Embed Size (px)

Citation preview

Micro Data For Macro ModelsTopic 2: Capital Investment

and Adjustment Costs

Thomas Winberry

November 7th, 2016

Plan for this Topic

1. An unfair summary of the empirical investment literature

2. Accounting for micro-level investment behavior with nonconvexadjustment costs

3. Macro implications of nonconvex adjustment costs

1

Plan for this Topic

1. An unfair summary of the empirical investment literature

2. Accounting for micro-level investment behavior with nonconvexadjustment costs

3. Macro implications of nonconvex adjustment costs

1

Plan for this Topic

1. An unfair summary of the empirical investment literature

2. Accounting for micro-level investment behavior with nonconvexadjustment costs

3. Macro implications of nonconvex adjustment costs

1

Plan for this Topic

1. An unfair summary of the empirical investment literature

2. Accounting for micro-level investment behavior with nonconvexadjustment costs

3. Macro implications of nonconvex adjustment costs

1

Empirical Investment Literature

The empirical investment literature is full ofdisappointments. From time to time waves of new ideaschallenge the aggregate investment equation, but thesechallenges are rarely successful, and progress is, at best, slow.There are serious theoretical obstacles, stemming mostly fromthe richness of the cross-sectional and time-series scenariosfaced by actual investors, from the complexity of theinvestment technologies available to them, and from the myriadincentive problems that these agents face. There are at least ascomplex, and perhaps insurmountable, data problems. Bothrigh- and left-hand side variables are seldom measured properly.

Caballero, Engel, and Haltiwanger, “Plant-Level Adjustment andAggregate Investment Dynamics”

2

Empirical Investment Literature

• Many early papers focus on neoclassical model

• “User cost” and “q theory” formulations• Finds model does not fit the data well at micro or macro level

• Two main responses:

1. Real adjustment frictions with nonconvexities2. Financial frictions to acquiring investment funds are important

2

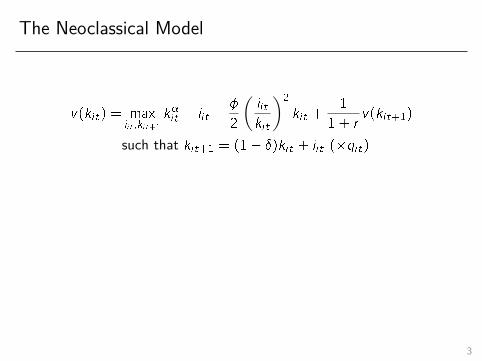

The Neoclassical Model

Consider production side of economy in time t with:

• Firms i 2 [0; 1] with production functionyit = k�it , � � 1

• Invest to accumulate capital kit+1 = (1� �)kit + iit

• Quadratic adjustment costs ��2

(iitkit

)2kit

• Discount future at constant rate r

v(kit) = maxiit ;kit+1

k�it � iit ��

2

(iitkit

)2

kit +1

1 + rv(kit+1)

such that kit+1 = (1� �)kit + iit

3

The Neoclassical Model

Consider production side of economy in time t with:

• Firms i 2 [0; 1] with production functionyit = k�it , � � 1

• Invest to accumulate capital kit+1 = (1� �)kit + iit

• Quadratic adjustment costs ��2

(iitkit

)2kit

• Discount future at constant rate r

v(kit) = maxiit ;kit+1

k�it � iit ��

2

(iitkit

)2

kit +1

1 + rv(kit+1)

such that kit+1 = (1� �)kit + iit

3

The Neoclassical Model

v(kit) = maxiit ;kit+1

k�it � iit ��

2

(iitkit

)2

kit +1

1 + rv(kit+1)

such that kit+1 = (1� �)kit + iit (�qit)

Take first order conditions:

1 + �(iitkit

) =qit

qit =v0(kit+1)

=1

1 + r

1∑s=0

(1� �

1 + r

)s (�k��1it+s+1 +�it+s+1

)

3

The Neoclassical Model

v(kit) = maxiit ;kit+1

k�it � iit ��

2

(iitkit

)2

kit +1

1 + rv(kit+1)

such that kit+1 = (1� �)kit + iit (�qit)

Take first order conditions:

1 + �(iitkit

) =qit

qit =v0(kit+1)

=1

1 + r

1∑s=0

(1� �

1 + r

)s (�k��1it+s+1 +�it+s+1

)2

The User Cost Model: � = 0

With � = 0, first order conditions simplify to

qit =1

�k��1it+1︸ ︷︷ ︸MPKit

= r + �︸ ︷︷ ︸user costt

• The user cost of capital is the implicit rental rate on capital

• Typically extended to incorporate other empirically relevant features:

ujt = pt︸︷︷︸relative price

�1�mjt � zjt

1� �t︸ ︷︷ ︸taxes

�(rt + �j)

3

The User Cost Model: � = 0

With � = 0, first order conditions simplify to

qit =1

�k��1it+1︸ ︷︷ ︸MPKit

= r + �︸ ︷︷ ︸user costt

• The user cost of capital is the implicit rental rate on capital

• Typically extended to incorporate other empirically relevant features:

ujt = pt︸︷︷︸relative price

�1�mjt � zjt

1� �t︸ ︷︷ ︸taxes

�(rt + �j)

3

Empirical Performance of the User Cost Model

• Typical regression takes the form

iitkit

= �i + � � uit + �� other variablesit + "it

• Two main failures of user cost model:1. Estimated user cost elasticity � small (� 0 to -0.5)2. Coefficients on other variables, especially cash flow, large and

significant

• Hall and Jorgensen (1967); Cummins, Hassett, and Hubbard (1994);Chirinko, Fazarri, and Meyer (1999)

4

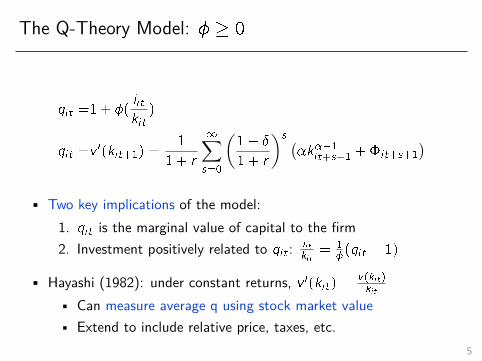

The Q-Theory Model: � � 0

qit =1 + �(iitkit

)

qit =v0(kit+1) =

1

1 + r

1∑s=0

(1� �

1 + r

)s (�k��1it+s+1 +�it+s+1

)

• Two key implications of the model:1. qit is the marginal value of capital to the firm2. Investment positively related to qit : iit

kit= 1

�(qit � 1)

• Hayashi (1982): under constant returns, v 0(kit) = v(kit)kit

• Can measure average q using stock market value• Extend to include relative price, taxes, etc.

5

The Q-Theory Model: � � 0

qit =1 + �(iitkit

)

qit =v0(kit+1) =

1

1 + r

1∑s=0

(1� �

1 + r

)s (�k��1it+s+1 +�it+s+1

)• Two key implications of the model:

1. qit is the marginal value of capital to the firm2. Investment positively related to qit : iit

kit= 1

�(qit � 1)

• Hayashi (1982): under constant returns, v 0(kit) = v(kit)kit

• Can measure average q using stock market value• Extend to include relative price, taxes, etc.

5

The Q-Theory Model: � � 0

qit =1 + �(iitkit

)

qit =v0(kit+1) =

1

1 + r

1∑s=0

(1� �

1 + r

)s (�k��1it+s+1 +�it+s+1

)• Two key implications of the model:

1. qit is the marginal value of capital to the firm2. Investment positively related to qit : iit

kit= 1

�(qit � 1)

• Hayashi (1982): under constant returns, v 0(kit) = v(kit)kit

• Can measure average q using stock market value• Extend to include relative price, taxes, etc.

5

Empirical Performance of the Q Model

• Typical regression takes the form

iitkit

= �i + � � qit + �� other variablesit + "it

• Two main failures of user cost model:1. Estimated coefficient � small and unstable2. Coefficients on other variables, especially cash flow, large and

significant

• Summers (1981); Cummins, Hassett, and Hubbard (1994); Ericksonand Whited (2000)

6

Doms and Dunne (1998)

Two responses to failure of neoclassical model:1. Real adjustment frictions featuring nonconvexities are important2. Financial frictions to acquiring investment funds are important

Doms and Dunne (1998):• Landmark descriptive study of investment in LRD

• Shows micro-level investment is lumpy, i.e., occurs mainly alongextensive margin

• Fluctuations in total investment mainly due to extensive margin

• Suggests important role for non-convex adjustment costs

7

Doms and Dunne (1998)

Two responses to failure of neoclassical model:1. Real adjustment frictions featuring nonconvexities are important2. Financial frictions to acquiring investment funds are important

Doms and Dunne (1998):• Landmark descriptive study of investment in LRD

• Shows micro-level investment is lumpy, i.e., occurs mainly alongextensive margin

• Fluctuations in total investment mainly due to extensive margin

• Suggests important role for non-convex adjustment costs

7

Measurement

• Use Census data from LRD, 1972 - 1988• After 1988, stopped collecting book value of capital

• Construct capital stock using perpetual inventory method• Focus on balanced panel

• Analyze the growth rate of capital for plant i at time t

GKit =iit � �kit�1

0:5� (kit�1 + kit)

8

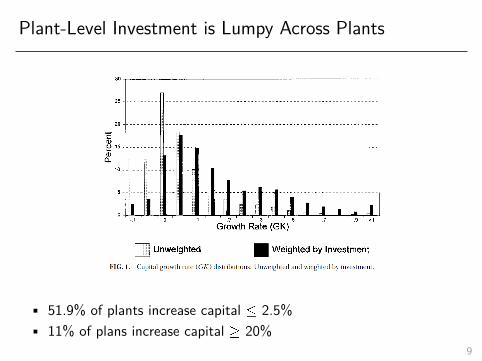

Plant-Level Investment is Lumpy Across Plants

• 51.9% of plants increase capital � 2.5%• 11% of plans increase capital � 20%

9

Plant-Level Investment is Lumpy Across Plants

• 51.9% of plants increase capital � 2.5%• 11% of plans increase capital � 20%

9

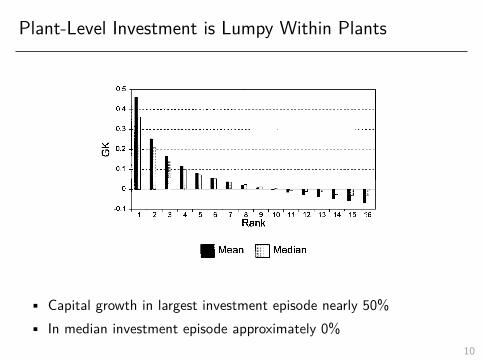

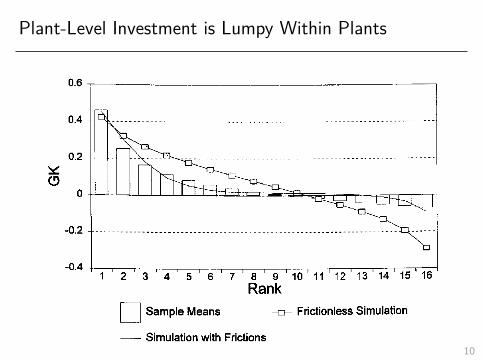

Plant-Level Investment is Lumpy Within Plants

• Capital growth in largest investment episode nearly 50%• In median investment episode approximately 0%

