Embed Size (px)

Citation preview

Asia-Pacific Economic Cooperation

APEC Roundtable on ‘Best Practices’ in Infrastructure Development

APEC Economic Committee (EC)

1996

TABLE OF CONTENTS FOREWORD ............................................................................................................................ 1 INFRASTRUCTURE “BEST PRACTICES” ROUNDTABLE: CONFERENCE SUMMARY ............................................................................................ 3 CASE STUDIES: I. TRANSPORTATION-RELATED CASE STUDIES

• Australia: Melbourne City Link Infrastructure Financing Structure ...................... 13 • Canada: Public/Private Partnering: The Northumberland Strait Crossing Project ......................................................................................... 23 • Hong Kong: A Build, Operate and Transfer Franchise for a New, Strategic Road Link .............................................................................. 39 • Indonesia: Toll Road Investment in Indonesia ........................................................ 51 • Japan: Japan's Possible Support to Private Initiatives in Infrastructure Development: Bangkok Subway Project in Thailand ................................... 65 • Korea: Private Investment in Transportation Infrastructure Development in Korea: The Case of Chang-won Tunnel Project ........................................................................................................... 73 • Chinese Taipei: The High Speed Rail in BOT ......................................................... 83

II. WATER-RELATED CASE STUDIES

• Australia: Outsourcing the Water and Wastewater Systems of Adelaide, South Australia ........................................................................ 93 • Malaysia: Labuan Water Supply Privatisation ...................................................... 101 • Mexico: La Zurda - Calderon Regional System ..................................................... 113 • World Bank: The Reality of Public-Private Partnerships in the Water and Wastewater Sector ..................................................... 121

III. POWER-RELATED CASE STUDIES

• Australia: National Electricity Market Reform ..................................................... 213 • Indonesia: Electricity Sector in Indonesia ............................................................. 225 • Japan: Pagbilao Power Project in the Philippines ................................................ 239

IV. TELECOMMUNICATIONS-RELATED CASE STUDIES

• New Zealand: Telecom New Zealand Limited Kiwi Share .................................... 249 V. ENVIRONMENT-RELATED CASE STUDIES

• Canada: Opportunities for "Green" Best Practices: Asia Pacific Infrastructure Projects .............................................................................. 257

ANNEXES I. PRESENTATION BY ROBERT PRIETO, EXECUTIVE VICE PRESIDENT,

PARSONS BRINCKERHOFF INC. ................................................................. 271 II. LIST OF ROUNDTABLE PARTICIPANTS ...................................................... 281

FOREWORD

The APEC Roundtable on Best Practices in Infrastructure Development was a critical element of this year’s APEC agenda for promoting free trade and investment in the region. The event brought together more than 100 businesspeople and government officials from 14 Asia-Pacific economies to discuss ways to accelerate infrastructure development in the region, which is crucial to continuing economic growth. A remarkable consensus on many issues and a healthy airing of other viewpoints was achieved among the roundtable participants regarding what was needed to facilitate business sector participation in infrastructure development in the Asia-Pacific region. Participants identified some aspects of “best practices” in such areas as mitigating the risks of infrastructure projects, creating a supportive policy environment and regulatory regime for infrastructure development, and improving communications between the community, public and private sectors regarding infrastructure needs. The proposed inputs into “best practices” and related case studies were presented at the APEC Senior Officials Meeting, on August 19-20 in Davao, The Republic of the Philippines. In addition, there are plans to prepare further infrastructure “best practices” brochures and reference guides with supporting case studies that serve to place successful practices in context as an aid to facilitating infrastructure projects for government officials as well as private developers, investors and lenders. The APEC Roundtable on Best Practices in Infrastructure Development was a dynamic exercise in identifying possible needs and possible approaches to advancing public-private cooperation. We invite you to read the recommendations and case studies presented by this superb group of delegates. We would like to thank the National Center for APEC for its splendid arrangements for the Roundtable, and also thank the sponsors and individual participants for sharing the tremendous range of their experience. Ruslan Diwiryo

Raymond E. Vickery, Jr. Secretary General Assistant Secretary for Ministry of Public Works Trade Development Republic of Indonesia U.S. Department of Commerce

APEC INFRASTRUCTURE BEST PRACTICES ROUNDTABLE

SUMMARY REPORT

Seattle, Washington, United States of America July 24-26, 1996

BACKGROUND At their November 1995 meeting in Osaka the APEC Ministers decided to explore activities such as compiling best practices and holding public-private dialogues in order to enhance the effectiveness of the infrastructure development process. To this end, Indonesia and the United States co-hosted a Roundtable in Seattle, Washington, USA, July 24-26, 1996. Representatives of the public and private sectors of Australia, Canada, The People’s Republic of China, Hong Kong, Indonesia, Japan, the Republic of Korea, Malaysia, Mexico, the Republic of the Philippines, Chinese Taipei, Thailand, and the United States attended. The APEC Secretariat and the World Bank were also represented. The meeting was co-chaired by Mr. Ruslan Diwiryo, Secretary General, Ministry of Public Works, Republic of Indonesia, and Mr. Raymond Vickery, Assistant Secretary of Commerce for Trade Development, U.S. Department of Commerce. The Roundtable was structured to allow representatives of the public and business/private sectors to conduct small group discussions of case studies prepared by the participants on successful approaches to infrastructure development. As next steps, the work of the Roundtable will be developed in follow-on activities identified in the APEC Infrastructure Work Plan, and plans exist to prepare an infrastructure “best practices” brochure that can serve as a guide to facilitating infrastructure projects for government officials as well as private developers, investors and lenders. ROUNDTABLE FOCUS AND OBSERVATIONS The Roundtable on Best Practices in Infrastructure Development, which brought together more than 100 business people and government officials from 14 Asia-Pacific economies, was a critical element of this year’s APEC agenda for promoting economic and technical cooperation in the region. A remarkable consensus emerged among the Roundtable participants regarding what was needed to facilitate infrastructure development in the Asia-Pacific region, which is critical to sustaining growth. Roundtable participants focused on four interrelated areas relevant to infrastructure development and project implementation: 1) mitigation of infrastructure risk: financing and investment management alternatives; 2) creation of a supportive policy environment for infrastructure development; 3) beneficial elements of institutional structures and regulatory regimes conducive to infrastructure development; and 4) the importance of effective communication between the public and private sectors. The participants reached several conclusions on these subject areas, as summarized below:

A. Infrastructure Risk Mitigation: Financing and Investment Management Alternatives

International infrastructure development is fraught with risks for all parties involved - host government, project sponsor, investors, lenders and suppliers. Typically the host government wants to transfer most of the project risks to the private sector, while the private sector is anxious to minimize its risk exposure. How the parties identify, manage and mitigate risk is fundamental to any infrastructure project. During the APEC Roundtable, the participants made the following observations: 1. The mitigation and allocation of risk between the public and private sector should

be made clear and should reflect the nature of the individual project. Government and private investors should break the risk into segments as much as possible to allow distribution of the risk to the most appropriate party. Financial hedging techniques can be used and measures to offset the risk should be examined (for example, on a rail project, giving the investor the right to develop adjacent real estate)

2. Process transparency is paramount to attracting private investment. Financing and

insurance costs decrease with greater transparency. Government must make clear to private investors whether it will allow future projects which will compete with that investor. (If there is a toll road project to the airport and the government plans a parallel railroad in the future, the toll road investor must be fully aware of the plan.)

3. Privatization is not a method for government to escape all risk. Government must

understand the perspective of the private investor and consider the need for borrowed capital to be paid back in a timely fashion, and that inflexible pricing by government will only delay projects or kill them. In this regard, government must include in its calculations the economic price of inaction in delaying infrastructure development

4. Accurate feasibility studies in which both government and private investors honestly

look at both downside risks and potential profits, should be provided where necessary to clarify the technical, economic and risk fundamentals of investments. Government must be aware of the high cost of feasibility studies and contract acquisition risk (the cost to a private investor of seeking a contract). Where feasibility studies are a major cost and therefore a risk factor in projects, government should consider means to cover some or all of these costs, from government sources or within the price of the winning bid for the project

5. Government must take the risk-return profile of projects into consideration in

creating support measures to develop a project that is attractive and viable from both the private sector and public interest viewpoints. This may include government guaranteeing a rate of return, mitigating the impact of inflation or currency devaluations, and/or borrowing the capital with the private investor assuming repayment

B. Supportive Policy Environment for Infrastructure Development In an environment of strong international competition for private finance, the challenge facing many APEC economies is to create a policy environment that will encourage

private investment, both foreign and domestic, in infrastructure projects. Without substantial commitment and cooperation on the part of host governments, such investment is unlikely to materialize. Indeed, experience suggests that a proactive government policy to attract infrastructure investments can be a decisive factor in the competition for foreign investment. A proactive policy also provides the host government with an opportunity to manage infrastructure investment in a coordinated way, thus ensuring that the national interest is served. The APEC Roundtable participants’ key observations included recommendations in the general areas identified below: 1. Government must recognize that privatizing infrastructure is a major departure

from previous practices, transforming government’s role from a monopoly provider to an enabler. Previously only government could afford to undertake large scale infrastructure projects, however, private development of such projects is now feasible. This requires a new legal framework, a new philosophy, new mechanisms, and new ways of integrating financial and market criteria

2. Government must make a strong commitment to infrastructure development as a

matter of public policy and follow that commitment up with strong, consistent planning. Government must create a comprehensive master plan. In addition, government must create a clear regulatory framework and outline of procedures

3. Government should make its policy toward infrastructure development clear.

Recognizing that civil servants are not paid to take risks, and in fact operate in a culture which penalizes risk-taking, government needs to create a can-do attitude within its bureaucracy. The top policy levels of government need to make known to the working levels of government their support for the success of privately-financed infrastructure projects

4. Both government and private investors have to understand that they are a

partnership, and there must be goodwill toward all parties and recognition of needs at all levels. For example, government has to explain how its land ownership laws and labor laws work and provide clear implementing regulations; the private investor has to work within that framework

5. Government should provide a legislative framework that allows for profit, and

government should realize that it must bear the cost of changing regulations which affect the private investor

