Embed Size (px)

Citation preview

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Result

Update

August 2, 2019

CMP: | 150 Target: | 145 ( -3%) Target Period: 12 months

Apollo Tyres (APOTYR)

HOLD

Replacement demand to the rescue…

Apollo Tyres (ATL) reported a steady performance in Q1FY20 with

replacement volume growth of ~12% in domestic operations helping it

overcome the muted prospects on the OEM front. Consolidated revenues

came in at | 4,331 crore (up 1.0% YoY). Revenues from APMEA increased

0.9% YoY to | 3,142.0 crore while revenue from Europe was up 2.4% YoY

at | 1,238.8 crore. Consolidated EBITDA declined 10.1% YoY to | 475 crore

(EBITDA margins at 11.0%, up 103 bps QoQ). While ATL’s gross margins

expanded 152 bps sequentially, gains were limited due to higher employee

cost as well as higher other expenses. Consequent, consolidated PAT

declined 43.9% YoY to | 141.6 crore.

Muted OEM dispatches to limit volume growth!

Demand prospects for automobile purchases were muted both domestically

as well as globally. Domestically, the situation is grimmer given high channel

inventory with key OEMs reporting a volume decline in the range of 15-35%

for July 2019. This is over and above the 12.4% volume decline witnessed

by the industry in Q1FY20. This will limit the volume growth for ATL, which

realises ~30% of its sales from auto OEMs. The replacement market, on the

other hand (constitute ~60% sales) is healthy and growing healthily in

double digits leading to largely flat to marginal positive volume outlook for

FY20E. In the international markets, especially Europe, the risk of trade

barrier as well as Brexit weigh on consumer demand. Consequently, we

build in sales growth of 6.4% CAGR in FY19-21E.

Increase in rubber prices to limit margin expansion!

Rubber & crude derivatives are key raw materials for tyre manufacturers.

With natural rubber prices on the rise and currently quoting at ~| 150/kg in

the domestic market vs. average landed costs of | 137/kg for ATL in Q1FY20

amid stable crude derivative prices, there exists limited scope for gross

margin & consequent EBITDA margin expansion. However, given the

management commentary on cost controls to aid increase in profitability we

build in 70 bps EBITDA margin expansion over FY19-21E.

Valuation & Outlook

ATL is in the midst of executing an aggressive plan, which entails further

loading of debt on its B/S. The interest coverage ratio, however, is

comfortably placed. Building in positives, we expect sales, PAT (excluding

exceptional loss due to IL&FS deposits) to grow at a CAGR of 6.4%, 5.4%,

respectively, in FY19-21E. At the current margin trajectory, RoCE profile is

also muted at ~8% and offers little comfort. With buoyant replacement

demand- the only solace, we maintain our HOLD rating on the stock with a

revised target price of | 145 i.e. 9X P/E on FY21E EPS of | 16.2/share.

Key Financials FY17 FY18 FY19 FY20E FY21E CAGR (FY19-21E)

Net Sales 13,180.0 14,840.5 17,548.8 18,656.6 19,873.4 6.4%

EBITDA 1,846.4 1,651.3 1,958.9 2,128.8 2,357.5 9.7%

EBITDA Margins (%) 14.0 11.1 11.2 11.4 11.9

Net Profit 1,098.6 723.9 680.0 847.5 925.1 16.6%

EPS (|) 19.2 12.7 11.9 14.8 16.2

P/E 7.8 11.9 12.6 10.1 9.3

RoNW (%) 15.1 7.4 8.3 8.0 8.2

RoCE (%) 13.6 7.7 8.0 7.7 8.2

Key Financial Summary

Source: ICICI Direct Research, Company

Particulars

Particular Amount

Market Capitalization | 8581 Crore

Total Debt (FY19) (| Crore) 4,930.7

Cash & Investments (FY19) (| Crore) 562.5

EV (| Crore) 12,948.8

52 week H/L (|) 294 / 144

Equity capital | 57.2 Crore

Face value | 1

Key Highlights

Volume growth was muted for the

quarter tracking weak OEM sales

domestically as well as weak

sentiment in the European markets

Gross margin expanded 150 bps

QoQ with overall gains at the

EBITDA margin being limited to 110

bps due to higher overheads

Management was cautious on the

demand outlook however will

actively engage in increasing

profitability over FY19-21E

Maintain HOLD with a revised target

price of | 145; valuing ATL at 9x P/E

on FY21E EPS. Valuation multiple is

limited by muted return ratios.

