Embed Size (px)

Citation preview

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 1/56

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 2/56

Nature of Manufacturing Business

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 3/56

Merchandisingincludes cost of

merchandise purchased

including the

transportation cost of

bringing merchandise to

the business place.

Manufacturinginvolves the conversion

of raw materials into

finished goods through

the application of labor

and various factory cost

incidental to the

production of products.

Manufacturing business makes major investments in

physical facilities such as factory site, factory building

and acquisition of various machinery and equipment to

be use in the factory.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 4/56

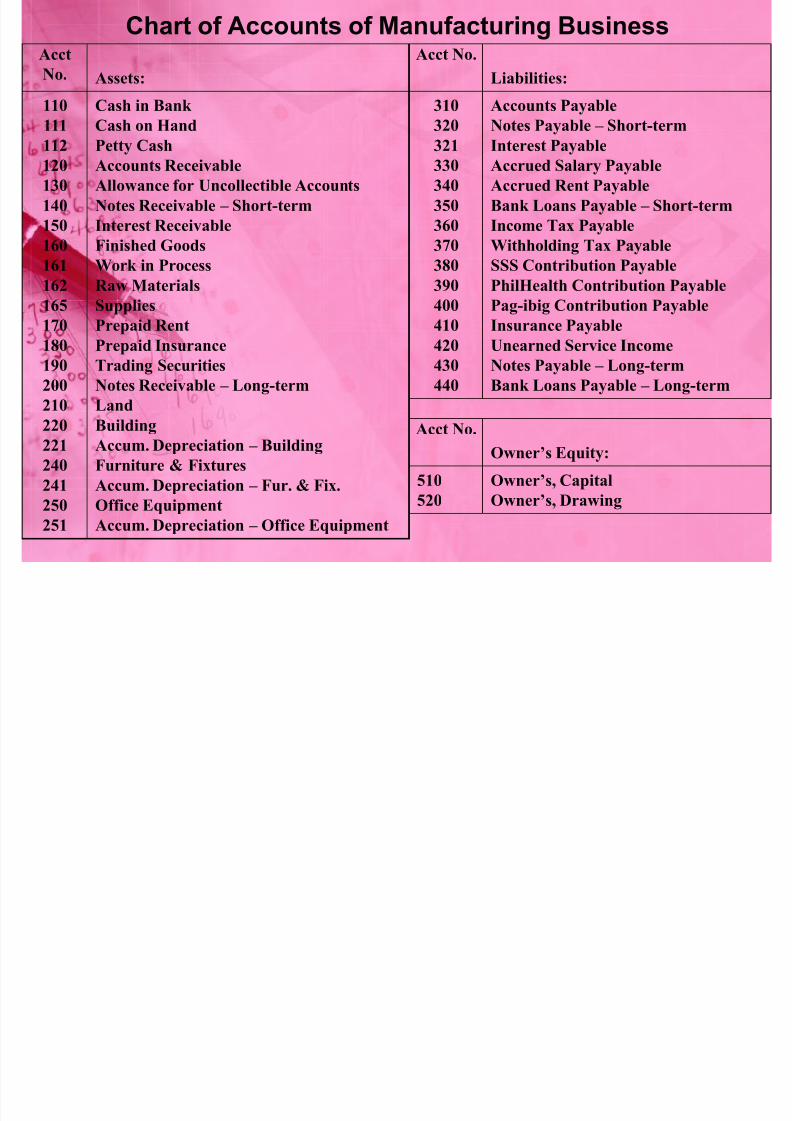

Chart of Accounts of Manufacturing BusinessAcct

No. Assets:

110

111112

120

130

140

150

160

161162

165

170

180

190

200

210

220

221

240

241

250

251

Cash in Bank

Cash on HandPetty Cash

Accounts Receivable

Allowance for Uncollectible Accounts

Notes Receivable – Short-term

Interest Receivable

Finished Goods

Work in ProcessRaw Materials

Supplies

Prepaid Rent

Prepaid Insurance

Trading Securities

Notes Receivable – Long-term

Land

Building

Accum. Depreciation – Building

Furniture & Fixtures

Accum. Depreciation – Fur. & Fix.

