Embed Size (px)

DESCRIPTION

financial accounting

Citation preview

1

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING 1

2

COURSE STRUCTURE

AIM

The aim of the module is to provide non-accounting students with an academically

challenging and intellectually stimulating study of foundation accounting.

ASSESSMENT

Assessment in this module is entirely via coursework.

Course work will consist of three 1 hour class tests, to be completed on days 6, 9 and 12

and one two hour class test which will take place on day 15.

The first class test will have an assessment weighting of 10%.

The second class test will have an assessment weighting of 20%.

The third class test will have an assessment weighting of 20% and the #

Final two hour class test a weighting of 50%.

3

READING LIST

Required Reading:

Atrill P., and McLaney, E., Accounting and finance for Non-Specialists, (6th ed), FT

Prentice Hall, 2008.

Recommended Reading:

Ryan B., Finance and Accounting for Business, (2nd ed), South Western Cengage

Learning, 2008.

Berry., A and Jarvis, R., Accounting in a business context, Thompson (2006)

Wood, F., and Sangster, A., Business Accounting 1, (11th Ed) Prentice Hall, 2008.

Websites:

Chartered Institute of Management Accountants (CIMA) www.cimaglobal.com

Association of Chartered Certified Accountants (ACCA) www.accaglobal.com

Journals:

The following journals are all of particular relevance to this module:

Accounting & Business Magazine

Management Accounting (UK)

4

SESSION TOPIC

SESSION 1 INTRODUCTION & ACCOUNTING EQUATION

SESSION 2 DOUBLE ENTRY

SESSION 3 PRACTICE QUESTIONS

SESSION 4 TRIAL BALANCE & INVENTORY

SESSION 5 ESSAY WRITING

SESSION 6 CAPITAL & REVENUE

SESSION 7 FINANCIAL STATEMENTS

SESSION 8 ACCOUNTING ADJUSTMENTS & ANALYSIS

SESSION 9 MOCK TEST 1

SESSION 10 EXAM 1

SESSION 11 MANAGEMENT ACCOUNTING INTRODUCTION

SESSION 12 JOB COSTING

SESSION 13 PRACTICE QUESTIONS

SESSION 14 MOCK TEST 2

SESSION 15 EXAM 2

SESSION 16 MATERIAL PRICING

SESSION 17 REMUNERATION

SESSION 18 PRACTICE QUESTIONS

SESSION 19 MOCK TEST 3

SESSION 20 EXAM 3

SESSION 21 MANUFACTURING ACCOUNTS

SESSION 22 MANUFACTURING ACCOUNTS QUESTIONS

SESSION 23 REVISION

SESSION 24 MOCK TEST 4

SESSION 25 EXAM 4

5

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION ONE

6

Introduction

The first question many people ask is “what is accounting?”

Basically accounting is broadly made up of two elements:

1. Recording business transactions - Book keeping

2. Presenting the information

7

WHAT IS A BUSINESS?

A business is a commercial organisation which exists with a view to making a profit.

An organisation is an arrangement of people, pursuing common goals achieving results

and standards of performance.

Businesses will fall into 3 main categories.

Sole Trader

This is a business that is owned and operated by one person

Partnership

This type of business is owned by more than one individual, some of which will actively

be involved in the business and others may not.

The main advantage of being a

sole trader is that you can make

your own decisions. You will also

keep all of the profit that you

hopefully will make. However,

there are also disadvantages.

These include having unlimited

liability and also raising finance

could be a problem.

8

Companies

A company is owned by shareholders and is operated on their behalf by a nominated

board of directors.

Responsibility for Financial Statements

The management of an enterprise has the primary responsibility for preparing and

presenting the enterprise's financial statements.

The Framework:

• Defines the objective of financial statements;

• Identifies the qualitative characteristics that make information in financial

statements useful; and

• Defines the basic elements of financial statements and the concepts for

recognising and measuring them in financial statements.

As with sole traders there will be

advantages and disadvantages in

entering into a partnership.

Advantages would include a wider

knowledge base and also more

people to share the workload.

Disadvantages would include losing

some control and maybe having to

compromise your opinions for the

good of the partnership.

9

Users and their Information Needs

The principal classes of users of financial statements are present and potential investors,

employees, lenders, suppliers and other trade creditors, customers, governments and

their agencies and the general public. All of these categories of users rely on financial

statements to help them in decision making.

The framework also concludes that because investors are providers of risk capital to the

enterprise, financial statements that meet their needs will also meet most of the general

financial information needs of other users. Common to all of these user groups is their

interest in the ability of an enterprise to generate cash and cash equivalents and of the

timing and certainty of those future cash flows.

The framework notes that financial statements cannot provide all the information that

users may need to make economic decisions. For one thing, financial statements show

the financial effects of past events and transactions, whereas the decisions that most

users of financial statements have to make relate to the future. Further, financial

statements provide only a limited amount of the non-financial information needed by

users of financial statements.

While all of the information needs of these user groups cannot be met by financial

statements, there are information needs that are common to all users, and general

purpose financial statements focus on meeting these needs.

Management accounts

Management accounts are produced as often as a business wants them (usually

monthly). They are produced for internal use and will not, usually be seen by people

outside of the organisation. Management accounts can be prepared using the

company’s own internal policies.

Financial accounts

Financial accounts are usually produced annually. They are based on historical

information and are rarely used internally. Financial accounts are useful to many

different types of people who are not part of the organisation.

10

Qualitative characteristics of financial statements

The four main characteristics are:

Understandability

Information should be presented in a way that is readily understandable by users who

have a reasonable knowledge of business and economic activities and accounting

and who are willing to study the information diligently.

Relevance

Information in financial statements is relevant when it influences the economic

decisions of users. It can do that both by

(a) helping them evaluate past, present, or future events relating to an enterprise and

(b) confirming or correcting past evaluations they have made.

Materiality is a component of relevance. Information is material if its omission or

misstatement could influence the economic decisions of users.

Timeliness is another component of relevance. To be useful, information must be

provided to users within the time period in which it is most likely to bear on their

decisions.

Reliability

Information in financial statements is reliable if it is free from material error and bias and

can be depended upon by users to represent events and transactions faithfully.

Information is not reliable when it is purposely designed to influence users' decisions in a

particular direction.

There is sometimes a tradeoff between relevance and reliability - and judgment is

required to provide the appropriate balance.

