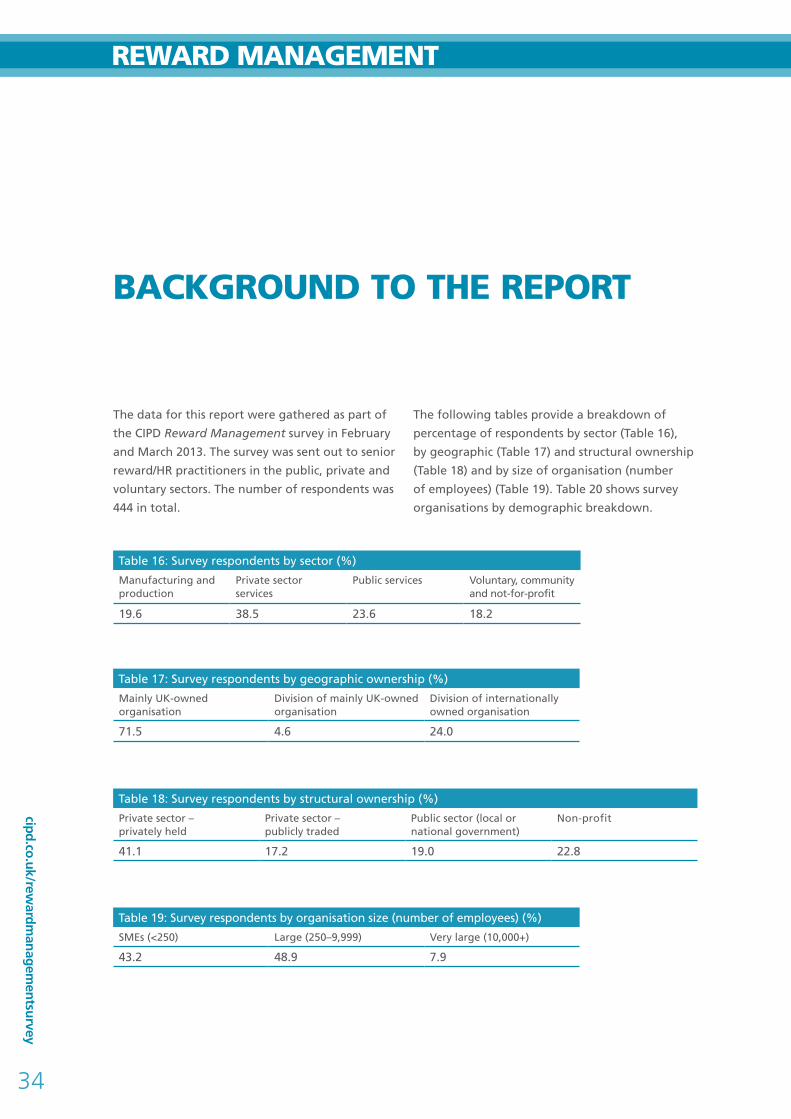

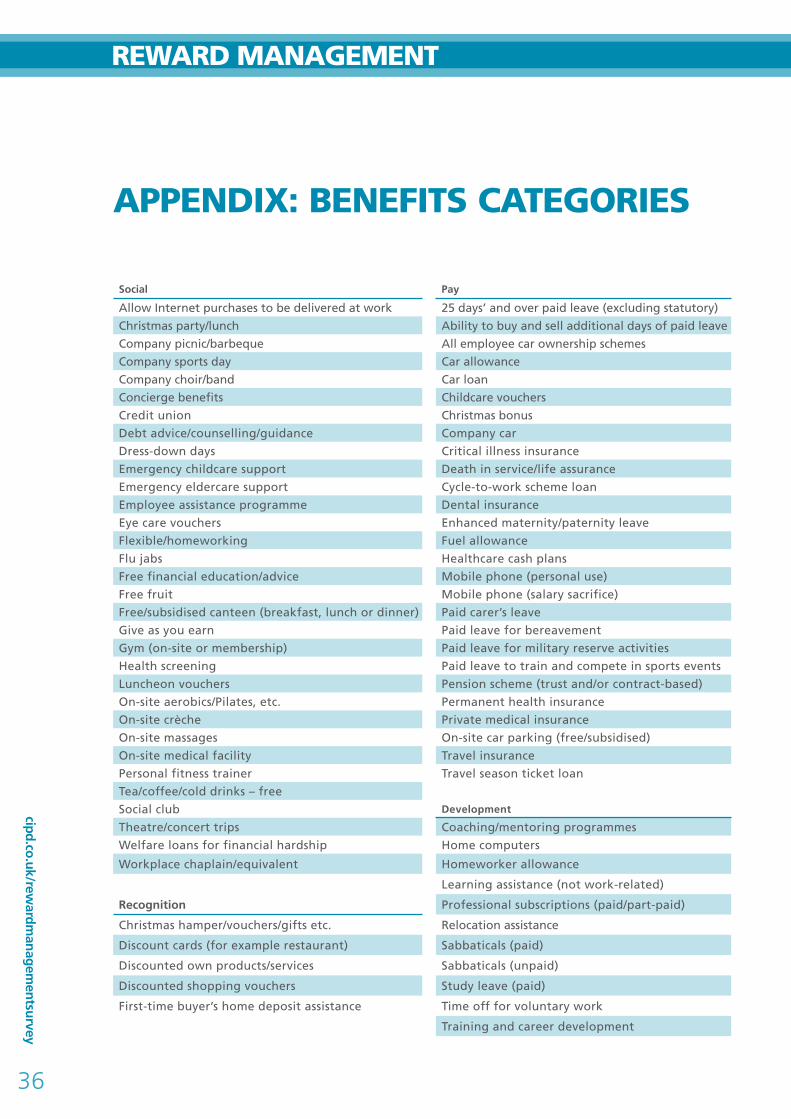

Embed Size (px)

Citation preview

REWARDMANAGEMENT

2013Annual survey report supplement 2013Aligning strategy and benefits

WORKFORCEWORK WORKPLACE

Championing better work and working lives

The CIPD’s purpose is to champion better work and working lives by improving practices in people and organisation development, for the benefit of individuals, businesses, economies and society. Our research work plays a critical role – providing the content and credibility for us to drive practice, raise standards and offer advice, guidance and practical support to the profession. Our research also informs our advocacy and engagement with policy-makers and other opinion-formers on behalf of the profession we represent.

To increase our impact, in service of our purpose, we’re focusing our research agenda on three core themes: the future of work, the diverse and changing nature of the workforce, and the culture and organisation of the workplace.

About us

The CIPD is the professional body for HR and people development. We have over 130,000 members internationally – working in HR, learning and development, people management and consulting across private businesses and organisations in the public and voluntary sectors. We are an independent and not-for-profit organisation, guided in our work by the evidence and the front-line experience of our members.

WORKOur focus on work includes what work is and where, when and how work takes place, as well as trends and changes in skills and job needs, changing career patterns, global mobility, technological developments and new ways of working.

WORKPLACEOur focus on the workplace includes how organisations are evolving and adapting, understanding of culture, trust and engagement, and how people are best organised, developed, managed, motivated and rewarded to perform at their best.

WORKFORCEOur focus on the workforce includes demographics, generational shifts, attitudes and expectations, the

changing skills base and trends in learning and education.

Rew

aR

d m

an

ag

em

en

t 2013

1

2013

COntentS

Foreword 2

Summary of key findings 4

Introduction 8

Business strategy 9

Workforce characteristics 15

HR outcomes 21

Benefits transparency 27

Conclusions and implications 32

Background to the report 34

Appendix: benefits categories 36

Endnotes 37

cipd.co.uk/rewardm

anagementsurvey

2

RewaRd management

fORewORd

A quick perusal of Google Scholar for academic

research on employee benefits produces thin

pickings for the reward professional. This lack

of academic interest is perhaps odd given the

significant amount of money that is spent each

year by employers on such rewards, both in the

UK and overseas. By contrast, the quantity, if

not quality, of academic research around pay is

significantly larger.

Despite the fact that little taxpayer-funded research

appears to be focusing on employee benefits,

reward professionals are nevertheless being criticised

by some academics for not making evidence-based

decisions when making reward choices.

This year, to help start to break this circle, the

CIPD asked the researchers involved with the

Reward Management survey to examine employee

benefits in more depth and so help create an

evidence base and encourage more academics to

review this unexplored area.

The objectives of this research have been to

explore the links between benefits provisions and

business strategy, workforce characteristics and

HR workplace outcomes. In addition, we have also

explored the associations between organisational

approaches to employee benefit transparency,

benefits management and workplace outcomes.

The research indicates that there is indeed a

relationship between an organisation’s business

strategy and the workplace benefits on offer to

the workforce. For instance, a firm exhibiting

a prospector strategy or one that focuses on

product quality is statistically more likely to

provide those benefits associated with employee

development (such as coaching and mentoring

or paid/part-paid professional subscription) than

a firm following a cost or defender strategy.

Of course, the implication for practitioners is

whether business strategy and employee benefits

strategy remain in sync or whether there is a lag

as practice catches up with strategy.

Workplaces where most of the workforce are

graduates are more likely to belong to a defined

contribution pension scheme than workplaces

where graduates are in the minority. Another

finding is that women are more likely to be at

workplaces where there is a still open defined

benefit pension scheme, but where share schemes

are not typically provided. However, these findings

are likely to be influenced by sector rather than

gender. That said, these results do highlight public

policy issues that flow from reforms to public

sector pensions or moves to increase the tax

breaks for share plans.

In terms of HR workforce outcomes, organisations

Rew

aR

d m

an

ag

em

en

t 2013

3

2013

that report having a positive employee relations

climate are statistically more apt to offer

development benefits to their staff. Similarly,

those organisations that are more likely to report

employee absenteeism difficulties are statistically

less likely to offer their staff: free tea/coffee;

a Christmas party; paid study leave; flexible

homeworking; training and career development;

and life assurance/death in service. It would be

wrong to think that the lack of a benefit such as

free tea at work leads to absenteeism difficulties,

rather that employers suffering from absenteeism

difficulties may be less likely to be able to afford

to provide this benefit. In turn, this makes the

organisation a less attractive place to work, which

exacerbates the problem.

Similar to last year, the research finds a positive

relationship between the amount of benefit

transparency and various HR outcomes, such

as employee relations, labour productivity and

employee absenteeism. Implications for practice

from this research include HR professionals

examining whether there is scope for greater

innovation in managing investment in total

reward; reviewing whether the business and

benefit strategies are still in sync; and whether

the amount of benefit secrecy, or otherwise, is

delivering intended or unintended consequences.

I would like to thank all those reward

and HR professionals who helped develop

the questionnaire, those that filled in our

questionnaire, those that have reviewed

this report and the team at the University of

Bedfordshire, London Metropolitan University,

the University of Sydney and the University of

Melbourne who helped create this report.

Charles Cotton

CIPD Performance and Reward Adviser

cipd.co.uk/rewardm

anagementsurvey

4

RewaRd management

SummaRy Of key findingS

This report uses data from the CIPD 2013 Reward Management survey report to explore the connections between benefits and pension practices and three aspects of organisations: business strategy, workforce characteristics and HR outcomes. In addition, the report considers the associations between organisational approaches to transparency of benefits systems, benefits management and HR outcomes. This study finds that there are compelling connections between these elements, which have important implications for reward and HR practitioners.

Business strategyOur results in Table 1 show that private sector

firms operationalising different types of business

strategy (based on competition preferences in

chosen product/service markets, for full business

strategy definitions see Table 5) have different

approaches to workplace benefits and pensions

provisions. In general, firms which prefer to take

a more innovative, market-leading approach

(prospectors and quality-focused firms) are more

likely to have a more extensive benefits provision,

while those operating in safe, stable markets

(defenders and cost-focused firms) are more likely

to be offering more traditional defined benefit

pension plans.

For HR practitioners, the implications of these

findings relate to questions around whether or

not business strategy and employee benefits

remain in sync, or whether there is a lag between

reorientation to meet competitive business needs

and aligning this with a key aspect of HRM.

Rew

aR

d m

an

ag

em

en

t 2013

5

2013

Workforce characteristicsTable 2 shows our findings for the associations

between benefits management and workforce

characteristics in all organisations (private, public

and not-for-profit sectors). While we need to be

mindful of sector and size of organisation factors,

these results show that higher proportions of

certain types of workforce (according to age,

gender and education level) are associated with

different workplace practices, particularly around

pensions provisions.