6. Government needs internal coordination and consistency concerning the regulation

of infrastructure projects, especially ensuring that financing mechanisms are consistent with tax rules

7. Government should ensure clear communication exists between the upper policy

levels of government, in which the commitment to private investment is clear, and the lower levels that are in closer contact with the public, and must implement public-private partnerships

C. Beneficial Institutional Structures and Regulatory Regimes The institutions and regulatory regimes in place for governing infrastructure projects are an important determinant in attracting private investors. An inadequate legal framework - or the lack of effective institutions for the enforcement of legal rights - will result in delay or undermine the strength and effectiveness of the various types of contracts that constitute the structure of the typical infrastructure project. In this regard, the participants of the APEC Roundtable made the following observations: Project Tendering & Selection Procedures 1. Government should make clear, understandable, and responsible long-term plans that

prioritize infrastructure projects. Bidding procedures should be disseminated widely and the expense of preparing bids should be kept to a minimum - early short-listing (pre-qualification) will prevent private investors from expending unnecessary money preparing bids for projects on which they have little chance of success

2. It is very important for all parties to develop clear project requirements as well as

clarity and maximum transparency in the process of choosing successful bidders. All investment restrictions should be laid out clearly in advance. Foreign investors should be clearly informed of any domestic preference so that they may make appropriate allowance for these in their bids. If foreign bidders are chosen, they should receive national treatment

3. Government needs to develop a “friendly,” non-adversarial, approach to the

preparation of bid documents and involve the private sector. In this process government can guarantee a rate of return and, to avoid monopolistic practices, receive income that exceeds an allowable revenue ceiling. But such agreements need to be mutual

4. Government should consider pre-qualifying bidders for a package of multiple

projects. If a bidder does not win one contract, they should not have to start all over to qualify for another project

5. Government should consider transparency procedures such as videotaping bid

presentations, having independent auditors present during the bid process, publicizing the names of those on selection committees, and preventing contact between selectors and bidders during the bidding process

6. Government should also allow the private sector to make unsolicited proposals that

fit overall policy parameters. Government should be impartial and objective in evaluating bids, so that bidders can focus on making their projects as cost effective as possible

7. If governments establish fair and clearly accountable selection processes, contracts

could be awarded by direct assignment or by solicited contracts. Privately financed projects should not have to be awarded through the same cumbersome competitive bidding process used when public funds are involved. The speed and lower cost achieved by doing this benefit both the investor and the public served by the

infrastructure project Project Administration, Approval and Decision-Making 8. Government should do as much pre-clearance of projects as possible. This could

include careful definition of the project, land acquisition, environmental clearances, and pre-approval of financing. The associated costs to government could be recouped by having the successful bidder pay a pre-clearance fee for these services

9. There is a need for a single point of registration of projects. At a minimum, the

government must identify clearly its organizational structure and process for the private investor. Government points of contact must have decision-making authority in the name of the government regarding specific projects. Internal government coordination should be the responsibility of this point of contact. The approval process for projects should be as consistent as possible across APEC economies

10. There should be a government-level body dedicated to bringing to fruition

privately financed infrastructure projects. This body should look at what needs to be done to finish the project, and not regard itself just as a regulatory body

11. Government needs to ensure that the project manager or agencies dealing with the

private investor are staffed with people with commercial experience or at least a proven ability to understand the investor’s point of view. This could prevent many disputes

12. Time limits must be established for each stage of the approval process. Government

should obtain as much information as possible from and about prospective bidders while they are preparing a tender. Government should narrow the field of bona fide contenders as early as possible to limit the cost of further bid preparation to only these contenders

Project Financing Considerations 13. Government should be sensitive to actions which affect the finances of the private

investor. Government may need to guarantee debt repayment or provide a stand-by cash flow to service senior debt repayment in the early days of some projects. Tax relief can be tied to performance and there can be time and tax penalty links, including compensations borne by government if it does not meet its performance timetables

14. Expedited approval procedures should be considered for privately-financed

infrastructure projects. Examples include a pre-clearance process and a time limit on government approval (i.e., if no action is taken by a certain date, approval is assumed)

15. Government should be willing to openly consider financial incentives, including

subsidies where appropriate to underwrite socially necessary infrastructure. Government should also consider indirect guarantees, such as taking steps to assure commuter volumes for a subway project through zoning and tax measures

16. Clear time-specific deadlines should be set, whenever practical, for government actions that affect finances

Dispute Settlement and Mediation 17. There must be a clearly understood dispute resolution mechanism. Government

should address potential disputes in a flexible and timely manner. If resolution cannot be achieved, there should be a move toward mediation and arbitration. It is essential that a body exists to enforce the rights of investors

18. Mediation and arbitration panels should have the appropriate expertise to avoid

reliance on local courts, where judges often have no understanding of the subject matter

Other Key Concerns 19. Projects, once selected, should be afforded a reasonable degree of regulatory

protection from potentially damaging competition. Ongoing regulation of a completed project should be objective, impartial, and should only interfere with private sector management where a matter of clear and pressing public interest exists that cannot be readily resolved by other means (providing the project is operating within established guidelines)

20. Government should play a major role in land acquisition, for example, underwriting

all or part of land acquisition where such intervention and support are needed to make projects feasible

21. The environmental impact of infrastructure projects must be taken into account.

Environmental standards should not be lowered in order to lower the initial cost of infrastructure projects; this will only increase community resistance and raise long-term costs

22. If government is to attract international investors to infrastructure projects, it must

protect any associated intellectual property rights of foreign investors D. Effective Communication Between Public and Private Sectors It is not enough that the host government have a commitment to promoting private investment in infrastructure - that commitment must be communicated both to the private sector and, no less critically, to the public at large. In addition, there must be opportunities for government to receive feedback. During this session, the participants in the APEC Roundtable made the following observations and recommendations: 1. Government must manage public perceptions by communicating clearly with the

community what the infrastructure project will entail. The private investor should also make its expectations clear to the community. There must be a clearly understood mediation mechanism to address any disputes that arise

2. Communication with the public must be credible and timely. Modern

communication techniques, including the Internet, should be employed. If necessary, professional communicators should be hired (government officials are often not accomplished in persuading the public). Information communicated to the community should be comprehensive but expressed simply, using easily understood graphics. Be consistent, totally open, and do not backtrack. Do not try to avoid responsibility for tough issues; face them directly

3. The mass media, including television, radio, and public meetings, are effective

elements in communication strategies. Communication should begin in the development phase of the project and continue through its implementation

4. Government should create a task force to pursue a coordinated communications

strategy to the community; public officials should be accessible; mass media should be used to explain the benefits of private financing; feedback received from the public should be acknowledged; and useful suggestions from the public to improve the project should be adopted

5. The main emphasis in persuading the public of the need for infrastructure projects

remains jobs and progress. Both government and the private sector must make it clear that privately financed infrastructure projects are part of a clear overall plan that benefits the general public. The benefits to be received must be emphasized to sell the project to the public

6. The benefits of the lower overall cost and accelerated flow of services from fast-track,

privately financed projects should also be emphasized. Newer technology can sometimes be more readily incorporated with privately financed projects. The costs of not carrying out needed projects should be recognized and publicized

SUGGESTED FOCUS FOR FURTHER APEC WORK Along with the elements identified in the APEC Infrastructure Work Plan, Roundtable participants felt the following areas, emerging from the above recommendations, could provide focus for future discussion: A. APEC should provide assistance to its developing members to create public health,

safety, and environmental standards that are consistent with those of the wider APEC membership. This will preclude private investors from having to deal with widely varying requirements

B. APEC should consider establishing a mediation mechanism for resolving disputes

related to infrastructure projects. It should also consider methods to enforce arbitration decisions obtained outside the host economy

C. Realizing that human resource problems still exist in some member economies, APEC

should concentrate on developing the human resource skills of government officials who deal with the private sector on infrastructure projects

D. APEC should consider conducting a public/private sector dialogue to discuss innovative ways to improve the coordination of overall infrastructure development planning within member economies

MELBOURNE CITY LINK

INFRASTRUCTURE FINANCING STRUCTURE

Prepared by

Greg Hosking and Robin Bishop Macquarie Corporate Finance Limited

MELBOURNE CITY LINK INFRASTRUCTURE FINANCING STRUCTURE

The Melbourne City Link Project, jointly undertaken by Transurban City Link Limited and Transurban City Link Unit Trust, is the first major infrastructure development in Victoria, Australia in which retail equity investors were given the opportunity to participate. It is Australia’s largest privately funded transport infrastructure project and, alongside the Hills Motorway in NSW, is Australia’s second listed toll road. The A$1,800 million Project involves the design, construction, financing, operation and maintenance of approximately 22 km of new and upgraded roadway through Melbourne (Australia’s second largest city). This paper outlines the Project’s ownership and investment structure and discusses the various factors that influenced its design. The structure uses a listed unit trust and a listed public company which have jointly issued parcels of “stapled” securities comprising shares in the Company, units in the Trust, and Equity Infrastructure Bonds issued by the Company. The strong level of demand at both the retail and institutional level suggests a widespread acceptance of complex structures by the investment community, provided the complexity has arisen as a result of a tailored structure that delivers identifiable benefits to investors.

BACKGROUND In July 1992 the State Government of Victoria (“the State”) sought expressions of interest to design, build, own, operate and maintain the proposed Melbourne City Link tollway (“the Link”). The Transurban Consortium, sponsored by Transfield Holdings (“Transfield”), Australia’s largest privately owned construction company and the Obayashi Corporation (“Obayashi”), a major Japanese construction company, lodged a submission and was one of two consortia short listed as a result of the expression of interest process. The Project was temporarily suspended and then relaunched on 1 July 1994. On 29 May 1995, after a nine month competitive bid process, the Melbourne City Link Authority, a government authority set up to oversee the tender process, selected the Transurban Consortium as the preferred tenderer. Following a further five months of negotiations, Transurban City Link Limited and Transurban City Link Unit Trust (jointly “Transurban”) executed a Concession Deed and financial close was achieved on 4 March 1996. The Concession Deed grants Transurban the right to construct and operate the Link and to impose tolls for approximately 34 years after completion of construction. At the expiration of this concession period, Transurban’s rights in respect of the Link are surrendered to the State of Victoria for no consideration. Consequently, the Project is an investment with a finite lifespan with no anticipated residual value for investors. As such, distributions received by investors during the concession period comprise both distributions of profit and the return of capital.

