Embed Size (px)

DESCRIPTION

Annual Report

Citation preview

For the year ended 31 March 2013

Anchor Trust

Annual Report & Financial Statements

Happy living for the years ahead

2Annual Report and Financial Statements

3For the year ended 31 March 2013

Contents4 Chairman’s and Chief Executive’s Statements

6 Operating and Financial Review

16 Corporate Governance Report

24 Board, Directors and Advisers

25 Directors’ Report

27 Independent Auditor’s Report

28 Consolidated Income and Expenditure Account

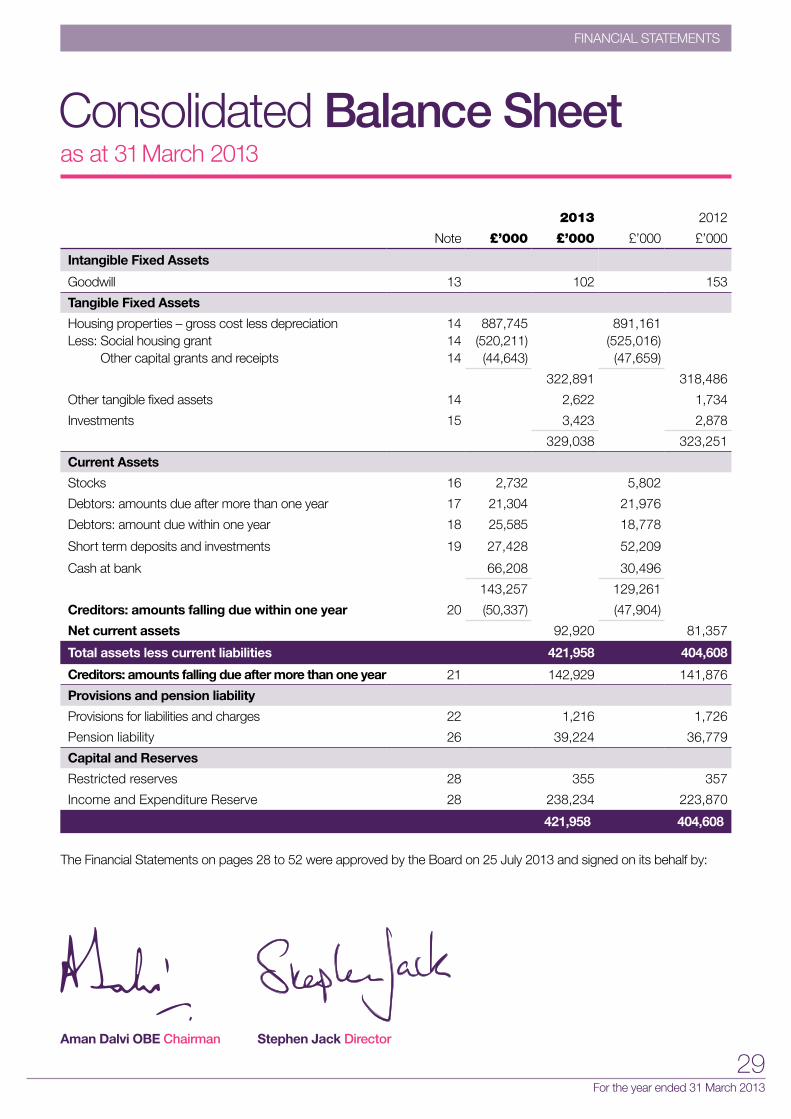

29 Consolidated Balance Sheet

30 Company Balance Sheet

31 Consolidated Cash Flow Statement

32 Notes to the Financial Statements

54 The Board

56 Executive Management Board

4Annual Report and Financial Statements

Chairman’s Statement

As I conclude my final full year as Anchor’s Chairman, I am delighted that the organisation continues its proud tradition of innovating to meet the changing needs of the older people it serves.

An ageing population and tough economic environment present

unique challenges and opportunities. Among those challenges, reductions in public funding and consumer spending power mean it is vital that we provide excellent value for money.

We are well-positioned to do so, thanks to our clear strategic direction, strong governance and pro-active executive team.

We are investing significantly in existing properties while delivering an ambitious development programme. Our newest development, West Hall in Surrey, won the Best Internal Dementia Design category in the National Dementia Care Awards 2012.

Our commitment to happy living goes beyond design though. Maintaining high levels of

customer satisfaction in our housing and care homes is a priority.

We are proud to be among the organisations to pioneer the Your Care Rating satisfaction survey. The survey, conducted by Ipsos MORI, is being used by a large and growing number of providers to enable care home residents to voice their views on a variety of areas, including activities, privacy, security, food and whether they would recommend the home.

It is crucial that customer involvement drives continuous improvement,

and we have a wide range of ways to gather feedback.

As part of this, the Board value the work of the Customer Services Committee and its regional forums.

We welcome recognition in government of the need to integrate housing and care, as well as the progress on social care funding reform. Anchor will continue to have a strong voice in this area as we believe it is crucial to delivering happy living for all older people.

Jane Ashcroft’s continued efforts to raise these issues up the political agenda were recognised in December, when she came top in Care Talk magazine’s Social Care Top 30. This was well-deserved and I thank her for her excellent leadership of Anchor.

I would also like to thank Vice Chairman Graham Watts, who this year concluded his term on Anchor’s Board, for his extremely valuable contribution to the organisation.

As my tenure as Chairman draws to a close, I am delighted that Pamela Chesters CBE will be succeeding me during the next financial year. With an impressive track record in housing and health as well as in the private sector, Pamela brings a wealth of experience which will be invaluable.

She joins an impressive Board and I am grateful to them and the executive team for guiding the organisation to ensure that Anchor provides happy living for older people for many years ahead.

CHAIRMAN’S STATEMENT

Aman Dalvi OBE Chairman

5For the year ended 31 March 2013

Chief Executive’s Statement

A strong demand for great housing and care coupled with tighter funding underpin our focus on quality value-for-money services.

Our ‘One Anchor’ approach is providing better integrated

services for our customers and clearer career paths for colleagues.

Our customers tell us they value the great support and service provided by Anchor people. Maintaining and improving that service, from an initial enquiry through the many years of our relationship with customers, is a priority.

We have invested in our colleagues through a reward plan which includes a commitment to move to the ‘living wage’, with strong progress made to date. And our ‘Your Say’ survey indicates colleagues feel they are benefiting from better learning and development opportunities. The achievement of a wide range of national awards, including an MBE for Customer Engagement Advisor Debbie Sharples, has been an excellent endorsement of this approach.

We are committed to openness and transparency, as has been evident in our work with our Customer Services Committee and Colleague Forum, just two of the many ways in which we listen to the views and advice of all customers and colleagues. Working with key stakeholders at a local and regional level ensures our services provide the best outcomes for everyone. The impact of loneliness on some older people has been identified nationally as a major issue, and I am proud that many people choose to live with Anchor because of the strong communities which my colleagues across England work so hard to support.

This approach has contributed to our strong performance on occupancy, quality of service, customer satisfaction and colleague engagement. It has also reinforced our commitment to maintaining

our scheme manager service, which we know is valued by housing customers and their families.

In these times of significant change, it is important that we focus on identifying and managing risk. This has been a priority for the executive team, with effective support and oversight from the Audit & Risk Committee members.

The hard work of all of my colleagues has contributed to a financial surplus which we are able to reinvest in our services for the benefit of existing and potential customers. Our five-year investment plan will ensure that our properties continue to be great places to live, and our plans for new services are continuing well, with further care villages and care homes in development and due to open in 2014.

We have been pleased to act with colleagues across the sector to improve the lives of older people, for example as members of the Care & Support Alliance, and to champion the development of new models as founder members of the Associated Retirement Community Operators (ARCO). We continue to meet the changing requirements of our current customers and, crucially, anticipate those of the older people of tomorrow.

Finally, I would like to take this opportunity to thank Aman for his contribution during his time on the Board and as Chairman of Anchor.