For those with responsibility in this area, careful

consideration needs to be given to the balance

between total reward mix and any intended

segmentation to align with diverse preferences

among employee groups, while being wary of

putting the organisation at risk of claims that

certain categories of employee are unfairly

treated – for example on grounds of gender.

Table 1: Business strategy and benefits management (private sector organisations only)

In defender strategy organisations… In prospector strategy organisations…

Defined benefit pension schemes are more likely.

Defined contribution pension schemes are less likely.

Defined benefit pension schemes are less likely to be closed in 2013.

A high number of different benefits are more likely to be offered.

Development, pay and social benefits are more likely to be offered.

Lower employer and employee DC pensions’ contributions are more likely.

In operating excellence/cost-focused organisations… In product leadership/quality-focused organisations…

Recognition benefits are more likely to be offered.

Voluntary/affinity benefits are more likely to be offered.

A contributory pension scheme is more likely to be offered.

Changes to pension schemes to meet auto-enrolment requirements are more likely in 2013.

A high number of different benefits are more likely to be offered.

Development and pay benefits are more likely to be offered.

Share schemes/long-term incentives are more likely to be offered.

A hybrid pension scheme is more likely. Lower employer pensions’ contributions are more likely.

Table 2: Workforce characteristics and benefits management (all organisations)

In sections of workforces with a majority of female employees…

In sections of workforces with a majority of young employees…

In sections of workforces with a majority of graduate employees…

Share schemes and LTIs are less likely to be used.

Defined benefit schemes are more likely to be open.

Pension schemes with employer contributions are less likely to be offered.

Defined benefit schemes (open and closed) are less common.

Lower levels of defined contribution pension scheme membership are more likely.

Higher levels of defined contribution pension scheme membership are more likely.

Changes to pension schemes are less likely.

cipd.co.uk/rewardm

anagementsurvey

6

RewaRd management

HR outcomesIn Table 3 results shown indicate that certain key

HR outcomes in the workplace (such as employee

relations climate, labour productivity, employee

recruitment, retention, absenteeism and pay

discontent) are associated with different benefits

management practices.

Implications for HR practitioners centre on

whether there is scope for greater innovation

in managing investment in total reward, paying

attention to the benefits aspects, and whether

or not there is a driver effect related to key HR

outcomes, mindful of employee engagement

aspirations as well as overall workforce

productivity.

Table 3: HR outcomes and benefits management (all organisations)

In organisations with a positive employee relations climate…

In organisations that have increased labour productivity in past three years…

Development benefits are more likely to be offered.

25+ days’ leave, eye care vouchers, Internet purchases delivered to work, training and career development, on-site parking (free/subsidised), flexible/homeworking are more likely to be offered.

In organisations that have experienced employee recruitment difficulties in the past 12 months…

In organisations that have experienced employee retention difficulties in the past 12 months…

Flexible/homeworking, enhanced maternity/paternity leave, paid leave for military reserve activities, pension scheme, training and career development, cycle to work scheme loan are less likely to be offered.

Flexible/homeworking, training and career development, paid study leave, pension scheme, Christmas party/lunch and death in service/life assurance are less likely to be offered.

Contributory pension schemes are less likely to be offered.

In organisations that have experienced employee absenteeism difficulties in the past 12 months…

In organisations that have experienced pay discontent raised by employees in the past 12 months…

Tea/coffee/cold drinks free, Christmas party/lunch, paid study leave, flexible/homeworking, training and career development and death in service/life assurance are less likely to be offered.

Defined benefit pension schemes are more likely to be open.

Share schemes and other long-term incentive plans are less likely to be used.

Tea/coffee/cold drinks free, Christmas party/lunch, Internet purchases delivered to work, on-site parking (free/subsidised), 25+ days’ paid leave, paid study leave are less likely to be offered.

Flexible benefits are less likely to be used.

Defined benefit pension schemes are more likely to be open.

Rew

aR

d m

an

ag

em

en

t 2013

7

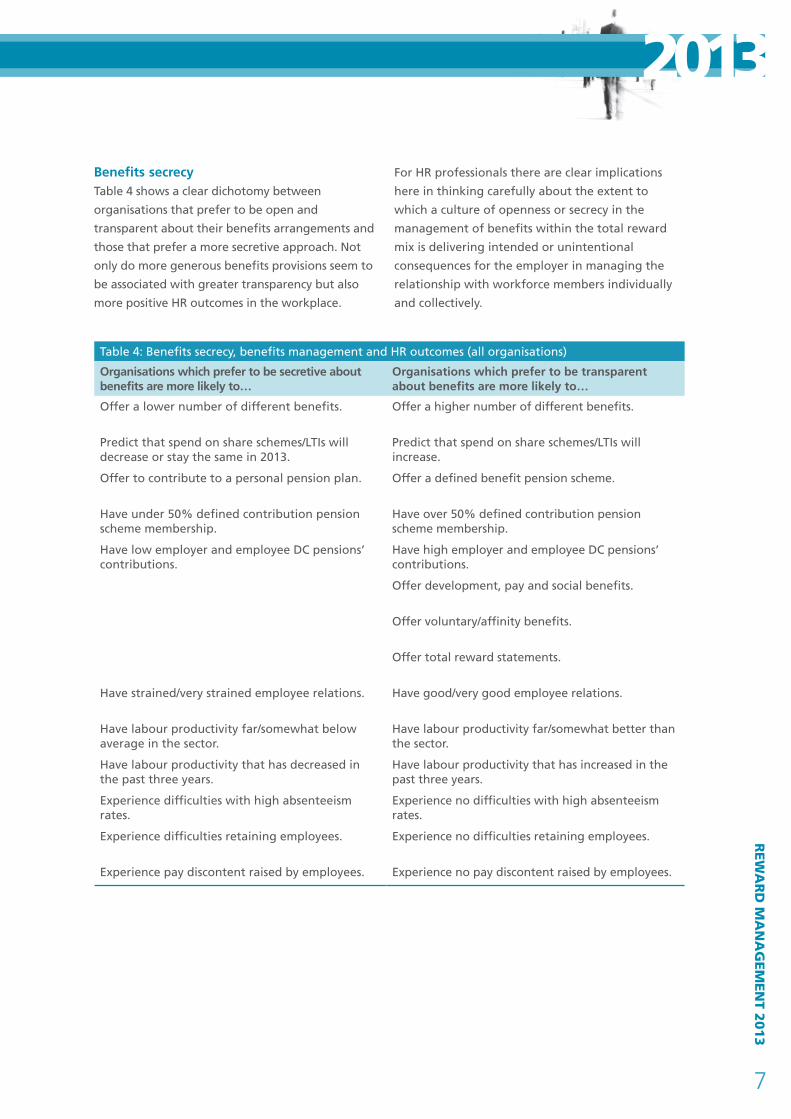

2013Benefits secrecyTable 4 shows a clear dichotomy between

organisations that prefer to be open and

transparent about their benefits arrangements and

those that prefer a more secretive approach. Not

only do more generous benefits provisions seem to

be associated with greater transparency but also

more positive HR outcomes in the workplace.

For HR professionals there are clear implications

here in thinking carefully about the extent to

which a culture of openness or secrecy in the

management of benefits within the total reward

mix is delivering intended or unintentional

consequences for the employer in managing the

relationship with workforce members individually

and collectively.

Table 4: Benefits secrecy, benefits management and HR outcomes (all organisations)

Organisations which prefer to be secretive about benefits are more likely to…

Organisations which prefer to be transparent about benefits are more likely to…

Offer a lower number of different benefits. Offer a higher number of different benefits.

Predict that spend on share schemes/LTIs will decrease or stay the same in 2013.

Predict that spend on share schemes/LTIs will increase.

Offer to contribute to a personal pension plan. Offer a defined benefit pension scheme.

Have under 50% defined contribution pension scheme membership.

Have over 50% defined contribution pension scheme membership.

Have low employer and employee DC pensions’ contributions.

Have high employer and employee DC pensions’ contributions.

Offer development, pay and social benefits.

Offer voluntary/affinity benefits.

Offer total reward statements.

Have strained/very strained employee relations. Have good/very good employee relations.

Have labour productivity far/somewhat below average in the sector.

Have labour productivity far/somewhat better than the sector.

Have labour productivity that has decreased in the past three years.

Have labour productivity that has increased in the past three years.

Experience difficulties with high absenteeism rates.

Experience no difficulties with high absenteeism rates.

Experience difficulties retaining employees. Experience no difficulties retaining employees.

Experience pay discontent raised by employees. Experience no pay discontent raised by employees.

cipd.co.uk/rewardm

anagementsurvey

8

RewaRd management

intROduCtiOn

In 2012, we produced a supplementary report

to the main Reward Management survey report

using inferential statistical analysis of the survey

data to examine the extent of strategic alignment

of pay practices and resulting HR outcomes. The

strategic reward alignment proposition predicts

that aligning reward strategies and practices with

business strategies and workforce characteristics

will generate better HR outcomes. For more

information on the background conceptual

framework of strategic reward, see Reward

Management 2012: Supplement aligning strategy

and pay (CIPD 2012).

Last year our findings showed some support for

the strategic reward alignment proposition; we

found:

• markedly different reward practices used by

private sector firms operationalising different

business strategies in their chosen product/

service sectors

• relationships between the composition of the

workforce and the reward practices employed

in organisations from all sectors

• particular HR outcomes associated with

certain reward management practices.

This year we have focused specifically on benefits

practices (including pensions and share schemes)

to further investigate the proposition that reward

alignment vertically, with business strategy, and

horizontally, with workforce characteristics, leads

to positive HR and organisational outcomes.

We have examined this proposition by testing the

following questions:

• Towhatextentdoprivatesectorfirmswith

different business strategies adopt different

benefits practices?

• Towhatextentdoorganisations(fromall

sectors) with different workforce characteristics

adopt different benefits practices?

• TowhatextentaredifferentHRoutcomes

associated with different benefits practices?

In addition, this report looks at the question of

secrecy versus transparency in the provision of

employee benefits. Last year, looking at pay secrecy,

our findings indicated that there may be positive

HR outcomes related to increasing the transparency

of pay arrangements in organisations. This year,

our focus will be on benefits and whether we see

similar or different results.

The statistical analysis undertaken for this report provides a probability value, that is, the likelihood that the result was due to chance rather than a specific effect or phenomenon. For more information please see the ‘Background to the report’ section.

Rew

aR

d m

an

ag

em

en

t 2013

9

2013

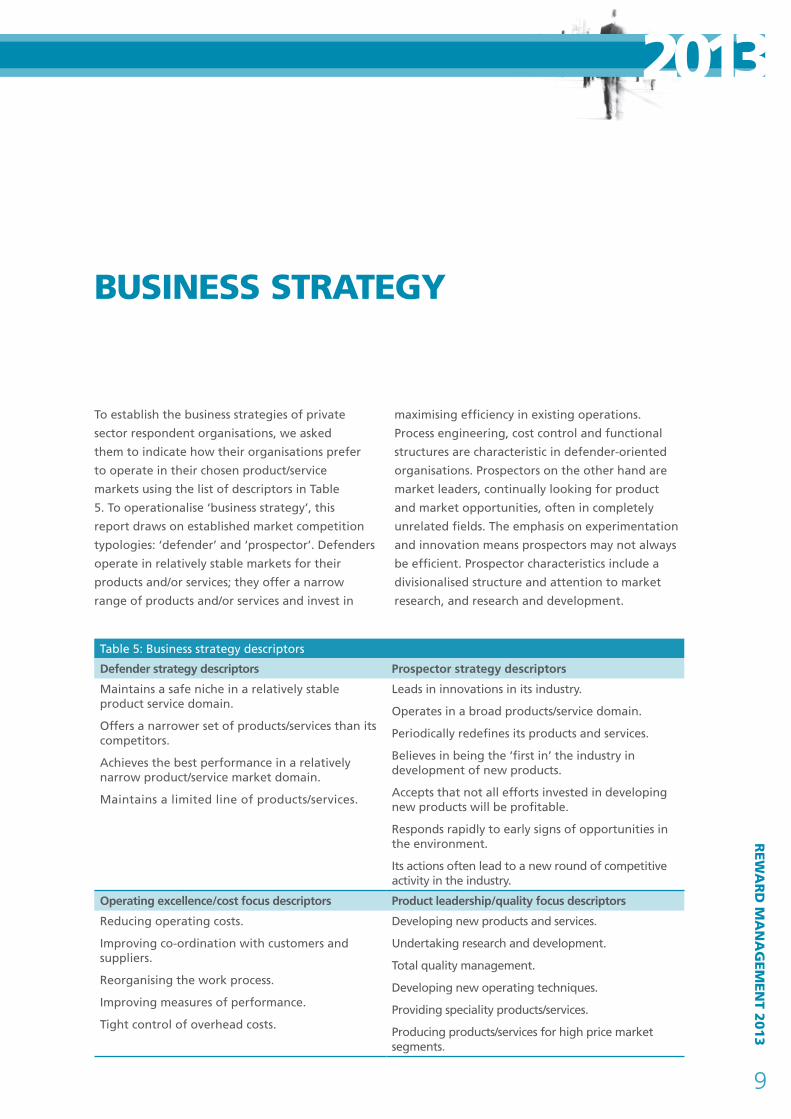

BuSineSS StRategy

To establish the business strategies of private

sector respondent organisations, we asked

them to indicate how their organisations prefer

to operate in their chosen product/service

markets using the list of descriptors in Table

5. To operationalise ‘business strategy’, this

report draws on established market competition

typologies: ‘defender’ and ‘prospector’. Defenders

operate in relatively stable markets for their

products and/or services; they offer a narrow

range of products and/or services and invest in

maximising efficiency in existing operations.

