Embed Size (px)

Citation preview

Annual Report

2009

82/83

Contents

1. Letter from the Head of Supervisory Board

Letter from the Chairman of the Board

2. Company’s Profile

3. History

4. Lines of Business

5. Key Initiatives 2009

5.1 Optimization of Operations under Crisis Conditions

5.2. Corporate Sales

5.3. Regional Network

5.4. Personal Insurance

5.5. Finance Management

5.6. Underwriting

5.7. Claims Handling

5.8. Staff

6. Public Activities

7. Financial Highlights

7.1. Financial Results 2009

7.2. Premium and Loss Trends

7.3. Premium Portfolio 2009

7.4. Premium Income on Major Lines of Business

7.5. Independent Auditor’s Opinion

7.6. Balance Sheet of the Company

7.7. Financial Results Report

8. Licenses

9. Our Offices

Letter from the Head of Supervisory Board

Alexander Grigoryev

Head of Supervisory Board of INGO Ukraine, Director General of «Ingosstrakh» OIJSS

Ladies and Gentlemen,

In 2009, INGO Ukraine was mainly focused on maintaining the maximum

efficiency within the downfall environments of the Ukrainian insurance

marketplace affected by the global financial crisis. I am pleased to note that in

spite of all the problems and difficulties, INGO Ukraine did manage to keep a

dominant position in the insurance market, fully meeting its obligations towards

its Customers in a timely manner.

Failing to avoid a decrease in the premium collection, the Company, however,

succeeded in minimizing the impact of the banking crisis, keeping the investments

effectiveness and closing the year at a profit, all this being possible due to the

anti-recessionary measures. The objectives of 2009, such as strengthening of

financial discipline and risk control, cutting of costs, optimization of business

processes, adequate risk pricing and liquidity maintaining, were successfully

attained.

Unfortunately, in 2009 the crisis was not over. Indeed, 2010 will be even

more complicated and will test many insurers for their sustainability. In these

circumstances, INGO Ukraine, as well as all other members of the INGO

International Insurance Group, may always count on the support and assistance

of their parent company. Whatever the situation might be, we confidently assure

our colleagues from different countries, including Ukraine, of our effective

cooperation so that the customers could benefit from a reliable insurance

protection and enjoy the highest standard of service.

84/85

Letter from the Chairman of the Board

Igor GORDIENKO

Chairman of the Board INGO Ukraine

Dear Friends,

In the previous year of ongoing global economy recession, our Company not

only passed one of the hardest “endurance” tests and fulfilled its obligations to

our clients who had entrusted to us their risks, but also managed to maintain

liquidity and augment its potential.

In our today’s business, we proceed from the fact that the environment is

undergoing drastic changes: structures of markets and products are getting more

complicated, standards of financial institution operations are being modified.

In mid-term perspective, the goal of the Company is to keep on implementing

the new business model of management, able to respond adequately to the new

challenges.

The projects initiated to develop business processes, risk management and IT

systems will be implemented in accordance with the applicable international

standards and requirements of the Ukrainian laws.

Our clients should be absolutely confident of INGO Ukraine as a reliable partner

able to meet its commitments, no matter what changes might happen in the

external circumstances.

Company`s Profile

86/87

2. Company`s Profile

INGO Ukraine Private Joint-Stock Insurance Company has a 19-year expertise in the insurance marketplace. With

a longstanding leadership in the amounts of claims paid, the Company finds itself among the biggest insurance

organizations in Ukraine in terms of premiums written and owned capital. It is a member of INGO International

Insurance Group and an affiliated company of “Ingosstrakh” JSIC.

The Company possesses 25 licenses for different types of compulsory and voluntary insurance and provides its

insurance services to corporate and retail clients.

INGO Ukraine has a network of 26 branches and more than 100 customer service offices throughout the

country.

Staffed with over 450 experts, the Company operates for its clients in all regions of Ukraine.

History

88/89

3. History

by «Business» newspaper as «The Most Professional Insurance Company in Ukraine». «INGO Ukraine» JSIC was awarded by the National Club of Indemnity Payment for the claims paid amount in the «Voluntary Medical Insurance» class.

2007

Following the rating of «Guards 500» the INGO Ukraine JSIC gained the leading stand in the nomination «The Most Favorite Insurance Company».

