Embed Size (px)

Citation preview

4/3/03 1

Competition, collaboration, & “offsets” in aircraft

• Industry characteristics contrast with those of the IT, biomedical sectors:– Exit, rather than entry, has dominated industry development

since 1945 in US, Europe.– User-innovation is much less common in commercial

aircraft.– “Vertical specialization” has very different characteristics.

• Asian markets and international production networks are important, similarly to IT.

• Governments are important actors in military & civil segments of the industry.– State-owned airlines, regulatory & other nontariff barriers to

market access.– Gov’t actions in military affect civil industry.

4/3/03 2

Other industry characteristics• High development costs (new Airbus: $11B).• Development requires complex “integration” of

numerous different technologies.– “Primes” work with huge # of suppliers.– Relatively few stable, well-defined “interfaces.”– Designs stay in production for decades.

• Markets are global, product support is critical.• Wide swings in demand for commercial aircraft.• Links between civil and military aerospace remain

important, but have changed since 1945.– Reduced “spillovers” from military to civil aircraft .– Military demand is more stable and supports R&D.

• Interfirm “alliances” are used for development, production of new commercial aircraft & engines.

4/3/03 3

Large US commercial aircraft shipments, 1971-2000

0

100

200

300

400

500

600

700

year

# of

airc

raft

4/3/03 4

Evolution of industry structure & markets

• 1970: 3 US airframe firms, 2 European.• 2003: 1 US, 1 European.• Japanese firms have failed to enter as “primes,” instead

are risk-sharing partners.– Small domestic “launch market” contrasts with

semiconductors, computers.

• US accounts for declining share of global aircraft demand.– Asia, esp. PRC, is projected to grow rapidly.– PRC has very large domestic “launch market.”

• In US, overall aerospace industry has shrunk since end of the Cold War.– Employment losses driven by military cutbacks.

4/3/03 5

4/3/03 6

4/3/03 71981: 75 firms 2001: 5 firms

4/3/03 8

1999-2019 projected growth in fleet capacity: Airbus Industrie

4/3/03 9N. American share of fleet declines from 43% in 1999 to 36% in 2019

4/3/03 10>300-seat aircraft share of fleet projected to grow from 15.5% to 26%

4/3/03 11

4/3/03 12

“Offsets”: What are they?• Promises of “workshare” (purchases of

components, subassemblies) for firms in nation ordering aircraft.– In some cases, offsets involve seller firm taking other

goods in “countertrade” (e.g., Polish hams for McDonnell Douglas aircraft).

– Offsets are a response to nontariff barriers to market access erected by gov’ts.

• Offsets are more pronounced and explicit in military aircraft procurement.

• Similar “offset-like” provisions are common in sales of telecom equipment, other expensive capital goods sold to state-owned or state-influenced firms.

4/3/03 13

Offsets originated in postwar US policy• US gov’t encouraged “coproduction” (licensed

production) of U.S. military aircraft in purchasing nations during the 1950s and 1960s.– Reconstruction of military allies’ economies an important

goal in the Cold War.– Encouragement for standardization.– 28 missile/aircraft coproduction agreements during 1950-80

• Coproduction agreements aided revival of aircraft industries in Japan, Germany, other allied economies, creating demand for offsets.

• Offsets remain important in foreign sales of US military aircraft.– December 2002: Polish purchase of $3.5 billion in F-16s

includes indirect offsets calculated at >$9 billion.

4/3/03 14

Evaluating military offsets• US gov’t data on share of offsets in military exports

reveal little evidence of strong trend.• Most military-aircraft offsets have transferred

employment & economic activity. Transfers of advanced technology have been relatively modest.

• US gov’t (witness Polish sale) has been ambivalent about offsets, criticizing them in general and supporting them in specific deals.– US industry retains primary responsibility for offsets

negotiation, but gov’t retains right to review agreements.

• US purchases of foreign military aircraft, other systems also include offset demands (domestic production).

• Presidential Commission established in 1999.

