Embed Size (px)

Citation preview

Are we ready for disruptors?

CONFIDENTIALPage 4 | May 2015 | ICPA Conference | Canada Post

Security and Trust

are Vital

What is Changing What will not Change

Brand Matters

Mail has a RoleConstant Connection

Multi-Channel Advertising

Mobile Transactions

More Online Shopping

Need for Convenience,

Simplicity & Reliability

Evolving customer and consumer needs are driving

change in our markets …

CONFIDENTIALPage 5 | May 2015 | ICPA Conference | Canada Post

… this is resulting in considerable pressures and change

within our core businesses

All focused on consumer experience and relevance

Labour

• Competing against low cost models

• Labour flexibility critical

Parcels

• Pressure on numerous fronts - faster, cheaper, & more convenient

• Retailers pursuing Click & Collect or ship from store

• Move to 1:1 or “1:Few”

Marketing

• Integrated solutions are the norm – stand alone solutions under pressure

• Highly targeted is a requirement

• Need for low complexity

CONFIDENTIALPage 6 | May 2015 | ICPA Conference | Canada Post

We’ve passed the point of uncertainty, competitors are

taking actions that threaten the role of Posts

Parcel CompetitorsDM Competitors

• Final mile

• Retail alliances

• Parcel lockers

• Upstream end-to-end

• Multi-channel

• Integrated end-to-end

• Data enabler

• Loyalty and consumer-preferences

Communications & Commerce Ecosystem

Traditional Competitors New Models

21

Retailers require solutions that enable their

business strategy in an omni-commerce era

Digitally enabled consumers with near unlimited choices are

highly demandingCompetitors are taking significant actions to address

changing market requirements

CONFIDENTIALPage 7 | May 2015 | ICPA Conference | Canada Post

In Canada, Direct Mail competitors have adapted to

meet marketer needs

+

�

� � � � �

� � � � �

� � � � �

� �

◑ ● ◑ ◑ ● ◑◕ ◕ ◕ ● ● ◕◑ ◑ ◑ ● ● ◑◑ ● ◑ ● ● ◑◑ ● ◑ ○ ● ◑

Pla

nn

ing

Ta

rge

tin

g

An

aly

tic

s

Dis

trib

ute

Pri

nt

Cre

ati

ve

Multi-Channel Assets End-to-End Services

Channel partners

Partner

Sticky customer relationships

Media breadth is immense asset

CONFIDENTIALPage 8 | May 2015 | ICPA Conference | Canada Post

How we position, sell and execute on Direct Mail must

evolve

Traditional Competitors

Digital Competitors

Communicate the Value /

Relevance of Direct Mail

Optimize Sales Channels

Innovate marketing product/

solution portfolio

Reduce Direct Mail Barriers

Our strategy addresses these threatsOur intermediation role is under threat

• Search

• Social

• Mobile

• Integrated solutions

• Delivery networks

• Digital properties

• Content creation

CONFIDENTIALPage 9 | May 2015 | ICPA Conference | Canada Post

Traditional Parcel (B2C and B2B) competitors aim to

win the e-commerce market

Acquisitions• Genco• Bongo

• i-parcel• Dynamex, Ensenda,

ICS, Canpar

Initiatives• Fedex Global

Returns • SenseAware

• ORION • UPS MyChoice• Temperature True Cryo

• TForce Integrated Solutions (TFI)

Expansion• Windsor Airport

Cargo Hub • Calgary Airport

• 3 BC operating centres• Calgary Healthcare

space

• Growth by acquisition (10 in past 4 years; 140

over 15 years)

Partnerships• Home Hardware • DocuSign Inc

• Access Points• Google Express• Amazon (Toronto)• Target

Competitors are expanding their assets & capabilities to serve the

changing market requirements for omni-commerce

CONFIDENTIALPage 10 | May 2015 | ICPA Conference | Canada Post

Those are traditional competitors, what about

new disruptors?

Largest taxi company owns no vehicles

Most popular media owner creates no content

Most valuable retailer has no inventory

Largest accommodation provider owns no real estateOur New

Reality

CONFIDENTIALPage 11 | May 2015 | ICPA Conference | Canada Post

New disruptors come in many forms ….

