Embed Size (px)

Citation preview

A Forecasting Model of Dry Bulk Freight Rate

- Using the Time-Varying Coefficient Model

in the Classical Framework

This report is written as an output of

constructing a forecasting model of dry bulk freight rate

August 2013

Ko, Byoung Wook

Shipping Market Research Center

Korea Maritime Institute (KMI)

i

Contents

Prologue ············································································································ 1

Ⅰ. Introduction ·································································································· 2

Ⅰ-1. Research Purpose ······································································································· 2

Ⅰ-2. Research Scope ·········································································································· 3

Ⅰ-3. Report Organization ··································································································· 5

Ⅱ. Prerequisite Study of Time Series Models ···················································· 6

Ⅱ-1. Basic Concepts of Time Series Data ·········································································· 6

Ⅱ-2. Univariate Case: AR, MA, Wold’s Decomposition, Impulse-Response Analysis, and Unit Root ··········· 8

Ⅱ-3. Multivariate Case: VAR, VECM, and Co-integration ·············································· 11

Ⅲ. Literature Review ······················································································· 13

Ⅲ-1. Literature on Forecasting in Other Fields Including Macroeconomics and Finance ······ 13

Ⅲ-2. Literature on Forecasting Dry Bulk Freight Rate ···················································· 20

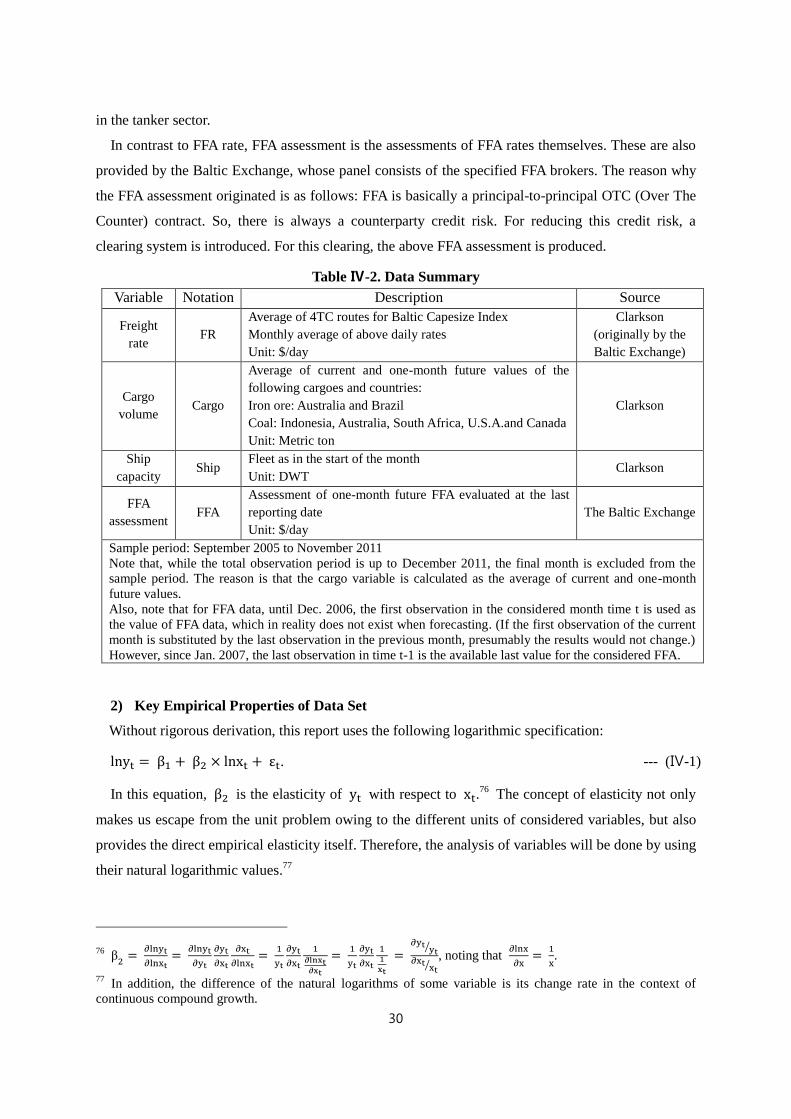

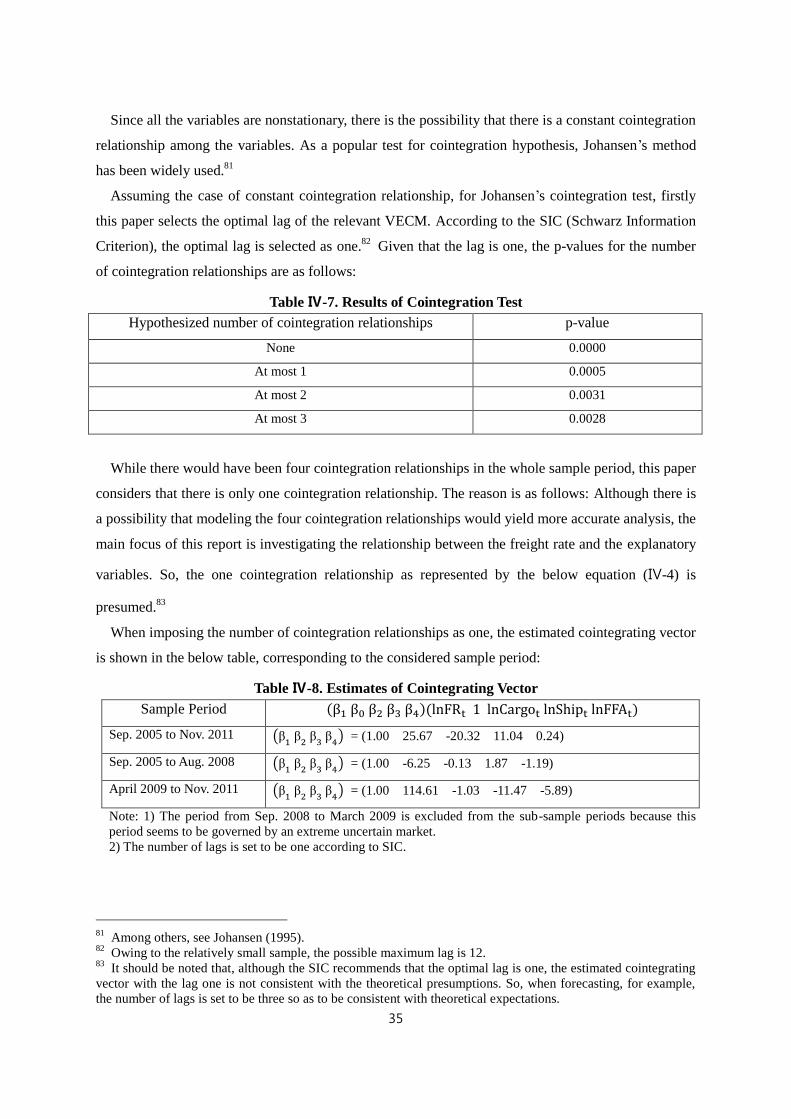

Ⅳ. Data and Time-Varying Coefficient Model ················································· 27

Ⅳ-1. Data ·························································································································· 27

Ⅳ-2. Time-Varying Coefficient Model ············································································· 36

ii

Ⅴ. Estimation and In-Sample/Out-of-Sample Forecasting with Evaluation ····· 42

Ⅴ-1. Estimation Results of Time-Varying Coefficient Model ·········································· 42

Ⅴ-2. In-Sample and Out-of-Sample Forecasting Results with their Evaluations ············ 47

Ⅵ. Conclusion ································································································· 53

Ⅵ-1. Summary ·················································································································· 53

Ⅵ-2. Future Research Direction ······················································································· 54

Epilogue ·········································································································· 56

Technical Appendix ························································································· 57

Shipping Terminology ······················································································ 59

References ······································································································· 61

