Embed Size (px)

DESCRIPTION

this project is on personal research of anmol setia on pardhan mantri jhan dhan yojana and bima yojana launch by modi government in 2014 and 2015. this research project is made with the help of oriental bank of commerce and data is collected from there .

Citation preview

1

A

PROJECT REPORT

“NEW SCHEMES LAUNCH BY PRIME MINISTER OF INDIA ”

UNDERTAKEN IN:-

SUBMITTED TO:- SUBIMTTED BY:-

Prof. ASHOK KUMAR JINDAL SIR ANMOL SETIA

(H.O.D of Post Graduation dept. Commerce dept.) (M.com 1st year (2nd SEM.))

R.S.D College, Ferozepur City Roll No: - 45425

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

2

DECLARATION

I hereby declare that , I have carried out summer training project on the topic enti t led “NEW SCHEMES LAUCH BY PRIME MINISTER OF INDIA”.

I further declare that this project work is based on my original work and no part of this project has not been previously submitted to any university for any examination.

ANMOL SETIA

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

3

ACKNOWLEDGEMENT

I have taken efforts in this project. However, it would not have been possible without the kind support and help of many individuals and organization . I would like to extend my sincere thanks to all of them. First of all, I would like to pay my heartiest thanks to entire family of OBC BANK especially Mr. Mahesh Kumar Gupta, Branch manager, who provided me such a wonderful opportunity to do Summer Training and provided their valuable suggestions in understanding the work of Research Project,.

I am highly indebted to H.O.D OF POST GRADUATION DEPARTMENT COMMERCE Prof. MR. ASHOK JINDAL for their guidance and constant supervision as well as for providing necessary information regarding the project & also their support in completing of this project. Working under them was an extremely knowledgeable and enriching experience for me. I am very thankful for all the value addition and enhancement done to me. No words can adequately express my overriding debt of gratitude to my parents whose support helps me in all the way. Above all I shall thank my friends who constantly encouraged and blessed me so as to enable me to do this work successfully.

The study had indeed helped me to explore more knowledgeable avenues related to my topic and I am sure it will help me in my future.

ANMOL SETIA

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

4

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

5

PREFACE

This project report attempts to bring under one cover the entire hard work and dedication put in by me in the completion of the project work on N.P.A and different schemes of present government of OBC bank.

Survey is an excellent tool for learning and exploration. No classroom routine can substitute which is possible while working in real situations. Application of theoretical knowledge to practical situations is the bonanzas of this survey. Without a proper combination of inspection and perspiration, it‘s not easy to achieve anything. There is always a sense of gratitude, which we express to others for the help and the needy services they render during the different phases of our lives. I have expressed my experiences in my own simple way. I hope who go through it will find it interesting and worth reading. All constructive feedback is cordially invited.

ANMOL SETIA

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

6

INDEX

SR NO. PARTICULARS PAGE NO.

1) DECLARATION 2

2) ACKNOWLEDGEMENT 3

3) CERTIFICATE 4

4) PREFACE 5

TABLE OF CONTENTS

5) CHAPTER-1COMPANY PROFILE HISTORY OF BANKING SECTOR IN

INDIA CURRENT PERIOD OF BANKING IN

INDIA HISTORY OF OBC BANK FACILITIES OFFERED BY OBC

BANK VISION & MISSION BALANCE SHEET FOR LAST

3YEARS OF OBC BANK CASH FLOW STATEMENT FOR LAST

3 YEARS OF OBC BANK

9-11

12-14

15-1819-20

2122-23

24

6)CHAPTER-2 BRANCH PROFILE & PARDHAN MANTRI JHAN DHAN YOJANA

INTRODUCTION OF BRANCH INTRODUCTION TO PMJDY PURPOSE OF PMJDY PERFORMANCE OF PMJDY CRITICISM OF PMJDY

2627-282829-3434-35

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

7

SR NO. TABLE OF CONTENTSPAGE NO.

7) CHAPTER-3 RESEARCH METHODOLOGY

NEED , OBJECTIVES, SCOPE SAMPLE DESIGN METHOD OF COLLECTION DATA CONDUCTING SURVEY KNOWLEDGE SHARING

373838-393939

8) CHAPTER-4 DATA ANALYSIS & INTREPRETATION

DATA ANALYSIS & INTREPRETATION

FINDING LIMITATIONS SUGGESTIONS

41-50

515253

9) CHAPTER-5 ATAL PENSION YOJANA

DETAIL OF SCHEME 55-64

CHAPTER-6 PARDHAN MANTRI JEEVAN JYOTI BIMA YOJANA AND PARDHAN MANTRI SURAKSHA BIMA YOJANA

OVERVIEW OF PMJJBY CRITICISM OF PMJJBY DATA ANALYSIS OVERVIEW OF PMSBY CRITICISM OF PMSBY DATA ANALYSIS

666667686970

BIBLIOGRAPHY 71

ANNEXURE 72-76

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

8

Chapter-1

COMPANY PROFILE

HISTORY OF BANKING SECTOR IN INDIA CURRENT PERIOD OF BANKING IN INDIA HISTORY OF OBC BANK FACILITIES OFFERED BY OBC BANK BALANCE SHEET FOR LAST 3YEARS OF OBC BANK CASH FLOW STATEMENT FOR LAST 3 YEARS OF OBC BANK

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

9

HISTORY OF BANKING SECTOR IN INDIA

Banking in India in the modern sense originated in the last decades of the 18th century. Among the first banks were the Bank of Hindustan, which was established in 1770 and liquidated in 1829-32; and the General Bank of India, established 1786 but failed in 1791.

The largest bank, and the oldest still in existence, is the State Bank of India. It originated as the Bank of Calcutta in June 1806. In 1809, it was renamed as the Bank of Bengal. This was one of the three banks funded by a presidency government; the other two were the Bank of Bombay and the Bank of Madras. The three banks were merged in 1921 to form the Imperial Bank of India, which upon India's independence, became the State Bank of India in 1955. For many years the presidency banks had acted as quasi-central banks, as did their successors, until the Reserve Bank of India was established in 1935, under the Reserve Bank of India Act, 1934.

In 1960, the State Banks of India was given control of eight state-associated banks under the State Bank of India (Subsidiary Banks) Act, 1959. These are now called its associate banks. In 1969 the Indian government nationalized 14 major private banks. In 1980, 6 more private banks were nationalized. These nationalized banks are the majority of lenders in the Indian economy. They dominate the banking sector because of their large size and widespread networks.

The Indian banking sector is broadly classified into scheduled banks and non-scheduled banks. The scheduled banks are those which are included under the 2nd Schedule of the Reserve Bank of India Act, 1934. The scheduled banks are further classified into: nationalized banks; State Bank of India and its associates; Regional Rural Banks (RRBs); foreign banks; and other Indian private sector banks. The term commercial bank refers to both scheduled and non-scheduled commercial banks which are regulated under the Banking Regulation Act, 1949.

Generally banking in India was fairly mature in terms of supply, product range and reach-even though reach in rural India and to the poor still remains a challenge. The

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

10

government has developed initiatives to address this through the State Bank of India expanding its branch network and through the National Bank for Agriculture and Rural Development with things like microfinance.

Post-IndependenceThe partition of India in 1947 adversely impacted the economies of Punjab and West Bengal, paralyzing banking activities for months. India's independence marked the end of a regime of the Laissez-faire for the Indian banking. The Government of India initiated measures to play an active role in the economic life of the nation, and the Industrial Policy Resolution adopted by the government in 1948 envisaged a mixed economy. This resulted into greater involvement of the state in different segments of the economy including banking and finance. The major steps to regulate banking included:

The Reserve Bank of India, India's central banking authority, was established in April 1935, but was nationalized on 1 January 1949 under the terms of the Reserve Bank of India (Transfer to Public Ownership) Act, 1948 (RBI, 2005b).[16]

In 1949, the Banking Regulation Act was enacted which empowered the Reserve Bank of India (RBI) "to regulate, control, and inspect the banks in India".

The Banking Regulation Act also provided that no new bank or branch of an existing bank could be opened without a license from the RBI, and no two banks could have common directors.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

11

Nationalization in the 1960Despite the provisions, control and regulations of the Reserve Bank of India, banks in India except the State Bank of India(SBI), continued to be owned and operated by private persons. By the 1960s, the Indian banking industry had become an important tool to facilitate the development of the Indian economy. At the same time, it had emerged as a large employer, and a debate had ensued about the nationalization of the banking industry. Indira Gandhi, the then Prime Minister of India, expressed the intention of the Government of India in the annual conference of the All India Congress Meeting in a paper entitled "Stray thoughts on Bank Nationalization." The meeting received the paper with enthusiasm.

Thereafter, her move was swift and sudden. The Government of India issued an ordinance ('Banking Companies (Acquisition and Transfer of Undertakings) Ordinance, 1969') and nationalized the 14 largest commercial banks with effect from the midnight of 19 July 1969. These banks contained 85 percent of bank deposits in the country. Jayaprakash Narayan, a national leader of India, described the step as a "masterstroke of political sagacity." Within two weeks of the issue of the ordinance, the Parliament passed the Banking Companies (Acquisition and Transfer of Undertaking) Bill, and it received the presidential approval on 9 August 1969.

