Embed Size (px)

Citation preview

Applicable Indian Accounting Applicable Indian Accounting StandardsStandards

Applicability of Accounting Standards Applicability of Accounting Standards

• Level I EnterpriseLevel I Enterprise

• Level II & III EnterpriseLevel II & III Enterprise

ACCOUNTING STANDARDACCOUNTING STANDARD

Applicable Indian Accounting Applicable Indian Accounting StandardStandard

• Level I EnterpriseLevel I Enterprise– Enterprises whose equity or debt securities are Enterprises whose equity or debt securities are listedlisted whether in whether in

India or outside India.India or outside India.– Enterprises which are Enterprises which are in the processin the process of listing their equity or debt of listing their equity or debt

securities as evidenced by the board of directors’ resolution in this securities as evidenced by the board of directors’ resolution in this regard.regard.

– BanksBanks including co-operative banks. including co-operative banks.– Financial institutionsFinancial institutions..– Enterprises carrying on Enterprises carrying on insuranceinsurance business. business.– All commercial, industrial and business reporting enterprises, whose All commercial, industrial and business reporting enterprises, whose

turnoverturnover for the immediately preceding accounting period on the for the immediately preceding accounting period on the basis of audited financial statements basis of audited financial statements exceeds Rs. 50 croreexceeds Rs. 50 crore. Turnover . Turnover does not include ‘other income’.does not include ‘other income’.

– All commercial, industrial and business reporting enterprises having All commercial, industrial and business reporting enterprises having borrowings including public depositsborrowings including public deposits, , in excess of Rs. 10 crorein excess of Rs. 10 crore at at any time during the accounting period.any time during the accounting period.

– Holding and subsidiary enterprisesHolding and subsidiary enterprises of of any one of the aboveany one of the above at any at any time during the accounting period.time during the accounting period.

List of Indian Accounting StandardList of Indian Accounting StandardAS 1 Disclosure of accounting policies

AS 2 Valuation of inventories

AS 3 Cash flow statements

AS 4Contingencies and events occurring after the balance sheet

date

AS 5 net profit or loss for the period, prior period items

AS 6 Depreciation Accounting

AS 7 Construction contract

AS 8 R & D replaced by AS 26 Impairment of Assets

AS 9 Revenue Recognition

AS 10 Fixed Assets

AS 11 Foreign Exchange

AS 12 Government Grants

AS 13 Investment

AS 14 Amalgamations

AS 15 Employee Costs

List of Indian Accounting StandardList of Indian Accounting Standard

AS 16 Borrowing Costs

AS 17 Segment Reporting

AS 18 Related Party Disclosure

AS 19 Leases

AS 20 Earning Per Share

AS 21 Consolidated Financial Statements

AS 22 Deferred Tax

AS 23 Investment in associates in CFS

AS 24 Discontinuing Operations

AS 25 Interim Financial Reporting

AS 26 Intangible Assets

AS 27 FR of interests in joint venture

AS 28 Impairment of assets

AS 29 Provision, Contingent liabilities and contingent assets

List of IASList of IASIAS 1 Presentation of Financial Statements

IAS 2 Inventories

IAS 7 Cash Flow Statements

IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

IAS 10 Events After the Balance Sheet Date.

IAS 11 Construction Contracts

IAS 12 Income Taxes

IAS 14 Segment Reporting (superseded by 8 on January 1, 2008)

IAS 16 Property, Plant and Equipment

IAS 17 Leases

IAS 18 Revenue

IAS 19 Employee Benefits

IAS 20 Accounting for Government Grants and Disclosure of Government Assistance

IAS 21 The Effects of Changes in Foreign Exchange Rates

IAS 23 Borrowing Costs

IAS 24 Related Party Disclosures

IAS 26 Accounting and Reporting by Retirement Benefit Plans

List of IASList of IAS

IAS 27 Consolidated Financial Statements

IAS 28 Investments in Associates

IAS 29 Financial Reporting in Hyperinflationary Economies

IAS 31 Interests in Joint Ventures

IAS 32Financial Instruments: Presentation (Financial instruments disclosures are in 7 Financial Instruments: Disclosures, and no longer in 32)

IAS 33 Earnings Per Share

IAS 34 Interim Financial Reporting

IAS 36 Impairment of Assets

IAS 37 Provisions, Contingent Liabilities and Contingent Assets

IAS 38 Intangible Assets

IAS 39 Financial Instruments: Recognition and Measurement

IAS 40 Investment Property

IAS 41 Agriculture

List of IFRSList of IFRS

IFRS 1First time Adoption of International Financial Reporting Standards

IFRS 2 Share-based Payment

IFRS 3 Business Combinations

IFRS 4 Insurance Contracts

IFRS 5Non-current Assets Held for Sale and Discontinued Operations

IFRS 6 Exploration for and Evaluation of Mineral Resources

IFRS 7 Financial Instruments: Disclosures

IFRS 8 Operating Segments[1]

AS 1 – AS 1 – Disclosure of Accounting Disclosure of Accounting

PoliciesPolicies

Fundamental Accounting AssumptionsFundamental Accounting Assumptionsa.a. Going Concern Going Concern b.b. ConsistencyConsistencyc.c. AccrualAccrual

The The accounting policiesaccounting policies refer to the refer to the specific accounting principles and the specific accounting principles and the methods of applying those principles methods of applying those principles adopted by the enterprise in the adopted by the enterprise in the preparation and presentation of financial preparation and presentation of financial statements. statements.

