMED SESSIONS

Delegates can select which Stream to attend from either Stream 1(Shipping and infrastructure challenges) or Stream 2 (Coal mineoperations and economics). Please indicate your preference on thedelegate registration form (page 10).

STREAM 1: SHIPPING AND INFRASTRUCTURE CHALLENGES

Chair: John C. Alexander, Senior Vice President - BusinessDevelopment, J. M. Baxi, Mumbai

1415 RAIL FREIGHT CHALLENGES IN INDIA� Future plans for development and expansion of the

rail network� Ensuring the rail network can cope with planned

port expansion� Ensuring there are sufficient wagons and rail infrastructure

to cope with expected demand� Overcoming congestion issues� Planning and prospects for future investment

1435 COAL TRANSPORT CHALLENGES� Key challenges in transporting and handling coal� Commissioning products and services for transportation

and handling of coal from ship� Wagon loading and unloading� Stacking, reclaiming and conveying� Technological advances to improve coal handling

and transportationSankar N. Mukhopadhyay, Sr. DivisionalManager (Business Development), TRF Ltd (A TATA Enterprise)

1455 SHIPPING CHALLENGES� Shipping economics in a volatile market� Trends in shipping bulk cargoes from China, Russia, South

Africa, Indonesia and Australia � Impact of changing coal supply movements to India on

global shipping movements and prices� Calculating the cost of cargo to market from different

destinations (eg South Africa vs China vs USA)Alex Harkess, Director, Clarksons Asia Ptd Ltd

1515 Questions & Answers

1530 Refreshment breakSponsored by SSM

1600 PORT DEVELOPMENT� Overview of the ports industry in India� How Indian ports will cope with the projected doubling of

coal imports � Plans for new ports to be developed� Key challenges� Long term strategies for the development of Indian portsR K Jain, Managing Director, Indian Ports Association

1620 FOLLOWED BY PANEL DISCUSSION: FUTUREOF INDIAN PORT DEVELOPMENTK. Raghuramaiah, Chairman, Paradip Port TrustDr A. K. Chanda, Chairman, Kolkata Port Trust

1650 PANEL: USER RESPONSE – PERSPECTIVE ONTHE PORTS� Review of what the end-users need from the portsModerator: Alex Harkess, Director, Clarksons Asia Pte LtdM.K Palanivel, Sr. Vice President-All India (Bulk &Tramp Division), Samsara Group

1720 Questions & Answers

1730 Close of conference

See next page for details of Stream 2

"Coaltrans India was very well organised and the list of delegates represented the who's who in the coal industry"

"Attracted a very large attendance, provided a wide coverage of coal, and had very good associated activities and functions"

7

All particpants at Coaltrans India will beable to purchase the Coaltrans World CoalMap at the discounted rate of $395 a saving of $100.For more information and to order your copyplease email [email protected] visit www.coaltrans.com

STREAM 2: COAL MINE OPERATIONS AND ECONOMICS

1415 MINE PLANNING AND ECONOMICS� Minimising cost of operations and increasing

recoverable reserves � Upgradation of technology � Improving quality N C Jha, Director Technical, Central Mine Planning & Design Institute

1435 MINE INFRASTRUCTURE AND OPERATIONS� Planning and site development� Coal handling systems� Site preparation and structural engineering� Case study: Sarshatali Coal MineAndrew Scrymgeour, Vice President –International, Norwest Corporation

1455 THE POTENTIAL FOR CONTRACT MINING INTHE INDIAN COAL INDUSTRY� Benefits of contractors to develop and operate coal mines� Key constraints, concerns and challenges in contract mining� Examples of latest developments in open pit miningBruce Munro, President Director, P.T. ThiessContractors Indonesia

1515 MINING EQUIPMENT MANAGEMENT -EFFICIENCY AND ASSET UTILISATIONJohn T. Bergin, Product Support Manager,Caterpillar Global Mining

1535 Questions & Answers

1540 Refreshment breakSponsored by SSM

1610 COMPLEX BALANCE OF EXTRACTION OF COALRESOURCES AND HUMAN ATTEMPTS FORRESTORATION � Air, water, noise pollution � Fauna and flora extinction � Local habitats, agriculture and land degradationD. Sengupta, General Manager, (Env. & CMC),Northern Coalfields Ltd

