Embed Size (px)

Citation preview

2019 EDITION

Tax Guidefor Property Managers

PAGE 4 Top Ten Deductions For Property ManagersCar Deductions Office Expenses Business Travel Advertising and Marketing Deducting Long-Term Assets Rent for Equipment and Tools Pass-Through Tax Deduction Legal and Professional Services Insurance Employees and Independent Contractors

Introduction by Stephen FishmanPAGE 3

What’s Inside...

Tax Credits

Important Dates

Filing Your Tax Returns

Resources

Filing IRS Form 1099

About the Author

About Buildium

PAGE 22

PAGE 35

PAGE 25

PAGE 38

PAGE 28

PAGE 40

PAGE 41

2019 has largely been a year of incremental adjustments to the tax code, just two years after the Tax Cuts and Jobs Act (TCJA) overhaul first took effect. The IRS used this time to clarify how many of the most important provisions of the TCJA should work in the real world, which includes added clarity on when rental property owners may claim the new pass-through deduction. All the significant updates and changes during 2019 are covered in this updated guide.

Whether you work alone or with others, full-time or part-time, you need to understand how taxes affect your property management business. This guide provides an invaluable overview of what expenses you can and cannot deduct, and important tax credits you may be able to claim.

By taking advantage of every deduction and credit you are entitled to, you’ll be able to minimize the taxes you have to pay on your property management income.

Of course, being entitled to tax deductions and credits will do you no good unless you file your tax return properly and on-time. This guide explains how to do this, too. If you live in one of the 43 states that have their own income taxes, you’ll also find information on how to file your state tax return.

One of a property manager’s most important tax responsibilities is to file IRS Form 1099s that report their clients’ rental receipts. Failure to do so can result in IRS penalties. A special section of this guide explains when and how you must make such filings.

Disclaimer: This guide is not a substitute for a tax professional, and likely does not answer every conceivable tax question you may have. It includes links to additional do-it-yourself tax resources that may help you answer your questions. Otherwise, seek assistance from a competent tax professional—a CPA or enrolled agent familiar with small business taxes.

IntroductionBy Stephen Fishman, J.D

32019 Tax Guide for Property Managers

42019 Tax Guide for Property Managers

Property managers are engaged in a service business and are entitled to the full array of business-re-lated tax deductions. Almost everything you buy for your business is tax deductible sooner or later, so long as it’s ordinary, necessary, and the cost isn’t unreasonable.

The Tax Cuts and Jobs Act established a new set of tax rates ranging from 10% to 37%. These rates are lower than those from 2017 and earlier—for example, the top rate for 2017 was 39.6%. The 2019 tax rates are shown below in the following chart:

2019 Federal Income Tax Rates

Rate Married Filing Jointly Individual Return

10% $0 - $19,400 $0 - $9,700

12% $19,401- $78,950 $9,701 - $39,475

22% $78,951 - $168,400 $39,476 - $84,200

24% $168,401 - $321,450 $84,201 - $160,725

32% $321,451 - $408,200 $160,726 - $204,100

35% $408,201 - $612,350 $204,201 - $510,300

37% over $612,350 over $510,300

Top Ten Deductions ForProperty Managers

In addition to federal income taxes, self-employed property managers must pay Social Security and Medicare tax on their net self-employment income.

The Social Security tax is a flat 12.4% tax up to an annual ceiling ($132,900 in 2019). The Medicare tax is a 2.9% tax up to $200,000 for single taxpayers and $250,000 for married couples filing jointly. All income above the $200,000/$250,000 ceiling is taxed at a 3.8% rate.

Add in state income tax, and a married taxpayer with an income of $100,000 can save as much as 22% (in federal income tax) + 15.3% (in self-employment taxes) + 6% (in state taxes, depending on which state you live in).

That adds up to a whopping 43.3% savings. In other words, for every dollar you spend on your business, you save about 43 cents in taxes.

Here are ten of the most common tax deductions taken by property managers.

52019 Tax Guide for Property Managers

62019 Tax Guide for Property Managers

The cost of driving around town for your business (with the exception of commuting to and from your home to work) is tax deductible. If you don’t mind record keeping, you should keep track of all your car expenses to figure your annual deduction.

There are two ways to deduct your car expenses: using the actual expense method or the standard mileage rate. The actual expense method is more work because it requires you to keep track of all your car expenses, such as gas and repairs, as well as the number of miles you drive for business. However, it can result in a larger deduction, especially if you have a high-priced car. This is because the Tax Cuts and Jobs Act greatly increased the depreciation deduction for cars. If you place a car into service in your business during 2019, you can deduct as much $18,100 in regular and bonus depreciation for the year. To deduct this much you’d have to buy a car that costs as least $50,000 and use it 100% for business—you’ll get a proportionally smaller deduction if you buy a cheaper car and/or use it for both business and personal driving.

But, if you’d rather not keep on top of how much you spend for gas, oil, repairs, car washes, and so forth, you can use the standard mileage rate. With the standard rate, you only need to keep track of how many miles you drive for the business, not how much you spend on your car.

For 2019, the standard mileage rate is 58 cents per mile. Note: If you want to use the standard mileage rate, you must use it the first year you use your car for business. You can later switch to the actual expense method if you want.

Car Deductions

01

Ed drove his car 10,000 miles for his property management business during the tax year, so he simply multiplies this by 58 cents to determine his car expense deduction (58 cents x 10,000 = $5,800). His federal income tax bracket is 24%, so this deduction saves him $1,392 in federal income tax for 2019. He also saves $893 in self-employment tax (Social Security and Medicare tax). His total federal tax savings is $2,285.

Example

82019 Tax Guide for Property Managers

The amounts you spend on your business office are deductible business expenses. For example, you may deduct the rent and utilities you spend for an office or other workspace (outside of your home).

If you work at home, you may deduct the cost of your home office, provided that you use the space exclusively for business. The amount of the deduction is based on the percentage of your home you use for your business office. Alternatively, you may use an optional simplified method of calculating the home office deduction which permits a deduction of $5 for every square foot of your home office (up to 300 square feet).

This deduction is particularly valuable if you’re a renter, because you are able to deduct a portion of your monthly rent, a sizeable expense that is ordinarily not deductible. For the ins and outs on taking the home office deduction, see Deduct It! Lower Your Small Business Taxes, by Stephen Fishman (Nolo).

If you own your home, the TCJA capped the personal deduction for state and local taxes, including property taxes, at $10,000 per year for 2018 through 2025. If you take the home office deduction, you have the option of deducting the home office percentage of your property tax payments as part of your home office deduction. If you do this, amount does not count toward the $10,000 cap.

