Embed Size (px)

Citation preview

Aurangabad Branch of Western India Regional Council

The Institute of Chartered Accountants of India

Seminar on Bank Branch Audit

Audit of Agricultural Advances

CA Prakash P. KulkarniMarch 25, 2018

• Concept of Agricultural Credit• Crop Loans & IRAC Norms• Interest Application• Interest Subvention• Restructuring of Loans in natural calamities• Verification of Agri Advances

Presentation Outline

2

3

Concept of Agricultural Credit

Crop Loan or Short Term Loan• For financing revenue expenditure of raising the crops.• Repayable after crop season. Medium Term Loan• Outlay of the replacement & maintenance of assets and for capital

investment designed to increase the output from land.• Purpose: deepening of wells, sinking of new wells, installation of pump

sets, purchase of agricultural machinery or a pair of bullocks, etc.• Repayable in 3 to 5 years.

Credit Needs of Agriculture

4

Long Term Loans• Capital investment in agriculture.• Sinking of new wells, construction of tube wells, land levelling, bunding,

terracing, purchase of tractors, power tillers & other costly machinery, electrical motors, purchase of land, etc.• Repayable over a period of 5 to 15 years and in exceptional cases in 20

years.

Credit Needs of Agriculture

5

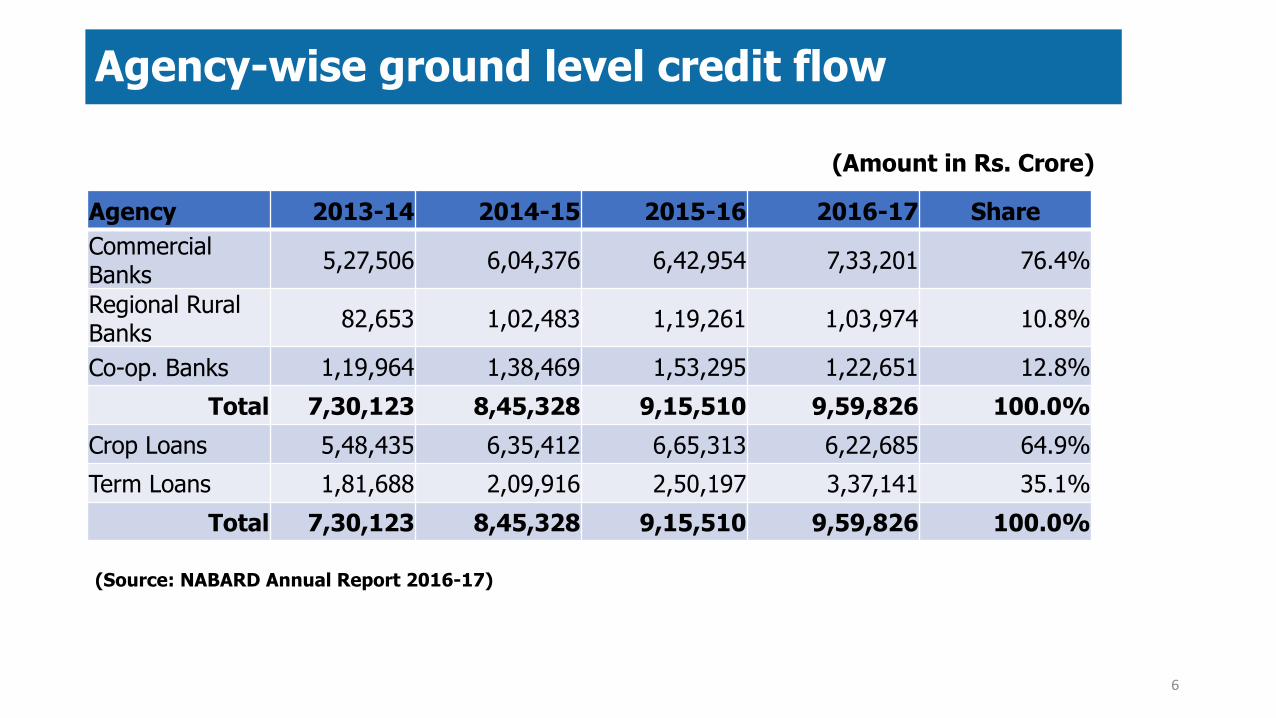

Agency-wise ground level credit flow

6

(Amount in Rs. Crore)

Agency 2013-14 2014-15 2015-16 2016-17 ShareCommercial Banks 5,27,506 6,04,376 6,42,954 7,33,201 76.4%

Regional Rural Banks 82,653 1,02,483 1,19,261 1,03,974 10.8%

Co-op. Banks 1,19,964 1,38,469 1,53,295 1,22,651 12.8%Total 7,30,123 8,45,328 9,15,510 9,59,826 100.0%

Crop Loans 5,48,435 6,35,412 6,65,313 6,22,685 64.9%Term Loans 1,81,688 2,09,916 2,50,197 3,37,141 35.1%

Total 7,30,123 8,45,328 9,15,510 9,59,826 100.0%

(Source: NABARD Annual Report 2016-17)

A farmer cultivating agricultural land (as owner or tenant or share cropper)Marginal Farmer§ Up to 1 hectare (2.5 acres)Small Farmers§ More than 1 up to 2 hectares (2.5 to 5 acres)Medium Farmers§ More than 2 up to 5 hectares (5 to 12.5 acres)Large Farmers§ More than 5 hectares (12.5 acres)

Classification of Farmers

7

• An inter-institutional forum for co-ordination & joint implementation of development programmes and policies by all the financial institutions operating in a state.

