Embed Size (px)

Citation preview

www.intertek.com1

April 2012Intertek Presentation

www.intertek.com2

This presentation contains certain forward-looking statements with respect to the financial condition, results, operations and business of Intertek Group plc. These statements and forecasts involve risk and uncertainty because they relate to events and depend upon circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by these forward-looking statements and forecasts. Nothing in this presentation should be construed as a profit forecast.

April 2012

Cautionary statement regarding forward-looking statements

www.intertek.com3

The Global Quality Partner

Origins back to 1885

Floated 2002, entered FTSE 100 in 2009

Market Capitalisation £4bn

2011 Sales £1.7bn, Operating Profit £281m

9% Average FY Organic Revenue growth 2002-11

www.intertek.com4

Investment Proposition

Strong structural growth drivers

High barriers to entry

Low customer penetration, high market fragmentation

Balanced portfolio (industries, geographies & customers)

Emerging market exposure

Low capital intensity, flexible cost structure

Highly cash generative

www.intertek.com5

0

1,000

2,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

10 years from IPO

A decade of consistent revenue growth

Revenue£m

OUR GROWTH DRIVERS

OUR PLATFORM

OUR STRATEGY

The Future

www.intertek.com6 6

We areElectrical engineersChemistsMechanical engineersMedical doctorsConsultantsBiologistsInspectorsGeologistsAdvisors to GovernmentAuditors

Our people

www.intertek.com7

Supporting our customers in their global tradeOur organisation The industries we operate in What we doOur organisation What we doThe industries we operate in

Our organisation Industries we operate inOur organisation Industries we operate in Services

Testing

Inspection

Certification

Auditing

Outsourcing

Advisory

Training

Quality Assurance

Commodities

Industry & Assurance

Consumer Goods

Commercial & Electrical

Chemical & Pharma

Aerospace & AutomotiveBuilding ProductsChemicalConsumer Goods & RetailersElectrical & ElectronicEnergyFood & AgricultureGovernment & InstitutionsIndustrialIT & TelecomMedical & PharmaceuticalPetroleumTextile, Apparel & FootwearToys, Games & Hardlines

30,000 employees

Inte

rtek

as O

neQuality Services

www.intertek.com8

What we do for our customers

SupportTheir products and processes in their global trade in all

quality related aspects

Protect

Reduce financial, operational,

reputational and environmental risks

Speed to MarketCut lead times

and costs without compromising qualitysafety or environment

www.intertek.com9

R&D Performance Performance Issues/Returns/

Recalls

Certification -Compliance(Tech, Env, Social)

Production Distribution

End userSupply/Value Chain

Our Strategy: Target the entire supply chain

Training

Advisory

Certification

Auditing

InspectionOutsourcing

QualityAssurance

Testing

CSR

www.intertek.com10

What is Quality?

Our Strategy: Target all Quality aspects

www.intertek.com11

45%45%10%Required 3rd Party

Obligation – In house/Outsourced

Voluntary

Regional statutory>$100bn

TIC Industry Total > $200bn

Global supply chain

>$100bn

TIC Industry Composition

www.intertek.com12

For the twelve months to 31 December 2011

Revenue £1,749m + 27% at actual+ 8.3% at constant organic(2)

Operating profit(1) £281.1m + 24% at actual+ 9.6% at constant organic(2)

Operating profit margin(1) 16.1% – 50bps at actual+ 20bps at constant organic(2)

Profit before tax(1) £260.1m + 23%

Diluted EPS(1) 107.2p + 20%

Operating cash flow(1) £314.8m + 14%

Financial Highlights

(1) Before separately disclosed items; see slide 6 and appendix slide 35 for further information

