Embed Size (px)

Citation preview

Annual Results 2010Annual Results 2010China Telecom Corporation Limited22 March 2011 | www.chinatelecom-h.com

Forward-Looking Statements

Certain statements contained in this document may be viewed as “forward-

looking statements” within the meaning of Section 27A of the U.S. Securities

Act of 1933 (as amended) and Section 21E of the U.S. Securities Exchange Act

of 1934 (as amended). Such forward-looking statements are subject to known

and unknown risks, uncertainties and other factors, which may cause the

actual performance, financial condition or results of operations of China

Telecom Corporation Limited (the “Company”) to be materially different from

any future performance, financial condition or results of operations implied by

such forward-looking statements. In addition, we do not intend to update

these forward-looking statements. Further information regarding these risks,

uncertainties and other factors is included in the Company’s most recent

Annual Report on Form 20-F filed with the U.S. Securities and Exchange

Commission (the “SEC”) and in the Company’s other filings with the SEC.

2

3

Presentation by

Chairman & CEO

President & COO

Executive Vice President & CFO

Executive Vice President

4

Agenda

Overview

Business Review

Financial Performance

1

2

3

OverviewOverview

6

Highlights

Effective integrated operation driving remarkable earnings recovery

Accelerate strategic broadband deployment to enhance sustainable core competence

Rapid mobile growth with scale benefits emerging

To strengthen differentiation development leveraging “Mobile Internet” to create more value

7

Solid Results

Adjusted Results 2009 2010 Change

Operating Revenue (RMB Mil) 208,219 219,367 5.4%

EBITDA (RMB Mil) 82,133 88,495 7.7%

EBITDA Margin 39.4% 40.3% 0.9pp

Net Profit (RMB Mil) 13,271 15,262 15.0%

EPS (RMB) 0.164 0.189 15.0%

Free Cash Flow (RMB Mil) 31,159 27,107 -13.0%

2009.12 2010.12 Change

Access Lines in Services (Mil) 188.56 175.05 -13.51

Mobile Subs (Mil) 56.09 90.52 34.43

Including: 3G Subs (Mil) 4.07 12.29 8.22

Wireline Broadband Subs (Mil) 53.46 63.48 10.02

Notes: Unless otherwise stated in this presentation1. All financial data were adjusted to exclude Upfront Connection Fees2. EBITDA was calculated before CDMA Network Leasing Fees (2009: RMB8,383 mil; 2010: RMB13,320 mil) to enhance comparability3. Net Profit represented profit attributable to equity holders of the Company4. Free Cash Flow = EBITDA – CDMA Network Leasing Fees – CAPEX – Income Tax Expenses

8

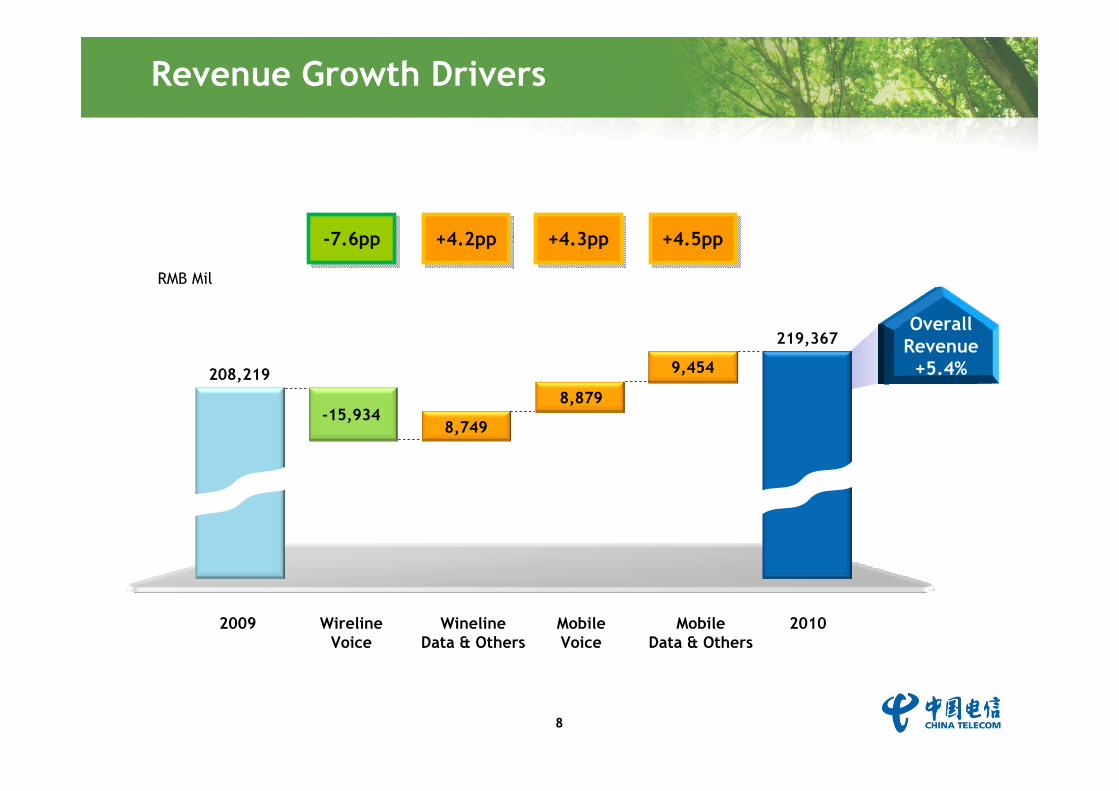

Revenue Growth Drivers

WirelineVoice

2009 WinelineData & Others

Mobile Voice

Mobile Data & Others

2010

-7.6pp +4.2pp +4.3pp +4.5pp

208,219

-15,934

RMB Mil

8,749

8,879

9,454

Overall Revenue

+5.4%

219,367

9

Strategic Transformation OptimizingRevenue Structure

Mobile business as a key growth driver:

• Revenue 51.5% yoy

• Revenue/total revenue: 24.6% ( 7.5pp yoy)

Robust growth across strategic businesses (mobile, wireline data & others):

• Revenue 20.9% yoy

• Revenue/total revenue:71.5% ( 9.2pp yoy)

Wireline operating risk further alleviated:

• Wireline voice revenue as a % of total revenue lowered to 28.5%

• PAS revenue only 2.1% of total revenue

Revenue Structure

2009

37.7%

2010

45.2%

9.6%7.5%

28.5%

46.9%

13.2%

11.4%Mobile Data &

Others

Mobile Voice

Wireline Data & Others

Wireline Voice

10

Rapid Mobile Expansion with Robust Quality

Mobile Subs Market Share

Mobile subs base expanding rapidly

• 2010 subs net add: 34.43 mil

• Subs base >90mil & market share >10%

• 3G subs base: 12.29 mil (13.6% of subs base)

Revenue & subs base growing in tandem (mobile ARPU of RMB54.2)

Invigorated value chain

• CDMA terminals: ~800 models

3G terminals: ~300 models ( 200 yoy)

3G terminals ASP 50% yoy

• Open channel terminal sales: 61% ( 9pp yoy)

• Open channel point-of-sales: ~580k ( 40k yoy)

RMB Mil

2009

30,003

2010

Service Revenue

47,722

Subscribers

3G Subs

Mil

56.094.07

2009

27.91

2008

90.5212.29

2010

4.5%7.7%

10.8%

11

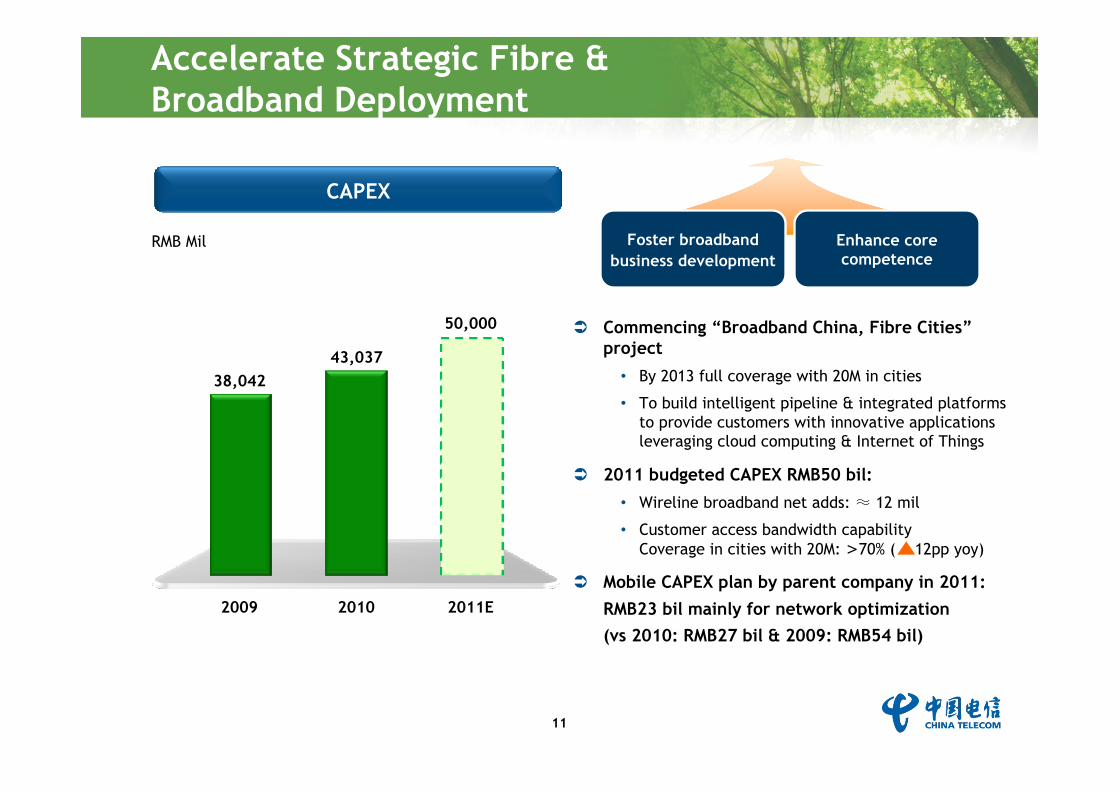

Commencing “Broadband China, Fibre Cities”project

• By 2013 full coverage with 20M in cities

• To build intelligent pipeline & integrated platforms to provide customers with innovative applications leveraging cloud computing & Internet of Things

