Embed Size (px)

Citation preview

Annual Meeting April 14, 2016

Note: All financial disclosure in this presentation is, unless otherwise noted, in US$

Forward-Looking Statements

Certain statements contained herein may constitute forward-looking information (within the meaning of Canadian securities legislation) and forward-looking statements (within the meaning of the United States Private Securities Litigation Reform Act of 1995). These statements can be identified by expressions of belief, expectation or intention, as well as those statements that are not historical fact. Forward-looking statements are based upon assumptions, estimates, opinions and analysis made by management in light of its experience, current conditions and its expectations of future developments that management believe to be reasonable and relevant, and are subject to known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Fairfax to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, but are not limited to: a reduction in net earnings if our loss reserves are insufficient; underwriting losses on the risks we insure that are higher or lower than expected; the occurrence of catastrophic events with a frequency or severity exceeding our estimates; changes in market variables, including interest rates, foreign exchange rates, equity prices and credit spreads, which could negatively affect our investment portfolio; the cycles of the insurance market and general economic conditions, which can substantially influence our and our competitors' premium rates and capacity to write new business; insufficient reserves for asbestos, environmental and other latent claims; exposure to credit risk in the event our reinsurers fail to make payments to us under our reinsurance arrangements; exposure to credit risk in the event our insureds, insurance producers or reinsurance intermediaries fail to remit premiums that are owed to us or failure by our insureds to reimburse us for deductibles that are paid by us on their behalf; the timing of claims payments being sooner or the receipt of reinsurance recoverables being later than anticipated by us; the inability of our subsidiaries to maintain financial or claims paying ability ratings; risks associated with implementing our business strategies; risks associated with our use of derivative instruments; the failure of our hedging methods to achieve their desired risk management objective; a decrease in the level of demand for insurance or reinsurance products, or increased competition in the insurance industry; the impact of emerging claim and coverage issues; the failure of any of the loss limitation methods we employ; our inability to access cash of our subsidiaries; our inability to obtain required levels of capital on favourable terms, if at all; the loss of key employees; technological or other change which adversely impacts demand, or the premiums payable, for the insurance coverages we offer; our inability to obtain reinsurance coverage in sufficient amounts, at reasonable prices or on terms that adequately protect us; the passage of legislation subjecting our businesses to additional supervision or regulation, including additional tax regulation, in the United States, Canada or other jurisdictions in which we operate; risks associated with government investigations of, and litigation and negative publicity related to, insurance industry practice or any other conduct; risks associated with political and other developments in foreign jurisdictions in which we operate; risks associated with legal or regulatory proceedings; failures or security breaches of our computer and data processing systems; the influence exercisable by our significant shareholder; adverse fluctuations in foreign currency exchange rates; our dependence on independent brokers over whom we exercise little control; an impairment in the carrying value of our goodwill and indefinite-lived intangible assets; our failure to realize deferred income tax assets; and assessments and shared market mechanisms which may adversely affect our U.S. insurance subsidiaries. We caution readers not to place undue reliance on these forward-looking statements, which speak only as of their dates. We disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, change in assumption or opinion or otherwise, except as may be required by applicable securities laws. Additional risks and uncertainties are described in our most recently issued Annual Report which is available at www.fairfax.ca and in our Supplemental and Base Shelf Prospectus (under “Risk Factors”) filed with the securities regulatory authorities in Canada, which is available on SEDAR at www.sedar.com.

Guiding Principles

Objectives

We expect to compound our book value per share over the

long term by 15% annually by running Fairfax and its

subsidiaries for the long term benefit of customers,

employees and shareholders – at the expense of short term

profits if necessary

Our focus is long term growth in book value per share and

not quarterly earnings. We plan to grow through internal

means as well as through friendly acquisitions

We always want to be soundly financed

We provide complete disclosure annually to our

shareholders

3

Guiding Principles

Structure

Our companies are decentralized and run by the presidents

except for performance evaluation, succession planning,

acquisitions and financing, which are done by or with

Fairfax. Cooperation among companies is encouraged to

the benefit of Fairfax in total

Complete and open communication between Fairfax and its

subsidiaries is an essential requirement at Fairfax

Share ownership and large incentives are encouraged

across the Group

Fairfax head office will always be a very small holding

company and not an operating company

4

Guiding Principles

Values

Honesty and integrity are essential in all of our relationships and will never be compromised

We are results-oriented — not political

We are team players — no "egos”. A confrontational style is not appropriate. We value loyalty — to Fairfax and our colleagues

We are hard working but not at the expense of our families

We always look at opportunities but emphasize downside protection and look for ways to minimize loss of capital

We are entrepreneurial. We encourage calculated risk-taking. It is all right to fail but we should learn from our mistakes

We will never bet the company on any project or acquisition

We believe in having fun — at work! 5

Fairfax – 30 Years

Value Creation

6

403

475

22 -

100

200

300

400

500

600

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Book Value

Fairfax share price (USD)

S&P 500 index

30 Year Compound Annual Growth Rate

Fairfax book value per share – 20.4%

Fairfax share price (USD) – 19.4%

S&P 500 Index – 7.9%

Fairfax – 30 Years

Then and Now

1985 2015 Growth

Insurance premiums (net) 10 million 7.5 billion 752x

Investment portfolios 24 million 29 billion 1,214x

Common shareholders’ equity 8 million 9 billion 1,178x

Shares outstanding 5 million 22 million 4.4x

Per share

Insurance premiums $ 2.00 $ 339 169x

Investment portfolios 4.80 1,306 272x

Book value 1.52 403 265x

Stock price (Cdn$) 3.25 657 202x

7

1985 2015 Growth

Insurance premiums (net) 10 million 7.5 billion 752x

Investment portfolios 24 million 29 billion 1,214x

Common shareholders’ equity 8 million 9 billion 1,178x

Shares outstanding 5 million 22 million 4.4x

Per share

Insurance premiums $ 2.00 $ 339 169x

Investment portfolios 4.80 1,306 272x

Book value 1.52 403 265x

Stock price (Cdn$) 3.25 657 202x

Fairfax – 30 Years

Financial Results

(1) Includes dividends paid

Growth in Average Average Total

5 Years Book Value Combined Return on

Ended per Share(1) Ratio Investments

1990 58% 107% 10%

1995 21% 104% 10%

2000 31% 114% 9%

2005 (1%) 105% 9%

2010 24% 100% 11%

2015 4% 97% 3%

8

Historic Performance vs. Peer Group

Compound Growth in Book Value per Share (30 Years: since Fairfax’s inception) (1)