Jane Ashcroft Chief Executive

CHIEF ExECuTIVE’S STATEMENT

6Annual Report and Financial Statements

OpeRAting And FinAnciAl Review

Operating and Financial Review

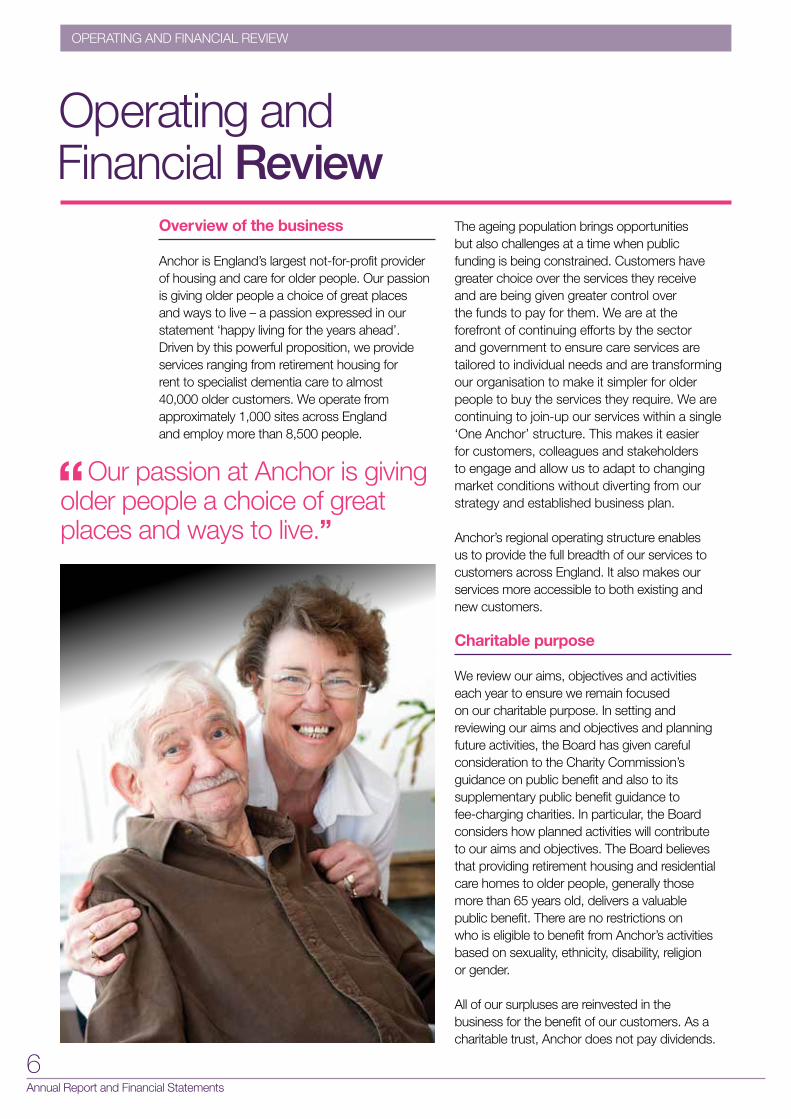

Overview of the business

Anchor is England’s largest not-for-profit provider of housing and care for older people. Our passion is giving older people a choice of great places and ways to live – a passion expressed in our statement ‘happy living for the years ahead’. Driven by this powerful proposition, we provide services ranging from retirement housing for rent to specialist dementia care to almost 40,000 older customers. We operate from approximately 1,000 sites across England and employ more than 8,500 people.

The ageing population brings opportunities but also challenges at a time when public funding is being constrained. Customers have greater choice over the services they receive and are being given greater control over the funds to pay for them. We are at the forefront of continuing efforts by the sector and government to ensure care services are tailored to individual needs and are transforming our organisation to make it simpler for older people to buy the services they require. We are continuing to join-up our services within a single ‘One Anchor’ structure. This makes it easier for customers, colleagues and stakeholders to engage and allow us to adapt to changing market conditions without diverting from our strategy and established business plan.

Anchor’s regional operating structure enables us to provide the full breadth of our services to customers across England. It also makes our services more accessible to both existing and new customers.

Charitable purpose

We review our aims, objectives and activities each year to ensure we remain focused on our charitable purpose. In setting and reviewing our aims and objectives and planning future activities, the Board has given careful consideration to the Charity Commission’s guidance on public benefit and also to its supplementary public benefit guidance to fee-charging charities. In particular, the Board considers how planned activities will contribute to our aims and objectives. The Board believes that providing retirement housing and residential care homes to older people, generally those more than 65 years old, delivers a valuable public benefit. There are no restrictions on who is eligible to benefit from Anchor’s activities based on sexuality, ethnicity, disability, religion or gender.

All of our surpluses are reinvested in the business for the benefit of our customers. As a charitable trust, Anchor does not pay dividends.

Our passion at Anchor is giving older people a choice of great places and ways to live.”

7For the year ended 31 March 2013

Operating and Financial review

We provide properties to rent at almost 700 locations and our leasehold property management activity provides services to leaseholders at 225 estates.”

Retirement housing

More than 30,000 people live in retirement housing owned or managed by Anchor. We provide properties to rent at almost 700 locations and our leasehold property management activity provides services to leaseholders at 225 estates. Anchor also provides extra-care services in a small number of locations. We have exciting plans to develop retirement villages and continue to develop additional retirement housing with on-site care, support and amenities available.

Residential care homes

Anchor is one of the largest not-for-profit providers of residential care homes in England and is increasingly developing specialist services for those customers living with dementia. Our 96 care homes have more than 4,300 rooms and provide residential, dementia and nursing care. West Hall, a 117-room care home in Surrey, was opened in July 2012 and we plan to build and open other care homes in future years.

Anchor’s business aims, objectives and strategy

Our passion at Anchor is giving older people a choice of great places and ways to live. We do this by treating our customers and our colleagues as individuals and by building meaningful, long-term relationships based on happiness, openness and respect.

We are three years through our five-year business plan, which extends to 2015 and supports an ambitious business development strategy at a time when there are unprecedented levels of economic, social and regulatory change. These changes are having a major impact on the lives of older people, the framework in which we operate, and on our competitors. We will continue to focus on services where we are or can be the market leader, which play to our core strengths and values, and in which we can be financially successful.

Growth will be achieved by meeting the following objectives:• Focusing on serving the needs of older people

– a rapidly increasing group spanning several generations as people live longer and have increasingly complex needs.

• Continuously improving our affordable housing offer.

• Building new models of housing for sale and market rent to deliver significant turnover.

• Achieving significant reductions in the cost of delivery.

• Becoming an employer of choice.

• Becoming synonymous with happy colleagues and happy customers.

Through meeting our objectives we will continue to deliver a significant public benefit.

The focus in the first three years of the business plan was to develop value for money services and improve processes to enable colleagues to focus on individual relationships. We also embedded the regional structure for our operational teams, which means we have better utilised local knowledge to make Anchor’s full range of services accessible to all customers. In previous years we exited from other businesses so we could focus all our efforts on providing housing for rent and sale, and an on-site care service to our customers at Anchor properties and residential care homes.

The year’s achievements included:• Ensuring our customers enjoyed a consistent

high standard of service. This included introducing a clearer property standard, so that customers know what to expect from an Anchor property.

• The opening of West Hall on 24 July 2012.

• The improvement of our website so that it is easier for customers and their families to use.

• The introduction of a ‘Manager Direct’ helpline, so Anchor colleagues can access the assistance they require – avoiding the cost of colleagues travelling to locations to assist.

8Annual Report and Financial Statements

OpeRAting And FinAnciAl Review

• Workshops for our colleagues on ‘The Anchor Way’, to help colleagues understand how they can contribute to the success of the business.

• The implementation of changes to reduce internal paperwork, including making customer care plans easier and quicker to complete.

• The removal of inefficiencies across a number of support activities and reorganisation of functions so decisions can be made quickly, with fewer managerial layers, and in so reducing the cost of delivery, providing more cost-effective services to our customers.

The focus for the next two years is to continue to provide the new and more cost effective services that our customers demand and ensure a highly engaged workforce.

Anchor’s principal risks

The key external risks that influence and could impact adversely on the operational and financial performance of Anchor are:

• Reduced public expenditureFunds available to local authorities for the provision of social care will continue to be reduced. Pressures from government to seek greater value for money and reduce

expenditure on all services will require Anchor to work more closely with local authorities and seek efficiencies across our operations.

• Performance of the housing marketOur business plan assumes that we will generate surpluses from future sales of our leasehold housing developments which will be used to reinvest in developments and services. The proceeds from future sales are sensitive to housing capacity and the economic environment.

• Changing customer buying trends and buying powerThe ‘golden generation’ of older people with healthy pensions is diminishing. Older people increasingly have to tackle the cost of care and the government continues with its agenda to provide individuals with personal budgets to manage their own care. Anchor is sensitive to these changing spending patterns, including both the reduction in the funds available to our customers and the impact of our customers managing their own financial affairs.

• Lending availabilityAnchor is currently comfortably meeting the financial covenants required by its lenders, has a strong financial track record and has access to further funds through facilities

The “golden generation” of older people with healthy pensions is diminishing. Older people increasingly have to tackle the cost of care.”

9For the year ended 31 March 2013

Operating and Financial review

The standards programme defines our service and accommodation offer. It allows us to deliver a consistent quality of service through a standardisation of the processes, equipment and furnishings used in the management and maintenance of our properties.

The business performance management programme introduces a better way of understanding what makes our business a success and using performance information to improve it further.

The tools for managing people programme will deliver new HR and payroll systems. Through streamlined processes and enhanced business intelligence, it will reduce the time and costs incurred through sickness and recruiting staff. A more cost effective HR advice service is being introduced without any loss of quality.

provided by its bankers. Limited access to new funds at reasonable prices could restrict Anchor’s ability to grow, although no such funds are required in the near future.

• Pensions Anchor’s defined benefit pension scheme liabilities, like those of very many others, are currently greater than the market value of the scheme’s assets due to reduced investment returns and increasing life expectancy rates. Although Anchor has agreed with the trustees of the scheme to make annual contributions towards the deficit, there is a risk that contributions may need to be increased in the future.

• RegulationExternal events, not involving Anchor, have increased the pressure on Anchor’s two main regulators – the Homes & Communities Agency (HCA) and Care Quality Commission (CQC) to increase the scope of regulation and degree of scrutiny. Increased regulation and additional scrutiny can increase the costs of compliance and may impact Anchor’s strategy for growth.

Value for money and operational performance

Anchor assesses how it delivers value for money by reference to its business plan, described in the section ‘Anchor’s business aims, objectives and strategy’. The business plan is reassessed each year against market changes to make sure it is still valid and progress against it is monitored through a series of key performance indicators (KPIs). These are reported to the Executive Management Board and by them to the Board and all levels of management throughout Anchor. A number of improvement projects and initiatives underpin the business plan. In 2012 four initiatives, closely monitored by the Executive Management Board, were launched to help deliver excellent service and value for money:

The customer experience programme ensures Anchor provides an outstanding customer experience in every interaction we have with our customers, from their initial enquiry until they leave. It checks that every step of our response adds value and when time and cost savings are identified, they are delivered without impacting on the quality of service to our customers.

Anchor is currently comfortably meeting the financial covenants required by its lenders.”