Reliability is affected by the use of estimates and by uncertainties associated with items

recognised and measured in financial statements. These uncertainties are dealt with, in

part, by disclosure and, in part, by exercising prudence in preparing financial

statements. Prudence is the inclusion of a degree of caution in the exercise of the

judgments needed in making the estimates required under conditions of uncertainty,

such that assets or income are not overstated and liabilities or expenses are not

understated. However, prudence can only be exercised within the context of the other

qualitative characteristics in the Framework, particularly relevance and the faithful

representation of transactions in financial statements. Prudence does not justify

deliberate overstatement of liabilities or expenses or deliberate understatement of

11

assets or income, because the financial statements would not be neutral and,

therefore, not have the quality of reliability.

Comparability

Users must be able to compare the financial statements of an enterprise over time so

that they can identify trends in its financial position and performance. Users must also

be able to compare the financial statements of different enterprises. Disclosure of

accounting policies is essential for comparability.

12

The elements of financial statements

Asset is a resource controlled by the enterprise as a result of past events and from

which future economic benefits are expected to flow to the enterprise.

Liabilities are an entity’s obligations to transfer economic benefits as a result of past

transactions or events.

Equity is the residual amount found by deducting all liabilities of the entity from all of the

entity’s assets.

Income is increases in economic benefits during the accounting period in the form of

inflows or enhancements of assets or decreases in liabilities that result in increases in

equity, other than those relating to contributions from equity participants.

Expenses are decreases in economic benefits during the accounting period in the form

of outflows or depletions of assets or incurrences of liabilities that result in decreases in

equity, other than those relating to distributions to equity participants.

Recognition of the elements of financial statements

In order to recognise anything in the Balance Sheet and income statement it must meet

all three of the following criteria:

- Meet the definition of the element (as above)

- Probable future economic benefit will flow to or from the entity

- The item can be measured reliably

13

The Fundamental Assumptions

Prudence

Due to the fact that lots of items within sets of accounts are subjective or uncertain then

a prudent approach must be adopted at all times. This basically means that

professional accountant will exercise a degree of caution in any judgements that have

to be made – to be sure that any assets have not be overstated and liabilities

understated.

Some key examples of this include any time a loss is foreseen then it MUS

recognised and accounted for immediately, and that profits can only be recognised

when they are realised.

The Fundamental Assumptions

When about to prepare a set of Financial Statements, it is

very important that the professional accountant follows

certain key assumptions.

Due to the fact that lots of items within sets of accounts are subjective or uncertain then

a prudent approach must be adopted at all times. This basically means that

professional accountant will exercise a degree of caution in any judgements that have

to be sure that any assets have not be overstated and liabilities

Some key examples of this include any time a loss is foreseen then it MUS

recognised and accounted for immediately, and that profits can only be recognised

When about to prepare a set of Financial Statements, it is

important that the professional accountant follows

Due to the fact that lots of items within sets of accounts are subjective or uncertain then

a prudent approach must be adopted at all times. This basically means that the

professional accountant will exercise a degree of caution in any judgements that have

to be sure that any assets have not be overstated and liabilities

Some key examples of this include any time a loss is foreseen then it MUST be

recognised and accounted for immediately, and that profits can only be recognised

14

Going Concern

The concept of “Going Concern” means that the entity will be considered to be a

going concern unless there is evidence to suggest otherwise. This means that it will

continue to operate in business for the “foreseeable future”. This is assuming that the

entity has no plans to go into liquidation or to significantly curtail (reduce) the scale of

its operations.

Accruals

This principal is often referred to as the “Matching Principal”. It means that income and

expenses must be accounted for in the period to which they relate.

So in other words if you have earned some income then any expenses you incurred to

get it in the first place must be matched against it.

Consistency

To enable the performance of the entity to be compared year on year, items included

must be included consistently from one period to the next – in other words included on

the same basis.

This should remain the situation unless there are any changes required by the issue of

new accounting standards or where there has been a major change in the business

itself such that a different presentation would give a fairer picture.

15

Fair Presentation

The Financial Statements must be presented fairly, in other words free from bias. IAS 1

includes detail on what specifically must be included to ensure that a fair presentation

is given;

• The entity has chosen and applied suitable accounting policies, which are

relevant to it, reliable and are understandable and comparable.

• The information is presented in such a way so that the user can understand,

compare and be able to draw relevant and reliable conclusions from it

• Where necessary additional disclosures have been included.

16

The Accounting Equation

Assets consists of property of all kinds, such as building, machinery, inventory (stock held

for resale), and motor vehicles. Other assets include debts owed by customers to the

business and the amount of money held by the business in cash or in the bank.

Liabilities are amounts owed by the business to a third party, that is other than the

owner.

Capital is often called the owners equity, net worth or net assets. It represents the

amount of money owed by the business to the owner. It is equal to the funds invested in

the business initially by the owner plus any profits earned by the business, less any profits

taken out of the business by the owner (drawings).

Drawings are cash/goods or services taken from the business for the proprietors own

use. They reduce capital but are recorded separately.

17

Three Basic Principles

1 Separate entity

A proprietor and the business are distinct. We look at the business from

Eg Fred puts £1,000 into his business. From the point of view of the business the dual

effect is

– it has £1,000 cash

– it owes Fred £1,000

The liability of a business to its proprietor is known as capital.

2 Dual effect

Every transaction has two effects.

Fred borrows £250 from Sid. The two effects are

– Fred has £250 in cash. The “having” is an ASSET

– Fred owes £250 to Sid. The “owing” is a LIABILITY

The two effects are equal and opposite, hence they balance.

A proprietor and the business are distinct. We look at the business from

Fred puts £1,000 into his business. From the point of view of the business the dual

ASSET

CAPITAL.

The liability of a business to its proprietor is known as capital.

Every transaction has two effects.

Fred borrows £250 from Sid. The two effects are

Fred has £250 in cash. The “having” is an ASSET

Fred owes £250 to Sid. The “owing” is a LIABILITY

The two effects are equal and opposite, hence they balance.

A proprietor and the business are distinct. We look at the business from its point of view.

Fred puts £1,000 into his business. From the point of view of the business the dual

18

3 Accounting equation

The first two principles lead to the third, the accounting equation. The Balance Sheet

(SFP) is based on the accounting equation.

Net assets Propr ietor's funds

Asse ts – liab ilit ies Capital + profits (or – losses) – d rawings

=

=

A BUSINESS

1 Introduce capital

You inherit £100,000 and use it to create a retail business selling books and stationary

called Fox Books. What is the dual effect?