(2) Growth excluding acquisitions at constant exchange rates

www.intertek.com13

Commodities 30% 24%

Industry & Assurance 27% 18%

Consumer Goods 18% 38%

Commercial & Electrical 17% 16%

Chemicals & Pharma 8% 4%

Divisional Mix

% of Group Revenue

% of Group Profit

Commodities

Industry & Assurance

Consumer Goods

Commercial & Electrical

Chemicals & Pharma

www.intertek.com14

Enduring Growth Drivers

1 Global Trade & Emerging Market Trade Growth

2 Market Drivers in our Industries

3 Network & Service Expansion

4 Outsourcing & Consulting Services

5 Industry Consolidation

www.intertek.com15

What

MarketDrivers

RegulationQuality, Safety and

Environmental standards

Supply Chain Changes

Shifting cycles, sourcing and complexity

New TechnologiesInnovation and product variety

Energy Growth & Diversity

Capex and Opex

End-User Quality Expectations & Diversity

Developed and emerging economies

Market Drivers in our Industries

www.intertek.com16

Global Trade: The Future?

Forecast Shipped Container Volumes (million TEUs)

Rate of growth in TEU Volume from 2010-30

ASIAUSA

EUROPE

Asia-USA

27

26

Asia-Europe

130

Intra-Asia

Asia -Australasia

10

Europe-Asia

25

USA-Asia

32

3

3

Intra-North America

18

Intra-Europe

USA-Europe

6

7

6

7

310% - 410%

>410%

200% - 310%

Based on Goldman Sachs Equity Research

310% - 410%

>410%

LATAM

17

6

Intra-LATAM

Asia - LATAM

8

USA-LATAM 3

www.intertek.com17

End-User Quality Demand in 2020

Source: Bain & Company

$10trillion extra

consumer spend from growth markets

1.3billion new consumers

$1trillion on

innovations for thenext big thing$5

trillion by ‘soft’ innovators onproduct variety

www.intertek.com18

Quality Expectations

Established and emerging brands use quality as a foundation

Apple GE 3M

Heineken McDonalds Caterpillar

Volkswagen Bombardier Total

Cisco Philips Maersk

Nestle BASF IKEA

Unilever Hermes Bose

L’Oreal Chevron Burberry

P&G Boeing ENI

Shell Rolls Royce Marks & Spencer

Carrefour Inditex Valero

Haier Tata

Anta Reliance

Samsung Baosteel

Vale LG

Dabur Petrobras

Vestel Huawei

Big Bazaar Pertamina

PetroChina Lenovo

Matahari Hyundai

Li-Ning Joyalukkas

www.intertek.com19 1

Industry consolidation

Widen the portfolio• Complementary services

We are an acquisitive company; our strategy is:

Increase scale• Service lines/industries

Leverage synergies• Group wide rollout

R&D • New expertise

Track record – Acquisitions since IPO in 2002

Annual average for in-fills: £54m spend on 8 acquisitionsOne strategic deal: Moody for £450m in 2011

www.intertek.com20

Moody Acquisition

• Purchased April 2011

• Large and complex acquisition

• Management structures integrated

Industry Services87% Revenue

System Certification13% Revenue

£450m acquisition

2,500+ People 60 Countries, 80 Offices

www.intertek.com21

Moody Acquisition Performance

Revenue History

• Performing ahead of expectations

• Strategic growth platform created

• Strong global customer demand

• Good cultural fit

• Key staff retained

• Locations consolidating0

100

200

300

400

2008 2009 2010 2011

£m

Margin % 14.3 14.4 11.3 12.0

8 months: 12.8

Pre-Acquisition

+ 15%Organic

www.intertek.com22

Summary

• Resilient business model

• Full year Moody in 2012 (8 months 2011)

• High single digit organic growth average

• Margin progression

• Industry consolidation

www.intertek.com23

Summary

GLOBAL TRADE

MARKET DRIVERS

NETWORK & SERVICE

OUTSOURCING & CONSULTING

INDUSTRY CONSOLIDATION

QUALITY

COMMODITIES& MATERIALS

RETAIL & MANUFACTURED

PRODUCTS

INDUSTRY ASSETS

www.intertek.com24

Appendix

www.intertek.com25

Revenue by Region

Americas

EMEA

Asia Pacific

32%

36%32%

Emerging Markets

34%

www.intertek.com26

1,374

1,749

112

268 (5)

