Embed Size (px)

Citation preview

Forward facing retailers continue to leverage next-gen analytics engines to accurately predict shopper behavior

Forward facing retailers continue to leverage next-gen analytics engines to accurately predict shopper behavior

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

A N R I S N E W S C U S T O M R E S E A R C H R E P O R T

risIBM_CustResearchReport_3.indd 1 10/22/15 11:48 AM

Advanced analytics is the way for-ward for retailers seeking to stay competitive in a world transformed by the likes of Amazon and Google and empowered, device-wielding consumers. Never has it been more critical to understand, and even better, predict consumer behaviors and adjust the retail organization to suit. Retailers are eager to mine their growing mountains of data for nuggets of insight that will enable them to create personalized, pleas-ing experiences that keep consum-ers coming back.

Dr. Andreas Weigand, founder and director of the Social Data Lab, says: “Data is the new oil, and just like oil you need to refi ne it.” Ac-cording to the retail tech guru, the abundance of crude oil (data) is vir-tually useless until it is processed and developed into something infi -nitely more valuable.

To gauge retailers’ progress in at-taining the sophisticated data analyt-ics capabilities needed to transform their own data in the merchandising arena, RIS News surveyed a select group of executives, partnered with IBM to identify key trends in mer-chandising analytics.

Analytics Confi dence is HighEffective use of data in retail typi-cally supports three desired out-comes: increased sales, decreased costs and increased productivity. Across disciplines, retailers report a high degree of confi dence in their current level of analytics sophistica-tion toward these goals (Figure 1).

WHERE DO YOU PLACE YOUR ORGINIZATION’S OVERALL ANALYTICS CAPABILITIES IN THE FOLLOWING CORE RETAIL APPLICATIONS?

FIGURE 1

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

2

MERCHANDISING 18% 63% 18% 3%

SUPPLY CHAIN 3%18% 67% 13%

MARKETING 5%8% 77% 10%

CUSTOMERMANAGEMENT 13% 62% 26%

PRICING/PROMOTIONS 3%23% 59% 15%

MARKDOWNDECISIONS 3%18% 72% 8%

STORE PERFORMANCE 10% 54% 36%

LABOR/WORKFORCEMANAGEMENT 18% 49% 33%

BASIC/REACTIVE: We know what happened

ADVANCED/PROACTIVE: We know what/who made it happen

SOPHISTICATED/PREDICTIVE: We know what will happen next

SOPHISTICATED/PRESCRIPTIVE: We know how to make it happen

risIBM_CustResearchReport_3.indd 2 10/22/15 11:48 AM

We asked retailers to rate their ana-lytics capabilities across disciplines on a four-point scale starting with basic/reactive and ending with so-phisticated/prescriptive (we know how to make it happen). In every category, the majority ranked their capabilities as advanced, meaning they know what happened and who made it happen.

Retailers are investing in solu-tions that support customer centric-ity and winning customer loyalty through a unique value proposition, and therefore ranked their market-ing analytics capability as most so-phisticated. Just 8% called these ca-pabilities basic/reactive, while this was the category with the largest number of those with sophisticated/prescriptive capabilities. However when it comes to markdown deci-sions for assortments inside the store, only 11% of them use pre-dictive and prescriptive analytics. These retailers recognized early on that attaining their customer goals would require advancing their abil-ity to develop deeper insights.

Gartner reports that by 2016, 89% of companies believe that customer experience both in store and out will be their primary ba-sis for competition, according to its report, “Predicts 2015: Digital Marketers Will Monetize Disruptive Forces.”

Pricing and promotion decision analytics has the largest number of basic, reactive users — but is also among the handful of categories

in which some are most advanced. This is among the newest applica-tion areas for sophisticated analyt-ics, with dynamic pricing for e-com-merce emerging only over the last few years. Those retailers feeling the most direct threat from the consider-able analytics talents of Amazon are most likely those to invest quickly in this level of capability, regardless of the size of the organization.

