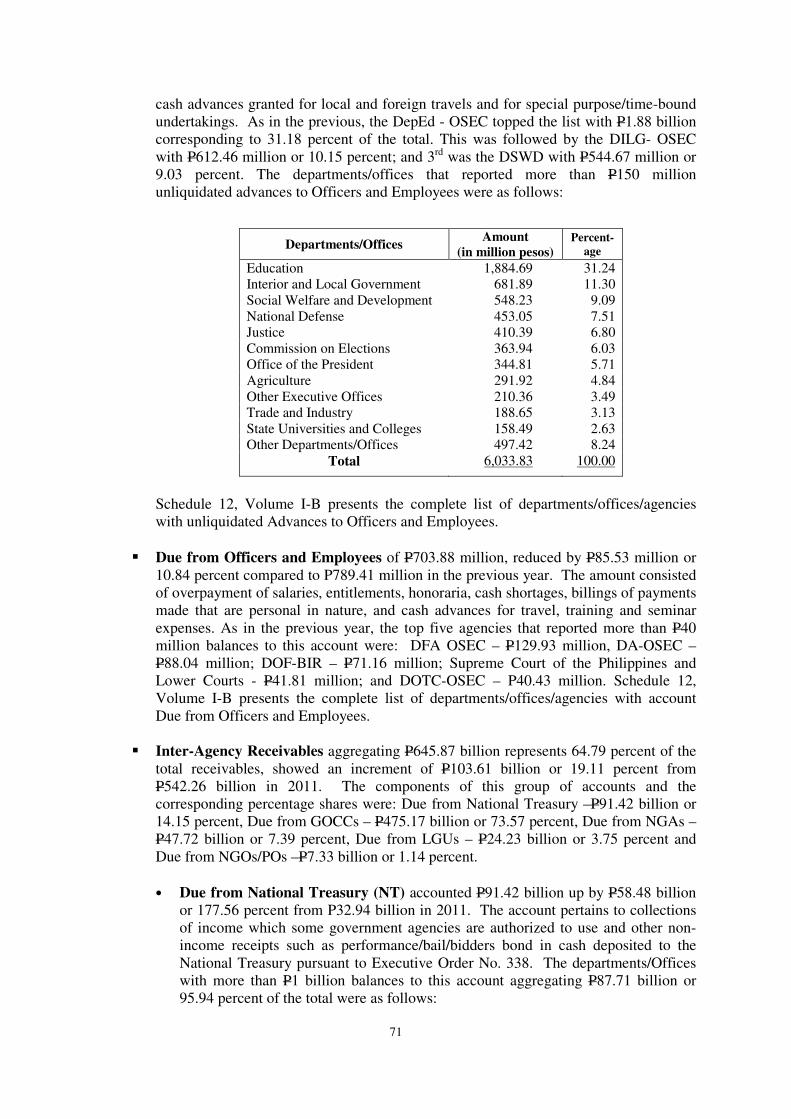

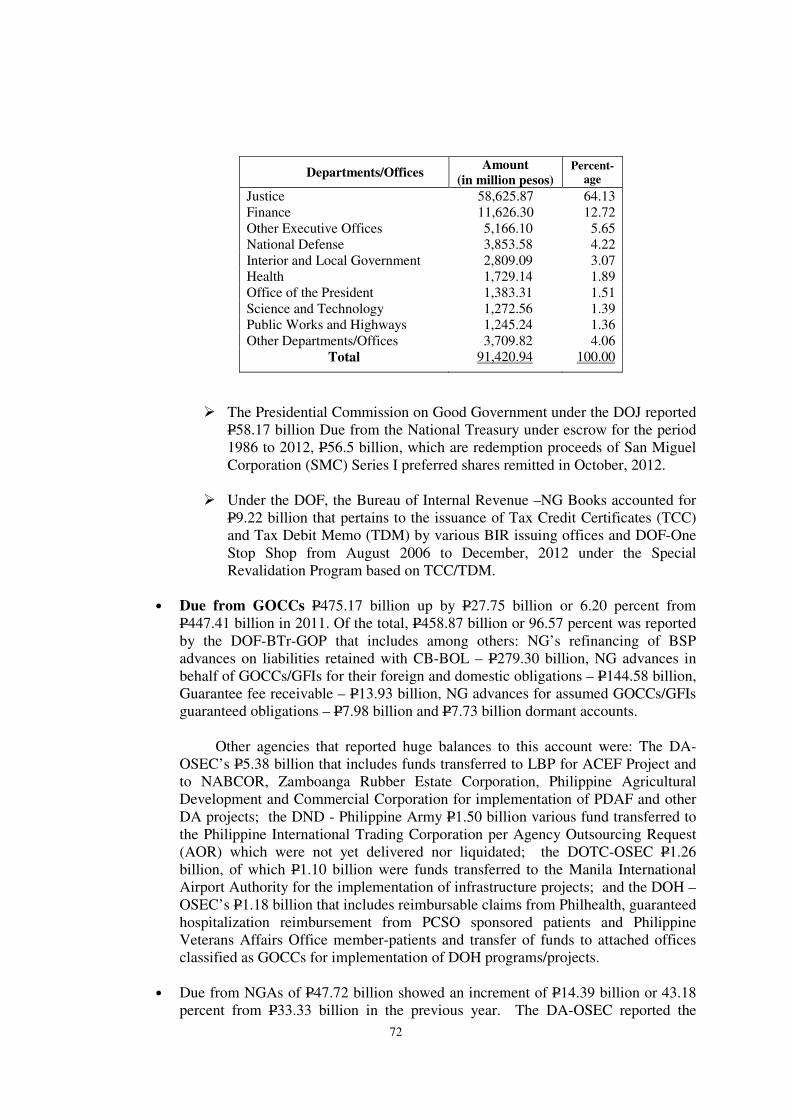

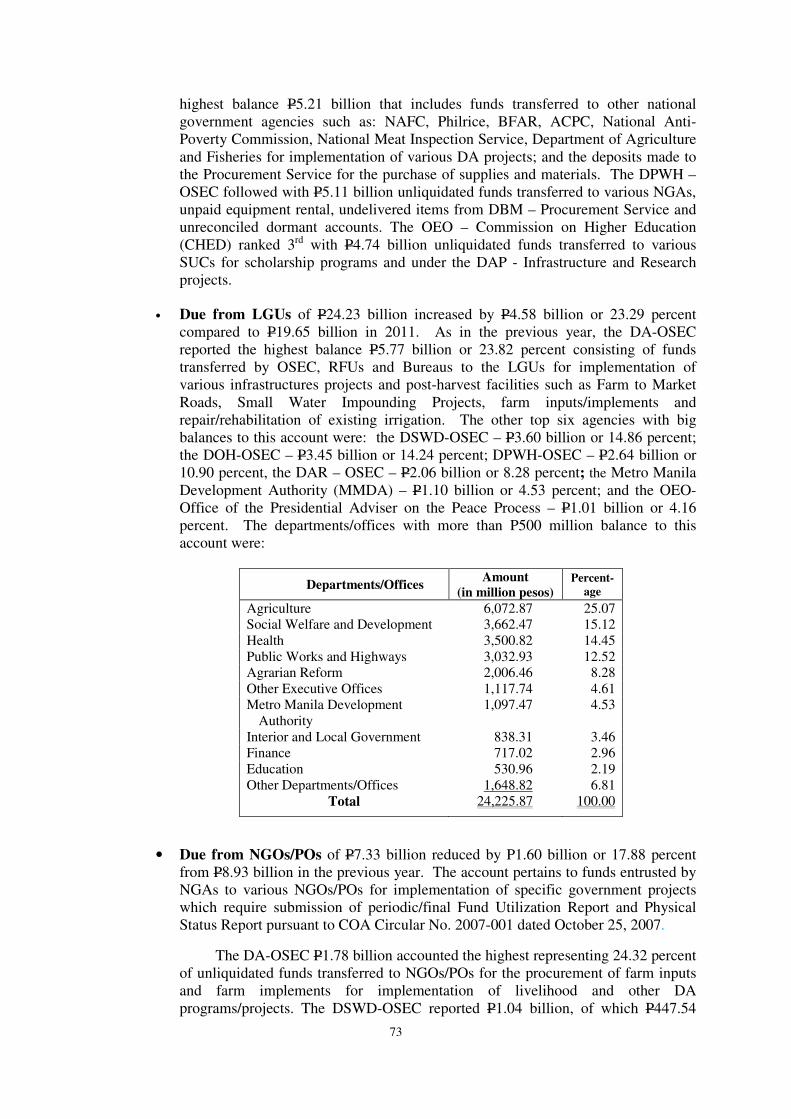

Embed Size (px)

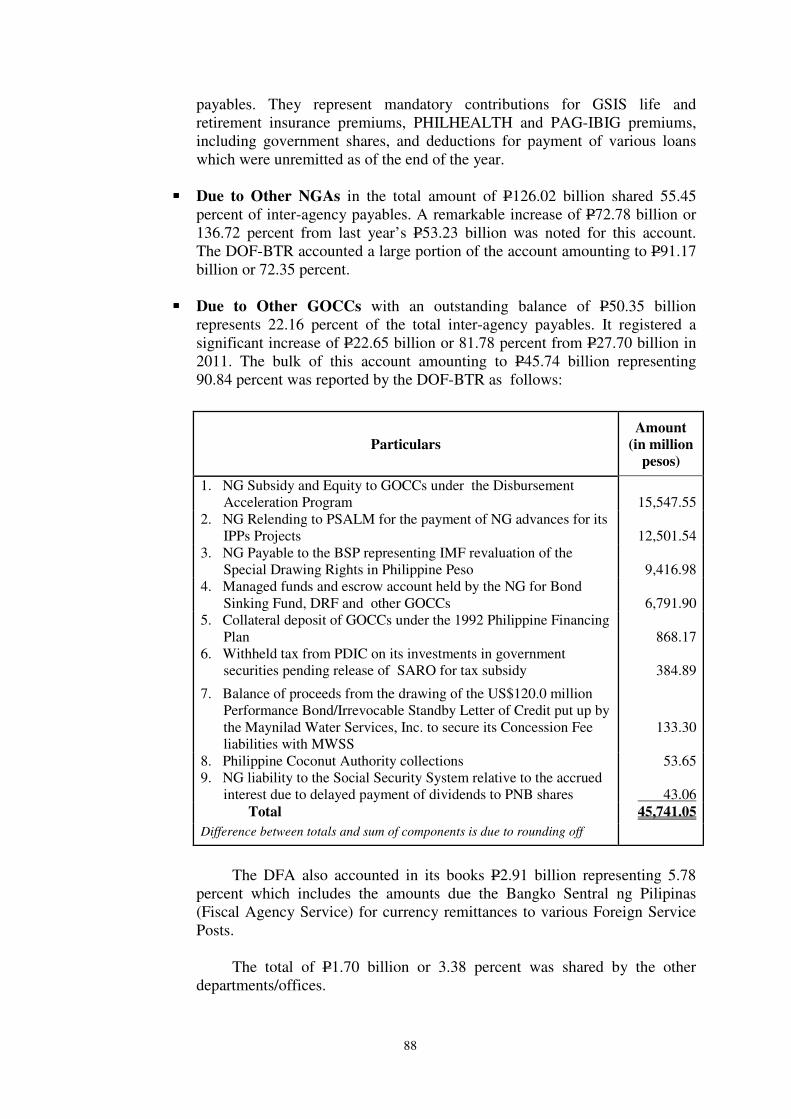

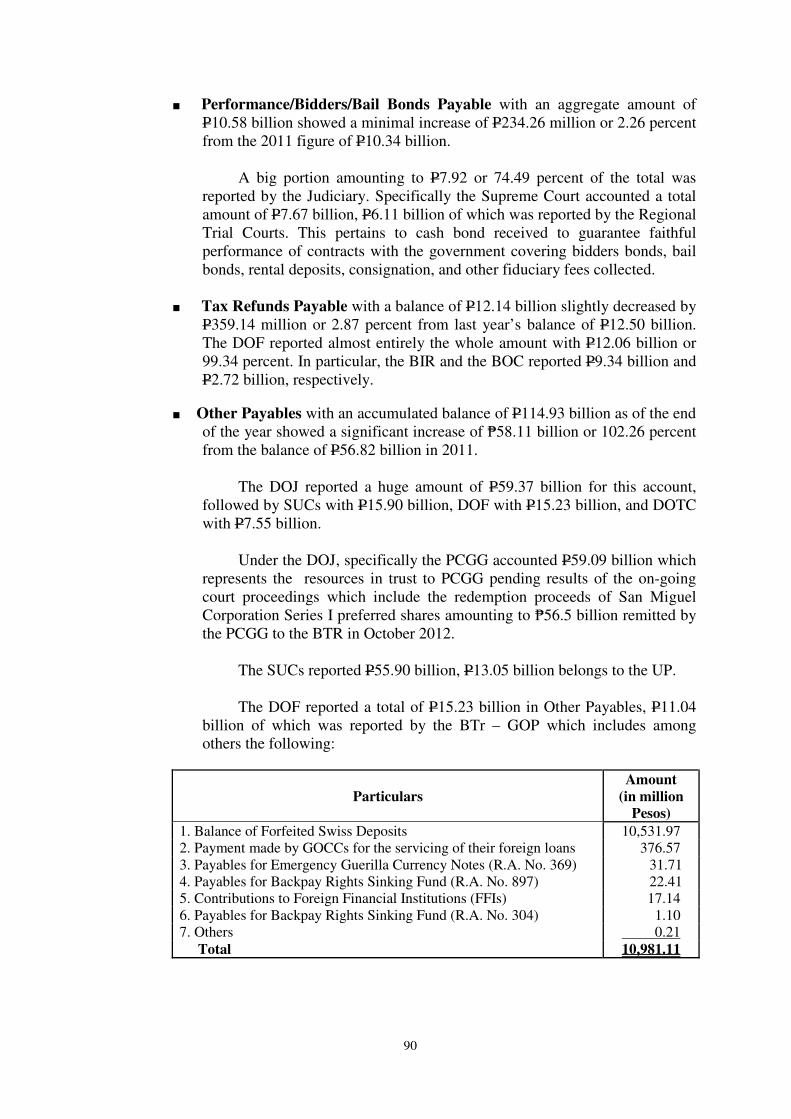

Citation preview

Republic of the Philippines

COMMISSION ON AUDIT Commonwealth Avenue, Quezon City

2012 Annual Financial Report

National Government Agencies

Volume I - A

FY 2012

Annual Financial Report

National Government

Volume I-A

Page

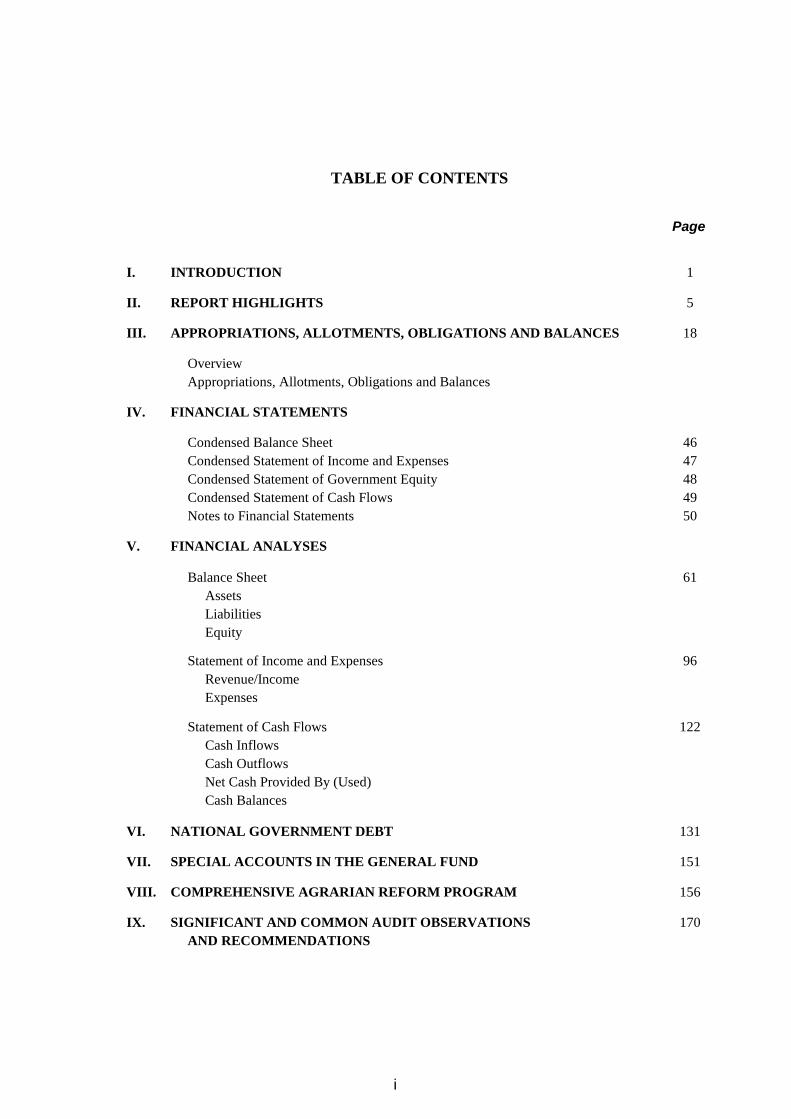

I. INTRODUCTION 1

II. REPORT HIGHLIGHTS 5

III. APPROPRIATIONS, ALLOTMENTS, OBLIGATIONS AND BALANCES 18

Overview

Appropriations, Allotments, Obligations and Balances

IV. FINANCIAL STATEMENTS

Condensed Balance Sheet 46

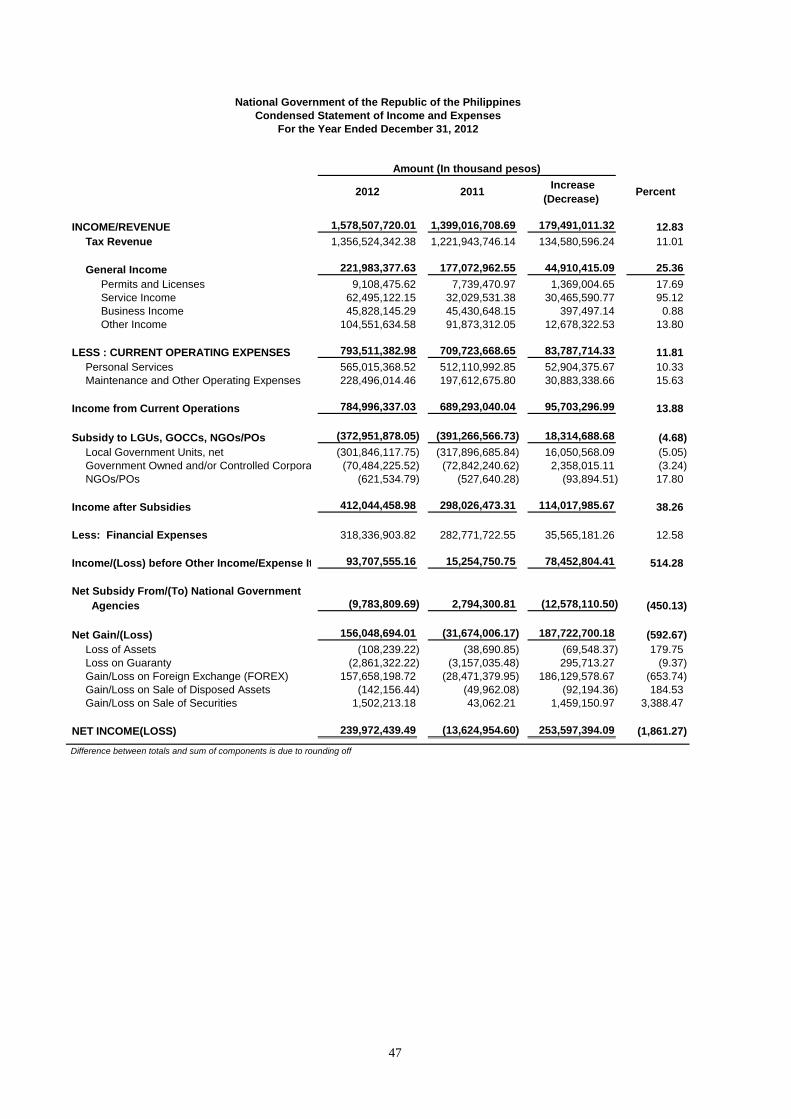

Condensed Statement of Income and Expenses 47

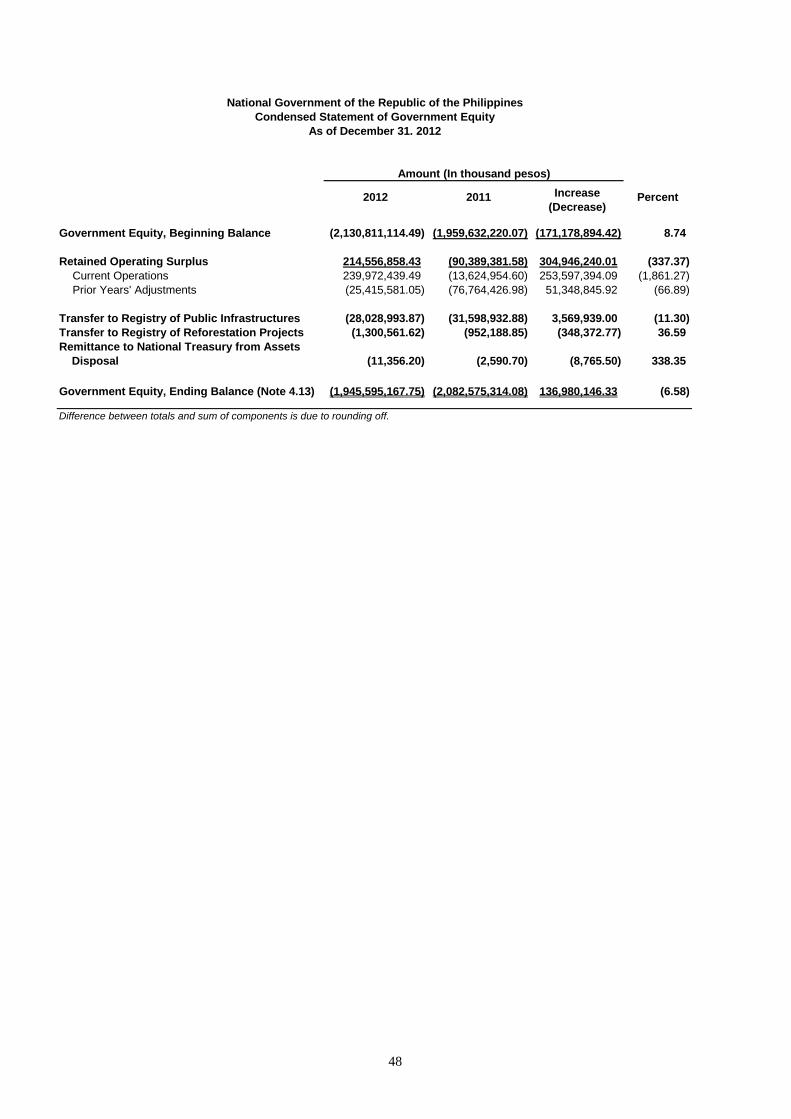

Condensed Statement of Government Equity 48

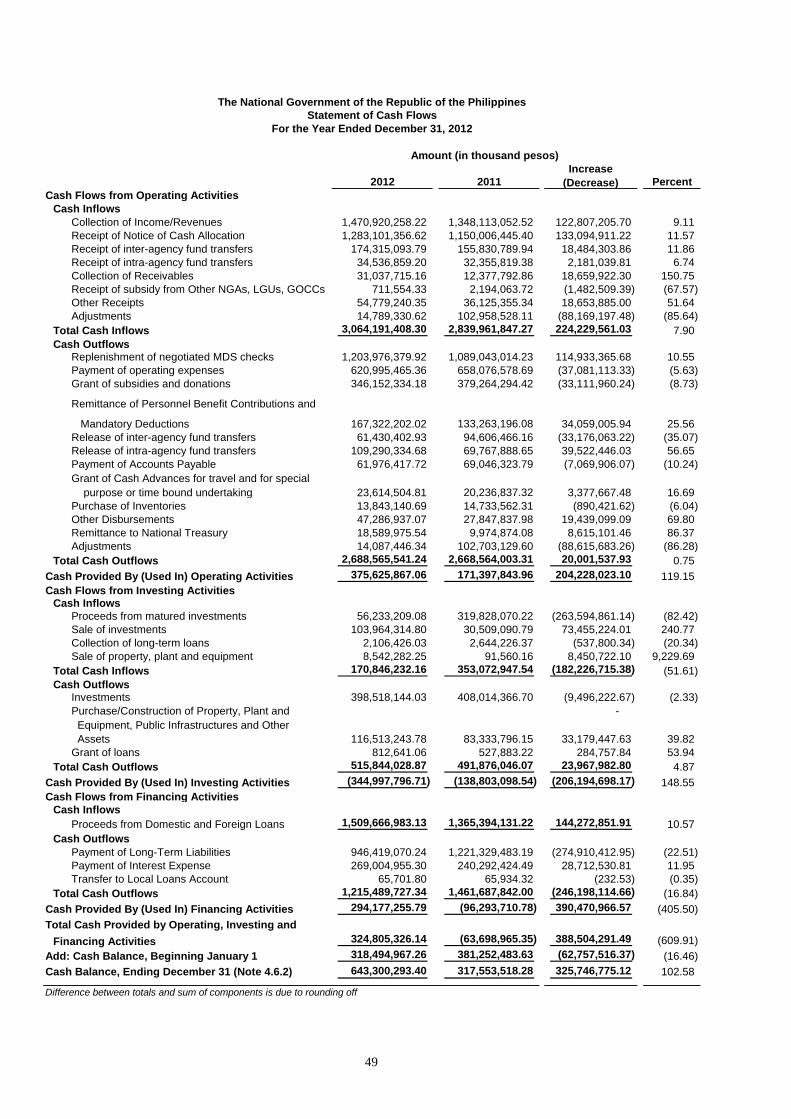

Condensed Statement of Cash Flows 49

Notes to Financial Statements 50

V. FINANCIAL ANALYSES

Balance Sheet 61

Assets

Liabilities

Equity

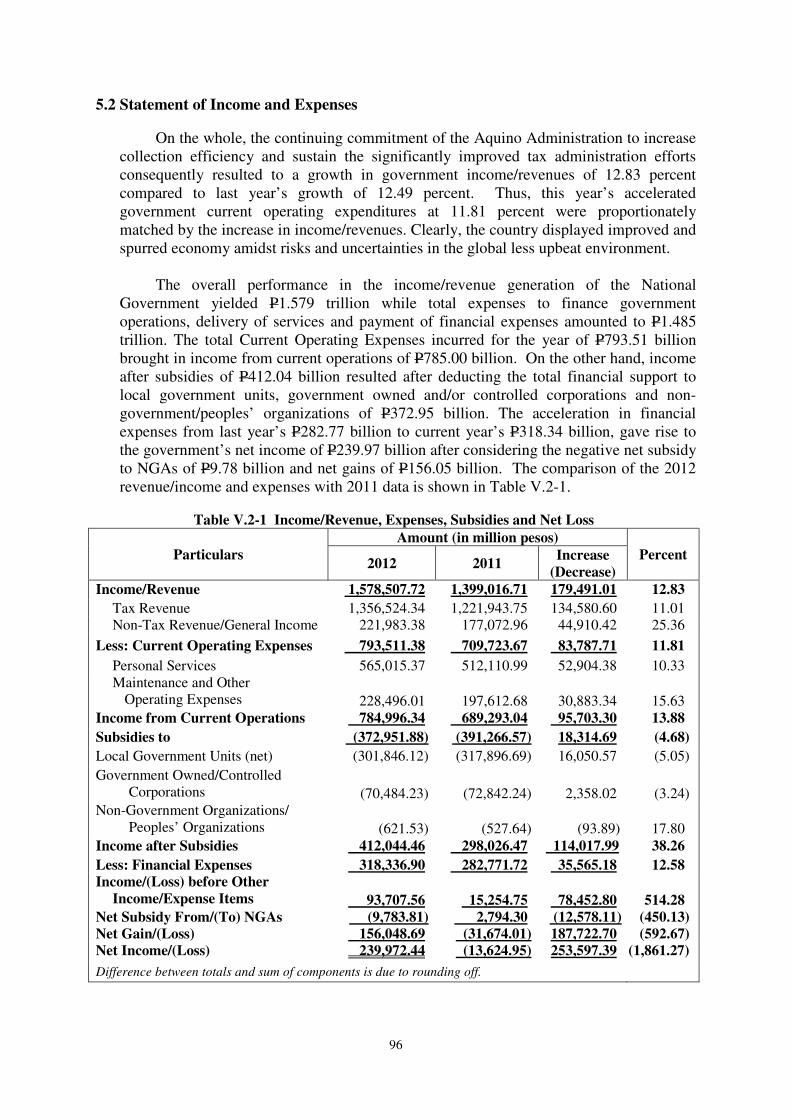

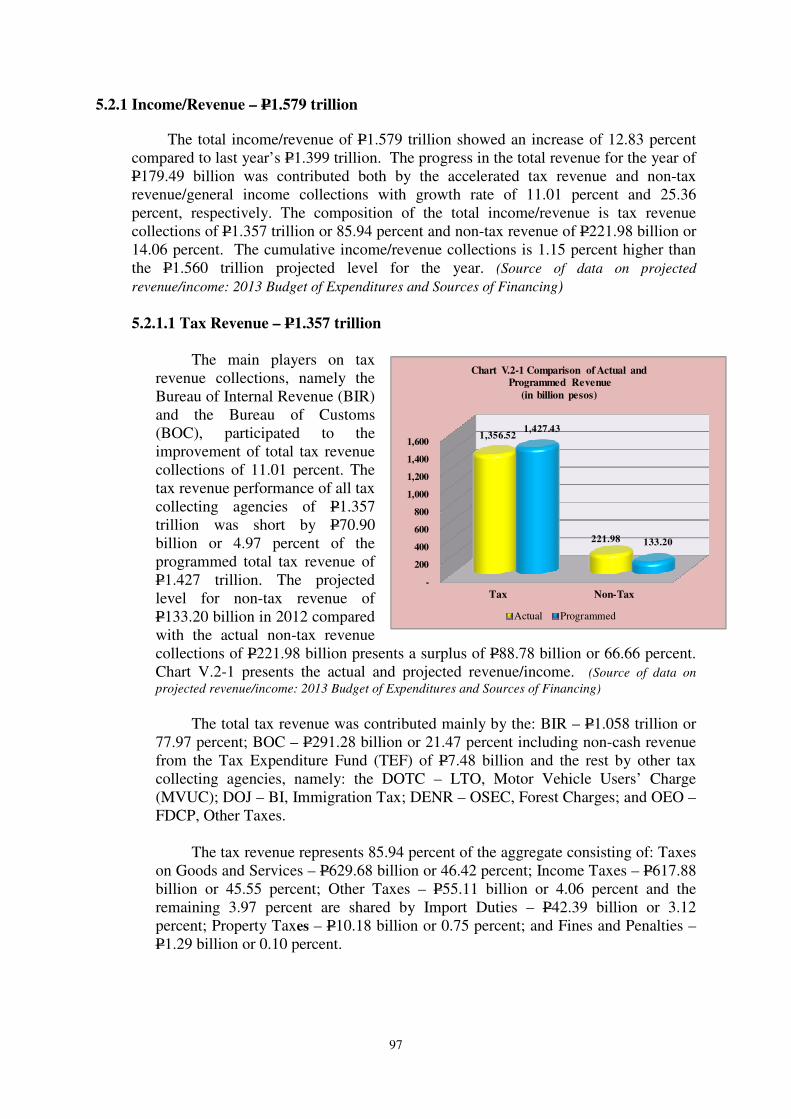

Statement of Income and Expenses 96

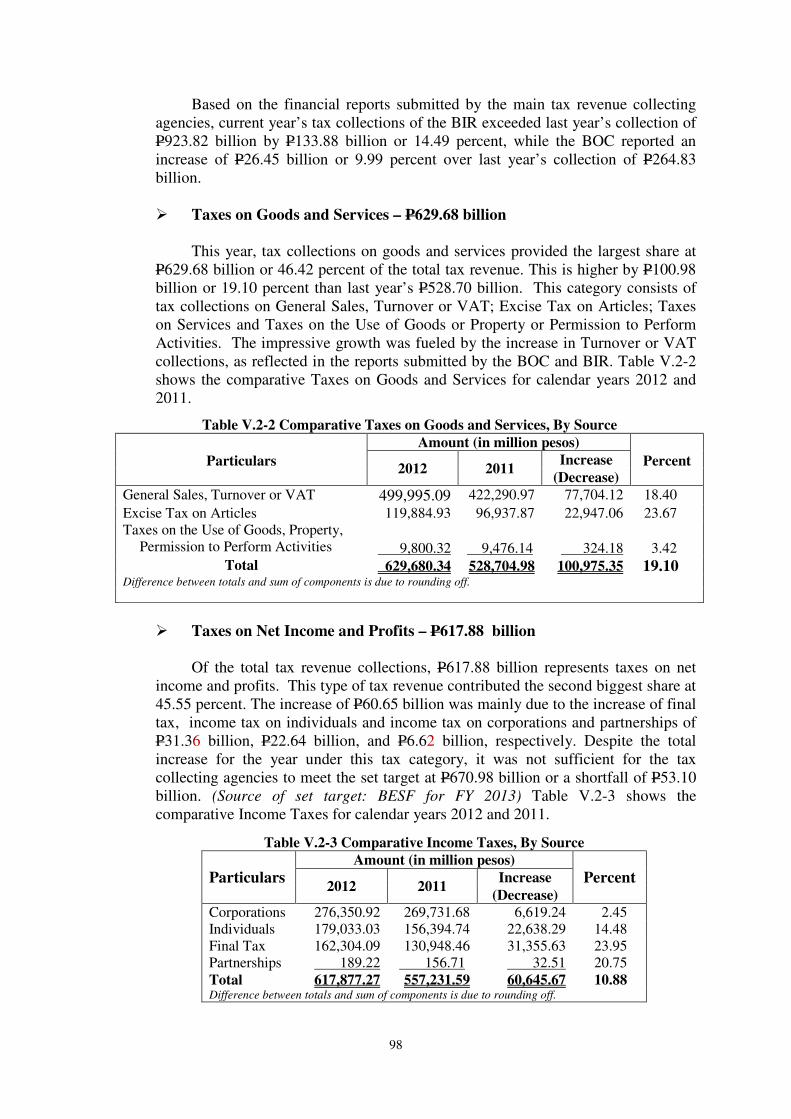

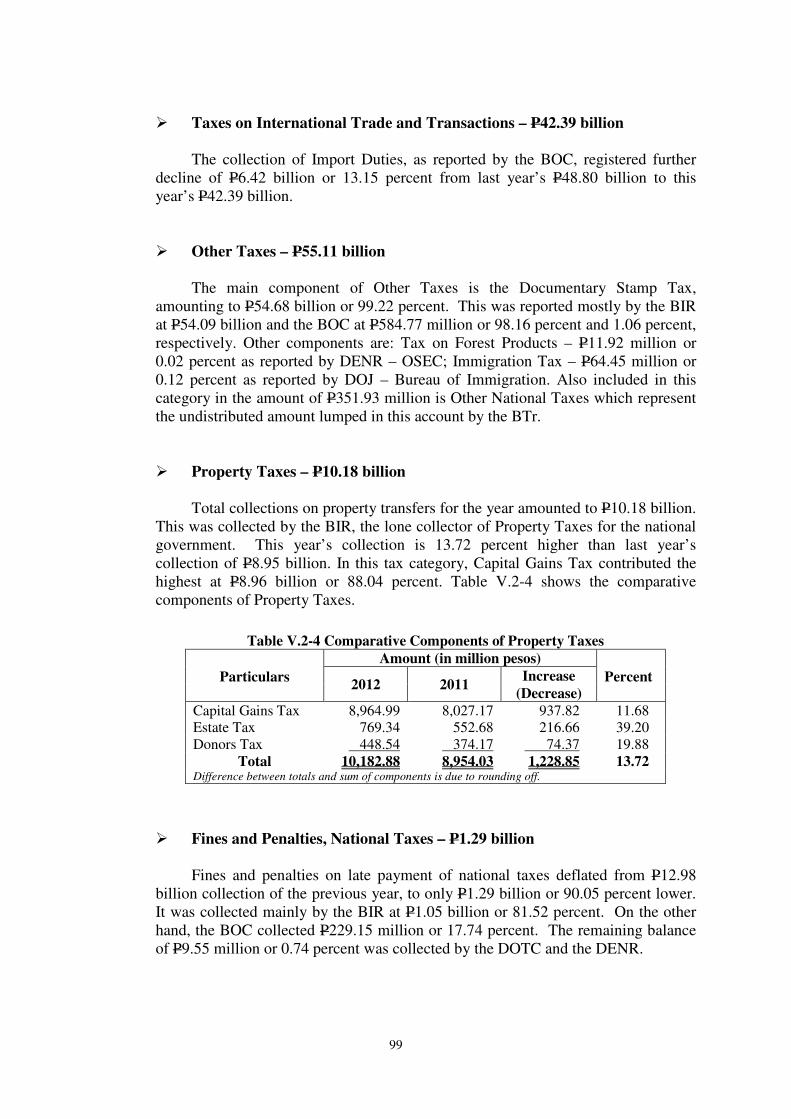

Revenue/Income

Expenses

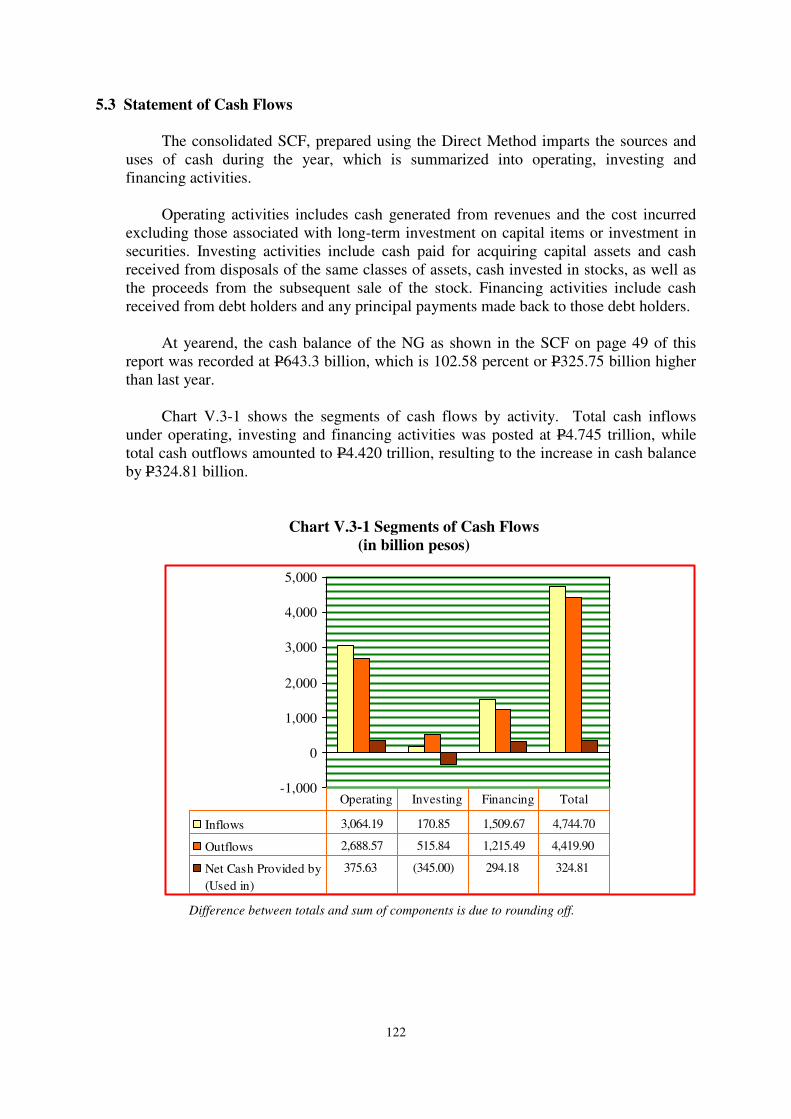

Statement of Cash Flows 122

Cash Inflows

Cash Outflows

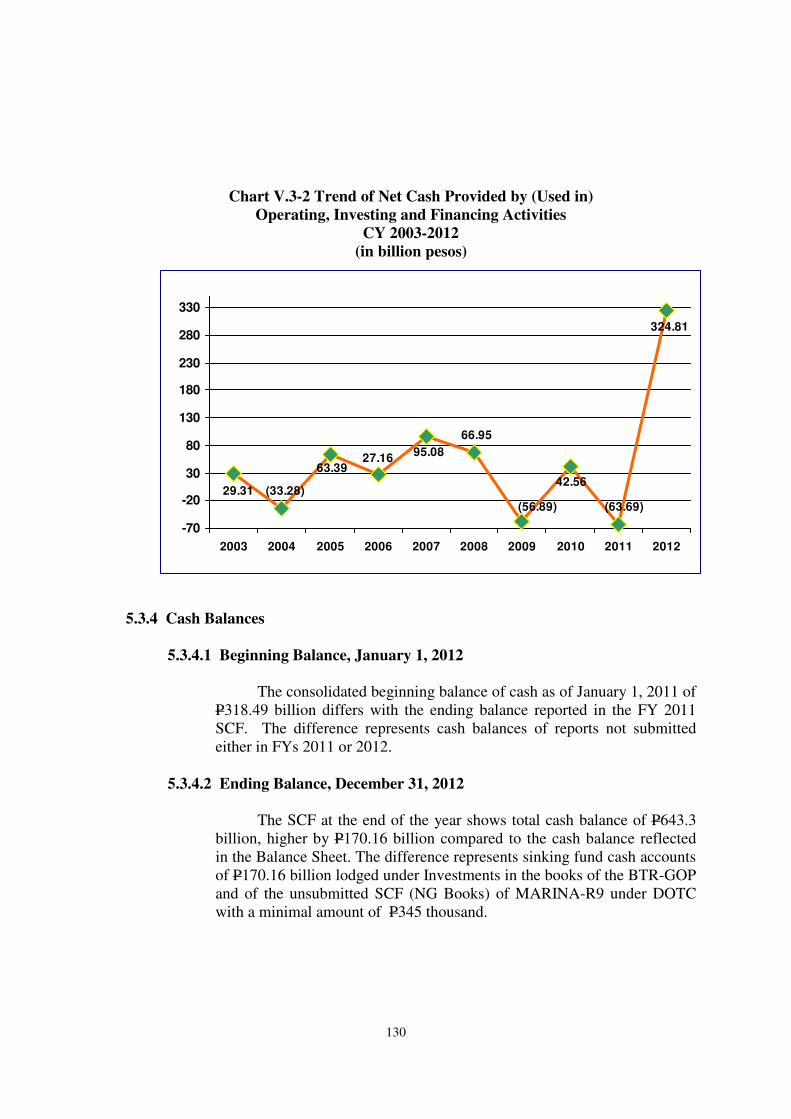

Net Cash Provided By (Used)

