Embed Size (px)

Citation preview

A Latin American Monetary FundRequired dimensions and modalities

Manuel Agosin

Universidad de Chile

CAF/FLAR Conference

Cartagena de Indias, July 6-7, 2012

Topics to be discussed

1. The international context and the need for a Latin American Monetary Fund

2. Recent financial crises: sequential or systemic?

3. LAMF Facilities

4. Suggested financial requirements

5. Conclusions

2

1. The international context

3

Financial crises: a consequence of financial globalization

• Recurring financial crises– Mexican crisis of 1994-95– Asian-Russian crisis of 1997-98– Argentinean crisis of 2001-03– The Great Recession of 2008-09– Unfolding euro crisis

• Accompanied by contagion: good domestic macro policies necessary but not sufficient in order to avoid financial crises

4

The response has been a huge increase in reserves at the national level

5

Some benefits of a regional arrangement

• Pooling of reserves is an obvious benefit: reserve holdings are costly

• Expeditious access to financing when needed (FLAR disburses in a few weeks; IMF complex and bureaucratic)

• Credible conditionality when appropriate– IMF conditionality got out of hand during the Asian

crisis

• Unconditional financing needed more than IMF is willing to recognize

6

2. Nature of financial crises

7

Key question: Are they sequential or simultaneous?

• Most have been sequential, with various degrees of contagion

• One large systemic crisis: the Great Recession (perhaps euro crisis could evolve in that direction)

• Systemic crises are more difficult to deal with by a regional fund, although we show that a regional fund of reasonable size could have dealt with the consequences of the Great Recession, given adequate support from the IMF

8

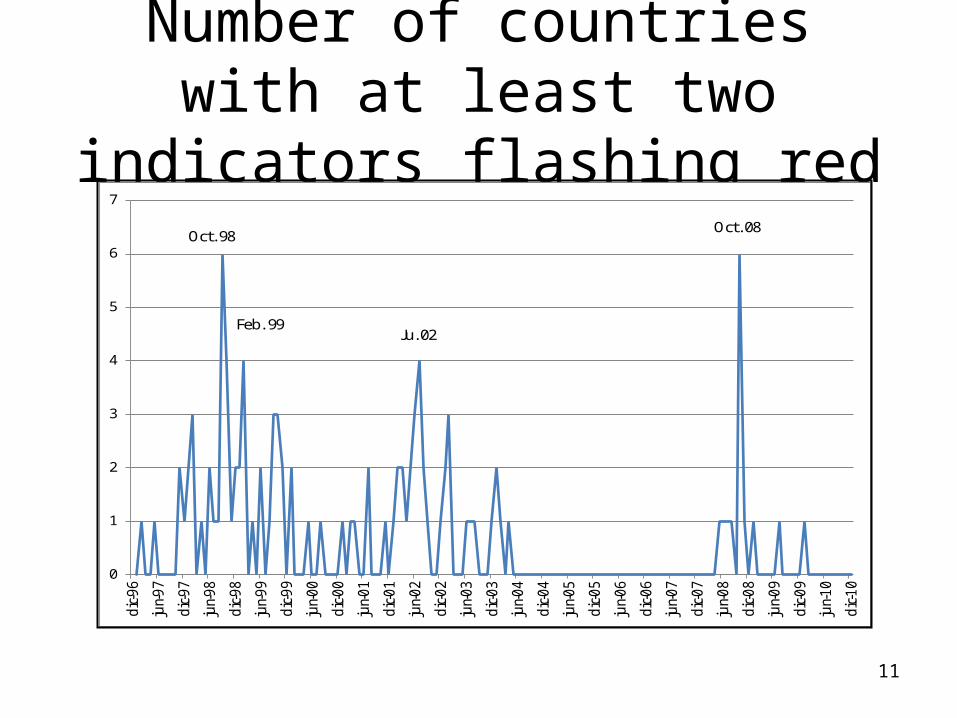

We develop an index of crisis intensity for 16 countries

• Three indicators of crises: reduction in reserves, nominal depreciation, and increases in interest rates

• Each indicator takes value of one when it is (in absolute terms) larger than one standard deviation from average of monthly observations over the period from Jan. 1997 to Dec. 2010