(1) Except for S&P 500 and TSX which are compound index returns excluding dividends

9

20.4%

16.4% 15.9%

14.0%

12.5% 12.4%

9.9%8.8%

7.9%

5.1%

10

Historic Performance vs. Peer Group

Compound Growth in Book Value per Share (5 Years ending 2015) (1)

(1) Except for S&P 500 and TSX which are compound index returns excluding dividends

11.5%

10.3% 10.2% 9.9% 9.7% 9.6%

7.3% 7.0%6.5% 6.4%

5.6% 5.5% 5.5%

3.0%

1.4%

-0.7%

23

%

11

%

10

%

8%

7

%

6%

5%

5

%

3%

3

%

3%

3%

2

%

(1%

) (3

%)

(3%

)

(3%

)

(4%

)

(5%

) (5

%)

(6%

)

(7%

)

(7%

) (8

%)

(8%

) (9

%)

(9%

) (1

2%

)

(13

%)

(14

%)

(14

%)

(14

%)

(15

%)

(16

%)

(17

%)

(18

%)

(18

%)

(19

%)

(19

%)

(19

%)

(22

%)

(24

%)

(31

%)

(32

%)

(37

%)

(37

%)

(43

%)

(48

%)

(65

%)

(10

0%

)

SOURCE: Dowling & Partners, IBNR #12

Fairfax and AIG calculated using the same methodology as Dowling & Partners, based on company data (AIG excludes government financing) 11

2008 Change in Book Value per Share

($ millions)

(1) Includes: non-insurance operations, runoff operating income, interest expense and corporate overhead & other

Sources of Net Earnings in 2015

Unrealized investment losses (1,811)

Hedging gains 502

Pre-tax income 625

Net earnings 642

12

Underwriting profit – (combined ratio of 89.9%) 705

Investment income – insurance and reinsurance 477

Operating income 1,182

Other (1) (298)

Realized investment gains 1,050

Pre-tax income including realized investment gains 1,934

Underwriting Results in 2015

13

Combined Underwriting

Ratio Profit

($ millions)

Northbridge 91.8% 72

Crum & Forster 97.7% 35

Zenith 82.5% 134

Brit (1) 94.9% 46

OdysseyRe 84.7% 337

Fairfax Asia 87.9% 35

Other Insurance and Reinsurance 89.6% 46

Consolidated 89.9% 705

(1) For the period since its acquisition on June 5, 2015

Net Gains on Investments 2010-2015

14

Equity and equity related investments

Equity hedges

Net equity

Bonds

CPI-linked derivatives

Other

4.2

(1.2)

3.0

1.7

0.0

0.1

4.8

(Losses)($ billions)

Realized

Gains

(1.4)

(2.0)

(3.4)

0.2

(0.4)

0.0

(3.6)

(Losses)($ billions)

Unrealized

Gains

2.8

(3.2)

(0.4)

1.9

(0.4)

0.1

1.2

(Losses)($ billions)

Net

Gains

Cost of Hedging

15

($ billions) 2010 2011 2012 2013 2014 2015 Total

Equity hedges (0.9) 0.4 (1.0) (2.0) (0.2) 0.5 (3.2)

CPI-linked derivatives 0.0 (0.2) (0.1) (0.1) 0.0 0.0 (0.4)

Total (0.9) 0.2 (1.1) (2.1) (0.2) 0.5 (3.6)

Importance of Float

16

Total Float Total Investments

($ millions) Per Share

1985 13 $ 2½

1990 164 30

1995 653 74

2000 5,877 449

2005 8,757 492

2010 13,110 641

2015 17,072 769

CAGR 21.5%

Total Investments

($ millions) Per Share

24 $ 5

289 53

1,222 138

10,400 794

14,869 835

23,300 1,139

29,016 1,306

20.5%

17

International Operations

(1) Full year 2015 premium

(2) Including Fairfax Eastern Europe

(3) For the 12 months ended September 30, 2015

ICICI Lombard (India)(3) 1,170 26% 299

Alltrust Insurance (China)(3) 1,063 15% 159

Gulf Insurance (Middle East)(3) 608 41% 252

BIC (Vietnam) 70 35% 25

Falcon Insurance (Thailand) 48 41% 20

2,959 755

Gross Fairfax's Share of

Premiums Gross Premiums

Written Ownership Written

($ millions) ($ millions)

Brit(1) 1,999 70% 1,400

First Capital (Singapore) 399 98% 390

Advent 241 100% 241

Fairfax Brasil 123 100% 123

Polish Re(2) 114 100% 114

Pacific Insurance (Malaysia) 108 100% 108

Falcon Insurance (Hong Kong) 69 100% 69

Union Assurance (Sri Lanka) 43 78% 34

Fairfax Indonesia 34 80% 28

3,130 2,507

Total 6,089 3,262

Runoff

18

RiverStone is one of the premier runoff groups in the world

Many successful runoff acquisitions

General Fidelity

Eagle Star

Brit Insurance

American Safety

Average return on acquisitions greater than 25%

397 employees: 265 in the United States and 132 in the United Kingdom

Cumulative pre-tax profit of $1.1 billion since 2007

Restaurant Business

19

2012 2013 2014 2015 2016

3rd largest restaurant group in Canada

Exceptional management led by Bill Gregson

Financially strong

Prime Restaurants

Purchase Price: $57

Ownership: 82%

Merger of Cara/Prime

Investment: $100

Prime Contribution: $57

Bill Gregson joined as President

Keg Restaurants

Purchase: $85

Ownership: 51%

Cara IPO

Fairfax MV: $458

Ownership: 41%

Cara Dec. 31, 2015

Fairfax MV: $600

Cara

Purchases

St-Hubert

(Cdn$ millions)

