Embed Size (px)

Citation preview

S t r a t e g y & P o l i c y

JetBlue Airways Corporation Case Analysis Chen Chen, Kathie Chang, Katelyn Foster, Anthony Hwang, Daniel Kang, Bion West, Shing Yip

Fall 10

08 Fall

2

Introduction

JetBlue Airways Corporation is a low-cost American airline. The company is headquartered in Forest Hills,

Queens in NYC with its main hub at John F. Kennedy International Airport. David Neeleman, founder of JetBlue,

along with several former colleagues from Southwest Airlines incorporated the company in 1999. They followed

Southwest’s approach of offering low cost travel but distinguished the airline through amenities such as in-flight

entertainment, including televisions with DIRECTV. In 2007, JetBlue was named the number one U.S. domestic

airline by Conde Nast Traveler magazine’s “Reader’s Choice Award” for the sixth year in a row (JetBlue). However,

in order to stay competitive in the domestic low carrier industry, JetBlue will need to analyze the external threats and

build upon existing value-adding activities to maintain a sustainable competitive advantage over its competitors.

External Analysis

Threat of new entrants

In the domestic airlines industry, there are high barriers to entry and high-expected retaliation from

incumbents. One significant entry barrier is the large capital requirements for new entrants. JetBlue’s initial

investment was $130 million and its airport expansion into JFK cost JetBlue $80 million. Operating expenses—

including labor, fuel, insurance, and maintenance costs—are also very high. Financing the capital requirements is

difficult for young entrants. Incumbents also contribute to high entry barriers because of their upper hand in brand

equity, flight routes, and industry knowledge. By having access to hubs in metropolitan areas (e.g. JFK), certain

airlines gain exposure to a greater market share than others. Most incumbents have been in the industry for many

years and have gained expansive knowledge and experience of the business giving them an edge over their

competitors.

Retaliation from incumbents is also high. There are resource-rich competitors who are willing to leverage

their company’s finances and excess aircraft capacity to compete aggressively with new entrants. Initiatives to push

out new competition may include operating in the flights operated by younger opponents. The combination of high

barriers to entry and high likelihood of retaliation from incumbents creates an environment with low threat to entry.

Bargaining power of customers

3

The bargaining power among customers can be classified as high. Domestic airlines industry customers can

be categorized into two groups: leisure travelers and business travelers. There are low switching costs for these

consumers because they are free to switch from one airline to another, at the cost of losing “frequent flyer” miles. In

addition, all airlines offer a relatively standardized service focusing on taking customers from one location to another.

Although companies may strive to distinguish their services through a mixture of cost cutting, on-board-services, and

marketing campaigns, they all fulfill the same objective.

The availability of substitute products also increases the bargaining power of customers. This is because

the demand for airline services is different for leisure and business travelers. For long-distance travel, both leisure and

business travelers have no alternatives to flying. However, for short and medium-distance travel, leisure and business

travelers exhibit different preferences in their choice of travel medium. Leisure travelers are more willing to use

substitute products such as driving or taking the train to reduce cost since short travel time is not their main concern.

This gives them more bargaining power against airline companies. Because reducing travel time is the number one

priority for business travelers, it significantly reduces their bargaining power. However, we believe that the decreased

bargaining power from this specific niche is not enough to lower the overall rating.

Bargaining power of suppliers

The bargaining power of suppliers is high. There are several key suppliers in the domestic airlines industry.

The first and most expensive source is the labor force. Skilled pilots, flight attendants, and crewmembers make up the

majority of the labor required for airlines. The second and third most expensive suppliers are the fuel suppliers and

aircraft manufacturers respectively.

Because fuel is a commodity, its suppliers are not concentrated. However, labor force and aircraft

manufacturer suppliers are. Because over 60% of the labor force in the airlines industry is unionized, there exists a

large influence over employers concerning union members’ job securities. The presence of a union also creates a

barrier for airlines to downsize their workforce. The aircraft manufacturers are primarily concentrated between the

two largest players—Airbus and Boeing— making the aircraft manufacturing industry a duopoly and a very

concentrated supplier market.