AS 1 – AS 1 – Disclosure of Accounting Disclosure of Accounting

PoliciesPolicies Areas in Which Differing Accounting Policies are Areas in Which Differing Accounting Policies are EncounteredEncountered

• Methods of depreciation, depletion and amortizationMethods of depreciation, depletion and amortization• Treatment of expenditure during constructionTreatment of expenditure during construction• Conversion or translation of foreign currency itemsConversion or translation of foreign currency items• Valuation of inventoriesValuation of inventories• Treatment of goodwillTreatment of goodwill• Valuation of investmentsValuation of investments• Treatment of retirement benefitsTreatment of retirement benefits• Recognition of profit on long-term contractsRecognition of profit on long-term contracts• Valuation of fixed assetsValuation of fixed assets• Treatment of contingent liabilities. Treatment of contingent liabilities.

The above list of examples is not intended to be exhaustive.The above list of examples is not intended to be exhaustive.

AS 1 – AS 1 – Disclosure of Accounting Disclosure of Accounting

PoliciesPolicies major considerations governing the selection and application of major considerations governing the selection and application of accounting policies are:—accounting policies are:—

a. a. PrudencePrudenceIn view of the uncertainty attached to future events, profits are not In view of the uncertainty attached to future events, profits are not anticipated but recognized only when realized though not necessarily in anticipated but recognized only when realized though not necessarily in cash. Provision is made for all known liabilities and losses even though cash. Provision is made for all known liabilities and losses even though the amount cannot be determined with certainty and represents only a the amount cannot be determined with certainty and represents only a best estimate in the light of available information. best estimate in the light of available information.

b. b. Substance over FormSubstance over Form The accounting treatment and presentation in financial statements of The accounting treatment and presentation in financial statements of transactions and events should be governed by their substance and not transactions and events should be governed by their substance and not merely by the legal form. merely by the legal form.

c. c. MaterialityMateriality Financial statements should disclose all “material” items, i.e. items the Financial statements should disclose all “material” items, i.e. items the knowledge of which might influence the decisions of the user of the knowledge of which might influence the decisions of the user of the financial statements. financial statements.

AS 1 – AS 1 – Disclosure of Accounting Disclosure of Accounting

PoliciesPolicies • All significant accounting policiesAll significant accounting policies adopted in the preparation and adopted in the preparation and

presentation of financial statements should be disclosed.presentation of financial statements should be disclosed.

• The disclosure of the significant accounting policies as such The disclosure of the significant accounting policies as such should form should form part of the financial statementspart of the financial statements and the significant accounting policies and the significant accounting policies should normally be should normally be disclosed in one placedisclosed in one place..

• Any changeAny change in the accounting policies which has a in the accounting policies which has a material effectmaterial effect in the in the current period or which is reasonably expected to have a material effect current period or which is reasonably expected to have a material effect in later periods should be disclosed. In the case of a change in in later periods should be disclosed. In the case of a change in accounting policies which has a material effect in the current period, accounting policies which has a material effect in the current period, the amount by which any item in the financial statements is affected by the amount by which any item in the financial statements is affected by such change should also be disclosed to the extent ascertainable. such change should also be disclosed to the extent ascertainable. Where such amount is not ascertainable, wholly or in part, the fact Where such amount is not ascertainable, wholly or in part, the fact should be indicated.should be indicated.

• If the If the fundamental accounting assumptionsfundamental accounting assumptions, viz. Going Concern, , viz. Going Concern, Consistency and Accrual are followed in financial statements, specific Consistency and Accrual are followed in financial statements, specific disclosure is not required. If a fundamental accounting assumption is disclosure is not required. If a fundamental accounting assumption is not followed, the fact should be disclosed.not followed, the fact should be disclosed.

AS 2 – AS 2 – Valuation of Valuation of InventoriesInventories • ScopeScope

This Statement should be applied in accounting for inventories This Statement should be applied in accounting for inventories other other thanthan::

1. work in progress arising under construction contracts, including 1. work in progress arising under construction contracts, including directly related service contracts (see Accounting Standard (AS) 7, directly related service contracts (see Accounting Standard (AS) 7, Accounting for Construction Contracts ;Accounting for Construction Contracts ;

2. work in progress arising in the ordinary course of business of service 2. work in progress arising in the ordinary course of business of service providers;providers;

3. shares, debentures and other financial instruments held as stock-in-3. shares, debentures and other financial instruments held as stock-in-trade; and trade; and

4. producers’ inventories of livestock, agricultural and forest products, 4. producers’ inventories of livestock, agricultural and forest products, and mineral oils, ores and gases to the extent that they are measured and mineral oils, ores and gases to the extent that they are measured at net realizable value in accordance with well established practices in at net realizable value in accordance with well established practices in those industries. those industries.

AS 2 – AS 2 – Valuation of Valuation of InventoriesInventories DefinitionsDefinitions

The following terms are used in this Statement with the The following terms are used in this Statement with the meanings specified:meanings specified:

Inventories Inventories are assets:are assets:1.1. held for sale in the ordinary course of business;held for sale in the ordinary course of business;2.2. in the process of production for such sale; orin the process of production for such sale; or3.3. in the form of materials or supplies to be consumed in in the form of materials or supplies to be consumed in

the production process or in the rendering of services. the production process or in the rendering of services.

• Net realizable value Net realizable value is the estimated selling price in the is the estimated selling price in the ordinary course of business less the estimated costs of ordinary course of business less the estimated costs of completion and the estimated costs necessary to make completion and the estimated costs necessary to make the sale.the sale.

AS 2 – AS 2 – Valuation of Valuation of InventoriesInventories • Measurement of InventoriesMeasurement of Inventories

Inventories should be valued at the lower of Inventories should be valued at the lower of cost and net realizable value.cost and net realizable value.

• Cost of InventoriesCost of Inventories

The cost of inventories should comprise all The cost of inventories should comprise all costs of purchase, costs of conversion and costs of purchase, costs of conversion and other costs incurred in bringing the other costs incurred in bringing the inventories to their present location and inventories to their present location and condition. condition.