The McEwan Group

Ownership: 45%

Gains (Losses) Per Share

($ millions)

1985 0.5 10¢

2008 2,144 $ 118

2009 1,981 $ 108

2010 (3) -

2011 691 $ 34

2012 643 $ 31

2013 (1,564) $ (77)

2014 1,736 $ 80

2015 (259) $ (12)

Cumulative Gains $11.4 billion

Pre-Tax Realized and Unrealized Gains

20

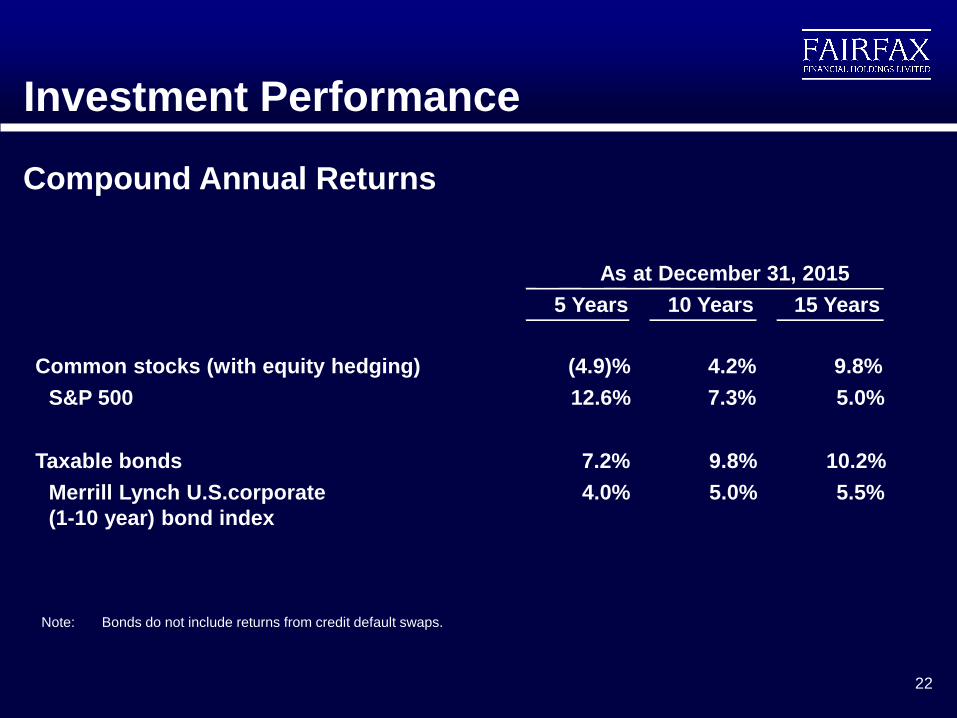

Investment Performance

21

5 Years 10 Years 15 Years

December 31, 2015

Common stocks (with equity hedging) (4.9%) 4.2% 9.8%

S&P 500 12.6% 7.3% 5.0%

December 31, 2014

Common stocks (with equity hedging) (2.7%) 6.5% 11.6%

S&P 500 15.5% 7.7% 4.2%

December 31, 2013

Common stocks (with equity hedging) 3.2% 7.6% 13.5%

S&P 500 17.9% 7.4% 4.7%

December 31, 2012

Common stocks (with equity hedging) 5.5% 14.5% 13.5%

S&P 500 1.7% 7.1% 4.5%

Compound Annual Returns

5 Years 10 Years 15 Years

December 31, 2015

Common stocks (with equity hedging) (4.9%) 4.2% 9.8%

S&P 500 12.6% 7.3% 5.0%

December 31, 2014

Common stocks (with equity hedging) (2.7%) 6.5% 11.6%

S&P 500 15.5% 7.7% 4.2%

December 31, 2013

Common stocks (with equity hedging) 3.2% 7.6% 13.5%

S&P 500 17.9% 7.4% 4.7%

December 31, 2012

Common stocks (with equity hedging) 5.5% 14.5% 13.5%

S&P 500 1.7% 7.1% 4.5%

Compound Annual Returns

5 Years 10 Years 15 Years

December 31, 2015

Common stocks (with equity hedging) (4.9%) 4.2% 9.8%

S&P 500 12.6% 7.3% 5.0%

December 31, 2014

Common stocks (with equity hedging) (2.7%) 6.5% 11.6%

S&P 500 15.5% 7.7% 4.2%

December 31, 2013

Common stocks (with equity hedging) 3.2% 7.6% 13.5%

S&P 500 17.9% 7.4% 4.7%

December 31, 2012

Common stocks (with equity hedging) 5.5% 14.5% 13.5%

S&P 500 1.7% 7.1% 4.5%

Compound Annual Returns

5 Years 10 Years 15 Years

December 31, 2015

Common stocks (with equity hedging) (4.9%) 4.2% 9.8%

S&P 500 12.6% 7.3% 5.0%

December 31, 2014

Common stocks (with equity hedging) (2.7%) 6.5% 11.6%

S&P 500 15.5% 7.7% 4.2%

December 31, 2013

Common stocks (with equity hedging) 3.2% 7.6% 13.5%

S&P 500 17.9% 7.4% 4.7%

December 31, 2012

Common stocks (with equity hedging) 5.5% 14.5% 13.5%

S&P 500 1.7% 7.1% 4.5%

Compound Annual Returns

5 Years 10 Years 15 Years

December 31, 2015

Common stocks (with equity hedging) (4.9%) 4.2% 9.8%

S&P 500 12.6% 7.3% 5.0%

December 31, 2014

Common stocks (with equity hedging) (2.7%) 6.5% 11.6%

S&P 500 15.5% 7.7% 4.2%

December 31, 2013

Common stocks (with equity hedging) 3.2% 7.6% 13.5%

S&P 500 17.9% 7.4% 4.7%

December 31, 2012

Common stocks (with equity hedging) 5.5% 14.5% 13.5%

S&P 500 1.7% 7.1% 4.5%

Compound Annual Returns

Investment Performance

Compound Annual Returns

Note: Bonds do not include returns from credit default swaps.