Office Expenses

02

Jake spends $1,000/month on the office and utilities he uses for his property management business. This results in a $12,000 tax deduction. His federal income tax bracket is 24%, so this saves him $2,880 in federal income tax for 2019. He also saves $441 in Social Security and Medicare tax. His total federal tax savings is $3,321.

Example

102019 Tax Guide for Property Managers

You may also deduct your expenses when you go out of town for business. Business-related meals are deductible when travelling or at home.

Travel: Deductible expenses include airfare, transportation (rental car, taxis, etc...), and hotel or lodging. But, you may only deduct 50% of the cost of meals when you travel for business. If you plan things right, you can even mix pleasure with business and still get a deduction.

Meals: 50% of meal costs are deductible if the meal is business related. Meals eaten while travelling on business are always deductible. Meals eaten at home are also 50% deductible if they are incurred in the course of your business. You or an employee need to be present at the meal. Moreover, the meal must be furnished to current or potential customers, consultants, clients or similar business contacts. The IRS does not require that you actually close a deal or get some other specific business benefit to take this deduction.

Business Travel and Meals

03

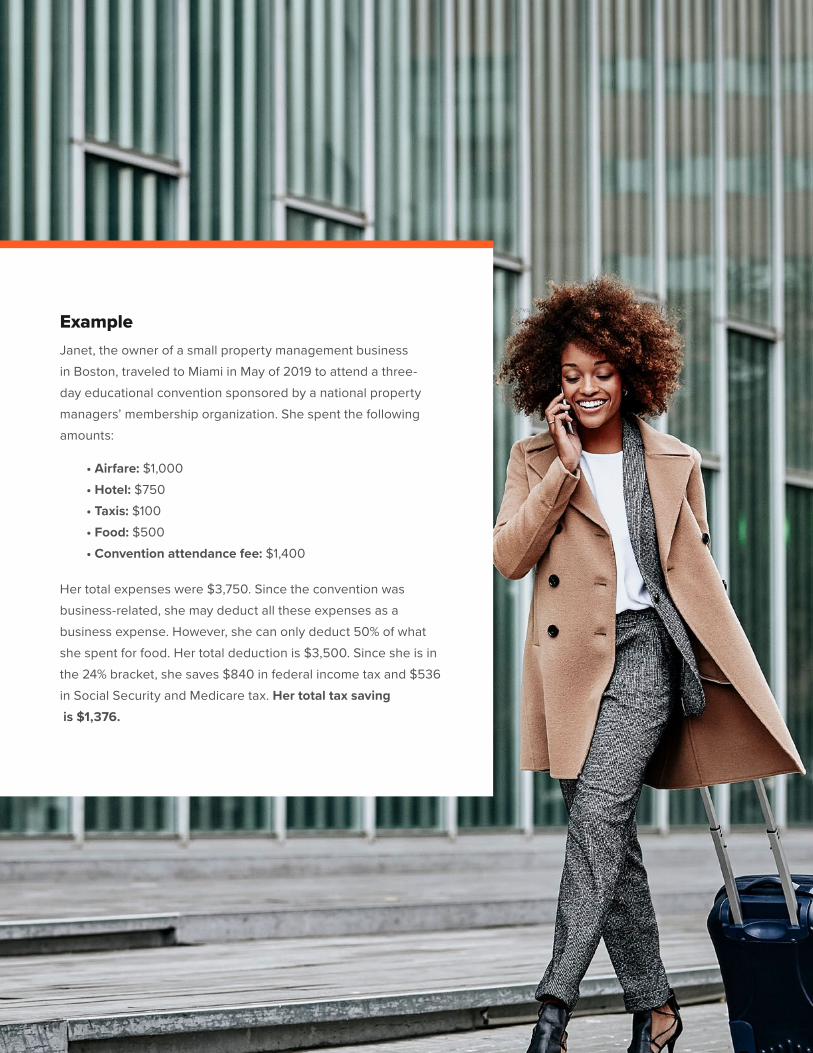

Janet, the owner of a small property management business in Boston, traveled to Miami in May of 2019 to attend a three-day educational convention sponsored by a national property managers’ membership organization. She spent the following amounts:

Example

• Airfare: $1,000 • Hotel: $750 • Taxis: $100 • Food: $500 • Convention attendance fee: $1,400

Her total expenses were $3,750. Since the convention was business-related, she may deduct all these expenses as a business expense. However, she can only deduct 50% of what she spent for food. Her total deduction is $3,500. Since she is in the 24% bracket, she saves $840 in federal income tax and $536 in Social Security and Medicare tax. Her total tax saving is $1,376.

122019 Tax Guide for Property Managers

Any expenses incurred to advertise and market your property management business are deductible. Advertising includes expenses for business cards and brochures; ads in newspapers, magazines, real estate publications, and online; fees paid to advertising and public relations agencies; and signage for your business.

However, advertising to influence government legislation is never deductible.

The costs of developing and maintaining a website for your business are also deductible operating expenses. This includes the costs of ongoing website hosting, maintenance, and updating. Money you spend to get people to view your website, such as SEO (search engine optimization) or Paid Search campaigns, is also a deductible advertising expense.

The cost of initially developing your website, though, may constitute a capital expense, not a currently deductible business operating expense. If so, the cost may have to be deducted over three years, unless it qualifies for Section 179 expensing. Section 179 allows businesses to deduct a substantial amount of capital expenses in a single year. (Learn more under the next section, “Deducting Long-Term Assets.”)

Advertising & Marketing

04

Acme Property Management, LLC spends $1,000 per month for advertising on Google Display Network, and $500 per month to keep its website up and running. The annual $18,000 expense is currently a deductible business operating expense. Since Acme is a limited liability company that is taxed like a partnership, its profits (after being reduced by its expenses) are passed through the company to its three owners who pay tax on them at a 24% rate. Thus, the $18,000 deduction saves them a total of $4,320 in federal income tax.

Example

132019 Tax Guide for Property Managers

Special tax rules apply to deducting property you buy for your business that has a useful life of more than one year (buildings, equipment, vehicles, books, office furniture, machinery, computers and other electronics). In the past, most business owners had to deduct the cost of such property a little at a time over several years—a process called depreciation. However, recent changes in the law permit small business owners to deduct the entire cost of such property in a single year. These deductions include:

Deducting Long-term Assets

De minimis safe harbor: What the IRS calls “de minimis safe harbor” allows for the deduction of the cost of personal property items you use in your business, up to $2,500 a piece, as shown on the invoice. If the cost exceeds $2,500 per invoice (or item), no part of the cost may be deducted by using the de minimis safe harbor. To use this deduction, you must file an annual election with your tax return—something that is easy to do.