2011 budgeted CAPEX RMB50 bil:

• Wireline broadband net adds: ≈ 12 mil

• Customer access bandwidth capabilityCoverage in cities with 20M: >70% ( 12pp yoy)

Mobile CAPEX plan by parent company in 2011:RMB23 bil mainly for network optimization(vs 2010: RMB27 bil & 2009: RMB54 bil)

Accelerate Strategic Fibre & Broadband Deployment

RMB Mil

2010 2011E2009

43,037

50,000

38,042

Foster broadband business development

Enhance core competence

CAPEX

12

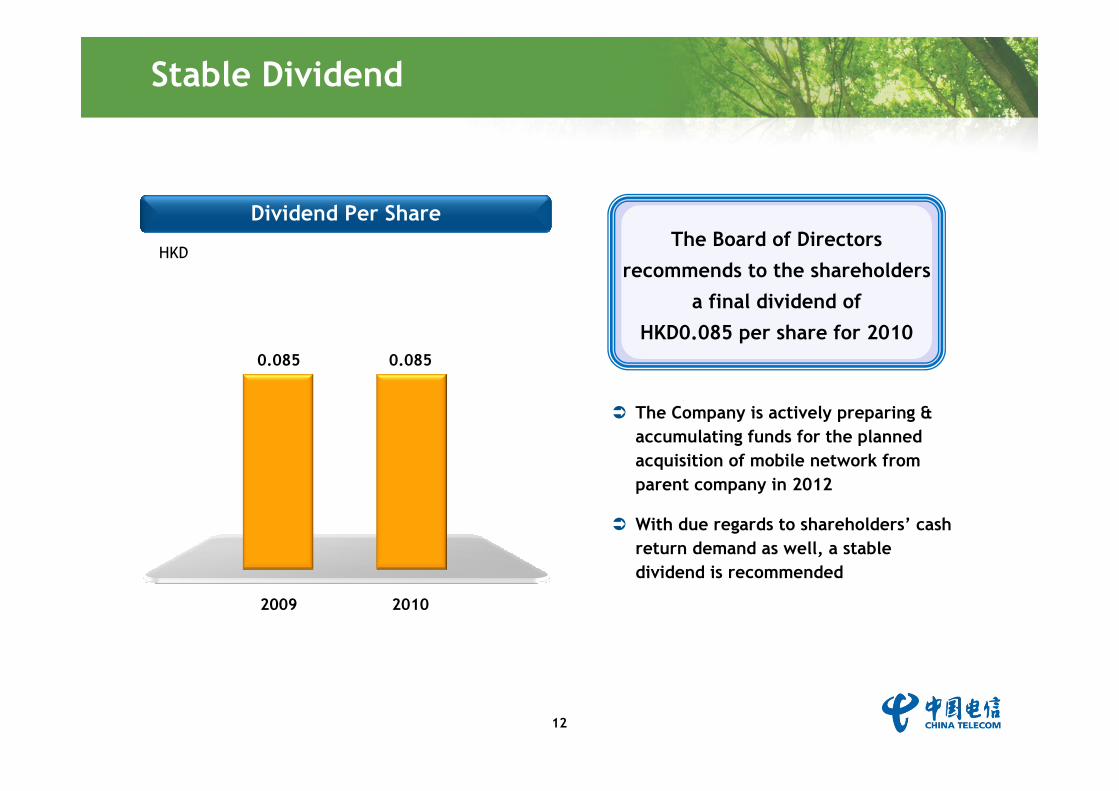

Stable Dividend

HKD

2009 2010

0.085 0.085

Dividend Per Share

The Company is actively preparing & accumulating funds for the planned acquisition of mobile network from parent company in 2012

With due regards to shareholders’ cash return demand as well, a stable dividend is recommended

The Board of Directors recommends to the shareholders

a final dividend of HKD0.085 per share for 2010

13

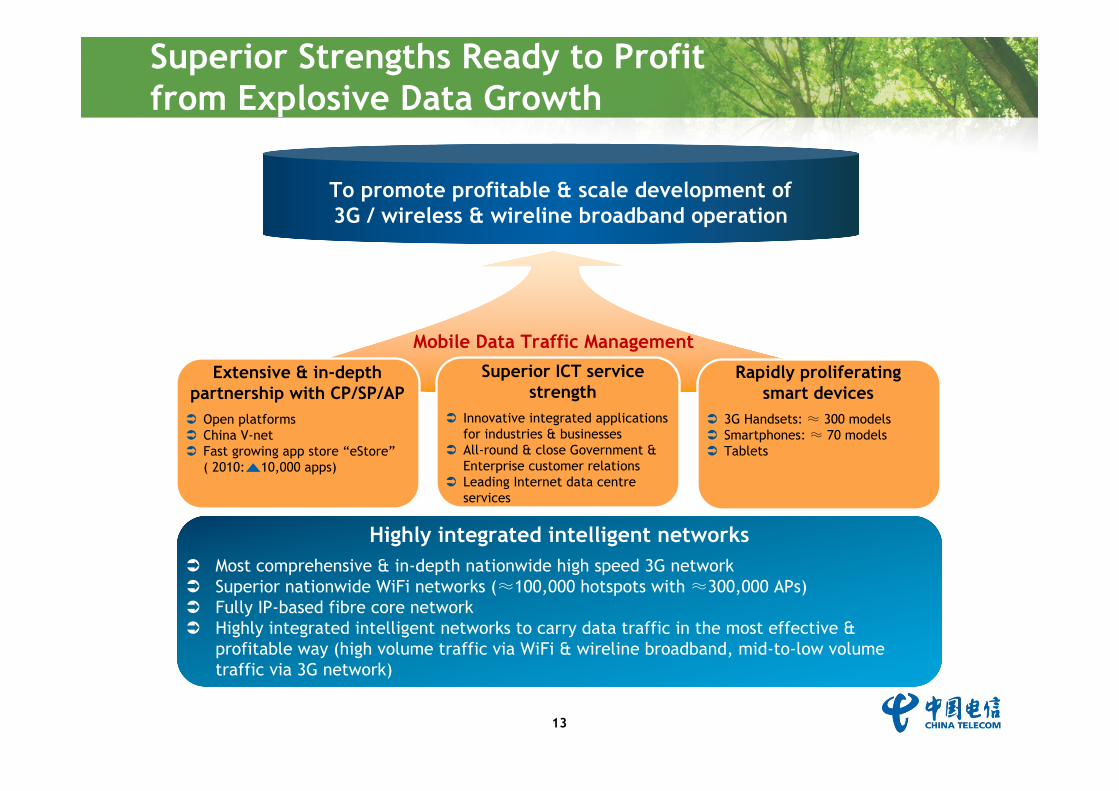

Superior Strengths Ready to Profitfrom Explosive Data Growth

Highly integrated intelligent networksMost comprehensive & in-depth nationwide high speed 3G networkSuperior nationwide WiFi networks (≈100,000 hotspots with ≈300,000 APs)Fully IP-based fibre core networkHighly integrated intelligent networks to carry data traffic in the most effective & profitable way (high volume traffic via WiFi & wireline broadband, mid-to-low volume traffic via 3G network)

Extensive & in-depth partnership with CP/SP/AP

Open platformsChina V-netFast growing app store “eStore”( 2010: 10,000 apps)

Superior ICT service strength

Innovative integrated applications for industries & businessesAll-round & close Government & Enterprise customer relationsLeading Internet data centre services

Rapidly proliferating smart devices

3G Handsets: ≈ 300 modelsSmartphones: ≈ 70 modelsTablets

To promote profitable & scale development of 3G / wireless & wireline broadband operation