A second dose of nationalization of 6 more commercial banks followed in 1980. The stated reason for the nationalization was to give the government more control of credit delivery. With the second dose of nationalisation, the Government of India controlled around 91% of the banking business of India. Later on, in the year 1993, the government merged New Bank of India with Punjab National Bank.[18] It was the only merger between nationalized banks and resulted in the reduction of the number of nationalised banks from 20 to 19. After this, until the 1990s, the nationalised banks grew at a pace of around 4%, closer to the average growth rate of the Indian economy.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

12

CURRENT PERIOD OF BANKING IN INDIA

All banks which are included in the Second Schedule to the Reserve Bank of India Act, 1934 are Scheduled Banks. These banks comprise Scheduled Commercial Banks and Scheduled Co-operative Banks. Scheduled Commercial Banks in India are categorised into five different groups according to their ownership and/or nature of operation. These bank groups are:

State Bank of India and its Associates Nationalised Banks Private Sector Banks Foreign Banks State Co-operative Banks.

In the bank group-wise classification, IDBI Bank Ltd. is included in Nationalised Banks. Scheduled Co-operative Banks consist of Scheduled State Co-operative Banks and Scheduled Urban Cooperative Banks.

By 2010, banking in India was generally fairly mature in terms of supply, product range and reach-even though reach in rural India still remains a challenge for the private sector and foreign banks. In terms of quality of assets and capital adequacy, Indian banks are considered to have clean, strong and transparent balance sheets relative to other banks in comparable economies in its region. The Reserve Bank of India is an autonomous body, with minimal pressure from the government.

With the growth in the Indian economy expected to be strong for quite some time-especially in its services sector-the demand for banking services, especially retail banking, mortgages and investment services are expected to be strong. One may also expect M&As, takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the first time an investor has been allowed to hold more than 5% in a private sector bank since the RBI announced

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

13

norms in 2005 that any stake exceeding 5% in the private sector banks would need to be vetted by them.

In recent years critics have charged that the non-government owned banks are too aggressive in their loan recovery efforts in connection with housing, vehicle and personal loans. There are press reports that the banks' loan recovery efforts have driven defaulting borrowers to suicide.

By 2013 the Indian Banking Industry employed 1,175,149 employees and had a total of 109,811 branches in India and 171 branches abroad and manages an aggregate deposit of 67504.54 billion (US$1.1 trillion or €1.0 trillion) and bank credit of 52604.59 billion (US$830 billion or €780 billion). The net profit of the banks operating in India was 1027.51 billion (US$16 billion or €15 billion) against a turnover of 9148.59 billion (US$140 billion or €140 billion) for the financial year 2012-13.

On 28 Aug, 2014, Pradhan Mantri Jan Dhan Yojana is a scheme for comprehensive financial inclusion launched by the Prime Minister of India, Narendra Modi. Run by Department of Financial Services, Ministry of Finance, on the inauguration day, 1.5 Crore (15 million) bank accounts were opened under this scheme By 10 January 2015, 11.5 crore accounts were opened, with around 8698 crore (US$1.4 billion) were deposited under the scheme which also has an option for opening new bank accounts with zero balance.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

14

The Chart shows the Structure of Banking in INDIA.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

15

Brief history of OBC bank

Rai Bahadur Lala Sohan Lal, the first Chairman of the Bank, founded OBC in 1943 in Lahore. Within four years of its coming into existence, OBC had to face Partition. The bank had to close down its branches in the newly formed Pakistan and shift its registered office from Lahore to Amritsar. Lala Karam Chand Thapar, the then Chairman of the Bank, in a unique gesture honored the commitments made to the depositors from Pakistan and paid every rupee to its departing customers.

The Bank has witnessed many ups and downs since its establishment. The period of 1970-76 is said to be the most challenging phase in the history of the Bank. At one time profit plummeted to 175 that prompted the owner of the bank, the Thapar House, to sell / close the bank. Then employees and leaders of the Bank came forward to rescue the Bank. The owners were moved and had to change their decision of selling the bank and in turn they decided to improve the position of the bank with the active cooperation and support of all the employees. Their efforts bore fruits and performance of the bank improved significantly. This was the turning point in the history of the bank

The bank was nationalized on 15 April 1980. At that time OBC ranked 19th among the 20 nationalized bank

In 1997, OBC acquired two banks: Bari Doab Bank and Punjab Cooperative Bank. The acquisition of these two banks brought with it no additional branches.

On 14 August 2004, OBC amalgamated Global Trust Bank (GTB). GTB was a leading private sector bank in India that was associated with various financial discrepancies

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

16

leading to a moratorium being imposed by RBI shortly before it merged into OBC. The acquisition brought with it 103 branches, which increased OBC's branch total to 1092.

Chairpersons

The Chairpersons (CMD) of the bank were as under :-

Name Period

Karam Chand

Thapar1946 to 1961

L. M. Thapar 1961 to 1969

R. P. Oberoi 1973 to 1976

M. K. Vig 1976 to 1983

P. S.

Gopalakrishnan1984 to 1988

S. P. Talwar 1988 to 1990

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

17

S. K. Soni 1990 to 1996

Dalbir Singh 1996 to 2000

B. D. Narang 2000 to 2005

K. N. Prithviraj 2005 to 2007

T. Y. Prabhu

August2009 to January 2011

Nagesh Paidah January 2011 to February 2012

S.L. Bansal March 2012 to September 2014

Sh. Animesh

Chauhan

December 2014 to Present (as Managing Director and Chief

Executive Officer of the bank)

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

18

OVERVIEW:-

The bank offers a wide range of banking products and services such as deposit accounts, loans, debit cards, credit cards (with tie up with SBI), Insurance products, ATMs, Internet banking, Mobile Banking, Self-banking halls, call centre, etc.

The Bank has launched yet another people's participation in the planning process at grass root level essentially to tackle the maladies of poverty. The Grameen Projects venture aims to alleviate poverty plus identify the reasons responsible for the failure or success.

OBC is already implementing a GRAMEEN PROJECT in Dehradun District (UK) and Hanumangarh District (Rajasthan). Formulated on the pattern of the Bangladesh Grameen Bank, the Scheme has a unique feature of disbursing small loans ranging from 75 (~US $1.5) onwards. The beneficiaries of the Grameen Project are mostly women. The Bank is engaged in providing training to rural folk in using locally available raw material to produce pickles, jams etc. This has provided self-employment and augmented income levels thus reforming lives of rural folk and encouraging cottage industries in rural areas.

OBC launched yet another unique scheme christened 'The Comprehensive Village Development Program on the auspicious day of Baisakhi, the 13th of April 1997 at three villages in Punjab namely Rurki Kalan (Distt. Sangrur), Raje Majra (Distt. Ropar) and Khaira Majha (Distt. Jaladhar) and two villages in Haryana, namely Khunga (Distt. Jind) and Narwal (Distt. Kaithal). The pilot launch was a great success. Emboldened by the success, Bank extended the programme to more villages. At present, it covers 15 villages; 10 in Punjab, 4 in Haryana and 1 in Rajasthan. The program focuses on providing a comprehensive and integrated package providing rural finance to the villagers with Village Development as its focus, thus contributing towards infrastructural development and augmentation of income for each farmer of the village. The Bank has implemented

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

19

14 point action plan for strengthening of credit delivery to women and has designated 5 branches as specialized branches for women entrepreneurs.

Facilities offered by OBC bank :-

The following services are being offered through Oriental Bank’s iBanking Services, Free of Cost:-

Services offered through Oriental Bank’s iBanking Presently following online facilities are offered through Internet Banking

Channel:- Online generation of Statement of Account – For a given period, Range of Cheque

Nos and Amount. Facility for Stop payment of Cheques, Cheque Status Inquiry and Clearing

Instruments. Customer can make NEFT/ RTGS payments without incurring any cost.1) Funds Transfer and Other Services :-

Funds Transfer to own linked accounts 3rd Party Funds Transfer to other Bank’s accounts (through NEFT/RTGS). 3rd Party Funds Transfer to other accounts within OBC. Loan EMI Payment Online creation of e-FDRs/ e-CDRs. Purchase of Air Tickets and Railway Tickets. Payment of Direct and Indirect taxes, VAT collection for Maharashtra Govt. Funds transfer facilities for Trading of Shares through ShareKhan.com FORM26AS – Online Tax credit view statement. Tracker ID through Email System for select Branches covered under J&K state. Facilitating online view of (DeMAT) Depository details for Retail Net Banking.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

20

Lien Based Online Share Trading with M/s. Karvy, Funds Transfer Transaction Limits for 3 rd Party Funds Transfer and e-Commerce

Transactions: Minimum Amount : Rs.100/- per transaction Maximum Amount : Rs. 2,00,000/- per transaction Per Day Maximum : Rs.4,00,000/-

2) Utility Bill Payment :-

E-Commerce (EShoppe):- More than 3000 Merchant establishments have been integrated with Bank’s Internet Banking Services.

User can make payment of various Utility Bills online viz. Electricity, Telephone, Mobile, LIC Premiums, Credit cards, Travel & Ticketing, Mutual Funds etc.

Customer can also make Donations and make Credit Card payments like ICICI Bank, SBI, CITI Bank, Barclays Bank etc.

3) Request for Issuance of Cheque Book, PO-DD etc :- Net Banking Customers can also put their request for issuance of Cheque Book,

PO/DD etc, which are processed at Backend by the Relationship Manager.