Bonus depreciation: If you purchase an item that costs more than $2,500, you may still be able to deduct the full cost in one year using bonus depreciation. Bonus depreciation allows a business owner to deduct a substantial amount of a long-term asset’s cost in the single year, instead of depreciating the cost over many years. As a result of the TCJA, the bonus depreciation amount was increased to 100% of an asset’s cost during 2018 through 2022. In other words, the full cost may be deducted in one year. In addition, bonus depreciation may be used for purchases of used as well as new property. Bonus depreciation may not be applied to real property—thus it may not be used for buildings and building improvements.

However, it may be used by landlords when they purchase new or used personal property for their rental activity—for example: appliances, furniture purchased for rental units, office furniture and equipment used in landlord and property manager offices, removable flooring and carpeting, cabinets and counters, wall paneling, and decorative and track lighting. Bonus depreciation may also serve as a deduction for depreciable land improvements such as swimming pools, sidewalks, fences, landscaping, hot tubs, and driveways

05

142019 Tax Guide for Property Managers

Section 179 can be used to deduct much the same property as bonus depreciation. However, unlike bonus depreciation, Section 179 is subject to an annual dollar limit. For 2019, the annual limit is $1,020,000. The annual limit amount is reduced (but not below zero) by the amount by which the cost of property placed in service during the year exceeds $2,550,000. However, a business owner may not deduct more than his or her net taxable business income for the year. Before 2018, Section 179 couldn’t be used to deduct personal property used in residential rental units—for example, kitchen appliances, carpets, drapes, or blinds. The Tax Cuts and Jobs Act eliminated this prohibition starting in 2018. Section 179 may also serve to deduct the cost of building components in nonresidential real property.

Regular depreciation: Items that can’t be deducted in a single year can always be deducted a portion at a time over several years using depreciation. Most of the assets you buy for your business will probably have to be depreciated over five to seven years.

Sam, who runs his small property management business as a sole proprietor, purchases a complete set of tools to perform repairs on his clients’ rentals. This includes hammers, saws, wrenches, screwdrivers, and similar items. He elects to deduct the entire $500 cost in 2019 using the de minimis safe harbor. Since he is in the 24% bracket, he saves $120 in federal income tax and $77 in Social Security and Medicare tax. His total tax savings is $197.

Sam purchases a $5,000 computer system for his business during 2019. This is too much to deduct with the de minimis safe harbor. However, he can deduct the entire $5,000 in 2019 by using 100% bonus depreciation. Since he is in the 24% bracket, he saves $1,200 in federal income tax and $765 in Social Security and Medicare tax. His total tax savings is $1,965.

Example 1

Example 2

152019 Tax Guide for Property Managers

Many business people don’t buy expensive equipment or vehicles—they rent them instead. The rent you pay for the property used for your business is fully deductible as a business expense. If you lease a car or other vehicle for your business, you have the option of deducting your actual expenses (monthly lease payments, gas, repairs), or deducting mileage according to the standard mileage rate (58 cents per mile in 2019).

Whichever method you choose, you must stick with it for the entire term of your lease plus any extensions. You cannot switch.

Rent For Equipment & Tools

06

Sam spends $250/month to lease office furniture for his property management business, a $3,000 annual deduction. This saves him $720 in his 24% federal income tax bracket, and $459 in Social Security and Medicare taxes.

Example

162019 Tax Guide for Property Managers

The vast majority of property managers have pass-through businesses—that is, they are sole proprietors, partners in partnerships, limited liability company (LLC) owners, or S corporation shareholders. The net income from the property management business is passed-through the business and taxed on the manager’s individual tax return at his or her individual tax rates. Starting in 2018, the TCJA established a brand new deduction for pass-through business owners, including property managers (new IRC Sec. 199A).

You can qualify to deduct from your income taxes up to 20% of your net business income, which is in addition to all your other business deductions.

If this deduction applies, you are effectively taxed on only 80% of business income. This is a personal deduction you can take on your return whether or not you itemize. This deduction is scheduled to end on Jan. 1, 2026 and is not available to employees.

Pass-through Tax Deduction

07

The pass-through deduction works as follows:

2019 Income Below $321,400 ($160,700 for Singles): You qualify for an income tax deduction equal to 20% of your net property management business income if your total taxable income for 2019 from all sources after deductions is below $321,400 if married filing jointly, or $160,700 if single. However, the deduction can never exceed 20% of your taxable income (income minus deductions).

2019 Income Above $421,400 ($210,700 for Singles): If your 2019 annual taxable income is over $421,400 if married filing jointly, or $210,700 if single, you are still entitled to a pass-through deduction of up to 20% of net business income. However, the deduction cannot exceed: • 50% of your applicable share of the W-2 employee wages paid by your business, or; • 25% of your share of the W-2 wages paid by the business, plus 2.5% of the original purchase price of the long-term property used in the production of income—for example, the real property or equipment used in the business.

172019 Tax Guide for Property Managers

Tom is single and operates his property management business as a sole proprietorship. His business earns $100,000 in net income during 2019. He also earned $32,200 in investment income and took the $12,200 standard deduction. His total taxable income for the year is $120,000 (($100,000 + $32,200) – $12,200 = $120,000). His pass-through deduction is 20% x $100,000 = $20,000. He may deduct $20,000 from his income taxes.

Example

If you have no employees, your deduction is limited to 2.5% of the cost of your depreciable property. The 2.5% deduction can be taken during the entire depreciation period for the property. However, it can be no shorter than 10 years. • Income $321,400 to $421,400 ($160,700 to $210,700 for Singles): If your 2019 taxable income is $321,4000 to $421,400 (married) or $160,700 to $210,700 (single), the W2 wages/property limitation is phased in—that is, only part of your deduction is subject to the limit and the rest is based on 20% of your net business income.

Service Businesses: The pass-through deduction is phased out for people whose business involves providing various types of services including accounting, consulting, financial services, brokerage services, and investing and investment management. Such individuals are entitled to a partial deduction if their 2019 taxable income is $160,700 to $210,700 (single) or $321,400 to $421,400 (married). The deduction is lost if taxable income exceeds these limits. However, IRS regulations provide that property managers are not subject to this phase-out. Thus, you can qualify for the full pass-through deduction now no matter how high your income!

Employees May Not Claim Pass-Through Deduction: The pass-through deduction may not be claimed by employees. Some employees may be tempted to have their employers reclassify them as independent contractors because independent contractors who are sole proprietors can qualify for the pass-through deduction. However, IRS regulations make it clear that employees cannot get the deduction simply by having their employers reclassify them as independent contractors. If a worker is reclassified as an employee but continues to perform the same work directly or indirectly for the hiring firm, the IRS will presume that worker doesn’t qualify for the pass-through deduction for the next three years. This presumption can be overcome only by convincing the IRS that the worker really qualifies as an independent contractor.