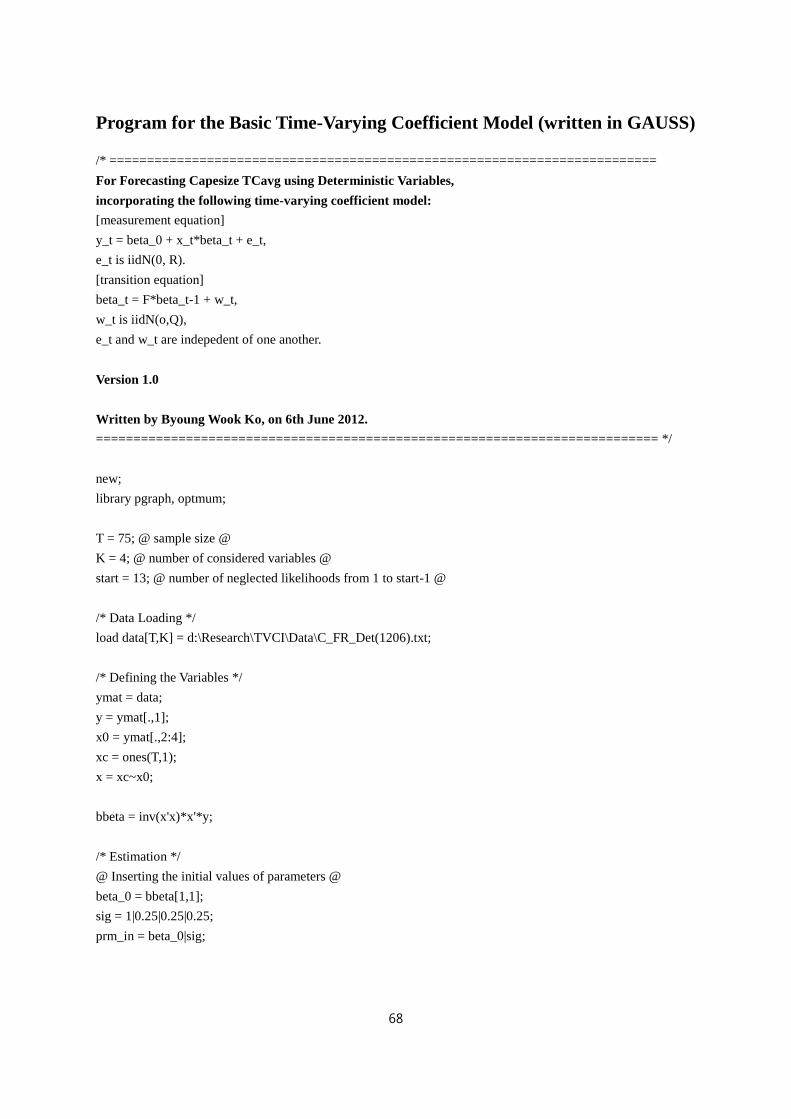

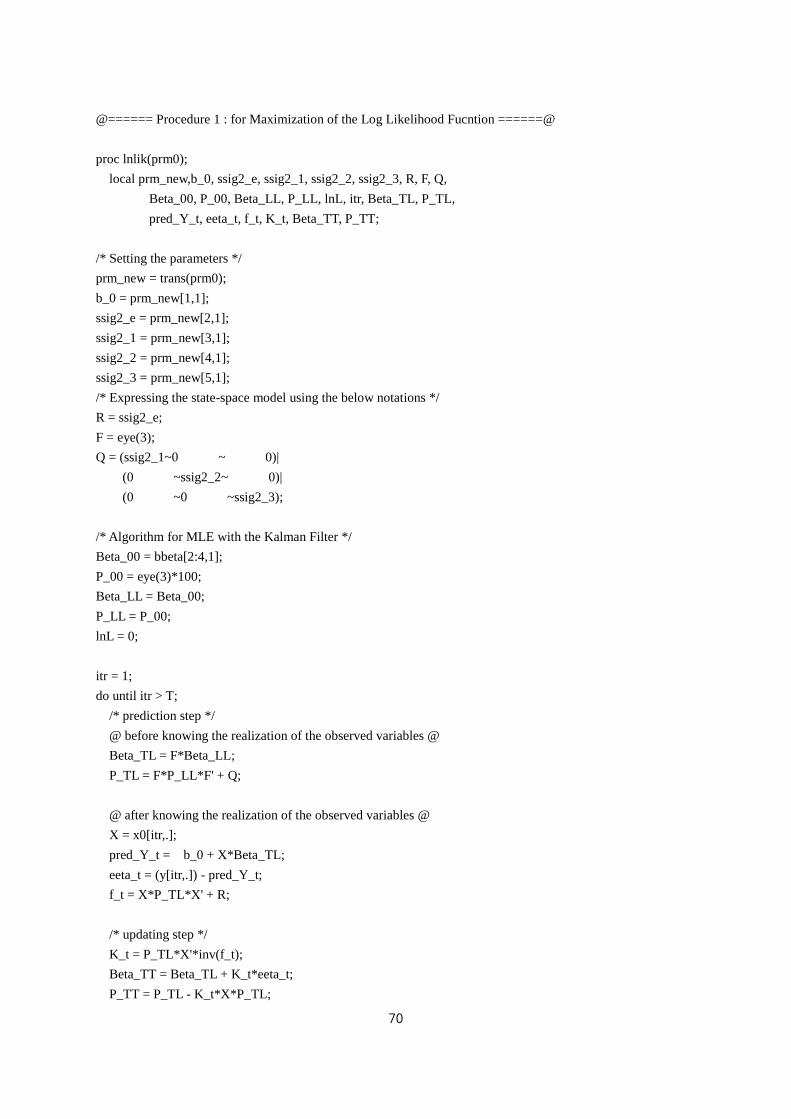

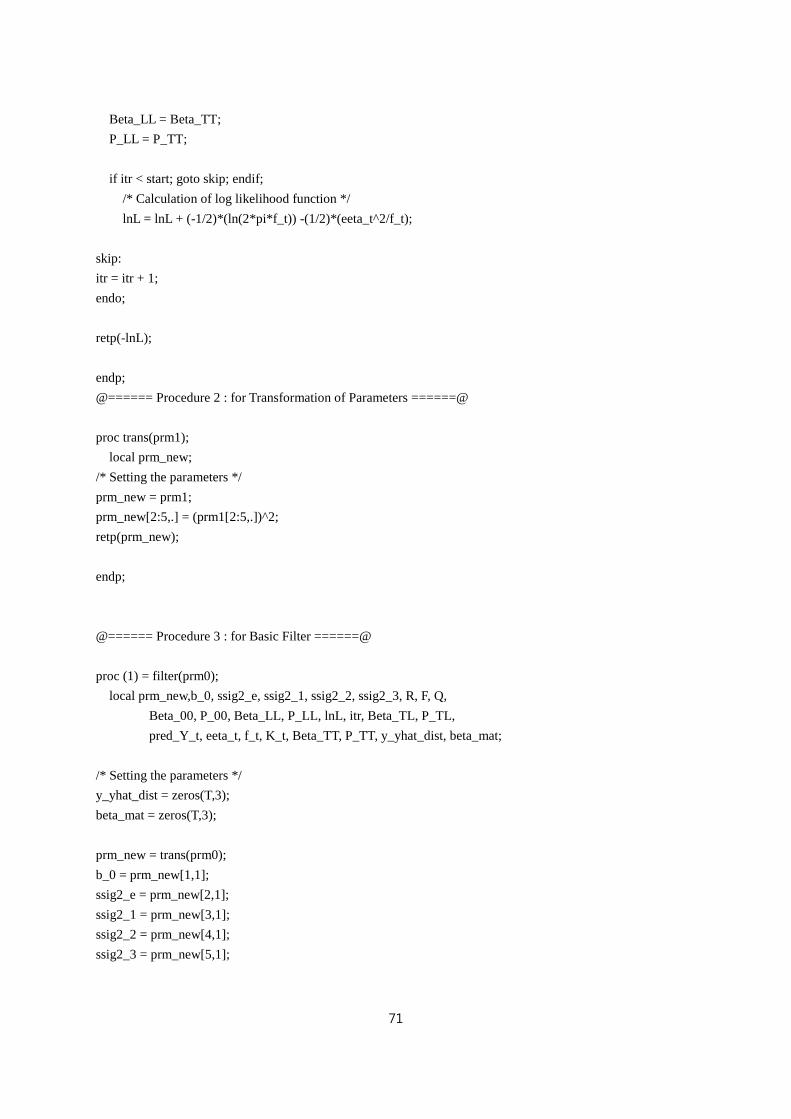

Program for the Basic Time-Varying Coefficient Model (written in GAUSS) ········ 68

Endnotes ·········································································································· 73

1

Prologue

To be frank, within human intellectual ability, we should forecast the course of future events only

based on the past experience. In other words, we cannot forecast or foresee the future perfectly.

However, there has been and will be a continuous demand for the future forecasting. I think that this

forecast demand stems from the necessity of some rational plan for future economic activity. The

research conducted for the writing of this report is also required for the same reason, i.e., some need

of a rational forecasting tool.

Performing this challenging task, I have tried to apply the so-called time-varying coefficient model

to forecasting the dry bulk freight rate. The results of this effort are presented in a reader-friendly

scheme as possible. However, owing to the limitation of author’s ability, this report lacks various

elements of shipping markets and econometrics. So, I’d like to say that incorporating more realistic

aspects of shipping markets and more rigorous econometric theorizing will remain as the important

future research topic. As a good reference, for shipping markets, it is strongly recommended to refer

to Stopford (2009) and, for econometric treatment of forecasting, refer to Diebold (2006).

If a new combination could be regarded as an innovation, I think that this research can be an

innovation in that it aims to combine the forecasting job in the dry bulk freight market with the

academic achievement of so-called time-varying coefficient model. Hence, it could be assessed as a

meaningful improvement of existing literature.

However, this report seems to be a little complicated so that it could be difficult to be understood. I

think that the difficulty is mainly from the positioning of the report in the existing literature, but not

from its essential contents. So, I hope that some requisite enduring investment of the interested

readers will make them understand the essential contents of this report.

Finally, I hope that this report as a good reference will help the readers to do their jobs.

2

Ⅰ. Introduction

Ⅰ-1. Research Purpose

Freight rate forecasting has become more important because the volatility of freight rate has

become larger and the demand for rational market risk management of shipping company, shippers,

investors, and so on, has also become larger.1

i So, the method of conducting the forecasting job for

freight rate should be rational in the sense that the related company can implement the business plan

by using all the relevant and available information at that time.ii For example, the company can

appropriately deal with or hedge against the market risk by the use of this forecasting process.

However, this rational forecasting can be a form of qualitative, quantitative, or mixed one. This report

focuses on the quantitative method of freight rate forecasting in dry bulk shipping market.2

In the fields of Macro-econometrics and financial economics, there are a large volume of literature

for forecasting the GDP, price levels (or inflation rate), interest rates, etc. Also, in the field of shipping

industry, there are a number of papers or reports, which deal with forecasting the freight rate, the

cargo volume, and so forth. However, to the best of my knowledge, there is a big gap between the

progresses of the two distinct fields, i.e., 1) the shipping research and 2) the Macro-econometrics and

financial economics research. For example, recently in Macro-econometrics and financial economics,

time-varying coefficient model incorporating the model uncertainty is widely used so that a

significant improvement in the prediction ability is reported. But, in shipping research, the usual

forecasting model considers only time-invariant coefficients.3

4 In addition to the improvement of

1 Stopford (2009), which is recognized as one of the most influential, classical textbooks of maritime (shipping)

economics, explains very well the purpose and limitation of maritime forecasting and market research.

(Especially, see Chapter 17 of Ibid.) Among others, the three reasons why, instead of formal statistical approach

such as the model of this report, the intuition of individual shipowner works are notable: “Firstly, some key

aspects of shipping markets are too subtle to capture in statistical models, for example the effect of congestion

and supply shortages which disrupt the demand side of the model and cause unexpected changes in the market.

Secondly, statistical data is limited and often arrives too late to be useful to a company trying to keep ahead of

the pack. Thirdly, some variables such as market sentiment are too mercurial to capture in a formal forecasting

model, so an experienced businessman close to the market has a far better chance of grasping what is really

happening than a team of analysts struggling to fit a model to inadequate data.” (See p.707. of Ibid.)

However, despite these shortcomings of formal statistical model for forecasting, he argues for its use in the

following way: “Humans cannot fly themselves, but with a little lateral thinking they came up with airplanes

which are almost as good (and much better on a transpacific trip!). In coming to terms with forecasting we need

to do the same sort of lateral thinking.” (See p.700. of Ibid.) Additionally, he says that the rational forecasting

can help to reduce the uncertainty which is faced by the related decision-makers. 2 However, although KMI uses this kind of quantitative model, the final results for forecasting are based on

both the qualitative and quantitative methods. 3 To the best of my knowledge, there has been one exceptional paper in shipping economics, Chung and Ha

(2010a). However, they consider the BDI determination mechanism but do not consider forecasting using their

model.

For a brief review, see the below section Ⅲ-2 of this report.

4 There have been various alternative methods to time-series linear regression approach. These reflect the time-

3

prediction ability, the lens using time-varying coefficient model could allow for us to see more

phenomena, which could not be observed through the lens of time-invariant coefficient model or

heteroskedasticity model (e.g., ARCH-type model).iii

Therefore, this report aims to fill this research gap and thus provide more rational forecasting tool

for the improvement of prediction ability. Because this report is written for the practitioners in the dry

bulk freight market, who do the freight rate forecastingiv with understanding of undergraduate-level

econometrics but without deep understanding of graduate-level econometrics, the author tries to

explain the relevant concepts and models as simple as possible.5

v Also, I endeavor to write the

report by using a consistent set of definitions, notations, and so on. For this aim of simple exposition,

I add a technical appendix, in which the readers can understand some basic statistics concepts

including, for example, maximum likelihood estimation.

The approach proposed in this report is not the only right method for forecasting the freight rate

quantitatively, but one potential useful tool for the more rational plan of shipping business. So, for

example, the player, who occupies more plentiful data sets, will perform better forecasting job than

the author while using the same proposed model.6

Also, this research will provide more concrete applications to time-series analysis. That is, it will

expand the field, where time-series models are used, by applying various time-series models to the

shipping industry, especially the dry bulk freight market. So, this report could be a guide for the new

coming econometricians to the shipping econometrics.

Ⅰ-2. Research Scope

The main purpose of this report is to provide an appropriate empirical model for forecasting the dry

bulk freight rate.7 For this aim, this report reviews the related literature, which could be classified

into two strands. The first is on the predictions of macroeconomic or financial variables and the

varying relationships among the considered variables of shipping (freight) markets. However, in most cases of

shipping economics, the model of time-series feature is time-invariant linear regression one. 5 It is known as the Einstein Principle that a scientific theory should be as simple as possible, but no simpler.

Some readers might consider the proposed models of this report as the simpler ones so that they could require

more realistic and complex models. Responding to this potential criticism, the author wants to say that this kind

of research with more abundant reality will be the topic of future research.

However, the readers, especially without professional technique of econometrics, is recommended to carefully

read this report while keeping in mind the following Einstein’s observation: Albert Einstein once observed that anyone who reads scientific material without a pencil and paper at

hand can’t seriously care about understanding it. (On p.xxi. of Obstfeld and Rogoff (1996)) 6 As stated in Stopford (2009), this tool can be circulated to colleagues and independently checked. Also, the

author believes that the usefulness of the proposed approach will be more to the big companies or pools with

more strong information. 7 Diebold (2006) classifies the forecast object into three ones. First is event outcome forecast, second is event

timing forecast, and the third is time series forecast. According to this classification, the freight rate forecast of

this report belongs to time series forecast.

4

second is on those of shipping freight rate variables.

Generally, the practice of quantitative forecasting involves the statistical inferences on the

underlying economic system. This statistical inference can be done based on the classical or Bayesian

framework. The former of classical approach presumes that we can observe a large number of

observations enough for us to get the right information on the true parameters of the system. In

contrast, the latter of Bayesian approach presumes that we can observe only limited some samples

which will help us to update our beliefs of the underlying economic system. Therefore, while the

classical framework is more appropriate for the natural science where repeating controlled

experiments is possible, the Bayesian framework is for the social science where controlled

experiments are in principle limited and the sample is relatively small.

However, this report focuses only on the classical approach to forecasting the dry bulk freight rate

but not on the Bayesian one, which is an important limitation of this research. The development of

Bayesian models will be the topic of future research. Despite this limitation, this report will show

some research results of Bayesian forecasting and empirical inferences of the existing literature,

which will help us to position this report among the recent relevant literature.