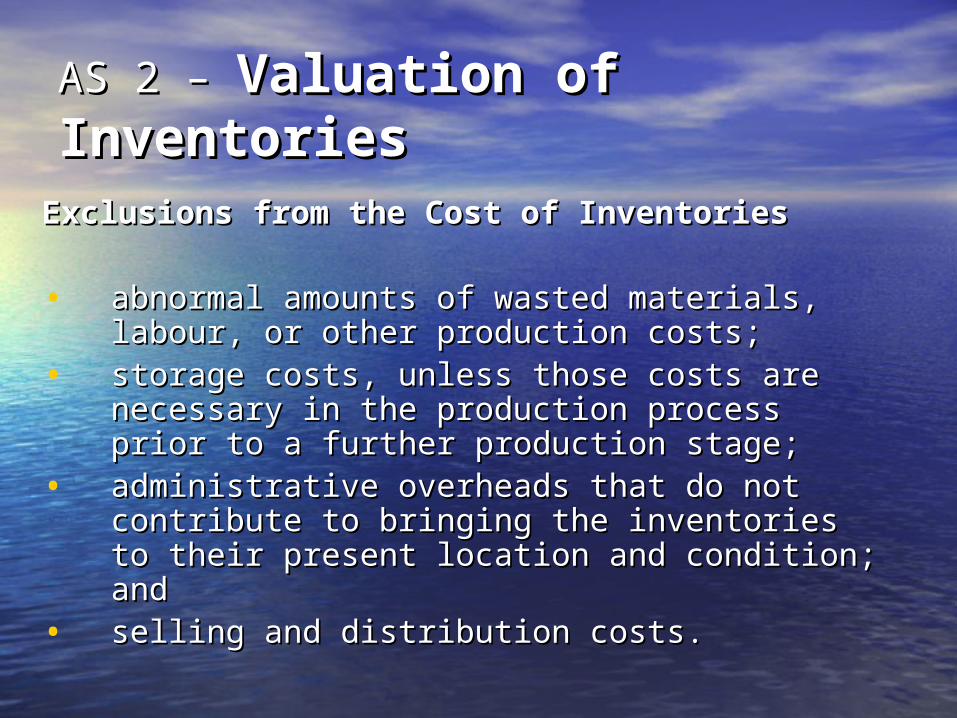

AS 2 – AS 2 – Valuation of Valuation of InventoriesInventories

Exclusions from the Cost of InventoriesExclusions from the Cost of Inventories

• abnormal amounts of wasted materials, labour, abnormal amounts of wasted materials, labour, or other production costs;or other production costs;

• storage costs, unless those costs are necessary storage costs, unless those costs are necessary in the production process prior to a further in the production process prior to a further production stage;production stage;

• administrative overheads that do not contribute administrative overheads that do not contribute to bringing the inventories to their present to bringing the inventories to their present location and condition; andlocation and condition; and

• selling and distribution costs. selling and distribution costs.

AS 2 – AS 2 – Valuation of Valuation of InventoriesInventories

Cost FormulasCost Formulas

• The cost of inventories of items that are not ordinarily The cost of inventories of items that are not ordinarily interchangeable and goods or services produced and interchangeable and goods or services produced and segregated for specific projects should be assigned by segregated for specific projects should be assigned by specific identificationspecific identification of their individual costs. of their individual costs.

• The cost of inventories, other than those dealt with in The cost of inventories, other than those dealt with in previous paragraph, should be assigned by using the previous paragraph, should be assigned by using the first-in, first-out (FIFO), or weighted average cost first-in, first-out (FIFO), or weighted average cost formulaformula. The formula used should reflect the fairest . The formula used should reflect the fairest possible approximation to the cost incurred in possible approximation to the cost incurred in bringing the items of inventory to their present bringing the items of inventory to their present location and conditionlocation and condition..

AS 2 – AS 2 – Valuation of Valuation of InventoriesInventories

DisclosureDisclosure

The financial statements should disclose: The financial statements should disclose:

• the accounting policies adopted in the accounting policies adopted in measuring inventories, including the cost measuring inventories, including the cost formula used; andformula used; and

• the total carrying amount of inventories the total carrying amount of inventories and its classification appropriate to the and its classification appropriate to the enterprise.enterprise.

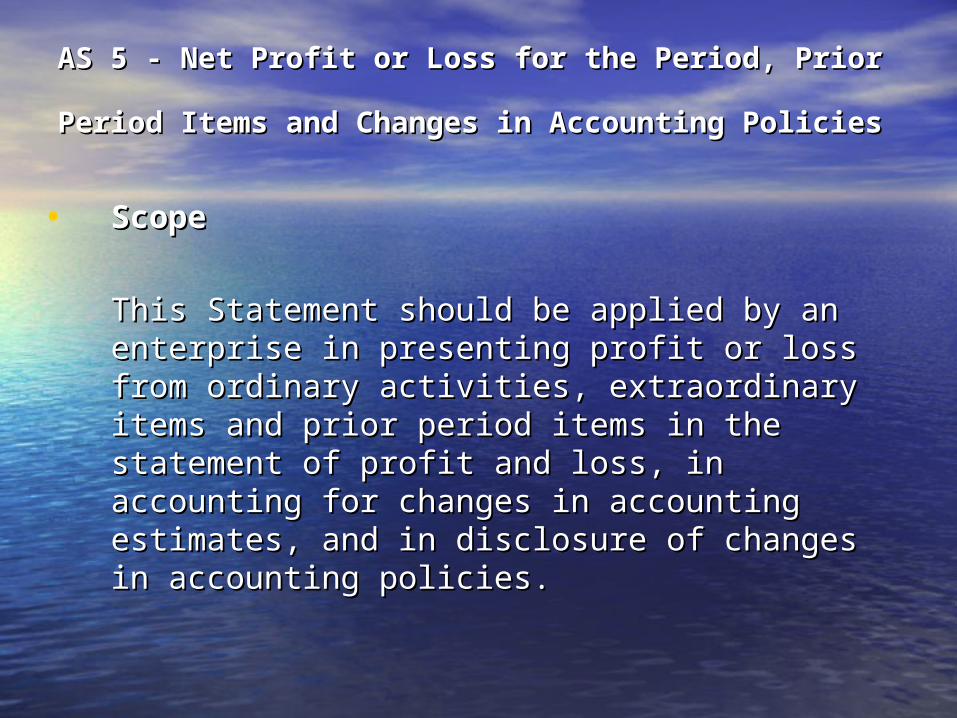

AS 5 - Net Profit or Loss for the Period, Prior AS 5 - Net Profit or Loss for the Period, Prior