Research Analyst

Shashank Kanodia, CFA

Jaimin Desai

ICICI Securities | Retail Research 2

ICICI Direct Research

Result Update | Apollo Tyres

Exhibit 1: Variance Analysis

(| crore) Q1FY20 Q1FY20E Q1FY19 YoY (%) Q4FY19 QoQ (%) Comments

Total Operating Income 4,331 4,351 4,288 1.0 4,274 1.3 Topline came in line with our estimates

Raw Material Expenses 2,453 2,558 2,409 1.8 2,485 -1.3

Savings were realised on the raw material costs front with RM

to sales for the quarter coming in at 56.6%, down 150 bps QoQ

Employee Expenses 642 629 607 5.8 618 3.8

Other expenses 762 720 744 2.4 746 2.2 Other expenses came in higher at 17.6% of sales

EBITDA 475 444 528 -10.1 425 11.8

EBITDA Margin (%) 11.0 10.2 12.3 -135 bps 9.9 103 bps

EBITDA margins were ahead of our estimates tracking beat on

the raw material costs. The gains, however, were limited by

higher employee as well as other expenses

Depreciation 267 220 184 45.2 231 15.5

Interest 58.4 51.4 43.0 35.7 43 34.5

Other income 27.5 11.1 40.6 -32.2 48.5 -43.3

Tax 35.1 46.8 89.8 -60.9 14 144.4 Tax rate came in at its usual run rate of 25%

PAT 141.6 136.8 252.2 -43.9 84.0 68.6

EPS (|) 2.5 2.4 4.4 -43.9 1.5 68.6Beat at the margin level leads to more than anticipated EPS for

Q1FY20

Key Metrics

Revenue (| crore)

India 3,142 3,128 3,114 0.9 3,103 1.2In India, volumes were down ~2% YoY however but sales value

were flat tracking better product mix and marginal price hikes

Europe 1,239 1,223 1,210 2.4 1,253 -1.1

EBIT Margin (%)

India 7.5 NA 8.6 (110) bps 10.9 (340) bps

Europe -1.0 NA -1.5 50 bps 0.9 (190) bps Margins in Europe came in muted at -1%

Source: Company, ICICI Direct Research

Exhibit 2: Change in estimates

(| Crore) Old New % Change Old New % Change Comments

Revenue 18,765 18,657 -0.6 20,587 19,873 -3.5Muted dispatches at OEM front, which forms ~30% of total sales

weigh on forward sales estimates for FY20E, FY21E

EBITDA 2,200 2,129 -3.2 2,492 2,358 -5.4

EBITDA Margin (%) 11.7 11.4 -31 bps 12.1 11.9 -24 bps Broadly maintain our estimates on margin front

