-

2020 | Victoria

AustralianFarmland Values

-

About the researchThe Australian Farmland Values report is based

on actual farm sales using data collected by the offi cial

government agency in each state and territory, which is then

compiled by PriceFinder.

The Australian Farmland Values report is a guide to market

trends of commercial farming property. To that end, where possible,

transactions between family members or where one party has

compulsory powers are excluded from the analysis. Further, small

farms are also excluded to limit the impact of ‘lifestyle farming’

on the results.

As property settlement periods vary, some 2019 sales will not be

captured in this report at the time of publication. The median

price for the most recent year is preliminary and will be revised

at least annually.

The values used in this report are based on the total sale price

and therefore include the value of capital improvements. The value

of water entitlements attached to a land title and therefore sold

with the property will be refl ected in the sale price of the land.

If water entitlements are sold separately from the land, this value

will not be captured in the sale price.

Median prices in the report are only a guide to market activity.

They are not a valuation. Median is used rather than mean as the

median is not as readily distorted by unusually high or low prices.

However, the median does have limitations. The mix of property sold

in a given year can cause the median price to move up or down in a

way that is unrelated to a move in value. For example, a higher

proportion of lower-value sales can result in a lower median and

vice-versa. In areas where there have been very few sales, this

effect can be especially pronounced and so in these cases the

median should be used with caution and may not be indicative of an

actual change in farmland value.

In order to track median price per hectare growth over a range

of time periods the report uses compound annual growth rate (CAGR).

Compound annual growth rate is a geometric mean that accounts for

compound growth, providing a more accurate measure of an

investments return compared to a simple arithmetic mean.

Farmland sales volume is reported as the number of transactions.

Farms can be sold as single or multiple lots, which obscures the

view of the number of farms sold, particularly in cases where one

farm is sold as multiple lots to multiple buyers. Accordingly, the

number of ‘transactions’ should not be interpreted as the number of

farms sold and should only be used as a guide to market

activity.

This report is not intended for use as a farm valuation tool. A

qualifi ed professional is required to assess the value of a

property.

For PriceFinder terms and conditions visit: www.pricefi

nder.com.au/terms-conditions/

About Rural BankRural Bank is a division of Bendigo and Adelaide

Bank Limited and provides exceptional fi nancial services,

knowledge and leadership for Australian farmers to grow.

-

Understanding the value of farmland is important to everyone in

agribusiness, especially Australia’s farmers.

The Australian Farmland Values report tells the story of

national and regional farmland performance over the past 25

years.

This report is intended to provide general information on a

particular subject or subjects and is not an exhaustive treatment

of such subject(s). The information herein is believed to be

reliable and has been obtained from public sources believed to be

reliable. Rural Bank, a Division of Bendigo and Adelaide Bank

Limited, ABN 11 068 049 178 AFSL/Australian Credit Licence 237879,

makes no representation as to or accepts any responsibility for the

accuracy or completeness of information contained in this report.

Any opinions, estimates and projections in this report do not

necessarily refl ect the opinions of Rural Bank and are subject to

change without notice. Rural Bank has no obligation to update,

modify or amend this report or to otherwise notify a recipient

thereof in the event that any opinion, forecast or estimate set

forth therein, changes or subsequently becomes inaccurate. This

report is provided for informational purposes only. The information

contained in this report does not take into account your personal

circumstances and should not be relied upon without consulting your

legal, fi nancial, tax or other appropriate professional.

© Copyright Bendigo and Adelaide Bank Ltd ABN 11 068 049 178

(1452805 –1456138) (04/20)

-

Foreword

Agriculture is volatile, or so the mythology goes. You only hear

about agriculture when it’s booming or facing another challenge or

crisis.

Rural Bank’s Australian Farmland Values 2020 report turns this

myth on its head, particularly when you consider our world is

grappling with the COVID-19 pandemic, a challenge with the

potential to deliver the greatest uncertainty or unknown economic

impact since World War II.