The global dry bulk markets include a large number of local markets and various kinds of markets,

for example, freight, shipbuilding, secondhand ship, and demolition markets. (For the explanation of

basic shipping terminology, see the attached “Shipping Terminology”) In reality, there are a big

amount of interactions among these markets. For example, the Asian market is related with the trans-

Atlantic market. And while the freight market influences the price of secondhand ship, the reverse

influence works. In spite of this diversity of dry bulk markets, this report analyzes the dry bulk freight

market and the representative freight rate, for example, the 4TC average of Cape-size ship.vi However,

the proposed model can be used for other ship-type or ship-size freight markets, which remains a

future research topic.

Also, this report provides only discrete time-series model of which time-varying coefficient model

will be extensively discussed. However, it is notable that there are many alternative models, for

example, artificial neural networks, system dynamics, etc.

In summary, this report constructs a forecasting model of Cape-size freight rate by using a time-

varying coefficient model in the classical framework.

5

Ⅰ-3. Report Organization

This report aims to provide the market practitioners with a time-varying coefficient model as one

forecasting tool for dry bulk freight rate. Since dealing with an econometric model requires

understanding some technical elements, this report starts with Chapter Ⅱ, “Prerequisite Study of

Time Series Models” and also attaches “Technical Appendix”. Based on these basic concepts, this

report goes ahead to understanding the contents of relevant literature in Chapter Ⅲ, “Literature

Review”, which reviews the two strands of the literature, 1) on forecasting in the other fields such as

Macroeconomics and Finance and 2) on forecasting dry bulk freight rate.

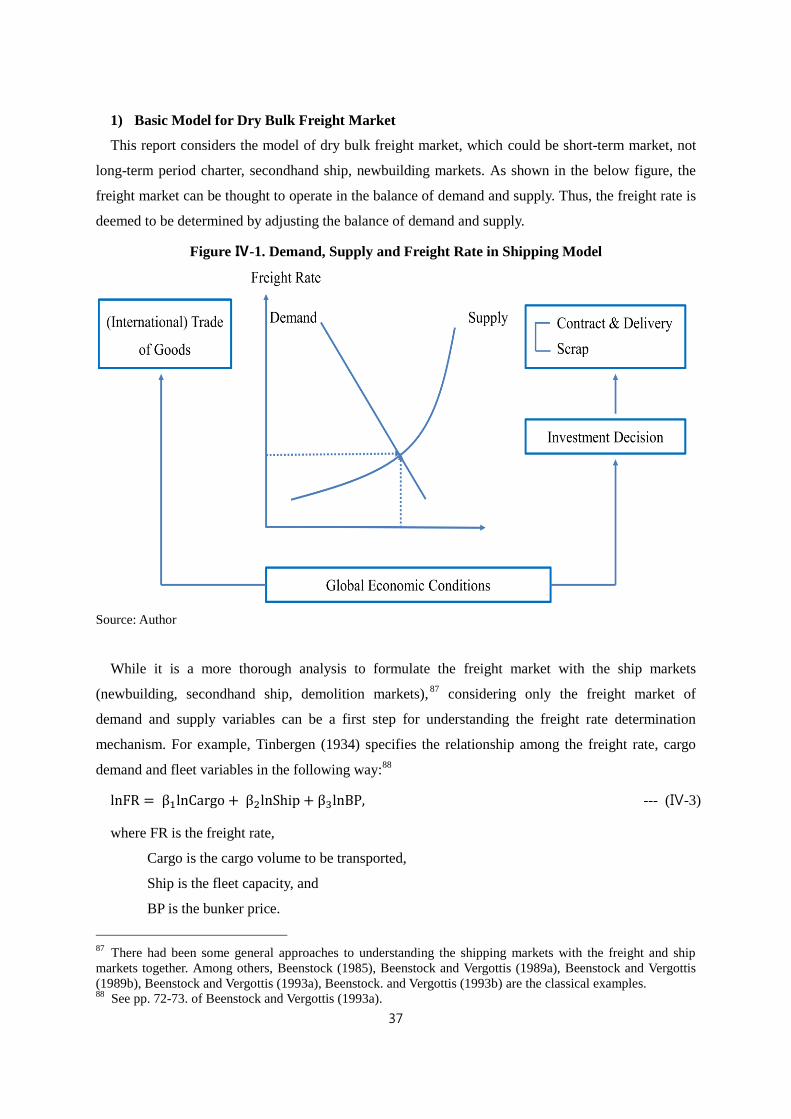

Chapter Ⅳ suggests the basis for the empirical study of this report. First, the used data set is

suggested with some explanatory analysis. Second, after considering the basic demand/supply model

for the determination of the freight rate, the theoretical time-varying coefficient model is introduced.

Chapter Ⅴ shows the estimation procedure and results of the time-varying coefficient model and

then presents the predicted values. These predictions are evaluated by comparing with the alternative

benchmark models such as the simple OLS, VECM with time-invariant cointegration and FFA’s

prediction ones.

The concluding Chapter Ⅵ summarizes the report and suggests the future research directions.

For the econometricians with deep understanding of time-series methods but without shipping

background, the Chapter “Shipping Terminology” is attached. Also, the readers, who are interested in

programming the time-varying coefficient model by themselves, are referred to the attached program,

“Program for the Basic Time-Varying Coefficient Model (written in GAUSS)”.

For the completeness of the report, I add the prologue and epilogue as the supplementary materials.

In these writings, I’d like to tell about the background and implications of this report in more detail.