• Two calculations: – sum of all positive indicators; – how many countries had, in any given month, two

positive indicators9

The number of positive crisis indicators track the recent crises well

10

0

2

4

6

8

10

12

14

16

18

ene-

97

jul-9

7

ene-

98

jul-9

8

ene-

99

jul-9

9

ene-

00

jul-0

0

ene-

01

jul-0

1

ene-

02

jul-0

2

ene-

03

jul-0

3

ene-

04

jul-0

4

ene-

05

jul-0

5

ene-

06

jul-0

6

ene-

07

jul-0

7

ene-

08

jul-0

8

ene-

09

jul-0

9

ene-

10

jul-1

0

Sept. 98Feb. 99

Jul. 02 Oct. 08

Number of countries with at least two indicators flashing red

11

0

1

2

3

4

5

6

7

dic-9

6

jun-

97

dic-9

7

jun-

98

dic-9

8

jun-

99

dic-9

9

jun-

00

dic-0

0

jun-

01

dic-0

1

jun-

02

dic-0

2

jun-

03

dic-0

3

jun-

04

dic-0

4

jun-

05

dic-0

5

jun-

06

dic-0

6

jun-

07

dic-0

7

jun-

08

dic-0

8

jun-

09

dic-0

9

jun-

10

dic-1

0

Oct. 08

Feb. 99Ju. 02

Oct. 98

Conclusions• Gradual and sequential contagion from Asian-

Russian crisis: regional fund might have help moderate it – (although we later show that it was even more severe

for LA countries than the Great Recession)

• In October 2008, six out of 16 countries had at least two crises indicators flashing red: this suggests that a more systemic response was needed than

• However, the fact that the crisis was short-lived also suggests that a regional fund might have been useful 12

3. LAMF Facilities

13

Four roles envisioned

1. Stand-by arrangements

2. Regional CFF

3. Regional Financial Account Facility

4. Surveillance and policy dialogue

14

Stand-by arrangements

• FLAR already has them• Balance-of-payments financing up to three

years, with a maximum of 2.5 times quota• A larger fund could reduce that multiple

and still give countries much greater access to resources

• Surveillance and conditionality are appropriate to ensure resource recovery

15

Regional CFF

• IMF has abandoned its own facility• Terms-of-trade variations are particularly large in

Latin America• Normally, the deterioration in the terms of trade

in some countries is accompanied by improvements in those of others: this makes the issue appropriate for a credit cooperative

• Adjustment is less efficient and has higher social costs then financing

16

Terms of trade ought to be stationary, although with breaks

17

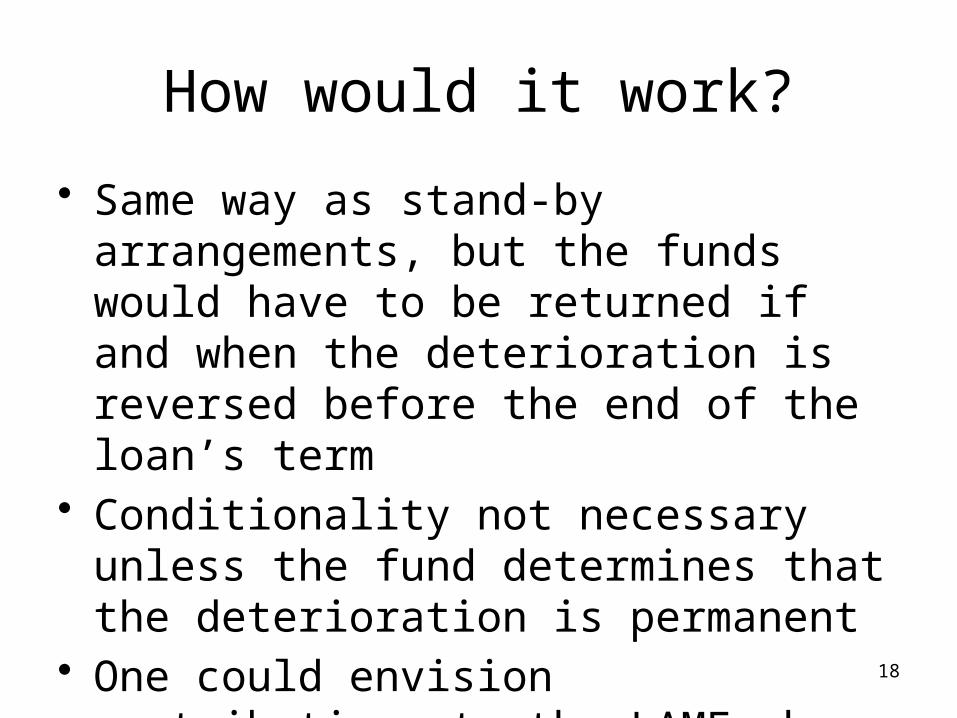

How would it work?