Cash Balances

VI. NATIONAL GOVERNMENT DEBT 131

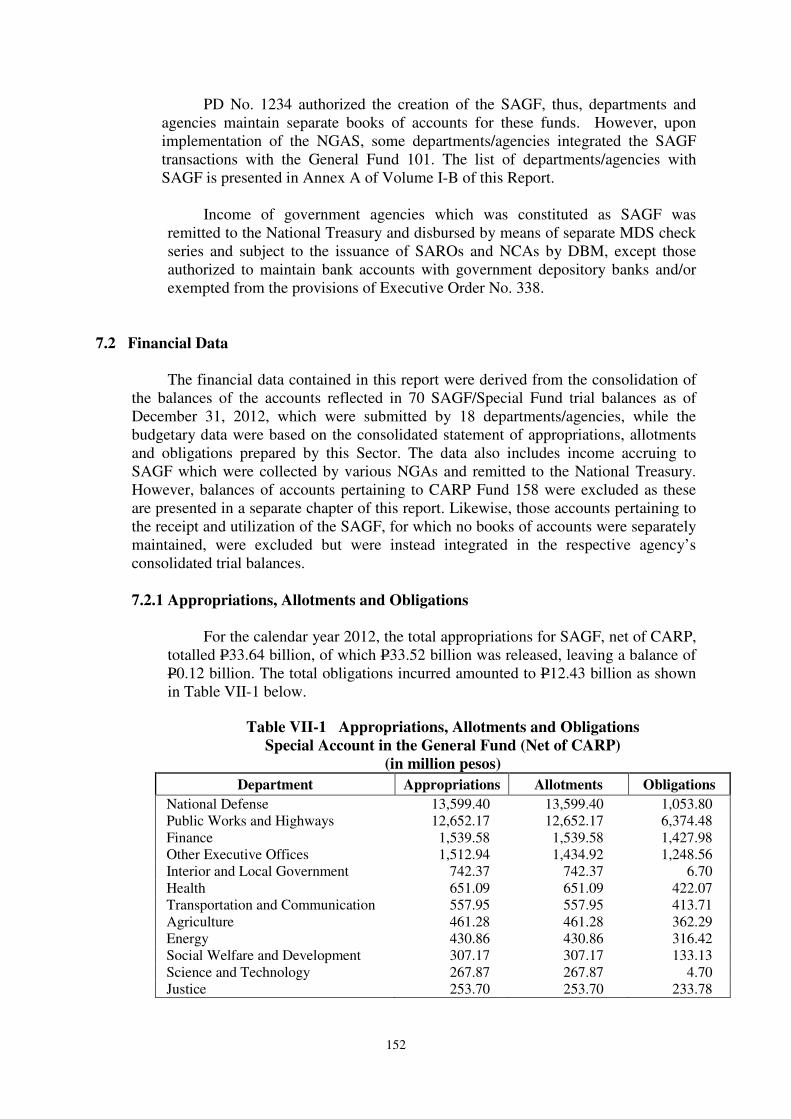

VII. SPECIAL ACCOUNTS IN THE GENERAL FUND 151

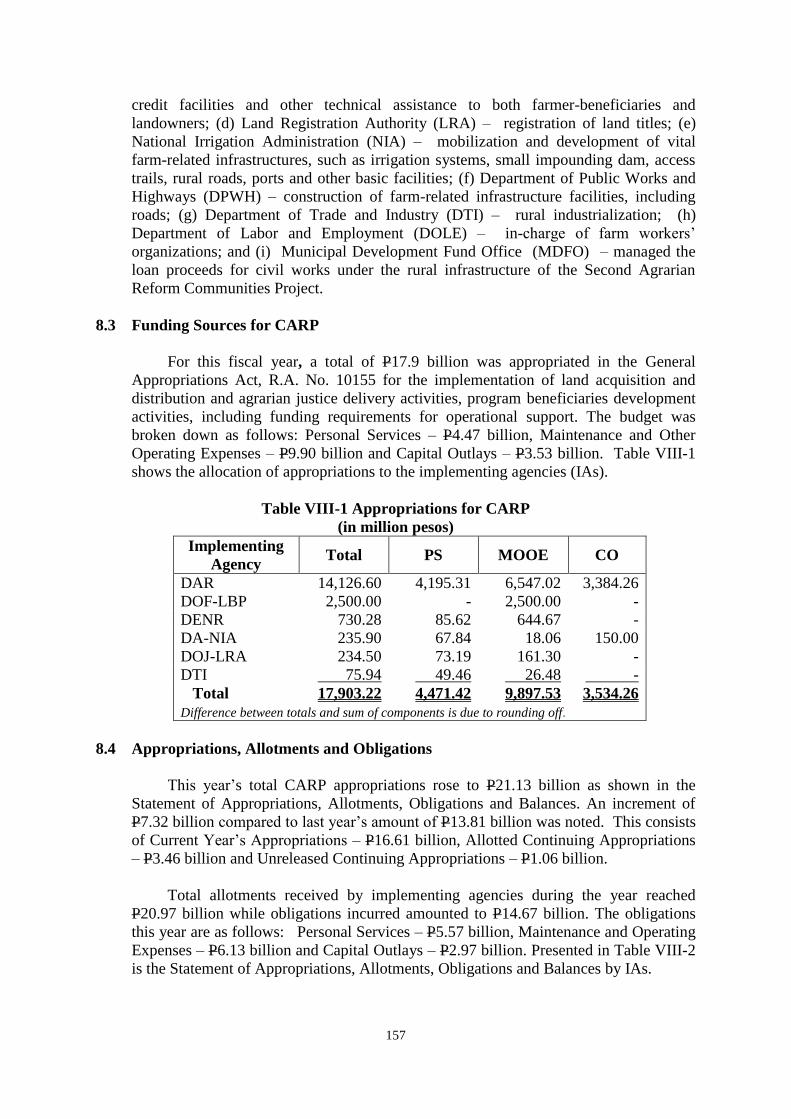

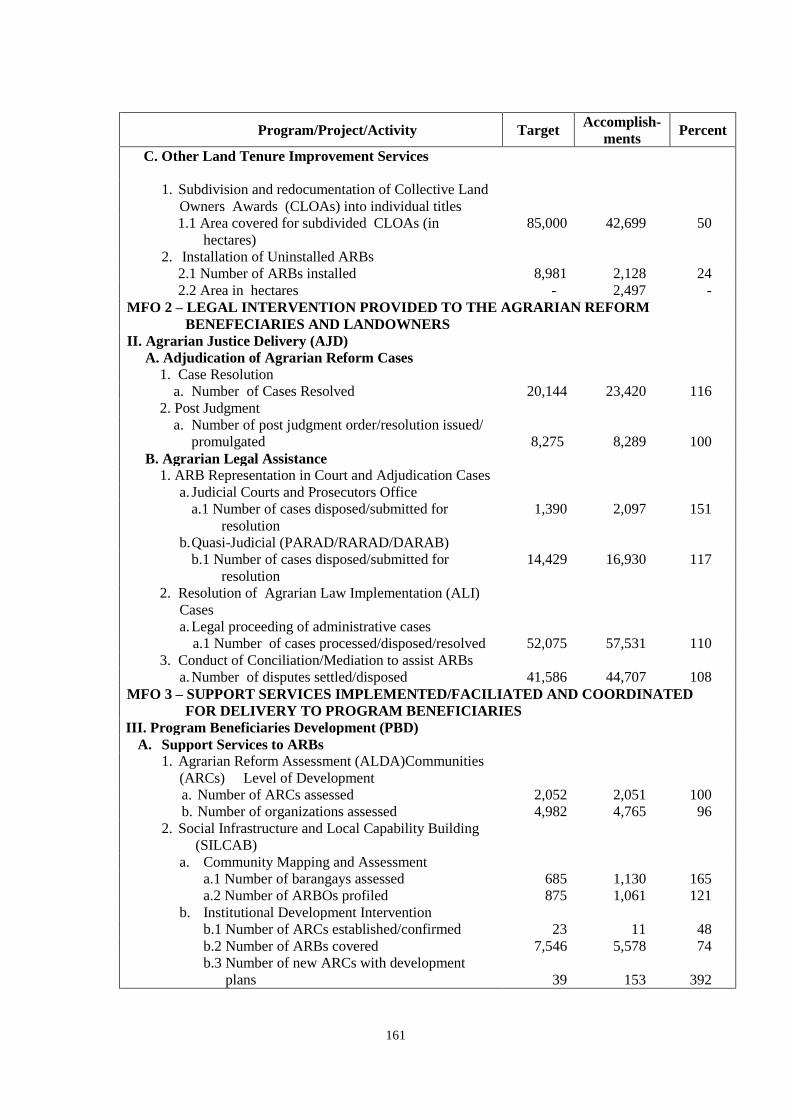

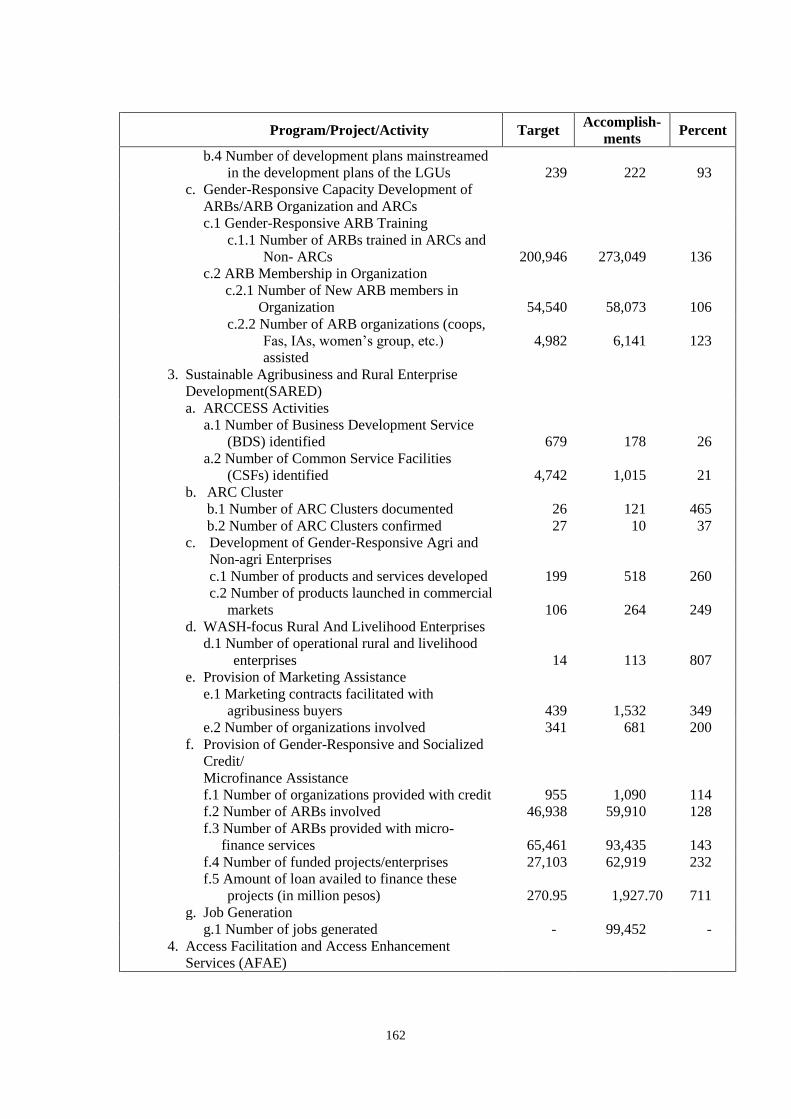

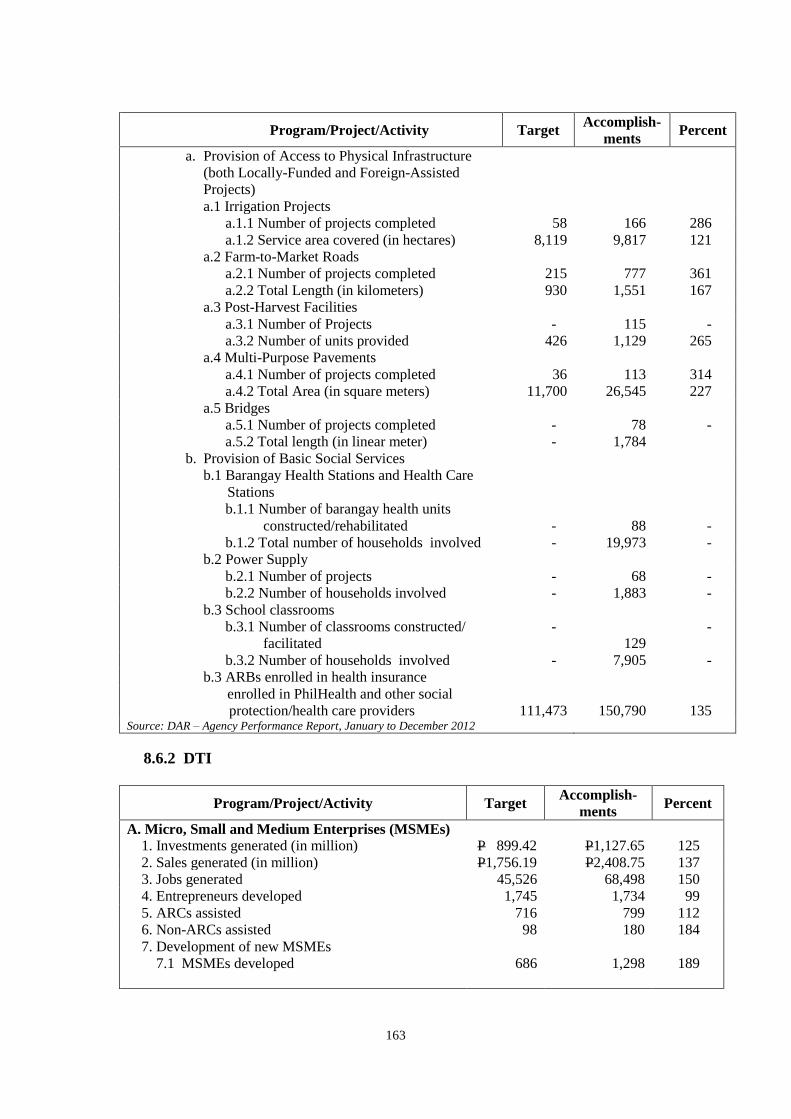

VIII. COMPREHENSIVE AGRARIAN REFORM PROGRAM 156

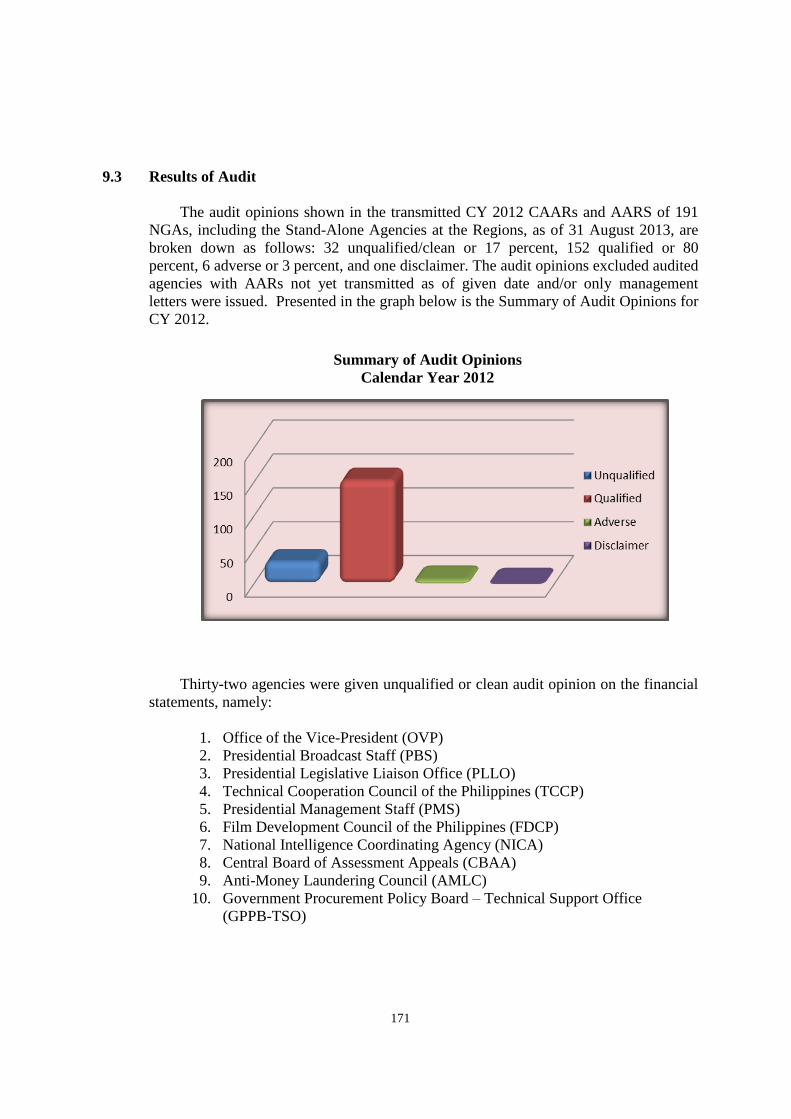

IX. SIGNIFICANT AND COMMON AUDIT OBSERVATIONS 170

AND RECOMMENDATIONS

TABLE OF CONTENTS

i

ii

List of Tables and Charts

Table No. Particulars Page

Report Highlights

II-1 Allotment by Source of Appropriations and Allotment Class 7

II-2 Obligations by Source of Appropriations and Expenditure Class 8

II-3 Unalloted/Unreleased Appropriations, by Source 9

II-4 Unobligated Allotments, by Source 10

II-5 Comparative Composition of Liabilities 13

Appropriations, Allotments, Obligations and Balances

III-1 Appropriations, Allotments, Obligations and Balances 20

III-2 Comparative Details of Appropriations 22

III-3 Comparative Regular Appropriations By Department/Agency 25

III-4 Appropriations for Special Purpose Funds 26

III-5 Appropriations for Unprogrammed Fund 27

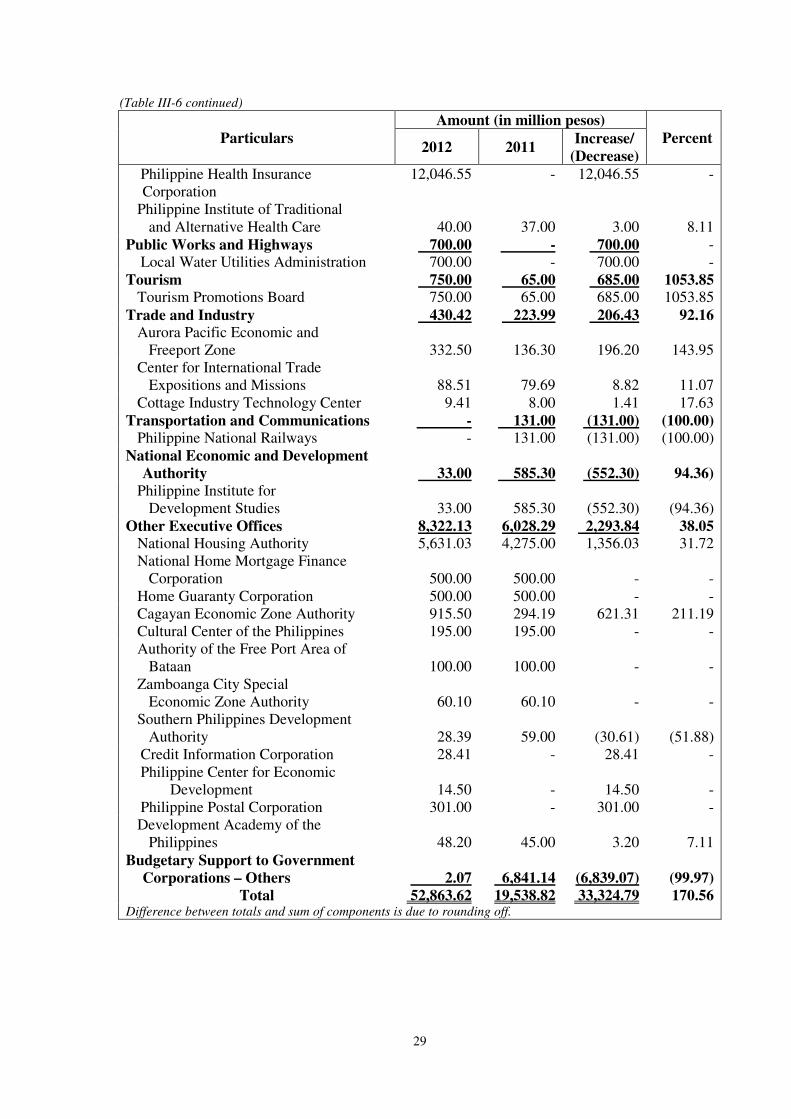

III-6 Budgetary Support to Government Corporations 28

III-7 Comparative Details of Allocations to LGUs 31

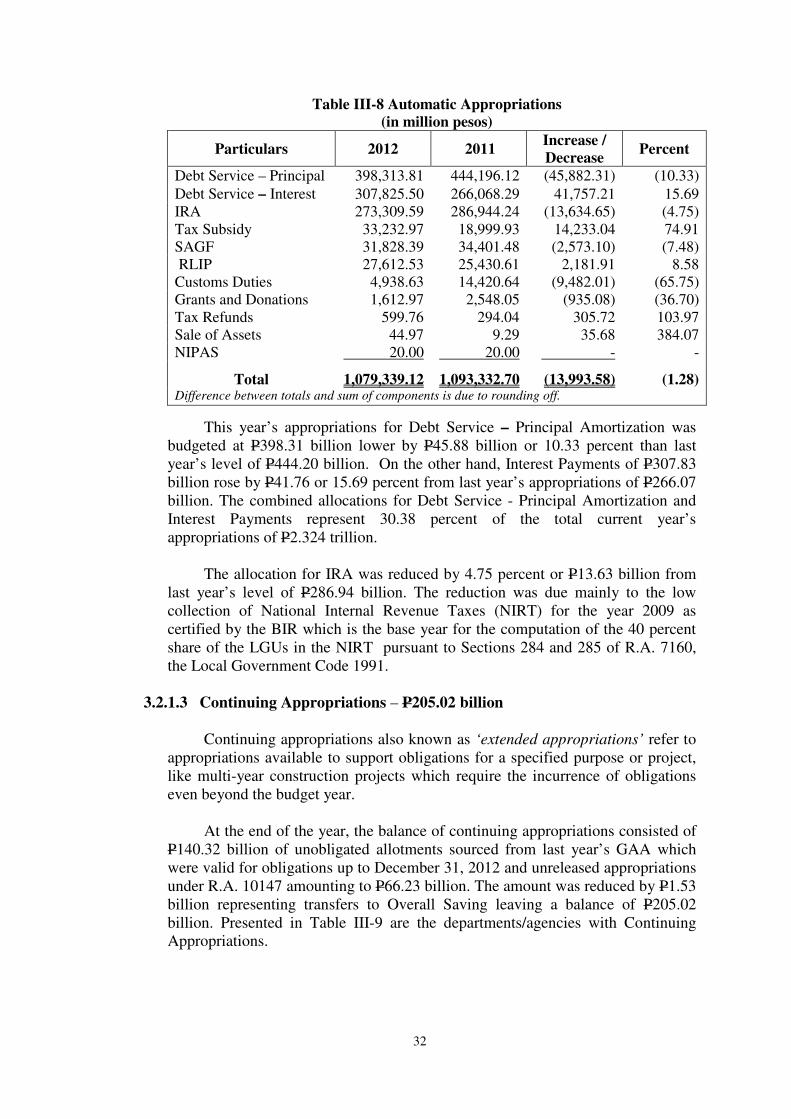

III-8 Automatic Appropriations 32

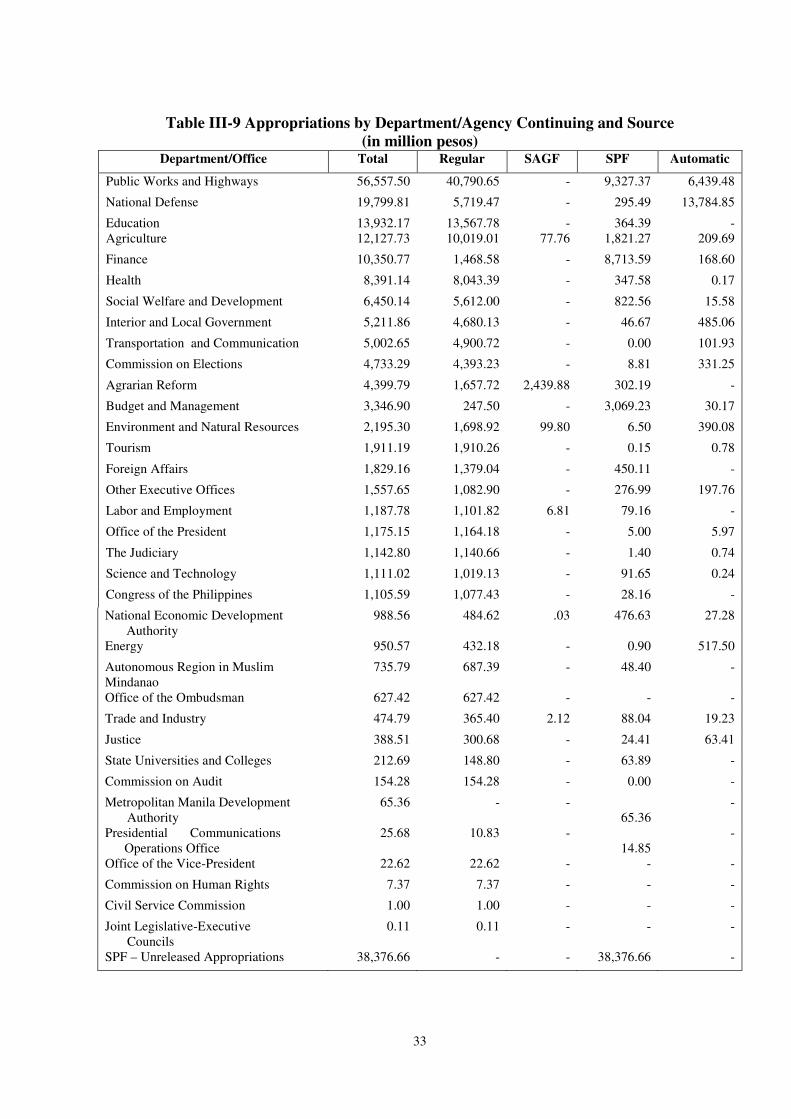

III-9 Appropriations by Department/Agency Continuing and Source 33

III-10 Sources and Nature of Allotments 34

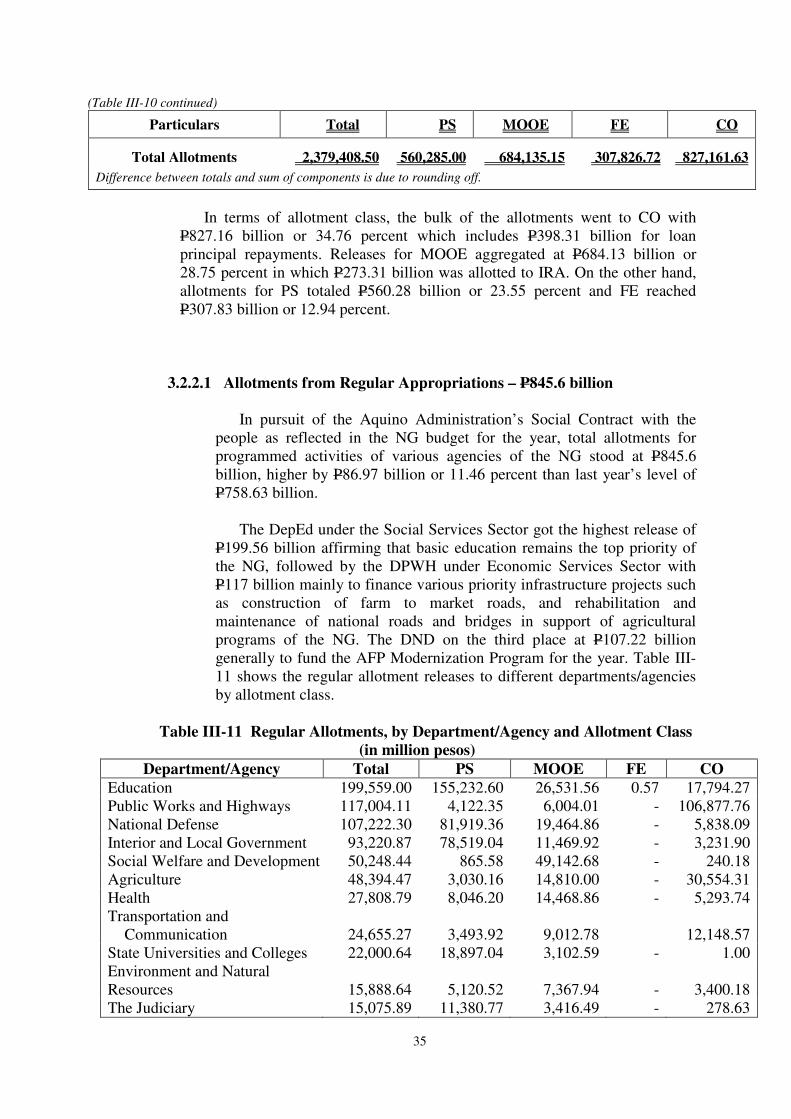

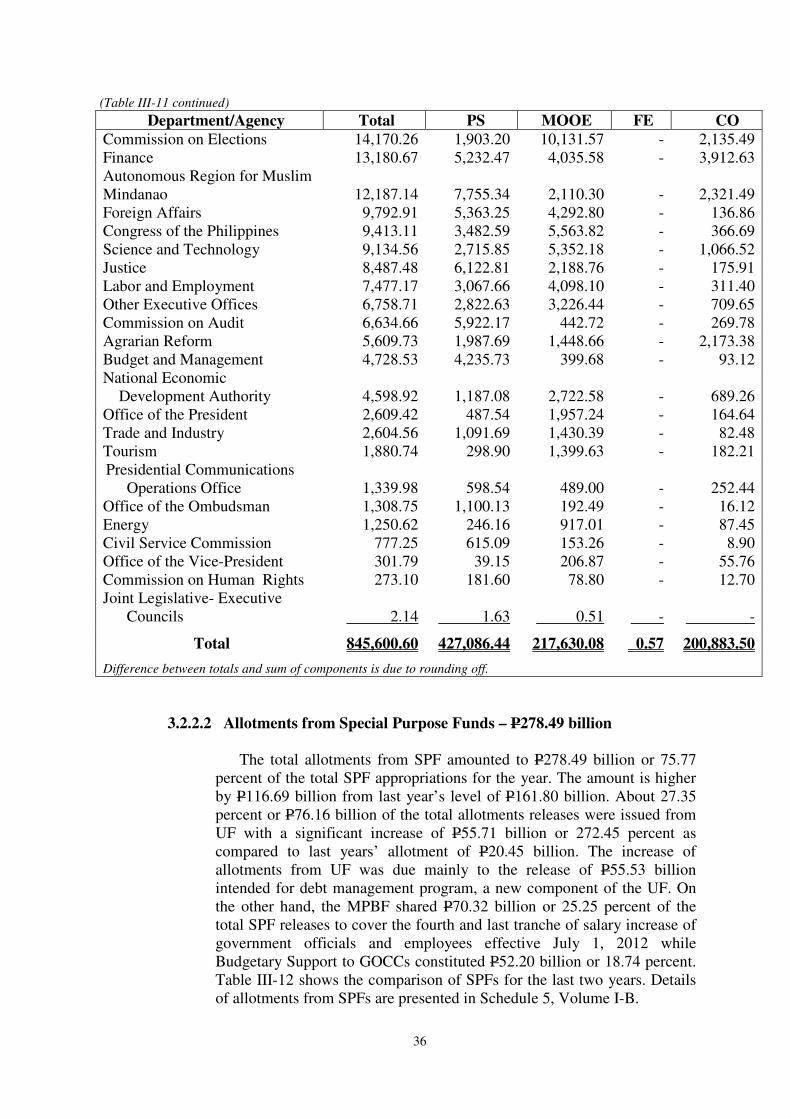

III-11 Regular Allotments, by Department/Agency and Allotment Class 35

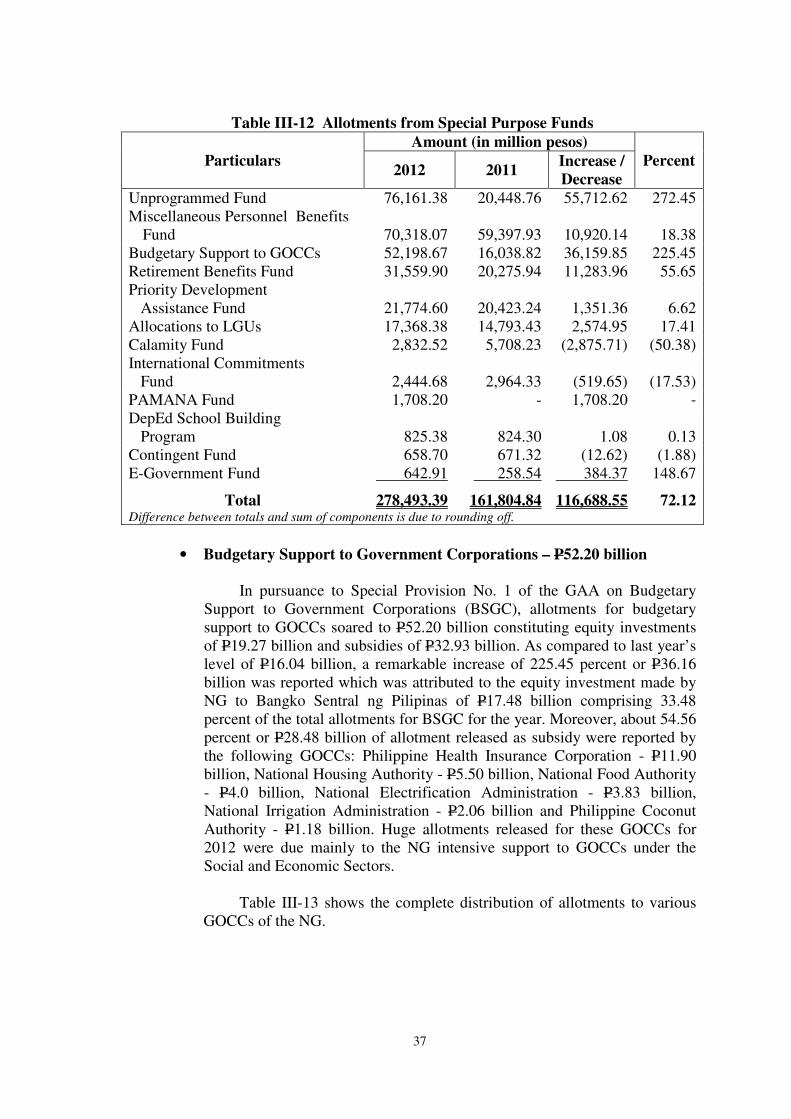

III-12 Allotment from Special Purpose Funds 37

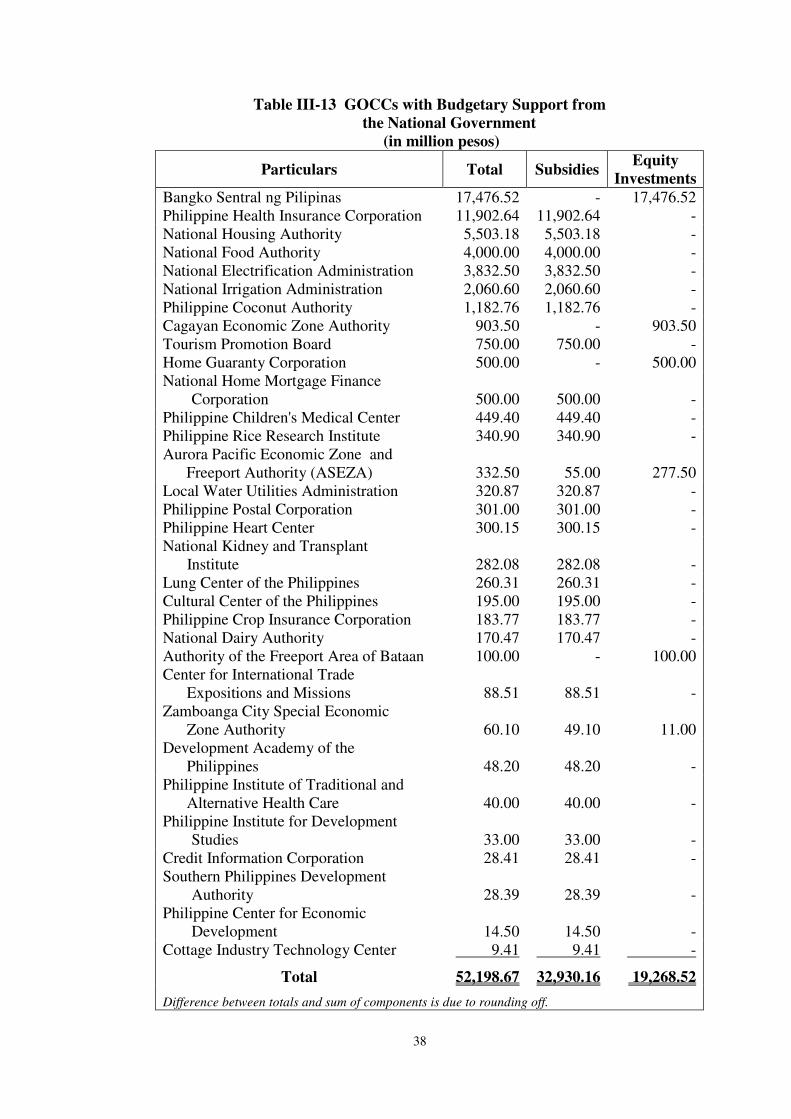

III-13 GOCCs with Budgetary Support from the National Government 38

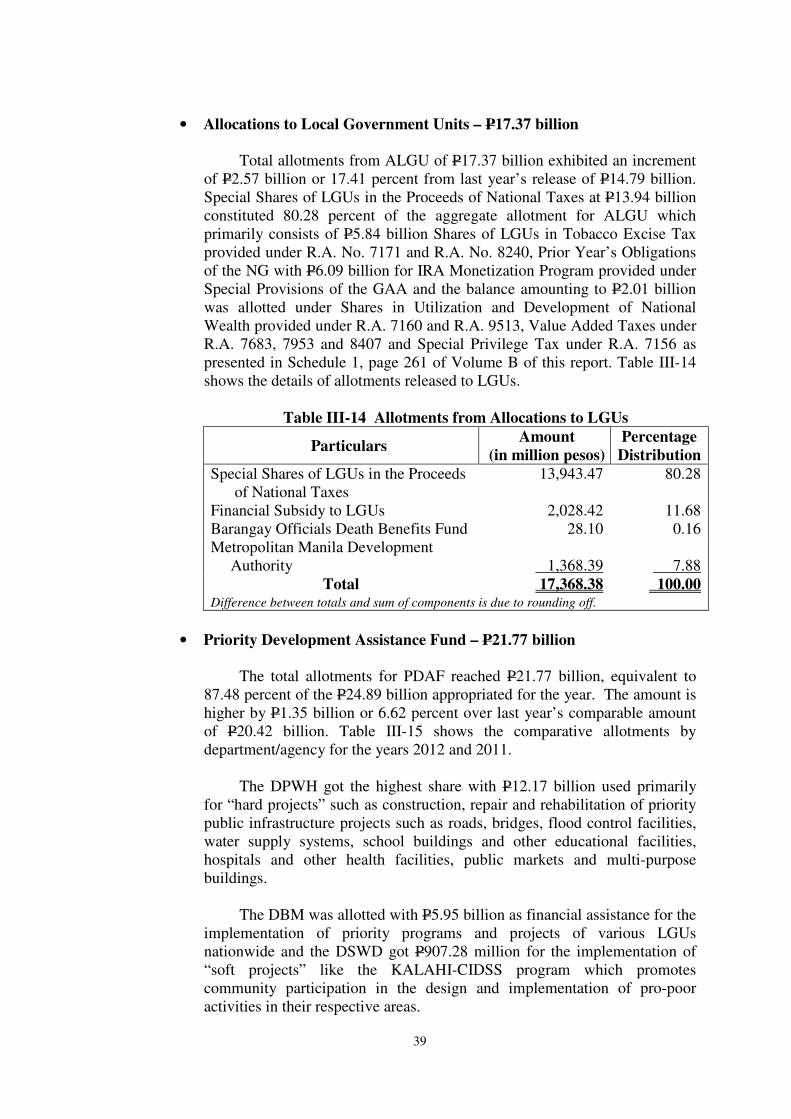

III-14 Allotments from Allocations to LGUs 39

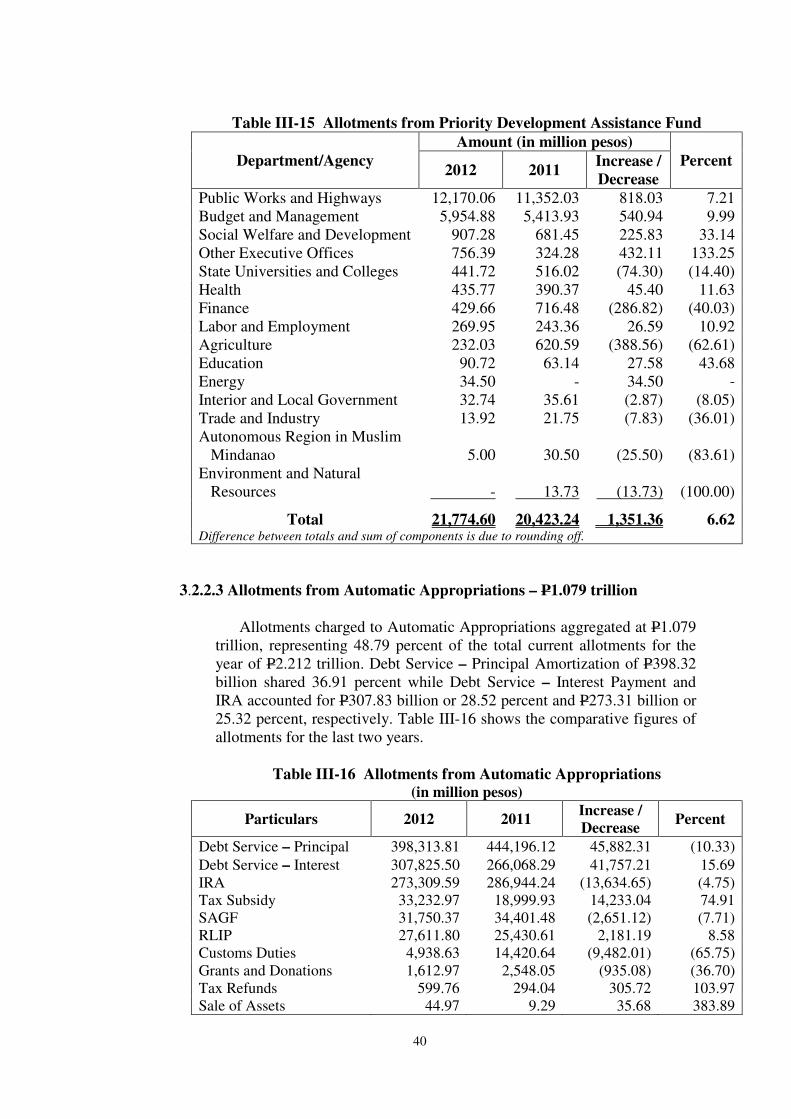

III-15 Allotment from Priority Development Assistance Fund 40

III-16 Allotments from Automatic Appropriations 40

III-17 Summary of Unreleased Appropriations 42

III-18 Summary of Allotments, Obligations and Balances 42

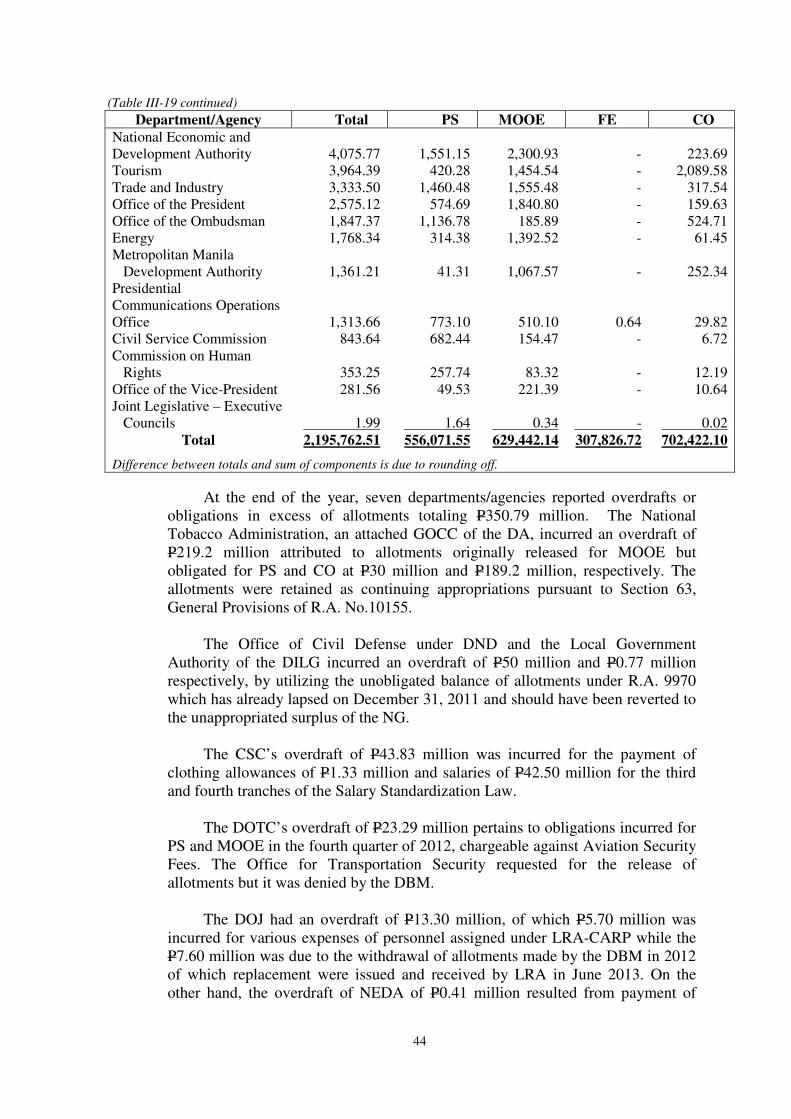

III-19 Obligations Covered by Allotments, by Department/Agency and Allotment

Class 43

III-20 Obligations Not Covered by Allotments, by Department/Agency and

Allotment Class 45

Financial Analyses

V.1-1 Assets, Liabilities and Equity 61

V.1-2 Annual Growth in Assets CYs 2008-2012 61

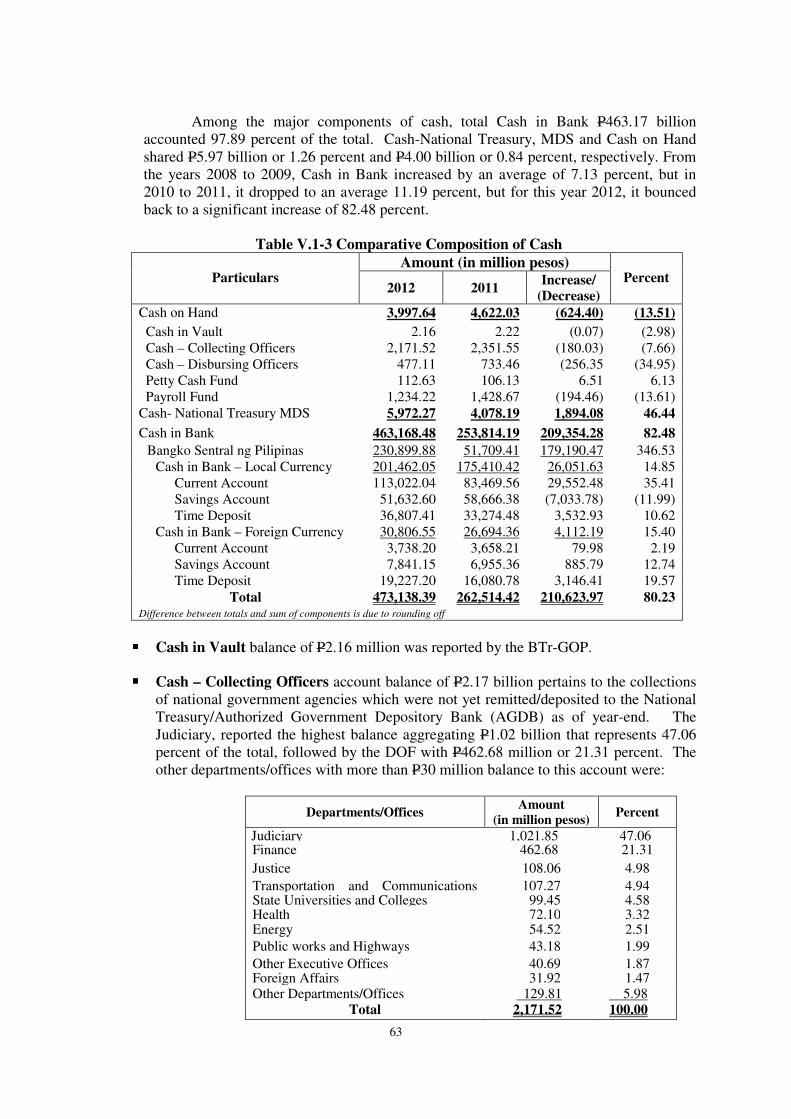

V.1-3 Comparative Composition of Cash 63

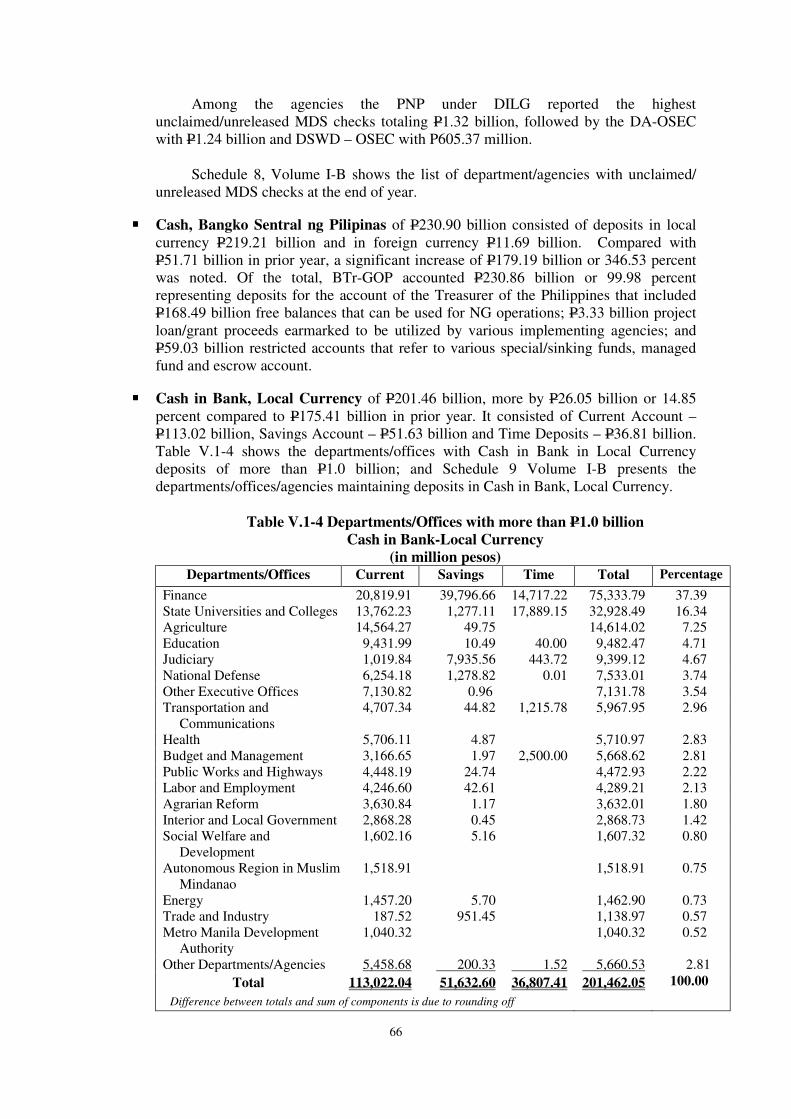

V.1-4 Departments/Offices with more than P1.0 billion Cash in Bank – Local

Currency 66

V.1-5 Departments/Offices with more than P100 million Cash in Bank – Foreign

Currency 68

iii

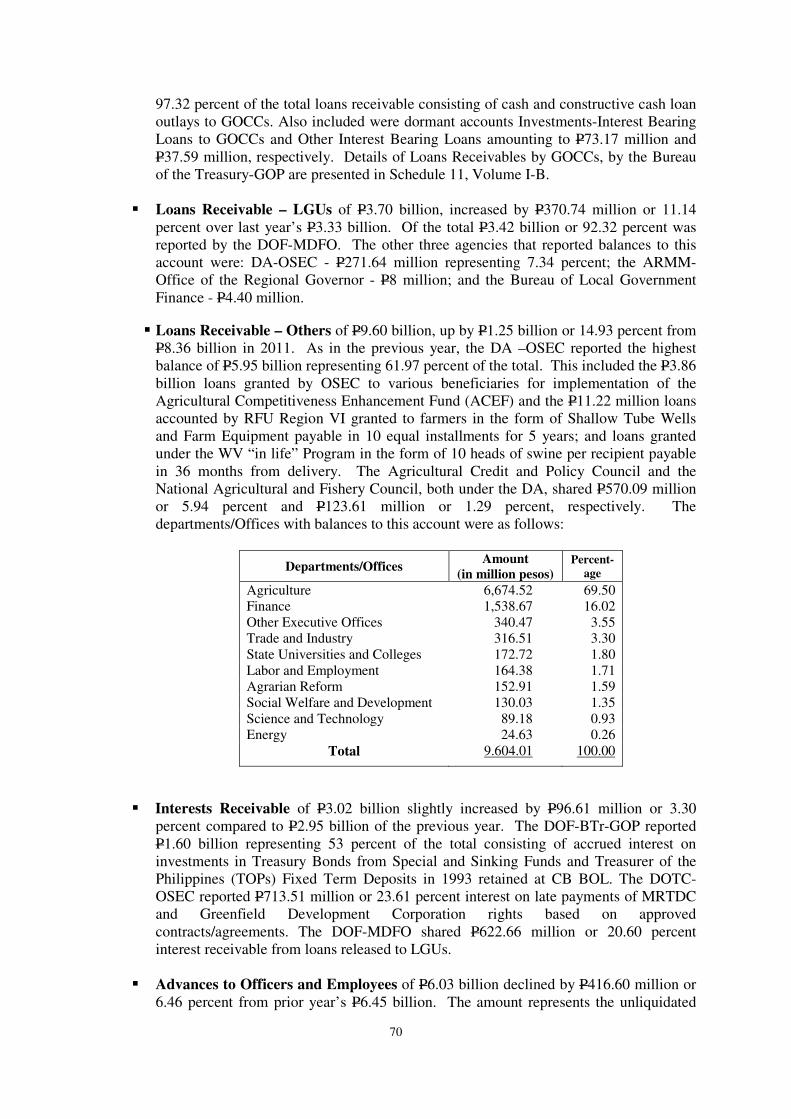

V.1-6 Details of Receivables by Account 69

V.1-7 Top Ten Departments with Huge Balances to Intra-Agency Receivable

Accounts 75

V.1-8 Composition of Investments 77

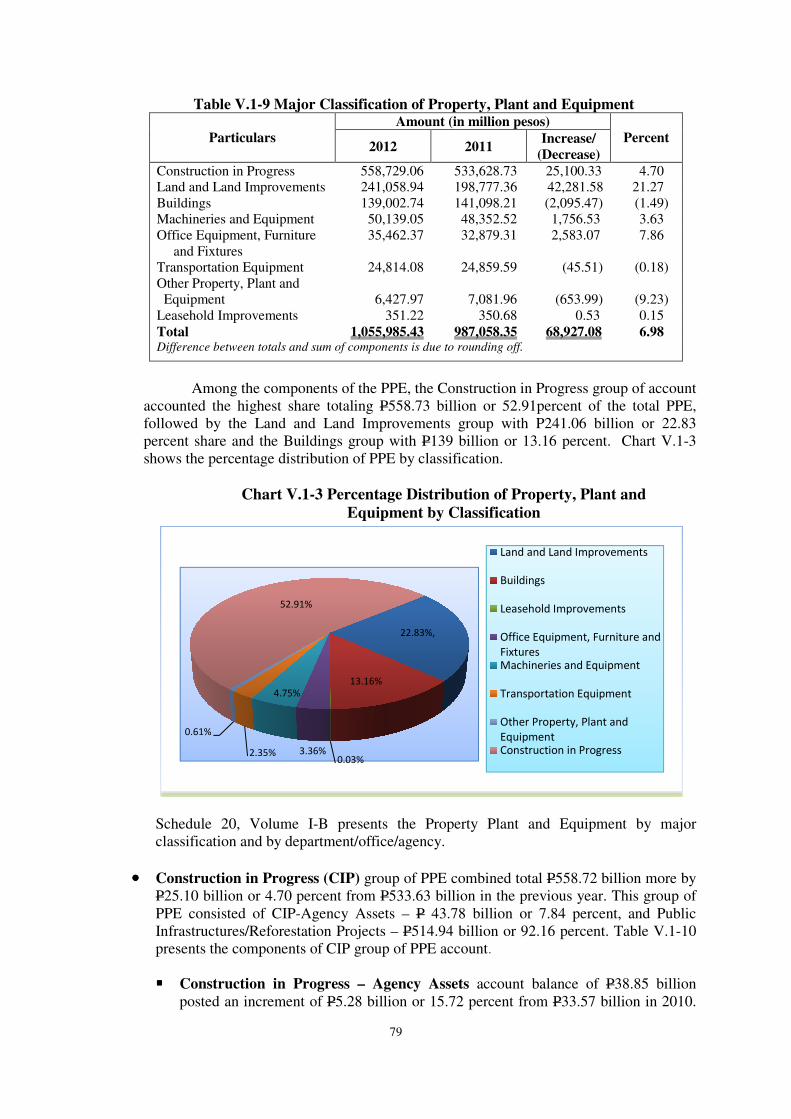

V.1-9 Major Classification of Property, Plant and Equipment 79

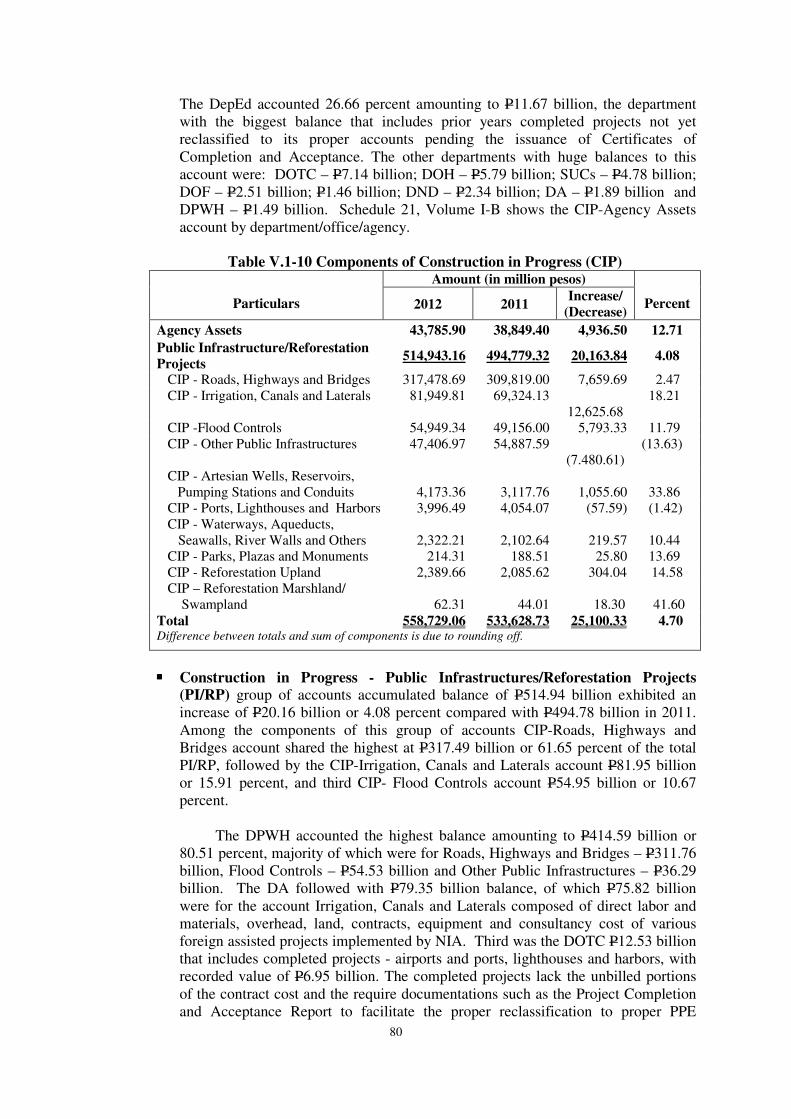

V.1-10 Components of Construction in Progress 80

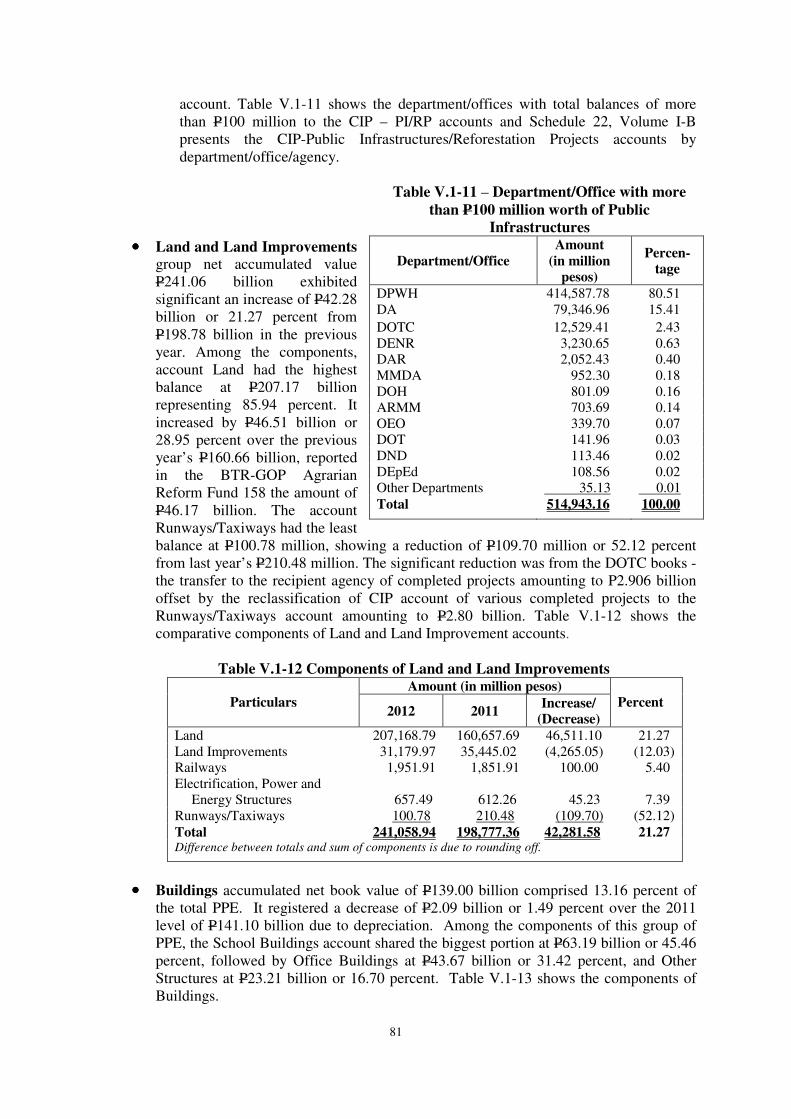

V.1-11 Departments with more than P100 million worth of Public Infrastructures 81

