Embed Size (px)

Citation preview

Addressing the South’s Challenges in the Global Economy in Crisis

Martin KhorSouth Centre

November 2011

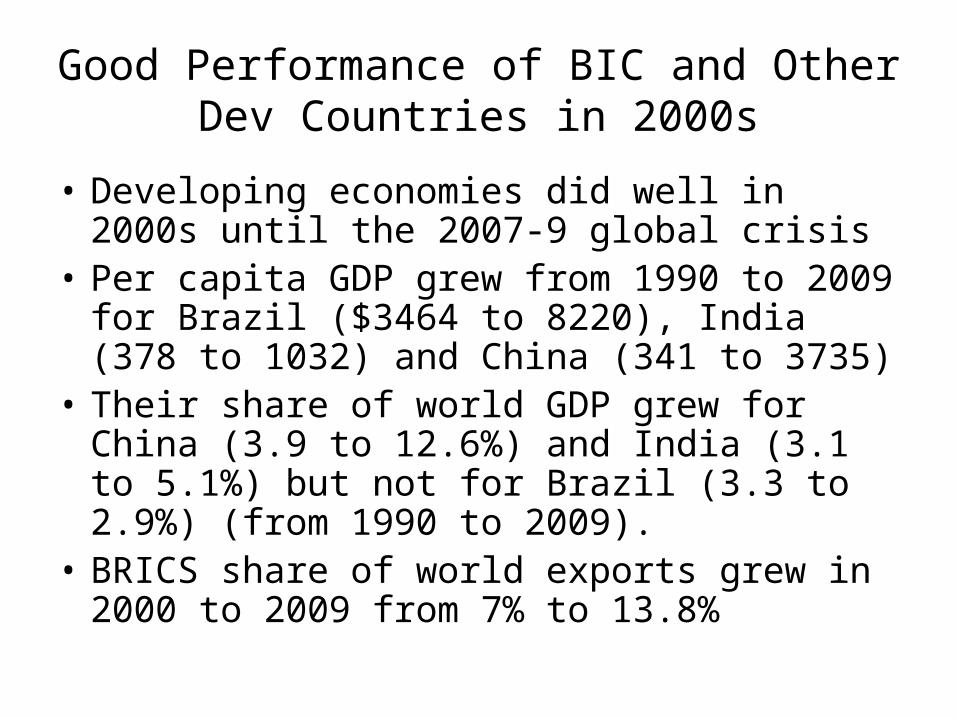

Good Performance of BIC and Other Dev Countries in 2000s

• Developing economies did well in 2000s until the 2007-9 global crisis

• Per capita GDP grew from 1990 to 2009 for Brazil ($3464 to 8220), India (378 to 1032) and China (341 to 3735)

• Their share of world GDP grew for China (3.9 to 12.6%) and India (3.1 to 5.1%) but not for Brazil (3.3 to 2.9%) (from 1990 to 2009).

