Embed Size (px)

Citation preview

Akorn, Inc. N a s d a q : A K R X

May 2014

Bank of America Merrill Lynch 2014 Health Care Conference

2

DISCLAIMER

• This presentation includes certain forward-looking statements regarding our views with respect to our business, operations, current and future acquisitions, economic model, and our expected performance for future periods, as well as the pharmaceutical industry conditions. These statements are intended as “forward-looking statements” under the Private Securities Litigation Reform Act of 1995.

• Actual results may differ materially from our expectations due to the risks, uncertainties and other factors that affect our business. These factors include, among others, changing market conditions in the overall economy and the industry; the success of implementing our corporate strategies; the effects of federal, state and other governmental regulation on our business; current and future litigation; the success of new acquisitions and new product launches; our success in developing, manufacturing, acquiring and marketing new products; the success of our strategic partnerships for the development and marketing of new products; our ability to obtain and maintain regulatory approvals for our products; and the effects of competition from other generic pharmaceuticals and from other pharmaceutical companies; loss of key personnel; our ability to obtain additional funding or financing to operate and grow our business; our liquidity; and other factors detailed in our Annual Report on Form 10-K and our other reports filed from time to time with the Securities and Exchange Commission (“SEC”).

• These factors also include factors specific to our pending acquisition of Hi-Tech Pharmacal Co., Inc. (“Hi-Tech”), including the occurrence of any event, change or other circumstances that could give rise to the termination of the merger agreement with Hi-Tech; the failure to satisfy conditions to completion of the merger, including receipt of regulatory approvals; changes in the business or operating prospects of Hi-Tech; our ability to successfully integrate Hi-Tech businesses and its products; and other factors related to the acquisitions and integration of Hi-Tech.

• If any of these risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may vary significantly from what we projected. Any forward-looking statement you see or hear during the presentation reflects Akorn, Inc.’s current views with respect to future events and is subject to these and other risks, uncertainties, and assumptions. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made.

• For more complete information about Akorn, you should read the reports filed by Akorn with the SEC. You may get these documents for free through EDGAR on the SEC website at www.sec.gov, which you may also access through our website at http://www.akorn.com.

• You should also read the reports filed by Hi-Tech with the SEC which are similarly available through EDGAR and Hi-Tech’s website at http://www.hitechpharm.com.

3

COMPANY OVERVIEW

Who We Are…

Fast growing niche pharmaceutical company

with proven execution of strategic initiatives

and focus on niche dosage forms

Increasingly diverse product portfolio including

injectables, ophthalmics, oral liquids, nasal

sprays and topical creams and ointments

Extensive line of OTC branded products and

growing line of store-branded private label

products

73 products on file with FDA representing an

addressable market of over $6.8bn

Over 1,500 employees

Distribution to over 20 countries; global

opportunity through Akorn India

Hospital / Injectables

33%

Contract 4%

$86 $137

$256 $318

$1 Billion

2010 2011 2012 2013 2014E Goal

$540-$560

G

U

I

D

A

N

C

E

Top-Line Momentum Building…

Headquarters: Lake Forest, IL

R&D: Vernon Hills, IL Copiague, NY

Diverse Manufacturing: Somerset, NJ Amityville, NY Decatur, IL Paonta Sahib, India

L

O

N

G

T

E

R

M

G

O

A

L

~ 60% CAGR 2010-2014E

4

Pace of consolidation to continue in specialty pharma & generics

Generic market opportunity remains strong (generics ~83% of Rx volume)*

Elevated scrutiny on both regulatory environment & approval process

Over 100 drugs currently on FDA shortage list, majority are sterile injectables

Globalization provides new opportunities in high growth emerging markets

Commitment to R&D, recent acquisitions and focused growth strategy support Akorn’s position as a key generics player

*Data from IMS - YTD September 2013

MARKET DYNAMICS & OPPORTUNITY

Focus on quality and robust R&D processes enables continued success and supports future growth

Akorn produces over a dozen products that have appeared on the FDA shortage list; the approval of Akorn India will increase overall injectable capacities for the U.S. market

Acquisition of manufacturing assets in India have positioned Akorn to pursue a global strategy over the long-term

Successful business transformation has positioned company well to be a key acquirer in the industry

5

Be #1 in generic ophthalmics

Be a top 5 player in generic injectables

Increase market leadership position for niche, non-sterile dosage forms

Expand sales reach to over 30 countries

Become a $1 billion revenue company

STRATEGIC GOALS

US Generic Ophthalmology Competitive Landscape

# 15 in Sales # 10 in Molecules

US Generic Injectable Competitive Landscape

IMS Data for 12 months ended 10/31/13. Some data may have been excluded based on company judgment of comparability.