• A bankers’ forum. Government officials are also included.

• In terms of RBI directives, SLBC of respective state required to determine “Duration of Crop” i.e. Crop Season” for each crop & overdue period for identification of NPAs.

• SLBC Maharashtra : Chairman Mr.Ravindra Marathe (MD & CEO of Bank of Maharashtra)

SLBC

8

• Till 31st March 2015ü Direct & Indirect Agricultural Advances• From 1st April 2015ü Farm Creditü Agri. Infrastructureü Ancillary Activities(Ref.: RBI-2014-15/573 FIDD.CO.Plan.BC.54/04.09.01/2014- 15 dated April 23, 2015)

Classification of Agricultural Advances

9

Loans to individual farmers [including Self Help Groups (SHGs) or Joint Liability Groups (JLGs)ü Proprietorship firms of farmersü directly engaged in Agriculture & Allied Activities, viz., dairy, fishery,

animal husbandry, poultry, bee-keeping & sericulture. a. Crop loans to farmers - traditional/non-traditional plantations,

horticulture, & loans for allied activities. b. Medium and & long-term loans to farmers - e.g. purchase of agricultural

implements & machinery, loans for irrigation & other developmental activities undertaken in the farm & developmental loans for allied activities.

c. Loans to farmers for pre & post-harvest activities, viz., spraying, weeding, harvesting, sorting, grading & transporting of their own farm produce.

1.1 Farm Credit to Individual farmers

10

d. Loans to farmers up to Rs. 50 lakh against pledge/ hypothecation of agricultural produce (including warehouse receipts) for a period not exceeding 12 months.e. Loans to distressed farmers indebted to non-institutional lenders.f. Loans to farmers under the Kisan Credit Card Scheme. g. Loans to small & marginal farmers for purchase of land for agri purposes.

1.1 Farm Credit to Individual farmers

11

• Loans to corporate farmers• Farmers' producer organizations - companies of individual farmers,

partnership firms & co-operatives of farmers• Directly engaged in Agriculture & Allied Activities, viz., dairy, fishery,

animal husbandry, poultry, bee-keeping & sericulture up to an aggregate limit of Rs. 2 crore per borrower.

1.2 Agri Loans to Organised Sectors

12

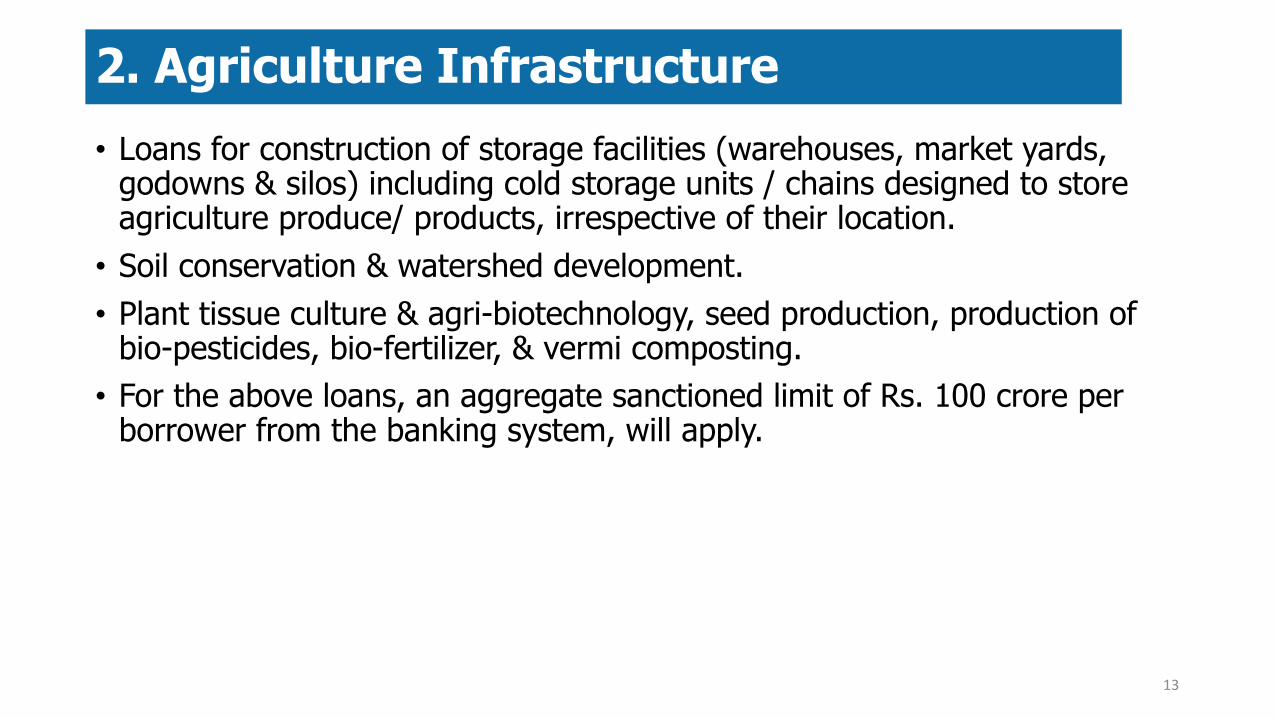

• Loans for construction of storage facilities (warehouses, market yards, godowns & silos) including cold storage units / chains designed to store agriculture produce/ products, irrespective of their location. • Soil conservation & watershed development. • Plant tissue culture & agri-biotechnology, seed production, production of

bio-pesticides, bio-fertilizer, & vermi composting.• For the above loans, an aggregate sanctioned limit of Rs. 100 crore per

borrower from the banking system, will apply.

