Embed Size (px)

Citation preview

A Question of EthicsPresented By:Kim Duong Aaron LamBen Lehman

Enron: What Happened and What we Can Learn From It•Likely the largest case of financial

misrepresentation in recent history•Provided high income and equity on

statements from 1997-2000, but in 2001 restated as lower income amounts▫544 million reduction in net income▫1.2 billion reduction in equity

•Filed for bankruptcy on December 2, 2001

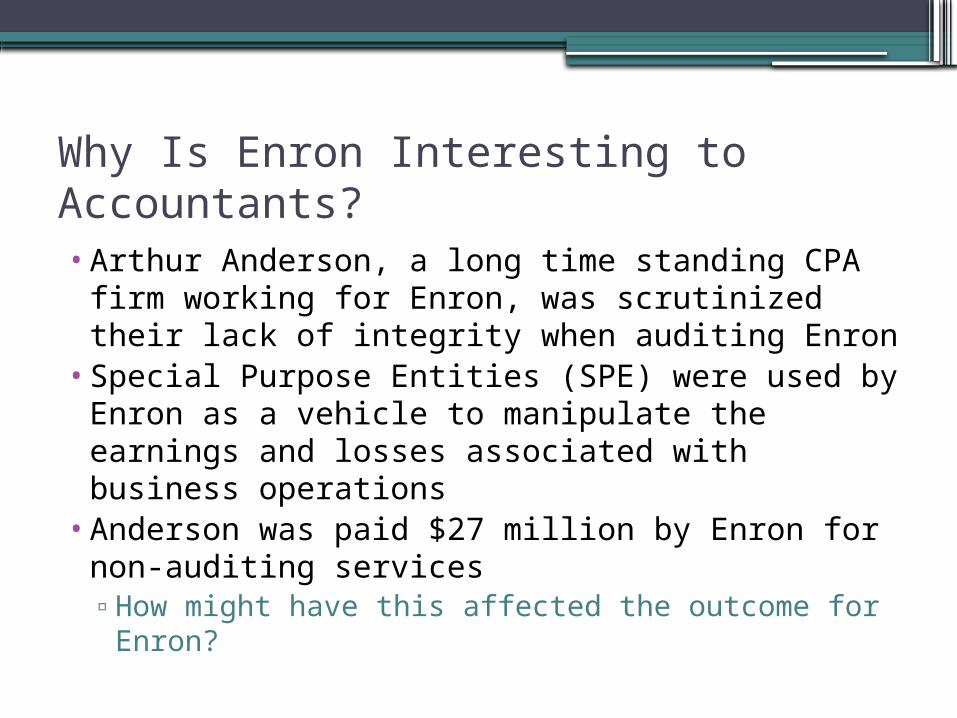

Why Is Enron Interesting to Accountants?•Arthur Anderson, a long time standing CPA

firm working for Enron, was scrutinized their lack of integrity when auditing Enron

•Special Purpose Entities (SPE) were used by Enron as a vehicle to manipulate the earnings and losses associated with business operations

•Anderson was paid $27 million by Enron for non-auditing services▫How might have this affected the outcome for

Enron?

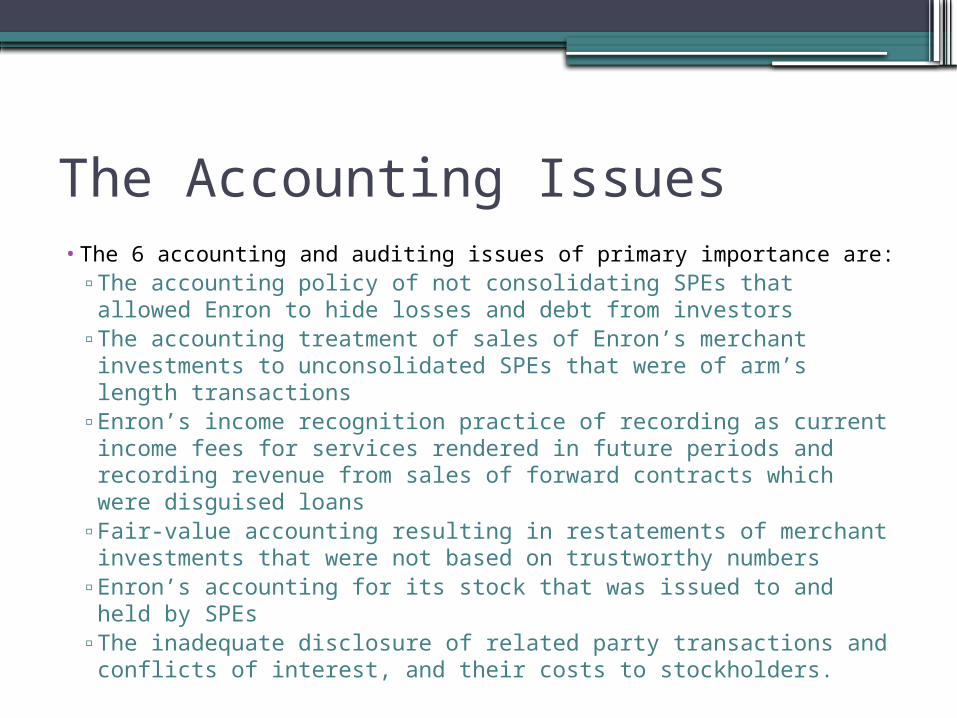

The Accounting Issues• The 6 accounting and auditing issues of primary importance are:

▫ The accounting policy of not consolidating SPEs that allowed Enron to hide losses and debt from investors

▫ The accounting treatment of sales of Enron’s merchant investments to unconsolidated SPEs that were of arm’s length transactions

▫ Enron’s income recognition practice of recording as current income fees for services rendered in future periods and recording revenue from sales of forward contracts which were disguised loans

▫ Fair-value accounting resulting in restatements of merchant investments that were not based on trustworthy numbers

▫ Enron’s accounting for its stock that was issued to and held by SPEs

▫ The inadequate disclosure of related party transactions and conflicts of interest, and their costs to stockholders.