1630 OPPORTUNITIES AND CHALLENGES IN COALWASHING IN INDIA G C Mrig, Managing Director, Aryan CoalBeneficiations Pvt. Ltd

1650 DRILLING AND BLASTING – LATESTDEVELOPMENTS IN TECHNOLOGY� Review of the most suitable technologies for the Indian market� Constraints, challenges and concerns for blasting Dr Arvind K. Mishra, Technical Services Manager,Indian Explosives Limited (A fully owned subsidiary ofOrica, Australia)

1710 Questions & Answers1730 Close of conference

Please indicate your stream preference on the delegate registration form (page 10)

* Invited

"Coaltrans India represented the happenings/present status of the coal industry, covering all the related topics and the events were well appreciated"

"This conference allowed my better comprehension of this fast growing market, and made possible the contacts with many local players"8

*Comments fromCoaltrans India2005 participants

www.coaltrans.com/india 9

SPONSORSHIP

EXHIBITION STANDS

Sponsorship and exhibition stand opportunities

Enhance your market position by taking one of these business development options

SPONSORSHIP AND EXHIBITION

Sponsorship at Coaltrans India is a prime opportunity toraise your company’s profile and brand in a growingmarket sector. You will receive increased exposure tosenior energy industry representatives and companiesoperating in India and internationally.

Sponsorship options include Platinum, Gold, Silver orBronze packages each coming with attendant benefits.There are also a variety of other sponsorship choices,which incorporate all budget needs.

The Coaltrans India exhibition will be locatedadjacent to the main conference auditorium, andwill be the central focus for refreshment breaks,with meeting areas to allow maximum contact withdelegates. Stand Spaces are available in 6sqm and12sqm packages. Pre-built stands are designed toallow you to exhibit with the minimum of effort. Thisis the ideal opportunity to establish new businesscontacts and promote new products or services tothe coal and energy market.

To make enquiries and receive a detailed sponsorship package or stand details pleasecontact Alastair MacDonald, Coaltrans Conferences, Nestor House, Playhouse Yard, London, EC4V 5EX, UK.

Tel: +44 20 7779 8917 Fax: +44 20 7779 8946 E:[email protected]

24

M

40 SqM

P A

S S

A G

E

3 M

P A

S S

A G

E

6 M

P A

S S

A G

E

3 M

COFFEEPOINT

P A S S A G E 4 M

MAIN ENTRANCE

SERVICE ENTRANCE

31

30

29

28

27

22

23

24

25

26

18

17

16

15

14

13

7

8

9

10

11

12

6

5

4

3

2

1

LOUNGE

BAR40 SqM

Total Exhibition Booths: 37 Nos. Size: 3M x 3M

COFFEEPOINT

32

33

34

35

36

37

COALTRANSSTAND

SERVICE ENTRANCE

21 20 19

GOLD SPONSOR

SILVER SPONSORS

GENERAL SPONSORS

BRONZE SPONSOR

SUPPORTERS

PLATINUM SPONSORS

OFFICIALPUBLICATION

Post: Coaltrans Conferences Ltd

Nestor House, Playhouse Yard London EC4V 5EX, UK

Four other waysto register

Fax:

+44 20 7779 8946

Telephone: +44 20 7779 8945

(quoting brochure ref:)

The easiest way to register is online at www.coaltrans.com/india

EARLY BIRD FEE $1,291.50 (by 27 January 2006) - STANDARD FEE $1,435 (after 27 January 2006)

Fee includes: 1. Attendance at all conference sessions 2. Full conferencedocumentation, which includes copies of all available speakers’ papers 3. Complimentary tours, refreshments, lunches and evening receptions

Brochure ref: WEB

Delegates By 27 January After 27 January Discount

�� 1 $1291.50 $1435.00

�� 2-4 $1162.35 $1291.50 10%

�� 5-8 $1097.78 $1219.75 15%

�� 9-11 $1033.20 $1148.00 20%

�� 12+ $986.63 $1076.25 25%

please quote this reference whenbooking your place

COALTRANS INDIA 2006 REGISTRATION FORM6-7 March 2006

10

COMPLIMENTARY PRE-CONFERENCE TOUR - 1000-1600City tour of New Delhi �� 5 March 2006I will be bringing my spouse: Name

DAY 2 : STREAM OPTIONS�� Stream 1: Shipping and Infrastructure �� Stream 2: Coal Mine Operations and Economics

VISAAll International participants can apply for visas on the basis of aninvitation letter, barring registrants from Afghanistan, Bangladesh, China,Pakistan and Sri Lanka who have to provide us with full passport details.This has now become mandatory.