Mobile Data Traffic Management

14

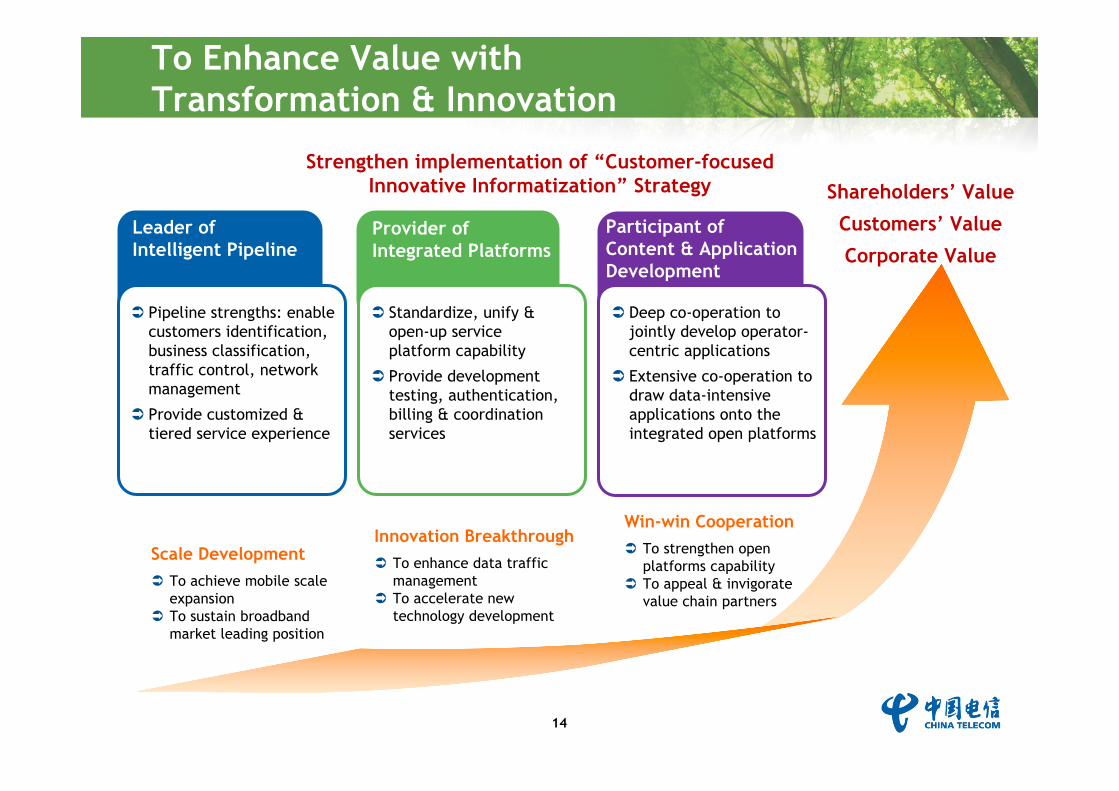

To Enhance Value withTransformation & Innovation

Pipeline strengths: enable customers identification, business classification, traffic control, network management

Provide customized & tiered service experience

Standardize, unify & open-up service platform capability

Provide development testing, authentication, billing & coordination services

Deep co-operation to jointly develop operator-centric applications

Extensive co-operation to draw data-intensive applications onto the integrated open platforms

Leader of Intelligent Pipeline

Provider of Integrated Platforms

Participant of Content & Application Development

Scale DevelopmentTo achieve mobile scale expansionTo sustain broadband market leading position

Innovation BreakthroughTo enhance data traffic managementTo accelerate new technology development

Win-win CooperationTo strengthen open platforms capabilityTo appeal & invigorate value chain partners

Shareholders’ Value

Customers’ Value

Corporate Value

Strengthen implementation of “Customer-focused Innovative Informatization” Strategy

Business Business ReviewReview

16

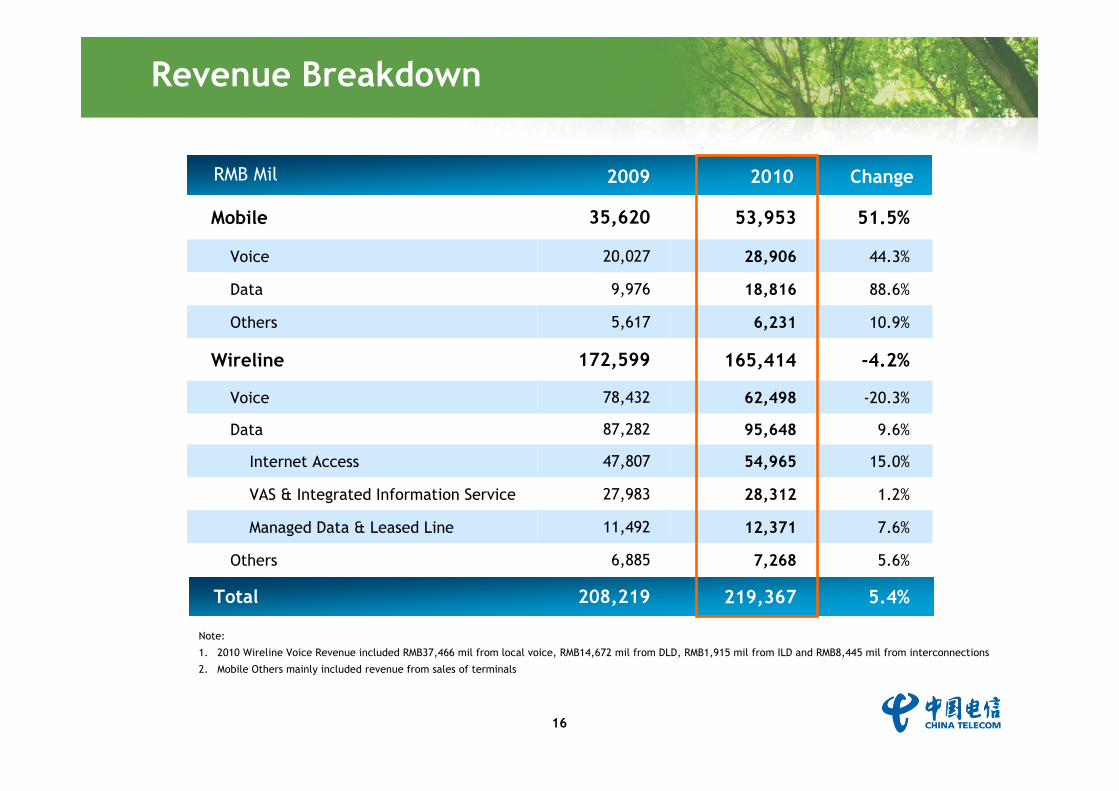

Revenue Breakdown

RMB Mil 2009 2010 Change

Mobile 35,620 53,953 51.5%

Voice 20,027 28,906 44.3%

Data 9,976 18,816 88.6%

Others 5,617 6,231 10.9%

Wireline 172,599 165,414 -4.2%

Voice 78,432 62,498 -20.3%

Data 87,282 95,648 9.6%

Internet Access 47,807 54,965 15.0%

VAS & Integrated Information Service 27,983 28,312 1.2%

Managed Data & Leased Line 11,492 12,371 7.6%

Others 6,885 7,268 5.6%

Total 208,219 219,367 5.4%

Note:

1. 2010 Wireline Voice Revenue included RMB37,466 mil from local voice, RMB14,672 mil from DLD, RMB1,915 mil from ILD and RMB8,445 mil from interconnections