2. Agriculture Infrastructure

13

• Loans up to Rs. 5 crore to co-operative societies of farmers for disposing of the produce of members. • Loans for setting up of Agriclinics and Agribusiness Centers. • Loans for Food & Agro-processing up to an aggregate sanctioned limit of

Rs. 100 crore per borrower from the banking system. • Loans to Custom Service Units managed by individuals, institutions or

organizations who maintain a fleet of tractors, bulldozers, well-boring equipment, threshers, combines, etc., and undertake farm work for farmers on contract basis. • Bank loans to Primary Agricultural Credit Societies (PACS), Farmers’

Service Societies (FSS) and Large-sized Adivasi Multi-Purpose Societies (LAMPS) for on-lending to agriculture. • Loans sanctioned by banks to MFIs for on-lending to agriculture sector as

per the conditions specified in paragraph 19 of these Master Directions. • Outstanding deposits under RIDF and other eligible funds with NABARD on

account of priority sector shortfall.

3. Ancillary activities

14

• Scheme for providing adequate & timely credit support, under single window, to the farmers for their cultivation & other needs• Short term credit limits ü To meet the short term credit requirement for cultivation of crops ü Post harvest expenses ü Produce marketing loan ü Consumption requirement of farmer household ü Working capital for maintenance of farm assets & activities allied to

agriculture like dairy, inland fishery etc.• Long term Credit LimitsüInvestment credit requirement for agriculture & allied activities like pump

sets, sprayers, dairy animals etc. • KCC is not a type of loan, but is a channel for granting either short term or

long term agricultural finance.

4. Kisan Credit Cards

15

• The aggregate of credits into the account during the 12 monthsperiod should at least be equal to the maximum outstanding inthe account.• No drawal in the account should remain outstanding for morethan 12 months in case of normal crops and 18 months in caseof sugarcane and banana crops.• In order to have operational and accounting convenience, thecard limit is bifurcated in to separate sub-limits for short termcash credit limit cum savings account and term loans.

4. Kisan Credit Cards

16

17

Crop Loans & IRAC Norms

• RBI Master Circular dated 1st July 2015 on IRAC Norms – para no. 2.1.2 (iv) & (v)• NPA classification of Agri Loans linked with:

ü Nature of cropü Duration of crop / crop season

• In India, several crops have different crop seasons in different states• Applying a single form for NPA & setting up the system parameters in CBS

difficult• System to be configured to capture relevant SLBC guidelines for crop seasons &

classification of crops• Implementation of relaxations due to natural calamities & de-monetisation of

HDNs • Auditors to verify the parameters in CBS to ensure correct implementation of

IRAC norms

NPA assessment of Agri Loans

18

“Long duration” Crops • Crops with season longer than one year.“Short duration” Crops • Crops which are not “long duration” crops.§ The period up to harvesting of the crops raised, includes period required for

sale of crops as well.§ Based on the sowing, harvesting period prevailing in the State, crop pattern,

agro climatic condition. § determined by the State Level Bankers’ Committee (SLBC) in each State

depending upon the duration of crops raised by an agriculturist.§ Same crop may have different harvesting season in different states as

decided by the respective SLBC of those states.Auditors’ Role• Whether crop seasons as defined by the SLBC mapped properly in CBS?• Any discrepancies may have a direct impact on identification of NPAs.

Crop Season

19

• Except sugarcane & banana, all other crops would be reckoned as Short duration crops.• Crops like paddy, sugarcane etc. may have a single crop or multiple crops,

depending on the state / manner of cultivation or manner of cultivation.

Kharif Crop• May – June• Due date of repayment may be fixed 31st March.Rabi Crop• Oct – November• Due date of repayment may be fixed 30th June.

Crop Season in Maharashtra

20

Crop PeriodSowing Harvesting

KharipRice May – September October – JanuaryBajra June – August September – NovemberMaize May – August September – DecemberCotton May – July December – April Tur June-July December – FebruaryGroundnut June-August September – December

21

Sowing & Harvesting period of few Principal Crops

Crop PeriodSowing Harvesting

RabiJowar September – October January – MarchMaize October – December January – MarchWheat October – December January – MarchCotton August – September February – April

Sugarcane June -July Next November - February(Adsali)

22

Sowing & Harvesting period of Principal Crops

Short duration Crop Loans• Loan treated as NPA, if the instalment of principal or interest thereon

remains overdue, from the repayment due date, for two crop seasons.Long duration Crop Loans• Loan treated as NPA, if the instalment of principal or interest thereon

remains overdue, from the repayment due date, for one crop season.

NPA norms for Crop Loans – RBI Circular

23

• Short Duration Crops• Kharip & Rabi Crops –

Loan treated as NPA of instalment of principal / interest remains overdue for 21 months from repayment due date.

•Horticulture Crops –Loan treated as NPA of instalment of principal / interest remains overdue for 24 months from repayment due date.

IRAC Norms – SLBC

24

• Long Duration Crops• Sugar Cane (Adsali) –

Loan treated as NPA of instalment of principal / interest remains overdue for 18 months from repayment due date.

• Banana (Mrig Bahar) –Loan treated as NPA of instalment of principal / interest remains overdue for 21 months from repayment due date.