10

Plant-Level Investment is Lumpy Within Plants

• Capital growth in largest investment episode nearly 50%• In median investment episode approximately 0%

10

Plant-Level Investment is Lumpy Within Plants

10

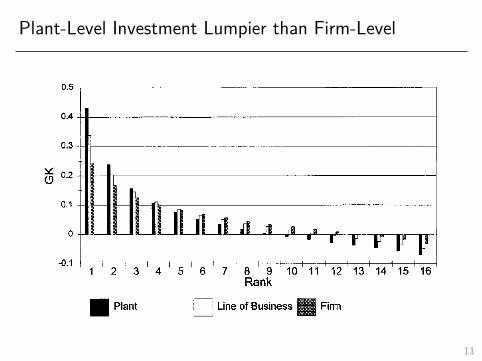

Plant-Level Investment Lumpier than Firm-Level

11

Frequency of Spikes Correlated with AggregateInvestment

12

Zwick and Mahon (2016)

Two responses to failure of neoclassical model:1. Real adjustment frictions featuring nonconvexities are important2. Financial frictions to acquiring investment funds are important

Zwick and Mahon (2016):

• Clean study exploiting exploiting policy-induced variation in cost ofcapital

• Shows investment very responsive to cost, especially forsmall/non-dividend paying firms

• Suggests important role for financial frictions (and potentially fixedcosts)

13

Zwick and Mahon (2016)

Two responses to failure of neoclassical model:1. Real adjustment frictions featuring nonconvexities are important2. Financial frictions to acquiring investment funds are important

Zwick and Mahon (2016):

• Clean study exploiting exploiting policy-induced variation in cost ofcapital

• Shows investment very responsive to cost, especially forsmall/non-dividend paying firms

• Suggests important role for financial frictions (and potentially fixedcosts)

13

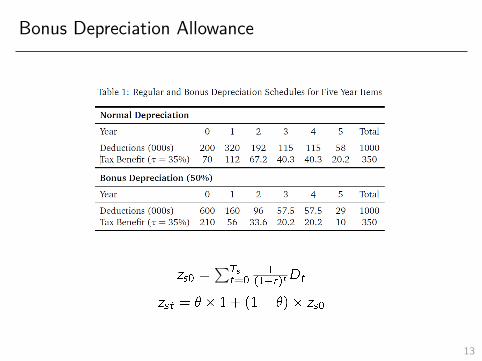

Bonus Depreciation Allowance

• Bonus shifts depreciation allowances from future to present• With discounting, lowers the total cost of investment

! Bonus more valuable for longer-lived investment

14

Bonus Depreciation Allowance

• Bonus shifts depreciation allowances from future to present• With discounting, lowers the total cost of investment

! Bonus more valuable for longer-lived investment14

Bonus Depreciation Allowance

zs0 =∑Ts

t=01

(1+r)tDt

zst = � � 1 + (1� �)� zs0

14

Bonus Depreciation Allowance

zs0 =∑Ts

t=01

(1+r)tDt

zst = � � 1 + (1� �)� zs0

13

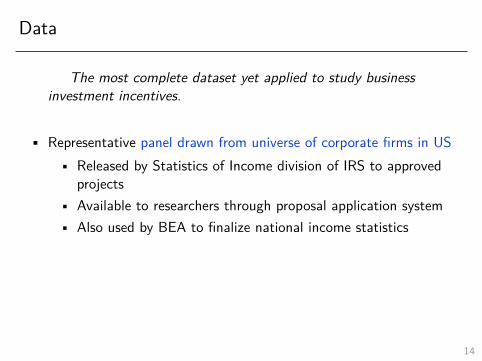

Data

The most complete dataset yet applied to study businessinvestment incentives.

• Representative panel drawn from universe of corporate firms in US• Released by Statistics of Income division of IRS to approved

projects• Available to researchers through proposal application system• Also used by BEA to finalize national income statistics

• Investment iit measured as expenditures on equipment eligible forBonus

• PV of depreciation allowances zst constructed at four digit levelusing r = 7%

14

Data

The most complete dataset yet applied to study businessinvestment incentives.

• Representative panel drawn from universe of corporate firms in US• Released by Statistics of Income division of IRS to approved

projects• Available to researchers through proposal application system• Also used by BEA to finalize national income statistics

• Investment iit measured as expenditures on equipment eligible forBonus

• PV of depreciation allowances zst constructed at four digit levelusing r = 7%

14

Data

The most complete dataset yet applied to study businessinvestment incentives.

• Representative panel drawn from universe of corporate firms in US• Released by Statistics of Income division of IRS to approved

projects• Available to researchers through proposal application system• Also used by BEA to finalize national income statistics

• Investment iit measured as expenditures on equipment eligible forBonus

• PV of depreciation allowances zst constructed at four digit levelusing r = 7%

14

Identification Strategy

• Identify effect of policy using difference-in-differences design• Treatment group: firms in long-lived industries• Control group: firms in short-lived industries

• Regression specification

f (iit ; kit) = �i + �t + � � g(zst) + Xit + "it

• f (iit ; kit): log iit , log pst

1�pst, or iit

kit

• g(zst): zst or 1��zst1��

• Key assumption for diff-in-diff: parallel trends holds15

Graphical Evidence

16

Overall Effect of Bonus on Investment

f (iit ; kit) = �i + �t + � � g(zst) + Xit + "it17

Larger Effect Than Existing Literature

18

Heterogeneity Suggestive of Financial Frictions

19

Heterogeneity Explains Larger Estimate than Literature

20

Unfair Review of Empirical Investment Lit

• Neoclassical model predicts investment very responsive to cost• User cost formulation: capital stock responds to implied rental

rate• Q theory formulation: investment responds to marginal value of

capital

• 1960s - 1990s: both formulations largely fail in data• Capital/investment unresponsive to cost• Other variables (cash flow) significant

• Two responses to failure of neoclassical model1. Adjustment costs feature nonconvexities2. Financial frictions influence investment behavior

21

Unfair Review of Empirical Investment Lit

• Neoclassical model predicts investment very responsive to cost• User cost formulation: capital stock responds to implied rental

rate• Q theory formulation: investment responds to marginal value of

capital

• 1960s - 1990s: both formulations largely fail in data• Capital/investment unresponsive to cost• Other variables (cash flow) significant

• Two responses to failure of neoclassical model1. Adjustment costs feature nonconvexities2. Financial frictions influence investment behavior

21

Unfair Review of Empirical Investment Lit

• Neoclassical model predicts investment very responsive to cost• User cost formulation: capital stock responds to implied rental

rate• Q theory formulation: investment responds to marginal value of

capital

• 1960s - 1990s: both formulations largely fail in data• Capital/investment unresponsive to cost• Other variables (cash flow) significant

• Two responses to failure of neoclassical model1. Adjustment costs feature nonconvexities2. Financial frictions influence investment behavior

21

The Rest of This Topic

Focus on role of nonconvex adjustment costs in explaining micro andmacro investment dynamics

1. Study models of micro-level investment behavior• What form of adjustment costs do we need to explain micro

data?

2. Study aggregate implications of these models• Aggregation• General equilibrium

22

The Rest of This Topic

Focus on role of nonconvex adjustment costs in explaining micro andmacro investment dynamics

1. Study models of micro-level investment behavior• What form of adjustment costs do we need to explain micro

data?

2. Study aggregate implications of these models• Aggregation• General equilibrium

22

The Rest of This Topic

Focus on role of nonconvex adjustment costs in explaining micro andmacro investment dynamics

1. Study models of micro-level investment behavior• What form of adjustment costs do we need to explain micro

data?

2. Study aggregate implications of these models• Aggregation• General equilibrium

22

Plan for this Topic

1. An unfair summary of the empirical investment literature

2. Accounting for micro-level investment behavior with nonconvexadjustment costs

3. Macro implications of nonconvex adjustment costs

22

The Gold Standard: Cooper and Haltiwanger (2006)

• What types of adjustment costs do we need to match micro-levelinvestment behavior?

• Pays special attention to lumpy nature of investment

• Answer using an estimated structural model• Simulated method of moments

• A note on terminology in this literature:• Partial equilibrium = analyzing decision rules with fixed prices• Does NOT mean equilibrium in one market! (which would be

correct)

23

The Gold Standard: Cooper and Haltiwanger (2006)

• What types of adjustment costs do we need to match micro-levelinvestment behavior?

• Pays special attention to lumpy nature of investment

• Answer using an estimated structural model• Simulated method of moments

• A note on terminology in this literature:• Partial equilibrium = analyzing decision rules with fixed prices• Does NOT mean equilibrium in one market! (which would be

correct)

23

The Gold Standard: Cooper and Haltiwanger (2006)

• What types of adjustment costs do we need to match micro-levelinvestment behavior?

• Pays special attention to lumpy nature of investment

• Answer using an estimated structural model• Simulated method of moments

• A note on terminology in this literature:• Partial equilibrium = analyzing decision rules with fixed prices• Does NOT mean equilibrium in one market!

(which would becorrect)

23

The Gold Standard: Cooper and Haltiwanger (2006)

• What types of adjustment costs do we need to match micro-levelinvestment behavior?

• Pays special attention to lumpy nature of investment

• Answer using an estimated structural model• Simulated method of moments

• A note on terminology in this literature:• Partial equilibrium = analyzing decision rules with fixed prices• Does NOT mean equilibrium in one market! (which would be

correct)23

LRD Data

Sample• Establishment-level observations• Balanced panel: model abstracts from entry and exit• 1972 - 1988: want to use data on expenditures and retirements

Measurement• Investment iit : expenditureit � retirmentsit• Capital kit : kit+1 = (1� �it)kit + iit

• Depreciation �it : constructed to reflect in-use depreciation

24

LRD Data

Sample• Establishment-level observations• Balanced panel: model abstracts from entry and exit• 1972 - 1988: want to use data on expenditures and retirements

Measurement• Investment iit : expenditureit � retirmentsit• Capital kit : kit+1 = (1� �it)kit + iit