10Annual Report and Financial Statements

OpeRAting And FinAnciAl Review

How the Executive Management Board monitors value for money

The following key performance indicators are monitored by the Executive Management Board and reported by them to the Board on a monthly basis to confirm we are meeting our business plan objectives.

How we assess customer valueWe continually assess the value and quality of the services provided to customers. Information from annual and quarterly customer satisfaction surveys, supported by mystery shopping exercises, is used to identify and deliver service improvements and to monitor the value customers place on our services.

Formal meetings regarding the quality and cost of services are held with customers at every rented housing location twice a year. Standards of service delivery to be met at each location are reviewed with customers and published every year.

A performance report developed with our Customer Services Committee (CSC) enables customers to monitor services that are important to them. A customer scrutiny panel enables the CSC to commission further research into the value, effectiveness and cost we incur in providing services to them.

Property and returns on assetsAnchor’s property team is undergoing a structural review with the twin aims of improving customer engagement and delivering improved value for money. Progress to date includes the centralisation of ordering and the classification of repairs. This has saved £1.5m compared to

2013 Actual 2013 Target

Customer value

Customers satisfied with Anchor 92.0% 90.0%

Customer complaints resolved within 14 days 97.1% 92.0%

Property and returns on assets

Planned works programme delivery 86.0% 85.0%

Reactive repairs completed on time 97.3% 97.0%

Disposals programme on schedule 82.4% 100%

Efficiency or cost reduction

Housing re-let days 43 days 30 days

Occupancy of care homes 92.2% 93.8%

Compliance

Gas safety checks 100% 100%

CQC compliance 87.3% 100%

People

Colleague engagement (staff survey) 72.0% 74.0%

Sickness absence 3.8% 3.0%

11For the year ended 31 March 2013

Operating and Financial review

the costs incurred in 2011/12. Current initiatives include collaborative working with responsive repairs contractors to achieve cost savings via bulk purchasing and product sourcing.

Last year our approach to tendering contributed to an overall saving of 7% against our planned works budget.

The Net Present Value (NPV) of all of our locations is kept under constant review as part of our asset management strategy. Locations where the NPV and marketability are unfavourable are subject to a long-term viability check including a full option assessment. If we cannot deliver a turnaround plan, the location will be earmarked for disposal. In just over two years we saved £0.3m on security on empty locations awaiting disposal by moving from a visiting patrol to a live-in security system.

Efficiency and cost reductionThe procurement team is aligned to all key organisational initiatives, with the team’s performance being partly monitored through savings made from the renewal of significant contracts. Renegotiated rates are fed into the annual budget planning process. In 2012/13 the team delivered savings, against budgeted rates, of £1.1m.

The team operates a category management approach enabling the aggregation of supply and spend information, the establishment of market expertise and the monitoring of innovations and best practice in those markets. The planned extension of our e-Procurement usage will bring further efficiencies.

We monitor fundamentals and prices in the energy market daily to enable purchasing at optimum prices. This helped us win Energy Buyer of the Year at the 2012 Energy Awards. We have calculated that the cost of our gas and electricity usage is £7m lower when compared to the lowest average domestic tariff rate published by the government.

We have a programme of installing remote boiler controls into our locations. Since 2003, 410 locations have been fitted with such equipment. On average, these controls save 15% on gas energy costs. All remaining locations that are suitable for them will have these controls fitted by 2018.

Empty properties directly affect receivable income. Our focus on driving up our occupancy rate

resulted in 466 voids in March 2013, half the 933 voids recorded in April 2010.

New operating models in our Customer Centre have increased the level of customer contact while reducing costs.

Peopleunder the direction of our People Strategy we are delivering value for money through our workforce. We have reviewed the majority of non-customer facing functions to reduce complexity and duplication, clarify accountability and to streamline and speed up decision-making. Cost savings from this exercise have been reinvested into frontline pay and supporting the up-skilling of our managers, through our Leaders’ Academy.

Financial results for the year

Anchor’s financial performance for the year was encouraging.

• Operating performance in retirement housing once again benefited from a programme to fill empty properties, and a combination of the annual rent uplift and reduction in costs.

• The operating surplus from housing remained strong, with the £1.0m decrease year-on-year reflecting the closure of 14 housing schemes in the year.

• The trading environment for residential care homes continues to be tough. Considerable efforts to control costs have been successful, but have been partly offset by set-up costs incurred for West Hall.

• All but a few properties were sold at Denham Garden Village and The Laureates.

12Annual Report and Financial Statements

OpeRAting And FinAnciAl Review

* In 2012, turnover and operating deficit relating to discontinued operations were £3.7m and £(0.1m) respectively and related to the home care service.

Turnover – continuing operationsIn the year to 31 March 2013, turnover from continuing operations was £264.9m (2012: £263.8m). The main area of focus for the business continued to be retirement housing lettings of £128.6m (2012: £124.3m) and residential care homes of £119.2m (2012: £117.4m). Turnover from providing on-site care at Anchor locations was £5.4m (2012: £5.6m).

Non-social housing turnover includes leasehold management, £3.2m (2012: £3.2m) and property sales at Anchor’s two mixed tenure retirement developments. In total, 13 properties at Denham Garden Village and seven at The Laureates were sold, generating total sales of £6.0m (2012: £10.8m). Turnover from other activities was £2.6m (2012: £2.5m).

Operating surplus – continuing operationsAnchor’s surplus from continuing operations was £18.1m (2012: £25.5m).

Retirement housing surplus decreased by £1.0m to £26.3m (2012: £27.3m) due primarily to the closure of 14 schemes during the year, combined with a switch in expenditure on major works away from capital works. Residential care homes operating surplus at £1.6m, decreased

from last year (2012: £2.1m) due largely to set-up costs incurred for West Hall.

Expenditure on major works to our properties was £42.4m (2012: £41.9m). The Income and Expenditure Account incurred a higher charge than the previous year of £11.8m (2012: £9.8m) and conversely a lower cost was capitalised of £30.6m (2012: £32.1m). This mix away from capital works contributed towards the decrease in the retirement housing surplus for this financial year.

Property sales at Denham Garden Village and The Laureates contributed a surplus of £2.6m (2012: £4.6m).

The decision was taken to sell or transfer 14 retirement housing schemes during the year (2012: 10). The costs of disposal were £3.9m less than 2012.

In both 2013 and 2012, the exceptional credit arose from the release of unutilised provisions relating to the separation costs for Anchor Staying Put.

Interest receivable of £3.4m (2012: £2.9m) was £0.5m higher than last year, mainly due to £0.4m increased exchange rate gains.

Interest payable for the year decreased to £7.9m (2012: £10.6m), mainly due to finance lease interest payments decreasing by £2.8m.

Year to 31 March

2013 All continuing

£m

2012* Total

£m

2011 Total

£m

2010 Total

£m

2009 Total

£m

Turnover 264.9 267.5 280.8 286.5 267.0

Operating surplus before exceptional items 18.1 25.4 19.4 21.0 5.7

Surplus/(deficit) for the year 21.8 22.2 10.3 7.8 (13.2)

Financial review

A summary of Anchor’s financial results over the past five years is set out below:

13For the year ended 31 March 2013

Operating and Financial review

Balance sheet performance

A summary of Anchor’s balance sheet over the past five years is set out below:

At 31 March

2013 £m

2012 £m

2011 £m

2010 £m

2009 £m

Goodwill 0.1 0.2 0.2 0.4 1.0

Housing properties at cost less depreciation 887.7 891.2 888.0 897.0 899.9

Social Housing Grant (520.2) (525.0) (543.8) (550.5) (553.2)

Other capital grants (44.6) (47.7) (53.0) (54.3) (54.5)

Housing properties – net book value 322.9 318.5 291.2 292.2 292.2

Other tangible fixed assets 2.6 1.7 4.4 5.3 5.4

Investments 3.4 2.9 2.7 1.9 2.1

Net current assets 92.9 81.4 64.9 52.0 42.0

Total assets less current liabilities 421.9 404.6 363.4 351.8 342.7

Cash and short term deposits increased to £93.6m (2012: £82.7m), mainly due to the timing of new development expenditure.

The disposal of housing schemes resulted in the attributable Social Housing Grant moving into the total Recycled Capital Grant Fund, increasing the fund’s balance to £10.3m (2012: £7.0m), shown in note 21 of the Financial Statements.

