Embed Size (px)

Citation preview

artmental Costkeepin g

S Busin esses .

&ULIU S LUNT&.

A .C .A.

Price

LONDON &

0 (PUBLI SH ERS ) LTD . , 3 4 MOOR&ATE STREET, E ‘C

c—lfl

B Y H . &ULIU S LUNT ,A .C .A .

THE necessity for correct records of manufacturi n g processes wi ll be felt in the futureto a much more intense degree than everin the past

,and the importance of reliable data ,

easily and correctly compiled , al ways up to datea n d readily avai lable , wi l l be found of immenseservi ce in businesses of every kind .

I t is inevitable that minor modifications wi l lbe requi red in any cut & an d & dried plan to suit thepeculiariti es of any particular business

,but when

the general lines are understood,the necessary

guidance to success is obtained .

In the plan now submitted an attempt has beenmade to show how the work can be arran ged toproduce useful results with as little complicationas po ssible , and at the same time the figures areavailable week by week

,and results can be watched

continually and can be checked with the periodicalstocktaking ,

and when special reli ance is to beplaced upon them .

Costing records are in some cases desired forpermanent historical survey of results

,in other

cases for provi di ng a basis for future work ,but in

this case the scheme provides a running outlineof present work from which deductions can beat once made

,and on which necessary action can

be immediately taken .

The most elaborate system is of little use whenits results are only obtained after the mischief is

done . A system which shows the tendencies of

the business , the way the current is flowing ,will

give a far greater return in usefulness for the t imespent on its working out .

The system here outlined is excellently adaptedfor bus in esses ‘

when the goods manufactured arebeing readily disposed of as they are made

,with

out any necessity for accumulating stock for seasontrade , and without the delay which is inevitablein many businesses before the work done assumesthe finished state .

0 o 0

To meet these cases,however

,spec i al provi s i on

i s made .

Part l .

& The Weekly Cost Sheet .

Part I I .

& The Cost Sheet Summaries .

Part I I I .

& The Cost Ledger .

PART I .

—THE WEE&LY Cosr SHEET .

The Departmen ts .

I t i s first of all necessary to decide upon theclassifications into which the business is to bedivided for the purpose of grouping the departments— either according to (a) the class ofarticles turned out , (6) the kind of material used ,

(0) the nature of the operat ions , and so on .

Each of these departments will then be lookedupon in the Cost Accounts as a separate busm ess

,

trading with the other departments and maintaining a clear division of m aterial and labour .

The purchases records will require to allocatematerials purchased to one or other of thesedepartmental accounts accordingly .

Where materials are bought for several departments they will require to be charged up to thedepartment chiefly concerned

,and the other

departments will draw supplies from that one .

The Purchases Invoice Book will require to beanalysed accordingly .

The sales must be classified also according tothe department concerned , and the Sales Day Book(and Returns Inwards Book) will require similaranalysis columns to record the output .

Form 2 . SALES DAY B OO& .

Name No F To tal Dep t . A Dep t . B . Dep t . C .

The clerks responsible for these analysesmust be supplied by the cost clerk with exactlists of items allocated to each department . A

weekly summary of the sales in the followingform should be regularly prepared .

Form 3 . SALES SUMMARY .

W ee k end ing

To tal Same Total

fi&& Av erage week las t & tol ils

a

t

te Av erage&uarter

YearYear

ep .

Dept . B .

Dep t . C .

Increase or decrease

Between these two records , &i&. purchases andsales , which are fairly readily obtainable , liethe following classes of transactions , each of whichmust be dealt with in its appropriate manner 2

(I ) Supplies of material from stock& room tothe various departments .

(2) Transfer of material from on e departmentto another .

(3) Wages paid in different departments .

(4) Packing labels and containers , &c alsoassignable to a particular department .

(5) &eneral expenses applying to the businessas a whole .

Raw Mater i a l .

Raw material in bulk is always to be kept i nstore & rooms under the charge of a storekeeper whois responsible for i ts correct use and for furnishingcorrect records of its use

,each department

having the materials assigned to it , as they arecharged up to it in the Invoice Book . I t may besufficient to warehouse such materi als under on e

stock& keeper,or circumstances may make it more

convenient to have ent irely separate stock& roomsfor each department , in close touch with thatdepartment .