2008

«Ingosstrakh» JSIC, «INGO Ukraine» JSIC and «Ingosstrakh-Zhyttya» IC LLC had founded «INGO Ukraine-Zhyttya» Company to broaden the range of services provided to the existing and new clients. «INGO Ukraine» JSIC became a leader regarding the amount of claims paid among all insurance companies of Ukraine.

2009

Start of practical risk management implementation into Company management system.

2002

Following the annual results the premiums written exceeded UAH 100 mln.

2003

«Ostra-Kyiv» JSIC gained «Grand Prix» at the «Insurance Internet of Ukraine, 2003» All-Ukrainian Contest. A large-scaled project on internal reorganization had started in the company.

2004

«Ingosstrakh» JSIC (Russia) had received the control packet of shares of «Ostra-Kyiv» JSIC. «Ostra-Kyiv» JSIC had entered the «INGO» International Insurance Group. A new strategy of the company’s develop-ment was adopted for the 2005-2008 pe-riod. «Ostra-Kyiv» JSIC changes its name for «INGO Ukraine» JSIC. «INGO Ukraine» JSIC had obtained the International Certificate of Partnership Reliability approved by the Inter-national Chamber of Commerce (Paris).

2005

A systematic work on realization of the company’s long-term strategy had started from the beginning of the year.

2006

Following the financial results of 2005 and 2006 “INGO Ukraine” JSIC was nominated

1990

«Ostra» Joint-Stock Insurance Company (ISIC) (Odessa) becomes the successor of the «Ingosstrakh» Open Insurance Joint-Stock Society (OIJSS) in Ukraine.

1991

The Kyiv branch of «Ostra» IJSS was founded.

1994

The Kyiv branch of «Ostra» IJSS was reregistered as the «Ostra-Kyiv» Joint-Stock Insurance Company.

1997

«Ingosstrakh» Transnational Group (TNG) was established. «Ostra-Kyiv» JSIC had obtained a full membership of the «Ingosstrakh» TNG.

1998

Following the financial results being nominated by «Business» newspaper «Ostra-Kyiv» JSIC was recognized as the leader among the insurance companies of Ukraine.

2000

«Ostra-Kyiv» JSIC offers the insurance programs for individuals in the market.

Lines of Business

90/91

4. Lines of Business

• Property, incl. Pledged Assets

• Business Interruption

• Motor fleet, incl. Third Party Liability

• Stocks and Cargo

• CAR & Technical Risks

• Professional Indemnity

• General Liability

• Export & Import Transactions

• Insurances for Employees

• Agricultural Risks

• Own Vehicles

• Real Estate & Property, incl. Mortgage Insurance

• Voluntary Medical Insurance

• Casualty Insurance

• Travel Insurance

• TPL

• Aviation Risks

• Marine Risks

• Transport Operators

Lines of Business

Legal Entities of all forms of

ownership

Individuals Special Lines

Key Initiatives 2009

92/93

5. Key Initiatives 2009

The reduced market capacity in 2009 enabled the Company to focus its utmost attention on the enhancement

of business efficiency. The major projects in 2009 involved initiatives aimed at business optimization, allowing

the Company to get adapted to the volumes of business that had grown up significantly in the recent years.

The implementation of such projects enabled the Company to weaken the impact of the crisis as well as to build

up opportunities for further development in the post-crisis period.

The projects included:

1. Update of risk assessment procedures.

2. Optimization of sales channels.

3. Reporting enhancement.

4. Implementation of a new claims handling model.

5. Workforce reallocation.

5. Key Initiatives 2009

5.1 Optimization of Operations under Crisis Conditions

Implementation of a New Claims Handling Model

Cooperation with authorized vehicle service stations.

Special software implementation.

Service enhancement.

Workforce Reallocation

Productivity increase.

Update of Risk Assessment Procedures

Mandatory risk audit for a big number of insured objects.

Change of risk assessment principles.

Tightening of risk management and underwriting procedures.

Review of pricing policy per type of insurance and customer segment.

Optimization of Sales Channels

Direct sales development.

Review of cooperation with intermediaries.

Sales optimization for bank-related products.

Reporting Enhancement

Shorter deadlines for financial accounting and corporate reporting.

Enhanced reporting discipline of the structural units.

To stabilize the situation, INGO Ukraine enforced a number of anti-crisis management short-term initiatives aimed to reduce losses and invigorate the structure of the Company within the shortest time possible.