Office Equipment

Accum. Depreciation – Office Equipment

Acct No.

Liabilities:

310

320321

330

340

350

360

370

380390

400

410

420

430

440

Accounts Payable

Notes Payable – Short-termInterest Payable

Accrued Salary Payable

Accrued Rent Payable

Bank Loans Payable – Short-term

Income Tax Payable

Withholding Tax Payable

SSS Contribution PayablePhilHealth Contribution Payable

Pag-ibig Contribution Payable

Insurance Payable

Unearned Service Income

Notes Payable – Long-term

Bank Loans Payable – Long-term

Acct No.

Owner’s Equity:

510

520

Owner’s, Capital

Owner’s, Drawing

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 5/56

Acct

No. Cost and Expenses:

810

811

812

813

814

815

820

830

840

850

860870

880

890

900

905

910

920

930

940

950

960

Purchases

Purchases returns

Purchases allowances

Purchases discounts

Freight-in

Cost of goods sold

Salary Expense

Rent Expense

Utilities Expense

Uncollectible Accounts Expense

Advertising ExpenseInsurance Expense

Taxes and Licenses

Supplies Expense

Interest Expense

Freight-out

Depreciation Expense

Employees Benefits Expense

Loss on Sale of Land (Building, Furniture

& Fixture or Office Equipment)

Unrealized Holding Loss – Trading Sec

Loss on Sale of Trading Securities

Miscellaneous Expense

Acct

No. Revenues:

610

611

612

613

620

630

640

650

660

Sales

Sales returns

Sales allowances

Sales discounts

Interest Income

Rent Income

Dividend Income

Gain on sale of Land (Building,

Furniture & Fixture or Office

Equipment)

Unrealized Holding Loss – Trading Sec

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 6/56

Operating Cycle of Manufacturing Business

Phase 1:

Buy Raw Materials

Phase 2:

Processed raw materials to

finished goods

(Raw materials + direct labor

+ factory overhead)

Phase 3:

Sell finished goods to

customers

Phase 4:

Collect from customers

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 7/56

Cost Elements of

Manufacturing Business

3 Types of Production Costs:

1. Raw Materials

2. Direct Labor3. Factory Overhead

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 8/56

Raw Materials

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 9/56

Direct Labor

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 10/56

Factory Overhead

The cost of factory overhead is called as

manufactur ing overhead cost . It refers to all indirectmaterials, indirect labor and other miscellaneous

items used in the making of a product.

Examples are:used factory supplies

salary of factory supervisors

factory depreciation

factory maintenance.

As a rule, if a cost could not be classified as

direct raw materials or direct labor, it is classified as

factory overhead.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 11/56

When the three elements of production cost are mixed,

the following costs can be determined until a product is

produced.

1.Manufacturing costs. This is the sum of the three (3)cost elements: direct materials, direct labor and factory

overhead. This is sometimes referred to as production

cost or factory cost .

2.Work-in-process. The portion of the total

manufacturing costs that pertains to the goods under

process which are not yet 100% completed at the end of

the accounting period.3.Cost of goods manufactured. The portion of the

total manufacturing costs pertaining to the work which

is 100% processed and completed, transferred to

finished goods.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 12/56

The unsold finished goods, unfinished goods-in-

process and unused raw materials at the end of the period

are inventories, which should be reported as part of the

current assets of the business.