4/3/03 15

Offsets % of US military exports, 1980-94

0

20

40

60

80

100

120

1980 1981 1982 1983 1984 1985 1986 1987 1993 1994

year

4/3/03 16

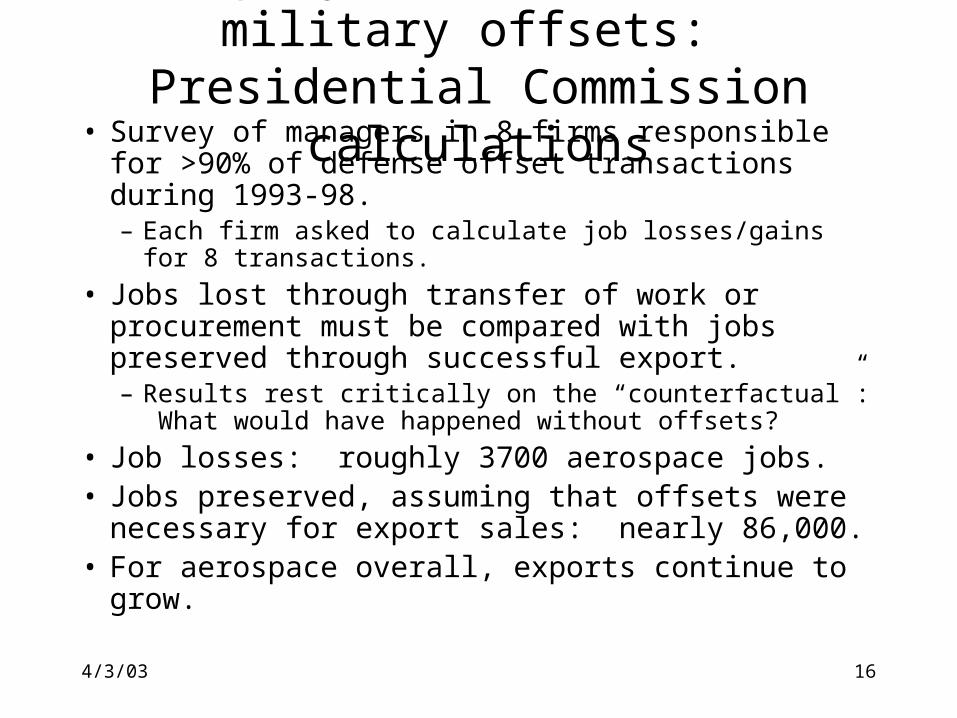

Employment effects of military offsets: Presidential Commission calculations

• Survey of managers in 8 firms responsible for >90% of defense offset transactions during 1993-98.– Each firm asked to calculate job losses/gains for 8

transactions.

• Jobs lost through transfer of work or procurement must be compared with jobs preserved through successful export.– Results rest critically on the “counterfactual”: What would

have happened without offsets?

• Job losses: roughly 3700 aerospace jobs.• Jobs preserved, assuming that offsets were necessary

for export sales: nearly 86,000.• For aerospace overall, exports continue to grow.

4/3/03 17

4/3/03 18

Alternative policy solutions to the offsets “problem”

• Pursue a multilateral “standstill” agreement.– Enforceable? WTO disciplines can be waived on “national

security” grounds.– US firms argue that a multilateral agreement would reduce

US military exports; gov’ts would “buy domestic” without the benefits offered through offsets..

• Encourage offsets that can be fulfilled through other “workshare” agreements with less significant effects on US employment

• Encourage collaboration with foreign firms “upstream,” in the R&D phase.– Huge controversy over outflows of US technology.– R&D collaboration may not reduce pressure for offsets

downstream.

4/3/03 19

Military offsets affected postwar commercial aircraft markets

• US coproduction & offset deals contribute to growth in production capacity (often state-owned) in other industrial economies, increasing political pressure on gov’ts to influence commercial aircraft purchases.– State-controlled airlines, state-controlled regulators,

state-controlled loan guarantees all provide leverage & can limit foreign firms’ access to markets.

– Result is formal, informal pressure for “offset-like” arrangements in large commercial sales.

• But international collaboration in commercial aircraft reflects other factors as well.

4/3/03 20

International collaboration in large (>100 seats) commercial aircraft

• Very common since the 1970s.– Boeing: collaboration with Japanese, British, Italian firms

in 747, 767, 777.– McDonnell Douglas: licensed production of MD-82 in

PRC, proposed collaboration with Taiwanese group.– Airbus: intra-European, little extra-European

collaboration.– Collaboration also is common in large engines.

• 3 broad motives:– Market access (“offset-like” arrangements).– Access to capital (from partner firms and/or partner-firm

gov’ts).– Access to technology (components, process technologies).

4/3/03 21

Managing collaboration• Management of technology transfer is crucial and

requires a balanced approach. – Partners typically share in development, as well as

production, for a given design.– “Senior partners” need to adopt a strategic view.– Blocking technology transfer creates problems.