182019 Tax Guide for Property Managers

NEW FOR 2019

Hal and Wanda are married and co-own their property management business through an LLC. Their taxable income this year is $500,000, including $400,000 in income they earned from the management business. They had two employees during the year to whom they paid $150,000 in W2 wages. They own the building in which their business is housed. They bought it four years ago for $600,000 and the land is worth $100,000, so its unadjusted acquisition basis is $500,000. Since their taxable income was over $421,400, their pass-through deduction is limited to the greater of (1) 50% of the W2 wages they paid their employees, or (2) 25% of W2 wages plus 2.5% of their building’s $500,000 basis. (1) is $75,000 (50% x $150,000 = $75,000); (2) is $50,000 (2.5% x $500,000) + (25% x $150,000) = $50,000. (1) is greater so their pass-through deduction is $75,000.

Example

192019 Tax Guide for Property Managers

Laura pays a CPA $1,000 to prepare her 2019 tax return, and $1,000 to an attorney to help her draft a standard client agreement. Her total 2019 deduction for legal and professional services is $2,000. Since she’s in the 24% federal income tax bracket, she saves $480 in federal income tax, and an additional $306 in Social Security and Medicare taxes.

Example

You can deduct fees paid to attorneys, accountants, consultants, and other professionals for any work they perform that’s related to your business.

Legal & Professional Services

08

202019 Tax Guide for Property Managers

Insurance you buy just for your business is deductible—for example, business liability insurance or insurance for business property. If you have a home office, you may deduct a portion of your homeowners insurance. Self-employed people are also allowed to deduct 100% of their health insurance premiums from their income taxes.

Bill pays $2,000 per year for professional liability insurance for his property management business and an additional $500 for insurance for his business property. He also uses a home office that takes up 10% of his home. This entitles him to deduct 10% of his homeowner’s insurance premiums (an additional $80). His total $2,580 insurance expense is currently deductible in 2019. Since he is in the 24% federal tax bracket, this saves him $619 in federal income tax, and an additional $395 in Social Security and Medicare tax.

Example

Insurance

09

212019 Tax Guide for Property Managers

If you hire one or more employees, your payroll and other costs (like health insurance and related benefits) are fully deductible.

When you hire an independent contractor—a person who is not your employee—to perform services for your business, the cost is deductible, too. For example, you may deduct the cost of hiring a bookkeeper to do your books or a custodian to clean your offices.

Employees & Independent Contractors

10

The Acme Property Management Company, LLC has two employees. Their total 2019 compensation is $90,000—including salary plus benefits, and health insurance. Acme also pays the employer share of the employees’ Social Security and Medicare taxes, for an additional $10,000 expense. The entire $100,000 amount is deductible. Assuming Acme’s three owners are each in the 24% federal tax bracket, altogether they save $24,000 in federal income tax. They can also save as much as $15,300 in Social Security and Medicare taxes—assuming their taxable income remains below the $132,900 Social Security tax ceiling for 2019.

Example

A tax credit lets you directly reduce the amount of taxes you pay by the amount of your credit. So if you have a $1,000 tax credit, you pay $1,000 less in taxes. Thus, a tax credit is much better than a tax deduction, which only reduces your taxable income.

If you’re in the 28% income tax bracket, a $1,000 tax deduction saves you only $280 in federal income taxes. A person in the 28% tax bracket would need $3,571 in tax deductions to save $1,000 in income taxes.

Tax Credits for Individuals There are several tax credits available to all individual taxpayers, no matter their income level. These include:

Hybrid car credit: You could qualify for a tax credit if you purchased a hybrid car in 2019. The size of the credit is determined with a complex formula based on the capacity of the battery used to fuel the vehicle, so different model hybrids qualify for different credit amounts. The maximum credit is $7,500.

To complicate matters, these credits are phased out once 200,000 of each model are produced by the manufacturer, counted from January 1, 2010. You can check to see which hybrid vehicles qualify for the credit, and how much, at https://www.fueleconomy.gov/feg.

Electric car credit: You could qualify for a tax credit if you purchased a hybrid car in 2019. The size of the credit is determined with a complex formula based on the capacity of the battery used to fuel the vehicle, so different model hybrids qualify for different credit amounts. The maximum credit is $7,500.

To complicate matters, these credits are phased out once 200,000 of each model are produced by the manufacturer, counted from January 1, 2010. You can check to see which hybrid vehicles qualify for the credit, and how much, at https://www.fueleconomy.gov/feg.

Tax Credits

222019 Tax Guide for Property Managers

30% Energy Tax Credit: You may claim a credit of up to 30 percent of the cost of certain energy installation projects for your main or second home (not including rental homes). This includes 30 percent of the cost (with no limit) of installing: • Solar energy systems, including solar water heaters and solar panels • Geothermal heat pumps • Small residential wind turbines

You can also get a 30 percent credit for installing a residential fuel cell in your main home. This credit is limited to $500 per .5 kilowatt of power capacity. For 2020, the credit will be reduced to 26%.

Such installations must meet strict Energy Star requirements in order to be eligible for the tax credit.

Tax Credits For Small Businesses A number of tax credits are also available for small business owners. To get one, your business must do something that Congress likes or views as socially beneficial. Broadly speaking, the main categories include:

Helping the disadvantaged or disabled: You may take a Work Opportunity Credit if you hire a veteran, welfare and food stamp recipient, low-income ex-felon, disabled person, or high-risk young person; a credit is also available if you pay to help make your office accessible to the disabled. The amount of the credit varies depending on who you hire—it’s $2,400 the first year for most types of employees, but goes up to $9,600 if you hire a veteran with a service-connected disability.

Improving the environment: You can get a credit of up to 30% of the cost of buying and installing solar power for your place of business.

Helping your employees: Get a credit of up to 25% of the cost of child care facilities and services you provide for employees up to $150,000 per year. You can also get a credit to help defray the cost of providing your employees with paid family and medical leave. This tax credit ranges from 12.5% to 25% of wages paid to employees on family or medical leave for up to 12 weeks. For more details on these and other business tax credits, see the IRS Business Tax Credits web page.

You may qualify for more than one business tax credit at the same time. There is an annual limit on total business credits, based on your tax liability. If you exceed the limit, you can use them in future years or apply them to previous years’ taxes—again, within limits.

