Embed Size (px)

Citation preview

4 - 1©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Professional EthicsProfessional Ethics

Chapter 4Chapter 4

4 - 2©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 1Learning Objective 1

Distinguish ethical from unethicalDistinguish ethical from unethical

behavior in personal andbehavior in personal and

professional contexts.professional contexts.

4 - 3©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

What Are Ethics?What Are Ethics?

Ethics can be defined broadly asEthics can be defined broadly asa set of moral principles or values.a set of moral principles or values.

Ethics can be defined broadly asEthics can be defined broadly asa set of moral principles or values.a set of moral principles or values.

Each of us has such a set of values.Each of us has such a set of values.Each of us has such a set of values.Each of us has such a set of values.

We may or may not have consideredWe may or may not have consideredthem explicitly.them explicitly.

We may or may not have consideredWe may or may not have consideredthem explicitly.them explicitly.

4 - 4©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Need for EthicsNeed for Ethics

Ethical behavior is necessary for a societyEthical behavior is necessary for a societyto function in an orderly manner.to function in an orderly manner.

Ethical behavior is necessary for a societyEthical behavior is necessary for a societyto function in an orderly manner.to function in an orderly manner.

The need for ethics in society is sufficientlyThe need for ethics in society is sufficientlyimportant that many commonly heldimportant that many commonly heldethical values are incorporated into laws.ethical values are incorporated into laws.

The need for ethics in society is sufficientlyThe need for ethics in society is sufficientlyimportant that many commonly heldimportant that many commonly heldethical values are incorporated into laws.ethical values are incorporated into laws.

4 - 5©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Illustrative PrescribedIllustrative PrescribedEthical PrinciplesEthical Principles

TrustworthinessTrustworthinessTrustworthinessTrustworthiness

ResponsibilityResponsibilityResponsibilityResponsibility

CaringCaringCaringCaring

RespectRespectRespectRespect

FairnessFairnessFairnessFairness

CitizenshipCitizenshipCitizenshipCitizenship

4 - 6©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Why People Act UnethicallyWhy People Act Unethically

The person’s ethical standards are differentThe person’s ethical standards are differentfrom those of society as a whole.from those of society as a whole.

The person’s ethical standards are differentThe person’s ethical standards are differentfrom those of society as a whole.from those of society as a whole.

The person chooses to act selfishly.The person chooses to act selfishly.The person chooses to act selfishly.The person chooses to act selfishly.

In many instances, both reasons exist.In many instances, both reasons exist.In many instances, both reasons exist.In many instances, both reasons exist.

4 - 7©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

A Person Chooses toA Person Chooses toAct Selfishly – ExampleAct Selfishly – Example

Person APerson A finds a briefcase containing importantfinds a briefcase containing importantpapers and $1,000.papers and $1,000.

Person APerson A finds a briefcase containing importantfinds a briefcase containing importantpapers and $1,000.papers and $1,000.

He tosses the briefcase and keeps the money.He tosses the briefcase and keeps the money.He tosses the briefcase and keeps the money.He tosses the briefcase and keeps the money.

He brags to his friends about his good fortune.He brags to his friends about his good fortune.He brags to his friends about his good fortune.He brags to his friends about his good fortune.

This action probably differs from most of society.This action probably differs from most of society.This action probably differs from most of society.This action probably differs from most of society.

4 - 8©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

A Person Chooses toA Person Chooses toAct Selfishly – ExampleAct Selfishly – Example

Person BPerson B faces the same situation butfaces the same situation butresponds differently.responds differently.

Person BPerson B faces the same situation butfaces the same situation butresponds differently.responds differently.

He keeps the money but leaves the briefcase.He keeps the money but leaves the briefcase.He keeps the money but leaves the briefcase.He keeps the money but leaves the briefcase.

He tells nobody and spends the money.He tells nobody and spends the money.He tells nobody and spends the money.He tells nobody and spends the money.

He has violated his own ethical standardsHe has violated his own ethical standardsand chose to and chose to act act selfishlyselfishly..

He has violated his own ethical standardsHe has violated his own ethical standardsand chose to and chose to act act selfishlyselfishly..

4 - 9©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 2Learning Objective 2

Resolve ethical dilemmas usingResolve ethical dilemmas using

an ethical framework.an ethical framework.

4 - 10©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Ethical DilemmasEthical Dilemmas

An ethical dilemma is a situation a personAn ethical dilemma is a situation a personfaces in which a decision must be madefaces in which a decision must be madeabout appropriate behavior.about appropriate behavior.

An ethical dilemma is a situation a personAn ethical dilemma is a situation a personfaces in which a decision must be madefaces in which a decision must be madeabout appropriate behavior.about appropriate behavior.

4 - 11©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

RationalizingRationalizingUnethical BehaviorUnethical Behavior

Everybody does it.Everybody does it.Everybody does it.Everybody does it.

If it’s legal, it’s ethical.If it’s legal, it’s ethical.If it’s legal, it’s ethical.If it’s legal, it’s ethical.

Likelihood of discovery and consequencesLikelihood of discovery and consequencesLikelihood of discovery and consequencesLikelihood of discovery and consequences

