Embed Size (px)

Citation preview

2018 Site Visit Presentation

February, 2018

Michael Carvill, Managing Director

Tony McCluskey, Finance Director

Ben Baxter, Chief Operating Officer

Jeremy Dibb, Corporate Development & Investor Relations

Disclaimer

2

This Presentation (the “Presentation”) hasbeen prepared and issued by KenmareResources plc (the “Company” or“Kenmare”). While this Presentation hasbeen prepared in good faith, the Companyand its respective officers, employees,agents and representatives expresslydisclaim any and all liability for the contentsof, or omissions from, this Presentation,and for any other written or oralcommunication transmitted or madeavailable to the recipient or any of itsofficers, employees, agents orrepresentatives.

No representations or warranties are or willbe expressed or are to be implied on thepart of the Company, or any of itsrespective officers, employees, agents orrepresentatives in or from this Presentationor any other written or oral communicationfrom the Company, or any of its respectiveofficers, employees, agents orrepresentatives concerning the Companyor any other factors relevant to anytransaction involving the Company or as tothe accuracy, completeness or fairness ofthis Presentation, the information or

opinions on which it is based, or any otherwritten or oral information made availablein connection with the Company.

This Presentation does not constitute orform part of, and should not be construedas, an offer, invitation or inducement topurchase or subscribe for any securities ofthe Company nor shall it or any part of itform the basis of, or be relied upon inconnection with, any contract or investmentdecision relating to such securities, nordoes it constitute a recommendationregarding the securities of the Company.

This Presentation is as of the date hereof.This Presentation includes certainstatements, estimates and projectionsprovided by the Company with respect tothe anticipated future performance of theCompany or the industry in which itoperates. Such statements, estimates andprojections reflect various assumptions andsubjective judgments by the Company’smanagement concerning anticipatedresults, certain of which assumptions andjudgments may be significant in the contextof the statements, estimates andprojections made. These assumptions and

judgments may or may not prove to becorrect and there can be no assurance thatany projected results are attainable or willbe realised. In particular, certainstatements in this Presentation relating tofuture financials, results, plans andexpectations regarding the Company’sbusiness, growth and profitability, as wellas the general economic conditions towhich the Company is exposed, areforward looking by nature and may beaffected by a variety of factors. TheCompany is under no obligation to updateor keep current the information containedin this Presentation, to correct anyinaccuracies which may become apparent,or to publicly announce the result of anyrevision to the statements made herein andany opinions expressed in the Presentationor in any related materials are subject tochange without notice.

Presentation overview

3

2017 highlights & company strategy

Simplified mining & processing flowsheets

Sustainable operating practices

Production & cost review

Outlook and guidance

Mine development

2017 Highlights

4

Production Cash costs(H1 2017)

EBITDA(H1 2017)

Ilmenite pricesNet debt(31 Dec 2017)

Zircon prices

US$131/t↓14% YoY

Ilmenite ~1,000,000t

US$30m↑US$41m YoY

Up strongly+ improving

↓toUS$34m

H1 ’17↑61% YoY + H2 increases

2017 production & cost guidance met

Company Strategy

5

Structured and disciplined approach to capital management

ST Short Term MT Medium Term

Maintain robust balance sheet and generate free cash flow

Increase utilisation rates and revenue capture

Continue to drive down cash costs

Optimise mining capacity for market conditions

Deliver shareholder returns

Balance sheet optimisation

Deliver safe operations

Operations schematic

6

Simplified mining flowsheet

7

Dredge 1 Dredge 2

Supplemental Dry Mining

Wet Concentrator

Plant A

Mining Pond A

Ore

Ore

Mining Pond B

Dredge 3

Wet Concentrator

Plant B

Supplemental Dry Mining

Ore

Ore

Heavy Mineral Concentrate

WCP A HMC Stockpile

WCP B HMC Stockpile

Ore

HMC HMC

Simplified processing flowsheet

8

Wet High Intensity Magnetic Separation

Plant (WHIMS)

WCP A HMC Stockpile

WCP B HMC Stockpile

HMC

Non‐magnetic

concentrate

Magneticconcentrate

Ilmenite Plant A

Ilmenite Plant B

Ilmenite

Wet circuit

Drycircuit

Rutile cleanercircuit

Product Storage

Wet zircon circuit

HMC Stockpile Mineral Separation Plant

Rutile

Zircon

Dry zircon circuit

400

425

450

475

500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecOpe

n Area

Decremen

t (Ha

)