1,2001,2501,3001,3501,4001,4501,5001,5501,6001,6501,7001,7501,800

2010

Org

anic

Acq

uisi

tions FX

2011

£m

1,374

1,749

277

57 2212 7

1,2001,2501,3001,3501,4001,4501,5001,5501,6001,6501,7001,7501,800

2010 I&A

Com

mod

ities

C&

E

CG

C&

P

2011

£m

Revenue Growth

+ 27.3%Actual rates

+ 8.3%Constant

rates

www.intertek.com27

Five Year Performance 2007 to 2011

Revenue Adjusted Operating Profit(1)

1,749

500

800

1,100

1,400

1,700

2,000

2007 2008 2009 2010 2011

£m

281

0

50

100

150

200

250

300

2007 2008 2009 2010 2011

£m23% CAGR 23% CAGR

107

0

30

60

90

120

2007 2008 2009 2010 2011

Pence

Adjusted Diluted EPS(1)

22% CAGR

(1) Before separately disclosed items

www.intertek.com28

Margin Enhancement Programme

• Underlying margin increase of 20bps in 2011

• Moody integration cost savings; £6m per annum from 2012

• Finance and IT outsourcing; £10m per annum from 2014

• Operational margin improvement and Intertek as One

• Economies of Scale

www.intertek.com29

Divisional Performance Summary

£m @ constant exchange

Revenue Margin

FY 11 ChangeOrganic change FY 11 Change

Organic change

Commodities 530.2 12.0% 11.9% 12.6% 110bps 110bps

Industry & Assurance 468.6 145.5% 7.5% 10.9% 230bps (60)bps

Consumer Goods 315.7 5.0% 4.8% 33.7% (130)bps (120)bps

Commercial & Electrical 291.0 8.7% 8.7% 15.2% 100bps 100bps

Chemicals & Pharma 143.9 5.5% 3.9% 8.9% 30bps 120bps

Group Total 1,749.4 27.8% 8.3% 16.1% (40)bps 20bps

FY 2011

www.intertek.com30

• Continued strong performance in Minerals and Government Trade Services

• Good demand for oil cargo and analytical testing driven by growth economies

• North America improving

Commodities

FY 11 Performance Developments

• Continued network and service expansion

• Emerging economies continuing to drive demand for commodities and product quality

£m @ constant exchange FY 11 Change

Organicchange

Revenue 530.2 12.0% 11.9%

Operating profit 67.0 22.8% 22.9%

Margin 12.6% 110bps 110bps

Outlook

• £24m invested in laboratories, equipment and network expansion

• Expansion of additive services, Minerals facilities in Asia and Africa

www.intertek.com31

£m @ constant exchange FY 11 Change

Organicchange

Revenue 468.6 145.5% 7.5%

Operating profit 50.9 208.5% (0.6)%

Margin 10.9% 230bps (60)bps

Industry & Assurance

• New growth platform in energy sector

• Benefitting from structural recovery

• Moody delivering ahead of plan

• Agri difficult first half; Food good performance

FY 11 Performance Developments

Add chart

• Increased energy sector investment in energy assets and diversification

• Portfolio of complementary services across infrastructure spectrum

• Further consolidation of global contracts

• Good Food opportunities

• Acquisitions in UK & Chile

• New global client contracts in Industry & Business Assurance

Outlook

www.intertek.com32

£m @ constant exchange FY 11 Change

Organicchange

Revenue 315.7 5.0% 4.8%

Operating profit 106.3 1.1% 1.2%

Margin 33.7% (130)bps (120)bps

Consumer Goods

• H1: HK and coastal China flat with textile industry rapid upsizing and downsizing

• H2: Improved growth and margin in Textiles

• Good demand in Auditing and Health & Beauty

FY 11 Performance

• Quality and safety demand increasing in growth economies

• Sustainability creating new opportunities

• Product variety and technological innovation by major global brands

• Higher brand awareness among emerging market consumers

Outlook

Developments

• New service innovations and network expansion: Guatemala, Bangladesh, Vietnam, Cambodia, Turkey