2. Mobile Others mainly included revenue from sales of terminals

17

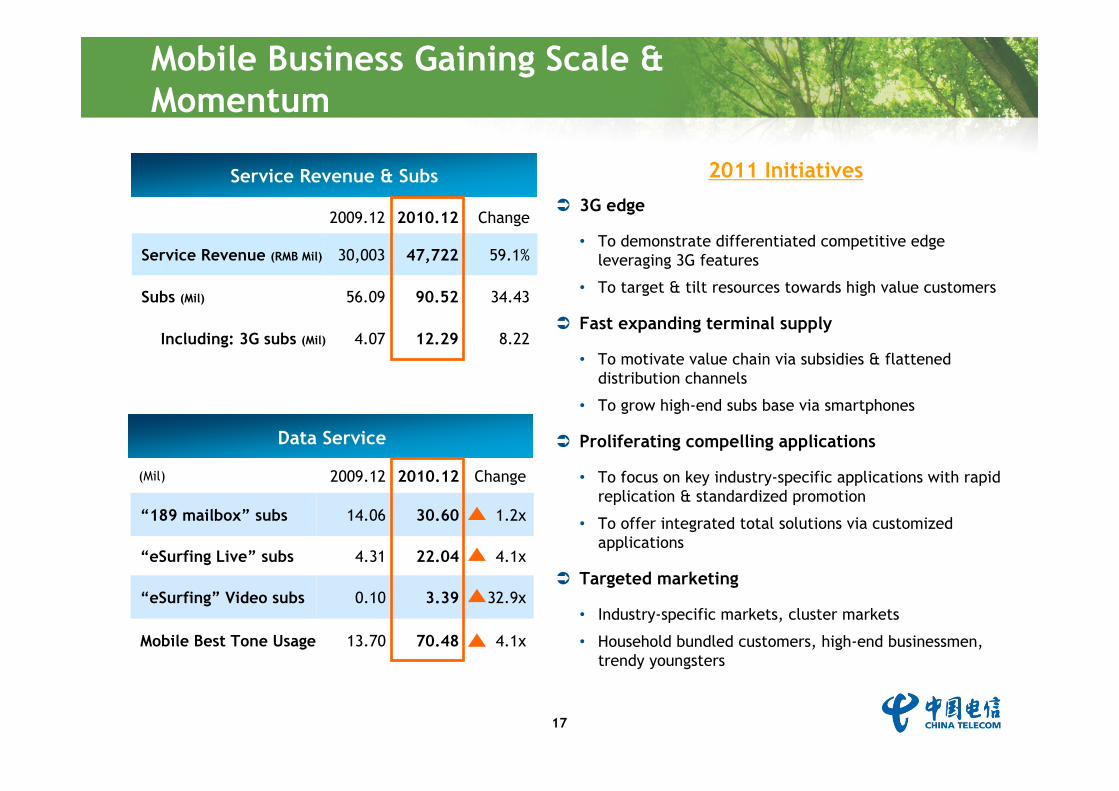

Mobile Business Gaining Scale & Momentum

2009.12 2010.12 Change

Service Revenue (RMB Mil) 30,003 47,722 59.1%

Subs (Mil) 56.09 90.52 34.43

Including: 3G subs (Mil) 4.07 12.29 8.22

Data Service

(Mil) 2009.12 2010.12 Change

“189 mailbox” subs 14.06 30.60 1.2x

“eSurfing Live” subs 4.31 22.04 4.1x

“eSurfing” Video subs 0.10 3.39 32.9x

Mobile Best Tone Usage 13.70 70.48 4.1x

3G edge

• To demonstrate differentiated competitive edge leveraging 3G features

• To target & tilt resources towards high value customers

Fast expanding terminal supply

• To motivate value chain via subsidies & flattened distribution channels

• To grow high-end subs base via smartphones

Proliferating compelling applications

• To focus on key industry-specific applications with rapid replication & standardized promotion

• To offer integrated total solutions via customized applications

Targeted marketing

• Industry-specific markets, cluster markets

• Household bundled customers, high-end businessmen, trendy youngsters

Service Revenue & Subs 2011 Initiatives

18

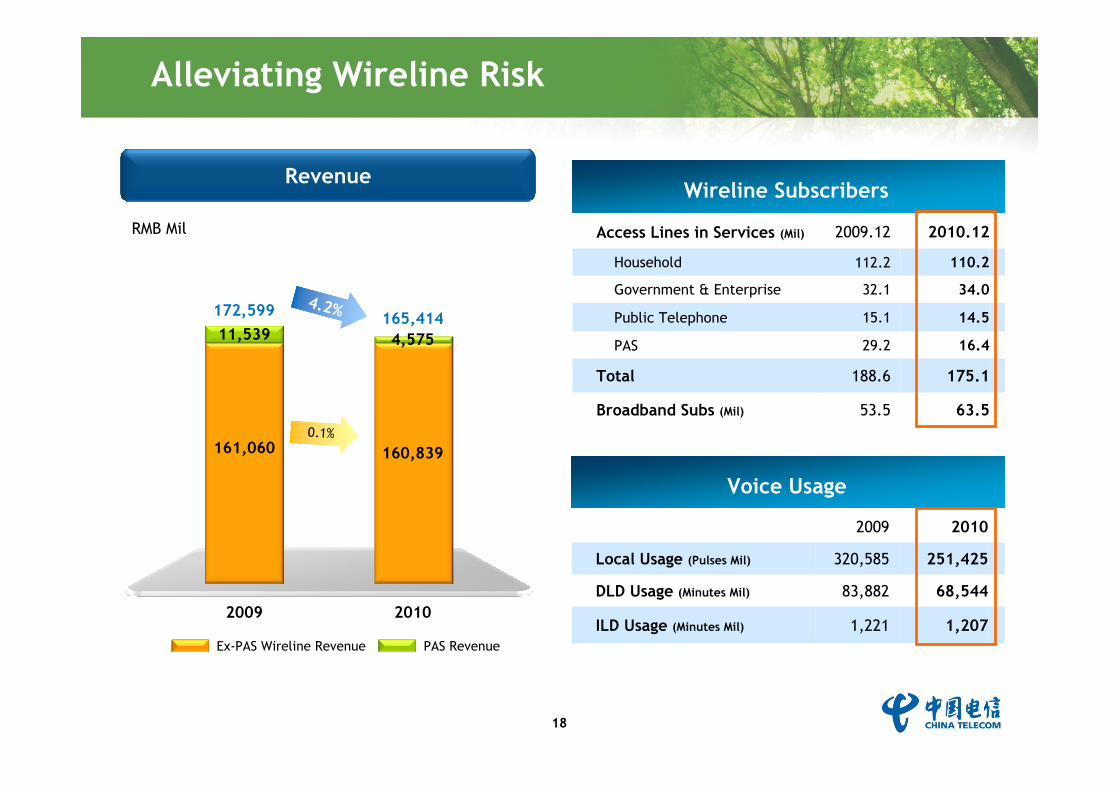

Alleviating Wireline Risk

Wireline Subscribers

2009

Revenue

RMB Mil

172,599 165,414

Ex-PAS Wireline Revenue PAS Revenue

Access Lines in Services (Mil) 2009.12 2010.12

Household 112.2 110.2

Government & Enterprise 32.1 34.0

Public Telephone 15.1 14.5

PAS 29.2 16.4

Total 188.6 175.1

Broadband Subs (Mil) 53.5 63.5

Voice Usage

2009 2010

Local Usage (Pulses Mil) 320,585 251,425

DLD Usage (Minutes Mil) 83,882 68,544

ILD Usage (Minutes Mil) 1,221 1,207

11,539

161,060

4,575

160,8390.1%

4.2%

2010

19

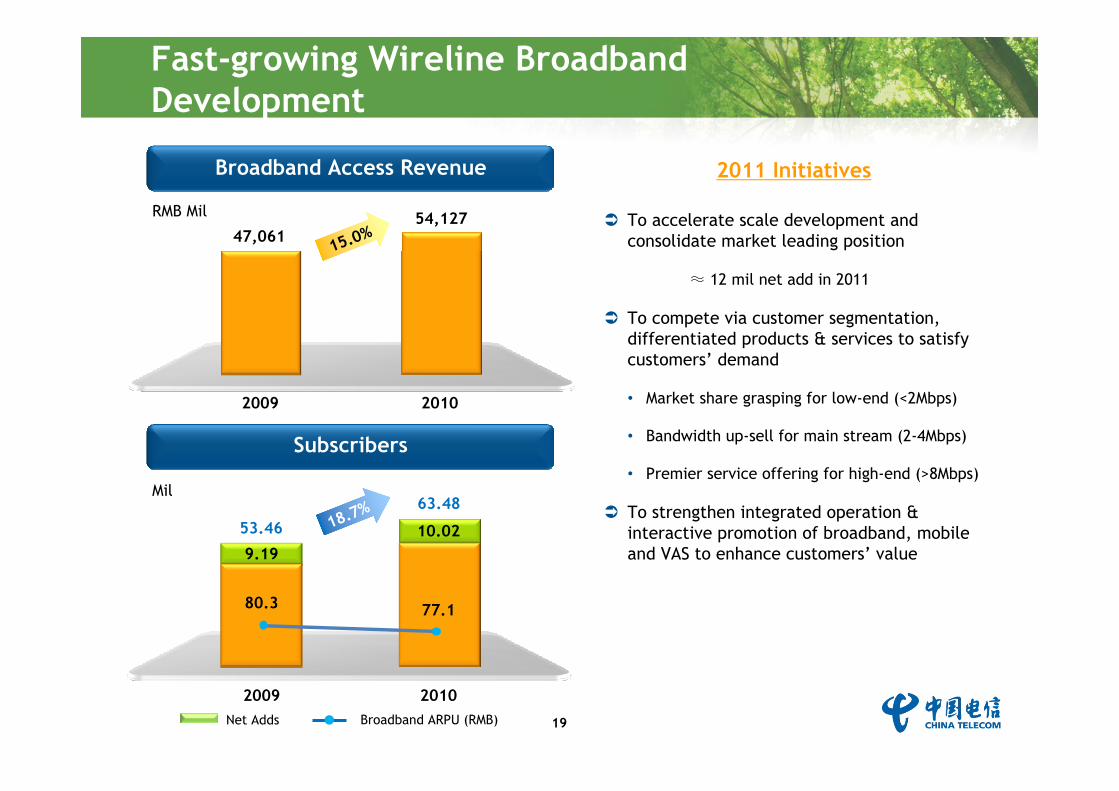

Fast-growing Wireline Broadband Development

Broadband Access Revenue

To accelerate scale development and consolidate market leading position

≈ 12 mil net add in 2011

To compete via customer segmentation, differentiated products & services to satisfy customers’ demand

• Market share grasping for low-end (<2Mbps)

• Bandwidth up-sell for main stream (2-4Mbps)

• Premier service offering for high-end (>8Mbps)

To strengthen integrated operation & interactive promotion of broadband, mobile and VAS to enhance customers’ value