The ending inventories of each type of business are

compared as follows:MERCHANDISING MANUFACTURING

1. Merchandise inventory

(Unsold merchandise at

the end of the period)

1. Finished goods inventory

(unsold)

2. Work-in-process inventory(incomplete)

3. Raw materials inventory

(unused)

4. Factory supplies inventory(unused)

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 13/56

Comparative Cost Flow

The comparative cost flow of merchandising and manufacturing

business could be outlined as follows:

MERCHANDISING

Merchandise beginning Pxxx

Add (Deduct) Net purchases

Purchases Pxxx

Freight-in xxx

Purchase discount (xxx)

Purchase allowances (xxx)

Purchase returns (xxx) xxxTotal goods available for sale Pxxx

Less: Unsold merchandise at

the end of the period xxx

Cost of goods sold Pxxx

MANUFACTURING Direct materials, beginning Pxxx

Add (Deduct) Net purchases

Purchases Pxxx

Freight-in xxx

Purchase discount (xxx)

Purchase allowances (xxx)

Purchase returns (xxx) xxx

Total direct materials for usePxxx

Less: Unused raw materials at the end of the

period xxx

Direct materials used Pxxx

Add: Direct labor Pxxx

Factory overhead xxx xxx

Total manufacturing costs Pxxx

Add: work-in-process, beg. xxx

Total work-put-in-process PxxxLess: work-in-process, end xxx

Total costs of goods manufacturedPxxx

Add: finished goods, beg. xxx

Total finished goods for sale Pxxx

Less: finished goods, end xxx

Cost of goods manufactured and sold Pxxx

The Cost of Sales can be described

as Cost of Goods Sold for a merchandising business since the items purchased are

already the final product sold.

On the other hand, it is described as

the Cost of Goods Manuf actured and

Sold for manufacturing firms because the

items purchased are converted into

finished products before they are sold.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 14/56

ASSETS IN THE BALANCE SHEET

Raw Materials

Direct Labor

Factory Overhead:

• Indirect Materials

• Indirect labor

• Factory depreciation

and other factory

expenses W O R K - I N - P R O C E S

S

I N V E N T O R Y

EXPENSE IN THEINCOME STATEMENT

Cost of

goods sold

F I N

I S H E D G O O D S

I N V E N T O R Y

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 15/56

Prime Cost and Conversion Cost

The cost elements of a manufacturing firm could be combined

and formed as (1) prime costs and (2) conversion costs.

1. Prime Costs consist of direct materials and direct labor used

to make the product . This cost is called prime cost or direct

cost because the primary materials and main labor are

combined in making the product.

2. Conversion Costs includes the costs of direct labor and

all indirect costs.

This is called conversion cost because the direct labor andoverhead costs transform the raw materials to finished goods.

Indirect manufacturing cost is also called manufacturing

overhead or factory overhead cost.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 16/56

The Cost of Goods

Manufactured and Sold

The cost of goods manufactured and sold

account is generally used to describe the

merchandise sold by a manufacturing

business. The schedule of cost of goods

manufactured and sold is presented as

follows (all amounts assumed):

VALROX Manufacturing

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 17/56

Raw materials used:

Beginning raw materials inventory P 70,000

Add: Net raw materials purchases

Raw materials purchases P 200,000

Freight-in 5,000

Gross raw materials purchases 205,000

Less: Purchase discounts P2,500

Purchase returns 1,500

Purchase allowances 1,000 5,000 200,000

Total raw materials available for use P 270000

Less: Ending raw materials inventory 20,000 P250000

Direct labor 400,000

Factory overhead 150,000

Total manufacturing cost P800000

Add: Work in process, beginning 100,000

Total cost of goods in process P900000

Less: Work in process, ending 150,000

Total cost of goods manufactured P750000

Add: Finished goods, beginning 50,000

Total finished goods available for sale P800000

Less: Finished goods, ending 150,000

Cost of oods manufactured and sold P650000

VALROX Manufacturing

Schedule of Cost of Goods Manufactured and Sold

For the Year Ended December 31, 200x

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 18/56

Cost versus Non-Cost SystemThe accounting for manufacturing activities may be done using

either Cost System or Non-Cost System.

1. Cost System maintains detailed perpetual records of the cost

of raw materials, work-in-process and finished goods

inventory. This system provides an updated information about

manufacturing costs which serves as helpful guide for pricedecision-making.