94/95

5. Key Initiatives 2009

5.2. Corporate Sales

The crisis emphasized the importance of transacting insurance business with

corporate customers as well as the necessity for higher standards of corporate

sales. Maintained liquidity, proven reliability and discharge of obligations towards

customers and partners were achieved by the Company mainly due to the

fulfillment of the following targets:

1. Optimization of business processes for costs cutting.

2. Risk audit.

3. Consultations for clients on risk management aspects.

4. Comprehensive customer service programs.

Olexandr MATSAK

Vice-Chairman of the Board

5. Key Initiatives 2009

5.3. Regional Network

The underlying principles of the regional policy of INGO Ukraine comprise the

necessity for its presence in all regional centers of the country to render top-class

services to the customers.

In the previous year, the following measures were taken:

1. Implementation of risk management system.

2. Procedural changes in the regional network management.

3. Introduction of enhanced claims handling model.

Victor SHEVCHENKO

Vice-Chairman of the Board

96/97

5. Key Initiatives 2009

5.4. Personal Insurance

In 2009, the Company was developing new medical insurance business model

within Ukraine for providing better medical services to its clients.

Gennadiy MYSNYK

Vice-Chairman of the Board

5. Key Initiatives 2009

5.5. Finance Management

The downturn in the global economy proved the need to optimize business processes

and centralize the accounting of branches, and the Company as a whole.

For these purposes, the following steps were undertaken:

1. Taking more conservative approaches to investment portfolio.

2. Changes to the internal audit and control system.

3. Implementation of the centralized system of cash flows including the regional

network.

4. Optimization of operational and administrative expenses.

Lyudmyla KOLISETSKA

Chief Financial Officer

98/99

5. Key Initiatives 2009

5.6. Underwriting

The next stage of underwriting development in the Company is related to the

introduction of risk management procedures pursuant to the international

principles and practices: IFRS accounting standards and European prudential

supervision requirements.

1. Implementation of risk management procedures for all types of insurance.

2. Standardization of risk management principles in line with the international

practice.

3. Utilization of risk management results for managerial decisions.

Sergiy KHANIN

Head of Undewriting Department

5. Key Initiatives 2009

5.7. Claims Handling

Measures introduced in 2009 allowed to:

1. Reduce car repair periods.

2. Enhance the quality of claims handling.

3. Minimize the set of documents required for claims handling. Victor SASIN

Head of Claims Handling Department

100/101

5. Key Initiatives 2009

5.8. Staff

The Company’s policy of manpower allocation enabled us to get adapted quickly

and efficiently to the changing external economic environment as well as to

actively initiate and successfully implement the changes required in the crisis

conditions.

In 2009, the Company coped with the following tasks:

1. Workforce reallocation.

2. Productivity increase.

3. Adequacy of costs incurred for staff training and upgrade to the results gained.

Maria DIBROVA

HR Manager

Public Activities

102/103

6. Public Activities

Tetiana RYZHOVA

Vice-Chairman of the Board

INGO Ukraine has a close cooperation and partnership with many national and

international organizations and associations:

• INGO International Insurance Group;

• Ukrainian Federation on Insurance;

• Motor (Transport) Insurance Bureau of Ukraine;

• Marine Insurance Bureau of Ukraine;

• Association of Shipbuilders of Ukraine;

• ICC Ukraine (Ukrainian National Committee of the International Chamber of

Commerce);

• American Chamber of Commerce in Ukraine;

• European Business Association;

• Kyiv Chamber of Commerce and Industry;

• Chamber of Commerce and Industry of Ukraine.

Financial Highlights

104/105

7. Financial Highlights

7.1. Financial Results 2009

Premiums written, UAH mln 438.4

Number of insurance policies 283 379

Claims paid, UAH mln 258.0

Technical reserves, UAH mln 210.9

Authorized capital, UAH mln 130.9

Own capital, UAH mln 141.9

Profit, UAH mln 15.1

Iryna CHEKURDA

Chief Accountant

7. Financial Highlights

7.2. Premium and Loss Trends

The 2009 financial results from business operations are outlined as follows:

1. The Company produced written premiums of UAH 438.4 mln, 17.45% less than in 2009, which corresponds to the general

tendencies of the insurance industry of Ukraine.