Period Items and Changes in Accounting PoliciesPeriod Items and Changes in Accounting Policies

• ScopeScope

This Statement should be applied by an This Statement should be applied by an enterprise in presenting profit or loss from enterprise in presenting profit or loss from ordinary activities, extraordinary items and ordinary activities, extraordinary items and prior period items in the statement of profit and prior period items in the statement of profit and loss, in accounting for changes in accounting loss, in accounting for changes in accounting estimates, and in disclosure of changes in estimates, and in disclosure of changes in accounting policies. accounting policies.

AS 5 - Net Profit or Loss for the Period, Prior AS 5 - Net Profit or Loss for the Period, Prior

Period Items and Changes in Accounting PoliciesPeriod Items and Changes in Accounting Policies •

Ordinary activities Ordinary activities are any activities which are undertaken by are any activities which are undertaken by an enterprise as part of its business and such related activities an enterprise as part of its business and such related activities in which the enterprise engages in furtherance of, incidental to, in which the enterprise engages in furtherance of, incidental to, or arising from, these activities.or arising from, these activities.

Extraordinary items Extraordinary items are income or expenses that arise from are income or expenses that arise from events or transactions that are clearly distinct from the events or transactions that are clearly distinct from the ordinary activities of the enterprise and, therefore, are not ordinary activities of the enterprise and, therefore, are not expected to recur frequently or regularly.expected to recur frequently or regularly.

Prior period items Prior period items are income or expenses which arise in the are income or expenses which arise in the current period as a result of errors or omissions in the current period as a result of errors or omissions in the preparation of the financial statements of one or more prior preparation of the financial statements of one or more prior periods.periods.

Accounting policiesAccounting policies are the specific accounting principles and are the specific accounting principles and the methods of applying those principles adopted by an the methods of applying those principles adopted by an enterprise in the preparation and presentation of financial enterprise in the preparation and presentation of financial statements. statements.

AS 5 - Net Profit or Loss for the Period, Prior AS 5 - Net Profit or Loss for the Period, Prior

Period Items and Changes in Accounting PoliciesPeriod Items and Changes in Accounting Policies Net Profit or Loss for the PeriodNet Profit or Loss for the Period

• All items of income and expense which are recognized in a period All items of income and expense which are recognized in a period should be included in the determination of net profit or loss for should be included in the determination of net profit or loss for the period unless an Accounting Standard requires or permits the period unless an Accounting Standard requires or permits otherwise.otherwise.

• The net profit or loss for the period comprises the following The net profit or loss for the period comprises the following components, each of which should be disclosed on the face of the components, each of which should be disclosed on the face of the statement of profit and loss: statement of profit and loss:

• profit or loss from ordinary activities; andprofit or loss from ordinary activities; and

• extraordinary items. extraordinary items.

• Extraordinary ItemsExtraordinary Items

Extraordinary items should be disclosed in the statement of profit Extraordinary items should be disclosed in the statement of profit and loss as a part of net profit or loss for the period. The nature and loss as a part of net profit or loss for the period. The nature and the amount of each extraordinary item should be separately and the amount of each extraordinary item should be separately disclosed in the statement of profit and loss in a manner that its disclosed in the statement of profit and loss in a manner that its impact on current profit or loss can be perceived.impact on current profit or loss can be perceived.

AS 5 - Net Profit or Loss for the Period, Prior AS 5 - Net Profit or Loss for the Period, Prior

Period Items and Changes in Accounting PoliciesPeriod Items and Changes in Accounting Policies • Profit or Loss from Ordinary ActivitiesProfit or Loss from Ordinary Activities

When items of income and expense within profit or loss from When items of income and expense within profit or loss from ordinary activities are of such size, nature or incidence that ordinary activities are of such size, nature or incidence that their disclosure is relevant to explain the performance of the their disclosure is relevant to explain the performance of the enterprise for the period, the nature and amount of such items enterprise for the period, the nature and amount of such items should be disclosed separately.should be disclosed separately.

• Prior Period ItemsPrior Period Items

The nature and amount of prior period items should be The nature and amount of prior period items should be separately disclosed in the statement of profit and loss in a separately disclosed in the statement of profit and loss in a manner that their impact on the current profit or loss can be manner that their impact on the current profit or loss can be perceived.perceived.

AS 5 - Net Profit or Loss for the Period, Prior AS 5 - Net Profit or Loss for the Period, Prior

Period Items and Changes in Accounting PoliciesPeriod Items and Changes in Accounting Policies • Changes in Accounting estimateChanges in Accounting estimate

The effect of a change in an accounting estimate should be The effect of a change in an accounting estimate should be included in the determination of net profit or loss in: included in the determination of net profit or loss in:

• the period of the change, if the change affects the period only; the period of the change, if the change affects the period only; oror

• the period of the change and future periods, if the change the period of the change and future periods, if the change affects both. affects both.

• The effect of a change in an accounting estimate should be The effect of a change in an accounting estimate should be classified using the same classification in the statement of classified using the same classification in the statement of profit and loss as was used previously for the estimate.profit and loss as was used previously for the estimate.