2. Non-cost system determines the cost of goods manufactured

based on the periodic actual physical count of ending inventory

for materials, work-in-process, and finished goods, converting

these into value using the adapted cost method (FIFO or

weighted average).

This chapter discusses the manufacturing accounting using the

non-cost system.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 19/56

Under the non-cost system, the manufacturing cost should be summarized

in manufacturing account which basically includes the following postings:

Debit Credit

1. Beginning 4. Purchase return

Inventory

5. Purchase discounts

2. Purchases

6. Manufacturing

3. Freight-In Summary

Direct Raw MaterialsDebit Credit

1. Work-in-process, 5. Work-in-process,

beginning end (per account)

2. Direct raw

materials used

6. Transferred to

3. Direct Labor Finished goods

(per account)

4. Factory overhead

Manufacturing Summary

Debit Credit1. Actual payroll

paid 3. Manufacturing

summary

2. Accrued payroll

Direct Labor

Debit Credit

1. Actual payroll,

indirect

2. Accrued payroll,

indirect

3. Factory utilities 7. Manufacturing

4. Taxes/Insurances Summary

5. Depreciation

Factory6. Factory supplies

Factory Overhead

Debit Credit

1. Manufacturing

Summary

Work-In-Process

Debit Credit

1. Beginning

Inventory

2. Manufacturing Finished goods sold Summary

Finished Goods

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 20/56

Notes:

1. The cost of goods manufactured and sold,

computed as follows:

Finished goods, beginning Pxxx Add: Transferred to finished goods xxx

Total Pxxx

Less: Finished goods inventory,end xxx

Cost of goods manufactured and sold Pxxx

2. The appropriate journal entry for the finished goods inventory end would be

Finished goods, end xxx

Income summary xxx

The debit to finished goods end represents the item to be reported in the SFP,while the credit to income summary is the finished goods end to the income

statement representing a reduction of the cost of finished goods sold during the

period.