Dual effect

The business has cash of £100,000 (asset)

The business owes you £100,000 (capital)

Fox’s position is

Assets Capital

£ £

19

2 Buy inventory with cash

Fox buys 500 books. The cost of each book is £5. What is the dual effect?

Dual effect

Fox’s position is

Assets Capital

£ £

20

3 Buy inventory on credit

In reality a business will not always pay for its purchases with cash but is more likely to

buy things on credit.

Fox buys inventory of 200 diaries. Each diary costs £10. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

21

4 Buy a delivery van

The delivery van will be a fixed asset because it is available for continuing use in the

business.

Fox buys a delivery van for £1,000 cash. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

22

5 Sell inventory for profit

Fox sells 200 books for £15 each. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

23

6 Sell inventory (on credit) for profit

It is equally likely that a business will sell goods on credit. When goods are sold on credit

an asset of the business called a receivable (debtor) is generated.

Fox sells 100 diaries to Badger . Badger will pay £12.50 per diary at the end of the

month. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

24

7 Pay expenses

In reality Fox will have been incurring expenses from its commencement. Fox

received and paid a gas bill for £500. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

25

8 Take out a loan

In order to fund your future expansion plans for Fox £20,000 is borrowed from Lendit

Bank.

The loan is to be repaid in two years’ time. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

26

9 Payment to trade payables

Fox pays cash of £1,500 towards the £2,000 owed to the supplier. What is the dual

effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

27

10 Receive cash from receivables

Fox’s receivable sends a cheque for £1,000. What is the dual effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

28

11 Drawings

You withdraw £1000 from the business. Such a withdrawal is merely a repayment of

the capital you introduced. Your withdrawal is called drawings. What is the dual

effect?

Dual effect

Fox’s position is

Net assets Capital

£ £

29

Practice question

Edward started a business as a sports equipment retailer on 1 July 2011

(1) Started the business by paying £5,000 into a business bank account.

(2) Bought a 10 tennis rackets for £50 each in cash.

(3) Bought 5 table tennis tables on credit from P Pong, for £100 each.

(4) Sold all the tennis racquets to for £750 cash.

(5) Sold 4 of the table tennis tables on credit to B Bjorg for £300 each.

(6) Paid rent of £250 cash.

(7) Drew £100 in cash out of the business for living expenses.

(8) Paid P Pong £250 on account.

(9) Received £1,200 from B Bjorg in full settlement of the amount due.

(10) Bought a van for use in the business for £4,000 cash.

(11) Paid a telephone bill for £150 in cash

Requirements

Show the accounting equation which results from the above transactions made

during Edward’s first two weeks of trading.

30

Alternative presentation

The accounting equation is often expressed in a financial position statement called the

balance sheet. It shows the financial position at a point in time (snapshot).

Balance Sheet as at 31 December 2010

Non – current assets

£

Buildings 138,000

Fixtures and fittings 33,750

Motor vehicles 12,740

184,490

Current assets

Inventory 13,777

Trade receivables 12,775

Cash 6,200

32,752

Current liabilities

Trade payables 12,445

Loan interest 1,000

Accruals 15,445

(28,890)

Net current assets 3,862

188,352

Non – current liabilities

Loan (20,000)

Net assets 168,352

Opening capital 152,465

Profit 51,787

Drawings (35,900)

168,352

31

Balance sheet classifications:

Non-current assets – are assets purchased not with the primary intention to re-sell them,

but rather to assist in the generation of future income.

Eg

Current assets – are assets which are cash or will be converted into cash within one

year, that is inventory, receivables or cash

Current Liabilities – are those liabilities which have the date of the balance sheet.

32

Edward Balance Sheet as at................

Non – current assets

Motor vehicles

Current assets

Inventory

Trade receivables

Cash

Current liabilities

Trade payables

________

Net current assets

NET ASSETS

Opening capital

Profit

Drawings

33

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION TWO

34

Double Entry Bookkeeping

Introduction

Bookkeeping is “the recording of monetary transactions” of a business. Each company

will employ a bookkeeper to ensure all the accounting records are kept up to date.

Double entry bookkeeping

Double entry bookkeeping is the fundamental concept underlying accountancy. All

accounting transactions should be recorded using the double entry system.

Every transaction is recorded individually in ledger accounts, and these accounts are

kept in the Nominal Ledger.

Ledger Accounts

A ledger account is sometimes called a T Account. It is called this because it looks like

the letter T.

It has two sides – the left side will be classed as the Debit side and the Right will be the

Credit side.

DR T Account CR

Every transaction in the ledger accounts will have a debit transaction and a credit

transaction in another account.

35

It is important to learn which entries are “DEBITS” and which are “CREDITS”

DR T Account CR

Asset Increase Asset Decrease

Liability Decrease Liability Increase

Profit Decrease Profit Increase

We can put the balance sheet into this format plus trading transactions:

Dr Cr

Non current assets

Non current liabilities

Inventory

Receivables Payables

Bank Bank overdraft

Cash

Drawings Capital

Losses Profits

Purchases Sales

Expenses Income

Purchases - buying goods for which the business has the prime intention of re-selling.

Sales – the of those goods which the business normally buys with the intention of selling

to make a profit called GROSS PROFIT

36

Example 1 – Edward again

Edward started a business as a sports equipment retailer on 1 July 2011

1st Started the business by paying £5,000 into a business bank account.

2nd Bought a 10 tennis rackets for £50 each in cash.

3rd Bought 5 table tennis tables on credit from P Pong, for £100 each.

4th Sold all the tennis racquets for £750 cash.

5th Sold 4 of the table tennis tables on credit to B Bjorg for £300 each.

6th Paid rent of £250 cash.

7th Drew £100 in cash out of the business for living expenses.

8th Paid P Pong £250 on account.

9th Received £1,200 from B Bjorg in full settlement of the amount due.

10th Bought a van for use in the business for £4,000 cash.

11th Paid a telephone bill for £150 in cash

Requirements

Show the accounting equation which results from the above transactions made

during Edward’s first two weeks of trading.

Bank/Cash

37

Capital

Purchases

P Pong (Payables)

38

Sales

B Bjorg (Receivables)

Rent

39

Drawings

Van

Telephone

40

Once the ledger accounts have been completed they will need to be balance. In

order to do this you must:

I. Rule off the ledger account

II. Add up the largest side

III. Put the largest side total on both sides

IV. Insert the required amount to ensure the smallest side balances (carried down

figure).