DOCUMENTATION�� I cannot attend but I would like to purchase the documentation for $350�� Soft copy or �� Hard copy

IT IS IMPORTANT TO FILL OUT ALL THE INFORMATION BELOWPlease photocopy this form for multiple bookings

1st Delegate detailsMr/Mrs/Ms ______ First name ____________________________________________________________

Surname _________________________________________________________________________________

Job title __________________________________________________________________________________

Tel ________________________________________ Fax___________________________________________

Email_____________________________________________________________________________________

2nd Delegate detailsMr/Mrs/Ms ______ First name ____________________________________________________________

Surname _________________________________________________________________________________

Job title __________________________________________________________________________________

Tel ________________________________________ Fax___________________________________________

Email_____________________________________________________________________________________

Organisation detailsCompany Name __________________________________________________________________________

Please supply your company description Company Activity (15-20 words)______________________________________________________________________________________________________________________________________________________________

Address ___________________________________________________________________________________

________________________________________________________________________________________________________

Postcode ___________________________ Country _____________________________________

Tel _______________________________________________ Fax___________________________________

PAYMENTPayment may be made in one of three ways - please tick appropriate box �

�� Conference fee �� Hotel deposit

�� 1. Please debit my CREDIT CARD No.

�� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��Visa/Master/Euro �� Amex �� (no other cards accepted)

Expiry date �� �� / �� ��Credit card payments will be processed in Sterling so exact fee may varyaccording to exchange rates

Signed......................................................................................................

�� Conference fee �� Hotel deposit

�� 2. Payment by BANK TRANSFER should be made through Lloyds Bank plc, PO Box 72, Bailey Drive, Gillingham Business Park, Kent ME8 0LS, account number 11127713, sort code: 30-12-18, Swift Code: LOYDGB2LCTY (all charges to be paid by sender)

�� Conference fee �� Hotel deposit�� 3. CHEQUES should be drawn on a UK Bank and made payable to

Coaltrans Conferences Ltd. A receipted invoice will be sent to all delegates.

Please complete and return this form together with a copy of your credit cardnumber, bank transfer or cheque, payable in US$ to Coaltrans Conferences Ltd,and send by post or fax to: Coaltrans Conferences Ltd Nestor House, Playhouse Yard, London EC4V 5EX, UK Tel: +44 20 7779 8945, Fax: +44 20 7779 [email protected] www.coaltrans.com/india

HOTELYou will be invoiced for a deposit of $300. Alternatively you can secureyour room by supplying a credit card number below. Arrival ________/________ Departure ________/________

�� Superior Single $185 �� Double $210 ���� Deluxe Single $210 �� Double $235 ���� Taj Club Room Single $270 �� Double $300 ��

Taj Palace Hotel, Sardar Patel Marg, Diplomatic Enclave, New Delhi 110 021, India Tel: (91-11) 2611 0202, Fax: (91-11) 2611 0808, www.tajhotels.com

Email: [email protected]

(quoting brochure ref:)

(EXAMPLE: Power GenCo operates three 200MW power plants in the UKand consumes 4MT of coal.)

CANCELLATIONSHotel deposits will be refunded in full, providing notification of cancellation is received one calendar month prior to the conference ie 6 February 2006. After thisdate, refunds minus 10% administration costs, will be issued after the conference, only if your room is re-sold. In the event of a no-show, you will be charged for allnights reserved.Conference fee: All cancellations must be received in writing by 6 February 2006 for a full refund, less a 10% administration charge. We cannot accept verbalcancellations. Cancellations received after 6 February 2006 are liable for the full conference fee. However, substitutions can be sent to attend in your place at noextra charge. If owing to a force majeure, Coaltrans is obliged to postpone or cancel the event, Coaltrans will not be liable for any travel or accommodationexpenses incurred by delegates or their organisations.Data protection: The information that you provide will be safeguarded by Coaltrans Conferences Ltd, a division of Euromoney Institutional Investor PLC group, whose subsidiaries may use it tokeep you informed of relevant products and services. We occasionally allow reputable companies outside the Euromoney Institutional Investor PLC group to contact you with details of products thatmay be of interest to you. As an international group, we may transfer your data on a global basis for the purposes indicated above. If you object to contact by telephone �� fax �� or email �� pleasetick the relevant box. If you do not want us to share your information with other reputable companies, please tick this box ��

* All bookings made on-site at the conference (6-7 March 2006) will be subject to a $50 administration charge

Rates include breakfast andEXCLUDE taxes at 12.5%Suites available on request