232019 Tax Guide for Property Managers

Small Business Health Care Tax Credit: If you have employees and provide them with health insurance coverage, one significant tax credit you may qualify for is the Small Business Health Care Tax Credit. For 2019, this credit is equal to 50% of the premiums small employers pay for their employees’ health insurance.

For example, if you paid $20,000 for employee health insurance in 2019, you’d be entitled to a $10,000 tax credit. If you don’t owe tax for the 2019 tax year, you can carry the credit back or forward to other tax years.

Also, you can take the credit and still claim a business expense deduction for the health care premiums you paid in excess of the credit. The tax credit is available to eligible employers for two consecutive tax years.

To qualify for the credit, you must: • Have had no more than 25 full-time equivalent employees (not including relatives) • Paid your employees average annual full-time wages of more than $26,000 and no more than $54,000 • Paid at least 50% of the annual premiums for your employees’ health insurance • Bought your employees’ health insurance through a Small Business Health Options Program (SHOP) Marketplace (these are health insurance exchanges specifically designed for businesses with 50 or fewer full-time employees; see www.healthcare.gov/small-businesses/employers)

If you have questions about whether you’re eligible for the Small Business Health Care Tax Credit refer to the IRS’s Small Business Health Care Tax Credit and the SHOP Marketplace page.

If you qualified for the credit during past years, but failed to apply for it, you may be able to amend your tax return for the year or years involved and claim the credit. However, an amended tax return must be filed no later than three years after the original return for the year was filed.

How you file your tax return and what forms to use depends on how you have legally organized your property management business. You can access all the IRS forms referenced below, along with instructions, at the IRS Forms and Instructions - Filing and Paying Business Taxes web page.

The five ways you can legally organize your property management business include: • Sole proprietor • LLC owner • Partnership • S corporation • Regular C corporation Please skip forward to the section that describes how your business is organized.

242019 Tax Guide for Property Managers

Sole Proprietor You’re a sole proprietor if you are the only person who owns your property management business and you haven’t formed a limited liability company (LLC) or corporation. When you’re a sole proprietor, you and your business are one and the same for tax purposes. You report the income you earn or losses you incur on your own personal tax return (IRS Form 1040).

If you earn a profit, the money is added to any other income you have—for example, interest income or your spouse’s income if you’re married and file a joint tax return—and that total is taxed.

To show whether you have a profit or loss from your sole proprietorship business, you must file IRS Schedule C, Profit or Loss from Business, with your tax return. On this form, you list all your business income and deductible expenses. If you have more than one business, you must file a separate Schedule C for each one.

You must also file IRS Form SE, Self-Employment Tax, to report and pay your Social Security Filing Your Tax Return and Medicare taxes for the year. You only need to file one Form SE, no matter how many unincorporated businesses you own. Add the SE tax to your income taxes on your personal income tax return (Form 1040) to determine your total tax due for the year.

LLC Owner If you have formed a limited liability company (LLC) to own and operate your business, your tax filing requirements depend on how many owners (or members) there are.

If your LLC has only one owner, it is a “disregarded entity” for IRS purposes. This means that for tax purposes, the LLC doesn’t exist. Thus, you, the sole LLC owner, are treated exactly the same as a sole proprietor.

If your LLC has two or more owners, it is ordinarily taxed the same as a partnership. However, LLC owners have the option of having their LLC taxed as a regular C corporation or S corporation.

Filing Your Tax Return

252019 Tax Guide for Property Managers

Partnership Your property management business is a partnership if it is owned by two or more people and you haven’t formed an LLC or corporation. You don’t have to have a written agreement to form a partnership, although it’s a good idea. Under partnership tax treatment, the business entity is a pass-through entity for tax purposes, which means it ordinarily pays no taxes itself.

Instead, the profits, losses, deductions, and tax credits of the business are passed through the business to the owner’s individual tax returns. If the business has a profit, the owners pay income tax on their ownership share on their individual returns at their individual income tax rates. If the business incurs a loss, it is likewise shared among the owners who may deduct it from other income on their individual returns, subject to certain limitations.

Unlike a sole proprietorship, a partnership is considered to be separate from the partners for the purposes of computing income and deductions. The partnership files its own tax return on IRS Form 1065, U.S. Return of Partnership Income. Form 1065 is not used to pay taxes; rather, it is an information return that tells the IRS about the partnership’s income, deductions, profits, losses, and tax credits for the year.

Form 1065 also includes a separate part called Schedule K-1 in which the partnership lists each partner’s share of the items listed on Form 1065. A separate Schedule K-1 must be provided to each partner and is filed with the individual partner’s personal income tax return for the year.

Each partner reports on his or her individual tax return (Form 1040) the partner’s share of the business’s net profit or loss as shown on Schedule K-1. Ordinary business income or loss is reported on IRS Schedule E, Supplemental Income or Loss.

However, certain items must be reported on other schedules. For example, capital gains and losses must be reported on Schedule D and charitable contributions on Schedule A. The total Schedule E income or loss is entered on Form 1040. The partners must also pay self-employment tax (Social Security and Medicare) based on their share of the partnership’s annual profits. This is reported on IRS Schedule SE.

Corporation If you’ve formed a corporation to own and operate your property management business, it will have its own tax filings to make. In addition, you’ll ordinarily work as an employee of your corporation.

The salary and other employee compensation you receive must be reported on your individual tax return (Form 1040). You’ll also have to report and pay tax on any dividends or other distributions you receive from your corporation in your capacity as a shareholder.

Your corporate tax filings depend on whether you’ve formed an S corporation or regular C corporation. They’re taxed very differently.

262019 Tax Guide for Property Managers

S Corporation: The S corporation, which is very popular for small businesses, is taxed much like a partnership. Like a partnership, an S corporation is a pass-through entity: income and losses pass through the corporation to the owners’ personal tax returns. S corporations also report their income and deductions much like partnerships.

An S corporation files an information return (Form 1120S) reporting the corporation’s income, deductions, profits, losses, and tax credits for the year. Like partners, shareholders must be provided a Schedule K-1 listing their shares of the items on the corporation’s Form 1120S. The shareholders file Schedule E with their personal tax returns (Form 1040) showing their share of corporation income or losses.

No business entity automatically starts out with the S corporation form of taxation. Instead, you must obtain it by filing an election with the IRS. This simply involves filing IRS Form 2253 with the IRS.

Regular C Corporation: A regular C corporation is the only business form that’s not a pass-through entity. Instead, a C corporation is taxed separately from its owners. C corporations must pay income taxes on their net income and file their own tax returns with the IRS, using Form 1120 or Form 1120-A. As a result of the TCJA, starting in 2018 all C corporations are taxed at a flat rate of 21% on their profits. This is lower than all but the bottom two individual tax rates.