Is agriculture immune or conditioned? History would tell you it

is.

When you remove the noise, agriculture is stable, consistent and

an under-recognised source of economic growth. If you know what you

are doing and are prepared to see through short-term vagaries and

variations, there are rewards to be harvested.

On average, Australian farmland has delivered compound annual

growth of 7.5 per cent over 20 years.

It’s a remarkable result and it highlights that investing in

farmland over the long-term will deliver, through good times and

bad.

We also know that farmland value is only one measure. It

certainly does not automatically translate to profi tability, or

growth.

It’s the base asset for Australia’s farming businesses, with

unique characteristics, strengths and weaknesses. But in every

case, every parcel of land requires smart, capable farmers to turn

a profi t.

Land with consistent access to water has continued to perform

far better than land without. Climate risk and reliable rainfall

continues to drive investment.

Farmers are also holding on to their land, with year-on-year

transaction volumes falling by 13.2 per cent. What is driving this?

Are lower sales volumes driving up price, or are farmers simply

optimistic about the future?

There is certainly no shortage of buyers, happy to invest.

Corporates have continued to strongly enter the market,

particularly in New South Wales and Queensland.

As much of the eastern half of Australia emerges from dry

conditions and drought, will land continue to be held on to for

longer, and what are the implications for traditional farming

businesses?

These are all important questions, requiring discussion.

As always, Rural Bank is looking to contribute evidence and

insight to this conversation, advocating for the agricultural

industry.

In these unprecedented times, the evidence suggests that if you

look to agriculture and farmland, it continues to perform well over

the long-term – whatever the circumstances.

Alexandra GartmannCEO, Rural Bank

4

-

Executive Summary

Farmland values have been resilient following several years of

challenging seasonal conditions. We expect growth in the value of

Australian farmland to continue over the long-term as ongoing

improvements in Australian agricultural productivity and profi

tability fuel strong demand for agricultural assets.

While factors such as strong commodity prices, a low interest

rate environment and tight supply of land support strong demand for

farmland in the short-term, this will be tempered by disruptions to

global economies. We expect farmland values to continue to grow but

at a reduced rate compared to the growth seen in the past six

years.

Across Australia the number of transactions declined 13.2 per

cent year-on-year to 7,164. This marks the lowest transaction

volume for the analysed period (1995–2019). The number of

transactions equates to a total of 6.5 million hectares of land

with a combined value of $8.7 billion.

Farmland values hold particular signifi cance when examined at a

localised level. In 2020 Rural Bank has researched trends in 29

regions across the country. The Australian Farmland Values 2020

report draws on more than 262,000 transactions, accounting for

303.9 million hectares of land with a combined value of $159

billion over 25 years.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

$6,000

$3,000

$5,000

$4,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

$2,000

$1,000

0

Australia – historic performance

2019 year-on-year median price growth

2019 year-on-year transaction

volume growth

NSW 17.2% -19.8%

QLD -0.8% -7.8%

SA 18.4% -8.3%

TAS 11.1% -5.8%

VIC 12.1% -12.9%

WA 28.2% -4.6%

NT -53.9% -36.2%

National 13.5% -13.2%

5

-

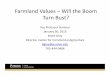

Victoria

Median price per hectare

$7,5872019 median price growth

12.1%Hectares of land traded

166,215Compound annual growth

over 20 years

7.1%

South West16.7%

Northern16.1%

North West31.9%

Gippsland-5.9%

Map shows median price movement in 2019.

-

Victoria

From the fi eld

“Victoria had its fourth consecutive year of growth in

median price per hectare in 2019. Contributing to the

increase in median was a decrease in the number of

transactions, whilst strong demand remained. North

West and Gippsland regions experienced the greatest

declines in transaction volume. Geographical risk

was a factor that was front of mind, as an increase

in the need for water security and diversifi cation

of location increased interest in irrigated and high

rainfall municipalities. Low interest rates have led to

a higher number of properties purchased rather than

leased, these properties were predominately off-

market transactions between lessee and landowner.