V.1-12 Components of Land and Land Improvements 81

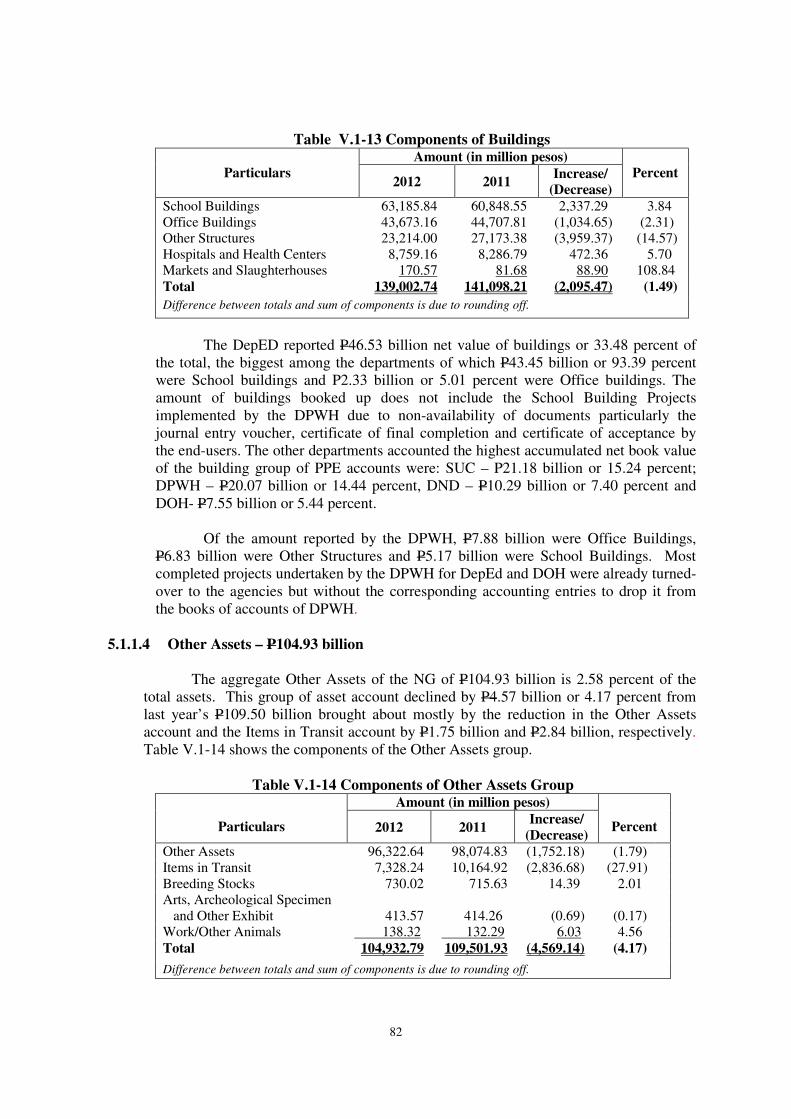

V.1-13 Components of Buildings 82

V.1-14 Components of Other Assets Group 82

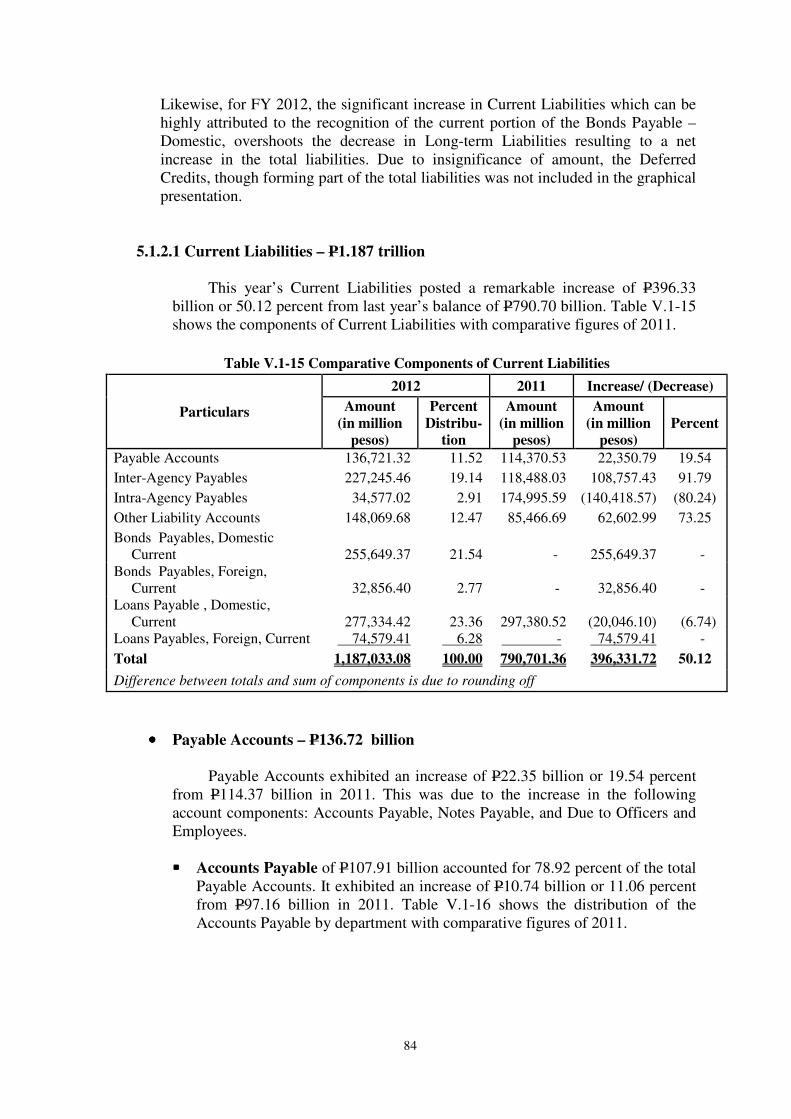

V.1-15 Comparative Components of Current Liabilities 84

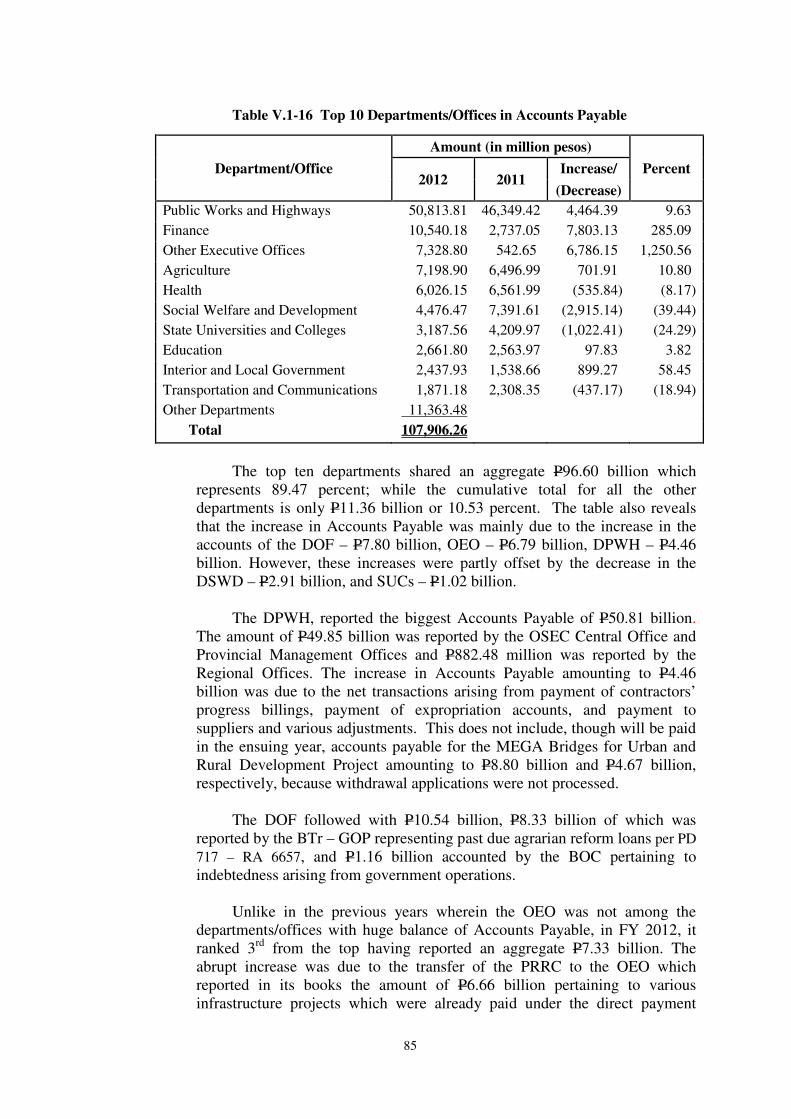

V.1-16 Top 10 Departments/Offices in Accounts Payable 85

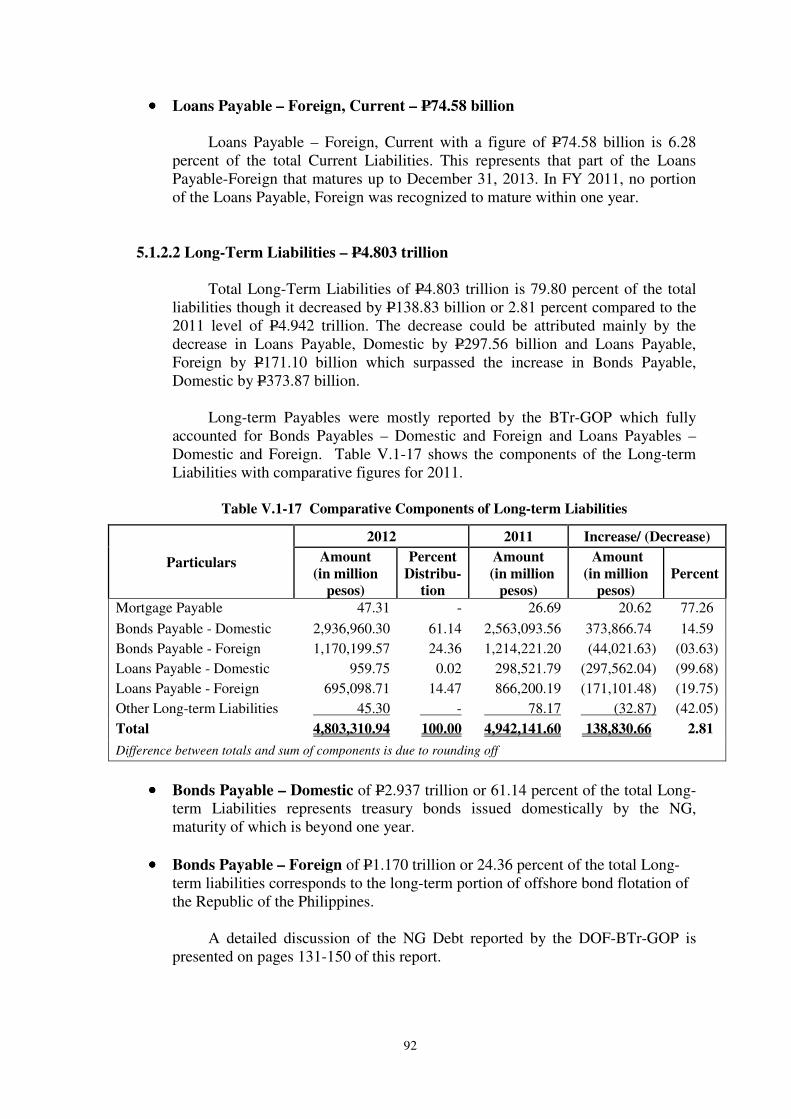

V.1-17 Comparative Components of Long-term Liabilities 92

V.1-18 Departments/Offices/Agencies with Completed Public Infrastructures and

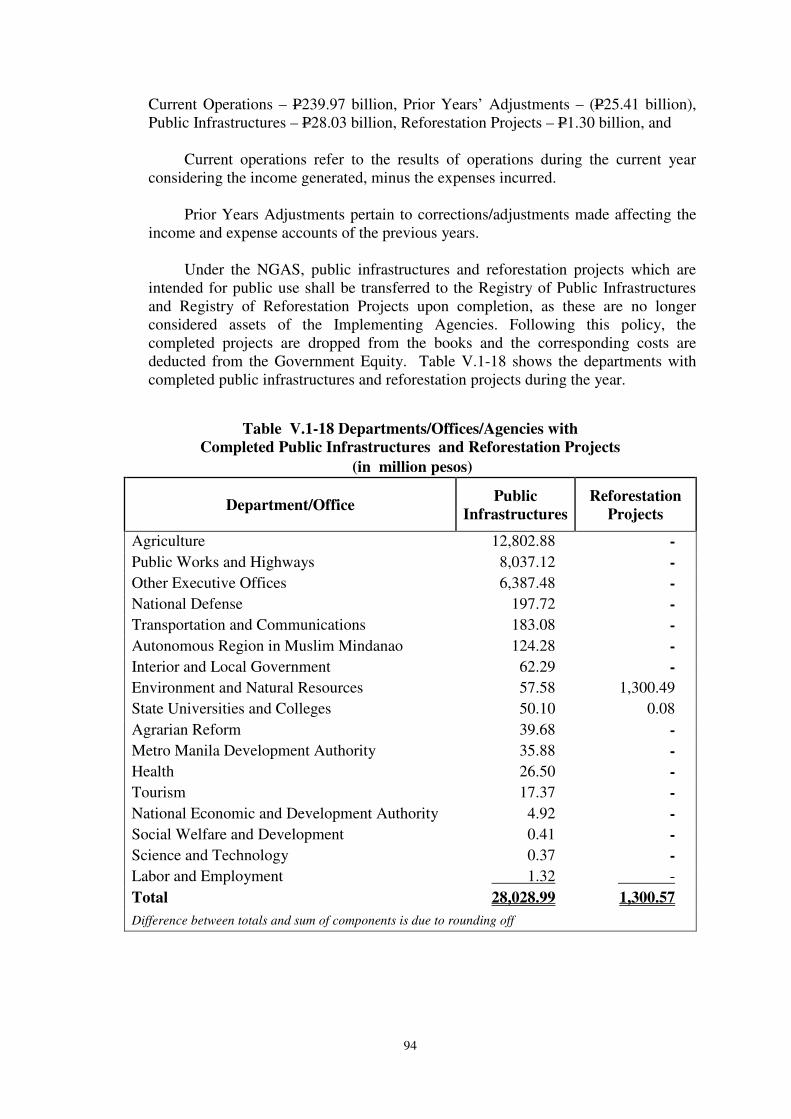

Reforestation Projects 94

V.2-1 Income/Revenue, Expenses, Subsidies and Net Loss 96

V.2-2 Comparative Income Taxes, By Source 98

V.2-3 Comparative Taxes on Goods and Services, By Source 98

V.2-4 Comparative Components of Property Taxes 99

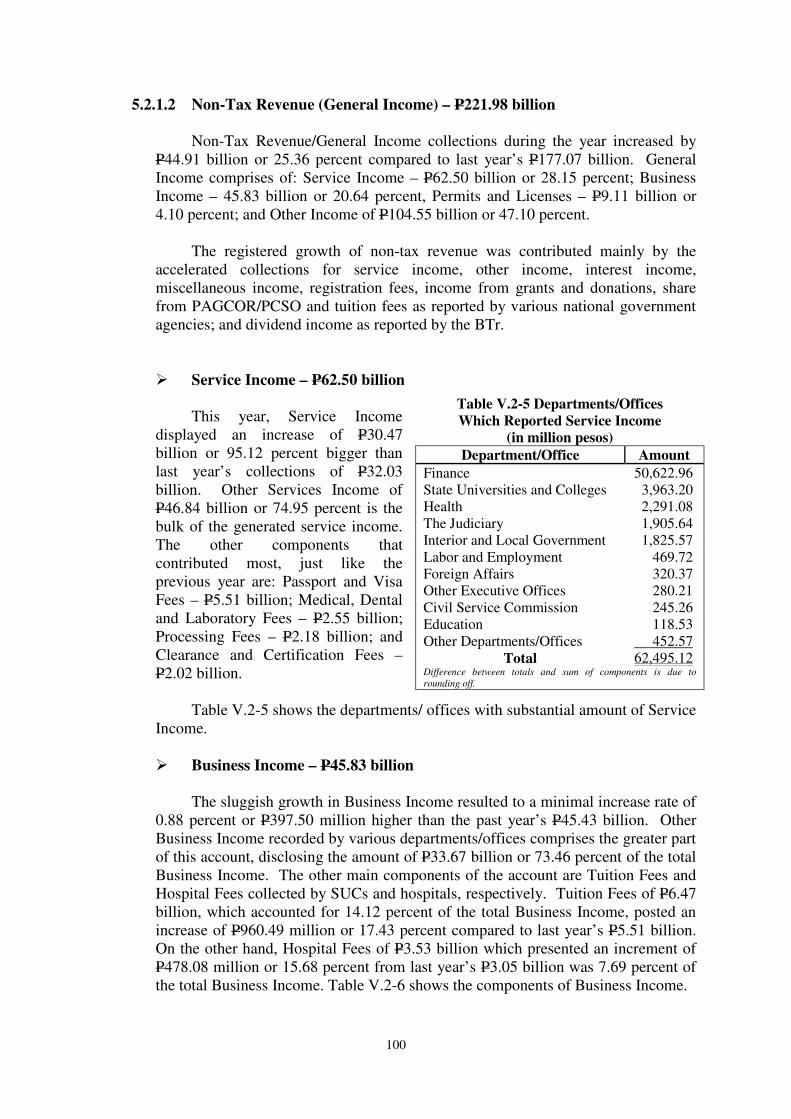

V.2-5 Departments/Offices Which Reported Service Income 100

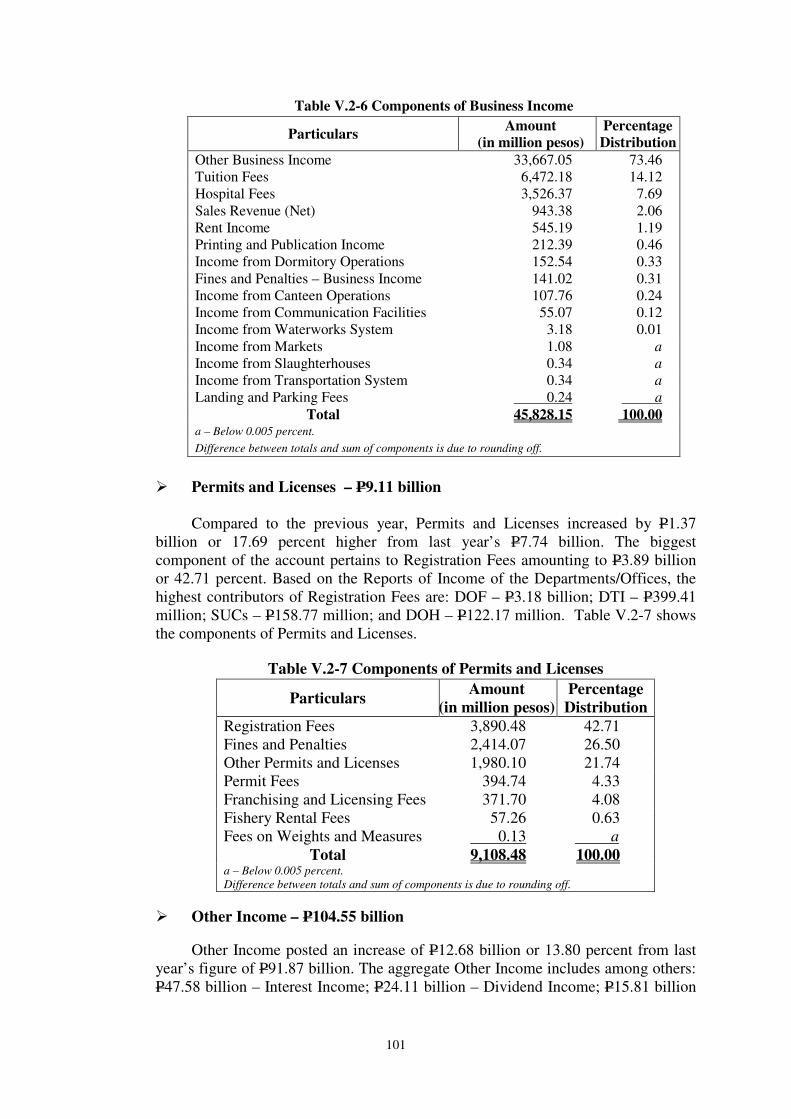

V.2-6 Components of Business Income 101

V.2-7 Components of Permits and Licenses 101

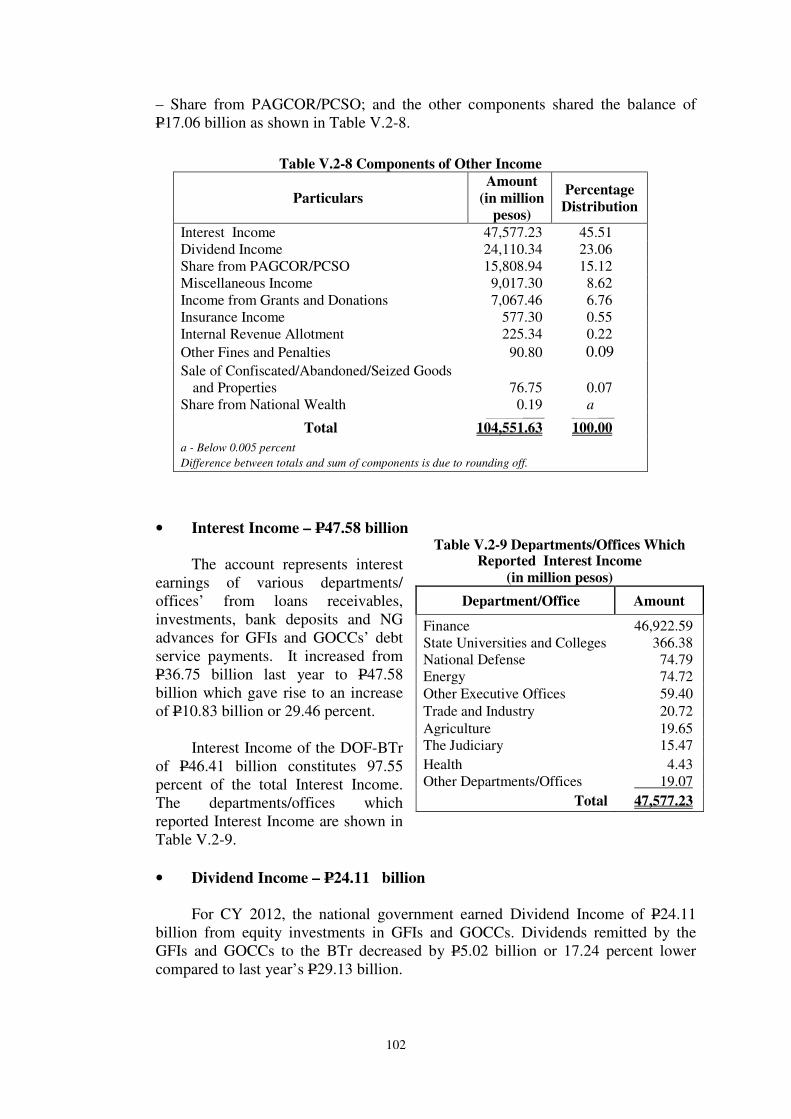

V.2-8 Components of Other Income 102

V.2-9 Departments/Offices which Reported Interest Income 102

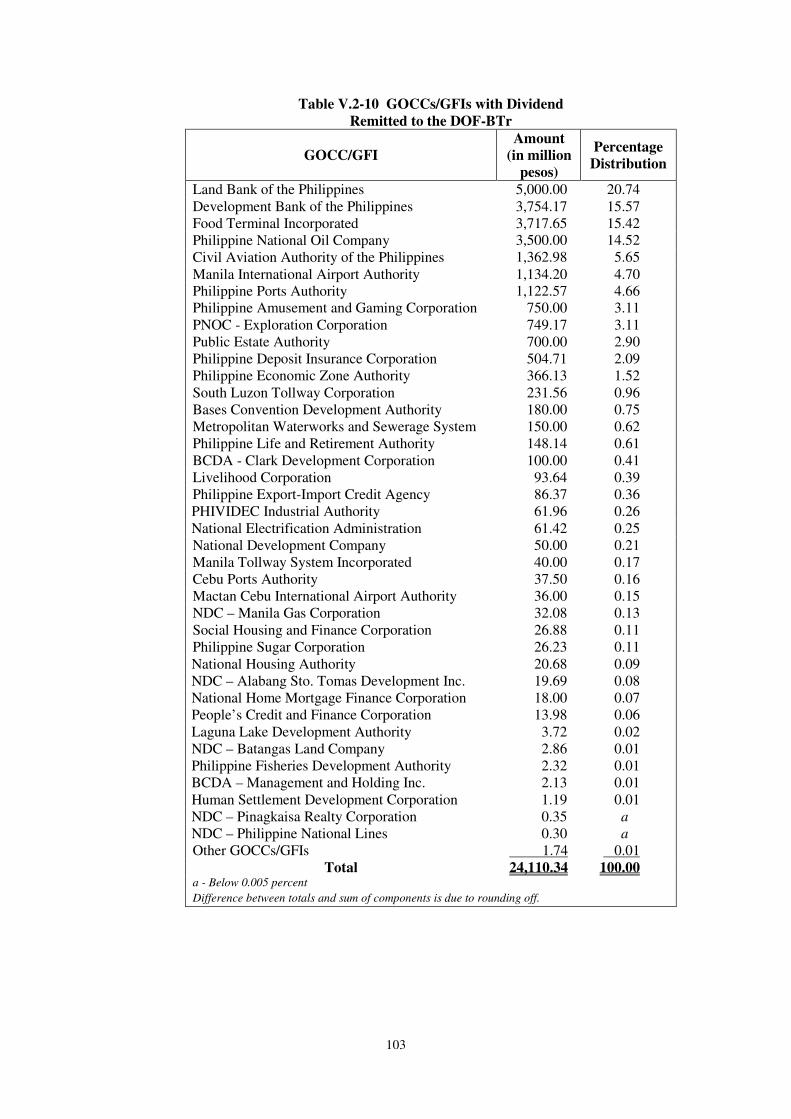

V.2-10 GOCCs/GFIs with Dividend 103

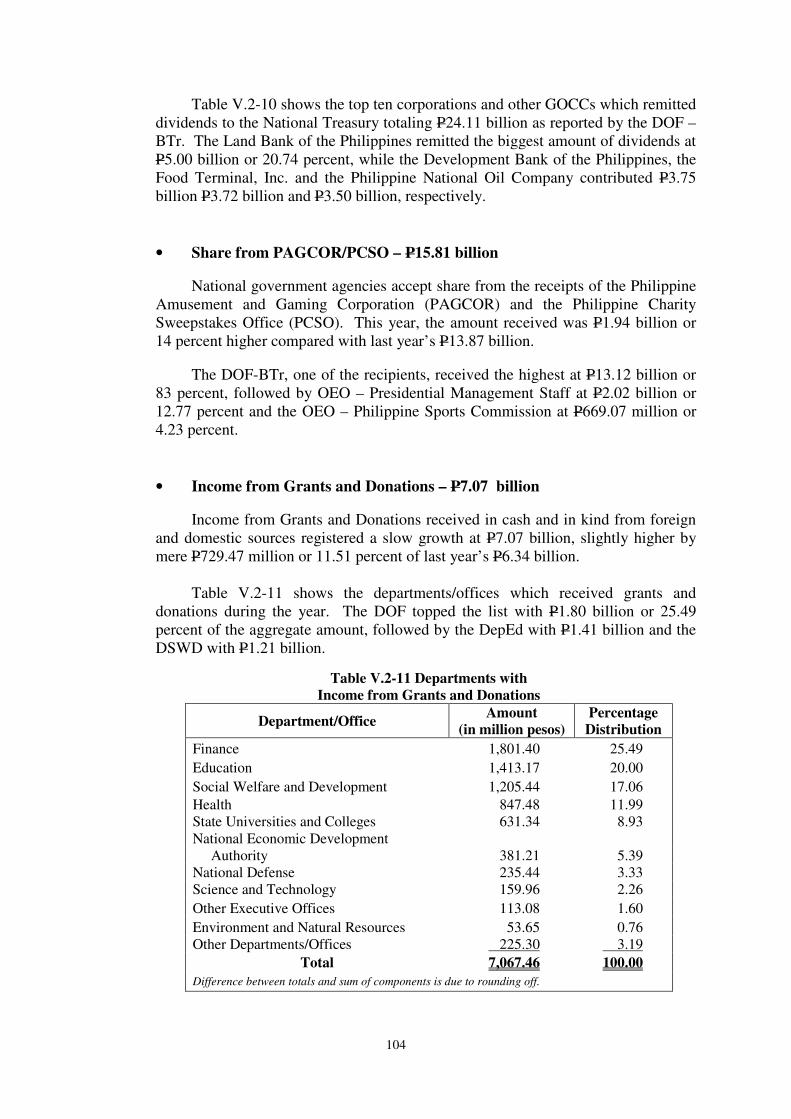

V.2-11 Departments with Income from Grants and Donations 104

V.2-12 Departments/Offices which Reported Miscellaneous Income 105

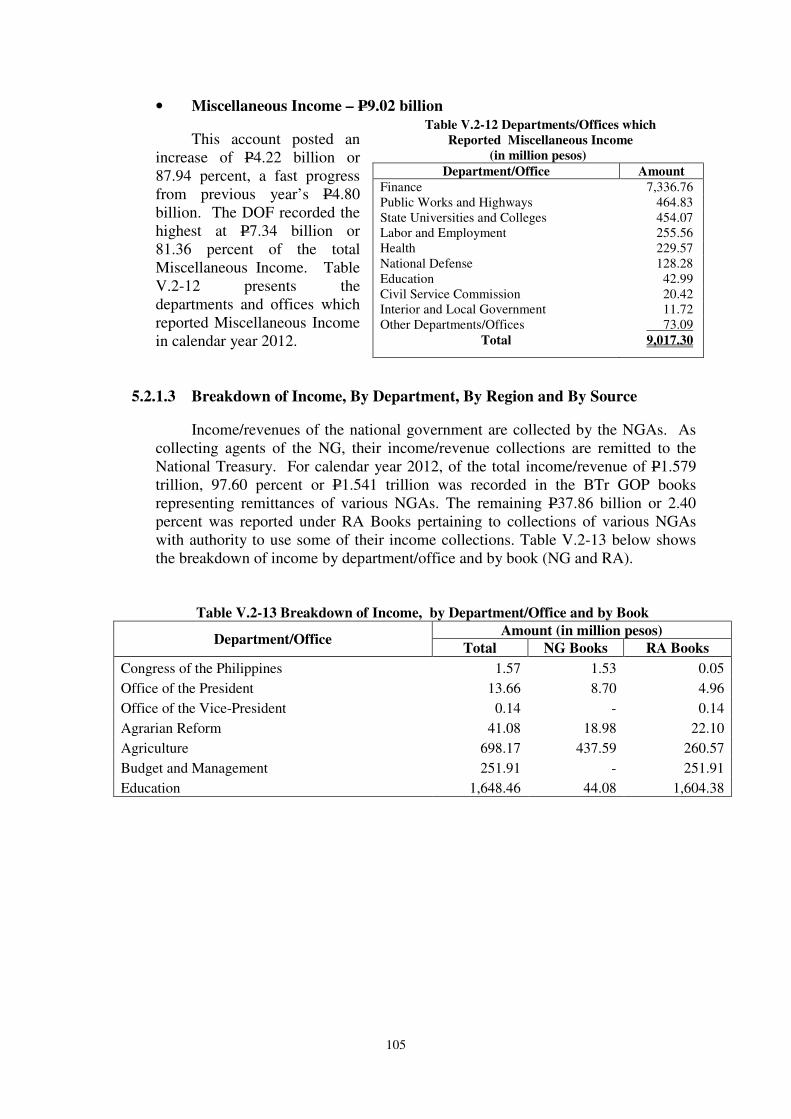

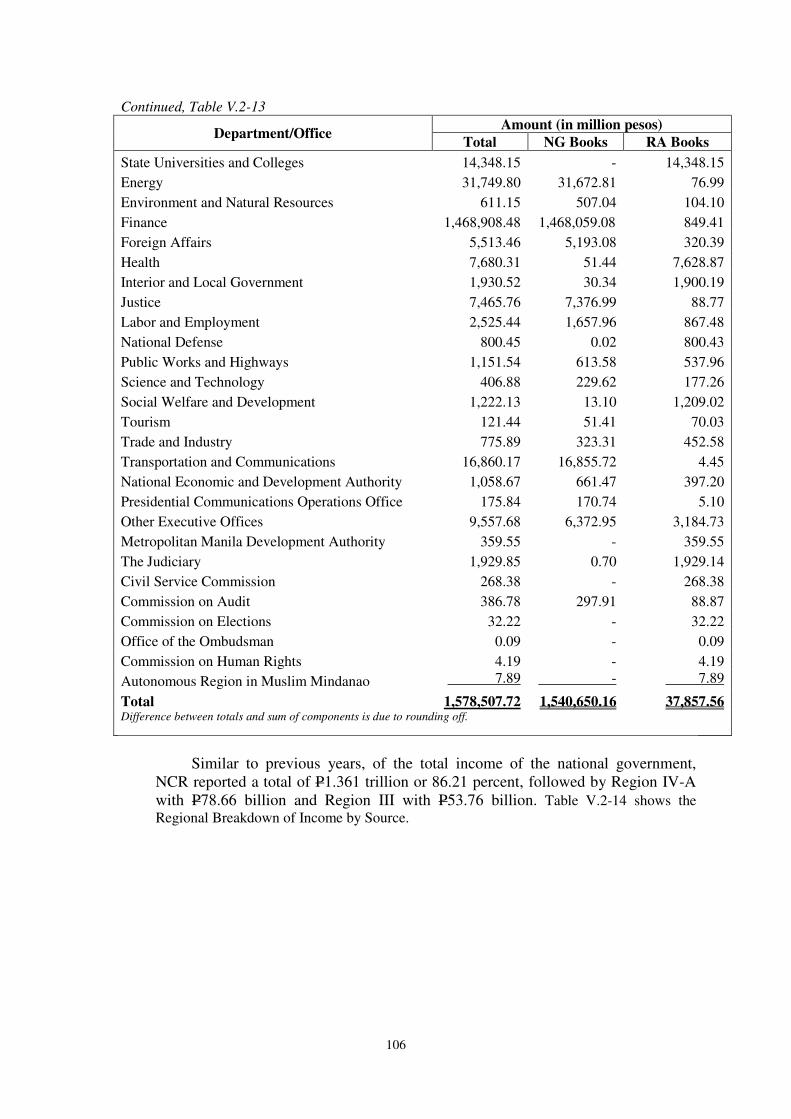

V.2-13 Breakdown of Income, by Department/Office and by Book 105

V.2-14 Regional Breakdown of Income by Source 107

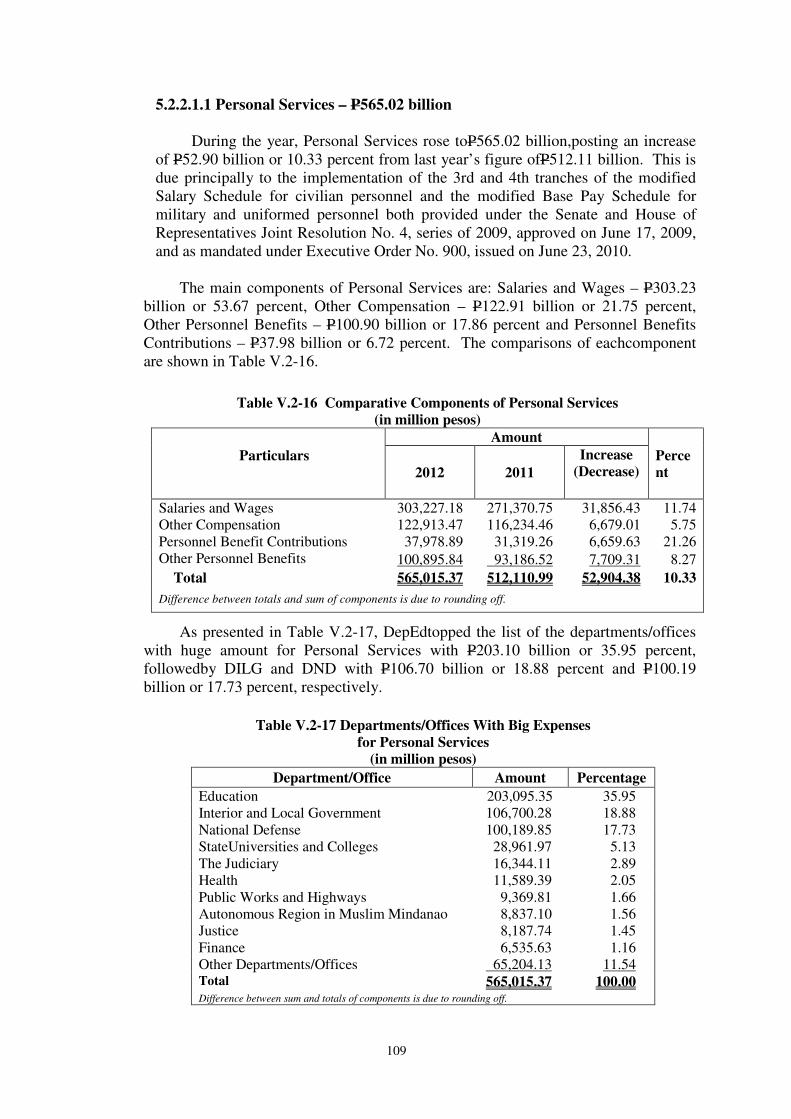

V.2-15 Departments/Offices with Highest Current Operating Expenses 108

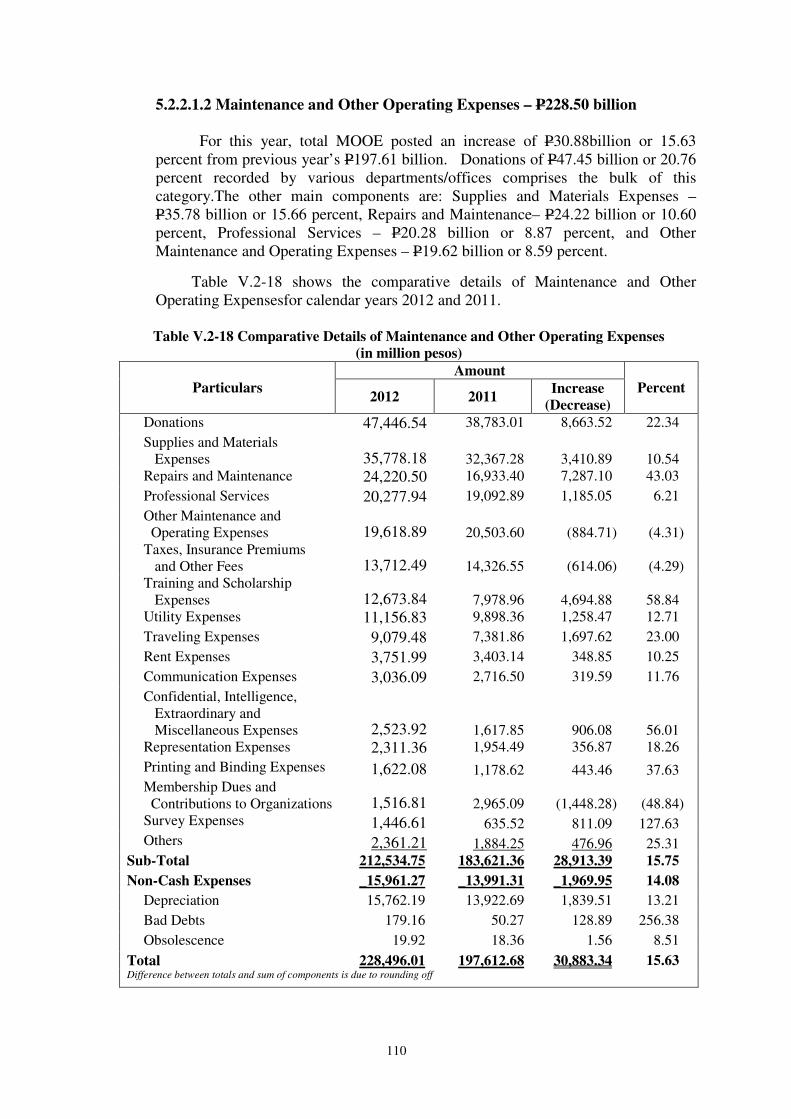

V.2-16 Comparative Components of Personal Services 109

V.2-17 Departments/Offices with Big Expenses for Personal Services 109

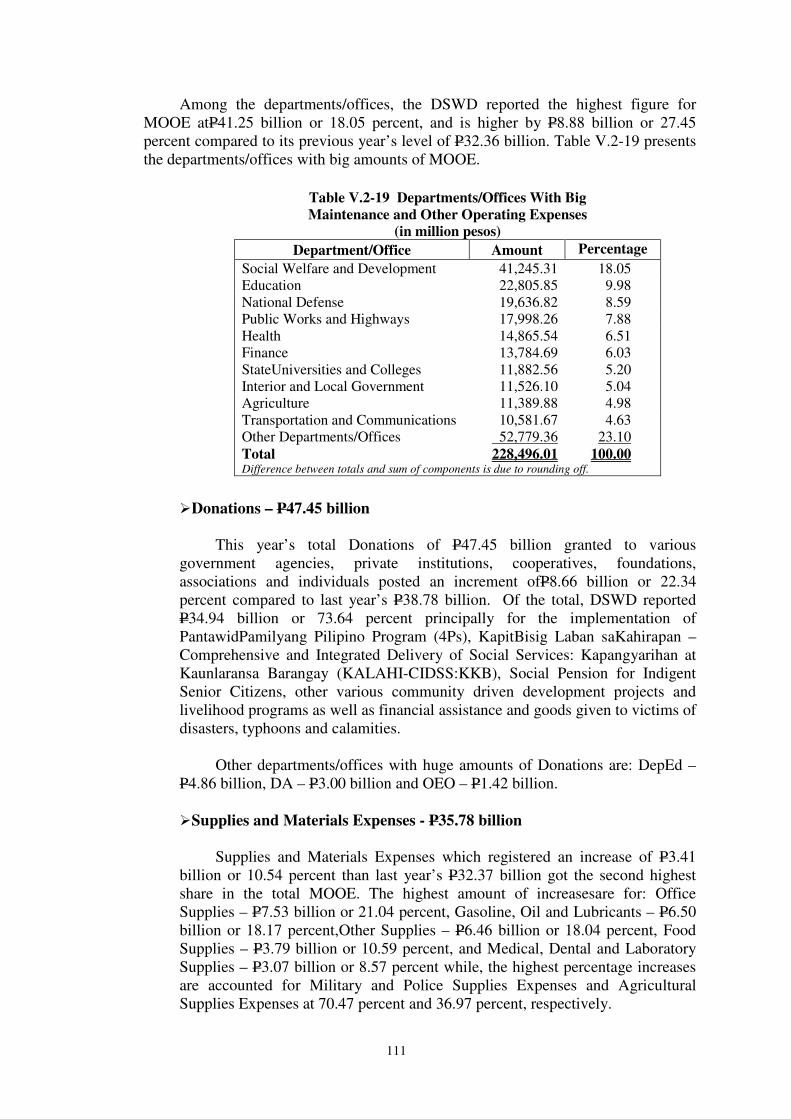