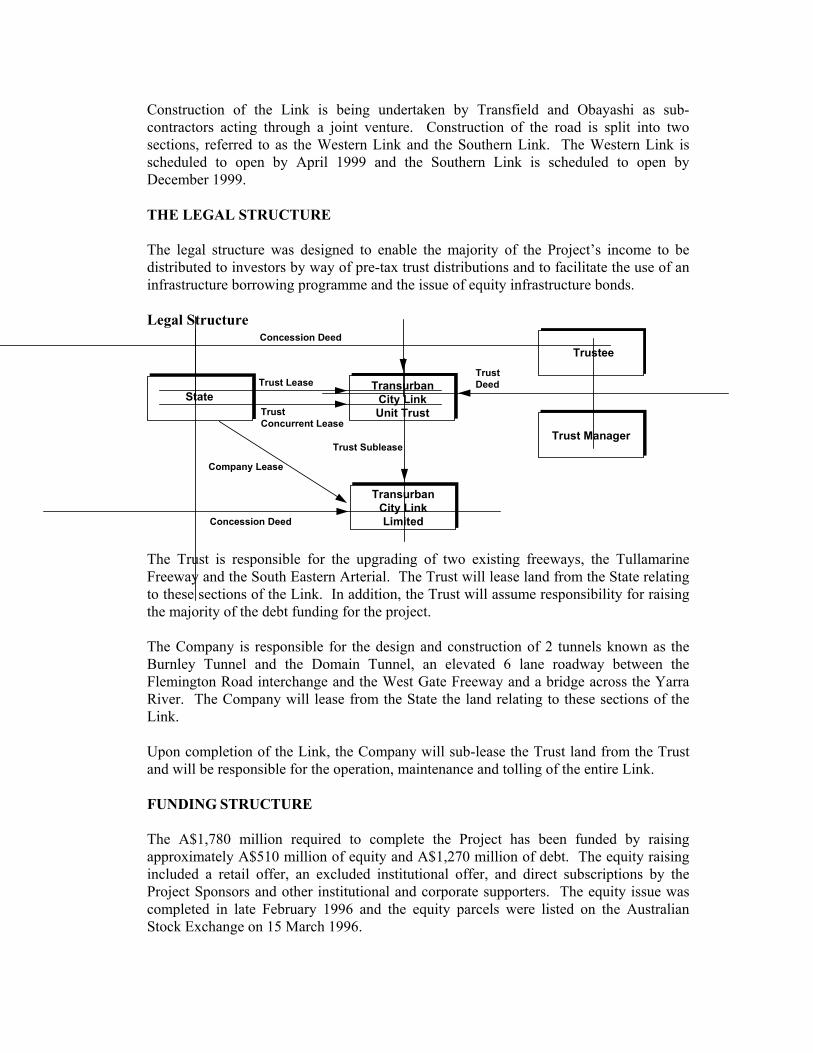

Construction of the Link is being undertaken by Transfield and Obayashi as sub-contractors acting through a joint venture. Construction of the road is split into two sections, referred to as the Western Link and the Southern Link. The Western Link is scheduled to open by April 1999 and the Southern Link is scheduled to open by December 1999. THE LEGAL STRUCTURE The legal structure was designed to enable the majority of the Project’s income to be distributed to investors by way of pre-tax trust distributions and to facilitate the use of an infrastructure borrowing programme and the issue of equity infrastructure bonds. Legal Structure

StateTransurban

City LinkUnit Trust

Trustee

Trust Manager

TransurbanCity LinkLimited

Concession Deed

TrustConcurrent Lease

Concession Deed

Trust Lease

Company Lease

Trust Sublease

TrustDeed

The Trust is responsible for the upgrading of two existing freeways, the Tullamarine Freeway and the South Eastern Arterial. The Trust will lease land from the State relating to these sections of the Link. In addition, the Trust will assume responsibility for raising the majority of the debt funding for the project. The Company is responsible for the design and construction of 2 tunnels known as the Burnley Tunnel and the Domain Tunnel, an elevated 6 lane roadway between the Flemington Road interchange and the West Gate Freeway and a bridge across the Yarra River. The Company will lease from the State the land relating to these sections of the Link. Upon completion of the Link, the Company will sub-lease the Trust land from the Trust and will be responsible for the operation, maintenance and tolling of the entire Link. FUNDING STRUCTURE The A$1,780 million required to complete the Project has been funded by raising approximately A$510 million of equity and A$1,270 million of debt. The equity raising included a retail offer, an excluded institutional offer, and direct subscriptions by the Project Sponsors and other institutional and corporate supporters. The equity issue was completed in late February 1996 and the equity parcels were listed on the Australian Stock Exchange on 15 March 1996.

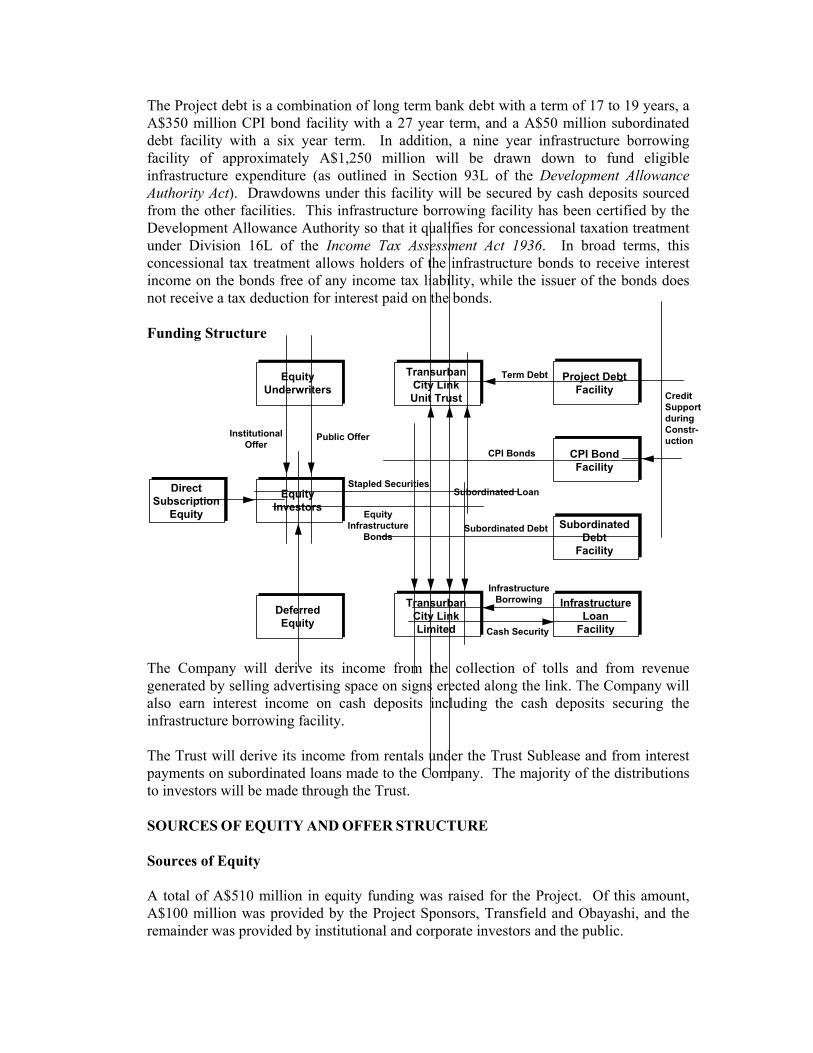

The Project debt is a combination of long term bank debt with a term of 17 to 19 years, a A$350 million CPI bond facility with a 27 year term, and a A$50 million subordinated debt facility with a six year term. In addition, a nine year infrastructure borrowing facility of approximately A$1,250 million will be drawn down to fund eligible infrastructure expenditure (as outlined in Section 93L of the Development Allowance Authority Act). Drawdowns under this facility will be secured by cash deposits sourced from the other facilities. This infrastructure borrowing facility has been certified by the Development Allowance Authority so that it qualifies for concessional taxation treatment under Division 16L of the Income Tax Assessment Act 1936. In broad terms, this concessional tax treatment allows holders of the infrastructure bonds to receive interest income on the bonds free of any income tax liability, while the issuer of the bonds does not receive a tax deduction for interest paid on the bonds. Funding Structure

TransurbanCity LinkUnit Trust Credit

SupportduringConstr-uction

Term DebtEquityUnderwriters

Project DebtFacility

CPI BondFacility

SubordinatedDebt

Facility

InfrastructureLoan

Facility

TransurbanCity LinkLimited

EquityInvestors

DeferredEquity

Subordinated Loan

CPI Bonds

EquityInfrastructure

Bonds

InstitutionalOffer

Public Offer

InfrastructureBorrowing

Cash Security

Stapled Securities

Subordinated Debt

DirectSubscription

Equity

The Company will derive its income from the collection of tolls and from revenue generated by selling advertising space on signs erected along the link. The Company will also earn interest income on cash deposits including the cash deposits securing the infrastructure borrowing facility. The Trust will derive its income from rentals under the Trust Sublease and from interest payments on subordinated loans made to the Company. The majority of the distributions to investors will be made through the Trust. SOURCES OF EQUITY AND OFFER STRUCTURE Sources of Equity A total of A$510 million in equity funding was raised for the Project. Of this amount, A$100 million was provided by the Project Sponsors, Transfield and Obayashi, and the remainder was provided by institutional and corporate investors and the public.