• BRICS share of world exports grew in 2000 to 2009 from 7% to 13.8%

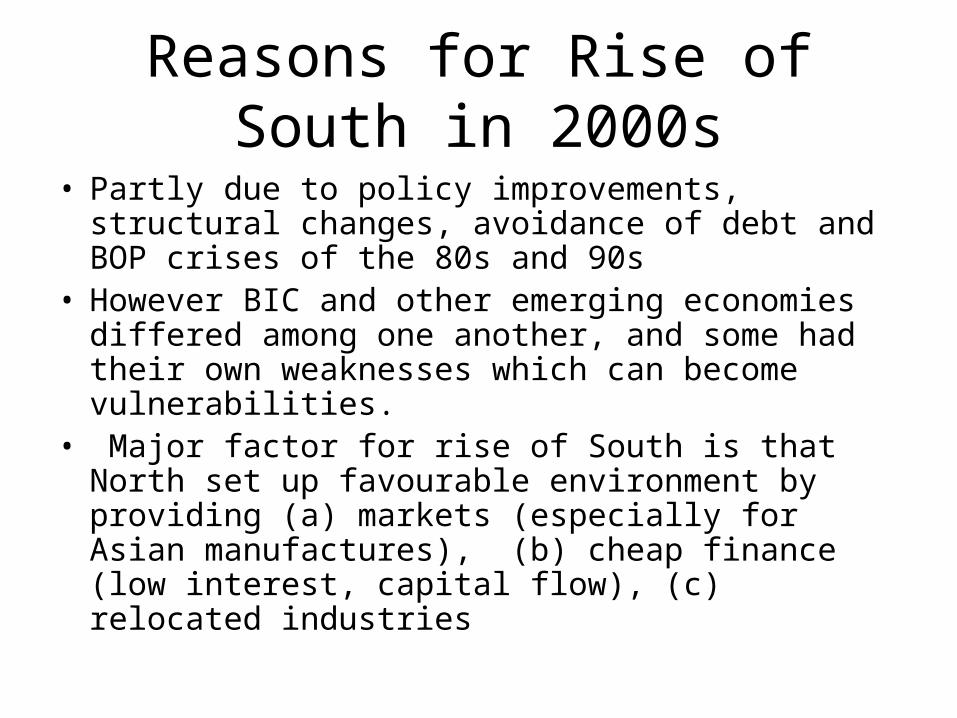

Reasons for Rise of South in 2000s

• Partly due to policy improvements, structural changes, avoidance of debt and BOP crises of the 80s and 90s

• However BIC and other emerging economies differed among one another, and some had their own weaknesses which can become vulnerabilities.

• Major factor for rise of South is that North set up favourable environment by providing (a) markets (especially for Asian manufactures), (b) cheap finance (low interest, capital flow), (c) relocated industries

2008-9 Crisis and Post Crisis

• The 2008-9 global crisis affected the South’s markets (exports fell), external finance (capital flows reversed) and GDP (from 2007-9, China GDP 13 to 8.7%; India 9.4 to 5.7%; Brazil 6.1 to -0.6%).

• Rapid recovery in 2009-2010 due to low-interest , easy monetary policy, bail-outs, Northern fiscal stimulus, and some South counties’ own reflation policies.

• South’s growth recovered due to as exports grew; capital inflows resumed. China’s recovery helped provide demand for commodity exports.

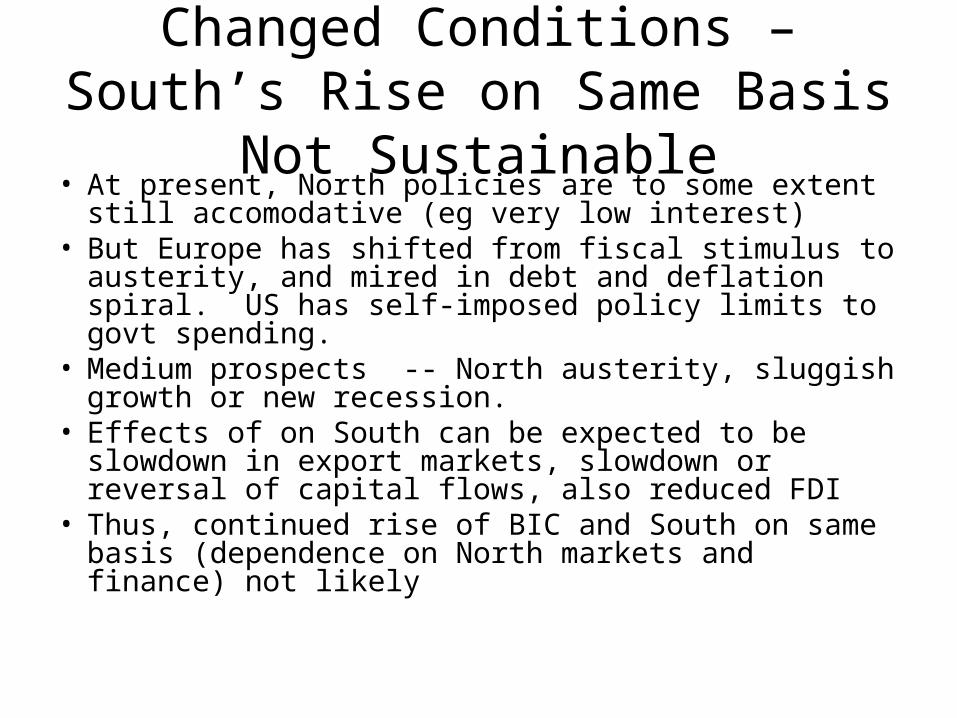

Changed Conditions – South’s Rise on Same Basis Not Sustainable

• At present, North policies are to some extent still accomodative (eg very low interest)

• But Europe has shifted from fiscal stimulus to austerity, and mired in debt and deflation spiral. US has self-imposed policy limits to govt spending.