The Supp ly Tickets .

Form 4 . SU PPLY R E&U ISITION TI C &ETfor Raw Materi a l , &c. ,

from Sto res in Stock & r oom .

To Stock & k eepe r ,Pl e a s e Supp l y

S igned

A supply requisition must be handed in to

the storekeeper for al l supplies obtained fromhim : to be init ialled by head of departmentdrawing supplies , and counter& initialled by personactually receiving from the stock& keeper . Theserecords form the bases of a weekly summary ofthe material used in each department . Theyare also to be entered up into the Stock Book, to

the credit of the stock of material in question .

(See Form

6

In case of goods purchased particularly foron e department and taken into use in thatd epartment where immed iate delivery is obtained ,

it is important to observe that the correct requisit ion i n g by means of a supply t icket i s carried out .

Tran sfers .

Form 5 . MATERIALS TRANS FER T IC &ETfor Mate r ia l , &c.

,f rom on e Dep a rtment t o anothe r .

From Depar tm ent

Besides the supplies of the chief stocks from thes tock & keeper there will usually be transfers ofm aterial from one department to another

,either

because they are in a prepared state or becausethat department holds the main stock , or for someS imilar reason

,and transfer t ickets must be filled

up and handed in to the department deliveringthe goods . These should be of a different colourfrom the supply requisit ions to facilitate class ificat ion .

They may be numbered and taken from duplicate books with advantage . They should be fil ledin with full detai l .

The cost clerk should collect these requisit ionsand transfer t ickets dai ly

,and classify them ready

for summarising at the end of the week .

The transfers require recording in an analysisbook called the Materials Transfer Book .

A separate sect ion is devoted to each department for goods recei ved into that department

,

with columns showing the department to be creditedin respect of each item .

From these records a separate Cost Sheet foreach department can be prepared .

Form 7 . C OS T SH EET B OO& .

Dep artm ent AW eek end ing .

&uan t ity &alueDetails of Supp l ies

Total Suppl ies

Transfers from Departments

Transfers to Departments

Net Consumpt ion

Amoun t Forward

Total

ContainersAmount Forward

Total

WagesAmount Forward

Total

Product ionAmount Forward

Total

8

C omp i lati oni

of the C ost Sheet.

(a) Summarise material received from stockkeeper .

(6) Add total of materials transferred into thedepartment .

(0) Subtract total of transfer book creditsmaterials sent out to other departments .

The weight or quantity should be totalled aswell as the value , and the totals should be carriedforward from week to week .

Wages .

The Wages Analysis Book must provide aclassificat ion of wages paid in different departments

,showing separately wages of staff— not

belonging to any one section,such as engineers

(in a factory) , general supervision ,stock & keeper

,

&c.

The wages should be recorded on the Cost Sheetand totalled from week to week for comparisonpurposes .

Form 8 . WA&ES ANALY SIS .

Dept . A Dep t . B Dept . C

s d s d s ( 1

Output .

Records of product ion should be compiled fromdelivery tickets handed in along with all finishedgoods

,init ialled or countersigned by department

managers delivering and receiving respectively,

or their deput ies .

Form 9 .

DELI&ERY TI C &ET (FINISH ED STOC &) .

Form 10. PRODUC TION SH EET .

W eek end in g

De ta ils &uant i ty

Mon . Tues . W ed . Thurs . Fri . Sat . Total &al ue

These records must be summari sed da i ly asthe work proceeds an d totalled at each week& end

,

the quantiti es either by count , weight , or measurement in each sect ion be ing extracted .

This total being recorded on each appropriateCost Sheet

,and totalled from week to

‘

week,gives

a most valuable guide to the working , v i&.

Average cost of material per per cwt .,

per yard, &c. , produced .

Average cost of wages per per cwt . ,per

yard,

produced .

I O

From these records a summary of outputshould be made in alphabet ical form— preferablyin a loose & leaf book— so that production of anyarticle from week to week . can be traced .

I t i s naturally of considerable importance tohave a correct grouping of work

,so that sim i lar

articles are together in the departments,and

dissim i lar articles s eparated .