4

There are no substitutes for fuel. All airlines must buy fuel at market price despite the increase in cost.

According to the FAA (Federal Aviation Administration), the cost of jet fuel rose by “20.1 percent in 2004, 40.5

percent in 2005, and 30.4 percent in 2006” (Hitt 212). These increases in cost cut the airlines’ profit margins by

enormous amounts – for every $1 increase in price for a barrel of fuel, the industry experiences a $450 million loss in

pretax profits (Hitt 212). Alternative energy options such as liquid coal can become a potential substitute in the

future, however, its slow development nullifies its viability as a substitute for fuel.

Rivalry among existing competitors

A high level of rivalry within the industry can be attributed to several factors. The high exit barriers make

leaving the industry very unattractive. Airplanes make up a large portion of an airline’s capital expenditure and will

only result in receiving salvage value in any future sale. Furthermore, the specific requirements for commercial

airliners limit any potential use in other industries such as the Aerospace sector. Despite the trend of airline

consolidation, there are still numerous competitors in this industry (43 mainline carriers and 79 regional carriers).

The slow growth within the industry and excess capacity has led airlines to engage in intense campaigns to try to

attain customers from their competitors.

In terms of competition based on price, the airlines face the issue of servicing a perishable product where

unfilled seats during flights result in unrecoverable losses in revenue. Traditional airlines have been discounting their

prices to avoid flying with empty seats and to compete against low-cost carriers. Filling an empty seat comes at a

minimal marginal cost to the airline, which further incentivizes these companies to cut fares in order to spur demand

for their service. Because rivalry is intense and competition is largely based on price, rivalry within the domestic

airlines industry is high.

Threat of substitute products or services

Substitutes to flying include traveling by car, bus, train, bicycle, walking, or not traveling at all. Although the

number of corporate customers who traveled by plane decreased after September 11, 2001, the trend began to reverse

just five years later. In 2006, 65% of corporations expect employees to travel more and 75% expect an increase in

business travel (Hitt 213). This trend lowers the threat of substitutes for that specific niche of business patrons.

5

For the leisure traveler, substitutes can look more attractive compared to air travel in case of low

discretionary income, natural disasters, bad weather, terrorist activity or changes in other macroeconomic variables.

In addition, leisure travelers are more price-sensitive than their business counterparts resulting in lower demand

within this market segment. This increases the threat of substitute services for leisure travelers. Since the threat of

substitute services is high for business travelers and low for leisure travelers, there is a medium level of threat of

substitute services.

External Analysis Conclusion

The attractiveness of an industry is based on the overall profitability of all incumbents within the industry as

well as conclusions drawn from a Porter’s Five Forces analysis. Exhibit 5 shows that five of the seven U.S. major

airlines listed were profitable in the fiscal year 2006. Delta was the least profitable with losses of $6.22 million and

UAL was the most profitable with profits of $22.4 million. Although some airlines struggled to breakeven and have

filed for bankruptcy in the past, most have managed to be profitable. Our analysis of Porter’s Five Forces concludes

that the U.S. airlines industry has a low threat of new entrants, high bargaining power of customers, high bargaining

power of suppliers, high rivalry among existing competitors, and a medium threat of substitute services. Based on our

Porter’s Five Forces analysis, we conclude that the domestic airline industry is unattractive.

Internal Analysis

Internal Analysis- Value Chain

The Value Chain Analysis “allows a firm to understand the parts of its operations that create value and those

that do not,”(Hitt 84). It consists of both Primary Activities, which are the activities directly involved in supplying a

product to a customer, and Support activities, which are the activities that provide the assistance that is essential for

the Primary Activities to occur (Hitt 84). Primary Activities consist of Inbound Logistics, Operations, Outbound

Logistics, Marketing and Sales, and Service while the Support Activities consist of Procurement, Technological

Development, Human Resource Management and Firm Infrastructure. Analyzing these activities can explain the

valuable parts of JetBlue’s firm structure.

