Embed Size (px)

Citation preview

AFM 31130

Strategic Management Accounting

By Isuru Manawadu

B.Sc in Accounting Sp. (USJP), ACA

ContentIntroduction to Management Accounting and Strategic Management AccountingA brief historical review of Management AccountingFinancial Accounting Vs. Management AccountingDecision Making processStrategic Management Accounting pracices Impact of Information Technology

3

What is Management Accounting ?

Management accounting is concerned with the provision and use of accounting information to managers within organizations, to facilitate the managers in their decision making and management control functions. Unlike financial accountancy information (which, for the most part, is made publicly available), management accounting information is used within an organization and is usually confidential.

3

4

Management Accounting is "the process of identification, measurement, accumulation, analysis, preparation, interpretation and communication of information used by management to plan, evaluate and control within an entity and to assure appropriate use of and accountability for its resources”.

- The Chartered Institute of Management Accountants (CIMA)

4

5

Financial Accounting focuses on preparing information for the use of internal and external decision makers.

Management Accounting focuses on the requirements of Managers within the organization & the information they require making decisions.

5

6

Financial Accounting Vs. Management Accounting

Financial Accounting

Management Accounting

Principal Objectives

Stewardship or business for the

benefit of shareholders

Seek to improve economy, efficiency and effectiveness of

operations

Time horizon

Past

Not only look at the past, but the present and the future

which affects the operation of the company

Report recipients

External/ Outsiders namely Shareholders and Government(tax)

Internal parties like Directors and Managers

6

7

Outputs

Summary (usually annual)

comprehensive income statement ,

financial position statement and cash

flow statement

Detailed monthly and annual

management accounts showing results by product

and function ad hoc reports

Regulating framework

Accounting standards, Accounting concepts

plus statutory requirement by the

companies Act

None prescribed

Financial Accounting Vs. M.A. Contd…

7

8

Cost Accounting Vs. Management Accounting

‘Cost Accounting is a systematic set of procedures for recording and reporting measurements of the cost of manufacturing goods and performing services in the aggregate and in detail. It includes methods for recognizing, classifying, allocating, aggregating and reporting such costs and comparing them with standard costs’

8

Decision Making ProcessPlanning process1. Identify objectives2. Search for alternative courses for action3. Gather data about alternatives4. Select alternative courses of action5. Implement the decisionsControl Process6. Compare actual and planned outcomes7. Respond to divergences from plan

STRATEGIC MANAGEMENT

“The fundamental idea of strategic planning is quite simple: Continuously re-assess what customers want, what competitors are doing, and other relevant environmental elements (such as emerging technology and trends in government legislation); size up these environmental changes; and use, or develop, available resources to turn these changes into advantages.

Obviously, carrying out strategic planning successfully is a lot more difficult than understanding what it is.”Atkinson, Anthony A., Rajiv D. Banker, Robert S. Kaplan, and S. Mark Young, Management Accounting, Prentice Hall, Inc., 1995, p. 471.

Strategic Management Accounting

“The provision and analysis of financial information on the firm’s product markets and competitors’ costs and cost structures and the monitoring of the enterprise’s strategies and those of its competitors in these markets over a number of periods”

(Bromwich, 1990: 28)

STRATEGIC MANAGEMENT ACCOUNTING

“Accounting exists within an business primarily to facilitate the development and implementation of business strategy...

Three important generalizations emerge from this way of viewing management accounting:

Accounting is not an end in itself, but only a means to help achieve business success

Specific accounting techniques or systems must be considered in terms of the role they are intended to play

In evaluating the overall accounting system... the key question is whether the overall fit with strategy is appropriate.”

Shank, John K. and Vijay Govindarajan, Strategic Cost Management, The Free Press, Macmillan, Inc., 1993, pp. 6-7.

Surveys of Strategic Management Accounting Practices.

Competitive position monitoring Strategic pricingCompetitor performance appraisalCompetitor cost assessmentStrategic costingValue chain costingBrand value monitoringBrand value budgetingQuality costingLife cycle costingTarget costing

Bromwich, 1990

STRATEGIC MANAGEMENT AND ACCOUNTING

Strategic ManagementStakeholder analysisCorporate objectivesSustainable competitive advantages

Strategic Management AccountingAppropriate analysisLong-term considerations Nonfinancial data

STRATEGIC MANAGEMENT AND ANALYSISStrategic considerationsStrategic Marketing AnalysisTotal Value-Chain AnalysisTarget CostingLife-Cycle Management and Costing

Operational considerationsActivity Based Analysis JIT Operations: A Management PhilosophyTotal-Quality Management and Costing

