Embed Size (px)

Citation preview

Applied Research in Financial Reporting: Text and Cases

Chapter 3

The Case Research Approach

Chapter Issues

• Definition of a Case Study

• Case Based Research:– Case Development Research

• Sources for case development

– Case Analysis Research• Differences with problem/exercise approach

• Simple vs. complex cases

Case Study Definition

• A case study is a documentation of a real world situation

• It focuses on problem situations in need of research and resolution

• Can be very detailed covering various functional areas (e.g., accounting, marketing)

• Can be short covering only one functional area (e.g., accounting)

Case Development Research

• Requires field work – Researcher must have the requisite knowledge and

experience of the field– Researcher must be a careful and unbiased listener

as well as a good evidence collector– Researchers must consult multiple sources, also

called triangulation, for evidence – A need for a detailed plan of action, or protocol– Staff must be trained to conduct evidence gathering

Sources for Case Development

• Archives of accounting firms– Supplanted with field research

• Archives of the SEC– Supplanted with field research

• Other sources (e.g., the Wall Street Journal reports on companies)

Cases vs. Problems/Exercises

(Exhibit 3-2)

1. Information Setup

2. Source of Information

3. Nature of Questions

4. Solution

5. Assumptions

6. Authoritative Source

Cases vs. Problems/Exercises

7. Synthesis

8. Discussion

9. Cognitive Demand

10. Justification

11. Report

12. Documentation

Models of Case Analysis

• Analysis of Simple Cases– These cases have specific requirements similar

to problems and exercises – The specific requirements are designed to

reduce the complexity of the case– Woodside Recreation, Inc. Is an example

Woodside Recreation, Inc. Facts• Campground, cabins and recreational

facilities within 3-hours of major cities• Membership cost of $6,000 plus $30/year • Use as many times as you want up to three

weeks each time, but don’t make it a year-round home

• Average campsites 300 to be sold to 3000 members

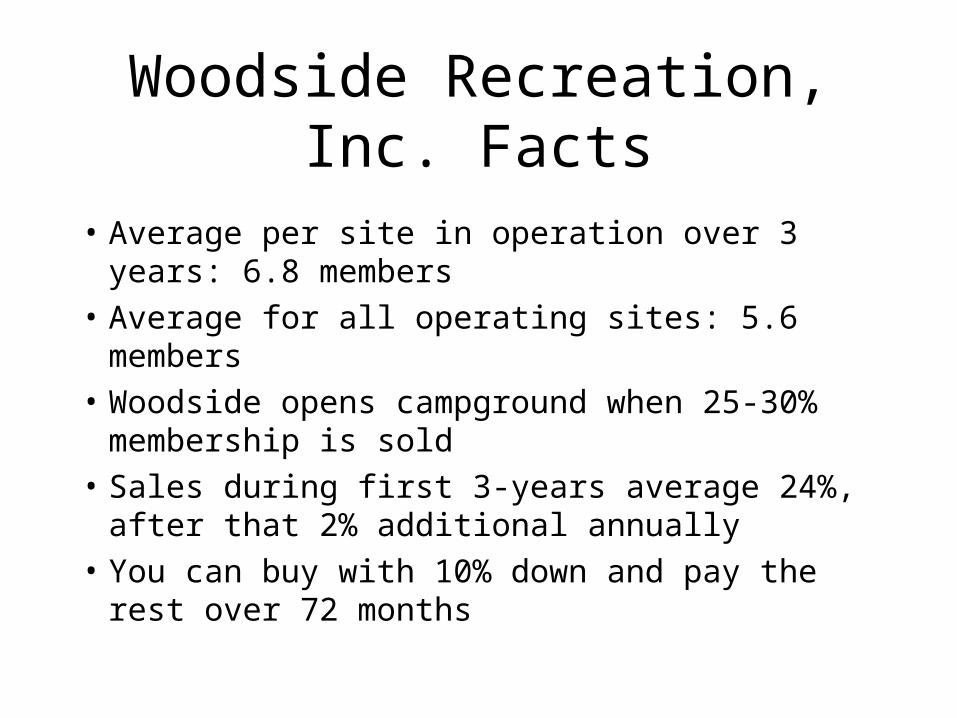

Woodside Recreation, Inc. Facts• Average per site in operation over 3 years: 6.8

members

• Average for all operating sites: 5.6 members

• Woodside opens campground when 25-30% membership is sold

• Sales during first 3-years average 24%, after that 2% additional annually

• You can buy with 10% down and pay the rest over 72 months

Woodside Recreation, Inc. Facts

• During the last 3 years, 23% of new members’ fees were received in cash

• Woodside books the entire membership amount as revenue

• 85% of revenues are from new sales

• Marketing costs are 45% of membership sales

Woodside Recreation, Inc. Facts• Land acquisition is capitalized and amortized by

the ratio of membership sold/maximum sites per campground

• Land acquisition is reported as “Operating Real Estate” net of an “Allowance for Costs of Membership Sales”

• Installment Contracts Receivables are used as collateral for debt.