2. During the year, the Company made 283’379 insurance contracts, including 174’818 signed with individuals.

3. Total assumed liability under insurance contracts entered into in 2009 made UAH 190’078’965’700.

4. Claims paid amounted to UAH 258 mln in total, including UAH 124.5 mln paid to individuals.

106/107

7. Financial Highlights

7.3. Premium Portfolio 2009

Motor insurance dominates in the premium income of INGO Ukraine. Easy-to-understand, this class of coverage becomes

the most “in-demand” product for individuals.

2009 witnessed an increased share of property insurance in the premium portfolio of INGO Ukraine. This was caused by

both external factors and corporate strategy and processes aimed at enhanced risk management and profit increase.

The reduced share of personal insurance, as compared to 2008, matches with the relevant trends prevailing on the

market.

7. Financial Highlights

7.4. Premium Income on Major Lines of Business

In 2009, premiums written for insurance contracts made with individuals amounted to UAH 156.6 mln, or 35.7% of the

total premium income.

The Company entered into 108’500 insurance contracts with corporate clients and approx. 175’000 contracts with

individuals.

In the previous year, the Company extended its cooperation with agricultural businesses, port operators, logistic companies

and transporters.

INGO Ukraine developed and marketed a number of new motor and household insurance products for its retail clients.

108/109

7. Financial Highlights

7.5. Independent Auditor`s Opinion

7. Financial Highlights

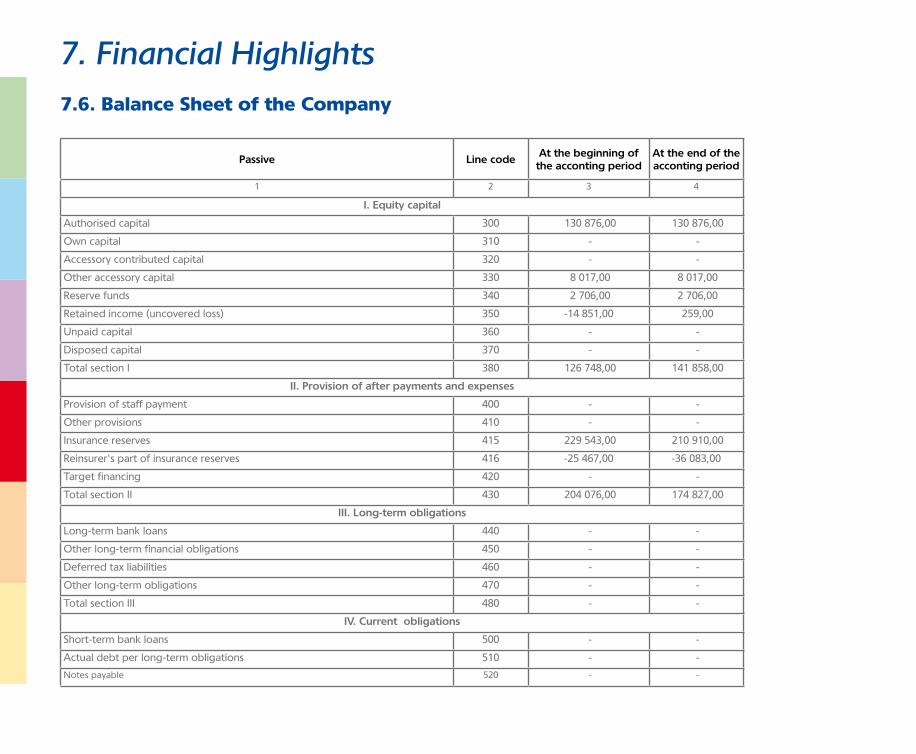

7.6. Balance Sheet of the Company

Active Line codeAt the beginning of

the acconting period

At the end of the acconting

period1 2 3 4

I. Capital assets

Intangible assets:

Residual cost 010 2 795 2 559

base cost 011 4 676 5 144

Accumulated depriciation 012 1 881 2 585

Non-complete building 020 1 443 11 718

Permanent assets:

Residual cost 030 25 917 23 359

base cost 031 40 532 40 121

Waste 032 14 615 16 762

Long-term financil investments:

Cumulated as permanent holdings 040 6 300 6 300

Other financil investments 045 22 212 19 072

Long-term receivables 050 3 944 3 915

Deffered tax assets 060 - -

Goodwill 065 - -

Other capital assets 070 - -

Total section I 080 62 611 66 923

II. Current assets

Inventory:

