Embed Size (px)

Citation preview

Accounts Payable and Other Liabilities

Chapter 14

McGraw-Hill/Irwin Copyright © 2010 by The McGraw-Hill Companies, Inc. All rights reserved.

14-2

Sources of Accounts PayableSources of Accounts Payable Short-term obligations arising from purchase of

goods and services in ordinary course of business; examples:

Acquisition of merchandise on credit Receipt of services such as advertising, repairs

Invoices and statements from suppliers usually evidence accounts payable

Interest-bearing obligations are not included in accounts payable; they are included as bonds, notes, etc.

14-3

Sources of Accrued LiabilitiesSources of Accrued Liabilities

Accrued liabilities Sometimes called accrued expenses Examples: Salaries, interest, rent Accumulate over time and management must

make accounting estimate at year-end.• Note that if management does not make such an

estimate, no entry will occur since the related transactions (e.g., interest) may have occurred months ago

14-4

Objectives for the Audit Accounts Objectives for the Audit Accounts Payable and PurchasesPayable and Purchases

1. Use the understanding of the client and its environment to consider inherent risk, including fraud risks, related to accounts payable.

2. Obtain an understanding of internal control over accounts payable.

3. Assess the risks of material misstatement and design tests of controls and substantive procedures that:

a. Substantiate the existence of accounts payable and the client’s obligation to pay these liabilities and establish the occurrence of purchase transactions

b. Establish the completeness of recorded accounts payablec. Verify the cutoff of transactions affecting accounts payabled. Establish the proper valuation of accounts payable and the

accuracy of purchase transactionse. Determine that the presentation and disclosure of accounts

payable are appropriate

14-5

Primary concernPrimary concern

Possibility of understatement or omission of liabilities Exaggerates the financial strength of

company Conceals fraud as effectively as

overstatement of assets Accompanied by understatement of expenses

and overstatement of net income

14-6

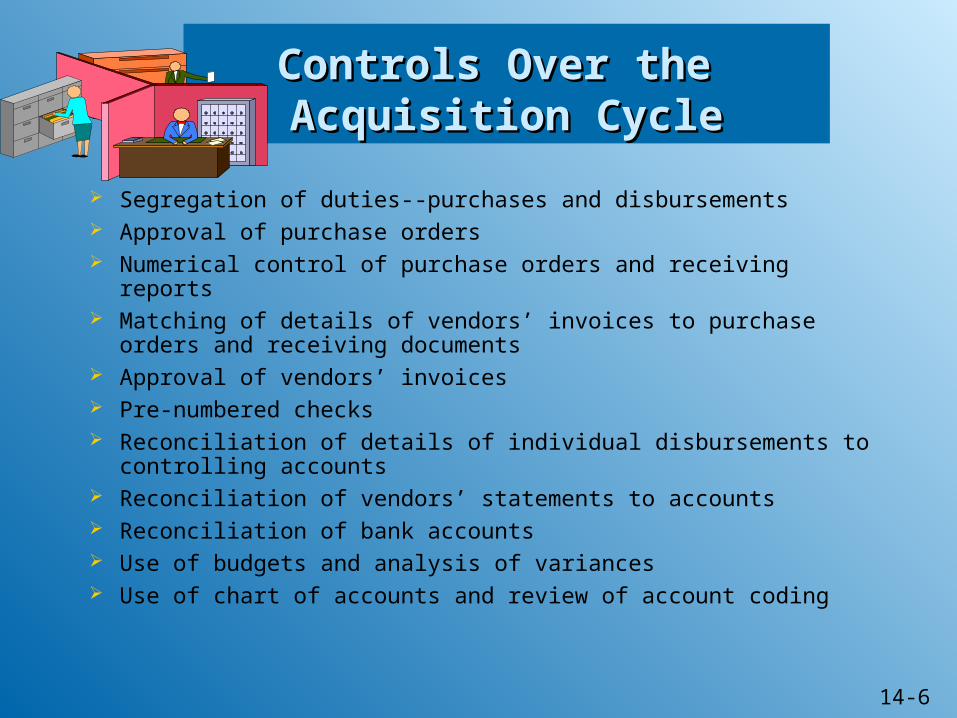

Controls Over the Controls Over the Acquisition CycleAcquisition Cycle

Segregation of duties--purchases and disbursements Approval of purchase orders Numerical control of purchase orders and receiving reports Matching of details of vendors’ invoices to purchase orders and

receiving documents Approval of vendors’ invoices Pre-numbered checks Reconciliation of details of individual disbursements to controlling

accounts Reconciliation of vendors’ statements to accounts Reconciliation of bank accounts Use of budgets and analysis of variances Use of chart of accounts and review of account coding