Considering the current economic environment

purchasing rather than leasing is expected to continue.”

Jonathon Hewitt, Rural Bank, Eastern Australia.

The median price per hectare of farmland in Victoria increased

by 12.1 per cent in 2019. This is now the fourth consecutive year

of growth, bringing the 10-year compound annual growth rate to 6.8

per cent. Competition remained high as there were a smaller number

of transactions in 2019. Whilst a favourable cropping season and

stronger livestock prices gave some confi dence to family farms

leading to healthier balance sheets allowing for new land

purchases. Should higher livestock prices remain, and favourable

cropping conditions persist this is expected to continue.

The total value of Victorian farmland traded in 2019 was

approximately $1.05 billion, a year-on-year decrease of 4.2 per

cent. Total hectares traded fell 16.2 per cent in 2019, however an

increase in the proportion of higher value transactions, especially

those above $12,500 per hectare led to growth in the median price

per hectare.

North West Victoria saw the largest year-on-year increase in

median price per hectare 31.9 per cent higher. South West and

Northern Victoria both continued to see an increase in growth with

the median price per hectare 16.7 per cent and 16.1 per cent higher

respectively. Whilst Gippsland, following a persistent drought saw

a decrease of 5.9 per cent year-on-year. Land close to and in

higher rainfall regions was in high demand as diversifying

geographical risk was an attraction for buyers.

There was a 12.9 per cent decrease in the volume of

transactions, to 1,464, this kept prices fi rm and heightened

competition between buyers. Dry conditions reduced the number

Number of transactions (RHS)Median price $/ha (LHS)

$8,000

$5,000

$4,000

$7,000

$6,000

3,000

2,500

2,000

1,500

1,000

500

0

$3,000

$2,000

$1,000

0

Victoria – historic performance

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

of listings in 2019. However, lower interest rates increased

buyer confi dence leading to an increase in the amount of

properties bought rather than leased. A trend likely to continue in

the coming years.

7

-

400

300

100

0

350

200

250

150

50

$0 – 2,500/ha

Num

ber o

f tra

nsac

tions

$2,500 – 5,000/ha $5,000 – 7,500/ha $7,500 –10,000/ha $10,000

–12,500/ha $12,500/ha+

2019

2018

Victoria – transactions by price range

In 2019, there was a larger proportion of higher valued

transactions contributing to the increase in the growth of median

price per hectare across the state. The number of transactions

greater than $12,500/ha was 7.8 per cent higher than 2018 and the

only price range where transaction volume increased.

The lower the price range the larger the decrease in volume of

transactions, following the trend seen in recent years of more high

value transactions and fewer low value transactions. In 2019

farmers with healthy balance sheets and large land holdings

were

able to unlock equity to chase additional land hence an increase

in higher value transactions.

This was especially evident in the South West region of the

state with increases in transaction volume of 61 per cent and 38

per cent in the $12,000–15,000/ha range and the greater than

$15,000/ha range. The South West, in addition to local purchases,

also saw an increase in the proportion of investors from the city

often out competing local buyers and pushing land values

higher.

Growth in median price per hectare occurred in all parcel sizes,

with parcels greater than 150ha experiencing the highest growth of

27.3 per cent. Small to medium sized parcels in the 50–100ha range

were also signifi cantly higher 15.5 per cent greater

year-on-year.

The transactions mix was different compared to 2018 as there was

a decline for all parcel sizes; however, the percentage of total

transactions for each range remained relatively unchanged.

The decline led to an increase in the competition for farmland

in 2019, resulting in a 12.1 per cent increase to the median price

per hectare for the state. An increase in cross industry

competition also aided the median price per hectare, as high

rainfall areas traditionally used for cropping were purchased with

the intention of running livestock.