IRAC Norms – SLBC

25

• Kisan Credit Card facility being in the nature of cash credit accommodationfor agricultural purposes, the prudential norms as applicable to suchfacilities would apply to the KCC accounts.• A KCC account would be deemed to be a Non-Performing Asset (NPA) if itremains out of order for a period of two crop seasons / one crop season(as the case may be, depending on the duration of the crops) after therepayment due date.• The crop seasons after the due date should refer to only those twoconsecutive crop seasons in which the farmer usually undertakes cropproduction.

• An account will be treated as out of order in the following circumstances:• There are no credits in the account continuously for two crop seasons as onthe date of balance sheet, or

• The credits in the account are not sufficient even to cover the interest debitedin respect of the account for two crop seasons, or

• The outstanding remains continuously in excess of the limit for two cropseasons as on the date of balance sheet.

Kisan Credit Cards

26

NPA Classification – Vehicle Loan

27

• Land located in irrigated area, with both Kharip & Rabbi crops.• Vehicle Loan granted in January 2016. • Repayment in half yearly instalments to start from October

2016 – April 2017 & onwards, linked to cropping pattern. • If the instalment due in October 2016 is not repaid by due date,

the same will be overdue from November 2016. • If the overdue continues for 2 crop seasons, the account will

slip to NPA, in November 2017.

NPA Classification – Vehicle Loan

28

Particulars Time LinesDate of finance January 2016Season Starts June / July 2016Harvesting time October 2016Due date for repayment of Instalment October 2016

First crop season after due date: (Rabbi)Season Starts October 2016Harvesting time February / March 2017Second crop season after due date: (Kharip)Season Starts June / July 2017Harvesting time October 2017NPA 1st November 2017

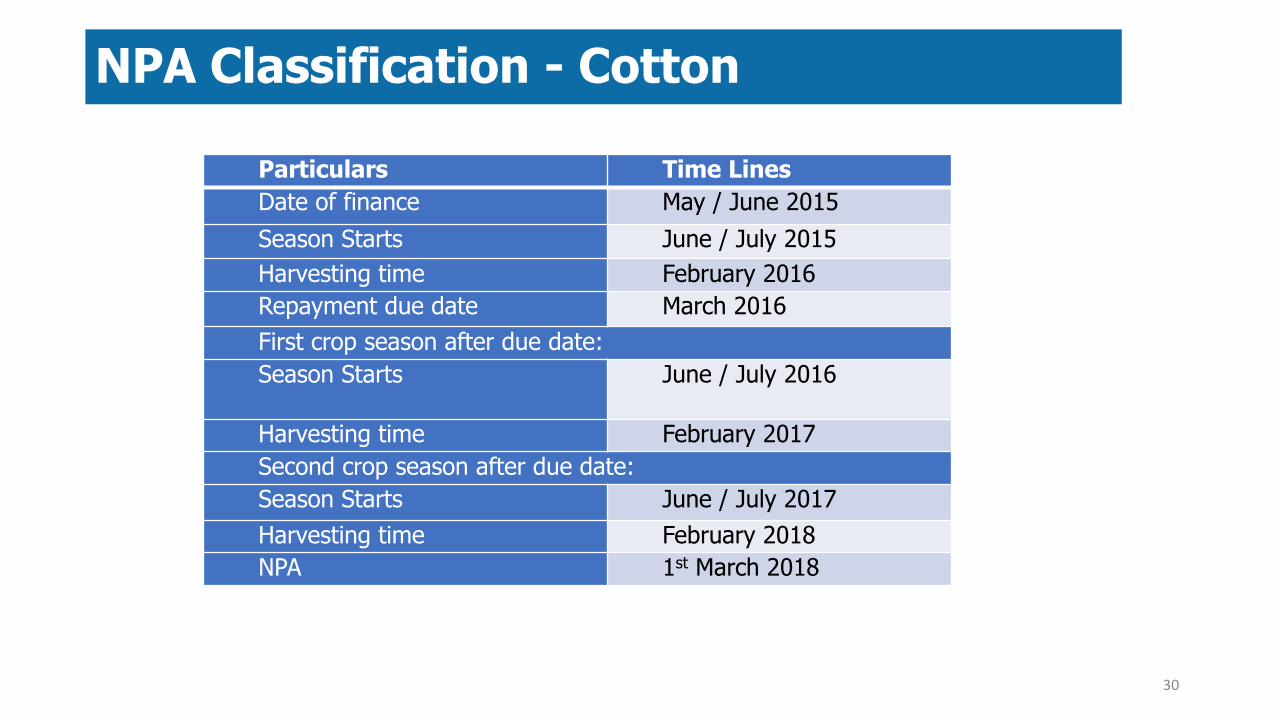

NPA Classification - Cotton

29

• Crop season similar to Kharip season (June to February).

• IRAC status - norms applicable to Kharip crops.

• Advance granted in May / June 2015 for cultivation of Cotton.

• Based on crop season, repayment due date - by March 2016.

• If not repaid by due date i.e. March 2016, the account shown as overdue.

• If overdues continue for 2 crop seasons, the account will slip to NPA - February / March 2018.

NPA Classification - Cotton

30

Particulars Time LinesDate of finance May / June 2015Season Starts June / July 2015Harvesting time February 2016Repayment due date March 2016First crop season after due date:Season Starts June / July 2016

Harvesting time February 2017Second crop season after due date:Season Starts June / July 2017Harvesting time February 2018NPA 1st March 2018

NPA Classification - Oranges

31

• Term loans granted right from the activity of land preparation.• Normally requires about 3-4 years to bear the fruit.• Repayment period stipulated beyond 10 years - up to 15 years. • Moratorium granted generally up to 5-6 years.• Interest during moratorium capitalised subject to sanction terms. • With moratorium for 5 years, first repayment due at the end of

6th year.• NPA at the end of 8 years.