Debit Credit

1. Finished goods

sold

Cost of Goods Manufactured and Sold

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 21/56

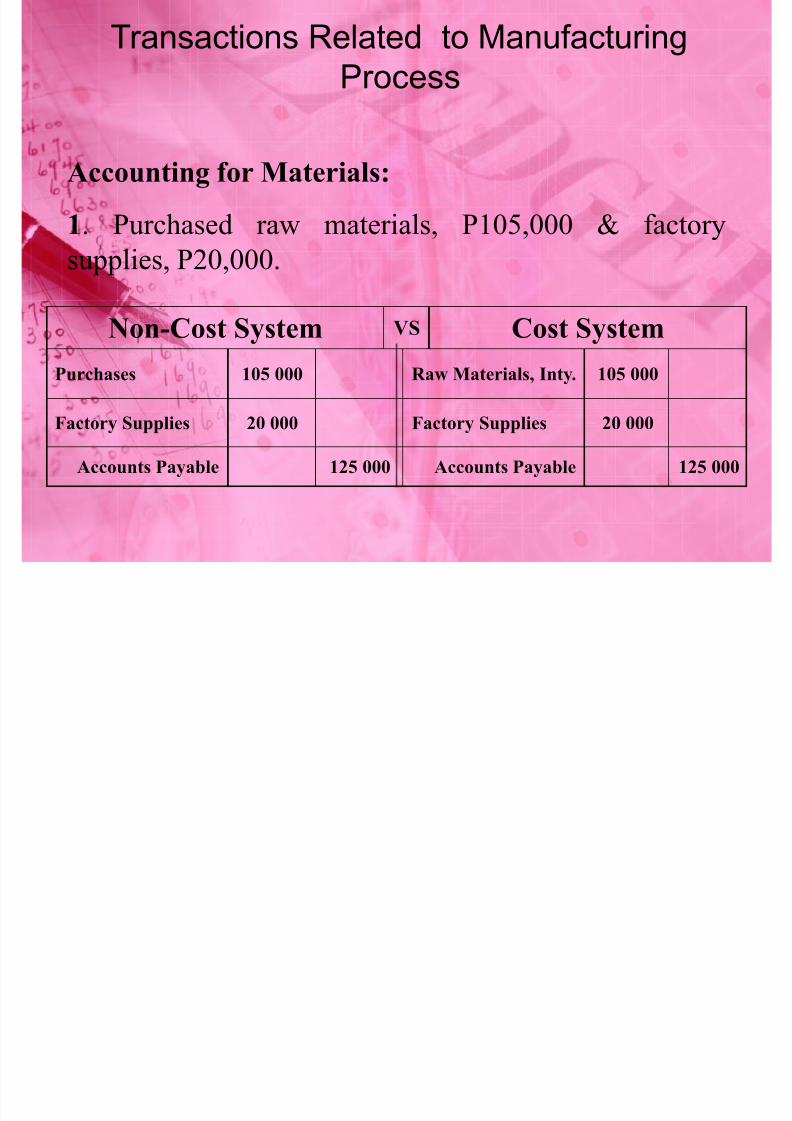

Transactions Related to ManufacturingProcess

Business transactions of manufacturing firms are

generally similar to the merchandising firm except that

a merchandising firm doest not produce goods.

The accounting for the production of goods includes

the following pro-forma entries ( comparing periodic

non cost accounting system from perpetual cost

accounting system):

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 22/56

Transactions Related to Manufacturi

Process

Business transactions of manufacturing

firms are generally similar to the merchan-

dising firm except that a merchandising firm

does not produce goods.

The accounting for the production of

goods includes the following pro-forma

entries (comparing periodic non-costaccounting system from perpetual cost

accounting system):

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 23/56

Transactions Related to Manufacturing

Process

Accounting for Materials:

1. Purchased raw materials, P105,000 & factory

supplies, P20,000.

Non-Cost System VS Cost System

Purchases 105 000 Raw Materials, Inty. 105 000

Factory Supplies 20 000 Factory Supplies 20 000

Accounts Payable 125 000 Accounts Payable 125 000

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 24/56

2. Returned defective raw materials to vendor, P5,000.

Non-Cost System VS Cost System

Accounts Payable 5 000 Accounts Payable 5 000

Purchase Returns 5 000 Raw materials, inty. 5 000

3. Paid the accounts payable less P2,000 cash discount.

Non-Cost System VS Cost SystemAccounts Payable 120 000 Accounts Payable 120 000

Cash 118 000 Cash 118 000

Purchase Returns 2 000 Raw materials, inty. 2 000

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 25/56

4. Issued raw materials, P97,000 & factory supplies,

P20,000 for factory use.

Non-Cost System VS Cost System

No entry WIP - Raw Materials 97 000

WIP - Overhead 20 000

Raw materials, Inty. 97 000

Factory Supplies 20 000

5. Returned excess raw materials to storeroom, P2,000.

Non-Cost System VS Cost System

No entry Raw materials, Inty. 2 000

WIP – Raw materials 2 000

Note : WIP means work-in-process

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 26/56

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 27/56

Accounting for Labor:

7. Paid payroll of factory: Direct workers, P100,000;Supervisor, P20,000; Janitor, P3,000.

Non-Cost System VS Cost System

Direct Labor 100 000 WIP, Direct Labor 100 000

Indirect Labor 23 000 WIP, Factor Overhead 23 000

Cash 123 000 Cash 123 000

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 28/56

8. Closed direct labor cost account.

Non-Cost System VS Cost System

WIP – Direct Labor 100 000 No Entry

Direct Labor 100 000

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 29/56

Accounting forFactory Overhead

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 30/56

Non- Cost System Cost System

Depreciation expense- Work-in-process, FOH 17,000

factory 12,000 Accum. Depreciation-

Insurance expense- factory machine 12,000

factory 4,000 Cash 5,000

Miscellaneous

expense-factory 1,000

Accum. Depreciation-

factory machine 12,000

Cash 5,000

9.Recorded other factory overhead expenses:

Depreciation of factory machine, P12,000; Paid

factory insurance expense, P4000 and miscellaneousfactory expense, P1,000.