4 - 12©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

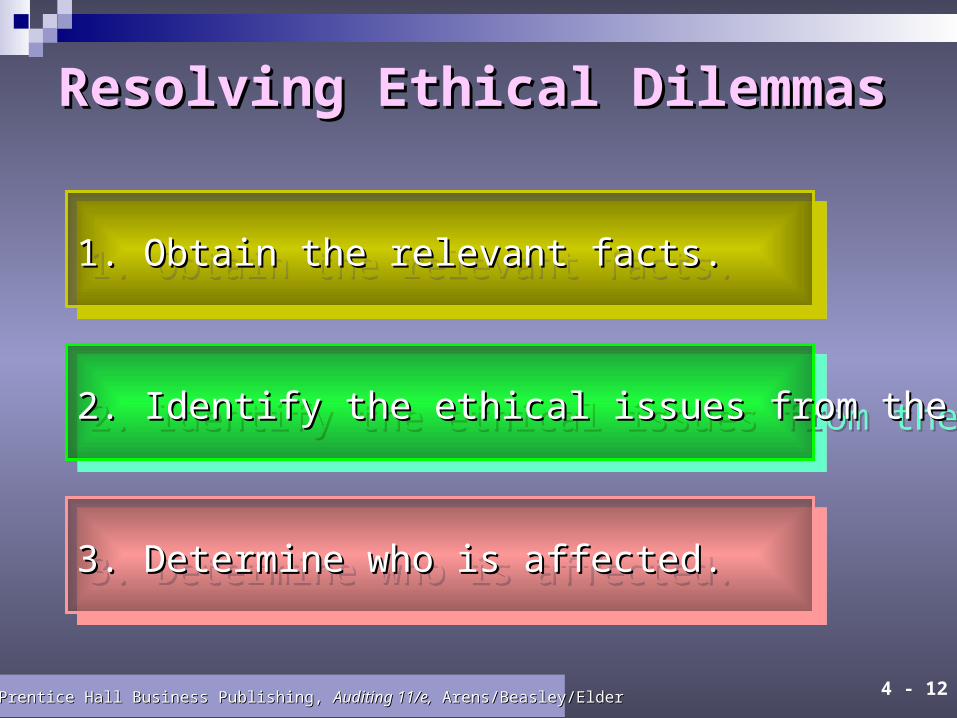

Resolving Ethical DilemmasResolving Ethical Dilemmas

1. Obtain the relevant facts.1. Obtain the relevant facts.1. Obtain the relevant facts.1. Obtain the relevant facts.

2. Identify the ethical issues from the facts.2. Identify the ethical issues from the facts.2. Identify the ethical issues from the facts.2. Identify the ethical issues from the facts.

3. Determine who is affected.3. Determine who is affected.3. Determine who is affected.3. Determine who is affected.

4 - 13©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

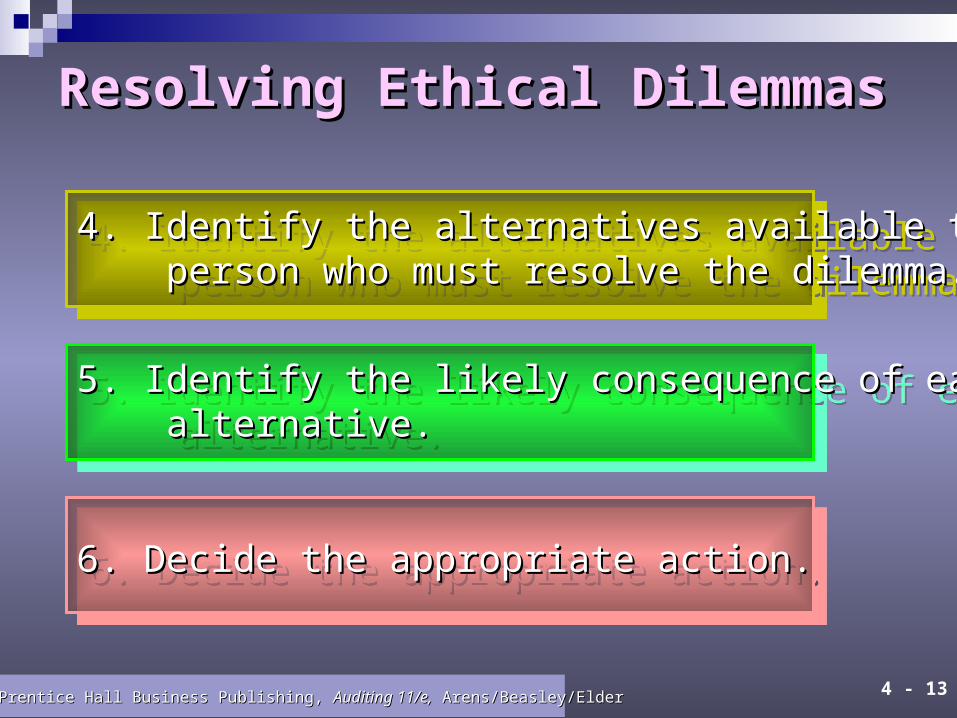

Resolving Ethical DilemmasResolving Ethical Dilemmas

4. Identify the alternatives available to the4. Identify the alternatives available to the person who must resolve the dilemmaperson who must resolve the dilemma..

4. Identify the alternatives available to the4. Identify the alternatives available to the person who must resolve the dilemmaperson who must resolve the dilemma..

5. Identify the likely consequence of each5. Identify the likely consequence of each alternative.alternative.

5. Identify the likely consequence of each5. Identify the likely consequence of each alternative.alternative.

6. Decide the appropriate action.6. Decide the appropriate action.6. Decide the appropriate action.6. Decide the appropriate action.

4 - 14©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

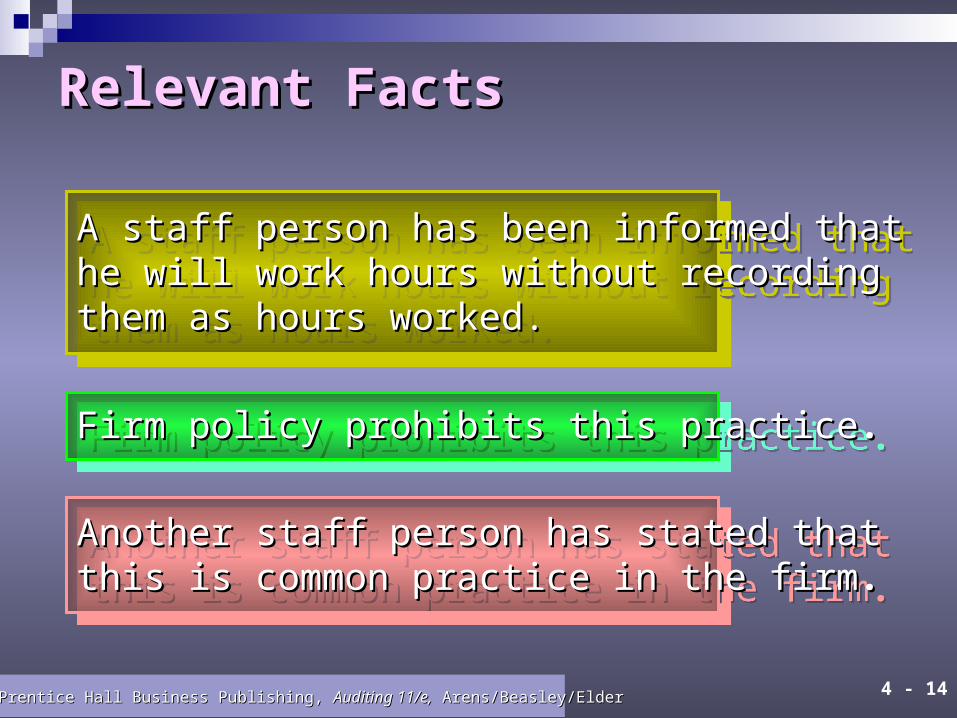

Relevant FactsRelevant Facts

A staff person has been informed thatA staff person has been informed thathe will work hours without recordinghe will work hours without recordingthem as hours worked.them as hours worked.