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2019 % change 10yr CAGR Decile 2019 YoY +/-

30–50 $10,499 3.4% 3.5% 10.0 450 -79

50–100 $8,167 15.5% 4.3% 10.0 508 -58

100–150 $5,393 9.5% 6.2% 10.0 234 -24

150+ $3,491 27.3% 8.6% 10.0 272 -56

Overall $7,587 12.1% 6.8% 10.0 1,464 -217

8

-

GippslandVIC

The median price per hectare in Gippsland decreased by 5.9 per

cent in 2019 to $11,002 per hectare. The decrease in 2019 follows

two consecutive years of growth of 15.4 and 15.2 per cent. There

was a greater proportion of larger parcels of land sold in 2019,

these characteristically sell for a lower value per hectare, this

was due to a supply shortage in small to medium sized parcels as a

result of rural property being held on to. This changed the overall

transaction mix and led to a decline in median price per hectare

for the region.

East Gippsland and Bass Coast had the largest declines in median

price per hectare both falling 7.5 per cent and 7.4 per cent

respectively. Whilst Latrobe and Wellington recorded the highest

growth in median price per hectare due to water security offered

with some of these properties.

The volume of transactions dropped in 2019 by 25.7 per cent to

243, drought was a key factor leading to a lower number of listings

in the area.

Number of transactions (RHS)Median price $/ha (LHS)

$14,000

$12,000

$8,000

$6,000

$10,000

700

600

500

300

100

400

200

0

$4,000

$2,000

0

Gippsland – historic performance

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

From the fi eld

“Gippsland experienced a supply shortage through 2019 with

prolonged drought

conditions impacting availability. Rural property was tightly

held, and lower supply

resulted in strong demand and fi rmer prices paid for larger

landholdings. Despite a

5.9 per cent decline in the median price across Gippsland, the

key irrigation areas

of the Latrobe and Wellington shires both experienced an

increase in property

prices in response to water security offered by some of these

land parcels.”

Josie Zilm, Rural Bank, Gippsland

2019 median price growth

-5.9%

Hectares of land traded

18,558

Compound annual growth over 20 years

6.3%

Median price per hectare

$11,002

10

-

Transaction volume decreased across all price per hectare ranges

in 2019. The most signifi cant drop in volume was for parcels

priced between $8,000–12,000/ha, 35 per cent lower than 2018, this

equates to 21 fewer transactions. This was particularly evident in

the Baw Baw, South Gippsland and Wellington municipalities. Whilst,

the volume of transactions priced between $12,000–16,000/ha and

greater than $20,000/ha were 28.9 per cent and 34.5 per cent lower

respectively.

An increase in the total share of transaction volume in East

Gippsland, which attracts a lower price per hectare compared to

other municipalities, contributed to the decline in median price

per hectare for the Gippsland region in 2019.

Median price per hectare declined for smaller parcels of land in

2019. Whilst there was an increase to the median price per hectare

for the larger parcels in the range of 70–90ha and greater than

90ha. Historically parcels greater than 90ha have returned the

highest compound annual growth rate.

An increase in the percentage of transactions that were lower in

value, particularly in the greater than 90ha range, was a pertinent

factor in the median price per hectare decreasing in 2019. There

was an increase of 2.5 per cent and 4.4 per cent to the share of

total transactions sized 50–70ha and greater than 90ha

respectively.

70

50

20

0

60

40

10

30

$0 – 4,000/ha

Num

ber o

f tra

nsac

tions

$4,000 – 8,000/ha $8,000 –12,000/ha $12,000 –16,000/ha $16,000 –

20,000/ha $20,000/ha+

2019

2018

Gippsland – transactions by price range

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2019 % change 10yr CAGR Decile 2019 YoY +/-

30–50 $13,274 -8.2% 4.4% 9.6 98 -54

50–70 $9,729 -17.9% 1.8% 8.3 64 -14

70–90 $9,944 25.3% 5.0% 9.6 25 -11

90+ $6,906 39.1% 11.8% 10.0 56 -5

Overall $11,002 -5.9% 5.5% 9.6 243 -84

11

-

North WestVIC

The median price per hectare of farmland in North West Victoria

increased by 31.9 per cent in 2019 to $3,092 per hectare. This

follows a slight decline of 1.9 per cent in 2018, however there has

been strong growth in recent years with the median price per

hectare increasing 85 per cent over the past fi ve years. Family

farms continue to be the main buyers of property as a favourable

cropping season and strong livestock prices gave confi dence to

large family farms, leading to new land purchases.