Equity commitments were required from the commencement of the bidding process in January 1995 to provide the State with financial certainty on the deliverability of the Transurban tender. The only viable sources of such long term underwriting commitments were some of Australia’s leading stockbroking firms (with support from their institutional clients) and a number of select institutional and corporate investors. JB Were, Macquarie Underwriting and SBC Warburg agreed to support the Transurban bid and subscription agreements were executed prior to the original bid submission in January 1995. As the tender process progressed, the investors and equity underwriters were required to reconfirm their commitment to the Project several times prior to the actual date for contribution of their funds. Notwithstanding the long period over which underwritten equity commitments had to be maintained, Transurban was committed to a retail issue to ensure a greater spread of investors to enhance liquidity and guarantee compliance with the Listing Rules of the Australian Stock Exchange. A retail issue also provided potential users of the road with the opportunity to invest directly in an asset they will subsequently use. The underwriters accommodated this decision and underwrote the retail Tranche over a period of 14 months setting a precedent for the duration of underwriting commitments in Australian equity markets. Ultimately, A$63.5 million was raised by way of an underwritten Public Issue under a prospectus issued jointly by Transurban City Link Limited and City Link Management Limited (the Trust manager). In hindsight, it is clear that the Public Issue could have been significantly larger, although it must be acknowledged that there is a practical limit to the retail market exposure that underwriters will bear over such an extended period. Due to the strong level of retail demand and the imperative to achieve financial close, the directors of the Company and the Trust Manager were able to close the Public Issue within a week of issuing the prospectus. Structure of Offer The majority of the Project’s equity was contributed at financial close and is referred to as initial equity. The balance of the equity funding was committed prior to financial close but is not scheduled to be contributed until the expected date for completion of construction (December 1999). Initial Equity The initial equity was raised in three separate issues and accounted for A$455 million of the total equity requirement. The three separate issues were:

Public Issue Pursuant to a prospectus, the public was invited to apply for parcels of securities worth A$63.5 million

Institutional Issue Pursuant to a separate offering memorandum, institutional investors were invited to apply for parcels of securities worth A$206.5 million. This was an excluded offer as defined in sub-section 66(2) of the Corporations Law

Direct Subscription Issue Transfield and a select group of institutional and corporate investors executed agreements to subscribe for parcels of securities worth A$185 million

The Public and Institutional issues (comprising A$270 million) were jointly underwritten by the equity underwriters. The remaining initial equity of A$185 million was raised by way of direct placement under the Direct Subscription Issue to investors who had supported the Transurban Consortium throughout the bid process. These investors were separate from the institutions supporting the equity underwriters. Deferred Equity Obayashi and Transroute (a major French toll road operator) executed agreements pursuant to which they will subscribe for A$50 million and A$5 million of equity respectively. This deferred equity was committed prior to financial close but is not scheduled to be paid up until 45 months after financial close (the expected construction completion date). The obligations of Obayashi and Transroute to subscribe deferred equity are supported by irrevocable bank letters of credit. INVESTMENT STRUCTURE Initial Equity The initial equity was subscribed for in the form of A$500 Parcels. During the construction period each Parcel comprises: Quantity Security Issue Price 499 Equity Infrastructure Bonds issued by the Company

at a price of A$1.00 each A$499.00

1 Share in the Company issued at 1 cent A$0.01 1 Unit in the Trust issued at 99 cents A$0.99 Total Issue Price A$500.00

The single share and single unit in each Parcel serve to establish ownership and voting rights in the Company and the Trust. All 501 separate securities are “stapled” together and cannot be traded separately.

Initial equity structure on financial close

TransurbanCity LinkUnit Trust

TransurbanCity LinkLimited

InstitutionalIssue$206.5m

EquityUnderwriters

Institutional andCorporateInvestors

InitialEquity

Investors

PublicIssue

$63.5mUnits$0.9m

Shares$0.001m

Stapled Securities

EquityInfrastructureBonds$454.1m

$185m

During the construction phase, distributions will be paid to investors by way of quarterly interest coupons on the Equity Infrastructure Bonds which will be tax exempt or debatable at 36% at the option of the holder. These coupons are forecast to be A$50.00 per Parcel per annum and while the distribution is not guaranteed, the cost to the Company of paying them has been factored into the financing plan. Forty-five months after financial close, the 499 Equity Infrastructure Bonds within each Parcel are scheduled to be redeemed from an additional A$454 million drawdown under the infrastructure borrowing facility. The redemption proceeds from each Bond will be automatically subscribed (on behalf of investors) for Stapled Securities that comprise one Share in the Company and one Unit in the Trust. The Equity Infrastructure Bonds will be redeemed at a price being the greatest of: • A$1.00 • issue price plus Consumer Price Index (“CPI”) indexation over the term of the issue • average market value of a Parcel for the month prior to the maturity date divided by

500 Any premium payable on redemption will be applied as a premium payable on subscription for units in the Trust. For capital gains tax purposes, investors’ cost base of each new Stapled Security is expected to equal the original issue price of the Equity Infrastructure Bond plus any premium on redemption of the Bond. After redemption of the Equity Infrastructure Bonds and the automatic subscription for Stapled Securities, each Parcel will contain 500 Shares and 500 Units with each Share being stapled to a Unit. At this time, the equity Parcels may be divided into individual Stapled Securities (each comprising one Share and one Unit). However, the stapling between each Share and each Unit cannot be undone.

Once the Link is opened to traffic, returns to investors will be dependent upon its operational performance (principally the volume of traffic using the toll road). Distributions during the operations phase will be primarily by way of pre-tax distributions from the Trust. They are expected to include tax exempt and tax deferred components arising from accumulated losses generated during the construction phase and depreciation allowances available to the Company and the Trust. To the extent that the Company derives taxable income it is proposed to distribute that income to investors by way of franked dividends. Deferred Equity Forty five months after financial close, the deferred equity will be subscribed for in the form of a Stapled Security that comprises one share in the Company fully paid to one cent and one unit in the Trust fully paid to 99 cents. These Stapled Securities will be identical in all respects to the Stapled Securities held by initial investors after the redemption of their Equity Infrastructure Bonds. LISTING AND REPORTING REQUIREMENTS Immediately after the date of issue of the Transurban prospectus, the Company and Trust applied to the Australian Stock Exchange for admission to the official list, and for the 499 Equity Infrastructure Bonds, the one Share and one Unit in each Parcel to be jointly quoted. The application was successful and the Parcels of securities were listed on the Australian Stock Exchange on Friday, 15 March 1996 at around a 20 percent premium to the issue price. While the Company and the Trust are separate legal entities, they have a unique relationship in that they have a common purpose to finance, construct and operate the Melbourne City Link for the term of the concession period, and they have common investors due to the Stapled Security capital structure. In order to simplify reporting requirements and present the aggregated economic entity, the Company and the Trust applied to the ASC for relief from the provisions of the Corporations Law which would have required the two entities to present separate accounts to investors (ss 313(1), 111AT & 1069(3)). This relief was granted allowing the two entities to prepare aggregated financial accounts. These aggregated accounts will be distributed to the Stapled Security holders of Transurban, together with a modified directors’ report, directors’ statement and auditor’s report. The directors’ report and statement will be consistent with the requirements of the Corporations Law applicable to a chief entity but will be signed jointly by the directors of the Company and the management company of the Trust. It is proposed that individual accounts for the two entities will nevertheless be prepared and will be available to investors on request. RATIONALE FOR STRUCTURE The size of the equity raising dictated that the Project would have to access as wide a range of investors as practically possible. As many investors have a strong preference for listed investments and given that many institutional investors are only permitted to invest in listed (or other liquid) investments under the terms of their respective investment guidelines, a listed investment structure of some form was required. Further, many of the potential investing funds preferred to receive returns in the form of pre-tax distributions

(their performance is often judged on their gross pre-tax returns). To satisfy this requirement either a partnership or trust structure was required. A unit trust structure was chosen as it is a structure many investors are familiar with and unlike a partnership, it can be easily listed on an equity exchange. Early returns The payment of a return during the construction period was also desired by many investors. The lack of earnings during the construction period would usually preclude any equity distributions other than by way of capital returns. Therefore, a “debt instrument” paying regular coupons was considered. It was determined that the most efficient form of “debt” available was an infrastructure borrowing programme which would be eligible for the Division 16L tax concessions. This led to the development of the Equity Infrastructure Bond instrument which comprises the majority of the securities of each listed Parcel during the construction period. However, the Division 16L tax concessions only contemplate infrastructure borrowings being made through a company, which would preclude equity distributions being made in a pre-tax form. Therefore, the dual company/trust structure was developed. Another consideration that led to the separate company and trust vehicles was the requirement that the Trust did not fall within the “Trading Trust” provisions of the Income Tax Act (Divisions 6B and 6C). Essentially, if Divisions 6B or 6C were to apply, the Trust would be treated as a company for taxation purposes, thus removing the ability to distribute pre-tax income. To ensure compliance with the Trading Trust provisions, the Trust cannot participate in the operation of the tollway. Accordingly, the Trust’s role in the Project is limited to the design and construction of certain sections of toll road which are leased to the Company and the raising of Project debt. Taxation advantages The utilisation of Equity Infrastructure Bonds as the major form of equity during the construction period delivers two extremely valuable tax advantages to investors. First, the coupons paid on the Equity Infrastructure Bonds are tax exempt (or rebateable at 36% at the discretion of the holder) which makes them very attractive for investors, particularly those on the highest marginal personal income tax rate. Secondly, the disposal of Equity Infrastructure Bonds is a tax exempt event. Therefore if investors sell their Parcels at a premium to their purchase price, no capital gains tax liability is incurred on the profit.

Notwithstanding its relative complexity, the jointly listed company and trust structure was utilised for Transurban because of the many advantages it offered investors over and above a more conventional corporate structure. The high level of demand for Transurban scrip at both the institutional and retail level suggests that investors will accept complex corporate and investment structures if they deliver identifiable benefits.

__________________________________________

* Macquarie Corporate Finance Limited was Financial Adviser to the Public Issue and provided general financial advice on the Project and the structuring of the Company and the Trust. Both Greg Hosking (Associate Director) and Robin Bishop (Executive)

worked extensively on the Project.