When you form a C corporation, you have to take charge of two separate taxpayers: your corporation and yourself. Your C corporation must pay tax on all of its income. You pay personal income tax on C corporation income only when it is distributed to you in the form of salary, bonuses, or dividends.

One of a property manager’s most important tax responsibilities is to file all required IRS Forms 1099-MISC with the IRS and state tax agencies. Failure to do so can result in a penalty of $250 for each unfiled 1099, with the penalty increased to $500 if the failure to file is viewed as intentional by the IRS.

272019 Tax Guide for Property Managers

What is Form 1099-MISC? IRS Form 1099-MISC (commonly referred to simply as a 1099) is an information return that must be filed to report various types of payments a taxpayer makes to third parties. The IRS and state tax agencies use the information on the form to help ensure that the people receiving such payments properly report them as

income on their tax returns.

What payments must be reported on Form 1099? There are two main types of payments that property managers need to be concerned about:

Rental income paid to property owners: A rental property manager must file a Form 1099-MISC whenever he or she, acting as a rental property owner’s agent, receives rental payments during the year totaling $600 or more. The gross amount of rent received must be reported—that is, don’t deduct the amount of your commissions or other fees or expenses. (IRS Reg. 1.6041-1.)

Payments for services performed by independent contractors: You may also need to file a 1099 when you pay an unincorporated independent contractor $600 or more in a year for work done on a rental property owner’s behalf or in the course of your own business. An independent contractor is a sole proprietor or member of a partnership or LLC.

However, there is an important exception to the 1099-MISC filing requirements for payments made electronically or by credit card, as described below. In addition, some business-related payments don’t have to be reported on Form 1099-MISC, although they may be taxable to the recipient. These include payments: • For non-business related services • To corporations (except for incorporated lawyers) • For merchandise, telephone, freight, storage, and similar items

Filing IRS Form 1099

282019 Tax Guide for Property Managers

Electronic and Credit Card Payments If a client or independent contractor is paid by credit card, debit card, or by using a third party settlement organization (TPSO) like PayPal or Payable, you need not file a 1099-MISC with the IRS. This is so even if you pay the client or contractor more than $600 during the year. The electronic payments may have to be reported to the IRS by the payment processor or on IRS Form 1099- K, Payment Card and Third Party Network Transactions.

Whether this is so depends on how the client or contractor is paid and how much.

Filing deadlines for Form 1099 There are multiple 1099-MISC filing deadlines you must comply with. If you file late, you’ll have to pay a penalty to the IRS. In practice, most companies file all their 1099-MISC forms on January 31, even they are allowed to file some of them later.

All 1099-MISC forms reporting payments to independent contractors must be filed with the IRS by January 31, 2020. This is so whether they are filed electronically or on paper. The recipient of the payments reported on the 1099-MISC—the independent contractor must also be provided a copy no later than January 31, 2019. Most states use the same filing deadline, although some may have a later deadline.

All 1099-MISC forms reporting payments of rent must be filed with the IRS by February 28, 2020, or March 31, 2020 if you file electronically. The recipient of the payments—the rental property owner—must be provided a copy no later than January 31, 2020. The filing deadline for most states is February 28, 2020, but some states have earlier filing deadlines. Check with your state tax department.

You can obtain a 30-day extension of the time to file a 1099-MISC form by filing IRS Form 8809, Application for Extension of Time to File Information Returns. If you need more time to file a 1099-MISC to report payments to independent contractors, Form 8809 must be filed by January 31, 2020. Otherwise, the form must be filed with the IRS by February 28, 2020(or March 31 if filing electronically).

The extension is not granted automatically: you must explain why you need it. The IRS will send you a letter of explanation approving or denying your request. See the instructions for Form 8809 for more information.

292019 Tax Guide for Property Managers

1099 E-Filing Today, a majority of businesses file their 1099s with the IRS electronically instead of on paper. If you are required to file 250 or more information returns, you must file electronically with the IRS. If you file this many 1099s, your state tax agency may require electronic filing, too. Check with your state tax department for details.

However, you must provide a paper copy of the 1099 to the recipient—rental property owner or vendor—unless he or she agrees to accept an electronic 1099.

If you file electronically, the deadline to provide your 1099s to the IRS is extended to March 31, 2020 to report payments to rental property owners. Also, you don’t have to file IRS Form 1096.

Unfortunately, you can’t simply go on the IRS website, fill out a 1099 online, and file it electronically. You must use software that meets IRS requirements.

Alternatively, you can use accounting software such as QuickBooks or Xero, or online 1099 filing services such as tax1099.com, and many others. You can also electronically file 1099s using tax filing software such as TurboTax.

You can also electronically file 1099s directly with the IRS by using its FIRE Production System. To do so, you must get permission from the IRS by filing IRS Form 4419, Application for Filing Information Returns Magnetically/Electronically.

For details, visit the IRS Filing Information Returns Electronically (FIRE) web page.

Filing paper 1099 Forms If you file fewer than 250 1099-MISC forms during the year, you have the option of filing them on paper. (The IRS prefers that you file electronically, though.)

To file on paper, you must obtain original 1099-MISC forms from the IRS for filing. You can’t photocopy this form because it contains several pressure-sensitive copies. Each 1099-MISC form contains three parts and can be used for three different payees.

302019 Tax Guide for Property Managers

You can efile your 1099 forms through the Buildium platform– visit buildium.com/features/1099-efiling/ for details.

All your 1099-MISC forms must be submitted together along with one copy of Form 1096, which is a transmittal form, the IRS equivalent of a cover letter. You must obtain an original Form 1096 from the IRS; you cannot submit a photocopy.

You can order these forms through the IRS website at www.irs.gov/Businesses/Online-Ordering- for-Information-Returns-and-Employer-Returns, or by calling the IRS at 800-TAX-FORM.

You can also obtain usable 1099-MISC forms from stationery stores and office supply companies. The software package TurboTax for Business can also generate 1099-MISC forms you can use.

Filling out Form 1099-MISC Filling out Form 1099-MISC is easy. Complete one 1099-MISC for each payee, whether a rental property owner or an independent contractor vendor. Be sure to fill in the right boxes or the IRS will consider Form 1099-MISC

invalid.

Follow this step-by-step approach:

1. List your name and address in the first box titled PAYER’S name.

2. Enter your taxpayer identification number in the box titled PAYER’S federal identification number.

3. The person you have paid (landlord or vendor) is called the “RECIPIENT” on this form, meaning the person who received the money. Provide the recipient’s taxpayer identification number, name, and address in the boxes indicated. For sole proprietors, list the individual’s name first, followed by the business name, but this is not required. You may not enter a business name alone for a sole proprietor.