Form 1 1 . PRODU C TION REC ORD .

oArt icl e

W eek ending &uan t i ty

Wrappi n gs— Pack i n g Label s , C on tai n ers , (30.

The readiest way of compiling this cost is asfollows :

The cost of wrappings for each article must beascertained

,and a price record kept Of same .

From the totals shown on the Production Sheet

(Form 1 0) the cost of Containers ,&c. , to correspondcan be readily calculated .

Alternatively,the requisitions for wrappings

supplied from stock must be charged up simi larlyto the goods .

I I

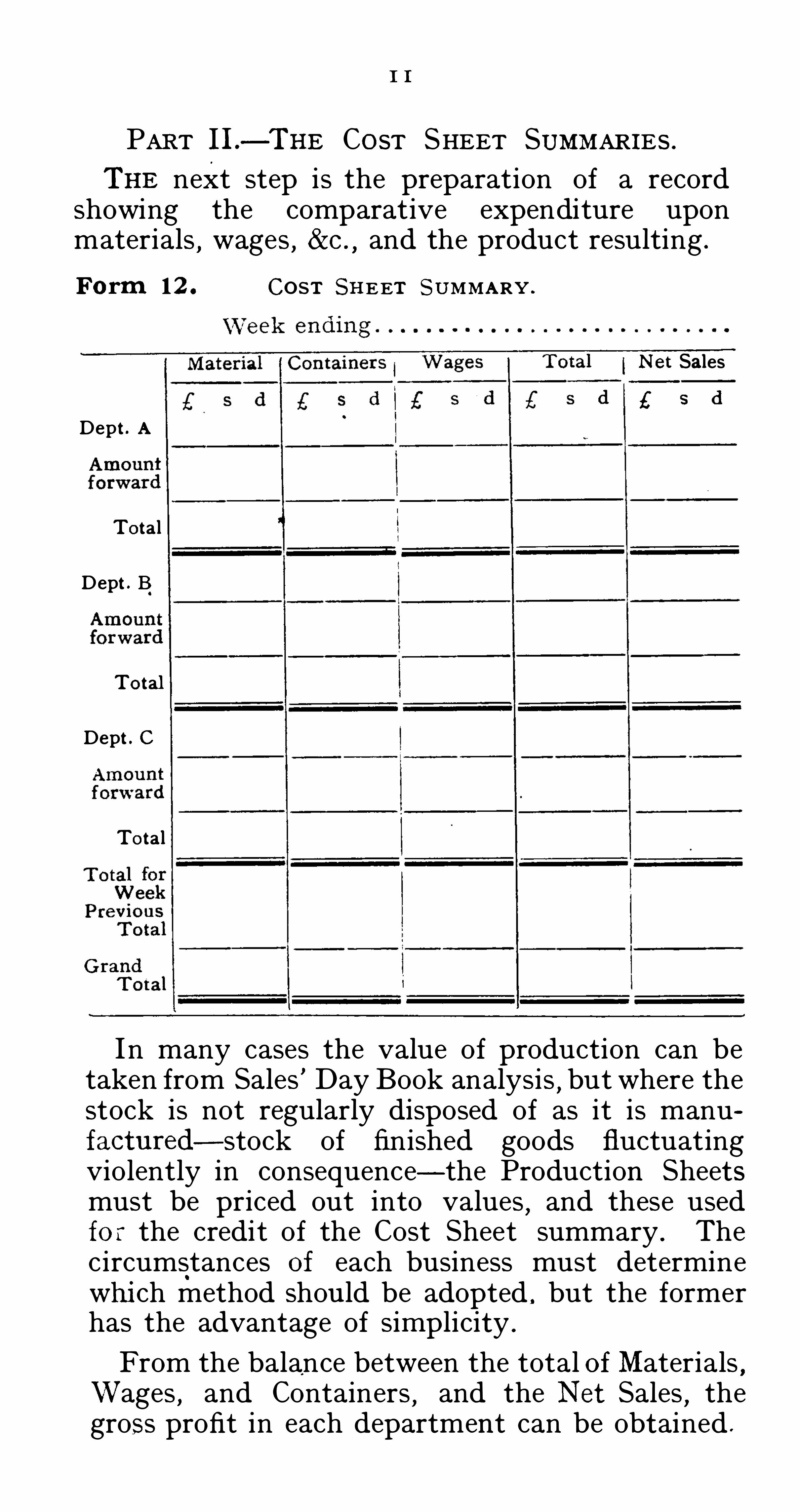

PART I I .