Store performance and labor/workforce management had the largest percentages of respondents at the sophisticated/predictive level, but these are areas that are very dif-fi cult for retailers to advance further. As major shifts such as buy online/pick up in store shift responsibili-ties and metrics, older metrics con-stantly become outdated, impacting labor standards.

Priorities and Pain PointsThe past few years have brought a host of new data types into retail, and retailers have been vocal about

· Integrating unstructured data

· Integrating data from multiple sources

· Making right merchandise and assortment decisions

· Interpreting results/strategy plan

· Lack of measurable results

FIGURE 2

RETAILERS’

TOP ANALYTICS

PAIN POINTS

More accurate and relevant merchandising

RETAILERS TOP ANALYTIC PRIORITIES THAT ARE THE BASIS FOR CREATING STRATEGIC AND BUDGET PLANS

Improve customer retention/loyalty

Increase marketing/ promotion effectiveness

Increase customer engagement through personalization

FIGURE 3

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

3

risIBM_CustResearchReport_3.indd 3 10/22/15 11:48 AM

the challenge of transforming it all into actionable insights. Integrat-ing unstructured data such as social and weather data is by far retailers’ biggest pain point, cited by 57.5% of respondents (Figure 2). The next biggest source of pain is integrating data from multiple sources (32.5%), followed by making the right mer-chandise and assortment decisions at the store level (22.5%). Both should change through the steady increase in the power of tools to each of these areas.

Relatively few call identifying and predicting product lines/categories that make most sense to promote to-gether a top pain point (7.5%), at least in comparison to the data manage-ment issues cited above.

Although retailers understand that driving lifetime customer val-ue is critical, when asked to name their top analytics priorities, only 22.5% sighted more accurate and relevant merchandising (Figure 3). Since having the right merchandise at store level plays a critical role in increasing lifetime value of custom-ers, merchants must increase their

investment in such analytics. The challenge of customer loyalty

has not been effectively addressed by most retailers to this day. Retail-ers are recognizing that driving true retailer “brand” loyalty must go be-yond the traditional mass, untargeted discount programs still in the major-ity of stores.

The next two priorities link closely to this: Increasing market/promotion effectiveness and increasing custom-er personalization were tied at 25%. Close behind was more accurate and relevant merchandising (22.5%) — all key activities for enhancing customer value and experience.

Interestingly, improving price an-alytics ranked relatively low among merchandisers’ priorities, most like-ly only in comparison to identifying customer shopping preferences and managing data; pricing is of critical importance to most merchandisers.

Science vs. ArtMerchandisers have debated for de-cades the proper balance between intuition and data when it comes to making decisions. But in the age of advanced analytics, the scales appear to be shifting toward data science.

This is particularly the case for building micro assortments. It’s not enough to allocate by A-B-C store types: individual variations in store histories and markets mean it pays to drill deeper into data to ensure just the right mix. As seen in Fig-ure 4, a majority of retail respon-dents rely more heavily on analytics versus experience and intuition to

FIGURE 4

55%Merchants make micro assortment decisions based on analytics versus experience and intuition

make these decisions (55%).Promotions was the next catego-

ry where merchandisers are more likely to lean toward analytics over experience (37.5%). Pricing was the least likely analytics-driven activity. With recent new advances in pricing tools, however, retailers’ confi dence on the recommendations they see in pricing analytics dashboards can be expected to grow.

These fi ndings confi rm the tip-ping of the scales toward analysis when it comes to what was once the art of merchandising. Retail Systems Research call this part of “the next dramatic shift in the retail business model. The enterprise is becom-ing more scientifi c, more numbers-oriented and paradoxically, more focused on employee enablement,” according to “Advanced Analytics: Retailers Fixate on the Customer.”

How Merchandisers Use Analytics ToolsMerchandisers are more likely to ap-ply analytics when they have easy access to analytics tools that allow

72.5%Merchants have direct access to analytics and are not reliant on others to fi nd insights for them

FIGURE 5

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

4

risIBM_CustResearchReport_3.indd 4 10/22/15 11:48 AM

them to create their own, custom-ized reports. To make this possible, many organizations have shifted responsibility for accessing data from IT to merchandising: 72.5% of respondents report that merchandis-ers have direct access to data, com-pared to just 27.5% where they must rely on others to fi nd insights.