Manufacturing inventory 100 649 657

Rearers and fatteners 110 - -

In-process inventory 120 - -

Final products 130 - -

Goods 140 - -

Notes receivable 150 - -

110/111

7. Financial Highlights

7.6. Balance Sheet of the Company

1 2 3 4

Receivables for goods, works, services :

Net realizable value 160 52 216 54 830

base cost 161 52 216 54 830

Provision for doubtful debts 162 - -

Receivables per calculation :

of budget 170 64 30

of advance paid out 180 1 490 1 823

of accrued assets 190 2 894 1 062

of internal payments 200 269 253

Other current receivables 210 17 569 35 886

Current financial investment 220 - 10 602

Money recources and match:

In national currency 230 111 115 109 784

In foreign currency 240 125 391 86 928

Other current assets 250 - -

Total section II 260 311 657 301 855

III. Relevant costs 270 452 362

Balance 280 374 720 369 140

7. Financial Highlights

7.6. Balance Sheet of the Company

Passive Line codeAt the beginning of

the acconting periodAt the end of the acconting period

1 2 3 4

I. Equity capital

Authorised capital 300 130 876,00 130 876,00

Own capital 310 - -

Accessory contributed capital 320 - -

Other accessory capital 330 8 017,00 8 017,00

Reserve funds 340 2 706,00 2 706,00

Retained income (uncovered loss) 350 -14 851,00 259,00

Unpaid capital 360 - -

Disposed capital 370 - -

Total section I 380 126 748,00 141 858,00

II. Provision of after payments and expenses

Provision of staff payment 400 - -

Other provisions 410 - -

Insurance reserves 415 229 543,00 210 910,00

Reinsurer's part of insurance reserves 416 -25 467,00 -36 083,00

Target financing 420 - -

Total section II 430 204 076,00 174 827,00

III. Long-term obligations

Long-term bank loans 440 - -

Other long-term financial obligations 450 - -

Deferred tax liabilities 460 - -

Other long-term obligations 470 - -

Total section III 480 - -

IV. Current obligations

Short-term bank loans 500 - -

Actual debt per long-term obligations 510 - -

Notes payable 520 - -

112/113

7. Financial Highlights

7.6. Balance Sheet of the Company

Payables for goods, works, services: 530 28 513,00 38 811,00

Current liabilities per calculation

of advances receive 540 5 019,00 4 710,00

of budget 550 7 310,00 4 680,00

of extra budgetary payments 560 - -

of insurance 570 652,00 573,00

Of payment for labor 580 1 725,00 1 385,00

Of participants 590 - -

of internal payments 600 - -

Other current obligations 610 677,00 2 295,00

Total section IV 620 43 896,00 52 454,00

III. Relevant costs 630 - 1,00

Balance 640 374 720,00 369 140,00

Chairman of the Board __________________________________ I. Gordienko

Chief Accountant _________________________________ I. Chekurda

7. Financial Highlights

7.7. Financial Results Report

ITEM Line code For year 2009 For year 2008

1 2 3 4

Income (revenue) from products realization (goods, works, services) 010 385 293 418 702

Value added tax 015 -

Excise tax 020 -

Other income allocations 030 -

Net income (revenue) from products realization (goods, works, services) 035 385 293 418 702

Prime cost of products sold (goods, works, services) 040 307 964 538 880

Gross:

Profit 050 77 329 -120 178

Loss 055

Other operating income 060 83 425 459 403

Administrative expenses 070 23 102 36 853

Distribution expenses 080 52 870 66 720

Other operating expenses 090 72 922 240 824

Financial result of operating activity

Profit 100 11 860 -5 171

Loss 105 -

Capital participation income 110 -

Other financial income 120 23 950 20 558

Other incomes 130 24 212

Financial expenses 140 - 21

Capital participation expenses 150 -

Other expenses 160 1 048 1 764

Financial results of ordinary activities before taxation:

Profit 170 34 786 13 814

Loss 175 -

Tax on ordinary activities' income 180 19 690 28 643

114/115

7. Financial Highlights

7.7. Financial Results Report

Financial statements of ordinary activities:

Profit 190 15 096 -14 828

Loss 195

Inordinary:

Profit 200 144 105

Loss 205 127 112

Tax on inordinary activities' income 210 3 16

Net:

