Embed Size (px)

Citation preview

Australian Power & Gas FY 2010 Investor Presentation

(ASX code: APK)

CEO, James MyattCFO, Warren Kember

For

per

sona

l use

onl

y

IMPORTANT INFORMATION This presentation (Presentation) has been prepared by Australian Power and Gas Limited (APK).

This Presentation does not purport to contain all the information that a prospective investor may require in connection with any potential investment in APK or its underlying business.

You must take into account all publicly available information and make your own independent assessment of APK before acquiring any shares in APK (Shares). You should not treat the contents of this Presentation, or any information provided in connection with it, as financial advice, financial product advice or advice relating to legal, taxation or investment matters. Before acquiring any Shares, you should consult your own advisers and conduct your own investigation and analysis in relation to APK.

The distribution of this Presentation may be restricted by law in certain jurisdictions. Recipients and any other persons who come into possession of this Presentation must inform themselves about, and observe any such restrictions.

This Presentation contains reference to certain intentions, expectations, future plans, strategy and prospects of APK which APK will work tirelessly to achieve however, those intentions, expectations, future plans, strategy and prospects may or may not be achieved. They are based on certain assumptions, which may not be met or which may be affected by known and unknown risks. The performance and operations of APK may be influenced by a number of factors, many of which are outside the control of APK.

Given that APK’s actual future results, performance or achievements may be influenced by factors outside APK’s control and be materially different from those expected, planned or intended, recipients should take this into account and not place undue reliance on these intentions, expectations, future plans, strategy and prospects. APK does not warrant or represent that the actual results, performance or achievements will be as expected, planned or intended. APK will use it best endeavours to achieve a positive outcome as planned for all shareholders.

FY 2010 Investor Presentation – Page 1

For

per

sona

l use

onl

y

AGENDA FY10 Highlights

FY11 Guidance Update

The Opportunity

The Business Model

Key Outcomes to Date

The Financials

Q1 2011 – Sales Results

Australian Consumer Law – Impact on Door to Door sales

Key Achievements Summary

FY 2010 Investor Presentation – Page 2

For

per

sona

l use

onl

y

Customer account: 145,000, an increase of 44% on the PCP

Revenues: $130.3M, an increase of 79% on the PCP

EBITDA: $12.1M, a $14.6M turnaround on the PCP

EBIT: $5.6M, a $15M turnaround on the PCP

Reported net loss after tax of $3.3M Following decision to recognise one-off significant items Related to renewal of $50M finance facility & expansion costs Significant items excluded, underlying after tax profit was $1.4M

FY10 HIGHLIGHTS

FY 2010 Investor Presentation – Page 3

For

per

sona

l use

onl

y

Customer accounts: 250,000

Revenues: $200M to $220M

EBITDA: $21M to $23M

EBIT: $10 to $12M

NPAT: $3.5M to $4.5M

FY11 GUIDANCE UPDATE

FY 2010 Investor Presentation – Page 4

For

per

sona

l use

onl

y

APK is an independent electricity and gas retailer

Catalyst was deregulation of the Australian retail energy market

The target market is residential electricity and gas users

APK Strengths:

Licences to operate in all eastern states

Proven product, operating and collection systems, and key management with

industry experience

An exclusive strategic agreement with The Cobra Group, the world’s biggest direct

sales company, allowing APK to grow aggressively in a low customer involvement

market.