• Depreciation �it : constructed to reflect in-use depreciation

24

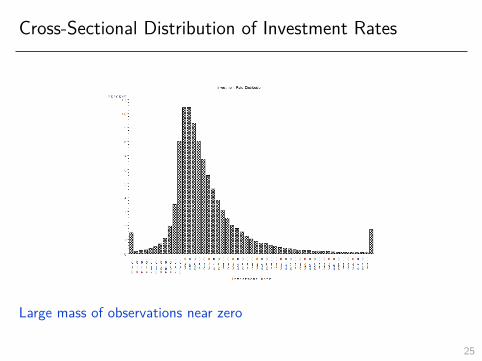

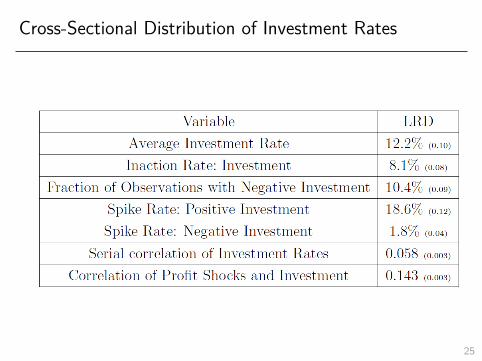

Cross-Sectional Distribution of Investment Rates

Large mass of observations near zeroHighly skewed and fat right tails

25

Cross-Sectional Distribution of Investment Rates

Large mass of observations near zero

Highly skewed and fat right tails

25

Cross-Sectional Distribution of Investment Rates

Large mass of observations near zeroHighly skewed and fat right tails

25

Cross-Sectional Distribution of Investment Rates

25

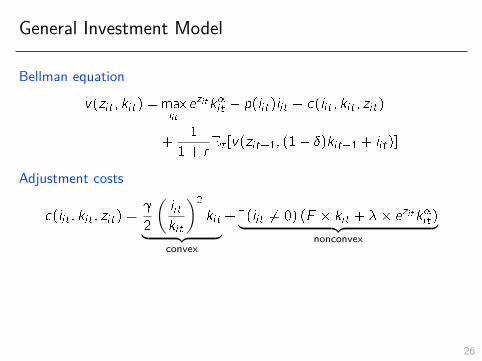

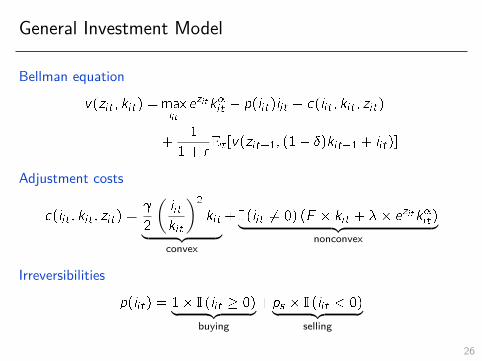

General Investment Model

Bellman equation

v(zit ; kit) =maxiitezitk�it � p(iit)iit � c(iit ; kit ; zit)

+1

1 + rEt [v(zit+1; (1� �)kit+1 + iit)]

Adjustment costs

c(iit ; kit ; zit) =

2

(iitkit

)2

kit︸ ︷︷ ︸convex

+ I (iit 6= 0) (F � kit + �� ezitk�it )︸ ︷︷ ︸

nonconvex

Irreversibilities

p(iit) = 1� I (iit � 0)︸ ︷︷ ︸buying

+ ps � I (iit < 0)︸ ︷︷ ︸selling

26

General Investment Model

Bellman equation

v(zit ; kit) =maxiitezitk�it � p(iit)iit � c(iit ; kit ; zit)

+1

1 + rEt [v(zit+1; (1� �)kit+1 + iit)]

Adjustment costs

c(iit ; kit ; zit) =

2

(iitkit

)2

kit︸ ︷︷ ︸convex

+ I (iit 6= 0) (F � kit + �� ezitk�it )︸ ︷︷ ︸

nonconvex

Irreversibilities

p(iit) = 1� I (iit � 0)︸ ︷︷ ︸buying

+ ps � I (iit < 0)︸ ︷︷ ︸selling

26

General Investment Model

Bellman equation

v(zit ; kit) =maxiitezitk�it � p(iit)iit � c(iit ; kit ; zit)

+1

1 + rEt [v(zit+1; (1� �)kit+1 + iit)]

Adjustment costs

c(iit ; kit ; zit) =

2

(iitkit

)2

kit︸ ︷︷ ︸convex

+ I (iit 6= 0) (F � kit + �� ezitk�it )︸ ︷︷ ︸

nonconvex

Irreversibilities

p(iit) = 1� I (iit � 0)︸ ︷︷ ︸buying

+ ps � I (iit < 0)︸ ︷︷ ︸selling

26

No Adjustment Costs

v(zit ; kit) =maxiitezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1 + iit)]

Optimal Behavior

1 =1

1 + rEt [v2(zit+1; kit+1)]

! user cost model: r + � = Et [�k��1it+1]

27

No Adjustment Costs

v(zit ; kit) =maxiitezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1 + iit)]

Optimal Behavior

1 =1

1 + rEt [v2(zit+1; kit+1)]

! user cost model: r + � = Et [�k��1it+1]

27

Convex Costs Only

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit

Optimal Behavior

1 +

(iitkit

)=

1

1 + rEt [v2(zit+1; kit+1)]

! q model: iitkit

=1

(Et [v2(zit+1; kit+1)]� 1)

28

Convex Costs Only

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit

Optimal Behavior

1 +

(iitkit

)=

1

1 + rEt [v2(zit+1; kit+1)]

! q model: iitkit

=1

(Et [v2(zit+1; kit+1)]� 1)

28

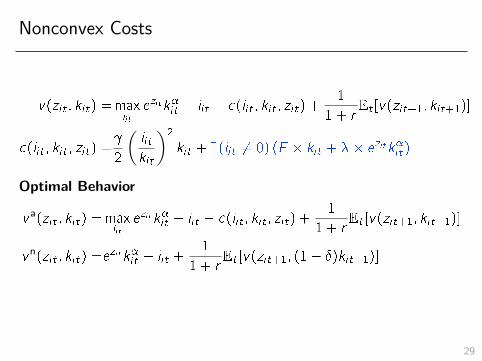

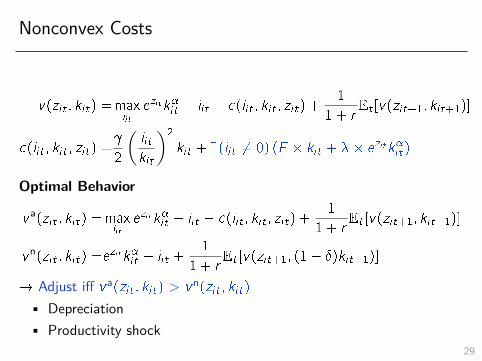

Nonconvex Costs

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit + I (iit 6= 0) (F � kit + �� ezitk�it )

Optimal Behavior

v a(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

vn(zit ; kit) =ezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1)]

! Adjust iff v a(zit ; kit) > vn(zit ; kit)

• Depreciation• Productivity shock

29

Nonconvex Costs

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit + I (iit 6= 0) (F � kit + �� ezitk�it )

Optimal Behavior

v a(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

vn(zit ; kit) =ezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1)]

! Adjust iff v a(zit ; kit) > vn(zit ; kit)

• Depreciation• Productivity shock

29

Nonconvex Costs

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit + I (iit 6= 0) (F � kit + �� ezitk�it )

Optimal Behavior

v a(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

vn(zit ; kit) =ezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1)]

! Adjust iff v a(zit ; kit) > vn(zit ; kit)

• Depreciation• Productivity shock

29

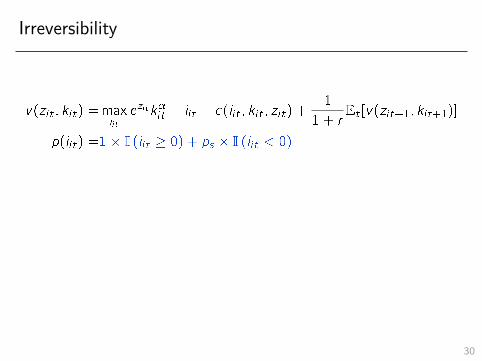

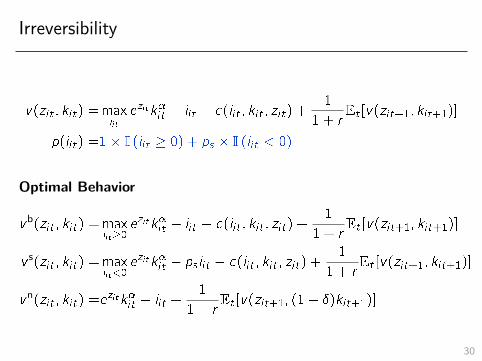

Irreversibility

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

p(iit) =1� I (iit � 0) + ps � I (iit < 0)

Optimal Behavior

vb(zit ; kit) =maxiit�0

ezitk�it � iit � c(iit ; kit ; zit) +1

1 + rEt [v(zit+1; kit+1)]

v s(zit ; kit) =maxiit<0

ezitk�it � ps iit � c(iit ; kit ; zit) +1

1 + rEt [v(zit+1; kit+1)]

vn(zit ; kit) =ezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1)]

! Also generates inaction

30

Irreversibility

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

p(iit) =1� I (iit � 0) + ps � I (iit < 0)

Optimal Behavior

vb(zit ; kit) =maxiit�0

ezitk�it � iit � c(iit ; kit ; zit) +1

1 + rEt [v(zit+1; kit+1)]

v s(zit ; kit) =maxiit<0

ezitk�it � ps iit � c(iit ; kit ; zit) +1

1 + rEt [v(zit+1; kit+1)]

vn(zit ; kit) =ezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1)]

! Also generates inaction

30

Irreversibility

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

p(iit) =1� I (iit � 0) + ps � I (iit < 0)

Optimal Behavior

vb(zit ; kit) =maxiit�0

ezitk�it � iit � c(iit ; kit ; zit) +1

1 + rEt [v(zit+1; kit+1)]

v s(zit ; kit) =maxiit<0

ezitk�it � ps iit � c(iit ; kit ; zit) +1

1 + rEt [v(zit+1; kit+1)]

vn(zit ; kit) =ezitk�it � iit +

1

1 + rEt [v(zit+1; (1� �)kit+1)]

! Also generates inaction30

Illustration of Various Frictions

31

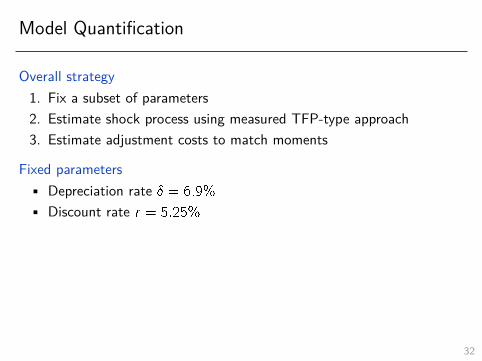

Model Quantification

Overall strategy1. Fix a subset of parameters2. Estimate shock process using measured TFP-type approach3. Estimate adjustment costs to match moments

Fixed parameters• Depreciation rate � = 6:9%

• Discount rate r = 5:25%

Estimate idiosyncratic shocks• Assume zit = "it + bt

• Assume AR(1) and use GMM onlog(�it) = �� log(�it�1) + �kit � ���kit�1 + bt � ��bt�1 + �it

• See paper for details

32

Model Quantification

Overall strategy1. Fix a subset of parameters2. Estimate shock process using measured TFP-type approach3. Estimate adjustment costs to match moments

Fixed parameters• Depreciation rate � = 6:9%

• Discount rate r = 5:25%

Estimate idiosyncratic shocks• Assume zit = "it + bt

• Assume AR(1) and use GMM onlog(�it) = �� log(�it�1) + �kit � ���kit�1 + bt � ��bt�1 + �it

• See paper for details

32

Model Quantification

Overall strategy1. Fix a subset of parameters2. Estimate shock process using measured TFP-type approach3. Estimate adjustment costs to match moments