Profit 220 15 110 -

Loss 225 - -14 851

ITEM Line code For year 2009 For year 2008

1 2 3 4

Average annual of ordinary shares 300 - -

Corrected average annual of ordinary shares 310 - -

Net income(loss) per one ordinary shares 320 - -

Corrected net income(loss) per one ordinary shares 330 - -

Dividents per ordinary share 340 - -

Chairman of the Board __________________________________ I. Gordienko

Chief Accountant _________________________________ I. Chekurda

RETURN ON EqUITy INDEx CALCULATION

7. Financial Highlights

7.7. Financial Results Report

ITEM Line code For year 2009 For year 2008

1 2 3 4

Material expenses 230 2 848 3 502

Labor costs 240 30 391 35 432

Allocations for social needs 250 9 913 11 470

Depreciation 260 4 388 4 199

Other operating expenses 270 409 318 828 673

Total 280 456 858 883 276

OPERATING ExPENSES ELEMENTS

116/117

8. Licenses

No. 299441 dated February 5, 2007 Volun-tary Insurance of liability of Aircraft Owners (in-cluding liability of air carriers)

No. 299442 dated February 5, 2007 Volun-tary Personal Accident Insurance

No. 299443 dated February 5, 2007 Volun-tary Insurance of liability to the third parties (ex-cept for the civil liability of overland transport owners, liability of air transport owners, liability of water transport owners (including liability of carriers)

No. 299444 dated February 5, 2007 Volun-tary Insurance against Fire and Acts of God

No. 299 445 dated February 5, 2007 Volun-tary Insurance of Financial Risks

No. 360158 dated August 27, 2007 Volun-tary Insurance of Credits (including liability of debtor for unpaid credit)

No. 396180 dated March 3, 2008 Compul-sory Personal Insurance of employees of de-partmental (except for those working at the es-tablishments and organizations financed from State Budget of Ukraine) and rural fire protec-tion service as well as members of voluntary fire protection guards (teams)

jects as well as objects which economic activity may lead to ecological, sanitary and epidemio-logical accidents

No. 299432 dated February 5, 2007 Volun-tary Health Insurance against occurrence of a disease

No. 299433 dated February 5, 2007 Volun-tary Medical Expenses Insurance

No. 299434 dated February 5, 2007 Volun-tary Cargo and Luggage Insurance

No. 299435 dated February 5, 2007 Volun-tary Property Insurance (except for railway, mo-tor, air, water transport (marine inland waters and other kinds of water transport), cargo and baggage

No. 299436 dated February 5, 2007 Vol-untary Insurance of liability of water transport owners (including liability of carriers)

No. 299437 dated February 5, 2007 Vol-untary Insurance of Water Transport (marine inland waters and other kinds of water trans-port)

No. 299438 dated February 5, 2007 Volun-tary Insurance of Aircrafts

No. 299439 dated February 5, 2007 Volun-tary Insurance of overland transport (except for railway transport)

No. 299440 dated February 5, 2007 Volun-tary Insurance of civil liability of overland trans-port owners (including liability of carriers)

No 100196 dated July 21, 2005 Voluntary insurance of railway transport

No. 100198 dated July 22, 2005 Compulsory insurance of liability for carriers of hazardous cargo in case of negative consequences caused by hazardous cargo carriage

No. 100259 dated August 12, 2005 Com-pulsory insurance of civil liability of Ukrainian citizens that own or otherwise legally possess weapons for the harm that may be caused to the third party or his/her property due to pos-sessing, keeping or use of such weapon

No. 396181 dated March 3, 2008 Compul-sory personal insurance against traffic accidents for drivers and passengers of motor transport

No. 398190 dated May 31, 2008 Voluntary Medical Expenses Insurance (Permanent Health Insurance)

No. 442496 dated April 16, 2009 Compul-sory Aviation Insurance (Civil Aviation)

No. 377568 dated January 17, 2008 Com-pulsory Motor Vehicle Owners Third Party Li-ability

No. 299192 dated December 22, 2006 Com-pulsory insurance of civil liability of operators of nuclear plants/facilities for damage that may be caused due to nuclear incident

No. 299431 dated February 9, 2007 Com-pulsory insurance of civil liability of economic subjects for harm that may be caused by fires and accidents at the objects of increased dan-ger, including fire and explosion hazardous ob-

9. Our Offices

8 Geroiv Stalingrada Str.,

building 5а, section 1

tel./fax: +38 044 332 1199;