VS

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 31/56

Non- Cost System Cost System

Manufacturing overhead

summary 60,000

factory supplies 20,000

Indirect labor 23,000 No entry

Dep’n expense -

factory

12,000

Insurance expense

- factory 4,000

Miscellaneous expense

- factory 1,000

10. Summarized factory overhead accounts.

VS

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 32/56

Non- Cost System Cost System

Work-in-process, FOH 60,000

Manufacturing

overhead

No entry

summary 60,000

11. Closed factory overhead

VS

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 33/56

Accounting for Cost of

Goods Manufactured

and Sold

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 34/56

Non- Cost System Cost System

*Cost of goods Cost of goods

Manufactured 196,000 Manufactured 196,00

0

WIP – Raw

materials

76,000 WIP – Raw

materials

76,000

WIP – Direct

labor

80,000 WIP – Direct labor 80,000

WIP - FOH 40,000 WIP – FOH 40,000

12. Recorded 80% goods completed.

VS

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 35/56

Non- Cost System Cost System

Cost of goods Cost of goods

Manufactured andsold

206,000 Manufactured andsold

206,000

*Finished goods,

end

10,000 Finished goods,

end

10,000

Finished goods,beg 20,000 Finishedgoods, beg20,000

Cost of goods Cost of goods

manufactured 196,000 manufactured 196,000

13. Closed cost elements of cost of sales (assuming

that finished goods - beginning, P20,000 and finished

goods – ending, P10,000)

VS

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 36/56

Non- Cost System Cost System

Sales 400,000 Sales 400,000

Cost of goods 206,000 Cost of goods 206,000

manufactured

and sold

194,000 manufactured

and sold

194,000

Incomesummary

Incomesummary

14. Closed revenue and cost of sales to

income summary (assuming that the total

sales is P400,000).

VS

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 37/56

CostAccumulation

Procedures

Process Costing

Job Order Costing

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 38/56

Process Costing

Is a system applicable to continuous

process of production of the same or

similar (i.e. homogenous) goods.

There is no need to determine thecosts of the different groups of

products because the product is

uniform. Thus, each processing

depar tment becomes a cost center .

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 39/56

Job Order Costing

Is a system of allocating costs to group of

unique products. It is applicable to the

production of customer’s specified

products. Each job becomes a cost center

from which costs are accumulated. A

subsidiary record called a JOB ORDER

SHEET is needed to keep track of all

unfinished jobs (work-in-process) and

finished jobs (finished goods).

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 40/56

Distinction between Process

Costing and Job Order Costing

Process Costing Job Order Costing1. Homogenous units pass through a

series of similar process.

1. Unique jobs are worked on a time

period.

2. Costs are accumulated by

processing department.

2. Costs are accumulated by

individual job order.

3. Unit costs are computed by dividing

the individual processing department’s

costs by the equivalent units of

production.

3. Unit costs are determine by dividing

the total costs on the job cost sheet by

the number of units on the job.

4. The cost of production report

provides the detail for the work-in-

process account for each processing

departments.

4. The job cost sheet provides the

detail for work-in-process account.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 41/56

Job Order

Costing

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 42/56

Job Order Costing

Assumptions: Raw materials are recorded under perpetual

inventory system. Total materials issuance for the period based on

store requisition slip, patrol costs per payroll summary, and cash

voucher and payable voucher for supplies is as follow:

J O B O R D E R S

Total 001 002 003 Direct raw

materials P1,500,000 P1,300,00 P100,000 P100,000

Direct labor 950,000 800,000 100,000 50,000

Indirect labor 475,000 350,000 85,000 40,000

Factory supplies 75,000 50,000 15,000 10,000

P3,000,000 P2,500,000 P300,000 P200,000

Status at the end of

accounting period Completed In process In process

Journal entries

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 43/56

Journal entries

1. To record the costs incurred

GENERAL LEDGER

Date Description Page number 200Debit Credit

(a) Work-in-process - materials 1,500,000

Work-in-process - direct labor 950,000

Work-in-process - indirect labor 475,000

Work-in-process - factory supplies 75,000

Raw materials 1,500,000

Cash 1,425,000

Accounts payable 75,000

Note: individual subsidiary ledger for each job order is maintained; hence the

above entries affecting the work-in-process accounts are posted in the general

ledger and subsidiary ledger.