Fixed parameters• Depreciation rate � = 6:9%

• Discount rate r = 5:25%

Estimate idiosyncratic shocks• Assume zit = "it + bt

• Assume AR(1) and use GMM onlog(�it) = �� log(�it�1) + �kit � ���kit�1 + bt � ��bt�1 + �it

• See paper for details32

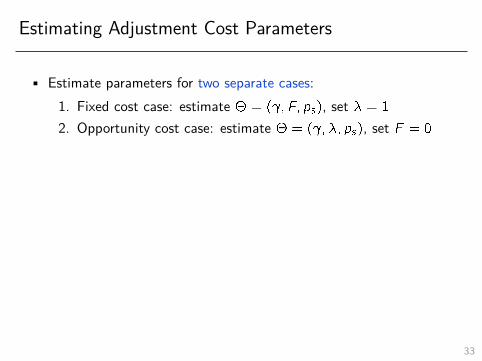

Estimating Adjustment Cost Parameters

• Estimate parameters for two separate cases:1. Fixed cost case: estimate � = ( ; F; ps), set � = 1

2. Opportunity cost case: estimate � = ( ; �; ps), set F = 0

• Simulated Method of Moments (SMM)

�̂ = argmin�

[d �s(�)]T W [d �s(�)]

• Data moments d: drawn from data• Model moments s(�): simulated panel of firms from model• Weighting matrix W : efficient matrix from GMM• Standard errors: GMM formulas plus factor for Monte Carlo

error

33

Estimating Adjustment Cost Parameters

• Estimate parameters for two separate cases:1. Fixed cost case: estimate � = ( ; F; ps), set � = 1

2. Opportunity cost case: estimate � = ( ; �; ps), set F = 0

• Simulated Method of Moments (SMM)

�̂ = argmin�

[d �s(�)]T W [d �s(�)]

• Data moments d: drawn from data• Model moments s(�): simulated panel of firms from model• Weighting matrix W : efficient matrix from GMM• Standard errors: GMM formulas plus factor for Monte Carlo

error33

Estimation Results: Fixed Cost Case

Estimated fixed cost F u 4% of capital stock

34

Estimation Results: Fixed Cost Case

Estimated fixed cost F u 4% of capital stock

34

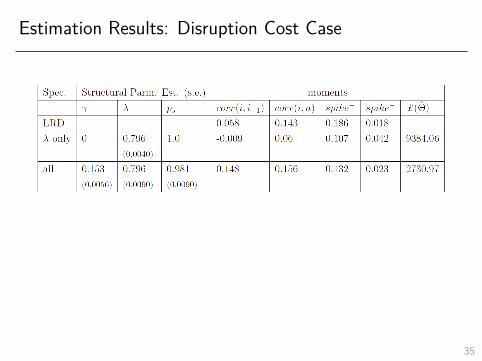

Estimation Results: Disruption Cost Case

Estimated disruption cost 1� � u 20% of profitsOn average, pay 3.1% of profits in AC when adjust

35

Estimation Results: Disruption Cost Case

Estimated disruption cost 1� � u 20% of profitsOn average, pay 3.1% of profits in AC when adjust

35

Cooper and Haltiwanger (2006): Wrapping Up

• What types of adjustment costs do we need to match micro data?

Non-convexities:• Fixed costs• Disruption costs• Irreversibilities

• Nice illustration of Simulated Method of Moments (SMM)methodology

• Specify moments of the data you think are important• Select parameters which are well-identified by those moments• Choose parameters to get model as close as possible to data

• My HW2 will give you practice in simple investment problem

36

Cooper and Haltiwanger (2006): Wrapping Up

• What types of adjustment costs do we need to match micro data?Non-convexities:

• Fixed costs• Disruption costs• Irreversibilities

• Nice illustration of Simulated Method of Moments (SMM)methodology

• Specify moments of the data you think are important• Select parameters which are well-identified by those moments• Choose parameters to get model as close as possible to data

• My HW2 will give you practice in simple investment problem

36

Cooper and Haltiwanger (2006): Wrapping Up

• What types of adjustment costs do we need to match micro data?Non-convexities:

• Fixed costs• Disruption costs• Irreversibilities

• Nice illustration of Simulated Method of Moments (SMM)methodology

• Specify moments of the data you think are important• Select parameters which are well-identified by those moments• Choose parameters to get model as close as possible to data

• My HW2 will give you practice in simple investment problem36

Asker, Collard-Wexler, and De Loecker (2014)

Shows Cooper-Haltiwanger (2006) model also explains much of MRPKit

dispersion documented by Hsieh and Klenow (2009)

Data: LRD, 1972 - 1997• Also use cross-country data for analysis in paper

Model: Cooper-Haltiwanger (2006) opportunity cost model

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit + I (iit 6= 0)�� ezitk�it

37

Asker, Collard-Wexler, and De Loecker (2014)

Shows Cooper-Haltiwanger (2006) model also explains much of MRPKit

dispersion documented by Hsieh and Klenow (2009)

Data: LRD, 1972 - 1997• Also use cross-country data for analysis in paper

Model: Cooper-Haltiwanger (2006) opportunity cost model

v(zit ; kit) =maxiitezitk�it � iit � c(iit ; kit ; zit) +

1

1 + rEt [v(zit+1; kit+1)]

c(iit ; kit ; zit) =

2

(iitkit

)2

kit + I (iit 6= 0)�� ezitk�it

37

Estimation

Estimate � = ( ; �) using SMM

�̂ = argmin�

[d �s(�)]T W [d �s(�)]

38

Estimation

Estimate � = ( ; �) using SMM

�̂ = argmin�

[d �s(�)]T W [d �s(�)]

38

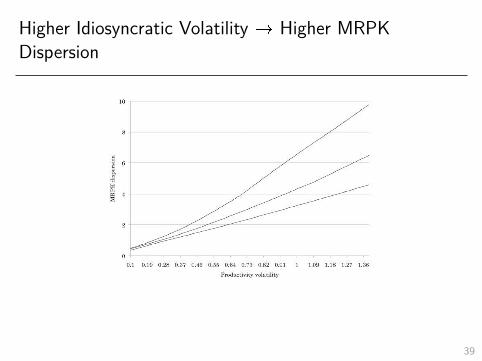

Higher Idiosyncratic Volatility ! Higher MRPKDispersion

• MRPKit = � yitkit

• Time to build ! ex-ante dispersion• Adjustment costs ! ex-post dispersion

39

Higher Idiosyncratic Volatility ! Higher MRPKDispersion

• MRPKit = � yitkit

• Time to build ! ex-ante dispersion• Adjustment costs ! ex-post dispersion 39

Idiosyncratic Volatility and MRPK Dispersion in Data

40

Idiosyncratic Volatility and MRPK Dispersion in Data

40

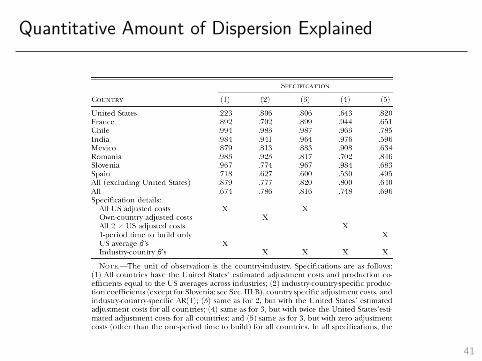

Quantitative Amount of Dispersion Explained

41

Plan for this Topic

1. An unfair summary of the empirical investment literature

2. Accounting for micro-level investment behavior with nonconvexadjustment costs

3. Macro implications of nonconvex adjustment costs

41

Aggregate Implications of Micro Investment Models

1. Aggregation of micro-level models holding prices fixed (partialequilibrium)

• Response of aggregate investment to shocks depends onnumber of firms who adjust

• Aggregate investment features time-varying elasticity w.r.t.shocks

• Representative firm instead predicts constant elasticity

2. Endogenize prices in general equilibrium• In benchmark RBC framework, procyclical real interest rate

eliminates time-varying elasticity• Modifications to benchmark model can break this irrelevance

result

42

Aggregate Implications of Micro Investment Models

1. Aggregation of micro-level models holding prices fixed (partialequilibrium)

• Response of aggregate investment to shocks depends onnumber of firms who adjust

• Aggregate investment features time-varying elasticity w.r.t.shocks

• Representative firm instead predicts constant elasticity

2. Endogenize prices in general equilibrium• In benchmark RBC framework, procyclical real interest rate

eliminates time-varying elasticity• Modifications to benchmark model can break this irrelevance

result42

General Lessons

1. Anytime you go from micro to macro, need to think about• Aggregation• General equilibrium

2. Macro models with micro heterogeneity are hard• Entire cross-sectional distribution of agents part of state vector• Difficult to numerically compute and estimate

• Aggregate implications of lumpy investment models good illustrationof these more general issues

• Each of these steps has been extensively studied• But people are largely tired of it by now

43

General Lessons

1. Anytime you go from micro to macro, need to think about• Aggregation• General equilibrium

2. Macro models with micro heterogeneity are hard• Entire cross-sectional distribution of agents part of state vector• Difficult to numerically compute and estimate

• Aggregate implications of lumpy investment models good illustrationof these more general issues

• Each of these steps has been extensively studied• But people are largely tired of it by now

43

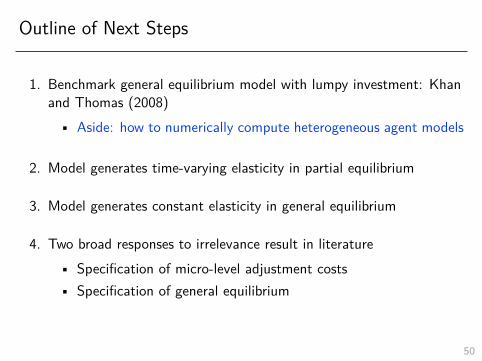

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

44

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

44

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

44

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

44

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

44

Model Overview

Heterogeneous Firms• Fixed mass• Idiosyncratic + aggregate productivity shocks• Fixed capital adjustment costs

Representative Household• Owns firms• Supplies labor• Complete markets

45

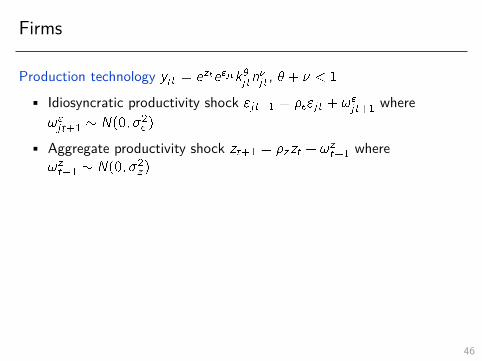

Firms

Production technology yjt = ezte"jtk�jtn�jt , � + � < 1

• Idiosyncratic productivity shock "jt+1 = ��"jt + !"jt+1 where

!"jt+1 � N(0; �2� )

• Aggregate productivity shock zt+1 = �zzt + !zt+1 where

!zt+1 � N(0; �2z )