Common stocks (with equity hedging) (4.9)% 4.2% 9.8%

S&P 500 12.6% 7.3% 5.0%

Taxable bonds 7.2% 9.8% 10.2%

Merrill Lynch U.S.corporate

(1-10 year) bond index

4.0% 5.0% 5.5%

5 Years 10 Years 15 Years

As at December 31, 2015

22

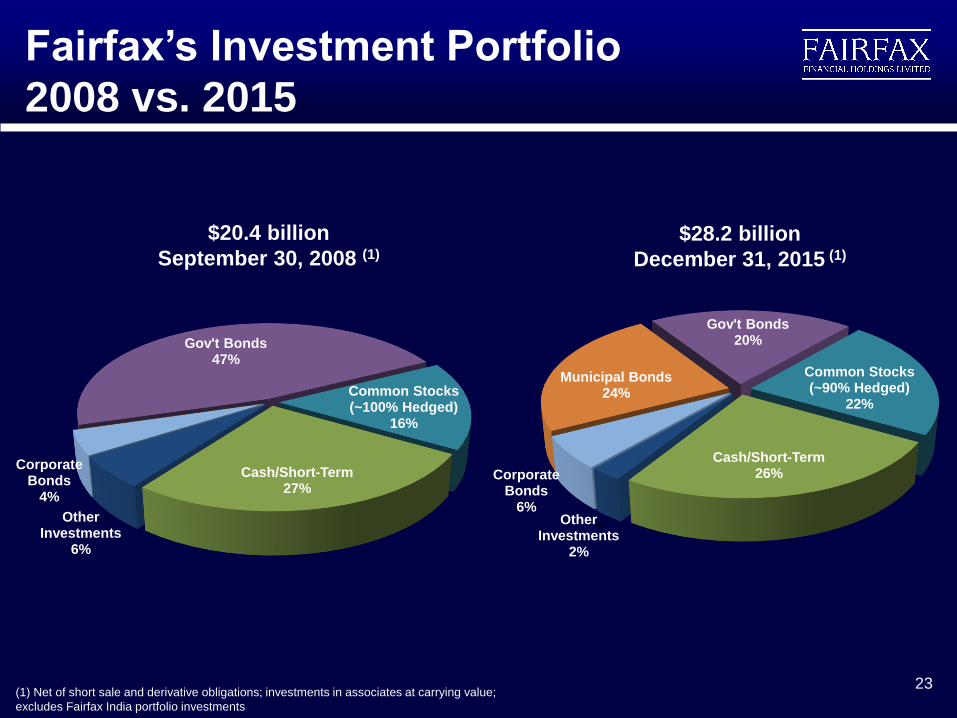

Fairfax’s Investment Portfolio

2008 vs. 2015

23 (1) Net of short sale and derivative obligations; investments in associates at carrying value;

excludes Fairfax India portfolio investments

$28.2 billion

December 31, 2015 (1)

$20.4 billion

September 30, 2008 (1)

Cash/Short-Term26%

Other Investments

2%

Corporate Bonds

6%

Municipal Bonds24%

Gov't Bonds20%

Common Stocks(~90% Hedged)

22%

Cash/Short-Term27%

Other Investments

6%

Corporate Bonds

4%

Gov't Bonds47%

Common Stocks(~100% Hedged)