2 To record the completed job order 001

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 44/56

GENERAL LEDGER

Date Description Page number 200

Debit Debit

(c) Accounts receivable 3,125,000

Sales 3,125,000

To record billing for job order 001.

(d) Cost of goods manufactured and sold 2,500,000Cost of goods manufactured 2,500,000

To record cost of goods sold

(e) Sales 3,125,000

Cost of goods manufactured and sold 3,125,000

Income summaryTo close revenue and cost of goods sold

GENERAL LEDGER

Date Description Page number 200

Debit Credit

(b) Cost of goods manufactured 2,500,000Work-in-process – Job 001 2,500,000

2. To record the completed job order 001

3. Supposing that Job Order 001 was billed at P3,125,000 (using

perpetual inventory system), the journal entries would be:

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 45/56

Just-in-time is a manufacturing model based on the

philosophy that storing inventory is a non-value added

activity that a company should try to reduce or

eliminate. Hence, the best decision is to maintain zero

or minimal inventories.

This manufacturing model implies that products

should be produced when needed in the quantities

needed by customers , so there is little need for work-

in-process or finish goods inventories. In addition, raw

materials should arrive when needed, in the quantities

needed for production.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 46/56

JIT is a pull system, that is productionis determined by customer demand , and the

need for raw materials is determined by

production. Accordingly, manufacturingfirms that adopt this model use the

backflush costing system, which is

described as follows:

1 The amount of raw materials purchased direct labor used and

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 47/56

1. The amount of raw materials purchased , direct labor used, and

manufacturing overhead applied on the cost of goods sold

account for the period will expensed during the same period.

2. At the end of the period, if any inventory remains on hand, it is

necessary to make an entry for the adjustment of the cost of

goods sold account to reflect the cost of the remaining

inventory.

3. The cost of the ending inventory , whether it is a raw material,

work-in-process, or finished goods, is recorded in a current

asset account called raw and in-process inventory.

This accounting method eliminates the need for separate

raw materials, work-in-process and finished goods inventory

accounts, so is saves record-keeping time and cost.

Illustration:

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 48/56

Illustration:

Japan company incurs the ff. cost in connection with

the production of a product named Kamukhamo:

Raw materials purchased P 100,000

Direct labor used 150,000

Manufacturing overhead applied 50,000

At the end of the period the cost of Kamukhamo

still-in-process is P10,000 and there are 5,000 raw material

still unused.

The journal entries of the above JIT production

activities using backflush accounting would be:

GENERAL JOURNAL

The recording of raw materials

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 49/56

Date Description Page Number 100

Debit Credit a) Cost of goods sold 100,000

Accounts payable 100,000 To record the purchase of

Inventory on acount b) Cost of goods sold 150,000

Accrued wages payable 150,000 To record the labor used in

production. c) Cost of goods sold 50,000

Factory overhead 50,000 To record the overhead applied

to production d) Raw and in-process inventory 15,000

Cost of goods sold 15,000 To record raw materials and

work-in-process inventory

The recording of raw materials,

labor and overhead is eliminated

because the products are

presumed to be in accordance

with the customer’s demand.

Accordingly, the cost of goods

sold account is immediately

debited upon requisition of the

basic manufacturing costs. This

is accordance with the principle

that the cost of finished goods

should be expensed at the periodof production.

At the end of the production

period, the raw material unused

and the work-in-process are

adjusted in the raw and in-

process inventory account.

The cost of goods sold, net of

raw and in-process inventory at

the end of the period is actually

the amount of the total cost of

goods manufactured and sold.