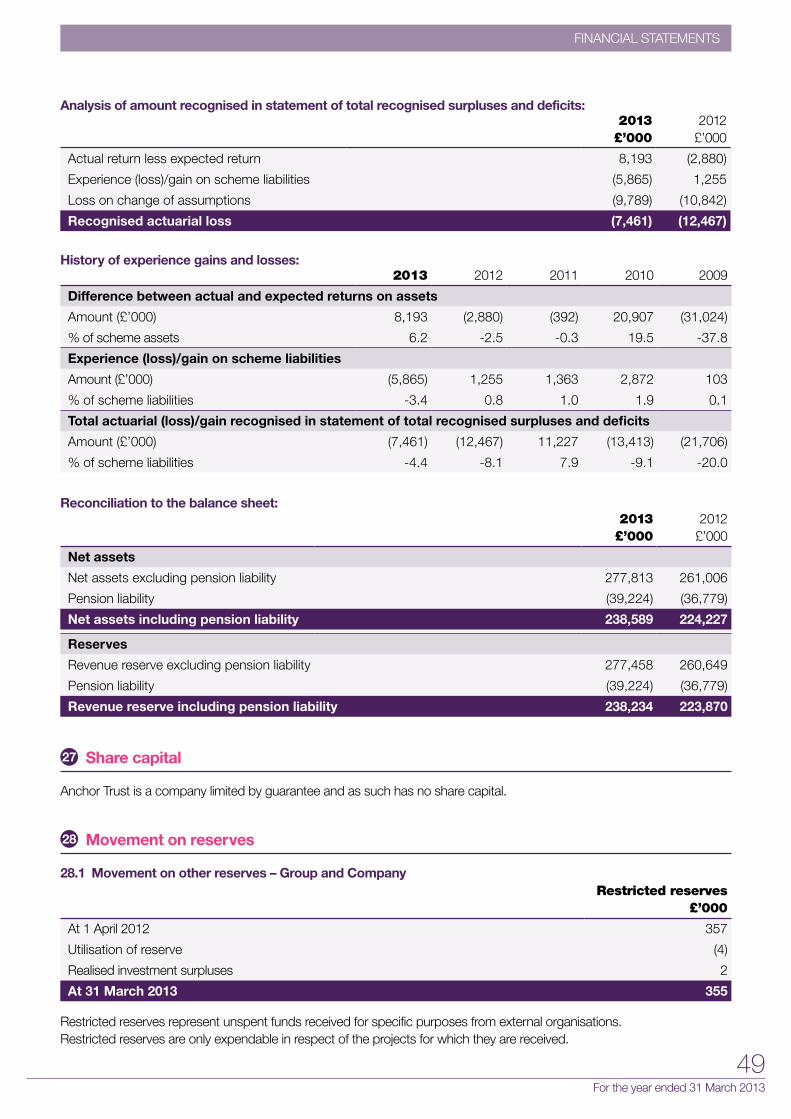

At 31 March 2013, Anchor’s total assets increased to £421.9m (2012: £404.6m), of which £238.2m was represented by accumulated Income and Expenditure Reserve (2012: £223.9m). The Income and Expenditure Reserve increased by £21.8m from the surplus generated during the year and reduced by £7.5m from an actuarial loss following the annual valuation (performed in accordance with Financial Reporting Standard 17) of Anchor’s defined benefit pension scheme.

Continuing investment in our housing properties and construction of new care homes and other developments resulted in the net book value of housing properties increasing to £322.9m (2012: £318.5m).

Within net current assets, Anchor’s stock of housing for sale analysed in note 16 of the Financial Statements, reduced to £2.6m (2012: £5.7m). This includes four remaining properties held for sale at The Laureates, and ten properties at Denham Garden Village currently let out at market rents.

14Annual Report and Financial Statements

OpeRAting And FinAnciAl Review

Cash flow

The net movement in operating cash flow for the year was an inflow of £41.8m (2012: £49.6m).

As shown in note 29.1 of the Financial Statements, this cash flow was generated from an operating surplus of £18.1m (2012: £25.8m) and, after allowing for depreciation and other non-cash expenditure, was reduced by a £4.6m (2012: £5.0m) payment towards Anchor’s pension scheme deficit and increased working capital.

As shown in note 29.4 of the Financial Statements, £42.7m (2012: £61.5m) of cash was used to develop housing properties, a decrease of £18.8m. Housing fixed assets disposal proceeds were £18.4m (2012: £14.9m).

Cash at bank was £66.2m (2012: £30.5m), a net increase in cash of £35.7m (2012: £19.5m). In line with Treasury Policy, £24.8m was transferred out of short-term deposits into instant access accounts.

Investment in new developments

At 31 March 2013, development costs of £11.1m (2012: £27.1m) were added to fixed assets – housing properties under construction.

Programmes commenced to build a retirement village in Bishopstoke, Hampshire. The village will have a 48-bed care home and 209 housing units for sale. Anchor will take over the lease at a residential care home in Esher, Surrey once the building work has been completed. West Hall in West Byfleet, Surrey, Anchor’s largest care home development, comprising 117 rooms, opened in July 2012.

Anchor continues to seek suitable sites on which to build care homes, retirement villages and assisted living housing schemes which meet the needs of our customers now and in the future, and a number of such sites are progressing through various stages of property development and construction.

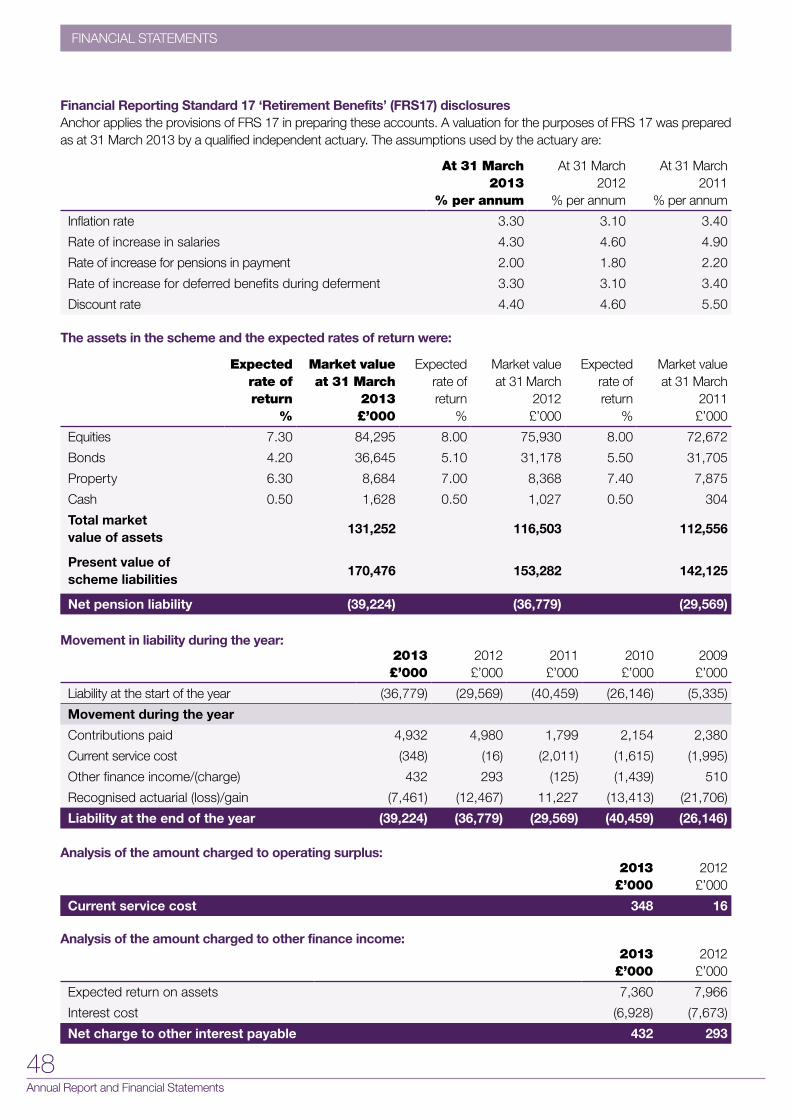

Pensions

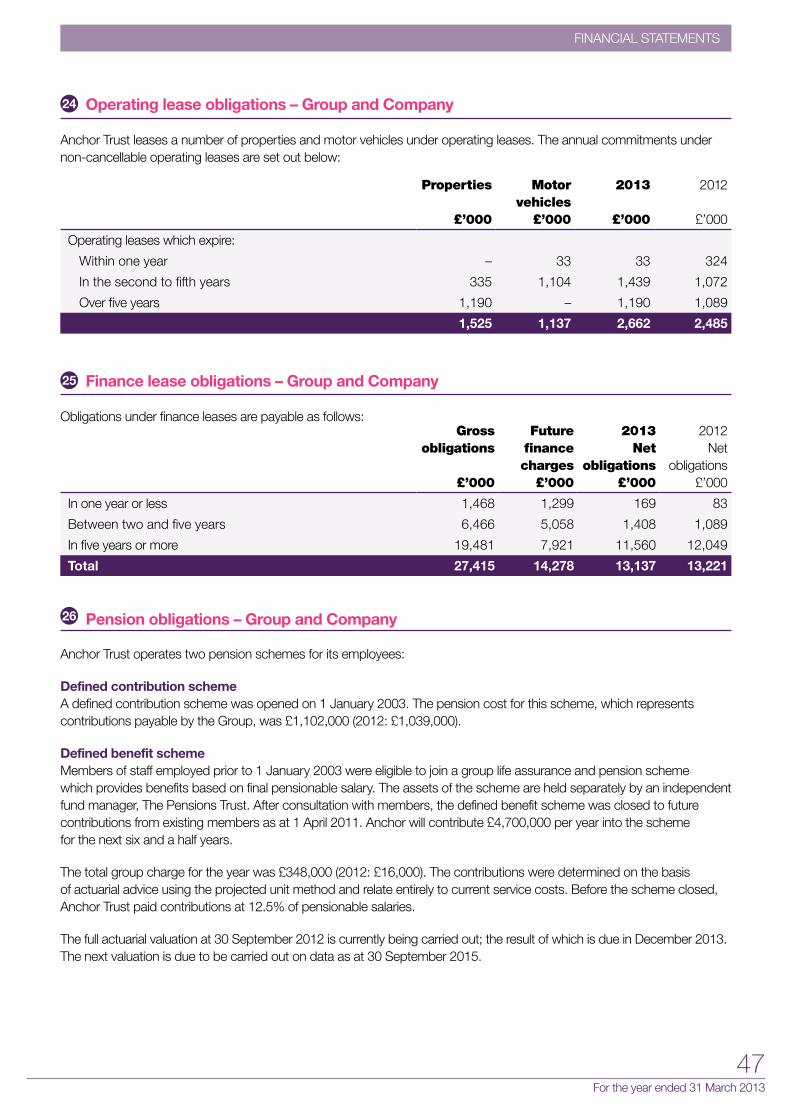

The latest triennial valuation of the Anchor Trust Final Salary Pension Scheme at 30 September 2012 has not been completed, and its results are not reflected in these Financial Statements. The Scheme was closed on 1 April 2011 to further contributions and no new entrants have been admitted since 2003. The service costs after finance income were £0.1m credit (2012: £0.3m credit). The actuarial loss was £7.5m (2012: £12.5m). Anchor had previously agreed with the trustees of the scheme to make additional payments towards the pension deficit, which amounted to £4.6m (2012: £5.0m) after costs in this financial year, and will be £4.7m (before costs) for each of the next six and a half years.