In regards to Primary Activities, the Inbound Logistics are the “activities like materials handling,

warehousing, and inventory control used to receive, store, and disseminate inputs to a product,” (Hitt 90). JetBlue’s

6

Inbound Logistics create value through customer ticketing (which is now done on the Internet to lower costs and

increase efficiency) and attaining fuel-efficient planes. JetBlue only uses two airplane models: the Airbus A-320 and

the Embraer E190. Since it only uses two models, the maintenance, training, and scheduling costs of the airline are

low.

JetBlue creates value in the Operations level of the Value Chain. The company uses advanced technology in

its test implementation of automated baggage handling and it creates “paperless cockpits”. These paperless cockpits

allow pilots to bring laptops in to the cockpit that can retrieve electronic flight manuals, which make pre-flight

loading and balancing calculations, saving the company 4,800 hours of labor per year. The firm also reduces costs

and departure preparation time by offering customers unlimited snacks and beverages instead of serving in-flight

meals. A final operational technique that creates value for the airline is its use of BlueTurn, JetBlue’s ground

operations that minimize aircrafts’ grounded time in order to shorten turnaround time for flights.

In contrast to these other parts of the Value Chain, there are few value-creating strategies within the

Outbound Logistics layer of the Value Chain for JetBlue. The central focus to this layer is the airline’s selectivity

with airports. The firm utilizes point-to-point routing and focuses on less congested airports in order to increase the

speed of turnaround.

The Marketing and Sales level of the Value Chain creates value for JetBlue in multiple ways. JetBlue treats

its employees like a family, so the employees spread a great deal of advertising for the company by word-of-mouth.

The company utilizes both telephone and Internet ticketing, which doubles its distribution channels and efficiently

targets its customers by pricing effectively for business travelers. JetBlue also “employs Omniture software to

increase efficiency of Internet searches, decreasing associated search conversion costs by 94 percent,” (Hitt 215).

Other forms of direct marketing, such as comical postcards and short story testimonials created value for the company

on the Marketing and Sales level of the Value Chain (Hitt 215).

Through the Service level of the Value Chain, JetBlue creates significant value. It boasts superior customer

service in its offering of unlimited snacks and beverages on every flight, the “Comfort Kiss” for long flights (which

consists of hot towels, Dunkin Donuts coffee, and other gifts), refunds for customer inconveniences, on-time flights,

7

few mishandled bags, the Customer Bill of Rights, and Customer Advisory Council (Hitt 210). Along with these

factors, the high employee morale increases service quality and efficiency.

Value is also created behind the scenes through the Supporting Activities. In order to handle high fuel costs,

JetBlue must secure the procurement of fuel-efficient aircrafts. It only owns two models of airplanes, the Airbus A-

320 and the Embraer E190, which reduce maintenance, scheduling and training costs. In relation to Technological

Development, JetBlue is testing the idea of automated baggage handling, and it has already incorporated online-

ticketing and paperless cockpits. This utilization of advanced technology creates value for the airline. On the support

level of Human Resource Management, the company creates value through the non-unionized workforce, which

enjoys high employee morale. Although JetBlue employees are non-unionized, the firm’s philosophy focuses on

keeping employees happy. Employees are referred to as ‘crewmembers’ and David Neeleman said, “the

crewmembers are the ‘real secret weapon’…because if crewmembers are treated well, they will in turn treat the

customers well,” (Hitt 215). The final level of Support Activities, Firm Infrastructure, creates value for JetBlue as

well. For Neeleman, the culture of the airline is extremely important because he wants experienced managers and

happy employees to work as a unit. For example, he has top managers fly with crewmembers each week and

“whenever they fly, they help the crew clean the plane after the flight to ensure a quick turnaround time,” (Hitt 215).

This demonstrates how the culture of the firm functions to create value for JetBlue.

JetBlue’s Value Chain shows its strengths in its strong brand, experienced management, superior customer

service, advanced technology, productive workforce, and low operating costs from efficient resources. Many of these

resources are valuable and rare, and thus can be deemed as competitive advantages for JetBlue. However, competitors

can easily imitate the majority of these strengths and resources. The one resource that JetBlue maintains is its

company culture—one that is valuable, rare, imperfectly imitable, and non-substitutable. It is JetBlue’s culture that

gives it a sustainable competitive advantage above its competitors. As previously mentioned, the founder believes

that his employees are the key to their success. The company atmosphere is one that makes sure that these employees,

from management to baggage handlers, are treated with respect and that their opinions are heard. The benefit of this

transparency results in better employee job performance and customer service, adding a tremendous amount of value

for the company. On the other hand, the main weaknesses of JetBlue is its high maintenance costs, rising payroll

8

expenses, limited hubs and destinations, vulnerability to high debt, and weak financial reporting. These weaknesses

can be seen as gaps in the Value Chain that can hinder JetBlue’s future advantages.