V.2-18 Comparative Details of Maintenance and Other Operating Expenses 110

V.2-19 Departments/Offices with Big Maintenance and Other Operating

Expenses 111

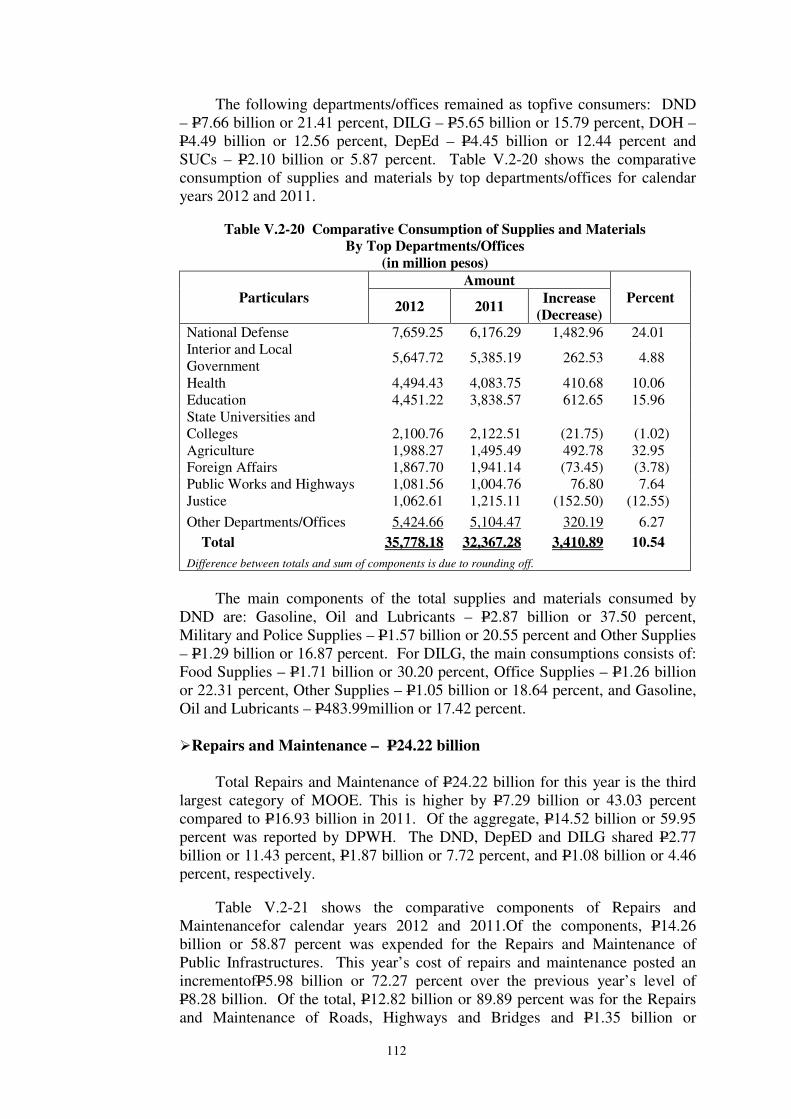

V.2-20 Comparative Consumption of Supplies and Materials,

By Top Departments/Offices 112

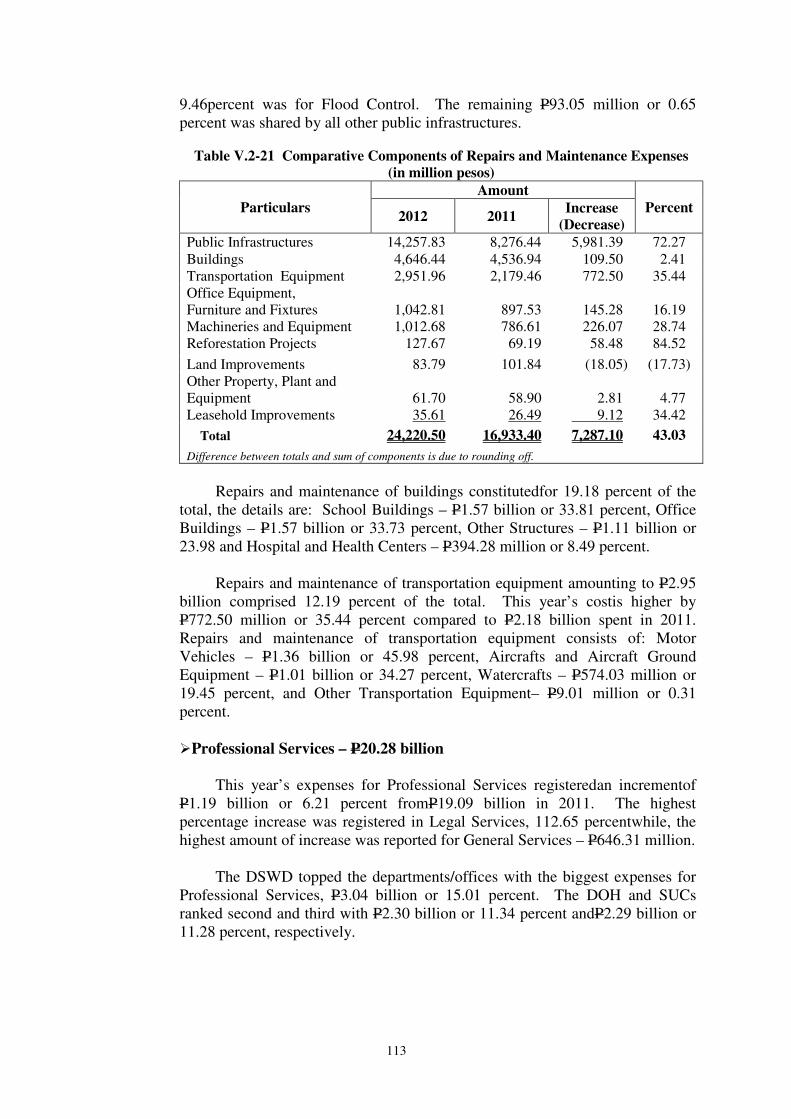

V.2-21 Comparative Components of Repairs and Maintenance Expenses 113

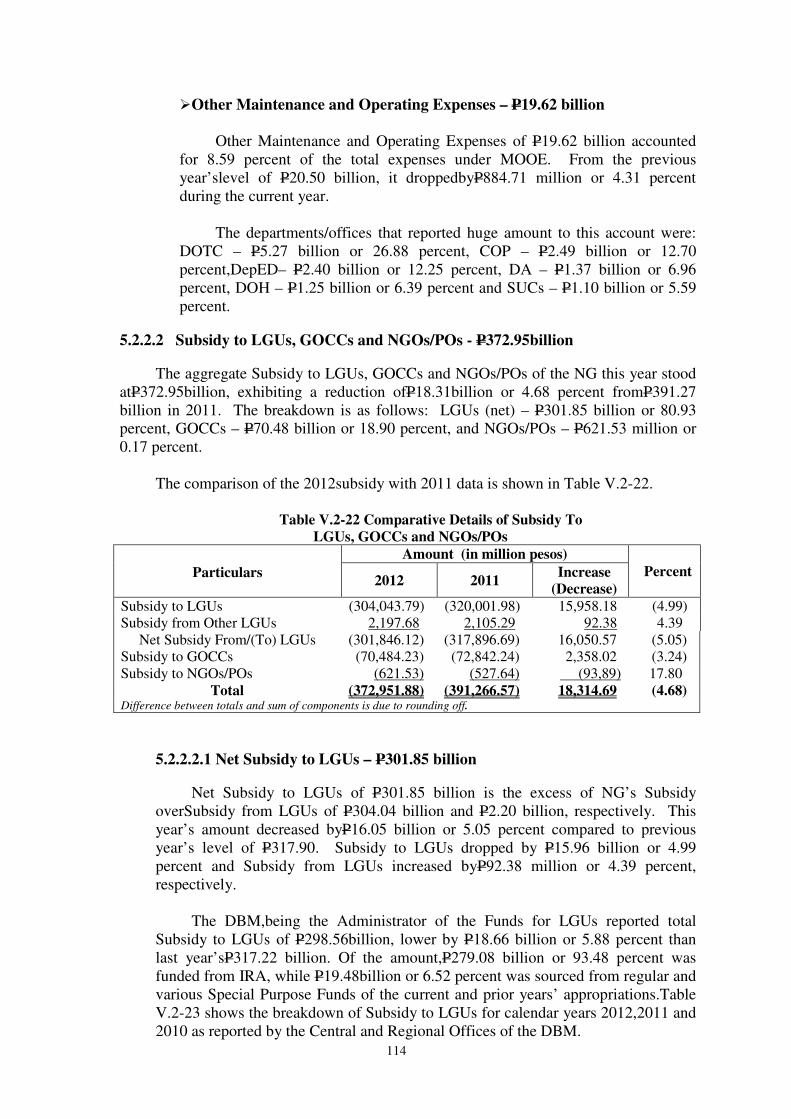

V.2-22 Comparative Details of Subsidy To LGUs, GOCCs and NGOs/POs 114

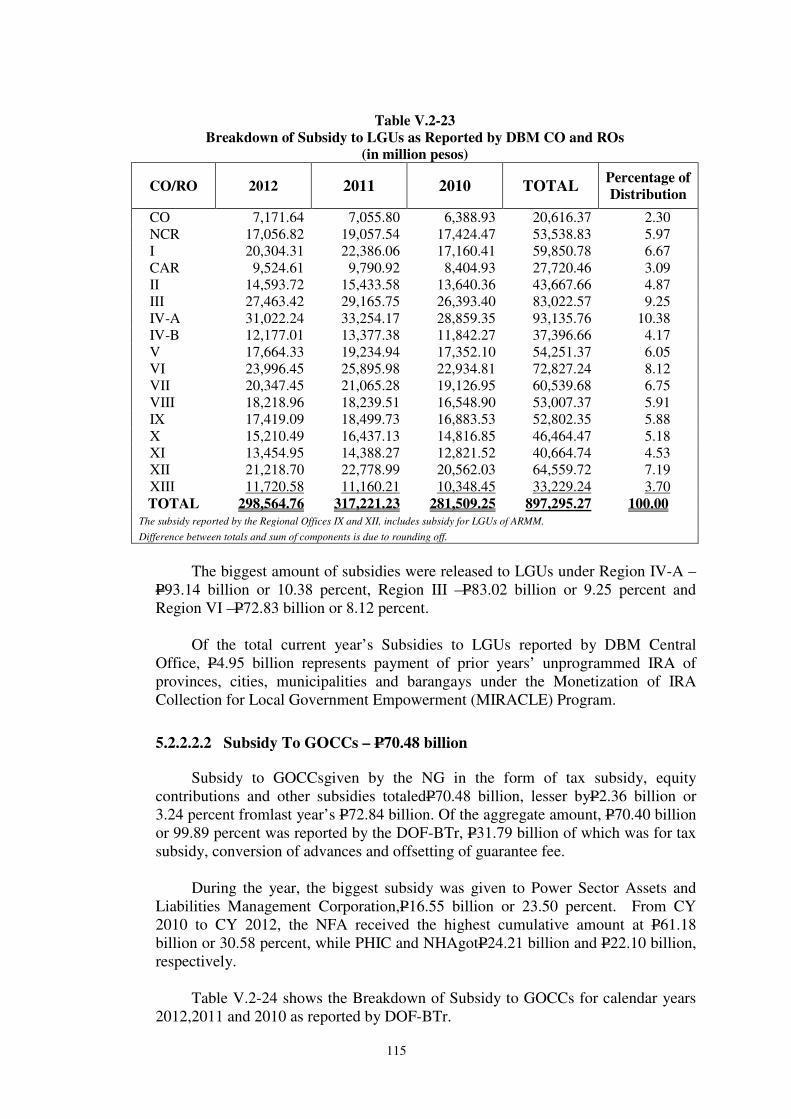

V.2-23 Breakdown of Subsidy to LGUs as Reported by DBM CO and ROs 115

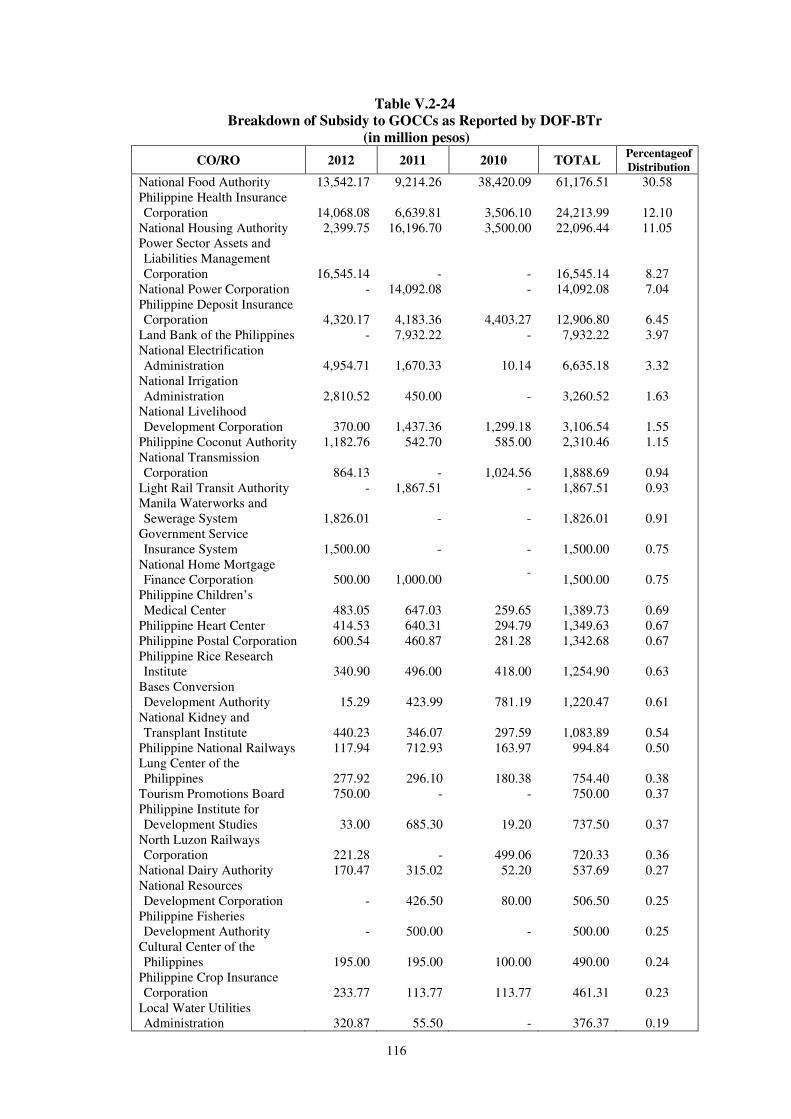

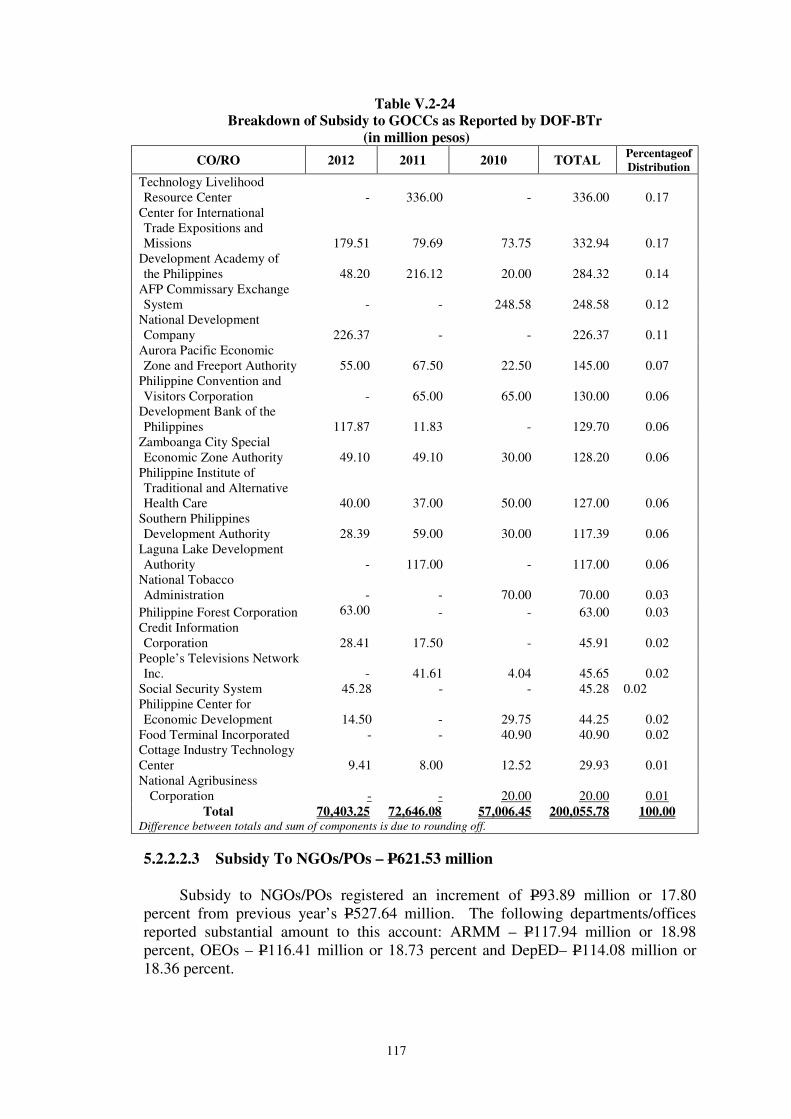

V.2-24 Breakdown of Subsidy to GOCCs as Reported by DOF-BTr 116

V.2-25 Comparative Components of Financial Expenses 118

V.2-26 Regional Breakdown of Expenses and Subsidies 118

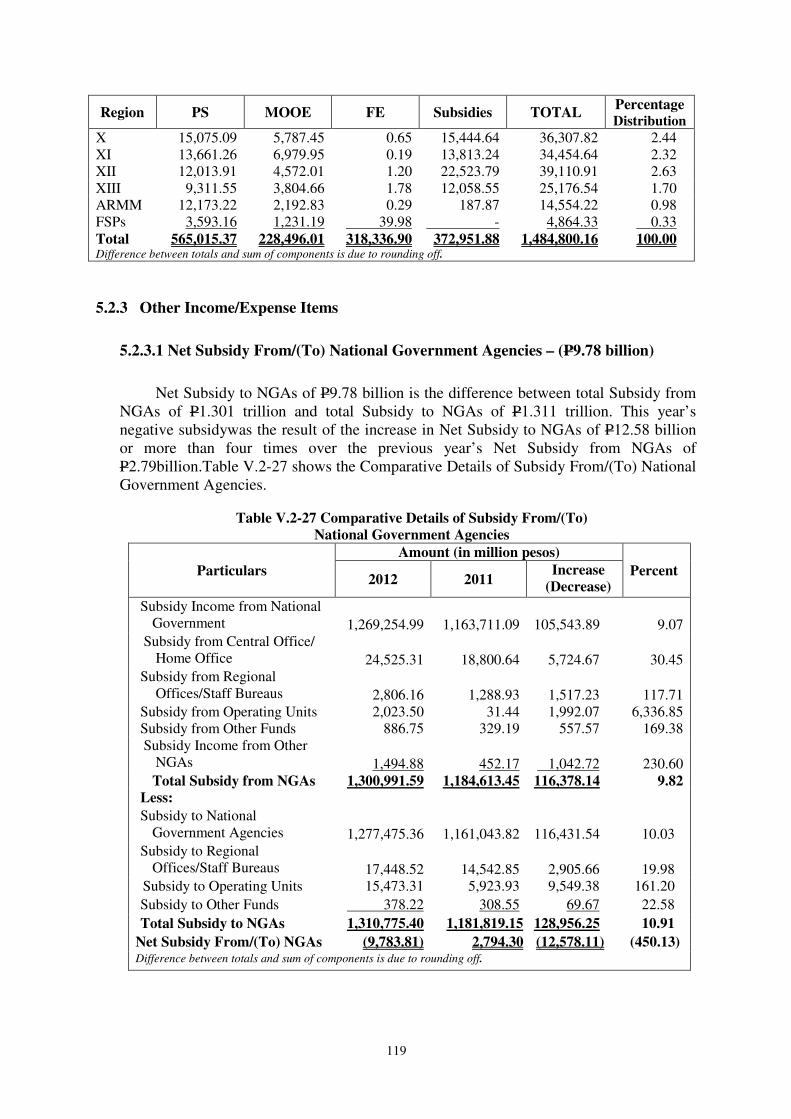

V.2-27 Comparative Details of Subsidy From (To) National Government Agencies 119

iv

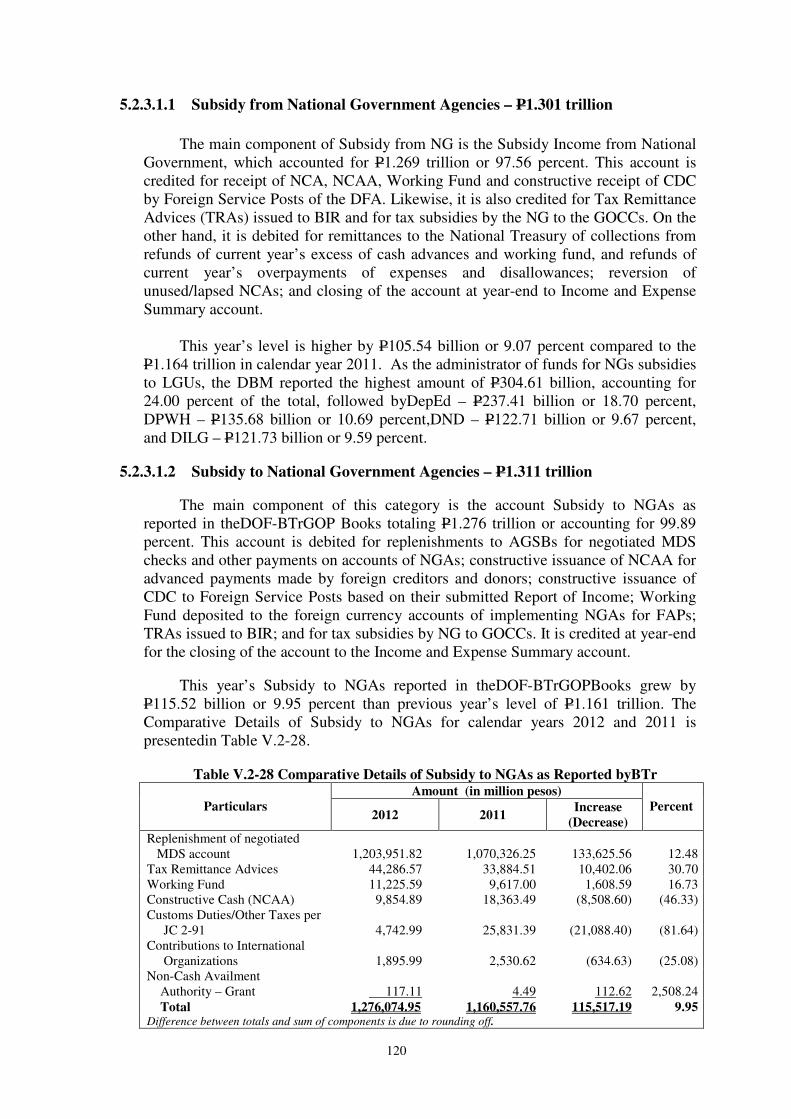

V.2-28 Comparative Details of Subsidy To NGAs as Reported by BTr 120

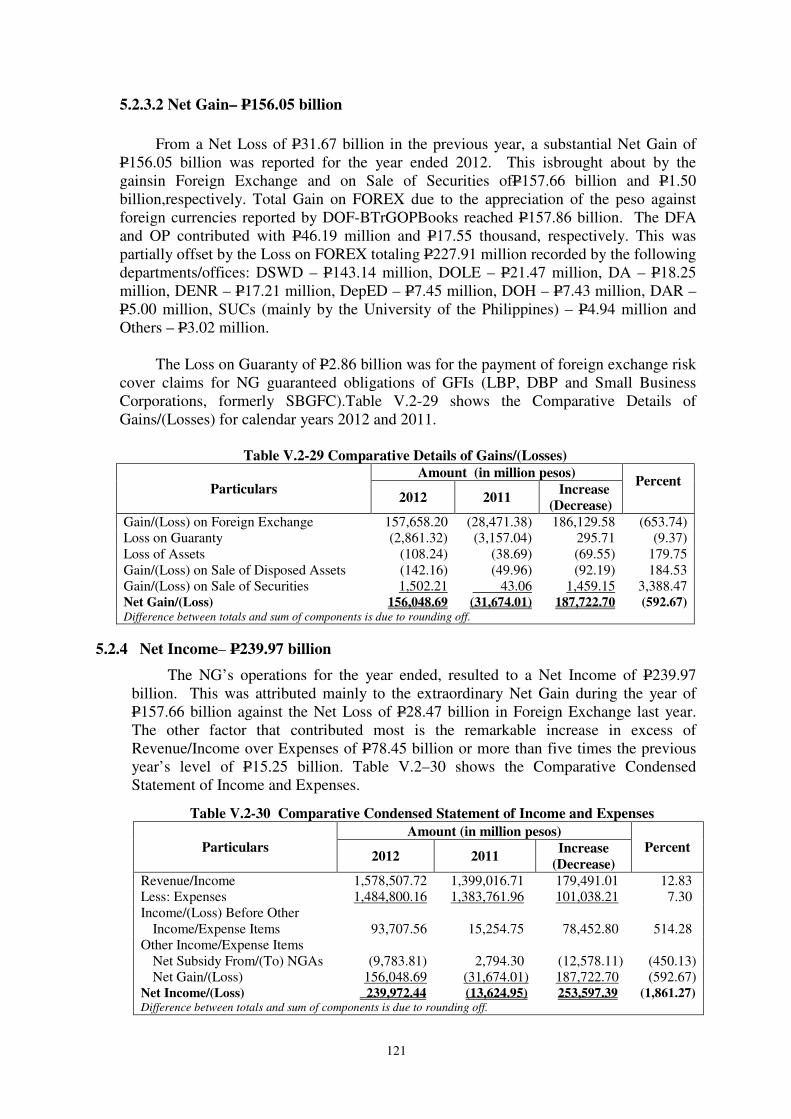

V.2-29 Comparative Details of Gains/(Losses) 121

V.2-30 Comparative Condensed Statement of Income and Expenses 121

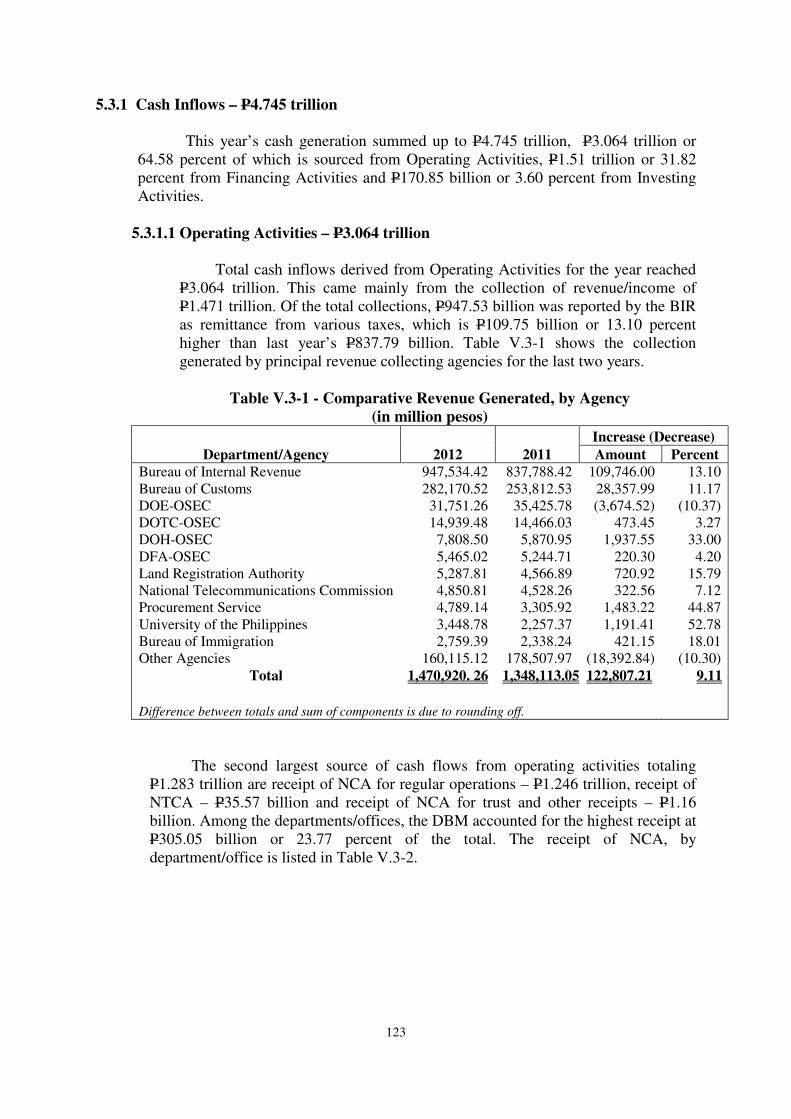

V.3-1 Comparative Revenue Generated, by Agency 123

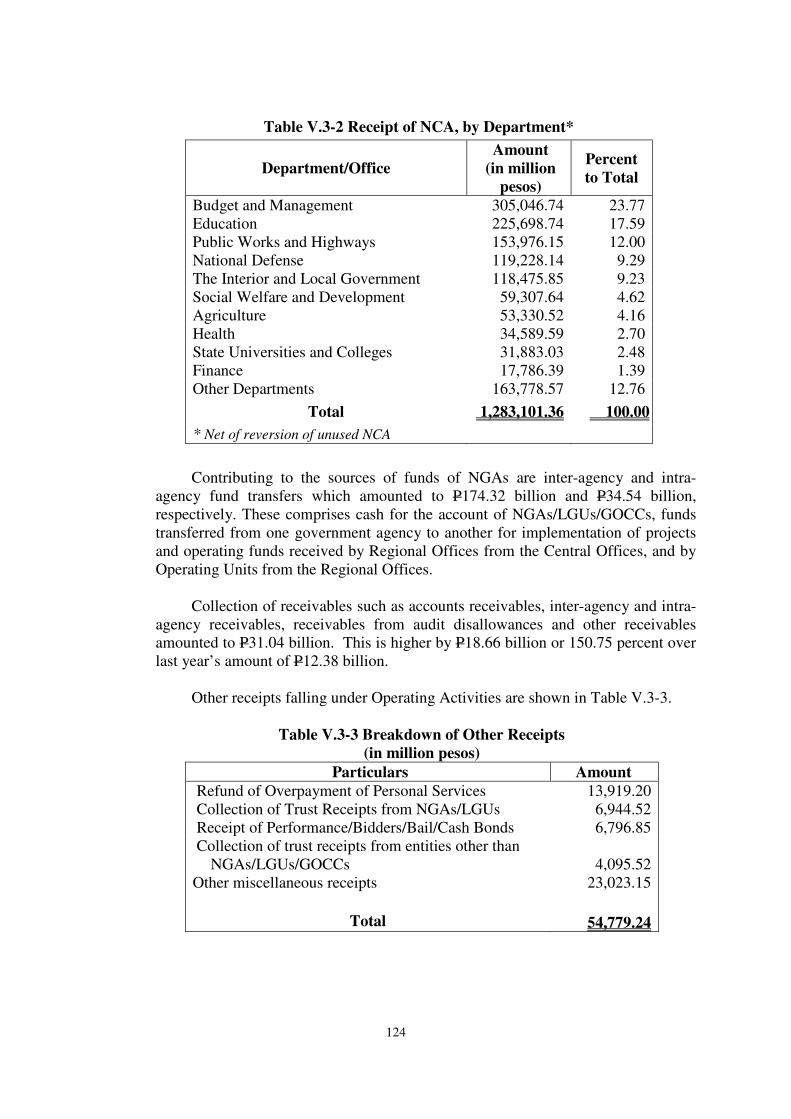

V.3-2 Receipt of NCA, By Department 124

V.3-3 Breakdown of Other Receipts 124

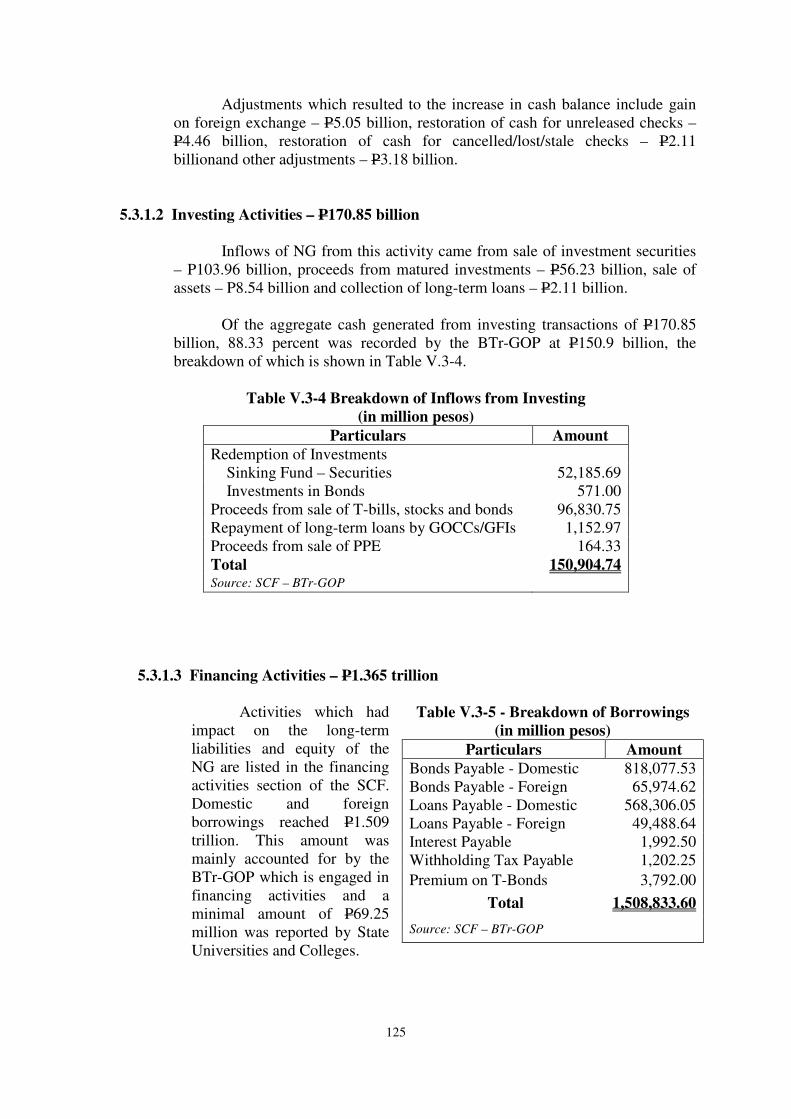

V.3-4 Breakdown of Inflows from Investing 125

V.3-5 Breakdown of Borrowings 125

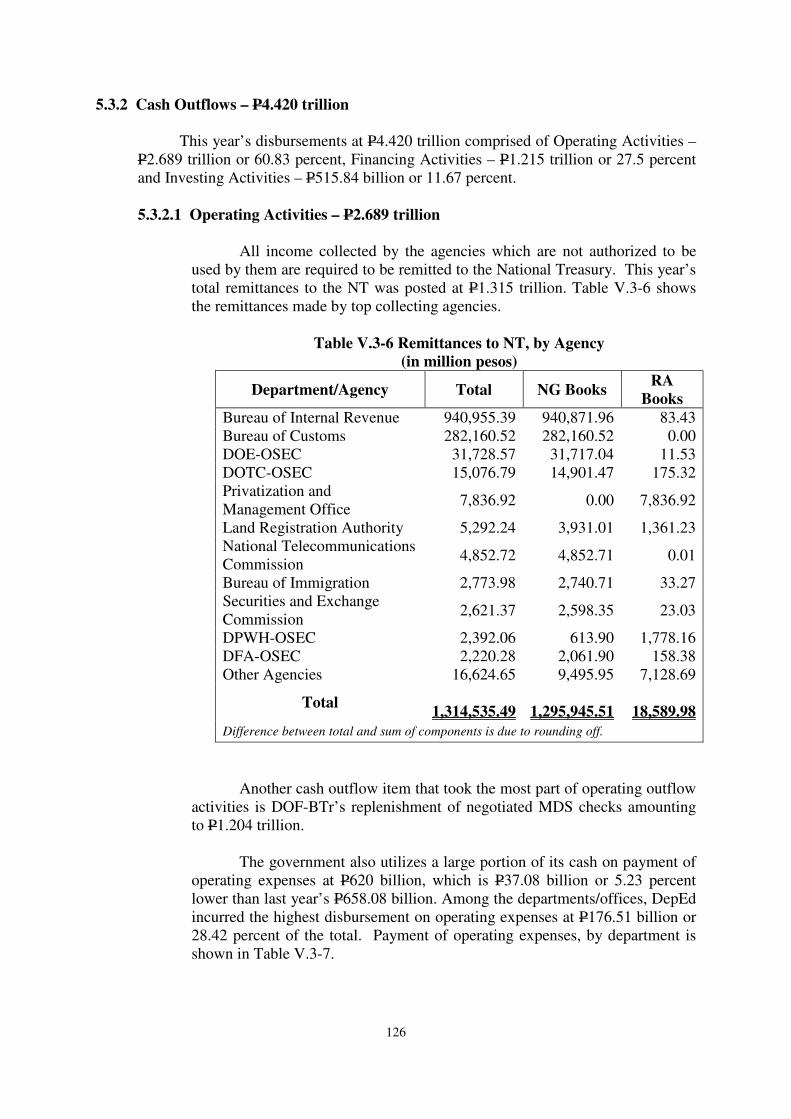

V.3-6 Remittances to NT, by Agency 126

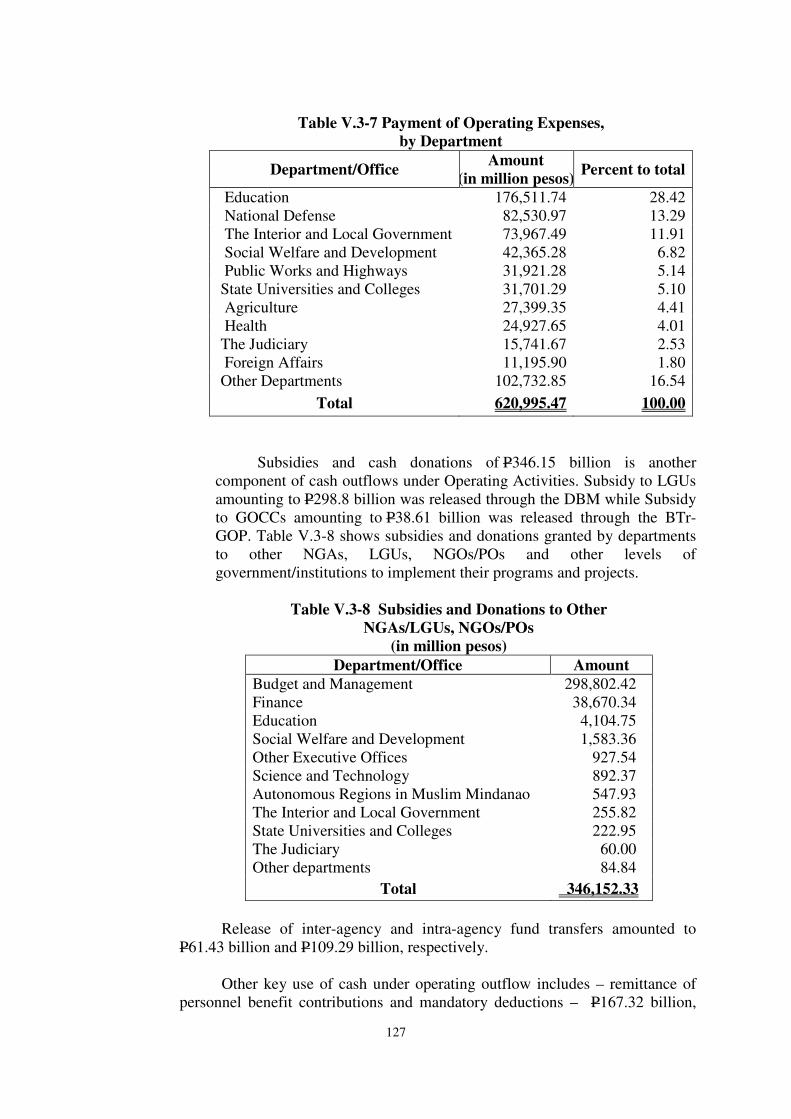

V.3-7 Payment of Operating Expenses, by Department 127

V.3-8 Subsidies and Donations to Other NGAs/LGUs, NGOs/POs 127

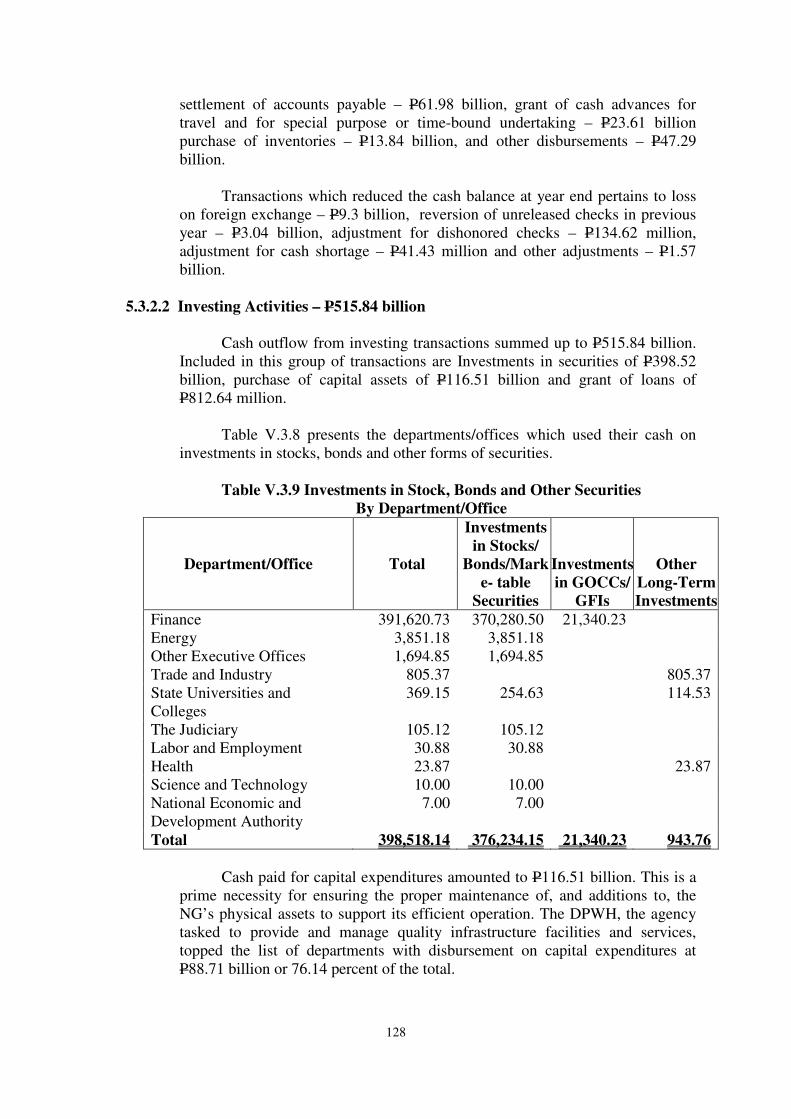

V.3-9 Investments in Stocks, Bonds and Other Securities, by Department/Office 128