PAT 873 848 -2.9 1,025 925 -9.7

EPS (|) 15.3 14.8 -3.2 17.9 16.2 -9.7

EPS estimates revised downward tracking increase in interest costs

& depreciation as company is in the midst of aggressive capacity

expansion

FY20E FY21E

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 3

ICICI Direct Research

Result Update | Apollo Tyres

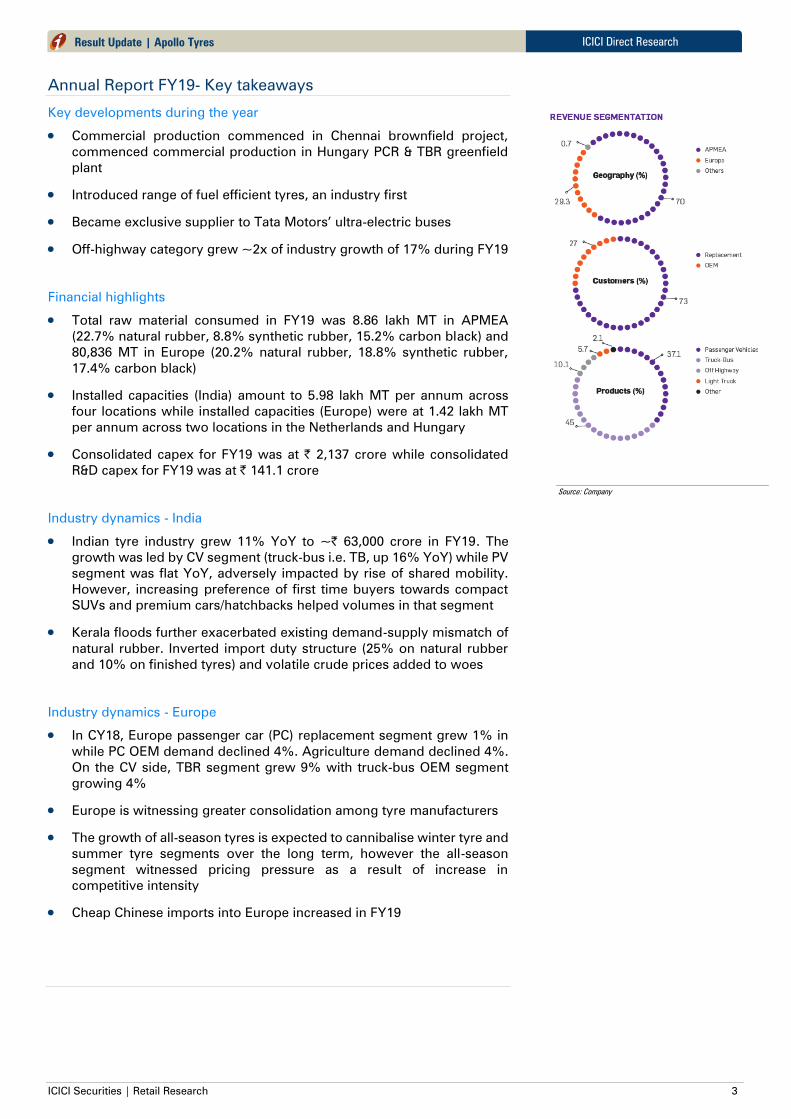

Annual Report FY19- Key takeaways

Key developments during the year

Commercial production commenced in Chennai brownfield project,

commenced commercial production in Hungary PCR & TBR greenfield

plant

Introduced range of fuel efficient tyres, an industry first

Became exclusive supplier to Tata Motors’ ultra-electric buses

Off-highway category grew ~2x of industry growth of 17% during FY19

Financial highlights

Total raw material consumed in FY19 was 8.86 lakh MT in APMEA

(22.7% natural rubber, 8.8% synthetic rubber, 15.2% carbon black) and

80,836 MT in Europe (20.2% natural rubber, 18.8% synthetic rubber,

17.4% carbon black)

Installed capacities (India) amount to 5.98 lakh MT per annum across

four locations while installed capacities (Europe) were at 1.42 lakh MT

per annum across two locations in the Netherlands and Hungary

Consolidated capex for FY19 was at | 2,137 crore while consolidated

R&D capex for FY19 was at | 141.1 crore

Industry dynamics - India

Indian tyre industry grew 11% YoY to ~| 63,000 crore in FY19. The

growth was led by CV segment (truck-bus i.e. TB, up 16% YoY) while PV

segment was flat YoY, adversely impacted by rise of shared mobility.

However, increasing preference of first time buyers towards compact

SUVs and premium cars/hatchbacks helped volumes in that segment

Kerala floods further exacerbated existing demand-supply mismatch of

natural rubber. Inverted import duty structure (25% on natural rubber

and 10% on finished tyres) and volatile crude prices added to woes

Industry dynamics - Europe

In CY18, Europe passenger car (PC) replacement segment grew 1% in

while PC OEM demand declined 4%. Agriculture demand declined 4%.

On the CV side, TBR segment grew 9% with truck-bus OEM segment

growing 4%

Europe is witnessing greater consolidation among tyre manufacturers

The growth of all-season tyres is expected to cannibalise winter tyre and

summer tyre segments over the long term, however the all-season

segment witnessed pricing pressure as a result of increase in

competitive intensity

Cheap Chinese imports into Europe increased in FY19

Source: Company

ICICI Securities | Retail Research 4

ICICI Direct Research

Result Update | Apollo Tyres

Conference call highlights

Management outlook/guidance and demand

The management sees no immediate demand recovery on OEM side but

is bullish on the replacement side. Overall it expects flattish revenue

growth for FY20E and raw material costs to increase slightly

In India, replacement volumes increased 12% YoY to highest ever level.

Replacement: OEM mix stands at 65:35 vs. normal levels of 60:30

Q1FY20 revenue contribution from trucks was 65% (25% bias, 40%

radial) and from cars was 17%

Overall volumes were up 3% QoQ but down 2% YoY. Better mix and

price hikes drove revenue growth.

Europe volumes were down 4% led by 9% decline in Germany.

Agriculture demand remains weak. The company did 5% volume

growth in passenger car tyres and the company sees healthy traction for

this segment going ahead. Truck radial volumes doubled YoY albeit on

a low base

On an overall basis the management expects India revenues to be

flattish for FY20E while Europe is expected to continue to post

improvements on revenue and profit front. India replacement demand

is seen growing in low single digits for the year

Sales, costs and margins

Europe revenues stood at €125 million vs. €120 million YoY, with

margins at 6.7%. Revenues at Reifen were flat YoY at €40 million, with

profit increasing slightly

Margins in the Europe operations are expected to improve given the

continuing Hungary ramp up, marketing cost control efforts and mix

improvement.