Strategy Formulation

Even though JetBlue operates within a very competitive industry, it is able to succeed by maintaining a dual

advantage. The airline is able to achieve this by implementing both a broad low-cost and broad differentiation

strategy. While there has been debate within the academic community on the viability of dual advantages (Ghemawat,

Rivkin), JetBlue successfully operates in the low cost domestic airline segment by focusing on replacing the trade-

offs associated with the lower cost airlines with “trade-ons” (Ghemawat, Rivkin).

Differentiation through Service

To implement JetBlue’s differentiation strategy, we first examine this by looking at the value chain. We

identified expertise in Human Resources Management as a support activity that adds the most value. Because JetBlue

values its employees by treating them with respect and paying a premium in wages, employees feel valued by the

company, which in turn leads to improved customer services. For instance, JetBlue ranks high in many customer

service categories such as flight completion. By the end of the third quarter of 2006, JetBlue had a 99.6% completion

rate. The company understands the importance of customers’ expectations and heavily emphasizes completion rates,

even at the expense of completing flights on time. JetBlue ranks first out of the 15 busiest airlines in the least number

of lost or mishandled bags in 2006. Management focuses on maintaining trust with their customers, particularly by

ensuring that customers receive their luggage at the end of the flight.

Excellent customer service creates a competitive advantage for JetBlue, but what allows it to charge a higher

price than its low-cost counterparts is by offering additional in-flight amenities. Southwest, another low-cost carrier,

may offer similar levels of customer service at low prices but not offer in-flight amenities. JetBlue’s status as a start-

up airline, unburdened by high legacy costs, gives it the flexibility to add luxury in-flight amenities. By offering in-

flight amenities in addition to excellent customer service, JetBlue adds value to its overall service (under primary

services of the value chain) than its low-cost counterparts. This allows JetBlue to increase willingness to pay within

the low cost segment carrier segment.

Low-Cost in Addition to Quality

9

JetBlue is able to provide low-cost prices to its customers because of its cost saving initiatives. For all airline

companies, one of the most obvious cost drivers is the airplane themselves. JetBlue’s initial use of just one model of

airplane, the Airbus A-320, allowed it to benefit from economies of scale. By exclusively operating one airplane

model, it reduced expenses and complexities in many areas including pilot training, scheduling, and maintenance

costs. However, this will change with the introduction of their second model, the Embraer E-190. Even so, the

company still benefits from only operating two distinct aircrafts compared to its competitors who utilize multiple

models of aircraft.

Labor costs are also a large factor in the operating expenses of JetBlue. In 2006, salaries, wages, and

benefits accounted for about 23% of total revenues. The company currently enjoys both a relatively low cost and

non-unionized labor pool. It has no need to comply with union laws such as specific hotel requirements and

minimum number of flights. JetBlue also requires its crewmembers to help clean up the cabin after flying. This

allows the company to lower turnaround time and save even more on supporting activities. Because JetBlue pays and

treats the workers well, employees are content with taking on extra work, meaning that JetBlue can find opportunities

for more employee participation and in turn lowering company overhead costs.

JetBlue’s investment in technology has added significant value to JetBlue’s primary and secondary services

by increasing operational efficiency to cut costs. For example, by establishing a paperless ticketing system, JetBlue

saves on processing and material costs. The airline also provides pilots and first officers with laptops which retrieve

critical information such as flight manuals, saving JetBlue thousands of labor hours. JetBlue’s telephone reservation

system allows reservation agents to work from home and use VoIP to make free phone calls. JetBlue saves by not

needing to provide office space for their customer service agents. Instead of focusing heavily on traditional

advertising, marketing costs are minimized by utilizing Omniture software to increase the efficiency of Internet

searches. While many airlines struggle to incorporate technology into their operations, JetBlue’s continued emphasis

on technology allows the company to exploit cost savings much more easily than their competitors.