• Medium prospects -- North austerity, sluggish growth or new recession.

• Effects of on South can be expected to be slowdown in export markets, slowdown or reversal of capital flows, also reduced FDI

• Thus, continued rise of BIC and South on same basis (dependence on North markets and finance) not likely

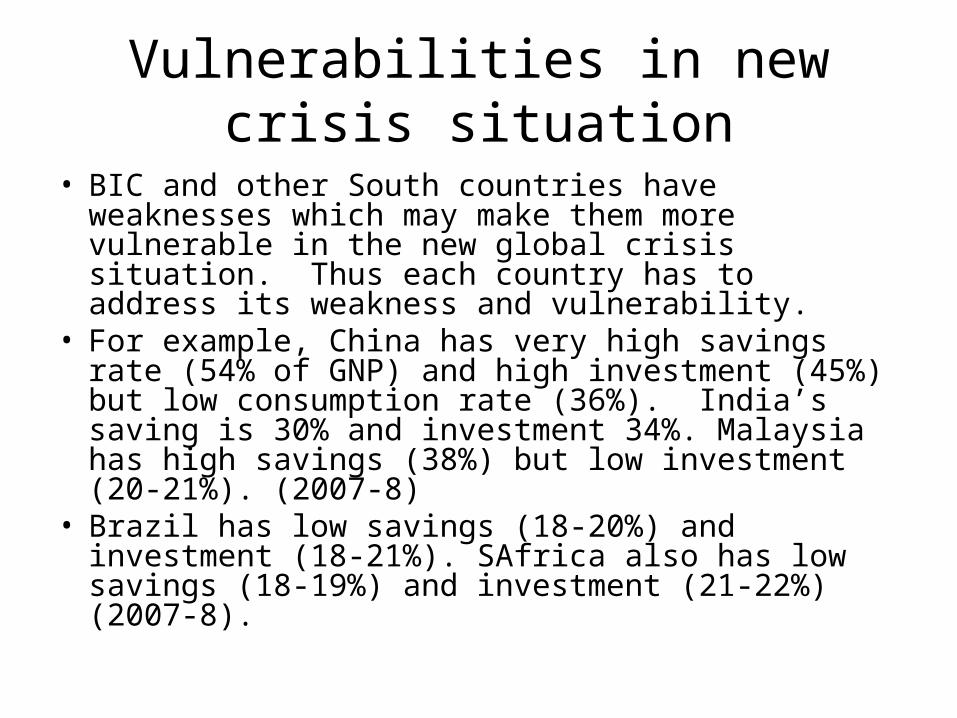

Vulnerabilities in new crisis situation

• BIC and other South countries have weaknesses which may make them more vulnerable in the new global crisis situation. Thus each country has to address its weakness and vulnerability.

• For example, China has very high savings rate (54% of GNP) and high investment (45%) but low consumption rate (36%). India’s saving is 30% and investment 34%. Malaysia has high savings (38%) but low investment (20-21%). (2007-8)

• Brazil has low savings (18-20%) and investment (18-21%). SAfrica also has low savings (18-19%) and investment (21-22%) (2007-8).

Vulnerability: Dependence on External Finance; Volatility in Capital Flows

• BICS also have different current account situations: In latest 12 month period, China has $303bil surplus, while others are in deficit – India $36b; Brazil $48b, SAfrica $11b.

• Major emerging economies have similar vulnerability in facing volatile and large capital flows, in boom-bust cycles. The latest boom led to inflation pressures, asset and stock market bubbles and currency appreciation (with import surges and loss of export competitiveness in some countries).

• Most vulnerable are countries with currency appreciation and current account deficit at same time.

Capital Flows: Effects and Areas of Fragility

1. CA deficits and currency appreciations

– Appreciations during pre-Lehman boom; declines in 2008-09 quickly reversed.

– Almost all dev countries appreciated, but faster in deficit (India, Brazil, Turkey, RSA) than surplus countries (China, Korea, SEA).

– Adverse effects on exports in some countries

2. Build-up of short-term private debt in some – risk of corporate default if reversed.

3. Asset bubbles

– Increased correlation between capital flows and equity prices (increased foreign presence in domestic equity and bond markets)

– Credit and asset bubbles , risk of hard landing.