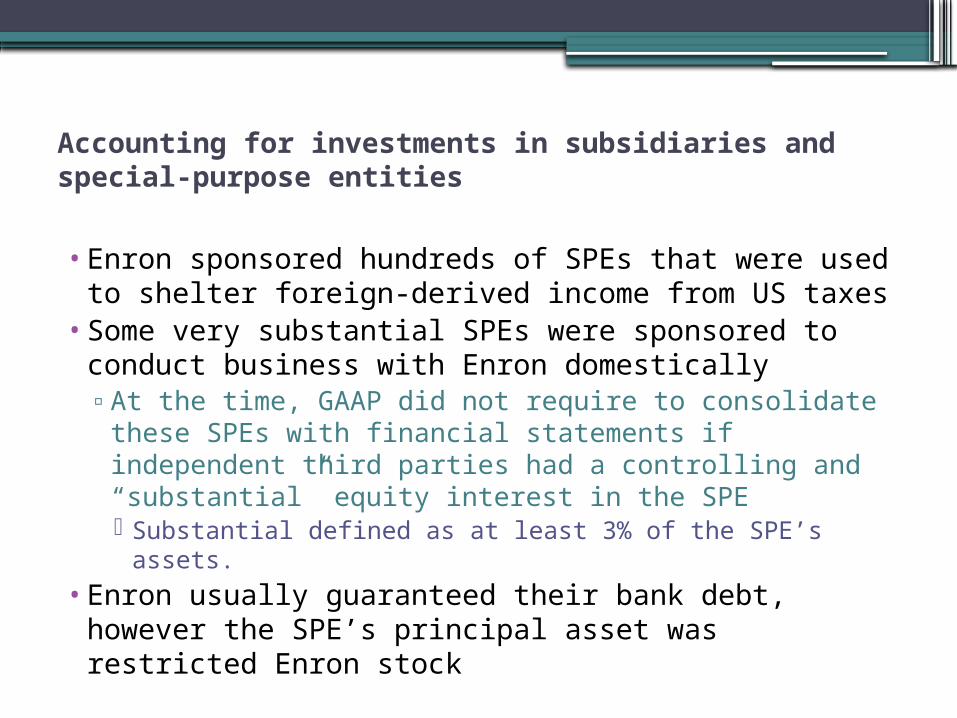

Accounting for investments in subsidiaries and special-purpose entities

• Enron sponsored hundreds of SPEs that were used to shelter foreign-derived income from US taxes

• Some very substantial SPEs were sponsored to conduct business with Enron domestically▫At the time, GAAP did not require to consolidate these

SPEs with financial statements if independent third parties had a controlling and “substantial” equity interest in the SPE Substantial defined as at least 3% of the SPE’s assets.

• Enron usually guaranteed their bank debt, however the SPE’s principal asset was restricted Enron stock

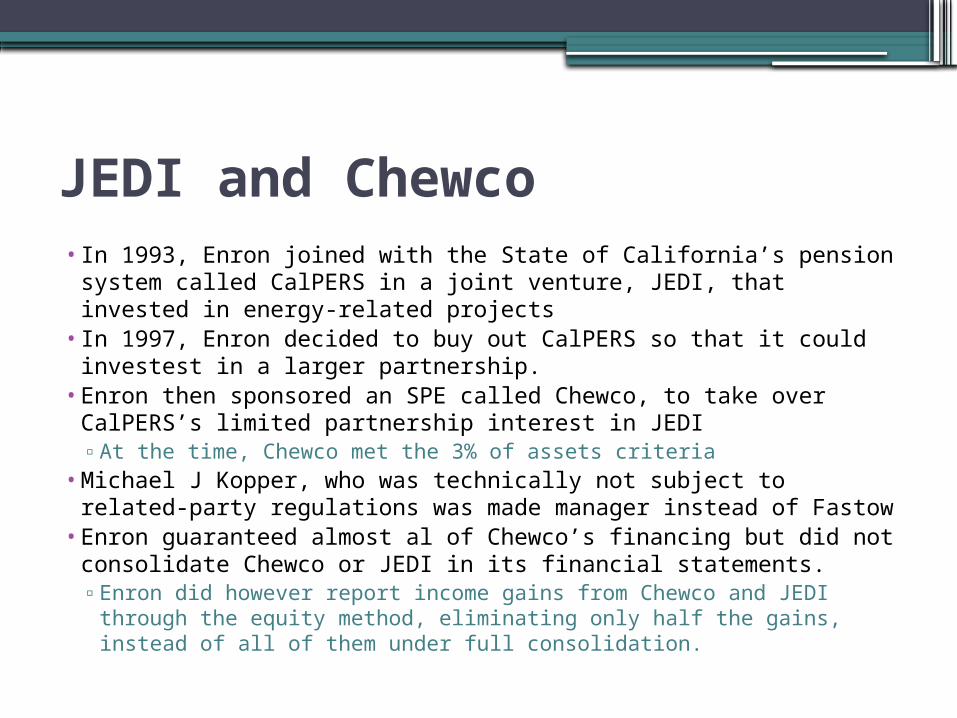

JEDI and Chewco• In 1993, Enron joined with the State of California’s pension

system called CalPERS in a joint venture, JEDI, that invested in energy-related projects

• In 1997, Enron decided to buy out CalPERS so that it could investest in a larger partnership.

• Enron then sponsored an SPE called Chewco, to take over CalPERS’s limited partnership interest in JEDI▫ At the time, Chewco met the 3% of assets criteria

• Michael J Kopper, who was technically not subject to related-party regulations was made manager instead of Fastow

• Enron guaranteed almost al of Chewco’s financing but did not consolidate Chewco or JEDI in its financial statements. ▫ Enron did however report income gains from Chewco and JEDI

through the equity method, eliminating only half the gains, instead of all of them under full consolidation.