4. Mails:- Customer can also exchange mails through Internet Banking for any queries.

5. Activity:- Customer can inquire various financial and non-financial activities performed

during a period of time. 6. Customize :- Facility provided to :

Change Sign On or Transaction password Registration for Online Password facility. Add Nick names to customer’s accounts for easy identification. Change display formats as per customer’s preferences like Date Format, Amount

Format, Add email id, Change your Salutation etc.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

21

Vision & Mission Statement

VISION STATEMENT "TO BE A CUSTOMER FRIENDLY PREMIER BANK COMMITTED TO ENHANCING STAKEHOLDER VALUE"

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

22

MISSION STATEMENT

Provide quality, innovative services with state-of-the-art technology in line with customer expectations.

Enhance employees’ professional skills and strengthen cohesiveness. Create wealth for customers and other stakeholders.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

23

OBC BANK BALANCE SHEET FOR LAST 3 YEARS

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

24

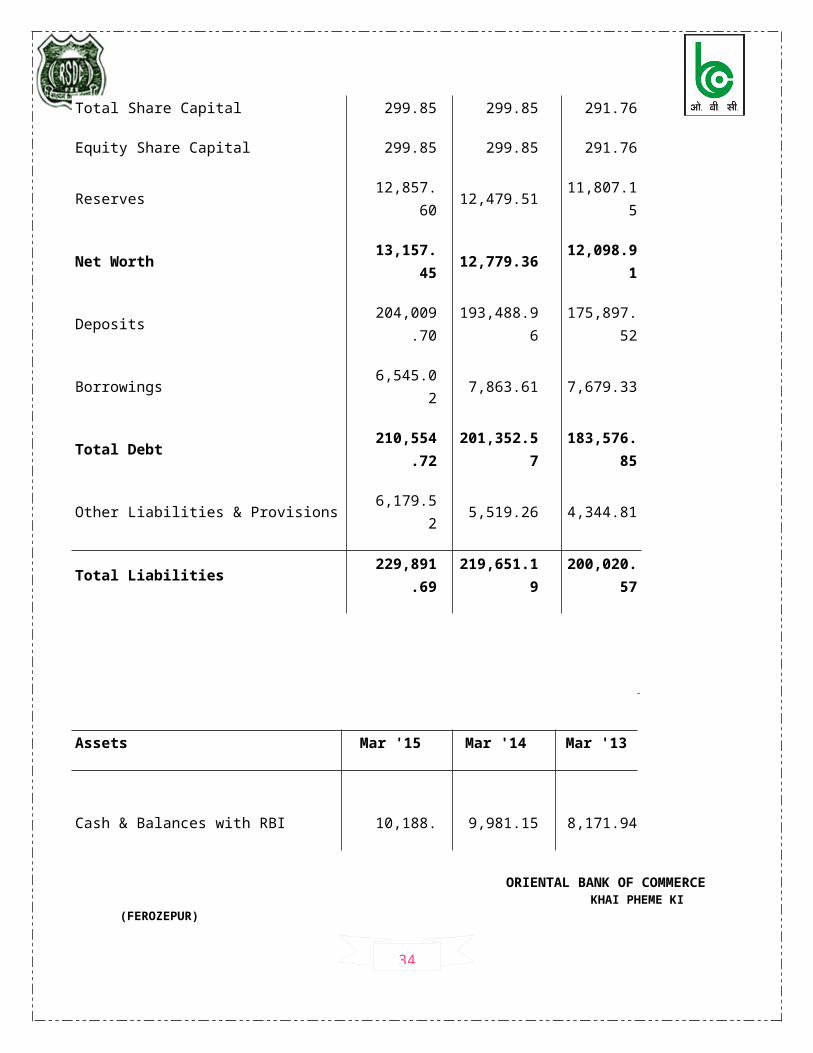

Balance Sheet of Oriental Bank of Commerce

-------------- in Rs. Cr. -------------------

Mar '15 Mar '14 Mar '13

12 months 12 mths 12 mths

Capital and Liabilities:

Total Share Capital 299.85 299.85 291.76

Equity Share Capital 299.85 299.85 291.76

Reserves 12,857.60 12,479.51 11,807.15

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

25

Net Worth 13,157.45 12,779.36 12,098.91

Deposits 204,009.70 193,488.96 175,897.52

Borrowings 6,545.02 7,863.61 7,679.33

Total Debt 210,554.72 201,352.57 183,576.85

Other Liabilities & Provisions 6,179.52 5,519.26 4,344.81

Total Liabilities 229,891.69 219,651.19 200,020.57

Assets Mar '15 Mar '14 Mar '13

Cash & Balances with RBI 10,188.38 9,981.15 8,171.94

Balance with Banks, Money at Call 587.42 4,287.77 417.68

Advances 145,261.30 139,079.84 128,955.06

Investments 68,440.45 61,472.23 58,554.66

Gross Block 1,342.38 1,224.23 1,210.50

Revaluation Reserves 621.90 651.32 676.63

Accumulated Depreciation 0.00 0.00 0.00

Net Block 720.48 572.91 533.87

Capital Work In Progress 10.15 31.34 16.91

Other Assets 4,683.49 4,225.94 3,370.45

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

26

Total Assets 229,891.67 219,651.18 200,020.57

Contingent Liabilities 61,103.01 79,547.15 93,198.91

Bills for collection 0.00 0.00 0.00

Book Value (Rs) 438.80 426.19 414.69

OBC BANK CASH FLOW STATEMENT FOR LAST 3 YEARS

Cash Flow of Oriental Bank of Commerce

----------- in Rs. Cr. ------------

Mar '15 Mar '14 Mar '13

12 mths 12 mths 12 mths

Net Profit Before Tax 497.08 1139.41 1327.95

Net Cash From Operating Activities -4154.05 6520.45 -496.16

Net Cash (used in)/fromInvesting Activities

-295.23 -167.69 -89.43

Net Cash (used in)/from Financing Activities 956.17 -673.45 448.25

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

27

Net (decrease)/increase In Cash and Cash Equivalents

-3493.11 5679.30 -137.33

Opening Cash & Cash Equivalents 14268.92 8589.62 8726.95

Closing Cash & Cash Equivalents 10775.81 14268.92 8589.62

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

28

Chapter-2

BRANCH PROFILE

INTRODUCTION OF BRANCH INTRODUCTION OF PMJDY PURPOSE OF PMJDY PERFORMANCE OF PMJDY CRITICISM OF PMJDY

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

29

INTRODUCTION OF BRANCH

ORIENTAL BANK OF COMMERCE - KHAI PHEME KE is located in PUNJAB state, FEROZEPUR district. This branch is firstly located in village MEHMA but after the terrorist attack this branch was transfer to KHAI PHEME KE IN 1980 .There are 7 staff members and a branch manager in the branch. This branch provides many services like:-

Speed clearing, ATM service, SMS Banking, Mobile Banking, Fund Transfer, Housing/Education/Vehicle Loans, Locker facility, Bill Payment, Internet banking, e-KYC

The IFSC Code is ORBC0100497. Branch code is the last six characters of the IFSC Code - 100497.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

30

NEW SCHEMES LAUNCH BY PRIME MINISTER OF INDIA IN BANKING SECTOR

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

31

PRADHAN MANTRI JHAN DHAN YOJNA (PMJDY)

Pradhan Mantri Jan Dhan Yojana (PMJDY) is National Mission for Financial Inclusion to ensure access to financial services, namely Banking Savings & Deposit Accounts, Remittance, Credit, Insurance, Pension in an affordable manner. This financial inclusion campaign was launched by the Prime Minister of India, on 28 August 2014. He had announced this scheme on his first Independence Day speech on 15 August 2014.

Purpose: -

In a run up to the formal launch of this scheme, the Prime Minister personally mailed to Chairman’s of all PSU banks to gear up for the gigantic task of enrolling over 7.5 crore (75 million) households and to open their accounts. In this email he categorically declared that a bank account for each household was a "national priority".

The scheme has been started with a target to provide 'universal access to banking facilities' starting with "Basic Banking Accounts" with overdraft facility of Rs.5000 after six months and RuPay Debit card with inbuilt accident insurance cover of Rs. 1 lakh and RuPay Kisan Card. In next phase, micro insurance & pension etc. will also be added.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

32

Under the scheme:

1) Account holders will be provided zero-balance bank account with RuPay debit card, in addition to accidental insurance cover of Rs 1 lakh (to be given by 'HDFC Ergo').

2) Those who open accounts by January 26, 2015 over and above the 1 lakh accident, they will be given life insurance cover of 30,000(to be given by LIC).

3) After Six months of opening of the bank account, holders can avail 5,000 overdrafts from the bank.

4) With the introduction of new technology introduced by National Payments Corporation of India (NPCI), a person can transfer funds, check balance through a normal phone which was earlier limited only to smart phones so far.

5) Mobile banking for the poor would be available through National Unified USSD Platform (NUUP) for which all banks and mobile companies have come together.

Performance:-

Due to the preparations done in the run-up, as mentioned above, on the inauguration day, 1.5 Crore (15 million) bank accounts were opened. The Prime Minister said on this occasion- "Let us celebrate today as the day of financial freedom." By September 2014, 3.02 crore accounts were opened under the scheme, amongst Public sector banks, SBI had opened 30 lakh (3 million) accounts, followed by Punjab National Bank with 20.24 lakh (2 million) accounts, Canara Bank 16.21 lakh (1.62 million) accounts, Central Bank of India 15.98 lakh (1.59 million) accounts and Bank of Baroda with 14.22 lakh (1.42 million) accounts. It was reported that total of 7 Crore (70 million) bank accounts have been opened with deposits totaling more than 5000 crore Rupees (approx 1 billion USD) as of November 6, 2014.