V. Bring the carried down figure forward on the opposite side (bought down figure).

NOW GO BACK AND BALANCE THE LEDGER ACCOUNTS OF EDWARD

41

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION THREE

42

1. F. Earls has the following assets and liabilities as of 30 November 2010: Accounts

payable 2,950, Equipment 10,500, Inventory 7,150, Motor Vehicle 5,290, Cash at

bank, 6280, Cash in hand 20 and Accounts receivable 5,790.

During the first week of December, Earls:

• Bought extra equipment on credit from P. Green for 1,500

• Bought extra inventory by cheque 670

• Accounts receivable paid to Erals 940 by cheque and 100 by cash

• Earls paid an account payable by cheque 950

• Earls puts an extra 500 cash into the business as capital.

Draw up a balance sheet after each of the above transactions have been

completed.

2. Write up the accounts for Charles to record the following transactions.

Dec 1 Started business with 1,000 in the bank

2 Bought a Motor Van for 1,000 paying by cheque

8 A loan from R. Kirk to the business of 2,000 cash is received

9 Paid 2,000 cash into the bank

10 Took 400 out of the bank for the cash till

11 Bought Motor Van on credit for 600, from P. Keenan

15 Paid P. Keenan 600 by cheque

16 Bought Fixtures by cheque for 500

20 Bought more fixtures on credit from A. Brown for 880

31 Bought more fixtures by cash 250.

43

3. Enter the following transactions in double entry.

Nov1 Credit sales, C. Flanagan £465, S. Morgan £300, F. Hutchinson £645,

A. Adair £987.

Nov2 Credit purchases, N. Ward £123, F. Wood, £465, S. Duffy £786, N.

Hynd £56.

Nov5 Credit sales, C. Flanagan £560, S. Ruddle £560.

Nov6 Credit purchases, F. Wood £79, N. Hynd £560.

Nov7 Goods returned to us by F. Hutchinson £45, S. Ruddle £60

Nov9 Cash paid to us (the business) by A. Adair £900, S. Ruddle £500.

Nov10 We (the business) returned goods to N. Ward £19, N. Hynd £60.

Nov12 We (the business) received cheques from F. Hutchinson £600, C.

Flanagan £456.

Nov 25 We (the business) sold goods on credit to C. Flanagan £50, S.

Morgan £45.

Nov26 We (the business) paid by cheque the following, N. Ward £100, F.

Wood £465, N. Hynd £56.

Nov28 We (the business) returned goods to N. Ward £4.

4. Balance off the personal accounts above and identify which are accounts

receivable and which are accounts payable.

44

5. Enter up the necessary acounts and balance off the accounts at the end of the

month.

20X7

Sept 1 Sales on credit as follows: C Latham £250, R Patch £455

Sept 4 Purchases made on credit for £190 from D Moynihan

Sept 11 Goods returned form R Patch worth £170

Sept 20 Credit sales of £680 made to E Bright

Sept 24 Purchases made on credit for £370 from C Peck

Sept 25 Cheque received from C Latham for £250

Sept 30 We return goods to Moynihan worth £150

45

6. You are required to enter up the necessary accounts based on the following

information. All accounts should be balanced off and a trial balance should be

extracted as at 31 October 20X8.

20X8

Oct 1 Started business with £5,000 deposited in bank

Oct 4 Purchased delivery van for £1,800 paying by cheque

Oct 5 Bought office equipment on credit from Eves Ltd for £800

Oct 8 Paid for advertising £54 cheque

Oct 11 Withdrew £300 cash from bank

Oct 14 Bought stock on credit from: S Gabriel £56 and S Phipps £76

Oct 16 Returned stock to Gabriel worth £10

Oct 19 Sold goods on credit to: S Suckling £113 and C Dimmock £89

Oct 21 Paid for stationery £23 cash

Oct 22 Withdrew £275 from bank for personal use

Oct 26 Goods retuned by Suckling worth £27

Oct 29 Sales made on credit to J Rudling for £96

Oct 30 Commission received by firm: £29 cash

46

47

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION FOUR

48

The Trial Balance

All the debit and credit balances extracted from the ledger accounts can then be

grouped together in a trial balance. This will check the accuracy of the entries made in

the ledger accounts.

EXAMPLE

The following are the balances on the accounts of Christine at 31 December 2010

£

Sales 47,140

Purchases 26,500

Trade receivables 7,640

Trade payables 4,320

General expenses 9,430

Loan 5,000

Fixtures & fittings 7,300

Motor vehicles 2,650

Drawings 7,500

Rent and rates 6,450

Electricity 1,560

Bank overdraft 2,570

Capital 10,000

Required

Prepare Christine’s trial balance as at 31st December 2010

49

DEBIT CREDIT

£ £

50

Some errors will be identified by extracting a trial balance:-

• Transposition error

• Unequal entries

• Extraction error

Some errors will not be identified by a trial balance:-

• Compensating error

• Error of omission

NOW COMPLETE THE TRIAL BALANCE FOR EDWARD

51

DEBIT CREDIT

£ £

52

Other movements in Inventories:

Dr Cr

Non current assets

Non current liabilities

Inventory

Receivables Payables

Bank Bank overdraft

Cash

Drawings Capital

Losses Profits

Purchases Sales

Expenses Income

Returns inwards Returns outwards

53

Example 2

Arathusa had the following transactions during July 2011.

1st Started a business with £10,000 cash.

2nd Purchased a display units for cash, £200.

3rd Paid rent for the premises for one month, £100.

4th Purchased goods on credit from Lion worth £1,000.

5th Returned goods to Lion to the value of £200.

6th Paid insurance for one month of £40.

7th Sold half of the goods on credit to Leopard for £400.

8th Took £60 cash for his own expenses.

9th Leopard returned half of the goods purchased.

10th Sold the remainder for the goods for cash of £420.

Required

Write up the relevant ledger accounts to record the above transactions then balance

the accounts.