• The nature and amount of a change in an accounting estimate The nature and amount of a change in an accounting estimate which has a material effect in the current period, or which is which has a material effect in the current period, or which is expected to have a material effect in subsequent periods, expected to have a material effect in subsequent periods, should be disclosed. If it is impracticable to quantify the should be disclosed. If it is impracticable to quantify the amount, this fact should be disclosed.amount, this fact should be disclosed.

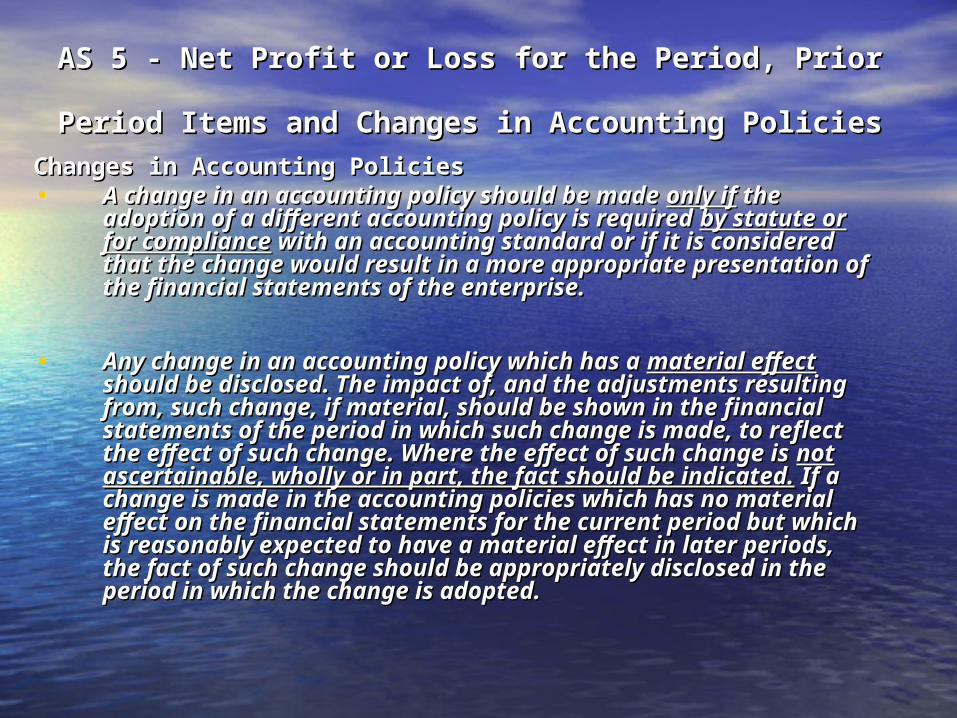

AS 5 - Net Profit or Loss for the Period, Prior AS 5 - Net Profit or Loss for the Period, Prior

Period Items and Changes in Accounting PoliciesPeriod Items and Changes in Accounting Policies Changes in Accounting PoliciesChanges in Accounting Policies• A change in an accounting policy should be made A change in an accounting policy should be made only ifonly if

the adoption of a different accounting policy is required the adoption of a different accounting policy is required by statute or for complianceby statute or for compliance with an accounting with an accounting standard or if it is considered that the change would standard or if it is considered that the change would result in a more appropriate presentation of the result in a more appropriate presentation of the financial statements of the enterprise.financial statements of the enterprise.

• Any change in an accounting policy which has a Any change in an accounting policy which has a material material effecteffect should be disclosed. The impact of, and the should be disclosed. The impact of, and the adjustments resulting from, such change, if material, adjustments resulting from, such change, if material, should be shown in the financial statements of the should be shown in the financial statements of the period in which such change is made, to reflect the period in which such change is made, to reflect the effect of such change. Where the effect of such change effect of such change. Where the effect of such change is is not ascertainable, wholly or in part, the fact should be not ascertainable, wholly or in part, the fact should be indicated.indicated. If a change is made in the accounting policies If a change is made in the accounting policies which has no material effect on the financial statements which has no material effect on the financial statements for the current period but which is reasonably expected for the current period but which is reasonably expected to have a material effect in later periods, the fact of to have a material effect in later periods, the fact of such change should be appropriately disclosed in the such change should be appropriately disclosed in the period in which the change is adopted.period in which the change is adopted.

AS 9 - Revenue RecognitionAS 9 - Revenue Recognition This Statement This Statement deals withdeals with the bases for recognition of the bases for recognition of revenue in the statement of profit and loss of an enterprise. revenue in the statement of profit and loss of an enterprise. The Statement is concerned with the recognition of revenue The Statement is concerned with the recognition of revenue arising in the course of the ordinary activities of the arising in the course of the ordinary activities of the enterprise from enterprise from

• the sale of goods, the sale of goods, • the rendering of services, and the rendering of services, and • the use by others of enterprise resources yielding interest, the use by others of enterprise resources yielding interest,

royalties and dividends. royalties and dividends.

This Statement This Statement does not deal withdoes not deal with the following aspects of the following aspects of revenue recognition to which special considerations apply: revenue recognition to which special considerations apply:

• Revenue arising from construction contracts; Revenue arising from construction contracts; • Revenue arising from hire-purchase, lease agreements; Revenue arising from hire-purchase, lease agreements; • Revenue arising from government grants and other similar Revenue arising from government grants and other similar

subsidies; subsidies; • Revenue of insurance companies arising from insurance Revenue of insurance companies arising from insurance

contracts. contracts.