The actuarial loss and service costs partially offset by finance income and the additional payment, described above, resulted in the value of the pension scheme liability on a Financial Reporting Standard 17 (FRS17) basis increasing by £2.4m (2012: £7.2m), being a £14.7m increase in the scheme’s assets and a £17.1m increase in the scheme’s liabilities. At the year end, the scheme had an FRS17 deficit of £39.2m (2012: £36.8m).

Treasury

Anchor’s treasury activities are managed to ensure sufficient cash is in place to fund operations and to reduce the impact of adverse movements in interest rates and the financial markets.

Treasury activities are carried out in accordance with a Board-approved treasury management policy and supporting procedures. A treasury

Anchor continues to seek suitable sites on which to build care homes, retirement villages and assisted living housing schemes.”

15For the year ended 31 March 2013

Operating and Financial review

strategy is in place to support delivery of the Group’s objectives and its operational and long-term plans are supported by financial budgets and forecasts. The treasury strategy is approved annually by the Board.

Cash flow requirements are monitored through a rolling forecasting process. Anchor’s policy is to minimise cash held by repaying debt as early as practicable, while ensuring sufficient access to funding to cover investment and development plans. This is achieved by the use of forecasts covering short, medium and long-term cash flows and the use of short-term investment and revolving facilities.

During 2013, surplus cash was held predominantly in a cash liquidity fund. A total of 50% of drawn borrowings were at fixed rates of interest at the year end (2012: 50%) for an average period of 13 years (2012: 14 years).

Anchor has access to undrawn committed borrowing facilities of £73.6m (2012: £73.6m). These facilities together with substantial unutilised security on the Balance Sheet ensure Anchor remains in a strong position to fund future growth plans and investment opportunities.

Net debt at 31 March 2013 was £30.0m (2012: £41.2m), as cash generated from operations was used to finance capital expenditure and working capital.

Anchor remains in compliance with its financial covenants, which are primarily based on interest cover and gearing. Covenants have been met with considerable headroom, due to low interest rates payable (as LIBOR has decreased) and a strong trading performance.

Tax and legal structure

Anchor has a non-charitable trading subsidiary company, Anchor 2020 Limited, which is used to procure design and construction services for the Group and manage the professional fees on new development projects.

Anchor has a second non-charitable trading subsidiary company, Anchor Lifestyle Developments Limited, which is used to operate any non-charitable services.

Surpluses from these subsidiaries are reinvested into Anchor Trust, for the benefit of Anchor Trust’s charitable activities.

Anchor remains in a strong position to fund future growth plans and investment opportunities.”

16Annual Report and Financial Statements

CoRpoRAte GoveRnAnCe RepoRt

Corporate Governance Report

Overview of Anchor’s corporate governance

Anchor is a private company limited by guarantee without share capital. Anchor does not have any shareholders and all of its surpluses are reinvested back into the business. As far as possible, Anchor is managed in line with corporate governance safeguards set out in the uK Corporate Governance Code. Anchor’s Board of Directors is entirely made up of Non-Executive Directors who normally serve for three-year terms, subject to a maximum of three terms.

The Board has the following committees: Audit & Risk (A&RC), Executive Remuneration and Nomination Committees. The Board also operates a Customer Services Committee which enables it to monitor the quality of services provided to Anchor’s customers.

Anchor is also monitored and supervised by external regulators including the Homes & Communities Agency, the Care Quality Commission and the Charity Commission.

The Board and its committees

At 31 March 2013, the Board comprised seven members led by the Chairman, Aman Dalvi. Graham Watts, Vice Chairman of the Board and Chairman of the Audit & Risk Committee, retired in September 2012 at the end of his term.

The Board controls Anchor’s strategic direction and reviews its operating and financial position. There is a formal schedule of matters reserved specifically to the Board, which ensures it takes all major strategy, governance, financial planning, investment and policy decisions. The appointment of the Chief Executive and the approval of standing orders and delegations of authority are matters reserved to the Board.

The Board undertakes an annual review of its schedule of matters reserved and the terms of reference for its committees to ensure that these documents remain in line with good practice.

During the financial year, an internal evaluation of the effectiveness of the Board, and the Board’s committees was undertaken and discussed at Board meetings. Overall, the Board concluded that Anchor has an effective governance structure and that there is strong teamwork and clear accountability in the way the Board operates.

The Board’s governance framework is designed to encourage all Board members to bring an independent judgement to bear on issues of strategy, performance, resources (including key appointments) and standards of conduct.

The Board controls Anchor’s strategic direction and reviews its operating and financial position.”

17For the year ended 31 March 2013

Corporate GovernanCe report

Board meetings

The Board met six times during the year. Member attendance at Board and committee meetings was as follows:

Each member of the Board brings different experiences and skills to the operation of the Board and its various committees. New Board members undergo a formal, tailored induction programme on joining. The programme includes background information about Anchor, details of meeting procedures, Board members’ responsibilities, including Directors’ Duties under the Companies Act 2006, and governance-related issues including the time commitment expected of Board members. The role of the Chairman and Chief Executive are clearly defined, with the former being a Non-Executive Director and the latter a member of the Executive Management Board.

The performance of each Board Director and the Chief Executive is evaluated by the Chairman. The Chairman’s performance is evaluated by Lesley James, Chair of the Nominations Committee.

The Board review and determine strategy for Anchor, based on the changing needs of older people, the economic environment, risk and opportunities. Regular reporting enables the Board to oversee the performance of the organisation and to work with the Chief Executive and Executive Management Board to determine priorities and areas for improvement.

The Board has in place formal procedures for the management of its meetings which require the Board to be supplied with timely and relevant information to enable it to discharge its duties. Board papers are distributed 10 days in advance of the relevant meeting, and the papers are sufficiently detailed to enable Board members to obtain a thorough grasp of Anchor’s management and financial performance. The Board’s terms of reference make provision for it to receive independent professional advice, at Anchor’s expense, to enable it to carry out its duties.

The Board composition is kept under review and when a new appointment is to be made, consideration is given to the experience which a potential new member could add to the existing mix. A transparent recruitment process is used, with advice from external consultants if required. Appointments to the Board are the responsibility of the full Board, with recommendations as appropriate from the Nominations Committee.

As described above, there are four committees of the Board: the Audit & Risk Committee, the Executive Remuneration Committee, the Nominations Committee and the Customer Services Committee.

* Retired in September 2012. ** Appointed to A&RC November 2012.

Board (6 meetings)

Audit & Risk Committee (4 meetings)

Executive Remuneration

Committee (3 meetings)

Nominations Committee (1 meeting)

Customer Services

Committee (3 meetings)

Aman Dalvi (Chairman) ������ ��� ���

Graham Watts (Vice-Chairman)* ��� � � �

Paul Doona ������ ���� ���

Angela Horsman ������ ��� � ���

Stephen Jack ������ ���� ��� �

Lesley James ������ ��� �

Rima Makarem** ������ � ��� � �

Chris Wood ������ ���� ���

Key: � Attended �

18Annual Report and Financial Statements

CoRpoRAte GoveRnAnCe RepoRt

Audit & Risk Committee (A&RC)

The committee consists of at least three Non-Executive Directors, two of whom constitute a quorum. Appointments to the A&RC are for an initial period of three years and are extendable for two further three-year periods.

Graham Watts chaired the A&RC until June 2012 when Stephen Jack took over as Chairman. Its other members during the year were Paul Doona, Chris Wood, and from November 2012, Rima Makarem. The committee structure requires the inclusion of at least one Non-Executive Director with significant, recent and relevant financial experience. Both Paul Doona and Stephen Jack fulfil this requirement.

The committee has written terms of reference that set out its authority and responsibilities. These are considered annually by the committee and any proposed changes are referred to the Board for approval.

The committee’s primary role is to provide assurance to the Board on:• the integrity of the financial reporting and

the audit process; and

• the maintenance of a sound internal control and risk management system.

In pursuing these objectives, the committee:• monitors and assesses the role of the internal

and the external auditors;

• considers the effectiveness of the internal and the external audit processes;

• reviews Anchor’s systems of internal control and the processes for monitoring and evaluating the risks facing Anchor; and

• makes recommendations to the Board on the appointment of the internal and external auditors.

The Chairman of the committee orally reports the outcome of each meeting to the Board and the Board receives an annual written report on the committee’s activities. In addition, the committee undertakes an annual effectiveness review.

In performing its duties, the committee has independent access to the services of the internal and external auditors, and may obtain outside professional advice as necessary. The internal and external auditors have direct access to the Chairman of the committee.

The Chairman of the committee attends the Annual General Meeting to answer questions on the activities of the committee.

The auditors were engaged to provide a range of services to Anchor, including advice on employment tax, advice on VAT, quality assurance of development business cases and pensions.”

19For the year ended 31 March 2013

Corporate GovernanCe report

Report on the committee’s activities for the financial year 2013

Meetings and attendanceThe committee met on four occasions timed to coincide with the internal and external financial reporting cycles of Anchor.

The Chief Executive, the members of the Executive Management Board and senior representatives of the internal and external auditors attended meetings by invitation. At each meeting there was an opportunity for the external and internal auditors to discuss matters with the committee without any executive management being present.