Process engineering, cost control and functional

structures are characteristic in defender-oriented

organisations. Prospectors on the other hand are

market leaders, continually looking for product

and market opportunities, often in completely

unrelated fields. The emphasis on experimentation

and innovation means prospectors may not always

be efficient. Prospector characteristics include a

divisionalised structure and attention to market

research, and research and development.

Table 5: Business strategy descriptors

Defender strategy descriptors Prospector strategy descriptors

Maintains a safe niche in a relatively stable product service domain.

Offers a narrower set of products/services than its competitors.

Achieves the best performance in a relatively narrow product/service market domain.

Maintains a limited line of products/services.

Leads in innovations in its industry.

Operates in a broad products/service domain.

Periodically redefines its products and services.

Believes in being the ‘first in’ the industry in development of new products.

Accepts that not all efforts invested in developing new products will be profitable.

Responds rapidly to early signs of opportunities in the environment.

Its actions often lead to a new round of competitive activity in the industry.

Operating excellence/cost focus descriptors Product leadership/quality focus descriptors

Reducing operating costs.

Improving co-ordination with customers and suppliers.

Reorganising the work process.

Improving measures of performance.

Tight control of overhead costs.

Developing new products and services.

Undertaking research and development.

Total quality management.

Developing new operating techniques.

Providing speciality products/services.

Producing products/services for high price market segments.

cipd.co.uk/rewardm

anagementsurvey

10

RewaRd management

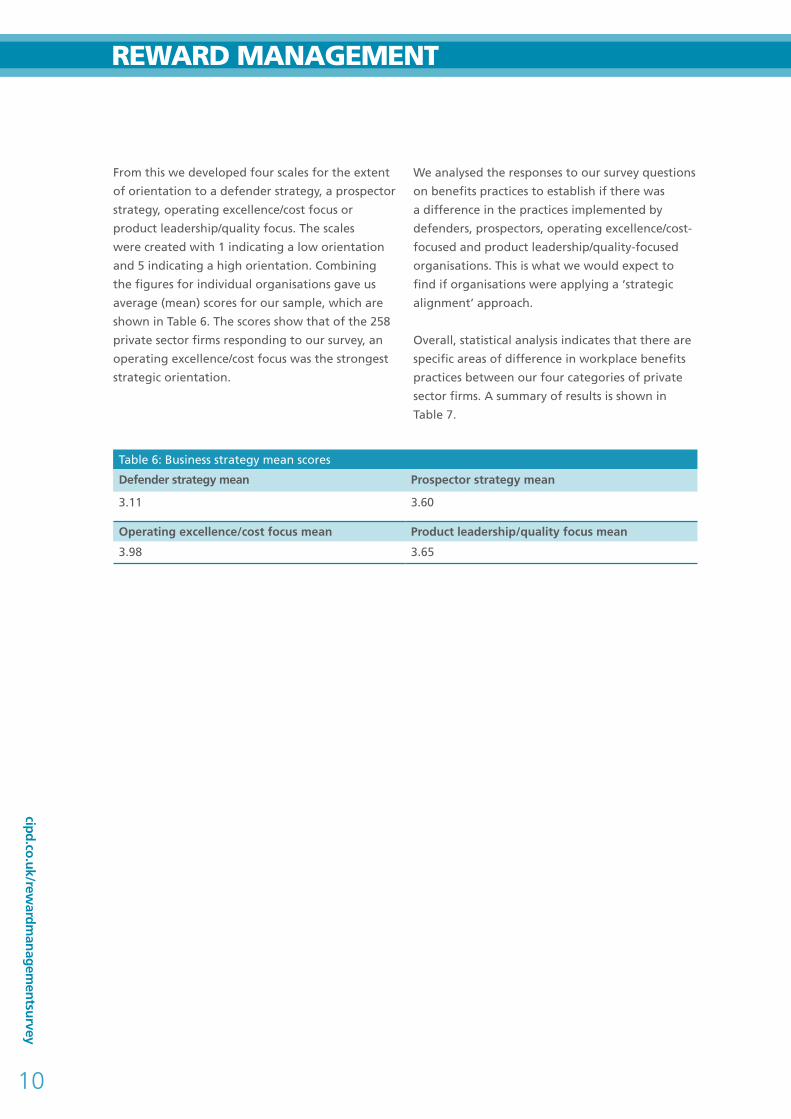

From this we developed four scales for the extent

of orientation to a defender strategy, a prospector

strategy, operating excellence/cost focus or

product leadership/quality focus. The scales

were created with 1 indicating a low orientation

and 5 indicating a high orientation. Combining

the figures for individual organisations gave us

average (mean) scores for our sample, which are

shown in Table 6. The scores show that of the 258

private sector firms responding to our survey, an

operating excellence/cost focus was the strongest

strategic orientation.

We analysed the responses to our survey questions

on benefits practices to establish if there was

a difference in the practices implemented by

defenders, prospectors, operating excellence/cost-

focused and product leadership/quality-focused

organisations. This is what we would expect to

find if organisations were applying a ‘strategic

alignment’ approach.

Overall, statistical analysis indicates that there are

specific areas of difference in workplace benefits

practices between our four categories of private

sector firms. A summary of results is shown in

Table 7.

Table 6: Business strategy mean scores

Defender strategy mean Prospector strategy mean

3.11 3.60

Operating excellence/cost focus mean Product leadership/quality focus mean

3.98 3.65

Rew

aR

d m

an

ag

em

en

t 2013

11

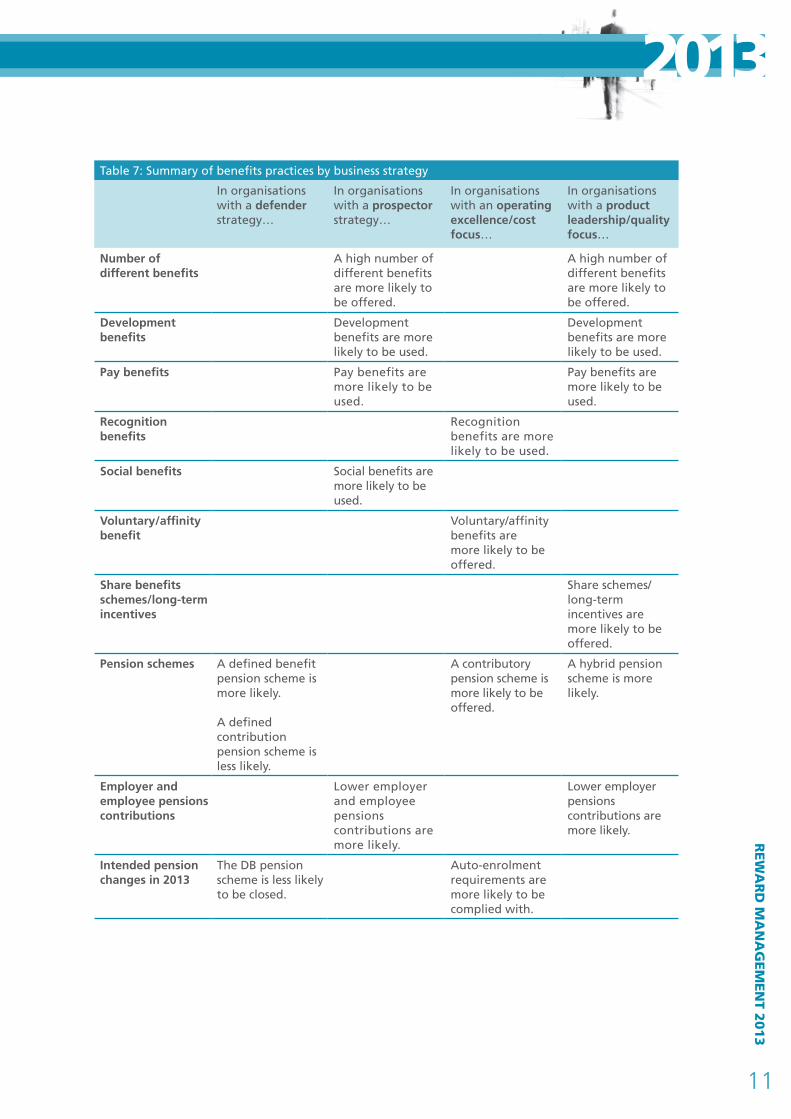

2013Table 7: Summary of benefits practices by business strategy

In organisations with a defender strategy…

In organisations with a prospector strategy…

In organisations with an operating excellence/cost focus…

In organisations with a product leadership/quality focus…

Number of different benefits

A high number of different benefits are more likely to be offered.

A high number of different benefits are more likely to be offered.

Development benefits

Development benefits are more likely to be used.

Development benefits are more likely to be used.

Pay benefits Pay benefits are more likely to be used.

Pay benefits are more likely to be used.

Recognition benefits

Recognition benefits are more likely to be used.

Social benefits Social benefits are more likely to be used.

Voluntary/affinity benefit

Voluntary/affinity benefits are more likely to be offered.

Share benefits schemes/long-term incentives

Share schemes/long-term incentives are more likely to be offered.

Pension schemes A defined benefit pension scheme is more likely.

A defined contribution pension scheme is less likely.

A contributory pension scheme is more likely to be offered.

A hybrid pension scheme is more likely.

Employer and employee pensions contributions

Lower employer and employee pensions contributions are more likely.

Lower employer pensions contributions are more likely.

Intended pension changes in 2013

The DB pension scheme is less likely to be closed.