16%

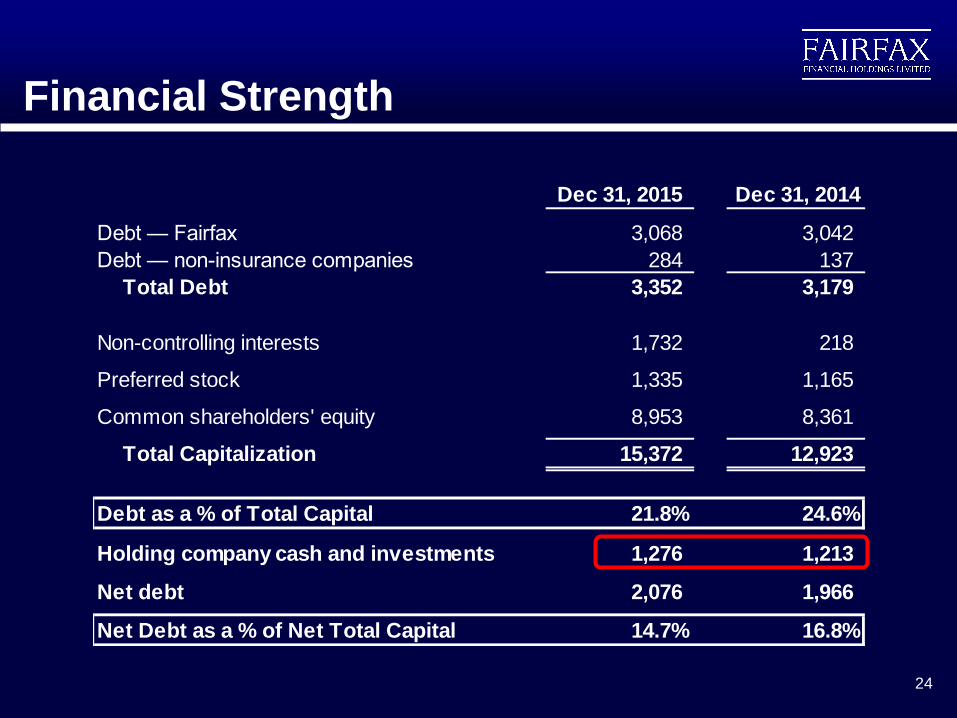

Dec 31, 2015 Dec 31, 2014

Debt — Fairfax 3,068 3,042

Debt — non-insurance companies 284 137

Total Debt 3,352 3,179

Non-controlling interests 1,732 218

Preferred stock 1,335 1,165

Common shareholders' equity 8,953 8,361

Total Capitalization 15,372 12,923

Debt as a % of Total Capital 21.8% 24.6%

Holding company cash and investments 1,276 1,213

Net debt 2,076 1,966

Net Debt as a % of Net Total Capital 14.7% 16.8%

24

Financial Strength

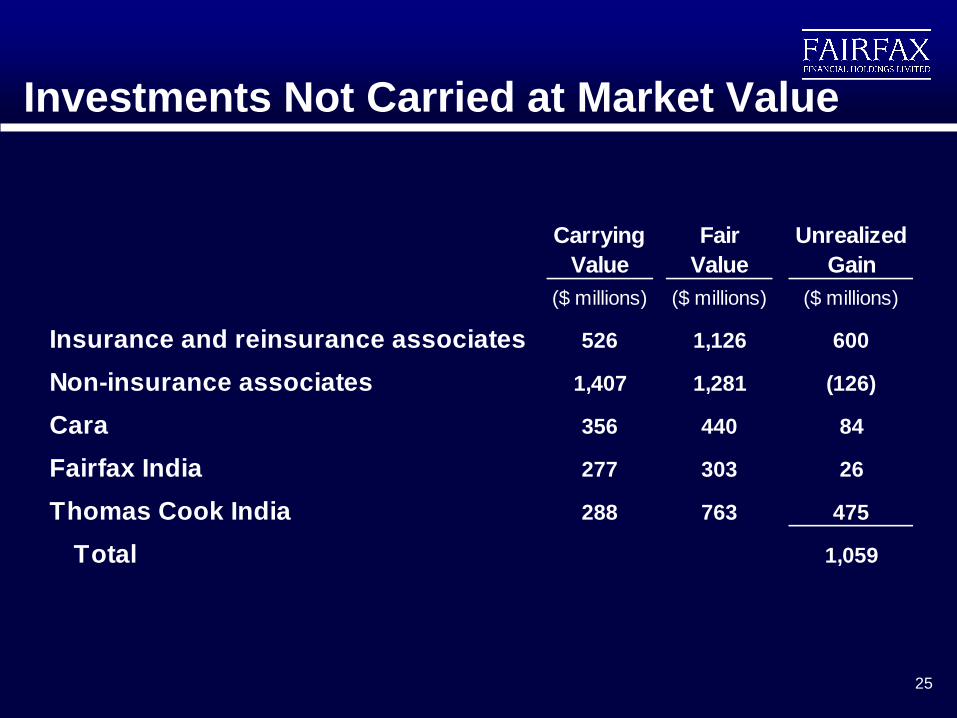

Investments Not Carried at Market Value

25

Carrying

Value

Fair

Value

Unrealized

Gain

($ millions) ($ millions) ($ millions)

Insurance and reinsurance associates 526 1,126 600

Non-insurance associates 1,407 1,281 (126)

Cara 356 440 84

Fairfax India 277 303 26

Thomas Cook India 288 763 475

Total 1,059

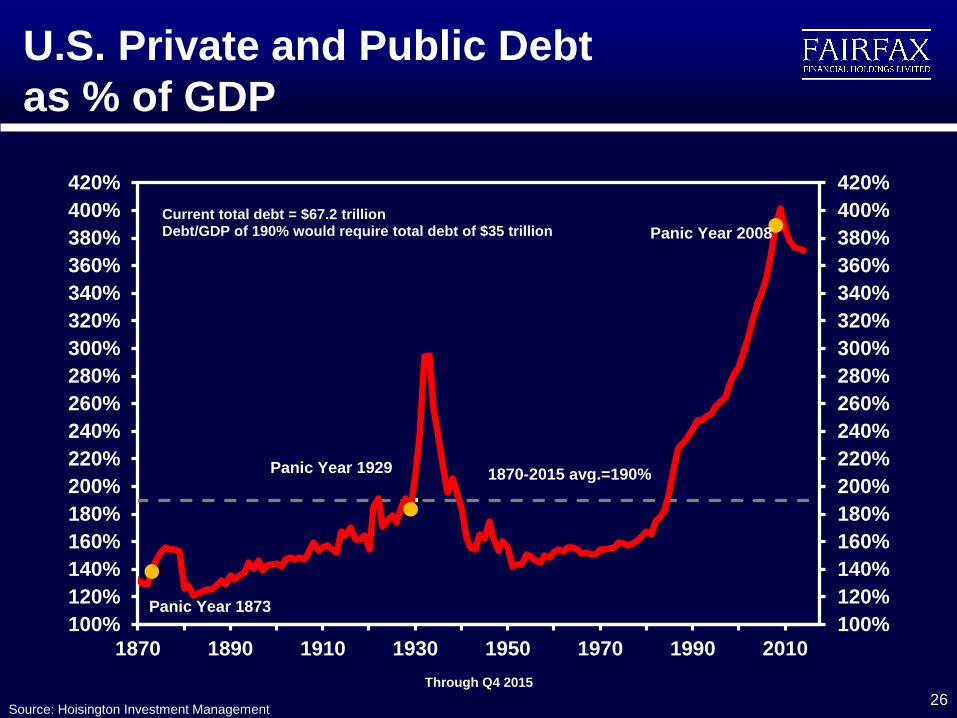

U.S. Private and Public Debt

as % of GDP

26 Source: Hoisington Investment Management

Through Q4 2015

100%

120%

140%

160%

180%

200%

220%

240%

260%

280%

300%

320%

340%

360%

380%

400%

420%

100%

120%

140%

160%

180%

200%

220%

240%

260%

280%

300%

320%

340%

360%

380%

400%

420%

1870 1890 1910 1930 1950 1970 1990 2010

Panic Year 2008

Panic Year 1929

Panic Year 1873

1870-2015 avg.=190%

Current total debt = $67.2 trillionDebt/GDP of 190% would require total debt of $35 trillion