54

Bank/Cash

DR CR

Capital

DR CR

Display Units

DR CR

55

Rent

DR CR

Purchases

DR CR

Lion (Payables)

DR CR

56

Purchase Returns

DR CR

Insurance

DR CR

Sales

DR CR

57

Leopard (Receivables)

DR CR

Drawings

DR CR

Sales Returns

DR CR

58

Different Types of Profit

Profit & Loss Account

£

Sales X

Cost of goods sold (X)

__

GROSS PROFIT X

Other Income X

Expenses (X) incurred during the day to day operations

__

NET PROFIT X

__

Other income – eg bank interest received, rent received, commission received

Expenses – eg telephone, motor expenses, electricity, rent, wages & salaries

59

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION SIX

60

Practice Question

Clooney commences business on 1 April 2011. The following transactions take place in

his first two weeks of trading.

1 April Invests £50,000 in to a business bank account

1 April Purchases £5,000 worth of goods on credit from Pitt

2 April Clooney returned £1,000 worth of goods to Pitt

2 April Sells half of the remaining inventory for £6,000 to Downey on credit

4 April He writes a cheque to pay for the goods he received from Pitt

5 April Pays his rent for April of £450 by cheque

6 April Downey returns half the goods he purchased to Clooney

7 April He sells the balance of his inventory for £6,000 on credit to Diggs

10 April Purchased goods on credit for £7,000 from Pitt

11 April Withdraws £500 for his personal expenses

14 April He purchases a delivery van for £7,000 cash

Required

Prepare the ledger accounts of Clooney for the first two weeks of trading and the trial

balance at 14th April.

What is Clooney’s gross profit & net profit for the first two weeks of trading?

61

Bank/Cash

DR CR

Capital

DR CR

62

Purchases

DR CR

Pitt (Payables)

DR CR

63

Purchase returns

DR CR

Sales

DR CR

64

Downey (Receivables)

DR CR

Rent

DR CR

Sales returns

DR CR

65

Diggs (Receivables)

DR CR

Drawings

DR CR

Van

DR CR

66

Clooney Trial Balance

Dr Cr

67

Profit & Loss Account

Sales

Less sales returns

______

Less cost of goods sold

Purchases

Less purchase returns

_____

Less closing inventory

_____

______

GROSS PROFIT

Expenses – Rent

______

NET PROFIT

W1 Closing inventory

Purchases

Returns

Sold

Sales Returns

Sold

Sales Returns

Sold

Purchases

68

Effect upon the Capital Account

The net profit generated will increase the amount the business owes to the owner

Looking at Clooney £

Opening capital of the business was

Now complete the balance sheet of Clooney from your trial balance. The net profit you

have calculated will be added to the capital section as below:

69

Clooney Balance Sheet

Non-current assets £ £

Motor van

Current assets

Inventory (same as in Gross Profit calc)

Receivables

-

Bank

Current liabilities

Payables

Net current assets

NET ASSETS

Capital

Profit for the period

Less Drawings

70

The owner/s will be very interested in the capital figure as it represents the amount of

money the business owes them. For this reason, the full details of movements in the

capital account are provided.

A business will have many credit suppliers and customers so the accounts will need to

be kept separately so balances due with and from each can be identified. These will

be called personal accounts.

Example - Nedge

Enter the following transactions in double entry, balance off the personal accounts,

and identify which are accounts receivable and accounts payable.

1 Jan Credit sales, K.Tyler £900, H Ford £600, L Aitchison £1,200, D Bird £1900.

2 Jan Credit purchases, B Ward £500, A Curtis £930, L Durnall £1,500, G Powell £110.

5 Jan Credit sales, K.Tyler £1,000, L Larkin £1,100.

6 Jan Credit purchases, A Curtis £150, G Powell £1,200.

7 Jan Goods returned to the business by L Aitchison £100, L Larkin £100

9 Jan Cash paid to the business by D Bird £1,500, L Larkin £900.

10 Jan The business returned goods to B Ward £50, G Powell £60.

12 Jan The business received cheques from L Aitchison £1,100, K.Tyler £900.

25 Jan The business sold goods on credit to K.Tyler £80, H Ford £70.

26 Jan The business paid by cheque the following, B Ward £200, A Curtis £900, G

Powell £110.

28 Jan The business returned goods to B Ward £10.

71

Bank

DR CR

Cash

DR CR

72

Sales

DR CR

Returns Inwards

DR CR

73

Purchases

DR CR

Returns outwards

DR CR

74

DR CR

DR CR

75

DR CR

DR CR

76

DR CR

DR CR

77

DR CR

DR CR

78

DR CR

79

Payables £ Receivables £

80

Other considerations

Carriage – when goods are delivered from suppliers or sent to customers, the cost of

delivering the goods is often an additional cost to goods purchased, or an additional

cost to the business for delivering the goods to the customer free of charge.

Carriage inwards – the cost incurred when goods are delivered by suppliers. This is

added to the cost of purchases in the calculation of gross profit.

Carriage outwards – the cost to the business to deliver goods to the customer. This

becomes a cost to the business if it is not recharged to the customer. It is deducted

from gross profit, like other costs, to calculate net profit.

81

Inventory and the second year of a business

Continuing with Edward from our first day. Here is his trial balance at the end of his first

two weeks of trading.

Edward Trial Balance

Dr Cr

Bank/cash 1,700

Capital 5,000

Purchases 1,000

P Pong (Payables) 250

Sales 1,950

B Bjorg (Receivables) -

Rent 250

Drawings 100

Van 4,000

Telephone 150

7,200 7,200

The accounting equation at the end of the two weeks was as follows:

£

Assets Van 4,000

Inventory 100

Receivables -

Cash (1850 – 150) 1,700

–––––

5,800

Liabilities Payables (250)

–––––

5,550

–––––

£

Capital 5,000

Profit (800 - 150) 650

–––––

5,650

Drawings (100)

–––––

5,550

–––––

82

The equation could also be expressed as follows:

Edward Balance Sheet

Non-current assets £ £

Motor van 4,000

Current assets

Inventory 100

Receivables -

Cash 1,700

–––––

1,800

Current liabilities

Payables 250

–––––

1,550

–––––

5,550

–––––

Capital 5,000

Profit for the period 650

–––––

5,650

Less Drawings 100

–––––

5,550

–––––

83

Lets now use these details as if it was the end of the accounting period. The closing

inventory of £100 is now the opening inventory for the next accounting period. This will

be adjusted in the calculation of cost of goods sold within the profit and loss account

as follows:

£

Sales X

Less sales returns (X)

______

X

Less cost of goods sold

Opening inventory 100

Purchases X

Less purchase returns (X)

_____

X

Less closing inventory (X)

_____

(X)

______

GROSS PROFIT X

84

Capital & Revenue Expenditure

Capital expenditure is incurred when a business spends money either to buy non-

current assets or add to the value of non-current assets

Revenue is spent on running the business on a day-to-day basis

Consider a delivery van:

Capital/Revenue Asset/Expense

Purchase price of the van

Motor insurance

Car tax

Adding a lift to the back of the van

Other examples:

£1,500 spent on machinery, of which;

£1000 relates to improvements

£500 relates to repairs

Rendering & painting the outside of a

new building

Three years later, painting the same

Building

85

Revenue expenditure is shown as a cost in the Trading, profit and loss account

Capital expenditure will result in an increase in non-current assets in the Balance Sheet

The difference is important as it affects the profit of the business and the assets of the

business which in turn impacts upon owners’ capital.