— THE COST SHEET SUMMARIES .

THE next step is the preparation of a recordshowing the comparative expenditure uponmaterials

,wages

,&c.

,and the product resulting .

Form 1 2 . C OST SH EET SUMMARY .

Net Sales

Dep t . A

Total

Dept . B

To tal

Dept . C

Total

In many cases the value of production can betaken from Sales

&

Day Book analysis,but where the

stock is not regularly disposed of as it is manufactured— stock of finished goods fluctuatingviolently in consequence— the Production Sheetsmust be priced out into values

,and these used

fo r the credit of the Cost Sheet summary . Thecircumstances Of each business must determinewhi ch method should be adopted . but the formerhas the advantage of sim plicity .

From the balance between the total ofMaterials,

Wages , and Containers , and the Net Sales , thegross profit in each department can be obtained .

1 2

Now, the percentage of expenses of t he businessis known from

&

previous experience . This shouldbe checked by examination of the currentexpenses as shown later (FormAllot to each department its percentage of

expense and the balance shows approximate netprofit .

Form 1 3 .

C OST DEPARTMENT W EE&LY REPORT .

Depm meflt A TO‘al to da teTotal Consump t ion

s dMaterial

Conta iners

W ages 1:

C r . Net Sales

B alance &ross Profit

Expenses

DEPARTMENTAL PROF ITS .

Expense Total

5 d 5 ( 1 3 dDept . A .

Dep t . B

I t i s necessary somet imes to allow a heavi erpercentage of expense to on e department than toanother . The Simplest plan i s to charge expensesaccording to percentage on net sales , but in somecases i t is necessary to Charge a percentageon amount Of wages paid , or part ly accordingto the amount Oi

& wages a n d partly according&

to

the value of materials used . The di fferent methodsare requi red in order to be fair as between on e

kind of work and another, and all these methods

I 3

are equally correct under different circumstancesI f the value of the materials differs widely indi fferent departments

,or if one department

exp ends considerable labour upon its products ,compared with another where little labour isrequired

,the division of expenses m ust be based

partly,at any rate— on the wages paid . But the

basis having been settled,i t is important to

Observe that the total of the amounts charged forexpenses actually covers the expenses beingincurred .

Parti al ly Made &oods .

An obj ection to thi s method li es in the factthat fluctuations of stock of partially madegoods are not accounted for that i s to say ,

thatit is assumed that the values of such goods wi llremain approximately at the same level . Thispoint must be borne in mind

,and unusual fluctua

t ions in such stock at the time of preparing theaccount when compared with the comm encementof the period under revi ew must be taken intoconsideration . This can be done best by addingan increase of partiall y made st ock to the net sales ,or deducting a decrease . In most cases

,however

,

the comparison of net sales with consumption Ofraw materi al can be sufficiently checked in respect Ofstock fluctuation by a periodi cal stocktaking Ofthe partly made and fin i shed goods— the fluctuation being accounted for to credit or debit of thedepartment concerned .