TOD

AY

3

– 5

YEA

R G

OA

LS

# 3 in Sales and Molecules

6 6

MANUFACTURING

CAPACITY

LEVERAGE

INFRASTRUCTURE

FOCUS ON OPHTHALMOLOGY

EXPAND NICHE

PORTFOLIO

ACCESS TO OTHER

GEOGRAPHIES

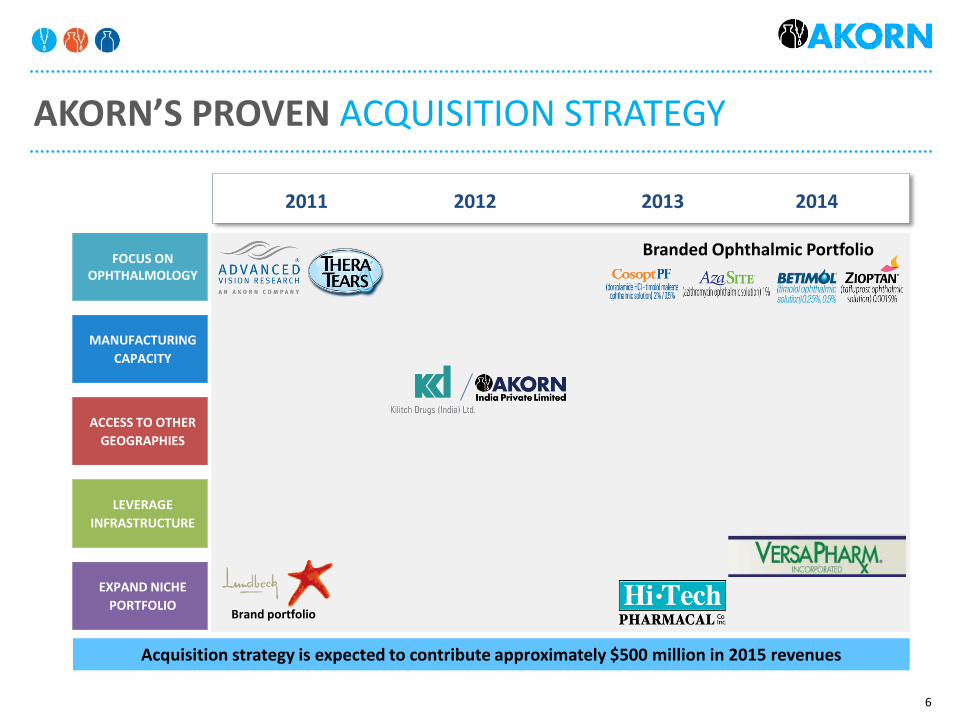

AKORN’S PROVEN ACQUISITION STRATEGY

2011 2012 2013 2014

Acquisition strategy is expected to contribute approximately $500 million in 2015 revenues

Brand portfolio

Branded Ophthalmic Portfolio

7

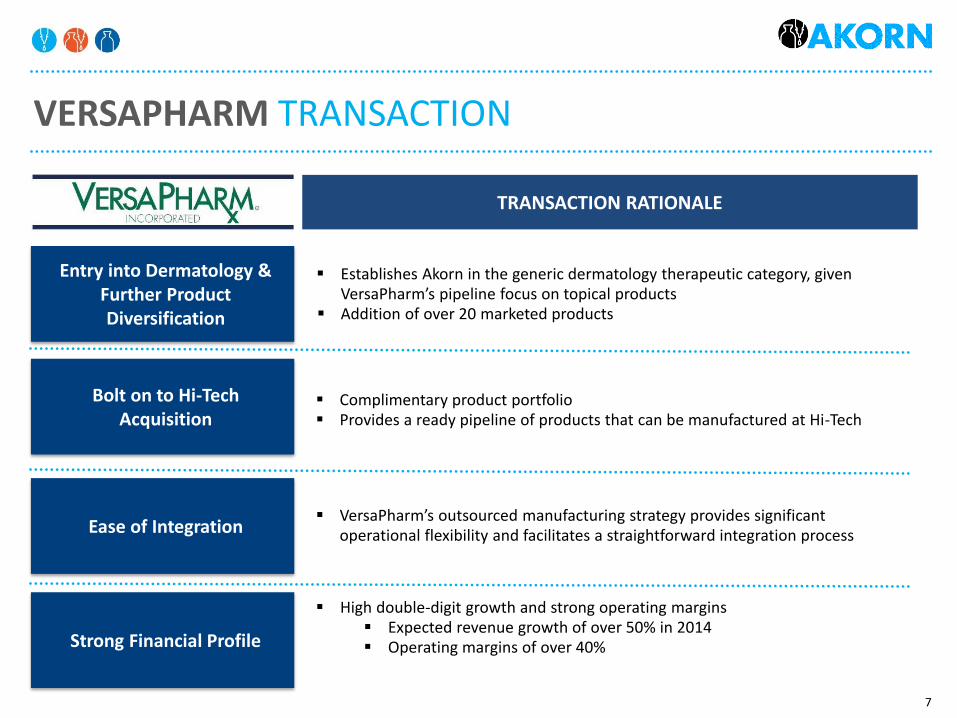

VERSAPHARM TRANSACTION

Entry into Dermatology & Further Product Diversification

Establishes Akorn in the generic dermatology therapeutic category, given VersaPharm’s pipeline focus on topical products

Addition of over 20 marketed products

Bolt on to Hi-Tech Acquisition

Ease of Integration

Strong Financial Profile

Complimentary product portfolio Provides a ready pipeline of products that can be manufactured at Hi-Tech

VersaPharm’s outsourced manufacturing strategy provides significant operational flexibility and facilitates a straightforward integration process

High double-digit growth and strong operating margins Expected revenue growth of over 50% in 2014 Operating margins of over 40%