As Figure 5 reveals, today’s mer-chandisers are most likely to lever-age analytics for promotions (55%). This is consistent with previous fi nd-ings regarding the higher level of in-vestment in sophisticated marketing analytics, since promotion is where merchandising and marketing meet.

Promotions have traditionally been the area in which marketers say, “Fifty percent of my marketing is working, I just don’t know which fi fty percent.” With the ability to ap-ply analytics capabilities such as lift analytics and social merchandising to this data, it’s clear that merchants are embracing the opportunity to disrupt

this paradigm to gain tangible ROI on their promotional activities.

Other areas of current analyt-ics use by merchandisers include store-level merchandising analytics (37.5%), where analytics are highly effective for tasks such as creat-ing planograms, and markdown decisions for specifi c product-line/category (25%) and real-time price changes (25%).

Looking deeper, in Figure 6 the majority of respondents rat-ed their organizations at par on a broad range of merchandising dis-ciplines. Social media marketing has the largest group rating their use of data-driven analytics as ad-vanced (29%), but it was also an area with a large group of laggards (26%). Retailers need to leverage social media analytics to identify the metrics that matter and get a better view of their performance relative to their peers.

An equal percentage of respon-

FIGURE 6

HOW ARE ANALYTICS LEVERAGED TODAY?

55% 37.5% 35% 25% 22.5%Promotions Merchandising Real-time price

changes Markdown decisions for specifi c product-line/category

Assortment planning

dents (29%) rate their analytics ca-pabilities in personalized market-ing as advanced, in keeping with previous fi ndings about the impor-tance of customer-centric analytics capabilities. This can be considered an Amazon effect, as those feeling the heat from the e-tailer are com-pelled to keep up with their person-alization engines.

About a quarter of respondents rank their promotion campaign man-agement (26%) and SKU optimiza-tion analytics capabilities (24%) as advanced, followed closely by mer-chandise planning and demand fore-casting (23% each).

Retailers have the most catch-ing up to do in mobile conversion, where the majority of respondents (53%) say their analytics capabili-ties lag. Retail industry analysts have been warning for some time that mobile shopping is growing rapidly. Gartner, for example, says that as of January 2015, U.S. cus-

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

5

risIBM_CustResearchReport_3.indd 5 10/22/15 11:48 AM

tomers’ mobile engagement be-havior was driving 22% of digital commerce revenue, but by 2017, this will rise to 50%. Retailers are well aware of their inability to keep up with consumers’ ever-changing mobile shopping patterns.

Productivity monitoring also had a sizeable groups of laggards (37%); as stated previous, constant-ly changing store requirements, particularly related to omnichannel, make this a tough area in which to stay current.

Analytics Wish ListThe survey asked retailers to identify the top fi ve areas they see as valu-able sources of data in the future. Given retailers’ admitted defi cits in mobile analytics, it’s not surprising that respondents see mobile analyt-ics as the clear leader as a top source (62.5%). (Figure 7)

Interaction data from sources such as call centers and e-mail rank next highest (40%). This data consists of both structured and un-structured data; as previous results

FIGURE 7

RETAILERS RATE THEMSELVES ON WHICH BUSINESS FUNCTIONS THEY EFFECTIVELY LEVERAGE DATA-DRIVEN ANALYTIC CAPABILITIES

reveal, harnessing the latter re-mains a big challenge for retailers’ analytics efforts, but one that prom-ises value as tools and processes emerge to normalize and analyze it.

Other vital sources of future value include proven areas such as web analytics (37.5%) and POS and order history data (32.5%) as well as social media data (30%), an area of considerable focus for analyt-ics investment. The jury is still out on the analytics value of data from emerging technologies including video analytics (2.5%) and micro-location (5%).