Standalone raw material cost for the quarter were at | 128/kg with

landed prices as follows: natural rubber | 137/kg, synthetic rubber

| 115/kg, steel cord | 145/kg & carbon black | 90/kg

Some part of higher staff and depreciation costs in India are expected to

sustain

Apollo undertook a price hike in August to the tune of 1-1.5% across

M&HCV & PV SKUs. It also took a price hike in European truck business

Other

FY20E capex guidance is | 2,700 crore (India) & €30 million (Europe).

FY21E capex guidance is ~| 1,700 crore (India) & €20-30 million (Europe)

In India, TBR capacity utilisation was at 90% while that for PCR was at

~80%

In Europe, passenger car capacity utilisation stands at 70% while that for

trucks stands below 50%

The company would defer half of the capex in Phase 1 of the Andhra

Pradesh plant, planning to achieve savings of | 400-500 crore as a result

Consolidated net debt levels were at ~| 5,500 crore, of which India net

debt stands at | 3,000 crore. Company expects debt levels to peak out

in FY21E

ICICI Securities | Retail Research 5

ICICI Direct Research

Result Update | Apollo Tyres

Financial story in charts

Exhibit 3: Geography wise revenue trend

8,682

8,934

10,300

12,354

13,277

14,260

3,284

4,091

4,630

5,261

5,390

5,614

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

FY16

FY17

FY18

FY19

FY20E

FY21E

(| crore)

India Europe

Source: Company, ICICI Direct Research

Exhibit 4: Consolidated revenue trend

13,180

14,841

17,549

18,657

19,873

11.2

12.6

18.2

6.3 6.5

0

2

4

6

8

10

12

14

16

18

20

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

FY17 FY18 FY19 FY20E FY21E

(%

)

(| crore)

Sales % growth

Source: Company, ICICI Direct Research

Exhibit 5: EBITDA margin trend

978

1,166

1,457

1,876

1,931

1,997

1,846

1,651

1,959

2,129

2,358

11.0

9.6

11.4

14.0

15.1

16.9

14.0

11.1

11.2

11.4 11.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

-

500

1,000

1,500

2,000

2,500

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E

(%

)

(| crore)

EBITDA EBITDA Margins (%)

Source: Company, ICICI Direct Research

We estimate ~4.8% CAGR (India) and ~5.0% CAGR

(Europe) volume growth during FY19-21E

We expect sales to grow at a CAGR of 6.4 % over

FY19-21E

We expect EBITDA margins at 11.4% and 11.9%, in

FY20E and FY21E, respectively

ICICI Securities | Retail Research 6

ICICI Direct Research

Result Update | Apollo Tyres

Exhibit 6: Margin movement with RM trend

52.4

56.9

50.8

53.4

49.5

49.9

49.2

51.9

52.7

57.2

59.8

58.0

56.3

55.4

56.7

57.8

59.8

59.5

15.8

16.6

17.7

16.1

17.2

16.0 16.3

14.2 14.4

11.1

8.3

10.5

12.312.8

12.3

11.0 11.2

9.9

36

40

44

48

52

56

60

64

4

6

8

10

12

14

16

18

20Q

3FY15

Q4FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Q1FY19

Q2FY19

Q3FY19

Q4FY19

(%

)

(%

)

Raw materials/Sales Contribution OPM (LHS)

Source: Company, ICICI Direct Research

Exhibit 7: Profitability trend

440

432

601

1,044

1,015

1,091

1,099.1

723.9

680.0

847.5

925.1

5.0

3.6

4.7

7.8 7.9

9.2

8.3

4.9

3.9

4.5 4.7

2

3

4

5

6

7

8

9

10

-

200

400

600

800

1,000

1,200

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E

(%

)

(| cro

re)

PAT PAT Margin (%)

Source: Company, ICICI Direct Research

Exhibit 8: Profitability trend

1,474

1,242

739 1,602

1,701

3,847

3,479

1,420

3,000

2,000

3,245

4,661

4,931

6,531

7,031

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY17 FY18 FY19 FY20E FY21E

(| crore)

CFO Capex Debt

Source: Company, ICICI Direct Research

Movement in prices of rubber and crude oil has a

prominent impact on the margin trajectory at tyre

companies including ATL

We build in PAT CAGR of 5.4% (excluding

exceptional items) over FY19-21E.