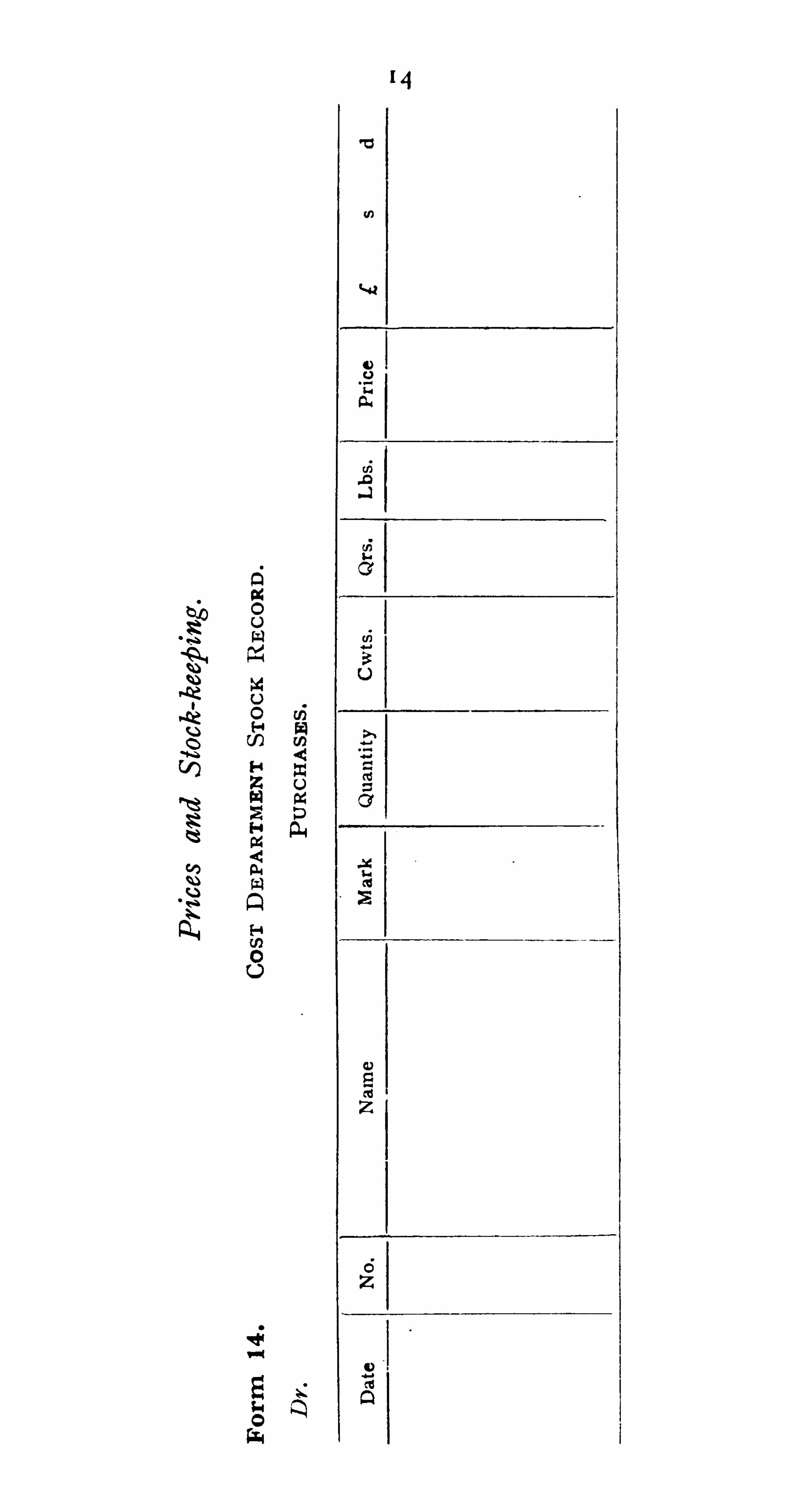

1 6

A Stock Record in the form shown abovegives an essential link between the cost clerk and

( 1 ) The purchases department .

(2 ) The stock& keeper .

From this record,which the cost clerk must

compile from the invoices,the prices of the

materials must be calculated .

To the credit Side are entered the total quantitiesissued weekly

,and the balance Should be agreed

weekly with a weekly stock& sheet Of materials onhand obtained from the stock& keeper .

PART I I I .— THE COST LED&ER— THE COST

&OURNAL .

IN addition to the weekly Cost Sheet andSummary a record in the form of a LedgerAccount completes the cost system

,and can be

prepared from the same original dockets .

A Ledger Account must be opened in the CostLedger for each department

,and also one for

&oods and one for Wages .

Each Departm ent Account must be debited withStock on hand , from stock inventory— credited&oods Account ,

Purchases,goods and containers

,from invoice

analysis— credited &oods Account,

Wages from wages analysis— credited WagesAccount ,

by means of periodical entries in the Cost &ournalThe Materials Transfer Summary must be

j ournalised and posted weekly,the respect ive

departments being credited and debited in respectof the materials which have passed between them .