AS 9 - Revenue RecognitionAS 9 - Revenue Recognition DefinitionsDefinitions

• RevenueRevenue is the gross inflow of cash, receivables or other is the gross inflow of cash, receivables or other consideration arising in the course of the ordinary activities of an consideration arising in the course of the ordinary activities of an enterprise from the sale of goods, from the rendering of services, enterprise from the sale of goods, from the rendering of services, and from the use by others of enterprise resources yielding and from the use by others of enterprise resources yielding interest, royalties and dividends. Revenue is measured by the interest, royalties and dividends. Revenue is measured by the charges made to customers or clients for goods supplied and charges made to customers or clients for goods supplied and services rendered to them and by the charges and rewards services rendered to them and by the charges and rewards arising from the use of resources by them. In an agency arising from the use of resources by them. In an agency relationship, the revenue is the amount of commission and not relationship, the revenue is the amount of commission and not the gross inflow of cash, receivables or other consideration. the gross inflow of cash, receivables or other consideration.

• Completed service contract methodCompleted service contract method is a method of accounting is a method of accounting which recognizes revenue in the statement of profit and loss only which recognizes revenue in the statement of profit and loss only when the rendering of services under a contract is completed or when the rendering of services under a contract is completed or substantially completed. substantially completed.

• Proportionate completion method Proportionate completion method is a method of accounting is a method of accounting which recognizes revenue in the statement of profit and loss which recognizes revenue in the statement of profit and loss proportionately with the degree of completion of services under a proportionately with the degree of completion of services under a contract. contract.

AS 9 - Revenue RecognitionAS 9 - Revenue Recognition Sale of goodsSale of goods

Rendering of servicesRendering of services

Others:Others:

• interest-charges for the use of cash interest-charges for the use of cash resources or amounts due to the enterprise; resources or amounts due to the enterprise;

• royalties-charges for the use of such assets royalties-charges for the use of such assets as know-how, patents, trade marks and as know-how, patents, trade marks and copyrights; copyrights;

• dividends-rewards from the holding of dividends-rewards from the holding of investments in shares investments in shares

AS 9 - Revenue RecognitionAS 9 - Revenue Recognition

• DisclosureDisclosure

In addition to the disclosures required In addition to the disclosures required by Accounting Standard 1 on by Accounting Standard 1 on ‘Disclosure of Accounting Policies’ (AS ‘Disclosure of Accounting Policies’ (AS 1), an enterprise should also disclose 1), an enterprise should also disclose the circumstances in which revenue the circumstances in which revenue recognition has been postponed recognition has been postponed pending the resolution of significant pending the resolution of significant uncertainties. uncertainties.

AS 6 – DepreciationAS 6 – Depreciation

• This Statement deals with depreciation This Statement deals with depreciation accounting and applies to all depreciable accounting and applies to all depreciable assets, assets, exceptexcept the following items to which the following items to which special considerations apply:—special considerations apply:—

• forests, plantations and similar regenerative forests, plantations and similar regenerative natural resources;natural resources;

• wasting assets including expenditure on the wasting assets including expenditure on the exploration for and extraction of minerals, oils, exploration for and extraction of minerals, oils, natural gas and similar non-regenerative natural gas and similar non-regenerative resources;resources;

• expenditure on research and development;expenditure on research and development;• goodwill;goodwill;• live stock. live stock.

AS 6 – DepreciationAS 6 – Depreciation

• DepreciationDepreciation is a measure of the wearing is a measure of the wearing out, consumption or other loss of value of a out, consumption or other loss of value of a depreciable asset arising from use, effluxion depreciable asset arising from use, effluxion of time or obsolescence through technology of time or obsolescence through technology and market changes. Depreciation is and market changes. Depreciation is allocated so as to charge a fair proportion of allocated so as to charge a fair proportion of the depreciable amount in each accounting the depreciable amount in each accounting period during the expected useful life of the period during the expected useful life of the asset. Depreciation includes amortization of asset. Depreciation includes amortization of assets whose useful life is predeterminedassets whose useful life is predetermined. .

• Depreciable assetsDepreciable assets• Useful lifeUseful life• Depreciable amountDepreciable amount

AS 6 – DepreciationAS 6 – Depreciation

The following information should be disclosed in The following information should be disclosed in the financial statements: the financial statements:

• the historical cost or other amount substituted the historical cost or other amount substituted for historical cost of each class of depreciable for historical cost of each class of depreciable assets;assets;

• total depreciation for the period for each class total depreciation for the period for each class of assets; andof assets; and

• the related accumulated depreciation the related accumulated depreciation

AS 26 – Intangible AssetsAS 26 – Intangible Assets

IntroductionIntroduction

• Effective from accounting periods commencing Effective from accounting periods commencing on or after 1on or after 1stst April 2003. April 2003.

• The following AS stand withdrawn w.e.f. The following AS stand withdrawn w.e.f. introduction of AS 26:introduction of AS 26:

AS 8 Accounting for Research and developmentAS 8 Accounting for Research and developmentAS 6 with respect to amortization of intangible AS 6 with respect to amortization of intangible assets;assets;AS 10 with respect to Fixed Assets like AS 10 with respect to Fixed Assets like Goodwill, Patents and Know- how (Para 16.3 to Goodwill, Patents and Know- how (Para 16.3 to 16.7, 37 & 38)16.7, 37 & 38)

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Not applicable in respect ofNot applicable in respect of

• Intangible assets covered by other ASIntangible assets covered by other AS• Financial assetsFinancial assets• Mineral rights and expenditure on explorationMineral rights and expenditure on exploration• Intangible assets arising in insurance Intangible assets arising in insurance

enterprises from contracts with policyholdersenterprises from contracts with policyholders• Intangible assets held for sale in ordinary Intangible assets held for sale in ordinary

course of businesscourse of business• Deferred tax assetsDeferred tax assets• Leases within the scope of AS 19 LeasesLeases within the scope of AS 19 Leases• Goodwill arising on amalgamationGoodwill arising on amalgamation

AS 26 – Intangible AssetsAS 26 – Intangible Assets

What is an intangible assets?What is an intangible assets?