Open Area (Actual vs Plan) Actual Open Area (Ha)Planned Open Area (Ha)

Sustainable operating practices

9

Safety performance Retained NOSA 5 star status YTD 9 x LTI’s, LTIFR 0.39 Deterioration in late 2017; focus on behaviours to

rectify performanceEnvironmental performance No significant environmental incidents Successful external environmental audit IFC (2012) action items completed

Malaria Prevention improved 11% in 2017 28% (2,000 day) reduction in work days lost

Rehabilitation performance: Big drive in 2017 to increase rehabilitation 292Ha rehabilitated v 171Ha opened up

0.000.05

0.10

0.150.20

0.25

0.300.35

0.400.45

0

1

2

3

4

5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

LTIFR

Lost Tim

e Injurie

s

Total Injuries and rolling 12 month LTIFR

No of LTI's 12 month rolling LTIFR Actual LTIFR Budget

Production profile

10

Ilmenite Production (000t) Zircon Production (000t)

2017 guidance met Record levels of production (and shipments) for all products 2018 production impacted by WCP B upgrade and lower HMC & intermediate stockpiles Shipment volumes expected to be maintained, subject to market conditions

* 2018 production range based on guidance given on 11 January 2018.

0

200

400

600

800

1,000

1,20020

13

2014

2015

2016

2017

2018

*0

10

20

30

40

50

60

70

80

2013

2014

2015

2016

2017

2018

*

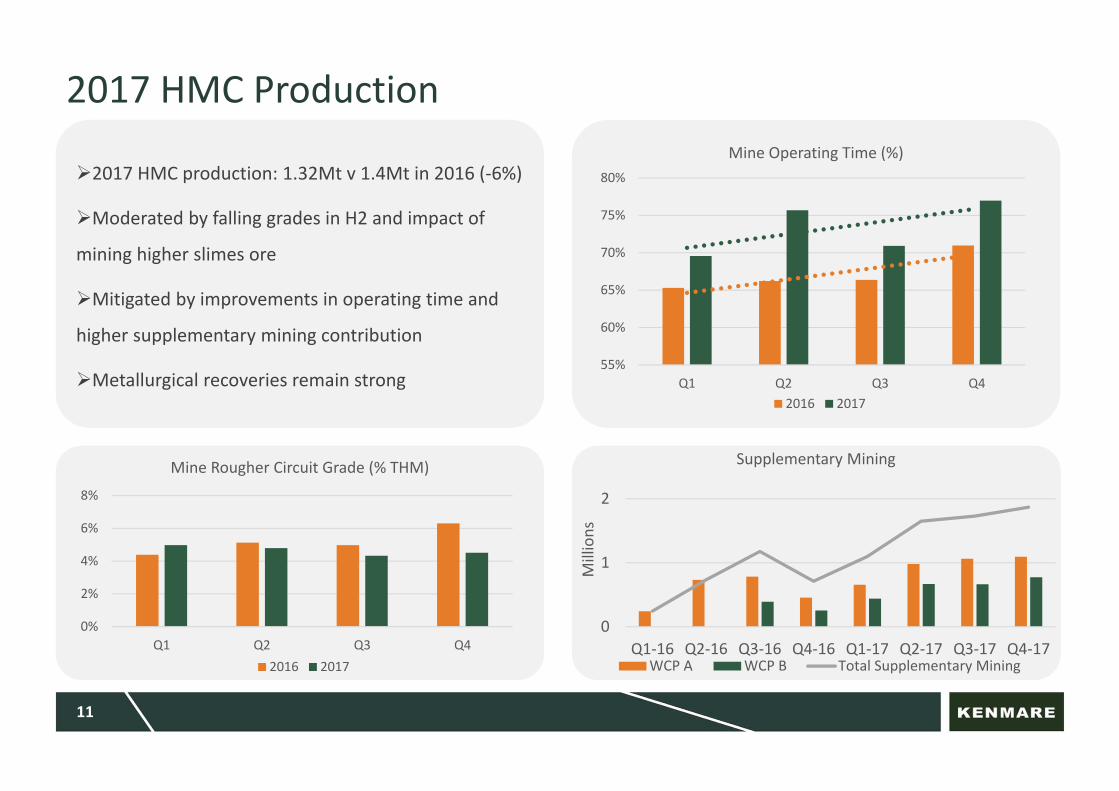

2017 HMC production: 1.32Mt v 1.4Mt in 2016 (‐6%)

Moderated by falling grades in H2 and impact of

mining higher slimes ore

Mitigated by improvements in operating time and

higher supplementary mining contribution

Metallurgical recoveries remain strong

2017 HMC Production

11

0%

2%

4%

6%

8%

Q1 Q2 Q3 Q4

Mine Rougher Circuit Grade (% THM)