PUBLIC/PRIVATE PARTNERING:

THE NORTHUMBERLAND STRAIT CROSSING PROJECT

Prepared by

J. David Pirie, Senior Vice-President Strait Crossing Inc., Calgary

PUBLIC/PRIVATE PARTNERING: THE NORTHUMBERLAND STRAIT CROSSING PROJECT

The Northumberland Strait Crossing Project represents the first major infrastructure project undertaken under the Public-Private Partnering format, which includes a full financial plan and 35-year concession period. The goal of the Developer, Strait Crossing Development Inc., was to achieve a non-recourse financing solution and to obtain an equitable balance of contractual risk with the Government of Canada. In structuring its financing model for this project, the Developer investigated traditional debt and equity options, limited and general partnerships and ultimately a unique form of real rate bond was developed for this project. The issues of security, risk transfer and other key contractual provisions are analyzed, including an overview of the ultimate resolution of each issue. The various project agreements were negotiated and finalized over a ten month period which resulted in financial closing of the project on October 7, 1993. The observations of Strait Crossing Inc. as the Sponsor of the Developer and a participant in other Public-Private Partnering projects together with some of the valuable “Lessons Learned” during this process are highlighted in this paper. PUBLIC PRIVATE PARTNERING - OVERVIEW Infrastructure in North America is deteriorating. It needs extensive repairs, expansion of capacity and additions in order to meet the requirements of the public now and into the 21st century. Our Governments are buried in debt and are spending an ever increasing percentage of Gross National Product to service debt. As this phenomenon continues, Government at all levels is affected by credit rating agencies and the ability to access monies from foreign and domestic Capital Markets. All levels of Government are spending less money on infrastructure repair and new projects and at the same time, are having to provide traditional government services to the taxpayers. Many jurisdictions are experiencing a growing gap between the infrastructure needs and the available funding. The symptoms range from collapsing bridges and ruptured water mains to growing congestion on highways and at airports. These problems, which confront all levels of Government, are occurring at a point in time when there is a mini taxpayer revolt in North America. Taxpayers are insisting that Governments downsize, act more efficiently and deliver government services on a more cost effective basis while at the same time, holding the line on tax increases. These factors have forced all levels of Government in North America to rethink how essential public services are to be supplied. One of the main opportunities for our Government to meet the requirements of the taxpayer is through privatization of projects and services traditionally provided by the Government. The main opportunities which have been created are in the areas of transportation systems, sewage and water treatment plant facilities, power generation facilities and out-sourcing of government services. The European Community has moved more quickly to embrace the concept of privatization, toll roads and general user pay models. In Europe, there is a public acceptance of higher gasoline taxes which has created enormous pools of funds to support

development, maintenance and operation of transportation facilities. In North America on the other hand, the 50¢ a litre price for gasoline is still a reality. A rapid increase of any carbon based tax or excise tax will be resisted in the first instance by the public and secondly by the very powerful lobby groups representing the oil and gas industry. Unfortunately, the United States and Canada also suffer from a love affair with the automobile and this has resulted in a complex road and highway system which is over built and under utilized in many areas and at excess of capacity in other areas. The one area of noticeable improvement in North America is that the public at large appears to be recognizing and accepting the need for direct user fees in lieu of taxes. There also appears to be a growing recognition that public/private partnerships or alliances are necessary to meet the demands and the requirements of the taxpayers. There is a growing tendency in all levels of Government to downsize and streamline the bureaucracy and to introduce to the bureaucracies a new "entrepreneurial" attitude towards the supply of government services. The public sector has begun to realize that there are certain areas in which the private sector can greatly assist in the financing and development of infrastructure projects. The balance of this paper will address the financial and contractual framework of the Northumberland Strait Crossing Project and conclude with some observations and lessons learned by Strait Crossing Inc. NORTHUMBERLAND STRAIT CROSSING PROJECT (NSCP) Background The NSCP is a 13.5 kilometer high level bridge structure linking Cape Tormentine in New Brunswick to Borden in Prince Edward Island. This $840 million bridge will replace an existing ferry service between these two points that, pursuant to Project Agreements, will cease operations upon opening of the bridge facility. The bridge facility and the existing ferry service are required as a result of a constitutional obligation between the Government of Canada and the Province of Prince Edward Island which is contained in the Terms of the Union Agreement executed at the time of Prince Edward Island joining Confederation in 1873. The Government issued a Request for Proposal and Prequalification in 1988 which attracted proposals from 12 international groups. The Government had clear evaluation criteria which reduced this group from 12 to 7. The remaining 7 were invited to submit preliminary designs, construction methods, a regional benefits assessment, a preliminary environmental assessment and a full description of the group's design, construction and project management capabilities. The initial proposals were not priced, though an outline of a financial plan and security package was required. The developers were also required to identify any contract terms and conditions that they would require in order to proceed with this Project. Out of the 7 invited bidders, 6 proposals were submitted. Based on well-documented evaluation criteria, a detailed evaluation process was undertaken with all 6 bidders and requests for clarification were made, followed by written resubmissions and a further round of discussions and clarifications. In September

1988, the Government of Canada announced that 3 consortiums had been selected to submit priced proposals and a full financial plan. The submission of final pricing was delayed in 1988 by a Federal election and the replacement of several key cabinet ministers. An environmental review process was also undertaken during this time period and, after initially overcoming some environmental obstacles, a fully priced submission and details of financial and security packages were submitted in May 1992. At this time, the Strait Crossing Consortium was declared to be the lowest bidder. Between May 1992 and October 1993, which was the Financial Closing, there was an extensive environmental court action which resulted in significant delays. Also during this time period, there was extensive negotiation to finalize the contract terms and conditions. The NSCP represented the first significant BOT Project undertaken by the Government of Canada and it was approached with considerable care and scrutiny by several Government departments (Public Works, Transport, Finance, Environment and Justice). FINANCIAL SOLUTION The Government of Canada, during the Proposal Call process, established two financing mechanisms to assist in obtaining financing for this project. The first assistance was in the form of an annual subsidy payment which would commence on the Date Certain, be indexed 100% to increases in CPI from the Bid Date of May 27, 1992, and would be paid commencing on the Date Certain whether or not the bridge was completed on time. The second financing mechanism was by way of a minimum floor level of toll revenue. The Stage III Proposal Call provided for toll rates to be determined based on the toll rates in force the year prior to the bridge opening. These toll rates, together with the traffic on the ferry service, the year before the bridge opened, would determine a minimum floor level of toll revenue. This minimum floor level of toll revenue was indexed 100% to increases in CPI during the 35-year Concession Period. The terms of the Bridge Operating Agreement allowed the Developer to increase tolls on an annual basis by a factor of 75% of the annual increase in CPI. If this annual increase, together with the current traffic in any year, is not sufficient to equal the minimum floor level of toll, as adjusted for 100% of CPI, the Developer was entitled to increase the toll rates by an amount which would allow the recapture in the following year of the deficiency between the minimum floor level of toll revenue and the actual toll revenue received in that prior year. The Developer, together with its financial advisors, Gordon Capital Corporation and Wood Gundy Inc., its legal advisors, Davies Ward & Beck and its tax and accounting advisors, Peat Marwick Thorne, worked to identify all possible options to be used to finance the Project. These options included: Traditional Use of Subsidy Payment Under this option, the Developer would arrange a construction loan during the period of construction and have this interim financing construction, or bridge financing if you will,

replaced by a take out debt financing on completion of the bridge based on the Government's promise to pay the annual indexed subsidy. This solution was ultimately discarded. The Developer was not prepared to take the risk of a floating rate construction financing during the 4.5 year period of construction and also, this financing would have been on a recourse basis to the members of the construction consortium. Toll Revenue Bonds The Developer reviewed extensively the issuance of toll revenue bonds. The Developer engaged the services of Peat Marwick Stevenson Kellogg to prepare a detailed traffic model and then the Developer prepared a forecast of net operating toll revenues internally based on this model and assumed toll rates. The Developer took the additional step of having this forecast of net operating toll revenues verified by Peat Marwick Thorne. The insurance markets of Canada were approached to market non-recourse toll revenue bonds. There was substantial appetite for the toll revenue bonds. This solution was also ultimately discarded due to the requirement to pay interest during the construction period. A substantial portion of the toll revenue bonds would be on a recourse basis to the construction consortium and the discount factor associated with the completion risk was too high. Tax Enhanced Equity The Developer and its financial advisors reviewed and prepared term sheets on tax enhanced partnership units, both general and limited. Tax ruling requests were submitted to Revenue Canada and advance tax rulings were ultimately given. In early 1992, the Government indicated that it was not prepared to see tax enhanced partnership units issued that would create tax write-offs in excess of the partners "at risk amount". The Developer and its financial and legal advisors, disagreed with this interpretation, however, the Developer proceeded to re-examine and restructure its Financial Proposal in order to achieve the closing of the Project. Traditional Equity Units The Developer and its financial advisors prepared a draft Offering Memorandum for purposes of issuing traditional equity units in the developer entity. This Project was the first significant BOT project undertaken in Canada and this factor, together with environmental challenges which were ongoing and the discount factor of the completion risk, would not allow the creation of a sufficient size of equity offering to justify the dilution that would occur to the construction consortium's ownership position. Final Solution - Real Rate Bonds The Developer came to recognize during this process, that the only way to achieve the final solution was to leave the completion risk with the construction consortium, rather than attempting to sell either debt or equity interests which were based in the first instance, on completing the bridge and in the second instance, on accepting the traffic forecasts and net operating revenues during the 35-year Concession Period. These factors