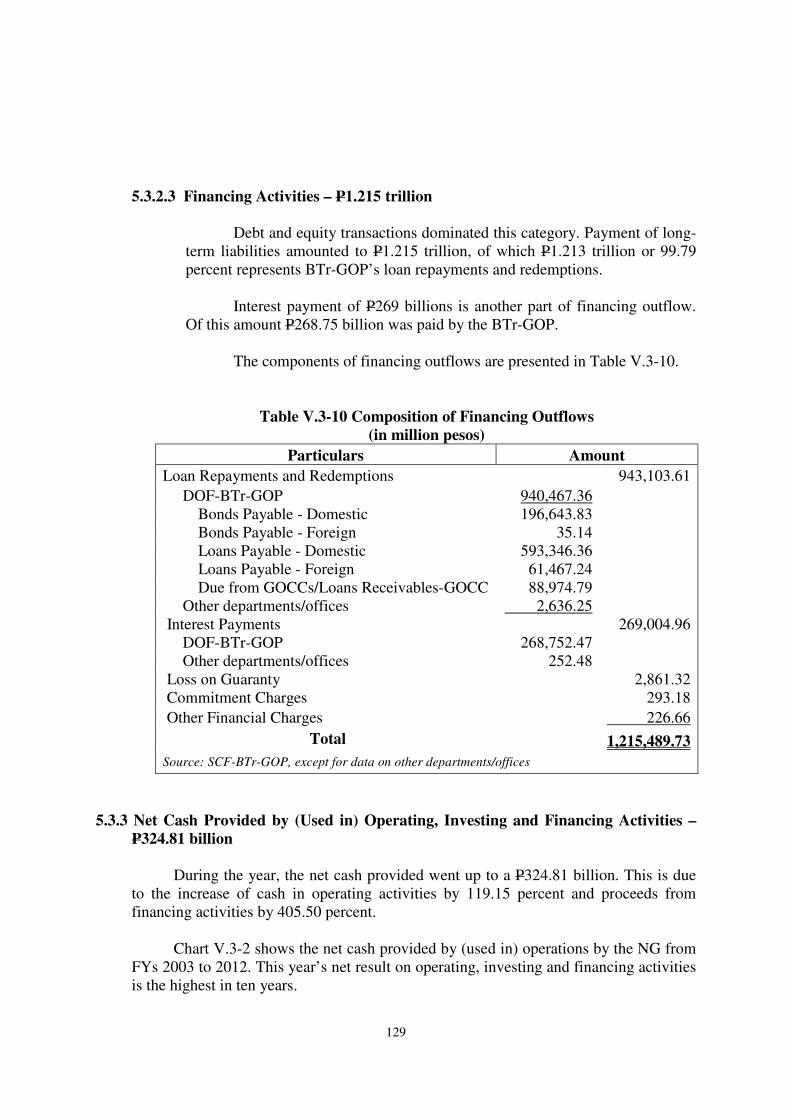

V.3-10 Composition of Financing Outflows 129

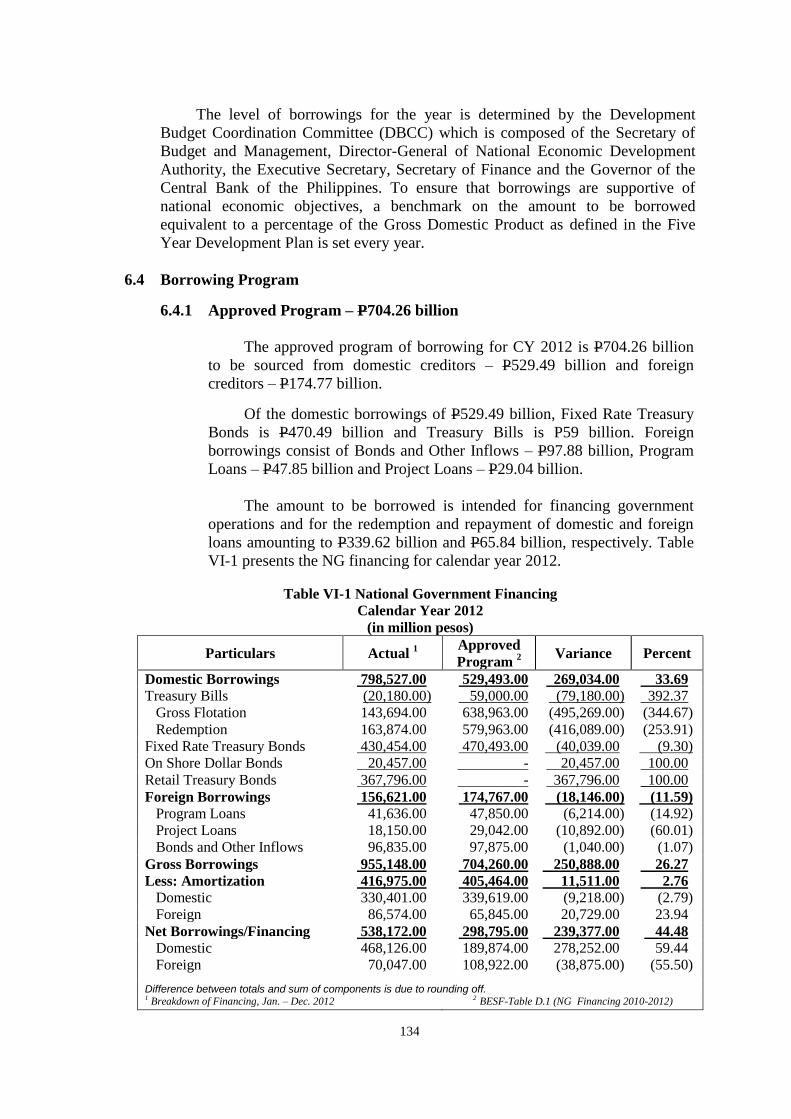

National Government Debt

VI-1 National Government Financing 134

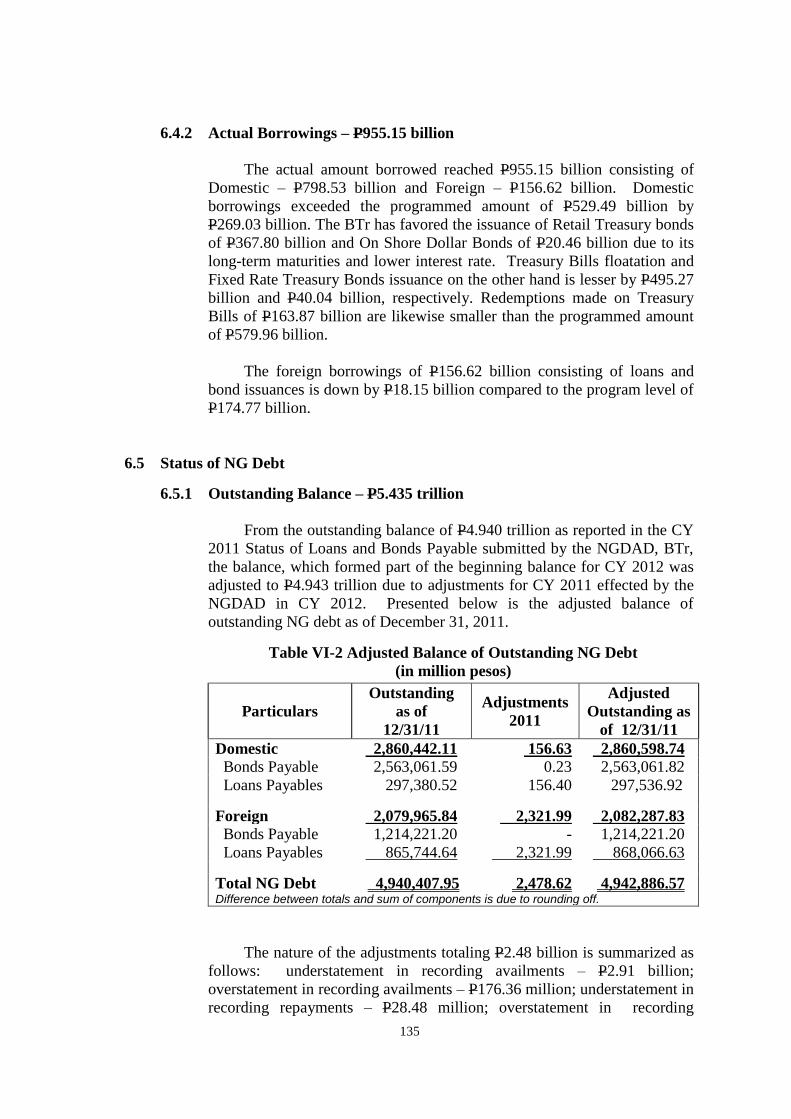

VI-2 Adjusted Balance of Outstanding NG Debt 135

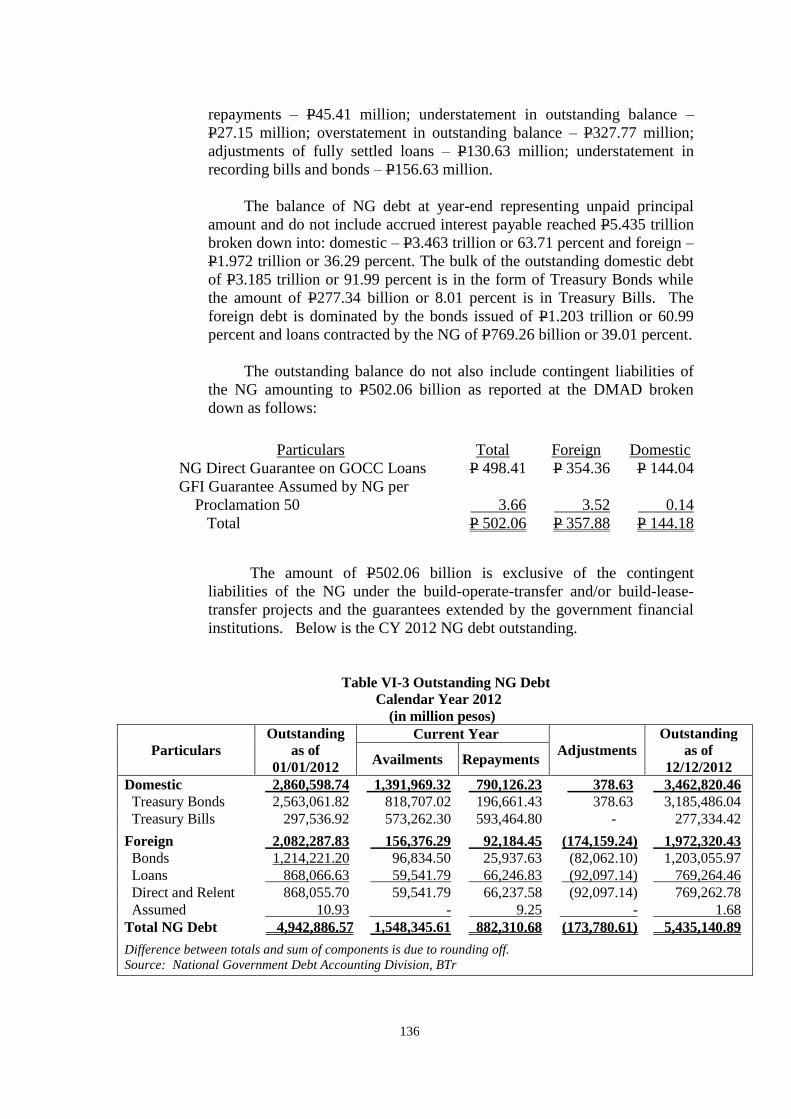

VI-3 Outstanding NG Debt, Calendar Year 2012 136

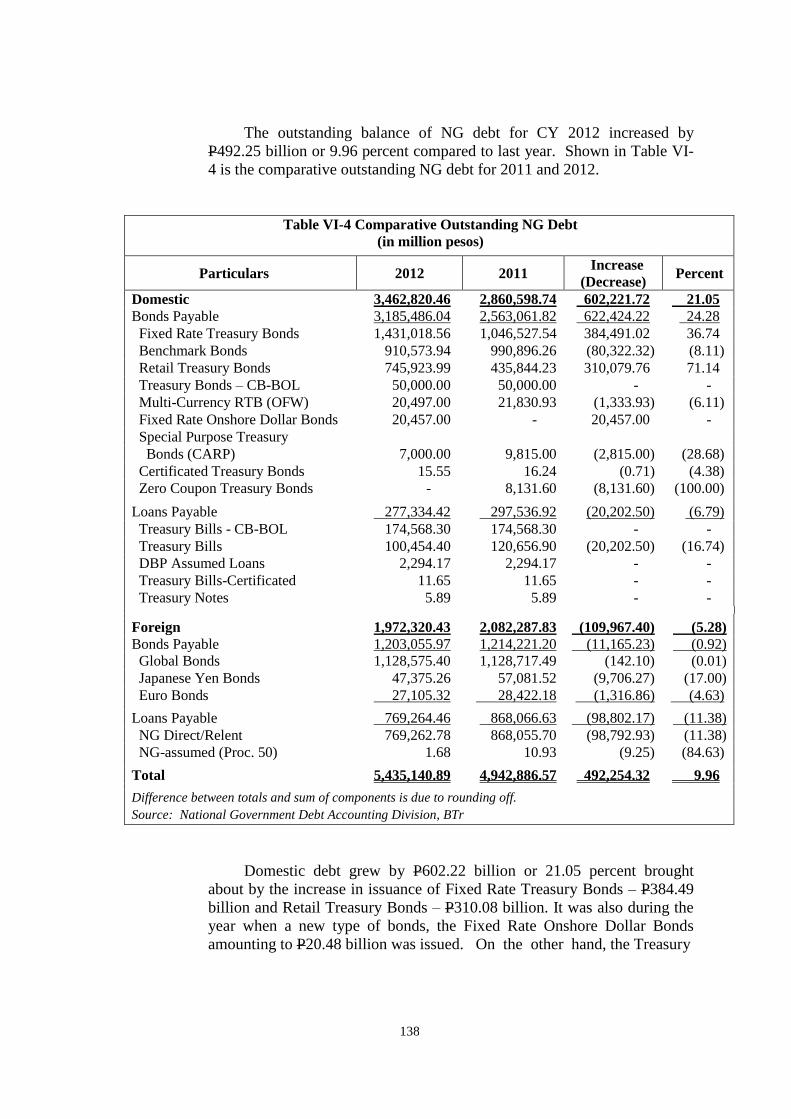

VI-4 Comparative Outstanding NG Debt 138

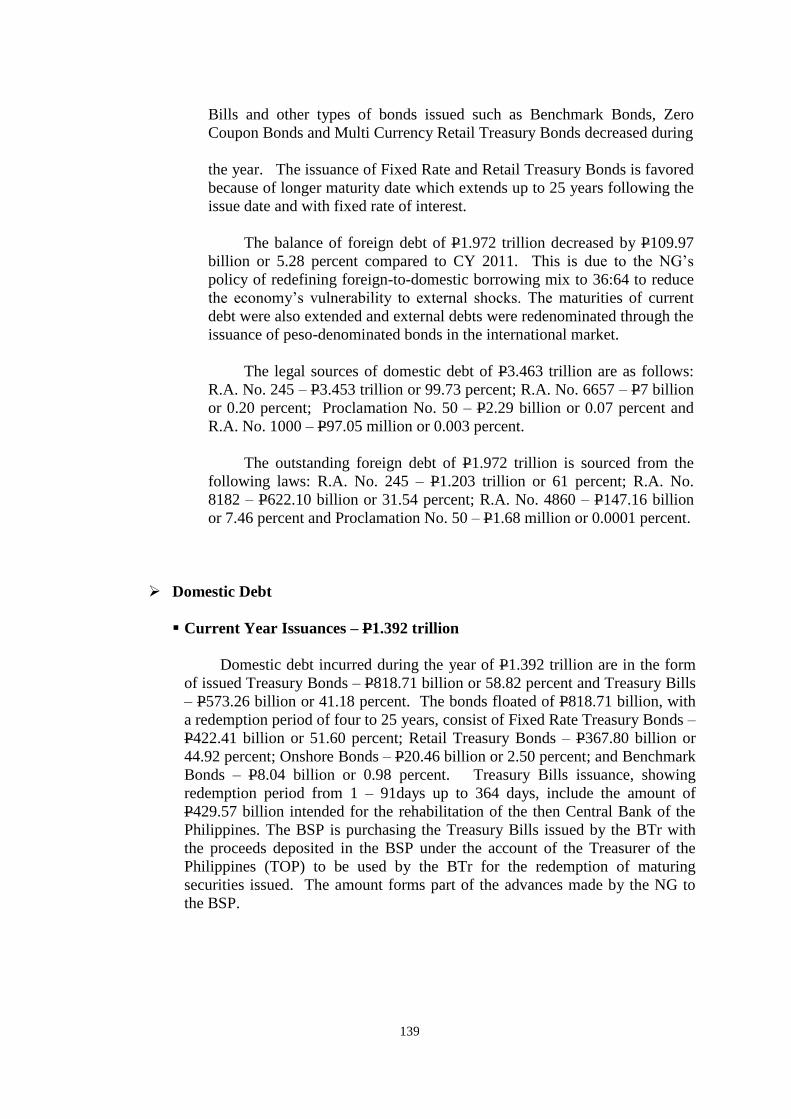

VI-5 Composition of Domestic Issuances 140

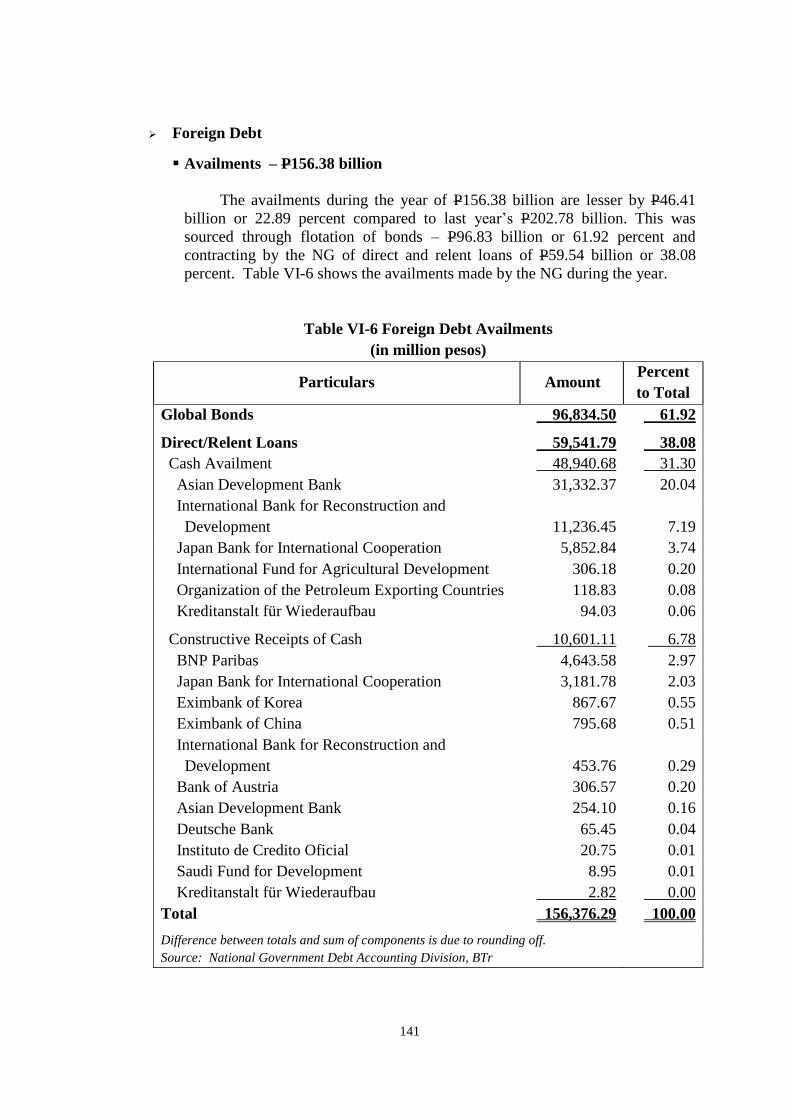

VI-6 Foreign Debt Availments 141

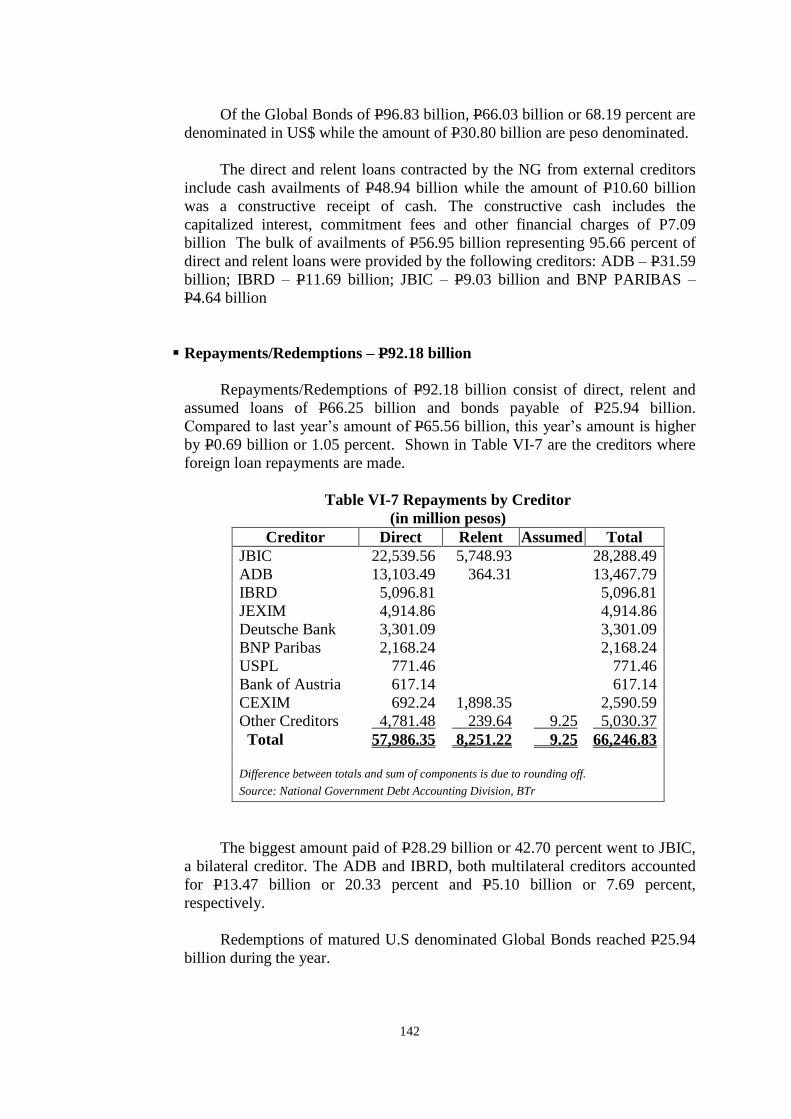

VI-7 Repayments by Creditor 142

VI-8 Growth of Outstanding NG Debt 143

VI-9 Comparative Interest Payments of the NG 145

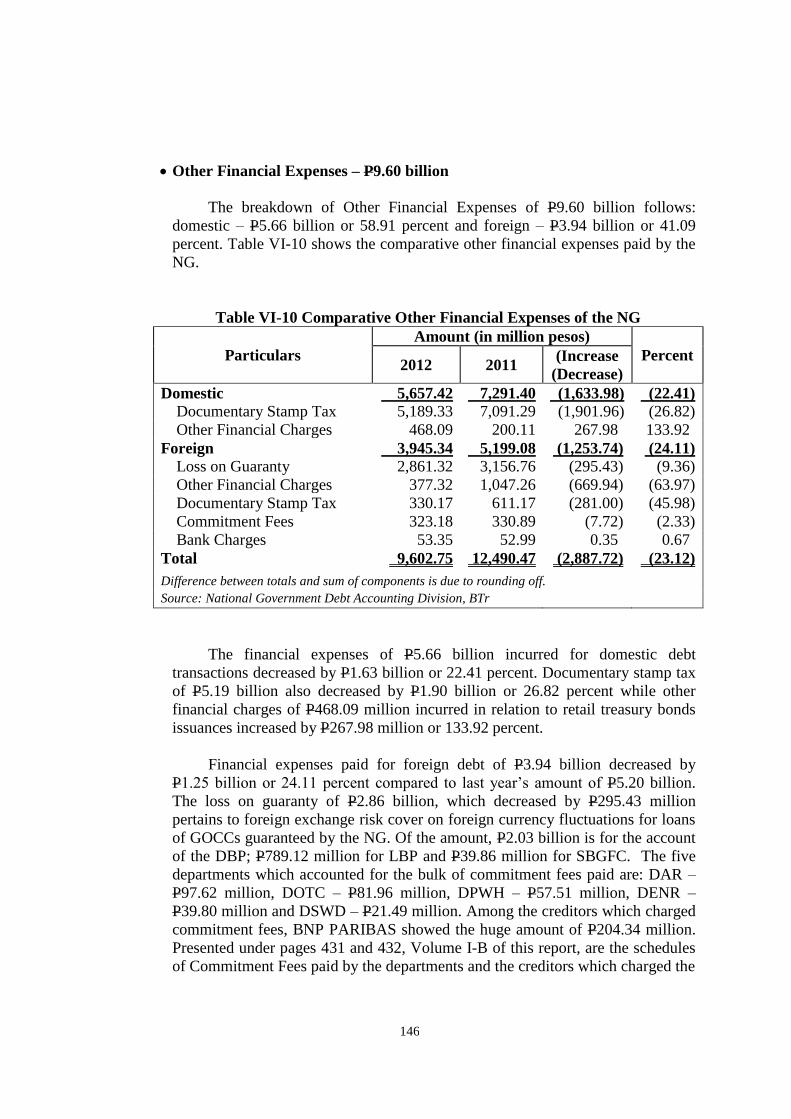

VI-10 Comparative Other Financial Expenses of the NG 146

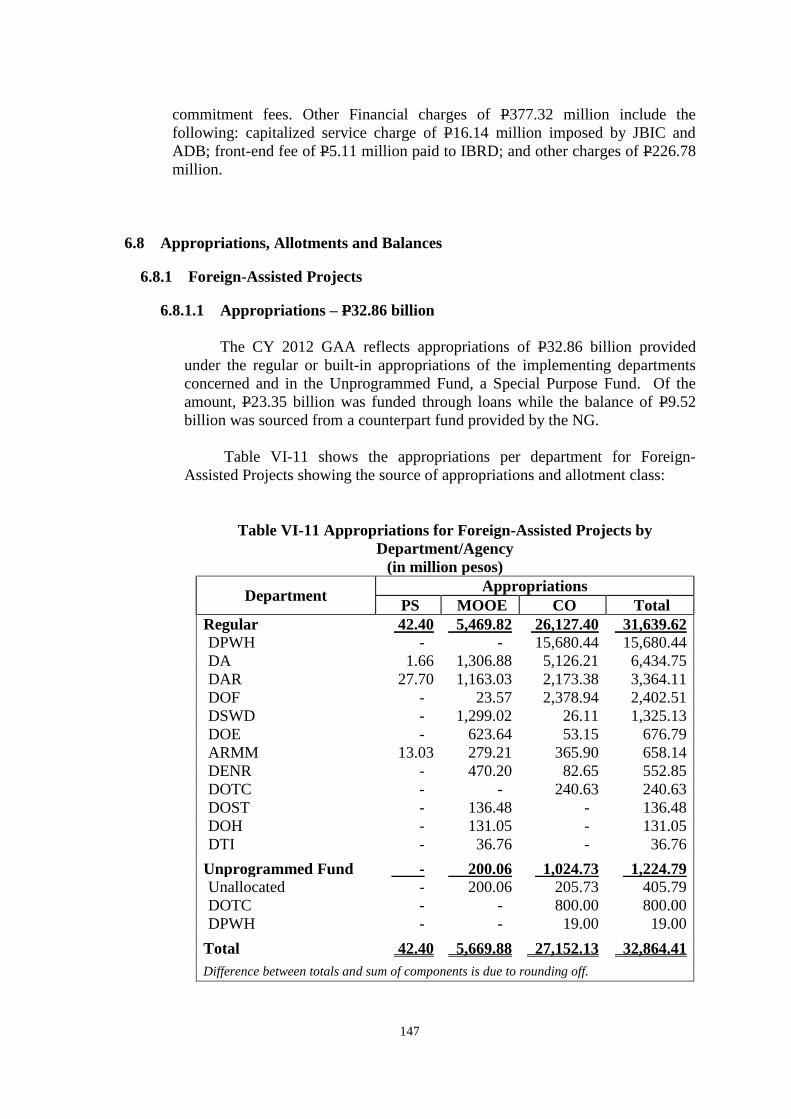

VI-11 Appropriations for Foreign-Assisted Projects by Department/Agency 147

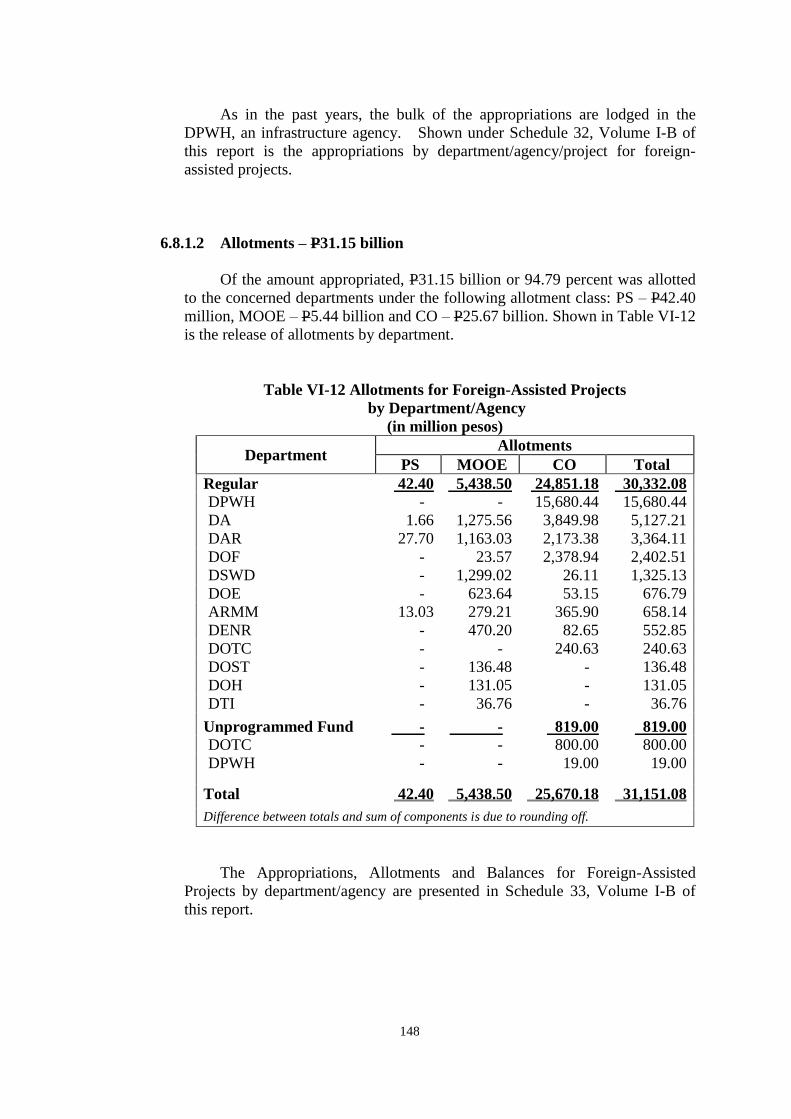

VI-12 Allotments for Foreign-Assisted Projects by Department/Agency 148

Special Account in the General Fund

VII-1 Appropriations, Allotments and Obligations, Special Account in the

General Fund (Net of CARP) 152

VII-2 Expenses by Department/Office Special Account in the General Fund

(Net of CARP) 155

Comprehensive Agrarian Reform Program

VIII-1 Appropriations for CARP 157

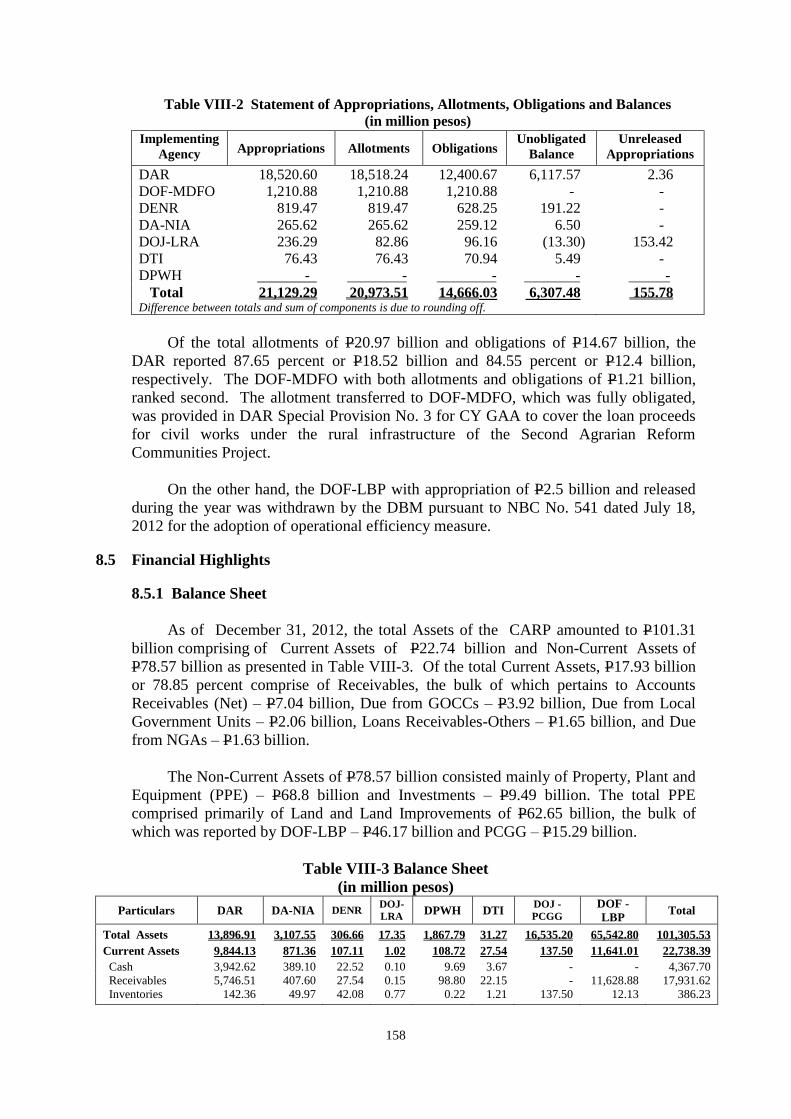

VIII-2 Statement of Appropriations, Allotments, Obligations and Balances 158

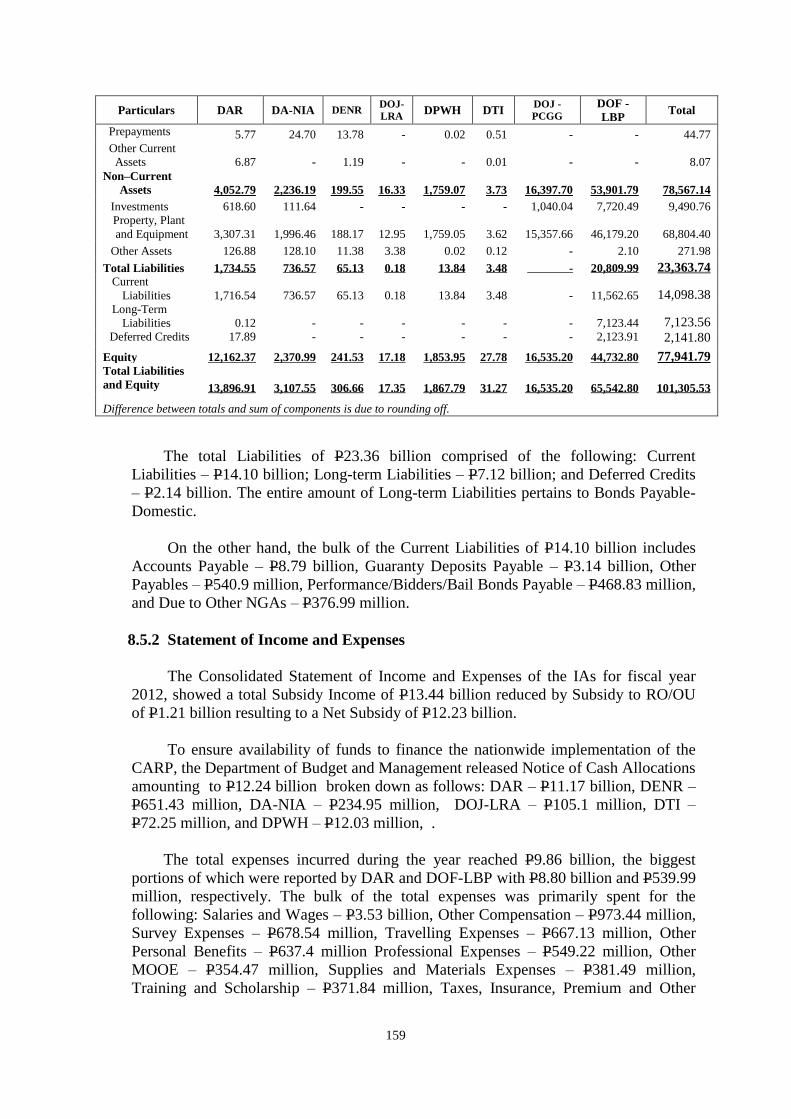

VIII-3 Balance Sheet 158

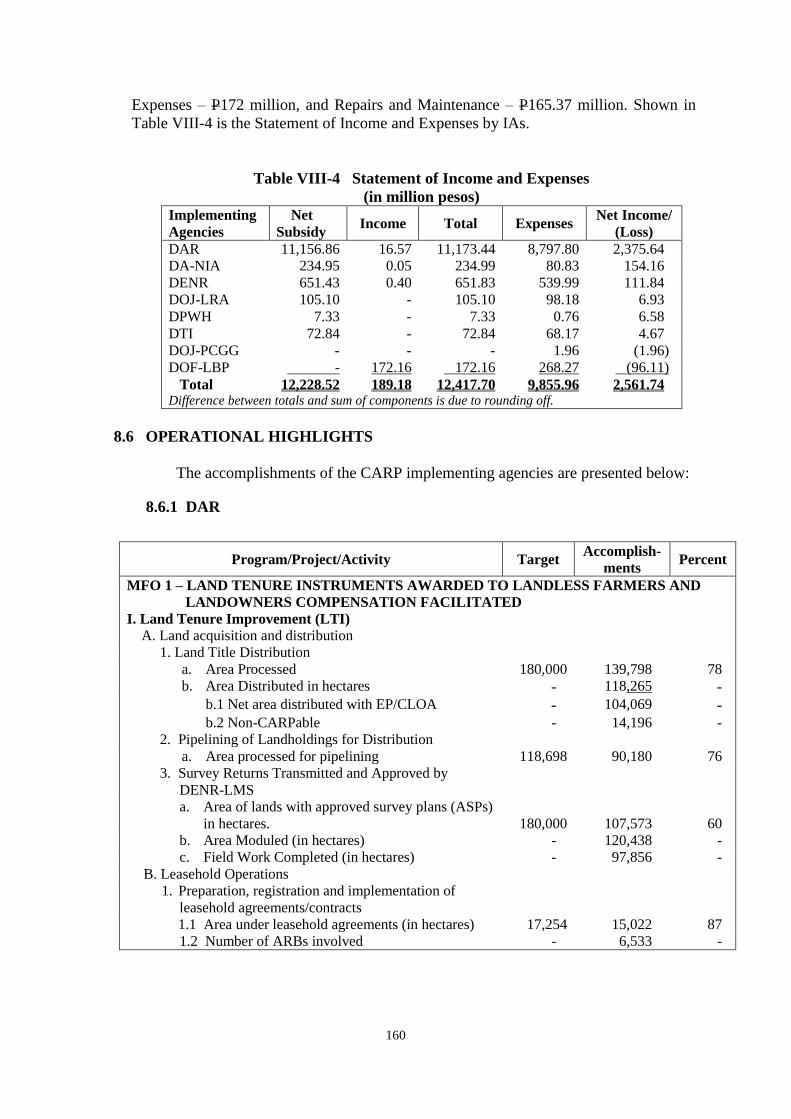

VIII-4 Statement of Income and Expenses 160

v

Chart No. Particulars Page

Report Highlights

II-1 Appropriations, Allotments and Obligations 5

II-2 Allotment by Class 8

II-3 Assets, Liabilities and Equity 12

II-4 Comparative Composition of Assets 12

II-5 Results of Current Operations 14

II-6 Cash Flows, by Activities 16

Appropriations, Allotments, Obligations and Balances

III-1 FY 2012 GAA Regular Appropriations by Sector 18

III-2 FY 2012 NG Budget by Allotment Class 21

III-3 Appropriations per GAA for FYs 2008 to 2012 23

III-4 Sources of Automatic Appropriations 31

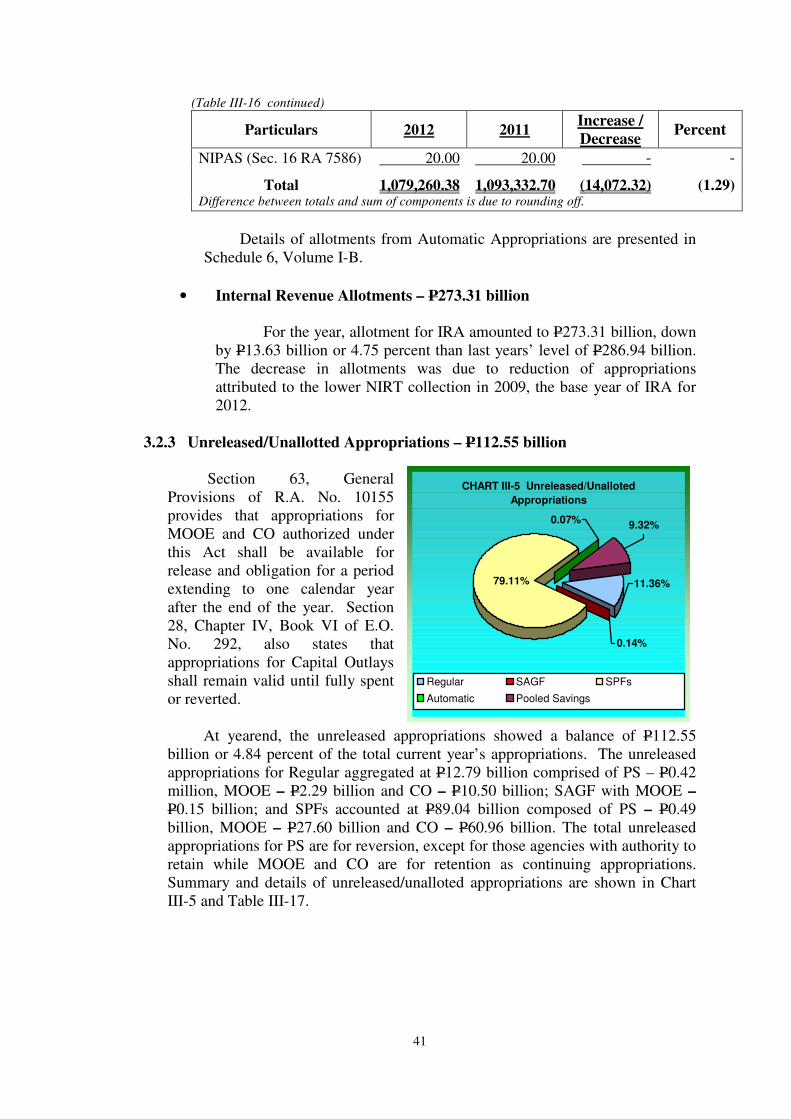

III-5 Unreleased/Unallotted Appropriations 41

Financial Analyses

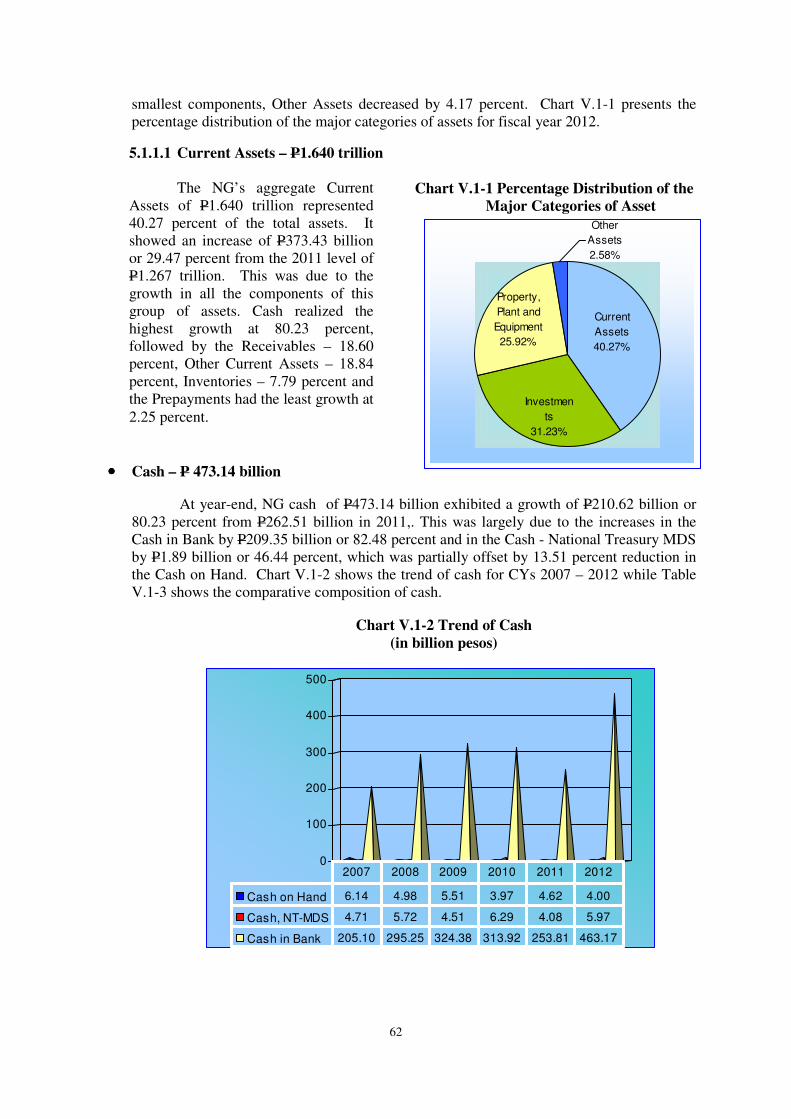

V.1-1 Percentage Distribution of the Major Categories of Assets 62

V.1-2 Trend of Cash 62

V.1-3 Percentage Distribution of Property, Plant and Equipment 79

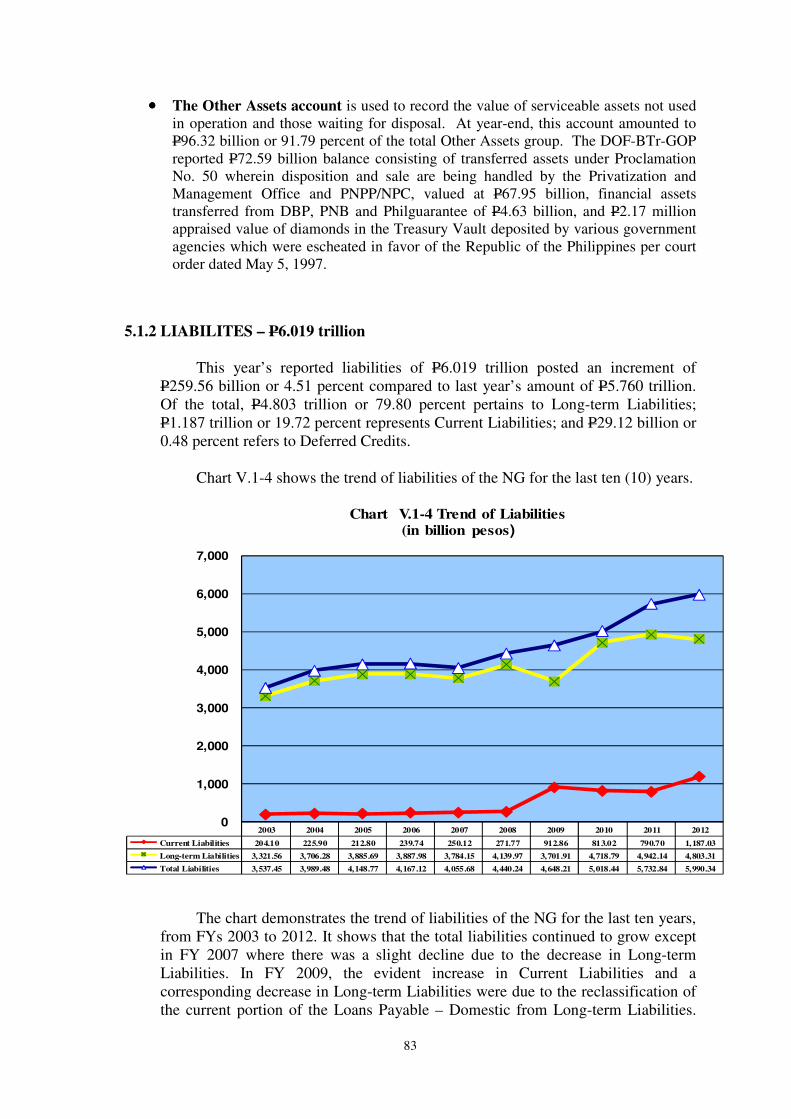

V.1-4 Trend of Liabilities 83

V.2-1 Comparison of Actual and Programmed Revenue 97

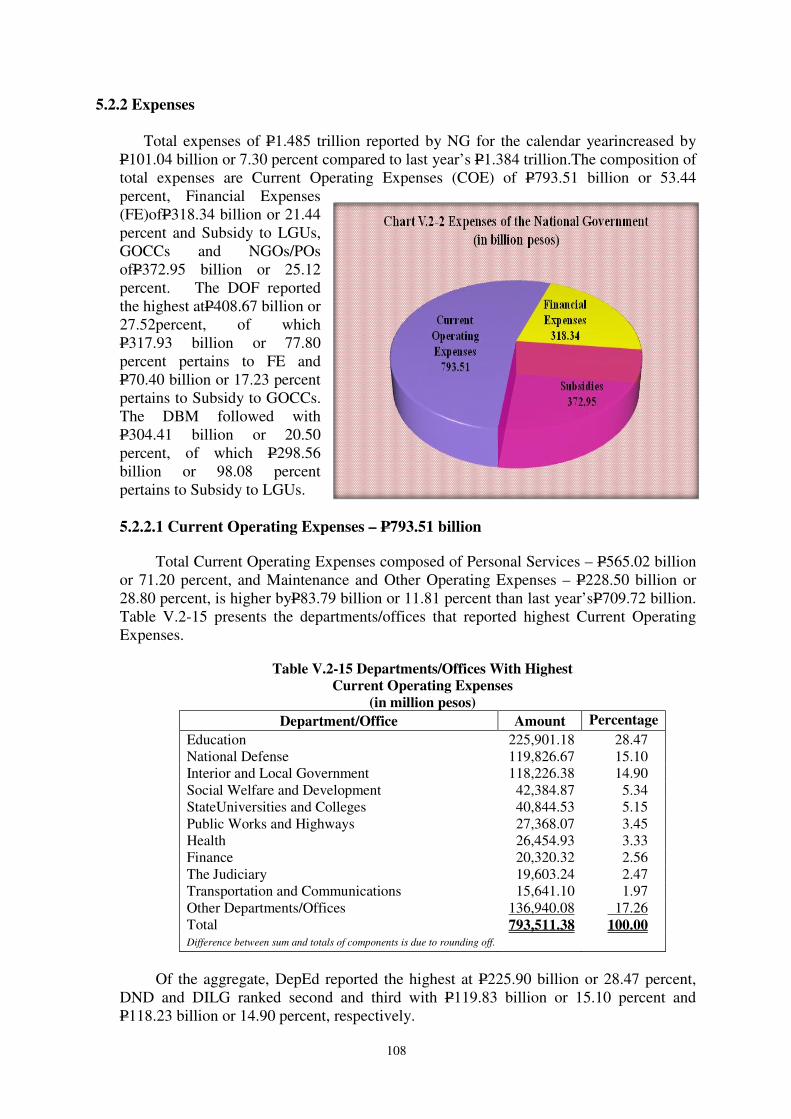

V.2-2 Expenses of the National Government 108

V.3-1 Segment of Cash Flows 122

V.3-2 Trend of Net Cash Provided by (Used in) Operating, Investing and Financing

Activities CY 2003-2012 130

National Government Debt

VI-1 NG Debt By Source for FY 2012 137

VI-2 NG Debt Growth 143

VI-3 Actual Debt Service Expenditure of the NG 144

Special Account in the General Fund

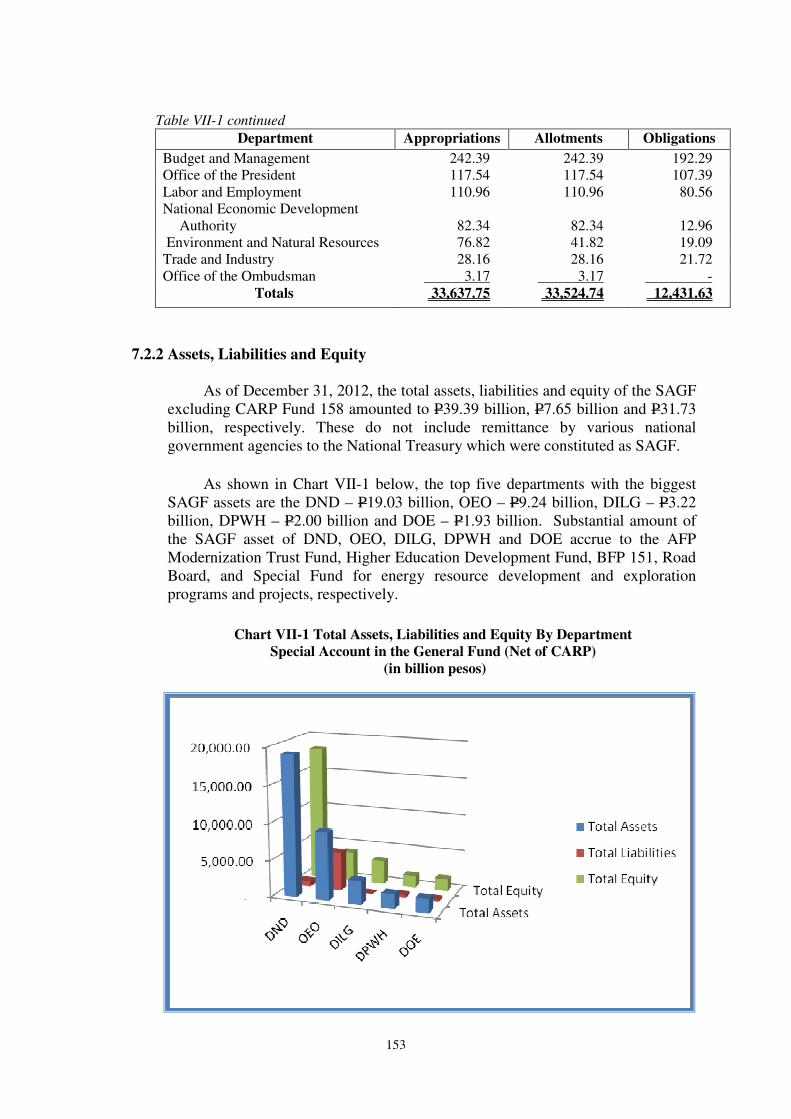

VII-1 Total Assets, Liabilities and Equity, By Department, Special Account

in the General Fund (Net of CARP) 153

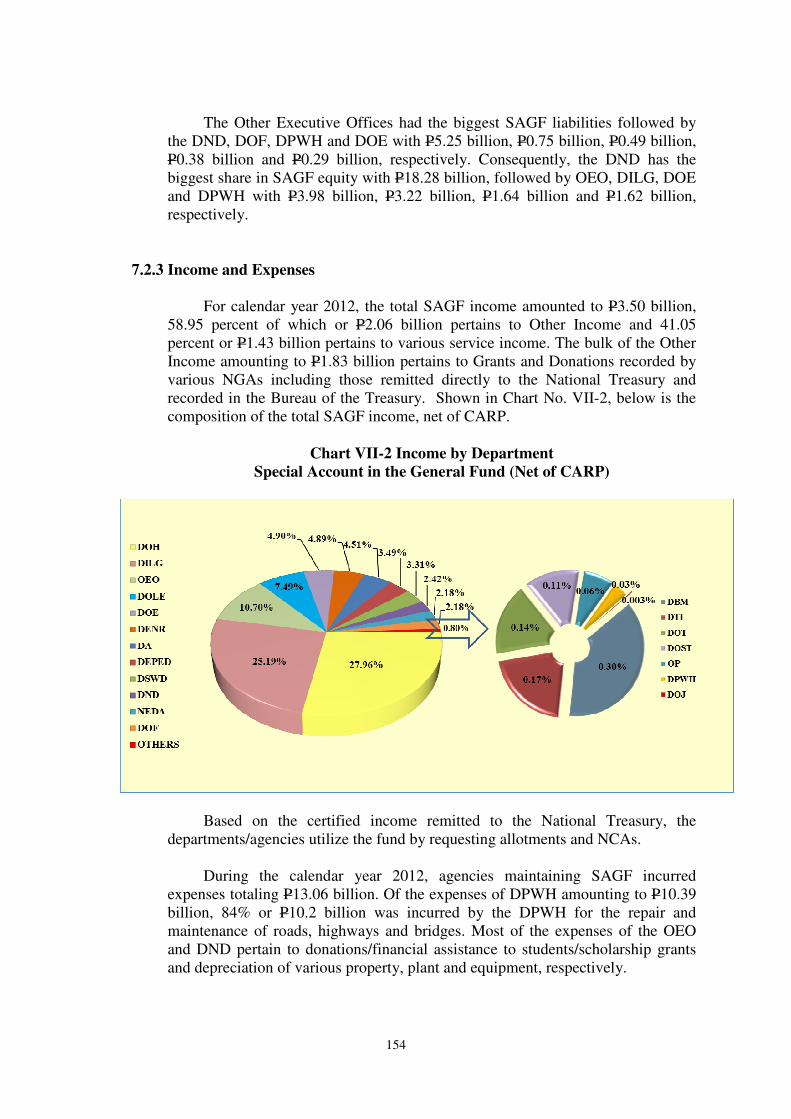

VII-2 Income by Department, Special Account in the General Fund (Net of CARP) 154

Significant and Common Audit Observations and Recommendations

IX-1 Summary of Audit Opinions Calendar Year 2012 171

ACRONYMS

AAB Authorized Agent Bank DPWH Department of Public Works and Highways

ACEF Agricultural Competitiveness Enhancement Fund DSF Debt Service Fund

ADB Asian Development Bank DSWD Department of Social Welfare and Development

AFAE Access Facilitation and Access Enhancement Services DTI Department of Trade and Industry

AFP Armed Forces of the Philippines E.O. Executive Order

AFPMATF AFP Modernization Act Trust Fund ECCDC Early Childhood Care and Development Council

AGDB Authorized Government Depository Bank EP Emancipation Patent

AGPF Agricultural Guarantee Pool Fund FAPs Foreign Assisted Projects

AGSBs Authorize Government Servicing Banks FDCP Film Development Council of the Philippines

AJD Agrarian Justice Delivery FE Financial Expenses

ALDA ARCs Level of Development Assessment FOREX Foreign Exchange

ALGU Allocations to Local Government Units FSP Foreign Service Post

AO Administrative Order FY Fiscal Year

ARBOs Agrarian Reform Beneficiaries Organizations GAA General Appropriations Act

ARBs Agrarian Reform Beneficiaries GE Government Equity

ARCs Agrarian Reform Communities GFIs Government Financial Institutions

ARF Agrarian Reform Fund GOCCs Government-Owned and/or Controlled Corporations

ARISP Agrarian Reform Infrasturture Support Projects GOP Government of the Philippines

ARMM Autonomous Region in Muslim Mindanao GSTLF Gasoline Station Training and Loan Fund

ASPs Approved Survey Plans GTEB Garments and Textile Export Board

BAC Bids and Award Committee HDMF Home Development Mutual Fund

BCDA Bases Conversion and Development Authority HEDF Higher Education Development Fund

BESF Budget of Expenditures and Sources of Financing HGC Home Guaranty Corporation

BFP Bureau of Fire Protection HSRC Human Settlement Regulatory Commission

BI Bureau of Immigration IACAT Inter Agency Council Against Trafficking

BIR Bureau of Internal Revenue IAs Implementing Agencies

BOC Bureau of Customs IBRD International Bank Reconstruction Development

BS Balance Sheet IMF International Monetary Fund

BSF Bond Sinking Fund IRA Internal Revenue Allotment

BSGC Budgetary Support to Government Corporations IT Information Technology

BSP Bangko Sentral ng Pilipinas JJWC Juvenile Justice Welfare Council

BSWM Bureau of Soils and Water Management KALAHI-CIDSS Kapit-Bisig Laban sa Kahirapan-Comprehensive

BTr Bureau of the Treasury and Integrated Delivery of Social Services

BTr-GOP Bureau of the Treasury-Government of the Phils. KKB Kapangyarihan at Kaunlaran sa Barangay

CARP Comprehensive Agrarian Reform Program LBP Land Bank of the Philippines

CB-BOL Central Bank of the Philippines – Board of Liquidators LGUs Local Government Units

CDC Cash Disbursement Ceiling LOI Letter of Instructions

CHED Commission on Higher Education LRA Land Registration Authority

CIDA Canadian International Development Agency LTO Land Transportation Office

CIP Construction in Progress MARINA Maritime Industry Authority

CLOAs Collective Land Owners Awards MDFO Municipal Development Fund Office

CO Capital Outlay MDS Modified Disbursement System

CO Central Office MIGA Multilateral Investment Guaranty Agency

COA Commission on Audit MMDA Metropolitan Manila Development Authority

COE Current Operating Expenses MOOE Maintenance and Other Operating Expenses

COMELEC Commission on Elections MPBF Miscellaneous Personnel Benefits Fund

COP Congress of the Philippines MRDP Mindanao Rural Development Program

CTU Cebu Technological University MRT Metro Rail Transit

CY Calendar Year MRTDC Metro Rail Transit Development Corporation

DA Department of Agriculture MVUC Motor Vehicle Users' Charge

DAP Disbursement Acceleration Program MWSS Metropolitan Waterworks and Sewerage System

DAR Department of Agrarian Reform NABCOR National Agribusiness Corporation

DBM Department of Budget and Management NBC National Budget Circular

DBP Development Bank of the Philippines NCA Notice of Cash Allocation

DDB Dangerous Drugs Board NCAA Non-Cash Availment Authority

DENR Department of Environment and Natural Resources NCCA National Commission for Culture and the Arts

DepEd Department of Education NCR National Capital Region

DFA Department of Foreign Affairs NDC National Development Company

DILG Department of the Interior and Local Government NEDA National Economic and Development Authority

DND Department of National Defense NFA National Food Authority

DOE Department of Energy NG National Government

DOF Department of Finance NGAs National Government Agencies

DOH Department of Health NGAS New Government Accounting System

DOJ Department of Justice NGDAD National Government Debt Accounting Division

DOLE Department of Labor and Employment NGOs Non-Governmental Organizations

DOST Department of Science and Technology NHA National Housing Authority

DOT Department of Tourism NIA National Irrigation Administration

DOTC Department of Transportation and Communications NIPAS National Integrated Protected Areas System

ACRONYMS

vi

NIRT National Internal Revenue Taxes

NORM Naturally Occuring Radio Active Materials

NPC National Power Corporation

NSDF National Sports Development Fund

NSO National Statistics Office

NT National Treasury

NTCA Notice of Transfer of Cash Allocation

OEO Other Executive Offices

OPSF Oil Price Stabilization Fund

OSEC Office of the Secretary

PAGCOR Philippine Amusement and Gaming Corporation

PAG-IBIG Pagtutulungan sa Kinabukasan: Ikaw, Bangko Industriya at Gobyerno

PARC Presidential Agrarian Reform Council

PBD Program Beneficiaries Development

PCAARRD Philippine Council for Agriculture, Aquatic and Natural Resources Research Development

PCGG Presidential Commission on Good Government

PCSO Philippine Charity Sweeptakes Office

PD Presidential Decree

PDAF Priority Development Assistance Fund

PDIC Philippine Deposit Insurance Corporation

PHIC/PHILHEALTH Philippine Health Insurance Corporation

PHILGUARANTEE Philippine Guarantee and Investment Corporation

PI/RP Public Infrastructure/Reforestation Project

PMO Privatization and Management Office

PNB Philippine National Bank

PNP Philippine National Police

PNPP Philippine Nuclear Power Plant

POs Peoples’ Organizations

PPA Philippine Ports Authority

PPE Property, Plant and Equipment

PPPP Pantawid Pamilyang Pilipino Program

PRRC Pasig River Rehabilitation Commission

PS Personal Services

PSC Philippine Sports Commission

PYA Prior Years' Adjustments

R.A. Republic Act

RA Regular Agency

RCO Regional Consular Offices

RFU Regional Field Unit

RLIP Retirement and Life Insurance Premium

ROP Republic of the Philippines

Ros Regional Offices

RPSU Regional Payroll Services Unit

SAAOB Statement of Appropriations, Allotments, Obligations & Balances

SAGF Special Account in the General Fund

SBGFC Small Business Guarantee and Finance Corporation

SCF Statement of Cash Flows

SGF Special Guaranty Fund

SILCAB Social Infrastructure and Local Capability Building

SING Subsidy Income from National Government

SPF Special Purpose Fund

SPTB Special Purpose Treasury Bonds

SRF Special Reserve Fund

SRTC Statistical Research and Training Center

SSF Securities Stabilization Fund

SUCs State Universities and Colleges

TDM Tax Debit Memo

TEF Tax Expenditure Fund

TOP Treasurer of the Philippines

TRAs Tax Remittance Advices

UF Unprogrammed Fund

UNDP United Nations Development Programme

UNFPA United Nations Population Fund

UP University of the Philippines

VAT Value Added Tax

WB World Bank

ACRONYMS

vii

I. INTRODUCTION

1

INTRODUCTION

1.1 Legal Bases

Section 4, Article IX-D of the Philippine Constitution directs the Commission on

Audit (COA) to submit to the President and Congress the Annual Financial Report

(AFR) of the National Government. Furthermore, Section 41 of Presidential Decree No.

1445, the Auditing Code of the Philippines, requires that annual report on the financial

condition and results of operations of all agencies of the government which shall

include recommendations of measures necessary to improve their effectiveness and

efficiency shall be submitted not later than September 30 of each year.

In compliance with this mandated function, the COA, through the Government

Accountancy Sector (GAS) submits to the President and Congress the Annual Financial

Report (AFR) of the National Government (NG) for calendar year (CY) 2012.

1.2 Objectives

The AFR provides information on the total approved budget, releases of

allotments, obligations incurred and Notice of Cash Allocations (NCA) and other

disbursement authorities received by national government agencies (NGAs), cash

inflows and outflows and the financial condition and results of operations as presented

in the consolidated financial statements of the NGAs. The budget informations serve as

useful tools for the Congress in the ratification of appropriations and other laws, while

the other financial data used guide the President, legislators, economic planners and

other government officials in the formulation of economic policies, in the development

of budget plans, and other deliberations in aid of legislation.

1.3 Contents/Features

The financial statements featured in the AFR are as follows: Balance Sheet (BS),

Statement of Income and Expenses (SIE), Statement of Government Equity (SGE) and

Statement of Cash Flows (SCF), in condensed and detailed form with comparative

figures for CYs 2011 and 2012.

It also shows the appropriations, allotments, obligations and balances by

department/agency and by source, and the common and significant audit observations

and recommendations.

The report comprises of the following:

Volume I-A – Contains the Report Highlights, Condensed Financial

Statements, and Financial Analyses, and write-ups on the

Appropriations, Allotments, Obligations and Balances, NG