A staff person has been informed thatA staff person has been informed thathe will work hours without recordinghe will work hours without recordingthem as hours worked.them as hours worked.

Firm policy prohibits this practiceFirm policy prohibits this practice.. Firm policy prohibits this practiceFirm policy prohibits this practice..

Another staff person has stated thatAnother staff person has stated thatthis is common practice in the firmthis is common practice in the firm..

Another staff person has stated thatAnother staff person has stated thatthis is common practice in the firmthis is common practice in the firm..

4 - 15©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

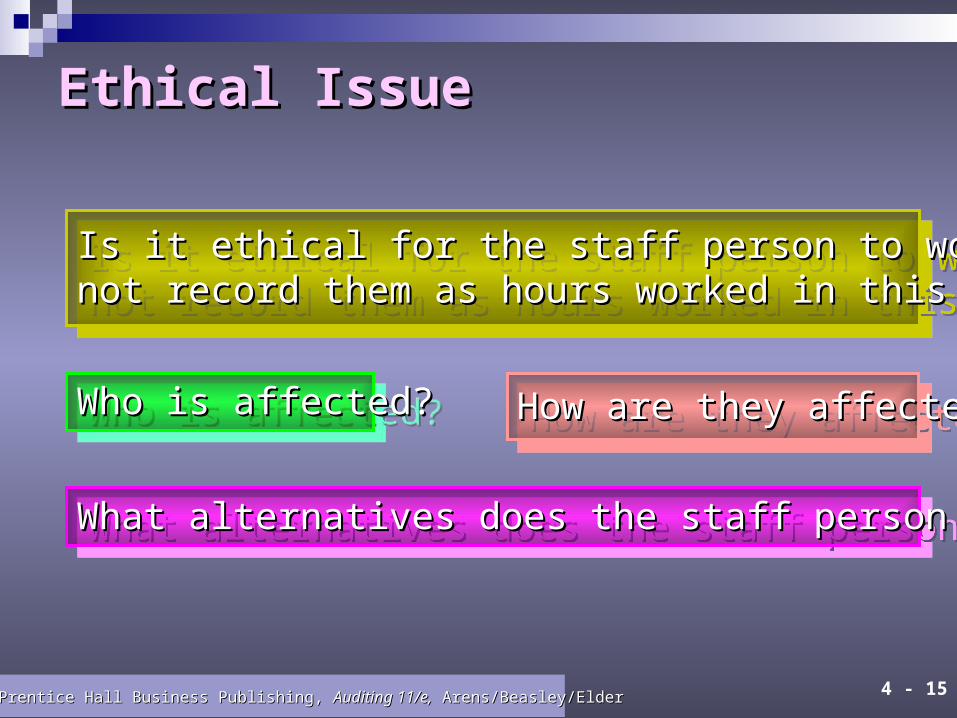

Ethical IssueEthical Issue

Is it ethical for the staff person to work hours andIs it ethical for the staff person to work hours andnot record them as hours worked in this situation?not record them as hours worked in this situation?

Is it ethical for the staff person to work hours andIs it ethical for the staff person to work hours andnot record them as hours worked in this situation?not record them as hours worked in this situation?

Who is affected?Who is affected?Who is affected?Who is affected? How are they affected?How are they affected?How are they affected?How are they affected?

What alternatives does the staff person have?What alternatives does the staff person have?What alternatives does the staff person have?What alternatives does the staff person have?

4 - 16©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 3Learning Objective 3

Explain the importance of ethicalExplain the importance of ethical

conduct for the accountingconduct for the accounting

profession.profession.

4 - 17©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Special Need for Ethical Conduct Special Need for Ethical Conduct in Professionsin Professions

Our society has attached a specialOur society has attached a specialmeaning to the term professional.meaning to the term professional.

Our society has attached a specialOur society has attached a specialmeaning to the term professional.meaning to the term professional.

A professional is expected to conductA professional is expected to conducthimself or herself at a higher levelhimself or herself at a higher levelthan most other members of society.than most other members of society.

A professional is expected to conductA professional is expected to conducthimself or herself at a higher levelhimself or herself at a higher levelthan most other members of society.than most other members of society.

4 - 18©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

CPAs Encouraged to ConductCPAs Encouraged to ConductThemselves at a High LevelThemselves at a High Level

Conduct of CPA firm personnelConduct of CPA firm personnelConduct of CPA firm personnelConduct of CPA firm personnel

CPACPAexaminationexamination

CPACPAexaminationexamination

GAAS andGAAS andinterpretationsinterpretations

GAAS andGAAS andinterpretationsinterpretations

Continuing educationContinuing educationrequirementsrequirements

Continuing educationContinuing educationrequirementsrequirements

4 - 19©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

CPAs Encouraged to ConductCPAs Encouraged to ConductThemselves at a High LevelThemselves at a High Level

Conduct of CPA firm personnelConduct of CPA firm personnelConduct of CPA firm personnelConduct of CPA firm personnel