• Acquisition: Product lifecycle analysis in Europe

www.intertek.com33

£m @ constant exchange FY 11 Change

Organicchange

Revenue 291.0 8.7% 8.7%

Operating profit 44.1 15.7% 15.7%

Margin 15.2% 100bps 100bps

Commercial & Electrical

• Good growth with excellent performance in high tech areas

• Strong performance in China

• H2 margin lower due to investments

• Technology innovations for better energy usage and communications

• Network and capability enhancement

• Technical standards increasing in new technology areas eg medical & lighting

• China producing more high-value, high-tech products

FY 11 Performance Developments

Outlook

• Organic capital investment of >£20m and business development to drive growth

• Value-adding services

www.intertek.com34

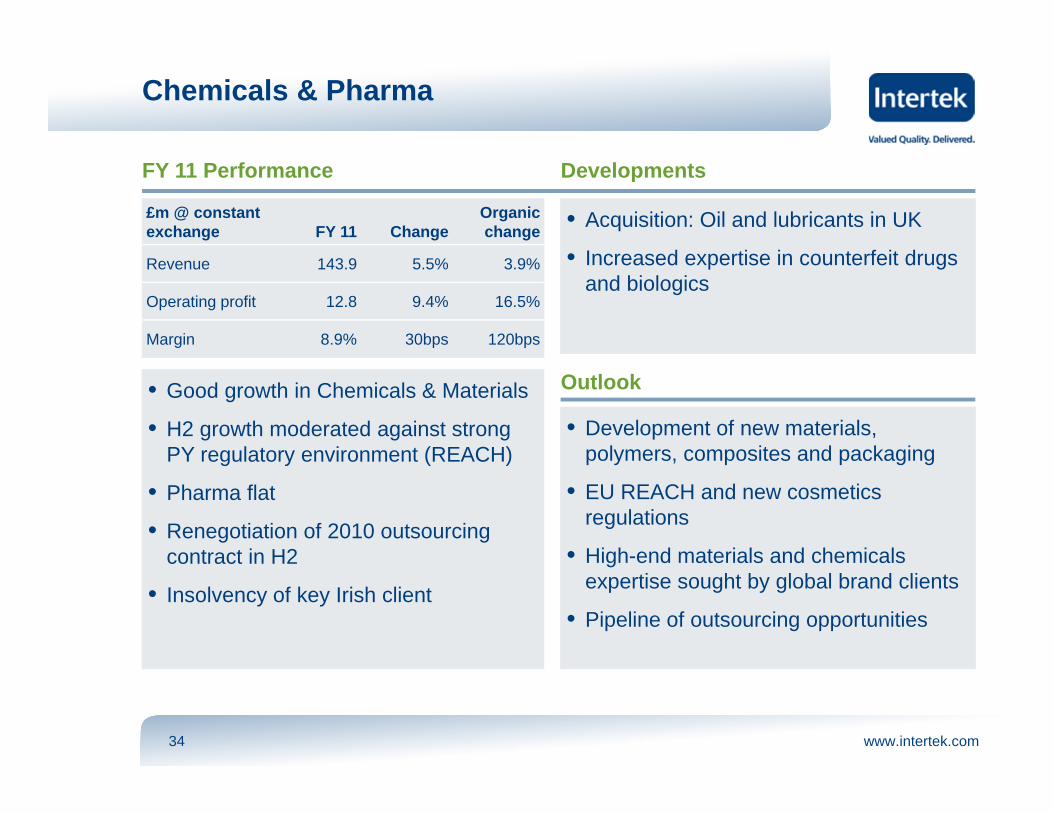

£m @ constant exchange FY 11 Change

Organicchange

Revenue 143.9 5.5% 3.9%

Operating profit 12.8 9.4% 16.5%

Margin 8.9% 30bps 120bps

Chemicals & Pharma

• Good growth in Chemicals & Materials

• H2 growth moderated against strong PY regulatory environment (REACH)