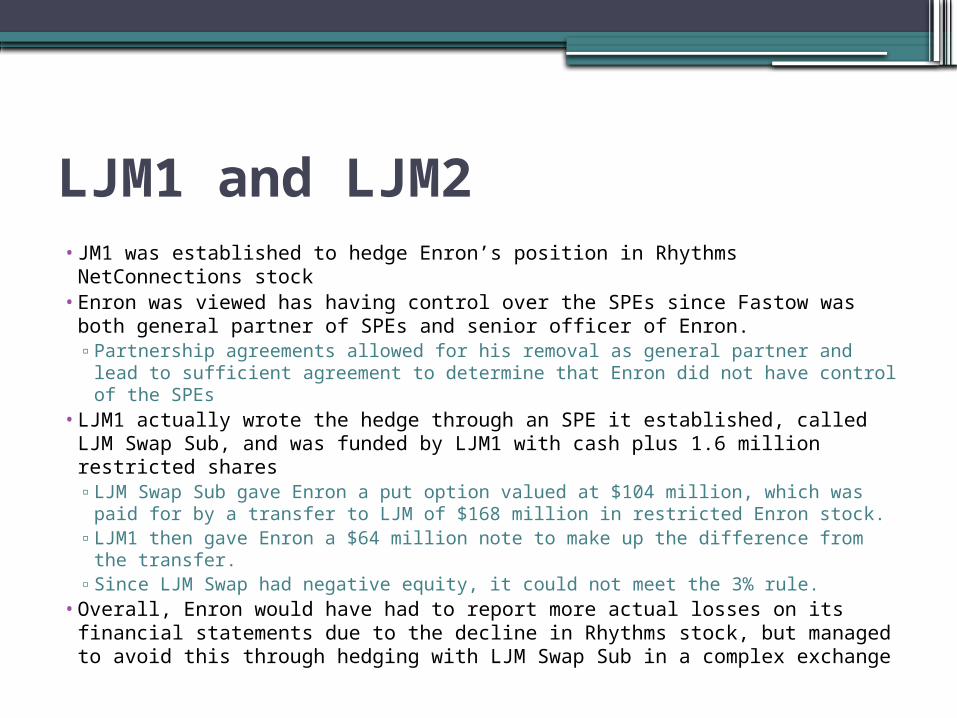

LJM1 and LJM2• JM1 was established to hedge Enron’s position in Rhythms

NetConnections stock• Enron was viewed has having control over the SPEs since Fastow was

both general partner of SPEs and senior officer of Enron. ▫ Partnership agreements allowed for his removal as general partner and lead

to sufficient agreement to determine that Enron did not have control of the SPEs

• LJM1 actually wrote the hedge through an SPE it established, called LJM Swap Sub, and was funded by LJM1 with cash plus 1.6 million restricted shares ▫ LJM Swap Sub gave Enron a put option valued at $104 million, which was

paid for by a transfer to LJM of $168 million in restricted Enron stock.▫ LJM1 then gave Enron a $64 million note to make up the difference from the

transfer. ▫ Since LJM Swap had negative equity, it could not meet the 3% rule.

• Overall, Enron would have had to report more actual losses on its financial statements due to the decline in Rhythms stock, but managed to avoid this through hedging with LJM Swap Sub in a complex exchange

Raptors (LJM2)• In 2000, Enron sponsored four SPEs called Raptor I to IV who sponsored other SPEs

that had the effect of keeping losses on its merchant investment portfolio from appearing on its financial statements.

• These SPEs sold Enron put options on several of its investments that allowed Enron to avoid showing losses when they declined in value, because these losses were offset by the put-option obligations of the SPEs.▫ If the investments decline in value, Enron had provided almost all the funds for the

SPEs to pay Enron back.▫ This lead to Enron’s shareholders absorbing all the losses and to Enron being able to

avoid showing these losses on their financial statements.• Raptor I created Talon, who was contractually obligated to pay LJM2 a fee for a six-

month put-option on Enron stock paid by Enron to Talon, and Enron was required to purchase LJM2’s interest in Talon.

• As the market prices of the merchant investments and Enron fell, Enron gave Talon a “costless collar” that obligated Enron to pay Talon for losses on Enron stock so that Talon would be able to meet its obligations on the derivatives owed to Enron

• If Enron’s stock price fell, that loss could not be covered▫ If it increased sufficiently to cover Talon’s obligation, the loss on its merchant

investments would be hidden, but the shareholders would have to pay through stock issued at less than its market price.

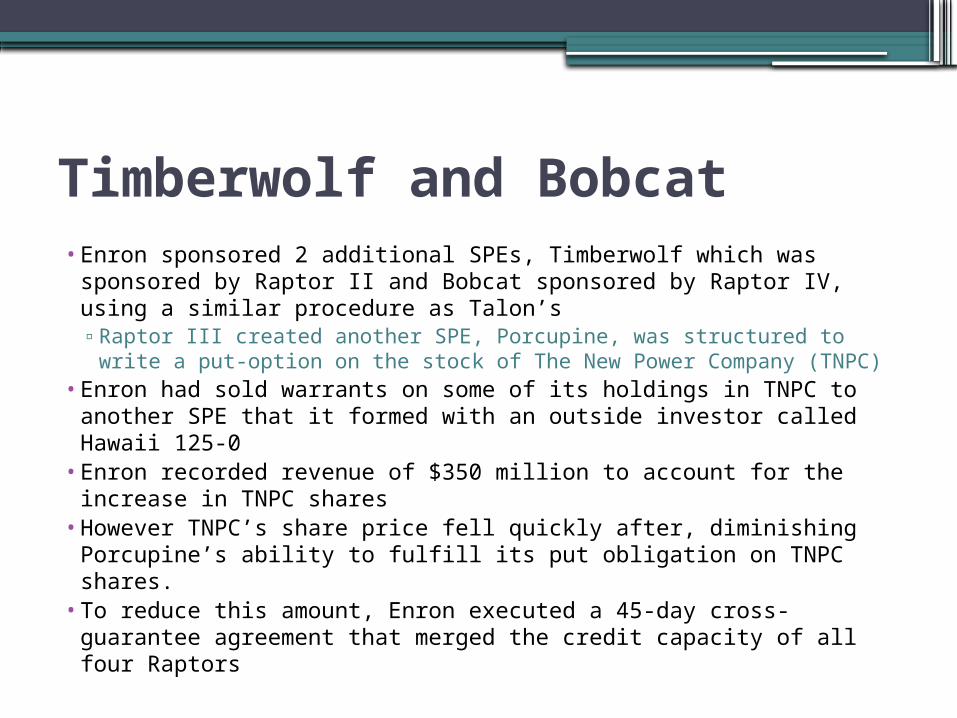

Timberwolf and Bobcat• Enron sponsored 2 additional SPEs, Timberwolf which was

sponsored by Raptor II and Bobcat sponsored by Raptor IV, using a similar procedure as Talon’s▫ Raptor III created another SPE, Porcupine, was structured to write

a put-option on the stock of The New Power Company (TNPC)• Enron had sold warrants on some of its holdings in TNPC to

another SPE that it formed with an outside investor called Hawaii 125-0

• Enron recorded revenue of $350 million to account for the increase in TNPC shares

• However TNPC’s share price fell quickly after, diminishing Porcupine’s ability to fulfill its put obligation on TNPC shares.