Parcel CompetitorsDM Competitors

• Final mile

• Retail alliances

• Parcel lockers

• Upstream end-to-end

• Multi-channel

• Integrated end-to-end

• Data enabler

• Loyalty and consumer-preferences

Communications & Commerce Ecosystem

Traditional Competitors New Models

21

Platforms

• New labour models

• Convenience & speed solutions

• Asset light & scalable

• Data & digital

3

Retailers require solutions that enable their

business strategy in an omni-commerce era

Digitally enabled consumers with near unlimited choices are

highly demandingCompetitors are taking significant actions to address

changing market requirements

CONFIDENTIALPage 12 | May 2015 | ICPA Conference | Canada Post

Disruptive platforms can (and do) act as intermediaries

in the Parcels & Courier market

Asset-free platforms coordinate

contracted resources & assets

Success depends on business adoption, contractor adoption, quality & logistics

management, net volume density

CONFIDENTIALPage 13 | May 2015 | ICPA Conference | Canada Post

The platform model challenges current postal & courier

business models

Postal courier experience is based

on cost, reach, trust, and speed

Platforms offer new combinations

of cost and convenience

Cost Reach(National)

SpeedConvenience &Flexibility

Trust & Security

VALUE DRIVER

ILLUSTRATIVE

Large cities only

CONFIDENTIALPage 14 | May 2015 | ICPA Conference | Canada Post

Platforms have the potential to serve consumers’

changing needs and intermediate many relationships

� Can facilitate optimal

delivery for time-

sensitive grocery

delivery (refrigerated

items, fresh produce,

etc.)

Groceries

� Could comingle

heavies from different

retailers to further

improve the

economics

Heavies

� Platform actions could

push this to be the

perceived standard

� Would allow a delivery

window of choice (i.e.

before work, after

work, etc.) and boost

convenience for

consumers

Same Day

� Focus on e-commerce

growth in urban areas

� Can facilitate faster

delivery, flexible

options (i.e. time of

day, location, etc.),

lower cost, and higher

convenience

Parcels

CONFIDENTIALPage 15 | May 2015 | ICPA Conference | Canada Post

Platforms can enable same day & ship-from-store

Platforms can rival our economics & experience for dense, local delivery

1-2 days @ ARP $X

Illustrative

VS

Hudson’s Bay Co.