• Pharma flat

• Renegotiation of 2010 outsourcing contract in H2

• Insolvency of key Irish client

• Development of new materials, polymers, composites and packaging

• EU REACH and new cosmetics regulations

• High-end materials and chemicals expertise sought by global brand clients

• Pipeline of outsourcing opportunities

FY 11 Performance Developments

Outlook

• Acquisition: Oil and lubricants in UK

• Increased expertise in counterfeit drugs and biologics

www.intertek.com35

• Adjusted cash flow from operations £315m

• Capex £81m, 4.6% of revenue

• 5 acquisitions for £460m

• Net debt: EBITDA of 1.6

• Interest charge £21m

• Adjusted effective tax rate at 28%

Financing, Tax & Investment

2012-1513%

2016+87%

Funding Maturity Profile

• £0.9bn facilities

• 50% Bond: 50% Bank

• Maturity profile strong

www.intertek.com36

Profit Before Tax & Separately Disclosed Items

£m @ actual exchange rates 2011 2010

Adjusted operating profit (1) 281.1 227.5

Separately disclosed items:

Amortisation of acquisition intangibles (25.3) (12.9)

Acquisition transaction and integration costs (14.1) (5.3)

Restructuring costs – Business Process Outsourcing (7.7) -

Claims and settlements - (2.8)

Statutory operating profit 234.0 206.5

Net interest expense (21.0) (16.6)

Profit before tax 213.0 189.9

(1) Before separately disclosed items

www.intertek.com37

Taxation

£m @ actual exchange rates 2011 2010

Profit before tax 213.0 189.9

Tax (61.9) (50.9)

Profit after tax 151.1 139.0

Reported tax rate 29.1% 26.8%

Effective tax rate on adjusted operating profit 28.2% 26.7%

www.intertek.com38

+14%

Operating Cash Flow

£m @ actual exchange rates 2011 2010

Operating Profit before changes in working capital and provisions 329.1 282.3

Changes in working capital:

Inventory (2.1) (1.3)

Debtors and prepayments (34.8) (32.5)

Creditors and accruals (3.5) 22.9

Cash generated from operations 288.7 271.4

Separately disclosed items – cash flow 26.1 5.3

Adjusted cash flow from operations 314.8 276.7

www.intertek.com39

+20%

Free Cash Flow

£m @ actual exchange rates 2011 2010

Operating cash flow 288.7 271.4

Net interest (20.3) (14.5)

Taxation (53.4) (61.7)

Net capital expenditure (79.0) (65.1)

Free cash flow 136.0 130.1

Separately disclosed items – cash flow 26.1 5.3

Adjusted free cash flow 162.1 135.4

www.intertek.com40

Dividend Increased by 20%

• Full year dividend of 33.7p, up 20%

• Full year pay-out of £54m

• Strong and consistent record of dividend growth

• Dividend cover of 3.2

Full Year Dividend Per Share

www.intertek.com41

Net Debt

£m @ actual exchange rates 2011 2010

Borrowings 762.6 386.7

Cash (181.9) (217.0)

Net debt 580.7 169.7

Net debt to EBITDA (Proforma 12mths Moody) 1.6x 0.6x

www.intertek.com42

Liquidity Position

£m @ actual exchange rates 2011 2010

Debt facilities 911.2 722.9

Borrowings (762.6) (386.7)

Undrawn committed borrowing facilities 148.6 336.2

Cash 181.9 217.0

Liquid funds 330.5 553.2

www.intertek.com43

Currency Analysis

Local currency to GBP 2011 2010

USD 3.5% 1.60 1.55

CNY 1.1% 10.35 10.47

EUR 1.7% 1.15 1.17

HKD 3.7% 12.47 12.00

AUD 9.0% 1.55 1.69

CAD 1.0% 1.59 1.60

Revenue By Currency

USD, CNY & HKD~ 55%

GBP & EUR~ 19%

Other~ 26%