Financial reportingDuring the year the committee reviewed a wide range of accounting and financial issues including the annual Financial Statements prior to submission to the Board. The committee focussed on key accounting policies and practices adopted by the organisation and any significant areas of judgement that materially affected the reported results.

External auditorsThe committee is responsible for the development, implementation and monitoring of Anchor’s policies on external audit. These policies are designed to maintain the objectivity and independence of the external auditors and the appointment of the external auditors to undertake non-audit work.

During the year the auditors were engaged to provide a range of services to Anchor apart from audit activity, including advice on employment tax, advice on VAT, quality assurance of development business cases and pensions. Each appointment was made taking into account the requirements of the Board’s policy on the use of the auditors for non-audit work to ensure the auditor’s objectivity and independence was safeguarded. The Board policy defines the non-audit services that are permitted to be carried out by auditors and the non-audit services that are prohibited to be carried out by auditors. The A&RC receives annual reports from the auditors describing the safeguards in place to maintain their independence and also receives an annual report from the Chief Financial Officer describing the non-audit work undertaken by auditors.

In accordance with its remit, the committee reviewed and approved:• the external auditor’s plans for the

audit of Anchor’s Financial Statements for 2012/13;

• the terms of engagement for the audit and the proposed audit fee and associated expenses; and

• the content of the formal annual audit letter provided by the external auditors and management’s response, including major issues that arose on the audit and their resolution.

Internal auditorsThe committee reviewed:

• the internal auditor’s plan for the year and the achievement of the plan;

• the adequacy of management’s response to the matters raised during the year in reports from the internal auditors, including the implementation of recommendations made; and

• reports on the adequacy and effectiveness of Anchor’s internal control and risk management procedures.

The committee receives reports on outstanding management actions to internal audit recommendations and follows up on the reasons for any actions being outstanding.

Whistle-blowingAnchor’s whistle-blowing policy sets out the arrangements for colleagues to raise concerns or complaints regarding accounting, risk issues, internal controls and related matters with relevant line management or senior company executives. These matters are advised to internal audit for consideration and reported to the committee as appropriate. Any matters considered sufficiently significant by the committee will be brought to the attention of the Board, which will decide how the matter will be handled, including referral to an external agency if appropriate.

The A&RC regularly reviews the arrangements in place for handling whistle-blowing cases, to ensure that they provide for the proportionate and independent investigation of issues raised and for appropriate follow-up action.

20Annual Report and Financial Statements

CoRpoRAte GoveRnAnCe RepoRt

Executive Remuneration Committee

The Executive Remuneration Committee consists of at least three Directors (all Non-Executive Directors of the Board), with a quorum of two. Membership is reviewed annually by the Chairman of the committee. The committee meet three times during the year.

Lesley James chairs the committee, which has benefitted from the membership of all the non-executive members of the Board. Its members are Aman Dalvi, Paul Doona, Angela Horsman, Stephen Jack, Rima Makarem and Chris Wood. No person other than the members of the committee is entitled to be present at meetings but others may be invited by the committee to attend. Neither the Company Secretary nor any members of the Executive Management Board are present when the committee considers matters relating to them.

The Executive Remuneration Committee is responsible for determining the pay and benefits and contractual arrangements for the Executive Management Board. The committee’s aims are to develop and recommend remuneration strategies that drive performance and reward it appropriately.

The committee has written terms of reference and its responsibilities are: • to determine on behalf of the Board

the organisation’s broad policy for executive remuneration;

• in doing so, to encourage the Executive Management Board to enhance the organisation’s performance and to ensure that they are fairly but responsibly rewarded for their individual contributions;

• by delegated authority from the Board, determine any changes to the remuneration including salary, bonus, and other emoluments and all terms and conditions of employment of the Chief Executive;

• by delegated authority from the Board, and taking into account the recommendation of the Chief Executive, determine any changes to the remuneration, including salary, bonus, any other emoluments, and all terms and conditions of employment relating to the Executive Management Board;

• to keep the service agreements and terms of engagement of executives under review;

• to comply with appropriate Codes of Best Practice, ensuring transparency and voluntarily having regard to the requirements for public companies and public sector organisations; and

• to report and account for their decisions by submitting minutes of meetings to the members of the Board and producing an annual statement on executive remuneration to be included in the Annual Report and Financial Statements of Anchor Trust.

The committee reviews its terms of reference annually and any proposed changes are referred to the Board for approval. The committee has an executive remuneration policy that sets out the objectives and the approach for the work of the committee. It states, “the objective of Anchor’s remuneration policy is to attract, retain and motivate high calibre senior executives through competitive pay arrangements which are also in the best interests of all stakeholders”. Total remuneration is benchmarked against a comparator group reflecting the market in which Anchor operates. Remuneration is targeted at a median position, moving to upper quartile for exceptional performance. It is assessed through personal objectives aligned to business key performance indicators, measured through the annual performance management process.

In 2012 the remuneration committee approved a bonus scheme for senior executives linked to the achievement of key business objectives. The targets include five areas which are critical to Anchor’s services – customer satisfaction, colleague engagement, income, surplus, and compliance and service delivery. These are weighted within the total bonus payment, and targets in each category are benchmarked to ensure excellence.

The committee also ensures that executive remuneration is aligned with the remuneration philosophy for all Anchor colleagues. It is underpinned by a stated set of common reward principles: performance delivery, alignment to strategy, competitive and motivating, equitable and fair, and value for money. The committee endorsed the Executive Management Board’s decision that from 1 April 2012 all Anchor colleagues are paid above the National Minimum Wage, with a commitment to progressing towards the

21For the year ended 31 March 2013

Corporate GovernanCe report

Living Wage. This supports Anchor’s objective of being an employer of choice and cements Anchor’s commitment to ensure customers receive high quality care from a motivated workforce.

The committee has access to such information and advice both from within Anchor and externally at the expense of Anchor as it deems necessary. During the year the committee sought advice from New Bridge Street consultants.

Nominations Committee

The committee consists of at least three Non-Executive Directors with a quorum of two. Membership is reviewed annually by the Chairman of the committee. The committee met once during the year.

Lesley James chairs the Nominations Committee. Its members are Angela Horsman, Rima Makarem and Chris Wood. No person other than the members of the committee is entitled to be present at meetings but others may be invited by the committee to attend.

The committee has written terms of reference, which include: • to maintain and regularly review a policy

on nominations to the Board;

• to comply with appropriate Codes of Best Practice.

The committee reviews its terms of reference annually and any proposed changes are referred to the Board for approval.

The committee noted that Anchor’s Board comprises seven members of whom three are women, and therefore complies with the ‘Women on Boards’ report for FTSE 100 companies, issued by Lord Davies in February 2011.

During the year, the committee interviewed candidates to succeed the Chairman who retires in September 2013 and recommended that Pamela Chesters be appointed to the role. The committee also recommended that David Slater join the Executive Management Board (EMB), in the new position of Director of Operations. The EMB members are classified as Directors in the Financial Statements, the emoluments for all these posts are included in Director emoluments, within note 8 to the Financial Statements. The total Director emoluments remain appropriate for an organisation of Anchor’s size and complexity – at 1.2% of total payroll and 0.5% of turnover.

The committee has access to such information and advice both from within Anchor and externally at the expense of Anchor as it deems necessary. Recruitment services were sought from an executive recruitment firm in relation to the appointments of Pamela Chesters and David Slater.

22Annual Report and Financial Statements

CoRpoRAte GoveRnAnCe RepoRt

Customer Services Committee (CSC)

The CSC is a committee of the Board. The chair of the committee is a customer elected by the members of the committee. The Board nominates one of its members to sit on the committee, and Aman Dalvi was nominated. Angela Horsman attends if he is unable to and Rima Makarem has also been nominated to attend. Other members of Anchor’s Board are also entitled to attend. The other members of the committee comprise of the chairs and deputy chairs of the eight regional customer forums.

A quorum constitutes 10 members. Members of the CSC are appointed for a period of three years, and this appointment can be renewed thereafter for a maximum period of six years.

The committee has written terms of reference, which include: • shaping housing management service

standards and service delivery;

• driving continuous improvement in the services provided to customers;

• scrutinising performance in the services provided to customers; and

• agreeing the content of the annual performance report made available to all rental housing customers.

The CSC reports to the Board quarterly with recommendations and the Board provides feedback to the CSC on previous recommendations. The Board may request the committee to consider particular issues and report back to the Board.

On 26 April 2012, the Board agreed that the CSC will comprise representation from Anchor’s care home and leasehold customers. The Board believes that the CSC is a more effective way of representing the needs of its customers than having customer Board members.

Internal control assurance statement

The BoardThe Board recognises and accepts its responsibility for Anchor’s system of internal control and reviewing its effectiveness. The Board demands a strong control environment that is designed to manage rather than eliminate the risk of failure to achieve Anchor’s business objectives and that provides reasonable assurance against material misstatement or loss. It accepts that a system of internal control cannot

23For the year ended 31 March 2013

Corporate GovernanCe report

provide absolute assurance against material misstatement or loss.

The Board, through the Audit & Risk Committee, has reviewed the effectiveness of Anchor’s internal controls and risk management for the year ended 31 March 2013 and up to the date of approval of these Financial Statements. There is a range of established strategic and operational policies that ensure Anchor is viable, well governed and well managed. These policies are supported by strong management structures and clear accountability, which have been strengthened further during the year.

The Board is satisfied that the system of internal control has been operating effectively for the year and there are no incidents of weaknesses leading to material loss, contingency or uncertainty that require separate disclosure in the Financial Statements.

Throughout the year under review, Anchor has operated an effective process for identifying, evaluating and managing the significant risks it faces. The process is subject to regular review to ensure it is effective in the face of changing external conditions and reflects actual experience and good practice. Continuing the practice of previous years, a self-assessment process was undertaken by senior managers. This ensures that managers are fully aware of the control environment and that controls are matched to risk levels. The process has identified key actions needed to ensure that the likelihood and/or impact of failure to achieve corporate objectives are reduced. Risk management processes have continued since the year end.