6

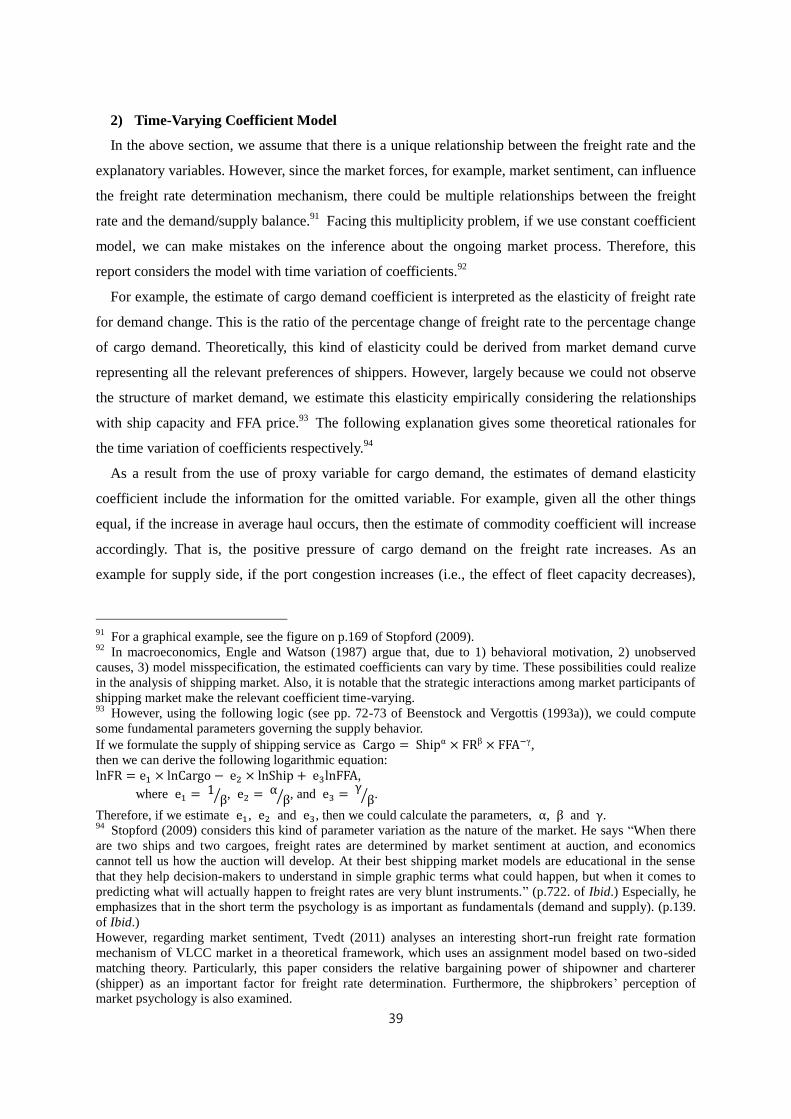

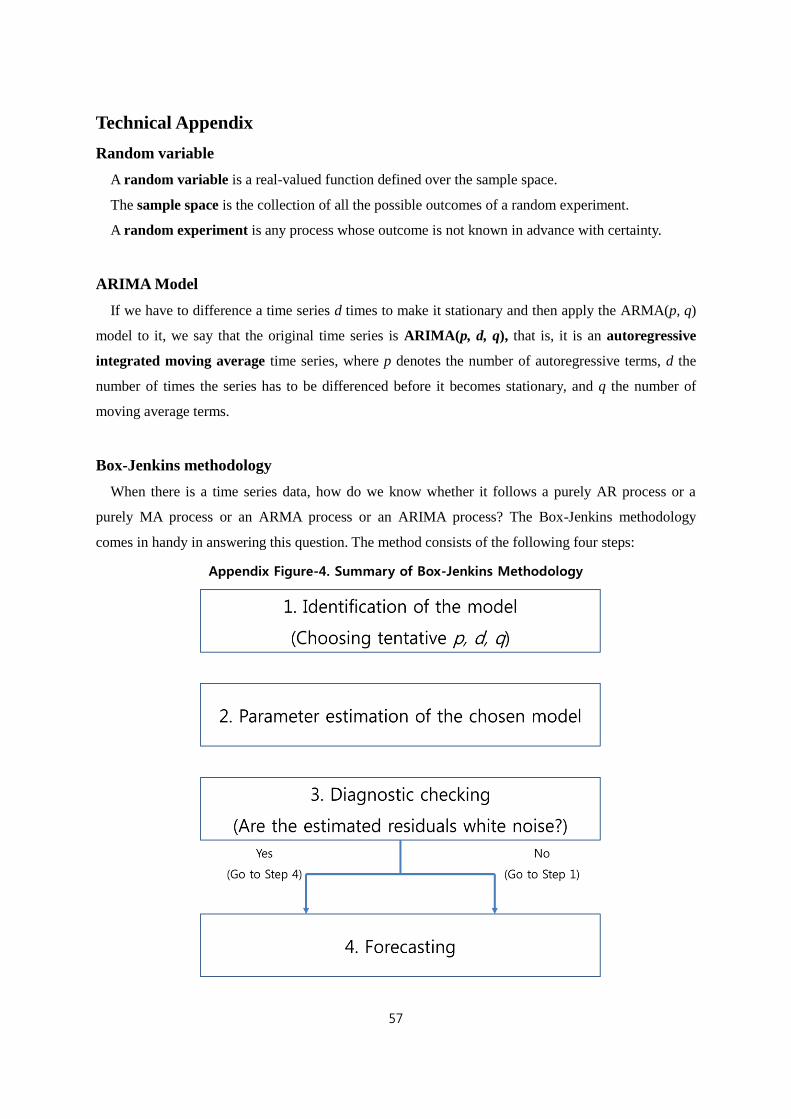

Ⅱ. Prerequisite Study of Time Series Models8

Ⅱ-1. Basic Concepts of Time Series Data

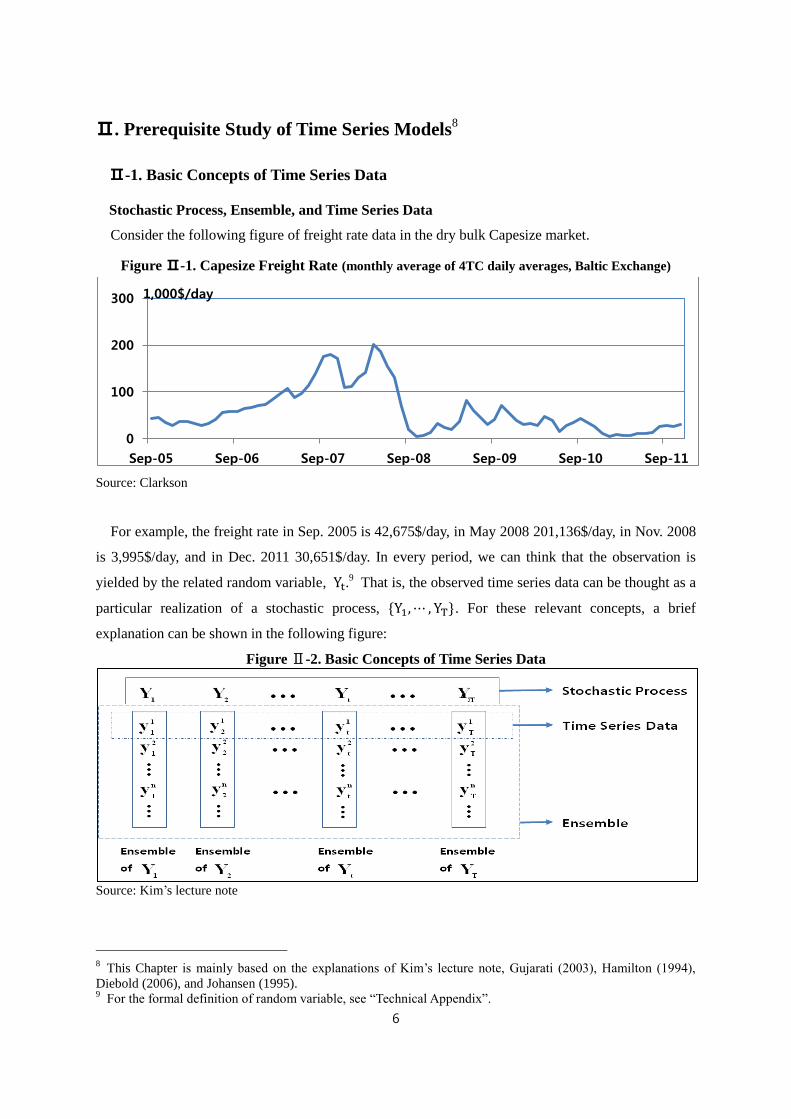

Stochastic Process, Ensemble, and Time Series Data

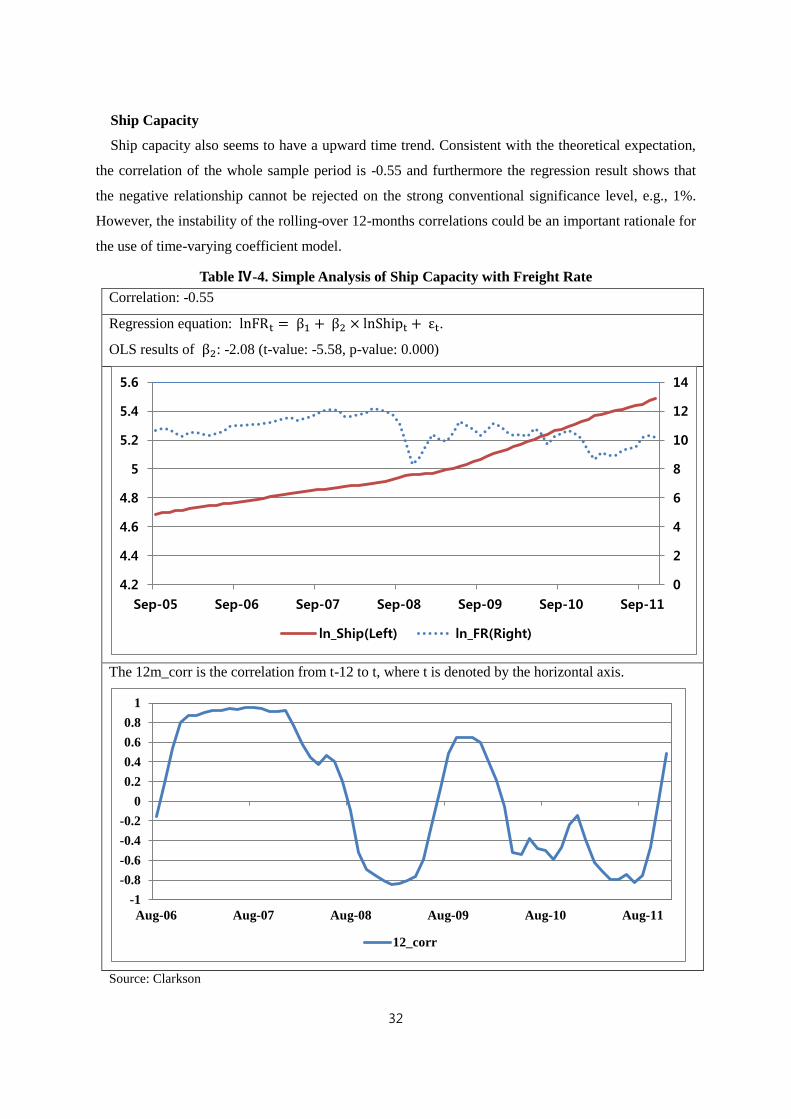

Consider the following figure of freight rate data in the dry bulk Capesize market.

Figure Ⅱ-1. Capesize Freight Rate (monthly average of 4TC daily averages, Baltic Exchange)

Source: Clarkson

For example, the freight rate in Sep. 2005 is 42,675$/day, in May 2008 201,136$/day, in Nov. 2008

is 3,995$/day, and in Dec. 2011 30,651$/day. In every period, we can think that the observation is

yielded by the related random variable, Yt.9 That is, the observed time series data can be thought as a

particular realization of a stochastic process, {Y1,⋯ , YT}. For these relevant concepts, a brief

explanation can be shown in the following figure:

Figure Ⅱ-2. Basic Concepts of Time Series Data

Source: Kim’s lecture note

8 This Chapter is mainly based on the explanations of Kim’s lecture note, Gujarati (2003), Hamilton (1994),

Diebold (2006), and Johansen (1995). 9 For the formal definition of random variable, see “Technical Appendix”.

0

100

200

300

Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11

1,000$/day

7

In words, a stochastic process is a sequence of random (stochastic) variables ordered in time.

Ensemble is a collection of all possible realizations of a stochastic process. Time series data is a

particular realization of a stochastic process. In typical situation, we have only a particular time series

data, {y11, y2

1,⋯ , yt1, ⋯ , yT

1}. In contrast with cross-sectional data, usually we cannot expand the data

set by repeating the relevant experiments or by surveying more samples.10

Stationarity and Ergodicity

Only using time series data, we should impose some assumptions on the stochastic process in order

to derive information from the time series data. For example, consider the following data, which are

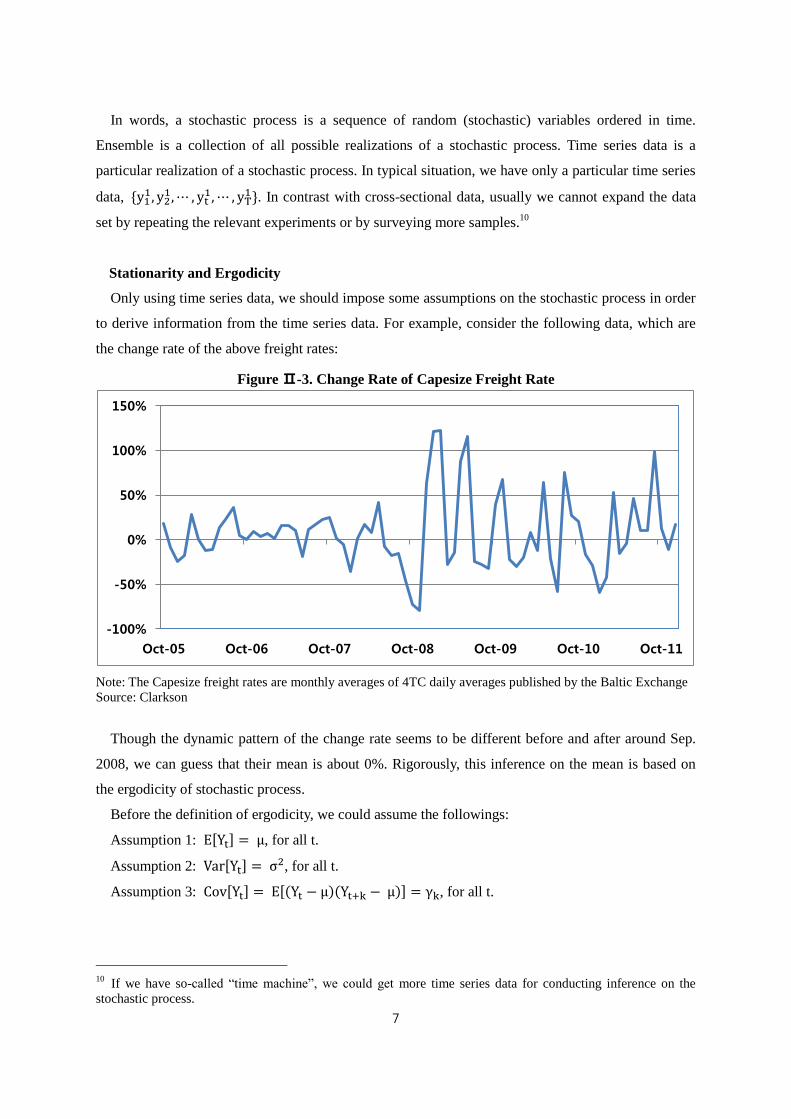

the change rate of the above freight rates:

Figure Ⅱ-3. Change Rate of Capesize Freight Rate

Note: The Capesize freight rates are monthly averages of 4TC daily averages published by the Baltic Exchange

Source: Clarkson

Though the dynamic pattern of the change rate seems to be different before and after around Sep.

2008, we can guess that their mean is about 0%. Rigorously, this inference on the mean is based on

the ergodicity of stochastic process.

Before the definition of ergodicity, we could assume the followings:

Assumption 1: E[Yt] = μ, for all t.

Assumption 2: Var[Yt] = σ2, for all t.

Assumption 3: Cov[Yt] = E[(Yt − μ)(Yt+k − μ)] = γk, for all t.

10

If we have so-called “time machine”, we could get more time series data for conducting inference on the

stochastic process.

-100%

-50%

0%

50%

100%

150%

Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Oct-10 Oct-11

8

If the above three assumptions hold, then the process for Yt is said to be covariance-stationary or

weakly stationary. Broadly speaking, a stochastic process is said to be stationary if its mean and

variance are constant over time and the value of the covariance between the two time periods depends

only on the distance or gap or lag between the two time periods and not the actual time at which the

covariance is computed.

In order to define the ergodicity, let’s define the time average of the time series as follows:

y̅ ≡ (1 T⁄ )∑ yt1T

t=1 . --- (Ⅱ-1)

A covariance-stationary process is said to be ergodic for the mean if (Ⅱ-1) converges in probability

to E[Yt] as T → ∞.11

For example, the below AR(1) and MA(1) are both covariance-stationary and

ergodic for the mean.12

Therefore, as shown in Figure Ⅱ-3, we could conclude that the average of change rate is about 0%,

given that the underlying process is ergodic for the mean and the sample size is sufficiently large.

Ⅱ-2. Univariate Case: AR, MA, Wold’s Decomposition, Impulse-Response Analysis,

and Unit Root13

Autoregressive (AR) Process

Consider the following first-order autoregressive (AR(1)) process:

yt = c + ∅ × yt−1 + εt, --- (Ⅱ-2)

where |∅| < 1, and {ϵt} is a white noise in the sense that E[εt] = 0, E[εt2] = σ2, and

E[εtετ] = 0 for t ≠ τ.14

It can be proven that, when |∅| < 1, the above AR(1) process is covariance-stationary and ergodic

for the mean.

11

This means that, if the sample size is sufficiently large, the time average becomes equal to the ensemble mean,

μ. 12

It is notable that the ergodicity is a sufficient condition for the covariance-stationarity but the covariance-

stationarity is not the sufficient condition for the ergodicity. So, the covariance-stationarity is a necessary

condition for the ergodicity. 13

After studying this section, for more understanding the related econometric concepts such as ARIMA and

Box-Jenkins methodology, see “Technical Appendix”. 14

For the notational simplicity, in this report, without a particular note, εt is assumed to be a white noise with

normal distribution is denoted by “~iidN(0, σ2)”, which is read “independently and identically distributed with

normal distribution, its mean is 0 and its variance is σ2”.

9

However, a generalized pth-order autoregression, denoted AR(p), is as follows:

yt = c + ∅1 × yt−1 + ⋯+ ∅p × yt−p + εt. --- (Ⅱ-3)

Moving Average (MA) Process

Consider the following first-order moving average (MA(1)) process:

yt = μ + εt + θ × εt−1. --- (Ⅱ-4)

It can also be proven that, regardless of the value of θ, the above MA(1) process is covariance-

stationary. Furthermore, if {ϵt} is Gaussian white noise, which means {ϵt} is a sequence of

independent random variables each of which has a N(0, σ2) distribution, then the MA(1) is ergodic

for all moments.15

Wold’s Decomposition Theorem and Impulse-Response Analysis

Wold’s decomposition theorem says that all of the covariance-stationary process can be written in

the following form:

yt = μ + ∑ ψj × εt−j∞j=0 , --- (Ⅱ-5)

where ∑ ψj2∞

j=0 < ∞ with ψ0 = 1.