2016 2017

55%

60%

65%

70%

75%

80%

Q1 Q2 Q3 Q4

Mine Operating Time (%)

2016 2017

0

1

2

Q1‐16 Q2‐16 Q3‐16 Q4‐16 Q1‐17 Q2‐17 Q3‐17 Q4‐17

Millions

Supplementary Mining

WCP A WCP B Total Supplementary Mining

2017 Production Ilmenite production 998kt (+11% on 2016) Record recoveries @ 91% Drawdown of HMC and intermediate inventories Consistent plant utilisation with improved

reliability

2018 Focus Consolidate higher levels of capacity Continue to improve quality

Ilmenite

12

0

100

200

300

Q1 Q2 Q3 Q4

Thou

sand

s

Quarterly Production

2016 2017

75%

80%

85%

90%

95%

100%

2016‐Q1

2016‐Q2

2016‐Q3

2016‐Q4

2017‐Q1

2017‐Q2

2017‐Q3

2017‐Q4

Ilmenite Recovery %

50%

60%

70%

80%

90%

100%

Q1 Q2 Q3 Q4

MSP Utilisation

2016 2017

2018 Focus Specific projects to maximise recoveries

Transition mineral from secondary to primary

zircon

Build capacity to consume intermediate zircon

stock

Implement new monazite concentrate product

2017 Production Zircon production 74.0kt (+8% on 2016) H2 impacted by lower HMC feed availability Non‐magnetic feed temporarily removed

Lower contamination & higher recoveries Phase 1 of improved process now

commissioned – time lag to process all stock Successfully moved material from secondary to

primary zircon (9% increase in Special grade)

Zircon

13

10

14

18

22

Q1 Q2 Q3 Q4

Thou

sand

s

Total Zircon Tonnes Produced

2016 2017

30%

40%

50%

60%

70%

80%

90%

Q1 Q2 Q3 Q4

Overall Zircon Recovery (Primary and Secondary)

2016 2017

2018 Focus

Continue to clean up product to make a pigment

grade rutile whilst maximising rutile revenue

2017 Production

Rutile production 9.1kt (+17% on 2016)

Improved recoveries in dry mill

Implemented revenue collection for zircon

concentrates (equivalent +33% TiO2 units)

Rutile

14

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1 Q2 Q3 Q4

Thou

sand

s

Rutile Production

2016 2017

20%

40%

60%2016‐Q

1

2016‐Q2

2016‐Q3

2016‐Q4

2017‐Q1

2017‐Q2

2017‐Q3

2017‐Q4

Rutile Recovery %

Mine

Production impacted by higher slimes, low HMC

stock and slightly lower grades in 2018

Focus on volume of sand treatment to mitigate

Bolster supplementary mining contribution

Continue utilisation gains

Manage slimes closely

Maintain good recoveries

Develop WCPB upgrade on time within budget

Investigating further automation opportunities

for productivity improvement

Mine & MSP Outlook

15

MSP

Strategy: Maximise HMC feed and recoveries to

maximise final product production

Focus for product recoveries

Metallurgical control

Spillage management

Use Aggreko power in summer months

Deliver existing and develop further

recovery projects

Transition mineral to higher revenue products

Develop new monazite concentrate product

Cash operating costs

^ 2017 costs based on guidance given on 16 January 2017. Final numbers to be provided with FY17 Financial Results.* 2018 numbers based on guidance given on 11 January 2018.Total cash operating costs include all mine production, transhipment, taxes, royalties, and corporate costs.