QualityQualitycontrolcontrol

QualityQualitycontrolcontrol

PeerPeerreviewreview

PeerPeerreviewreview

Legal liabilityLegal liabilityLegal liabilityLegal liability

4 - 20©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

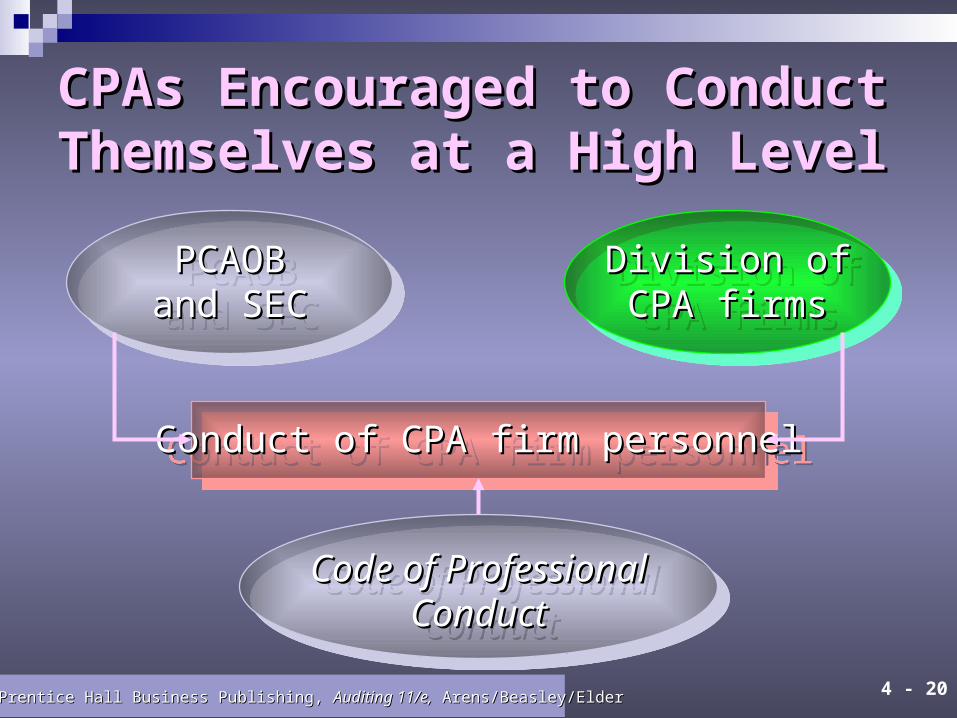

CPAs Encouraged to ConductCPAs Encouraged to ConductThemselves at a High LevelThemselves at a High Level

Conduct of CPA firm personnelConduct of CPA firm personnelConduct of CPA firm personnelConduct of CPA firm personnel

PCAOBPCAOBand SECand SEC

PCAOBPCAOBand SECand SEC

Division ofDivision ofCPA firmsCPA firms

Division ofDivision ofCPA firmsCPA firms

Code of ProfessionalCode of ProfessionalConductConduct

Code of ProfessionalCode of ProfessionalConductConduct

4 - 21©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 4Learning Objective 4

Describe the purpose and content Describe the purpose and content

of the AICPA of the AICPA Code of ProfessionalCode of Professional

ConductConduct..

4 - 22©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

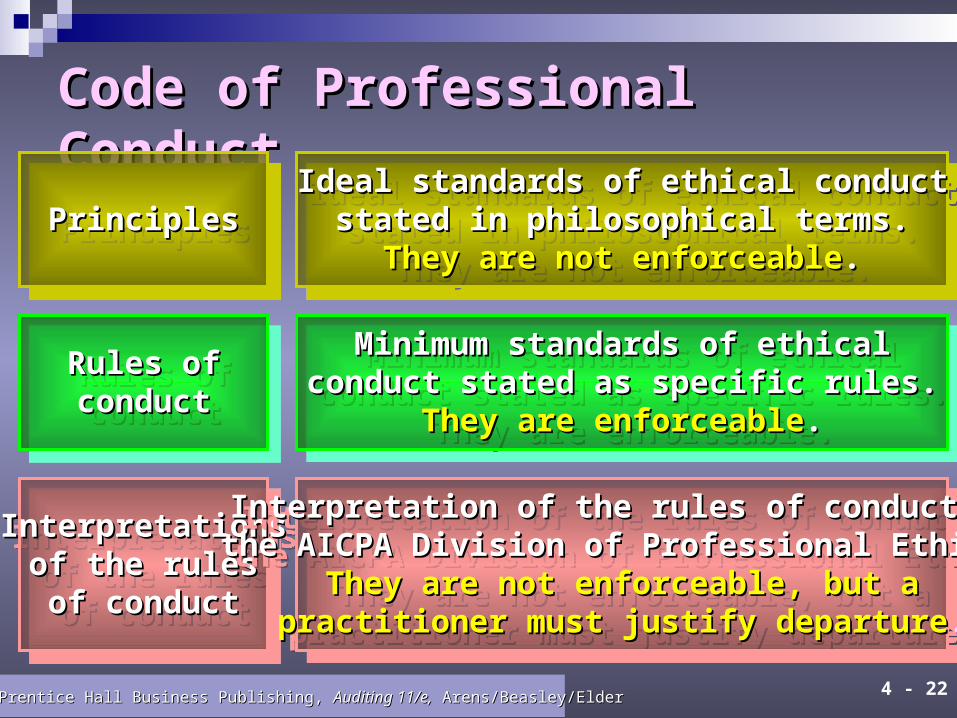

Code of Professional ConductCode of Professional Conduct

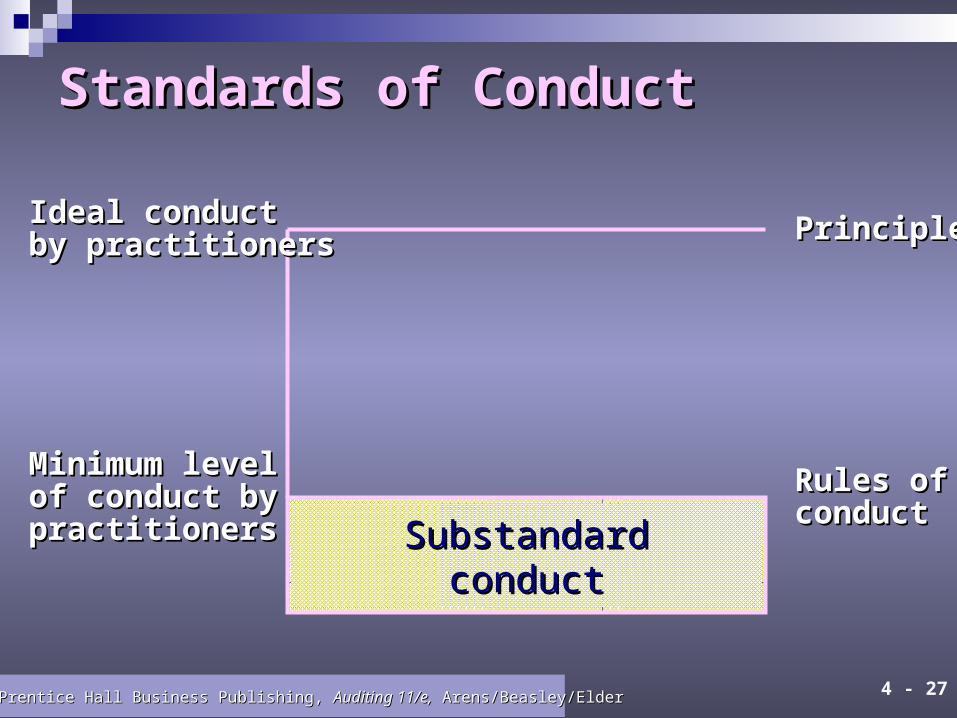

PrinciplesPrinciplesPrinciplesPrinciplesIdeal standards of ethical conductIdeal standards of ethical conduct

stated in philosophical terms.stated in philosophical terms.They are not enforceableThey are not enforceable..