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 50/56

Cost of Goods Sold Account

No.16 Debit Credit

Direct Materials 100,000 Raw and in-process 15,000 Direct Labor 150,000

Factory Overhead 50,000 300,000 285,000 Raw and In-Process Inventory Account

No. 18 Debit Credit

Cost of goods sold 15,000

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 51/56

Activity-BasedCosting System

(ABC SYSTEM)

C ( C) S

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 52/56

Activity-Based Costing (ABC) System

Activity-based costing uses more than one predetermined

overhead rate to assign overhead costs for each activity utilized

in production. Accordingly, this method ensures that the amount

of overhead assigned represents the resources consumed.

When companies use an activity-based costing(ABC)

system, they first assign estimated manufacturing overheadcosts to activity level called cost pools. A cost pool is a group of

costs that change in response to the same cost driver. Cost

Drivers measure activity in the conversion cycle and are

assumed to cause the change of conversion cycle cost. A goodexample of cost driver is the number of hours used for a

particular type of activity.

The following activity-based costing overview facilitates an understanding of the

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 53/56

concept:ACTIVITY-BASED COSTING OVERVIEW

Activity Level Types of Activities Types of Costs Example of Cost Drivers

Facility Owning buildings Depreciation Number of square feetsustaining Occupying buildings Property taxes Number of square feet

Using buildings Utilities BTUs of heat produced

Maintaining buildings Insurance Number of square feet

Product Testing products Testing costs* Number of tests required

sustaining Designing products Design costs* Number of hours of design timeMaintaining products inventory Carrying costs* Number of parts required

Using specialized machinery Depreciation No. of specialized processes required

Batch related Ordering parts Ordering costs* Number of orders placed

Setting up machines Setup costs* Number of setups required

Handling materials Moving costs* Number of moves required

Requisitioning parts Requisition cost Number of requisition made

Unit related Cutting/drilling units Power costs Number of machine hours

Assembling units Indirect labor Number of labor hours

Painting units Indirect material Direct materials cost

Inspecting units Rework costs* Number of units reworked*Includes the salaries and wa es of those individuals involved in the acitivit .

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 54/56

Illustration

Assume the following costs and cost drivers of the cost

pools of New Products Manufacturing Company:

Predetermined overhead rates:

Cost drivers Costs assigned Total cost driver Cost driver per unit

Building costs P400,000 100,000 sq. ft. P4 per square foot

Development costs P200,000 20,000 hoursP10 per development

hour

Product testing costs P 30,000 30 quality test P1,000 per test

Setup and inspection P150,000 150 production runsP1,000 per production

run

Machine usage costs P 50,00010,000 machine

hoursP5 per machine hour

Assuming that during the period the production of New

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 55/56

Assuming that during the period, the production of New

Products Manufacturing Company actually required the

following resources to produce Kamukhamo products:

•3,000 square feet of building space•2,000 hours of development time

•10 quality tests

•150 production runs

•1,000 machine runs

Using the predetermined overhead rates, the manufacturing overhead

is applied to the production, as follows:

Building costs: (P 4x 3,000 sq.feet) = P 12,000

Development costs: (P10x 2,000 devt.hours) = 20,000Product testing costs: (P1,0000x10 quality tests) = 10,000

Setup and inspection costs: (P1,000x150 production runs) = 150,000

Machine usage costs: (P5x1000) = 5,000

Total Manufacturing overhead applied in the period = P 197,000

8/13/2019 Accounting for Manufacturing Business

http://slidepdf.com/reader/full/accounting-for-manufacturing-business 56/56

The appropriate journal entry to reflect the applied

manufacturing overhead costs for the period would be:

GENERAL JOURNAL

Page

100

Number

Date Descriptions Debit Credita) Work-in-process inventory – Kamukhamo 197,000

Factory overhead – Building 12,000

Factory overhead – Development 20,000

Factory overhead – Testing 10,000

Factory overhead –

Setup and inspection 150,000

Factory overhead – Machining 5,000

To record applied manufacturing overhead for

The period