In 2019, the municipalities of Swan Hill and Hindmarsh recorded

strong growth in median price per hectare. In contrast,

Yarriambiack recorded a decline.

Transaction volume decreased substantially in 2019, down 21 per

cent to 147 transactions, persistent drought particularly in the

North West Mallee contributed to the decline.

Number of transactions (RHS)Median price $/ha (LHS)

$3,500

$3,000

$2,500

$1,500

$1,000

$2,000

300

250

200

100

150

50

0

$500

0

North West – historic performance

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

From the fi eld

“Demand for grazing and cropping land in the southern Wimmera

and Swan

Hill area was high in 2019. Family farms remained the major

buyers in both the

Wimmera and Mallee. There were more off market transactions as

neighbouring

farmers came to agreeance on price without going to market. Low

interest rates

and high lease costs are contributing to an increase preference

of buying land over

leasing. Demand is set to remain high in 2020 with anecdotally

less supply to the

market and the expectation of more private sales.”

Greg Kuchel, Rural Bank, Swan Hill.

2019 median price growth

31.9%

Hectares of land traded

34,244

Compound annual growth over 20 years

7.7%

Median price per hectare

$3,092

12

-

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2019 % change 10yr CAGR Decile 2019 YoY +/-

30–100 $3,413 -7.4% 1.8% 6.7 36 -4

100–200 $3,089 26.3% 5.3% 10.0 43 -14

200–300 $3,254 48.3% 9.1% 10.0 37 -12

300+ $1,710 22.5% 7.6% 10.0 31 -9

Overall $3,092 31.9% 8.9% 10.0 147 -39

In 2019, there were fewer low value transactions, which resulted

in an increase to the median price per hectare. In contrast to

2018, there was a signifi cant increase in the volume of

transactions for land priced between $3,000–4,000/ha and greater

than $5,000/ha up 40 per cent and 16 per cent respectively.

A decrease to the total share of transactions in Mildura,

historically a lower value municipality, was a factor that led to a

higher median price per hectare. Whilst increased transactions of a

higher value in the Hindmarsh and Swan Hill municipalities also

contributed to the year-on-year increase in median price per

hectare. Demand remains above supply with low interest rates and

high leasing costs prompting farmers to buy land rather than lease,

where possible.

The municipalities of Mildura and Horsham reported a decline in

transaction volume in 2019. In contrast, volume increased in Swan

Hill.

In 2019, smaller parcel sizes of 30–100ha made up a higher

percentage of total transactions. However, the mix of sizes

remained relatively consistent with previous years despite a

decline in activity across all parcel sizes. Median price per

hectare for 200–300ha range increased by 48.3 per cent. In

contrast, parcels 30–100ha declined by 7.4 per cent. The 200–300ha

range returned the highest ten-year compound annual growth

rate.

60

40

0

50

20

30

10

$0 – 1,000/ha

Num

ber o

f tra

nsac

tions

$1,000 – 2,000/ha $2,000 – 3,000/ha $3,000 – 4,000/ha $4,000 –

5,000/ha $5,000/ha+

2019

2018

North West – transactions by price range

13

-

NorthernVIC

The median price per hectare in Northern Victoria increased by

16.1 per cent in 2019 to $7,331. This is the eighth consecutive

year of growth for the region as demand for properties remains high

and supply remains tight.