Firms accumulate capital according to kjt+1 = (1� �)kjt + ijt

• If ijtkjt=2 [�a; a], pay fixed cost �jt in units of labor

• Fixed cost �jt � U[0; �]

46

Firms

Production technology yjt = ezte"jtk�jtn�jt , � + � < 1

• Idiosyncratic productivity shock "jt+1 = ��"jt + !"jt+1 where

!"jt+1 � N(0; �2� )

• Aggregate productivity shock zt+1 = �zzt + !zt+1 where

!zt+1 � N(0; �2z )

Firms accumulate capital according to kjt+1 = (1� �)kjt + ijt

• If ijtkjt=2 [�a; a], pay fixed cost �jt in units of labor

• Fixed cost �jt � U[0; �]

46

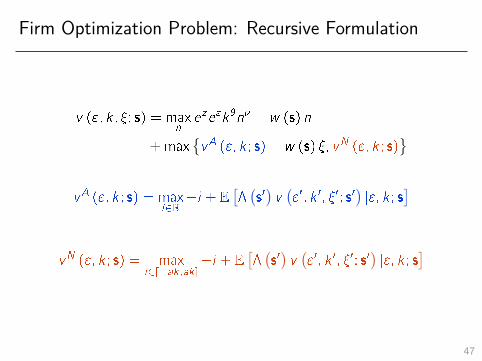

Firm Optimization Problem: Recursive Formulation

v ("; k; �; s) = maxneze"k�n� � w (s) n

+max{vA ("; k ; s)� w (s) �; vN ("; k ; s)

}

47

Firm Optimization Problem: Recursive Formulation

v ("; k; �; s) = maxneze"k�n� � w (s) n

+max{vA ("; k ; s)� w (s) �; vN ("; k ; s)

}vA ("; k ; s) = max

i2R�i + E

[�(s0)v("0; k 0; �0; s0

)j"; k ; s

]

vN ("; k ; s) = maxi2[�ak;ak]

�i + E[�(s0)v("0; k 0; �0; s0

)j"; k ; s

]

47

Firm Optimization Problem: Recursive Formulation

v ("; k; �; s) = maxneze"k�n� � w (s) n

+max{vA ("; k ; s)� w (s) �; vN ("; k ; s)

}

v̂ ("; k ; s) = maxneze"k�n� � w (s) n

+�̂ ("; k ; s)

�

(vA ("; k ; s)� w (s)

�̂ ("; k ; s)

2

)

+

(1�

�̂ ("; k ; s)

�

)vN ("; k ; s)

47

Household

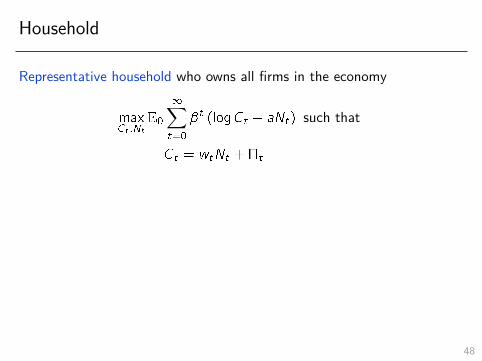

Representative household who owns all firms in the economy

maxCt ;Nt

E0

1∑t=0

�t (logCt � aNt) such that

Ct = wtNt +�t

Complete markets implies that �t;t+1 = �(Ct+1

Ct

)�1• Firms maximize their market value• Market value given by expected present value of dividends using

stochastic discount factor• With complete markets, SDF is household’s marginal rate of

substitution

48

Household

Representative household who owns all firms in the economy

maxCt ;Nt

E0

1∑t=0

�t (logCt � aNt) such that

Ct = wtNt +�t

Complete markets implies that �t;t+1 = �(Ct+1

Ct

)�1• Firms maximize their market value• Market value given by expected present value of dividends using

stochastic discount factor• With complete markets, SDF is household’s marginal rate of

substitution48

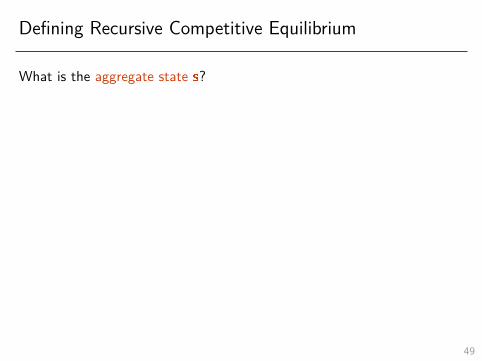

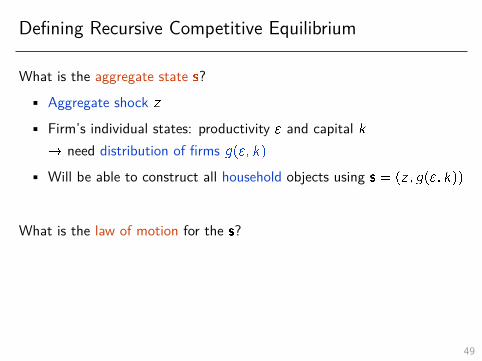

Defining Recursive Competitive Equilibrium

What is the aggregate state s?

• Aggregate shock z• Firm’s individual states: productivity " and capital k! need distribution of firms g("; k)

• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

Defining Recursive Competitive Equilibrium

What is the aggregate state s?• Aggregate shock z

• Firm’s individual states: productivity " and capital k! need distribution of firms g("; k)

• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

Defining Recursive Competitive Equilibrium

What is the aggregate state s?• Aggregate shock z• Firm’s individual states: productivity " and capital k

! need distribution of firms g("; k)• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

Defining Recursive Competitive Equilibrium

What is the aggregate state s?• Aggregate shock z• Firm’s individual states: productivity " and capital k! need distribution of firms g("; k)

• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

Defining Recursive Competitive Equilibrium

What is the aggregate state s?• Aggregate shock z• Firm’s individual states: productivity " and capital k! need distribution of firms g("; k)

• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

Defining Recursive Competitive Equilibrium

What is the aggregate state s?• Aggregate shock z• Firm’s individual states: productivity " and capital k! need distribution of firms g("; k)

• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

Defining Recursive Competitive Equilibrium

What is the aggregate state s?• Aggregate shock z• Firm’s individual states: productivity " and capital k! need distribution of firms g("; k)

• Will be able to construct all household objects using s = (z; g("; k))

What is the law of motion for the s?

gt+1("0; k 0

)=

∫ [1 f�""+ �"!

0" = "0g

�∫1 fk 0t ("; k; �) = k 0g dG(�)

]� p

(!0")gt ("; k) d!

0"d"dk

49

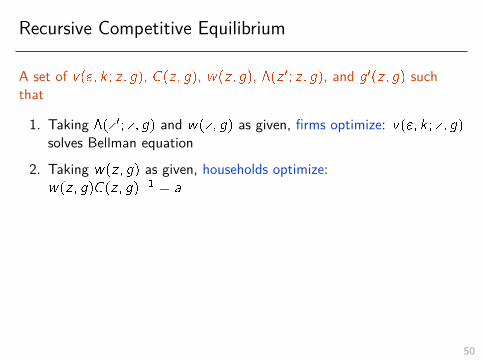

Recursive Competitive Equilibrium

A set of v("; k ; z; g), C(z; g), w(z; g), �(z 0; z; g), and g0(z; g) suchthat

1. Taking �(z 0; z; g) and w(z; g) as given, firms optimize: v("; k ; z; g)solves Bellman equation

2. Taking w(z; g) as given, households optimize:w(z; g)C(z; g)�1 = a

3. Markets clear and aggregate consistency conditions hold:

�(z 0; z; g) = �

(C(z 0; g0(z; g))

C(z; g)

)�1C(z; g) =

∫(y("; k; �; z; g)� i("; k; �; z; g))dG(�)g("; k)d"dk

g0("; k) satisfies law of motion for distribution

50

Recursive Competitive Equilibrium

A set of v("; k ; z; g), C(z; g), w(z; g), �(z 0; z; g), and g0(z; g) suchthat

1. Taking �(z 0; z; g) and w(z; g) as given, firms optimize: v("; k ; z; g)solves Bellman equation

2. Taking w(z; g) as given, households optimize:w(z; g)C(z; g)�1 = a

3. Markets clear and aggregate consistency conditions hold:

�(z 0; z; g) = �

(C(z 0; g0(z; g))

C(z; g)

)�1C(z; g) =

∫(y("; k; �; z; g)� i("; k; �; z; g))dG(�)g("; k)d"dk

g0("; k) satisfies law of motion for distribution

50

Recursive Competitive Equilibrium

A set of v("; k ; z; g), C(z; g), w(z; g), �(z 0; z; g), and g0(z; g) suchthat

1. Taking �(z 0; z; g) and w(z; g) as given, firms optimize: v("; k ; z; g)solves Bellman equation

2. Taking w(z; g) as given, households optimize:w(z; g)C(z; g)�1 = a

3. Markets clear and aggregate consistency conditions hold:

�(z 0; z; g) = �

(C(z 0; g0(z; g))

C(z; g)

)�1C(z; g) =

∫(y("; k; �; z; g)� i("; k; �; z; g))dG(�)g("; k)d"dk

g0("; k) satisfies law of motion for distribution

50

Recursive Competitive Equilibrium

A set of v("; k ; z; g), C(z; g), w(z; g), �(z 0; z; g), and g0(z; g) suchthat

1. Taking �(z 0; z; g) and w(z; g) as given, firms optimize: v("; k ; z; g)solves Bellman equation

2. Taking w(z; g) as given, households optimize:w(z; g)C(z; g)�1 = a

3. Markets clear and aggregate consistency conditions hold:

�(z 0; z; g) = �

(C(z 0; g0(z; g))

C(z; g)

)�1C(z; g) =

∫(y("; k; �; z; g)� i("; k; �; z; g))dG(�)g("; k)d"dk

g0("; k) satisfies law of motion for distribution

50

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

50

Computing Equilibrium

• Key challenge: aggregate state g is infinite-dimensional

• Two steps:1. Compute steady state without aggregate shocks ! distribution

constant at g�

2. Compute full model with aggregate shocks ! distributionvaries over time

• Today will give you an overview to help you read papers• My HW2: solve steady state• With Greg: compute aggregate dynamics

51

Computing Equilibrium

• Key challenge: aggregate state g is infinite-dimensional

• Two steps:1. Compute steady state without aggregate shocks ! distribution

constant at g�

2. Compute full model with aggregate shocks ! distributionvaries over time

• Today will give you an overview to help you read papers• My HW2: solve steady state• With Greg: compute aggregate dynamics

51

Computing Equilibrium

• Key challenge: aggregate state g is infinite-dimensional

• Two steps:1. Compute steady state without aggregate shocks ! distribution

constant at g�

2. Compute full model with aggregate shocks ! distributionvaries over time

• Today will give you an overview to help you read papers• My HW2: solve steady state• With Greg: compute aggregate dynamics