27

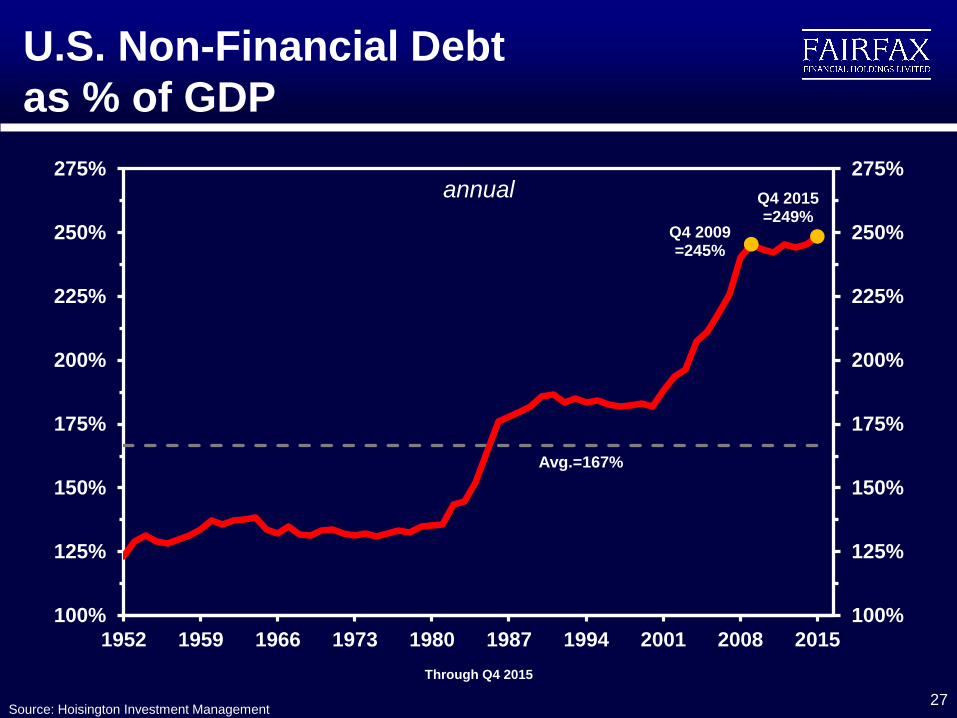

U.S. Non-Financial Debt

as % of GDP

Source: Hoisington Investment Management

annual

Through Q4 2015

100%

125%

150%

175%

200%

225%

250%

275%

100%

125%

150%

175%

200%

225%

250%

275%

1952 1959 1966 1973 1980 1987 1994 2001 2008 2015

Avg.=167%

Q4 2009=245%

Q4 2015=249%

0%

100%

200%

300%

400%

500%

600%

700%

1979 1983 1987 1991 1995 1999 2003 2007 2011 2015

0%

100%

200%

300%

400%

500%

600%

700%

Canada

U.S.

Eurozone

U.K

Japan

Australia

China

250%-275%

28

Total Public and Private Debt

as a % of GDP – Major Countries

Source: Hoisington Investment Management

annual

Through Q3 2015, except U.S. which is through Q4 2015.

29

Velocity of Money 1900-2015

Equation of Exchange: GDP (nominal) = M*V

Source: Hoisington Investment Management

annual

1.00

1.25

1.50

1.75

2.00

2.25

1.00

1.25

1.50

1.75

2.00

2.25

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

1918 = 2.0

1946 = 1.2

1997 = 2.2

1.49

Avg. 1900 to present = 1.73

Avg. 1953 to 1983 = 1.75

30

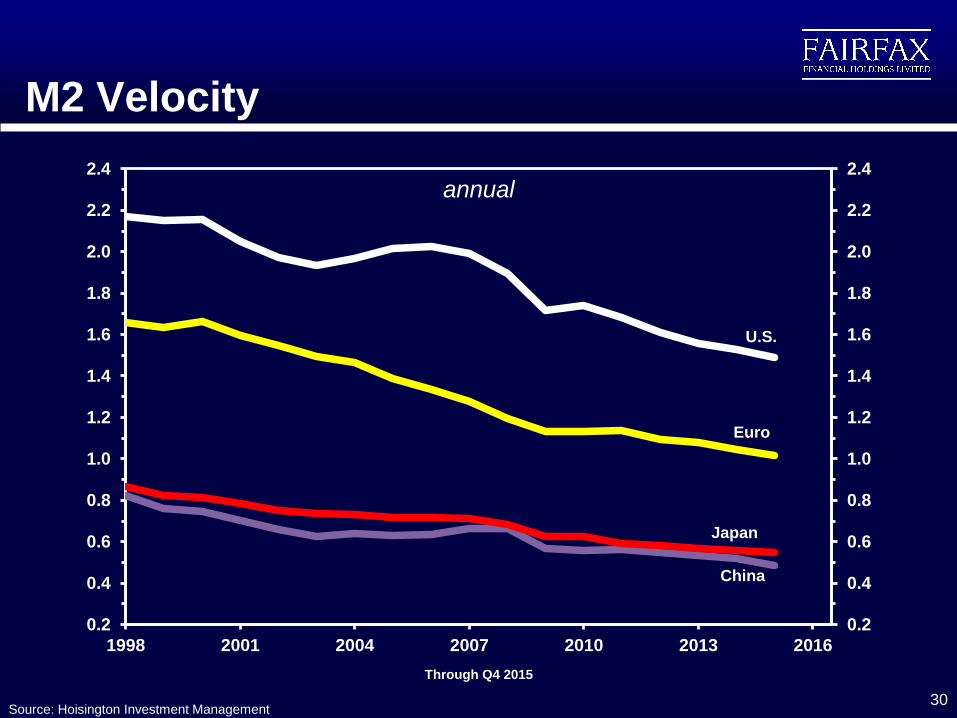

M2 Velocity

Source: Hoisington Investment Management

annual

Through Q4 2015

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

1998 2001 2004 2007 2010 2013 2016

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

China

U.S.