14-7

Acquisition Cycle--Documents Acquisition Cycle--Documents

Purchase order Receiving report Vendor’s invoice Vendor’s statement

14-8

14-9

Audit DocumentationAudit Documentation

Working papers Lead schedule for accounts payable Trial balances of various types of accounts

payable Confirmation requests for accounts payable Listing of unrecorded accounts payable

14-10

14-11

Risks of Material MisstatementRisks of Material Misstatement

Controls against misstatements Auditors found serially numbered receiving

reports are prepared Serially numbered vouchers are prepared Payments made promptly on due dates Immediately recorded in accounting records Independent employee reconciles subledger

to general ledger

14-12

Risks of Material MisstatementRisks of Material Misstatement Risks of misstatements

Subsidiary records not in agreement with general ledger

Receiving reports and vouchers used haphazardly

Purchase transactions often not recorded until payment is made

Many accounts payable long past due Risks such as these indicate the need for

extensive substantive procedures

14-13

Accounts Payable Audit Accounts Payable Audit Steps (1 of 4)Steps (1 of 4)

A. Use the understanding of the client and its environment to consider inherent risks,

including fraud risks, related to accounts payable.

B. Obtain an understanding of internal control over accounts payable.

C. Assess the risks of material misstatement and design further audit procedures.

14-14

Accounts Payable Audit Accounts Payable Audit Steps (2 of 4)Steps (2 of 4)

D. Perform further audit procedures—tests of controls.1. Examples of tests of controls.

a. Verify a sample of postings to the accounts payable control account.

b. Vouch to supporting documents a sample of postings in selected accounts of the accounts payable subsidiary ledger.

c. Test IT application controls.

2. If necessary, revise the risks of material misstatement based on the results of tests of controls.

14-15

Accounts Payable Audit Accounts Payable Audit Steps (3 of 4)Steps (3 of 4)

E. Perform further audit procedures—substantive procedures for accounts payable.

1. Obtain or prepare a trial balance of accounts payable as of the balance sheet date and reconcile with the general ledger.

2. Vouch balances payable to selected creditors by inspection of supporting documents.

3. Reconcile liabilities with monthly statements from creditors.

4. Confirm accounts payable by direct correspondence with vendors.

14-16

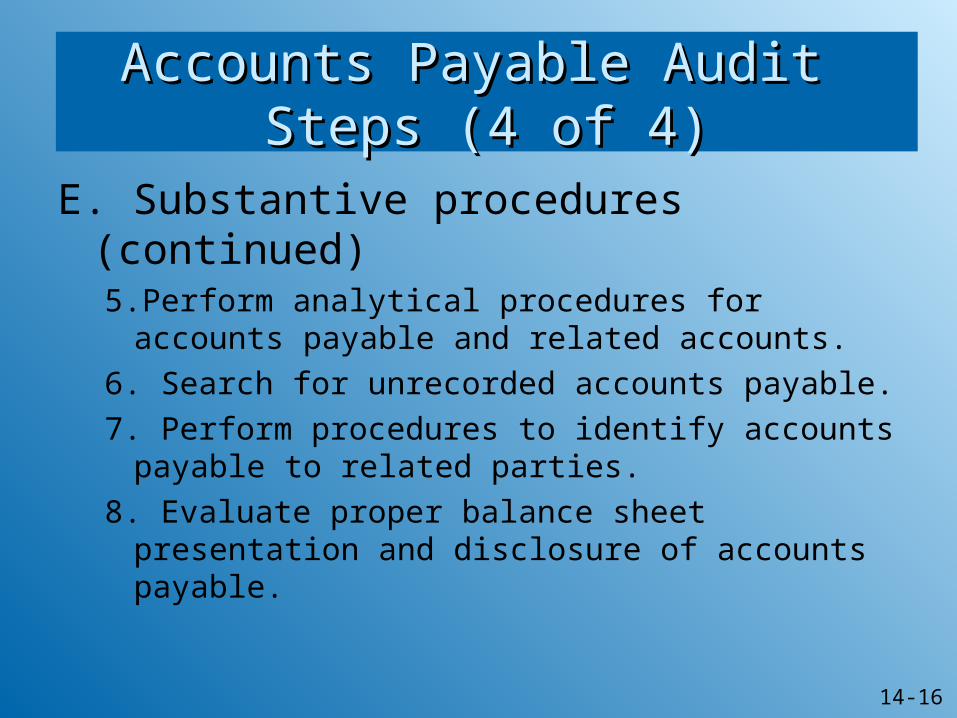

Accounts Payable Audit Accounts Payable Audit Steps (4 of 4)Steps (4 of 4)

E. Substantive procedures (continued)5.Perform analytical procedures for accounts payable

and related accounts.