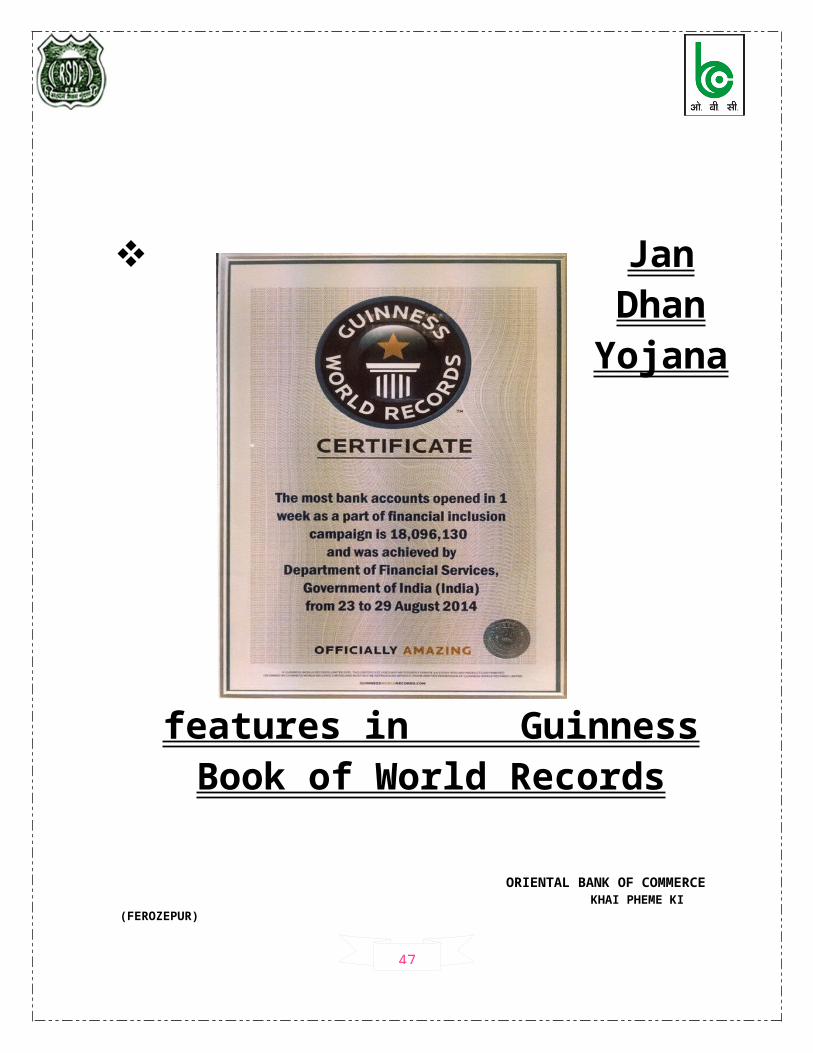

As the government met the target, Union Finance Minister Arun Jaitley has revised the target for opening of bank accounts under the Pradhan Mantri Jan Dhan Yojana (PMJDY), the ambitious financial inclusion scheme launched by the government, from 7.5 crore to 10 crore by January 26, 2015. On 20th January 2015, the scheme entered into Guinness book of world records setting new record for 'The most bank accounts opened in one week'.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

33

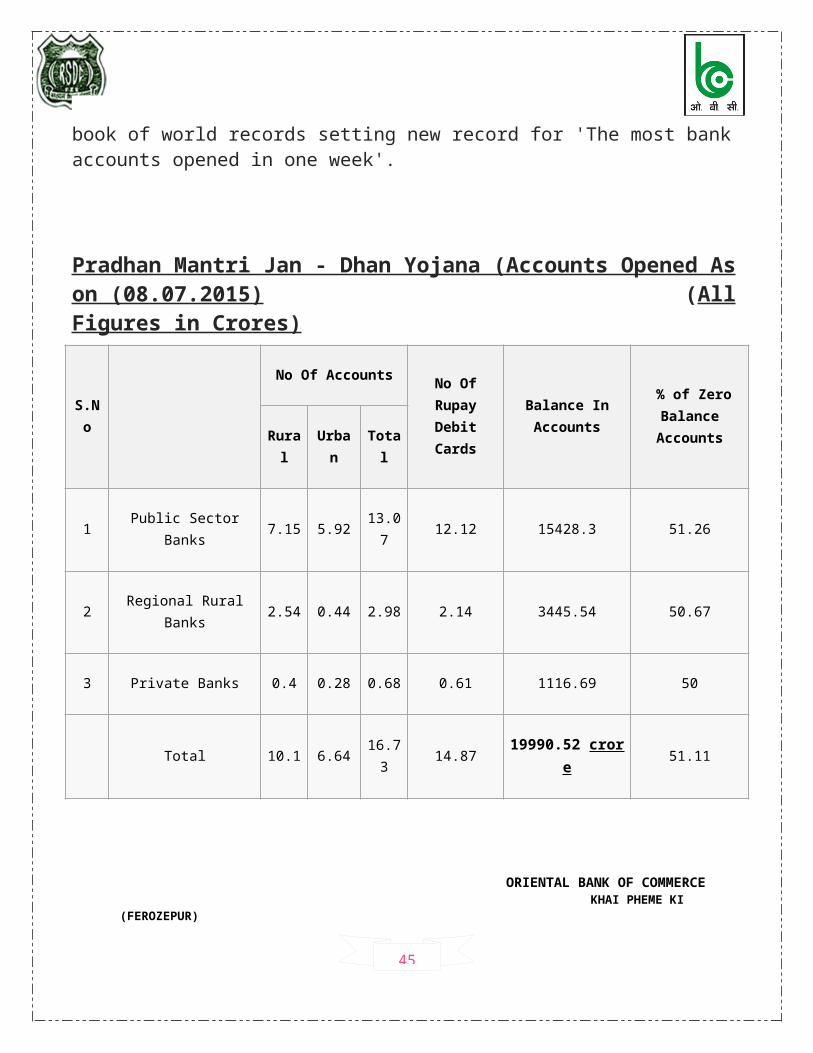

Pradhan Mantri Jan - Dhan Yojana (Accounts Opened As on (08.07.2015) (All Figures in Crores)

S.No

No Of AccountsNo Of Rupay Debit Cards

Balance In Accounts

% of Zero Balance

AccountsRural

Urban

Total

1 Public Sector Banks 7.15 5.9213.0

712.12 15428.3 51.26

2Regional Rural

Banks2.54 0.44 2.98 2.14 3445.54 50.67

3 Private Banks 0.4 0.28 0.68 0.61 1116.69 50

Total 10.1 6.6416.7

314.87

19990.52 crore

51.11

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

34

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

35

Jan Dhan Yojana features in Guinness Book of World Records

"Most of India today is included in the banking system," finance minister Arun Jaitley told reporters on Tuesday. The Pradhan Mantri Jan-Dhan Yojana (PMJDY), launched by Prime Minister Narendra Modi in August, was recognised for opening the most bank accounts—about 1.80 crore— in one week as part of the financial inclusion campaign.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

36

The government has already rolled out direct transfer of benefits for various programs. This includes the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) in 300 districts that's expected to cover 4.3 crore beneficiaries with a fund flow of Rs 15,000 crore annually besides transfers under various pension and scholarship schemes.

"Full rollout will take total beneficiaries under MGNREGS up to 10 crore with Rs 33,000 crore funds flow annually," said financial services secretary Hasmukh Adhia.

Apart from transfers worth Rs 51,029 crore under various welfare schemes and rural jobs program, cooking gas subsidies are also being transferred to 15.34 active consumers. This is part of the plan to link it with bank accounts under a modified direct benefit transfer for LPG from January 1. The government has already disbursed Rs 6,688.98 crore to 8.03 crore LPG customers up to January 14 and the figure could go up to Rs 25,000-Rs 30,000 crore annually.

The government has rolled out 34 welfare schemes on the direct benefits transfer (DBT) platform with around 9.90 crore beneficiaries, including the partial linking of benefits under the rural jobs scheme.

The number of accounts opened under PMJDY stood at 11.5 crore as of January 17 after a survey of 21.02 crore households. Of total bank accounts opened, 3.23 crore have deposits worth Rs 9,188 crore.Rupay cards have been issued to more than 10 crore beneficiaries. "This is an unprecedented initiative. Bank employees have physically visited all households except the inaccessible areas," said Jaitley, adding that the government has far exceeded its target and will decide later on whether to continue with the incentives given to customers on opening a bank account.

The finance minister said the idea was to move to cash-less society in the long run. The overdraft facility under the scheme will act as a micro financing platform with no exploitative interest rates.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

37

According to reports, 16.73 crore accounts were opened by banks across the country as of January 16. Of this, 8.24 crore account are zero balance.Public sector banks alone opened 13.07 crore accounts, followed by regional rural banks which opened about 2.98 crore accounts. 13 private sector banks together open just 68 lakh accounts.

Criticism:-

The scheme has been criticized by many experts from the banking sector as an effort to please voters that has created unnecessary work-burden on the public-sector banks. The opposition party Congress alleged that Mr Modi was trying to take credit of the financial inclusion scheme started by UPA government and the new yojana had got nothing new.