• To reduce this amount, Enron executed a 45-day cross-guarantee agreement that merged the credit capacity of all four Raptors

Subsequent actions and accounting changes as Enron’s stock prices declined

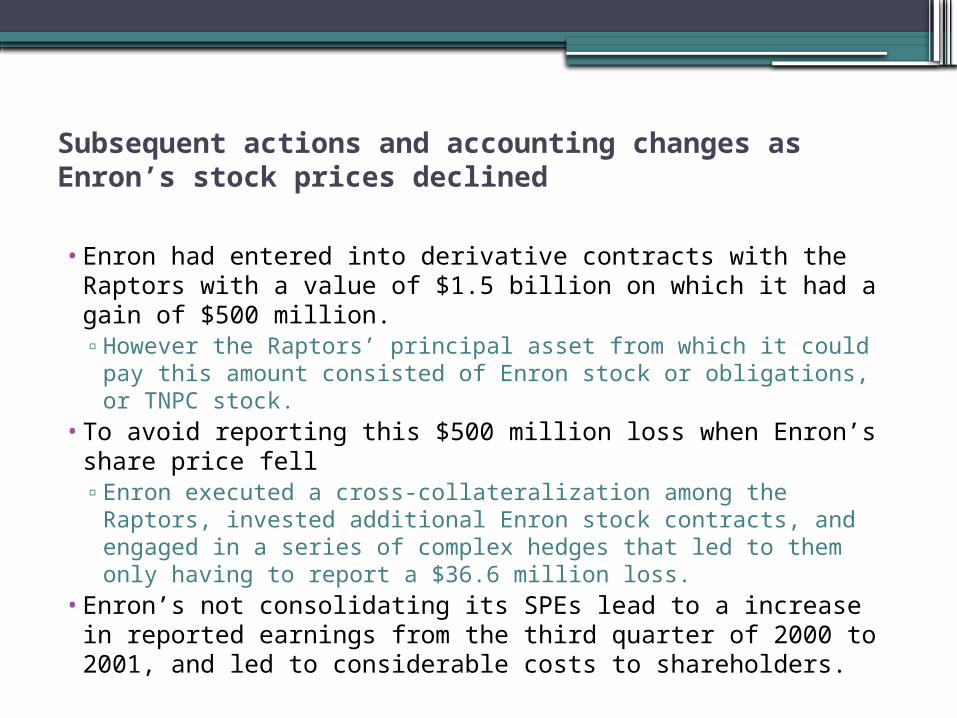

• Enron had entered into derivative contracts with the Raptors with a value of $1.5 billion on which it had a gain of $500 million. ▫ However the Raptors’ principal asset from which it could pay

this amount consisted of Enron stock or obligations, or TNPC stock.

• To avoid reporting this $500 million loss when Enron’s share price fell▫ Enron executed a cross-collateralization among the Raptors,

invested additional Enron stock contracts, and engaged in a series of complex hedges that led to them only having to report a $36.6 million loss.

• Enron’s not consolidating its SPEs lead to a increase in reported earnings from the third quarter of 2000 to 2001, and led to considerable costs to shareholders.

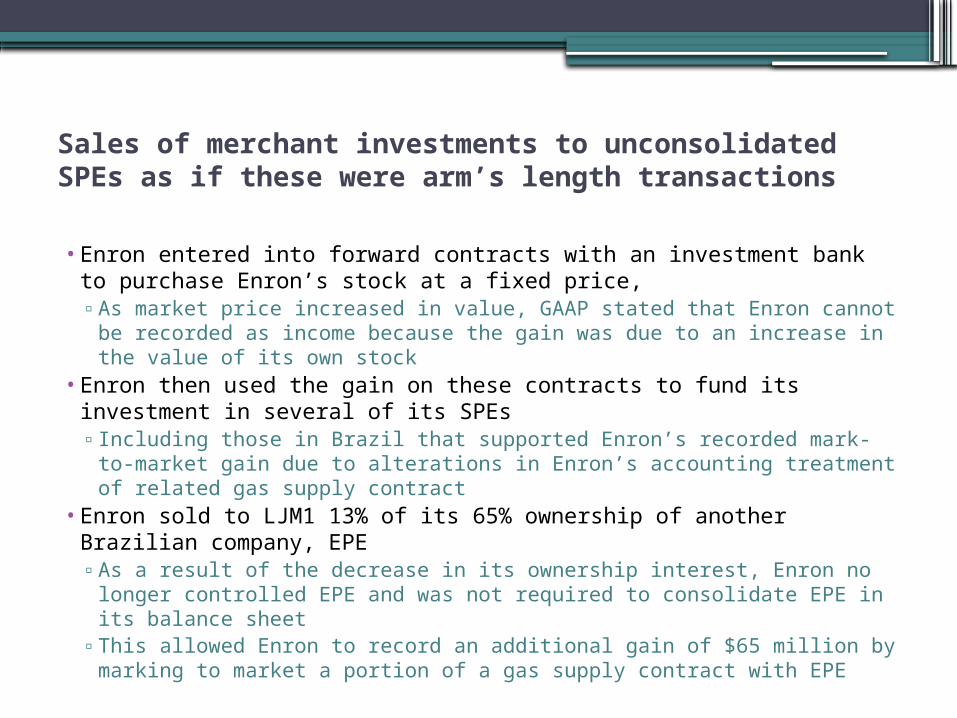

Sales of merchant investments to unconsolidated SPEs as if these were arm’s length transactions

• Enron entered into forward contracts with an investment bank to purchase Enron’s stock at a fixed price,▫ As market price increased in value, GAAP stated that Enron cannot be

recorded as income because the gain was due to an increase in the value of its own stock

• Enron then used the gain on these contracts to fund its investment in several of its SPEs▫ Including those in Brazil that supported Enron’s recorded mark-to-

market gain due to alterations in Enron’s accounting treatment of related gas supply contract

• Enron sold to LJM1 13% of its 65% ownership of another Brazilian company, EPE▫ As a result of the decrease in its ownership interest, Enron no longer

controlled EPE and was not required to consolidate EPE in its balance sheet

▫ This allowed Enron to record an additional gain of $65 million by marking to market a portion of a gas supply contract with EPE