NPA Classification - Examples

32

ParticularsYear of Finance

Kharif Season

Rabi Season

Horticulture Crop

Perennial crop Sugarcane

(Adsali)Perennial crop

Banana

Date of finance 01-06-2015 01-10-2015 Aug-2014 01-07-2014 01-06-2014Season starts Jun-2015 Oct-2015 Sep-2014 01-07-2014 01-06-2014

Harvesting time Oct Nov-2015 Mar-2016 May-2015 Dec-2015 /Jan-2016

Jun-2015 /Jul-2015

Repayment due date 31-03-2016 30-06-2016 30-06-2015 30-06-2016 30-09-2015

First crop season after due dateSeason starts Jun-2016 Oct-2016 Sep-2015 01-07-2016 01-06-2016

Harvesting time Oct Nov-2016 Mar-2017 May-2016 Dec-2017 /Jan-2018

Jun-2017 /Jul-2017

Second crop season after due dateSeason starts Jun-2017 Oct-2017 Sep-2016Harvesting time Oct Nov-2017 Mar-2018 May-2017NPA date 31-12-2017 31-03-2018 30-06-2017 31-12-2017 30-06-2017Months 21 months 21 months 24 months 18 months

• Fishery activity established in coastal areas of the then Andhra State (e.g. Bheemavaram, Rajamundri etc.)

• “Fish Ponds” cultivated in the agri. fields by farmers by irrigating water

• Main fish produce - Rohu, Katla, Shrimps etc. being exported to Kolkata, Orissa as well as outside countries

• Groups of farmers co-ordinated with specific fish export houses (formed by them coming together in some cases)

• Thousands of such cases were financed, typical size being Rs. 1-2 crore per borrower. Export houses also financed separately for their working capital.

Case study: Fishery Loans

33

• What went wrong• Fish Pond Land offered as collateral security over-valued to avail higher

loans. (Since 100% collateral insisted in many cases)

• Sanctioned finance not based on repayment capacity as per size of pool and expected yield

• Fishing activity took major hit due to natural calamities, lack of expertise as well as fraudulent intentions in few cases.

• Lack of pre & post disbursement monitoring through visits• Thus, primary security was Nil in almost all cases.

• Prices of land affected adversely due to Telangana issue, plus government lands fraudulently offered in some cases, thus erosion in collateral of 90% or more

• Result : 100% Provision by Banks for majority loans.

Case study: Fishery Loans

34

35

Interest Application

• Interest at monthly rests not applicable to Agri Advances• Charging of interest linked to Crop Seasons - at bi-annual or

annual rests.• Compounding generally not permitted, unless overdue.• Total Interest debited not to exceed the Principal Amount –

Short Term Advances to Small & Marginal Farmers• (Reference Para no. 4 (ii) RBI Master Circular – Interest on

Advances – 1st July 2015.• Interest Application Annexure 1• Interest Application Annexure 2

Features of Interest on Agri Loans

36

37

Interest Subvention to farmers

• RBI Circular dated 16th August 2017 – Approved scheme by Govt. of India towards the implementation of interest subvention scheme for FY 2017-18 for short term crop loans up to Rs.3 Lakhs.• Eligibleü Public / Private Sector Scheduled Commercial Banks (in respect of loans

given by the rural and semi urban branches)• Interest subvention of 2% p.a. on their own funds used for short term

crop loans up to Rs.3.00 lakh per farmer• Short term credit made available at 7% p.a. to farmers.• Calculated on the crop loan amount from the date of its disbursement/

drawal up to the date of actual repayment of the crop loan by the farmer or up to the due date of the loan fixed by the banks, whichever is earlier, subject to a maximum period of one year.

Interest subvention on loans disbursed

38

• From 2011-12, additional interest subvention of 3% to those farmers, who repay their short term crop loans promptly and on or before the due date.• Farmers, who promptly repay their crop loans as per the repayment

schedule fixed by the banks, extended loans at an effective interest rate of 4% p.a.

Interest subvention scheme to post harvest loans • Scheme extended to small & marginal farmers (having Kisan Credit Card)

for a further period up to six months post harvest, against negotiable warehouse receipt for keeping their produce in warehouses. • To discourage distress sale by farmers & to encourage them to store their

produce in warehouses against warehouse receipts.

Additional Interest subvention

39

• Certificate of Interest Subvention to be submitted alongwith annual accounts • Audit procedure w.r.t. certification:-

• Obtaining borrower-wise list of short term credit disbursed during 2017-18 by thebranch

• To check system put in place by the banks to carry out due diligence to ensurethat only genuine farmers avail concessional crop loans.

• Review of documentation including recording of land details held by the branch.• Selective test check and documentation by referring to the sanction letters and

system records to ensure that short term production credit up to Rs. 3 Lakhs aredisbursed @ 7% p.a.

• In respect of additional subvention @ 3%, scrutiny of accounts selected in testcheck to ensure that the loans were repaid in time and subvention @ 3% hasbeen already passed on to the borrower by credit to his loan account.