Ideal standards of ethical conductIdeal standards of ethical conductstated in philosophical terms.stated in philosophical terms.

They are not enforceableThey are not enforceable..

Rules ofRules ofconductconduct

Rules ofRules ofconductconduct

Minimum standards of ethicalMinimum standards of ethicalconduct stated as specific rules.conduct stated as specific rules.

They are enforceableThey are enforceable..

Minimum standards of ethicalMinimum standards of ethicalconduct stated as specific rules.conduct stated as specific rules.

They are enforceableThey are enforceable..

InterpretationsInterpretationsof the rulesof the rulesof conductof conduct

InterpretationsInterpretationsof the rulesof the rulesof conductof conduct

Interpretation of the rules of conduct byInterpretation of the rules of conduct bythe AICPA Division of Professional Ethics.the AICPA Division of Professional Ethics.

They are not enforceable, but aThey are not enforceable, but apractitioner must justify departurepractitioner must justify departure..

Interpretation of the rules of conduct byInterpretation of the rules of conduct bythe AICPA Division of Professional Ethics.the AICPA Division of Professional Ethics.

They are not enforceable, but aThey are not enforceable, but apractitioner must justify departurepractitioner must justify departure..

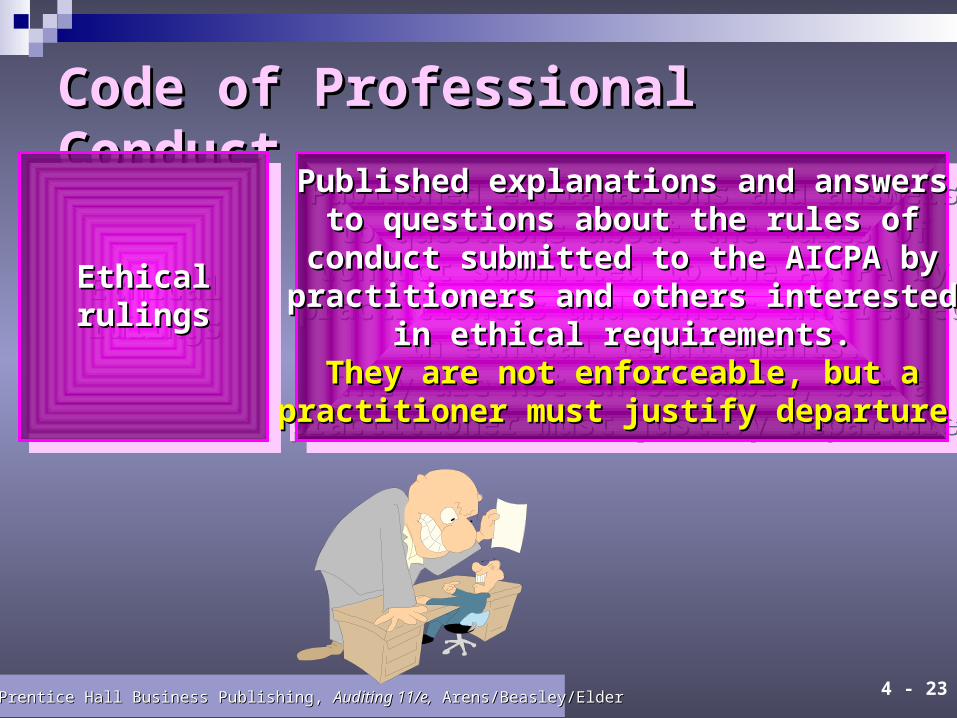

4 - 23©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Code of Professional ConductCode of Professional Conduct

EthicalEthicalrulingsrulings

EthicalEthicalrulingsrulings

Published explanations and answersPublished explanations and answersto questions about the rules ofto questions about the rules of

conduct submitted to the AICPA byconduct submitted to the AICPA bypractitioners and others interestedpractitioners and others interested

in ethical requirements.in ethical requirements.They are not enforceable, but aThey are not enforceable, but a

practitioner must justify departurepractitioner must justify departure..

Published explanations and answersPublished explanations and answersto questions about the rules ofto questions about the rules of

conduct submitted to the AICPA byconduct submitted to the AICPA bypractitioners and others interestedpractitioners and others interested

in ethical requirements.in ethical requirements.They are not enforceable, but aThey are not enforceable, but a

practitioner must justify departurepractitioner must justify departure..

4 - 24©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

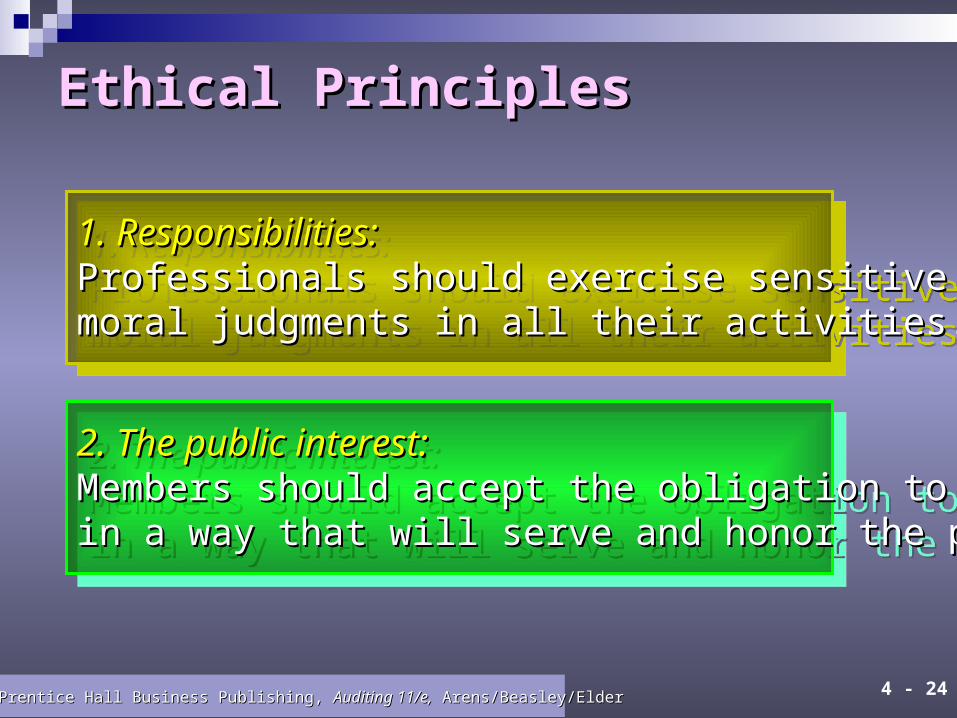

Ethical PrinciplesEthical Principles

1. Responsibilities:1. Responsibilities:Professionals should exercise sensitive andProfessionals should exercise sensitive andmoral judgments in all their activities.moral judgments in all their activities.