According to the experts, temptations presented by the Prime Minister like zero balance, free insurance and overdraft facility would result in duplication. Many individuals who

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

38

already have bank accounts may have had accounts created for themselves, lured by the insurance covers and overdraft facilities. As per the scheme, a very few people are eligible to get the life insurance worth 30,000 with a validity of just five years. However, these 'secret' conditions were not shown in the TV advertisements of the scheme. The claimed overdraft facility has been completely left upon the banks. As per the government notice, only those people would get the overdraft facility whose transaction record is satisfactory as per the banks. It is quite unlikely that many people would get this facility as the banks would avoid potential NPAs. The claimed accidental insurance has also proved to be a non-existing scheme as the Rupay card holders have got no legal paper for any such accidental insurance.

Chapter-3

RESEARCH METHODOLOGY

NEED, OBJECTIVE, SCOPE SAMPLE DESIGN METHOD OF DATA COLLECTION CONDUCTING SURVEY KNOWLEDGE SHARING

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

39

Need of the study

Whether those who could not get banking facility earlier have got it now after announcement of PMJDY.

Whether all eligible and desirous have been able to established banking relationship with bank in the village.

Having opened the account, whether all of them have met the criteria of getting Life Insurance, Personal Accident cover And Rupay card.

Rational objectives of the study

To identify level of awareness on PMJDY among resident of village Khai Pheme Ki, District Ferozepur, Punjab.

To identify the level of usage of benefits arising out of PMJDY.

Scope of the study

The target group includes unemployed people, house wife, and people engaged in small business in village.

The target groups are people residing in village Khai Pheme Ki, District Ferozepur, Punjab.

Banking habits and awareness about financial product and services come with preview of study.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

40

RESEARCH METHODOLOGY

The project aims at understand the level of awareness and achievement of RBI and Govt. of INDIA efforts in achieving the dreams target financial inclusion. The survey was conducted among 50 residents of village Khai Pheme ki, District Ferozepur, Punjab.

SAMPLE DESIGN:-

Target population:- The target audience includes the residents of village Khai Pheme Ki, Distict Ferozepur , Punjab

Sample Size: - The sample size for the research is 50 residents. Sample Method:- The sample method included conducting a survey with resident

either through personal interaction. Convenience sampling technique was adopted.

METHOD OF DATA COLLECTION:-

The method included preparing a questionnaire with question mainly related to awareness of basic banking. The process included visiting the village and generating information about their facilities they are using.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

41

The meeting was done as per the preference of the resident it was done in the following two ways:-

1) Personal interaction: - This method was most preferred as it results in increase in knowledge of both the parties and adds a personal touch, which is not present in telephonic interaction.

2) Telephonic interaction:- This method was less preferred, as it didn’t gave an idea as who is responding to the questions, it was like blindly trusting the respondent about his identity.

CONDUCTING SURVEY:-

The survey was conducted with the help of questionnaire. It was either filled by me or by the respondents. In 55% cases the respondent was unable to fill the questionnaire in his/her writing.

KNOWLEDGE SHARING:-

A person learns throughout his life, so keeping this in mind, knowledge was shared both ways. I learnt the problem of respondents, the way they work and I created awareness about PMJDY.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

42

Chapter-4

DATA ANALYSIS & INTERPRETATION

ANALYSIS & INTERPRETATION FINDINGS LIMITATIONS SUGGESTIONS

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

43

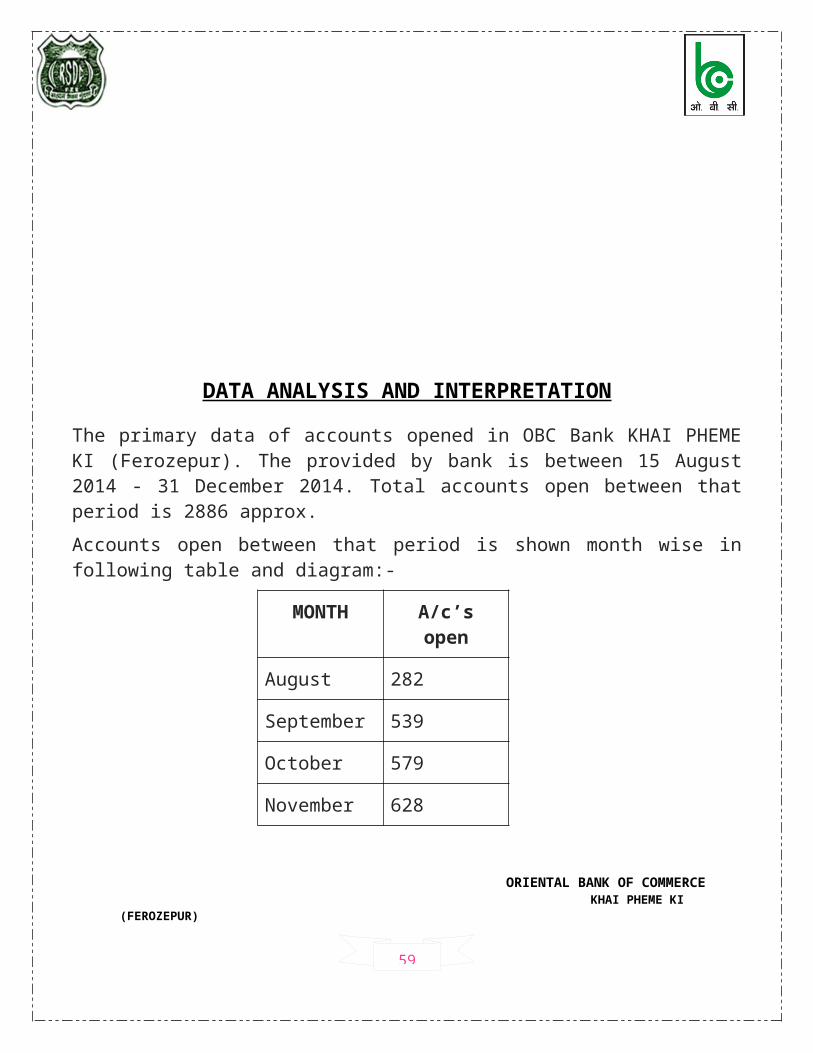

DATA ANALYSIS AND INTERPRETATION

The primary data of accounts opened in OBC Bank KHAI PHEME KI (Ferozepur). The provided by bank is between 15 August 2014 - 31 December 2014. Total accounts open between that period is 2886 approx.

Accounts open between that period is shown month wise in following table and diagram:-

MONTH A/c’s open

August 282

September 539

October 579

November 628

December 858

Augus

t

Decem

ber

0

400

800

A/c's opened under Pardhan Mantri Jhan Dhan Yojana in OBC

Bank KHAI PHEME KI (Fer-ozepur)A/c's opened under

Pardhan Mantri Jhan Dhan Yojana in OBC Bank KHAI PHEME KI (Ferozepur)

Polynomial (A/c's opened under Pardhan Mantri Jhan Dhan Yojana in OBC Bank KHAI PHEME KI (Ferozepur))

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

44

Q1). For how long you have been staying in this village?

a). Less than a year b). 1 to 5 years c). More than 5 years

2

10

38

how long you have been staying in this village

Less than a year 1 to 5 yearsMore than 5 years

ANALYIS

According to the given information from secondary sources it was conclude that 76% people in the village are staying more than 5 years in the village .

Q2). Whether your family is Joint or Nuclear family?

a). Joint family b). Nuclear Family

02040

1436

Families

Family

ANALYIS

From the survey, I get that most of the families are nuclear family.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

45

Q3). Does any one in your family have bank account?

a). Yes b). No

Yes No0

10

20

30

40

50

Bank account

bank account

ANALYIS

According the secondary data most of the people in the village have their bank a/c.

Q3.1) No of account in your family?

i) 1 iii) 3 ii) 2 iv) more than 3

2711

43

Bank a/c

123more than 3

ANALYIS

From the above pie chart we get that 60%people have one bank a\c and 25% have 2 bank a/c in family and rest have 3 or more than 3 bank a/c.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

46

Q3.2) which type of account do you have?

i) Saving a/c iii) Fixed deposit a/c

ii) Current a/c iv) Recurring deposit a/c

0102030

33

7 3 3

Account type

Account type

ANALYIS

According to secondary data, the most of the accounts in the village are saving account. Only few people have current a/c as well as other two accounts.

Q3.3) what were the reasons that your family opened the account?

i) To receive government payments from NREGA

ii) To receive government payments from scheme other than NREGA

iii) For saving

iv) To request a loan

v) If other , please specify _______________________________

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

47

12

5

21

52

Reasons that your family opened the account

To receive government payments from NREGA

To receive government payments from scheme other than NREGA

For saving

To request a loan

Other reason

ANALYIS

From the above chart it is clear that 47% people open account for saving , 27% open for payment from NREGA and 11% open for other schemes and loan request each and 4% have some other reason .

Q3.4) who helped you while opening the account?

i) Village panchayat official

ii) Bank official

iii) Neighbors/Friends/Relatives/Employer

iv) Business correspondent/Post office

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

48

Villag

e pa

ncha

yat o

fficial

Bank

official

Neigh

bors

/Frie

nds/Rel

atives

Busines

s co

rres

pond

ent/P

ost offi

ce

048

1216

Who helped you while opening the account

Who helped you while open-ing the account

ANALYSIS

According to secondary data, most of the accounts are opened with the help of Bank Official and after that village panchayat helped to open.

Q4). Reason for not having even a single bank account in your family?