Auditors’ Role

40

41

Restructuring of Loansin Natural Calamities

RBI Master DirectionDrought HailstormPest attack Cold wave/frost Cyclone EarthquakeFire FloodTsunami LandslideAvalanche Cloud burst

NPA norms upon restructuring

42

RBI Master Direction FIDD.CO.FSD.BC.No. 8/5.10.001/2017-18 dated July 03, 2017.• Natural calamity - SLBC or District Consultative Committee (DCC) to evolve a

coordinated action plan for implementing the relief programme.• Relief measures - Crop loss assessed should be 33% or more.• Banks allowed to restructure loans to borrowers affected by natural calamities.• All short-term loans, except those which are overdue at the time of occurrence of

natural calamity, eligible for restructuring.• Principal amount of the short-term loan & interest due for repayment in the year

of the natural calamity may be converted into term loan.• Moratorium period of at least one year.• Banks not insist on additional collateral security for such restructured loans.• The existing term loan instalments should be rescheduled keeping in view the

repaying capacity of the borrower and the nature of natural calamity.

NPA norms upon restructuring

43

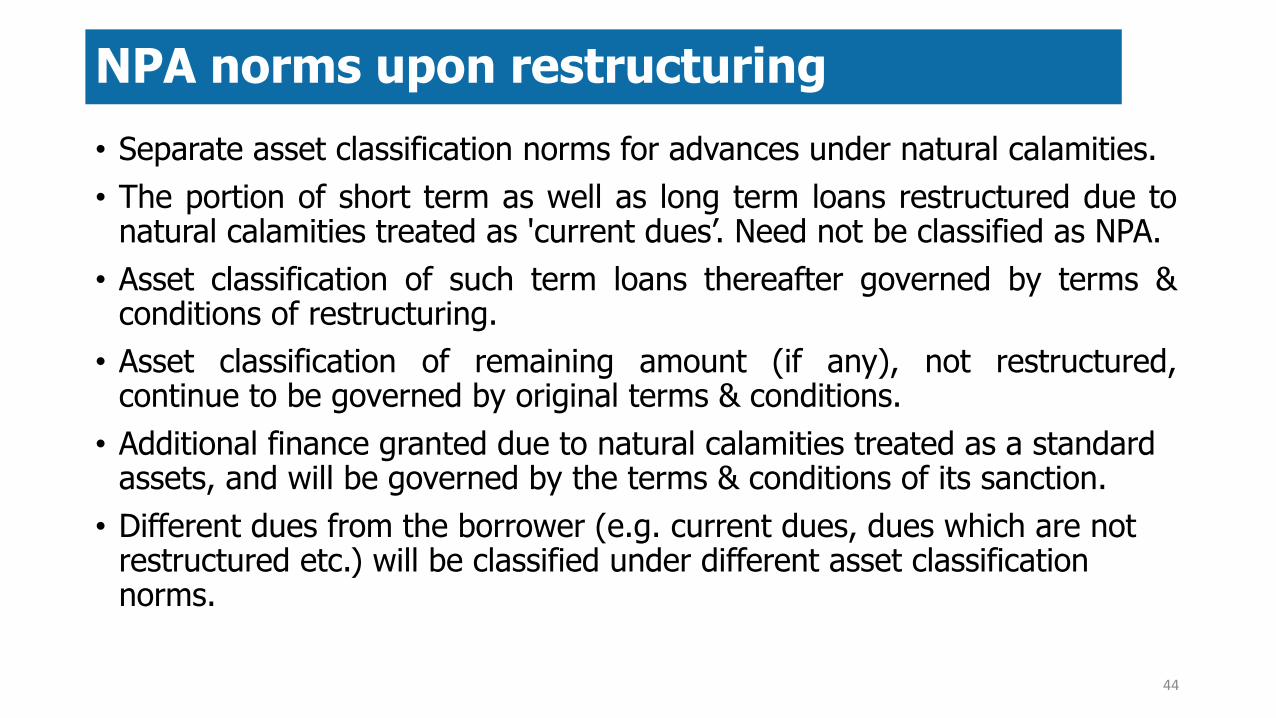

• Separate asset classification norms for advances under natural calamities.• The portion of short term as well as long term loans restructured due to

natural calamities treated as 'current dues’. Need not be classified as NPA.• Asset classification of such term loans thereafter governed by terms &

conditions of restructuring.• Asset classification of remaining amount (if any), not restructured,

continue to be governed by original terms & conditions.• Additional finance granted due to natural calamities treated as a standard

assets, and will be governed by the terms & conditions of its sanction. • Different dues from the borrower (e.g. current dues, dues which are not

restructured etc.) will be classified under different asset classification norms.

NPA norms upon restructuring

44

• Accepted departure from the basic principle of IRAC norms, i.e. NPAshould be borrower-wise and not facility-wise.• Banks are required to make higher provisions for such restructuredstandard advances as prescribed by Department of Banking Regulationfrom time to time. (At present @ 5%).

NPA norms upon restructuring

45

46

Verification of Advances

Component in Kind• Based on the cost of inputs - fertilizers, seeds, pesticides etc. - essential

for cultivation of crops.• Amount disbursed directly to the supplier of inputs to ensure end use of

funds. Cash Component• Mainly for expenses - hired labourers, hire charges for tractors, machinery,

electricity charges etc.Disbursement• Meeting the current expenditure in connection with raising of crops.• In stages linked up with inspection to ensure ultimate use of funds.

Production Loans / Farm Credit

47

• Short term loans extended to labourers engaged for cutting of sugar cane crops and transportation thereof to the sugar factory. (i.e. “Toli Finance”)

• Loans are primarily unsecured, guaranteed by the sugar factory.

• Repayment of Loans from pay bills released by sugar factory. Proportionate remittance to banks from each bill.

• Repayment depends totally on capacity and financial health of the sugar factory, as such careful assessment thereof is also required.

• KYC of labourers required to be done carefully.

• Bank should ensure proper end-use of funds.

• Pre & Post Disbursement visit are essential.