The combination of JetBlue’s efficient processes and cost cutting initiatives translates into tremendous cost

savings for the company. It does so by investing in a single plane model for all of its trips, having non-unionized

labor, and leveraging technology on all fronts of the value chain. Coupling this with premium priced flights as

10

competitive as that of legacy airlines, JetBlue has been able to successfully execute both low-cost and differentiation

strategies, creating a dual advantage for the company.

Threats and Competitive Advantages

JetBlue’s dual advantages are difficult to sustain, particularly its low-cost strategy. With more tenured

employees, an aging fleet, and increased fuel prices, cost savings that JetBlue have previously benefited are

diminishing. We examined its sustainability of dual advantages by looking at the implications of the threat from low-

cost carriers, low-cost subsidiaries of legacy airlines, and traditional airlines.

Threat from other low-cost carriers

The largest threat within the low cost carrier segment is Southwest Airlines. It is the leading low-fare U.S.

carrier with a focus on Midwest and West Coast locations. Similar to JetBlue’s low-cost strategy, Southwest also

emphasizes low-cost and operational efficiency accomplished through online ticketing, utilizing a single aircraft

model (Boeing 737s), and unassigned seating. The airline also focuses on a friendly company culture and high quality

customer service. They limit their in-flight amenities in order to target customers who looking for the lowest price

(Reed). This is where JetBlue differs significantly from Southwest. JetBlue leverages its in-flight amenities to

penetrate into niche markets: the business travelers and customers who are willing to pay more for excellent services.

Furthermore, in regards to JetBlue’s Embraer E-190s, analysts have been saying that the airline has increased

capacity beyond what was necessary for its current expansion initiatives. This further creates opportunities to fill

capacity by penetrating into the Midwest and smaller airports.

There is also potential for Southwest to enter JetBlue’s markets but it would be difficult for the company to

gain the necessary government permission to utilize airports such as JetBlue’s JFK hub. Government regulation in

relation to expansion into new markets will result in more expenses. The lack of low cost options in larger,

metropolitan airports for customers creates a potential opportunity for Southwest to exploit. However it is still

difficult to penetrate into such markets. For example, JFK has limited excess capacity and airlines are unwilling to

give up their spots to operate in such a high-volume market. The trade-off between costs for exposure to a bigger

market is not favorable for Southwest.

Ted and Song

11

Ted is a divisional brand of United Airlines that targets vacation destinations. Ted tries to imitate JetBlue’s

excellent customer service by providing one-class service, extra legroom, and a personal entertainment system.

Delta’s Song Airlines is another potential threat. Its airplanes are fitted with leather seats and free personal

entertainment systems. With a focus on a sophisticated flight experience, Song offers free beverages but charges for

meals and liquor. The airline also has a menu selection that offers snacks and healthy organic meals. Song has utilized

celebrities such as Kate Spade to design the crew uniforms, Rande Gerber to create customized cocktails, and David

Barton to create in-flight exercise programs (McDonald).

Even with the initial success of these two carriers, their business models do not allow them to sustain their

success. Operating as airlines within large traditional airlines, the companies will eventually realize the inability to

have two different business models simultaneously succeed. Legacy costs, including airplane maintenance and union

contracts, are still factored in the operational budgets for these new companies. Another problem exists is the

cannibalization on routes where both the parent and legacy carriers operate. Ted and Song also incur associated costs

by operating under the legacy carriers. This makes it difficult for the airlines to implement a luxury, low-cost

strategy. The companies will eventually understand the impracticality of their strategy and will be forced to close or

abandon the “airline within an airline” strategy.

Threat from legacy carriers

Legacy carriers do not only pose a threat to JetBlue through their low cost carrier offshoots, but they also

pose a threat in the flight segments in which JetBlue is trying to expand. Since legacy carriers are partnering up to

share routes, risks in expansions is lessened. However, JetBlue’s sustainable advantage comes from not competing

in market share or the number of customers, but rather from what has and still works for the company – its customer

service.