Debt, Special Accounts in the General Fund, and

Comprehensive Agrarian Reform Program

2

Volume I- B – Includes the Detailed Financial Statements by Department/

Office, Schedules and Annexes

1.4 Methodologies

1.4.1 Appropriations, Allotments, Obligations and Balances

The budget data presented in this report comprise the total current year’s

appropriations, prior year’s continuing appropriations set by law to be available

until the end of the year and automatic appropriations which do not require

periodic action by Congress. The total allotments released by the Department of

Budget and Management (DBM) during the year are monitored and recorded in

the Registry of Appropriations and Allotments (RAPAL) maintained by COA-

GAS. These informations are consolidated together with the obligations incurred

sourced from the Statement of Allotments, Obligations and Balances submitted

by NGAs.

The appropriations and allotments were reconciled with the records of the

DBM and the NGAs and necessary corrections and adjustments were

communicated and effected accordingly. Similarly, obligations incurred by

agencies were confirmed to ascertain that such commitments were duly covered

by allotments and overdraft in allotments, if any, was properly coordinated with

the concerned agency.

1.4.2 Financial Statements

The overall consolidated financial data presented in the AFR were culled

from the 2012 financial reports of the NG which were prepared by agency

accountants in accordance with the rules and regulations under the New

Government Accounting System (NGAS). The accounts in the advance copies

of trial balances submitted by NGAs were uploaded into the AFR System from

which the individual agency BS, SIE as well as the SGE were generated and

compared with the audited FS submitted by the COA audit sector. The system

also generated the overall consolidated FS by department/office.

The elimination of inter-agency and intra-agency accounts was based on the

overall BS. The inter-agency receivables were eliminated with the inter-agency

payables to show the amount of cash expected to be realized from the

receivables and the actual payables subsisting between NGAs, LGUs and

GOCCs. On the other hand, the intra-agency receivables were also eliminated

with intra-agency payables to show the balances of reciprocal accounts

subsisting between the Central Offices (COs), the Regional Offices (ROs)/Staff

Bureaus, and the Operating Units (OUs). Inasmuch as the inter-agency and

intra-agency accounts are not reconciled at the agency level, these accounts still

reflect balances even after the elimination was done.

3

The aggregate income of the NG was based on the consolidated SIE

generated from the system presented by Regular Agency (RA) Book and

National Government (NG) Book. The details of the total income presented in

this report was based on the consolidated Report of Income (ROI) submitted by

the NGAs, since under the NG Book maintained by the Bureau of the Treasury

(BTr.), the various tax revenue accounts are categorized as Other National Taxes

while majority of non-tax revenue accounts are classified as Other Service

Income.

The SCF submitted by NGAs were analyzed and converted into the

prescribed format to expedite inputting and processing of data into the AFR

system. Due to the absence of a module to offset collections of income/revenue

against remittances to the National Treasury, manual computation was done.

The offsetting, however, was made on the overall SCF due to lack of

information as to the nature of remittances made. The intra-agency and inter-

agency transfers were likewise not eliminated in the absence of data as to the

transferor/donor and transferee/recipient. The system generated the overall

consolidated SCF by book, by department/office and by agency.

1.4.3 National Government Debt

The data on NG debt were based on the 2012 advance copy of the FS,

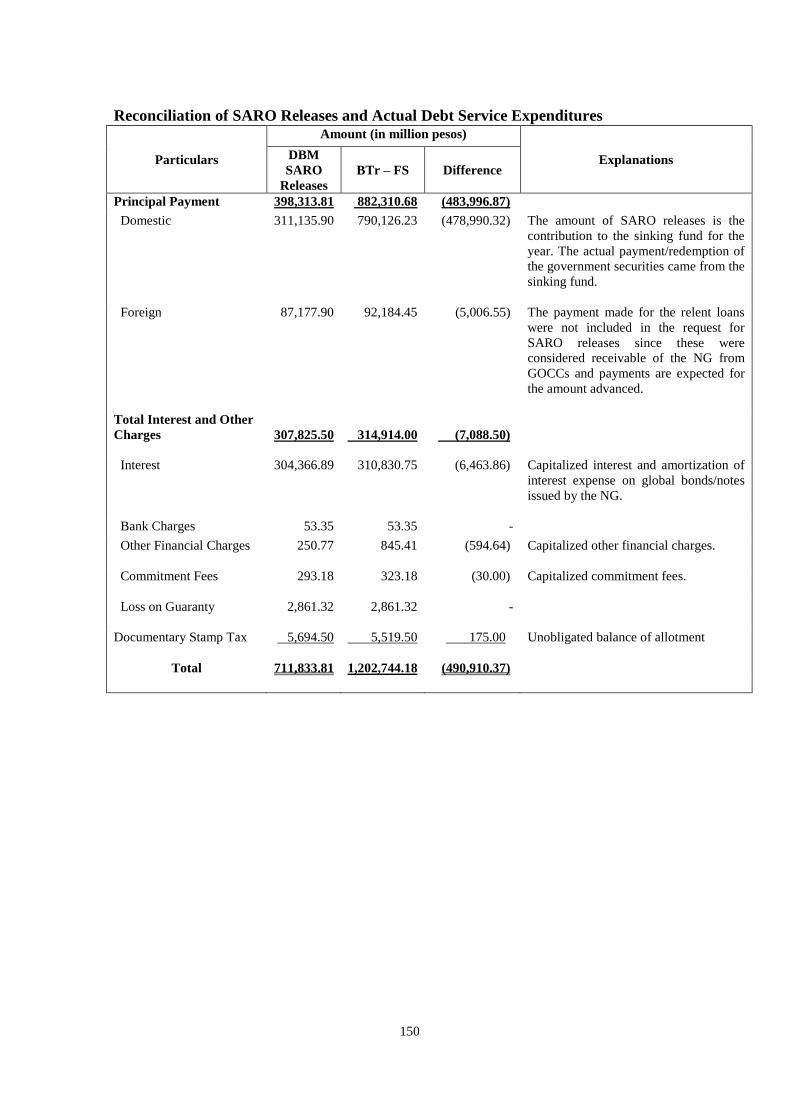

Actual Debt Service Expenditures provided by the BTr, Department of Finance.

Budget information were sourced from the 2013 Budget of Expenditures and

Sources of Financing (BESF) and the 2012 General Appropriations Act (GAA),

R.A. No. 10155, furnished by the Department of Budget and Management

(DBM). The National Government Debt Accounting Division (NGDAD), BTr

submits to COA-GAS the analyses of loans and bonds payable, both foreign and

domestic. Based on the analyses, the data on beginning balances of outstanding

NG debt are reconciled with the ending balances reflected in the 2011 report. The

availments and repayments during the year were also based on the NGDAD

analyses. The ending balance of NG debt is reconciled with the Loans and Bonds

Payable, foreign and domestic, appearing in the BS of the BTr - NG Book.

Appropriations for foreign assisted projects by department/agency were taken

from the 2012 GAA, while releases of allotments were based on the Agency

Budget Matrices (ABMs) and individual Special Allotment Release Orders

(SAROs) of the particular agencies. Comparative data between programmed and

actual budget for NG debt were based on the BESF and the COR.

1.4.4 Special Account in the General Fund (SAGF)

The financial information for SAGF as of December 31, 2012 were obtained

after the consolidation of the trial balances submitted by national government

agencies except the CARP (Fund 158) which is presented in Part VIII of this

report. Not included herein are the transactions pertaining to SAGF, which were

integrated in the General Fund 101 of the departments/agencies since no separate

books were maintained. However, the income collected by various NGAs and

remitted to the National Treasury was included based on the actual income

4

recorded in the books of the BTr either as Grants and Donations or Other Service

Income. The utilization of the amount is subject to the approval of special budget

released through SAROs and issuance of NCAs.

1.4.5 Comprehensive Agrarian Reform Fund (CARP)

The data on budget/appropriations, allotments and obligations exhibited in

this portion were gathered from the financial reports of implementing agencies

which received fund releases during the year to implement CARP projects,

materials submitted by the Presidential Agrarian Reform Council (PARC) and

reports from the DAR auditing unit in-charge of the consolidation of the CARP.

For Fiscal Year 2012, the entire budget data of DAR for all funds were

consolidated into the CARP inasmuch as it is its mandate. Besides it is difficult

to determine how much from Funds 101 and 102 are not CARP related.

Furthermore, two implementing agencies were no longer components of the data

on appropriations, allotments and obligations for this year since no releases of

allotments were made to the DPWH while the appropriation intended for DOF-

LBP was withdrawn by the DBM and transferred to the pooled savings.

However, there was transfer of funds to DOF-Municipal Development Fund

Office (MDFO) for CARP implementation.

This year’s consolidated data on assets, liabilities, equity, income and

expenses were based on the Balance Sheet and Statement of Income and

Expenses of all CARP implementing agencies including DOF-LBP and DOF-

MDFO.

1.5 Coverage

The financial information presented in this AFR were gathered from the audited

and advance copies of financial statements (FS)/reports of 323 national government

agencies (NGAs). There were 505 Preliminary Trial Balances (PTB)/FS of the cited

number of NGAs which were uploaded into the AFR System in order to generate the

Over-all Consolidated Financial Statements of the National Government. It is worth

mentioning that for Fiscal Year 2012, there was 100 percent submission of advanced

copies of FS by the NGAs’ accounting units compared to last year of 98.48 percent.

On the other hand, of the total 323 agencies, only 264 or 81.73 percent audited

financial reports were submitted by the auditors and downloaded from the COA Web.

Compared to last year audited FS of 224, there was an increment of 40 or 17.86

percent. This year’s unsubmitted audited FS of the 59 agencies/offices were received by

GAS after the cut-off date.

II. REPORT HIGHLIGHTS

5

REPORT HIGHLIGHTS

2.1 Budget Information

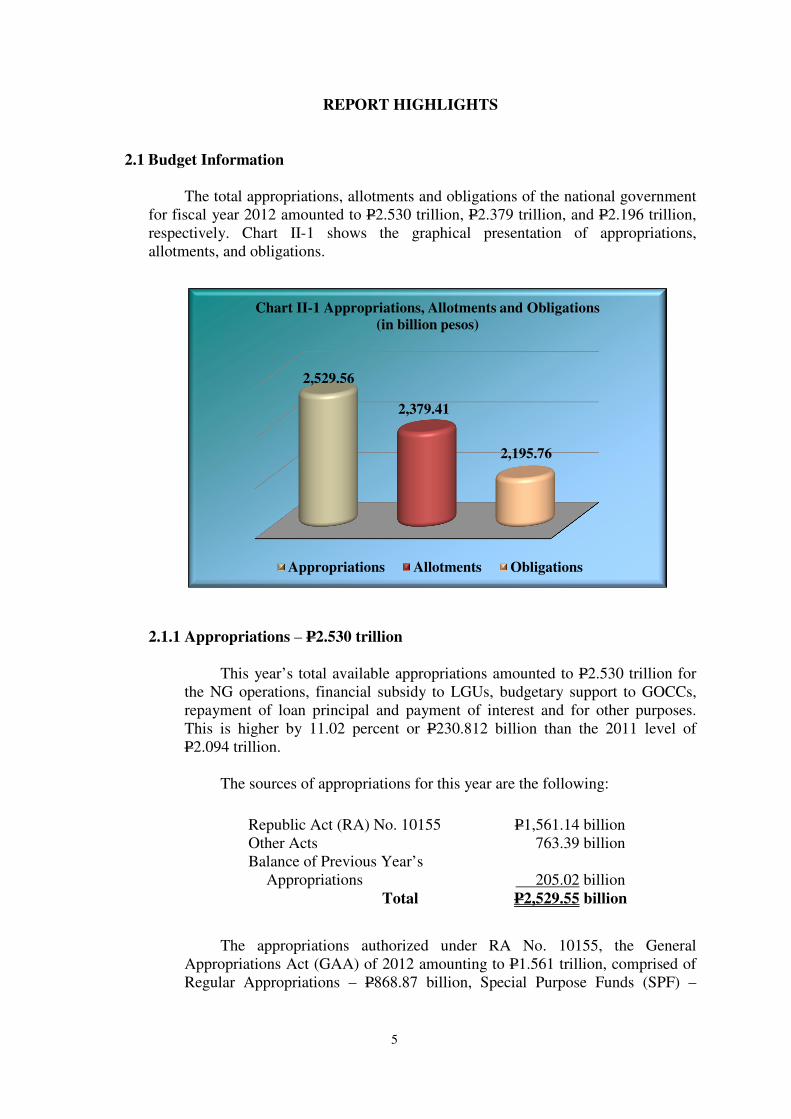

The total appropriations, allotments and obligations of the national government

for fiscal year 2012 amounted to P2.530 trillion, P2.379 trillion, and P2.196 trillion,

respectively. Chart II-1 shows the graphical presentation of appropriations,

allotments, and obligations.

2.1.1 Appropriations – P2.530 trillion

This year’s total available appropriations amounted to P2.530 trillion for

the NG operations, financial subsidy to LGUs, budgetary support to GOCCs,

repayment of loan principal and payment of interest and for other purposes.

This is higher by 11.02 percent or P230.812 billion than the 2011 level of

P2.094 trillion.

The sources of appropriations for this year are the following:

The appropriations authorized under RA No. 10155, the General

Appropriations Act (GAA) of 2012 amounting to P1.561 trillion, comprised of

Regular Appropriations – P868.87 billion, Special Purpose Funds (SPF) –

Republic Act (RA) No. 10155 P1,561.14 billion

Other Acts 763.39 billion

Balance of Previous Year’s

Appropriations

205.02 billion

Total P2,529.55 billion

2,529.56

2,379.41

2,195.76

Chart II-1 Appropriations, Allotments and Obligations

(in billion pesos)

Appropriations Allotments Obligations

6

P367.54 billion, Automatic Appropriations – P315.95 billion and Special

Account in the General Fund – P8.78 billion.

The details of appropriations authorized under Other Acts or laws for the

year totaling P763.39 billion are as follows:

Amount

(in million pesos)

1. Debt Service Fund (DSF) 706,139.31

Principal Repayment 398,313.81

Interest Payment 307,825.50

2. Special Account in the General Fund (SAGF) 29,637.87

3. Retirement and Life Insurance Premium 27,612.53

Total 763,389.70

Note: Difference between totals and sum of components is due to rounding off.

The unobligated/unreleased balance of the preceding year’s

appropriations authorized to be used in the current year under RA No. 10147,

the 2011 GAA, and other laws amounting to P205.02 billion consisted of the

following:

Amount

(in million pesos)

1. Unobligated Allotments

140,318.35

RA No. 10147 114,256.35

Regular Appropriations 96,627.92

Special Purpose Fund 14,050.12

Automatic Appropriations 1,951.92

Special Account in the General Fund 1,626.39

Other Acts 26,062.00

Regular Appropriations 5,224.14

Automatic Appropriations 20,837.85

2. Unreleased Appropriations 64,704.62

RA No. 10147 64,704.62

Regular Appropriations 12,537.32

Special Purpose Fund 51,167.29

Special Account in the General Fund 1,000.00

Total 205,022.97 Note: Difference between totals and sum of components is due to rounding off.

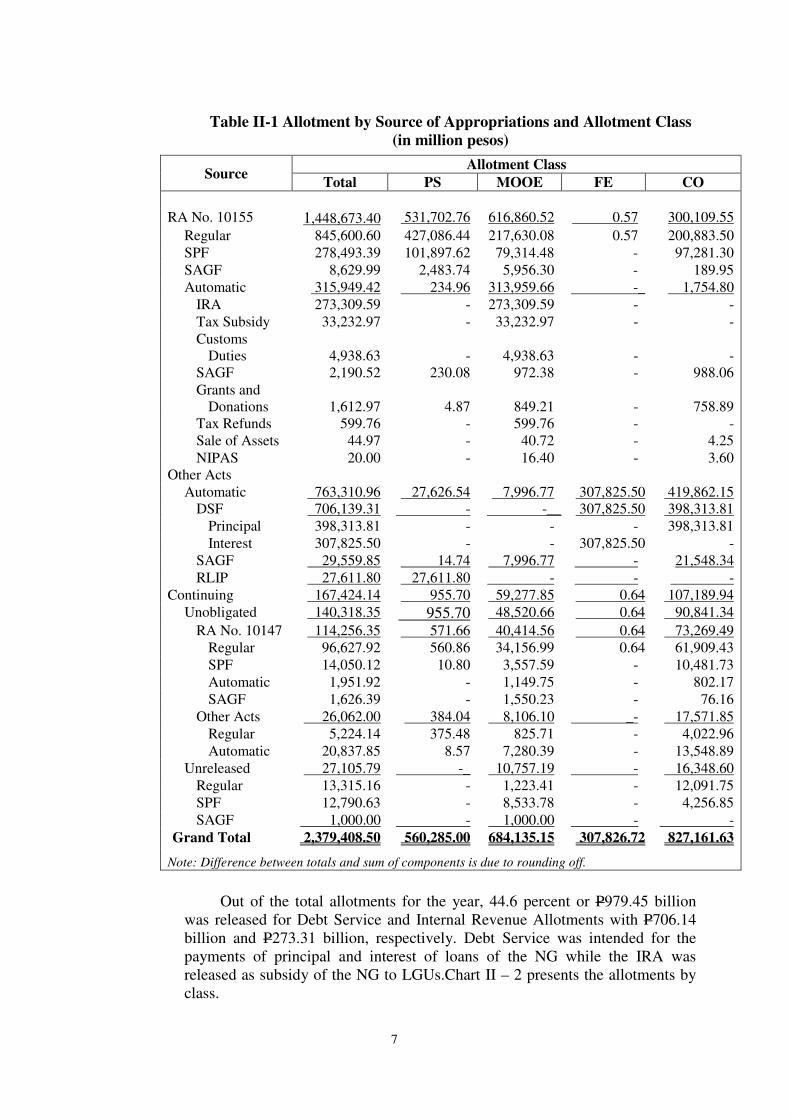

2.1.2 Allotments – P2.379 trillion

Of the total available appropriations, P2.379 trillion or 94.06 percent was

released/allotted to fund the programs and projects of various NGAs, including

repayment of loan principal, and payment of interest, commitments fees and

other charges. These were sourced from the following: RA No. 10155 – P1.449

trillion, Other Acts – P763.31 billion and forwarding balances of continuing

appropriations – P167.42 billion. Table II-1 presents the details of allotments

by source and allotment class.

7

Table II-1 Allotment by Source of Appropriations and Allotment Class

(in million pesos)

Source Allotment Class

Total PS MOOE FE CO

RA No. 10155 1,448,673.40 531,702.76 616,860.52 0.57 300,109.55

Regular 845,600.60 427,086.44 217,630.08 0.57 200,883.50

SPF 278,493.39 101,897.62 79,314.48 - 97,281.30

SAGF 8,629.99 2,483.74 5,956.30 - 189.95

Automatic 315,949.42 234.96 313,959.66 -_ 1,754.80

IRA 273,309.59 - 273,309.59 - -

Tax Subsidy 33,232.97 - 33,232.97 - -

Customs

Duties

4,938.63

-

4,938.63

-

-

SAGF 2,190.52 230.08 972.38 - 988.06

Grants and

Donations

1,612.97

4.87

849.21

-

758.89

Tax Refunds 599.76 - 599.76 - -

Sale of Assets 44.97 - 40.72 - 4.25

NIPAS 20.00 - 16.40 - 3.60

Other Acts

Automatic 763,310.96 27,626.54 7,996.77 307,825.50 419,862.15

DSF 706,139.31 - -__ 307,825.50 398,313.81

Principal 398,313.81 - - - 398,313.81

Interest 307,825.50 - - 307,825.50 -

SAGF 29,559.85 14.74 7,996.77 - 21,548.34

RLIP 27,611.80 27,611.80 - - -

Continuing 167,424.14 955.70 59,277.85 0.64 107,189.94

Unobligated 140,318.35 955.70 48,520.66 0.64 90,841.34

RA No. 10147 114,256.35 571.66 40,414.56 0.64 73,269.49

Regular 96,627.92 560.86 34,156.99 0.64 61,909.43

SPF 14,050.12 10.80 3,557.59 - 10,481.73

Automatic 1,951.92 - 1,149.75 - 802.17

SAGF 1,626.39 - 1,550.23 - 76.16

Other Acts 26,062.00 384.04 8,106.10 _- 17,571.85

Regular 5,224.14 375.48 825.71 - 4,022.96

Automatic 20,837.85 8.57 7,280.39 - 13,548.89

Unreleased 27,105.79 -_ 10,757.19 - 16,348.60

Regular 13,315.16 - 1,223.41 - 12,091.75

SPF 12,790.63 - 8,533.78 - 4,256.85

SAGF 1,000.00 - 1,000.00 - -

Grand Total 2,379,408.50 560,285.00 684,135.15 307,826.72 827,161.63

Note: Difference between totals and sum of components is due to rounding off.