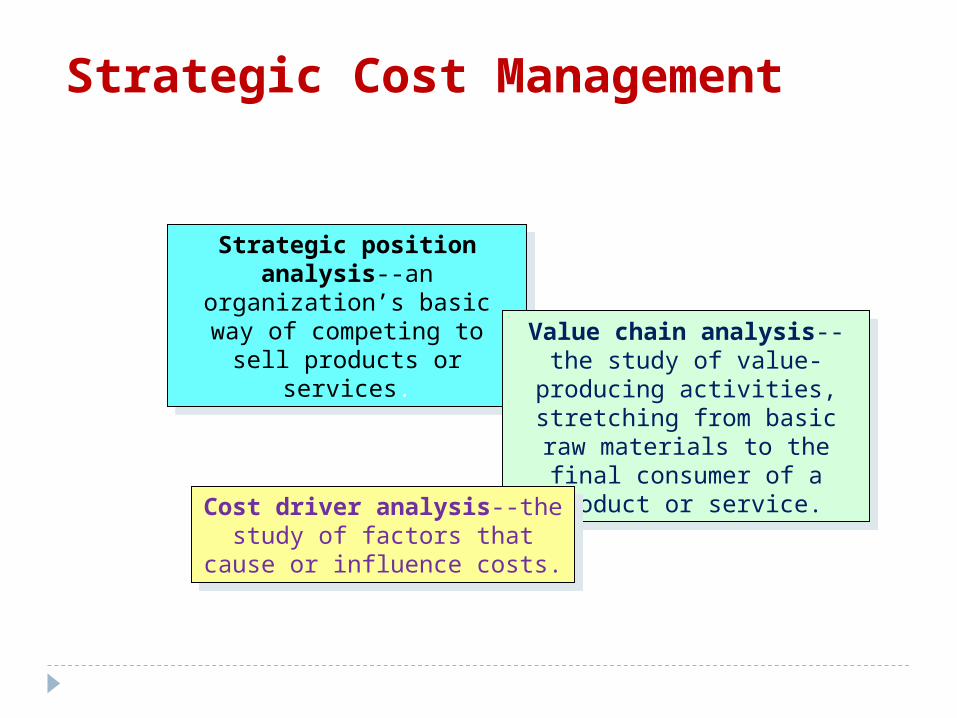

Strategic Cost Management

Strategic position analysis--an organization’s basic way of competing to sell products or

services.

Strategic position analysis--an organization’s basic way of competing to sell products or

services.Value chain analysis--the study

of value-producing activities, stretching from basic raw

materials to the final consumer of a product or service.

Value chain analysis--the study of value-producing activities,

stretching from basic raw materials to the final consumer

of a product or service.

Cost driver analysis--the study of factors that cause or influence

costs.

Cost driver analysis--the study of factors that cause or influence

costs.

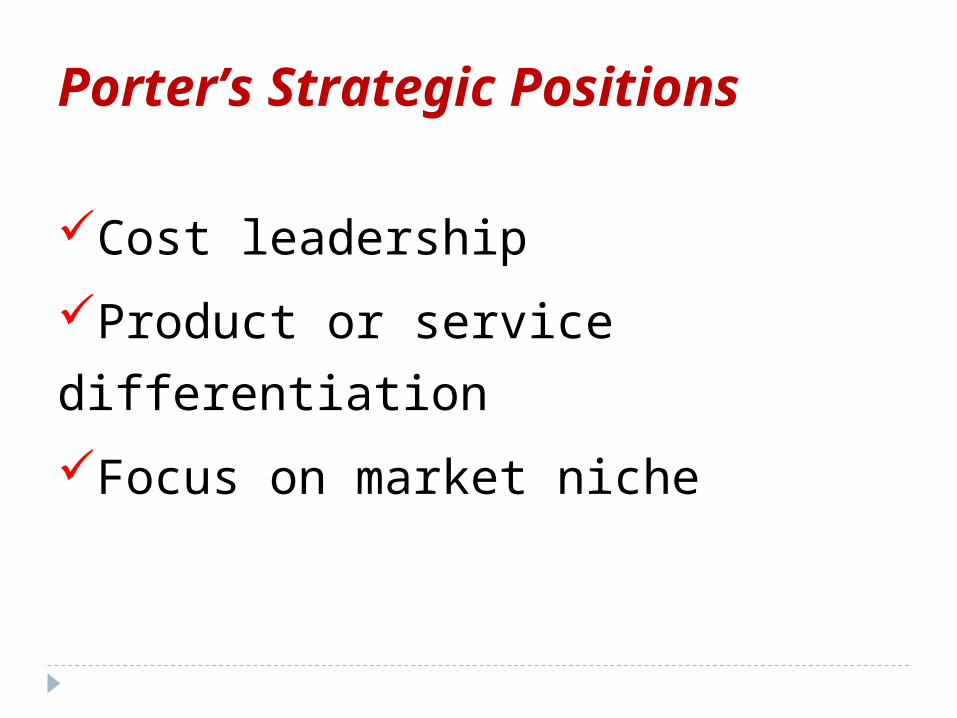

Porter’s Strategic Positions

Cost leadership

Product or service differentiation

Focus on market niche

DEVELOPING COMPETITIVE ADVANTAGE

DifferentiationAdvantage

Stuck-in-theMiddle

Differentiationwith Cost

Advantage

LowCost

Advantage

Relative Cost Position

Inferior Superior

RelativeDifferentiation

Position

Inferior

Superior

VALUE CHAIN ANALYSISFocus of the analysis

External vs. Internal (traditional)Highlights profit improvement areas

Linkages with suppliersLinkages with customersProcess linkages within a business unitLinkages across business units

Steps in the analysis

Identify an industry’s value chainAssign costs, revenues, and assets to value activitiesDiagnose cost driversDevelop sustainable competitive advantages

VALUE-CHAIN & STRATEGIC MANAGEMENT

Customer Customer FocusFocus

Customer Customer FocusFocus

Research Research and and

DevelopmentDevelopment

Research Research and and

DevelopmentDevelopmentProductProduct

AndAndServiceServiceProcessProcessDesignDesign

ProductProductAndAnd

ServiceServiceProcessProcessDesignDesign

ProductionProductionProductionProduction

MarketingMarketingMarketingMarketing

DistributionDistributionDistributionDistribution

ServiceServiceServiceService

ESTABLISHMENT OF TARGET COSTS

MarketResearch

DefineProduct/Customer

Niche

Define ProductFeatures

RequiredProfit

Target Cost

CompetitorAnalysis

UnderstandCustomer

Requirements

EstimatedMarketPrice

RequiredProfit

Group ActivityInstructions- Each group should have 5 students- At least two members should present

about the findings Topic -Explain the impact to the Strategic Management Accounting on Information Technology

Explain the impact to the Strategic Management Accounting on Information Technology

E- CommerceERPS

Lecturer - Isuru Manawadu24

&Questions

Answers