51

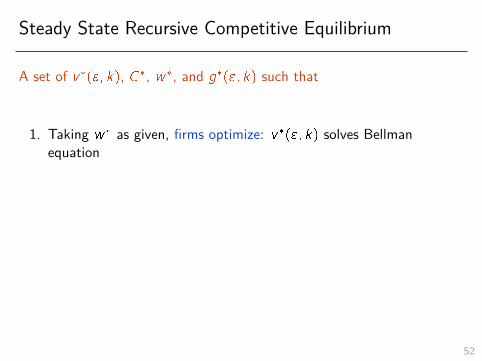

Steady State Recursive Competitive Equilibrium

A set of v�("; k), C�, w�, and g�("; k) such that

1. Taking w� as given, firms optimize: v�("; k) solves Bellmanequation

2. Taking w� as given, households optimize: w�(C�)�1 = a

3. Markets clear and aggregate consistency conditions hold:

C� =

∫(y("; k; �)� i("; k; �))dG(�)g�("; k)d"dk

g�("; k) satisfies law of motion for distribution given g�

52

Steady State Recursive Competitive Equilibrium

A set of v�("; k), C�, w�, and g�("; k) such that

1. Taking w� as given, firms optimize: v�("; k) solves Bellmanequation

2. Taking w� as given, households optimize: w�(C�)�1 = a

3. Markets clear and aggregate consistency conditions hold:

C� =

∫(y("; k; �)� i("; k; �))dG(�)g�("; k)d"dk

g�("; k) satisfies law of motion for distribution given g�

52

Steady State Recursive Competitive Equilibrium

A set of v�("; k), C�, w�, and g�("; k) such that

1. Taking w� as given, firms optimize: v�("; k) solves Bellmanequation

2. Taking w� as given, households optimize: w�(C�)�1 = a

3. Markets clear and aggregate consistency conditions hold:

C� =

∫(y("; k; �)� i("; k; �))dG(�)g�("; k)d"dk

g�("; k) satisfies law of motion for distribution given g�

52

Steady State Recursive Competitive Equilibrium

A set of v�("; k), C�, w�, and g�("; k) such that

1. Taking w� as given, firms optimize: v�("; k) solves Bellmanequation

2. Taking w� as given, households optimize: w�(C�)�1 = a

3. Markets clear and aggregate consistency conditions hold:

C� =

∫(y("; k; �)� i("; k; �))dG(�)g�("; k)d"dk

g�("; k) satisfies law of motion for distribution given g�

52

Hopenhayn-Rogerson (1993) Algorithm

Start with guess of w�

• Solve firm optimization problem ! v�("; k)

• Compute stationary distribution g�("; k)

• Compute implied aggregate consumption C�

• Check household optimization w�(C�)�1 = a

Update guess of w�

53

Hopenhayn-Rogerson (1993) Algorithm

Start with guess of w�

• Solve firm optimization problem ! v�("; k)

• Compute stationary distribution g�("; k)

• Compute implied aggregate consumption C�

• Check household optimization w�(C�)�1 = a

Update guess of w�

53

Hopenhayn-Rogerson (1993) Algorithm

Start with guess of w�

• Solve firm optimization problem ! v�("; k)

• Compute stationary distribution g�("; k)

• Compute implied aggregate consumption C�

• Check household optimization w�(C�)�1 = a

Update guess of w�

53

Hopenhayn-Rogerson (1993) Algorithm

Start with guess of w�

• Solve firm optimization problem ! v�("; k)

• Compute stationary distribution g�("; k)

• Compute implied aggregate consumption C�

• Check household optimization w�(C�)�1 = a

Update guess of w�

53

Hopenhayn-Rogerson (1993) Algorithm

Start with guess of w�

• Solve firm optimization problem ! v�("; k)

• Compute stationary distribution g�("; k)

• Compute implied aggregate consumption C�

• Check household optimization w�(C�)�1 = a

Update guess of w�

53

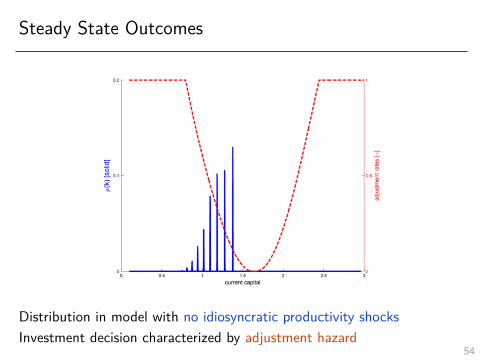

Steady State Outcomes

Distribution in model with no idiosyncratic productivity shocksInvestment decision characterized by adjustment hazard

54

Steady State Outcomes

Distribution in model with no idiosyncratic productivity shocks

Investment decision characterized by adjustment hazard

54

Steady State Outcomes

Distribution in model with no idiosyncratic productivity shocksInvestment decision characterized by adjustment hazard

54

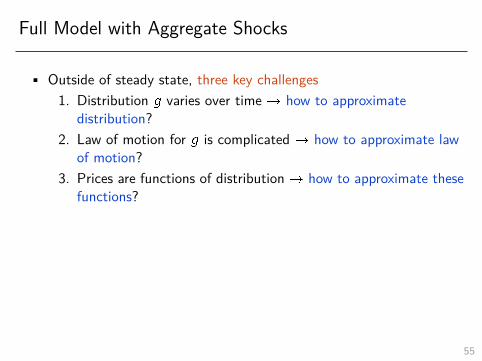

Full Model with Aggregate Shocks

• Outside of steady state, three key challenges

1. Distribution g varies over time ! how to approximatedistribution?

2. Law of motion for g is complicated ! how to approximate lawof motion?

3. Prices are functions of distribution ! how to approximate thesefunctions?

• Will briefly describe two approaches to dealing with these challenges1. Krusell and Smith (1998): approximate distribution with

moments2. Winberry (2016): approximate distribution with flexible

parametric family

• Next quarter you will learn how continuous time makes this easier(Ahn-Kaplan-Moll-Winberry-Wolf)

55

Full Model with Aggregate Shocks

• Outside of steady state, three key challenges1. Distribution g varies over time ! how to approximate

distribution?

2. Law of motion for g is complicated ! how to approximate lawof motion?

3. Prices are functions of distribution ! how to approximate thesefunctions?

• Will briefly describe two approaches to dealing with these challenges1. Krusell and Smith (1998): approximate distribution with

moments2. Winberry (2016): approximate distribution with flexible

parametric family

• Next quarter you will learn how continuous time makes this easier(Ahn-Kaplan-Moll-Winberry-Wolf)

55

Full Model with Aggregate Shocks

• Outside of steady state, three key challenges1. Distribution g varies over time ! how to approximate

distribution?2. Law of motion for g is complicated ! how to approximate law

of motion?

3. Prices are functions of distribution ! how to approximate thesefunctions?

• Will briefly describe two approaches to dealing with these challenges1. Krusell and Smith (1998): approximate distribution with

moments2. Winberry (2016): approximate distribution with flexible

parametric family

• Next quarter you will learn how continuous time makes this easier(Ahn-Kaplan-Moll-Winberry-Wolf)

55

Full Model with Aggregate Shocks

• Outside of steady state, three key challenges1. Distribution g varies over time ! how to approximate

distribution?2. Law of motion for g is complicated ! how to approximate law

of motion?3. Prices are functions of distribution ! how to approximate these

functions?

• Will briefly describe two approaches to dealing with these challenges1. Krusell and Smith (1998): approximate distribution with

moments2. Winberry (2016): approximate distribution with flexible

parametric family

• Next quarter you will learn how continuous time makes this easier(Ahn-Kaplan-Moll-Winberry-Wolf)

55

Full Model with Aggregate Shocks

• Outside of steady state, three key challenges1. Distribution g varies over time ! how to approximate

distribution?2. Law of motion for g is complicated ! how to approximate law

of motion?3. Prices are functions of distribution ! how to approximate these

functions?

• Will briefly describe two approaches to dealing with these challenges1. Krusell and Smith (1998): approximate distribution with

moments2. Winberry (2016): approximate distribution with flexible

parametric family

• Next quarter you will learn how continuous time makes this easier(Ahn-Kaplan-Moll-Winberry-Wolf)

55

Full Model with Aggregate Shocks

• Outside of steady state, three key challenges1. Distribution g varies over time ! how to approximate

distribution?2. Law of motion for g is complicated ! how to approximate law

of motion?3. Prices are functions of distribution ! how to approximate these

functions?

• Will briefly describe two approaches to dealing with these challenges1. Krusell and Smith (1998): approximate distribution with

moments2. Winberry (2016): approximate distribution with flexible

parametric family

• Next quarter you will learn how continuous time makes this easier(Ahn-Kaplan-Moll-Winberry-Wolf) 55

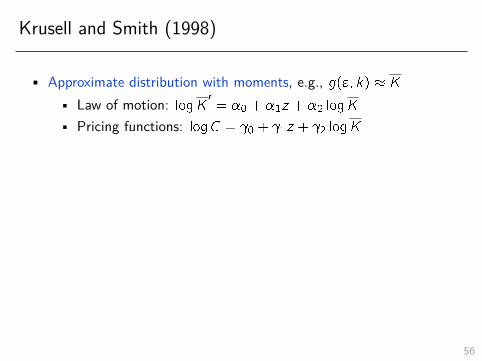

Krusell and Smith (1998)

• Approximate distribution with moments, e.g., g("; k) � K

• Law of motion: logK0= �0 + �1z + �2 logK

• Pricing functions: logC = 0 + 1z + 2 logK

• Given guess � and

• Compute individual decisions v("; k ; z;K)• Simulate decision rules ! fKt ; Ct ; ztg

• Update � and using OLS

• R2 on regressions typical accuracy measure• Problems with this measure: Den Haan (2010)• Only K matters ! distribution not important (“approximate

aggregation”)

56

Krusell and Smith (1998)

• Approximate distribution with moments, e.g., g("; k) � K

• Law of motion: logK0= �0 + �1z + �2 logK

• Pricing functions: logC = 0 + 1z + 2 logK

• Given guess � and

• Compute individual decisions v("; k ; z;K)• Simulate decision rules ! fKt ; Ct ; ztg

• Update � and using OLS

• R2 on regressions typical accuracy measure• Problems with this measure: Den Haan (2010)• Only K matters ! distribution not important (“approximate

aggregation”)

56

Krusell and Smith (1998)

• Approximate distribution with moments, e.g., g("; k) � K

• Law of motion: logK0= �0 + �1z + �2 logK

• Pricing functions: logC = 0 + 1z + 2 logK

• Given guess � and

• Compute individual decisions v("; k ; z;K)• Simulate decision rules ! fKt ; Ct ; ztg

• Update � and using OLS

• R2 on regressions typical accuracy measure• Problems with this measure: Den Haan (2010)• Only K matters ! distribution not important (“approximate

aggregation”)

56

Krusell and Smith (1998)

• Approximate distribution with moments, e.g., g("; k) � K

• Law of motion: logK0= �0 + �1z + �2 logK

• Pricing functions: logC = 0 + 1z + 2 logK

• Given guess � and

• Compute individual decisions v("; k ; z;K)• Simulate decision rules ! fKt ; Ct ; ztg

• Update � and using OLS

• R2 on regressions typical accuracy measure• Problems with this measure: Den Haan (2010)• Only K matters ! distribution not important (“approximate

aggregation”)

56

Krusell and Smith (1998)