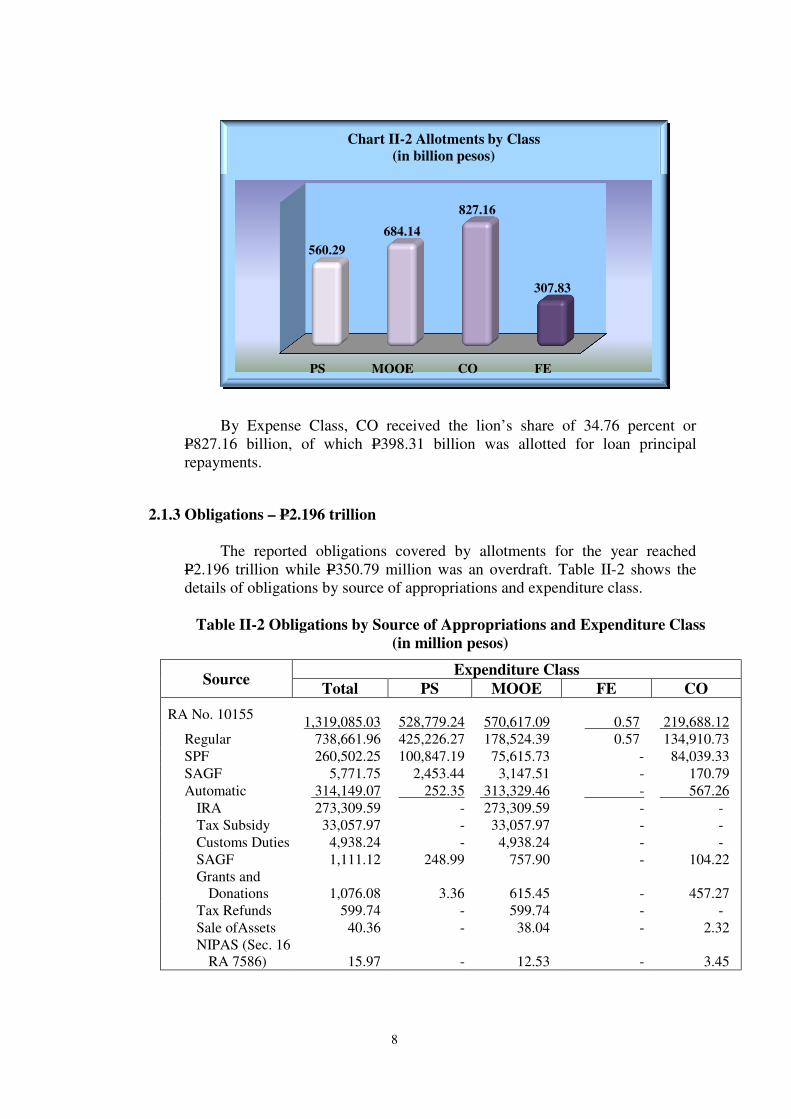

Out of the total allotments for the year, 44.6 percent or P979.45 billion

was released for Debt Service and Internal Revenue Allotments with P706.14

billion and P273.31 billion, respectively. Debt Service was intended for the

payments of principal and interest of loans of the NG while the IRA was

released as subsidy of the NG to LGUs.Chart II – 2 presents the allotments by

class.

8

By Expense Class, CO received the lion’s share of 34.76 percent or

P827.16 billion, of which P398.31 billion was allotted for loan principal

repayments.

2.1.3 Obligations – P2.196 trillion

The reported obligations covered by allotments for the year reached

P2.196 trillion while P350.79 million was an overdraft. Table II-2 shows the

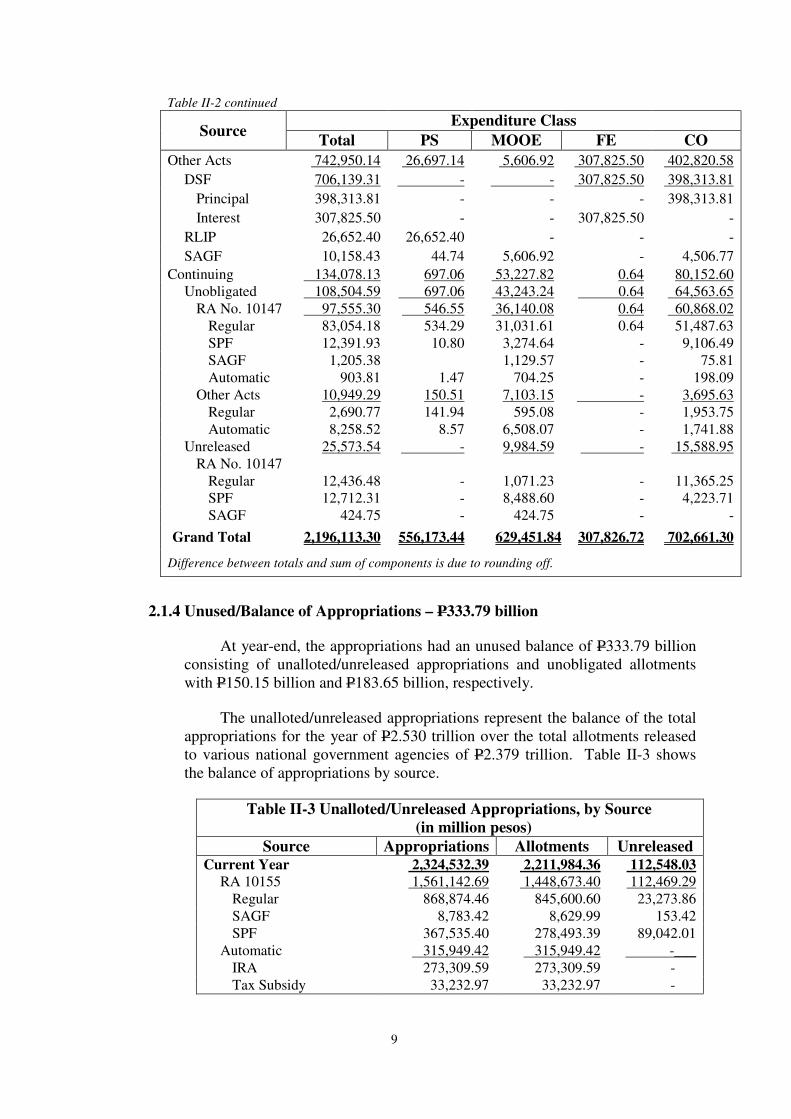

details of obligations by source of appropriations and expenditure class.

Table II-2 Obligations by Source of Appropriations and Expenditure Class

(in million pesos)

Source Expenditure Class

Total PS MOOE FE CO

RA No. 10155

1,319,085.03

528,779.24

570,617.09

0.57

219,688.12

Regular 738,661.96 425,226.27 178,524.39 0.57 134,910.73

SPF 260,502.25 100,847.19 75,615.73 - 84,039.33

SAGF 5,771.75 2,453.44 3,147.51 - 170.79

Automatic 314,149.07 252.35 313,329.46 - 567.26

IRA 273,309.59 - 273,309.59 - -

Tax Subsidy 33,057.97 - 33,057.97 - -

Customs Duties 4,938.24 - 4,938.24 - -

SAGF 1,111.12 248.99 757.90 - 104.22

Grants and

Donations

1,076.08

3.36

615.45

-

457.27

Tax Refunds 599.74 - 599.74 - -

Sale ofAssets 40.36 - 38.04 - 2.32

NIPAS (Sec. 16

RA 7586)

15.97

-

12.53

-

3.45

PS MOOE CO FE

560.29

684.14

827.16

307.83

Chart II-2 Allotments by Class

(in billion pesos)

9

Table II-2 continued

Source Expenditure Class

Total PS MOOE FE CO

Other Acts 742,950.14 26,697.14 5,606.92 307,825.50 402,820.58

DSF 706,139.31 - - 307,825.50 398,313.81

Principal 398,313.81 - - - 398,313.81

Interest 307,825.50 - - 307,825.50 -

RLIP 26,652.40 26,652.40 - - -

SAGF 10,158.43 44.74 5,606.92 - 4,506.77

Continuing 134,078.13 697.06 53,227.82 0.64 80,152.60

Unobligated 108,504.59 697.06 43,243.24 0.64 64,563.65

RA No. 10147 97,555.30 546.55 36,140.08 0.64 60,868.02

Regular 83,054.18 534.29 31,031.61 0.64 51,487.63

SPF 12,391.93 10.80 3,274.64 - 9,106.49

SAGF 1,205.38 1,129.57 - 75.81

Automatic 903.81 1.47 704.25 - 198.09

Other Acts 10,949.29 150.51 7,103.15 - 3,695.63

Regular 2,690.77 141.94 595.08 - 1,953.75

Automatic 8,258.52 8.57 6,508.07 - 1,741.88

Unreleased 25,573.54 - 9,984.59 - 15,588.95

RA No. 10147

Regular 12,436.48 - 1,071.23 - 11,365.25

SPF 12,712.31 - 8,488.60 - 4,223.71

SAGF 424.75 - 424.75 - -

Grand Total 2,196,113.30 556,173.44 629,451.84 307,826.72 702,661.30

Difference between totals and sum of components is due to rounding off.

2.1.4 Unused/Balance of Appropriations – P333.79 billion

At year-end, the appropriations had an unused balance of P333.79 billion

consisting of unalloted/unreleased appropriations and unobligated allotments

with P150.15 billion and P183.65 billion, respectively.

The unalloted/unreleased appropriations represent the balance of the total

appropriations for the year of P2.530 trillion over the total allotments released

to various national government agencies of P2.379 trillion. Table II-3 shows

the balance of appropriations by source.

Table II-3 Unalloted/Unreleased Appropriations, by Source

(in million pesos)

Source Appropriations Allotments Unreleased Current Year 2,324,532.39 2,211,984.36 112,548.03

RA 10155 1,561,142.69 1,448,673.40 112,469.29

Regular 868,874.46 845,600.60 23,273.86

SAGF 8,783.42 8,629.99 153.42

SPF 367,535.40 278,493.39 89,042.01

Automatic 315,949.42 315,949.42 -___

IRA 273,309.59 273,309.59 -

Tax Subsidy 33,232.97 33,232.97 -

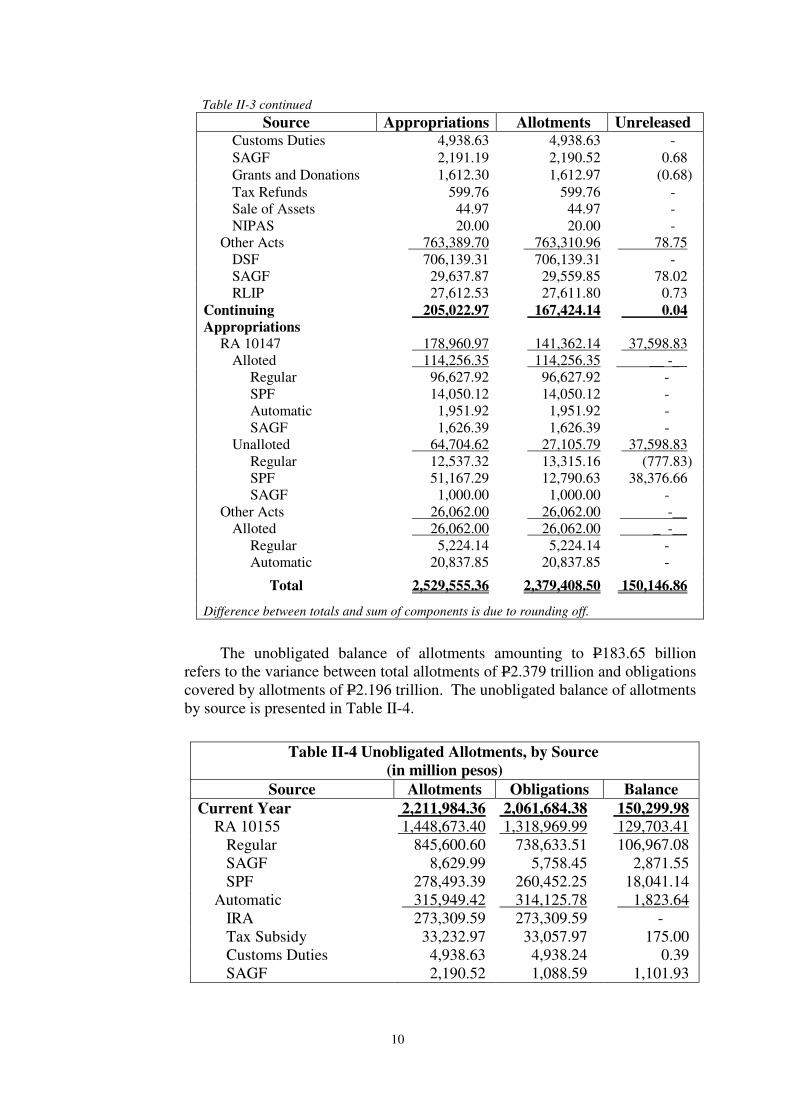

10

Table II-3 continued

Source Appropriations Allotments Unreleased

Customs Duties 4,938.63 4,938.63 -

SAGF 2,191.19 2,190.52 0.68

Grants and Donations 1,612.30 1,612.97 (0.68)

Tax Refunds 599.76 599.76 -

Sale of Assets 44.97 44.97 -

NIPAS 20.00 20.00 -

Other Acts 763,389.70 763,310.96 78.75

DSF 706,139.31 706,139.31 -

SAGF 29,637.87 29,559.85 78.02

RLIP 27,612.53 27,611.80 0.73

Continuing

Appropriations

205,022.97 167,424.14 0.04

RA 10147 178,960.97 141,362.14 37,598.83

Alloted 114,256.35 114,256.35 __ -__

Regular 96,627.92 96,627.92 -

SPF 14,050.12 14,050.12 -

Automatic 1,951.92 1,951.92 -

SAGF 1,626.39 1,626.39 -

Unalloted 64,704.62 27,105.79 37,598.83

Regular 12,537.32 13,315.16 (777.83)

SPF 51,167.29 12,790.63 38,376.66

SAGF 1,000.00 1,000.00 -

Other Acts 26,062.00 26,062.00 -__

Alloted 26,062.00 26,062.00 _ -__

Regular 5,224.14 5,224.14 -

Automatic 20,837.85 20,837.85 -

Total 2,529,555.36 2,379,408.50 150,146.86

Difference between totals and sum of components is due to rounding off.

The unobligated balance of allotments amounting to P183.65 billion

refers to the variance between total allotments of P2.379 trillion and obligations

covered by allotments of P2.196 trillion. The unobligated balance of allotments

by source is presented in Table II-4.

Table II-4 Unobligated Allotments, by Source

(in million pesos)

Source Allotments Obligations Balance

Current Year 2,211,984.36 2,061,684.38 150,299.98

RA 10155 1,448,673.40 1,318,969.99 129,703.41

Regular 845,600.60 738,633.51 106,967.08

SAGF 8,629.99 5,758.45 2,871.55

SPF 278,493.39 260,452.25 18,041.14

Automatic 315,949.42 314,125.78 1,823.64

IRA 273,309.59 273,309.59 -

Tax Subsidy 33,232.97 33,057.97 175.00

Customs Duties 4,938.63 4,938.24 0.39

SAGF 2,190.52 1,088.59 1,101.93

11

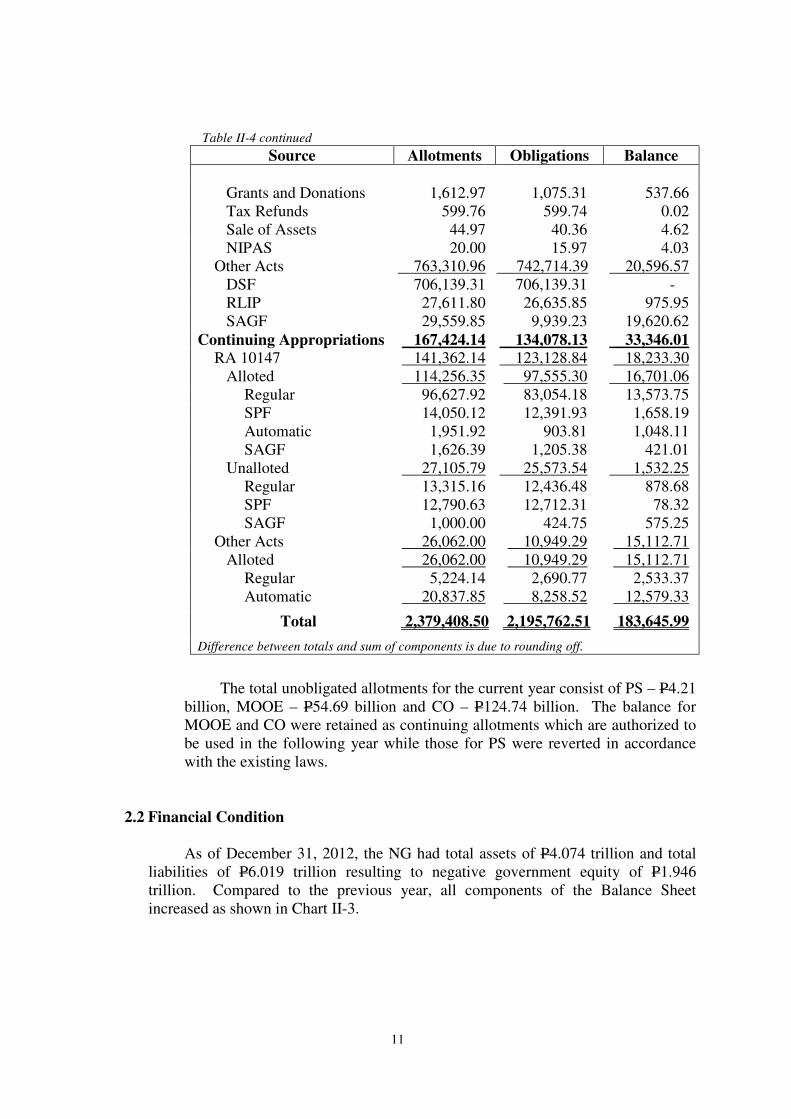

Table II-4 continued

Source Allotments Obligations Balance

Grants and Donations 1,612.97 1,075.31 537.66

Tax Refunds 599.76 599.74 0.02

Sale of Assets 44.97 40.36 4.62

NIPAS 20.00 15.97 4.03

Other Acts 763,310.96 742,714.39 20,596.57

DSF 706,139.31 706,139.31 -

RLIP 27,611.80 26,635.85 975.95

SAGF 29,559.85 9,939.23 19,620.62

Continuing Appropriations 167,424.14 134,078.13 33,346.01

RA 10147 141,362.14 123,128.84 18,233.30

Alloted 114,256.35 97,555.30 16,701.06

Regular 96,627.92 83,054.18 13,573.75

SPF 14,050.12 12,391.93 1,658.19

Automatic 1,951.92 903.81 1,048.11

SAGF 1,626.39 1,205.38 421.01

Unalloted 27,105.79 25,573.54 1,532.25

Regular 13,315.16 12,436.48 878.68

SPF 12,790.63 12,712.31 78.32

SAGF 1,000.00 424.75 575.25

Other Acts 26,062.00 10,949.29 15,112.71

Alloted 26,062.00 10,949.29 15,112.71

Regular 5,224.14 2,690.77 2,533.37

Automatic 20,837.85 8,258.52 12,579.33

Total 2,379,408.50 2,195,762.51 183,645.99

Difference between totals and sum of components is due to rounding off.

The total unobligated allotments for the current year consist of PS – P4.21

billion, MOOE – P54.69 billion and CO – P124.74 billion. The balance for

MOOE and CO were retained as continuing allotments which are authorized to

be used in the following year while those for PS were reverted in accordance

with the existing laws.

2.2 Financial Condition

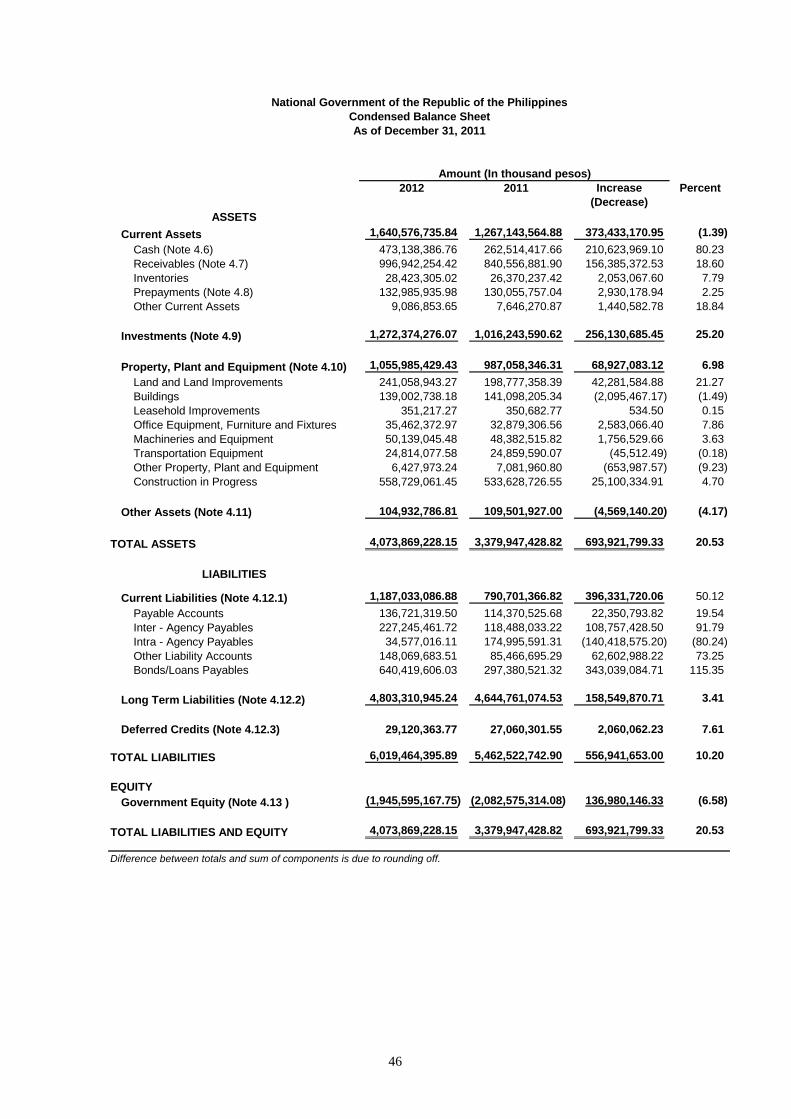

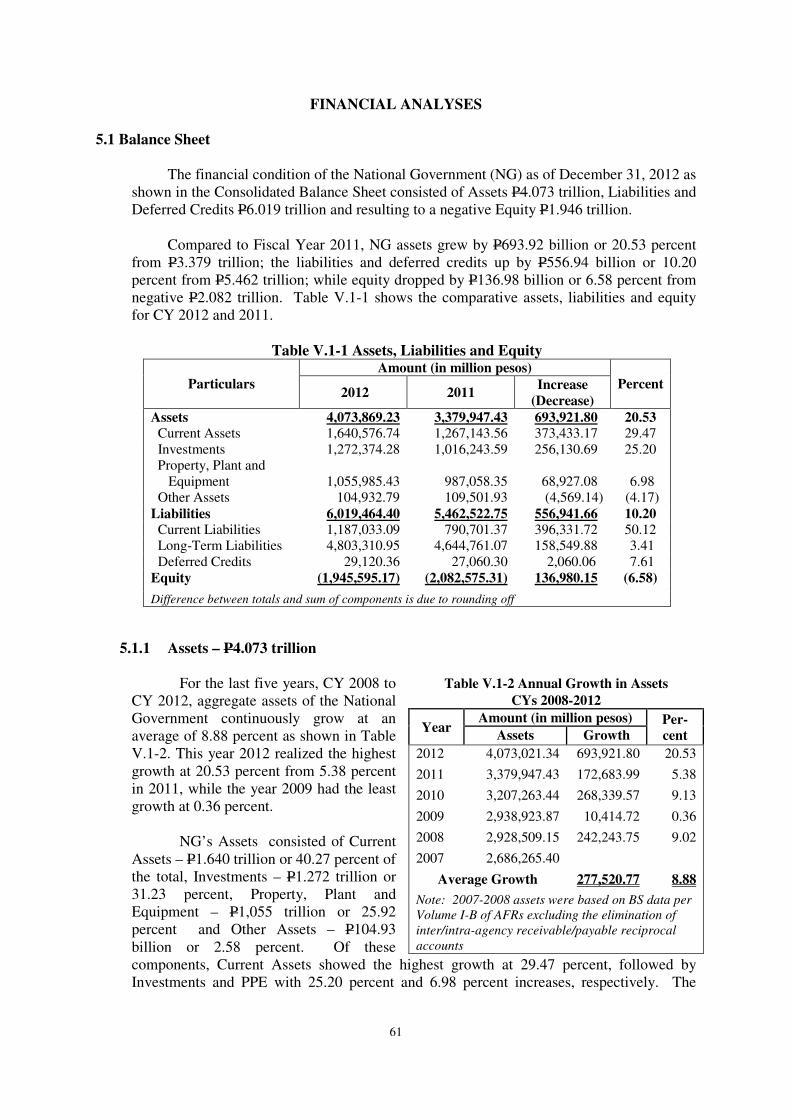

As of December 31, 2012, the NG had total assets of P4.074 trillion and total

liabilities of P6.019 trillion resulting to negative government equity of P1.946

trillion. Compared to the previous year, all components of the Balance Sheet

increased as shown in Chart II-3.

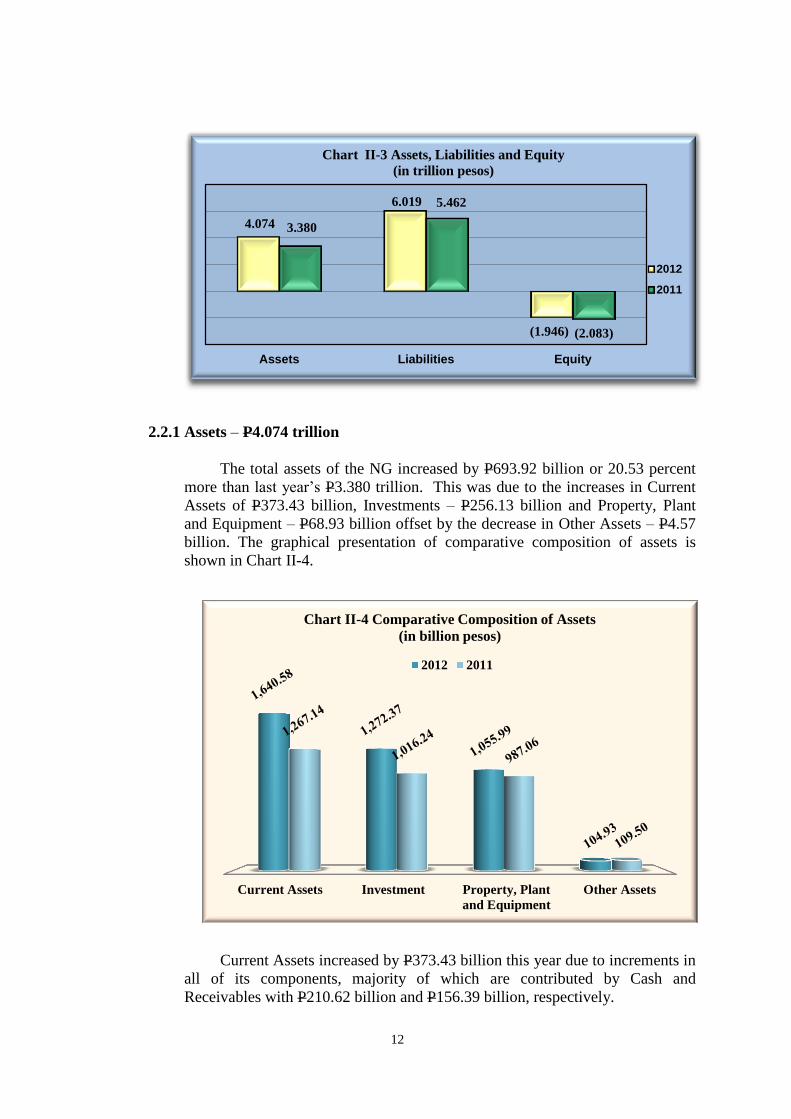

12

2.2.1 Assets – P4.074 trillion

The total assets of the NG increased by P693.92 billion or 20.53 percent

more than last year’s P3.380 trillion. This was due to the increases in Current

Assets of P373.43 billion, Investments – P256.13 billion and Property, Plant

and Equipment – P68.93 billion offset by the decrease in Other Assets – P4.57

billion. The graphical presentation of comparative composition of assets is

shown in Chart II-4.

Current Assets increased by P373.43 billion this year due to increments in

all of its components, majority of which are contributed by Cash and

Receivables with P210.62 billion and P156.39 billion, respectively.

Current Assets Investment Property, Plant

and Equipment

Other Assets

Chart II-4 Comparative Composition of Assets

(in billion pesos)

2012 2011

4.074

6.019

(1.946)

3.380

5.462

(2.083)

Assets Liabilities Equity

Chart II-3 Assets, Liabilities and Equity

(in trillion pesos)

2012

2011

13

Investments’ growth of P256.13 billion this year is brought about by the

P155.41 billion increments in Sinking Fund contributions and P100.72 billion

improvement in Investment in Securities.

Property, Plant and Equipment, net of accumulated depreciation showed

minimal increase of 6.98 percent or P68.93 billion while Other Assets

decreased by P4.57 billion.

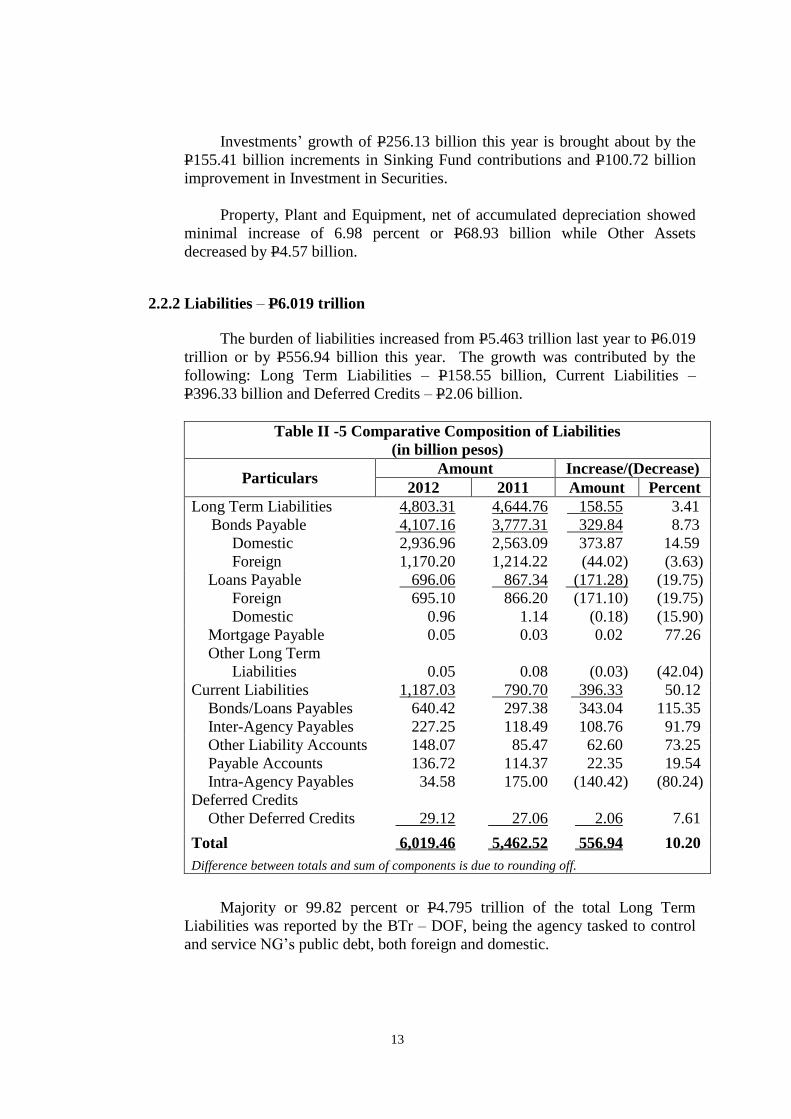

2.2.2 Liabilities – P6.019 trillion

The burden of liabilities increased from P5.463 trillion last year to P6.019

trillion or by P556.94 billion this year. The growth was contributed by the

following: Long Term Liabilities – P158.55 billion, Current Liabilities –

P396.33 billion and Deferred Credits – P2.06 billion.

Table II -5 Comparative Composition of Liabilities

(in billion pesos)

Particulars Amount Increase/(Decrease)

2012 2011 Amount Percent

Long Term Liabilities 4,803.31 4,644.76 158.55 3.41

Bonds Payable 4,107.16 3,777.31 329.84 8.73

Domestic 2,936.96 2,563.09 373.87 14.59

Foreign 1,170.20 1,214.22 (44.02) (3.63)

Loans Payable 696.06 867.34 (171.28) (19.75)

Foreign 695.10 866.20 (171.10) (19.75)

Domestic 0.96 1.14 (0.18) (15.90)

Mortgage Payable 0.05 0.03 0.02 77.26

Other Long Term

Liabilities

0.05

0.08

(0.03)

(42.04)

Current Liabilities 1,187.03 790.70 396.33 50.12

Bonds/Loans Payables 640.42 297.38 343.04 115.35

Inter-Agency Payables 227.25 118.49 108.76 91.79

Other Liability Accounts 148.07 85.47 62.60 73.25

Payable Accounts 136.72 114.37 22.35 19.54

Intra-Agency Payables 34.58 175.00 (140.42) (80.24)

Deferred Credits

Other Deferred Credits 29.12 27.06 2.06 7.61

Total 6,019.46 5,462.52 556.94 10.20

Difference between totals and sum of components is due to rounding off.

Majority or 99.82 percent or P4.795 trillion of the total Long Term

Liabilities was reported by the BTr – DOF, being the agency tasked to control

and service NG’s public debt, both foreign and domestic.

14

2.2.3 Government Equity – (P1.946 trillion)

As in previous years, liabilities of the NG exceeded the assets resulting to

negative balance of P1.946 trillion in equity. This year’s level posted a positive

increase of P136.98 billion or 6.58 per cent compared to negative P2.083

trillion reported in 2011.

The decrease in the negative balance was brought about by net income –

P239.97 billion offset by adjustments related to prior years’ transactions –

P25.42 billion, completed public infrastructures – P28.03 billion and

reforestation projects – P1.30 billion, which were transferred to the Registry of

Public Infrastructures and Registry of Reforestation Projects, respectively, and

the remittance to National Treasury for disposal of assets – P11.36 million.

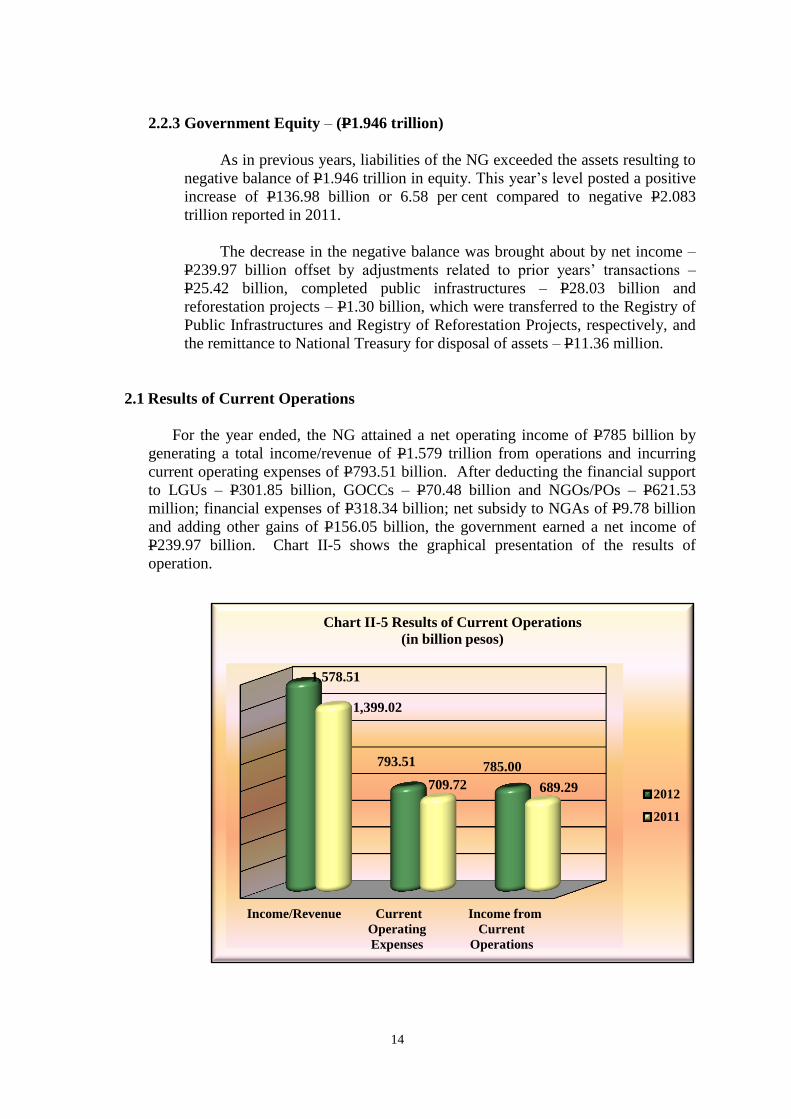

2.1 Results of Current Operations

For the year ended, the NG attained a net operating income of P785 billion by

generating a total income/revenue of P1.579 trillion from operations and incurring

current operating expenses of P793.51 billion. After deducting the financial support

to LGUs – P301.85 billion, GOCCs – P70.48 billion and NGOs/POs – P621.53

million; financial expenses of P318.34 billion; net subsidy to NGAs of P9.78 billion

and adding other gains of P156.05 billion, the government earned a net income of

P239.97 billion. Chart II-5 shows the graphical presentation of the results of

operation.

Income/Revenue Current

Operating

Expenses

Income from

Current

Operations

1,578.51

793.51 785.00

1,399.02

709.72 689.29

Chart II-5 Results of Current Operations

(in billion pesos)

2012

2011

15

1.3.1 Income/Revenue – P1.579 trillion

This year’s income/revenue of P1.579 trillion grew by P179.49 billion or

12.83 percent compared to previous year’s P1.399 trillion and surpassed the

projected amount of P1.561 trillion1 by P17.89 billion. The actual

income/revenue was generated from taxes – P1.357 trillion and non-taxes –

P221.98 billion.

The NG failed to realize its projected tax revenue of P1.427 trillion2 by

4.9 percent or P70.90 billion while general income of P221.98 billion exhibited

a 66.66 percent or P88.79 billion favorable variance over the estimated amount

of P133.20 billion.

Tax revenue of P1.357 trillion registered an increase of P134.58 billion

compared to last year’s figure of P1.222 trillion. This year’s tax revenue came

from the following sources:

Amount

(in million pesos)

Value Added Tax 365,316.80

Income Tax - Corporations 276,350.92

Income Tax - Individuals 179,033.03

Final Tax 162,304.09

Excise Tax on Articles 119,884.93

Value Added Tax - Expanded 80,484.26

Documentary Stamp Tax 54,678.11

Import Duties 42,386.03

Business Tax 54,134.95

Fines and Penalties - National Taxes 1,291.42

Motor Vehicles Users Charge 9,593.59

Capital Gains Tax 8,964.99

Other National Taxes 2,101.22

Total 1,356,524.34

Note: Difference between totals and sum of components is due to rounding off.

On the other hand, the general income increased by P44.91 billion from

P177.07 billion in 2011 to P221.98 billion this year. It is composed of Other

Income – P104.55 billion, Service Income – P62.50 billion, Business Income –

P45.83 billion and Permits and Licenses – P9.11 billion.

1.3.2 Current Operating Expenses – P793.51 billion

The current operating expenses of the NG totaling P793.51 billion

surpassed last year’s amount of P709.72 billion by 11.81 percent or P83.79

billion. The composition of the current operating expenses are as follows: PS –

P565.02 billion or 71.20 percent and MOOE – P228.50 billion or 28.80 percent.

1Table C.1, Revenue Program, by Source, 2011-2013, page 199,Budget of Expenditures and Sources of

Financing, Department of Budget and Management 2Ibid

16

Expenses for PS rose by P52.90 billion this year primarily due to the

implementation of the 4th tranche of the modified Salary Schedule for civilian

personnel and the modified Base Pay Schedule for military and uniformed

personnel, both provided under the Senate and House of Representatives Joint

Resolution No. 4, series of 2009, approved on June 17, 2009, and as mandated

under Executive Order No. 900, issued on June 23, 2010.

1.3.3 Income from Current Operations – P785.00billion

The current operation of the government for fiscal year 2012 resulted to

an income of P785.00 billion, exhibiting 13.88 percent growth or P95.70 billion

more than last year’s P689.29 billion.

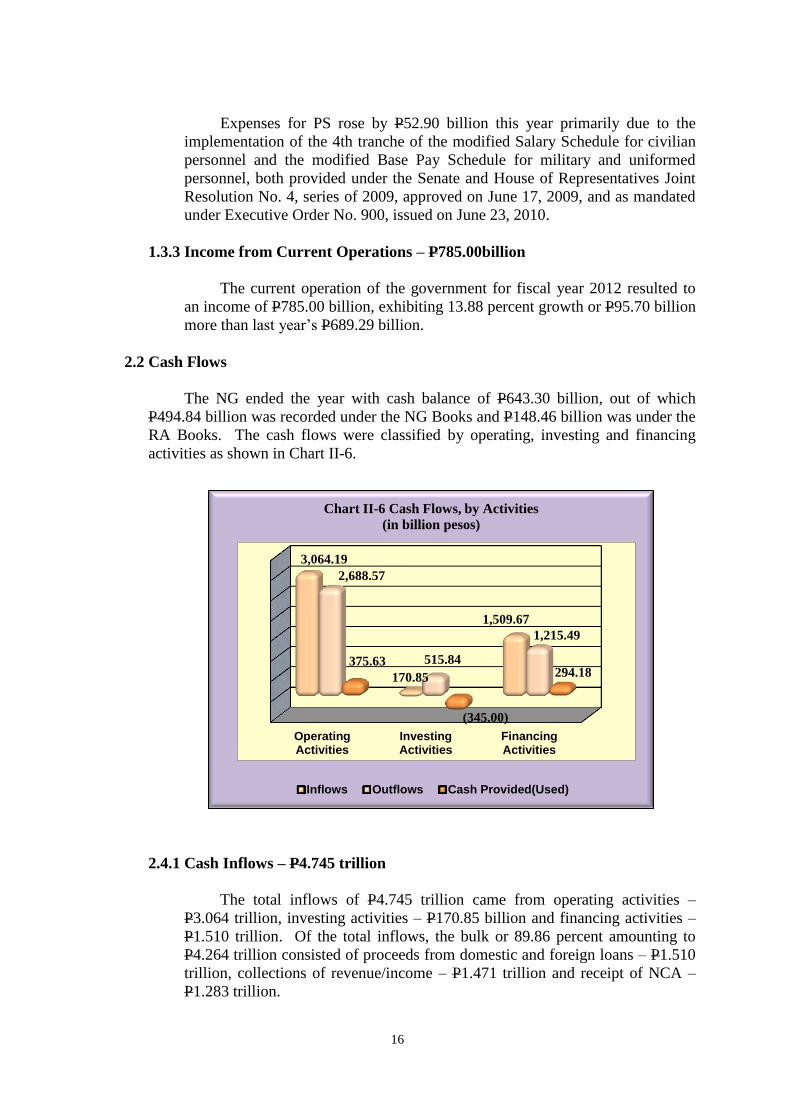

2.2 Cash Flows

The NG ended the year with cash balance of P643.30 billion, out of which

P494.84 billion was recorded under the NG Books and P148.46 billion was under the

RA Books. The cash flows were classified by operating, investing and financing

activities as shown in Chart II-6.

2.4.1 Cash Inflows – P4.745 trillion

The total inflows of P4.745 trillion came from operating activities –

P3.064 trillion, investing activities – P170.85 billion and financing activities –

P1.510 trillion. Of the total inflows, the bulk or 89.86 percent amounting to

P4.264 trillion consisted of proceeds from domestic and foreign loans – P1.510

trillion, collections of revenue/income – P1.471 trillion and receipt of NCA –

P1.283 trillion.

OperatingActivities

InvestingActivities

FinancingActivities

3,064.19

170.85

1,509.67

2,688.57

515.84

1,215.49

375.63

(345.00)

294.18

Chart II-6 Cash Flows, by Activities

(in billion pesos)

Inflows Outflows Cash Provided(Used)

17

2.4.2 Cash Outflows – P4.420trillion

The aggregate cash outflows reached P4.420 trillion, the bulk or 94.53

percent of which was used for the replenishment of negotiated MDS checks –

P1.204 trillion, payment of long term liabilities – P946.42 billion, payment of

operating expenses – P621 billion, investment – P398.52 billion, grant of

subsidies and donations – P346.15 billion, payment of interest expense – P269

billion, remittance of personnel benefit contributions and mandatory deductions

– P167.32 billion, purchase/construction of property, plant and equipment and

public infrastructures – P116.51 billion and release of intra-agency fund

transfers – P109.29 billion.

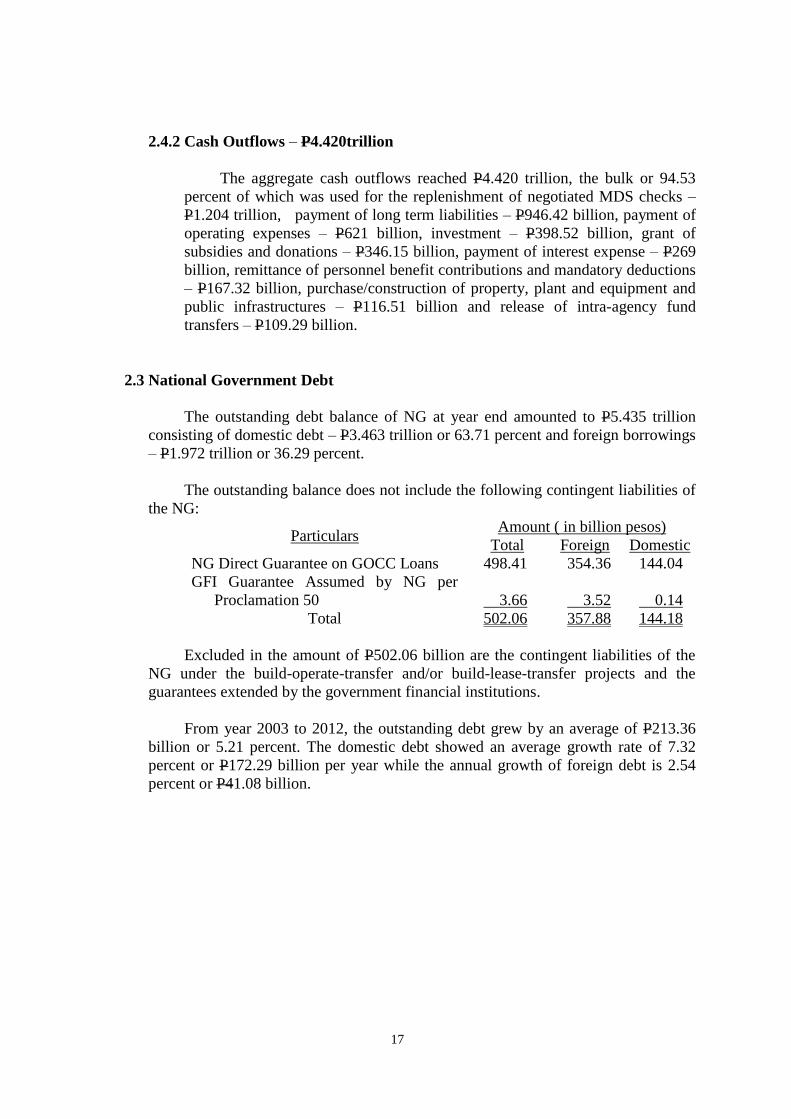

2.3 National Government Debt

The outstanding debt balance of NG at year end amounted to P5.435 trillion

consisting of domestic debt – P3.463 trillion or 63.71 percent and foreign borrowings

– P1.972 trillion or 36.29 percent.