Audit & Risk Committee (A&RC)The A&RC has reviewed its terms of reference during the year to ensure that it continues to provide assurance to the Board on Anchor Trust’s financial reporting, internal control and risk management, internal audit arrangements and external audit arrangements.

The A&RC has monitored the integrity of the Financial Statements and reviewed the actions and judgements of management in their preparation before they were submitted to the Board for approval. The A&RC pays particular attention to strategic processes for risk management, internal control and governance, critical accounting policies and practices.

The A&RC has reviewed the effectiveness of the internal control systems and is satisfied that the policies in relation to financial control, delegated authority, treasury management, fraud detection and reporting, risk management, internal audit, project management, strategic planning, business planning, asset management and performance reporting contribute to an effective control environment.

In reaching this conclusion the A&RC has considered reports from external and internal auditors, specifically, the annual report of the company’s internal auditors in which the internal auditors state, “our work identified low, moderate and high rated findings. Based on the work completed, it believes that these are isolated to specific systems and processes and when taken in aggregate are not considered pervasive to the system of internal control as a whole”. The A&RC has also considered reports from external regulatory bodies such as the Care Quality Commission, Homes & Communities Agency and the Charity Commission and from quality assurance and accreditation bodies. It has also reviewed the fraud register maintained in accordance with regulatory requirements.

The A&RC regularly reviews the ‘whistle-blowing’ policy during the year and continues to have responsibility for oversight of this.

Executive Management Board (EMB)The Executive Management Board is responsible for the operation of the internal control environment within Anchor.

Risk management procedures are applied throughout Anchor to support the achievement of the organisation’s objectives, with key strategic risks and the action taken to mitigate them reported to the Audit & Risk Committee and the Board. Risk identification and mitigation planning is included in the business planning process and also in the project management methodology adopted across Anchor.

The Executive Management Board has been diligent in taking action to mitigate risk where this has been needed. Where improvements in internal control have been needed, steps have been taken to ensure that systems and controls are improved and that material error or misstatement has not occurred.

24Annual Report and Financial Statements

BOARD, DIRECTORS AND ADVISERS

Board, Directors and Advisers

Patron

HRH Princess Alexandra

Members of the Board*

ChairmanAman Dalvi OBE

Members Paul Doona Angela Horsman Stephen Jack Lesley James CBE Rima Makarem Chris Wood

Executive Management Board **

Chief ExecutiveJane Ashcroft

Chief Financial OfficerDavid Springthorpe

MembersDavid Edwards Sue Ingrouille Howard Nankivell David Slater (Appointed July 2012)

Registered Office

2nd Floor 25 Bedford Street London WC2E 9ES

External Auditors

KPMG LLP

Internal Auditors

PricewaterhouseCoopers LLP

Bankers

Lloyds Banking Group PLC

Investment Managers

Schroder Investment Management Limited

Solicitors

Eversheds LLP

Treasury Advisers

Traderisks Limited

* Members are classified as Directors for the purposes of the Companies Act 2006. ** Members of the Executive Board are not classified as Directors for the purposes of the Companies Act 2006.

25For the year ended 31 March 2013

Directors’ reportDIRECTORS’ REPORT

Directors’ Report Legal status

Anchor Trust is a company limited by guarantee (number 3147851). It is registered under the Housing Act 1996 (registration number LH4095) and is a charity (number 1052183).

Review of the business

A review of the business is provided in the Chairman’s statement, Chief Executive’s statement and the Operating and Financial Review.

Directors

The Directors at 31 March 2013 and the date of approval of the Financial Statements are those listed on page 24.

On 27 July 2012, David Slater filled the newly created post of Director of Operations and joined the Executive Management Board. On 31 August 2012 Ian Morris and Gill Powell left the Executive Management Board.

Employment – equality and diversity

Our people strategy aims to cultivate motivated and supported colleagues who understand how they contribute to the organisation. Anchor consults with employees, who are called colleagues, in a range of ways, both formally and informally.

Anchor strives to comply with employment legislation and seeks to ensure that we employ a richly diverse and skilled workforce.

Applications for employment by disabled persons are always fully considered, bearing in mind the aptitudes of the individuals concerned. In the event of colleagues becoming disabled, every effort is made to ensure their employment within Anchor is continued and any necessary adaptations to their working environment or routine are made.

Health and safety

Anchor recognises the importance of managing health and safety risks in order to keep customers and colleagues safe. Anchor’s health and safety performance continues to be satisfactory with

health and safety measures being included in the key performance indicators and compliance in areas such as gas safety, electrical safety and lift maintenance being consistently good. Senior management provide clear and strong direction in striving for high standards of health and safety compliance and there is a health and safety management system in place to achieve this. A health and safety plan is in place with clear targets to further improve health and safety performance.

Donations

Neither Anchor nor any of its subsidiaries made any charitable donations or political donations, or incurred any political expenditure during the year.

Creditor payment policy

It is Anchor’s policy to settle the terms of payment with any suppliers when agreeing the terms of each transaction; to ensure those suppliers are made aware of the terms of payment; and to abide by them. Generally Anchor pays its creditors within 30 days. At the year end, there were 22 days (2012: 22 days) worth of purchases in trade creditors.

Post balance sheet events

There were no post balance sheet events that require disclosure in the Financial Statements.

Going concern

After making enquiries and examining major areas which could give rise to significant financial exposure, the Directors are satisfied that no material or significant exposures exist other than as reflected in these Financial Statements and that Anchor has adequate resources to continue its operations for the foreseeable future. For this reason they continue to adopt the going concern basis in preparing the Financial Statements.

Our people strategy aims to cultivate motivated and supported colleagues.”

26Annual Report and Financial Statements

DiRectoRS’ RepoRt

Auditor

KPMG LLP has expressed its willingness to continue in office as auditor to Anchor. A resolution proposing their reappointment will be made at the Annual General Meeting.

Disclosure of information to auditors

The Directors who held office at the date of approval of this Directors’ Report confirm that, so far as they are each aware, there is no relevant audit information (as defined in Section 418(2) of the Companies Act 2006) of which the company’s auditors are unaware; and each Director has taken all the steps that they ought to have taken as a Director to make themselves aware of any relevant audit information and to establish that the company’s auditors are aware of that information.

Statement of Directors’ responsibilities in respect of the Directors’ Report and the Financial Statements

The Directors are responsible for preparing the Directors’ Report and the Financial Statements in accordance with applicable law and regulations.

Company law requires the Directors to prepare Financial Statements for each financial year. under that law they have elected to prepare the Financial Statements in accordance with uK Accounting Standards and applicable law (uK Generally Accepted Accounting Practice).

under company law, the Directors must not approve the Financial Statements unless they are satisfied that they give a true and fair view of the state of affairs of the company and of

the surplus or deficit for that period. In preparing these Financial Statements, the Directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and estimates that are reasonable and prudent; and

• state whether applicable uK Accounting Standards and Statements of Recommended Practice have been followed, subject to any material departures disclosed and explained in the Financial Statements.

The Directors are responsible for keeping adequate accounting records that are sufficient to show and explain the company’s transactions and disclose with reasonable accuracy at any time the financial position of the company and enable them to ensure that the Financial Statements comply with the Companies Act 2006, the Housing and Regeneration Act 2008 and the Accounting Direction for Private Registered Providers of Social Housing 2012. They have general responsibility for taking such steps as are reasonably open to them to safeguard the assets of the company and to prevent and detect fraud and other irregularities.

The Directors are responsible for the maintenance and integrity of the corporate and financial information included on the company’s website. Legislation in the uK governing the preparation and dissemination of Financial Statements may differ from legislation in other jurisdictions.

By order of the Board

David Edwards Company Secretary 25 July 2013

27For the year ended 31 March 2013

Independent AudItor’s report

Independent Auditor’s Report Independent auditor’s report to the members of Anchor Trust

We have audited the Financial Statements of Anchor Trust Group and Company (“the company”) for the year ended 31 March 2013 set out on pages 28 to 52. The financial reporting framework that has been applied in their preparation is applicable law and uK Accounting Standards (uK Generally Accepted Accounting Practice).

This report is made solely to the company’s members, as a body, in accordance with section 128 of the Housing and Regeneration Act 2008 and Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company’s members, as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditor

As explained more fully in the Directors’ Responsibilities Statement set out on page 26, the Directors are responsible for the preparation of the Financial Statements and for being satisfied that they give a true and fair view. Our responsibility is to audit, and express an opinion on, the Financial Statements in accordance with applicable law and International Standards on Auditing (uK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the Financial Statements

A description of the scope of an audit of Financial Statements is provided on the Financial Reporting Council’s website at www.frc.org.uk/auditscopeukprivate.

Opinion on Financial Statements

In our opinion the Financial Statements: • give a true and fair view of the state of affairs

of the company as at 31 March 2013 and of its surplus for the year then ended;

• have been properly prepared in accordance with uK Generally Accepted Accounting Practice; and

• have been prepared in accordance with the Companies Act 2006, the Housing and Regeneration Act 2008 and the Accounting Direction for Private Registered Providers of Social Housing 2012.

Opinion on other matters prescribed by the Companies Act 2006

In our opinion the information given in the Directors’ Report for the financial year for which the Financial Statements are prepared is consistent with the Financial Statements.

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

• adequate accounting records have not been kept, or returns adequate for our audit have not been received from branches not visited by us; or

• the Financial Statements are not in agreement with the accounting records and returns; or

• certain disclosures of Directors’ remuneration specified by law are not made; or

• we have not received all the information and explanations we require for our audit.