2017 unit cash costs expected to be within guidance Labour cost savings moderating; Metical & Rand appreciation against the US$

2018 higher expected unit costs largely driven by lower expected production Cost control: strong focus will remain

Continued improvements in maintenance through year Focus on efficiencies in procurement and materials management commenced

500

750

1,000

1,250

$100

$120

$140

$160

$180

$200

$220

2012 2013 2014 2015 2016 2017^ 2018*

Volume (ktton

nes)

Costs (US$/t)

Final Production (RHS) Unit cash costs (LHS)

Guidance

17

2018 Guidance*

ProductionIlmenite kt 900,000‐1,000,000

Zircon kt 65,000‐72,000of which primary kt 42,000‐46,000

of which secondary kt 23,000‐25,000

Rutile kt 7,000‐8,000

CostsTotal cash operating costs US$m 133‐147Cash costs per tonne of finished product US$/t 130‐143

Production in 2018 is expected to moderate, mainly due to lower opening HMC inventories and slightly lower grades, although ilmenite shipment volumes are expected to be maintained as finished goods inventory is drawn down.

Impact of downtime for WCPB upgrade commissioning US$19 million approved for projects & studies in 2018 Sustaining capital costs in 2018 are expected to be approximately US$22 million.

* Guidance provided on 11 January 2018

1 Based on mineral resources and reserves as at 31/12/2016.

Moma is not one orebody

Differing ore zones:

Grades

Size

Mineral assemblage

Orebody knowledge works improved to understand mineability:

Water table

Slimes

Hardness

Provide alternative value enhancing options compared to current long term plan

Pilivili: Highest grade, free flowing sands, good co‐products

Congolone: high quality and good grades

100+ Year Life of Mine

18

Mineral Resources Zone Sand (Mt) % THM*

Congolone 276 3.4Marrua 54 4.1Mpitini 287 3.6Mualadi 327 3.2Namalope 515 3.5Nataka 6,206 2.8Pilivili 296 4.2Quinga North 71 3.5TOTAL RESOURCES 8,031 3.0

Sustaining Production – Near Term

19

Facing grade reduction as Namalope mining is concluded Additional mining capacity required to sustain production levels at around 1Mt ilmenite

per annum

WCPB Upgrade Modification of existing plant providing +20% throughputs (to 2400tph) Project underway using Hatch EPCM contractor Expected delivery H218 $16m capital, negligible impact on operating costs Supplementary mining being increased to deliver additional ore

Namalope Supplementary Mining Operation Small 500tph dredge and wet concentrator plant close to existing operations

Levers off existing mine infrastructure to minimise capital and operating costs Mines wet portion of WCPA dry mining area Approx 10 year life close to MSP Feasibility studies underway Targeting H219 commissioning

Mine Development – Medium Term

20

WCPB completes mining in Namalope at the end of 2020

requires a move to a new ore zone

already built into company plan

Prefeasibility studies show that relocation to Pilivili (rather than

Nataka) is preferred

HMC production will increase to meet MSP capacity

A large scale additional plant is therefore not required in medium

term

Environment Social and Health impact assessment (ESHIA)

underway, submission to MITADER mid 2018

Definitive Feasibility Study (DFS) completion Q1 2019

Mine Development – Long Term

21

WCPA completes mining in Namalope in 2025/26

requires a move to a new ore zone

already built into company plan

Current plan is to move to Nataka, however Congolone presents advantage of:

higher grades

lower slimes and

higher quality ilmenite

Feasibility studies underway to:

Assess optimal mining solution for Congolone

Understand the potential to relocate WCPA

Trade off studies to optimise mine plan

Summary of development

22

Maximising processing efficiency

Improving the higher value product mix for zircon and rutile

Increasing recovery of minerals such as through new monazite project with

negligible operating cost impacts

Strategic goal to increase ilmenite production in a capitally efficient manner

Fully utilise installed infrastructure and plant capacity

Optimised mineplan for grade

Reduces unit operating costs

Increases margins and cashflow stability through the cycle

Further studies underway to firm up the plan

![Page 2 Phone 087 2513126 • 087 2330398 Kenmare News News Feb 2013.pdf · Page 2 Phone 087 2513126 • 087 2330398 Kenmare News Dear Editor, ... wedding album; The wedding [book]](https://img.dokumen.tips/doc/110x75/5b78280a7f8b9a515a8e9ea6/page-2-phone-087-2513126-087-2330398-kenmare-news-feb-2013pdf-page-2-phone.jpg)