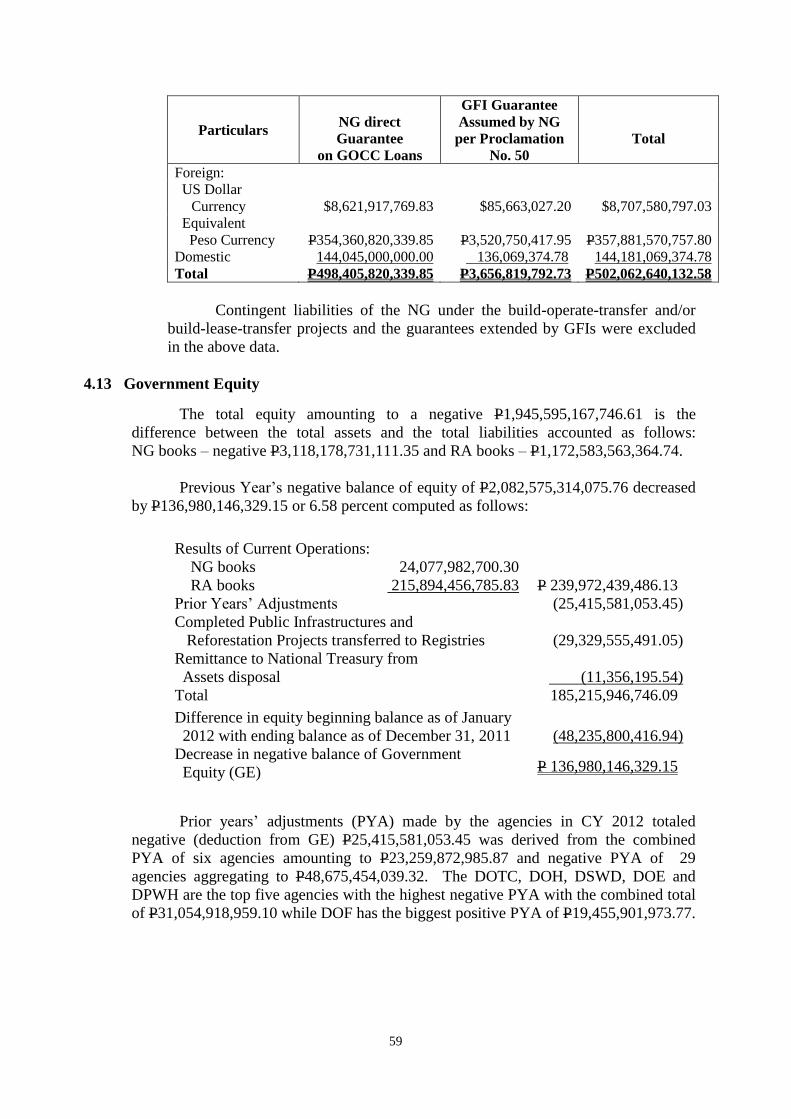

The outstanding balance does not include the following contingent liabilities of

the NG:

Particulars Amount ( in billion pesos)

Total Foreign Domestic

NG Direct Guarantee on GOCC Loans 498.41 354.36 144.04

GFI Guarantee Assumed by NG per

Proclamation 50

3.66

3.52

0.14

Total 502.06 357.88 144.18

Excluded in the amount of P502.06 billion are the contingent liabilities of the

NG under the build-operate-transfer and/or build-lease-transfer projects and the

guarantees extended by the government financial institutions.

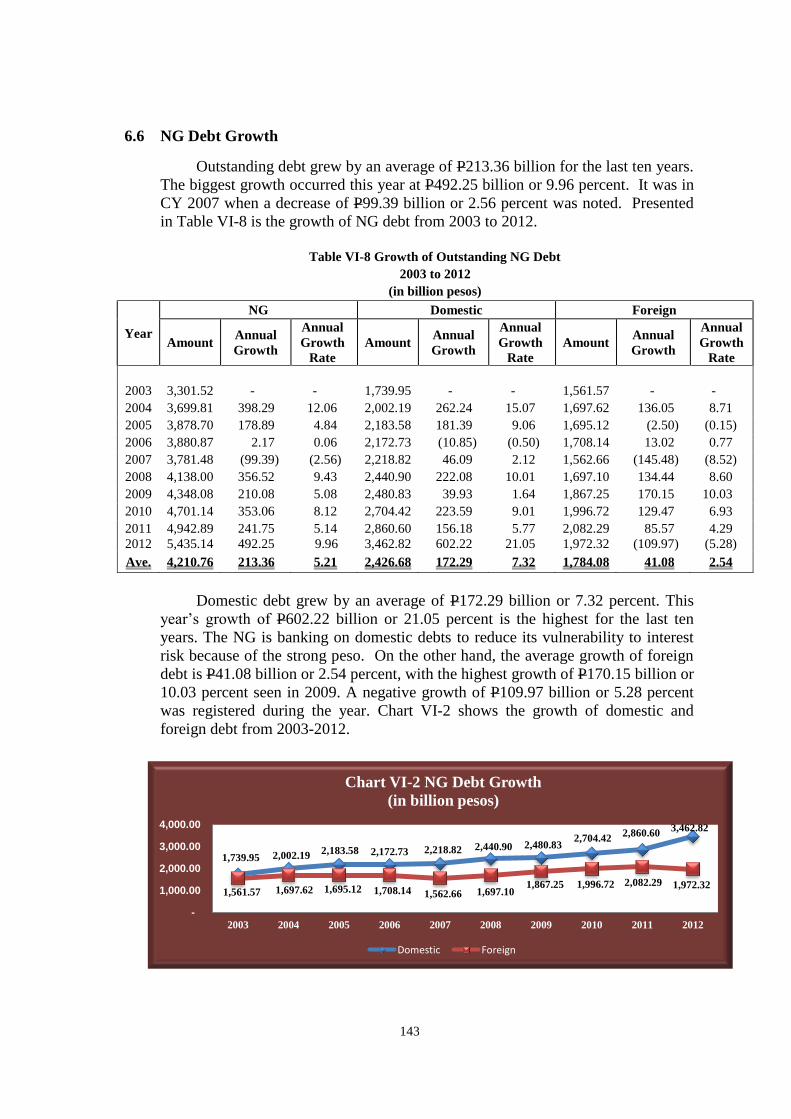

From year 2003 to 2012, the outstanding debt grew by an average of P213.36

billion or 5.21 percent. The domestic debt showed an average growth rate of 7.32

percent or P172.29 billion per year while the annual growth of foreign debt is 2.54

percent or P41.08 billion.

III. APPROPRIATIONS,

ALLOTMENTS,

OBLIGATIONS AND

BALANCES

18

APPROPRIATIONS, ALLOTMENTS, OBLIGATIONS AND BALANCES

3.1 Overview

The National Government (NG) budget for the year was described by

President Aquino as ‘Results-Focused Budget’ anchored on the five areas of priority

towards the achievement of his Administration’s Social Contract with the people,

namely: anti-corruption and good governance, poverty reduction and empowerment of

the poor, inclusive economic growth, just and lasting peace and the rule of law, and

integrity of the environment.

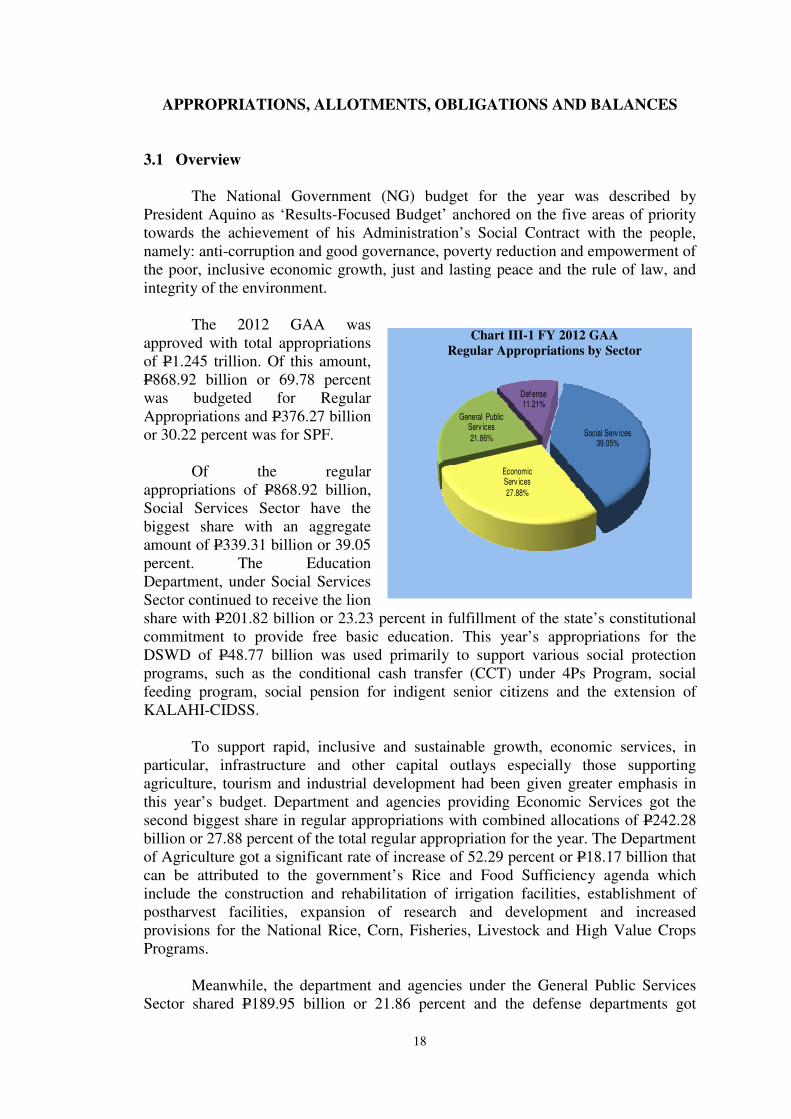

The 2012 GAA was

approved with total appropriations

of P1.245 trillion. Of this amount,

P868.92 billion or 69.78 percent

was budgeted for Regular

Appropriations and P376.27 billion

or 30.22 percent was for SPF.

Of the regular

appropriations of P868.92 billion,

Social Services Sector have the

biggest share with an aggregate

amount of P339.31 billion or 39.05

percent. The Education

Department, under Social Services

Sector continued to receive the lion

share with P201.82 billion or 23.23 percent in fulfillment of the state’s constitutional

commitment to provide free basic education. This year’s appropriations for the

DSWD of P48.77 billion was used primarily to support various social protection

programs, such as the conditional cash transfer (CCT) under 4Ps Program, social

feeding program, social pension for indigent senior citizens and the extension of

KALAHI-CIDSS.

To support rapid, inclusive and sustainable growth, economic services, in

particular, infrastructure and other capital outlays especially those supporting

agriculture, tourism and industrial development had been given greater emphasis in

this year’s budget. Department and agencies providing Economic Services got the

second biggest share in regular appropriations with combined allocations of P242.28

billion or 27.88 percent of the total regular appropriation for the year. The Department

of Agriculture got a significant rate of increase of 52.29 percent or P18.17 billion that

can be attributed to the government’s Rice and Food Sufficiency agenda which

include the construction and rehabilitation of irrigation facilities, establishment of

postharvest facilities, expansion of research and development and increased

provisions for the National Rice, Corn, Fisheries, Livestock and High Value Crops

Programs.

Meanwhile, the department and agencies under the General Public Services

Sector shared P189.95 billion or 21.86 percent and the defense departments got

Social Serv ices39.05%

Economic Serv ices

27.88%

General Public Serv ices

21.86%

Def ense11.21%

Chart III-1 FY 2012 GAA

Regular Appropriations by Sector

19

P97.37 billion or 11.21 percent of the total regular appropriation for the year. Chart

III-1 shows the sectoral distribution of the regular appropriations under the GAA for

2012.

3.2 Appropriations, Allotments, Obligations and Balances

An appropriation is an authorization under past Acts of Congress,

Presidential Decrees or other legislative enactments, for payments to be made with

funds of the government under specified condition and/or for specified purpose.

Allotments on the other hand, are the authorizations issued by the DBM to NGAs

to incur obligations or commitment to pay a sum of money for the implementation

of specific programs, projects and other expenditure items

In the Philippines, there are two sources of budgets being executed in a

given year, namely: the GAA for the current year which contains appropriations

intended to finance the programmed activities of departments and agencies and

special projects and other programs of the NG; and the balances of prior year’s

appropriations which are set by law to be available as continuing appropriations

until the end of the following year. In addition to these, automatic appropriations

provided by standing appropriation laws and Presidential Decrees also form part

of the total NG budget for the year.

The FY 2012 total NG budget aggregated at P2.529 trillion. Of this

amount, P1.245 trillion was provided under this year’s GAA, The balance was

sourced from Automatic Appropriations of P1.079 trillion and Continuing

Appropriations amounting to P205.02 billion.

Total allotments released by the DBM to carry out the functions of the NG

amounted to P2.379 trillion or 94.06 percent of the total NG budget for the year.

Of this amount, P1.133 trillion was released from this year’s GAA and the balance

was issued from the Automatic Appropriations of P1.079 trillion and Continuing

Appropriations of P167.42 billion.

Obligations incurred for the year aggregated to P2.196 trillion equivalent

to 92.28 percent of the total allotments released for the year. Of this amount,

P1.005 trillion was incurred under the GAA, P1.057 trillion for Automatic and

P134.08 billion for Continuing Appropriations.

The balances of unreleased appropriations and unobligated allotments for

this year’s budget stood at P150.15 billion and P183.64 billion, respectively, a

total of P333.79 billion.

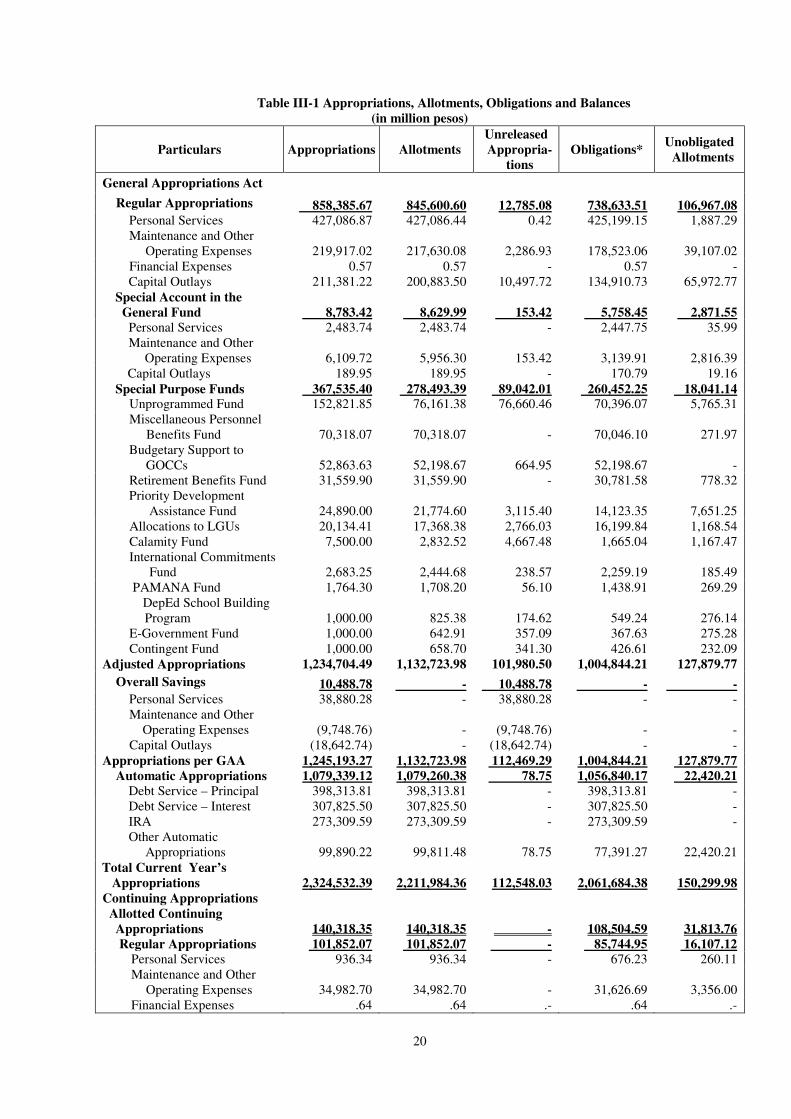

Table III-1 shows the summary of appropriations, allotments, obligations

incurred and balances for the year which are separately discussed in the

succeeding pages of this report. The details are presented by appropriation source

in Schedules 1 and 2, and by department/agency in Schedules 3 and 4, Volume I-

B.

20

Table III-1 Appropriations, Allotments, Obligations and Balances

(in million pesos)

Particulars Appropriations Allotments

Unreleased

Appropria-

tions

Obligations* Unobligated

Allotments

General Appropriations Act

Regular Appropriations 858,385.67 845,600.60 12,785.08 738,633.51 106,967.08 Personal Services 427,086.87 427,086.44 0.42 425,199.15 1,887.29

Maintenance and Other

Operating Expenses 219,917.02 217,630.08 2,286.93 178,523.06 39,107.02

Financial Expenses 0.57 0.57 - 0.57 -

Capital Outlays 211,381.22 200,883.50 10,497.72 134,910.73 65,972.77

Special Account in the

General Fund 8,783.42 8,629.99 153.42 5,758.45 2,871.55

Personal Services 2,483.74 2,483.74 - 2,447.75 35.99

Maintenance and Other

Operating Expenses 6,109.72 5,956.30 153.42 3,139.91 2,816.39

Capital Outlays 189.95 189.95 - 170.79 19.16

Special Purpose Funds 367,535.40 278,493.39 89,042.01 260,452.25 18,041.14 Unprogrammed Fund 152,821.85 76,161.38 76,660.46 70,396.07 5,765.31

Miscellaneous Personnel

Benefits Fund 70,318.07 70,318.07 - 70,046.10 271.97

Budgetary Support to

GOCCs 52,863.63 52,198.67 664.95 52,198.67 -

Retirement Benefits Fund 31,559.90 31,559.90 - 30,781.58 778.32

Priority Development

Assistance Fund 24,890.00 21,774.60 3,115.40 14,123.35 7,651.25

Allocations to LGUs 20,134.41 17,368.38 2,766.03 16,199.84 1,168.54

Calamity Fund 7,500.00 2,832.52 4,667.48 1,665.04 1,167.47

International Commitments

Fund

2,683.25 2,444.68 238.57 2,259.19 185.49

PAMANA Fund 1,764.30 1,708.20 56.10 1,438.91 269.29

DepEd School Building

Program

1,000.00 825.38 174.62 549.24 276.14

E-Government Fund 1,000.00 642.91 357.09 367.63 275.28

Contingent Fund 1,000.00 658.70 341.30 426.61 232.09

Adjusted Appropriations 1,234,704.49 1,132,723.98 101,980.50 1,004,844.21 127,879.77

Overall Savings 10,488.78 - 10,488.78 - -

Personal Services 38,880.28 - 38,880.28 - -

Maintenance and Other

Operating Expenses (9,748.76) - (9,748.76) - -

Capital Outlays (18,642.74) - (18,642.74) - -

Appropriations per GAA 1,245,193.27 1,132,723.98 112,469.29 1,004,844.21 127,879.77

Automatic Appropriations 1,079,339.12 1,079,260.38 78.75 1,056,840.17 22,420.21

Debt Service – Principal 398,313.81 398,313.81 - 398,313.81 -

Debt Service – Interest 307,825.50 307,825.50 - 307,825.50 -

IRA 273,309.59 273,309.59 - 273,309.59 -

Other Automatic

Appropriations

99,890.22 99,811.48 78.75 77,391.27 22,420.21

Total Current Year’s

Appropriations 2,324,532.39 2,211,984.36 112,548.03 2,061,684.38 150,299.98

Continuing Appropriations

Allotted Continuing

Appropriations

140,318.35

140,318.35

. -

108,504.59

31,813.76

Regular Appropriations 101,852.07 101,852.07 - 85,744.95 16,107.12

Personal Services 936.34 936.34 - 676.23 260.11

Maintenance and Other

Operating Expenses

34,982.70

34,982.70

-

31,626.69

3,356.00

Financial Expenses .64 .64 .- .64 .-

21

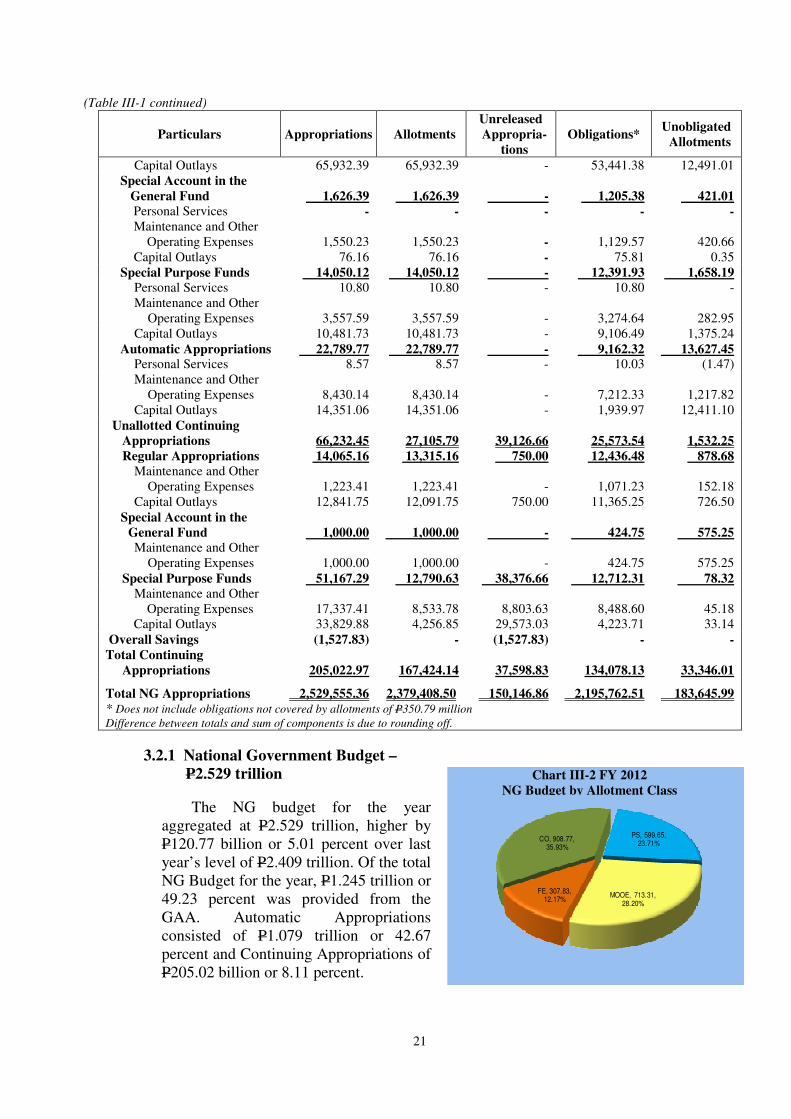

(Table III-1 continued)

Particulars Appropriations Allotments

Unreleased

Appropria-

tions

Obligations* Unobligated

Allotments

Capital Outlays 65,932.39 65,932.39 - 53,441.38 12,491.01

Special Account in the

General Fund 1,626.39 1,626.39 - 1,205.38 421.01

Personal Services - - - - -

Maintenance and Other

Operating Expenses 1,550.23 1,550.23 - 1,129.57 420.66

Capital Outlays 76.16 76.16 - 75.81 0.35

Special Purpose Funds 14,050.12 14,050.12 - 12,391.93 1,658.19 Personal Services 10.80 10.80 - 10.80 -

Maintenance and Other

Operating Expenses

3,557.59

3,557.59 -

3,274.64

282.95

Capital Outlays 10,481.73 10,481.73 - 9,106.49 1,375.24

Automatic Appropriations 22,789.77 22,789.77 - 9,162.32 13,627.45 Personal Services 8.57 8.57 - 10.03 (1.47)

Maintenance and Other

Operating Expenses

8,430.14

8,430.14

-

7,212.33

1,217.82

Capital Outlays 14,351.06 14,351.06 - 1,939.97 12,411.10

Unallotted Continuing

Appropriations

66,232.45

27,105.79

39,126.66

25,573.54

1,532.25

Regular Appropriations 14,065.16 13,315.16 750.00 12,436.48 878.68

Maintenance and Other

Operating Expenses

1,223.41

1,223.41

-

1,071.23

152.18

Capital Outlays 12,841.75 12,091.75 750.00 11,365.25 726.50

Special Account in the

General Fund

1,000.00

1,000.00 -

424.75

575.25

Maintenance and Other

Operating Expenses

1,000.00

1,000.00

-

424.75

575.25

Special Purpose Funds 51,167.29 12,790.63 38,376.66 12,712.31 78.32

Maintenance and Other

Operating Expenses

17,337.41

8,533.78

8,803.63

8,488.60

45.18

Capital Outlays 33,829.88 4,256.85 29,573.03 4,223.71 33.14

Overall Savings (1,527.83) - (1,527.83) - -

Total Continuing

Appropriations

205,022.97

167,424.14

37,598.83

134,078.13

33,346.01

Total NG Appropriations 2,529,555.36 2,379,408.50 150,146.86 2,195,762.51 183,645.99

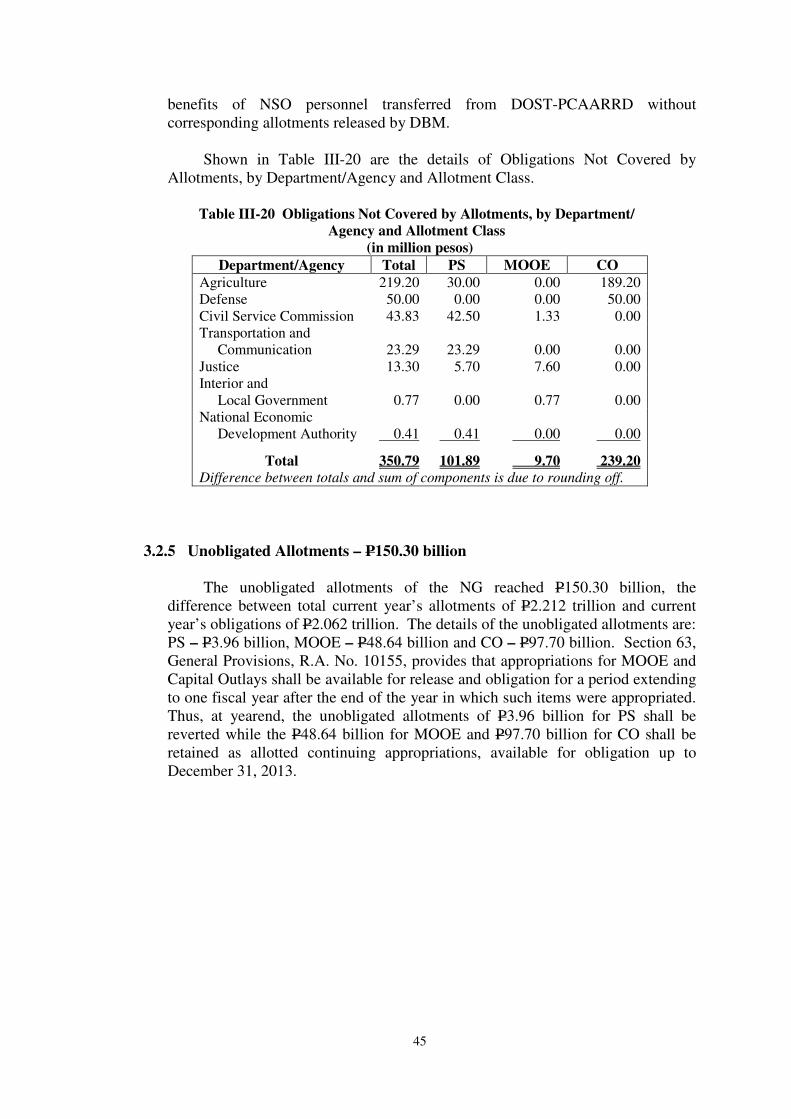

* Does not include obligations not covered by allotments of P350.79 million

Difference between totals and sum of components is due to rounding off.

3.2.1 National Government Budget –

P2.529 trillion

The NG budget for the year

aggregated at P2.529 trillion, higher by

P120.77 billion or 5.01 percent over last

year’s level of P2.409 trillion. Of the total

NG Budget for the year, P1.245 trillion or

49.23 percent was provided from the

GAA. Automatic Appropriations

consisted of P1.079 trillion or 42.67

percent and Continuing Appropriations of

P205.02 billion or 8.11 percent.

PS, 599.65, 23.71%

MOOE, 713.31, 28.20%

FE, 307.83, 12.17%

CO, 908.77, 35.93%

Chart III-2 FY 2012

NG Budget by Allotment Class

22

Chart III-2 shows the distribution of the FY 2012 NG Budget by Allotment

Class and Table III-2 shows the comparative details of the total NG Budget for

fiscal years 2012 and 2011.

Table III-2 Comparative Details of Appropriations

Particulars

Amount (in million pesos)

Percent 2012 2011

Increase /

(Decrease)

Regular Appropriations 858,385.67 765,405.33 92,980.34 12.15

Personal Services 427,086.87 399,406.94 27,679.93 6.93

Maintenance and Other

Operating Expenses 219,917.02 185,401.47 34,515.55 18.62

Financial Expenses 0.57 2.57 (2.00) (77.73)

Capital Outlays 211,381.22 180,594.35 30,786.86 17.05

Special Account in the

General Fund 8,783.42 12,566.90 (3,783.48) (30.11)

Personal Services 2,483.74 2,372.55 111.19 4.69

Maintenance and Other

Operating Expenses 6,109.72 9,969.80 (3,860.08) (38.72)

Capital Outlays 189.95 224.55 (34.60) (15.41)

Special Purpose Funds 367,535.40 229,210.85 138,324.55 60.35

Personal Services 102,385.39 91,363.21 11,022.18 12.06

Maintenance and Other

Operating Expenses 106,913.46 75,111.78 31,801.68 42.34

Capital Outlays 158,236.55 62,735.86 95,500.69 152.23

Overall Savings 10,488.78 (6,795.32) 17,284.10 (254.35)

General Appropriations Act 1,245,193.27 1,000,387.76 244,805.51 24.47

Automatic Appropriations 1,079,339.12 1,093,332.70 (13,993.58) (1.28)

Debt Service – Principal 398,313.81 444,196.12 (45,882.31) (10.33)

Debt Service – Interest 307,825.50 266,068.29 41,757.21 15.69

IRA 273,309.59 286,944.24 (13,634.65) (4.75)

Other Automatic

Appropriations 99,890.22 96,124.05 3,766.17 3.92

Total Current Year’s

Appropriations 2,324,532.39 2,093,720.46 230,811.93 11.02

Continuing Appropriations

Allotted Continuing

Appropriations 140,318.35 91,315.22 49,003.13 53.66

Unallotted Continuing

Appropriations 66,232.45 207,136.70 (140,904.25) (68.02)

Overall Savings (1,527.83) 16,613.50 (18,141.33) (109.20)

Total Continuing

Appropriations 205,022.97 315,065.42 (110,042.45) (34.93)

Total 2012 NG Appropriations 2,529,555.36 2,408,785.89 120,769.47 5.01 Difference between totals and sum of components is due to rounding off.

23

3.2.1.1 General Appropriations Act (R.A. No. 10155) – P1.245 trillion

In his Budget message, President Aquino described the FY 2012 GAA as a

“Result-Focused Budget’ that embodies his Administration’s commitment to lift

the marginalized sector from poverty through honest and effective governance. It

is focused on fulfilling the Social Contract with the people and firmly anchored on

Aquino Administration’s vision and priorities. Chart III-3 presents the NG

Appropriations per GAA for the years 2008 to 2012.

The 2012 GAA (R.A.

No. 10155) was signed by the

President on June 29, 2011

with total appropriations for

the year of P1.245 trillion.

The amount is higher by

24.47 percent over last year’s

GAA of P1 trillion. Of the

approved GAA for the year,

P868.92 billion or 69.78

percent was allocated for

Regular Appropriations and

P376.27 billion or 30.22

percent was for SPF.

For Regular Appropriations, Social Services Sector got the largest share of

P339.31 billion or 39.05 percent followed by the Economic Services at P242.28

billion or 27.88 percent. On the other hand, the General Public Services shared

P189.95 billion or 21.86 percent while the Defense was shared at P97.37 billion or

11.21 percent.

The amount of P339.31 billion provided for Social Services Sector was

sliced for the following components: Education, Culture and Manpower

Development - P232.21 billion; Social Security, Welfare and Development –

P61.33 billion; Health Services – P44.08 billion; Other Social Services – P1.36

billion and Housing and Community Development – P329.90 million.

The Economic Services Sector allocation of P242.28 billion was composed

of: Communication, Roads and Other Transport – P144.48 billion; Agriculture

and Agrarian Reform – P71.17 billion; Natural Resources and Environment –

P17.32 billion; Trade and Industry – P3.81 billion; Tourism – P1.63 billion;

Power and Energy – P1.58 billion; Water Resources Development and Flood

Control – P50.63 million and Other Economic Services – P2.24 billion.

• Regular Appropriations – P858.39 billion

The regular appropriations for programmed activities of the

departments and agencies of the NG amounted to P868.92 billion. This

includes P11.28 billion SAGF which was appropriated in pursuit of specific

800 1,000 1,200 1,400

2008

2009

2010

2011

2012

1,066.18

1,170.33

1,304.41

1,000.39

1,245.00

Chart III-3 Appropriations per GAA for

FYs 2008 to 2012

(in billion pesos)

24

programs provided in the Special Provisions of the GAA, leaving an available

allocation of P857.64 billion. Of this amount, P12.03 billion of the regular

appropriations of DOH was transferred to SPF particularly Budgetary Support

to GOCCs and transfers from Overall Savings of P12.78 billion were made.

Thus, the adjusted Regular Appropriations for the year stood at P858.39

billion higher by P92.98 billion or 12.15 percent than last year’s comparable

amount of P765.41 billion.

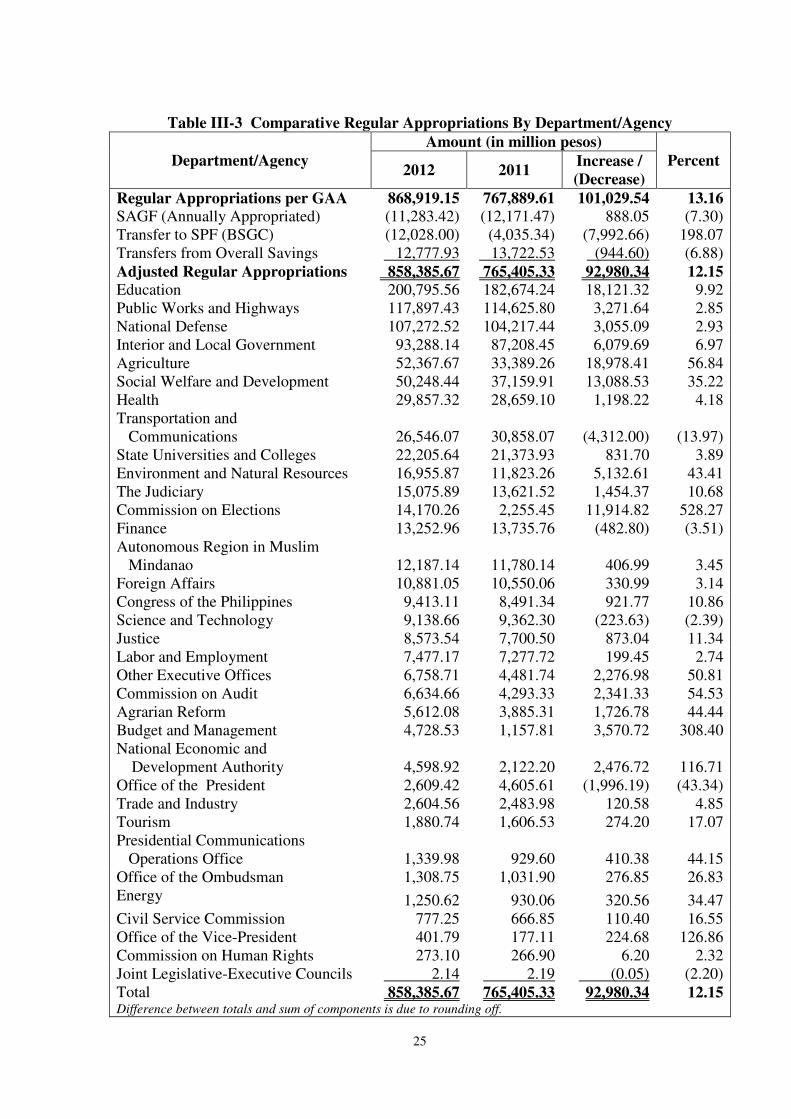

The DepEd remained on top with P200.80 billion, higher by P18.12

billion or 9.92 percent than last year’s P182.67 billion. This year’s

appropriations of the Education Department was utilized primarily for the

implementation of universal kindergarten program and hiring of new school

teachers to fill the gap for teachers shortages, procurement of more than 2.53

million school desks, chairs and textbooks, rehabilitation of classrooms, and

provision for other educational facilities. Meanwhile the largest rate of

budgetary increase for the Comelec at 528.27 percent can be attributed to the

preparations for the holding of the nationwide midterm elections of national

and local officials on May 2013.

The budget of the Social Welfare Department grew by 35.22 percent or

P13.09 billion from last year’s P37.16 billion. This year’s appropriations of

DSWD was expended for the implementation of various social protection

programs of the NG such as the expansion of the coverage of conditional cash

transfer under the 4Ps Program which supported three million households

(from 2.3 million last year), Social Feeding Program and the extension of the

KALAHI-CIDSS, rice subsidy, and pensions for indigent senior citizens,

among others. These are clear indications of the Aquino Administration’s

sincerity in alleviating the condition and protecting the interest of the

vulnerable sectors.

The significant 56.84 percent increase in the appropriations of the DA

from last year’s level of P33.39 billion to this year’s P52.37 billion was due

mainly to the government’s Rice and Food Sufficiency Program which

includes the construction and rehabilitation of irrigation facilities,

establishment of postharvest facilities, expansion of research and development

and provision for the National Rice, Corn, Fisheries, Livestocks and High

Value Crops Program.

The DBM had a substantial increase of 308.40 percent pertaining to the

transfers from pooled savings amounting to P3.46 billion needed to complete

the full requirement for the one-time payment of the unremmitted NG share in

the premium to the GSIS contribution of DepEd personnel.

Comparative details of regular appropriations by department/agency

are shown in Table III-3.

25

Table III-3 Comparative Regular Appropriations By Department/Agency

Department/Agency

Amount (in million pesos)

Percent 2012 2011

Increase /

(Decrease)

Regular Appropriations per GAA 868,919.15 767,889.61 101,029.54 13.16

SAGF (Annually Appropriated) (11,283.42) (12,171.47) 888.05 (7.30)

Transfer to SPF (BSGC) (12,028.00) (4,035.34) (7,992.66) 198.07

Transfers from Overall Savings 12,777.93 13,722.53 (944.60) (6.88)

Adjusted Regular Appropriations 858,385.67 765,405.33 92,980.34 12.15

Education 200,795.56 182,674.24 18,121.32 9.92

Public Works and Highways 117,897.43 114,625.80 3,271.64 2.85

National Defense 107,272.52 104,217.44 3,055.09 2.93

Interior and Local Government 93,288.14 87,208.45 6,079.69 6.97

Agriculture 52,367.67 33,389.26 18,978.41 56.84

Social Welfare and Development 50,248.44 37,159.91 13,088.53 35.22

Health 29,857.32 28,659.10 1,198.22 4.18

Transportation and

Communications 26,546.07 30,858.07 (4,312.00) (13.97)

State Universities and Colleges 22,205.64 21,373.93 831.70 3.89

Environment and Natural Resources 16,955.87 11,823.26 5,132.61 43.41

The Judiciary 15,075.89 13,621.52 1,454.37 10.68

Commission on Elections 14,170.26 2,255.45 11,914.82 528.27

Finance 13,252.96 13,735.76 (482.80) (3.51)

Autonomous Region in Muslim

Mindanao 12,187.14

11,780.14 406.99 3.45

Foreign Affairs 10,881.05 10,550.06 330.99 3.14

Congress of the Philippines 9,413.11 8,491.34 921.77 10.86

Science and Technology 9,138.66 9,362.30 (223.63) (2.39)

Justice 8,573.54 7,700.50 873.04 11.34

Labor and Employment 7,477.17 7,277.72 199.45 2.74

Other Executive Offices 6,758.71 4,481.74 2,276.98 50.81

Commission on Audit 6,634.66 4,293.33 2,341.33 54.53

Agrarian Reform 5,612.08 3,885.31 1,726.78 44.44

Budget and Management 4,728.53 1,157.81 3,570.72 308.40

National Economic and

Development Authority

4,598.92

2,122.20

2,476.72

116.71

Office of the President 2,609.42 4,605.61 (1,996.19) (43.34)

Trade and Industry 2,604.56 2,483.98 120.58 4.85

Tourism 1,880.74 1,606.53 274.20 17.07

Presidential Communications

Operations Office

1,339.98

929.60

410.38

44.15

Office of the Ombudsman 1,308.75 1,031.90 276.85 26.83

Energy 1,250.62 930.06 320.56 34.47

Civil Service Commission 777.25 666.85 110.40 16.55

Office of the Vice-President 401.79 177.11 224.68 126.86

Commission on Human Rights 273.10 266.90 6.20 2.32

Joint Legislative-Executive Councils 2.14 2.19 (0.05) (2.20)

Total 858,385.67 765,405.33 92,980.34 12.15 Difference between totals and sum of components is due to rounding off.

26

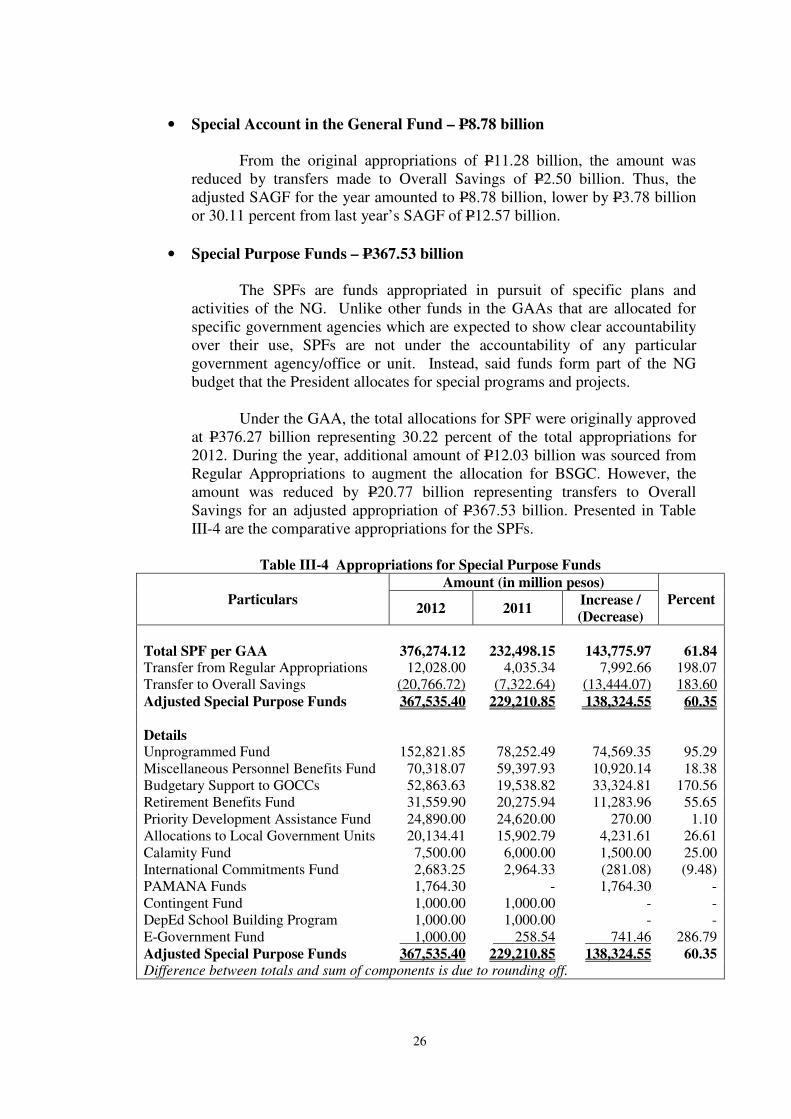

• Special Account in the General Fund – P8.78 billion

From the original appropriations of P11.28 billion, the amount was

reduced by transfers made to Overall Savings of P2.50 billion. Thus, the

adjusted SAGF for the year amounted to P8.78 billion, lower by P3.78 billion

or 30.11 percent from last year’s SAGF of P12.57 billion.

• Special Purpose Funds – P367.53 billion

The SPFs are funds appropriated in pursuit of specific plans and

activities of the NG. Unlike other funds in the GAAs that are allocated for

specific government agencies which are expected to show clear accountability

over their use, SPFs are not under the accountability of any particular

government agency/office or unit. Instead, said funds form part of the NG

budget that the President allocates for special programs and projects.

Under the GAA, the total allocations for SPF were originally approved

at P376.27 billion representing 30.22 percent of the total appropriations for

2012. During the year, additional amount of P12.03 billion was sourced from

Regular Appropriations to augment the allocation for BSGC. However, the

amount was reduced by P20.77 billion representing transfers to Overall

Savings for an adjusted appropriation of P367.53 billion. Presented in Table

III-4 are the comparative appropriations for the SPFs.

Table III-4 Appropriations for Special Purpose Funds

Particulars

Amount (in million pesos)

Percent 2012 2011

Increase /

(Decrease)

Total SPF per GAA 376,274.12 232,498.15 143,775.97 61.84 Transfer from Regular Appropriations 12,028.00 4,035.34 7,992.66 198.07

Transfer to Overall Savings (20,766.72) (7,322.64) (13,444.07) 183.60

Adjusted Special Purpose Funds 367,535.40 229,210.85 138,324.55 60.35

Details Unprogrammed Fund 152,821.85 78,252.49 74,569.35 95.29

Miscellaneous Personnel Benefits Fund 70,318.07 59,397.93 10,920.14 18.38

Budgetary Support to GOCCs 52,863.63 19,538.82 33,324.81 170.56

Retirement Benefits Fund 31,559.90 20,275.94 11,283.96 55.65

Priority Development Assistance Fund 24,890.00 24,620.00 270.00 1.10