4. Report rental payments to a rental property owner in Box 1, entitled Rents.

5. Report payments to independent contractor vendors in Box 7, entitled Nonemployee Compensation. If you’ve done backup withholding for a vendor who has not provided you with a taxpayer ID number, enter the amount withheld in Box 4.

312019 Tax Guide for Property Managers

Form 1099-MISC contains five copies. These must be filed as follows: • Copy B and Copy 2 are for the recipient of the payments reported on the form — the rental property owner or independent contractor. • Copy A must be filed with the IRS. • Copy 1 is for your state taxing authority if your state has a state income tax and • Copy C is for you to retain for your files.

When you file the 1099s with the IRS, file them all together with IRS Form 1096, the simple transmittal form (see below). Add up all the payments reported on all the 1099-MISC forms and list the total in the box indicated on Form 1096. File the forms with the IRS Service Center listed on the reverse of Form 1096.

322019 Tax Guide for Property Managers

Do Not Staple 6969

Form 1096Department of the Treasury Internal Revenue Service

Annual Summary and Transmittal of U.S. Information Returns

OMB No. 1545-0108

2019FILER'S name

Street address (including room or suite number)

City or town, state or province, country, and ZIP or foreign postal code

Name of person to contact Telephone number

Email address Fax number

For Official Use Only

1 Employer identification number 2 Social security number 3 Total number of forms 4 Federal income tax withheld

$

5 Total amount reported with this Form 1096

$6 Enter an “X” in only one box below to indicate the type of form being filed.

W-2G 32

1097-BTC 50

1098 81

1098-C 78

1098-E 84

1098-F 03

1098-Q 74

1098-T 83

1099-A 80

1099-B 79

1099-C 85

1099-CAP 73

1099-DIV 91

1099-G 86

1099-INT 92

1099-K 10

1099-LS 16

1099-LTC 93

1099-MISC 95

1099-OID 96

1099-PATR

97

1099-Q 31

1099-QA 1A

1099-R 98

1099-S 75

1099-SA 94

1099-SB 43

3921 25

3922 26

5498 28

5498-ESA 72

5498-QA 2A

5498-SA 27

7 Form 1099-MISC with NEC in box 7, check . . . . . ▶

Return this entire page to the Internal Revenue Service. Photocopies are not acceptable.

Under penalties of perjury, I declare that I have examined this return and accompanying documents and, to the best of my knowledge and belief, they are true, correct, and complete.

Signature ▶ Title ▶ Date ▶

InstructionsFuture developments. For the latest information about developments related to Form 1096, such as legislation enacted after it was published, go to www.irs.gov/Form1096.

Reminder. The only acceptable method of electronically filing information returns listed on this form in box 6 with the IRS is through the FIRE System. See Pub. 1220.

Purpose of form. Use this form to transmit paper Forms 1097, 1098, 1099, 3921, 3922, 5498, and W-2G to the IRS.

Caution: If you are required to file 250 or more information returns of any one type, you must file electronically. If you are required to file electronically but fail to do so, and you do not have an approved waiver, you may be subject to a penalty. For more information, see part F in the 2019 General Instructions for Certain Information Returns.

Forms 1099-QA and 5498-QA can be filed on paper only, regardless of the number of returns.

Who must file. Any person or entity who files any of the forms shown in line 6 above must file Form 1096 to transmit those forms to the IRS.

Enter the filer’s name, address (including room, suite, or other unit number), and taxpayer identification number (TIN) in the spaces provided on the form. The name, address, and TIN of the filer on this form must be the same as those you enter in the upper left area of Forms 1097, 1098, 1099, 3921, 3922, 5498, or W-2G.

When to file. File Form 1096 as follows.

• With Forms 1097, 1098, 1099, 3921, 3922, or W-2G, file by February 28, 2020.

Caution: We recommend you file Form 1099-MISC, as a stand-alone shipment, by January 31, 2020, if you are reporting nonemployee compensation (NEC) in box 7. Also, check box 7 above.

• With Forms 5498, file by June 1, 2020.

Where To FileSend all information returns filed on paper with Form 1096 to the following.

If your principal business, office or agency, or legal residence in

the case of an individual, is located in

Use the following address

▲ ▲

Alabama, Arizona, Arkansas, Delaware, Florida, Georgia, Kentucky, Maine, Massachusetts, Mississippi, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Texas, Vermont, Virginia

Department of the Treasury Internal Revenue Service Center

Austin, TX 73301

For more information and the Privacy Act and Paperwork Reduction Act Notice, see the 2019 General Instructions for Certain Information Returns.

Cat. No. 14400O Form 1096 (2019)

332019 Tax Guide for Property Managers

Acme Property Management, LLC manages a rental home owned by Ed. Linda, the sole proprietor of a painting business, charged $1,750 to paint the home. Acme paid Linda, and must report the $1,750 payment on Form 1099-MISC.

Acme pays $2,500 during 2019 to Laura, a sole proprietor bookkeeper, for bookkeeping services for Acme. Acme must file a 1099 reporting the payment.

Example 1

Example 2

352019 Tax Guide for Property Managers

2019 Tax Calendar

Date Action

January 15, 2020 Last estimated tax payment for 2019 by individual taxpayers is due. (However, you do not have to make this payment if you file your 2019 return (Form 1040) and pay any tax due by January 31, 2019.)

January 31, 2020 All Forms 1099-MISC must be filed with IRS and provided to independent contractor or rental property owner recipients.

February 28, 2020 Paper 1099-MISC forms reporting rental payments must be filed with IRS

March 16, 2020 Partnership tax returns due; S Corporation tax return due (if calendar year used)

April 1, 2020 Electronic 1099-MISC forms reporting rental payments must be filed with IRS

April 15, 2020 Individual income tax return due (unless extension obtained); C Corporations tax return due (if calendar year used); First estimated tax payment for 2020 due

April 20, 2020 Individual income tax returns due in Hawaii.

May 1, 2020 Individual income tax returns due in Delaware, Iowa and Virginia.

May 15, 2020 Individual income tax returns due in Louisiana.

June 15, 2020 Second IRS estimated tax payment for 2020 is due.

September 15, 2020 Third IRS estimated tax payment for 2020 is due.

October 15, 2020 This is the due date to file an individual 2019 tax return (Form 1040) if you obtained an automatic six-month extension of time to file.

December 15, 2020 Fourth IRS 2020 estimated tax payment by corporations is due.

Important Dates

Most people tend to focus on federal income and payroll taxes, but every state has its own taxes that individuals and businesses must pay. Depending on the state where you do business, such taxes can be substantial.