TRANSACTION RATIONALE

8

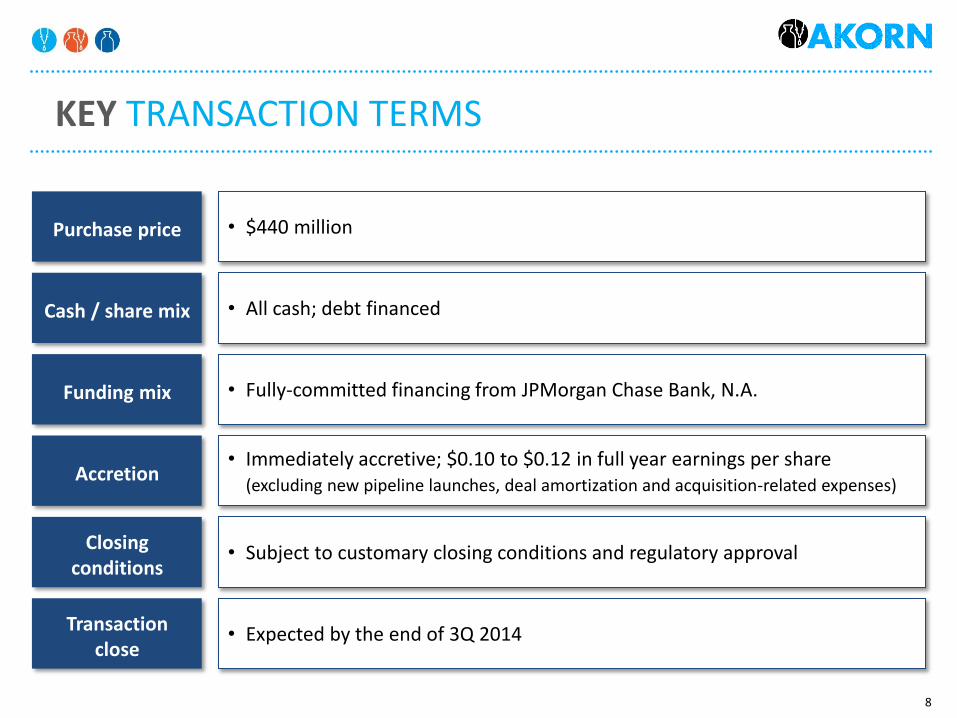

KEY TRANSACTION TERMS

Purchase price • $440 million

Cash / share mix • All cash; debt financed

Funding mix • Fully-committed financing from JPMorgan Chase Bank, N.A.

Accretion • Immediately accretive; $0.10 to $0.12 in full year earnings per share

(excluding new pipeline launches, deal amortization and acquisition-related expenses)

Closing conditions

• Subject to customary closing conditions and regulatory approval

Transaction close

• Expected by the end of 3Q 2014

9

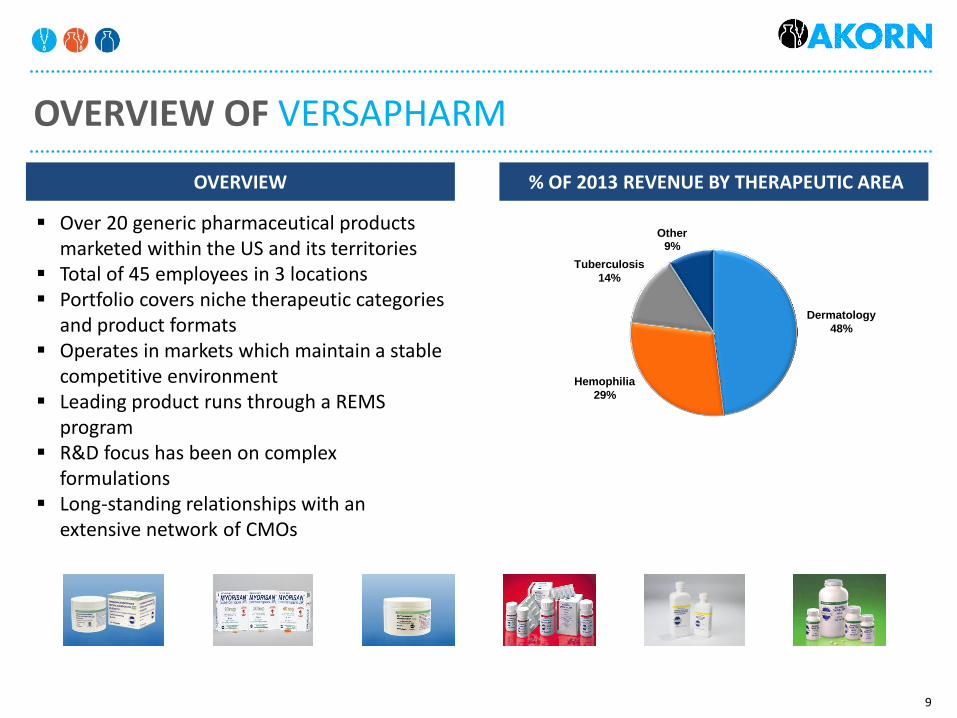

OVERVIEW % OF 2013 REVENUE BY THERAPEUTIC AREA

Over 20 generic pharmaceutical products marketed within the US and its territories

Total of 45 employees in 3 locations Portfolio covers niche therapeutic categories

and product formats Operates in markets which maintain a stable

competitive environment Leading product runs through a REMS

program R&D focus has been on complex

formulations Long-standing relationships with an

extensive network of CMOs

Other 9%

Hemophilia

29%

Dermatology

48%

Tuberculosis

14%

OVERVIEW OF VERSAPHARM

10

VERSAPHARM R&D CAPABILITIES AND PIPELINE

PIPELINE STATS OVERVIEW

• VersaPharm has built a robust pipeline of over

20 products, including 11 ANDAs filed with the

FDA

• Staff of 24 professionals based at the R&D

center in Warminster, PA

• Majority of the 11 filed products can be

manufactured at Hi-Tech

• Ability for filed products to be manufactured in-

house would leverage excess capacity

• Development efforts target dermatology and

other niche market segments

$250

$450

$700

$0

$200

$400

$600

$800

Filed UnderDevelopment

Total

IMS

Mkt

Siz

e (m

illio

ns)