9

NET PRIVATE CAPITAL FLOWS TO DEEs (% of GDP)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

Brazil

60

70

80

90

100

110

120

130

140

150

160

Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

-4

-2

0

2

4

6

8

10

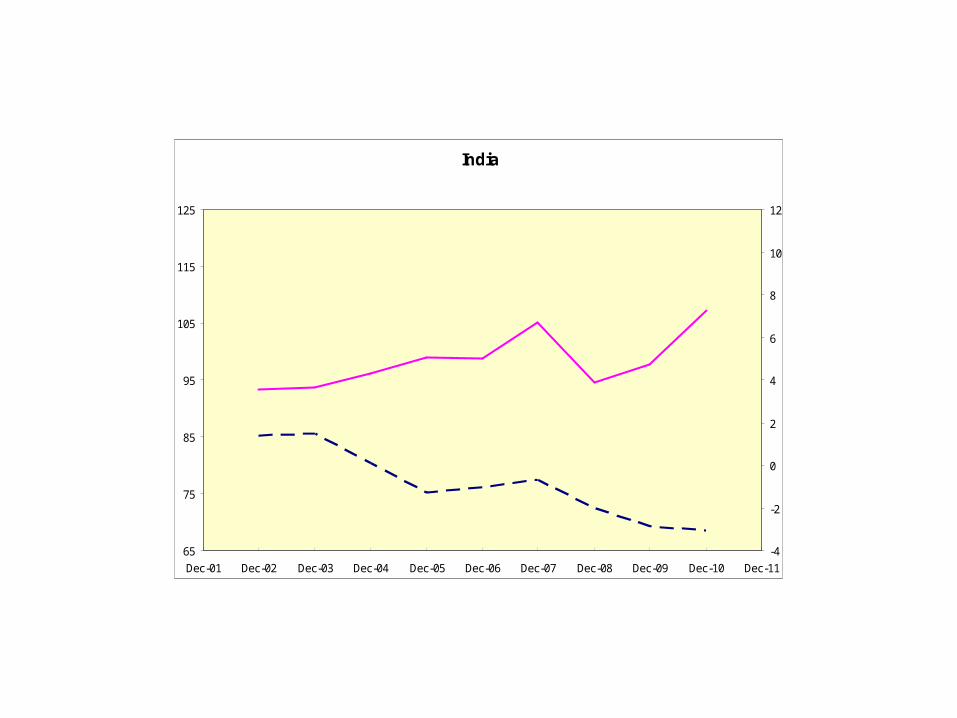

India

65

75

85

95

105

115

125

Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

-4

-2

0

2

4

6

8

10

12

China

65

75

85

95

105

115

125

Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

-4

-2

0

2

4

6

8

10

12

13

RECENT COMMODITY CYCLES

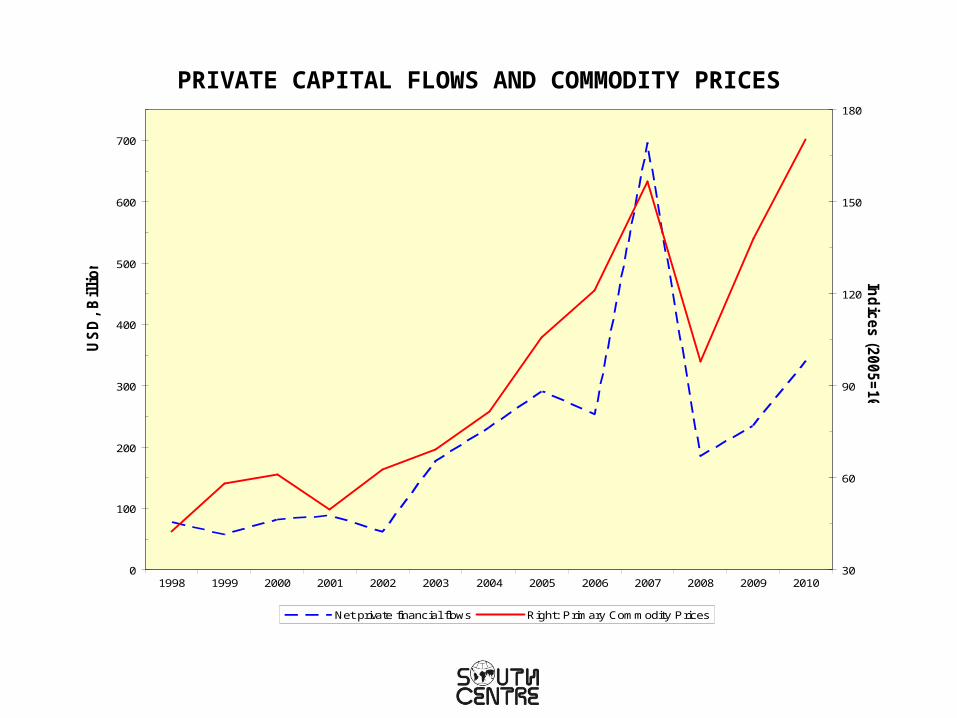

• Commodity cycles overlapping with cycles in capital flows and dollar

– Price rises started in 2003, accelerated in 2006 and continued initially in 2008, like capital flows.

– Started to fall in August 2008, about the same time as capital flows fell and dollar rose as crisis deepened (Lehman); flight to safety, $ rising.

– Started to rise again in Spring 2009 with QE and low interest rates, together with the boom in capital flows and fall of the dollar.

• Financialization of commodity markets: between 2003 and 2010 the number of contracts in commodity derivatives (futures and options) rose from 13 million to 66 million and investment in index trading rose from $13 billion to $320 billion.