Auto-enrolment requirements are more likely to be complied with.

cipd.co.uk/rewardm

anagementsurvey

12

RewaRd management

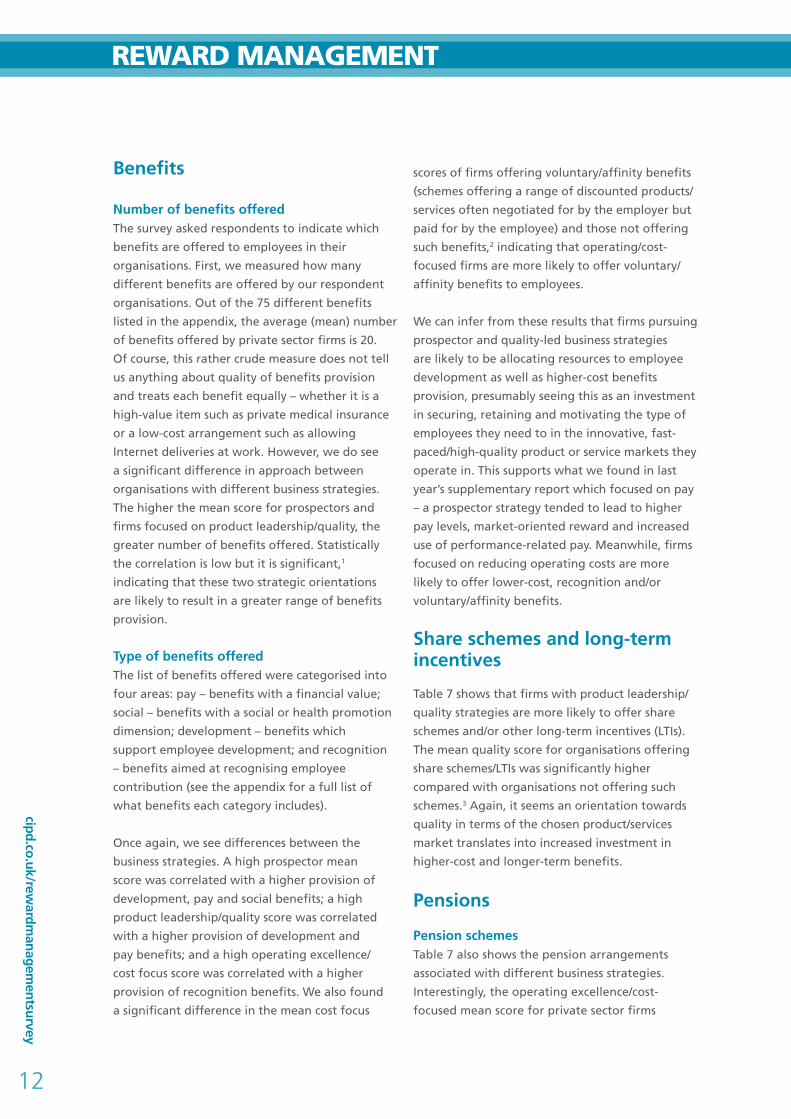

Benefits

Number of benefits offered The survey asked respondents to indicate which

benefits are offered to employees in their

organisations. First, we measured how many

different benefits are offered by our respondent

organisations. Out of the 75 different benefits

listed in the appendix, the average (mean) number

of benefits offered by private sector firms is 20.

Of course, this rather crude measure does not tell

us anything about quality of benefits provision

and treats each benefit equally – whether it is a

high-value item such as private medical insurance

or a low-cost arrangement such as allowing

Internet deliveries at work. However, we do see

a significant difference in approach between

organisations with different business strategies.

The higher the mean score for prospectors and

firms focused on product leadership/quality, the

greater number of benefits offered. Statistically

the correlation is low but it is significant,1

indicating that these two strategic orientations

are likely to result in a greater range of benefits

provision.

Type of benefits offeredThe list of benefits offered were categorised into

four areas: pay – benefits with a financial value;

social – benefits with a social or health promotion

dimension; development – benefits which

support employee development; and recognition

– benefits aimed at recognising employee

contribution (see the appendix for a full list of

what benefits each category includes).

Once again, we see differences between the

business strategies. A high prospector mean

score was correlated with a higher provision of

development, pay and social benefits; a high

product leadership/quality score was correlated

with a higher provision of development and

pay benefits; and a high operating excellence/

cost focus score was correlated with a higher

provision of recognition benefits. We also found

a significant difference in the mean cost focus

scores of firms offering voluntary/affinity benefits

(schemes offering a range of discounted products/

services often negotiated for by the employer but

paid for by the employee) and those not offering

such benefits,2 indicating that operating/cost-

focused firms are more likely to offer voluntary/

affinity benefits to employees.

We can infer from these results that firms pursuing

prospector and quality-led business strategies

are likely to be allocating resources to employee

development as well as higher-cost benefits

provision, presumably seeing this as an investment

in securing, retaining and motivating the type of

employees they need to in the innovative, fast-

paced/high-quality product or service markets they

operate in. This supports what we found in last

year’s supplementary report which focused on pay

– a prospector strategy tended to lead to higher

pay levels, market-oriented reward and increased

use of performance-related pay. Meanwhile, firms

focused on reducing operating costs are more

likely to offer lower-cost, recognition and/or

voluntary/affinity benefits.

Share schemes and long-term incentives

Table 7 shows that firms with product leadership/

quality strategies are more likely to offer share

schemes and/or other long-term incentives (LTIs).

The mean quality score for organisations offering

share schemes/LTIs was significantly higher

compared with organisations not offering such

schemes.3 Again, it seems an orientation towards

quality in terms of the chosen product/services

market translates into increased investment in

higher-cost and longer-term benefits.

Pensions

Pension schemesTable 7 also shows the pension arrangements

associated with different business strategies.

Interestingly, the operating excellence/cost-

focused mean score for private sector firms

Rew

aR

d m

an

ag

em

en

t 2013

13

2013offering contributory pension schemes was

significantly higher than the score for firms not

offering contributory pension schemes,4 indicating

these firms are more likely to offer contributory

pension schemes. This could be linked to

size of organisation – we would expect large

organisations to be more likely to contribute to

pension schemes (not least because of recent

changes to pensions regulation) and we also see

the cost focus mean scores increase as companies

get larger (although due to small numbers of very

large organisations in this survey it is not possible

to say this with certainty).

We also found that having a defender strategic

orientation was more likely to result in a defined

benefit pension scheme being offered5 and less

likely (p<0.05) to result in a defined contribution

scheme being offered6 (see Figure 1). This seems to

be an example of expected ‘fit’ between strategy

and practice – defenders are more likely to be

in traditional, stable product markets where we

would expect to find remnants of private sector

DB pension schemes.

In contrast, Figure 2 shows that the product

leadership/quality strategic orientation was more

likely to result in hybrid pension schemes being

offered to employees.7 While hybrid pensions remain

relatively rare (the 2013 CIPD Reward Management

survey showed only 7% of respondents with a

pension scheme offering a hybrid scheme), they

may well be growing in popularity due to the

‘halfway house’ nature of the provision – sharing risk

between employer and employee rather than asking

one party to shoulder it all. It is interesting that it

should be the quality-led strategy that is connected

with such schemes, perhaps as a result of these

organisations’ inclination to try newer ideas.

figure 1: Pension schemes by defender strategy

3.00

3.60

3.103.20

Definedbenefitscheme

Defined contribution

scheme

Management Other

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Def

end

er s

core

figure 2: Hybrid pension schemes by product leadership/quality focus

3.60

3.90

Hybridpensionscheme

No hybridpensionscheme

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Pro

du

ct le

ader

ship

/qu

alit

y fo

cus

sco

re

cipd.co.uk/rewardm

anagementsurvey

14

RewaRd management

Employer and employee pensions contributionsWhen it comes to the level of employer and

employee contributions to occupational pension

schemes, results show that a prospector strategy is

directly correlated to lower contributions from both

employers and employees8 (that is, the higher the

prospector mean score the lower the contribution

levels and vice versa). The correlation is quite low

and, as with all correlations, there is no causality

indicated (we cannot say for example that a

prospector strategy causes low contribution rates or

vice versa; the result may be due to a third influence

outside the scope of study) but there is a connection

here worth investigating further, especially as

this seems out of kilter with other results which

indicate prospectors are more likely to invest in

employee benefits provision. Similarly results show

a correlation between product leadership/quality

strategy and low employer contributions, which

again do not fit the pattern of results so far. This

may well be an area for future research focus.

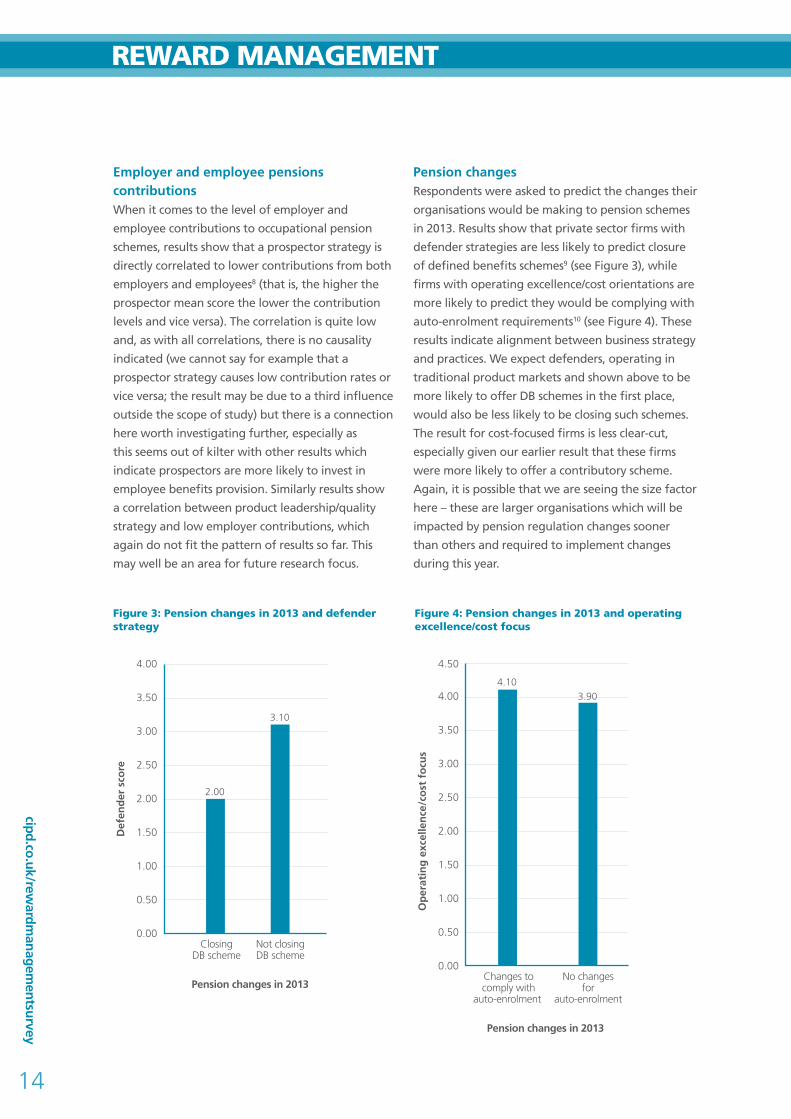

Pension changesRespondents were asked to predict the changes their

organisations would be making to pension schemes

in 2013. Results show that private sector firms with

defender strategies are less likely to predict closure

of defined benefits schemes9 (see Figure 3), while

firms with operating excellence/cost orientations are

more likely to predict they would be complying with

auto-enrolment requirements10 (see Figure 4). These

results indicate alignment between business strategy

and practices. We expect defenders, operating in

traditional product markets and shown above to be

more likely to offer DB schemes in the first place,

would also be less likely to be closing such schemes.

The result for cost-focused firms is less clear-cut,

especially given our earlier result that these firms

were more likely to offer a contributory scheme.