APK - THE OPPORTUNITY

FY 2010 Investor Presentation – Page 5

For

per

sona

l use

onl

y

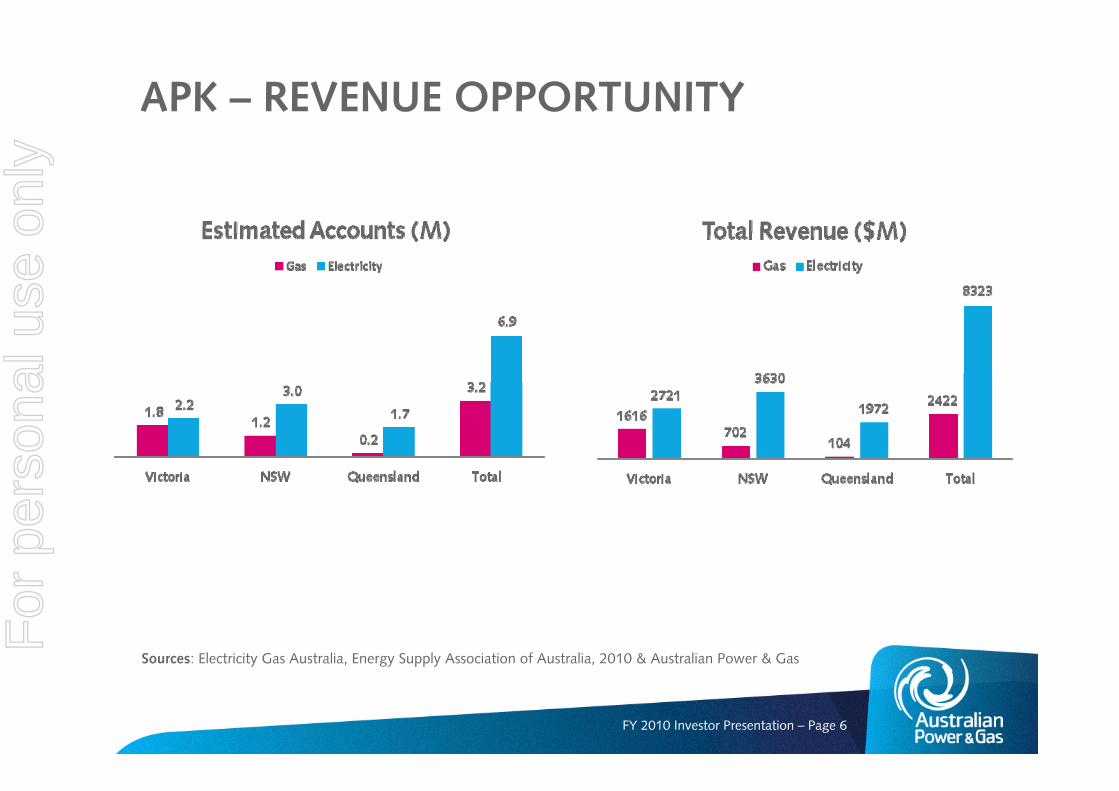

APK – REVENUE OPPORTUNITY

Sources: Electricity Gas Australia, Energy Supply Association of Australia, 2010 & Australian Power & Gas

FY 2010 Investor Presentation – Page 6

For

per

sona

l use

onl

y

THE COMPETITIVE LANDSCAPE

FY 2010 Investor Presentation – Page 7

For

per

sona

l use

onl

y

Value proposition

saves consumers money on their existing energy bills

No cyclicality

residential retail energy is a recession proof business

Lean cost base

highly variable cost structure and outsourced business model

Flexible

outsourced sales channels are able to more readily recruit sales staff

Cash focus

billing cycles running daily ensuring that cash is collected on a daily basis

Management of outstanding debt

systems and processes in place to manage and handle these issues at industry leading level

Channel strategy

the direct sales channel has proven to be effective in this consumer market as customers don’t actively seek

to change retailers

other channels such as web switching are being developed to take advantage of change in consumer switch