Euro

Japan

0%

1%

2%

3%

4%

5%

6%

7%

0%

1%

2%

3%

4%

5%

6%

7%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Long Term Government Bond Yields

Following Historic Panic Years

U.S. 2008

U.S. 1929

Japan 1989

31 Source: Hoisington Investment Management

annual average

32

U.S., Germany and Japan

Long Term Government Yields

Source: Bloomberg

Quarterly through Q1 2016

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

1994 1997 2000 2003 2006 2009 2012 2015

GER 30 YR UST 30 YR JAP 20 YR

Source: Bloomberg

Current RatesU.S. 2.6%

Germany 0.8%Japan 0.4%

33

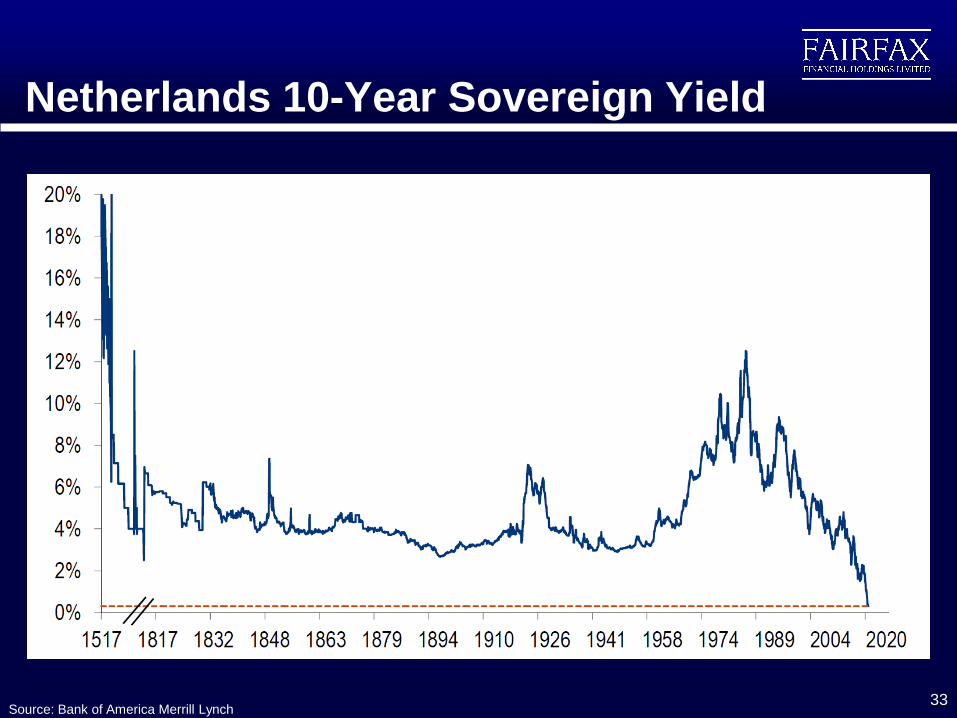

Netherlands 10-Year Sovereign Yield

Source: Bank of America Merrill Lynch

34

0

5

10

15

20

25

30

35

40

45

50

0

5

10

15

20

25

30

35

40

45

50

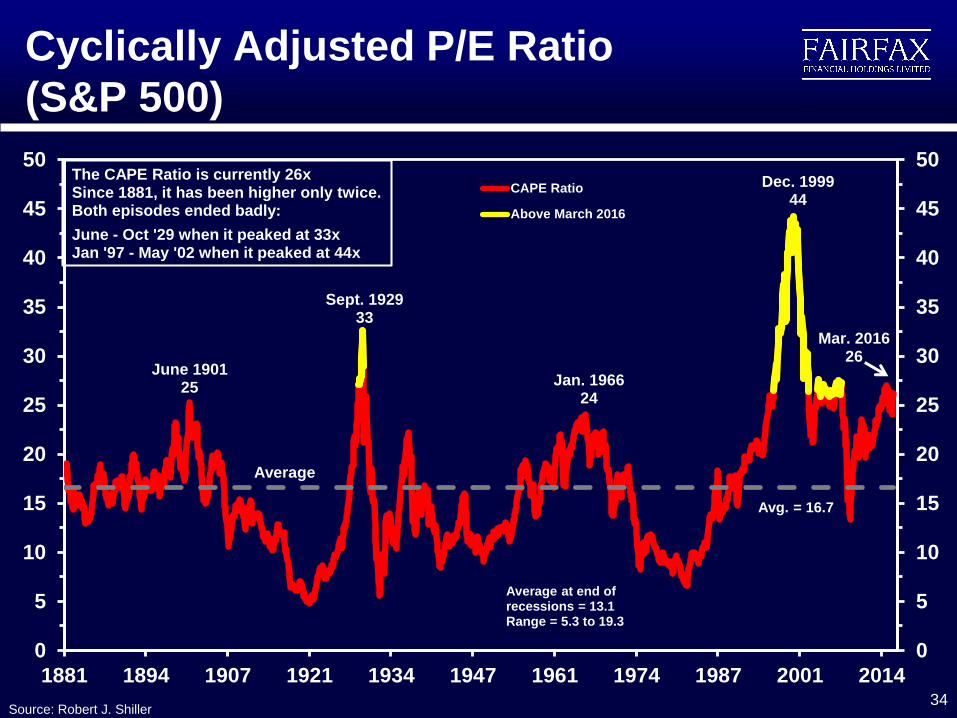

1881 1894 1907 1921 1934 1947 1961 1974 1987 2001 2014

CAPE Ratio

Above March 2016

June 190125

Sept. 192933

Jan. 196624

Dec. 199944

Average at end of recessions = 13.1Range = 5.3 to 19.3

Average

Avg. = 16.7

The CAPE Ratio is currently 26xSince 1881, it has been higher only twice. Both episodes ended badly:

June - Oct '29 when it peaked at 33xJan '97 - May '02 when it peaked at 44x

Mar. 201626

Cyclically Adjusted P/E Ratio

(S&P 500)