• Decisionmaking can be problematic.– Need to avoid pushing decisions upward within partner

organizations.– JVs with a “dominant partner” appear to operate more

smoothly.

• Especially in “partnerships of equals,” competition in other product lines may undercut collaboration.

• Cost management: Partner workshares based on transfer prices, rather than costs.

4/3/03 22

Evaluating the effects of collaboration in commercial aircraft

• As in the case of military-aircraft offsets, what is the counterfactual? – Would a given sale have occurred without collaboration?– McDonnell Douglas: limited collaboration=>dwindling

product line and eventual exit through acquisition.– Boeing: more extensive collaboration=> broader product

line. No “prime” has entered yet.

• Primes’ engineering, production workers (Boeing labor strikes) and US supplier firms likely to feel greatest employment losses from collaboration.– “Prime contractor” firms are globalizing their production

network, supply sources.– But US aircraft-component trade balance has improved.

4/3/03 23

Exports & Imports, aircraft components, 1994-2002

0

5000

10000

15000

20000

25000

30000

1994 1995 1996 1997 1998 1999 2000 2001 2002

year

Mill

ion

$$ exports

imports

4/3/03 24

Trade policy and collaboration• Market access barriers affect motives for collaboration.

– WTO “procurement code” limits scope for gov’ts to use public procurement strategically.

– PRC not yet a full signatory to procurement code, and its huge market gives it enormous leverage.

• US and EU have negotiated for decades over subsidies for Airbus, DoD R&D support for US aircraft firms.– EU: US firms benefit from NASA and DoD R&D.– US: EU firms benefit from “soft” loans for product launch.– US firms remain reluctant to invoke trade sanctions.– Boeing remains largest single customer for US Export-

Import Bank, supplier of subsidized credit for exports.

4/3/03 25

Airbus v. Boeing• Airbus: founded in 1967 as a collaboration among

“national champions,” has become much stronger with the gradual removal of direct state control.– New assembly techniques enabled more widely

distributed worksharing among European partners.– Arguably has been more aggressive in incorporating

new technologies.– The A380 “super-jumbo” aircraft targets trans-Pacific,

Europe-Asian routes.

• Boeing shelved the “Sonic Cruiser,” now is reconsidering another upgrade of a 35-year-old design, the 747.

• Airbus has gained market share since the 1980s.

4/3/03 26

4/3/03 27

Asia and the commercial aircraft industry

• A major source of future demand growth (especially PRC).

• Airbus 380 targeted on Asian long-haul routes.• Japan, Korea, Taiwan, PRC all have considered or

participated in collaborative commercial aircraft ventures.

• Japan in particular has largely given up on independent entry.– Small domestic market.– Despite long experience as a risk-sharing partner in

commercial ventures, co-production agreements, leading Japanese aircraft firms lack the design & systems integration skills for “prime contractor” entry.

– Domestic defense market is much more profitable.

4/3/03 28

The outlook

• Asian markets (esp. PRC) will dominate US, European firms’ strategies for the next decade.

• Gov’ts matter, but their interests don’t always coincide with those of firms.

• Airbus will maintain and/or intensify pressure on Boeing, which is reducing dependence on commercial aircraft.

• US defense market may grow more rapidly; military export market more uncertain.

• Continued growth of international production networks and alliances (offsets and “offset-like”), many of which will focus on PRC.

• Continued erosion of employment in US aircraft industry (military and civilian) is likely.

4/3/03 29

4/3/03 30

"Net orders," Boeing, MCDAC, & Airbus, 1993-2001

0

100

200

300

400

500

600

700

1993 1994 1995 1996 1997 1998 1999 2000 2001

year

# of

airc

raft

Boeing net orders

MCDAC net orders

Airbus net orders

4/3/03 31

The politics of offsets: Japan, US, & the “FSX”

• 1985: Japanese aerospace firms lobby Japanese Ministry of Defense for independent development of next-generation fighter aircraft.

• 1987: US & Japan negotiate a “co-development” agreement for the FSX.– Huge controversy over transfer of military-aircraft

technologies with (alleged) civil applications from US to Japanese aerospace firms.

• 1988: Co-development agreement renegotiated, providing US firms greater access to Japanese aerospace firms’ technologies.

• 1997: “F-2” project is over budget ($4B vs $1.1B), and US firms have expressed little interest in technology “flowbacks.”