Chris Wilson Senior Statutory Auditor for and on behalf of KPMG LLP Statutory Auditor Chartered Accountants Arlington Business Park, Theale, Reading RG7 4SD 25 July 2013

28Annual Report and Financial Statements

FinAnciAl StAtementS

Consolidated Income and Expenditure Accountfor the year ended 31 March 2013

Note2013 £’000

2012 £’000

Turnover:Continuing operations Discontinued operations

264,851

–

263,756

3,706

Total turnover 4 264,851 267,462

Operating costs 4 (246,742) (242,071)

Operating surplus: Continuing operations Operating deficit: Discontinued operations

18,109 –

25,534 (143)

Operating surplus before exceptional items 4 18,109 25,391Exceptional items 5 34 451

Operating surplus: Continuing operations Operating surplus: Discontinued operations

18,109 34

25,534 308

Operating surplus 18,143 25,842

Surplus on disposal of fixed assets 14 8,192 3,721

Surplus on disposal of discontinued operations 4 – 323

Interest receivable and other income 10 3,350 2,874

Interest payable and similar charges 11 (7,860) (10,562)

Surplus for the year 21,825 22,198

Statement of total recognised surpluses and deficits Note2013 £’000

2012 £’000

Surplus for the year Actuarial loss on pension fund

26

21,825 (7,461)

22,198 (12,467)

Total recognised surplus for the year 14,364 9,731

Note of historical cost surpluses and deficits Note2013 £’000

2012 £’000

Reported surplus for the year Realised investment gains

15

21,825 (545)

22,198 (149)

Historical cost surplus for the year 21,280 22,049

The accompanying accounting policies and notes on pages 32 to 52 form an integral part of these Financial Statements.

29For the year ended 31 March 2013

Financial StateMentS

Consolidated Balance Sheetas at 31 March 2013

2013 2012

Note £’000 £’000 £’000 £’000

Intangible Fixed Assets

Goodwill 13 102 153

Tangible Fixed Assets

Housing properties – gross cost less depreciation Less: Social housing grant

Other capital grants and receipts

14 14 14

887,745 (520,211) (44,643)

891,161 (525,016) (47,659)

322,891 318,486

Other tangible fixed assets 14 2,622 1,734

Investments 15 3,423 2,878

329,038 323,251

Current Assets

Stocks 16 2,732 5,802

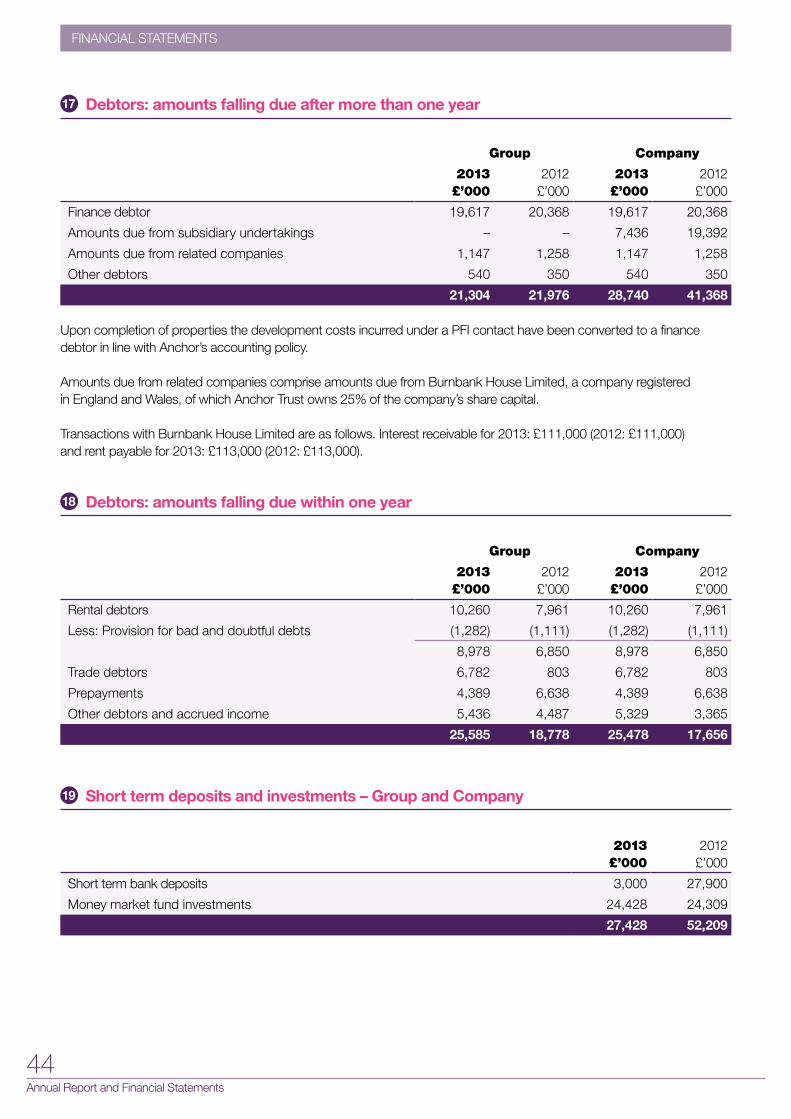

Debtors: amounts due after more than one year 17 21,304 21,976

Debtors: amount due within one year 18 25,585 18,778

Short term deposits and investments 19 27,428 52,209

Cash at bank 66,208 30,496

143,257 129,261

Creditors: amounts falling due within one year 20 (50,337) (47,904)

Net current assets 92,920 81,357

Total assets less current liabilities 421,958 404,608

Creditors: amounts falling due after more than one year 21 142,929 141,876

Provisions and pension liability

Provisions for liabilities and charges 22 1,216 1,726

Pension liability 26 39,224 36,779

Capital and Reserves

Restricted reserves 28 355 357

Income and Expenditure Reserve 28 238,234 223,870

421,958 404,608

The Financial Statements on pages 28 to 52 were approved by the Board on 25 July 2013 and signed on its behalf by:

Stephen Jack DirectorAman Dalvi OBE Chairman

30Annual Report and Financial Statements

FinAnciAl StAtementS

Company Balance Sheetas at 31 March 2013

2013 2012

Note £’000 £’000 £’000 £’000

Intangible Fixed Assets

Goodwill 13 53 104

Tangible Fixed Assets

Housing properties – gross cost less depreciation Less: Social housing grant

Other capital grants and receipts

14 14 14

888,171 (520,211) (44,643)

878,916 (525,016) (47,659)

323,317 306,241

Other tangible fixed assets 14 2,622 1,734

Investments 15 3,423 2,878

Investments in subsidiary undertakings 15 2,301 2,301

331,716 313,258

Current Assets

Stocks 16 2,732 5,802

Debtors: amounts due after more than one year 17 28,740 41,368

Debtors: amounts due within one year 18 25,478 17,656

Short term deposits and investments 19 27,428 52,209

Cash at bank 63,782 29,621

148,160 146,656

Creditors: amounts falling due within one year 20 (49,266) (45,536)

Net current assets 98,894 101,120

Total assets less current liabilities 430,610 414,378

Creditors: amounts falling due after more than one year 21 142,929 141,876

Provisions and pension liability

Provisions for liabilities and charges 22 1,216 1,726

Pension liability 26 39,224 36,779

Capital and Reserves

Restricted reserves 28 355 357

Income and Expenditure Reserve 28 246,886 233,640

430,610 414,378

The Financial Statements on pages 28 to 52 were approved by the Board on 25 July 2013 and signed on its behalf by:

Stephen Jack DirectorAman Dalvi OBE Chairman

31For the year ended 31 March 2013

Financial StateMentS

Consolidated Cash Flow Statementfor the year ended 31 March 2013

Note2013 £’000

2012 £’000

Net cash inflow from operating activities 29.1 41,831 49,558

Returns on investments and servicing of finance

Net cash outflow from returns on investments and servicing of finance

29.4 (5,457) (3,617)

Capital expenditure and finance investment

Net cash outflow from capital expenditure and financial investment 29.4 (25,259) (47,925)

Net cash inflow / (outflow) before use of liquid resources and financing 11,115 (1,984)

Management of liquid resources

Net cash inflow / (outflow) from management of liquid resources 29.4 24,781 (3,164)

Net cash inflow / (outflow) before financing 35,896 (5,148)

Financing

Net cash (outflow) / inflow from financing 29.4 (184) 24,652

Increase in cash 35,712 19,504

The accompanying accounting policies and notes on pages 32 to 52 form an integral part of these Financial Statements.

32Annual Report and Financial Statements

FinAnciAl StAtementS

1 Basis of accounting

The Financial Statements have been prepared on a going concern basis under the historical cost convention as modified by the revaluation of fixed asset investments and in accordance with accounting standards applicable in the united Kingdom.

They have been prepared in accordance with the Accounting Direction for Private Registered Providers of Social Housing 2012.

2 Basis of consolidation

The Group Financial Statements comprise those of Anchor Trust and its subsidiary undertakings.

3 Principal accounting policies

i) Turnover

Turnover is net of voids and Value Added Tax and includes:• Rents and service charges from

social housing lettings and leasehold management

• Residential care home charges• Home care charges• Revenue grants• Sales of leasehold properties• Supporting People contract income.

Turnover has been analysed in accordance with the requirements of the Accounting Direction for Private Registered Providers of Social Housing 2012 (see note 4).

Charges for services provided and Supporting People income are recognised as income when Anchor has provided the service concerned. Grants made as contributions to revenue expenditure are credited to income in the period in which the related expenditure is incurred.

Notes to the Financial Statementsfor the year ended 31 March 2013