• Approximate distribution with moments, e.g., g("; k) � K

• Law of motion: logK0= �0 + �1z + �2 logK

• Pricing functions: logC = 0 + 1z + 2 logK

• Given guess � and

• Compute individual decisions v("; k ; z;K)• Simulate decision rules ! fKt ; Ct ; ztg

• Update � and using OLS

• R2 on regressions typical accuracy measure• Problems with this measure: Den Haan (2010)• Only K matters ! distribution not important (“approximate

aggregation”)56

Winberry (2016)

• Approximate distribution with parametric family:

g ("; k) �= g0 expfg11

("�m1

1

)+ g21

(k �m2

1

)+

ng∑i=2

i∑j=0

gji

[("�m1

1

)i�j (k �m2

1

)j�mj

i

]g

! Aggregate state approximated by (z; g("; k)) � (z;m)

• Compute law of motion + prices directly by integration

• Compute aggregate dynamics using perturbation methods• Solve for steady state in Matlab• Solve for aggregate dynamics using Dynare

57

Winberry (2016)

• Approximate distribution with parametric family:

g ("; k) �= g0 expfg11

("�m1

1

)+ g21

(k �m2

1

)+

ng∑i=2

i∑j=0

gji

[("�m1

1

)i�j (k �m2

1

)j�mj

i

]g

! Aggregate state approximated by (z; g("; k)) � (z;m)

• Compute law of motion + prices directly by integration

• Compute aggregate dynamics using perturbation methods• Solve for steady state in Matlab• Solve for aggregate dynamics using Dynare

57

Winberry (2016)

• Approximate distribution with parametric family:

g ("; k) �= g0 expfg11

("�m1

1

)+ g21

(k �m2

1

)+

ng∑i=2

i∑j=0

gji

[("�m1

1

)i�j (k �m2

1

)j�mj

i

]g

! Aggregate state approximated by (z; g("; k)) � (z;m)

• Compute law of motion + prices directly by integration

• Compute aggregate dynamics using perturbation methods• Solve for steady state in Matlab• Solve for aggregate dynamics using Dynare

57

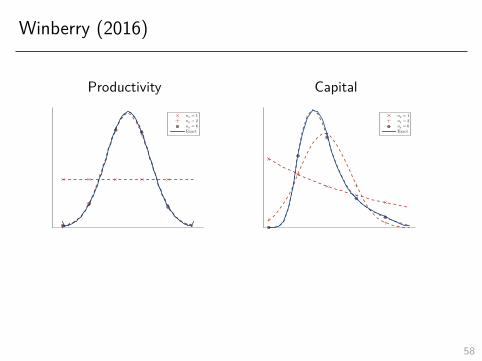

Winberry (2016)

Productivity Capitalng = 1

ng = 2

ng = 6

Exact

ng = 1

ng = 2

ng = 6

Exact

• Run time � 20 - 40 seconds for accurate approximation• Fast enough for likelihood-based estimation• Codes at my website

58

Winberry (2016)

Productivity Capitalng = 1

ng = 2

ng = 6

Exact

ng = 1

ng = 2

ng = 6

Exact

• Run time � 20 - 40 seconds for accurate approximation• Fast enough for likelihood-based estimation• Codes at my website

58

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

58

Khan and Thomas (2008) Calibration

Parameter Description ValueHouseholds� Discount factor :961

Labor disutility N� = 13

Firms� Labor share :64

� Capital share :256

� Capital depreciation :085

� Fixed cost :0083

a No fixed cost region :011

�" Idiosyncratic TFP AR(1) :859

�" Idiosyncratic TFP AR(1) :022

Aggregate shock�z Aggregate TFP AR(1) :859

�z Aggregate TFP AR(1) :014

59

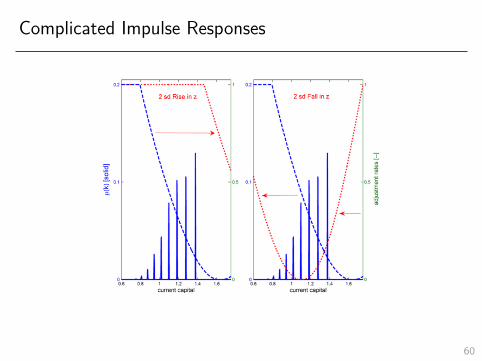

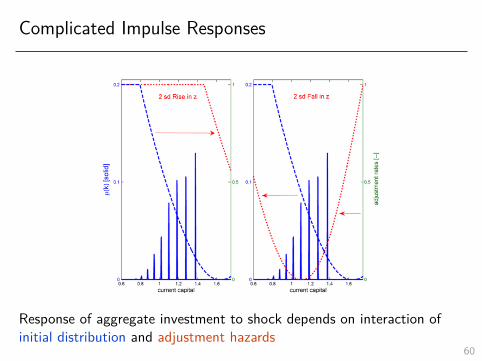

Complicated Impulse Responses

Response of aggregate investment to shock depends on interaction ofinitial distribution and adjustment hazards

60

Complicated Impulse Responses

Response of aggregate investment to shock depends on interaction ofinitial distribution and adjustment hazards

60

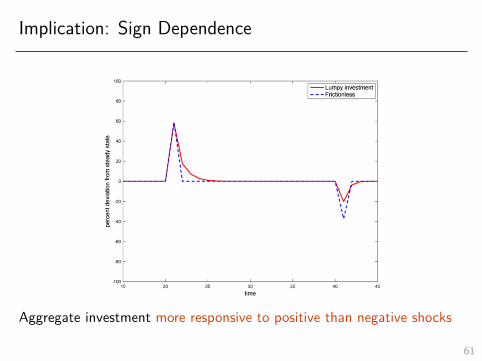

Implication: Sign Dependence

Aggregate investment more responsive to positive than negative shocksNote true in frictionless model

61

Implication: Sign Dependence

Aggregate investment more responsive to positive than negative shocks

Note true in frictionless model

61

Implication: Sign Dependence

Aggregate investment more responsive to positive than negative shocksNote true in frictionless model

61

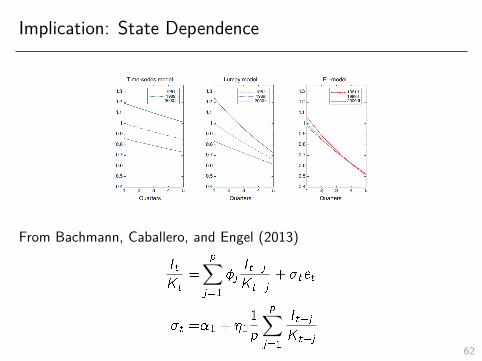

Implication: State Dependence

From Bachmann, Caballero, and Engel (2013)

It

Kt

=

p∑j=1

�jIt�jKt�j

+ �tet

�t =�1 + �11

p

p∑j=1

It�jKt�j

62

Aggregate Nonlinearities

• Both of these are examples of nonlinear aggregate dynamics• Linear model has constant loading on aggregate shock

• Some evidence in aggregate data• Sign and state dependence ! distribution of It

Ktpositively

skewed• State dependence ! dynamics of It

Ktfeature conditional

heteroskedasticity

• My view: time series evidence is suggestive at best• Predictions are about extreme states, which are rare• But that is exactly when we care about these predictions!! rely on cross-sectional data + carefully specified generalequilibrium model

63

Aggregate Nonlinearities

• Both of these are examples of nonlinear aggregate dynamics• Linear model has constant loading on aggregate shock

• Some evidence in aggregate data• Sign and state dependence ! distribution of It

Ktpositively

skewed• State dependence ! dynamics of It

Ktfeature conditional

heteroskedasticity

• My view: time series evidence is suggestive at best• Predictions are about extreme states, which are rare• But that is exactly when we care about these predictions!! rely on cross-sectional data + carefully specified generalequilibrium model

63

Aggregate Nonlinearities

• Both of these are examples of nonlinear aggregate dynamics• Linear model has constant loading on aggregate shock

• Some evidence in aggregate data• Sign and state dependence ! distribution of It

Ktpositively

skewed• State dependence ! dynamics of It

Ktfeature conditional

heteroskedasticity

• My view: time series evidence is suggestive at best• Predictions are about extreme states, which are rare• But that is exactly when we care about these predictions!! rely on cross-sectional data + carefully specified generalequilibrium model

63

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

5. If time, discuss policy implications63

Distribution of Aggregate It

Kt

in Partial Equilibrium

64

Distribution of Aggregate It

Kt

in General Equilibrium

65

Distribution of Aggregate It

Kt

in General Equilibrium

65

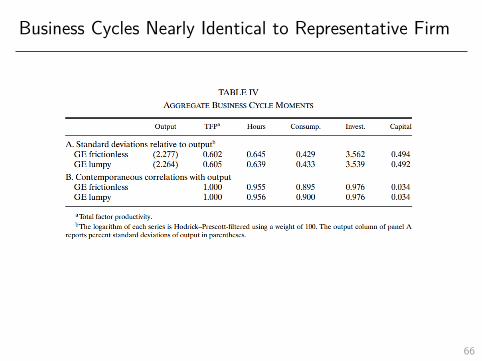

Business Cycles Nearly Identical to Representative Firm

66

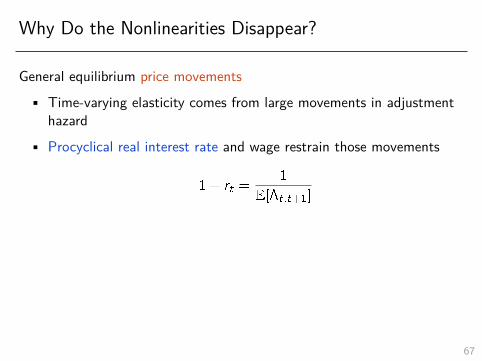

Why Do the Nonlinearities Disappear?

General equilibrium price movements• Time-varying elasticity comes from large movements in adjustment

hazard• Procyclical real interest rate and wage restrain those movements

1 + rt =1

E[�t;t+1]

Specification of adjustment costs• Calibrated adjustment costs small

67

Why Do the Nonlinearities Disappear?