Based on this excellent property of covariance-stationarity, we can analyse the impulse-response

mechanism. For example, how much will Yt+j change by the unit shock, εt? This response of Yt+j

from the impulse εt is measured as ψj, based on the following reason:

∂yt+j

∂εt=

∂yt

∂εt−j= ψj.

Unit Root Stochastic Process

Up to now, we discuss the properties of stationary process. However, in reality, many time series

data seem to be nonstationary, which simply means “not stationary” in the sense just defined above. In

other words, a nonstationary time series will have a time-varying mean or a time-varying variance or

both.

A well-known nonstationary stochastic process is the random walk model.16

Random walk without

15

Without introducing the rigorous definitions of all moments, simply speaking, the first moment is the mean

and the second moment is variance. Similarly, higher moments can be defined. 16

The term random walk is often compared with a drunkard’s walk. Leaving a bar, the drunkard moves a

random distance εt at time t, and, continuing to walk indefinitely, will eventually drift farther and farther away

10

drift has the following form:

yt = yt−1 + εt. --- (Ⅱ-6)

In contrast, random walk with drift17

has the following form:

yt = μ + yt−1 + εt. --- (Ⅱ-7)

This random walk process is a typical unit root18

stochastic process. We also call the random walk

model as “integrated of order 1, denoted as I(1)”.19

Similarly, if a stochastic process has to be

differenced twice to make it stationary, we call it as “integrated of order 2”. In general, if a stochastic

process has to be differenced d times to make it stationary, that time series is said to be “integrated of

order d”. A stochastic process yt integrated of order d is denoted as yt ~ I(d).

With regard to the random walk with drift, we should distinguish the “difference stationary process

(DSP)” from the “detrend stationary process (TSP)”. We can write (Ⅱ-7) as the following:

yt − yt−1 = ∆yt = μ + εt. --- (Ⅱ-8)

It means that yt will exhibit a positive (μ > 0) or negative (μ < 0) trend. Such a trend is called a

stochastic trend. Equation (Ⅱ-8) is a DSP because the nonstationarity in yt can be eliminated by

taking first difference of the process.

In contrast, consider the following deterministic trend model:

yt = β1 + β2 × t + εt. --- (Ⅱ-9)

It is called as a TSP (deTrend Stationary Process). Though the mean of yt is β1 + β2 × t, which

is not constant, its variance is constant as E[εt2]. It is notable that, once the values of β1 and β2 are

known, the mean can be forecast perfectly. Therefore, if we subtract the mean of yt from yt, the

resulting process will be stationary, hence the name is detrend stationary.

from the bar. The same is said to about stock prices. Today’s stock price is equal to yesterday’s stock price plus a

random shock. (On p.798. of Gujarati (2003)) 17

In the equation (Ⅱ-7), μ is known as the drift parameter. 18

From yt = yt−1 + εt, we get yt − yt−1 = (1 − L)yt = εt, where L is the lag operator. The term unit root

refers to the root of the polynomial in the lag operator: If you set (1-L) = 0, we obtain L = 1, hence the name is

unit root. (On p.802. of Gujarati (2003)) 19

The expression, “integration” comes by the analogy with calculus. As we can undo an integral by taking a

derivative, we say that a nonstationary series is integrated if its nonstationarity is appropriately undone by

differencing. (On p.289. of Diebold (2006))

11

Ⅱ-3. Multivariate Case: VAR, VECM, and Co-integration

Consider the following 2-dimensional second-order autoregressive process (x1t x2t)′:

x1t = π11,1 × x1,t−1 + π12,1 × x2,t−1 + π11,2 × x1,t−2 + π12,2 × x2,t−2 + c1 + ε1t , --- (Ⅱ-10)

x2t = π21,1 × x1,t−1 + π22,1 × x2,t−1 + π21,2 × x1,t−2 + π22,2 × x2,t−2 + c2 + ε2t . --- (Ⅱ-11)

These two individual equations can be expressed in the following matrix form:

xt = Π1xt−1 + Π2xt−2 + C + εt , --- (Ⅱ-12)

where xt = [x1t

x2t], Πp = [

π11,p π12,p

π21,p π22,p] with p = 1 or 2, C= [

c1

c2], and εt = [

ε1t

ε2t].

This equation is called a vector autoregressive (VAR) model. It can also be generalized to the

VAR(p) model.20

From (Ⅱ-12), we can derive the following equation:

xt − xt−1 = (Π1 − I)xt−1 + Π2xt−2 + C + εt

= (Π1 + Π2 − I)xt−1 − Π2(xt−1 − xt−2) + C + εt

= Πxt−1 − Π2(xt−1 − xt−2) + C + εt, --- (Ⅱ-13)

where Π = Π1 + Π2 − I.

As implied by (Ⅱ-13), we can write VAR(p) in the following vector error correction model

(VECM):21

Δxt = Πxt−1 + ∑ ΓiΔxt−ip−1i=1 + C + εt , --- (Ⅱ-14)

where Π = ∑ Πipi=1 − I and Γi = −∑ Πj

pj=i+1 .

Up to now, we have not discussed the stationarity problem of VAR model. However, similar with

univariate case, there are many VAR processes which are nonstationary. For example, consider the

following stochastic processes:

x1t = μt + ε1t, --- (Ⅱ-15)

x2t = μt + ε2t, --- (Ⅱ-16)

20

The use of VAR model in macroeconomics is strongly advocated by Sims (1980). 21

Engle and Granger (1987) and Johansen (1988) deal with this VECM approach.

12

μt = μt−1 + ε3t. --- (Ⅱ-17)

Given the dynamics of the above vector (x1t x2t)′, it is not stationary. That is, because μt is the

random walk without drift, xit with i = 1, 2 is not stationary. However, as in the univariate case, the

first-difference of the vector is stationary. Furthermore, μt functions as a common stochastic trend in

the processes of x1t and x2t. Therefore, x1t and x2t could have a long-run relationship. Simply

speaking, the information on this long-run relationship is contained in the matrix Π of (Ⅱ-14). In

literature, the variables which has long-run relationship among them is said to be cointegrated.22

23

Assuming Π = αβ′24 transforms (Ⅱ-14) into the following:

Δxt = αβ′xt−1 + ∑ ΓiΔxt−ip−1i=1 + C + εt . --- (Ⅱ-18)

When xt is 2-dimensional, the first-line equation is expressed as follows:

Δx1t = α1 × (β1 × x1t−1 + β2 × x2t−1 ) + ∑ Γ1,ip−1i=1 Δxt−i + c1 + ε1t. --- (Ⅱ-19)

The vector (β1 β2) is said to be a cointegrating vector which represents the long-run relationship

between two variables. The parameter α1 governs the adjustment speed of Δx1t for the deviation

from the long-run equilibrium, (β1 × x1t−1 + β2 × x2t−1). However, (β1 β2) is not unique. That is,

for nonzero k, (kβ1 kβ2) can also be a cointegrating vector. Therefore, some normalization is

required.

For example, from the model consisting of the equations, (Ⅱ-15) ~ (Ⅱ-17), consider the following

process:

zt ≡ x1t − x2t = ε1t − ε2t. --- (Ⅱ-20)

In this case, the cointegrating vector representing the long-run relationship is (1 -1). The deviation

from the long-run equilibrium is zt.

In summary, given that xt ~ I(1), if there is long-run relationship among the variables, which can

be represented by the cointegrating vector β, then β′xt~ I(0).

22

According to Watson (1994), the I(1) cointegrated model is represented in the following four ways: 1) VECM

representation, 2) moving average representation, 3) common trends representation, and 4) triangular

representation. 23

Regarding the cointegration, the spurious problem should be understood. For this problem, see “Technical

Appendix”. 24

The condition for the existence of such αβ′ is suggested on p.49. of Johansen (1995).

13

Ⅲ. Literature Review

Ⅲ-1. Literature on Forecasting in Other Fields Including Macroeconomics and Finance

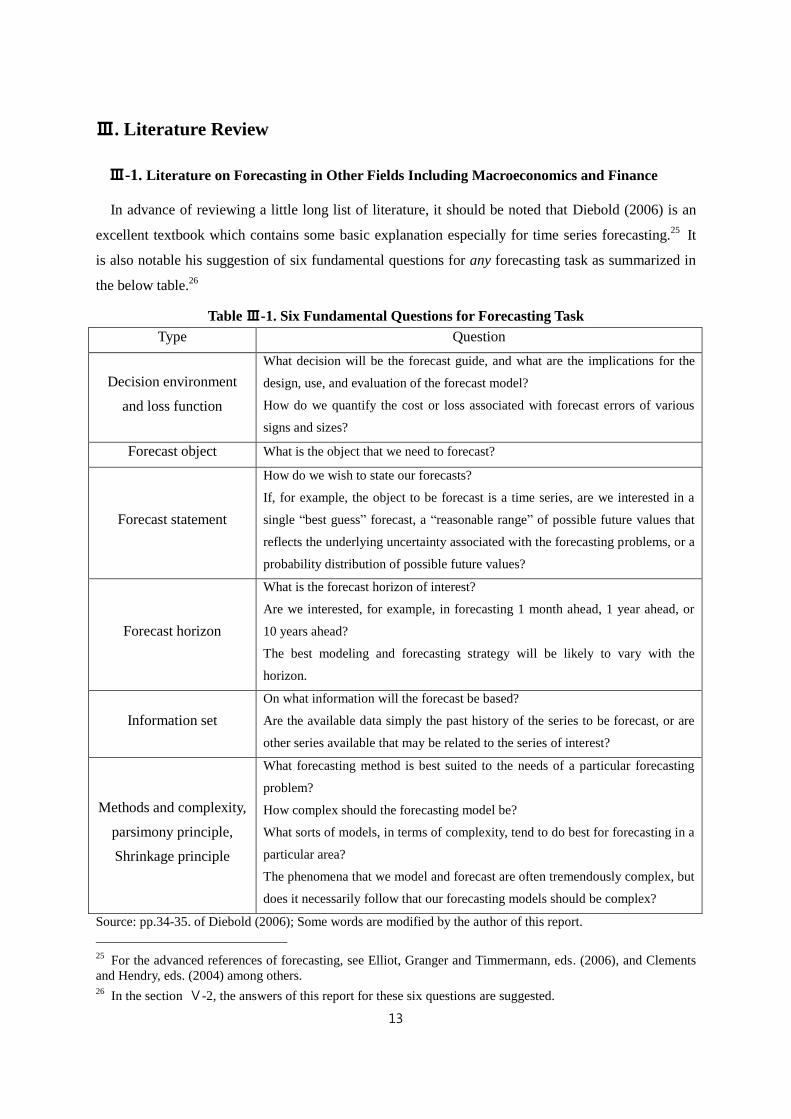

In advance of reviewing a little long list of literature, it should be noted that Diebold (2006) is an

excellent textbook which contains some basic explanation especially for time series forecasting.25

It

is also notable his suggestion of six fundamental questions for any forecasting task as summarized in

the below table.26

Table Ⅲ-1. Six Fundamental Questions for Forecasting Task

Type Question

Decision environment

and loss function

What decision will be the forecast guide, and what are the implications for the

design, use, and evaluation of the forecast model?

How do we quantify the cost or loss associated with forecast errors of various

signs and sizes?

Forecast object What is the object that we need to forecast?

Forecast statement

How do we wish to state our forecasts?

If, for example, the object to be forecast is a time series, are we interested in a

single “best guess” forecast, a “reasonable range” of possible future values that

reflects the underlying uncertainty associated with the forecasting problems, or a

probability distribution of possible future values?

Forecast horizon

What is the forecast horizon of interest?

Are we interested, for example, in forecasting 1 month ahead, 1 year ahead, or

10 years ahead?

The best modeling and forecasting strategy will be likely to vary with the

horizon.

Information set

On what information will the forecast be based?

Are the available data simply the past history of the series to be forecast, or are

other series available that may be related to the series of interest?

Methods and complexity,

parsimony principle,

Shrinkage principle

What forecasting method is best suited to the needs of a particular forecasting

problem?

How complex should the forecasting model be?