behaviour

THE BUSINESS MODEL

FY 2010 Investor Presentation – Page 8

For

per

sona

l use

onl

y

NET CUSTOMER ACCOUNT GROWTH

FY 2010 Investor Presentation – Page 9

For

per

sona

l use

onl

y

REVENUE GROWTH

FY 2010 Investor Presentation – Page 10

For

per

sona

l use

onl

y

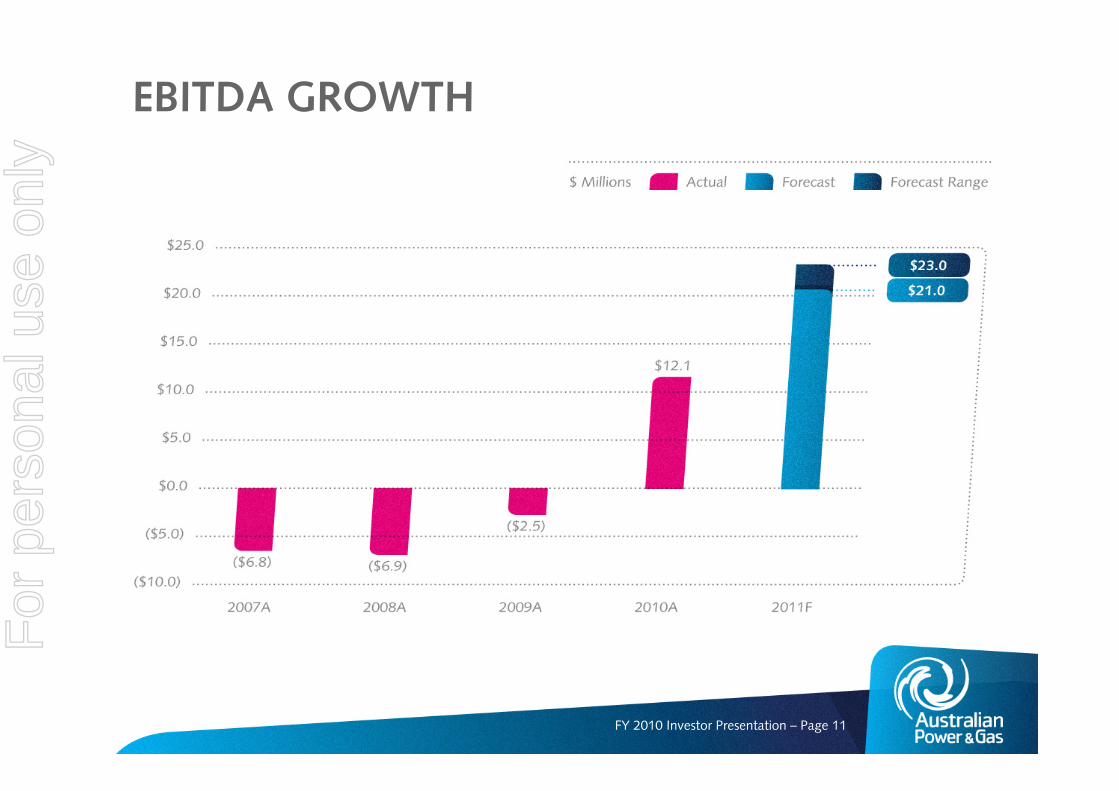

EBITDA GROWTH

FY 2010 Investor Presentation – Page 11

For

per

sona

l use

onl

y

EBIT GROWTH

FY 2010 Investor Presentation – Page 12

For

per

sona

l use

onl

y

NPAT OUTLOOK

FY 2010 Investor Presentation – Page 13

For

per

sona

l use

onl

y

UNDERLYING CASH FLOW POSITION

FY 2010 Investor Presentation – Page 14

For

per

sona

l use

onl

y

APK DEBT MATURITY PROFILE

FY 2010 Investor Presentation – Page 16

For

per

sona

l use

onl

y

APK – GEARING (Net debt to equity)

FY 2010 Investor Presentation – Page 17

For

per

sona

l use

onl

y

The Cobra Group Pty Limited 32,707,851 28.10%

Arthur Phillip Nominees Pty Limited 27,065,680 23.20%

JP Morgan Nominees Australia Limited 6,526,429 5.60%

Highgate Administration Services Pty Limited 3,857,144 3.30%

Mrs Amanda Poole 3,008,371 2.60%

DZP Investments Pty Limited 2,393,915 2.10%

PCF Group Pty Ltd 2,007,557 1.70%

Stewart Hartley 1,925,604 1.70%

S Ward Holdings Pty Limited 1,783,566 1.50%

Gabo Investments Pty Limited 1,403,693 1.20%

Mrs Sue McGregor 1,266,784 1.10%

Arthur Phillip Pty Limited 1,042,845 0.90%

Mr Craig Burton 1,000,000 0.90%

Communications Power Incorporated (Aust) Pty Limited 1,000,000 0.90%

Mollyjacks Pty Limited 918,062 0.80%

Man Holdings Pty Limited 750,000 0.60%

OIC Nominees Limited 733,333 0.60%

AJP Investment Services Pty Limited 710,000 0.60%

National Nominees Limited 634,619 0.50%

ANZ Nominees Limited 600,015 0.50%

91,335,422 78.40%

Name of shareholder Number of shares held

% to total on issue

TOP 20 SHAREHOLDERS as at 20/09/2010

For

per

sona

l use

onl

y

Q1 2011- Sales Results

FY 2010 Investor Presentation – Page 17

• QLD & NSW growing in line with targets - 3 consecutive record sales months since July

• Total net active accounts across all states now in excess of 170,000

• QLD electricity supply contracts completed

• VIC electricity supply contract extension in final stages of completion

• VIC gas supply contract extension in final stages of completion

For

per

sona

l use

onl

y

Australian Consumer Law

Implications on Door to Door Selling

For

per

sona

l use

onl

y

Door to Door Selling – 2010 Changes

• Australian Consumer Law Changes – Restricting door to door selling after 6pm from Mon – Friday

• QLD already under a 6pm restriction – customer consent for appointments after 6pm is allowed

• Clarification being sought by ERAA on specific rules allowing customers to give consent for post 6pm appointments to be made

• ERAA also establishing a self regulatory scheme to be overseen by a new company Energy Assured Limited

• Energy Assured limited will oversee implementation of measures such as standardised training & recruitment practices and national registration of all agents.