Source: Robert J. Shiller

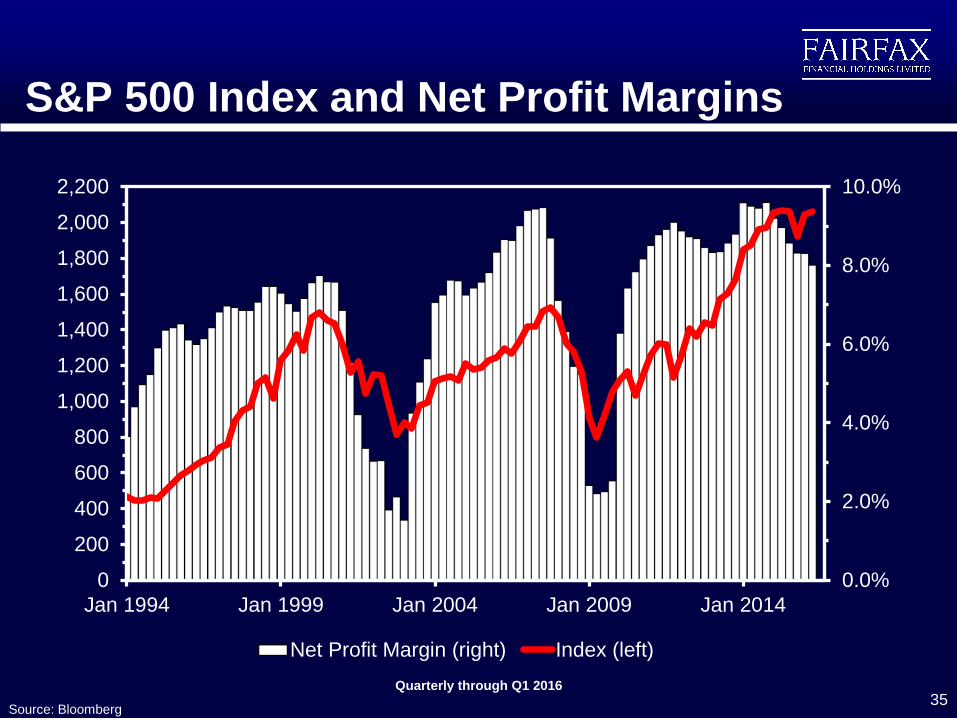

S&P 500 Index and Net Profit Margins

35 Source: Bloomberg

Quarterly through Q1 2016

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Jan 1994 Jan 1999 Jan 2004 Jan 2009 Jan 2014

Net Profit Margin (right) Index (left)Source: Bloomberg

U.S. Corporate After-Tax Profits

36

Quarterly through Q4 2015

Source: Hoisington Investment Management

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

'10 '11 '12 '13 '14 '15 '16

Lowest since Q1 2011

(billions) (billions)

Commodity Price Declines

37

S&P GSCI Commodity Index, monthly

Source: Hoisington Investment Management, Bloomberg

Through March 2016

0

100

200

300

400

500

600

700

800

900

1000

0

100

200

300

400

500

600

700

800

900

1000

'85 90 '95 '00 '05 '10 '15

Source: Hoisington Investment Management

Inflation Expectations

38

10 year breakeven inflation rate

Source: Bloomberg

Through March 2016

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

U.S.

Eurozone

-15%

-10%

-5%

0%

5%

10%

-15%

-10%

-5%

0%

5%

10%

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

2000

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Annual Inflation Annual Deflation Cumulative

(1) In April 2014 Japan raised its consumption tax from 5% to 8% (2) Estimate - Japan Cabinet Office

39

Deflation in Japan

Source: The World Bank

(1) (2)

40

Deflation in U.S.

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

193

0

193

1

193

2

193

3

193

4

193

5

193

6

193

7

193

8

193

9

194

0

Annual Inflation Annual Deflation Cumulative

Source: Hoisington Investment Management

41

CPI-Linked Derivative Contracts

December 31, 2015

Weighted average remaining term to maturity is 6.6 years

Notional

Amount Cost

Underlying CPI Index ($ bn) ($ mm) Dec 31,14 Dec 31,15

United States 46 285 79 99

United States - 0.5% floor 13 39 72 84

European Union 42 287 70 74

United Kingdom 5 24 5 3

France 3 21 12 13

109 656 238 273

Market Value ($ millions)

42

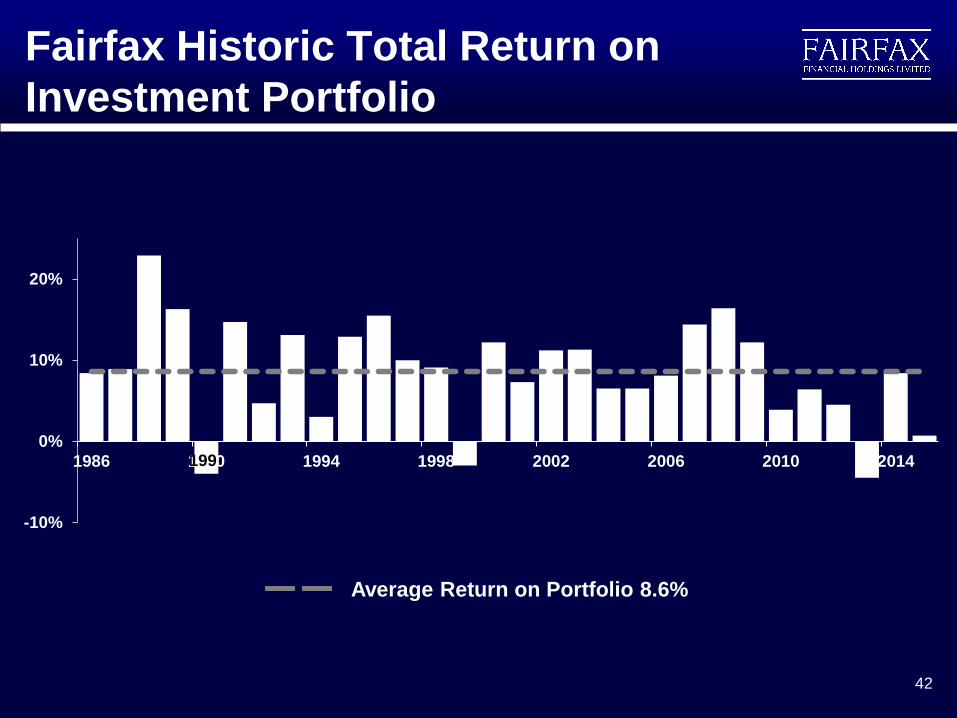

Fairfax Historic Total Return on

Investment Portfolio

-10%

0%

10%

20%

1986 1990 1994 1998 2002 2006 2010 2014

Average Return on Portfolio 8.6%

199

Ready for the Next Decade -

Building on Fairfax’s Strengths

Our guiding principles have remained intact

Excellent long term performance

Demonstrated strengths

Strong operating subsidiaries focused on underwriting profitability

and prudent reserving

Conservative investment management providing excellent long

term returns

Well positioned for the future

Fair and friendly Fairfax culture

43