are "non-traditional risks" for the debt and equity markets and resulted in a substantial discount to proceeds which would otherwise have been anticipated. To solve these problems, the Developer developed a real rate bond product which in many ways was similar to the Government of Canada's real rate bond instruments. This real rate bond instrument discounted the future value of the 35-year stream of annual indexed payments to be made by the Federal Government. The structure of the bond was to pay a yield equal to 4.5% plus the annual increase in inflation. This instrument was largely purchased by the Pension Funds of Canada who found the indexed nature of the yield to be a near perfect match to the indexed liabilities which they have to their Pension Plan participants. The Developer deposited the bond proceeds of $661 million with Montreal Trust Company, the Project Trustee. As part of the Financial Closing Documents, SCI negotiated with the Government a reinvestment strategy which permitted the Developer to direct the Project Trustee to invest the $661 million in accordance with this reinvestment program strategy. The Developer hired CIBC/Wood Gundy to assist in this reinvestment program. The Developer, by detailing its anticipated drawdown schedules, was able to provide to CIBC/Wood Gundy a drawdown schedule which allowed the purchase of a series of investments with maturity dates to match this drawdown schedule. This reinvestment program, together with the construction consortium's commitment of 10% funding by way of a Letter of Credit, provided financing for a total anticipated Project cost of $840 million. It was a condition of the Stage III Proposal Call that all of the construction costs, in this case $840 million, be deposited with the Project Trustee or otherwise in the control of the Project Trustee as of the date of Financial Closing. In order to maximize the proceeds from the real rate bond offering, the Developer, with the cooperation and support of Government officials in New Brunswick, established SCFI. SCFI as a Provincial crown corporation, was the ultimate issuer of the real rate bonds (the "Bonds"). This step was taken in order to ensure that there was no construction, project or operating risk that could at any time in the future, disrupt the flow of annual subsidy payments from the Government of Canada through SCFI to the ultimate holders of the Bonds. This step, together with the sovereign credit rating of the Government of Canada, allowed the SCFI Bonds to be rated AAA by both Standard & Poors and Moodys. This allowed the Bonds to be issued at a rate of approximately 15 to 20 basis points behind the Government of Canada's own real rate bond program. This was an extremely efficient and well priced financing instrument and ultimately enabled this project to proceed. CONTRACTUAL ISSUES In structuring this transaction, the Developer's key goal was to create non-recourse debt for this project. This was achieved through the issuance of the Real Rate Bonds described above. The organizational structure for the Developer and the project are described in Table 1 following this Section. In order to achieve this goal, it was necessary for the Government of Canada to agree to make the first payment to bond holders on May 31, 1997, the estimated Date of Completion of the bridge, whether the bridge was completed or not. This put a unique

pressure on the "completion risk" associated with this project. If the Developer was late, the Government of Canada would find itself in the position of making the first annual indexed subsidy payment and continuing to operate the ferry service. This was not a risk that was acceptable to the Government of Canada and in the negotiation process, the Developer was required to reimburse the Government for operating costs associated with the ferry service in the event completion of the bridge was delayed beyond May 31, 1997. A very extensive security package comprised of parent company guarantees, a $200 million Performance Bond and a $20 million Labour and Material Payment Bond were supplied to secure the Government against the completion risk. In addition to the "completion risk", the Government was very concerned about the "cost overrun risk". The Government required a separate Letter of Credit for $73 million to be set aside as extra protection against cost overruns. The Government also hired financial advisors, Rothschild of Canada and Doane Raymond, to undertake an extensive review of the financial model. In addition to Public Works Canada's own engineers, the Government had an independent engineer, Buckland & Taylor of Vancouver, extensively review the design, construction methods, construction price and schedule of the Developer and write a detailed report approving this program prior to financial closing. The Developer had focused its main return on the concession period with the up-front real rate bond financing and interest during construction covering the design and construction costs. In order to maintain a positive return, the Developer had to approach the balance of the contract negotiations to ensure that no contractual terms during the 35 year concession would negatively affect the Developer's ability to place toll revenue bonds on the project. The Developer's financial advisors were provided with summaries of negotiating positions and contract terms to make sure that toll revenue bond holders were not exposed to risk and credit uncertainties. There were extensive negotiations to deal with normal contractual terms and conditions such as:

Applicable Laws Subsurface and Geotechnical Risks

Taxation Issues Force Majeure

Workers' Compensation Insurance Program

Strikes and Lockouts Design Approval

Acceptance of Construction

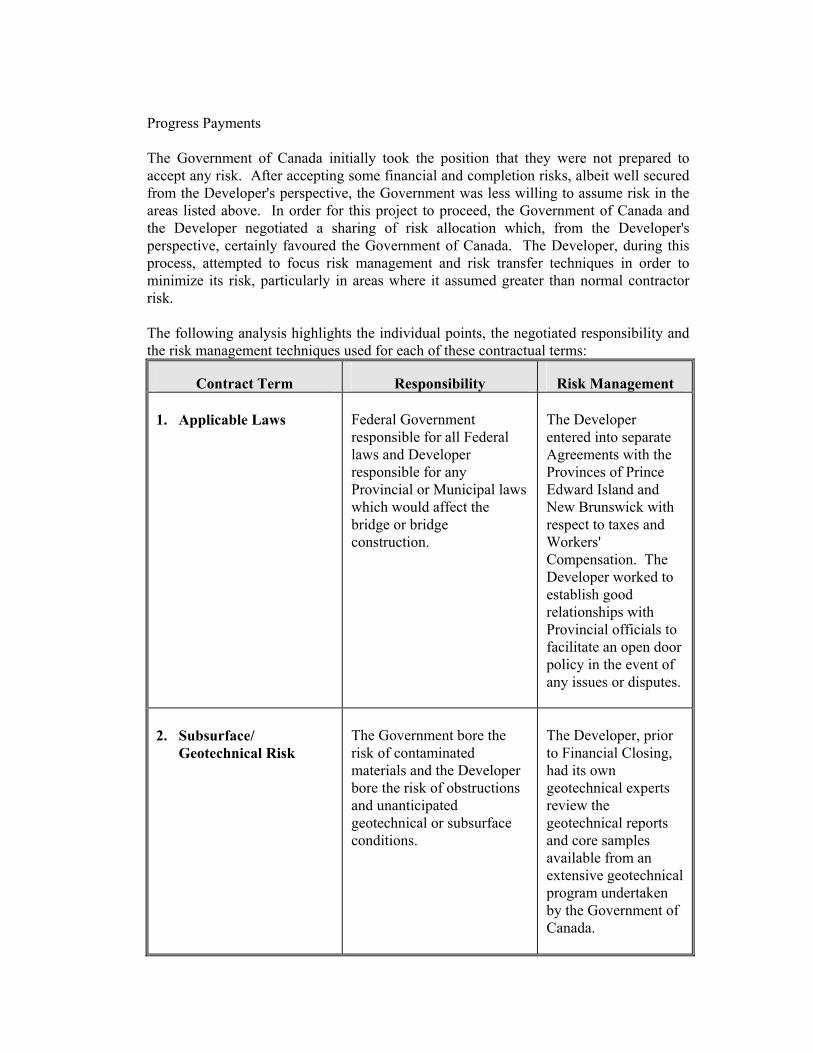

Progress Payments The Government of Canada initially took the position that they were not prepared to accept any risk. After accepting some financial and completion risks, albeit well secured from the Developer's perspective, the Government was less willing to assume risk in the areas listed above. In order for this project to proceed, the Government of Canada and the Developer negotiated a sharing of risk allocation which, from the Developer's perspective, certainly favoured the Government of Canada. The Developer, during this process, attempted to focus risk management and risk transfer techniques in order to minimize its risk, particularly in areas where it assumed greater than normal contractor risk. The following analysis highlights the individual points, the negotiated responsibility and the risk management techniques used for each of these contractual terms:

Contract Term

Responsibility

Risk Management

1. Applicable Laws

Federal Government responsible for all Federal laws and Developer responsible for any Provincial or Municipal laws which would affect the bridge or bridge construction.

The Developer entered into separate Agreements with the Provinces of Prince Edward Island and New Brunswick with respect to taxes and Workers' Compensation. The Developer worked to establish good relationships with Provincial officials to facilitate an open door policy in the event of any issues or disputes.

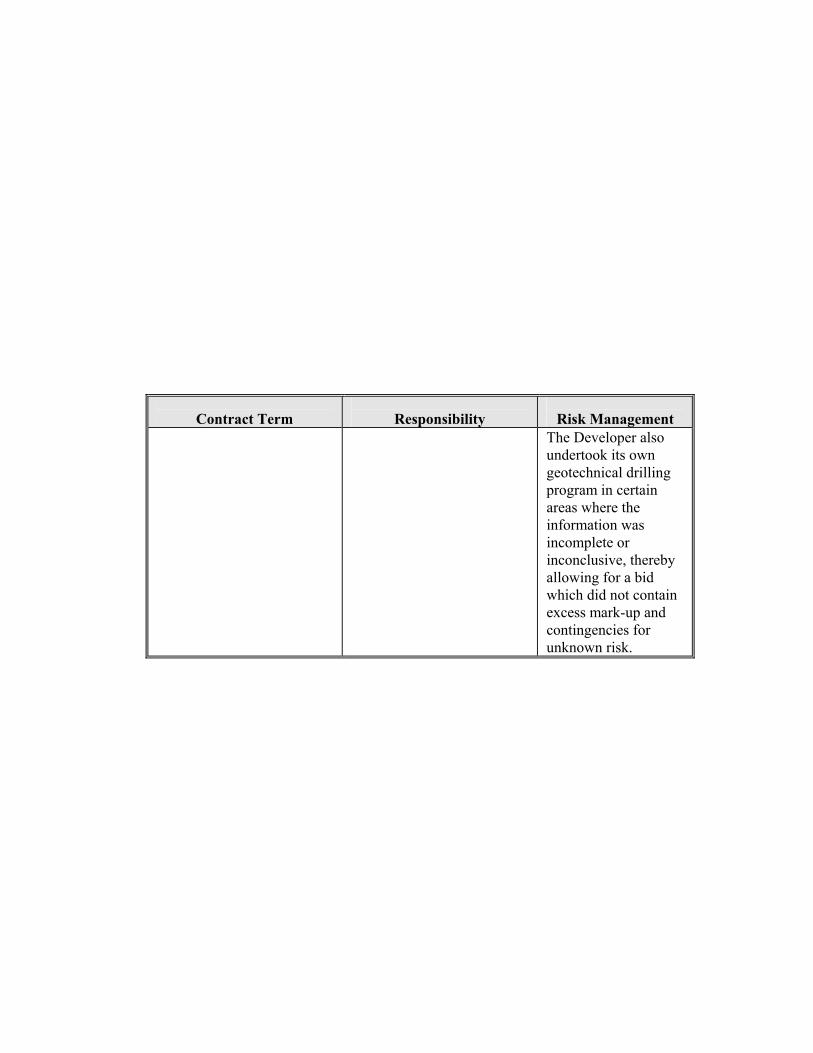

2. Subsurface/ Geotechnical Risk

The Government bore the risk of contaminated materials and the Developer bore the risk of obstructions and unanticipated geotechnical or subsurface conditions.