Again, it is possible that we are seeing the size factor

here – these are larger organisations which will be

impacted by pension regulation changes sooner

than others and required to implement changes

during this year.

figure 3: Pension changes in 2013 and defender strategy

figure 4: Pension changes in 2013 and operating excellence/cost focus

3.10

2.00

ClosingDB scheme

Not closingDB scheme

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Def

end

er s

core

Pension changes in 2013

3.904.10

Changes tocomply with

auto-enrolment

Pension changes in 2013

No changesfor

auto-enrolment

0.00

1.00

0.50

2.00

1.50

4.00

4.50

3.50

3.00

2.50

Op

erat

ing

exc

elle

nce

/co

st f

ocu

s

Rew

aR

d m

an

ag

em

en

t 2013

15

2013

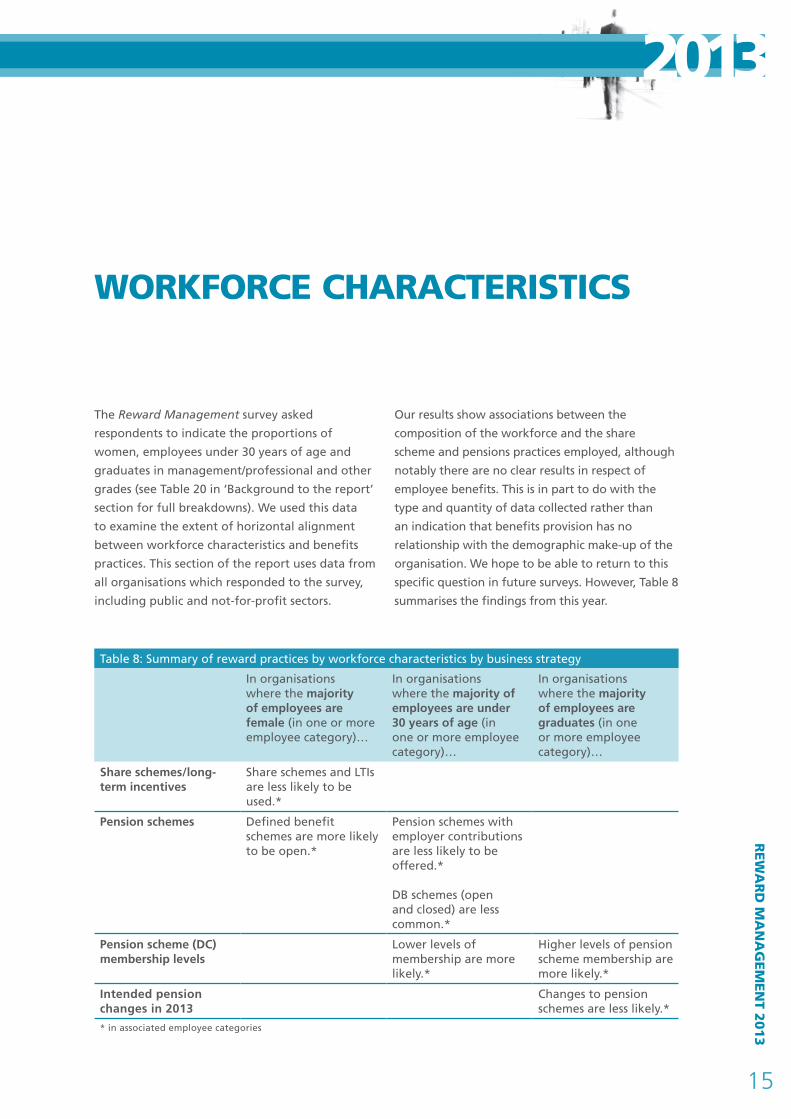

wORkfORCe CHaRaCteRiStiCS

The Reward Management survey asked

respondents to indicate the proportions of

women, employees under 30 years of age and

graduates in management/professional and other

grades (see Table 20 in ‘Background to the report’

section for full breakdowns). We used this data

to examine the extent of horizontal alignment

between workforce characteristics and benefits

practices. This section of the report uses data from

all organisations which responded to the survey,

including public and not-for-profit sectors.

Our results show associations between the

composition of the workforce and the share

scheme and pensions practices employed, although

notably there are no clear results in respect of

employee benefits. This is in part to do with the

type and quantity of data collected rather than

an indication that benefits provision has no

relationship with the demographic make-up of the

organisation. We hope to be able to return to this

specific question in future surveys. However, Table 8

summarises the findings from this year.

Table 8: Summary of reward practices by workforce characteristics by business strategy

In organisations where the majority of employees are female (in one or more employee category)…

In organisations where the majority of employees are under 30 years of age (in one or more employee category)…

In organisations where the majority of employees are graduates (in one or more employee category)…

Share schemes/long-term incentives

Share schemes and LTIs are less likely to be used.*

Pension schemes Defined benefit schemes are more likely to be open.*

Pension schemes with employer contributions are less likely to be offered.*

DB schemes (open and closed) are less common.*

Pension scheme (DC) membership levels

Lower levels of membership are more likely.*

Higher levels of pension scheme membership are more likely.*

Intended pension changes in 2013

Changes to pension schemes are less likely.*

* in associated employee categories

cipd.co.uk/rewardm

anagementsurvey

16

RewaRd management

Female employees

Share schemes and long-term incentive plans (LTIs)Table 8 and Figure 5 show a very clear association

between the proportion of women employed in

organisations and the offering of a share scheme or

other LTI plan. Where women are in the majority,

organisations are far less likely to offer employee

share plans.11 The reason for this may not be readily

apparent but is likely to be due to the occupational

segregation of women into public sector jobs where

share schemes are unavailable. Our survey results

show that 81% of public sector organisations have a

general workforce of which over half are women as

opposed to 59.7% of private sector services and 39%

of manufacturing and production companies. Yet the

public sector only accounts for 23.6% of respondents,

so there may well be other factors at work here.

Pension schemesFigure 6 shows that organisations with higher

proportions of women in non-management/

professional roles are more likely to offer

a defined benefit pension scheme12 while

organisations with fewer women in this employee

category are more likely to offer a defined

contribution scheme.13 Once again we may well

be seeing the influence of higher proportions of

women working in the public sector, where DB

pensions are still common.

While we cannot discount the link between

proportion of women employees and benefits

practices, the results in this area would seem to

indicate that sectoral influence is a stronger factor in

determining share scheme and pension arrangements

than the gender composition of the workforce.

figure 5: Share schemes and proportion of women in management/professional roles (% of respondents)

figure 6: Pension scheme types and proportion of women in non-management/professional roles (% of respondents)

None The minority About half The majority

Proportion of women in management/professional roles

0

20

10

40

30

80

100

90

70

60

50

Res

po

nd

ents

%

Share schemes

Share schemes (all respondents)

No share schemes

No share schemes (all respondents)

The minority About half The majority

Proportion of women in non-management/professional roles

0

20

10

40

30

70

60

50

Res

po

nd

ents

%

Defined benefit

Defined benefit (all respondents)

Defined contribution

Defined contribution (all respondents)

Rew

aR

d m

an

ag

em

en

t 2013

17

2013Young employees

Pension schemesResults show a clear relationship between

the proportion of young workers (under 30

years old) and whether or not employers

contribute to an occupational pension scheme

(see Figure 7). Where younger workers are

the majority of management/professionals,

a contributory pension scheme is less likely.14

This seems to be a straightforward example

of alignment of workforce characteristics with

pension arrangements; presumably employees

under 30 years of age are less likely to value a

contributory pension scheme and therefore it

is not needed to recruit and retain them so a

proportion of organisations are choosing not to

offer it. Size of organisation may well also be a

factor here. We know that SMEs are less likely

to contribute to pension schemes than their

larger counterparts (just 81.2% compared with

97.7% of large organisations and 100% of very

large organisations) and we also found that the

proportion of young managers/professionals is

greater in SMEs. However, results show that there

is also a relationship between proportions of non-

management young workers and contribution

to pension scheme where the difference in rates

of employment by organisation size is far less

pronounced, so it does seem there is an alignment

of practice and workforce composition here.

In addition, results show that defined benefit

pension schemes are less common in organisations

with higher proportions of young people in both

management and non-management employee

categories. Presumably this is due to younger

people working in more non-traditional sectors of

the labour market where DB pension schemes are

no longer (or never have been) offered.

figure 7: Contributory pension schemes and proportion of young (under 30 years of age) managers/professionals (% of respondents)

The minority About half The majority

Proportion of young people in management/professional roles

0

20

10

40

30

70

80

90

100

60

50

Res

po

nd

ents

%

Contributorypension scheme

Contributorypension scheme (all respondents)

No contributorypension scheme

No contributorypension scheme (all respondents)

cipd.co.uk/rewardm

anagementsurvey

18

RewaRd management

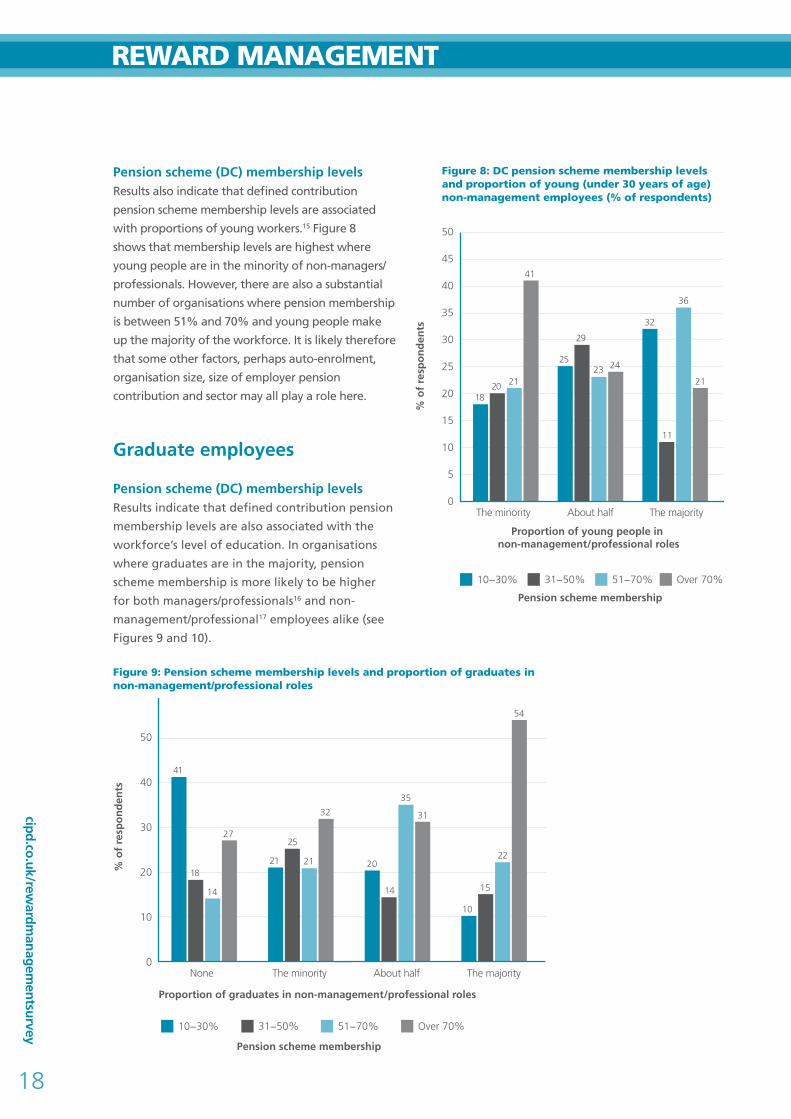

Pension scheme (DC) membership levelsResults also indicate that defined contribution

pension scheme membership levels are associated

with proportions of young workers.15 Figure 8

shows that membership levels are highest where

young people are in the minority of non-managers/

professionals. However, there are also a substantial

number of organisations where pension membership

is between 51% and 70% and young people make

up the majority of the workforce. It is likely therefore

that some other factors, perhaps auto-enrolment,

organisation size, size of employer pension

contribution and sector may all play a role here.

Graduate employees

Pension scheme (DC) membership levelsResults indicate that defined contribution pension

membership levels are also associated with the

workforce’s level of education. In organisations

where graduates are in the majority, pension

scheme membership is more likely to be higher

for both managers/professionals16 and non-

management/professional17 employees alike (see

Figures 9 and 10).

figure 8: dC pension scheme membership levels and proportion of young (under 30 years of age) non-management employees (% of respondents)

figure 9: Pension scheme membership levels and proportion of graduates in non-management/professional roles

1820 21

41

25

29

23

32

11

36

21

24

% o

f re

spo

nd

ents

Proportion of young people in non-management/professional roles

10−30% 31−50% 51−70% Over 70%

0

20

10

15

5

25

50

30

35

40

45

The minority About half The majority

Pension scheme membership

41

18

14

27

21

25

21 20

14

35

31

10

22

15

54

32

% o

f re

spo

nd

ents

Proportion of graduates in non-management/professional roles

Pension scheme membership

0

20

10

40

30

60

50

10−30% 31−50% 51−70% Over 70%

None The minority About half The majority

Rew

aR

d m

an

ag

em

en

t 2013

19

2013Reasons for these results could be in part due

to the influence of industry sector. Public sector

services employ a higher proportion of graduates

in management/professional roles than any

other sector (37% compared with 33% in private

sector services, 32% in the voluntary sector and

26% in manufacturing and production firms)

and also have the highest levels of DC pension

scheme membership levels (63% of public

sector organisations have membership over

70% compared with 34% of manufacturing and

production, 27% of private sector services and

25% of voluntary sector employers).