• Same way as stand-by arrangements, but the funds would have to be returned if and when the deterioration is reversed before the end of the loan’s term

• Conditionality not necessary unless the fund determines that the deterioration is permanent

• One could envision contributions to the LAMF when a country’s terms of trade improve 18

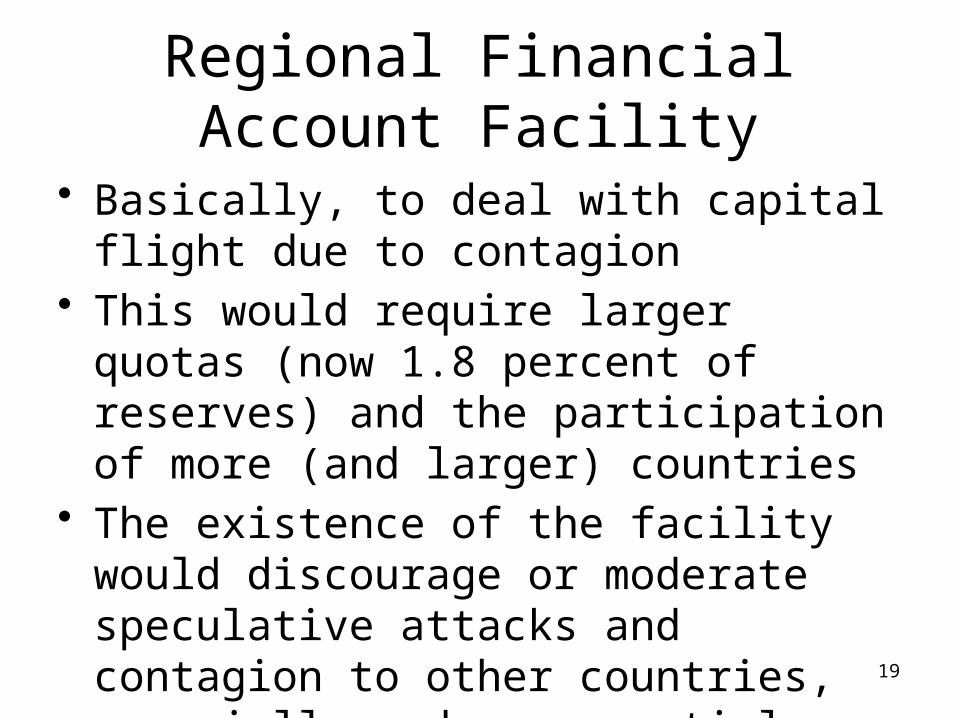

Regional Financial Account Facility

• Basically, to deal with capital flight due to contagion

• This would require larger quotas (now 1.8 percent of reserves) and the participation of more (and larger) countries

• The existence of the facility would discourage or moderate speculative attacks and contagion to other countries, especially under sequential contagion

19

Surveillance and policy consultation/coordination

• “Friendly” surveillance• Turn surveillance into policy coordination• Appropriate policies would reduce the need to deploy

resources• Should include regulation of financial sectors and

indebtedness in international money markets (see Shin proposal)

• Without being an explicit objective, policy consultation plus financing would help stabilize regional exchange rates and promote inter-regional trade

20

4. Financial requirements

21

Back-of the-envelope calculation

• Criteria:– It should be of sufficient size for its objectives– It should not be too large to scare off potential

and actual members• Considered all of the current FLAR

members and added Argentina, Brazil, Chile, Mexico, and Paraguay

• Total volume of fund, with indebtedness and IMF credit line: $ 125 billion

22

Basic framework of the fund

A. Paid-in capital: 4% of reserves (as of Dec. 2010), $25 billion (remunerated)

B. Bond placement with joint guarantees: 8% of reserves, $50 billion

C. IMF credit line: 8% of reserves, to be used only when fund has exhausted half of A and B, $50 billion

This is equivalent to CMIM

23

Can a fund of this size deal with crises like recent ones?

• Total impact of Great Recession was $94 billion (decline in financial inflows excluding reserve transactions and FDI of 12 countries in 2008-09, in 2010 US$)

• In fact, the decline in capital inflows was larger during the Asian-Russian crisis, but its sequential nature could have helped the fund to deal with it

• Size looks adequate, if it can arrange credit lines with IMF in specified circumstances

24

Why would big non-member countries be interested?

• They have more reserves than the total resources proposed for the LAMF

• So do China, Japan and Korea in the CMIM

• Brazil and Mexico potentially interested in a stable and growing region

• It would cost them little and have influence over the fund relative to their quotas

25

5. Conclusions

26

Benefits of a LAMF

• Regional CFF: TT fluctuations particularly severe

• Establishment of effective and permanent system of regional policy monitoring, leading to policy dialogue

• Provision of conventional balance-of-payments financing with appropriate conditions

• Have on hand sufficient resources to stem contagious financial account crises

• Channel between IMF and countries in the region 27