14

PRIVATE CAPITAL FLOWS AND COMMODITY PRICES

0

100

200

300

400

500

600

700

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

US

D,

Bil

lio

ns

30

60

90

120

150

180

Ind

ices (2

005=

100)

Net private financial flows Right: Primary Commodity Prices

15

END OF BOOMS IN CAPITAL FLOWS AND COMMODITY PRICES

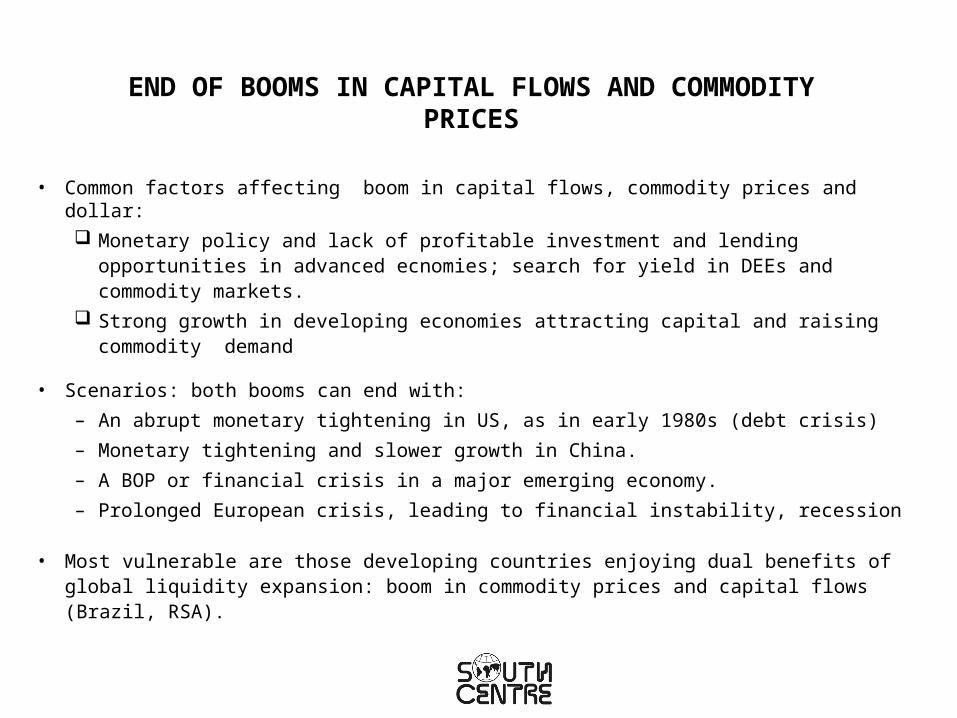

• Common factors affecting boom in capital flows, commodity prices and dollar: Monetary policy and lack of profitable investment and lending opportunities in

advanced ecnomies; search for yield in DEEs and commodity markets. Strong growth in developing economies attracting capital and raising commodity

demand

• Scenarios: both booms can end with:– An abrupt monetary tightening in US, as in early 1980s (debt crisis)– Monetary tightening and slower growth in China.– A BOP or financial crisis in a major emerging economy. – Prolonged European crisis, leading to financial instability, recession

• Most vulnerable are those developing countries enjoying dual benefits of global liquidity expansion: boom in commodity prices and capital flows (Brazil, RSA).