Putting Resources in PlaceAnother important measure of re-tailers’ commitment to increasing their analytics acumen can be seen in their investment in supporting re-sources. The emphasis on analytics for marketing and customer experi-ence is refl ected in the 29.7% that place ownership of merchandising analytics under the purview of the chief marketing offi cer; retail “lead-ers” were much more likely to place it here. In addition, nearly one in fi ve (18.9%) put ownership of the organi-zation’s analytics activity under the ownership of the VP of loyalty/CRM — this was much more likely at $1 billion-plus retailers.

Another sizeable group (21.6%), however, have created a VP of ana-lytics title to oversee analytics, im-plying that analytics is viewed as an enterprise-wide initiative.

When it comes to budget, while 45% of the respondents spend 1% to

ADVANCED

LAGGING

PERSONALIZED MARKETING

SOCIAL MEDIA MARKETING

PROMOTION CAMPAIGN MANAGEMENT

SKU OPTIMIZATION

MOBILE CONVERSION RATES

PRODUCTIVITY MONITORING (HR)

SOCIAL MEDIA MARKETING

PROCUREMENT/VENDOR MANAGEMENT

29%

29%

26%

24%

37%

26%

23%

53%

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

6

risIBM_CustResearchReport_3.indd 6 10/22/15 11:48 AM

5% of their IT budgets on develop-ing their analytics capabilities, the big fi nding is that half are spending more than 5% (Figure 8). A signifi -cant 20% are investing much more aggressively, spending 15% to 20% of their IT budgets. This group is dominated by retailers with annual sales of $1 billion or more.

This confi dence is testimony to Dr. Weigend’s assertion about data as the new oil. Retailers are acting decisively to increase their analyt-

ics acumen so they can compete on today’s most prized competitive playing fi eld, the affections of the customer.

The Analytics PayoffMany retailers see analytics as the key to unlocking the customer in-sights that will help them compete. They are well aware of the customer surveys that consistently show that more relevant engagement would increase their loyalty. So the survey asked retailers to postulate, “If you are not the market leader for your re-tail segments in engagement, what sales increase do you anticipate would occur if you were equivalent to the market leaders in your analyt-ics capability?” In other words, what is the payoff from analytics that make retail content more engaging for the customer?

The overwhelming response, by 67.5%, was a 5% to 10% increase in sales — a very signifi cant gain. One in fi ve retailers foresees even stron-ger results, of 10% to 20%. These results make clear the high level of confi dence that merchandisers feel

FIGURE 8

MOST VALUABLE SOURCES OF DATA TO USE IN THE FUTURE

Mobile

Interaction Data(E-MAIL, CALL CENTER, ETC)

Web Analytics

POS and Order History

Social Media

MOST VALUABLE SOURCES OF DATA TO USE IN THE FUTURE

TOP5

45

321

FIGURE 9

PRIMARY OWNER/LEADER OF THE ORGANIZATION’S ANALYTIC RESPONSIBILITIES

29.7% 21.6% 18.9%

CHIEF MARKETING

OFFICER

VP OF ANALYTICS

VP OF LOYALTY/CRM

in the power of analytics as a tool to help them make signifi cant strides toward achieving their enterprise-wide goals.

Establishing Analytics ArchitectureAs the trajectory for the explosion in data types and analytics technolo-gies became clear over the past few years, retailers have been concerned about the mechanics of amassing, cleaning, storing and evaluating this data: Would the in-house approach of the past continue to serve this rapidly expanding need?

Retailers say no. Right now, for the majority (57.5%) the dominant analytics platform is internally host-ed and managed (Figure 9), but as seen in Figure 10, this will give way to a hybrid of internal and external architecture over the next two to fi ve years.

The hybrid approach addresses two common concerns: the volume and security of data. Retailers are most likely to keep the most sensi-tive data in house, while outsourc-ing the heavy lifting of the majority

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

7

risIBM_CustResearchReport_3.indd 7 10/22/15 11:48 AM

to third party partners. Use of cloud and SaaS will also

grow from 7.5% today to 17.6% in a few years’ time, particularly among retail leaders, while outsourcing to third parties will remain pretty con-sistent.

Retailers, like most companies in other industries, are looking to lever-age their IT investments to ensure cost-effective, yet high-performance capabilities for now and in the fu-ture. Many see cloud and SaaS as important ways to implement these strategies.