IMS Market Size*

11 9+ 20+ Number of

ANDAs

*IMS Market Size is based on IMS Health data for the 12 months ended Feb 2014

11

INTEGRATE Acquisitions

• Leverage scale and diversification

• Tap into non-sterile platform

• Capture synergies

DEVELOP New

Products

• Continue R&D investment

• Strengthen Hi-Tech’s R&D pipeline

• Maturing R&D pipeline

• Private label opportunity

PURSUE Strategic

M&A

• Strategic fit

• Revenue enhancing

• Accretive

BUILD Brand

Platform

• Maximize value from recent acquisitions

• Leverage & expand existing ophthalmology sales infrastructure

EXECUTE India

Strategy

• Obtain regulatory approvals in US and RoW

• Effectively manage approval timelines

• Leverage new manufacturing capacity

STRATEGIC EXECUTION

12

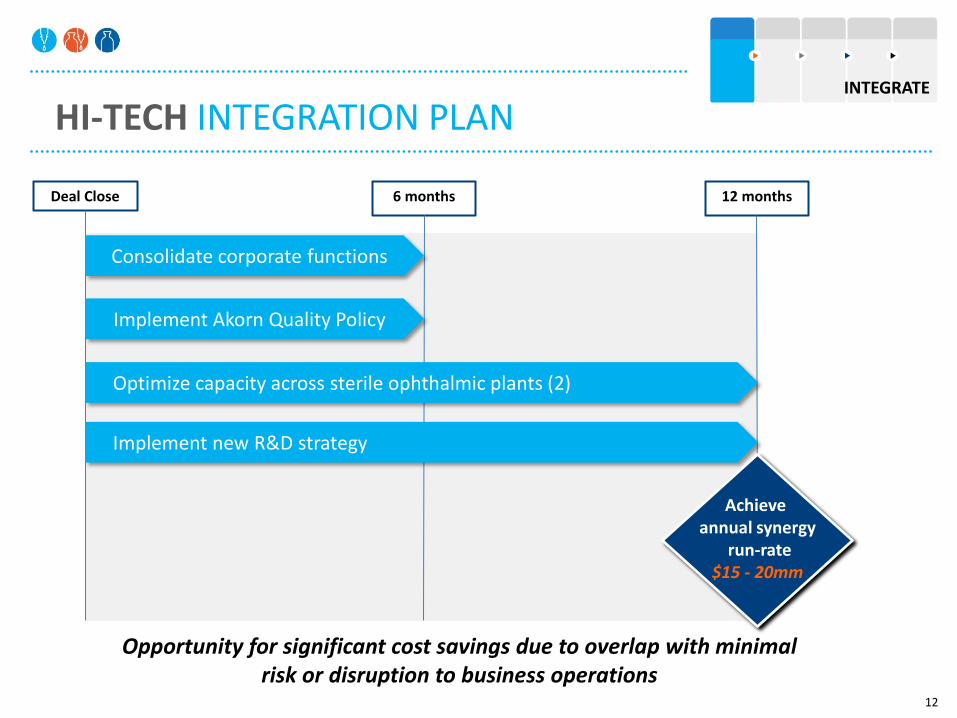

HI-TECH INTEGRATION PLAN

Deal Close 6 months 12 months

Consolidate corporate functions

Implement Akorn Quality Policy

Optimize capacity across sterile ophthalmic plants (2)

Implement new R&D strategy

Achieve annual synergy

run-rate $15 - 20mm

INTEGRATE

Opportunity for significant cost savings due to overlap with minimal risk or disruption to business operations

13

3 6

2 3 1

22 25

12

2010 2011 2012 2013

Hi-Tech

Akorn

$7.0

$11.6

$15.9

$19.9

$39-$42 8.1% 8.4% 6.2% 6.3%

7.35%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

2010 2011 2012 2013 2014

($mm) % of Revenue

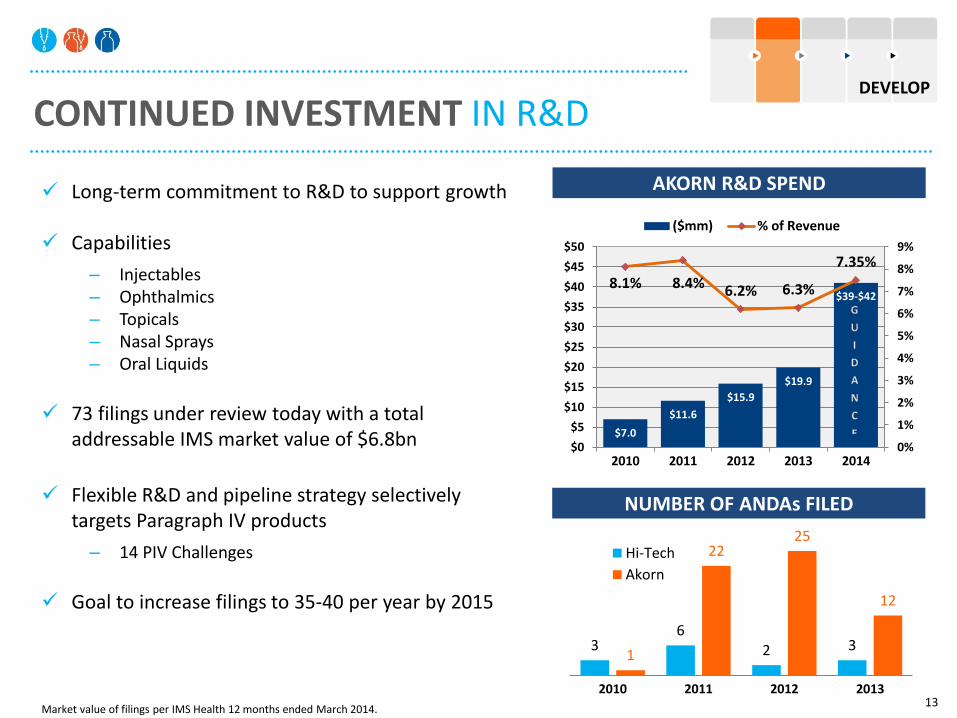

Long-term commitment to R&D to support growth

Capabilities

– Injectables – Ophthalmics – Topicals – Nasal Sprays – Oral Liquids

73 filings under review today with a total

addressable IMS market value of $6.8bn

Flexible R&D and pipeline strategy selectively targets Paragraph IV products

– 14 PIV Challenges

Goal to increase filings to 35-40 per year by 2015

AKORN R&D SPEND

DEVELOP

NUMBER OF ANDAs FILED

CONTINUED INVESTMENT IN R&D

Market value of filings per IMS Health 12 months ended March 2014.