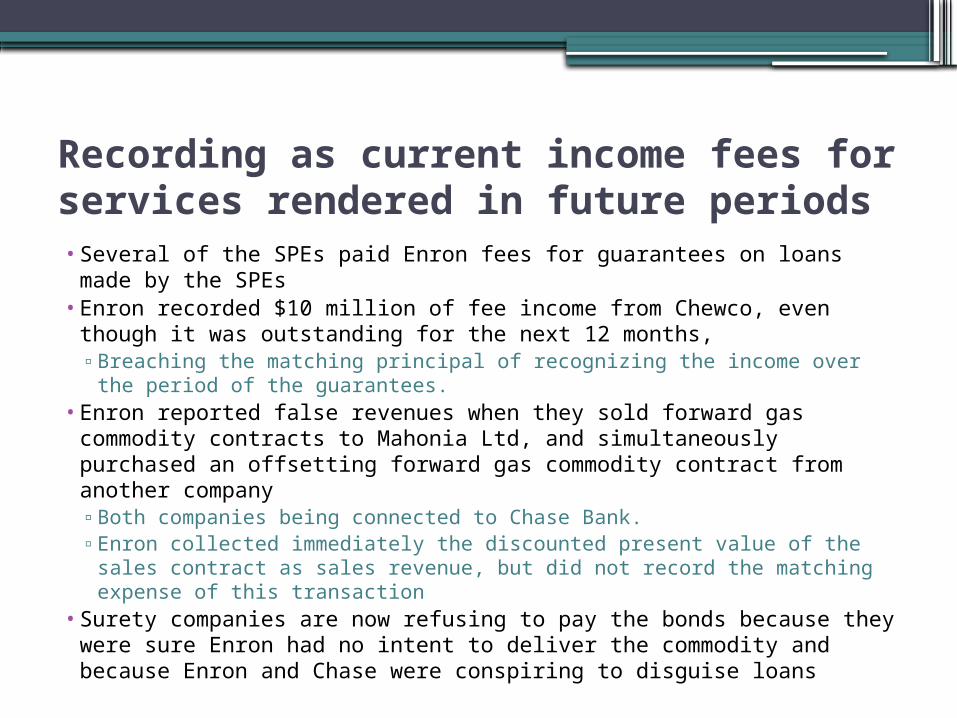

Recording as current income fees for services rendered in future periods• Several of the SPEs paid Enron fees for guarantees on loans made by

the SPEs• Enron recorded $10 million of fee income from Chewco, even though

it was outstanding for the next 12 months, ▫ Breaching the matching principal of recognizing the income over the

period of the guarantees. • Enron reported false revenues when they sold forward gas

commodity contracts to Mahonia Ltd, and simultaneously purchased an offsetting forward gas commodity contract from another company ▫ Both companies being connected to Chase Bank. ▫ Enron collected immediately the discounted present value of the sales

contract as sales revenue, but did not record the matching expense of this transaction

• Surety companies are now refusing to pay the bonds because they were sure Enron had no intent to deliver the commodity and because Enron and Chase were conspiring to disguise loans

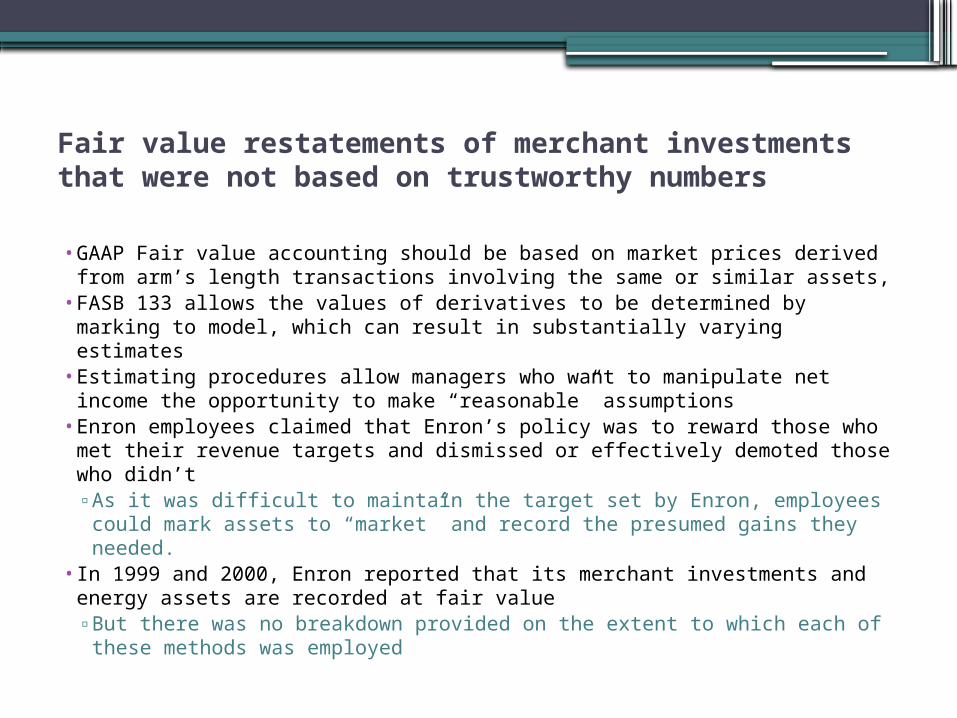

Fair value restatements of merchant investments that were not based on trustworthy numbers

• GAAP Fair value accounting should be based on market prices derived from arm’s length transactions involving the same or similar assets,

• FASB 133 allows the values of derivatives to be determined by marking to model, which can result in substantially varying estimates

• Estimating procedures allow managers who want to manipulate net income the opportunity to make “reasonable” assumptions

• Enron employees claimed that Enron’s policy was to reward those who met their revenue targets and dismissed or effectively demoted those who didn’t▫ As it was difficult to maintain the target set by Enron, employees

could mark assets to “market” and record the presumed gains they needed.

• In 1999 and 2000, Enron reported that its merchant investments and energy assets are recorded at fair value▫ But there was no breakdown provided on the extent to which each

of these methods was employed

Broadband and blockbuster inc partnership, braveheart• In 2000, Jeffrey Skilling told stock market analysts

that Enron was about to create a market for trading space on the high-speed fiber optic networks that form the backbone for internet traffic▫Revenue was generated by a sale of excess unused

(dark) fiber-optic connections to LJM2, the SPE owned by Andy Fastow since LJM2’s principal asset was Enron stock

• Another broadband venture was Project Braveheart▫Enron assigned the partnership a value of $124

million based on its projections of the revenue and earnings potential although the venture was incorporated in the same year