With high capex spend the Debt is expected to

further increase to ~| 7,000 crore in FY21E

ICICI Securities | Retail Research 7

ICICI Direct Research

Result Update | Apollo Tyres

Exhibit 9: Valuation Summary

Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE

(| cr) (%) (|) (%) (x) (x) (%) (%)

FY17 13,180 11.2 19.2 (2.2) 7.8 6.0 15.1 13.6

FY18 14,841 12.6 12.7 (34.1) 11.9 6.8 7.4 7.7

FY19 17,549 18.2 11.9 (6.1) 12.6 6.6 8.3 8.0

FY20E 18,657 6.3 14.8 24.6 10.1 6.8 8.0 7.7

FY21E 19,873 6.5 16.2 9.2 9.3 6.4 8.2 8.2

Source: Bloomberg, ICICI Direct Research

Exhibit 10: Apollo Tyres currently trades in line with long term two year forward P/E multiple of ~9.3x

0

50

100

150

200

250

300

350

400

450

Mar-09

Jul-09

Nov-09

Mar-10

Jul-10

Nov-10

Mar-11

Jul-11

Nov-11

Mar-12

Jul-12

Nov-12

Mar-13

Jul-13

Nov-13

Mar-14

Jul-14

Nov-14

Mar-15

Jul-15

Nov-15

Mar-16

Jul-16

Nov-16

Mar-17

Jul-17

Nov-17

Mar-18

Jul-18

Nov-18

Mar-19

Jul-19

(|)

Price 20x 17x 15x 12x 10x 7x 5x

Source: Reuters, ICICI Direct Research

ICICI Securities | Retail Research 8

ICICI Direct Research

Result Update | Apollo Tyres

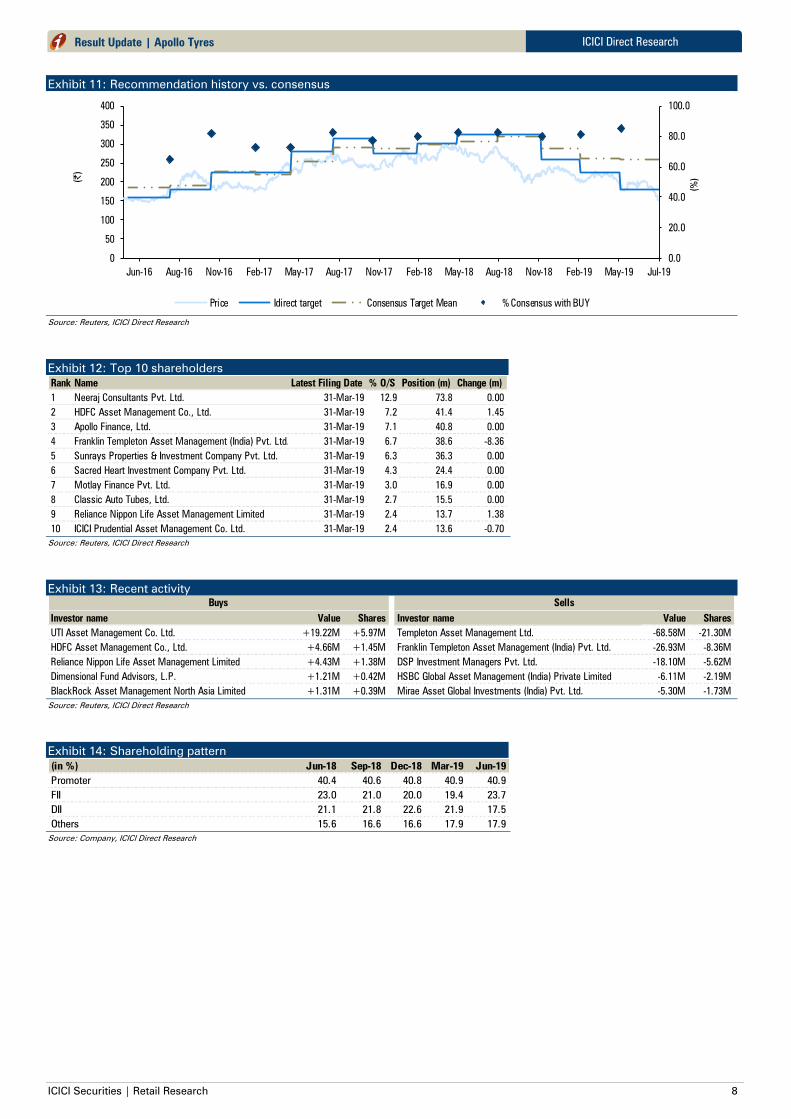

Exhibit 11: Recommendation history vs. consensus

0.0

20.0

40.0

60.0

80.0

100.0

0

50

100

150

200

250

300

350

400

Jul-19May-19Feb-19Nov-18Aug-18May-18Feb-18Nov-17Aug-17May-17Feb-17Nov-16Aug-16Jun-16

(%

)(|)

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Reuters, ICICI Direct Research

Exhibit 12: Top 10 shareholders

Rank Name Latest Filing Date % O/S Position (m) Change (m)