What sorts of models, in terms of complexity, tend to do best for forecasting in a

particular area?

The phenomena that we model and forecast are often tremendously complex, but

does it necessarily follow that our forecasting models should be complex?

Source: pp.34-35. of Diebold (2006); Some words are modified by the author of this report.

25

For the advanced references of forecasting, see Elliot, Granger and Timmermann, eds. (2006), and Clements

and Hendry, eds. (2004) among others. 26

In the section Ⅴ-2, the answers of this report for these six questions are suggested.

14

The papers reviewed in this section are all about 1) cointegration in VAR framework, 2) time-

variation of parameters, 3) Bayesian versus classical frameworks, 4) endogeneity problem, especially

correlation between the stochastic regressor and disturbance term, and 5) out-of-sample forecasting.

These issues are dealt with simultaneously in the individual paper. So, the sub-title leading to the

reviewed papers is only about the main topic, not the exclusive descriptive qualifier.

Cointegration in VAR framework

Stock and Watson (2001) show the usefulness of VAR model in forecasting macroeconomic

variables, while they argue that the VAR models have been proven to be powerful and reliable tools in

the jobs of data description and forecasting but have not been proven in the jobs of structural

inference and policy analysis.

De Mello (2009) argues that more structured VAR model could yield more accurate forecast of the

UK tourism expenditure shares for France, Spain and Portugal. Their following sentences are notable:

“When well specified, these models can provide not only a precise description of the data generating

process but also, and subsequently, accurate predictions for the values of the variable of interest. Thus,

the building of econometric models, even for the sole purpose of forecasting, must not disregard the

fundamental dimension of an appropriate formal specification. It is this dimension that allows

econometric models to provide reliable information for both explaining the past and predicting the

future”.27

Time-Variation of Parameters

Quintos and Phillips (1993) propose an approach to testing for coefficient stability in cointegrating

regressions of time series models. The considered test statistic is the one-sided version of the

Lagrange Multiplier (LM) test. Their null hypothesis is that there is cointegration. The basic notion is

that a test for the hypothesis that the long-run coefficient is constant can be interpreted as testing the

null hypothesis of cointegration. This notion leads to that, in the time-varying coefficient model, the

shock variance of the random work process for the coefficient dynamics should be zero under the null

hypothesis of cointegration. Though, as explained in Chapter Ⅱ, usually the cointegrating vector is

assumed to be constant, there is no a prior rationale for excluding the possibility of time variation of

cointegrating vector.28

Facing a lot of evidences for the absence of cointegration in economic variables, Park and Hahn

(1999) propose that there could be time-varying cointegration relationship. That is, there could be

27

This view point is almost the same for the structural models in the macroeconomic forecasting as explained

in Diebold (1998) or chapter 14 of Diebold and Rudebusch (1999). 28

This time variation in the cointegrating vector is the main property of the empirical model of this report.

15

parameter instability in the cointegration regressions. Their model is as follows:

yt = αt′ xt + εt, --- (Ⅲ-1)

αt = α(t

n), --- (Ⅲ-2)

where α is a smooth function defined on [0, 1] and n is the sample size.

They use the Fourier flexible form to approximate the smooth time-varying parameter

unparametrically. In order to illustrate the practical relevancy of their model, they consider the U.S.

automobile demand function. Using some test statistics, they argue that the cointegrated model with

time-varying coefficient is strongly supported by the data. In addition, they argue that, without

coefficient time variation, there could be mistakes as from the spurious regression problem.29

Zuo and Park (2011) apply the smooth time-varying cointegrating regression approach suggested

by Park and Hahn (1999) to the money demand analysis of China. They use the quarterly data from

1996Q1 through 2009Q1. Particularly, they show the properties of time-varying income, interest rate,

real stock price elasticities of money demand.

Similar to Park and Hahn (1999), Bierens and Martins (2010) consider the following time-varying

VECM representation:

Δxt = Πtxt−1 + ∑ ΓiΔxt−ip−1i=1 + εt . --- (Ⅲ-3)

Their objective is to test the null hypothesis of standard time-invariant cointegration with the

alternative hypothesis of time-varying cointegration. They approximate the dynamics of cointegration

time variation by using orthogonal Chebyshev time polynomials, which captures smooth time

transition of the cointegrating vectors. For estimation, they use MLE. As an empirical application,

they deal with the purchase power parity (PPP) theory.

Park and Kim (2009) apply the time-varying cointegration model to investigating the consequence

of the existence of firms which are not paying out dividends on the relationship between aggregate

dividends and stock price. In order to test the constant cointegration null hypothesis against the time

varying cointegration between the aggregate dividends and stock price, they employ the two test

methods. One is nonparametric which is suggested by Park and Hahn (1999). The other is parametric

which is suggested by Bierens and Martins (2010). Furthermore, for predicting stock returns,30

they

estimated a new predictor variable, which is stationary deviation from the time-varying cointegration

29

Spurious regression problem is that, when the relevant variables are I(1) and they are not related in fact, the

regression results could show that there seem to be statistically significant relationships. 30

Fama and Schwart (1977) is an early example of stock return prediction. In order to estimate the extent to

which various assets were hedges against the expected and unexpected components of the inflation rate during

the period 1953-1971, they use a kind of predictive regression model.

16

relationship between dividends and stock price.31

According to their analysis, this newly developed

variable has stable and strong ability to forecast stock returns from the out-of-sample analysis as well

as in-sample analysis.

Brown, Song and McGillivray (1997) consider the time-varying coefficient model with the

following form:32

yt = β1x1t + β2tx2t + εt, --- (Ⅲ-5)

β2t = β2t−1 + γzt + ω1t. --- (Ⅲ-6)

Regarding this time-varying coefficient model as a basic forecasting model, they also compare the

three different forecasting results of 1) recursive least square estimation, 2) cointegration approach

with constant parameter, and 3) VAR and AR estimation. In conclusion, they argue that the TVC

specification outperforms the alternative constant parameter specifications of UK house prices.

Bayesian versus Classical Frameworks

Sims (1993) applies the time-varying parameter model in the Bayesian framework to forecasting

macroeconomic variables. Particularly, it is evaluated so that it produces drastically better forecasts of

the price level variable than the previous Bayesian VAR model.

Using a Bayesian model averaging approach, Dangl and Halling (2011) apply predictive regression

model with the time-varying coefficients to financial data, for example, monthly S&P 500 index.

Especially, regarding the predictability problem, they conclude that there are statistical and economic

evidence of out-of-sample predictability: relative to an investor using the historic mean, an investor

using their methodology (a kind of Bayesian averaging approach with time-varying coefficients)

could have earned consistently positive utility gains (between 1.8% and 5.8% p.a. over different time

periods). They also argue that predictive models with constant coefficients are dominated by models

with time-varying coefficients. In this paper, it is notable that the poor performance of regime-

switching model for out-of-sample forecasting is due to the unreliable estimates of the timing of

breaks and of the size of the shift in real-time context.33

Also, they mention that the coefficient

variation can stem from the changes in market sentiment, which property is presumed to be the main

cause of the coefficient variation of this report. Finally, as in this report, they model the dynamics of

the coefficients as a random walk process.

31

When deriving this deviation, they use the time-varying cointegration regression approach of Park and Hahn

(1999). 32

The variable zt of (Ⅲ-6) is called as “driver variable”. 33

This point is originally suggested in Lettau and S. Van Nieuwerburgh (2008).

17

Koop, Leon-Gonzalez and Strachan (2011) point out that both economic theory and empirical

reality need a time-varying parameter vector error correction model (TVP-VECM) comparable to the

TVP-VAR.34

However, while there are a large number of theoretical and empirical papers that model

the nonlinearity in cointegrating relationship, as they argue, this effort is non-Bayesian with few

exceptions. So, they aim to develop Bayesian methods for TVP-VECM.

Particularly, they consider the following kind of TVP-VECM:

Δxt = αtβt′xt−1 + ∑ Γi,tΔxt−i

p−1i=1 + ct + εt , --- (Ⅲ-4)

where εt are independent N(0, Ωt).

However, the time-varying cointegrating space is modeled as similar to stationary AR(1) process by

using the methods from the directional statistics literature. They point out that this kind of stationarity

condition of the cointegrating space is necessary to ensure the property that “the cointegration space

today has a distribution that is centered over last period’s cointegrating space”.35

They also note the

problem that, if the cointegrating space is a random walk process, the cointegrating vector would

wander far from the origin.36

However, in their specification, the expected value of cointegrating

space at time t equals the cointegrating space at time t-1.

Regarding the notion of cointegration, their following remark is notable:

We note that cointegration is typically thought of as a long-run property, which might suggest a

permanence which is not relevant when the cointegrating space is changing in every period.

Time-varying cointegration relationships are better thought of as equilibria toward which the

variables are attracted at any particular point in time but not necessarily at all points in time.

These relations are slowly changing. (On p.212. of Ibid.)

As an empirical application, they consider the Fisher effect by using UK quarterly data. Importantly,

they argue that, instead of finding support for or against an economic hypothesis, we can conclude

that it (economic theory, i.e., Fisher effect hypothesis) holds at some points in time, but not others.

Also, they show that allowing for time-variation only in the cointegrating space and error covariance

matrix yields the best empirical model.

34

In their paper, as usually done in TVP-VAR, all the coefficients of VECM except the cointegration

coefficients are assumed to follow the random walk if they are time-varying. 35

It is notable that this property is desired in specifying random walk evolution for VAR parameters of TVP-

VAR molel. 36

This problem is applied to the model of this report. Since this report does not develop an econometric theory

on the suggested time-varying cointegration coefficients with random walk dynamics, the associated statistical

properties should be analysed for more rigorous inference. So, this econometric development will be an

important future research topic.

18

When forecasting as in this report, we presumably think that the true conditional expected value of

dependent variable is equal to the regression-based conditional mean. This is true if the predictor

variables are perfect in the sense that the equality should hold. However, in reality, there seem to be a

large number of cases where the equality does not hold. Facing with this problem, Pastor and

Stambaugh (2009) propose a Bayesian solution, which is called as “predictive system” compared to

the usual “predictive regression”.37

They argue that their proposed Bayesian “predictive system”

approach allows us to conduct clean finite-sample inference about various properties of the expected

value.

In the case in which the endogenous variables are given as the point values or some interval for

conditional forecasting, there had been no method of computing the exact finite sample distribution of

conditional forecast. Waggoner and Zha (1999) provide a solution to this problem by using Bayesian

methods. Also, this paper considers the issue of parameter uncertainty. In order to derive the finite-

sample distribution of conditional forecasts, they use two algorithms. One is for the hard conditions,

where the future values of variables are fixed at some points. The other is for the soft conditions,

where the future values of variables are restrained over some interval.38

Endogeneity Problem (Correlation between the Stochastic Regressor and Disturbance Term)

Stambaugh (1999) deals with a kind of endogeneity problem in predictive regression method.

Particularly, when there is correlation between the stochastic regressor and the disturbance term, it

shows that the p-value with conventional significance level, e.g., 5%, under the classical framework

would makes us to accept a null hypothesis but the posterior distribution under the Bayesian

framework has lower probability that the null hypothesis holds than 5%. That is, this paper attempts to

show the differential properties of classical and Bayesian approaches.

Similar to the motivation of Stambaugh (1999), Kim (2006) considers the endogeneity problem in

the case in which there exists correlation between the stochastic regressor and the disturbance term.

However, the model considered in Kim (2006) is the time-varying parameter model. In order to

appropriately handle the endogeneity problem, he derives a Heckman-type two-step approach.39

Also,

the conventional Kalman filter is applied to the regression equation by implementing appropriate bias

correction terms obtained from the first-step regression. With this proposed two-step approach, we can

obtain consistent estimates of the hyper-parameters of the model and the conventional Kalman filter

37

In this terminology, when the predictors approach perfection, the system-based conditional expected value

approaches the regression-based conditional mean. 38

Since the sample of this report is relatively small, this method, which provides the exact finite-sample

distribution of conditional forecasts for time-varying parameter multivariate model (e.g., VAR) by using

Bayesian approach, will be very helpful for the improvement of the forecasting task which uses the model of

cointegration regression with time-varying coefficients. However, this topic remains as a future research subject. 39

Heckman (1976).

19

provides us with correct inferences on the time-varying coefficients.