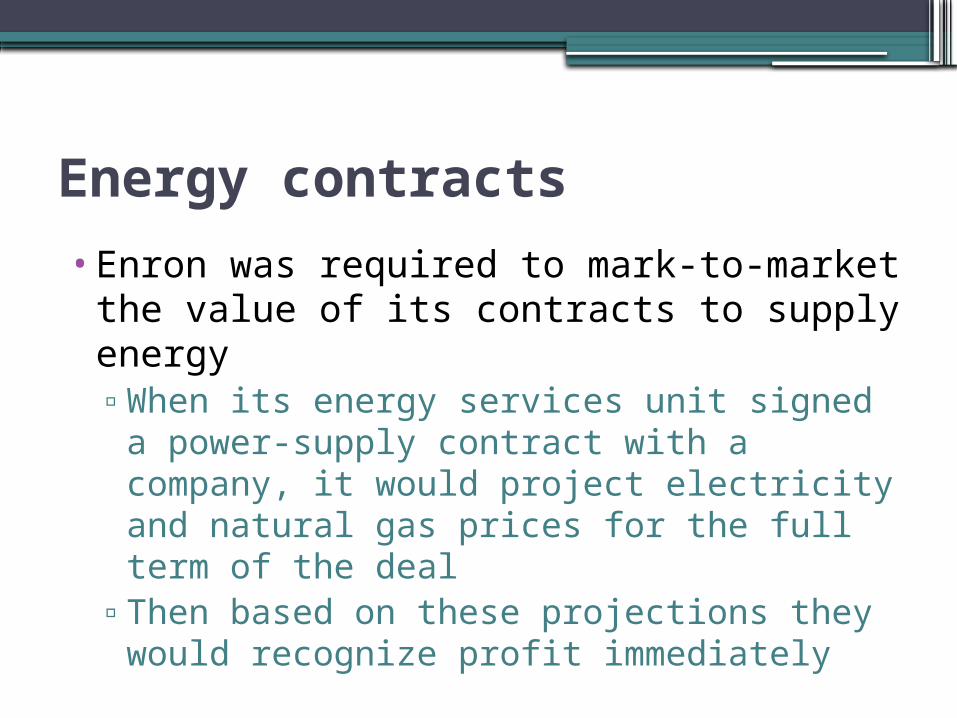

Energy contracts

•Enron was required to mark-to-market the value of its contracts to supply energy▫When its energy services unit signed a

power-supply contract with a company, it would project electricity and natural gas prices for the full term of the deal

▫Then based on these projections they would recognize profit immediately

Enron’s merchant investments

•Enron’s merchant investments portfolio was apparently organized as an investment fund▫Under GAAP they must revalue such assets

at fair value▫Since reliable market prices were not

available, Enron had the opportunity of assigning values that permitted it to record earned revenue

Accounting for Enron stock issued to and held by SPEs• JEDI, owned 12 million shares of Enron

stock, and recorded at market and recognized income from the amount of increased market value▫Though GAAP does not permit a corporation

to record as income increases in the value of its own stock.

▫Enron accounted for its investment in JEDI with the equity method, and recorded the appreciation in market value on its own financial statements

Disclosure of conflicts of interest and its costs to stockholders• SEC Regulation requires disclosure of transactions

exceeding $60,000 in which an executive officer of a corporation has a material interest▫ Disclosure is also required for material related-party

transactions. Enron’s transactions with the SPEs LJM1 and LJM2 however do not appear to have been made at arm’s length.

• Andrew Fastow and employees who reported to him were on both sides of the transactions and benefited personally from Enron’s dealings

• An example of this would be in 1999 when Enron sold several investments to LJM1 and LJM2, SPEs of which Fastow was general partner, at what appears to be inflated profits

What Happened Because of Enron?

•Financial Literacy of all individuals working within the auditing committee became required, with one individual being a financial expert being required▫However, Enron’s committee seemed to

have exceeded this requirement already▫Given this fact, why do you think the

dishonest behaviour still occurred?

What Happened Because of Enron?

•SPE creation and maintenance became a much more important topic to accountants▫Enron’s negligence in disclosing their

investments and connection with SPEs is the reason for this

▫Vinson and Elkins were Enron’s outside attorneys at the time and were held liable for the errors

What Did Enron Do?

•Vinson and Elkins were criticized for their negligence on assessing the SPEs▫Although the Enron vice president Sherron

Watkins took action to address the issues, they were still considered: Not worthy of “further widespread

investigation by independent council or auditors”

But also “a serious risk of adverse publicity and litigation”

What Did Enron Do?

•Class Question: Which of theories can be applied to explain the actions and response of the parties involved in the SPE matter? How can they be applied?

Response of the SEC•The SEC has the power to discipline CPAs

who do not demonstrate a proper care for auditing activities through disallowance of auditing capabilities▫This can be exercised in the case of either

dishonest accounting, or in the case of negligent acts on behalf of the accountant

▫Despite this, the SEC rarely attempts to suspend independent auditors – what kind of economic consequences may occur to do this?

Lessons From Enron

•GAAP is often interpreted and followed by the letter, but in doing so, companies can bypass the basic objectives of the system▫GAAP should remain constantly changing

to match an ever-changing world How might an ever changing GAAP be

relevant to the fundamental dilemma of Financial Accounting Theory?

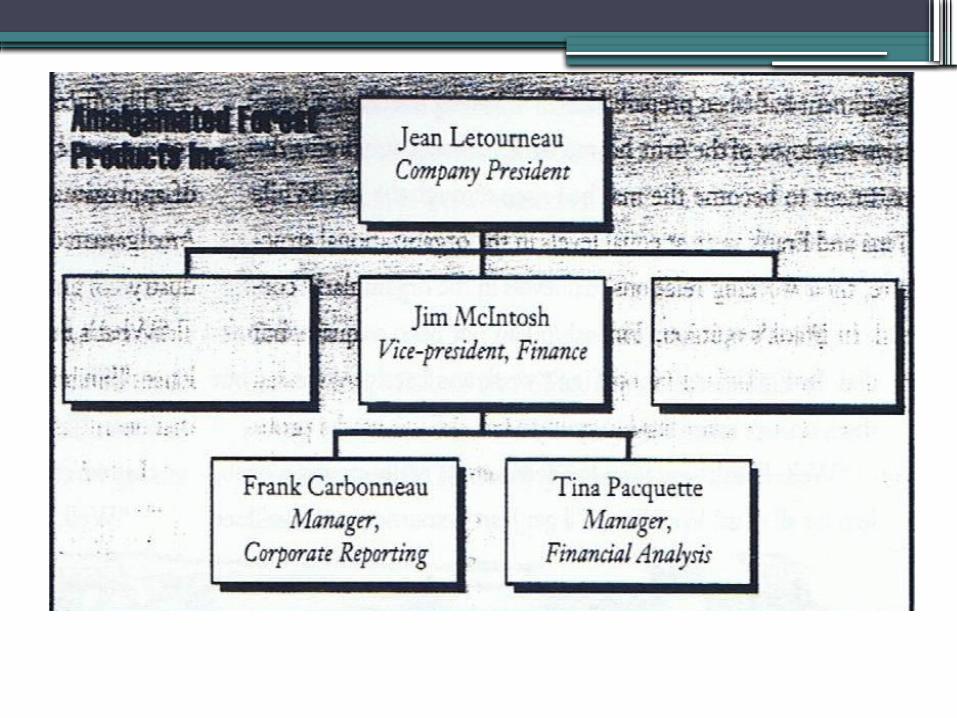

Article: The Ethical Dilemma at Northlake•Article by Grant Russel•Associate professor or management

accounting at the University of Waterloo•Director-at-large for The Society of

Management Accountants of Canada•Based on fictitious people and

circumstances•Amalgamated Forest Products Inc.•Four members of the company involved