RMB Mil

2009

47,06154,127

2010

Mil

2009

53.46

2010

Subscribers

63.48

9.1910.02

80.3 77.1

Broadband ARPU (RMB)Net Adds

15.0%

18.7%

2011 Initiatives

20

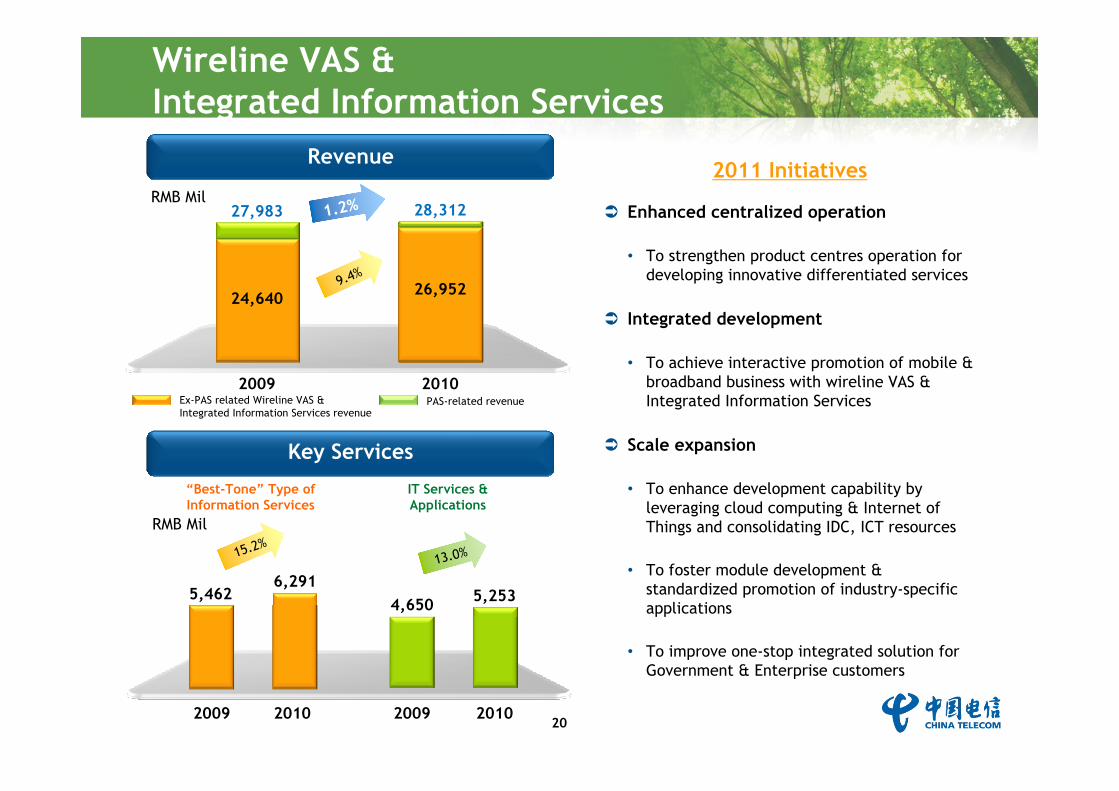

Wireline VAS & Integrated Information Services

15.2%

Revenue

Enhanced centralized operation

• To strengthen product centres operation for developing innovative differentiated services

Integrated development

• To achieve interactive promotion of mobile & broadband business with wireline VAS & Integrated Information Services

Scale expansion

• To enhance development capability by leveraging cloud computing & Internet of Things and consolidating IDC, ICT resources

• To foster module development & standardized promotion of industry-specific applications

• To improve one-stop integrated solution for Government & Enterprise customers

RMB Mil

2009 2010

Key Services

6,2915,462

RMB Mil

2009

27,983

2010

24,6409.4%

28,312

26,952

Ex-PAS related Wireline VAS & Integrated Information Services revenue

PAS-related revenue

13.0%

2009 2010

5,2534,650

IT Services & Applications

“Best-Tone” Type of Information Services

1.2%

2011 Initiatives

21

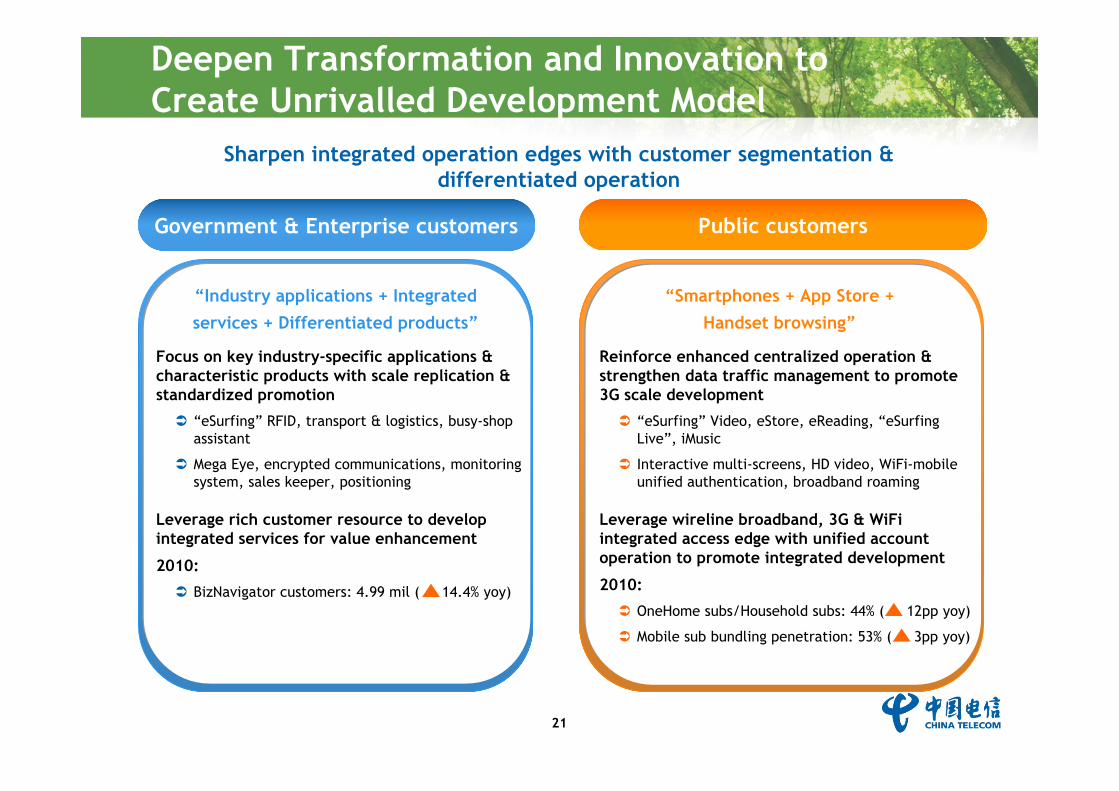

Deepen Transformation and Innovation to Create Unrivalled Development Model

Sharpen integrated operation edges with customer segmentation & differentiated operation

“Smartphones + App Store + Handset browsing”

Focus on key industry-specific applications & characteristic products with scale replication & standardized promotion

“eSurfing” RFID, transport & logistics, busy-shop assistant

Mega Eye, encrypted communications, monitoring system, sales keeper, positioning

Leverage rich customer resource to develop integrated services for value enhancement

2010:

BizNavigator customers: 4.99 mil ( 14.4% yoy)

Reinforce enhanced centralized operation & strengthen data traffic management to promote 3G scale development

“eSurfing” Video, eStore, eReading, “eSurfingLive”, iMusic

Interactive multi-screens, HD video, WiFi-mobile unified authentication, broadband roaming

Leverage wireline broadband, 3G & WiFiintegrated access edge with unified account operation to promote integrated development

2010:

OneHome subs/Household subs: 44% ( 12pp yoy)

Mobile sub bundling penetration: 53% ( 3pp yoy)

Government & Enterprise customers Public customers

“Industry applications + Integrated services + Differentiated products”