The Developer, prior to Financial Closing, had its own geotechnical experts review the geotechnical reports and core samples available from an extensive geotechnical program undertaken by the Government of Canada.

Contract Term

Responsibility

Risk Management

The Developer also undertook its own geotechnical drilling program in certain areas where the information was incomplete or inconclusive, thereby allowing for a bid which did not contain excess mark-up and contingencies for unknown risk.

Contract Term

Responsibility

Risk Management 3. Taxation Issues The Developer was

responsible for satisfying itself as to all applicable taxation issues prior to financial closing.

The Developer applied for and obtained detailed GST and Income Tax Rulings which permitted the Real Rate Bonds to be issued. These rulings also assured the Developer of specific tax treatment that better matched the cash flow profile of the 35 year Concession Period.

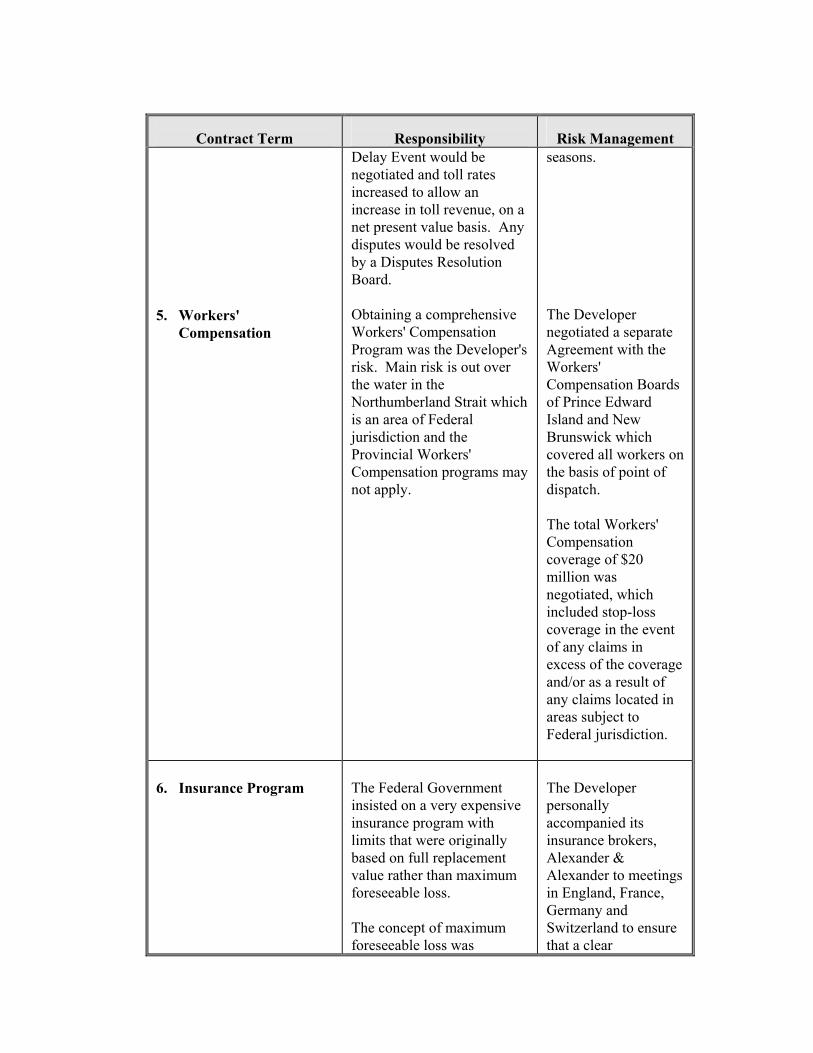

4. Force Majeure Clause

The normal force majeure clause was replaced with a concept of Project Risk Event which would only allow compensable delay under acts of Government, acts of war and the most extreme weather conditions. All the risks within the "normal" force majeure clauses were assumed by the Developer. The Developer also negotiated a concept of "Project Delay Event" which allowed for an adjustment to toll rates during the concession period as a result of events beyond the Developer's reasonable control. The quantum of compensation for a Project

The Developer undertook an extensive review of construction methods and windows of weather during the marine seasons. Construction methods were focused on land based production of precast elements and obtaining the best possible marine erection equipment. The Svanen marine erection rig used on the Storbaelt Project was purchased to ensure that the marine erection process could be completed in the available marine

Contract Term

Responsibility

Risk Management 5. Workers' Compensation

Delay Event would be negotiated and toll rates increased to allow an increase in toll revenue, on a net present value basis. Any disputes would be resolved by a Disputes Resolution Board. Obtaining a comprehensive Workers' Compensation Program was the Developer's risk. Main risk is out over the water in the Northumberland Strait which is an area of Federal jurisdiction and the Provincial Workers' Compensation programs may not apply.

seasons. The Developer negotiated a separate Agreement with the Workers' Compensation Boards of Prince Edward Island and New Brunswick which covered all workers on the basis of point of dispatch. The total Workers' Compensation coverage of $20 million was negotiated, which included stop-loss coverage in the event of any claims in excess of the coverage and/or as a result of any claims located in areas subject to Federal jurisdiction.

6. Insurance Program

The Federal Government insisted on a very expensive insurance program with limits that were originally based on full replacement value rather than maximum foreseeable loss. The concept of maximum foreseeable loss was

The Developer personally accompanied its insurance brokers, Alexander & Alexander to meetings in England, France, Germany and Switzerland to ensure that a clear

Contract Term

Responsibility

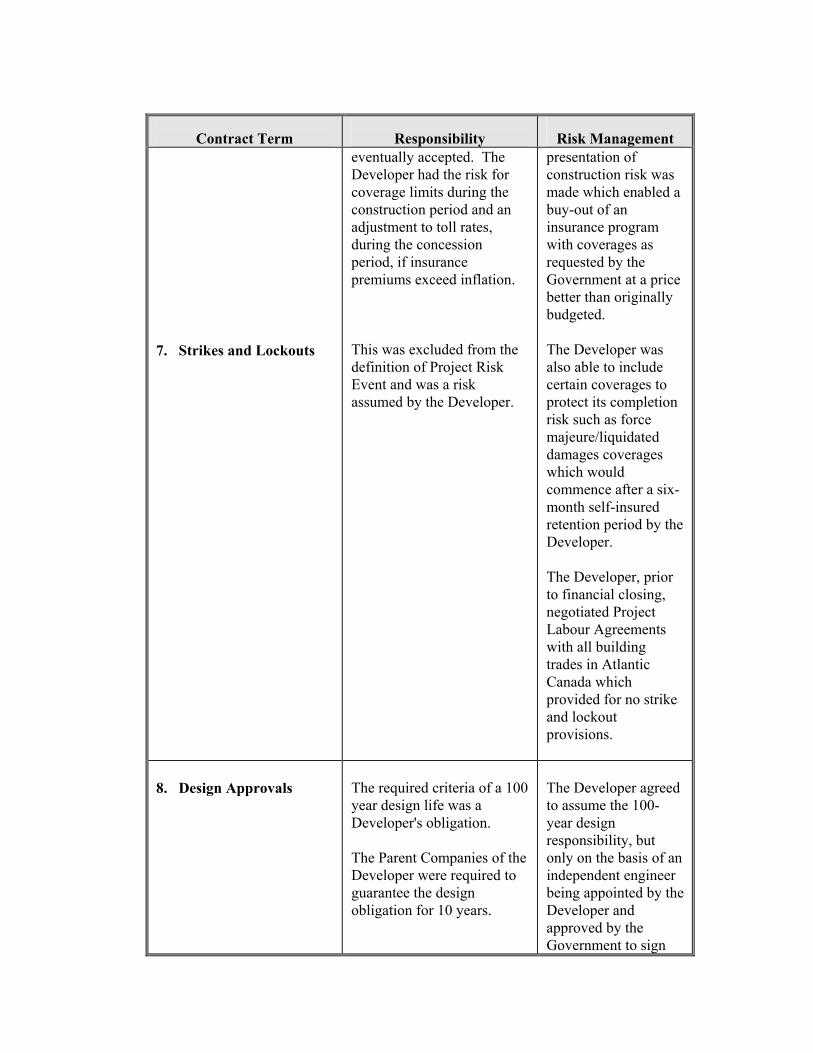

Risk Management 7. Strikes and Lockouts

eventually accepted. The Developer had the risk for coverage limits during the construction period and an adjustment to toll rates, during the concession period, if insurance premiums exceed inflation. This was excluded from the definition of Project Risk Event and was a risk assumed by the Developer.

presentation of construction risk was made which enabled a buy-out of an insurance program with coverages as requested by the Government at a price better than originally budgeted. The Developer was also able to include certain coverages to protect its completion risk such as force majeure/liquidated damages coverages which would commence after a six- month self-insured retention period by the Developer. The Developer, prior to financial closing, negotiated Project Labour Agreements with all building trades in Atlantic Canada which provided for no strike and lockout provisions.

8. Design Approvals

The required criteria of a 100 year design life was a Developer's obligation. The Parent Companies of the Developer were required to guarantee the design obligation for 10 years.