Vulnerability of Countries that are Dependent on both Commodities and Capital Inflows

• They enjoyed dual benefits of global liquidity expansion: boom in commodity prices and capital flows.

• Their growth performance depends on two factors that are largely beyond their control-- commodity prices and capital flows.

• Usually these two are positively correlated. When commodity markets flatten, they start running deficits; at same time capital flows tend to dry up.

17

POLICY CONCLUSIONS ON CAPITAL FLOWS

• Developing Countries:

– Need determined action to control capital flows – inward and outward. Should not allow currencies and CA to get out of hand. Commodity exporters should run surplus at times of boom, keep them in (earned) reserves as self-insurance for rainy days (Prebisch).

– Developing countries as a group no longer depend on capital flows from North. Need to introduce reliable and stable mechanisms for south-south recycling from surplus to deficit countries without going through Wall Street or the City.

• Reform of the international financial architecture to reduce systemic instability:

Reform of Reserves system Surveillance of systemically important countries Regulation of international capital flows, including in source countries. Regulating of trading in commodity futures.

Role of and Changes in China• As North slows, can China replace it as growth engine of BIC and

South?• China itself will face its own problems. Exports contribute about

50% of its recent (pre-crisis) growth. If its export growth slows from 24-30% (2002-6) to 10%, its GDP growth may reach only 7%.

• Domestic engine of growth: Needs to switch from investment to consumption-led (consumption ratio fell from 55% late 1990s to 36% in 2008). Share of wages and household income (including government transfers) in GNP has to rise. Greater public spending on health, housing, etc. needed.

• A shift from export led to consumption led growth needs industrial restructuring (may include phasing out of some low-paying labour-intensive and high-polluting industries)

Changes in China will affect other developing countries

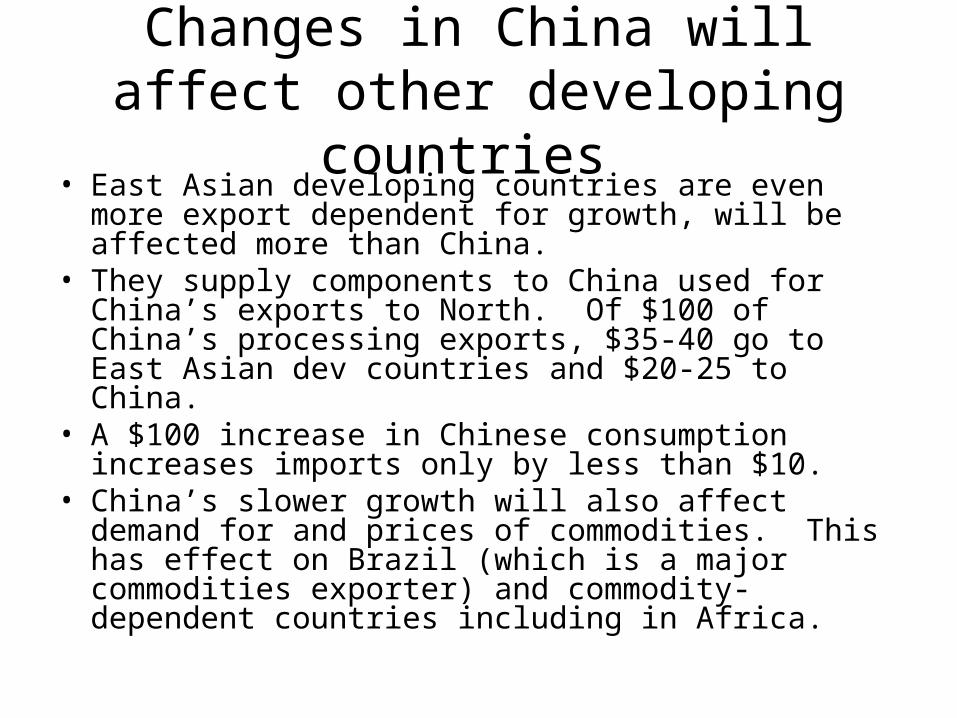

• East Asian developing countries are even more export dependent for growth, will be affected more than China.