At the following stocktaking the total sales an dstock on hand will be credited to each department ,the balance Showing the gross profit .

This wi ll agree with the gross profit shown inthe Cost Department Reports (sub j ect to the latterbeing adj usted in respect of fluctuat ions in theamounts of stock of partly manufactured an d

finished goods) , and the two records serve to

check on e another in this way.

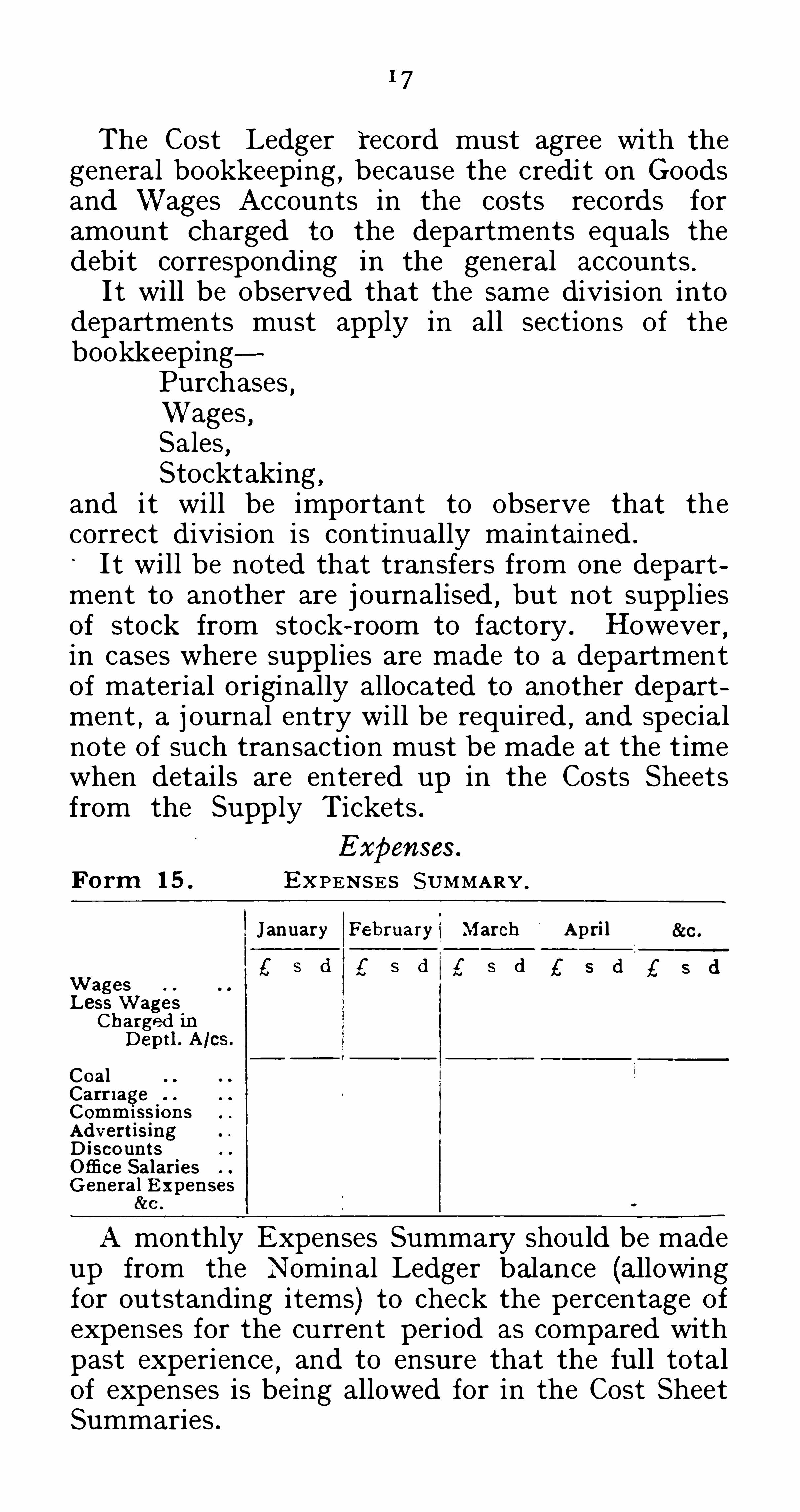

I 7

The Cost Ledger record must agree with thegeneral bookkeeping

,because the credi t on &oods

and Wages Accounts in the costs records foramount Charged to the departm ents equals thedebit corresponding in the general accounts .