Top Analytics ProjectsEnriching their analytics is a top priority for many retailers, but the scope is broad. The trend is toward investing in those areas that will ad-vance customer-centric goals and help them differentiate the brand.

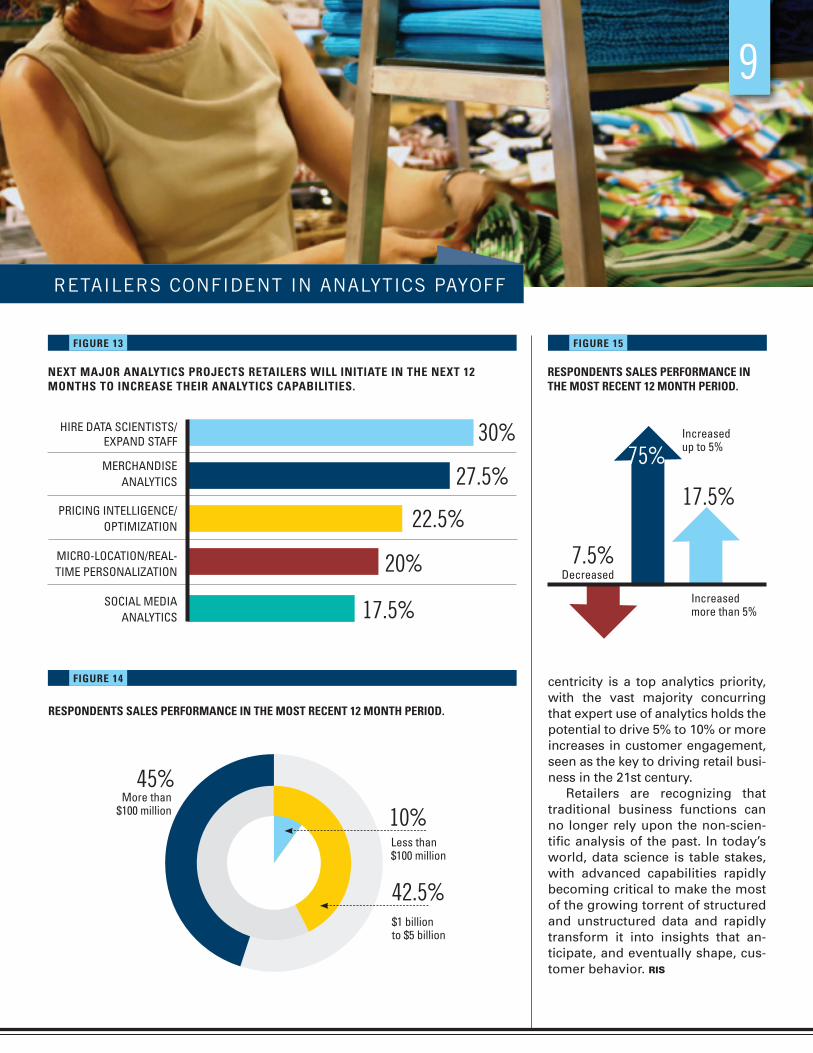

In addition to architecture, re-tailers have identifi ed staffi ng as a critical building block for analytics programs. Hiring data scientists and expanding staff is the top-ranked planned analytics project (Figure 10).

Esteban Arcaute senior director and head of data science at Walmart, says that despite the widespread belief that retailers must hire data scientists to achieve their analyt-ics vision, other data professionals can handle a signifi cant portion of retail analytic work. Data scientists are best leveraged to solve business problems, not manage day-to-day analytics workfl ows. That’s good news, given the extremely high de-mand for data science talent.

Merchandisers are the next most likely to be planning projects in mer-chandise analytics, followed by price intelligence/optimization, micro-lo-cation/real-time personalization and social media analytics. This aligns well with the priorities cited in Fig-ure 3 — improving customer reten-tion and loyalty, increasing market-ing and promotion effectiveness and increasing customer engagement through personalization.