14

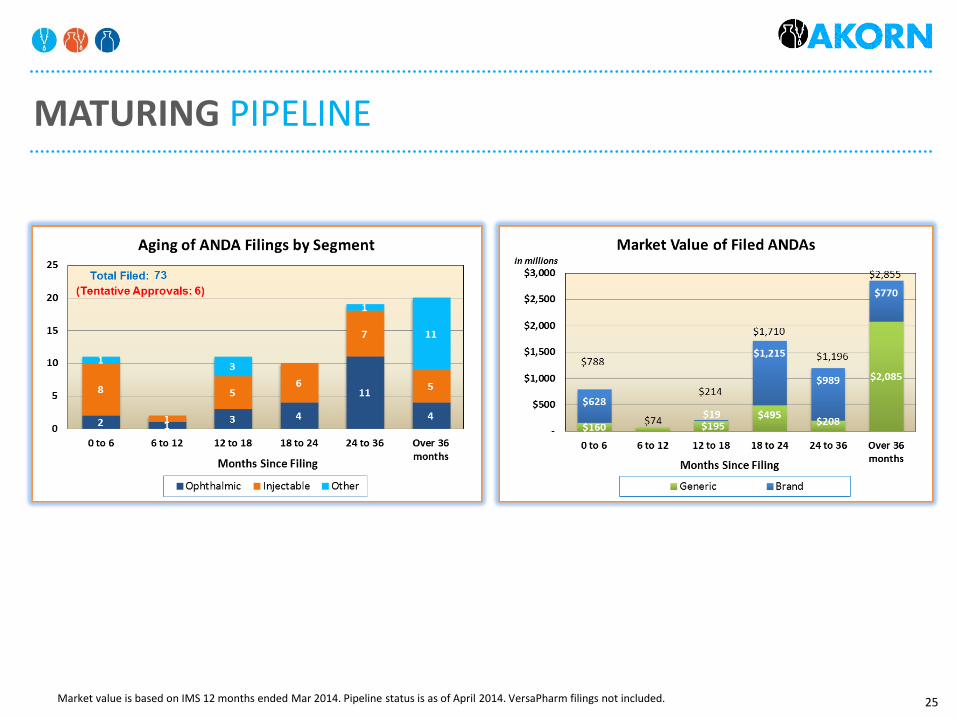

A growing number of products have been with the FDA for over 36 months.

DEVELOP

MATURING PIPELINE

15

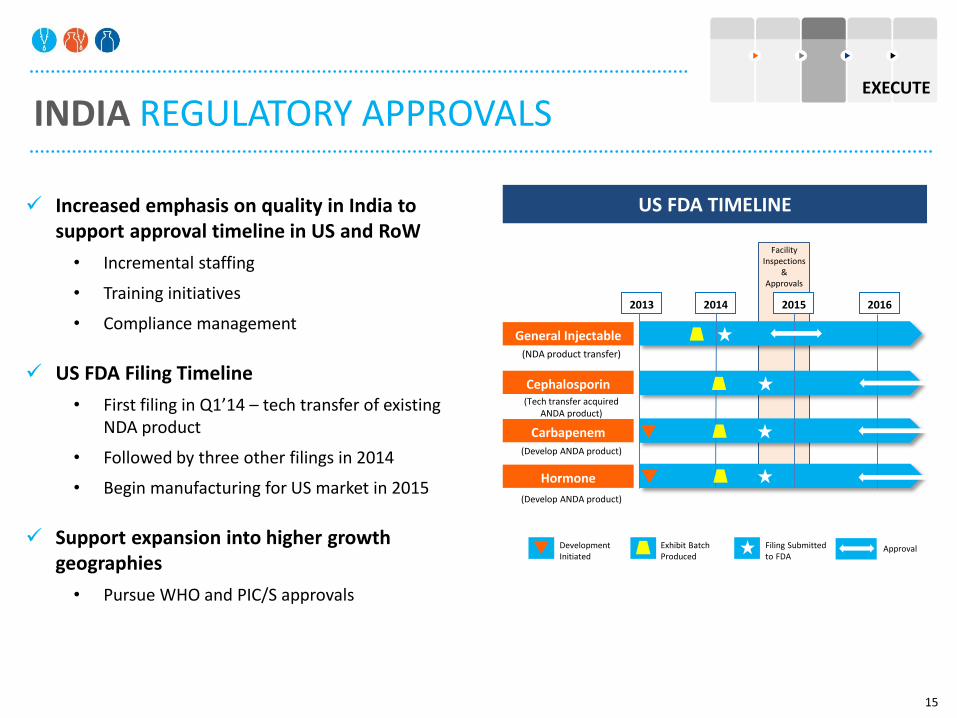

Increased emphasis on quality in India to support approval timeline in US and RoW

• Incremental staffing

• Training initiatives

• Compliance management

US FDA Filing Timeline

• First filing in Q1’14 – tech transfer of existing NDA product

• Followed by three other filings in 2014

• Begin manufacturing for US market in 2015

Support expansion into higher growth geographies

• Pursue WHO and PIC/S approvals

US FDA TIMELINE

Development Initiated

Exhibit Batch Produced

Filing Submitted to FDA

Approval

General Injectable

2013 2014 2015 2016

Cephalosporin

Carbapenem

Hormone

(NDA product transfer)