Financial Financial PerformancePerformance

23

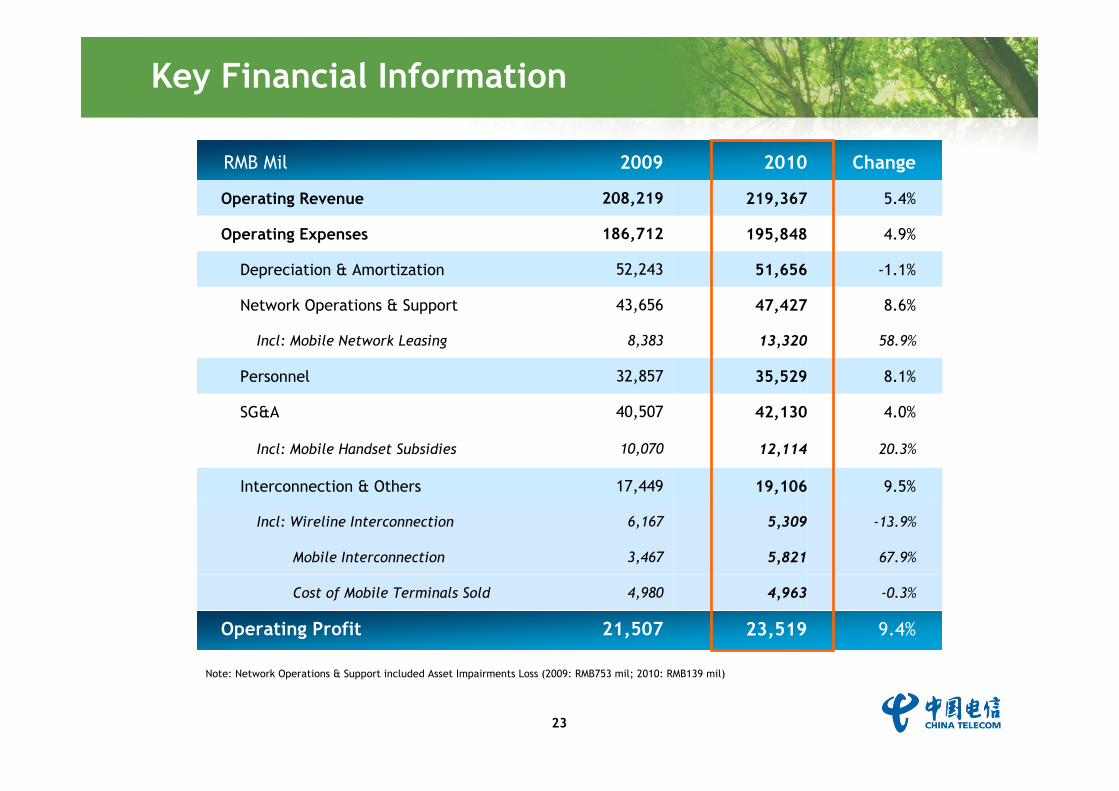

Key Financial Information

RMB Mil 2009 2010 Change

Operating Revenue 208,219 219,367 5.4%

Operating Expenses 186,712 195,848 4.9%

Depreciation & Amortization 52,243 51,656 -1.1%

Network Operations & Support 43,656 47,427 8.6%

Incl: Mobile Network Leasing 8,383 13,320 58.9%

Personnel 32,857 35,529 8.1%

SG&A 40,507 42,130 4.0%

Incl: Mobile Handset Subsidies 10,070 12,114 20.3%

Interconnection & Others 17,449 19,106 9.5%

Incl: Wireline Interconnection 6,167 5,309 -13.9%

Mobile Interconnection 3,467 5,821 67.9%

Cost of Mobile Terminals Sold 4,980 4,963 -0.3%

Operating Profit 21,507 23,519 9.4%

Note: Network Operations & Support included Asset Impairments Loss (2009: RMB753 mil; 2010: RMB139 mil)

24

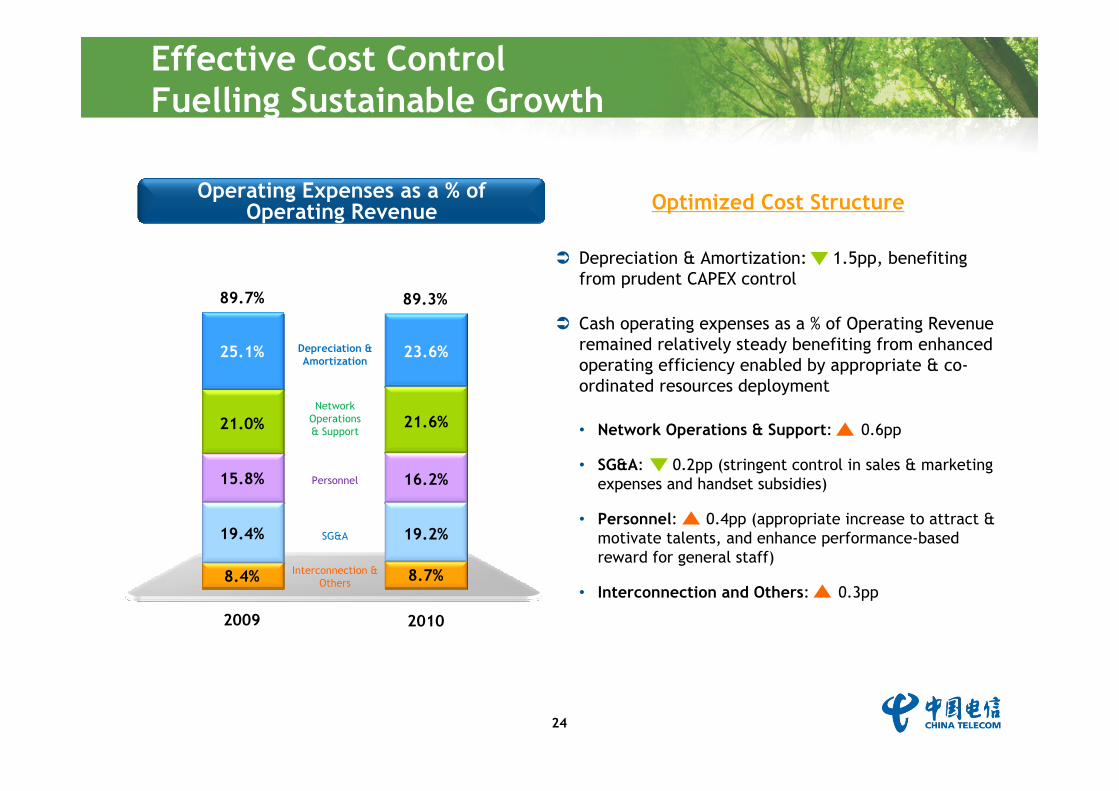

Effective Cost Control Fuelling Sustainable Growth

2009

8.4%

2010

Operating Expenses as a % of Operating Revenue

21.0%

15.8%

25.1%

89.7%

19.4%

8.7%

21.6%

16.2%

23.6%

89.3%

19.2%

Optimized Cost Structure

Network Operations & Support

Depreciation & Amortization

Interconnection & Others

SG&A

Personnel

Depreciation & Amortization: 1.5pp, benefiting from prudent CAPEX control

Cash operating expenses as a % of Operating Revenue remained relatively steady benefiting from enhanced operating efficiency enabled by appropriate & co-ordinated resources deployment

• Network Operations & Support: 0.6pp

• SG&A: 0.2pp (stringent control in sales & marketing expenses and handset subsidies)

• Personnel: 0.4pp (appropriate increase to attract & motivate talents, and enhance performance-based reward for general staff)

• Interconnection and Others: 0.3pp

25

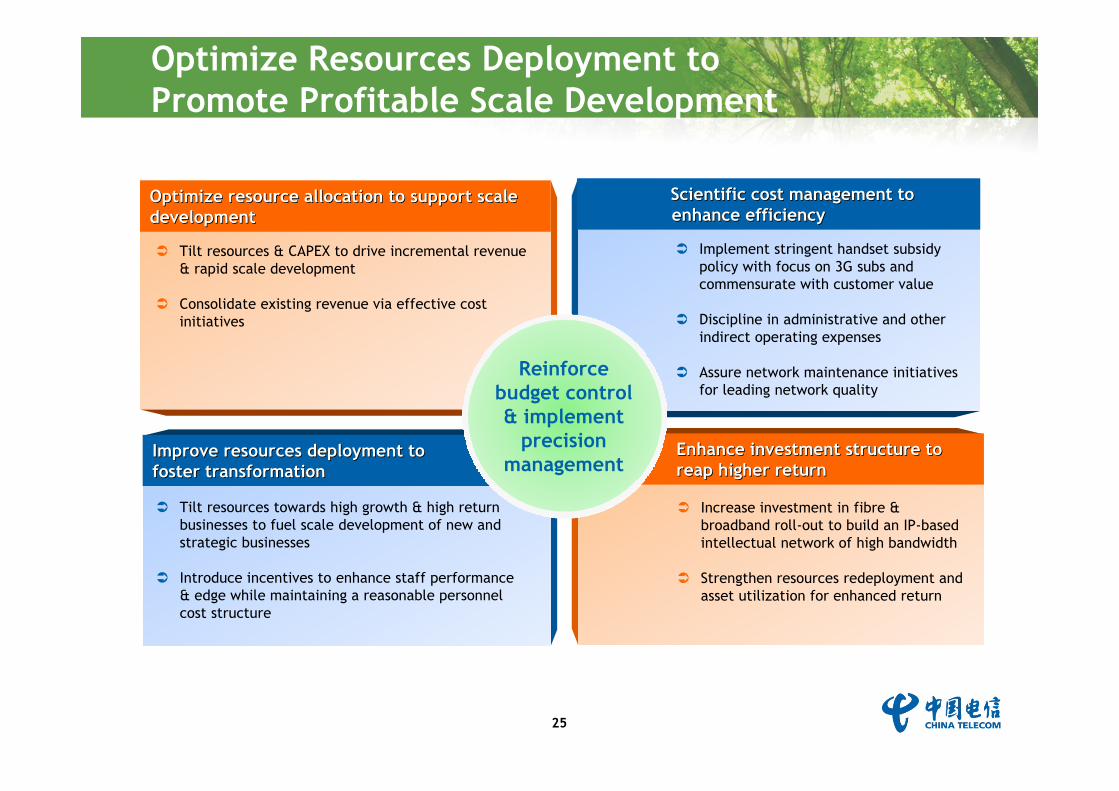

Optimize Resources Deployment to Promote Profitable Scale Development

Optimize resource allocation to support scale Optimize resource allocation to support scale developmentdevelopment

Scientific cost management to Scientific cost management to enhance efficiencyenhance efficiency

Improve resources deployment to Improve resources deployment to foster transformationfoster transformation

Enhance investment structure to Enhance investment structure to reap higher returnreap higher return

Tilt resources towards high growth & high return businesses to fuel scale development of new and strategic businesses