In the same way that purchasing a non-current asset is capital expenditure the

proceeds from the disposal of a non-current asset is a capital receipt and not sales

revenue.

86

87

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION SEVEN

88

Financial Statements

Profit & Loss Account for the year ended........

Sales

Less sales returns

Less cost of goods sold

Purchases

Less purchase returns

Less closing inventory

GROSS PROFIT

Other income

Expenses

Rent

Electricity

Telephone

Wages

Stationary

Cleaning

89

Balance Sheet

Non-current assets £ £

Buildings

Equipment

Motor vehicles

Current assets

Inventory (same as in Gross Profit calc)

Receivables

-

Bank

–-––––

Current liabilities

Overdraft

Payables

–––––-

Net current assets

––-–––

NET ASSETS

––-–––

Capital

Profit for the period

–––-––

Less Drawings

––-–––

––-–––

90

Practice Question

From the following trial balance of Bonnie, you are asked to draw up a profit and loss

account (income statement) for the year ended 31 March 2011 and a balance sheet

as at that date.

Dr Cr

£ £

Advertising 410

Bank 11,990

Capital as at 1 April 2010 153,700

Carriage inwards 460

Carriage outwards 390

Cash in hand 1,754

Drawings 23,080

Equipment 37,000

Insurance 1,500

Inventory as at 1 April 2010 8,660

Motor repairs 1,180

Premises 150,000

Purchases 199,990

Rates 8,700

Rent 6,520

Returns inwards 750

Returns outwards 1,120

Sales 336,000

Sundry expenses 656

Trade receivables 17,900

Trade payables 23,120

Vehicles 24,000

Wages 19,000

513,940 513,940

Inventory as at 31 March 2011 was valued at £23,710

91

Bonnie

Income statement for year ended 31 March 2011

£ £

Sales

Less Returns inwards

Net turnover

Less Cost of goods sold

Opening inventory

Add Purchases

Less Returns outwards

Add Carriage inwards

Less Closing inventory

Gross profit

Less Expenses

Wages

Insurance

Advertising

Motor repairs

92

Carriage outwards

Sundries

Rent

Rates

Net profit

93

Bonnie

Balance Sheet as at 31 March 2011

£ £

Non-current Assets

Premises

Equipment

Vehicles

Current Assets

Inventory

Trade receivables

Bank

Cash

Current Liabilities

Trade payables

Financed by:

Capital

Add Net profit

Less Drawings

94

Depreciation

Expenditure

Capital Revenue

Balance Sheet Profit & Loss

Assets

Buildings

Machinery

Costs

One off expenses

Electricity

Repairs

Including

“Improvement to an asset”

95

BSC BUSINESS STUDIES

BUSINESS ACCOUNTING

SESSION EIGHT

96

Materiality Concept

The Framework that we looked at in chapter 1 says;

“Information is material if its omission or misstatement could influence the economic

decisions of users.”

This means that a company will normally have a capital expenditure limit based on

materiality. Above this monetary limit the asset is recorded in the balance sheet as it is

considered to meet the above definition.

Below the limit the asset will be written off as a cost in the profit and loss account.

Non-current assets

Generally non-current assets will be owned by the business for more than one year.

They are carried in the balance sheet as capital expenditure but are used within the

business on a day to day basis to help generate income rather than resold. They are

initially recorded at their HISTORICAL COST.

As a result of their continued use, most non-current assets will wear out over time or use.

In accordance with the accruals or matching concept the cost of consuming these

assets need to be matched with the income they generate but based on the

accounting:

Asset is in the Income is in the

Balance Sheet Profit & Loss Account

This does not follow matching. To solve this problem we will use DEPRECIATION.

97

Depreciation

“Depreciation is the systematic allocation of the depreciable amount of an asset over it

useful life.”

Depreciable amount - The cost of an asset less its residual value.

Residual value - The estimated amount that an entity would currently obtain from

disposal of the asset, after deducting the estimated costs of disposal.

Useful life is;

- The period over which an asset is expected to be available for use by an entity;

or

- The number of production or similar units expected to be obtained from the

asset by the entity

Useful life is a matter of judgement.

Methods of depreciation

There are two main methods of calculating depreciation:

Straight line (based on time)

(Cost – residual value)

______________________ = constant depreciation charge

useful life of the asset

Eg If a delivery van was bought by a business for £22,000. The van has an expected life

within the business of four years, after which it could sell it for £2,000.

The cost of depreciation would be:

98

If the van was expected to be scrapped after the four years and had no residual value,

the cost of depreciation would be:

Remember we considered the difference between capital and revenue. Consider the

delivery van as it gets older – would you expect revenue expenditure to increase or

decrease?

Why?

Practice Question

Violet purchased a pressing machine for £23,000. Violet estimated that the machine

will last 5 years and will have a residual value of £3,000. How much depreciation will be

charged each year?

99

Example – Choice of policy

Pete purchased a non-current asset on 1st July for £50,000. The asset has an expected

useful life of 5 years and a residual value of £5,000. Pete has a year end of 31

December.

If the business is attempting to ‘match’ costs with the revenues (sales) from the use of

the non-current asset then it may be more appropriate to use a different method of

calculating depreciation.

100

Reducing balance

NBV x selected % = falling depreciation charge

(NBV is cost less accumulated depreciation)

Using the same delivery van costing £22,000 but applying a reducing balance rate of

20%. The depreciation cost for the first three years would be;

Over time the depreciation charge reduces but as the asset ages the repairs and

maintenance increases.

101

It could be argued that the reducing balance method is better at matching the total

costs (capital and revenue) of a non-current asset with the revenues (sales) generated

from its use.

Accounting Entries:

Once you have calculated the depreciation charge it will be entered into the

accounts via a journal.