(see organizational chart)

Frank’s Achievements With Company

•Worked Amalgamated Forest Products for over ten years after completing high school

•Worked as yard helper, then accounting clerk

•University studies arranged by company•Complete Certified Management

Accountant (CMA) designation following graduation

Frank’s Achievements With Company (cont’d)•Awarded CMA Gold Medal •Appointed new position in corporate

reporting•Promoted as manager of corporate

reporting after a year

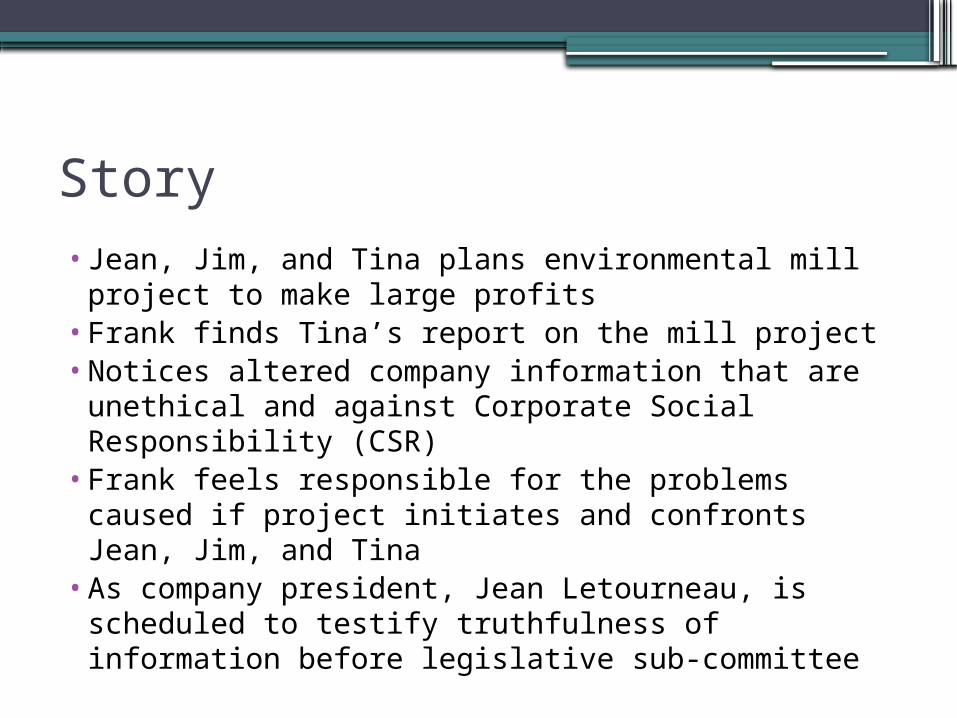

Story• Jean, Jim, and Tina plans environmental mill

project to make large profits• Frank finds Tina’s report on the mill project • Notices altered company information that are

unethical and against Corporate Social Responsibility (CSR)

• Frank feels responsible for the problems caused if project initiates and confronts Jean, Jim, and Tina

• As company president, Jean Letourneau, is scheduled to testify truthfulness of information before legislative sub-committee