• They supply components to China used for China’s exports to North. Of $100 of China’s processing exports, $35-40 go to East Asian dev countries and $20-25 to China.

• A $100 increase in Chinese consumption increases imports only by less than $10.

• China’s slower growth will also affect demand for and prices of commodities. This has effect on Brazil (which is a major commodities exporter) and commodity-dependent countries including in Africa.

New Directions Needed• Especially with bleak prospects from global crisis in medium

term, BIC and other South countries need to plan reforms• China and Asean need to reduce dependence on Northern

markets, develop domestic engines of growth (China through consumption-based growth, Malaysia etc through productive investments), and expand regional and S-S trade and production cooperation.

• Dev Countries with trade/CAccount deficits have to reduce dependence on external financing and capital inflows.

• Both sets of countries require restructuring, strong industrial policy, overall development policies and a developmental state

Balanced, Equitable and Sustainable Development

• Better balance also required in future development, with regard to economic/social development; reducing income and rural/urban inequalities; and tackling environment concerns

• BICS have initiated climate-friendly development with national programmes and national targets/pledges that are rather ambitious

• Besides implementing national measures, stronger collaboration within BICS and between them and other South institutions and countries is essential

Managing Strategic Challenges in BICS and South

• Managing strategic change: Big challenge to combine economic growth with social equity and environmental goals, in midst of global slowdown

• Thus, need for strategic thinking, research in BICS & South governments, academics, think-tanks:

(1) National policy (2) South-South cooperation in economic, social, environ areas: (3) Managing N-S relations; (4) Reviewing and reforming international institutions and order• Need to strengthen or create institutions at national, BICS, Regional

and South levels (trade, financial and production cooperation)

New Challengs in N-S Relations

• Managing barriers thrown up by North: The North should also manage its decline in context of positive international cooperation. However it appears the mood for such cooperation has darkened considerably.

• Non or little cooperation in providing financial resources, tech-transfer, trade relations

• Desire of North to redefine the South – new categorisation (advanced developing countries, etc) and only recognising LDCs or SVEs for development treatment (WTO, UNFCCC, Rio-Plus-20, etc). All others to be treated similarly as North re obligations

Potential Obstacles from North

• Emphasis on new IPR barriers and TRIPS Plus enforcement, affecting technology development

• New trade protection measures, using climate change, border adjustment taxes, airline emission charges, carbon footprint standards

• Renewed attack on subsidies used by the South (US vs China---solar panels, wind energy cases and review of 200 subsidies) even as North dragging its feet on reducing its agricultural subsidies.

• Insistence on new unfair barriers to development, especially climate emission reduction obligations

Trade and Investment Agreements• WTO: Imbalanced Uruguay Round agreements but South has

organised itself better in Doha talks; thus impasse (possibly permanent); but South must prepare itself for what comes next. Dangers of recategorising developing countries and new treaties on “new issues” even when “old issues” like agriculture subsidies are not settled

• North-South FTAs can threaten financial stability and new industrial and development policies. Includes US, EU bilaterals, EU’s regional EPAs and US TPP.

• Bilateral investment treaties also constrain finance stability policy measures and need to be reformed

• Can South-South agreements be better?

Moves for financialisation of climate, forests, natural resources

• Possibly fastest growing area of new financial markets is in climate change. Growth of carbon markets.

• Green Climate Fund with potential of $10bil a year now and $100 bil by 2020. Design of Fund: North demands a private sector facility with own governance and rules, including “leveraging” private funds through loan guarantees etc. – financial engineering that had contributed to current crisis. Decision to be made in Durban Dec 2011 and after

• Moves to extend financial markets to other environmental areas---like biodiversity and natural resources. Initiatives include Green Economy (Rio Plus 20), REDD plus (forests), payment for environmental services, etc.

Conclusions

• Challenges are enormous, and have to be faced simultaneously: addressing global crisis’s effects, addressing need for global financial system reform, addressing weaknesses in national economy, changing the basis of effective demand and developing new markets and structures, and addressing social equity and environmental issues.

• The moment for reflection for strategic and practical measures has come. BICS and South require their own strong policy institutions to reflect collectively and nationally on future trends and strategic options.