• An intangible asset is an identifiable non –monetary An intangible asset is an identifiable non –monetary assets, without physical substance, held for use in the assets, without physical substance, held for use in the production or supply of goods or services, for rental to production or supply of goods or services, for rental to others, or for administrative purposesothers, or for administrative purposes

• • As asset is a resources:As asset is a resources:• Controlled by an enterprise as a result of past events; and Controlled by an enterprise as a result of past events; and • From which future economic benefits are expected to flow From which future economic benefits are expected to flow

to the enterpriseto the enterprise• Monetary assets are money held and assets to be Monetary assets are money held and assets to be

received in fixed or determinable amounts of moneyreceived in fixed or determinable amounts of money• Non- monetary assets are assets other than monetary Non- monetary assets are assets other than monetary

assetsassets

AS 26 – Intangible AssetsAS 26 – Intangible Assets

IndexIndex

• Applicability and objectiveApplicability and objective• DefinitionsDefinitions• OverviewOverview• Internally Generated Intangible AssetsInternally Generated Intangible Assets• Recognition of expensesRecognition of expenses• Subsequent ExpenditureSubsequent Expenditure• Amortization of intangiblesAmortization of intangibles• Impairment of lossesImpairment of losses• Disclosure requirementsDisclosure requirements

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Recognition and initial measurementRecognition and initial measurement

An intangible asset should be recognized if:An intangible asset should be recognized if:it is probable that the future economic benefits it is probable that the future economic benefits that are attributable to the asset will flow to the that are attributable to the asset will flow to the enterprise;enterprise;

AndAndthe cost of the asset can be measured reliablythe cost of the asset can be measured reliably

An intangible asset should be measured initially at An intangible asset should be measured initially at costcost

AS 26 – Intangible AssetsAS 26 – Intangible Assets

AS 26

Control

Future Economic benefits

Identifiably

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Internally Generated Intangible AssetsInternally Generated Intangible Assets

To assess whether an internally generated To assess whether an internally generated intangible asset meets criteria for recognition, intangible asset meets criteria for recognition, the generation of asses is classified into:the generation of asses is classified into:

Research phase; andResearch phase; andDevelopment phaseDevelopment phase

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Internally Generated Intangible AssetsInternally Generated Intangible Assets

Research activities….Research activities….• activities aimed at obtaining new knowledgeactivities aimed at obtaining new knowledge• Search, evaluation & final selection of Search, evaluation & final selection of

applications of research findingsapplications of research findings• Search for alternatives for materials, devices, Search for alternatives for materials, devices,

products, processes, systems or servicesproducts, processes, systems or services• Formulation, design, evaluation and final Formulation, design, evaluation and final

selection of possible alternatives for new or selection of possible alternatives for new or improved materials, devices, products, improved materials, devices, products, processes, systems or servicesprocesses, systems or services

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Internally Generated Intangible AssetsInternally Generated Intangible Assets

Development activities….Development activities….• Design, construction and testing of pre – Design, construction and testing of pre –

production or pre – use prototypes and models;production or pre – use prototypes and models;• Design of tools, jigs, moulds and dies involving Design of tools, jigs, moulds and dies involving

new technology;new technology;• Design, construction and operation of a pilot Design, construction and operation of a pilot

plant that is not of a scale economically plant that is not of a scale economically feasible for commercial production; andfeasible for commercial production; and

• Design, construction and testing of a chosen Design, construction and testing of a chosen alternative for new or improved materials, alternative for new or improved materials, devices, products, processes, systems or devices, products, processes, systems or servicesservices

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Internally Generated Intangible AssetsInternally Generated Intangible Assets

Development activities….Development activities….• Design, construction and testing of pre – Design, construction and testing of pre –

production or pre – use prototypes and models;production or pre – use prototypes and models;• Design of tools, jigs, moulds and dies involving Design of tools, jigs, moulds and dies involving

new technology;new technology;• Design, construction and operation of a pilot Design, construction and operation of a pilot

plant that is not of a scale economically plant that is not of a scale economically feasible for commercial production; andfeasible for commercial production; and

• Design, construction and testing of a chosen Design, construction and testing of a chosen alternative for new or improved materials, alternative for new or improved materials, devices, products, processes, systems or devices, products, processes, systems or servicesservices

AS 26 – Intangible AssetsAS 26 – Intangible Assets

AmortizationAmortization

Intangible asset should be Intangible asset should be amortized over the best estimate of amortized over the best estimate of its useful life, with a rebuttable its useful life, with a rebuttable presumption that the useful life will presumption that the useful life will not exceed ten years from the date not exceed ten years from the date when the asset is available for use.when the asset is available for use.