JetBlue must be able to maintain its service despite the fact that the company is growing in size. Maintaining

its personable culture might also become increasingly difficult. It should devote significant resources to this category.

Looking at the biggest airlines including American, Delta and United in the categories of flight problems, reservation-

related issues, mishandled baggage, and customer service, it is obvious that excellent service and culture have been

great assets to the success of the company and should continue to be sources of sustainable advantage going forward.

12

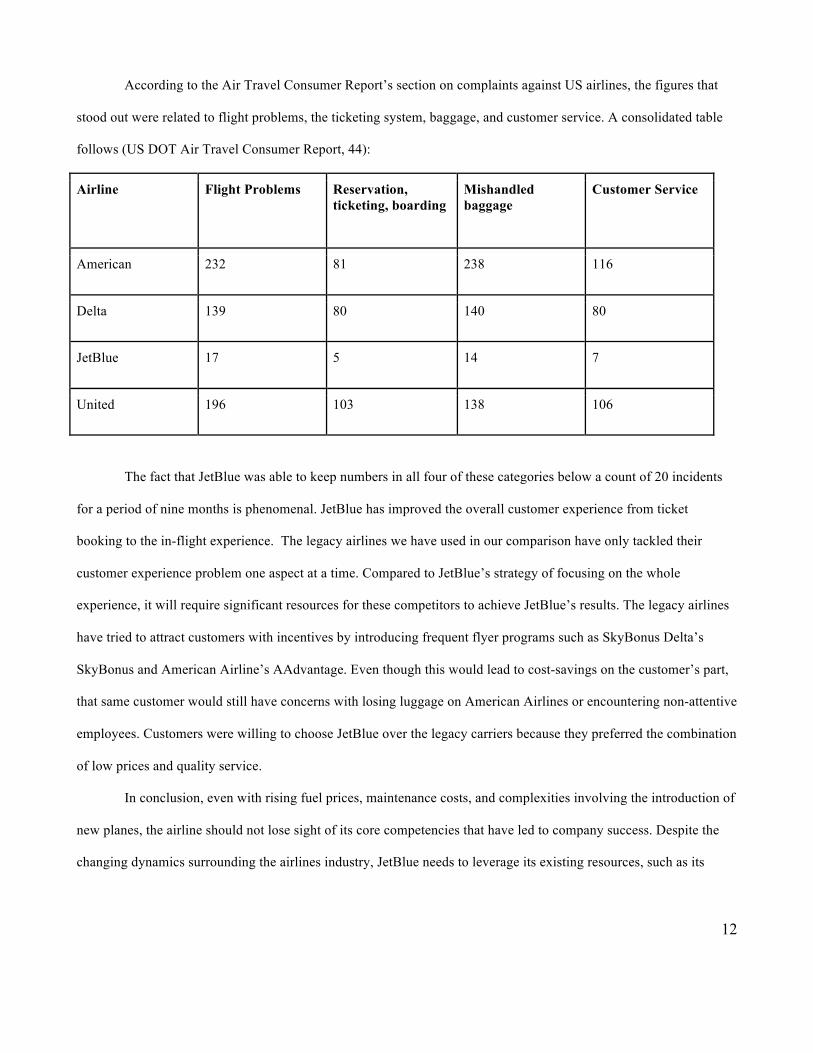

According to the Air Travel Consumer Report’s section on complaints against US airlines, the figures that

stood out were related to flight problems, the ticketing system, baggage, and customer service. A consolidated table

follows (US DOT Air Travel Consumer Report, 44):

Airline Flight Problems Reservation, ticketing, boarding

Mishandled baggage

Customer Service

American 232 81 238 116

Delta 139 80 140 80

JetBlue 17 5 14 7

United 196 103 138 106

The fact that JetBlue was able to keep numbers in all four of these categories below a count of 20 incidents

for a period of nine months is phenomenal. JetBlue has improved the overall customer experience from ticket

booking to the in-flight experience. The legacy airlines we have used in our comparison have only tackled their

customer experience problem one aspect at a time. Compared to JetBlue’s strategy of focusing on the whole

experience, it will require significant resources for these competitors to achieve JetBlue’s results. The legacy airlines

have tried to attract customers with incentives by introducing frequent flyer programs such as SkyBonus Delta’s

SkyBonus and American Airline’s AAdvantage. Even though this would lead to cost-savings on the customer’s part,

that same customer would still have concerns with losing luggage on American Airlines or encountering non-attentive

employees. Customers were willing to choose JetBlue over the legacy carriers because they preferred the combination

of low prices and quality service.