1 Neeraj Consultants Pvt. Ltd. 31-Mar-19 12.9 73.8 0.00

2 HDFC Asset Management Co., Ltd. 31-Mar-19 7.2 41.4 1.45

3 Apollo Finance, Ltd. 31-Mar-19 7.1 40.8 0.00

4 Franklin Templeton Asset Management (India) Pvt. Ltd. 31-Mar-19 6.7 38.6 -8.36

5 Sunrays Properties & Investment Company Pvt. Ltd. 31-Mar-19 6.3 36.3 0.00

6 Sacred Heart Investment Company Pvt. Ltd. 31-Mar-19 4.3 24.4 0.00

7 Motlay Finance Pvt. Ltd. 31-Mar-19 3.0 16.9 0.00

8 Classic Auto Tubes, Ltd. 31-Mar-19 2.7 15.5 0.00

9 Reliance Nippon Life Asset Management Limited 31-Mar-19 2.4 13.7 1.38

10 ICICI Prudential Asset Management Co. Ltd. 31-Mar-19 2.4 13.6 -0.70

Source: Reuters, ICICI Direct Research

Exhibit 13: Recent activity

Investor name Value Shares Investor name Value Shares

UTI Asset Management Co. Ltd. +19.22M +5.97M Templeton Asset Management Ltd. -68.58M -21.30M

HDFC Asset Management Co., Ltd. +4.66M +1.45M Franklin Templeton Asset Management (India) Pvt. Ltd. -26.93M -8.36M

Reliance Nippon Life Asset Management Limited +4.43M +1.38M DSP Investment Managers Pvt. Ltd. -18.10M -5.62M

Dimensional Fund Advisors, L.P. +1.21M +0.42M HSBC Global Asset Management (India) Private Limited -6.11M -2.19M

BlackRock Asset Management North Asia Limited +1.31M +0.39M Mirae Asset Global Investments (India) Pvt. Ltd. -5.30M -1.73M