Facility Inspections

& Approvals

(Tech transfer acquired ANDA product)

(Develop ANDA product)

(Develop ANDA product)

INDIA

INDIA REGULATORY APPROVALS EXECUTE

16

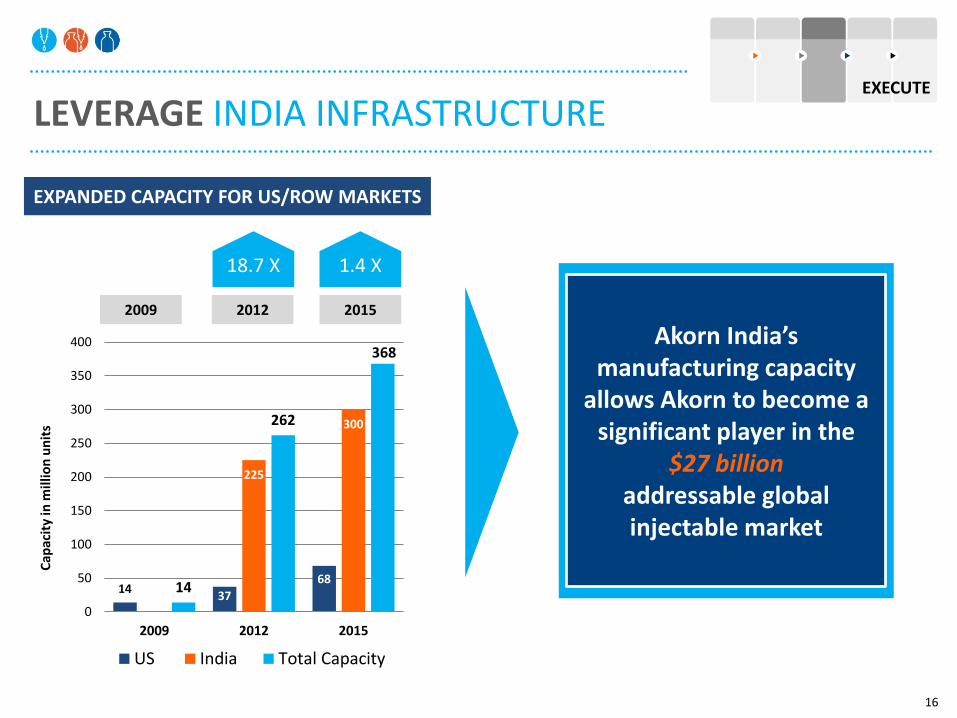

14 37

68

225

300

14

262

368

0

50

100

150

200

250

300

350

400

2009 2012 2015

Cap

acit

y in

mil

lion

un

its

US India Total Capacity

2009 2012 2015

18.7 X 1.4 X

EXPANDED CAPACITY FOR US/ROW MARKETS

Akorn India’s manufacturing capacity

allows Akorn to become a significant player in the

$27 billion addressable global injectable market

EXECUTE

LEVERAGE INDIA INFRASTRUCTURE

17

BUILD

BRANDED OPHTHALMOLOGY PLATFORM

Plan to utilize and expand sales team to reinvigorate revenues of five branded ophthalmic products recently acquired from Merck and Santen

– Leverages existing ophthalmic sales force and physician relationships

– Elevates Akorn’s reputation with prescribers

– Creates a prescription branded ophthalmic strategy

– Broadens existing platform that includes TheraTears, Akten, and IC Green

Platform supports future acquisitions and in-licensing of branded ophthalmic products

Recent product acquisitions will add $54 - $59 million in revenues annually

18

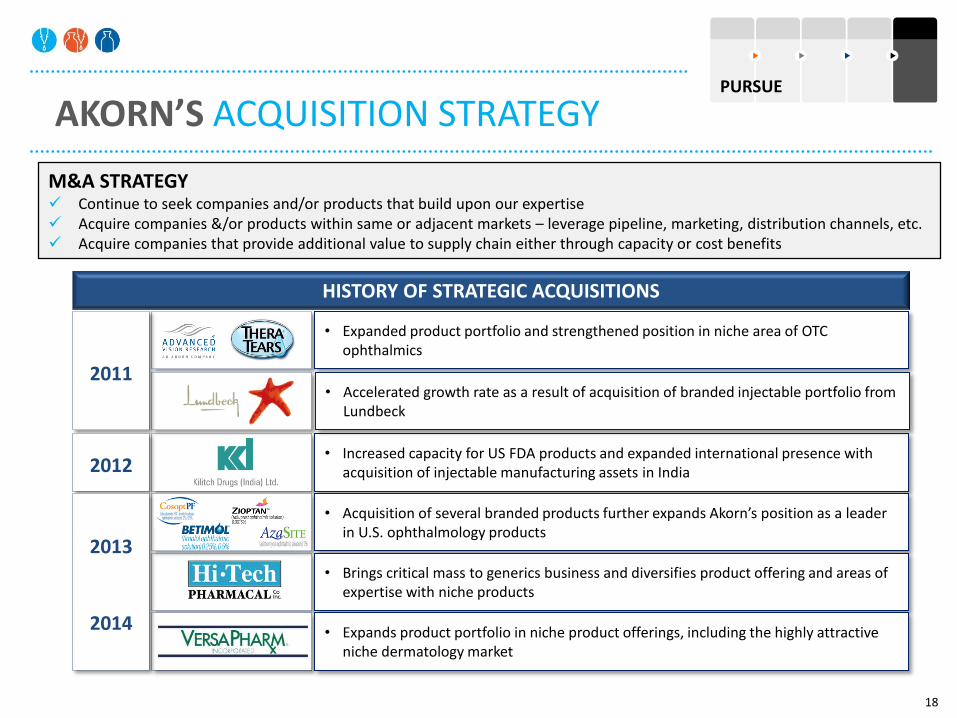

AKORN’S ACQUISITION STRATEGY

HISTORY OF STRATEGIC ACQUISITIONS

• Increased capacity for US FDA products and expanded international presence with acquisition of injectable manufacturing assets in India