Introduce incentives to enhance staff performance & edge while maintaining a reasonable personnel cost structure

Tilt resources & CAPEX to drive incremental revenue & rapid scale development

Consolidate existing revenue via effective cost initiatives

Increase investment in fibre & broadband roll-out to build an IP-based intellectual network of high bandwidth

Strengthen resources redeployment and asset utilization for enhanced return

Reinforce budget control & implement

precision management

Implement stringent handset subsidy policy with focus on 3G subs and commensurate with customer value

Discipline in administrative and other indirect operating expenses

Assure network maintenance initiatives for leading network quality

26

Strictly control investment in traditional wireline business and increase investment in transformation business to enhance network servicing capability

Speed up fibre & broadband roll-out to maintain edge and enhance sustainable development:

Broadband & Internet 10.1pp yoy

VAS & Integrated Information Services 3.9pp yoy

IT & Support 0.8pp yoy

Wireline Voice 1.8pp yoy

Infrastructure & Others 3.6pp yoy

17.9m broadband access capacity in 2010

Customer access bandwidth capability:

Coverage in cities

Enhanced CAPEX Structure Supporting Strategic Transformation

CAPEX Structure

Note:1. Broadband & Internet included data network, transmission network, broadband access equipment & cable2. VAS & Integrated Information Services included VAS platform & ICT3. IT & Support included enterprise informatization services4. Wireline Voice included switches, voice access equipment & cable5. Infrastructure & Others included air-conditioning supply facilities, conduits, buildings, minor purchases, R&D, etc.

4M:

20M:

98%

58% 22pp yoy

3pp yoy

2009

54.1%

2010

20.2%

17.8%

3.7%

64.2%

16.6%

13.9%

2.9%IT & Support

VAS & Integrated Information Services

Broadband & Internet

Wireline Voice4.2% 2.4%

Infrastructure & Others

27

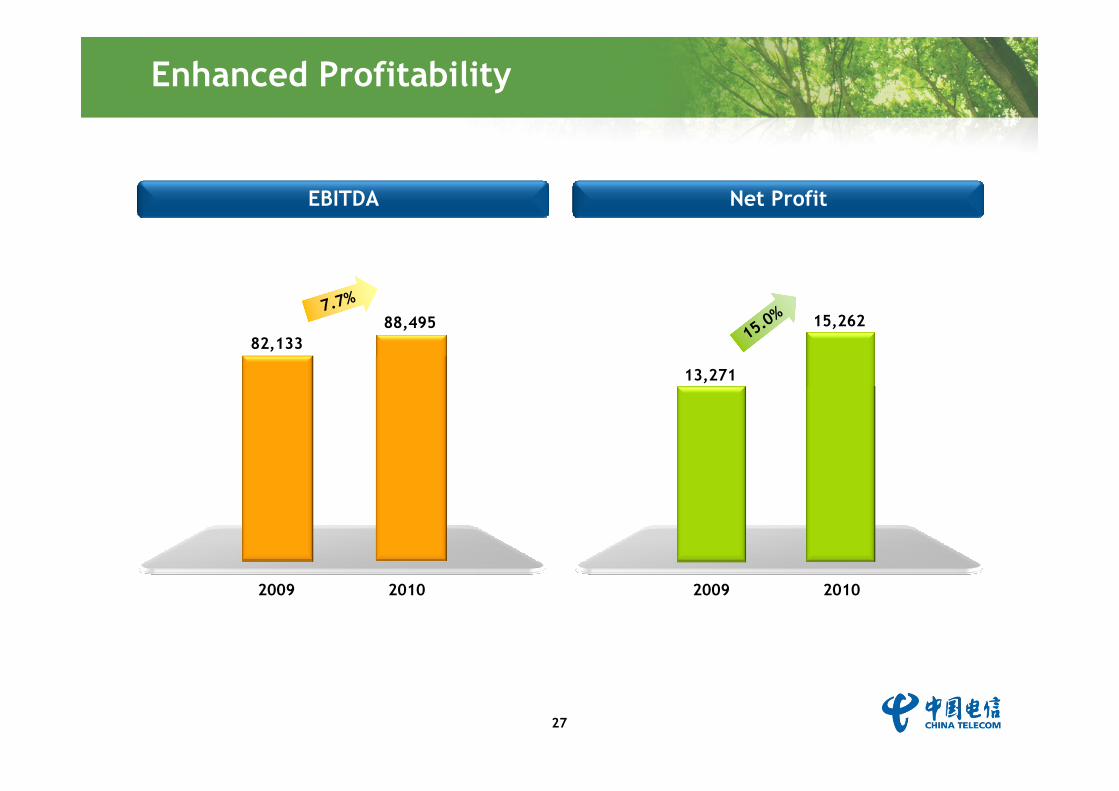

Enhanced Profitability

2009 2010

88,495

EBITDA

2009 2010

Net Profit

13,271

15,26282,133

7.7%

15.0%

28

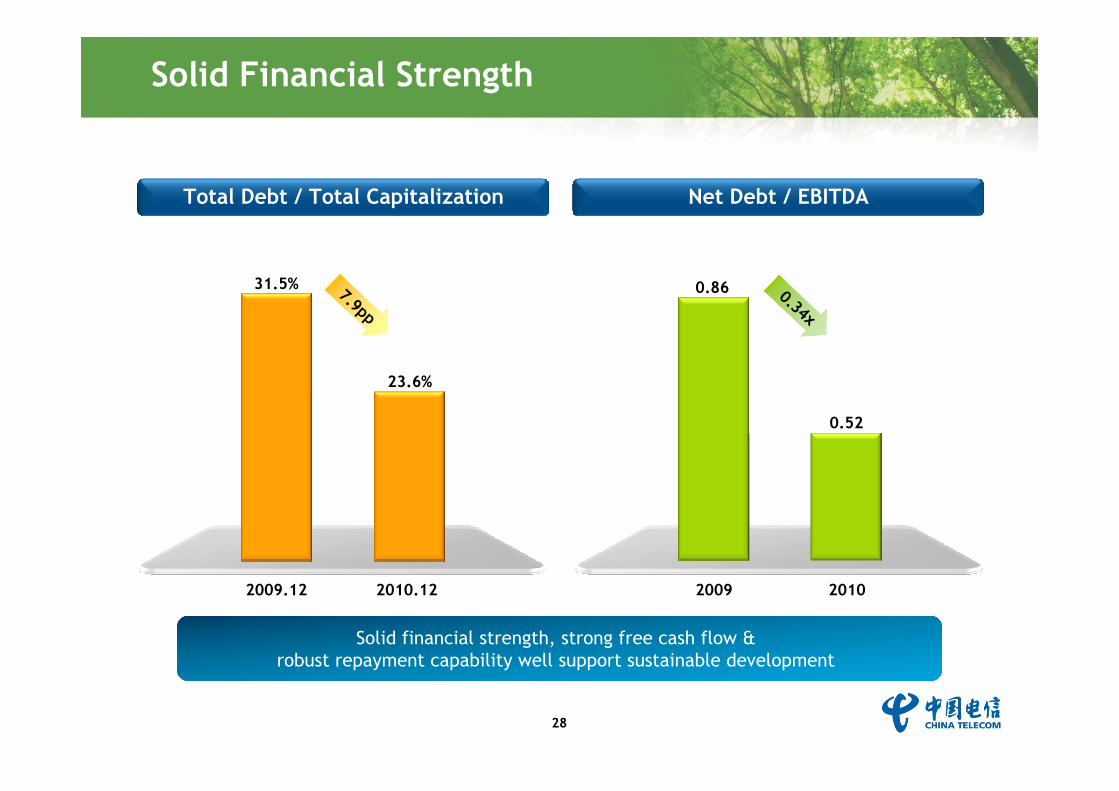

2009.12 2010.12 2009 2010

Solid Financial Strength

23.6%

Total Debt / Total Capitalization Net Debt / EBITDA

0.86

0.52

31.5%

Solid financial strength, strong free cash flow & robust repayment capability well support sustainable development