Buys Sells

Source: Reuters, ICICI Direct Research

Exhibit 14: Shareholding pattern

(in %) Jun-18 Sep-18 Dec-18 Mar-19 Jun-19

Promoter 40.4 40.6 40.8 40.9 40.9

FII 23.0 21.0 20.0 19.4 23.7

DII 21.1 21.8 22.6 21.9 17.5

Others 15.6 16.6 16.6 17.9 17.9

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 9

ICICI Direct Research

Result Update | Apollo Tyres

Financial Summary

Exhibit 15: Profit and loss statement | crore

(Year-end March) FY18 FY19 FY20E FY21E

Total operating Income 14,840.5 17,548.8 18,656.6 19,873.4

Growth (%) 12.6 18.2 6.3 6.5

Raw Material Expenses 8,395.5 10,126.2 10,678.9 11,335.4

Employee Expenses 2,156.6 2,456.2 2,619.7 2,765.8

Other Expenses 2,637.1 3,007.5 3,229.2 3,414.6

Total Operating Expenditure 13,189.3 15,589.9 16,527.8 17,515.9

EBITDA 1,651.3 1,958.9 2,128.8 2,357.5

Growth (%) -10.6 18.6 8.7 10.7

Depreciation 592.6 812.7 858.2 894.3

Interest 162.9 181.1 251.8 305.1

Other Income 116.5 123.1 111.9 109.1

PBT 1012.3 888.2 1130.7 1267.2

Exceptional items 0.0 200.0 0.0 0.0

Total Tax 288.4 208.3 283.2 342.2

Reported PAT 723.9 680.0 847.5 925.1

Growth (%) -34.1 -6.1 24.6 9.2

EPS (|) 12.7 11.9 14.8 16.2

Source: Company, ICICI Direct Research

Exhibit 16: Cash flow statement | crore

(Year-end March) FY18 FY19 FY20E FY21E

Profit after Tax 723.9 680.0 847.5 925.1

Add: Depreciation 592.6 812.7 858.2 894.3

(Inc)/dec in Current Assets -682.6 -205.6 -505.9 -369.9

Inc/(dec) in CL and Provisions 607.8 -548.5 402.0 251.4

CF from operating activities 1241.6 738.6 1601.8 1700.8

(Inc)/dec in Investments -944.6 1,339.0 0.0 0.0

(Inc)/dec in Fixed Assets -3,479.0 -1,419.7 -3,000.0 -2,000.0

Others 450.2 -561.3 32.2 35.4

CF from investing activities -3973.4 -642.0 -2967.8 -1964.6

Issue/(Buy back) of Equity 0.0 0.0 6.3 0.0

Inc/(dec) in loan funds 1,416.6 269.5 1,600.0 500.0

Dividend paid & dividend tax -219.3 -237.6 -240.3 -257.4

Others 1,796.7 -164.8 -6.3 0.0

CF from financing activities 2994.0 -132.9 1359.7 242.6

Net Cash flow 262.2 -36.3 -6.2 -21.2

Opening Cash 336.6 598.8 562.5 556.3

Closing Cash 598.8 562.5 556.3 535.1

Source: Company, ICICI Direct Research

Exhibit 17: Balance Sheet | crore

(Year-end March) FY18 FY19 FY20E FY21E

Liabilities

Equity Capital 57.2 57.2 57.2 57.2

Reserve and Surplus 9,719.4 9,982.6 10,589.8 11,257.5

Total Shareholders funds 9,776.6 10,039.8 10,647.0 11,314.7

Total Debt 4,661.2 4,930.7 6,530.7 7,030.7

Deferred Tax Liability 838.9 823.1 875.1 932.1

Total Liabilities 16,152.1 16,591.0 18,891.3 20,161.1

Assets

Gross Block 15,640.9 17,808.7 20,828.8 23,328.8

Less: Acc Depreciation 6,112.2 6,924.9 7,783.1 8,677.4

Net Block 10,867.8 10,883.9 13,045.8 14,651.4

Capital WIP 2,268.2 1,520.1 1,500.0 1,000.0

Total Fixed Assets 13,136.0 12,404.0 14,545.8 15,651.4

Investments 1,342.5 6.0 6.0 6.0

Goodwill on consolidation 206.1 199.3 199.3 199.3

Inventory 2,945.4 3,484.1 3,680.2 3,920.2

Debtors 1,435.0 1,154.7 1,431.2 1,524.5

Loans and Advances 75.7 42.8 45.5 48.4

Other current assets 504.6 484.7 515.3 548.9

Cash 598.8 562.5 556.3 535.1

Total Current Assets 5,559.5 5,728.8 6,228.5 6,577.3

Creditors 2,447.1 2,248.3 2,555.7 2,722.4

Provisions 338.1 251.7 286.1 304.8

Total Current Liabilities 2,785.2 2,500.0 2,841.8 3,027.2

Net Current Assets 2,774.3 3,228.8 3,386.6 3,550.1

Application of Funds 16,152.1 16,591.0 18,891.3 20,161.1

Source: Company, ICICI Direct Research

Exhibit 18: Key ratios

(Year-end March) FY18 FY19 FY20E FY21E

Per share data (|)

EPS 12.7 11.9 14.8 16.2

Cash EPS 23.0 26.1 29.8 31.8

BV 170.9 175.5 186.1 197.8

DPS 3.0 3.3 3.5 3.8

Cash Per Share 10.5 9.8 9.7 9.4

Operating Ratios (%)

EBITDA Margin 11.1 11.2 11.4 11.9

PBT / Net sales 7.1 6.5 6.8 7.4

PAT Margin 4.9 4.7 4.5 4.7

Inventory days 72.4 72.5 72.0 72.0

Debtor days 35.3 24.0 28.0 28.0

Creditor days 60.2 46.8 50.0 50.0

Return Ratios (%)

RoE 7.4 8.3 8.0 8.2

RoCE 7.7 8.0 7.7 8.2

RoIC 8.5 8.0 7.7 8.0

Valuation Ratios (x)

P/E 11.9 10.3 10.1 9.3

EV / EBITDA 6.8 6.6 6.8 6.4

EV / Net Sales 0.8 0.7 0.8 0.8

Market Cap / Sales 0.6 0.5 0.5 0.4

Price to Book Value 0.9 0.9 0.8 0.8

Solvency Ratios

Debt/Equity 0.5 0.5 0.6 0.6

Current Ratio 1.8 2.1 2.0 2.0

Quick Ratio 0.7 0.7 0.7 0.7

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 10

ICICI Direct Research

Result Update | Apollo Tyres

Exhibit 19: ICICI Direct Research coverage universe (Auto & Auto Ancillary)

Sector / Company CMP M Cap

(|) TP(|) Rating (| Cr) FY19 FY20E FY21E FY19 FY20E FY21E FY19 FY20E FY21E FY19 FY20E FY21E FY19 FY20E FY21E

Amara Raja (AMARAJ) 650 590 Reduce 11108 28.3 31.1 33.8 22.3 20.3 18.6 11.0 9.7 8.7 21.2 21.0 20.5 14.5 14.3 14.0

Apollo Tyre (APOTYR) 150 145 Hold 8581 11.9 14.8 16.2 12.6 10.1 9.3 6.8 6.8 6.4 8.0 7.7 8.2 8.3 8.0 8.2