• Expanded product portfolio and strengthened position in niche area of OTC ophthalmics

• Acquisition of several branded products further expands Akorn’s position as a leader in U.S. ophthalmology products

• Accelerated growth rate as a result of acquisition of branded injectable portfolio from Lundbeck

2011

2012

2013

2014

• Brings critical mass to generics business and diversifies product offering and areas of expertise with niche products

• Expands product portfolio in niche product offerings, including the highly attractive niche dermatology market

M&A STRATEGY Continue to seek companies and/or products that build upon our expertise Acquire companies &/or products within same or adjacent markets – leverage pipeline, marketing, distribution channels, etc. Acquire companies that provide additional value to supply chain either through capacity or cost benefits

PURSUE

19

FINANCIAL PERFORMANCE

20

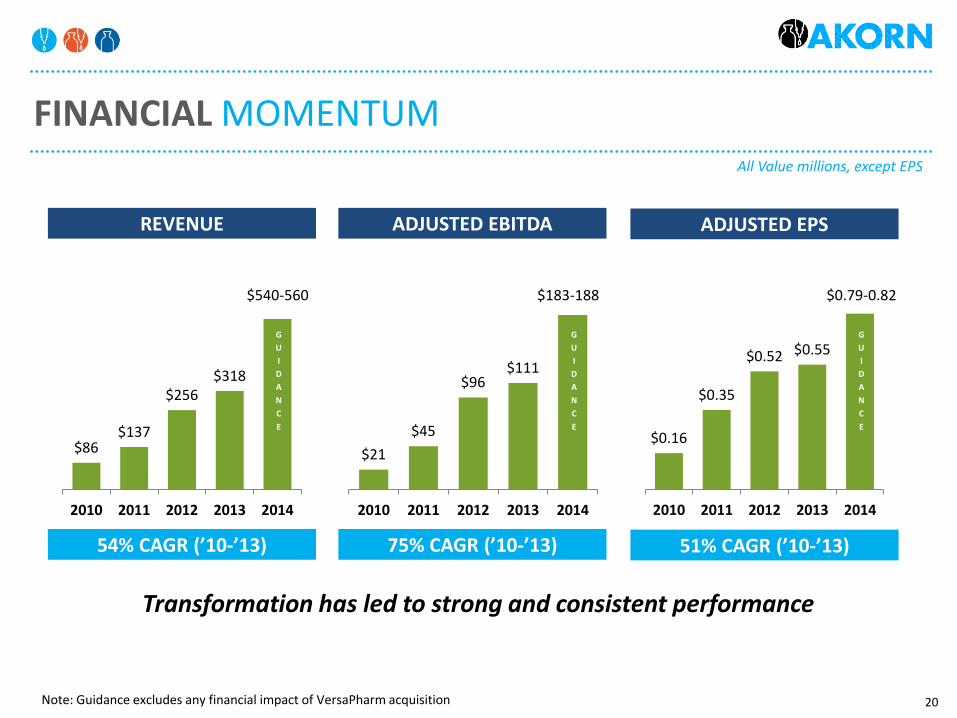

FINANCIAL MOMENTUM

REVENUE ADJUSTED EBITDA ADJUSTED EPS

54% CAGR (’10-’13) 75% CAGR (’10-’13) 51% CAGR (’10-’13)