However, Figure 10 shows the same association

between higher pension membership and higher

proportion of graduates but in non-management

roles where there is no sectoral effect. Presumably,

then, graduates themselves are more likely to join

pension schemes or are working in organisations that

are more likely to offer and promote DC pensions.

figure 10: Pension scheme membership levels and proportion of graduates in management/professional roles

26 26 26

22

31

20

1513

26

33

28

13

2119

47

34

% o

f re

spo

nd

ents

Proportion of graduates in management/professional roles

0

20

10

40

30

60

50

10−30% 31−50% 51−70% Over 70%

None The minority About half The majority

Pension scheme membership

cipd.co.uk/rewardm

anagementsurvey

20

RewaRd management

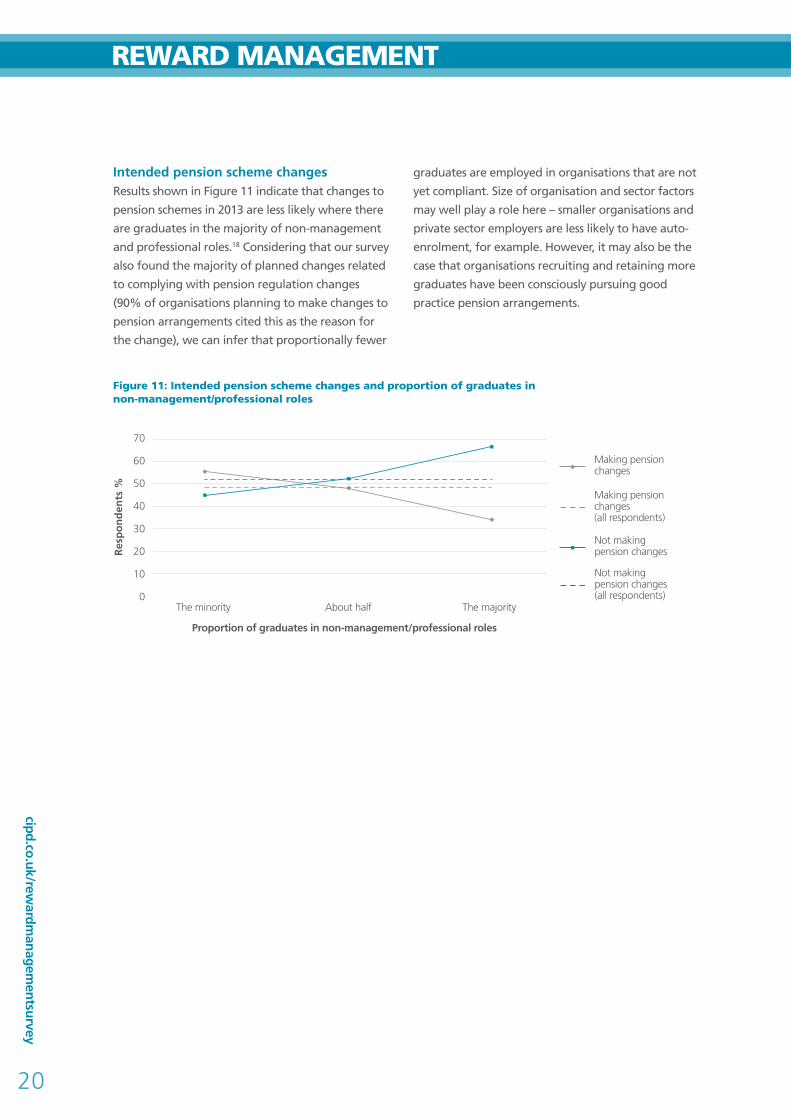

Intended pension scheme changesResults shown in Figure 11 indicate that changes to

pension schemes in 2013 are less likely where there

are graduates in the majority of non-management

and professional roles.18 Considering that our survey

also found the majority of planned changes related

to complying with pension regulation changes

(90% of organisations planning to make changes to

pension arrangements cited this as the reason for

the change), we can infer that proportionally fewer

graduates are employed in organisations that are not

yet compliant. Size of organisation and sector factors

may well play a role here – smaller organisations and

private sector employers are less likely to have auto-

enrolment, for example. However, it may also be the

case that organisations recruiting and retaining more

graduates have been consciously pursuing good

practice pension arrangements.

The minority About half The majority

Proportion of graduates in non-management/professional roles

0

20

10

40

30

70

60

50

Res

po

nd

ents

%

Making pensionchanges

Making pensionchanges (all respondents)

Not makingpension changes

Not makingpension changes (all respondents)

figure 11: intended pension scheme changes and proportion of graduates in non-management/professional roles

Rew

aR

d m

an

ag

em

en

t 2013

21

2013

For the second year, the CIPD Reward Management

survey asked respondents to comment on general

HR conditions within their organisations as well

as specific reward-related subjects. This allowed

us to determine if particular benefits practices are

associated with positive or negative HR outcomes

in the workplace and results have shown this to be

the case to some extent.

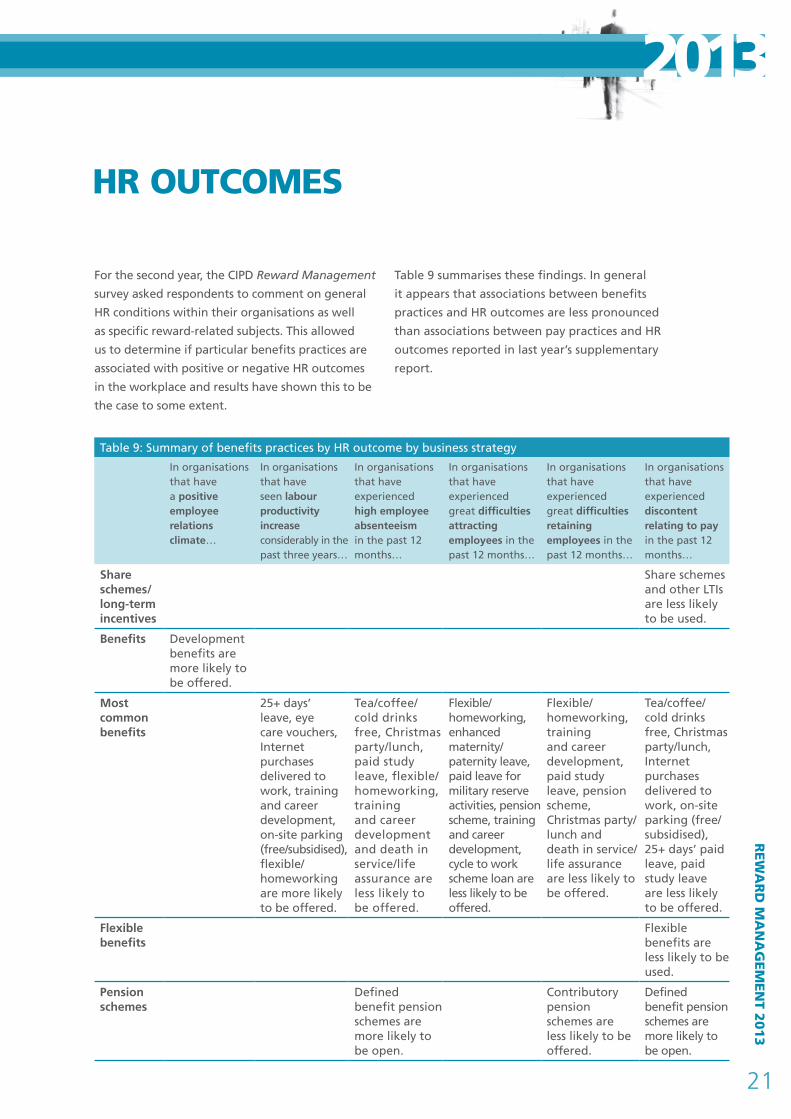

Table 9 summarises these findings. In general

it appears that associations between benefits

practices and HR outcomes are less pronounced

than associations between pay practices and HR

outcomes reported in last year’s supplementary

report.

Table 9: Summary of benefits practices by HR outcome by business strategy

In organisations that have a positive employee relations climate…

In organisations that have seen labour productivity increase considerably in the past three years…

In organisations that have experienced high employee absenteeism in the past 12 months…

In organisations that have experienced great difficulties attracting employees in the past 12 months…

In organisations that have experienced great difficulties retaining employees in the past 12 months…

In organisations that have experienced discontent relating to pay in the past 12 months…

Share schemes/long-term incentives

Share schemes and other LTIs are less likely to be used.

Benefits Development benefits are more likely to be offered.

Most common benefits

25+ days’ leave, eye care vouchers, Internet purchases delivered to work, training and career development, on-site parking (free/subsidised), flexible/homeworking are more likely to be offered.

Tea/coffee/cold drinks free, Christmas party/lunch, paid study leave, flexible/homeworking, training and career development and death in service/life assurance are less likely to be offered.

Flexible/homeworking, enhanced maternity/paternity leave, paid leave for military reserve activities, pension scheme, training and career development, cycle to work scheme loan are less likely to be offered.

Flexible/homeworking, training and career development, paid study leave, pension scheme, Christmas party/lunch and death in service/life assurance are less likely to be offered.

Tea/coffee/cold drinks free, Christmas party/lunch, Internet purchases delivered to work, on-site parking (free/subsidised), 25+ days’ paid leave, paid study leave are less likely to be offered.

Flexible benefits

Flexible benefits are less likely to be used.

Pension schemes

Defined benefit pension schemes are more likely to be open.

Contributory pension schemes are less likely to be offered.

Defined benefit pension schemes are more likely to be open.

HR OutCOmeS

cipd.co.uk/rewardm

anagementsurvey

22

RewaRd management

Employee relations climate

Figure 12 shows extensive development-

oriented benefits are more likely to be offered in

organisations with good or very good employee

relations climates and less likely to be offered

by organisations with neither good nor bad,

somewhat strained or very strained employee

relations climates.19 This finding suggests a clear

relationship between the provision of employee

development and employee relations, which has

implications for organisations assessing the impact

of their total reward offering.

Labour productivity

Our results showed that organisations that had

seen labour productivity increase considerably in

the past three years are more likely to offer 25+

days’ leave (offered by 81.7% of respondents

with labour productivity that had increased

considerably in the past three years compared

with the 73.0% of all respondents which offer 25+

days’ leave); eye care vouchers (63.4% compared

with 60.9%); allow Internet purchases delivered

to work (63.4% compared with 58.6%); training

and career development (87.8% compared with

83.1%); free/subsidised on-site parking (62.2%

compared with 58.1%); and flexible/homeworking

(46.3% compared with 43.2%). We need to be

cautious about overstating these links and treating

each of them in isolation; however, we can say

that these benefits are offered in organisations

that have increased in productivity and there may

be an association.

Recruitment, retention andabsenteeism

BenefitsTables 10, 11 and 12 show benefits which are less

likely to be offered by organisations which have

experienced absenteeism (Table 10), recruitment

(Table 11) and retention (Table 12) difficulties in

the past 12 months. There are some intriguing

findings here: flexible/homeworking and training/

career development feature on all three lists;

pension schemes and Christmas parties – while

opposite ends of the scale in terms of employer

investment – are equally well represented.