In conclusion, even with rising fuel prices, maintenance costs, and complexities involving the introduction of

new planes, the airline should not lose sight of its core competencies that have led to company success. Despite the

changing dynamics surrounding the airlines industry, JetBlue needs to leverage its existing resources, such as its

13

emphasis on customer service, its new fleet of Embraer E-190s, and its location advantages to add value to the

company.

Recommendation

The airline’s expansion has threatened to dilute JetBlue’s culture. Top management has historically

attributed the company’s crewmembers as an important factor to the company’s success. As it grows, top

management will inevitably lose its level of interaction with their employees. This presents a strategic opportunity

for the company to implement a new management-training program that builds on top of their new hire-training

program. The new program would focus on teaching managers the JetBlue culture from a management perspective

and prepare them for tasks including flying with crewmembers and listening to their comments. This program

provides both short and long-term benefits. First, the company is able to maintain the management’s connection with

their employees even in a time of rapid expansion. Long term, JetBlue would be able to build a stronger overall

management base that retains the founding values of the company. By instilling the up and coming managers with

these values, JetBlue ensures that its unique company culture will continue to be a part of the company after the

departure of David Neeleman and his executive team.

Recent struggles have led JetBlue to reevaluate its operations highlighted by its “Return to Profitability” plan

introduced in 2006. We support many of the initiatives but also suggest that the company maintain its current level of

IT spending. While some may classify it as discretionary, we argue that the investment in IT has led to many

innovative cost saving solutions including its telephone reservation system and BlueTurn. The cost savings found in

these programs have allowed the company to successfully absorb other expenses such as higher fuel prices and

increased labor costs. The investments in these systems have consistently proven their worth. Going forward, we

feel that the industry as a whole will be aggressively investing in technology to achieve greater efficiencies and cost

savings. By maintaining IT spending during tough economic conditions, the company can work to further innovate

and refine value added programs that will help JetBlue to maintain its competitiveness going forward.

Management has been involved in discussions regarding expansion into the international market. We

recommend against this initiative. Entering into joint ventures has several flaws including losing some of JetBlue’s

competitive advantage through knowledge sharing, relinquishing a degree of control surrounding decision-making,

14

and realizing some as opposed to all revenues from the venture. In addition, JetBlue’s strategic focus has been in the

US markets. Expanding into the international market requires vast amounts of knowledge that the existing

management of JetBlue does not have.

International expansion is further made difficult due to the heavy government regulations. Despite the fact

that US lobbyists and politicians have been fighting for fewer restrictions on international air travel, it is uncertain if

these efforts will result in any changes. The increased associated costs eliminate much of the potential benefit for

JetBlue. The combination of the disadvantages of a joint venture, heavy government scrutiny surrounding

international travel, and the lack of expertise in the international markets makes this venture unattractive.

JetBlue should expand into the Midwest and/or smaller airports with a focus to compete against regional

airlines. These airlines are growing twice as fast as their national counterparts presenting a great opportunity for

growth. JetBlue can successfully compete against these smaller airlines by leveraging their dual advantages. For

example, JetBlue will be able to offer a better customer experience at a similar or lower price compared to these

smaller, regional airlines. JetBlue will be able to utilize their new Embraer fleet because of the emphasis on point-to-

point travel in this market. The growth in these regional markets will allow JetBlue to offset the loss of the

economies of scales when the company shifts to a multiple aircraft fleet.

JetBlue faces many opportunities and threats as it continues to grow. Although no one can be certain of

future changes within the industry, we feel confident that our analysis and recommendation will allow JetBlue to

continue in their success.