Kim and Nelson (2006) apply this Heckman-type two-step approach to investigating the history of

the U.S. Fed’s conduct of monetary policy. As a result, contrast with the conventional division of the

sample into Pre-Volcker and Volcker-Greenspan periods, they divide the history since the early 1970s

into the 1970s, the 1980s, and the 1990s.

Out-of-Sample Forecasting

In this report, the forecasting performance is evaluated under the so-called out-of-sample context.

Regarding this out-of-sample exercise, Hjalmarsson (2006) provides important information by using a

simple Monte Carlo experiment. According to its argument, similar out-of-sample results to those of

Goyal and Welch (i.e., no predictive gains of virtually all variables that have been proposed as

predictors of future stock returns)40

are found even when the postulated forecasting model is in fact

the true data generating process. This is thought of as due to the fact that any predictive component in

stock returns must be small, if it does exist. So, in order to accurately estimate a very small coefficient,

large amounts of data are needed. That is, when testing for stock return predictability, the sample sizes

in most relevant cases are too small relative to the size of the slope coefficient for any predictive

ability to show up in out-of-sample exercises. In summary, it argues that we should not disregard the

econometric in-sample results in favor of out-of-sample results.

Ibrahim and Florkowski (2007) compare the out-of-sample forecast performances among 1)

univariate ARIMA, Engle-Granger two-step,41

Johansen’s models42

by using the monthly U.S. time

series data set for the period from 1991 to 2004. According to their results, ARIMA models seem to be

useful for short-term forecasts, but for longer-term forecasts the cointegration technique seems to be

useful.

40

Goyal and Welch (2003) and Goyal and Welch (2004). 41

Engle and Granger (1987). 42

Johansen (1998).

20

Ⅲ-2. Literature on Forecasting Dry Bulk Freight Rate43

Alizadeh and Nomikos (2010) provide a comprehensive review on the subject of structure, dynamic

properties, and the relationships in the dry bulk sub-markets which can be classified by size into Cape,

Panamax, and Hany-class markets and by relevant activity into freight markets (spot versus time-

charter markets), newbuilding, secondhand ship, and demolition markets.

Using Forward or Futures Variables44

Alizadeh and Nomikos (2003) show that market participants can get more accurate forecasts of

freight rates by using FFAs rather than BIFFEX (Baltic International Freight Futures Exchange for

trading freight futures contracts with settlement based on the Baltic Freight Index) contracts, in which

they consider the 2 Panamax routes and 2 Capesize routes.

Similar with Kavussanos and Nomikos (2003),45

Batchelor, Alizadeh and Visvikis (2007) apply

various time series models of ARIMA, VAR, VECM, S-VECM (Seemingly unrelated regression

equations VECM) to investigating the relationship between the Panamax spot rates and FFA rates and

then forecasting these variables. The considered routes are Panamax Atlantic routes 1 and 1A whose

daily sample is 16. Jan. 1997 to 31 July 2000, and Panamax Pacific routes 2 and 2A whose sample

period is 16. Jan. 1997 to 30 April 2001.46

47

They take the hypothesis that, if the forward market is liquid enough to embody some information

about futures spot rates into the forward prices, we should observe cointegration between them, and

convergence of spot towards forward rates, rather than vice versa. Indeed, according to their test

results for the cointegration relationship, the spot and FFA prices are cointegrated in all routes. Also,

across all routes the adj-R2 for changes in spot rates are higher than those of forward rates, indicating

potentially higher predictability in spot rates than forward rates.48

But in the respect of adjustment

43

Even though a large number of researchers try to insist that their (empirical) findings could apply to the

course of future events, the fact that their results should be based on the past events, not on the future ones,

could imply limitation of their usefulness for the forecasting purpose. This aspect would require that we should

cautiously review the literature focusing on the data set. 44

Regarding FFA, there are some interesting researches. Using the so-called GJR-GARCH model (suggested in

Glosten, Jagannathan and Runkle (1993)), Kavussanos, Visvikis, and Batchelor (2004) examine the impact of

FFA trading on spot market price volatility in Panamax market. Using VECM-GARCH model, Kavussanos and

Visvikis (2004) investigate the lead-lag relationship in daily returns and volatilities in Panamax market. 45

In contrast, Kavussanos and Nomikos (2003) deal with BIFFEX rates. 46

The former sample is ended earlier than the latter one because, after 31 July 2000, the FFA brokers stopped

publishing the relevant FFA quotes, which is the data source. 47

The data sources are as follows: For spot rate, it is the Baltic Exchange and for FFA rate it is collected

manually from the records of Clarkson’s Securities Ltd. 48

The highest adj-R2 is 0.5892 for spot rate and 0.0715 for FFA rate, respectively. This relatively low adj-R2

could imply there is some omitted variables in the regression equations. So, regression equations with more

variables are required so that, first, the resulting adj-R2 will increase and thus our perception of the relevant

shipping markets will be improved.

21

speed, contrary to their expectation, forward rates adjust more strongly than spot rates in three of the

four routes.49

However, out-of-sample forecasting with the VECM models shows that they are not

helpful in predicting forward rate behavior, but do help predict spot rates, which is more consistent

with market efficiency.50

Alizadeh, Adland and Koekebakker (2007) examine whether the 6-month implied forward time

charter (IFTC) rate is an unbiased predictor of future TC rates. The data set is weekly and its sample

period is 1 Jan. 1989 to 27 June 2003. The considered ship sizes are 1) Capesize (127,000 DWT), 2)

Panamax (65,000 DWT), 3) Handymax (40,000 DWT).51

The IFTC is calculated in the following way: At time t, there are two separate TC rates, i.e., 6-

month and 12-month TC rates. Based on the present value model and efficient market hypothesis

(EMH), the expectation of 6-months ahead 6-month TC rate can be calculated, which is the same as

the IFTC.

As one of the tests of unbiasedness, the cointegraion approach requires that the IFTC at 6-month

early time and present TC should be cointegrated. According to their test results, we cannot reject the

cointegration relationship at any significance level.

However, apart from the unbiasedness, EMH could imply that IFTC should provide “the most

accurate forecast for the future values of TC rates amongst all competing forecast methods”. With

regard to this predictability, there are some contradicting empirical results. First, Based on RMSE

metric and Theil’s U statistic,52

the comparisons of the forecasting performance with those of ARIMA,

VAR, and VECM models show that IFTC provides the most accurate forecast, which is in line with

the notion of the EMH in freight rate formation. But, based on the simple chartering strategy, MA

strategy, there has been economically significant excess profit. Although this fact could imply that

there has been a time-varying risk premium, it also implies that there has been “predictable mispricing

of the implied forward freight rate”. This would imply that the market is inefficient. So, we could

conclude that the validity of the unbiasedness hypothesis, in the context of the term structure of

freight rates, is a necessary but not sufficient condition for the EMH to hold.

Additionally their following result is notable: The market forecasts a future 6-month TC rate that is

too low during upturns in the freight market. This bias implies that, based on the unbiasedness, the

market must forecast a future 6-month TC rate that is too high during market downturns.

49

In this regard, they note the dangers of forecasting with VECM when the underlying market is evolving and

the parameter estimates conflict with sensible theoretical priors. This caution about the evolution of market is

reflected in this report in the sense that the time-variation of parameters could incorporate the information on the

market evolution. 50

In contrast to Kavussanos and Nomikos (2003) with overlapping forecast intervals, Batchelor, Alizadeh and

Visvikis (2007) use the “independent out-of-sample N-period ahead forecasts” as suggested in Tashman (2000). 51

The data source is Clarkson’s Shipping Intelligence Network (SIN). 52

These two formulas are popular tools used for the evaluation of forecasting model. For example, for RMSE

(root mean squared error) metric see p.261 of Diebold (2006) and for Theil’s U statistic see p.324 of Ibid.

22

Kavussanos, Visvikis and Menachof (2004) consider the unbiasedness in the freight forward market.

In their introduction, there are two notable remarks, one is about the nature of forward freight market

and the second is about the purpose of investigating the unbiasedness hypothesis.

First, they explain the nature of forward freight market as follows: “The non-storable nature of FFA

market implies that spot and FFA prices are not linked by a cost-of-carry (storage) relationship, as in

financial and agricultural derivatives markets. Another feature of this derivative OTC market is the

asymmetric transaction costs between spot and FFA markets. These costs are higher in the spot freight

market (in relation to the FFA market), as it is the case for commodity spot versus futures market”.

Second, the purposes of investigating the unbiasedness hypothesis are as follows:

First, the underlying asset is a service. Second, the price discovery function provides a strong

and simple theory of the determination of spot prices that may prevail in the future. Third, if

forward prices fulfill their price discovery role, they provide accurate forecasts of the realized

spot prices, and consequently provide new information in the market and in allocating economic

resources (Stein (1981)). Decisions in the physical market are thus facilitated and can help

secure market agents’ cash-flow (transportation costs). … However, it must be noted that

market agents can initiate trade for several motives, such as heterogeneous expectations or

heterogeneous income/cost structures (Calvet, Gonzalez-Eiras and Sodini (2004)). Finally, the

apparent lack of research in the freight forward trades further motivates this investigation as

this is the only derivative instrument available to agents in the bulk shipping industry for

hedging purposes. Evidnece on whether agents in the shipping industry can use FFAs of

different maturities and for different routes, as unbiased predictors of spot freight rates, is very

important and provides a free source of information for decision-making. (On pp.243-244. of

Ibid.)

Their data set are monthly FFA and spot rates. The sample period is 1996:01 to 2000:12. The

considered routes are Panamax 1, 1A, 2, and 2A. For FFA variable, the average (mid-point) of bid and

offer quotes is used.53

FFA rate is from Clarkson Securities and spot rate is from Datastream.

The unbiasedness hypothesis is examined by testing the restrictions β1 = 0 and β2 = 1 in the

cointegration relationship β′xt = (1 β1 β2)(st−1 1 Ft−1,t−n−1′) where S is spot rate, F is FFA rate

and n is considered maturity. If these restrictions hold, then the price of the FFA contract is an

unbiased predictor of the realized spot price. According to their results, for the one- and two-months

53

We can get the Baltic assessment of FFA rates since Aug. 2005. This assessment data set could function as the

“best” daily price for forward (or futures) prices of dry bulk freight rate. However, when there has not existed

this data set, Kavussanos, Visvikis and Menachof (2004) say that, owing to the absence of this reliable data set,

it is more difficult to investigate whether derivatives prices informationally lead spot prices in the shipping

market than in organized futures exchanges. (See p.243. of Ibid.)

23

FFA prices, and for route 2 and 2A three-months FFA prices, the unbaiasedness hypothesis cannot be

rejected at conventional levels of significance. So, for the investigated routes and maturities for which

the unbiasedness holds, market agents can use the FFA prices as indicators of the future course of spot

prices in order to guide their physical market decisions.

Regarding the error correction coefficient (adjustment speed), both spot and FFA prices respond to

the long-run equilibrium in the one-month maturity, while in the two- and three-months maturities

only FFA prices respond to the previous period’s deviations from the long-run equilibrium

relationship. This finding is consistent with the hypothesis that past forecast errors affect the current

forecasts of the realized spot prices, i.e., FFA prices, but not the spot prices themselves.

Similar to Batchelor, Alizadeh and Visvikis (2007), Kavussanos and Nomikos (2003) apply various

time series models of ARIMA, VAR, VECM and random-walk models to investigating the

relationship between the Panamax spot rates and futures (BIFFEX)54

rates and then forecasting these

variables. The considered main issue is that, due to the non-storable nature of the shipping market,

spot and futures prices would not linked by a cost-of-carry relationship, and hence futures prices may

not contribute to the discovery of new information to the same extent as the markets for storable

commodities.55

For tackling this issue, they use the daily data set. Their sample period is 1 Aug. 1988 to 30 April

1998. The spot rates are from LIFFE (London International Financial Futures Exchange) and futures

are from Knight Ridder, Financial Times, and LIFFE.

Their major findings can be summarized as follows:

First, spot and futures prices stand in a long-run relationship between them.: hence, a VECM

can be used to investigate the short-run dynamics and the price movements in the two markets.

Second, causality tests and impulse response analysis indicate that futures prices tend to

discover new information more rapidly than spot prices. This pattern is thought to reflect the

fundamentals of the underlying asset since, due to the limitations of short-selling the underlying

spot index, investors who have collected and analysed new information would prefer to trade in

the futures rather than in the spot market. Third, information from the futures prices can be

used to generate more accurate forecasts of the spot prices but not the other way round. This

reflects that causality from futures to spot runs stronger than the other way and that most of the

variability in the futures returns is attributed to pure innovations which cannot be predicted.