Ashok Leyland (ASHLEY) 68 70 Hold 19961 6.8 5.3 5.5 10.1 12.8 12.4 6.1 6.6 6.2 26.9 23.1 22.7 24.3 17.4 16.7

Bajaj Auto (BAAUTO) 2462 2360 Reduce 71243 161.6 160.5 168.7 15.4 15.5 14.8 11.0 10.3 9.4 21.0 19.2 25.3 19.9 19.1 18.1

Balkrishna Ind. (BALIND) 703 740 Hold 13590 40.5 40.9 45.3 19.2 19.0 17.2 11.8 10.6 9.1 20.4 19.0 19.3 16.7 19.0 19.3

Bharat Forge (BHAFOR) 421 535 Buy 32590 22.2 23.8 25.4 21.0 19.5 18.3 11.9 11.0 10.3 18.4 18.5 19.1 19.1 17.9 17.5

Bosch (MICO) 14378 15550 Reduce 43883 523.6 538.6 573.1 32.5 31.6 29.7 23.3 22.0 20.5 17.5 15.9 15.0 25.8 23.5 22.3

Eicher Motors (EICMOT) 16350 15875 Hold 44570 808.1 821.9 903.2 20.2 19.9 18.1 14.3 13.6 11.7 32.5 27.7 26.1 24.8 20.8 19.4

Escorts (ESCORT) 462 430 Reduce 4106 54.6 47.3 53.4 8.5 9.8 8.6 5.1 4.9 4.2 21.6 18.0 18.0 15.6 12.3 12.3

Exide Industries (EXIIND) 182 200 Reduce 15428 9.1 9.5 10.4 21.7 22.5 20.8 12.7 11.8 10.7 18.4 17.8 17.5 12.9 12.3 12.1

Hero Moto (HERHON) 2275 2200 Hold 45430 169.5 187.4 175.5 13.6 12.3 13.1 8.4 8.2 7.4 37.1 32.0 31.5 26.3 22.5 22.1

JK Tyre & Ind (JKIND) 70 100 Buy 1598 7.8 4.6 7.9 10.3 17.4 10.1 6.3 7.2 6.2 10.9 9.1 10.5 10.3 6.5 9.5

Mahindra CIE (MAHAUT) 174 230 Buy 6568 13.2 14.1 17.1 14.8 13.8 11.4 7.8 7.8 6.4 12.4 11.1 11.9 13.2 12.6 14.2

Maruti Suzuki (MARUTI) 5523 5000 Reduce 166837 248.3 221.2 250.0 22.8 25.5 22.6 12.3 13.6 11.6 16.3 12.0 13.0 16.3 13.4 13.9

Motherson (MOTSUM) 105 125 Hold 33221 5.1 5.0 6.5 23.5 23.9 18.4 8.5 8.5 6.6 13.5 12.3 16.0 14.7 13.2 15.5

Tata Motors (TELCO) 135 160 Hold 50934 -84.6 9.3 21.4 -1.8 16.1 7.0 3.9 3.6 3.1 5.4 9.1 11.3 7.1 9.8 15.4

Wabco India (WABTVS) 6089 6510 Hold 11549 148.8 157.7 178.3 41.7 39.3 34.8 26.6 24.5 21.5 15.9 14.5 14.3 23.0 21.4 21.0

RoE (%)EPS (|) P/E (x) EV/EBITDA (x) RoCE (%)

Source: Reuters, ICICI Direct Research

ICICI Securities | Retail Research 11

ICICI Direct Research

Result Update | Apollo Tyres

RATING RATIONALE

ICICI Direct endeavors to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorizes them as Buy, Hold,

Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined

as the analysts' valuation for a stock

Buy: >15%

Hold: -5% to 15%;

Reduce: -15% to -5%;

Sell: <-15%

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 12

ICICI Direct Research

Result Update | Apollo Tyres

ANALYST CERTIFICATION

I/We, Shashank Kanodia, CFA, MBA (Capital Markets), and Jaimin Desai, CA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect

our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. It is also confirmed that

above mentioned Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies

mentioned in the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a SEBI registered

Research Analyst with SEBI Registration Number – INH000000990. ICICI Securities Limited SEBI Registration is INZ000183631 for stock broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank

and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on

www.icicibank.com

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship

with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the

securities or derivatives of any companies that the analysts cover.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions, trading volume etc as opposed to focusing on a company's fundamentals and, as

such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical Research Reports.

Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions expressed in this document may or may

not match or may be contrary with the views, estimates, rating, target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected

recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would

endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI

Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in

circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein

is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers

simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting

and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who

must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient.

The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks

associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-

managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other

benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of

interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of

the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this

report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in

all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.