A). Very little money to put in

B). No banking facilities in area

C). Lengthy procedures

D). Many charges are there

E). Tried to open but was refused

F). other (please specify) _______________

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

49

06

1218 14

05 7

19

0

Reason for not having even a single bank account in your fam-

ily

Reason for not having even a single bank account in your fam-ily

ANALYSIS

After the survey we get that people in the village tried to open the account but their was refusal by bank due to not fulfillment of KYC norms of the person who want to open the account and people in the village also have very liitle money and they don’t want any charges on that money also.

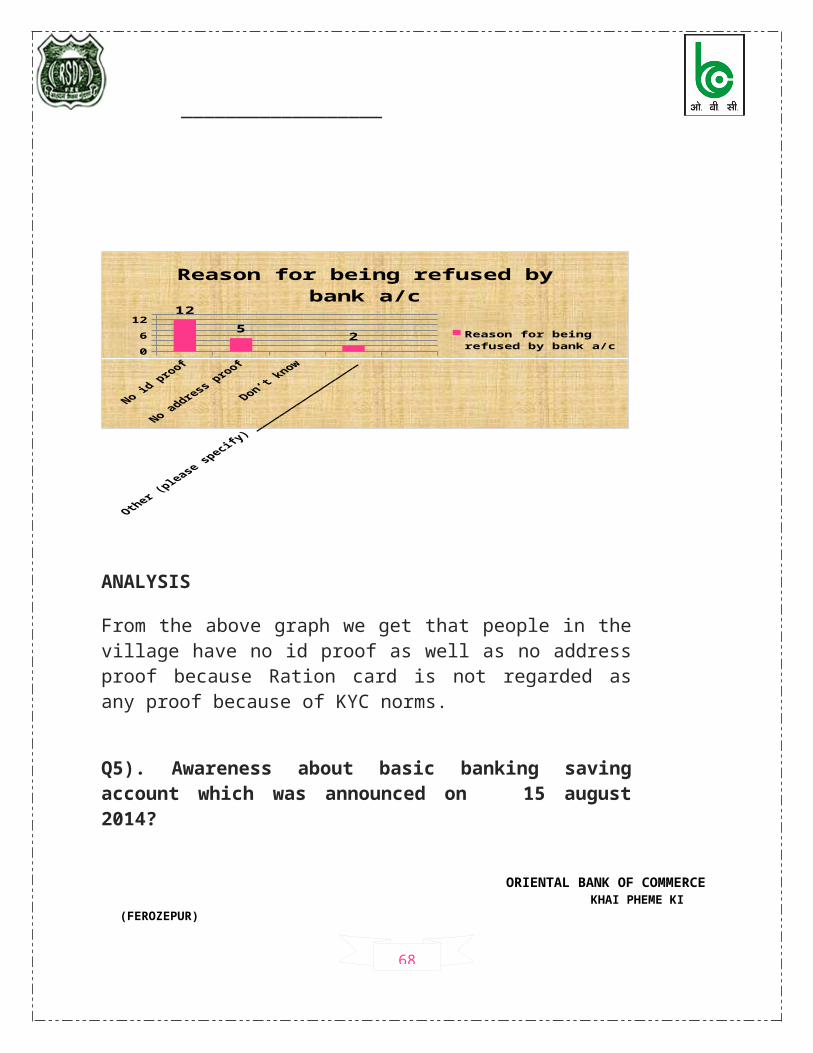

Q4.1) Reason for being refused by bank a/c?

i) No id proofii) No address proofiii) Don’t knowiv) Other (please specify) __________________

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

50

048

1212

52

Reason for being refused by bank a/c

Reason for being refused by bank a/c

ANALYSIS

From the above graph we get that people in the village have no id proof as well as no address proof because Ration card is not regarded as any proof because of KYC norms.

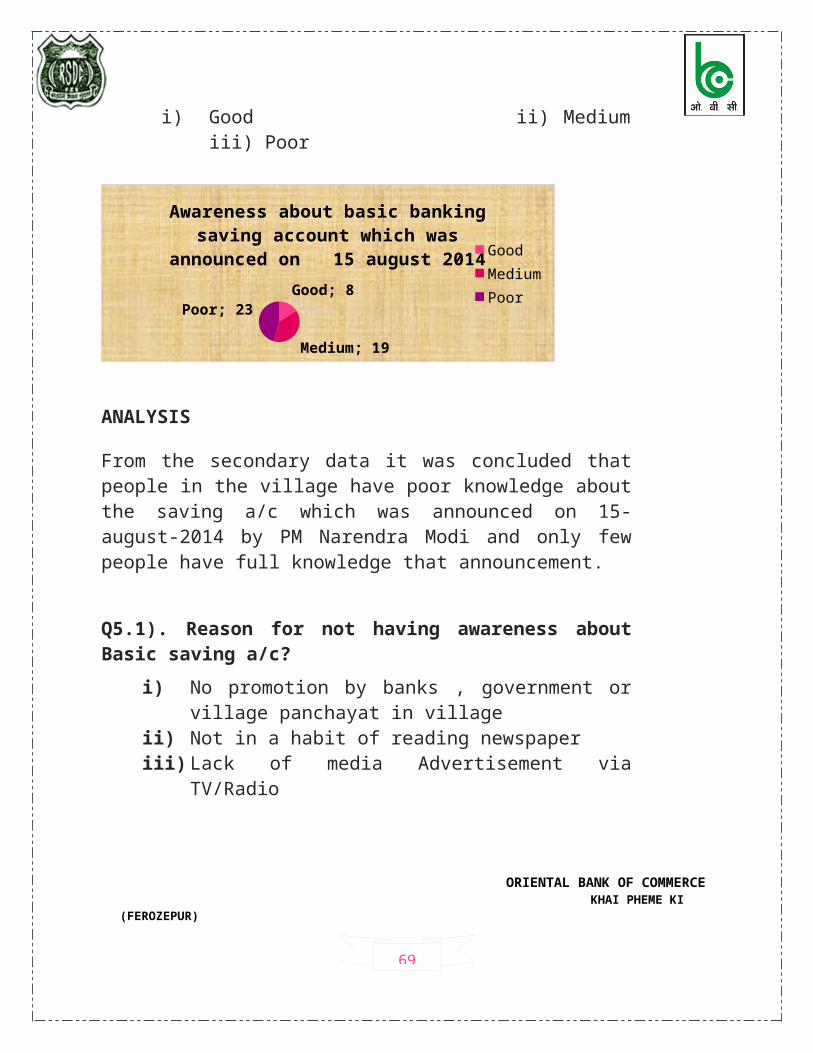

Q5). Awareness about basic banking saving account which was announced on 15 august 2014?

i) Good ii) Medium iii) Poor

Good; 8

Medium; 19

Poor; 23

Awareness about basic banking saving account which was an-nounced on 15 august 2014 Good

Medium

Poor

ANALYSIS

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

51

From the secondary data it was concluded that people in the village have poor knowledge about the saving a/c which was announced on 15-august-2014 by PM Narendra Modi and only few people have full knowledge that announcement.

Q5.1). Reason for not having awareness about Basic saving a/c?

i) No promotion by banks , government or village panchayat in village

ii) Not in a habit of reading newspaperiii) Lack of media Advertisement via TV/Radio

06

1218

0

17

6

Reason for not having awareness about Basic sav-

ing a/c

Reason for not hav-ing awareness about Basic saving a/c

ANALYSIS

From the graph we get that people in the village have not habit of reading news paper and there is also some lack of media advertisement also.

Q6) Are you aware about the various facilities covered under PMJDY like :-

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

52

(I- Overdraft facility of 5,ooo, II – Life insurance cover, III – Personal accident cover , VI- Rupay card )

i) Yesii) No

34%

66%

Are you aware about the various facilities

covered under PMJDY YesNo

ANALYSIS

According to secondary data 34% people in the village are aware about the PMJDY, they don’t know about Overdraft facility of 5,ooo , Life insurance cover , Personal accident cover , Rupay card facilities under PMJDY.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

53

FINDINGS

Through survey following things have been find out:-

Out of 50 household 5 families don’t have bank a/c. Majority of the people open bank account in order to save money i.e. 33 people

have saving a/c and 12 people open a/c to receive payment from NREGA. Bank officials are doing there level best so most of the accounts are opened by

them and after that village pancahyat help them to open. People in the village tried to open the account but they don’t have valid proofs to

open the account. They also have very little money to put in so they avoid opening the a/c.

People in the village are also not aware of PMJDY which was inaugurated by Narendra Modi on 15-august-2014 due to lack advertising and people have not habit of reading the newspaper.

They are also not aware about the facilities covered under PMJD only 34% people are fully aware about those facilities.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

54

Limitations of the study

There is shortage of time to conduct the study. Due to shortage of time smaller sample size has been taken which may not be true representative of whole universe.

Due to time constraint, it was not possible to observe every aspect of financial inclusion program.

Due to conservative nature, it may be possible some respondents may not have their responses in the questionnaire in fully true manner.

Since the respondents may be busy with busy schedule so many people may be reluctant to answer.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

55

SUGGESTIONS

Some suggestions regarding the research are as follows:-

Promote financial product and services:- Reserve bank and government bank should give the suggestion to commercial bank to promote the financial product and services of banking through all the educational institution.

Develop financial literacy: - The government of India should help to develop financial literacy among the population, particularly in low income families. That can be done by teaching it in Primary school, High school, and collage.

Telecom companies:- Telecom companies should be allowed to provide payments and money transfer services.