54

In contrast, Batchelor, Alizadeh and Visvikis (2007) deal with FFA rates. 55

As Garbade and Silber (1983) is suggested as a reference, Kavussanos and Nomikos (2003) note that the

primary benefits of futures markets to economic agents are price discovery and risk management through

hedging. Price discovery is the process of revealing information about the future spot prices through the futures

markets. Risk management refers to hedgers using futures contracts to control their spot price risk. The dual

roles of price discovery and risk transfer provide benefits that cannot be offered in the spot market alone and are

often presented as the justification for futures tradeing. (On. p.203. of Ibid.)

24

Finally, the price discovery role of futures prices has strengthened in the period after the

exclusion of the handysize routes from the BFI: this is thought to be the result of the more

homogeneous composition of the index for this period. Overall, despite the non-storable nature

of the market and the thin trading, futures prices contribute to the discovery of new information

in the spot market, as in the case of other commodity and financial futures market. (On p.225. of

Ibid.)

Given that the above literature which shows that the futures, forward or implied freight rates could

inform the market participants of the course of future rates, the naturally resulting question will be

“Even though we can anticipate the future course of the spot rates with the futures, forward or implied

freight rates, at first without themselves, how can we predict the spot rates or themselves?”56

Freight Rate Determination Mechanism Model

Rim, Kim and Ko (2010) analyse the dynamic interrelationship among the demand, supply and

freight rate variables in the dry bulk market. For the empirical tool, they use a recursive VAR model.

The data set includes BDI, cargo volume and fleet capacity, which are similar to that of this report

except that this report adds the FFA assessment variable. While they don’t tackle the problem of

forecasting, their VAR model could be used as a forecasting tool.

The consecutive papers of Chung and Ha (2010b) and Chung and Ha (2010a) should be noted. Both

of them consider the China’s iron import, 3-month Eurodollar interest rate, and U.S. industry stock

price index as the explanatory variables for BDI. The first variable reflects a direct shipping demand

of China, the second is a proxy for the international financial condition which can influence the global

macroeconomic cycles, and the third shows whether U.S. economy is in the phase in boom or

recession. Particularly, Chung and Ha (2010b) show that there has been a cointegration relationship

between the BDI and the aforementioned explanatory variables by using the Pesaran’s cointegration

method and Chung and Ha (2010a) investigate the structural changes in the relationship between the

same variables by using the Kalman filter.

Importantly, the model structure of Chung and Ha (2010a) is the same as that of this report in that

both of them consider the time-varying coefficient model for the determination mechanism of dry

bulk freight rate. However, they differ substantially in the use of explanatory variables and thus the

relevant theory for the underlying economic shipping market. Moreover, this report considers both of

the freight rate determination mechanism and its forecasting performance, while Chung and Ha

(2010a) considers only the former theme, i.e., the freight rate determination.

56

This question shows the reason why this report considers the demand/supply model.

25

Forecasting Using VAR Model

Veenstra and Franses (1997) apply a VEC model to forecasting the freight rates of Capesize and

Panamax ships. They argue that the fact that the specification of the long-term relationship defined in

the VEC model does not improve the accuracy of short- or long-term forecasts can be interpreted as a

corroboration of the efficient market hypothesis.

Alternative Freight Rate Forecasting Methods Including Non-Linear Models

There have been some efforts to forecast dry bulk freight rate by using alternative methods to linear

regression approach.

Chang, Hsieh and Lin (2012) propose a non-linear regression model for the prediction of Capesize

dry bulk freight rate by using monthly data set of Clarkson. They use the exponential function for

finding the relationship between the market variables and time period, which is their nonlinearity. By

treating the secondhand ship prices as explanatory variable after some selection procedures, they

show the extent of prediction accuracy based on in terms of MAPE (Mean Absolute Percentage Error).

However, they don’t consider the nonlinearity in the relationship between the freight rate and

explanatory variables.57

Zhongzhen, Lianjie and Minghua (2011) apply the wavelet transform and support vector machine

combined model to forecasting BPI (Baltic Panamax Index) using the monthly average of BPI from

Jan. 2001 to May 2009. They insist that the proposed model has a very high goodness of fitness,

particularly in the peak and trough.

Veenstra and van Dalen (2011) suggest an interesting conjecture that brokers’ estimates58

add

something to a time series and this guesstimate may reflect the term structure model which exists in

the minds of the brokers, but perhaps not in practice. For this argument, they construct the weighted

unit value indices and duration indices59

solely based on actual fixtures which have been obtained

from Maritime Research Inc. (MRI) in the U.S.A. Furthermore, they argue that their duration indices

contain more information than the unit value indices or brokers’ estimates such as those of the Baltic

Exchange and Clarkson.

Similarly, while pointing out that many of popular freight rate time series do not reflect cost of use

or average charter levels in the market of new and existing contracts, Gratsos, Thanopoulou and

Veenstra (2012) show the stable relationship between contract duration and freight level. They argue

57

Their sample period is from Nov. 1995 to Sep. 2008, which excludes the period after 2008 global financial

crisis. Since they cannot consider the parameter change from the collapse of dry bulk markets of the crisis, their

nonlinearity model could not explain this post-crisis phenomenon. 58

When, for a specific commodity or route, there are no actual contracts reported, the Baltic Exchange indices

or Clarkson’s indices are completed based on brokers’ estimates. 59

The basic rationale for the duration indices is that the freight rates of both the newly concluded contracts and

the running fixtures are part of the economic reality and should therefore be included in the index construction.

26

that, while the shipper wishes to control the transport cost over a long period of time and/or encourage

the construction of bigger ships by using long-term period charters, the shipowners disagree that the

freight rates remain at low levels at a time of ample supply of tonnage like 1998 to 2003 owing to

long-term contract. This kind of argument is interpreted as suggesting that the incorporation of

contract duration is necessary for the improvement in accessing and forecasting the dry bulk freight

rate.

It is notable that Goulielmos and Psifia (2009) suggest an alternative approach to forecasting

weekly freight rates for one-year time charter 65,000 DWT bulk carrier. As analytical tools, they use

Rescaled Range Analysis, the related Hurst Exponent, Power Spectrum Analysis, V-statistic and BDS

Statistic. By nature, these tools are non-linear. They argue that this kind of non-linear analysis is

superior in forecasting vis-à-vis GARCH.

Although the analyzed market is the tanker one, there have been some efforts using Artificial

Neural Networks (hereafter ANN). First, Li and Parsons (1997) apply the ANN model to the tanker

market based on the monthly data set consisting of dirty tanker spot rate, tanker demand and the

tanker supply from January 1980 to October 1995. Second, Lyridis, Zacharioudakis, Mitrou, Mylonas

(2004) also apply the ANN model to the tanker market based on the monthly sample from October

1979 to December 2003. This ANN model is considered as a powerful tool for complex time series

data set because it can reflect the unstable relationships among the independent and dependent

variables.

Dikos, Marcus, Papadatos, Papakonstantinou (2006) apply a system-dynamics approach60

to tanker

freight modeling, While their method of system dynamics captures the essential features of several

shipping-industry situations, it also provides a powerful tool for evaluating managerial decisions and

what-if scenarios. Randers and Goluke (2007) also report the research efforts using the system

dynamics in tanker market. According to their results, the system dynamics succeeded in forecasting

turning points in the relevant shipping freight markets.

60

In comparison, Engelen, Dullaert, Vernimmen (2009) use a system dynamics method to assess the Efficient

Market Hypothesis (EMH) in the dry bulk shipping market.

27

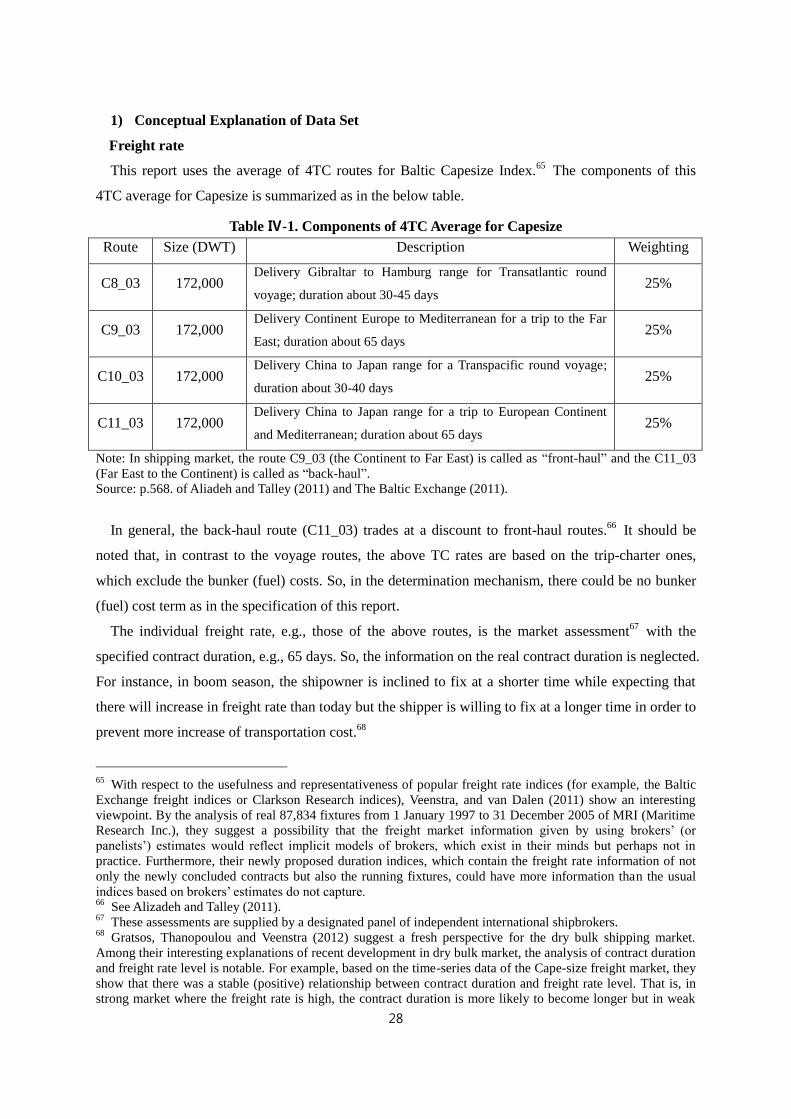

Ⅳ. Data and Time-Varying Coefficient Model

Ⅳ-1. Data

Explanation of data set would be given after the introduction of the underlying economic model.

However, in the dry bulk shipping industry, the availability of data is somewhat limited partly because

there is no public entity with enforcement power which can collect the relevant information such as

the tonnage supply, seaborne transport demand, port congestion, lay-up ships, etc. These data are

gathered basically by the private organization. Therefore, the limitation of data set imposes the

constraint on the structure of the economic model for dry bulk freight market.61

As a result, the author

firstly introduces the data set used in this research.vii

This report aims to forecast the Cape-size dry bulk freight rate in so-called macro level.62

Usually,

the freight rate can be considered differently across the time span.63

For example, if the shipowner

expects that the future freight rate will increase, then he wants to fix a shorter-term contract (e.g.,

voyage or trip-charter contract). In the opposite case, he will try to fix a longer-term contract (e.g.,

Contract of Affreightment). However, this report deals with the freight rate, supply, demand and FFA

assessment at the monthly frequencies, hence this report is useful for the freight rate risk management

based on the monthly period.64

For example, many of the popular derivatives of dry freight rate based

on the Baltic Exchange indices are traded by using the settlement prices of the monthly average. In

addition, this time domain of this report is due to the fact that the supply/demand variables can be

observed on at least monthly basis.

61

This problem of data quality in the shipping market is not unique. The famous high-quality macro data, GDP,

is also related with this kind of data quality problem. Furthermore, from this problem, we cannot assess exactly

the performance of forecasting model. Stopford (2009) quotes the following sentence of M. Baranto: ‘The

analysis of forecasting errors is not a simple process – ironically it is as difficult as making forecasts’. This

means that care is needed to produce forecasts that are capable of being monitored quickly and easily by users.

(See p.741. of Ibid.) 62

In contrast, Alizadeh and Talley (2011) analyse the freight rate determination in micro level. So, it can be said

that the identification of the significant level of detail to work at is a very important issue. In theory more

information should lead to a more reliable result. However, the danger is that it is very time-consuming and can