Each state has its own tax forms and procedures. Contact your state tax department to learn about your state’s requirements and get the necessary forms. You can find your state’s tax agency at www.irs.gov/businesses/small-businesses-self-employed/state-government-websites

State Income Taxes All states except Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming impose their own income taxes on businesses and the self-employed. New Hampshire and Tennessee impose income taxes on dividend and interest income only.

Most states charge a percentage of the income shown on your federal income return. Depending on the state in which you live, these percentages range from 3% to 12%. If your business is incorporated, your corporation will likely have to pay state income taxes and file its own state income tax return, too.

In most states, you pay your state income taxes during the year in the form of estimated taxes. These are usually paid at the same time you pay your federal estimated taxes.

You’ll also have to file an annual state income tax return with your state tax department. In all but five states—Delaware, Hawaii, Iowa, Louisiana, and Virginia—the return must be filed by April 15, the same deadline as

your federal tax return.

State Employment Taxes If you live in a state with income taxes and you have employees, you’ll likely have to withhold state income taxes from their paychecks and send the money to your state tax department. You’ll also provide your employees with unemployment compensation insurance by paying taxes to your state unemployment compensation agency.

State Taxes

362019 Tax Guide for Property Managers

Other State Taxes Other State Taxes Various states impose a hodgepodge of other taxes on businesses, too numerous and

diverse to explain here. For example:

• Hawaii imposes a general excise tax on businesses based on their gross receipts.

• Washington State has a business and occupation tax on most businesses with a gross annual

income over $12,000.

Contact your state tax department for information on these and other similar taxes your state might impose.

Special Tax Rules For Landlords Some states also have special tax rules that apply only to rental property owners. For example:

• California requires residential rental property owners who live out-of-state to withhold 7% of their

rental payments over $1,500 (however, this requirement does not apply to corporations, LLCs or

limited partnerships qualified to do business in California). For details, see the California Franchise

Tax Board Nonresident Withholding page.

• Minnesota requires, by January 31, that all rental property owners, managers, or operators

provide a Certificate of Rent Paid to each person who rented from them during the year. Renters

use this certificate to obtain a state tax refund.

• Hawaii requires all landlords to pay a 4% general excise tax on their gross receipts (4.5% for

rent to a person for less than 180 consecutive days. For details, An Introduction to the Transient

Accommodations Tax

Again, contact your state tax department for information on these and other similar taxes your state might impose.

372019 Tax Guide for Property Managers

Information from the IRS The IRS has made a huge effort to inform the public about the tax law. It has created hundreds of informative

publications, an excellent website, and a telephone answering service.

IRS Website: The IRS has one of the most useful Internet websites of any federal government agency. Among

other things, almost every IRS form and informational publication can be downloaded from the site. The url is

www.irs.gov.

The IRS website has a special Self-Employed Individuals Tax Center that you should check out.

IRS Publications: The IRS also publishes more than 350 free booklets explaining the Tax Code, many of which

are clearly written and useful. These IRS publications range from several pages to several hundred pages in

length. Reading IRS publications is a useful way to obtain information on IRS procedures and to get the agency’s

view of the tax law.

Keep in mind, though, that these publications only present the IRS’s interpretation of the law, which may be very

one-sided and even contrary to court rulings. That’s why you shouldn’t rely exclusively on IRS publications for

information.

The following IRS publications cover basic tax information that every business owner should know about:

• Publication 334, Tax Guide for Small Business

• Publication 505, Tax Withholding and Estimated Tax

• Publication 15 (Circular E), Employer’s Tax Guide

Download any of these guides from the IRS’s website at www.irs.gov.

Resources

382019 Tax Guide for Property Managers

Other Online Tax Resources In addition to the IRS website, there are hundreds of privately created websites on the Internet that provide tax

information and advice. Some of this information is good, and some is awful. A comprehensive collection of web

links about all aspects of taxation can be found at www.taxsites.com.

Books About Taxes There are many books that try to make the tax law comprehensible to the average person.

The best known are the paperback tax preparation books published every year. These books emphasize

individual taxes but also have useful information for small businesses.

Two of the best are: • The Ernst & Young Tax Guide (Ernst & Young), and

• J.K. Lasser’s Your Income Tax (John Wiley & Sons)

Nolo.com also publishes several books that deal with tax issues:

• Deduct It! Lower Your Small Business Taxes, by Stephen Fishman (Nolo), emphasizes deductions

for small businesses.

• Stand Up to the IRS, by Frederick W. Daily (Nolo), explains how to handle an IRS audit.

• Working with Independent Contractors, by Stephen Fishman (Nolo), shows small businesses how to

hire independent contractors without running afoul of the IRS or other government agencies.

• Working for Yourself, by Stephen Fishman (Nolo), covers the whole gamut of legal issues facing

the one-person business.

• Every Landlord’s Tax Deduction Guide, by Stephen Fishman (Nolo), provides detailed guidance on

tax deductions for small residential landlords.

392019 Tax Guide for Property Managers

About the Author Stephen Fishman has dedicated his career as an attorney and author

to writing useful, authoritative, and recognized guides on taxes

and business law for small businesses, entrepreneurs, independent

contractors, and freelancers. He is the author of 20 books and hundreds

of articles, and has been quoted in The New York Times, Wall Street Journal,

Chicago Tribune, and many other publications.

Among his books are Every Landlord’s Tax Deduction Guide, Deduct It! Lower Your Small Business Taxes, and

Working for Yourself: Law and Taxes for Independent Contractors, Freelancers & Consultants. All are published

by nolo.com. His website can be found at fishmanlawandtaxfiles.com.

402019 Tax Guide for Property Managers

About Buildium Buildium is the only property management solution that helps real estate professionals win new business

from property owners and community associations seeking services. Backed by expert advice and relentless

support, Buildium enables you to outperform across all facets of your business with intuitive software that

balances power, simplicity, and ease of use. Buildium services customers in more than 50 countries, totaling

over 1.9 million residential units under management. In 2015, Buildium acquired All Property Management, a

leading online marketing service for property managers, making Buildium the only company to give property

managers a way to acquire new customers and increase revenue. For more information, visit buildium.com, and

connect with us on Twitter, LinkedIn, and Facebook.

© 2019 Buildium LLC

Attract and keep tenants with the best services possible. Try Buildium FREE. Give us a call today at 877-396-7876 or visit our website to schedule a demo.

SIGN UP

REQUEST A DEMO www.buildium.com/contact-sales

READ OUR BLOG www.buildium.com/blog

CONTACT US 877.396.7876 or [email protected]

SIGN UP FOR A FREE TRIAL www.buildium.com/free-trial/