Add extra incentives to lend in rural area:- The RBI should mandate the commercial banks have a certain percentage of their portfolio in small loans. The children have to attend the school before they are eligible for loan. Similar some conditions have been imposed for eligibility of loan in INDIA. The government could also add some extra incentives to lend in rural area.

Encourage people to access banking services: - The bank should step up to over whelm all these problems and to disseminate its services to remote area. The bank should encourage the people to access banking services by way of no frill account.

Directing government benefits through service area bank:- Any government or social security payments or payments under all the govt. schemes should be strictly routed through the service area bank account.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

56

Chapter-5

ATAL PENSION YOJANA

DETAIL OF SCHEME

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

57

ATAL PENSION YOJANA

Details of the Scheme:-

1. Introduction:-

The Government of India is extremely concerned about the old age income security of the working poor and is focused on encouraging and enabling them to join the National Pension System (NPS). To address the longevity risks among the workers in unorganized sector and to encourage the workers in unorganized sector to voluntarily save for their retirement, who constitute 88% of the total la bour force of 47.29 crore as per the 66th Round of NSSO Survey of 2011-12, but do not have any formal pension provision, the Government had started the Swavalamban Scheme in 2010-11. However, coverage under Swavalamban Scheme is inadequate mainly due to lack of guaranteed pension benefits at the age of 60.

The Government announced the introduction of universal social security schemes in the Insurance and Pension sectors for all Indians, specially the poor and the under-privileged, in the Budget for the year 2015-16. Therefore, it has been announced that the Government will launch the Atal Pension Yojana (APY), which will provide a defined pension, depending on the contribution, and its period. The APY will be focused on all citizens in the unorganized sector, who join the National Pension System (NPS) administered by the Pension Fund Regulatory and Development Authority (PFRDA). Under the APY, the subscribers would receive the fixed minimum pension of Rs. 1000 per month, Rs. 2000 per month, Rs. 3000 per month, Rs. 4000 per month, Rs. 5000 per month, at the age of 60 years, depending on their contributions, which itself would be based on the age of joining ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

58

the APY. The minimum age of joining APY is 18 years and maximum age is 40 years. Therefore, minimum period of contribution by any subscriber under APY would be 20 years or more. The benefit of fixed minimum pension would be guaranteed by the Government. The APY would be introduced from 1st June, 2015.

2. Benefit of APY:-

Fixed pension for the subscribers ranging between Rs. 1000 to Rs. 5000, if he joins and contributes between the age of 18 years and 40 years. The contribution levels would vary and would be low if subscriber joins early and increase if he joins late.

3. Eligibility for APY:-

Atal Pension Yojana (APY) is open to all bank account holders. The Central Government would also co-contribute 50% of the total contribution or Rs. 1000 per annum, whichever is lower, to each eligible subscriber account, for a period of 5 years, i.e., from Financial Year 2015-16 to 2019-20, who join the NPS between the period 1st June, 2015 and 31st December, 2015 and who are not members of any statutory social security scheme and who are not income tax payers. However the scheme will continue after this date but Government Co-contribution will not be available.

The Government co-contribution is payable to eligible PRANs by PFRDA after receiving the confirmation from Central Record Keeping Agency at such periodicity as may be decided by PFRDA.

4. Age of joining and contribution period:-

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

59

The minimum age of joining APY is 18 years and maximum age is 40 years. The age of exit and start of pension would be 60 years. Therefore, minimum period of contribution by the subscriber under APY would be 20 years or more.

5. Focus of APY:-

Mainly targeted at unorganized sector workers.

6. Enrolment and Subscriber Payment:-

All bank account holders under the eligible category may join APY with auto debit facility to accounts, leading to reduction in contribution collection charges. The subscribers should keep the required balance in their savings bank accounts on the stipulated due dates to avoid any late payment penalty. Due dates for monthly contribution payment is arrived based on the deposit of first contribution amount. In case of repeated defaults for specified period, the account is liable for foreclosure and the GoI co-contributions, if any shall be forfeited. Also any false declaration about his/her eligibility for benefits under this scheme for whatsoever reason, the entire government contribution shall be forfeited along with the penal interest. For enrolment, Aadhaar would be the primary KYC document for identification of beneficiaries, spouse and nominees to avoid pension rights and entitlement related disputes in the long-term. The subscribers are required to opt for a monthly pension from Rs. 1000 - Rs. 5000 and ensure payment of stipulated monthly contribution regularly. The subscribers can opt to decrease or increase pension amount during the course of accumulation phase, as per the available monthly pension amounts. However, the switching option shall be provided once in year during the month of April. Each subscriber will be provided with an acknowledgement slip after joining APY which would invariably record the guaranteed pension amount, due date of contribution payment, PRAN etc.

7. Enrolment agencies:-

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

60

All Points of Presence (Service Providers) and Aggregators under Swavalamban Scheme would enroll subscribers through architecture of National Pension System. The banks, as POP or aggregators, may employ BCs/Existing non - banking aggregators, micro insurance agents, and mutual fund agents as enablers for operational activities. The banks may share the incentives received by them from PFRDA/Government, as deemed appropriate.

8. Operational Framework of APY:-

It is Government of India Scheme, which is administered by the Pension Fund Regulatory and Development Authority. The Institutional Architecture of NPS would be utilized to enroll subscribers under APY. The offer document of APY including the account opening form would be formulated by PFRDA.

9. Funding of APY:-

Government would provide (i) fixed pension guarantee for the subscribers; (ii) would co-contribute 50% of the total contribution or Rs. 1000 per annum, whichever is lower, to eligible subscribers; and (iii) would also reimburse the promotional and development activities including incentive to the contribution collection agencies to encourage people to join the APY.

10. Migration of existing subscribers of Swavalamban Scheme to APY:-

The existing Swavalamban subscriber, if eligible, may be automatically migrated to APY with an option to opt out. However, the benefit of five years of government Co-contribution under APY would not exceed 5 years for all subscribers. This would imply that if, as a Swavalamban beneficiary, he has received the benefit of government Co-Contribution of 1 year, then the Government co-contribution under APY would be available only 4 years and so on. Existing Swavalamban beneficiaries opting out from the proposed APY will be given Government co-contribution till 2016- 17, if eligible, and the NPS Swavalamban continued till such people attained the age of exit under that scheme.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

61

The existing Swavalamban subscribers between 18-40 years will be automatically migrated to APY. For seamless migration to the new scheme, the associated aggregator will facilitate those subscribers for completing the process of migration. Those subscribers may also approach the nearest authorised bank branch for shifting their Swavalamban account into APY with PRAN details.

The Swavalamban subscribers who are beyond the age of 40 and do not wish to continue may opt out the Swavalamban scheme by complete withdrawal of entire amount in lump sum, or may prefer to continue till 60 years to be eligible for annuities there under.

11. Penalty for default:-

Under APY, the individual subscribers shall have an option to make the contribution on a monthly basis. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Rs. 1 per month to Rs 10/- per month as shown below:

o Rs. 1 per month for contribution upto Rs. 100 per month. o Rs. 2 per month for contribution upto Rs. 101 to 500/- per month.o Rs. 5 per month for contribution between Rs 501/- to 1000/- per month. o Rs. 10 per month for contribution beyond Rs 1001/- per month. The

fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Discontinuation of payments of contribution amount shall lead to following:

o After 6 months account will be frozen. o After 12 months account will be deactivated. o After 24 months account will be closed.

12. Operation of additional amount for delayed payments:-

APY module will raise demand on the due date and continue to raise demand till the amount is recovered from the subscriber’s account.

The due date for recovery of monthly contribution may be treated as the first day /or any other day during the calendar month for each subscriber. Bank can recover ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

62

amount any day till the last day of the month. It will imply that contribution are recovered as and when funds are available any point during the month.

Monthly contribution will be recovered on FIFO basis- earliest due installment will recovered first along with the fixed amount of charges as mentioned above.

More than one monthly contribution can be recovered in month subject to availability of the funds. Monthly contribution will be recovered along with the monthly fixed due amount, if any. In all cases, the contribution is to be recovered along with the fixed charges. This will be banks’ internal process. The due amount will be recovered as and when funds are available in the account.

13. Investment of the contributions under APY:-

The amount collected under APY are managed by Pension Funds appointed by PFRDA as per the investment pattern specified by the Government. The subscriber has no option to choose either the investment pattern or Pension Fund.

14. Continuous Information Alerts to Subscribers:-

Periodical information to the subscribers regarding balance in the account, contribution credits etc. will be intimated to APY subscribers by way of SMS alerts. The subscribers will have the option to change the non – financial details like nominee’s name, address, phone number etc whenever required.

All subscribers under APY remain connected on their mobile so that timely SMS alerts can be provided to them at the time of making their subscription, autodebit of their accounts and the balance in their accounts.

15. Exit and pension payment:-

Upon completion of 60 years, the subscribers will submit the request to the associated bank for drawing the guaranteed monthly pension.

Exit before 60 years of age is not permitted, however, it is permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

63

16. Age of Joining, Contribution Levels, Fixed Monthly Pension and Return of Corpus to the nominee of subscribers:-

The Table of contribution levels, fixed minimum monthly pension to subscribers and his spouse and return of corpus to nominees of subscribers and the contribution period is given below. For example, to get a fixed monthly pension between Rs. 1,000 per month and Rs. 5,000 per month, the subscriber has to contribute on monthly basis between Rs. 42 and Rs. 210, if he joins at the age of 18 years. For the same fixed pension levels, the contribution would range between Rs. 291 and Rs. 1,454, if the subscriber joins at the age of 40 years.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

64

Table of contribution levels, fixed monthly pension of Rs. 1,000 per month to subscribers and his spouse and return of corpus to nominees of subscribers and the contribution period under Atal Pension Yojana.