Speculating about the reasons for these results,

it is perhaps helpful to think of the absence of

these benefits as characteristic of organisations

experiencing these employee problems rather

than as cause and effect equations. It would

be erroneous, for example, to deduce that

the lack of free tea or coffee at work leads to

absenteeism difficulties. However, we could expect

Good Very good Neither goodnor bad

Somewhatstrained

Verystrained

Employee relations climate

0

4

2

8

6

16

14

12

10

Res

po

nd

ents

%

Over 50% ofdevelopmentbenefits offered

Over 50% ofdevelopmentbenefits offered (all respondents)

figure 12: development benefits and employee relations climate

Rew

aR

d m

an

ag

em

en

t 2013

23

2013

Table 10: Benefits less likely to be offered by organisations with employee absenteeism difficulties

Benefit % of all respondents offering benefit

% of respondents that have experienced absenteeism difficulties to a great extent in the past year offering benefit

% difference

Tea/coffee/cold drinks free 64.6 32.4 32.2

Christmas party/lunch 66.0 45.9 20.1

Paid study leave 45.9 29.7 16.2

Flexible/homeworking 43.2 29.7 13.5

Training and career development 82.9 70.3 12.6

Death in service/life assurance 66.7 54.1 12.6

Table 11: Benefits less likely to be offered by organisations with employee recruitment difficulties

Benefit % of all respondents offering benefit

% of respondents that have experienced recruitment difficulties to a great extent in the past year offering benefit

% difference

Flexible/homeworking 43.3 20.5 22.8

Enhanced maternity/paternity leave 55.8 43.2 12.6

Paid leave for military reserve activities 48.5 36.4 12.1

Pension schemes 82.5 70.5 12.0

Training and career development 82.7 72.7 10.0

Cycle to work scheme loans 45.6 36.4 9.2

Table 12: Benefits less likely to be offered by organisations with employee retention difficulties

Benefit % of all respondents offering benefit

% of respondents that have experienced employee retention difficulties to a great extent in the past year offering benefit

% difference

Flexible/homeworking 43.5 16.7 26.8

Training and career development 82.6 66.7 15.9

Paid study leave 45.8 31.0 14.8

Pension schemes 82.6 69.0 13.6

Christmas party/lunch 65.9 52.4 13.5

Death in service/life assurance 66.6 54.8 11.8

that organisations experiencing recruitment

and retention difficulties would be less likely to

agree to flexible working requests if they were

already under-staffed. Overall, we get a picture

of organisations perhaps unable to offer certain

benefits because of employee problems, which in

turn makes them less attractive places to work,

which exacerbates the problems and so on.

cipd.co.uk/rewardm

anagementsurvey

24

RewaRd management

Pension schemesWhen it comes to pension arrangements, we found

organisations which have experienced employee

retention difficulties in the past year are less likely to

offer a contributory pension scheme to employees20

(see Figure 13) and organisations which have

experienced absenteeism problems are more likely to

operate an open defined benefit pension scheme21

(see Figure 14). It is probable there are other factors

such as sector or size of organisation influencing

these findings; we know, for example, that higher

absenteeism rates and open DB pension schemes are

both more common in the public sector.

To a great extent To some extent Not at all

Employee retention difficulties

74

78

76

82

80

88

90

92

94

86

84

Res

po

nd

ents

% Contributorypension scheme

Contributorypension scheme (all respondents)

figure 13: Contributory pension scheme and employee retention difficulties

figure 14: Open defined benefit pension scheme and employee absenteeism

To a great extent To some extent Not at all

Employee absenteeism

0

10

5

20

15

35

40

45

50

30

25

Res

po

nd

ents

% Defined benefitpension scheme

Defined benefitpension scheme (all respondents)

Rew

aR

d m

an

ag

em

en

t 2013

25

2013Pay discontent

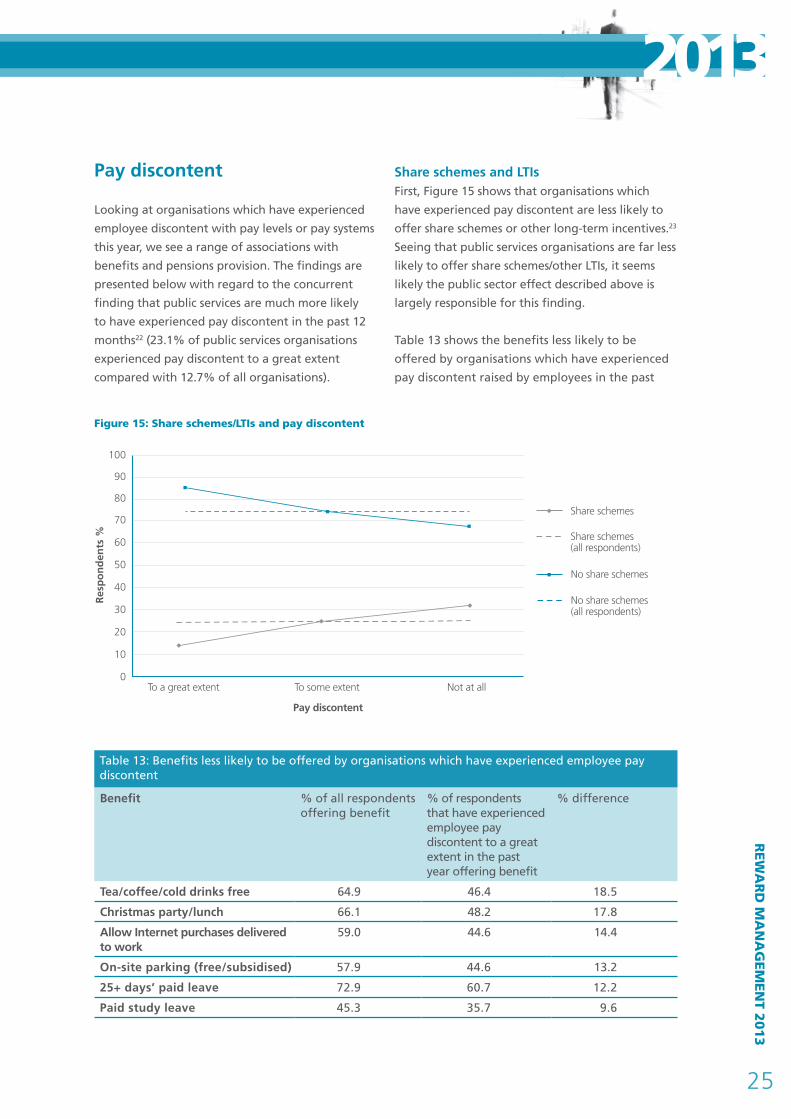

Looking at organisations which have experienced

employee discontent with pay levels or pay systems

this year, we see a range of associations with

benefits and pensions provision. The findings are

presented below with regard to the concurrent

finding that public services are much more likely

to have experienced pay discontent in the past 12

months22 (23.1% of public services organisations

experienced pay discontent to a great extent

compared with 12.7% of all organisations).

Share schemes and LTIsFirst, Figure 15 shows that organisations which

have experienced pay discontent are less likely to

offer share schemes or other long-term incentives.23

Seeing that public services organisations are far less

likely to offer share schemes/other LTIs, it seems

likely the public sector effect described above is

largely responsible for this finding.

Table 13 shows the benefits less likely to be

offered by organisations which have experienced

pay discontent raised by employees in the past

figure 15: Share schemes/Ltis and pay discontent

To a great extent To some extent Not at all

Pay discontent

0

20

10

40

30

70

80

90

100

60

50

Res

po

nd

ents

%

Share schemes

Share schemes (all respondents)

No share schemes

No share schemes (all respondents)

Table 13: Benefits less likely to be offered by organisations which have experienced employee pay discontent

Benefit % of all respondents offering benefit

% of respondents that have experienced employee pay discontent to a great extent in the past year offering benefit

% difference

Tea/coffee/cold drinks free 64.9 46.4 18.5

Christmas party/lunch 66.1 48.2 17.8

Allow Internet purchases delivered to work

59.0 44.6 14.4

On-site parking (free/subsidised) 57.9 44.6 13.2

25+ days’ paid leave 72.9 60.7 12.2

Paid study leave 45.3 35.7 9.6

cipd.co.uk/rewardm

anagementsurvey

26

RewaRd management

year.24 This set of data, viewed in its entirety,

gives us a picture of benefits provision where pay

levels and/or systems have been raised as an issue

by employees. Surprisingly few of these benefits

are high-cost items, which we might anticipate

if pay is also restricted. The public sector factor

is likely to be an influence here, however, as we

find these more informal benefits – free tea/

coffee, employer-funded Christmas parties and

Internet purchases delivered to work – are also less

common in large public services organisations.

Results also show that organisations experiencing pay

discontent to a great extent are less likely to operate

flexible benefits25 (85.5% of organisations with a

great extent of pay discontent do not offer flexible

benefits compared with 75.2% of all organisations).

But once again, public sector organisations are also

less likely to offer flexible benefits.

Pension schemesFinally in this section, Figure 16 shows the

association between pay discontent and open

DB pension schemes. And, once again, this

result is likely to be primarily due to open DB

schemes being much more common in the public

sector, where we know pay is an ongoing cause

of employee discontent as austerity measures

continue to be felt.

figure 13: Contributory pension scheme and employee retention difficulties

To a great extent To some extent Not at all

Pay discontent

0

10

5

20

15

35

30

25

Res

po

nd

ents

%

Defined benefitpension scheme

Defined benefitpension scheme (all respondents)

Rew

aR

d m

an

ag

em

en

t 2013

27

2013

Following on from last year’s investigation into pay

secrecy versus transparency in organisations, for

2013 we asked respondents about the approach to

transparency of benefits specifically and the extent

to which organisations are prepared to disclose

to employees information about pensions and

employee benefits and how individuals or groups

of employees are treated the same or differently.

Table 14 shows the findings. The results as a whole

give a very clear picture of organisations which

prefer a more transparent approach to benefits

having a well-developed benefits offering, active

pension arrangements and indications of a total

reward approach, while the reverse is the case for

organisations which prefer to be secretive about

employee benefits. While we need to be cautious

Table 14: Benefits secrecy and benefits management practices

Organisations which prefer to be secretive about benefits are…

Organisations that prefer to be transparent about benefits are…

Number of different benefits More likely to offer a lower number of different benefits.

More likely to offer a higher number of different benefits.

Development benefits Less likely to offer development benefits.

More likely to offer development benefits.

Pay benefits Less likely to offer pay benefits. More likely to offer pay benefits.

Social benefits Less likely to offer social benefits.

More likely to offer social benefits.

Voluntary/affinity benefits Less likely to offer voluntary/affinity benefits.

More likely to offer voluntary/affinity benefits.

Total reward statements Less likely to offer total reward statements.

More likely to offer total reward statements.

Change in spend on share schemes/LTIs

More likely to predict that spend on share schemes/LTIs will decrease or stay the same.

More likely to predict that spend on share schemes/LTIs will increase.

Pension schemes More likely to offer to contribute to a personal pension plan.

More likely to offer a defined benefit pension scheme.

Auto-enrolment to a DC pension scheme

Less likely to auto-enrol employees into a pension scheme.

More likely to auto-enrol employees into a pension scheme.

Pension scheme (DC) membership levels

More likely to have under 50% pension scheme membership.

More likely to have over 50% pension scheme membership.

Employer and employee pensions contributions

More likely to have low employer and employee contributions.

More likely to have high employer and employee contributions.

BenefitS tRanSPaRenCy

cipd.co.uk/rewardm

anagementsurvey

28

RewaRd management

about causality – we cannot claim, for example,

that a secretive approach to benefits causes a

poorer benefits offering or vice versa – there

does seem to be a coherent picture of results that

suggests a strong link between how advanced

an organisation’s benefits provisions are and its

approach to secrecy/transparency.

Benefits and total reward

Table 14 details the benefits provision of

organisations which either prefer to remain

secretive about benefits or are actively transparent

about benefits. Organisations preferring

transparency are more likely to offer a high number

of different workplace benefits and more likely to

offer development-oriented benefits, pay benefits

and social benefits.26 While the correlations are

fairly low,27 the results are clear that the greater the

benefits secrecy, the poorer the benefits offering and,

accordingly, the greater the benefits transparency, the

more extensive the benefits offering.

The results cannot tell us why this is, however

we can presume that organisations which have

well-developed, generous and universal benefits

provisions will naturally want to communicate it to

all employees as a key part of the reward offering

and as a recruitment and retention tool. On the other

hand, organisations which offer limited benefits or

offer benefits for only small, probably senior, sections

of the workforce would be more inclined to keep

these matters confidential. Once again we cannot

discount the sectoral effect here. The main survey

report shows that a more transparent approach to

benefits is found in the public and voluntary sectors,

whereas rather more private sector firms than public

services/voluntary organisations tend towards the

more secretive approaches.