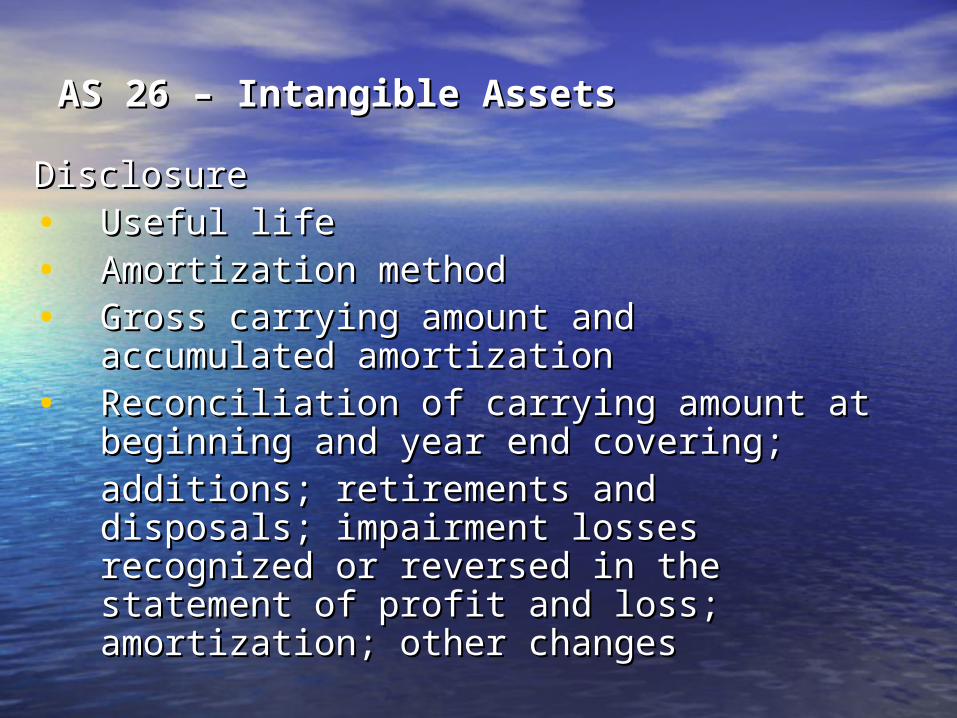

AS 26 – Intangible AssetsAS 26 – Intangible Assets

DisclosureDisclosure• Useful lifeUseful life• Amortization methodAmortization method• Gross carrying amount and accumulated Gross carrying amount and accumulated

amortizationamortization• Reconciliation of carrying amount at Reconciliation of carrying amount at

beginning and year end covering;beginning and year end covering;additions; retirements and disposals; additions; retirements and disposals; impairment losses recognized or impairment losses recognized or reversed in the statement of profit and reversed in the statement of profit and loss; amortization; other changesloss; amortization; other changes

AS 26 – Intangible AssetsAS 26 – Intangible Assets

Additional disclosureAdditional disclosure• Whether a intangible asset is amortised Whether a intangible asset is amortised

over more than ten years, its reasons over more than ten years, its reasons describing the factors that played a describing the factors that played a significant role in determining the useful significant role in determining the useful life;life;

• For an individual material intangible For an individual material intangible asset; description, carrying amount and asset; description, carrying amount and remaining period of amortisation;remaining period of amortisation;

• Restricted titles, pledged assets and Restricted titles, pledged assets and commitments for acquisitioncommitments for acquisition

• Aggregate amount of R & D expenditure Aggregate amount of R & D expenditure recognised as expenses during the recognised as expenses during the period.period.

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

• ApplicabilityApplicability

• ScopeScope

• ObjectiveObjective

• ComputationComputation

• Accounting treatmentAccounting treatment

• DisclosureDisclosure

• Transitional ProvisionsTransitional Provisions

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

• ScopeScope

Applies to all assets other thanApplies to all assets other than

1.1. Inventories (AS 2)Inventories (AS 2)

2.2. Assets arising from construction contract Assets arising from construction contract (AS 7)(AS 7)

3.3. Financial Assets/Instruments (AS 30/31)Financial Assets/Instruments (AS 30/31)

4.4. Deferred Tax AssetsDeferred Tax Assets

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

• ObjectivesObjectives

To identify assets which are carried at To identify assets which are carried at amounts in excess of their recoverable amounts in excess of their recoverable amount amount

AS 28 defines recoverable amount as the AS 28 defines recoverable amount as the higher of value in use and net selling higher of value in use and net selling priceprice

Assets is impaired if carrying amount Assets is impaired if carrying amount exceeds recoverable amountexceeds recoverable amount

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

• Indications of impairmentIndications of impairment

Assess at each Balance Sheet date Assess at each Balance Sheet date whether an asset may be impaired on whether an asset may be impaired on the basis of following factors;the basis of following factors;Internal sources of informationInternal sources of information

• Physical damage of assetPhysical damage of asset• When enterprise plan to discontinue or When enterprise plan to discontinue or

restructure operationsrestructure operations• Internal reporting on economic Internal reporting on economic

performance of an asset performance of an asset

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

External sources of informationExternal sources of information• An assets market value has declined An assets market value has declined

significantly due to passage of time or significantly due to passage of time or normal use.normal use.

• Change in technology, market, economic Change in technology, market, economic or legal environment in which the or legal environment in which the enterprise operatesenterprise operates

• Market interest rateMarket interest rate• Carrying amount of the net assets of the Carrying amount of the net assets of the

enterprise is more than its market enterprise is more than its market capitalisationcapitalisation

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

Impairment LossImpairment Loss• If carrying amount < = recoverable If carrying amount < = recoverable

amount, then asset is not impairedamount, then asset is not impaired

• If carrying amount > recoverable If carrying amount > recoverable amount, then asset is impairedamount, then asset is impaired

• Impairment Loss = any excess of Impairment Loss = any excess of carrying amount over recoverable carrying amount over recoverable amountamount

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

Measuring Recoverable AmountMeasuring Recoverable Amount

• Recoverable amount is the higher of net Recoverable amount is the higher of net selling price and its value in useselling price and its value in use

• Net selling priceNet selling price

Assets market price less cost of disposalAssets market price less cost of disposal

• Value in useValue in use

Present value factor * (Estimated future Present value factor * (Estimated future net value cash flows arising from use of net value cash flows arising from use of the asset + disposal value)the asset + disposal value)

AS 28 – Impairment of AssetsAS 28 – Impairment of Assets

Measuring Recoverable AmountMeasuring Recoverable Amount

• Recoverable amount is the higher of net Recoverable amount is the higher of net selling price and its value in useselling price and its value in use

• Net selling priceNet selling price

Assets market price less cost of disposalAssets market price less cost of disposal

• Value in useValue in use

Present value factor * (Estimated future Present value factor * (Estimated future net value cash flows arising from use of net value cash flows arising from use of the asset + disposal value)the asset + disposal value)