1. Responsibilities:1. Responsibilities:Professionals should exercise sensitive andProfessionals should exercise sensitive andmoral judgments in all their activities.moral judgments in all their activities.

2. The public interest:2. The public interest:Members should accept the obligation to actMembers should accept the obligation to actin a way that will serve and honor the public.in a way that will serve and honor the public.

2. The public interest:2. The public interest:Members should accept the obligation to actMembers should accept the obligation to actin a way that will serve and honor the public.in a way that will serve and honor the public.

4 - 25©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Ethical PrinciplesEthical Principles

3. Integrity:3. Integrity:Members should perform all responsibilitiesMembers should perform all responsibilitieswith integrity to maintain public confidence.with integrity to maintain public confidence.

3. Integrity:3. Integrity:Members should perform all responsibilitiesMembers should perform all responsibilitieswith integrity to maintain public confidence.with integrity to maintain public confidence.

4. Objectivity and independence:4. Objectivity and independence:Members should be objective, independent,Members should be objective, independent,and free of conflicts of interest.and free of conflicts of interest.

4. Objectivity and independence:4. Objectivity and independence:Members should be objective, independent,Members should be objective, independent,and free of conflicts of interest.and free of conflicts of interest.

4 - 26©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Ethical PrinciplesEthical Principles

5. Due care:5. Due care:Members should observe the profession’sMembers should observe the profession’sstandards and strive to improve competence.standards and strive to improve competence.

5. Due care:5. Due care:Members should observe the profession’sMembers should observe the profession’sstandards and strive to improve competence.standards and strive to improve competence.

6. Scope and nature of services:6. Scope and nature of services:A member in public practice should observe A member in public practice should observe the the Code of Professional Conduct.Code of Professional Conduct.

6. Scope and nature of services:6. Scope and nature of services:A member in public practice should observe A member in public practice should observe the the Code of Professional Conduct.Code of Professional Conduct.

4 - 27©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Standards of ConductStandards of Conduct

PrinciplesPrinciples

Rules ofRules ofconductconduct

SubstandardSubstandardconductconduct

Ideal conductIdeal conductby practitionersby practitioners

Minimum levelMinimum levelof conduct byof conduct bypractitionerspractitioners

4 - 28©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 5Learning Objective 5

Understand Sarbanes-Oxley ActUnderstand Sarbanes-Oxley Act

and other SEC independenceand other SEC independence

requirements and otherrequirements and other

factors that influencefactors that influence

auditor independence.auditor independence.

4 - 29©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

IndependenceIndependence

The value of auditing depends heavilyThe value of auditing depends heavilyon the public’s perception of theon the public’s perception of theindependence of auditors.independence of auditors.

The value of auditing depends heavilyThe value of auditing depends heavilyon the public’s perception of theon the public’s perception of theindependence of auditors.independence of auditors.

Independence in factIndependence in factIndependence in factIndependence in fact

Independence in appearanceIndependence in appearanceIndependence in appearanceIndependence in appearance

4 - 30©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Sarbanes-Oxley Act and SEC Sarbanes-Oxley Act and SEC Provisions Addressing Auditor Provisions Addressing Auditor IndependenceIndependence

The SEC adopted rules strengthening auditorThe SEC adopted rules strengthening auditorindependence in January 2003 Consistent withindependence in January 2003 Consistent withthe requirements of the Sarbanes-Oxley Act.the requirements of the Sarbanes-Oxley Act.

The SEC adopted rules strengthening auditorThe SEC adopted rules strengthening auditorindependence in January 2003 Consistent withindependence in January 2003 Consistent withthe requirements of the Sarbanes-Oxley Act.the requirements of the Sarbanes-Oxley Act.

The Sarbanes-Oxley Act and the revised SECThe Sarbanes-Oxley Act and the revised SECrules further restrict, but do not completelyrules further restrict, but do not completelyeliminate the type of nonaudit serviceseliminate the type of nonaudit servicesthat can be provided to the public.that can be provided to the public.

The Sarbanes-Oxley Act and the revised SECThe Sarbanes-Oxley Act and the revised SECrules further restrict, but do not completelyrules further restrict, but do not completelyeliminate the type of nonaudit serviceseliminate the type of nonaudit servicesthat can be provided to the public.that can be provided to the public.