Transformation has led to strong and consistent performance

$86 $137

$256 $318

2010 2011 2012 2013 2014

$540-560

G

U

I

D

A

N

C

E

$21

$45

$96 $111

2010 2011 2012 2013 2014

$183-188

G

U

I

D

A

N

C

E

$0.16

$0.35

$0.52 $0.55

2010 2011 2012 2013 2014

$0.79-0.82

G

U

I

D

A

N

C

E

All Value millions, except EPS

Note: Guidance excludes any financial impact of VersaPharm acquisition

21

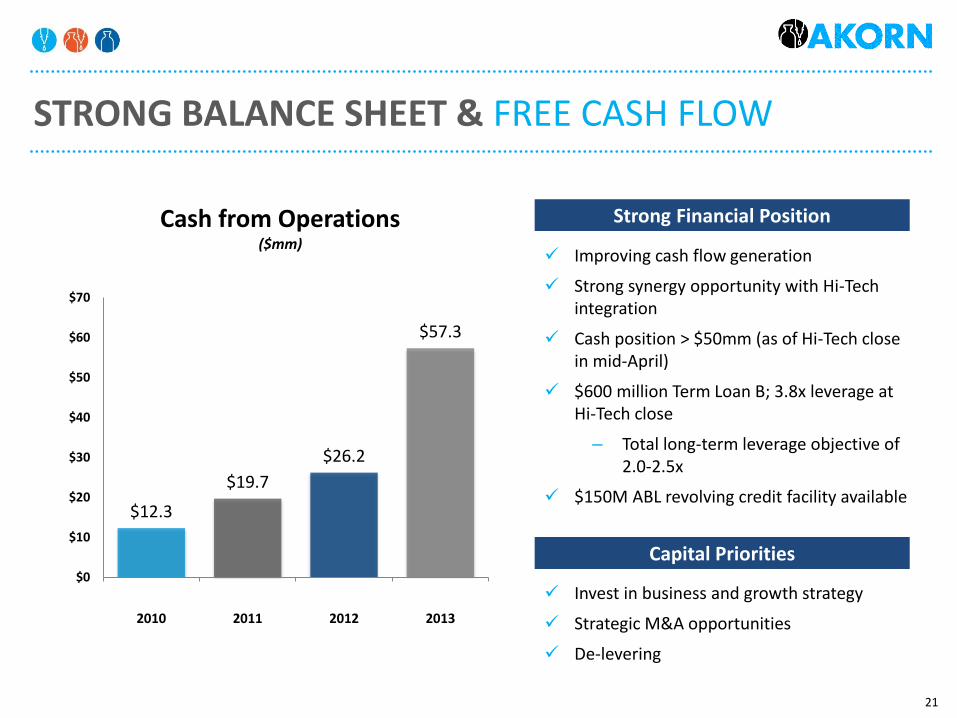

STRONG BALANCE SHEET & FREE CASH FLOW

$12.3

$19.7

$26.2

$57.3

$0

$10

$20

$30

$40

$50

$60

$70

2010 2011 2012 2013

Improving cash flow generation

Strong synergy opportunity with Hi-Tech integration

Cash position > $50mm (as of Hi-Tech close in mid-April)

$600 million Term Loan B; 3.8x leverage at Hi-Tech close

– Total long-term leverage objective of 2.0-2.5x

$150M ABL revolving credit facility available

Strong Financial Position

Capital Priorities

Invest in business and growth strategy

Strategic M&A opportunities

De-levering

Cash from Operations ($mm)

22

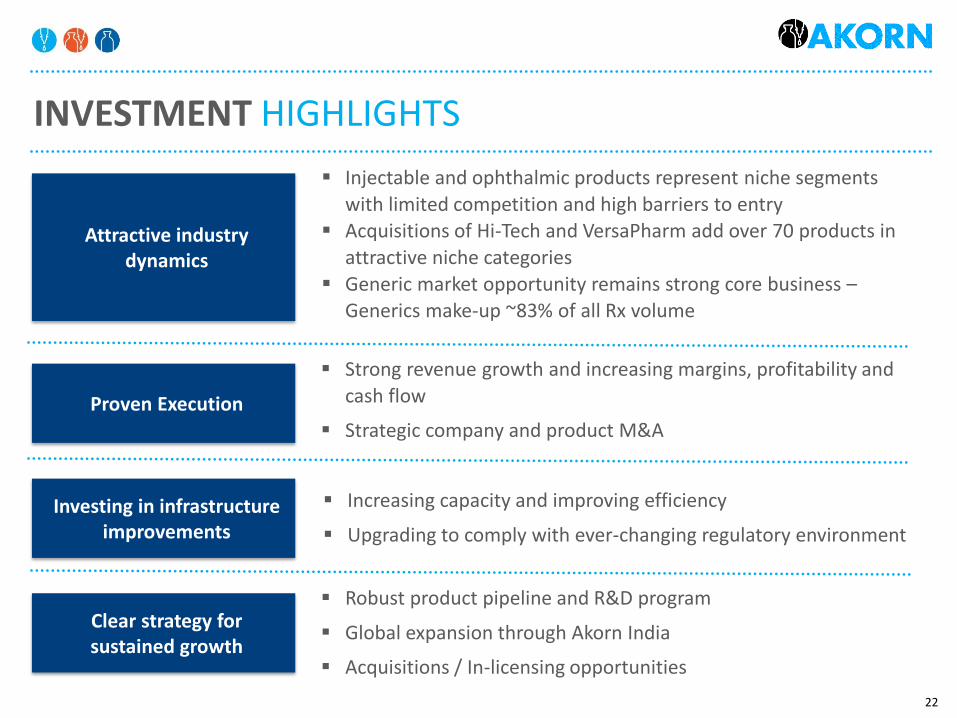

Attractive industry dynamics

Injectable and ophthalmic products represent niche segments

with limited competition and high barriers to entry Acquisitions of Hi-Tech and VersaPharm add over 70 products in

attractive niche categories

Generic market opportunity remains strong core business – Generics make-up ~83% of all Rx volume

Proven Execution

Investing in infrastructure improvements

Clear strategy for sustained growth

Strong revenue growth and increasing margins, profitability and

cash flow

Strategic company and product M&A

Increasing capacity and improving efficiency

Upgrading to comply with ever-changing regulatory environment

Robust product pipeline and R&D program

Global expansion through Akorn India

Acquisitions / In-licensing opportunities

INVESTMENT HIGHLIGHTS

23

24

ROBUST R&D PIPELINE DETAILS (US MARKET)

Market value is based on IMS 12 months ended Mar 2014. Pipeline status is as of April 2014. VersaPharm filings not included.

Filed In Development Total

Mkt Value Count Mkt Value Count Mkt Value Count Mkt Value Count

Brand $3,620 27 $1,243 7 $2,596 22 $7,460 56

Generic $3,217 46 $756 7 $1,818 34 $5,790 87

Total $6,837 73 $1,999 14 $4,414 56 $13,250 143

To Be Filed Filed To Be Filed In Development Total

Mkt Value Count Mkt Value Count Mkt Value Count Mkt Value Count

Ophthalmic $2,506 25 $387 5 $506 11 $3,398 41

Injectable $2,563 32 $1,160 7 $2,626 35 $6,350 74

Other $1,768 16 $452 2 $1,282 10 $3,503 28

Total $6,837 73 $1,999 14 $4,414 56 $13,250 143

25

MATURING PIPELINE

Market value is based on IMS 12 months ended Mar 2014. Pipeline status is as of April 2014. VersaPharm filings not included.