Median price per hectare increased notably in Bendigo and

Loddon. Whilst the municipalities of Wodonga and Mansfi eld

recorded a decline.

In 2019, the volume of transactions declined 3.6 per cent to

568. This follows a 15.6 per cent decline in 2018 and is the lowest

number of transactions in the analysed period. However, equity from

sales of allocated water in the Campaspe shire and Katunga was a

factor in the increase in land purchases closer to the Great

Dividing Range. Indigo and Mansfi eld both recording an increase to

the number of transactions in 2019.

Number of transactions (RHS)Median price $/ha (LHS)

$8,000

$7,000

$5,000

$4,000

$6,000

1,200

1,000

800

600

400

200

0

$3,000

$2,000

$1,000

0

Northern – historic performance

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

From the fi eld

“Cropping land was in high demand in 2019, particularly in the

north of the region

around Yarrawonga. In the high rainfall grazing regions interest

from farmers looking

to diversify their geographic risk led to an increase in demand.

Private off market

transactions between neighbouring properties were popular across

the region, with

sellers often naming their price. Corporate buying activity

centred around Katunga

where irrigated properties with deep lead bore water were sought

after.”

Kate Hemphill, Rural Bank, Shepparton.

2019 median price growth

16.1%

Hectares of land traded

57,538

Compound annual growth over 20 years

6.9%

Median price per hectare

$7,331

14

-

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2019 % change 10yr CAGR Decile 2019 YoY +/-

30–50 $9,884 3.5% 5.2% 10.0 202 5

50–100 $7,513 25.1% 6.4% 10.0 196 -16

100–150 $4,881 9.2% 7.7% 10.0 93 -9

150+ $3,523 8.5% 9.3% 10.0 77 -1

Overall $7,331 16.1% 7.0% 10.0 568 -21

Transaction volume increased signifi cantly at the top end of

the market in 2019. The volume of transactions between

$8,000–10,000/ha and above $10,000/ha increased 26.2 per cent and

14.4 per cent respectively. Transaction volume in the lower median

price per hectare ranges fell by the amount that the top end ranges

gained, $0–2,000/ha and $2,000–4,000/ha were 14.3 per cent and 27.9

per cent lower in 2019. Fewer lower value sales and increased high

value sales contributed to the median price per hectare

increasing.

Decreases in the total share of transaction in the Gannawarra

and Loddon municipalities contributed signifi cantly to a decrease

in the number of transactions priced between $2,000–4,000/ha. A

lower amount of lower value transactions was a key driver of a

higher median price per hectare in 2019 for the Northern

region.

The municipalities of Gannawarra, Mitchell, Mount Alexander,

Strathbogie and Wangaratta reported a decline of above 30 per cent

to the volume of transactions in 2019.

The transaction mix remained relatively similar to previous

years with fewer transactions in the 50–100ha and 100–150ha parcel

sizes, 7.5 per cent and 8.8 per cent lower. In contrast 30–50ha

parcels increased 2.5 per cent compared to 2018. Median price per

hectare growth was greatest in the 50–100ha range increasing 25.1

per cent. Larger parcels greater than 150ha recorded the highest

compound annual growth rate over the past ten years.

200

100

0

150

50

$0 – 2,000/ha

Num

ber o

f tra

nsac

tions

$2,000 – 4,000/ha $4,000 – 6,000/ha $6,000 – 8,000/ha $8,000

–10,000/ha $10,000/ha+

2019

2018

Northern – transactions by price range

15

-

South WestVIC

The median price per hectare of farmland in South West Victoria

increased by 16.7 per cent in 2019 to $8,649 per hectare. This

follows an increase of 13.3 per cent in 2018, an increase in the

number of investors from the city often outcompeting local buyers

pushed land values higher.

Median price per hectare recorded strong growth in the

municipalities of West Wimmera and Glenelg. In contrast, Hepburn

recorded a decline. Areas of high rainfall were sought after

especially from farmers outside of the region looking to purchase

cropping land with the intention of running livestock.