The journal for depreciation is:

Dr Depreciation expense (Profit and loss account)

Cr Accumulated Depreciation (Balance Sheet)

Choice of method

The purpose of depreciation is to spread or allocate the total cost of a non-current

asset over the periods in which it is to be used.

The method chosen should be that which allocates cost to each period in accordance

with the proportion of the overall economic benefit from using the asset over its useful

life (the total period over which it is going to be used).

The choice is subjective but is supported by accounting policies and concepts:

Accruals/Matching

Going concern

Both of which we considered earlier

102

Increases in value of non-current assets

All non-current assets are initially recorded at their HISTORICAL COST ie what you paid

for them.

According to IAS 16 it is possible to carry your asset at its market value rather than

historical cost. This adjustment is referred to as a REVALUATION.

Dr Non-current asset

Cr Revaluation reserve

The new increased value of the asset is then depreciated over its remaining useful

economic life

Example

Willow buys a machine on 1 January 2002 for £500,000. The machine has an estimated

useful economic life of ten years with a residual value of £20,000. A straight line method

of depreciation was adopted.

On 1 January 2007 willow decides to revalue its machine to £750,000 in line with IAS 16.

The useful economic life remains unchanged.

Required:

Show how the revaluation would be accounted for and the subsequent depreciation

charge following the revaluation.

103

Land and Buildings

Due to its nature land does not normally require depreciation. Only land subject to

extraction eg coal mines or oil fields would be depreciated.

Buildings however must be depreciated as although the value of property generally

increases over time a building suffers wear and tear also.

IT IS IMPORTANT TO REMEMBER THAT DEPRECIATION IS A METHOD OF ALLOCATING THE

COST OF A NON-CURRENT ASSET TO THE PROFIT AND LOSS ACCOUNT IT IS NOT A

VALUATION METHOD.

Net book value is merely the difference between the cost or valuation of the asset and

the accumulated depreciation to date. It does not represent the market value of the

asset.

104

Investment Properties

These types of properties have an accounting standard of their own SSAP 19.

There are defined as

Investment property

An interest in land and/ or buildings:

• In respect of which construction work and development have been completed

and

• Which is held for its investment potential, any rental income being negotiated at

arm’s length

Investment properties should NOT be depreciated instead they are included in the

balance sheet at market value and a revaluation reserve created.

Note: IAS 40 the international standard for investment properties states that the gains

and losses arising on the property are included in the profit and loss account.

105

IAS 8 Accounting policies, Changes in accounting estimates and errors

Accounting policies

The specific principles, bases, conventions, rules and practices applied by an entity in

preparing and presenting the financial statements.

SELECTING ACCOUNTING POLICIES

In selecting accounting policies an entity must firstly consider the requirements of the

applicable accounting standards.

In all other situations policies should be selected so as to result in information that is

relevant and reliable in line with the framework.

Relevant – to the economic decision making needs of users; and

Reliable

• Faithful representation

• Reflect the substance

• Neutral, free from bias

• Prudent

• Complete

Consistency – when a business chooses to treat certain transactions in a particular way

it should continue to treat similar transactions in the same way.

Disclosure

As each business will adopt its own set of accounting policies its is important for

comparability that each business discloses its chosen policies. That way any differences

in policies can be taken into account when comparing different businesses.

This will include the chosen policy for depreciation – the useful life for the straight line or

the percentage used for reducing balance method.

106

Changing accounting policies

An accounting policy may be changed if and only if the new policy will give a more fair

representation of the transactions and balances of the entity. We discussed the idea of

FAIR PRESENTATION (TRUE & FAIR VIEW) in chapter 1. A change in accounting policy

should be to meet this concept and not to improve the figures reported.

Remember – accounting information should be free from bias.

107

QUESTIONS TO BE ATTEMPTED IN CLASS

1. Which of the following is not a reason for providing for depreciation of non-current

assets?

A Wear and tear of assets

B Technical obsolescence

C Assets may increase in value

D Depletion

2. An asset was purchased on 1.1.20X3 for £5,500 and is to be depreciated at 20%

reducing balance. What would be the net book value of the asset as at 31.12.20X5?

A £3,300

B £2,200

C £3,520

D £2,816

3. Keeping the same depreciation policy even if it may not give a realistic asset value

at the year end is an example of:

A Prudence

B Accruals

C Going concern

D Consistency

4. Equipment was purchased on 1.1.20X6 for £25,000 and is to be depreciated at 30%

reducing balance. What would be the net book value of the asset as at 31.12.20X7?

A £12,250.

B £10,000.

C £5,250.

D £17,500.

108

5. The accruals concept states that:

a) Transactions should be recorded at historical cost

b) A company can not change its accounting policy

c) A business should be consistent in how it treats accounting transactions both within

an accounting period, and from one period to the next

d) Revenues and costs for an accounting period should be matched in order to

calculate the profit for the period.

6. The buildings from which the business trades, should not be depreciated because:

a) They increase in value with the passage of time

b) IAS 40 (Investment property) states they may not be depreciated

c) The accruals concept indicates that they are not subject to depreciation

d) None of the above.

7. Depreciation is:

a) Transferred to the Depreciation Account

b) The salvage value of a non-current asset

c) The part of the cost of anon-current asset consumed during its period of use by the

business

d) The amount of money spent in replacing assets.

109

R Grey is in business as a wholesale supplier of motor equipment. The following is his trial

balance as at 31 March 2011.

DR CR

£ £

Capital (at 1 April 2010) 9,000

Accounts payable 10,000

Bank 400

Accounts receivable 16,000

Drawings 11,000

Insurance 500

Wages 12,600

Opening inventory 5,000

Purchases 62,000

Rent 1,500

Sales 100,000

Motor vehicle 10,000

119,000 119,000

You are provided with the following additional information.

1. The value of closing inventory at 31 March 2011 was £6,000.

2. Depreciation of £6,000 is to be charged this year for the motor vehicle.

3. Goods taken for personal use during the year was estimated to be worth £1,000.

Required:

Prepare R Grey’s income statement for the year to 31 March 2011 and a Balance Sheet

as at that date.