• Current debt to equity ratio = 3.5 to 1.0

Woodside Recreation, Inc. Discussion

• Requirement 1: Earnings quality– defined as correlation of earnings to cash flows– at issue is whether the reported earnings can be

sustained over the longer period of time– Books sales with only 10% down– Over three years, only 23% have paid cash for

purchases

Woodside Recreation, Inc. Discussion

• Requirement 1: Earnings quality– This can be fine per APB No. 10 if appropriate

provision for uncollectible accounts exists• But aggressive marketing and liberal credit granting

makes collection questionable• Allocating cost of land acquisition on the basis of

expected members/maximum membership underestimates amortization cost due to slow sales

• Installment sale (SFAS 66) may be appropriate (used by analogy to make a point)

Woodside Recreation, Inc. Discussion

• Requirement 2: What financials should be changed?– Use installment sales– Defer revenue until a certain percentage of the

contract is collected– Increase provision for doubtful account– Increase write-off for land and improvement

costs

Woodside Recreation, Inc. Discussion

• Requirement 2: What financials should be changed?

• (Dollars in thousands)

• As Reported As Revised

• Membership sales $28,000 $28,000

• Dues and miscellaneous 5,000 5,000

• Provision for doubtful accounts (5,600) (7,000)

• Net operating revenues 27,400 26,000 – Marketing expenses (45%) 12,600 12,600

• Land and improvement costs 12,000 15,000

• 24,600 27,600

• Income (loss) $ 2,800 $(1,600)

Woodside Recreation, Inc. Discussion

• Requirement 3: Cash flows– Signs of trouble:

• Installment sales, but 45% marketing expense

• Debt/equity ratio is high at 3.5

• Almost all installment contracts receivable are used as collateral for debt

Woodside Recreation, Inc. Discussion

• Requirement 3: Cash flows• (Dollars in thousands)• 20X3 Cash Collected• • Installment contracts receivable 1/1/X3 $35,300• 20X3 Membership sales 28,000 • Total to collect 63,300• Accounts written-off ( 1,500)*• 61,800• Less: Installment contracts receivable 12/31/X3 (45,600)• Cash collected 16,200• Dues and miscellaneous (assumed collected) 5,000 • $21,200 • *Beginning allowance $4,200 plus provision $5,600 less ending allowance $8,300.• 21.6 million is needed just to cover marketing costs (12.6) and land acquisition (9.0)

– Woodside has a cash flow problem!

Woodside Recreation, Inc. Discussion

• Requirement 4: Other issues– Marketing costs are too high– Lifetime campground sales may be a fad– The membership fee ($6,000) is too high in

comparison to public campgrounds– Needs additional members to grow

Models of Case Analysis

• Analysis of Complex Cases:– A general model is needed (Exhibit 3-3):

• Identify the Objectives of the Case

• Begin with a set of key words to search the literature

• Discuss the literature

• List Alternative Solutions

• Suggested Solution

• Provide supplements, if any

• Provide addendum, if any

Cullen Provision Corp.

Analysis

Using the Case Analysis Model (Exhibit 3-3)

Cullen Provision Corp. Facts

• Returned ham from the Army of $880,000 was written off against 20X1 income

• The ham was rejected by the Army, but was not returned in time, resulting in spoilage

• Cullen filed a claim against the the Army in 20X1, but did not disclose it in its 20X1 report

Cullen Provision Corp. Facts• Early in 20X3 (before issuing its annual report to public),

Cullen settled for $475,000, a material amount compared to Cullen’s income

• Management does not want to report it in its 20X2 income, because:

– it occurred in 20X3,

– has not been received

– IRS will want its share in 20X2

– $600,000 will have to be paid to previous owner

Cullen Provision Corp.Identify Case Objectives

• Timing of recognition of the contingent gain

• What if the settlement involves a contingent gain or loss?

Cullen Provision Corp.Professional Literature

• SAS No. 1, Section 560, “Subsequent Events” • SFAS No. 5, “Accounting for Contingencies”• ARB No. 50, “Contingencies” for gain

contingencies• SFAS No. 16, “Prior Period Adjustments”• CON No. 5, “Recognition and Measurement in

Financial Statements of Business Enterprises”

Cullen Provision Corp.Discussion

• Objective 1: Timing of recognition – Per SAS 1, Section 560, recognize in the period

if subsequent discovery of the fact that the condition existed at the balance sheet date

– Otherwise SAS 1 does not require recognition at the previous balance sheet date

Cullen Provision Corp.Discussion

• Objective 1: Timing of recognition – Contingency situation per SFAS No. 5– Gain contingency per ARB No. 50– OK per CON No. 5 to postpone to 20X3– OK per SFAS 16 to postpone to 20X3

• But what about the previous owner?

Cullen Provision Corp.Discussion

• Objective 2: What if it was a loss contingency?– Conservatism would have changed the picture.

Cullen Provision Corp.Alternative Solutions

• Were discussed in relation to case requirements – To realize gain in 20X2 – What if it was a contingent loss?

Cullen Provision Corp.Suggested Solution

• See Discussion of Objectives 1 & 2

Cullen Provision Corp.Supplements

• None

Cullen Provision Corp.Addendum

• None