General equilibrium price movements• Time-varying elasticity comes from large movements in adjustment

hazard• Procyclical real interest rate and wage restrain those movements

1 + rt =1

E[�t;t+1]

Specification of adjustment costs• Calibrated adjustment costs small

67

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium

67

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs: Bachmann,

Caballero, Engel (2013), Gourio and Kashyap (2007)• Specification of general equilibrium

67

Bachmann, Caballero, and Engel (2013)

• Argue Khan and Thomas’ calibration of adjustment costsresponsible for irrelevance result

• Calibrate larger adjustment costs and recover aggregatenonlinearities

• Argument based on decomposition between AC smoothing and PRsmoothing

• Frictionless partial equilibrium model excessively volatile• AC smoothing: dampening due to adjustment costs• PR smoothing: dampening due to price movements

• Measure AC smoothing in data and target in calibration ! higheradjustment costs

68

Bachmann, Caballero, and Engel (2013)

• Argue Khan and Thomas’ calibration of adjustment costsresponsible for irrelevance result

• Calibrate larger adjustment costs and recover aggregatenonlinearities

• Argument based on decomposition between AC smoothing and PRsmoothing

• Frictionless partial equilibrium model excessively volatile• AC smoothing: dampening due to adjustment costs• PR smoothing: dampening due to price movements

• Measure AC smoothing in data and target in calibration ! higheradjustment costs

68

Model

Production technology yjt = ezte"ste"jtk�jtn�jt , � + � < 1

• Idiosyncratic productivity shock "jt+1 = ��"jt + !"jt+1 where

!"jt+1 � N(0; �2� )

• Aggregate productivity shock zt+1 = �zzt + !zt+1 where

!zt+1 � N(0; �2z )

• Sectoral productivity shock "st+1 = ��"st + !"st+1 where

!"st+1 � N(0; �2�s )

Firms accumulate capital according to kjt+1 = (1� �)kjt + ijt

• If don’t pay fixed cost, must undertake maintenance investment�� �kjt

• Otherwise, pay fixed cost �jt in units of labor• Fixed cost �jt � U[0; �]

69

Model

Production technology yjt = ezte"ste"jtk�jtn�jt , � + � < 1

• Idiosyncratic productivity shock "jt+1 = ��"jt + !"jt+1 where

!"jt+1 � N(0; �2� )

• Aggregate productivity shock zt+1 = �zzt + !zt+1 where

!zt+1 � N(0; �2z )

• Sectoral productivity shock "st+1 = ��"st + !"st+1 where

!"st+1 � N(0; �2�s )

Firms accumulate capital according to kjt+1 = (1� �)kjt + ijt

• If don’t pay fixed cost, must undertake maintenance investment�� �kjt

• Otherwise, pay fixed cost �jt in units of labor• Fixed cost �jt � U[0; �]

69

Calibration

Set most parameters exogenously

Choose �z , �, and � to match degree of AC-smoothing• Identify AC-smoothing using volatility of sectoral investment rates

• Aggregated enough to capture interaction of distribution andhazards

• Small enough to not generate price response

• Targets:1. Volatility of aggregate investment rate2. Average volatility of sectoral investment rates3. Amount of conditional heteroskedasticity

70

Calibration

Set most parameters exogenously

Choose �z , �, and � to match degree of AC-smoothing• Identify AC-smoothing using volatility of sectoral investment rates

• Aggregated enough to capture interaction of distribution andhazards

• Small enough to not generate price response

• Targets:1. Volatility of aggregate investment rate2. Average volatility of sectoral investment rates3. Amount of conditional heteroskedasticity

70

AC vs. PR Smoothing Decomposition

UB = log [�(none)=�(AC)] = log [�(none)=�(both)]LB =1� log [�(none)=�(PR)] = log [�(none)=�(both)]

71

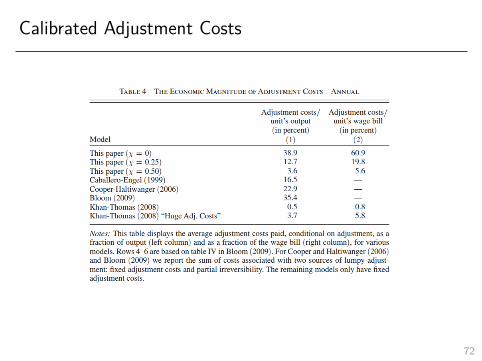

Calibrated Adjustment Costs

72

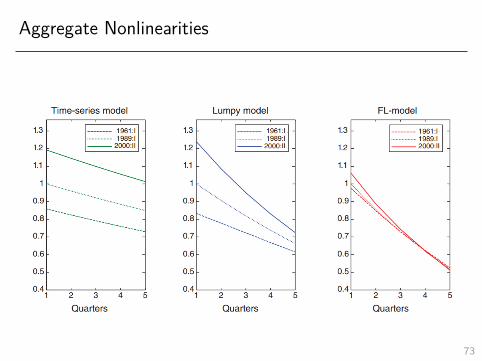

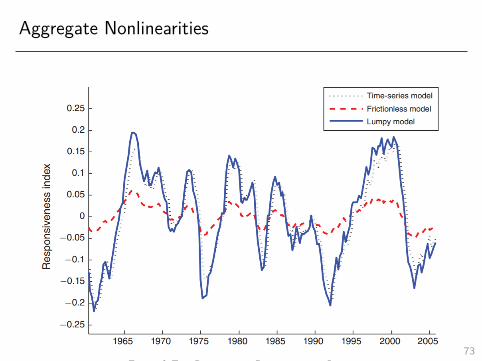

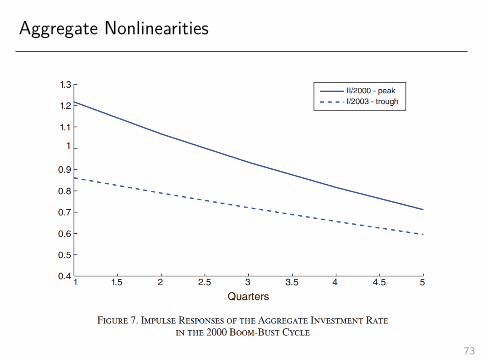

Aggregate Nonlinearities

73

Aggregate Nonlinearities

73

Aggregate Nonlinearities

73

Aggregate Nonlinearities

73

Outline of Next Steps

1. Benchmark general equilibrium model with lumpy investment: Khanand Thomas (2008)

• Aside: how to numerically compute heterogeneous agent models

2. Model generates time-varying elasticity in partial equilibrium

3. Model generates constant elasticity in general equilibrium

4. Two broad responses to irrelevance result in literature• Specification of micro-level adjustment costs• Specification of general equilibrium: Winberry (2016),

Bachmann and Ma (2016), Cooper and Willis (2014)

73

Winberry (2016)

• Argue that procyclical interest rate in Khan and Thomas’ modelinconsistent with data

• Cooper and Willis (2014): feed in from data• Winberry (2016): general equilibrium model

• When consistent with data recover aggregate nonlinearities

� (rt) � (rt ; yt�1) � (rt ; yt) � (rt ; yt+1)

T-bill 2.18% -0.08 -0.17 -0.251AAA 2.34% -0.29 –0.37 -0.40BAA 2.43% -0.32 -0.41 -0.45Stock 24.7% -0.24 -0.14 0.02RBC 0.16% 0.61 0.97 0.74

74

Winberry (2016)

• Argue that procyclical interest rate in Khan and Thomas’ modelinconsistent with data

• Cooper and Willis (2014): feed in from data• Winberry (2016): general equilibrium model

• When consistent with data recover aggregate nonlinearities

� (rt) � (rt ; yt�1) � (rt ; yt) � (rt ; yt+1)

T-bill 2.18% -0.08 -0.17 -0.251AAA 2.34% -0.29 –0.37 -0.40BAA 2.43% -0.32 -0.41 -0.45Stock 24.7% -0.24 -0.14 0.02RBC 0.16% 0.61 0.97 0.74

74

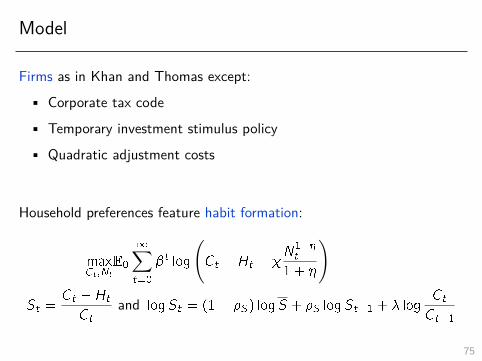

Model

Firms as in Khan and Thomas except:• Corporate tax code• Temporary investment stimulus policy• Quadratic adjustment costs

Household preferences feature habit formation:

maxCt ;Nt

E0

1∑t=0

�t log

(Ct �Ht � �

N1+�t

1 + �

)

St =Ct �Ht

Ctand logSt = (1� �S) logS + �S logSt�1 + � log

Ct

Ct�1

75

Model

Firms as in Khan and Thomas except:• Corporate tax code• Temporary investment stimulus policy• Quadratic adjustment costs

Household preferences feature habit formation:

maxCt ;Nt

E0

1∑t=0

�t log

(Ct �Ht � �

N1+�t

1 + �

)

St =Ct �Ht

Ctand logSt = (1� �S) logS + �S logSt�1 + � log

Ct

Ct�1

75

Calibration

Set most parameters exogeneously

Choose parameters governing micro heterogeneity and habit formation tomatch micro investment data and real interest rate dynamics

• Real interest rate dynamics pin down capital supply and demandcurves

• Capital supply: households smoothing consumption ! habitformation

• Capital demand: firms demanding future capital ! shocks andadjustment costs

• Micro investment data pins down shocks and adjustment costs

76

Calibration

Set most parameters exogeneously

Choose parameters governing micro heterogeneity and habit formation tomatch micro investment data and real interest rate dynamics

• Real interest rate dynamics pin down capital supply and demandcurves

• Capital supply: households smoothing consumption ! habitformation

• Capital demand: firms demanding future capital ! shocks andadjustment costs

• Micro investment data pins down shocks and adjustment costs

76

Calibration

76

Calibration

76

State Dependence of Stimulus Policy

price of investment = 1� subt

77

Increasing Cost Effectiveness of Policy

subjt = �1 � n�2jt

78

Conclusion: Takeaways from Topic 2

1. Investment is lumpy in the microdata

2. Structural micro models provide evidence for nonconvex adjustmentcosts

• SMM estimation

3. Calibrated macro models indicate possibly generates time-varyingaggregate elasticity

• Aggregation and general equilibrium both important• Solving models with distribution in state vector

79

Conclusion: Takeaways from Topic 2

1. Investment is lumpy in the microdata

2. Structural micro models provide evidence for nonconvex adjustmentcosts

• SMM estimation

3. Calibrated macro models indicate possibly generates time-varyingaggregate elasticity

• Aggregation and general equilibrium both important• Solving models with distribution in state vector

79

Conclusion: Takeaways from Topic 2

1. Investment is lumpy in the microdata

2. Structural micro models provide evidence for nonconvex adjustmentcosts

• SMM estimation

3. Calibrated macro models indicate possibly generates time-varyingaggregate elasticity

• Aggregation and general equilibrium both important• Solving models with distribution in state vector

79

![Welcome 1 [kirtoninlindseytownhall.co.uk]...white labels 2” x 1” (5cm. x 2.5cm) positioned 1” (2.5cm) from the bottom of the bottle. Special rules for Class A23 and C20 are included](https://img.dokumen.tips/doc/110x75/5f0c70e37e708231d4356a58/welcome-1-kir-white-labels-2a-x-1a-5cm-x-25cm-positioned-1a-25cm.jpg)

![5cr+ lcm 5mm 2.5cm 24 2.5cm lcm 26cm 26cm 16cm 3.5cm lcm … · 2019-08-06 · .5cr+ lcm 5mm 2.5cm 24 2.5cm lcm 26cm 26cm 16cm 3.5cm lcm vol. : 10 era 19.5cm 25cm [7] (A4#4ÃL1-E)](https://img.dokumen.tips/doc/110x75/5f56c58c967c2a15a3138f0b/5cr-lcm-5mm-25cm-24-25cm-lcm-26cm-26cm-16cm-35cm-lcm-2019-08-06-5cr-lcm.jpg)