• Instances of diversion of these funds towards factory activities.

Harvesting & Transportation (H&T) Loans

48

• Warehouses provide temporary advances to farmers against stored crops

• Insulation of farmers against adverse price movements

• Advances purely short term in nature & seasonal (3- 6 months)

• Banks finance warehouses against such temporary advances given to farmers

• Pre & Post Disbursement visit is absolutely essential to ensure genuineness

• Instances of diversion of these funds towards warehouses

Loans to Warehouses

49

• Constitute a major portion of agricultural finance.

• Certain relaxations from normal gold loans• Maximum LTV Ratio of 25% is not required to be maintained• Interest on half yearly basis as against monthly• Repayment linked to crop season as against maximum tenor of 12

months

• Banks to ensure genuineness of Agricultural Operations (through documentary proofs and pre & post disbursement visits)

• Instances of normal loans being reflected as agri. loans are evident.

Agri. Loans against Gold: RBI guidelines

50

Scale of Finance• The credit requirement for raising a particular crop termed as “Scale of

Finance”.• Determined by a Technical Group, comprising members of DCCB, PACS,

Agriculture, State Govt., Lead Bank of the district etc.• Approved by District Consultative Committee.Eligibility• Eligibility for loan / size of loan determined not with reference to the value

of land or any other tangible security.• On the basis of the size of holding that he cultivates & the cost of

cultivation of crops, which the farmer proposes to grow.

Scale of Finance & Eligibility

51

Primary Security• Standing crops under cultivation.Secondary Security• Loans against security of NSC, KVP or Fixed Deposits of Banks, utilised for

agricultural purposes, allowed to be classified as Agri. loans.

Primary & Secondary Security for Crop Loans

52

ApplicationSanction• Sanction as per scale of finance applicable to the land under cultivation &

crop being cultivated.• Loan extended only after obtaining ‘No dues / No objection Certificate’

from the existing credit agencies.Disbursement• Disbursement in various ‘stages’ based on the requirements of farming

activity.• Expenditure incurred by farmers from own sources or from non-

institutional lenders & subsequently reimbursed by banks.• Verify the facts from the documents / evidence available on record.• Documents evidencing the utilisation of loans for agricultural activities.

Key Audit aspects for Agri Loans

53

Inspection• Primary security - standing crops under cultivation.• Pre & post sanction visits by the Agri. Officers.• Adequate documentation of visit report.Security• To confirm legal enforceability of security.• Standing crops, Agricultural machinery & implements secured by

hypothecation.• Agricultural land secured by a mortgage charge.

Key Audit aspects for Agri Loans

54

• Auditors should ensure:ü Copy of the land revenue extracts (7 /12 extract)ü Land Tax Assessment & payment receipt.ü Copy of record with sub-registrar (wherever applicable)ü Original title deeds.ü Search of title deeds & opinion from Advocate on the Bank’s

approved panel about the title of the borrower.ü Valuation of land from a Valuer on the Bank’s approved panel.

Key Audit aspects for Agri Loans

55

Recovery• Serviced through realisation of sale proceeds to crop.• Auditors to verify the nature and timing credits coming in to service the

agri. loans, to ensure genuine sources.

• Reimbursement of Expenses already incurred by farmer • Some times farmers incur expenses from own source, and are later on

reimbursed by banks by way of disbursement of loans to savings of farmer or by cash withdrawals

• Such transactions require careful scrutiny

• Bank to ensure authenticity of such transactions by collecting documentary proofs

Key Audit aspects for Agri Loans

56

Auditors to should examine following aspects:• Adoption of SoF fixed by the Technical Group (TG) – whether the SoF was

fixed by TG followed uniformly by all the branches. If the scale of finance fixed by TG was used as indicative, whether the range of variation was reasonable?• Annual verification of entries therein with revenue records, verification of

cropping pattern of borrowing members indicated in the Normal Credit Limit (NCL) Statement with the land records for avoiding inflated/ghost acreage for crops carrying higher scales of finance, etc.,• Whether all the borrowers of crop loans were issued Kisan Credit Card

(KCC). If not, the reasons and the extent to which covered under KCC.• Disparity in the scales of finance and actual disbursements-specific

reasons may be ascertained and commented in cases where the banks had higher scales of finance but disbursements were made at a very low level.

Audit of Crop Loans

57

• Action taken by banks in implementing the various production programmes sponsored by GoI/State Governments.

• Whether the norms for identifying small farmers are those fixed by Nationalised Bank? If not, the actual norms followed by the bank

• Examine the Crop Insurance Scheme introduced in the area of operation of the bank covering the following aspects:

(a) Names of blocks in the district where the scheme is in operation.(b) Crops covered.(c) Farmers covered - No. of farmers to whom loans were disbursed.(d) Area (in hectares) covered crop-wise.(e) Amount of loans disbursed crop-wise.(f) Sum insured (100% of (e) subject to a maximum limit of Rs.10,000 per farmer)(g) Insurance charges recovered.

58

Audit of Crop Loans

• Amount of subsidy obtained/to be obtained in the case of small and marginal farmers.• Whether insurance premium deducted out of loans has been passed on to

the General Insurance Corporation (GIC).• On receipt of claim amount from GIC/State Insurance Fund, whether the

bank has passed on the amounts to the concerned borrower giving full details of the notified area/crop to which the claim relates and the percentage of the sum insured or loan which has been reimbursed and credited the amounts to the respective accounts.