7.9pp0.34x

29

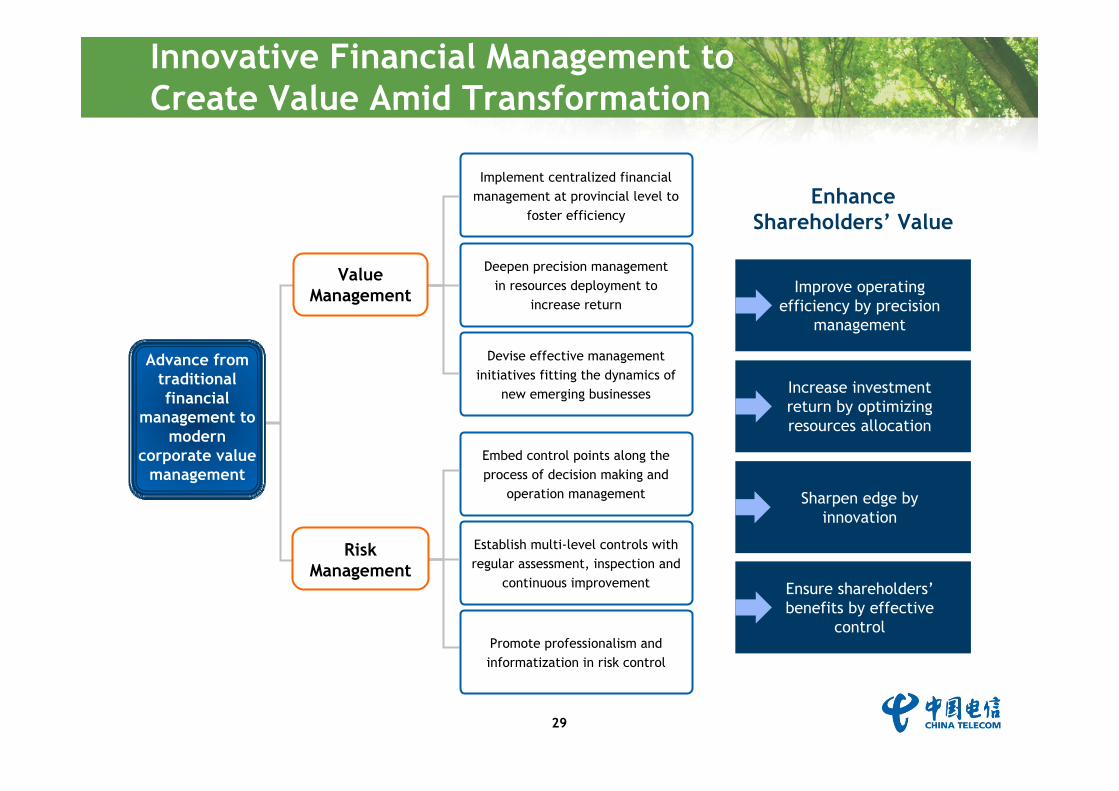

Innovative Financial Management to Create Value Amid Transformation

Advance from traditional financial

management to modern

corporate value management

Value Management

Implement centralized financial management at provincial level to

foster efficiency

Deepen precision management in resources deployment to

increase return

Devise effective management initiatives fitting the dynamics of

new emerging businesses

Risk Management

Embed control points along the process of decision making and

operation management

Establish multi-level controls with regular assessment, inspection and

continuous improvement

Promote professionalism and informatization in risk control

Enhance Shareholders’ Value

Improve operating efficiency by precision

management

Ensure shareholders’benefits by effective

control

Sharpen edge by innovation

Increase investment return by optimizing resources allocation

Thank You!Thank You!

For further information & enquiries, please contact our Investor Relations Department at [email protected]

31

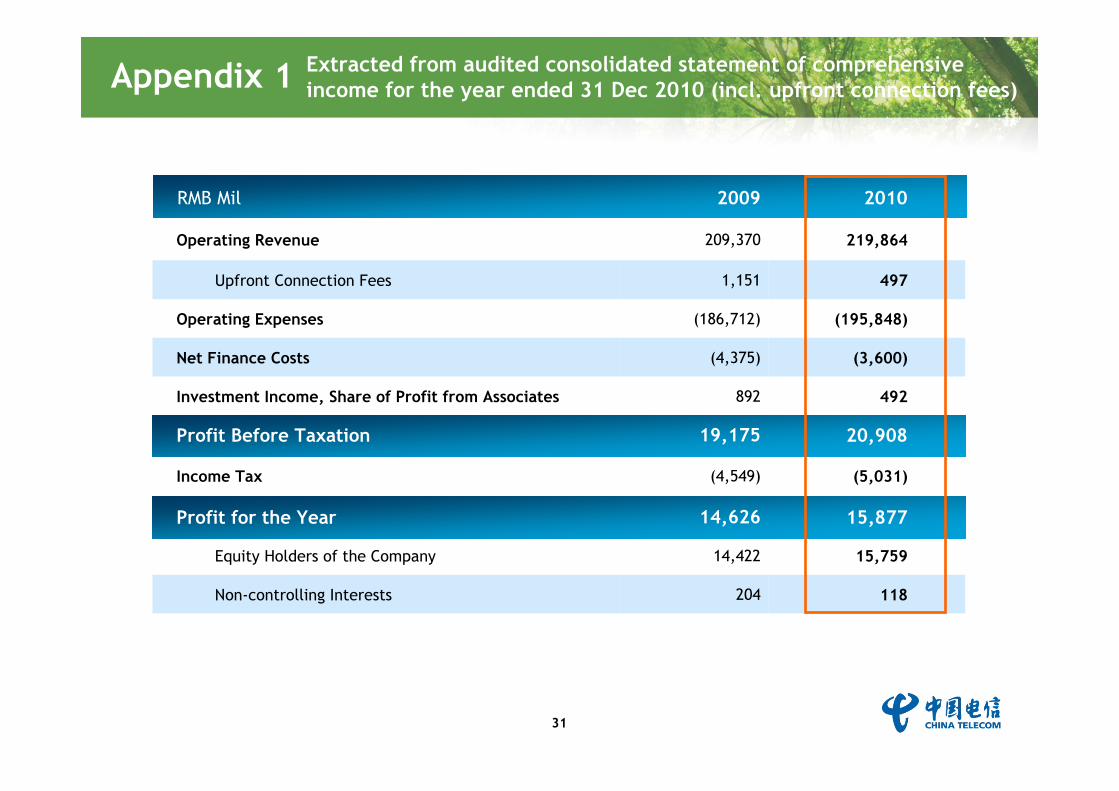

Appendix 1

RMB Mil 2009 2010

Operating Revenue 209,370 219,864

Upfront Connection Fees 1,151 497

Operating Expenses (186,712) (195,848)

Net Finance Costs (4,375) (3,600)

Investment Income, Share of Profit from Associates 892 492

Profit Before Taxation 19,175 20,908

Income Tax (4,549) (5,031)

Profit for the Year 14,626 15,877

Equity Holders of the Company 14,422 15,759

Non-controlling Interests 204 118

Extracted from audited consolidated statement of comprehensive income for the year ended 31 Dec 2010 (incl. upfront connection fees)

32

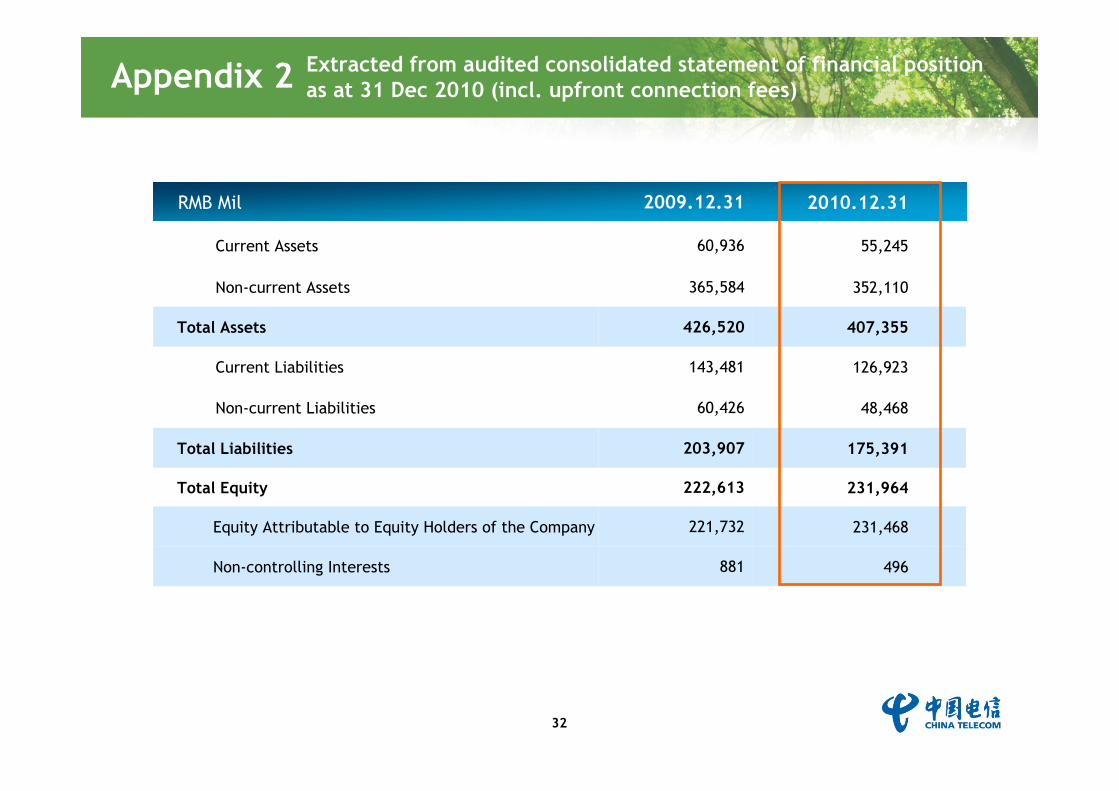

RMB Mil 2009.12.31 2010.12.31

Current Assets 60,936 55,245

Non-current Assets 365,584 352,110

Total Assets 426,520 407,355

Current Liabilities 143,481 126,923

Non-current Liabilities 60,426 48,468

Total Liabilities 203,907 175,391

Total Equity 222,613 231,964

Equity Attributable to Equity Holders of the Company 221,732 231,468

Non-controlling Interests 881 496

Appendix 2 Extracted from audited consolidated statement of financial position as at 31 Dec 2010 (incl. upfront connection fees)