Transaction volume was lower in 2019, decreasing by 12.6 per

cent to 506. This was driven by high commodity prices for both

livestock and grain, resulting in land becoming tightly held as

opposed to be offered up for sale. This trend is expected to

continue in 2020, further strengthening buyers balance sheets and

aiding competition for available land.

Number of transactions (RHS)Median price $/ha (LHS)

$10,000

$9,000

$7,000

$8,000

$5,000

$4,000

$6,000

900

800

700

600

500

300

100

400

200

0

$3,000

$2,000

$1,000

0

South West – historic performance

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

From the fi eld

“Demand for land in South West Victoria remained high in 2019.

Corporate

investors competed with local buyers resulting in land price

growth. Traditional

cropping land sold to graziers from outside the region looking

to take advantage of

the region’s high rainfall. Buying power was aided by low

interest rates and solid

commodity prices, this trend is expected to continue in

2020.”

John King, Rural Bank, Colac.

2019 median price growth

16.7%

Hectares of land traded

55,876

Compound annual growth over 20 years

7.8%

Median price per hectare

$8,649

16

-

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2019 % change 10yr CAGR Decile 2019 YoY +/-

30–50 $10,384 18.1% 2.0% 10.0 142 -25

50–100 $9,275 17.4% 6.5% 10.0 184 -18

100–150 $7,108 3.3% 7.8% 10.0 88 -7

150+ $5,672 34.9% 7.7% 10.0 92 -23

Overall $8,649 16.7% 7.2% 10.0 506 -73

The transaction mix by price range changed most at the top end

of the market in 2019. There was a notable increase of 61.4 per

cent in the volume of transactions between $12,000–$15,000/ha and

an increase of 38 per cent in the greater than $15,000/ha range.

The increase in high value transactions was a key driver of median

price per hectare growth in 2019.

At municipality level, a 55 per cent increase to the number of

transactions in Corangamite, a high value municipality, contributed

to the 16.7 per cent increase to the median price per hectare for

the region. In contrast, transaction volume declined signifi cantly

in Ballarat and Moorabool 42.9 per cent and 35.3 per cent

lower.

Median price per hectare increased for every parcel size

accompanied by a reduced number of transactions across all sizes.

Parcels greater than 150ha recorded the highest growth, up by 34.9

per cent, whilst the 100–150ha range recorded modest growth of 3.3

per cent following a 33 per cent increase in 2018. Historically

larger parcel sizes have recorded the highest compound annual

growth rate.