110

Income statement for the year ended 31 March 2011

111

Balance Sheet as at 31 March 2011

112

Accounting Ratios and Analysing Accounts

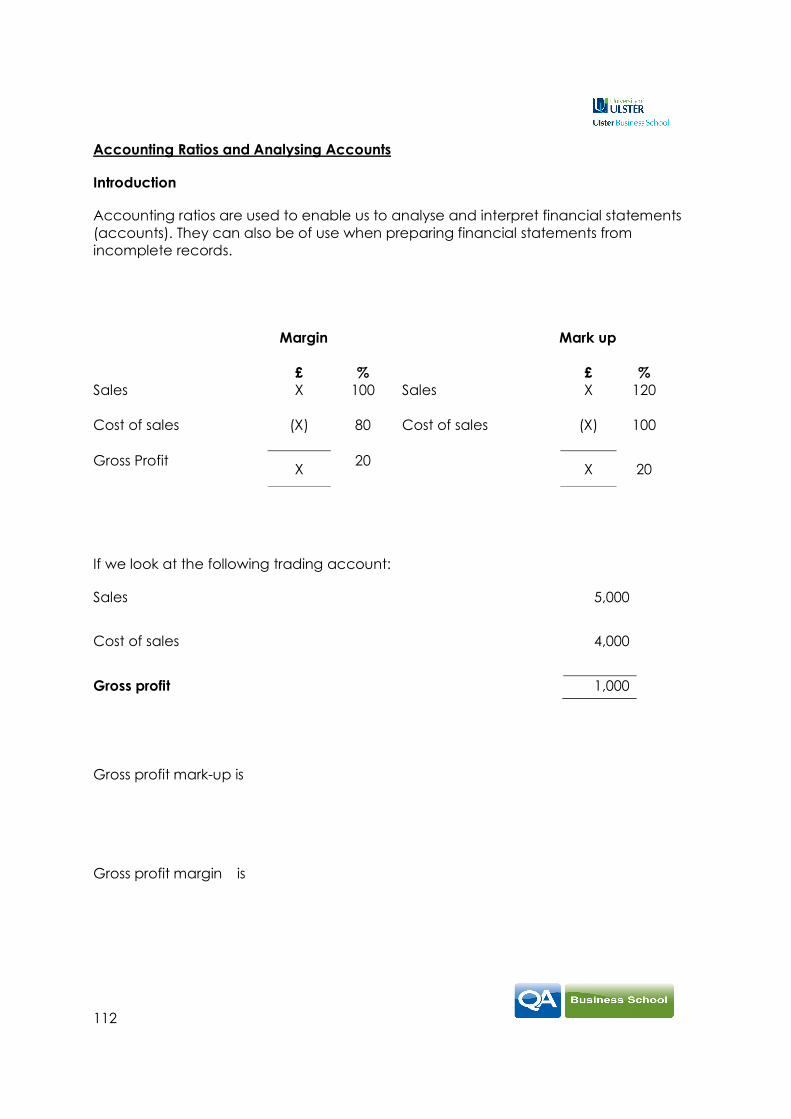

Introduction

Accounting ratios are used to enable us to analyse and interpret financial statements

(accounts). They can also be of use when preparing financial statements from

incomplete records.

Margin Mark up

£ % £ %

Sales X 100 Sales X 120

Cost of sales (X) 80 Cost of sales (X) 100

Gross Profit X

20 X 20

If we look at the following trading account:

Sales 5,000

Cost of sales 4,000

Gross profit 1,000

Gross profit mark-up is

Gross profit margin is

113

Example

Margin 25% Sales £1,000

Required:

What is the gross profit and cost of sales?

£ %

Sales

Cost of sales

Gross profit

Example

Mark-up 25% Cost of sales £600

Required:

What is gross profit and sales?

£ %

Sales

114

Cost of sales

Gross profit

Example

Mark-up 10%

Sales £6,600

Opening inventory £300

Closing inventory £500

Required:

Complete a trading account from the above information.

£ %

Sales

Cost of sales

Opening inventory

Purchases (Balancing Figure)

Closing inventory

Gross profit

115

Example

Margin 5%

Purchases £2,840

Opening inventory £800

Closing inventory £600

Required:

Complete a trading account from the above information.

£ %

Sales

Cost of sales

Opening inventory

Purchases

Closing inventory

Gross profit

116

Calculating missing figures

Using the information that you have and the cost structure it is possible to calculate

missing figures in the trading account eg if inventory is lost or damaged or if

sale/purchase invoices go missing.

Example – lost inventory

Margin 20%

Sales £100,000

Opening inventory £1,000

Closing inventory (after fire) £3,000

Purchases £82,000

Required:

Complete a trading account from the above information.

Sales

£ £ %

Cost of sales

Opening inventory

Purchases

Closing inventory

Inventory lost in fire (balancing figure)

Gross profit

117

Example – purchases

Margin 25%

Sales £150,000

Opening inventory £10,000

Closing inventory £20,000

Purchases ?

Required:

Complete a trading account from the above information.

Sales

£ £ %

Cost of sales

Opening inventory

Purchases - (balancing figure)

Closing inventory

Gross profit

118

Example – sales

Mark-up 20%

Sales ?

Opening inventory £15,000

Closing inventory £30,000

Purchases £120,000

Required:

Complete a trading account from the above information.

Sales – (balancing figure)

£ £ %

Cost of sales

Opening inventory

Purchases

Closing inventory

Gross profit

119

Gross Profit Margin

Gross Profit

_______________ x 100

Sales Revenue

The gross profit margin represents the amount of gross profit generated for every £100 of

sales revenue.

It is referred as an accounting ratio and is used as a test of profitability and the pricing

policy of a business.

Consider the following:

Trading, profit and loss account for the year ended 31 December....

2009 2010

£ £

Sales

7,000 8,000

Cost of sales

(5,600) (7,000)

Gross profit

1,400

1,000

Calculate the gross profit margin for each year

2009 2010

120

Now consider the information you have:

Increased/Fallen

What has happened to sales?

What has happened to cost of sales?

Gross profit margin has therefore

Can you think of any reasons for this?

• Cost of goods sold have increased without an increase in selling price

Why would you not increase selling price?

• Perhaps goods have been wasted or stolen resulting in higher cost but not

increased income

• There may have been a change in the types of goods sold what we call the

SALES MIX

• Perhaps the sales price has been reduced without a drop in cost of the goods

Why would this be done?

![[Morten Balling, Frank Lierman, Andy Mullineux]_Financial Markets in org](https://img.dokumen.tips/doc/110x75/543d32d6afaf9fb40a8b45c9/morten-balling-frank-lierman-andy-mullineuxfinancial-markets-in-org.jpg)