537 6918

87/30 Zhylyanska Str.

tel./fax: +38 044 239 3925

28 Predslavynska, Off. 102

tel.: +38 044 459 7070; 459 7073;

fax: +38 044 459 7072

KHARKIV

90 Sumska Str.

tel.: +38 057 700 2539; 700 4858;

KHERSON

7 9-Sichnya Str., Off. 1

tel.: +38 0552 46 1374; 46 1366;

fax: +38 0552 46 1369

DNIPROPETROVSK

20 K. Marksa Av.

tel.: +38 056 790 5328; 790 5333

IVANO-FRANKIVSK

4 Nezalezhnosti Str., Off. 316

tel.: +38 0342 55 9683; 71 0444

fax: +380342 77 9720

KYIV

14 a A. Akhmatovoi Str., Off. 24

tel./fax: +38 044 331 8768

18 Verkhnii Val

tel./fax: +38 044 592 9194;

592 9154

24 Veresneva Str.

(car market “Novyi”)

tel./fax: +38 044 200 7229

HEAD OFFICE:

33 Vorovskoho Str., Kyiv

tel.: +38 044 490 2744 /45

fax: +38 044 490 2748

email: [email protected]

REGIONAL OFFICES:

CHERKASY

37 Baydy Vyshnevetskoho Str.,

Off. 413,414

tel.: +38 0472 36 8583

fax: +38 0472 33 0474

CHERNIHIV

52, Kotsubinskoho Street, Off. 3

tel./fax: +38 0462 61 4444; 61 4445

CHERNIVTSI

127 Nezalezhnosti Av.

tel.: +38 0372 58 4208

DONETSK

102 Artema Str., 23 Shchorsa Str.

tel.: +38 062 345 3761 (62,63);

tel.: +38 062 349 9831 (32,33)

118/119

9. Our Offices

TERNOPIL

3 Zamkova Str.tel.: +38 0352 55 0094

UZHGOROD

3 Kyivska Naberezhna Str.tel.: +38 0312 66 0608; 61 4379

VINNYTSIA

13 Internatsionalna Str.tel.: +38 0432 57 9223; 57 9424;fax: +38 0432 67 6968

ZHYTOMYR

5-А Kafedralna Str., Off. 205tel.: +38 0412 41 8166; 46 3265

ZAPORIZHZHIA

21 Metalurhiv Av.tel.: +38 061 228 3200

LVIV

80a Sakharova Str.tel.: +38 032 295 8700

MYKOLAYIV

3в Sadova Str.tel./fax: +38 0512 76 7100 (01,02)

ODESA

4д Shevchenko Av., Off. 1; 34tel.: +38 048 776 0001 (02,03)

POLTAVA

19f Komsomolska Str., Off. 1tel.: +38 0532 50 0135;61 3455fax: +38 0532 50 0134

RIVNE

21 Kyivska Str., Off. 302; 308; 310tel.: +38 0362 63 4683; 63 4636

SIMFEROPOL

40 Karla Marksa Str.tel.: +38 0652 79 0190 (91,92,93); fax: +38 0652 79 0194

SUMY

29-D Soborna Str.tel.: +38 0542 62 2351

KHMELNITSKIY

22 Svobody Str., Floor 3

tel.: +38 0382 78 7670

fax: +38 0382 78 7671

KIROVOGRAD

18/21 Frunze Str.

tel.: +38 0522 22 1426

fax: +38 0522 22 4408

KREMENCHUK

30 Proletarska Str., Off. 6tel.: +38 0536 79 3485;fax: +38 0536 74 3491

KRYVYI RIH

14-А Meleshkina Str., Off. 305

tel.: +38 0564 40 0886; 64 8310

LUGANSK

7е Khersonska Str.tel.: +38 0642 98 0943

LUTSK

6 Voli Av., Off. 23tel.: +38 0332 72 5168; 72 3647

![新建 Microsoft Word 文档jiaowu.dlpu.edu.cn/Edit4/uploadfile/20140923095009323.pdf · [2009] 61 2009 2009 c 2009) 65 & ) 2009 2009 39 Y), 2009 160 n, 100 60M](https://img.dokumen.tips/doc/110x75/5f57628b37d0bc70511eab4d/-microsoft-word-2009-61-2009-2009-c-2009-65-2009-2009-39.jpg)