4 - 31©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

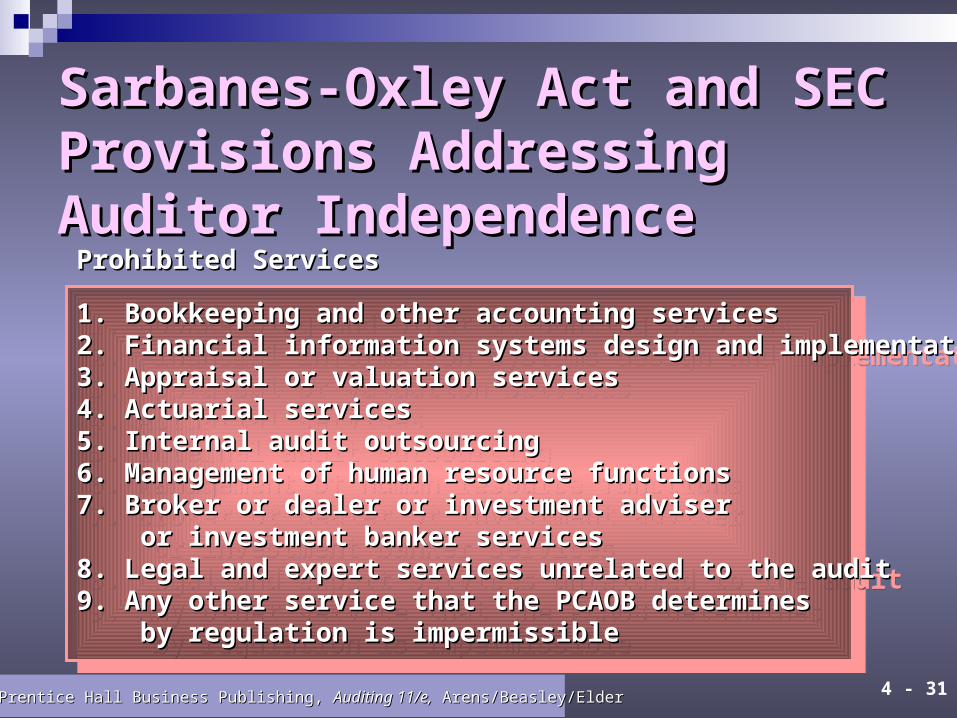

Sarbanes-Oxley Act and SEC Sarbanes-Oxley Act and SEC Provisions Addressing Auditor Provisions Addressing Auditor IndependenceIndependence

1. Bookkeeping and other accounting services1. Bookkeeping and other accounting services2. Financial information systems design and implementation2. Financial information systems design and implementation3. Appraisal or valuation services3. Appraisal or valuation services4. Actuarial services4. Actuarial services5. Internal audit outsourcing5. Internal audit outsourcing6. Management of human resource functions6. Management of human resource functions7. Broker or dealer or investment adviser7. Broker or dealer or investment adviser or investment banker servicesor investment banker services8. Legal and expert services unrelated to the audit8. Legal and expert services unrelated to the audit9. Any other service that the PCAOB determines9. Any other service that the PCAOB determines by regulation is impermissibleby regulation is impermissible

1. Bookkeeping and other accounting services1. Bookkeeping and other accounting services2. Financial information systems design and implementation2. Financial information systems design and implementation3. Appraisal or valuation services3. Appraisal or valuation services4. Actuarial services4. Actuarial services5. Internal audit outsourcing5. Internal audit outsourcing6. Management of human resource functions6. Management of human resource functions7. Broker or dealer or investment adviser7. Broker or dealer or investment adviser or investment banker servicesor investment banker services8. Legal and expert services unrelated to the audit8. Legal and expert services unrelated to the audit9. Any other service that the PCAOB determines9. Any other service that the PCAOB determines by regulation is impermissibleby regulation is impermissible

Prohibited ServicesProhibited Services

4 - 32©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Audit CommitteesAudit Committees

An audit committee is a selected numberAn audit committee is a selected numberof members of a company’s board of directorsof members of a company’s board of directorswhose responsibilities include helpingwhose responsibilities include helpingauditors remain independent of management.auditors remain independent of management.

An audit committee is a selected numberAn audit committee is a selected numberof members of a company’s board of directorsof members of a company’s board of directorswhose responsibilities include helpingwhose responsibilities include helpingauditors remain independent of management.auditors remain independent of management.

Most audit committees are made up of threeMost audit committees are made up of threeto five or sometimes as many as sevento five or sometimes as many as sevendirectors who are not a part of companydirectors who are not a part of companymanagementmanagement

Most audit committees are made up of threeMost audit committees are made up of threeto five or sometimes as many as sevento five or sometimes as many as sevendirectors who are not a part of companydirectors who are not a part of companymanagementmanagement

4 - 33©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Audit CommitteesAudit Committees

The Sarbanes-Oxley Act requires that allThe Sarbanes-Oxley Act requires that allmembers of the audit committeemembers of the audit committeebe independent.be independent.

The Sarbanes-Oxley Act requires that allThe Sarbanes-Oxley Act requires that allmembers of the audit committeemembers of the audit committeebe independent.be independent.

Companies must disclose whether or notCompanies must disclose whether or notthe audit committee includes at leastthe audit committee includes at leastone financial expert.one financial expert.

Companies must disclose whether or notCompanies must disclose whether or notthe audit committee includes at leastthe audit committee includes at leastone financial expert.one financial expert.

4 - 34©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Conflicts Arising from Conflicts Arising from Employment RelationshipsEmployment Relationships

The SEC has added a one year “cooling off ”The SEC has added a one year “cooling off ”period before a member of the auditperiod before a member of the auditengagement team can work for theengagement team can work for theclient in certain key management positions.client in certain key management positions.

The SEC has added a one year “cooling off ”The SEC has added a one year “cooling off ”period before a member of the auditperiod before a member of the auditengagement team can work for theengagement team can work for theclient in certain key management positions.client in certain key management positions.

4 - 35©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Partner RotationPartner Rotation

The Sarbanes-Oxley Act requires thatThe Sarbanes-Oxley Act requires thatthe lead and concurring audit partnerthe lead and concurring audit partnerrotate off the audit engagement rotate off the audit engagement after a period of five years.after a period of five years.

The Sarbanes-Oxley Act requires thatThe Sarbanes-Oxley Act requires thatthe lead and concurring audit partnerthe lead and concurring audit partnerrotate off the audit engagement rotate off the audit engagement after a period of five years.after a period of five years.

4 - 36©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Ownership InterestsOwnership Interests

SEC rules adopted in 2000 on financialSEC rules adopted in 2000 on financialrelationships narrow the restrictions onrelationships narrow the restrictions onownership in clients to those personsownership in clients to those personswho can influence the audit.who can influence the audit.

SEC rules adopted in 2000 on financialSEC rules adopted in 2000 on financialrelationships narrow the restrictions onrelationships narrow the restrictions onownership in clients to those personsownership in clients to those personswho can influence the audit.who can influence the audit.

4 - 37©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Independence Standards BoardIndependence Standards Board

It was dissolved in July 2001.It was dissolved in July 2001.It was dissolved in July 2001.It was dissolved in July 2001.

ISB pronouncements and interpretationsISB pronouncements and interpretationsremain enforceable unless they conflictremain enforceable unless they conflictwith the independence rulingswith the independence rulingsissued by the SEC.issued by the SEC.

ISB pronouncements and interpretationsISB pronouncements and interpretationsremain enforceable unless they conflictremain enforceable unless they conflictwith the independence rulingswith the independence rulingsissued by the SEC.issued by the SEC.