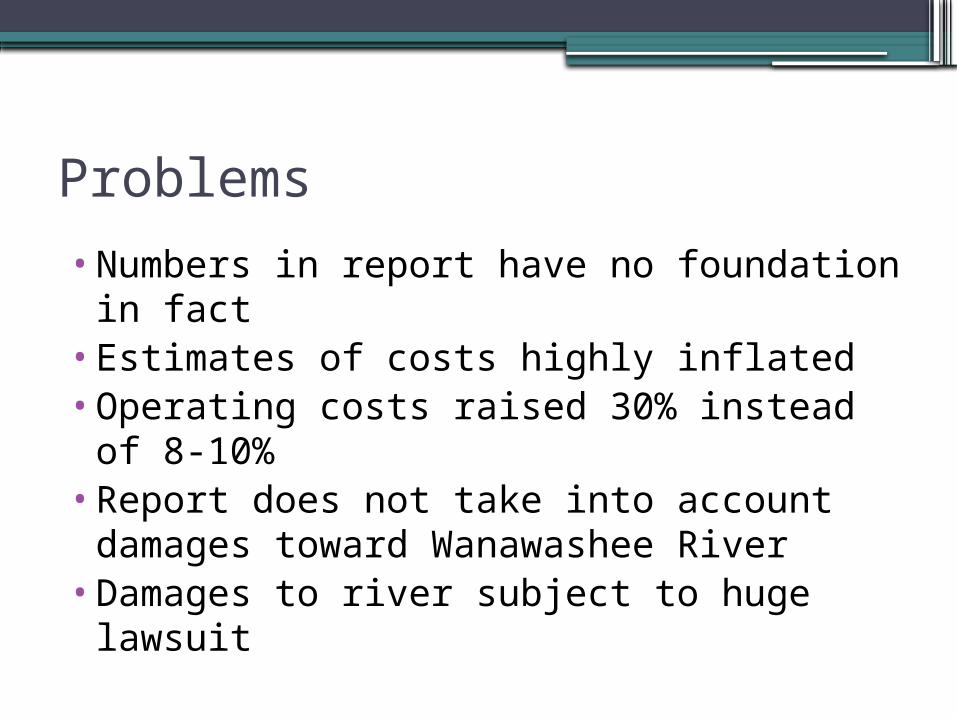

Problems

•Numbers in report have no foundation in fact

•Estimates of costs highly inflated•Operating costs raised 30% instead of 8-

10%•Report does not take into account

damages toward Wanawashee River •Damages to river subject to huge lawsuit

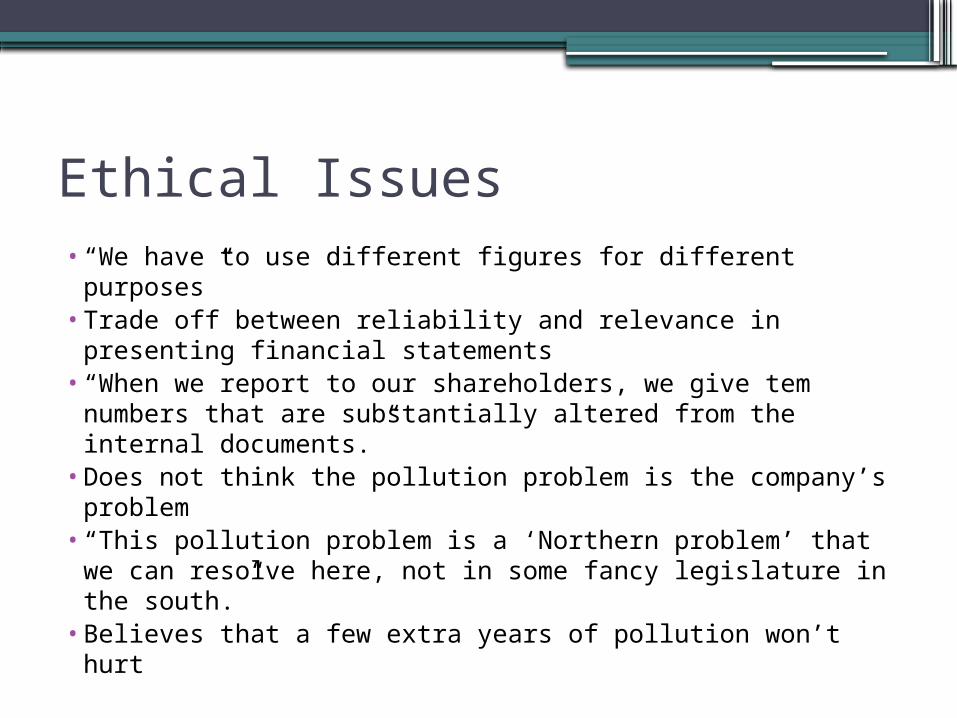

Ethical Issues • “We have to use different figures for different

purposes”• Trade off between reliability and relevance in

presenting financial statements• “When we report to our shareholders, we give tem

numbers that are substantially altered from the internal documents.”

• Does not think the pollution problem is the company’s problem

• “This pollution problem is a ‘Northern problem’ that we can resolve here, not in some fancy legislature in the south.”

• Believes that a few extra years of pollution won’t hurt

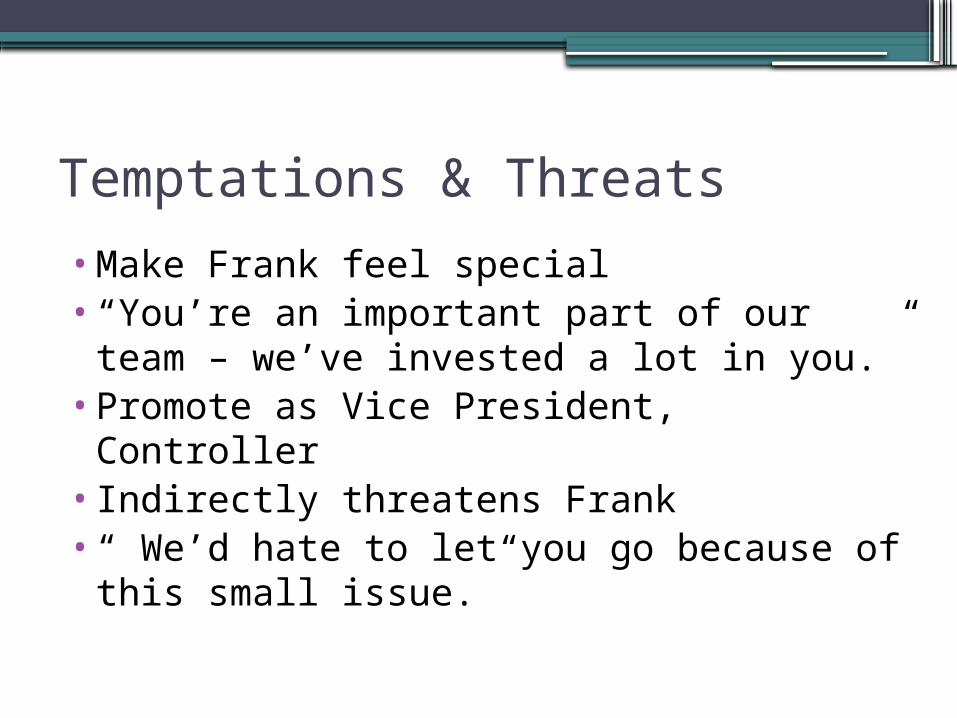

Temptations & Threats

•Make Frank feel special•“You’re an important part of our team –

we’ve invested a lot in you.”•Promote as Vice President, Controller•Indirectly threatens Frank •“ We’d hate to let you go because of this

small issue.”

Temptations & Threats (cont’d)

•Indirectly tells Frank it doesn’t concern him

•“Besides, Jim tells me this isn’t even your responsibility.”

•If Frank interferes, company will not survive and workers will blame him for unemployment

Class ThoughtsWHAT DO YOU GUYS THINK?

How should Frank react to this situation?1. Do nothing: it’s not his problem – the problem is Tina’s2. Do nothing: the personal consequences to Frank are greater

than the ethical problem3. Do nothing: the personal consequences to Frank are greater

than the ethical problem4. Do nothing: he has already informed his supervisors,

nothing else is appropriate5. Do nothing: his cocal management understands the

situation better than the legislative committee6. Write an anonymous note to the local/national press7. Resign: write a signed note to the local/national press

Class Thoughts (cont’d)

Frank’s decision should be made:1. By himself2. With legal counsel3. With his family4. With confidential friends5. With assistance from the Society of

Management Accountants

Class Thoughts (cont’d)

If Frank approaches the Society of Management Accountants for assistance, the Society should:1. Do nothing: this is the member’s

personal responsibility2. Provide confidential advice to Frank3. Provide support to Frank in the event he

needs to seek new employment (e.g. letter of reference)

![[VNMATH.COM]-Duong thang-duong tron_Nguyen Tuan Lam.pdf](https://img.dokumen.tips/doc/110x75/56d6beb31a28ab3016933955/vnmathcom-duong-thang-duong-tronnguyen-tuan-lampdf.jpg)

![[Bài giảng, ngực bụng] duong dan truyen tk, bs lam](https://img.dokumen.tips/doc/110x75/55ac2df11a28ab106b8b46ef/bai-giang-nguc-bung-duong-dan-truyen-tk-bs-lam.jpg)