200

100

0

150

50

$0 – 3,000/ha

Num

ber o

f tra

nsac

tions

$3,000 – 6,000/ha $6,000 – 9,000/ha $9,000 – 12,000/ha $12,000

–15,000/ha $15,000/ha+

2019

2018

South West – transactions by price range

17

-

VIC

Farmland sales by municipality

MunicipalityMedian $/ha Number of transactions

2019 5yr CAGR 10yr CAGR 20yr CAGR 2019 YoY +/-

Gippsland

Bass Coast $15,904 5.6% 1.9% 6.4% 12 -6

Baw Baw $18,650 6.5% 4.6% 5.9% 31 -16

Cardinia $19,242 -0.2% -0.3% 5.4% 11 -3

East Gippsland $4,898 3.0% 5.0% 6.3% 57 -1

Latrobe $14,832 12.9% 2.6% 8.9% 12 -9

South Gippsland $14,431 5.3% 3.8% 6.5% 62 -18

Wellington $10,421 3.6% 7.4% 6.9% 58 -31

Gippsland $11,002 3.1% 5.5% 6.3% 243 -84

North West

Buloke $2,471 13.4% 7.5% 6.6% 35 -7

Hindmarsh $3,632 11.5% 11.4% 8.5% 29 1

Horsham $6,150 13.7% 15.0% 6.7% 21 -11

Mildura $1,417 6.0% 4.9% 7.6% 20 -12

Swan Hill $3,287 21.4% 10.2% 11.9% 21 5

Yarriambiack $3,413 9.3% 6.2% 6.1% 21 -7

North West $3,092 12.2% 8.9% 7.6% 147 -39

Northern

Alpine $12,812 16.6% 9.5% 7.5% 14 0

Benalla $8,022 7.4% 7.8% 7.6% 34 -7

Bendigo $8,431 15.5% 9.4% 8.8% 30 1

Campaspe $5,448 5.5% 5.1% 5.2% 68 3

Gannawarra $3,108 7.4% 6.0% 3.0% 26 -14

Indigo $9,681 8.1% 5.0% 8.2% 31 12

Loddon $3,637 11.4% 6.4% 5.4% 36 -9

Mansfield $10,508 7.0% 4.2% 7.3% 25 2

Mitchell $9,652 12.3% 8.9% 7.3% 19 -14

Moira $7,371 6.5% 5.6% 3.7% 67 -10

Mount Alexander $7,403 -0.2% 2.1% 10.2% 14 -13

Murindindi $8,852 9.9% 7.4% 7.6% 32 6

Shepparton $7,756 8.5% 4.9% 4.5% 62 2

Strathbogie $6,138 7.8% 3.2% 6.3% 46 -21

Towong $6,706 4.7% 11.0% 10.2% 25 -4

Wangaratta $8,388 10.4% 7.4% 6.9% 34 -23

Wodonga $8,945 0.5% 5.6% 4.1% 5 1

Northern $7,331 9.1% 7.0% 6.9% 568 -21

18

-

MunicipalityMedian $/ha Number of transactions

2019 5yr CAGR 10yr CAGR 20yr CAGR 2019 YoY +/-

South West

Ararat $6,384 8.4% 5.6% 7.4% 26 -10

Ballarat $13,359 10.2% 6.0% 9.2% 4 -3

Central Goldfields $6,101 16.1% 17.5% 9.3% 7 -1

Colac - Otway $11,013 10.2% 5.0% 6.0% 38 -15

Corangamite $10,749 7.7% 6.4% 7.3% 93 33

Glenelg $9,670 13.1% 6.1% 8.0% 50 3

Golden Plains $9,899 16.5% 6.7% 9.3% 27 -6

Hepburn $8,655 5.8% 4.1% 6.1% 14 4

Macedon Ranges $15,659 25.2% 7.2% 7.3% 12 2

Moorabool $11,223 5.9% 5.9% 5.8% 11 -6

Moyne $10,440 7.1% 2.3% 7.6% 82 17

Northern Grampians $3,306 9.1% 5.8% 7.3% 34 -3

Pyrenees $6,212 5.9% 6.9% 7.9% 31 -7

South Grampians $5,703 7.1% 5.0% 6.8% 36 -13

Surf Coast $8,846 6.5% 0.8% 6.1% 7 1

West Wimmera $5,189 18.5% 8.1% 8.3% 34 -10

South West $8,649 12.1% 7.2% 7.8% 506 -73

Victoria $7,587 9.1% 6.8% 7.1% 1,464 -217

CAGR: Compound Annual Growth Rate

Price information with a small volume of transactions should be

used with caution. The median price for municipalities with less

than four transactions in 2019 is not reported.

*Municipalities with no transactions in 2019 have compound

annual growth rate for fi ve, ten and twenty years presented using

the 2018 median.

19

-

For report enquiries

For more detailed and in depth insights or customised reports

email: [email protected]

Subscribe

Visit ruralbank.com.au/subscribe to receive future research and

analysis to support you in making informed business decisions on

your farm.

For banking enquiries

Rural Bank products are available through Elders and Bendigo

Bank branches.

To fi nd out more about Rural Bank’s range of specialist farm fi

nance products and services contact your local Rural Bank

Agribusiness Relationship Manager, call 1300 660 115 or visit

ruralbank.com.au