Platforms enable convenient “1: Few” relationships at a competitive price

Order by 5pmDelivered 7-9PM

@ ARP $X

CONFIDENTIALPage 16 | May 2015 | ICPA Conference | Canada Post

Social Shipping Landscape

CONFIDENTIALPage 17 | May 2015 | ICPA Conference | Canada Post

� On-demand, asset-light final mile delivery

� Rapid & flexible delivery

� Good urban urban reach

Requires sufficient density and infrastructure

A contracted final mile would hit the very core of the

Post advantage

Contracted Final Mile

CONFIDENTIALPage 18 | May 2015 | ICPA Conference | Canada Post

New disruptors come in many forms …. Ecosystem players

are also massive threats for disruption

Parcel CompetitorsDM Competitors Ecosystems

• Final mile

• Retail alliances

• Parcel lockers

• Upstream end-to-end

• Multi-channel

• Integrated end-to-end

• Data enabler

• Loyalty and consumer-preferences

• End-to-end solutions

• Convenience & speed solutions

• Scalable

• Data & digital

Communications & Commerce Ecosystem

Traditional Competitors New Models

2 41

Platforms

• New labour models

• Convenience & speed solutions

• Asset light & scalable

• Data & digital

3

Retailers require solutions that enable their

business strategy in an omni-commerce era

Digitally enabled consumers with near unlimited choices are

highly demandingCompetitors are taking significant actions to address

changing market requirements

CONFIDENTIALPage 19 | May 2015 | ICPA Conference | Canada Post

Amazon has a dominant lead in developing its

ecosystem of solutions and could expand into delivery

Business Model

MarketingWebshop Services

Market places

DeliveryPaymentCustomer

ServiceReturns

Transport

Warehousing

Fulfillment

Amazon could expand its delivery capabilities through an Uber-like model

Contracted Delivery Now

Retail or Locker Network 1 Year

Warehouse Network 1-3 Years

Volume Density Required 1-3 Years

Amazon aims to own a complete ecosystem

CONFIDENTIALPage 20 | May 2015 | ICPA Conference | Canada Post

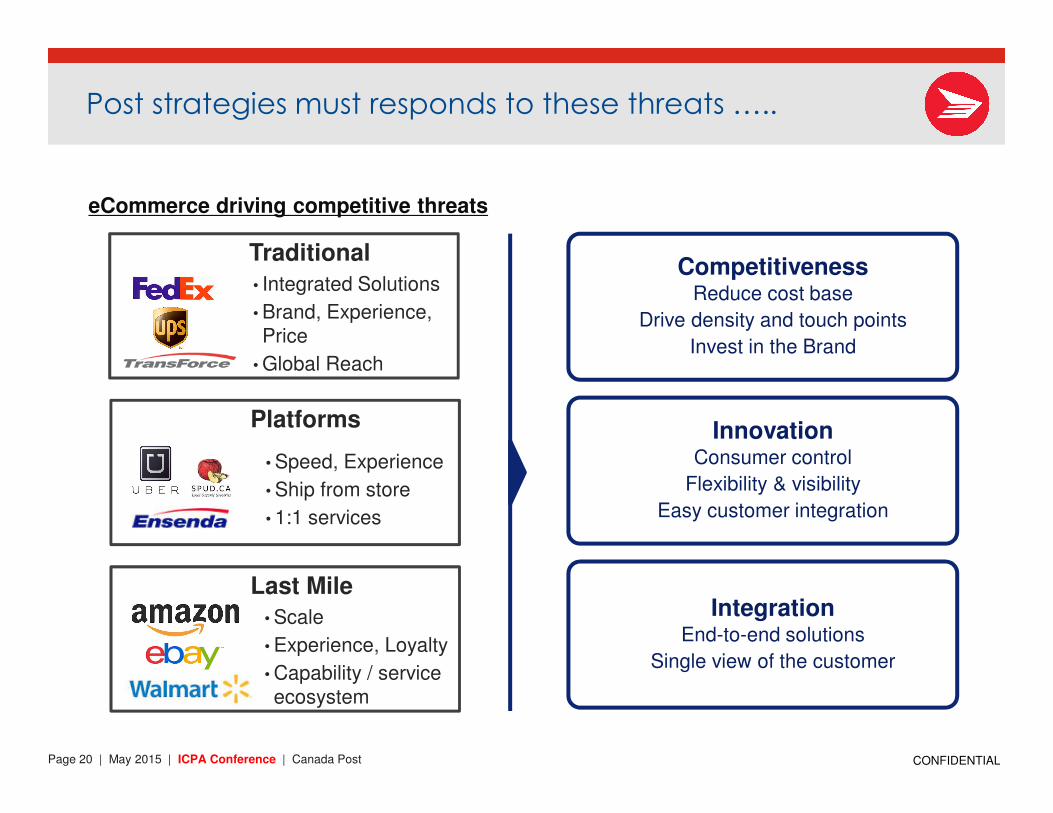

Post strategies must responds to these threats …..

Competitiveness Reduce cost base

Drive density and touch points

Invest in the Brand

InnovationConsumer control

Flexibility & visibility

Easy customer integration

IntegrationEnd-to-end solutions

Single view of the customer

Traditional

Last Mile

Platforms

eCommerce driving competitive threats

• Scale

• Experience, Loyalty

• Capability / service ecosystem

• Integrated Solutions

• Brand, Experience, Price

• Global Reach

• Speed, Experience

• Ship from store

• 1:1 services

![Welcome toVN].I.EN.1.1.[BASIC] Guidelines... · competitors Develop the customer loyalty Encourage them to keep shopping at Lazada For detailed guidance, please ... (Docusign + Hard](https://img.dokumen.tips/doc/110x75/5aa646c27f8b9a1d728e3bb1/welcome-to-vnien11basic-guidelinescompetitors-develop-the-customer-loyalty.jpg)