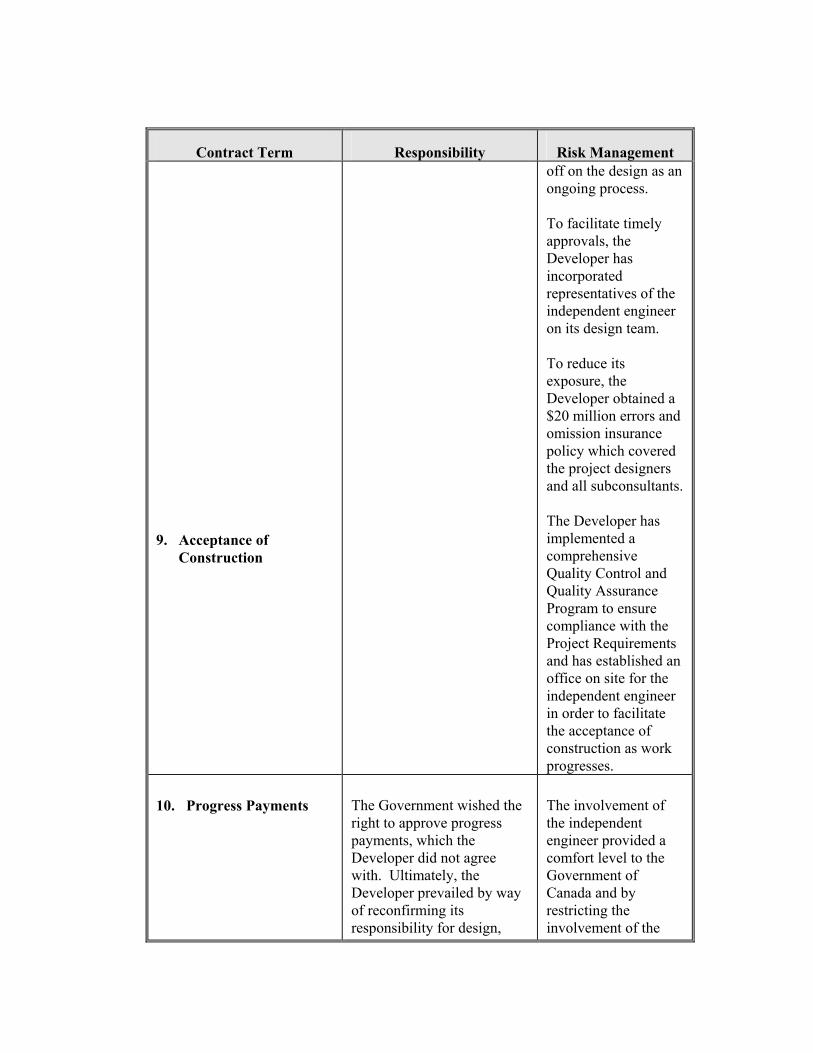

The Developer agreed to assume the 100-year design responsibility, but only on the basis of an independent engineer being appointed by the Developer and approved by the Government to sign

Contract Term

Responsibility

Risk Management 9. Acceptance of Construction

off on the design as an ongoing process. To facilitate timely approvals, the Developer has incorporated representatives of the independent engineer on its design team. To reduce its exposure, the Developer obtained a $20 million errors and omission insurance policy which covered the project designers and all subconsultants. The Developer has implemented a comprehensive Quality Control and Quality Assurance Program to ensure compliance with the Project Requirements and has established an office on site for the independent engineer in order to facilitate the acceptance of construction as work progresses.

10. Progress Payments

The Government wished the right to approve progress payments, which the Developer did not agree with. Ultimately, the Developer prevailed by way of reconfirming its responsibility for design,

The involvement of the independent engineer provided a comfort level to the Government of Canada and by restricting the involvement of the

Contract Term

Responsibility

Risk Management construction and completion

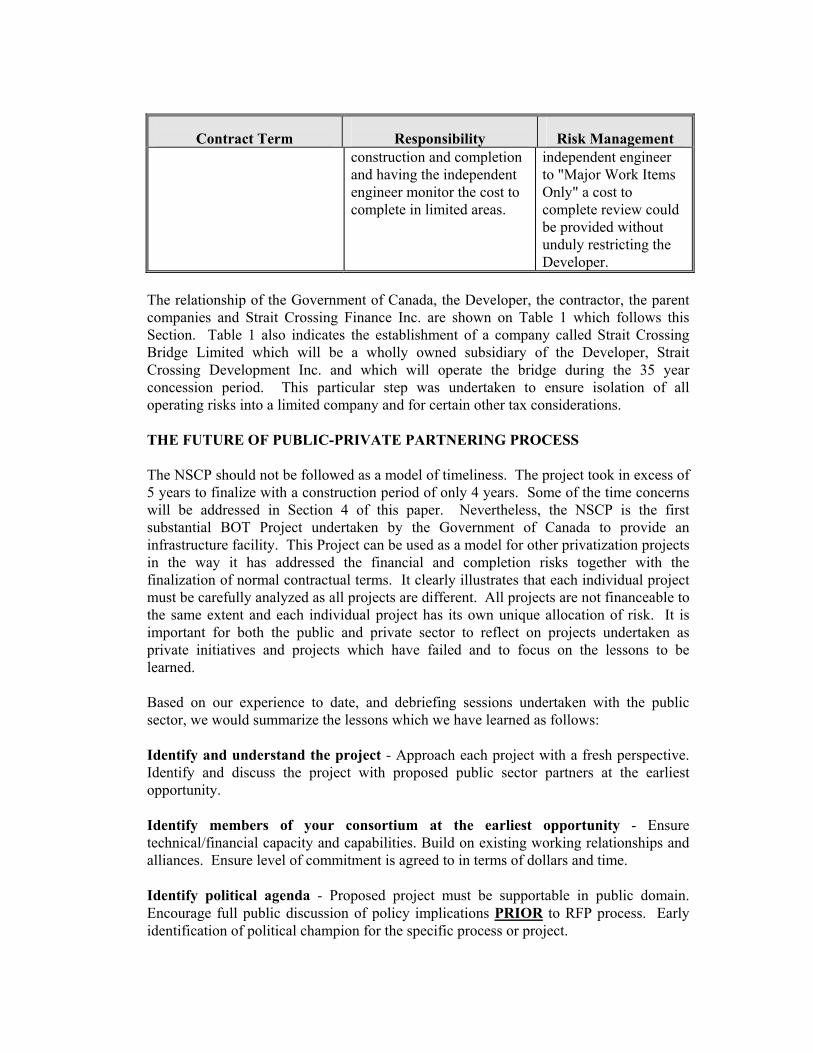

and having the independent engineer monitor the cost to complete in limited areas.

independent engineer to "Major Work Items Only" a cost to complete review could be provided without unduly restricting the Developer.

The relationship of the Government of Canada, the Developer, the contractor, the parent companies and Strait Crossing Finance Inc. are shown on Table 1 which follows this Section. Table 1 also indicates the establishment of a company called Strait Crossing Bridge Limited which will be a wholly owned subsidiary of the Developer, Strait Crossing Development Inc. and which will operate the bridge during the 35 year concession period. This particular step was undertaken to ensure isolation of all operating risks into a limited company and for certain other tax considerations. THE FUTURE OF PUBLIC-PRIVATE PARTNERING PROCESS The NSCP should not be followed as a model of timeliness. The project took in excess of 5 years to finalize with a construction period of only 4 years. Some of the time concerns will be addressed in Section 4 of this paper. Nevertheless, the NSCP is the first substantial BOT Project undertaken by the Government of Canada to provide an infrastructure facility. This Project can be used as a model for other privatization projects in the way it has addressed the financial and completion risks together with the finalization of normal contractual terms. It clearly illustrates that each individual project must be carefully analyzed as all projects are different. All projects are not financeable to the same extent and each individual project has its own unique allocation of risk. It is important for both the public and private sector to reflect on projects undertaken as private initiatives and projects which have failed and to focus on the lessons to be learned. Based on our experience to date, and debriefing sessions undertaken with the public sector, we would summarize the lessons which we have learned as follows: Identify and understand the project - Approach each project with a fresh perspective. Identify and discuss the project with proposed public sector partners at the earliest opportunity. Identify members of your consortium at the earliest opportunity - Ensure technical/financial capacity and capabilities. Build on existing working relationships and alliances. Ensure level of commitment is agreed to in terms of dollars and time. Identify political agenda - Proposed project must be supportable in public domain. Encourage full public discussion of policy implications PRIOR to RFP process. Early identification of political champion for the specific process or project.

Identify all affected interest groups (pro and against) - The need to identify at the earliest possible stage, a particular interest group or issue which may affect the project. If only anti-voices exist, you may need to create or sponsor a pro-business group to support the project. The Press should be treated as a special interest group and jointly formulate, with the public sector, a Communication Plan at the early stages of the project. Early finalization of legislative/regulatory requirements - This must occur at the front end of the project in order to provide a comfort level for all participants and to establish contractual framework for the project. This issue is particularly important to financial lenders and given the cost of pursuing financial proposals in the capital markets of the world, there can be no room for doubt or uncertainty in this area. Early finalization of time lines for the project - The Proposal Call or RFP process must clearly identify the time lines associated for the project and address issues of compensation to the Developer where either a project is canceled or time lines are extended. In order to ensure the best quality of submissions, public sector is slowly moving towards compensation to bidders where the RFP process is complex or anticipated to be greater than 6 months. There must be an assumption of responsibility by the public sector where there is an extensive slippage in time line due to litigation, regulatory approval or environmental challenge. Appropriate RFPs will foster appropriate responses - State clear and honest objectives in the RFP. State explicitly the evaluation criteria and avoid any perception of bias. Statements of goals are preferable over a detailed requirement. Do not tighten the definition of the project to the point of forestalling innovations and potential cost efficiencies. Define an appropriate procedure for addressing unsolicited proposals. Shorten bidder list at first opportunity - It is in the best interest of both the public and private sector to reduce the participants in an RFP process as soon as possible. In complex infrastructure proposals, there should not be more than 2 or 3 final bidders in order to ensure that you obtain the best effort and best price of the participants involved in the project. Until the rules and procedures change, the privatization process is too expensive for the private sector to participate from start to finish in all RFP opportunities. Early nomination of an "empowered" negotiating committee - It is imperative that the public sector establish a negotiating committee and empower specific individuals to make decisions. These decision makers should be known to the private sector participants. There should be no hidden agenda and there should be no "empty chair" negotiations. All affected agencies within the Government must either be part of the negotiating committee or have delegated their authority to other members of the negotiating committee. This can best be achieved through the legislative or regulatory framework. Once established, the negotiating committee should not change until finalization of all Project Agreements. Maintain flexibility in your financial plan - Circumstances change, time lines change and financial markets change. The Developer must always have some flexibility in its financial plan to deal with the unexpected. The financial plan must provide an adequate rate of return to the Developer and its lenders to reflect assumption of risk.