59

Audit of Crop Loans

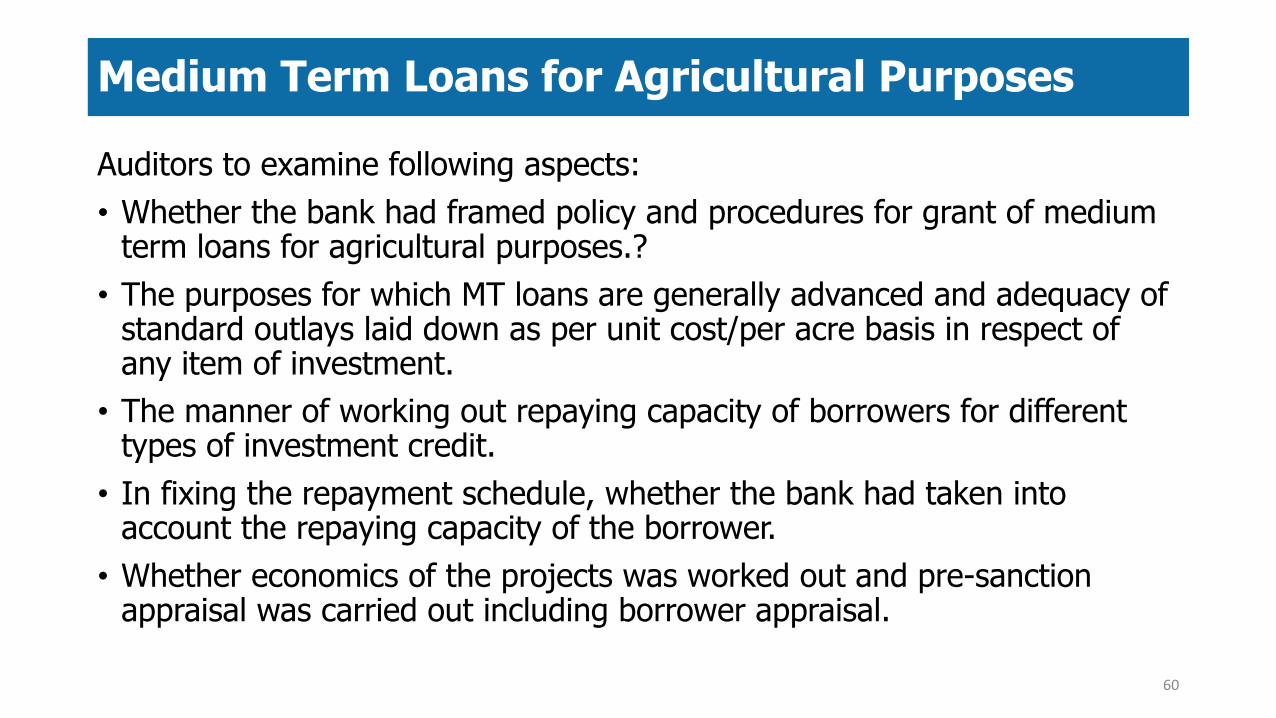

Auditors to examine following aspects:• Whether the bank had framed policy and procedures for grant of medium

term loans for agricultural purposes.?• The purposes for which MT loans are generally advanced and adequacy of

standard outlays laid down as per unit cost/per acre basis in respect of any item of investment.• The manner of working out repaying capacity of borrowers for different

types of investment credit.• In fixing the repayment schedule, whether the bank had taken into

account the repaying capacity of the borrower.• Whether economics of the projects was worked out and pre-sanction

appraisal was carried out including borrower appraisal.

60

Medium Term Loans for Agricultural Purposes

• Whether security obtained for various medium term loans were as per the norms fixed by the RBI from time to time?• Method followed for valuation of land and its reasonableness.• Whether the due dates were fixed in accordance with the cash flow?• Whether utilisation/end-use of the credit was monitored and records

available for visits carried out by the field staff?• Whether insurance of assets acquired was insisted and whether available

during the pendency of the loan?

61

Medium Term Loans for Agricultural Purposes

Auditors to examine following aspects:-• Verify whether the movement of keys is properly recorded in the Key

Custody Register?• Whether the duplicate set of godown keys duly sealed are held under dual

control?• Confirm that the bank’s name plate is displayed.• Confirm holding of the original invoices/ lodgement letters and properly

executed delivery orders.• Confirm that the goods pledged are fully paid for.• Verify delivery goods are against payment & not against pledge of goods.• The value of the goods pledged is as per the invoices and the invoices are

in the borrower’s name. The value is not inflated to accommodate excess drawing power.

Advances against Commodities under Pledge

62

• Whether proper stipulated margin is maintained?• Identify the accounts secured by long outstanding unsold/stale/obsolete

stock. Furnish the steps taken by the bank/branch to close such loans.• Whether letter of access is obtained wherever necessary.• Carry out a test check of weight, contents and quality of goods pledged ,if

required in the presence of the borrower or his representatives.• Verify whether godown chart and godown registers are maintained and

kept up to date.• Whether the drawing power is revised and recorded from time to time?• Verify whether advances against commodities like cotton, tobacco

requiring licence /permits for dealings/storing/transportation are obtained and held with the bank/branch?

63

Advances against Commodities under Pledge

• Confirm that the goods pledged are properly insured and bank’s interest is noted in the insurance policy.• Ensure that the description of goods and godowns agrees with that

mentioned in the policy.• Verify whether the branch is maintaining market report book for local

commodity and recovering the additional margin whenever the prices fall.• Verify whether the Interest and penal interest have been collected as per

the terms and conditions from the borrowers periodically.

64

Advances against Commodities under Pledge

Questions ???

65

Thanks !!!

66