Table of contribution levels, fixed monthly pension of Rs. 2,000 per month to subscribers and his spouse and return of corpus to nominees of subscribers and the contribution period under Atal Pension Yojana.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

65

Table of contribution levels, fixed monthly pension of Rs. 3,000 per month to subscribers and his spouse and return of corpus to nominees of subscribers And the contribution period under Atal Pension Yojana.

Table of contribution levels, fixed monthly pension of Rs. 4,000 per month to subscribers and his spouse and return of corpus to nominees of subscribers and the contribution period under Atal Pension Yojana.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

66

Table of contribution levels, fixed monthly pension of Rs. 5,000 per month to subscribers and his spouse and return of corpus to nominees of subscribers and the contribution period under Atal Pension Yojana.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

67

Chapter-6

PARDHAN MANTRI JEEVAN JYOTI BIMA YOJANA AND PARDHAN MANTRI SURAKSHA BIMA YOJANA

OVERVIEW OF PMJJBY CRITICISM OF PMJJBY DATA ANALYSIS OVERVIEW OF PMSBY CRITICISM OF PMSBY DATA ANALYSIS

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

68

Pradhan Mantri Jeevan Jyoti Bima Yojna

Pradhan Mantri Jeevan Jyoti Bima Yojana is a government-backed Life insurance scheme in India. It was originally mentioned in the 2015 Budget speech by Finance Minister Arun Jaitley in February 2015. It was formally launched by Prime Minister Narendra Modi on 9 May in Kolkata. As of May 2015, only 20% of India's population has any kind of insurance, this scheme aims to increase the number.

OVERVIEW:-

Pradhan Mantri Jeevan Jyoti Bima Yojana is available to people between 18 and 50 years of age with bank accounts. It has an annual premium of 300 excluding service tax, which is above 14% of the premium. The amount will be automatically debited from the account. In case of death due to any cause, the payment to the nominee will be 200,000.

This scheme will be linked to the bank accounts opened under the Pradhan Mantri Jan Dhan Yojana scheme. Most of these account had zero balance initially. The government aims to reduce the number of such zero balance accounts by using this and related schemes.

Criticism:-

The banks have complained that revenue received will be very low. Some bankers have claimed that amount they are receiving is not sufficient to cover the service costs. Since, this a group insurance scheme, banks have not received instruction regarding cases where excessive claims are in a year. Insurers have also pointed out that no health certificate or information of pre-existing disease is required for joining.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

69

DATA ANALYSIS

The primary data of Pradhan Mantri Suraksha Bima Yojana in OBC Bank KHAI PHEME KI (Ferozepur) . The provided by bank is between 9-May-2015 to 18-July-2015. Total accounts open between that period is 1336 approx.

No. of Insurance policy done between that period is shown month wise in following table and diagram:- Months May June JulyNo. of Insurance 357 438 541

May June July0

100

200

300

400

500

600

357438

541

No. of Insurance

No. of Insurance

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

70

Pradhan Mantri Suraksha Bima Yojna

Pradhan Mantri Suraksha Bima Yojana is a government-backed accident insurance scheme in India. It was originally mentioned in the 2015 Budget speech by Finance Minister Arun Jaitley in February 2015. It was formally launched by Prime Minister Narendra Modi on 9 May in Kolkata. As of May 2015, only 20% of India's population has any kind of insurance, this scheme aims to increase the number.

OVERVIEW :-

Pradhan Mantri Suraksha Bima Yojana is available to people between 18 and 70 years of age with bank accounts. It has an annual premium of 12 excluding service tax, which is about 14% of the premium. The amount will be automatically debited from the account. In case of accidental death or full disability, the payment to the nominee will be 200,000 and in case of partial disability 100,000. Full disability has been defined as loss of use in both eyes, hands or feet. Partial disability has been defined as loss of use in one eye, hand or foot.

This scheme will be linked to the bank accounts opened under the Pradhan Mantri Jan Dhan Yojana scheme. Most of these account had zero balance initially. The government aims to reduce the number of such zero balance accounts by using this and related schemes.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

71

Criticism:-

The banks have complained that revenue received will be very low. Some bankers have claimed that amount they are receiving is not sufficient to cover the service costs.

Mode of Payment of Premium :-

The premium amount will be deducted from the account holder’s savings bank account through ‘auto debit’ facility in one installment for the entire year, as per the option to be given on enrolment. Members may also give one-time mandate for auto-debit every year till the scheme is in force, subject to re-calibration that may be deemed necessary on review of experience of the scheme from year to year

Termination of Benefit Cover:-

In following cases the cover will be terminated and no benefit will be payable to the subscribers.

1) On attaining age 70 years or the age nearest birth day 2) At the time of renewal in subsequent years, due to insufficiency of balance to keep the insurance in force the account gets closed. 3) In case a subscriber is covered by more than one account and premium is paid by the subscriber intentionally, insurance cover will be restricted to one only and the premium shall be liable to be forfeited. 4) If the insurance cover is ceased due to any technical reasons such as insufficient balance on due date or due to any administrative issues, the same can be reinstated on receipt of full annual premium, subject to conditions that are to be issued in future. During this period, the risk cover will be" suspended" and reinstatement of risk cover will be at the sole discretion of Insurance Company.

Pradhan Mantri Suraksha Bima Yojana Participating banks will deduct the premium amount in the same month when the auto debit option is given, preferably in May of every year, and remit the amount due to the Insurance Company in that month itself.

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

72

DATA ANALYSIS

The primary data of Pradhan Mantri Suraksha Bima Yojana in OBC Bank KHAI PHEME KI (Ferozepur) . The provided by bank is between 9-May-2015 to 18-July-2015. Total accounts open between that period is 1860 approx.

No. of Insurance policy done between that period is shown month wise in following table and diagram:-

Months May June JulyNo. of Insurance 495 589 776

May, 495

June, 589

July, 776

No. of Insurance

May

June

July

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

73

BIBLIOGRAPHY

In this project report, while finalizing and for analyzing quality problems in detail following books, magazines, journals, websites have been referred. All the material detailed below provides effective help and a guiding layout while designing this text report.

SOURCES OF INFORMATION

BOOKS:-

Research Methodology-C.R. Kothari

WEBSITES:- www.goggle.com www.obcindia.co.on www.pmjdy.gov.in www.atalpensionyojna.com www.india.com www.scirb.com www.wikipedia.com www.business-standard.com

NEWSPAPERS:- BUSINESS STANDARD ECONOMIC TIMES

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

74

ANNEXURE

Questionnaire-1

“Awareness on PMJDY”

Respected sir /madam,

I am student of M.com at R.S.D collage (Panjab University); Ferozepur a study related to “To

identify the awareness of PMJDY among the people of village” is being carried out for the

fulfillment of M.com summer training project. Your kind co-operation in answering this questionnaire

will add value to my project.

Q1). For how long you have been staying in this village?

a). Less than a year b). 1 to 5 years c). More than 5 years

Q2). Who all are there in your family?

a). Joint family b). Nuclear Family

Q3). Does any one of you have bank account?

a). Yes b). No

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

Name :- ________________ Age :- _________________

Gender :- Male/female Occupation:-___________

Address :- ____________________________________________

_____________________________________________________

Mobile no. :- __________________________________________

75

Q3.2). Which type of account do you have?

iii) Saving a/c iii) Fixed deposit a/c

iv) Current a/c iv) Recurring deposit a/c

Q3.3). What were the reasons that your Household opened the account?

vi) To receive government payments from NREGA

vii) To receive government payments from scheme other than NREGA

viii) For saving

ix) To request a loan

x) If other , please specify _______________________________

Q3.4). Who helped you while opening the account?

v) Village panchayat official

vi) Bank official

vii) Neighbors/Friends/Relatives/Employer

viii) Business correspondent/Post office

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

If yes, kindly answer the following questions otherwise go to Q4.

Q3.1). No of account in your household?

i) 1 iii) 3ii) 2 iv) More than 3

76

Q4). Reason for not having even a single bank account in your family?

a). Very little money to put in

b). No banking facilities in area

c). Lengthy procedures

d). Many charges are there

e). Tried to open but was refused

f). Other ( please specify) _______________

If refused by bank to open a/c answer this , otherwise go to Question 5

Q4.1) Reason for being refused by bank a/c?

v) No id proofvi) No address proofvii) Don’t knowviii) Had to maintain minimum balanceix) Other (please specify) __________________

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)

77

Q5). Awareness about basic banking saving account which was announced on 15 august 2014?

ii) Good ii) Medium iii) Poor

If not aware about services answer this , otherwise go to Question6

Q5.1). Reason for not having awareness about Basic saving a/c?

I) No promotion by banks , government or village panchayat in village

II) Not in a habit of reading newspaperIII) Lack of media Advertisement via TV/Radio

Q6).Are you aware about the various facilities covered under PMJDY like :-

( I- Overdraft facility of 5,ooo , II – Life insurance cover , III – Personal accident cover , VI- Rupay card )

iii) Yesiv) No

ORIENTAL BANK OF COMMERCE KHAI PHEME KI (FEROZEPUR)