6. Search for unrecorded accounts payable.

7. Perform procedures to identify accounts payable to related parties.

8. Evaluate proper balance sheet presentation and disclosure of accounts payable.

14-17

Summary of Substantive Tests of Summary of Substantive Tests of Accounts PayableAccounts Payable

14-18

Contrasting Confirmation of Accounts Contrasting Confirmation of Accounts Payable and Accounts ReceivablePayable and Accounts Receivable

Accounts Payable Accounts Receivable

Primary Audit Completeness Existence Objective

Other Evidence External evidence Internal evidence Available held by client (i.e.., (i.e., sales invoices, vendors’ invoices receiving reports)

and statements)

Confirmation Generally No Yes Required?

14-19

Search for Unrecorded A/PSearch for Unrecorded A/P

Be alert during reconciliations, confirmations and analytical procedures for unrecorded liabilities

Examine transactions recorded following year-end Compare cash payments after year-end to a/p

trial balance Examine cash disbursements over specific

dollar amounts during subsequent period

14-20

Potential Sources of Potential Sources of Unrecorded A/PUnrecorded A/P

Unmatched invoices and unbilled receiving reports

Vouchers payable entered in the voucher register subsequent to balance sheet date

Invoices received after balance sheet date Consignments in which client acts as a

consignee

14-21

14-22

Adjusting entry needed?Adjusting entry needed?

Misstatements and omissions are judged based on impact on the financial statements Materiality

• Effect on net income• Need to consider cumulative effect on the financial

statements

14-23

Amounts withheld from Amounts withheld from employees’ payemployees’ pay

Income taxes withheld from employees’ pay but not remitted as of balance sheet date

Trace amounts withheld to payroll summary sheets

Test computations of taxes withheld and accrued

Determine that taxes have been deposited in accordance with law

14-24

Sales Tax PayableSales Tax Payable

Required to collect sales tax imposed by state and local governments

Not an expense, just collecting agent Liabilities until remitted Verify liability by reviewing tax return Test reasonableness of amount Test invoices for correct tax charge

14-25

Unclaimed wagesUnclaimed wages

Subject to misappropriation Concerned with adequacy of internal

control Should not be left for more than a few day Prompt deposit in special bank account

Analyze unclaimed wages to determine Credit represents all unclaimed wages after

each payroll distribution Debits represent authorized payments

14-25

14-26

Customers’ DepositsCustomers’ Deposits

Deposits on returnable containers or to guarantee payment of bills

Review procedures followed in accepting and returning deposits

Verify list of individual deposits and compare to general ledger account

Generally do not confirm

14-27

Accrued Liabilities (1 of 3)Accrued Liabilities (1 of 3)

Obligations payable sometime during the succeeding period for services or privileges received before balance sheet date

Examples: Interest payable, accrued property taxes Accounting estimates

Review and test management’s process of developing the estimate

Review subsequent events Independently develop estimate to compare

14-28

Accrued Liabilities (2 of 3)Accrued Liabilities (2 of 3)

Basic audit steps1. Examine any contracts or other documents on hand that provide the

basis for the accrual.

2. Appraise the accuracy of the detailed accounting records maintained for this category of liability.

3. Identify and evaluate the reasonableness of the assumptions made that underlie the computation of the liability.

4. Test the computations made by the client in setting up the accrual.

5. Determine that accrued liabilities have been treated consistently at the beginning and end of the period.

6. Consider the need for accrual of other accrued liabilities not presently considered (that is, test completeness).

7. For significant estimates, perform a retrospective analysis of the prior year’s estimates for evidence of management bias.

14-29

Accrued Liabilities (3 of 3)Accrued Liabilities (3 of 3)

Accrued Property Taxes Accrued Payrolls Pension Plan Accruals Postemployment Benefits other than Pensions Accrued Vacation Pay Product Warranty Liabilities Accrued Commission and Bonuses Income Tax Payable Accrued Professional Fees

14-30

PresentationPresentation

Current liability Accrued expenses Deferred income tax for next year Deferred credits for rent Deposits on contracts

Long-term liability Deferred income tax - noncurrent

14-31

Time of ExaminationTime of Examination

Most effective when performed immediately after the balance sheet date

Little value if done before because concern with understatements

Some can be done at interim: Accrued property taxes Amounts withheld from employees’ pay