4 - 38©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Other IssuesOther Issues

Shopping for accounting principlesShopping for accounting principlesShopping for accounting principlesShopping for accounting principles

Engagement and payment ofEngagement and payment ofaudit fees by managementaudit fees by management

Engagement and payment ofEngagement and payment ofaudit fees by managementaudit fees by management

4 - 39©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 6Learning Objective 6

Apply the AICPA Apply the AICPA CodeCode rules and rules and

interpretations on independenceinterpretations on independence

and explain their importance.and explain their importance.

4 - 40©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Rules of ConductRules of Conduct

Rule 101 – IndependenceRule 101 – IndependenceRule 101 – IndependenceRule 101 – Independence

A member in public practice shall beA member in public practice shall beindependent in the performance ofindependent in the performance ofprofessional services as required byprofessional services as required bystandards promulgated by bodiesstandards promulgated by bodiesdesignated by Council.designated by Council.

A member in public practice shall beA member in public practice shall beindependent in the performance ofindependent in the performance ofprofessional services as required byprofessional services as required bystandards promulgated by bodiesstandards promulgated by bodiesdesignated by Council.designated by Council.

4 - 41©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Financial InterestsFinancial Interests

Interpretations of Rule 101 prohibitInterpretations of Rule 101 prohibitcovered members from owning anycovered members from owning anydirect investments in audit clients.direct investments in audit clients.

Interpretations of Rule 101 prohibitInterpretations of Rule 101 prohibitcovered members from owning anycovered members from owning anydirect investments in audit clients.direct investments in audit clients.

Covered membersCovered membersCovered membersCovered members

Direct versus indirect financial interestDirect versus indirect financial interestDirect versus indirect financial interestDirect versus indirect financial interest

Material or immaterialMaterial or immaterialMaterial or immaterialMaterial or immaterial

4 - 42©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Related FinancialRelated FinancialInterests IssuesInterests Issues

Former practitionersFormer practitioners Normal lending proceduresNormal lending procedures Financial interests and employmentFinancial interests and employment of immediate and close familyof immediate and close family Joint investor or investeeJoint investor or investee relationship with clientrelationship with client Director, officer, management,Director, officer, management, or employee of a companyor employee of a company

Former practitionersFormer practitioners Normal lending proceduresNormal lending procedures Financial interests and employmentFinancial interests and employment of immediate and close familyof immediate and close family Joint investor or investeeJoint investor or investee relationship with clientrelationship with client Director, officer, management,Director, officer, management, or employee of a companyor employee of a company

4 - 43©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Litigation Between CPA FirmLitigation Between CPA Firmand Clientand Client

A lawsuit or intent to start a lawsuitA lawsuit or intent to start a lawsuitbetween a CPA firm and its client is abetween a CPA firm and its client is aviolation of Rule 101 for the current audit.violation of Rule 101 for the current audit.

A lawsuit or intent to start a lawsuitA lawsuit or intent to start a lawsuitbetween a CPA firm and its client is abetween a CPA firm and its client is aviolation of Rule 101 for the current audit.violation of Rule 101 for the current audit.

4 - 44©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Bookkeeping and Other ServicesBookkeeping and Other Services

The AICPA The AICPA CodeCode permits a CPA firmpermits a CPA firmto do both bookkeeping and auditingto do both bookkeeping and auditingfor the same client.for the same client.

The AICPA The AICPA CodeCode permits a CPA firmpermits a CPA firmto do both bookkeeping and auditingto do both bookkeeping and auditingfor the same client.for the same client.

4 - 45©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Bookkeeping and Other ServicesBookkeeping and Other Services

1. Client must accept full responsibility1. Client must accept full responsibility for the financial statements.for the financial statements.

1. Client must accept full responsibility1. Client must accept full responsibility for the financial statements.for the financial statements.

2. The CPA must not assume the role2. The CPA must not assume the role of employee or of management.of employee or of management.

2. The CPA must not assume the role2. The CPA must not assume the role of employee or of management.of employee or of management.

3. The audit must conform to GASS.3. The audit must conform to GASS.3. The audit must conform to GASS.3. The audit must conform to GASS.

4 - 46©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Bookkeeping and Other ServicesBookkeeping and Other Services

The SEC does not allow audit firmsThe SEC does not allow audit firmsto provide bookkeeping servicesto provide bookkeeping servicesto public company audit clients.to public company audit clients.

The SEC does not allow audit firmsThe SEC does not allow audit firmsto provide bookkeeping servicesto provide bookkeeping servicesto public company audit clients.to public company audit clients.

Consulting and other nonaudit servicesConsulting and other nonaudit servicesConsulting and other nonaudit servicesConsulting and other nonaudit services

Unpaid feesUnpaid feesUnpaid feesUnpaid fees

4 - 47©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 7Learning Objective 7

Understand the requirements ofUnderstand the requirements of

other rules under the AICPA other rules under the AICPA CodeCode..

4 - 48©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Other Rules of ConductOther Rules of Conduct

102 – Integrity and objectivity102 – Integrity and objectivity201 – General standards201 – General standards202 – Compliance with standards202 – Compliance with standards203 – Accounting principles203 – Accounting principles301 – Confidential client information301 – Confidential client information

102 – Integrity and objectivity102 – Integrity and objectivity201 – General standards201 – General standards202 – Compliance with standards202 – Compliance with standards203 – Accounting principles203 – Accounting principles301 – Confidential client information301 – Confidential client information

4 - 49©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Other Rules of ConductOther Rules of Conduct

302 – Contingent fees302 – Contingent fees501 – Acts discreditable501 – Acts discreditable502 – Advertising and other forms502 – Advertising and other forms

of solicitationof solicitation503 – Commissions and referral fees503 – Commissions and referral fees505 – Form of organization and name505 – Form of organization and name

302 – Contingent fees302 – Contingent fees501 – Acts discreditable501 – Acts discreditable502 – Advertising and other forms502 – Advertising and other forms

of solicitationof solicitation503 – Commissions and referral fees503 – Commissions and referral fees505 – Form of organization and name505 – Form of organization and name

4 - 50©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 8Learning Objective 8

Describe the enforcementDescribe the enforcement

mechanisms for the rulesmechanisms for the rules

of conduct.of conduct.

4 - 51©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

EnforcementEnforcement

Action by AICPAAction by AICPAProfessional Ethics DivisionProfessional Ethics Division

Action by AICPAAction by AICPAProfessional Ethics DivisionProfessional Ethics Division

Action by a state BoardAction by a state Boardof Accountancyof Accountancy

Action by a state BoardAction by a state Boardof Accountancyof Accountancy

4 - 52©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

End of Chapter 4End of Chapter 4