For

per

sona

l use

onl

y

Channel diversification already implemented

• 75% of all sales over past 6 months have been delivered from new channels and from D2D sales prior to 6pm

• APK doorknockers currently not sent into field until around 1pmFor

per

sona

l use

onl

y

Channel diversification already implemented

• We can see clearly here that the new channels deployed by APK are increasing to level that matches the post 6pm Door to Door sales.

• The APK channel diversification strategy has been a very successful initiative deployed well ahead of changes to Consumer Law.For

per

sona

l use

onl

y

Test of early agent deployment on 30th Sep

• APK proved by early deployment of Door Knockers it was able to significantly increase sales prior to 6pm by over 3 times the normal rate.

• APK believes churn will increase prior to 6pm and decrease post 6pm with negligible net impact on overall salesFor

per

sona

l use

onl

y

Quarterly comparison – VIC to QLD

• QLD delivering 81% sales prior to 6pm & VIC delivering 60% sales prior to 6pm

• QLD agents currently using time prior to 6pm to make appointments after 6pm

For

per

sona

l use

onl

y

Summary

• APK’s channel diversification strategy largely offsets the impact of Consumer Law Changes

• 75% of all gross sales currently coming from new channels and D2D sales prior to 6pm

• By deploying door to door agents earlier the impact can be further offset

• To prove the point on Sept 30 APK tested early deployment of agents from 9am to 6pm and delivered over a 300% increase in sales prior to 6pm

• Our conclusion is the only impact will be a higher churn rate prior to 6pm and a lower churn rate post 6pm

• The combination of channel diversification and earlier agent deployment will largely negate any significant impact on gross sales.

For

per

sona

l use

onl

y

THE EXECUTIVE MANAGEMENT TEAMJames Myatt – CEO and Managing Director25 years industry experience, previously held senior positions with Energy Australia,Duke Energy International, TXU Australia and Solaris Power.

Andrew Butler – GM Sales, Marketing and PR

Services Marketing professional, previously held senior positions with AGL, CitiPower, Solaris Power, Transurban and Connector Motorways.

Warren Kember –Chief Financial Officer

25 years experience in financial management and corporate systems, previously held senior positions with Transfield Telecommunications, AGL and ADT Security.

Joanne Shatrov –General Counsel

Joanne is an experienced lawyer in wholesale and retail energy, previously held positions with Ergon Energy, Duke Energy and Ebsworth & Ebsworth Lawyers.

Deborah Dickens –GM Commercial Operations16 years commercial and financial experience, previously held senior positions with British Airways in the UK and on the UATP Board.

FY 2010 Investor Presentation – Page 19

For

per

sona

l use

onl

y

THE BOARDIan McGregor – ChairmanIan has over 25 years of professional experience as a financial officer and business manager. He was previously the Company Secretary and Chief Financial Officer of Broadcast Services Australia Limited, and the Chief Financial Officer of Unwired Group Limited.

Richard PooleRichard is a qualified lawyer who specialises in mergers and acquisitions. He is a principal of Arthur Phillip Pty Limited, and has been involved in a range of fund raising and advisory projects for public and private clients.

Michael HoggMichael is the Chief Executive Officer of The Cobra Group Australia, part of the Global Cobra Group, a direct sales organisation with over 10,000 sales representatives in 20 countries worldwide.

FY 2010 Investor Presentation – Page 20

For

per

sona

l use

onl

y

Customer growth: 145,000, an increase of 44% on the PCP

Revenues: $130.3M, an increase of 79% on the PCP

EBITDA: $12.1M, a $14.6M turnaround on the PCP

Customer cash receipts $115.2M for the FY10, up 86% on previous corresponding period

Underlying positive cash flow of $4.3M for FY10, up from $0.9M on previous corresponding period

Ranked number one on Business Review Weekly’s 2010 Fast Starters List

Five sales channels successfully launched into the Victorian market

Expansion into Queensland and New South Wales markets underway

Secured a major growth platform:$18.9M C-note funding facility completed$50M receivables facility extendedLoad following electricity supply contract for Queensland signed

KEY ACHIEVEMENT SUMMARY

FY 2010 Investor Presentation – Page 21

For

per

sona

l use

onl

y

Thank you & Questions

FY 2010 Investor Presentation – Page 22

For

per

sona

l use

onl

y