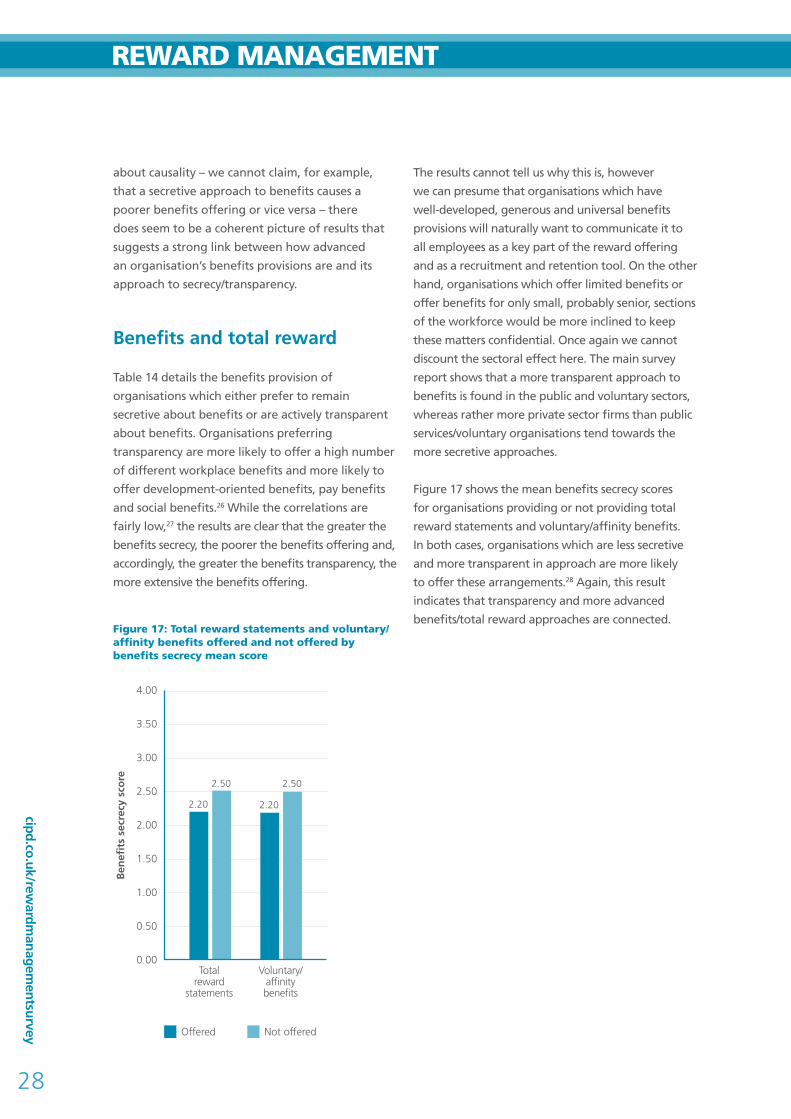

Figure 17 shows the mean benefits secrecy scores

for organisations providing or not providing total

reward statements and voluntary/affinity benefits.

In both cases, organisations which are less secretive

and more transparent in approach are more likely

to offer these arrangements.28 Again, this result

indicates that transparency and more advanced

benefits/total reward approaches are connected.figure 17: total reward statements and voluntary/affinity benefits offered and not offered by benefits secrecy mean score

2.50

2.20 2.20

2.50

Totalreward

statements

Voluntary/affinitybenefits

Offered Not offered

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Ben

efit

s se

crec

y sc

ore

Rew

aR

d m

an

ag

em

en

t 2013

29

2013

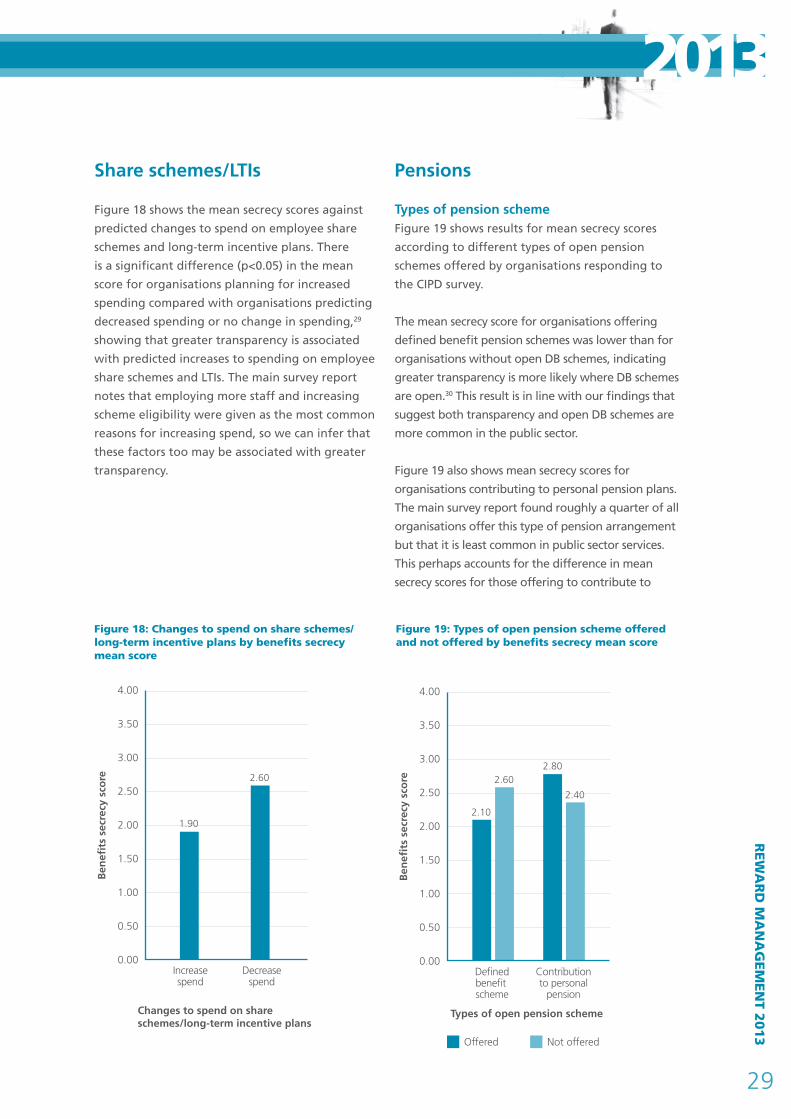

figure 18: Changes to spend on share schemes/long-term incentive plans by benefits secrecy mean score

1.90

2.60

Increasespend

Decreasespend

Changes to spend on share schemes/long-term incentive plans

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Ben

efit

s se

crec

y sc

ore

Share schemes/LTIs

Figure 18 shows the mean secrecy scores against

predicted changes to spend on employee share

schemes and long-term incentive plans. There

is a significant difference (p<0.05) in the mean

score for organisations planning for increased

spending compared with organisations predicting

decreased spending or no change in spending,29

showing that greater transparency is associated

with predicted increases to spending on employee

share schemes and LTIs. The main survey report

notes that employing more staff and increasing

scheme eligibility were given as the most common

reasons for increasing spend, so we can infer that

these factors too may be associated with greater

transparency.

Pensions

Types of pension schemeFigure 19 shows results for mean secrecy scores

according to different types of open pension

schemes offered by organisations responding to

the CIPD survey.

The mean secrecy score for organisations offering

defined benefit pension schemes was lower than for

organisations without open DB schemes, indicating

greater transparency is more likely where DB schemes

are open.30 This result is in line with our findings that

suggest both transparency and open DB schemes are

more common in the public sector.

Figure 19 also shows mean secrecy scores for

organisations contributing to personal pension plans.

The main survey report found roughly a quarter of all

organisations offer this type of pension arrangement

but that it is least common in public sector services.

This perhaps accounts for the difference in mean

secrecy scores for those offering to contribute to

figure 19: types of open pension scheme offered and not offered by benefits secrecy mean score

2.60

2.10

2.80

2.40

Definedbenefit scheme

Contributionto personal

pension

Offered Not offered

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Ben

efit

s se

crec

y sc

ore

Types of open pension scheme

cipd.co.uk/rewardm

anagementsurvey

30

RewaRd management

personal pensions compared with those not offering

such a provision, indicating secrecy is a more common

approach among organisations contributing to

personal pension plans.31

Figure 20 shows a significant difference

between mean benefits secrecy scores for

organisations auto-enrolling employees into

defined contribution schemes and those without

auto-enrolment.32 This indicates an association

between pension scheme auto-enrolment and

greater transparency. Similarly, Figure 21 shows

membership levels of defined contribution

schemes are higher in organisations which favour

a more transparent approach. It is unlikely that

greater transparency in the public sector is an

influence here as only 7.2% of open DC schemes

are in public sector organisations. These results

are a clear indication that there is a relationship

between greater transparency and more advanced

pension scheme arrangements.

Employer and employee pensions contributions to DC schemesOur results also show that there is a low, but

significant, negative correlation between benefits

secrecy scores and rates of employer33 and

employee34 contributions to defined contribution

pension schemes; the greater the benefits secrecy,

the lower the employer and employee contribution

rates. Once again, findings suggest that more

generous pensions provisions are associated with

greater transparency.

Benefits transparency and HR outcomes

In addition to finding that approaches to benefits

transparency are associated with benefits practices,

we also looked at the associations between

transparency/secrecy and HR outcomes. The findings

are summarised in Table 15. They show a consistent

figure 21: membership levels in main defined contribution pension schemes by benefits secrecy mean score

2.30

2.60

Over 50% 50% orlower

Membership levels in mainDC scheme

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Ben

efit

s se

crec

y sc

ore

figure 20: auto-enrolment in defined contribution pension schemes by benefits secrecy mean score

2.20

2.50

Auto-enrolment Noauto-enrolment

Auto-enrolment in DC scheme

0.00

1.00

0.50

2.00

1.50

4.00

3.50

3.00

2.50

Ben

efit

s se

crec

y sc

ore

Rew

aR

d m

an

ag

em

en

t 2013

31

2013picture of more secretive organisations experiencing

negative HR outcomes while more transparent

organisations experience positive results.

For once it is unlikely that there is a sectoral

influence here, or alternatively results have been

arrived at despite the sectoral influence, as we know

the public sector is more likely to experience high

absenteeism and pay discontent, for example, as

well as greater transparency and yet, Table 15 shows

clearly that greater transparency is linked to neither

of these employee problems.

Why should greater benefits transparency be

associated with positive HR outcomes? There are

different possible explanations. One is that where

benefits provisions are extensive and generous,

organisations want to actively promote their

pensions and benefits packages and adopt a

transparent approach; there is a positive employee

experience which encourages employee behaviour

which translates into positive HR outcomes.

Alternatively, we could envisage that organisations

with poor employee relations, productivity levels

and a range of employee problems are unlikely to

be able to invest in extensive and generous benefits

provisions and are inclined not to want to shout

about their poor or unequal benefits offering so

prefer a more secretive approach. On the other

hand, a third unknown factor may be responsible

for both the extent of secrecy/transparency as well

as the positive/negative HR outcomes. However,

despite this caveat, the results are clear – these two

aspects are connected in some way and this could

have profound implications for the communication

of benefits arrangements to employees within

organisations.

Table 15: Benefits secrecy and HR outcomes

Organisations which prefer to be more secretive about benefits are more likely to have…

Organisations that prefer to be more transparent about benefits are more likely to have…

Employee relations climate Strained/very strained employee relations.

Good/very good employee relations.

Labour productivity compared with sector

Labour productivity far/somewhat below average in the sector.

Labour productivity far/somewhat better than the sector.

Labour productivity compared with three years ago

Labour productivity that has decreased in the past three years.

Labour productivity that has increased in the past three years.

Employee absenteeism in past 12 months

Difficulties with high absenteeism rates.

No difficulties with high absenteeism rates.

Employee retention in past 12 months

Difficulties retaining employees. No difficulties retaining employees.

Pay discontent raised by employees in past 12 months

Pay discontent raised by employees.

No pay discontent raised by employees.

cipd.co.uk/rewardm

anagementsurvey

32

RewaRd management

COnCLuSiOnS and imPLiCatiOnS

Employers in the UK invest significantly in

providing their workforce members with non-

cash employee benefits. According to the

benchmarking study published in May 2013,

to which this report is a supplement, many

employers aspire to increase the proportion of

their employee investment related to benefits

compared with the pay element of overall

remuneration.

What this study does is to address questions as to

the strategic nature of investment in employee

benefits: whether statistically significant variation

can be discerned between benefits expenditure

associated with the direction of business strategy

an organisation adopts; whether or not workforce

characteristics play a part in benefits provision

and administration; what the implications

appear to be in terms of HR outcomes; and the