I t wi ll be observed that the same division intodepartments must apply in all sections of thebookkeeping

Purchases,

Wages ,Sales

,

Stocktaking,

and it will be important to observe that thecorrect division is continually maintained .

I t will be noted that transfers from one department to another are j ournalised , but not suppliesof stock from stock & room to factory . H owever

,

in cases where supplies are m ade to a departmentof material originally allocated to another departm ent , a j ournal entry will be required ,

and specialnote of such transaction must be made at the t im ewhen detai ls are entered up in the Costs Sheetsfrom the Supply Tickets .

Expen ses .

Fo rm 1 5 E&PENSES SUMMARY .

&anuary February j March Apri l

W ag esLess W agesC harged i n

Dep t l . A/cs .

CoalCarr i ageComm i ss ionsAdv ert is ingD iscountsOffi ce Salaries&eneral Expenses

A monthly Expenses Summary should be madeup from the Nominal Ledger balance (allowingfor outstanding item s) to check the percentage ofexpenses for the current period as compared withpast experience

,and to ensure that the full total

of expenses is being allowed for in the Cost SheetSummaries .

I 9

A monthly balance Of the Nominal Ledger i salso useful for ensuring that the post ings

, &c.,are

correct and up to date . For this purpose , of

course , sectional accounts for Purchase Ledger andSales Ledger are essent ial .

WOR&S IN STRUCTIONS .

S tock Room to Work s or Forward i n g Departmen t.

Materials supplied from stores must be signedfor on Supply Requisition Tickets .

&

On e Departmen t to An other Departmen t.

&oods part l y.prepared (or materials) from onedepartment to another must be signed for onTransfer Tickets .

Departmen t to F i n i shed S tock or Forwardi n gDepartmen t .

Finished goods must be signed for on DeliveryTickets .

COST DEPARTMENT ENTRIES .

Supply Tickets to charge up to Cost Sheets ofrespect ive departments .

Supply Tickets to enter up in Stock Book .

Transfer Tickets to analyse in Transfer Book .

Totals of Summaries in Transfer Book to enterin Cost &ourn al to debit and credit of respectiveaccounts in Cost Ledger .

Same to debit and credit of respective CostSheets .

Delivery Notes to summarise on ProductionSheets . Wrappings to calculate from ProductionSheet totals and enter Cost Sheet Summary .

Complete the Cost Sheets by bringing forwardweekly totals recordi ng total consumption ofmaterial

,containers and wages

,and production .

Totals Of consumption and wages from CostSheets to Cost Sheet Summ ary .

20

Wages Analysis to charge to respect ive departments— i n Cost &ournal— post to Cost Ledger .

Purchase Invoice Book Analysis to charge torespective departments in Cost &ournal— post inCost Ledger .

Purchase invoices to enter in Stock Book .

Li st of Forms an d B ook s from which Records are

Obtai n ed .

Forms .

Sales SummarySupply RequisitionsMaterial Transfer Tickets .

Delivery TicketProduction SheetCost Sheet SummaryCost Department Weekly ReportExpense SummaryNominal Ledger Monthly BalanceB ook s .

Invoice Analysis BookSales Day BookMaterial Transfer BookCost Sheet BookWages AnalysisProduction RecordStock Book

UNI&ERS ITY OF CALIFORNIA HIBRARY,

a B ER&ELEY

THI S B OO& I S DUE ON THE LAST DATE

STAMPED B ELOWB ook s n ot retu rned on t ime a re subj ect to a fin e of

5 00 per volume after the th i rd day overdue, i n cto per v olume after the s ixth d ay. Book s n ot i ndemand m ay be renewed if app l icat ion i s m ade beforeexp i rat ion of loan per iod .