Data Analytics Competence, Confi dence on the RiseRetailers’ confi dence in their ana-lytics abilities is growing alongside their sophistication, particularly in areas such as social media market-ing. A signifi cant number are invest-ing sizeable portions of their budgets in moving up the analytics maturity curve and creating senior-level posi-tions to oversee their efforts. Many still struggle with the mechanics of harnessing multiple data streams, but continue to drive forward, eye-ing hybrid IT environments as the way forward. Enhancing customer

FIGURE 11

50%Retailers that currently spend 5% or more of annual IT budget on developing analytics capabilities.

FIGURE 10

ARCHITECTURE APPROACH TO THEIR ANALYTIC HARDWARE AND SOFTWARE RETAILERS DESCRIBE AS THE MOST DOMINANT IN THEIR ORGANIZATION TODAY?

• Internally hosted and managed • Hybrid of internal and external • Outsourced to third-party providers • Cloud data services and SaaS applications

57.5%25%

10%7.5%

FIGURE 12

WHERE RETAILER’S ARCHITECTURE APPROACH IS HEADED IN 2 TO 5 YEARS

• Hybrid of internal and external • Cloud data services and SaaS applications• Outsourced to third-party providers • Internally hosted and managed

67.7%17.6%

11.8% 2.9%

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

8

risIBM_CustResearchReport_3.indd 8 10/22/15 11:48 AM

centricity is a top analytics priority, with the vast majority concurring that expert use of analytics holds the potential to drive 5% to 10% or more increases in customer engagement, seen as the key to driving retail busi-ness in the 21st century.

Retailers are recognizing that traditional business functions can no longer rely upon the non-scien-tifi c analysis of the past. In today’s world, data science is table stakes, with advanced capabilities rapidly becoming critical to make the most of the growing torrent of structured and unstructured data and rapidly transform it into insights that an-ticipate, and eventually shape, cus-tomer behavior. RIS

FIGURE 13

NEXT MAJOR ANALYTICS PROJECTS RETAILERS WILL INITIATE IN THE NEXT 12 MONTHS TO INCREASE THEIR ANALYTICS CAPABILITIES.

RETAILERS CONFIDENT IN ANALYTICS PAYOFF

9

RESPONDENTS SALES PERFORMANCE IN THE MOST RECENT 12 MONTH PERIOD.

RESPONDENTS SALES PERFORMANCE IN THE MOST RECENT 12 MONTH PERIOD.

FIGURE 14

30%

27.5%

22.5%

20%

17.5%

HIRE DATA SCIENTISTS/EXPAND STAFF

MERCHANDISE ANALYTICS

PRICING INTELLIGENCE/OPTIMIZATION

MICRO-LOCATION/REAL-TIME PERSONALIZATION

SOCIAL MEDIA ANALYTICS

7.5%

75%

17.5%

Increased up to 5%

Increased more than 5%

Decreased

10%

42.5%

45%

Less than$100 million

More than$100 million

$1 billion to $5 billion

FIGURE 15

risIBM_CustResearchReport_3.indd 9 10/22/15 11:48 AM

ABOUT IBM

IBM is a globally integrated technology and consulting company headquar-tered in Armonk, New York. With operations in more than 170 countries, IBM attracts and retains some of the world’s most talented people to help solve problems and provide an edge for businesses, governments and non-profi ts.

Innovation is at the core of IBM’s strategy. The company develops and sells software and systems hardware and a broad range of infrastructure, cloud and consulting services.

Today, IBM is focused on fi ve growth initiatives - Cloud, Big Data and Analytics, Mobile, Social Business and Security. IBMers are working with customers around the world to apply the company’s business consulting, technology and R&D expertise to enable systems of engagement that deliver dynamic insights for businesses and governments worldwide.

For more information about IBM Analytics for Retail, visit:ibm.com/analytics/us/en/industry/retail/index.html

Follow us on Twitter at:@IBMRetail, @IBManalytics and @IBMbigdata and at www.ibmbigdatahub.com and ibm.com/retail.

Join the conversation:#ibmanalytics and #ibmbigdata

risIBM_CustResearchReport_3.indd 10 10/22/15 11:49 AM